Midyear Outlook 2017 Spread - IHT Wealth Management...D positive so far in 2 0 could also benefit t...

9

Member FINRA/SIPC

Transcript of Midyear Outlook 2017 Spread - IHT Wealth Management...D positive so far in 2 0 could also benefit t...

Member FINRA/SIPC

U.S

. Sm

all

Cap

Stoc

ksU

.S. s

mal

l cap

s h

ave

ben

efite

d f

rom

acc

om

ay b

enefi

t fr

om

fisc

al p

olic

y ch

ang

es, t

h

Emer

ging

M

arke

ts (E

M)

Nea

r-te

rm c

atal

ysts

(g

lob

al g

row

th, m

on

ete

rm t

ren

ds

(six

bill

ion

co

nsu

mer

s) o

ffer

Cycl

ical

Se

ctor

sTe

ch

no

log

y is

po

siti

on

ed t

o b

enefi

t fr

om

g

row

th a

s b

usi

nes

s in

vest

men

t p

ote

nti

alp

rod

uct

ivit

y. In

du

str

ials

may

ben

efit

fro

man

d in

fras

tru

ctu

re p

roje

cts

and

str

on

ger

gsh

ou

ld b

enefi

t fr

om

der

egu

lati

on

th

at m

ad

ivid

end

s, w

hile

tig

hte

r m

on

etar

y p

olic

y

Mas

ter L

imite

d Pa

rtne

rshi

psT

he

Tru

mp

ad

min

istr

atio

n’s

stan

ce o

n e

ne

yiel

ds

rem

ain

ver

y at

trac

tive

bu

t in

tro

du

c

Inve

stm

ent-

Gra

de

Corp

orat

esW

e co

ntin

ue to

find

rel

ativ

e va

lue

in in

vest

cont

inue

d st

reng

th in

cre

dit m

arke

ts a

nd th

Mor

tgag

e-B

acke

d Se

curi

ties

(MB

S)A

mo

ng

hig

h-q

ual

ity

bo

nd

s, M

BS

co

nti

nu

trad

e-o

ff b

etw

een

yie

ld a

nd

inte

rest

rat

e

Ban

k Lo

ans

Att

ract

ive

yiel

ds

and

co

up

on

pay

men

ts t

hm

ake

ban

klo

ans

less

likel

yto

suff

erp

rice

Econ

omy

GD

P G

row

th N

ea

r 2

.5%

W

e co

ntin

ue to

look

for t

he

U.S

. eco

nom

y to

exp

and

up

to 2

.5%

in 2

017,

alth

ough

po

tent

ial d

elay

s in

pas

sing

m

ajor

fisc

al p

olic

ies

intr

oduc

e so

me

risk

to th

e do

wns

ide.

D

ata

on c

onsu

mpt

ion,

em

ploy

men

t, ho

usin

g,

man

ufac

turin

g, a

nd s

ervi

ces

all p

oint

tow

ard

impr

ovem

ent

in th

e m

onth

s an

d qu

arte

rs

ahea

d fo

llow

ing

slug

gish

firs

t qu

arte

r GD

P gr

owth

.

Stoc

ks6 –

9%

Re

turn

s

As

inve

stor

s in

crea

sing

ly tr

ust

that

the

econ

omy

can

stan

d on

its

own

with

out t

he n

eed

of m

onet

ary

polic

y su

ppor

t, bu

sine

ss fu

ndam

enta

ls s

houl

d ta

ke o

ver a

s th

e pr

imar

y m

arke

t eng

ine

and

corp

orat

e pr

ofits

will

take

on

incr

easi

ng

impo

rtan

ce. W

e ha

ve s

light

ly

rais

ed o

ur 2

017

S&P

500

Inde

x to

tal r

etur

n fo

reca

st to

6 –

9%

, co

mm

ensu

rate

with

exp

ecte

d ea

rnin

gs g

ains

.

Inter

natio

nal

Em

erg

ing

ove

r D

ev

Thou

gh fu

ndam

enta

ls

firm

ing,

gro

wth

in E

uro

and

Japa

n ha

s on

ly g

rim

prov

ed fr

om lo

w le

vM

onet

ary

polic

y ha

s f

econ

omic

and

fina

ncia

gain

s w

ith c

entr

al b

anco

ntin

uing

, yet

eco

nom

refo

rms

are

still

nee

dere

mai

n ca

utio

us o

n de

inte

rnat

iona

l mar

kets

,m

ore

cons

truc

tive

on

mar

kets

(EM

).

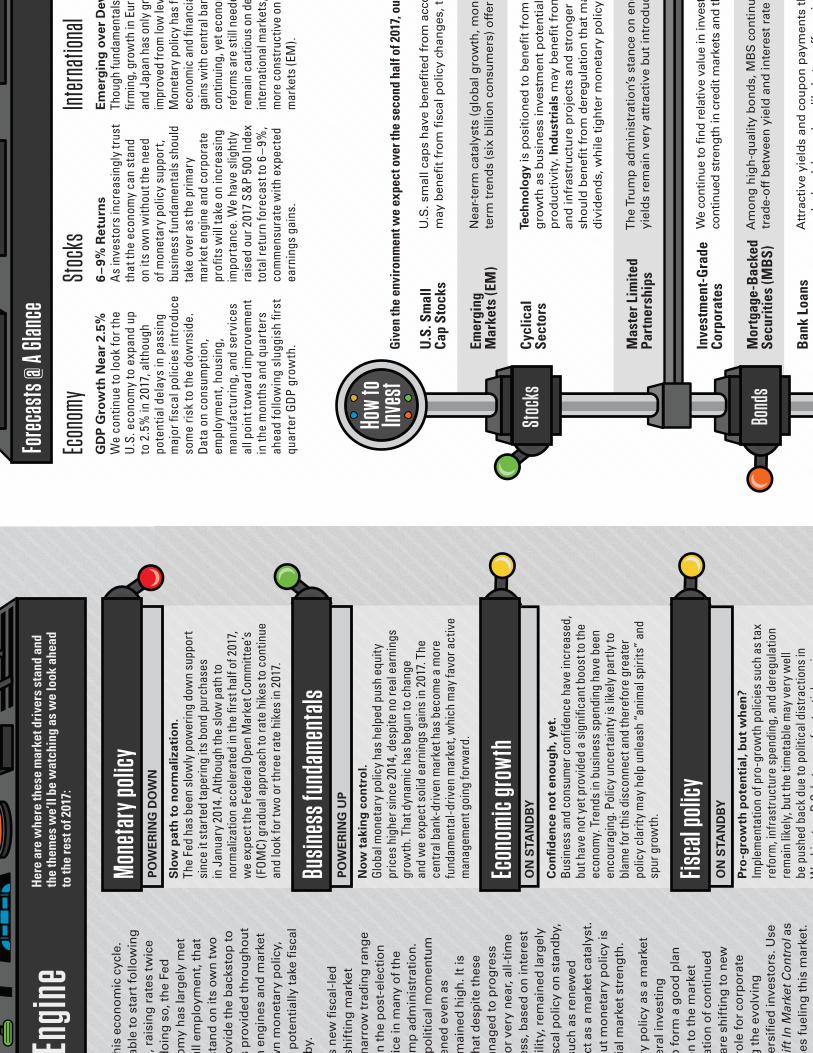

Mon

etar

y po

licy

Slo

w p

ath

to

no

rma

liza

tio

n.

The

Fed

has

been

slo

wly

pow

erin

g do

wn

supp

ort

sinc

e it

star

ted

tape

ring

its b

ond

purc

hase

s in

Jan

uary

201

4. A

lthou

gh th

e sl

ow p

ath

to

norm

aliz

atio

n ac

cele

rate

d in

the

first

hal

f of 2

017,

we

expe

ct th

e Fe

dera

l Ope

n M

arke

t Com

mitt

ee’s

(F

OMC)

gra

dual

app

roac

h to

rate

hik

es to

con

tinue

an

d lo

ok fo

r tw

o or

thre

e ra

te h

ikes

in 2

017.

Busi

ness

fund

amen

tals

No

w t

ak

ing

co

ntr

ol.

Glob

al m

onet

ary

polic

y ha

s he

lped

pus

h eq

uity

pr

ices

hig

her s

ince

201

4, d

espi

te n

o re

al e

arni

ngs

grow

th. T

hat d

ynam

ic h

as b

egun

to c

hang

e an

d w

e ex

pect

sol

id e

arni

ngs

gain

s in

201

7. Th

e ce

ntra

l ban

k-dr

iven

mar

ket h

as b

ecom

e a

mor

e fu

ndam

enta

l-driv

en m

arke

t, w

hich

may

favo

r act

ive

man

agem

ent g

oing

forw

ard.

Econ

omic

gro

wth

Co

nfi

de

nce n

ot

en

ou

gh

, ye

t.

Busi

ness

and

con

sum

er c

onfid

ence

hav

e in

crea

sed,

bu

t hav

e no

t yet

pro

vide

d a

sign

ifica

nt b

oost

to th

e ec

onom

y. T

rend

s in

bus

ines

s sp

endi

ng h

ave

been

en

cour

agin

g. P

olic

y un

cert

aint

y is

like

ly p

artly

to

blam

e fo

r thi

s di

scon

nect

and

ther

efor

e gr

eate

r po

licy

clar

ity m

ay h

elp

unle

ash

“ani

mal

spi

rits”

and

sp

ur g

row

th.

Fisc

al p

olic

y

Pro

-gro

wth

po

ten

tia

l, b

ut

wh

en

?

Impl

emen

tatio

n of

pro

-gro

wth

pol

icie

s su

ch a

s ta

x re

form

, inf

rast

ruct

ure

spen

ding

, and

der

egul

atio

n re

mai

n lik

ely,

but

the

timet

able

may

ver

y w

ell

be p

ushe

d ba

ck d

ue to

pol

itica

l dis

trac

tions

in

Was

hing

ton

DC

Inte

rms

ofpo

tent

iale

arni

ngs

ON

STA

ND

BY

PO

WE

RIN

G U

P

PO

WE

RIN

G D

OW

N

ON

STA

ND

BY

his

eco

no

mic

cyc

le.

able

to

sta

rt f

ollo

win

g

, rai

sin

g r

ates

tw

ice

do

ing

so,

th

e Fe

d

om

y h

as la

rgel

y m

et

ull

emp

loym

ent,

th

at

stan

d o

n it

s o

wn

tw

o

ovi

de

the

bac

ksto

p t

o

s p

rovi

ded

th

rou

gh

ou

t h

en

gin

es a

nd

mar

ket

wn

mo

net

ary

po

licy,

p

ote

nti

ally

tak

e fi

scal

b

y.

s n

ew fi

scal

-led

sh

ifti

ng

mar

ket

nar

row

tra

din

g r

ang

e n

th

e p

ost

-ele

ctio

n

ice

in m

any

of t

he

mp

ad

min

istr

atio

n.

po

litic

al m

om

entu

m

ened

eve

n a

s m

ain

ed h

igh

. It i

s h

at d

esp

ite

thes

e an

aged

to

pro

gre

ss

or

very

nea

r, al

l-ti

me

ess,

bas

ed o

n in

tere

st

ility

, rem

ain

ed la

rgel

y sc

al p

olic

y o

n s

tan

db

y,

such

as

ren

ewed

ct

as

a m

arke

t cat

alys

t.

bu

t mo

net

ary

po

licy

is

ial m

arke

t str

eng

th.

ry p

olic

y as

a m

arke

t er

al in

vest

ing

o

fo

rm a

go

od

pla

n

on

to

th

e m

arke

t at

ion

of c

on

tin

ued

ar

e sh

ifti

ng

to

new

ro

le f

or

corp

ora

te

g t

he

evo

lvin

g

ersi

fied

inve

sto

rs. U

se

hif

t In

Mar

ket C

on

tro

l as

nes

fu

elin

g t

his

mar

ket.

Her

e ar

e w

here

thes

e m

arke

t dri

vers

sta

nd a

nd

the

them

es w

e’ll

be w

atch

ing

as w

e lo

ok a

head

to

the

rest

of 2

017:

Stoc

ks

Fore

cast

s @

A G

lanc

eEn

gine

Bond

s

Give

n th

e en

viro

nmen

t we

expe

ct o

ver t

he s

econ

d ha

lf of

201

7, ou

How

to

Inve

st

mie

s al

ike,

the

abi

lity

cent

ral b

ank

supp

ort

ts o

ver

the

bala

nce

of

supp

ort

as it

m

aliz

atio

n. C

onsi

derin

g an

d la

rgel

y st

eady

, he

Fed

no

long

er

leve

l pol

icy

mea

sure

s.

ree

rate

hik

es in

ua

lly re

mov

es it

s S

. gro

wth

am

id lo

w

ccom

pani

ed b

y co

re

bove

the

Fed

tar

get

on. B

ut t

here

are

stil

l on

infla

tion,

incl

udin

g y,

a lo

w la

bor

forc

e st

able

dol

lar,

that

an

ove

the

Fed’

s 2%

ged

abou

t 18

5,00

0 is

like

ly to

slo

w a

t

this

sta

ge o

f th

e bu

sine

ss c

ycle

. But

eve

n if

payr

oll

grow

th w

ere

to d

eclin

e to

a 1

00,0

00 to

125

,000

m

onth

ly p

ace,

we

susp

ect

the

Fed

wou

ld s

till s

tay

on t

rack

to h

ike

rate

s at

leas

t tw

ice

this

yea

r. W

age

grow

th a

t 2.

5% re

mai

ns b

elow

the

4.0

% p

ace

that

ha

s hi

stor

ical

ly c

ause

d ce

ntra

l ban

kers

to r

aise

rat

es

aggr

essi

vely

, but

has

impr

oved

eno

ugh

to k

eep

the

Fed

on it

s st

ated

tra

ck.

Whi

le s

uch

a ra

te h

ike

path

wou

ld b

e co

nsis

tent

w

ith t

he F

OM

C’s

sta

tem

ents

, mon

etar

y of

ficia

ls

will

nee

d to

bal

ance

the

ir em

ploy

men

t an

d in

flatio

n m

anda

tes

with

the

pot

entia

l U.S

. dol

lar

impa

ct.

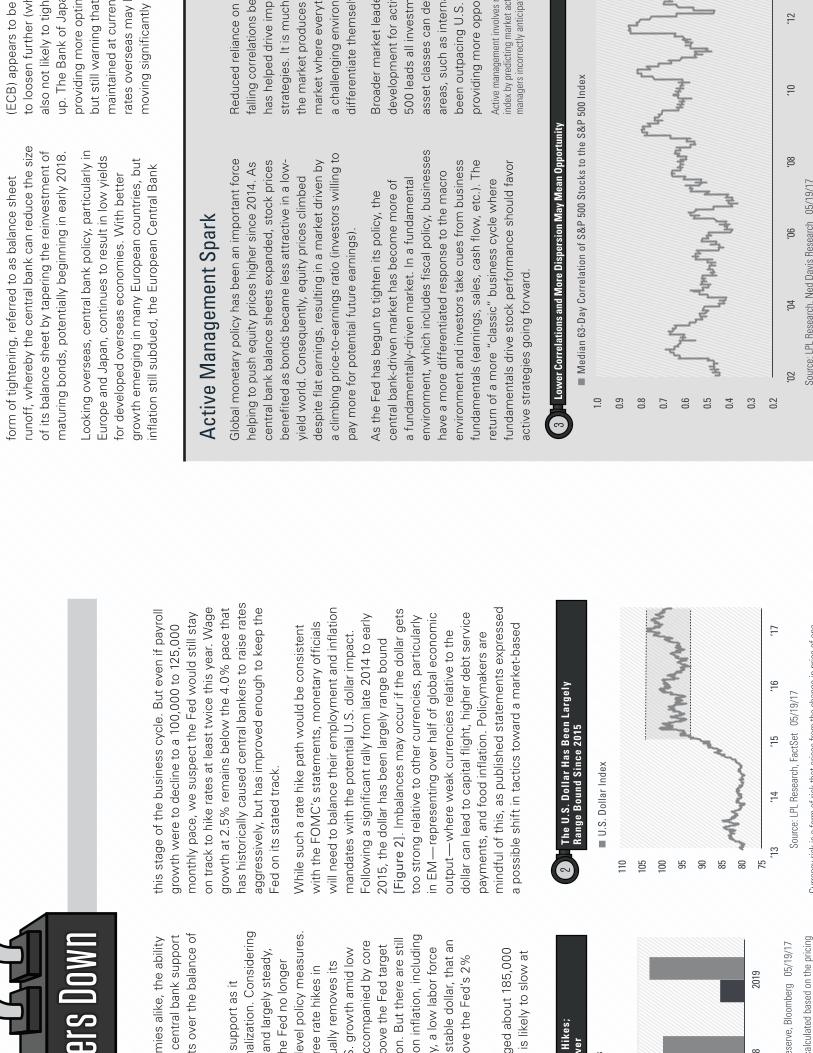

Follo

win

g a

sign

ifica

nt r

ally

fro

m la

te 2

014

to e

arly

20

15, t

he d

olla

r ha

s be

en la

rgel

y ra

nge

boun

d [F

igu

re 2

]. Im

bala

nces

may

occ

ur if

the

dol

lar

gets

to

o st

rong

rela

tive

to o

ther

cur

renc

ies,

par

ticul

arly

in

EM

— re

pres

entin

g ov

er h

alf

of g

loba

l eco

nom

ic

outp

ut —

whe

re w

eak

curr

enci

es re

lativ

e to

the

do

llar

can

lead

to c

apita

l flig

ht, h

ighe

r de

bt s

ervi

ce

paym

ents

, and

food

infla

tion.

Pol

icym

aker

s ar

e m

indf

ul o

f th

is, a

s pu

blis

hed

stat

emen

ts e

xpre

ssed

a

poss

ible

shi

ft in

tac

tics

tow

ard

a m

arke

t-ba

sed

form

of

tight

enin

g, re

ferr

ed to

as

bala

nce

shee

t ru

noff

, whe

reby

the

cen

tral

ban

k ca

n re

duce

the

siz

e of

its

bala

nce

shee

t by

tap

erin

g th

e re

inve

stm

ent

of

mat

urin

g bo

nds,

pot

entia

lly b

egin

ning

in e

arly

201

8.

Look

ing

over

seas

, cen

tral

ban

k po

licy,

par

ticul

arly

in

Euro

pe a

nd J

apan

, con

tinue

s to

resu

lt in

low

yie

lds

for

deve

lope

d ov

erse

as e

cono

mie

s. W

ith b

ette

r gr

owth

em

ergi

ng in

man

y Eu

rope

an c

ount

ries,

but

in

flatio

n st

ill s

ubdu

ed, t

he E

urop

ean

Cen

tral

Ban

k

(EC

B) a

ppea

rs to

be

to lo

osen

fur

ther

(wh

also

not

like

ly to

tig

htup

. The

Ban

k of

Jap

apr

ovid

ing

mor

e op

timbu

t st

ill w

arni

ng t

hat

mai

ntai

ned

at c

urre

nra

tes

over

seas

may

km

ovin

g si

gnifi

cant

ly

Glo

bal m

onet

ary

polic

y ha

s be

en a

n im

port

ant

forc

e he

lpin

g to

pus

h eq

uity

pric

es h

ighe

r si

nce

2014

. As

cent

ral b

ank

bala

nce

shee

ts e

xpan

ded,

sto

ck p

rices

be

nefit

ed a

s bo

nds

beca

me

less

att

ract

ive

in a

low

-yi

eld

wor

ld. C

onse

quen

tly, e

quity

pric

es c

limbe

d de

spite

flat

ear

ning

s, re

sulti

ng in

a m

arke

t dr

iven

by

a cl

imbi

ng p

rice-

to-e

arni

ngs

ratio

(inv

esto

rs w

illin

g to

pa

y m

ore

for

pote

ntia

l fut

ure

earn

ings

).

As

the

Fed

has

begu

n to

tig

hten

its

polic

y, t

he

cent

ral b

ank-

driv

en m

arke

t ha

s be

com

e m

ore

of

a fu

ndam

enta

lly-d

riven

mar

ket.

In a

fun

dam

enta

l en

viro

nmen

t, w

hich

incl

udes

fisc

al p

olic

y, b

usin

esse

s ha

ve a

mor

e di

ffer

entia

ted

resp

onse

to t

he m

acro

en

viro

nmen

t an

d in

vest

ors

take

cue

s fr

om b

usin

ess

fund

amen

tals

(ear

ning

s, s

ales

, cas

h flo

w, e

tc.)

. The

re

turn

of

a m

ore

“cla

ssic

” bu

sine

ss c

ycle

whe

re

fund

amen

tals

driv

e st

ock

perf

orm

ance

sho

uld

favo

r ac

tive

stra

tegi

es g

oing

forw

ard.

Red

uced

relia

nce

on

falli

ng c

orre

latio

ns b

eha

s he

lped

driv

e im

prst

rate

gies

. It

is m

uch

the

mar

ket

prod

uces

m

arke

t w

here

eve

ryt

a ch

alle

ngin

g en

viro

ndi

ffer

entia

te t

hem

sel v

Bro

ader

mar

ket

lead

ede

velo

pmen

t fo

r ac

tiv50

0 le

ads

all i

nves

tmas

set

clas

ses

can

det

area

s, s

uch

as in

tern

abe

en o

utpa

cing

U.S

. pr

ovid

ing

mor

e op

po

820

19

s

Sour

ce: L

PL R

esea

rch,

Ned

Dav

is R

esea

rch

05/

19/1

7

110

105

100 95 90 85 80 75

‘16‘15

‘14‘13

‘17

U.S

. Dol

lar I

ndex

The

U.S

. Dol

lar

Has

Bee

n La

rgel

y R

ange

Bou

nd S

ince

201

52

Hik

es;

wer

Sour

ce: L

PL R

esea

rch,

Fac

tSet

05

/19/

17

Curre

ncyr

iskis

afo

rmof

riskt

hata

rises

from

the

chan

gein

price

ofon

e

eser

ve, B

loom

berg

05

/19/

17

calc

ulat

ed b

ased

on

the

pric

ing

1.0 0.9 0.8 0.7 0.6 0.5 0.4 0.3 0.2

‘04‘02

‘06‘08

‘10‘12

Med

ian

63-D

ay C

orre

latio

n of

S&

P 50

0 St

ocks

to th

e S&

P 50

0 In

dex

Activ

e M

anag

emen

t Spa

rk

ers Do

wn

Low

er C

orre

latio

ns a

nd M

ore

Disp

ersi

on M

ay M

ean

Opp

ortu

nity

3

Activ

e m

anag

emen

t inv

olve

s r

inde

x by

pre

dict

ing

mar

ket a

ctm

anag

ers

inco

rrect

ly a

ntic

ipat

%4 3 2 1 0

‘08‘06

‘04‘02

‘00‘96

‘94‘92

‘90‘98

Grow

th in

U.S

. Rea

l Out

put p

er H

our (

5-Ye

ar A

vera

ge)

Gro

wth

Nee

ds a

Pro

duct

ivit

y In

ject

ion

5 cent

ral b

ank.

Mea

nwhi

le, a

ntic

ipat

ed fi

scal

le

gisl

atio

n m

ay p

rovi

de f

urth

er in

cent

ives

for

bu

sine

sses

to

take

eco

nom

ic r

isks

, suc

h as

in

vest

ing

in p

rope

rty,

pla

nt, a

nd e

quip

men

t,

to p

ositi

on f

or f

utur

e gr

owth

. Thi

s w

ould

be

a ch

ange

fro

m r

ecen

t ye

ars,

whe

re m

any

busi

ness

es u

sed

low

rat

es t

o re

turn

cas

h to

in

vest

ors

by is

suin

g de

bt a

nd b

uyin

g ba

ck s

hare

s or

pay

ing

divi

dend

s, c

hoos

ing

the

finan

cial

ris

k fr

om m

ore

debt

on

thei

r ba

lanc

e sh

eets

ove

r th

e ec

onom

ic r

isk

of in

vest

ing

in t

heir

busi

ness

es. A

n im

prov

emen

t in

cap

ital i

nves

tmen

t tr

ends

wou

ld

also

like

ly b

oost

pro

duct

ivit

y, w

hich

is e

ssen

tial

for

rais

ing

livin

g st

anda

rds.

Pro

duct

ivity

gro

wth

rem

ains

the

key

to a

ny

sust

aina

ble

incr

ease

in t

he r

ate

of e

cono

mic

gro

wth

ov

er t

he lo

ng te

rm. T

here

are

tw

o pr

imar

y dr

iver

s of

eco

nom

ic g

row

th: a

larg

er w

orkf

orce

and

an

incr

ease

in w

hat

a m

embe

r of

the

wor

kfor

ce c

an

prod

uce,

thr

ough

bet

ter

trai

ning

or

bett

er re

sour

ces.

Th

e la

tter

is w

hat

we

call

prod

uctiv

ity a

nd it

has

sl

owed

con

side

rabl

y th

roug

hout

the

exp

ansi

on

[Fig

ure

5].

The

re a

this

, inc

ludi

ng d

imi

deve

lopm

ent

and

lco

ntra

ctio

n in

em

pcr

isis

. Bus

ines

s in

vof

impr

ovin

g pr

odu

pick

up

in t

he fi

rst

prod

uctiv

ity w

ill h

aar

e to

see

impr

ove

Fisc

al p

olic

y co

uld

spen

ding

to h

elp

dap

proa

ch m

ay li

mi t

dolla

r, el

imin

atin

g t

inte

rfer

e w

ith e

xpo

mak

es d

omes

tic g

obu

yers

). G

loba

l GD

posi

tive

so f

ar in

20

coul

d al

so b

enefi

t t

expo

rts.

Con

side

rinin

vest

men

t, g

over

nar

e st

icki

ng w

ith o

ugr

owth

in 2

017.

S. e

cono

my

to

houg

h po

tent

ial d

elay

s in

trod

uce

som

e w

-tre

nd p

ace

is s

till

ajec

tory

tha

t th

e ou

ghou

t th

e ex

pans

ion

com

e, p

rodu

ctio

n,

evel

s ac

hiev

ed in

, we

still

see

U.S

. 20

17 f

orec

ast

with

on

in 2

018.

Firs

t w

as d

isap

poin

ting,

w

eakn

ess

has

been

ar

s as

a c

ombi

natio

n pe

rhap

s an

en

t pr

oces

s ha

s pr

oved

gro

wth

in

on

cons

umpt

ion,

ac

turin

g, a

nd s

ervi

ces

all p

oint

tow

ard

pote

ntia

l im

prov

emen

t in

the

m

onth

s an

d qu

arte

rs a

head

fol

low

ing

slug

gish

firs

t qu

arte

r G

DP

gro

wth

.

Whi

le c

onfid

ence

am

ong

cons

umer

s an

d bu

sine

sses

rem

ains

ver

y hi

gh (s

o ca

lled

“sof

t da

ta”)

, mea

sure

s of

act

ual e

cono

mic

act

ivity

(“ha

rd

data

”), s

uch

as G

DP,

hav

e no

t be

en a

s st

rong

in t

he

first

par

t of

201

7. T

he s

oft

data

nee

ds to

tra

nsla

te

into

str

onge

r ec

onom

ic a

ctiv

ity to

reac

h ou

r G

DP

gr

owth

fore

cast

for

2017

. One

like

ly re

ason

for

this

dis

conn

ect

is c

ontin

ued

polic

y un

cert

aint

y,

alth

ough

we

have

see

n a

rece

nt p

icku

p in

bus

ines

s in

vest

men

t. W

hile

ena

ctin

g ef

fect

ive

pro

-gro

wth

po

licy

wou

ld a

lmos

t ce

rtai

nly

bene

fit t

he e

cono

my,

gr

eate

r po

licy

clar

ity m

ay b

e en

ough

to u

nlea

sh

“ani

mal

spi

rits”

and

hel

p sp

ur g

row

th.

The

rece

nt im

prov

emen

t in

job

grow

th w

ith

mod

erat

e w

age

gain

s al

low

s fo

r co

nsum

ptio

n gr

owth

with

out

the

need

for

an

acco

mm

odat

ive

cess

ion

Q1

‘09 Q

1‘10

Q1

‘11 Q

1‘12

Q1

‘13 Q

1‘14

Q1

‘15 Q

1‘16

Q1

‘17‘17

E

oduc

t: Qu

antit

y In

dex

(% C

hang

e fro

m P

rior Q

uarte

r, Se

ason

ally

Adj

uste

d An

nual

Rat

e)

Actu

al(Q

uarte

rly)

Estim

ated

(Ann

ual)

U.S

. Eco

nom

ic G

row

th i

n 20

17

reau

of

s 0

5/19

/17

on.

is th

e m

onet

ary

valu

e of

all

the

finis

hed

good

s an

d se

rvic

es p

rodu

ced

with

in a

cou

ntry

’s bo

rder

s in

a

Sour

ce: L

PL R

esea

rch,

Bur

eau

of L

abor

Sta

tistic

s 0

5/19

/17

hedu

led M

ainten

ance

Due

10-Year Treasury Yield

S&P

500

Trai

ling

PE R

atio

Annual CPI Change

%%

18 16 14 12 10 8 6 4 2 0

16 14 12 10 8 6 4 2 0 -2 -40

205

2510

3015

350

5

Trai

ling

PE v

s. 1

0-Ye

ar T

reas

ury

Yiel

d

Low

er In

flatio

n an

d Lo

wer

Inte

rest

Rat

es H

ave

Hist

oric

ally

Cor

rela

ted

to H

ighe

r Pric

e-to

-E

Trai

ling

PE v

Curre

nt

that

the

eco

nom

y he

nee

d of

ne

ss f

unda

men

tals

y

mar

ket

driv

er.

will

be

incr

easi

ngly

ba

lanc

e of

201

7 th

at e

arni

ngs

r th

e ba

lanc

e of

ai

se o

ur 2

017

ecas

t to

6 –

9%

, ou

sly,

driv

en b

y:

row

th; 2

) mid

- to

s; 3

) a s

tabl

e pr

ice-

0; a

nd 4

) pro

spec

ts

ings

in 2

018.

ratin

g ea

rnin

gs

sica

lly fl

at, a

t qu

ently

, mar

ket

een

larg

ely

due

earn

ings

rat

io

This

dyn

amic

n

2017

, we

profi

ts, d

riven

by p

oten

tial i

mpr

ovem

ent

in e

cono

mic

gro

wth

, re

silie

nt p

rofit

mar

gins

, a s

tabl

e U

.S. d

olla

r, an

d re

boun

ding

ene

rgy

profi

ts. W

e be

lieve

S&

P 5

00

earn

ings

gro

wth

nea

r 10

% is

att

aina

ble,

put

ting

earn

ings

for

the

inde

x in

the

ran

ge o

f $1

30 p

er

shar

e, e

ven

with

out

any

mat

eria

l im

pact

fro

m

fisca

l pol

icy

chan

ges

this

yea

r.

Cor

pora

te A

mer

ica

is o

ff to

a g

ood

star

t tow

ard

hitt

ing

our e

arni

ngs

targ

et. F

irst q

uart

er e

arni

ngs

seas

on w

as a

ver

y go

od o

ne, w

ith S

&P

500

profi

ts ri

sing

by

a m

uch

bett

er th

an e

xpec

ted

15%

yea

r ove

r yea

r (Th

omso

n da

ta) [

Fig

ure

6]

whi

le c

ompa

ny g

uida

nce

for

the

rem

aind

er

of t

he y

ear

was

als

o po

sitiv

e. T

he b

ar fo

r gr

owth

was

fai

rly lo

w, a

s th

e co

mpa

rison

was

re

lativ

ely

easy

con

side

ring

the

stru

ggle

s of

ea

rly 2

016,

par

ticul

arly

in t

he e

nerg

y se

ctor

. But

ev

en e

xclu

ding

the

str

ong

cont

ribut

ion

from

re

boun

ding

ene

rgy

sect

or p

rofit

s, S

&P

500

ea

rnin

gs w

ere

still

up

over

10%

yea

r ov

er y

ear

in

the

first

qua

rter

. Eve

n if

the

earn

ings

tra

ject

ory

slow

s so

me

over

the

cou

rse

of t

he y

ear

as

com

paris

ons

with

201

6 ge

t to

ughe

r, bu

sine

ss

Q1

‘15 Q

1‘16

Q2

‘15 Q

2‘16

Q3

‘15 Q

3‘16

Q4 14 Q

4‘15

Q4

‘16 Q

1‘17

2018

E20

17E

arni

ngs

Grow

th

Actu

alRe

sults

Cons

ensu

sEs

timat

es

Hig

her

Valu

atio

ns H

ave

A F

air

Am

ount

of S

uppo

rt7

Sour

ce: L

PL R

esea

rch,

Fac

tSet

, Tho

mso

n Re

uter

s, H

aver

Ana

lytic

s 0

5/19

/17

Data

are

mon

thly

goi

ng b

ack

to 1

962.

The

PE ra

tio (p

rice-

to-e

arni

ngs

ratio

) is

a m

easu

re o

f the

pric

e pa

id fo

r a s

hare

rela

tive

to th

e an

firm

per

sha

re. I

t is

a fin

anci

al ra

tio u

sed

for v

alua

tion:

a h

ighe

r PE

ratio

mea

ns th

at in

vest

ors

a rso

the

stoc

k is

mor

e ex

pens

ive

com

pare

d to

one

with

low

er P

E ra

tio.

Cons

umer

pric

e in

flatio

n is

the

reta

il pr

ice

incr

ease

as

mea

sure

d by

a C

onsu

mer

Pric

e In

dex

(CP

r G

ear

Reut

ers

05/

19/1

7

fund

amen

tals

may

stil

l poi

nt to

war

d fu

rthe

r gr

owth

in o

utpu

t an

d pr

ofits

.

We

look

for

stoc

ks to

see

gai

ns c

omm

ensu

rate

w

ith p

rofit

gro

wth

, con

sist

ent

with

his

toric

al

mid

-to

-late

eco

nom

ic c

ycle

per

form

ance

. At

19 –

20

times

tra

iling

S&

P 5

00 e

arni

ngs,

sto

cks

are

expe

nsiv

e re

lativ

e to

the

ir lo

ng-t

erm

his

tory

. H

owev

er, w

hen

view

ed a

gain

st in

tere

st r

ates

an

d in

flatio

n st

ill n

ear

hist

oric

low

s [F

igu

re 7

],

valu

atio

ns lo

ok f

air

to u

s. M

oreo

ver,

the

pote

ntia

l po

licy

upsi

de to

ear

ning

s in

201

8 on

top

of a

n al

read

y up

war

d tr

ajec

tory

for

corp

orat

e pr

ofits

co

uld

prov

ide

furt

her

supp

ort

for

equi

ties.

R

emem

ber,

hist

ory

is li

tter

ed w

ith e

xam

ples

sh

owin

g th

at v

alua

tions

hav

e be

en p

oor

pred

icto

rs o

f on

e-ye

ar s

tock

mar

ket

perf

orm

ance

.

Add

ition

al c

larit

y on

cor

pora

te t

ax re

form

in

the

com

ing

mon

ths

will

pro

vide

fur

ther

insi

ght

into

201

8 pr

ofit

grow

th a

nd p

oten

tially

just

ify

elev

ated

sto

ck m

arke

t va

luat

ions

. In

fact

, al

thou

gh w

e ha

ve li

ttle

mor

e th

an a

hig

h-le

vel

fram

ewor

k to

go

on a

s Ju

ne b

egin

s, t

he p

oten

tial

exis

ts fo

r co

rpor

ate

tax

refo

rm to

boo

st S

&P

50

0 ea

rnin

gs b

y 5%

or

mor

e in

201

8, w

ith t

he

obvi

ous

cond

ition

tha

t th

e Tr

ump

adm

inis

trat

ion

dC

tth

k

that

can

get

eno

ugh

Sen

ate.

Far

fro

m a

sm

ore

likel

y th

an n

ot.

Whi

le a

ccel

erat

ing

epr

ovid

e fu

rthe

r su

ppim

plem

entin

g P

resi

dad

ditio

nal F

ed r

ate

hbo

uts

of s

tock

mar

k est

ocks

fro

m a

ddin

g m

gain

s. F

isca

l pol

icy

ism

eani

ngfu

l pro

gres

sof

cor

pora

te t

ax re

fofo

r co

rpor

ate

profi

ts

fund

amen

tal j

ustifi

c a

Inve

stor

s sh

ould

fee

stoc

k m

arke

t is

as

thap

proa

ches

. The

eco

pois

ed to

con

tinue

afu

ndam

enta

ls, t

his

epr

obab

ly c

ontin

ue a

she

lp m

uch

this

yea

r, vo

latil

ity a

s m

onet

ary

but

we

thin

k st

ocks

st

and

on t

heir

own

are

mov

ed a

nd d

eliv

erth

dh

lff

20

dame

ntals

Back

At Th

e Con

trols

%25 20 15 10 5 0 -5 -10

-15

-20

-25

2011

2012

2013

2014

2015

Unite

d St

ates

Earn

ings

Gro

wth

Deve

lope

d In

tern

atio

nal

Emer

ging

Mar

kets

its a

ccom

mod

ativ

e st

ance

. St

rong

er e

arni

ngs

in E

urop

e an

d Ja

pan

have

pow

ered

ear

ning

s gr

owth

for t

he M

SC

I EA

FE

Inde

x so

lidly

hig

her i

n 20

17 a

fter

ea

rnin

gs d

eclin

es in

five

out

of

the

last

six

yea

rs [

Fig

ure

9].

As

has

typi

cally

bee

n th

e ca

se,

emer

ging

mar

ket

econ

omie

s ar

e de

pend

ent

on C

hine

se

dem

and,

yet

giv

en m

assi

ve

inve

stm

ent

acro

ss E

M, f

uele

d in

larg

e pa

rt b

y do

llar-

deno

min

ated

deb

t, t

hey

rem

ain

sens

itive

to

cha

nges

in U

.S. m

onet

ary

polic

y. S

tead

y gl

obal

de

man

d ha

s bo

oste

d ou

tput

for

the

larg

ely

expo

rt-

driv

en e

cono

mie

s an

d dr

iven

rene

wed

ear

ning

s gr

owth

, whi

le f

allin

g co

mm

odity

pric

es c

an h

ave

mix

ed re

sults

for

prod

ucer

s an

d ex

port

ers.

Fort

unat

ely,

thes

e fu

ndam

enta

ls h

ave

been

larg

ely

supp

ortiv

e of

glo

bal e

quiti

es, d

rivin

g w

hat c

an b

e

de In ne is

em m re EA

ou De

glin

vest

men

ts o

utsi

dof

ris

ks t

hat

will

ne

Thes

e in

clud

e a

pogo

vern

men

t, t

he p

in E

urop

e, p

oten

ti ale

avin

g th

e Eu

rope

vuln

erab

ilitie

s in

Ch

geop

oliti

cal u

ncer

taK

orea

and

Syr

ia.

cont

endi

ng w

ith

nce

betw

een

Fund

amen

tals

an

, and

eco

nom

ic

prov

ing

from

low

te

mpt

to

reco

ver

etar

y po

licy

has

omic

and

fina

ncia

l k

supp

ort

cont

inui

ng,

need

ed t

o ad

dres

s re

, we

rem

ain

atio

nal m

arke

ts.

ance

bet

wee

n ar

kets

hav

e a

long

r

ever

sal [

Fig

ure

8].

ts h

ave

offe

red

the

risks

end

emic

as

var

ying

eco

nom

ic

d un

cert

ain

polit

ics.

au

se o

f lim

itatio

ns

olic

y in

Eur

ope,

EM

may

pro

vide

mor

e st

abili

ty, w

hile

pot

entia

l ris

ks

rela

ted

to “

Bre

xit,”

upc

omin

g el

ectio

ns in

Ital

y an

d G

erm

any,

and

str

uctu

ral c

halle

nges

suc

h as

im

mig

ratio

n an

d la

bor

mar

ket

refo

rm m

ay w

eigh

on

dev

elop

ed m

arke

ts.

Pol

itics

and

pol

icy

asid

e, f

unda

men

tals

are

firm

ing

in E

urop

e an

d th

e E

CB

has

giv

en n

o cl

ear

sign

al

rega

rdin

g w

hen

the

inev

itabl

e re

duct

ion

of s

uppo

rt

will

tak

e pl

ace.

Val

uatio

ns a

nd d

ivid

end

yiel

ds

in E

urop

e ap

pear

att

ract

ive

whi

le fi

rmin

g gl

obal

de

man

d, im

prov

ing

earn

ings

, and

the

elim

inat

ion

of t

he w

orst

-cas

e sc

enar

ios

from

the

Fre

nch

and

Dut

ch e

lect

ions

hav

e al

so p

rovi

ded

mar

ket

supp

ort.

The

back

drop

look

s to

be

mor

e fa

vora

ble

for g

loba

l eq

uity

inve

stor

s in

Jap

an, w

here

pol

itica

l lea

ders

hip

was

str

engt

hene

d la

st y

ear.

The

com

bina

tion

of g

over

nmen

t spe

ndin

g, m

onet

ary

polic

y, a

nd

stru

ctur

al re

form

s ap

pear

s to

be

supp

ortiv

e of

eco

nom

ic a

nd p

rofit

gro

wth

, whi

le p

olic

y ta

ilwin

ds re

mai

n in

pla

ce a

s th

e B

OJ

mai

ntai

ns

‘99‘01

‘03‘05

‘07‘09

‘11‘13

‘15‘17

o S&

P 50

0M

SCI E

mer

ging

Mar

kets

Inde

x Re

lativ

e to

S&

P 50

0

Run

s in

Cyc

les

5/19

/17

mar

kets

secu

ritie

sin

volv

essp

ecia

ladd

ition

alris

ks.T

hese

risks

incl

ude,

buta

reno

tlim

ited

to,c

urre

ncy

Earn

ings

Boo

st: N

ot J

ust a

U.S

. Sto

ry9

Sour

ce: L

PL R

esea

rch,

Fac

tSet

05

/19/

17

Earn

ings

fore

cast

s ar

e ba

sed

on T

hom

son

Reut

ers

and

Fact

Set c

onse

nsus

.

Expe

ctat

ions

for

earn

ings

glo

bally

ha

ve in

crea

sed.

M

ore

evid

ence

th

ey w

ill b

e m

et is

re

quire

d fo

r us

to

incr

ease

inve

stm

ent.

RKET

S

ntil R

eady

digi

t re

turn

s fo

r th

e B

loom

berg

B

arcl

ays

Agg

rega

te B

ond

Inde

x. A

t th

at le

vel,

how

ever

, in

tern

atio

nal d

eman

d m

ay

once

aga

in r

etur

n as

val

uatio

ns

wou

ld b

ecom

e ve

ry a

ttra

ctiv

e re

lativ

e to

oth

er s

over

eign

s,

mos

t no

tabl

y to

Jap

anes

e G

over

nmen

t B

onds

(JG

B) a

nd

Ger

man

Bun

ds [

Fig

ure

11]

.

Ris

ks t

o ou

r ra

te c

all i

nclu

de

dela

ys in

pro

-gro

wth

po

licie

s, g

eopo

litic

al r

isk,

and

po

tent

ially

mix

ed m

essa

ges

from

eco

nom

ic d

ata.

As

dem

onst

rate

d ea

rlier

in t

he

year

, del

ays

in p

ro-g

row

th

polic

y co

uld

drag

dow

n lo

nger

-te

rm y

ield

s an

d su

ppor

t U

.S. T

reas

urie

s. G

eopo

litic

al

tens

ions

cou

ld fl

are

up a

t an

y tim

e (e

.g.,

Nor

th K

orea

, S

yria

) and

driv

e de

man

d fo

r

Tre

be an an lea

wo

De

m in

ou fix in

pr du str

as he Alt

be inc

to th div

as b

een

a pr

etty

goo

d fo

r eco

nom

ic a

nd

e se

e lit

tle s

tres

s rk

ets.

Of c

ours

e,

easu

ry p

rices

hav

e he

yie

ld c

urve

pp

roac

h to

tigh

teni

ng.

low

ing

a sh

arp

the

elec

tion,

per

iodi

c op

oliti

cal t

hrea

ts,

on, a

nd a

ttra

ctiv

e er

eign

s, h

ave

kept

er

, the

spr

ead

men

t-gr

ade

corp

orat

e es

, and

the

cost

to

te d

efau

lts h

ave

g th

reat

s [F

igu

re 1

0].

econ

omic

gro

wth

as

e ca

se f

or o

ne t

o n

2017

(m

akin

g tw

o bo

nd p

rices

und

er

such

, we

cont

inue

to f

avor

fixe

d-in

com

e po

sitio

ning

with

neu

tral

to

belo

w-b

ench

mar

k in

tere

st r

ate

sens

itivi

ty. D

espi

te

our

expe

ctat

ion

for

stab

ility

in c

redi

t m

arke

ts,

outp

erfo

rman

ce o

f th

e hi

gh-y

ield

sec

tor

rela

tive

to h

igh

-qua

lity

fixed

inco

me

has

led

to t

ight

sp

read

s ve

rsus

long

-ter

m a

vera

ges,

lim

iting

ret

urn

pote

ntia

l and

war

rant

ing

caut

ion

for

inve

stor

s.

With

litt

le a

dditi

onal

roo

m f

or c

apita

l app

reci

atio

n,

yiel

d is

poi

sed

to b

e th

e do

min

ant

driv

er o

f re

turn

.

Our

vie

w o

n in

tere

st r

ates

rem

ains

unc

hang

ed

from

the

firs

t ha

lf of

201

7. W

e co

ntin

ue t

o be

lieve

th

at t

he c

ombi

natio

n of

gov

ernm

ent

polic

y, c

entr

al

bank

pol

icy,

and

ste

ady

econ

omic

gro

wth

has

th

e po

tent

ial t

o pu

sh t

he 1

0-y

ear

Trea

sury

yie

ld

high

er, a

nd t

hat

our

year

-end

tar

get

of b

etw

een

2.25

% a

nd 2

.75%

rem

ains

rea

sona

ble.

Our

bia

s is

to

war

d th

e up

per

end

of t

he r

ange

, and

we

coul

d se

e th

e 10

-yea

r Tr

easu

ry y

ield

ris

e as

hig

h as

3%

, sho

uld

Con

gres

s m

ake

mea

ning

ful p

rogr

ess

tow

ard

enac

ting

fisca

l stim

ulus

. Sce

nario

ana

lysi

s ba

sed

on t

his

pote

ntia

l int

eres

t ra

te r

ange

and

the

du

ratio

n of

the

inde

x in

dica

tes

low

- to

mid

-sin

gle

-

2015

2016

2017

te S

prea

d Hi

gh-Y

ield

Spr

ead

%3.5 3.0 2.5 2.0 1.5 1.0 0.5 0.0 -0.5

-1.0

‘07‘08

‘09‘10

‘11‘12

‘13‘14

10-Y

ear T

reas

ury

Yiel

d Ad

vant

age

to B

und

10-Y

ear T

reas

ury

Yiel

d Ad

vant

age

to

g C

onfi

denc

e in

Cre

dit M

arke

ts, b

ut E

xpen

sive

Val

uati

ons

05/

19/1

7

berg

Bar

clay

s U.

S. C

orpo

rate

Bon

d In

dex.

Opt

ion

adju

sted

spr

ead

for B

loom

berg

Bar

clay

s U.

S. C

orpo

rate

Hig

h

ble

mat

urity

Trea

surie

s

Trea

suri

es S

till

Sho

win

g P

ower

Rel

ativ

e to

Ger

man

Bun

d an

d JG

B11

Sour

ce: L

PL R

esea

rch,

Blo

ombe

rg

05/1

9/17

Inve

stin

g in

fore

ign

and

emer

ging

mar

kets

deb

t sec

uriti

es in

volv

es s

peci

al a

dditi

onal

risk

s. T

hese

ris

curre

ncy

risk,

geo

polit

ical

and

regu

lato

ry ri

sk, a

nd ri

sk a

ssoc

iate

d w

ith v

aryi

ng s

ettle

men

t sta

ndar

ds.

We

cont

inue

to

belie

ve th

at th

e co

mbi

natio

n of

go

vern

men

t pol

icy,

ce

ntra

l ban

k po

licy,

and

ste

ady

econ

omic

gro

wth

ha

s th

e po

tent

ial

to p

ush

the

10-

year

Tre

asur

y yi

eld

high

er, a

nd

that

our

yea

r-en

d ta

rget

of b

etw

een

2.25

% a

nd 2

.75%

re

mai

ns re

ason

able

.

To Ov

erloa

d

he

gro

wth

en

gin

e fo

r th

e U

.S. e

con

om

y an

d m

arke

ts is

ar

y p

olic

y is

po

wer

ing

do

wn

, bu

sin

ess

fun

dam

enta

ls

and

fisc

al p

olic

y an

d e

con

om

ic g

row

th a

re o

n t

he

ken

off

sta

nd

by.

Th

e Fe

d h

as s

ho

wn

incr

easi

ng

n

om

y h

as r

eco

vere

d a

nd

th

at m

arke

t fo

rces

can

n

seq

uen

tly,

we

loo

k fo

r fi

scal

po

licy

to s

up

ple

men

t as

th

e m

arke

t’s

nex

t d

rive

rs. I

n g

ener

al, c

on

sum

ers

eel p

rett

y g

oo

d a

bo

ut

eco

no

mic

co

nd

itio

ns.

Co

nsu

mer

fi

den

ce is

hig

h, l

ikel

y p

rovi

din

g t

he

nex

t b

oo

st t

o

inve

stm

ent.

full

tran

sfer

aw

ay f

rom

mo

net

ary

po

licy

hav

e d

ent

in h

ead

lines

in t

he

med

ia a

bo

ut

ho

w t

he

Tru

mp

ag

end

a m

ay b

e in

dan

ger

. Sto

ck m

arke

t le

ader

ship

has

t

ho

se a

reas

of

the

mar

ket

bes

t p

osi

tio

ned

to

ben

efit

d fi

scal

po

licie

s. T

he

late

st s

tall

cou

ld p

ush

th

e ke

y s

into

201

8, o

r p

oss

ibly

der

ail t

hem

. Th

e o

dd

s st

ill

ax r

efo

rm b

ein

g a

chie

ved

, wh

ile p

rosp

ects

fo

r th

e re

st

y b

eco

me

ten

uo

us.

inve

sto

rs t

o a

pp

reci

ate

the

imp

licat

ion

s o

f a

dri

ver.

Mu

ch li

ke a

po

rtfo

lio c

an b

enefi

t fr

om

e

eco

no

my

and

mar

kets

can

ben

efit

fro

m d

iffe

ren

t t

dif

fere

nt

tim

es. A

s m

on

etar

y p

olic

y p

ow

ers

do

wn

, en

tals

po

wer

up

, an

d w

e w

ait

for

fisc

al p

olic

y to

hel

p

om

y o

ff o

f st

and

by

mo

de,

we

ho

pe

LPL

Res

earc

h’s

A

Sh

ift

In M

arke

t C

on

tro

l will

en

able

yo

u t

o id

enti

fy

t m

ay a

rise

, nav

igat

e th

e ch

alle

ng

es t

hat

will

an

d h

elp

yo

u s

tick

to

yo

ur

lon

g-t

erm

inve

stin

g p

lan

.

IMPO

RTA

NT

DIS

CLO

SURE

S

The

opin

ions

voi

ced

in th

is m

ater

ial a

re fo

r gen

eral

info

rmat

ion

only

and

are

not

inte

nded

to p

rovi

de o

rsp

ecifi

c in

vest

men

t adv

ice

or re

com

men

datio

ns fo

r any

indi

vidu

al s

ecur

ity. T

o de

term

ine

whi

ch in

vest

myo

u, c

onsu

lt yo

ur fi

nanc

ial a

dvis

or p

rior t

o in

vest

ing.

All

perfo

rman

ce re

fere

nced

is h

isto

rical

and

is n

o Al

l ind

exes

are

unm

anag

ed a

nd c

anno

t be

inve

sted

into

dire

ctly.

Econ

omic

fore

cast

s se

t for

th m

ay n

ot d

evel

op a

s pr

edic

ted,

and

ther

e ca

n be

no

guar

ante

e th

at s

trat

succ

essf

ul.

Inve

stin

g in

sto

ck in

clud

es n

umer

ous

spec

ific

risks

incl

udin

g: th

e flu

ctua

tion

of d

ivid

end,

loss

of p

rinof

the

inve

stm

ent i

n a

falli

ng m

arke

t.

Ther

e is

no

guar

ante

e th

at a

div

ersi

fied

portf

olio

will

enh

ance

ove

rall

retu

rns

or o

utpe

rform

a n

on-d

iDi

vers

ifica

tion

does

not

ens

ure

agai

nst m

arke

t ris

k.

Bond

s ar

e su

bjec

t to

mar

ket a

nd in

tere

st ra

te ri

sk if

sol

d pr

ior t

o m

atur

ity. B

ond

and

bond

mut

ual f

unde

clin

e as

inte

rest

rate

s ris

e an

d bo

nds

are

subj

ect t

o av

aila

bilit

y an

d ch

ange

in p

rice.

Gove

rnm

ent b

onds

and

Tre

asur

y bi

lls a

re g

uara

ntee

d by

the

U.S.

gov

ernm

ent a

s to

the

timel

y pa

yme

inte

rest

and

, if h

eld

to m

atur

ity, o

ffer a

fixe

d ra

te o

f ret

urn

and

fixed

prin

cipa

l val

ue. H

owev

er, t

he v

agu

aran

teed

and

will

fluc

tuat

e.

Mor

tgag

e-ba

cked

sec

uriti

es a

re s

ubje

ct to

cre

dit,

defa

ult,

prep

aym

ent r

isk

that

act

s m

uch

like

call

r ipr

inci

pal b

ack

soon

er th

an th

e st

ated

mat

urity

, ext

ensi

on ri

sk, t

he o

ppos

ite o

f pre

paym

ent r

isk,

mar

k

Bank

loan

s ar

e lo

ans

issu

ed b

y be

low

inve

stm

ent-g

rade

com

pani

es fo

r sho

rt-te

rm fu

ndin

g pu

rpos

es w

ite

rm d

ebt a

nd in

volv

e ris

k.

Inve

stin

g in

MLP

s in

volv

es a

dditi

onal

risk

s as

com

pare

d w

ith th

e ris

ks o

f inv

estin

g in

com

mon

sto

ckca

sh fl

ow, d

ilutio

n, a

nd v

otin

g rig

hts.

MLP

s m

ay tr

ade

less

freq

uent

ly th

an la

rger

com

pani

es d

ue to

tw

hich

may

resu

lt in

erra

tic p

rice

mov

emen

t or d

ifficu

lty in

buy

ing

or s

ellin

g. M

LPs

are

subj

ect t

o si

gnbe

adv

erse

ly a

ffect

ed b

y ch

ange

s in

the

regu

lato

ry e

nviro

nmen

t, in

clud

ing

the

risk

that

an

MLP

cou

ldpa

rtner

ship

. Add

ition

al m

anag

emen

t fee

s an

d ot

her e

xpen

ses

are

asso

ciat

ed w

ith in

vest

ing

in M

LP

IND

EX D

EFIN

ITIO

NS

The

U.S.

Dol

lar I

ndex

(DXY

) ind

icat

es th

e ge

nera

l int

erna

tiona

l val

ue o

f the

U.S

. dol

lar.

The

DXY

Ind e

the

exch

ange

rate

s be

twee

n th

e U.

S. d

olla

r and

six

maj

or w

orld

cur

renc

ies.

The

S&P

500

Inde

x is

a c

apita

lizat

ion-

wei

ghte

d in

dex

of 5

00 s

tock

s de

sign

ed to

mea

sure

per

form

anec

onom

y th

roug

h ch

ange

s in

the

aggr

egat

e m

arke

t val

ue o

f 500

sto

cks

repr

esen

ting

all m

ajor

indu

s t

The

Bloo

mbe

rg B

arcl

ays

U.S.

Agg

rega

te B

ond

Inde

x is

a b

road

-bas

ed fl

agsh

ip b

ench

mar

k th

at m

eas

U.S.

dol

lar-d

enom

inat

ed, fi

xed-

rate

taxa

ble

bond

mar

ket.

The

inde

x in

clud

es T

reas

urie

s, g

over

nmen

tse

curit

ies,

MBS

(age

ncy

fixed

-rate

and

hyb

rid A

RM p

ass-

thro

ughs

), AB

S, a

nd C

MBS

(age

ncy

and

no

The

Bloo

mbe

rg B

arcl

ays

U.S.

Cor

pora

te B

ond

Inde

x m

easu

res

the

inve

stm

ent g

rade

, fixe

d-ra

te, t

axa

It in

clud

es U

.S. d

olla

r-den

omin

ated

sec

uriti

es p

ublic

ly is

sued

by

U.S.

and

non

-U.S

. ind

ustri

al, u

tility

The

Bloo

mbe

rg B

arcl

ays

U.S.

Cor

pora

te H

igh

Yiel

d Bo

nd In

dex

mea

sure

s th

e U.

S. d

olla

r-den

omin

ate

corp

orat

e bo

nd m

arke

t. Se

curit

ies

are

clas

sifie

d as

hig

h yi

eld

if th

e m

iddl

e ra

ting

of M

oody

’s, F

itch

abe

low

. Bon

ds fr

om is

suer

s w

ith a

n em

ergi

ng m

arke

ts c

ount

ry o

f ris

k, b

ased

on

Barc

lays

EM

cou

ntry

The

MSC

I Em

ergi

ng M

arke

ts In

dex

is a

free

floa

t-adj

uste

d, m

arke

t cap

italiz

atio

n in

dex

that

is d

esig

nm

arke

t per

form

ance

of e

mer

ging

mar

kets

.

The

MSC

I EAF

E In

dex

is a

free

floa

t-adj

uste

d, m

arke

t-cap

italiz

atio

n in

dex

that

is d

esig

ned

to m

easu

perfo

rman

ce o

f dev

elop

ed m

arke

ts, e

xclu

ding

the

Unite

d St

ates

and

Can

ada.

To Ef

ficien

cy

RES 5106 0617Tracking #1-615392 (Exp. 06/18)

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an

affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

Member FINRA/SIPC