MIDSTREAM CANADA LTD.€¦ · MIDSTREAM CANADA LTD. ... To de-risk full cycle hydrocarbon resource...

33

CORPORATE OVERVIE MIDSTREAM CANADA LTD. CREATING VALUE FEB 2016

-

Upload

doannguyet -

Category

Documents

-

view

214 -

download

0

Transcript of MIDSTREAM CANADA LTD.€¦ · MIDSTREAM CANADA LTD. ... To de-risk full cycle hydrocarbon resource...

CORPORATE OVERVIE

MIDSTREAM CANADA LTD.CREATING VALUE

FEB 2016

CONFIDENTIAL TO QUALIFYING

ACCREDITED AND SOPHISTICATED INVESTORS

DISCLAIMER: This presentation (the “Presentation”) in respect of Midstream Canada Ltd. (“MCL” or the “Company”) and its financial plans has been prepared by the Company solely for use by qualified exempt investors to assist in their evaluating the Company.

Nothing in this report is, or should be relied on as, a promise or representation, as to the future. All discussions about future events and expectations are speculative and merely management’s belief in that future based upon their reasonable knowledge and limited experience to date. In furnishing this Presentation, neither MCL, nor any of its affiliates undertake to provide the recipient with access to any additional information or to update this Presentation or to correct any inaccuracies therein which may become apparent. This Presentation is confidential to the recipient and his advisers. It and any further confidential information made available to the prospective investor must be held in complete confidence and documents containing such information may not be used or disclosed without prior written consent of the Company.

Prospective investors should not construe the contents of this Presentation as investment, legal, business, accounting, tax or other advice. In making an investment decision, prospective investors must rely on their own examination of MCL and the terms of the offering, including the merits and risks involved. The Company is a start-up company with all the risks inherent and management’s experience is limited and unproven in this endeavour. Each prospective Investor should consult his own attorneys, business advisers and/or tax advisers as to legal, business, accounting, tax and related matters concerning this offering. An investment in MCL involves significant risks. Investors should have the financial ability and willingness to accept the risk characteristics of an investment in MCL including the risk of losing the entirety of their investment.

NOTICE TO READER: The information contained herein is confidential and is intended only for the user or the person to whom it is directly given by a director or officer of MCL. Neither the plan nor any part of it may be copied, disclosed or transferred without express written consent of MCL.

MIDSTREAM CANADA LTD. (MCL)

INTRODUCTION

Opportunity

Vision

Execution Plan

Project Metrics

Repeatable Business Model

PROJECTS

Projects In Development

Projects for Development

Project for Execution – Quirk Creek

Description

Assumptions

Pro-forma

EXPERIENCE

Management Team

Strategic Relationships

APPENDIX

Finance

Capital Schedule

Capital Structure

Development Plan

Foothills Gas Development

North Coleman, Savanna Creek, Sullivan Creek

Gas Plant

Methanol Facility

Demand

Process / Technology

Project Description

Potential Locations

Compared to Liquefied Natural Gas (LNG)

Strategic Relationships

BSG Engineering

3

OPPORTUNITY

Current commodity market for oil and gas products has created extreme pressure on Producers to de-risk balance sheet, de-leverage debt ratio; a forced sale of assets, both resource and facilities

Traditional facility transactions will not create sufficient capital for Producers

Need for more than just a “Midstream Company”

Non-traditional midstream option for Producer exit

“New” and “Traditional” approach to Midstream/Resource relationship

Application of seasoned team with experience in

Midstream

Upstream resource development

Facility and Upstream Operations

Facility Design and Construction

“Energy Value Chain” Business Development

4

VISION

Repeatable Investments:

Strong EBITDA from infrastructure

Disciplined “Key Project Metrics”

Multi-year growth plan and deal flow

Multi-Billion dollar Market Cap

Numerous small to medium size projects

Multiple Commodity Markets

Price to Earnings Ratio for Infrastructure Companies > 10

5

Large CapEnterprise Product Partners

17.35

Kinder Morgan

36.49

Spectra Energy

19.1

Ultrapar Participacoes

17.26

Plains Midstream

17.2

Mid CAPMartin Midstream Partners

34

Valero Energy Partners

23.9

NGL Energy Partners

33

Philips 66 Partners

27.2

Semgroup Corp

31.2

Small CAPBluenight Energy Partners

18.0

Delek Logistics Partners

11.9

Par Pete Corp

12.0

Transmontaign Partners

11.6

World Point Terminals

13.8

Methanol/UreaMethanex

29.9

Methanol Chemicals Co.

30.0

*Price to Earnings ratio (P/E

for illustration only

EXECUTION PLAN

New & Traditional approach to Midstream/Resource relationship

New

To Purchase existing brownfield facilities

To take resources as the current and future fee to allow Producers to white map an area

Current commodity prices offer limited exposure to further resource write-down

Midstream Canada’s resource ownership positioned for resource value appreciation

Traditional

To help Producers monetize assets into fee for service business

To provide mezzanine financing and Cost-of-Service models

To target expansion into other low-risk energy opportunities

To de-risk full cycle hydrocarbon resource economics

Over riding objective

Long-term win-win relationship/partnership Producer to provide menu of financial

leveraging products

Arms length and independent commercial relationship, yet symbiotic

Low risk investment with growth opportunity

6

PROJECT METRICS

Pro Forma

18-22% Internal rate of Return (IRR)

15+ year project life cycle

Sustainable at low commodity price

Oil price WTI $40 USD / bbl

Gas price AECO $2.25 CDN / MMBtu

Located in Western Canada

Working Experience & Relationships

Talent Pool

Geo-Political Environment

Canadian dollar

7

REPEATABLE BUSINESS MODEL

Acquisitions based on 3 – 5 x Net Operating Income

Sound Economics

Expandable Facilities

Low commodity prices allow

Active deal flow

Cash flow positive opportunities

Project execution

Upside opportunity projects on new acquisitions

Sustainable revenue

Higher commodity prices means increased IRR than anticipated

Utilize progressive hedging which removes price volatility,

provides predictable and bankable revenue stream.

8

PROJECTS IN DEVELOPMENT9

Facility Location

Capacity

(MMScfd /

kbpd)

Current

(MMScfd /

kbpd)

Capital

(MM$ CDN)

EBITDA

(MM$ CDN)

Per yearStatus

Gas Plant Alberta 91 21 15 6.5 Operating

Gas Plant Alberta 23 0 ->23 44 8 Brown Field

Gas Plant Alberta 12 0->12 22 5 Brown Field

Gas Plant Alberta 25 0->25 48 9 Brown Field

Gas Plant Alberta 125 59 ->125 240 46 Operating

Gas Plant Alberta 273 120 267 53 Operating

Gas Plant Alberta 286 135 234 47 Operating

Battery Alberta 18 1 10 3 Operating

Methanol TBC–AB/BC/SK 67 67 495 126 Producing / Brown Field

Methanol/Urea TBC–AB/BC/SK 67 67 455 126 Producing / Brown Field

Total 969 417 1,830 418

*Data is in development phase, Battery not included in Total and Current Capacity

PROJECTS FOR DEVELOPMENT10

Facility Location

Capacity

(MMScfd /

kbpd)

Current

(MMScfd /

kbpd)

Capital

(MM$ CDN)

EBITDA

(MM$ CDN)

Per yearStatus

Gas Plant Alberta 91 21 15 6.5 Operating

Gas Plant Alberta 23 0 ->23 44 8 Brown Field

Gas Plant Alberta 12 0->12 22 5 Brown Field

Methanol TBC–AB/BC/SK 67 67 495 126 Green Field

Total 193 95 576 145

*Data is in development phase

PROJECTS FOR EXECTION11

Facility Location

Capacity

(MMScfd /

kbpd)

Current

(MMScfd /

kbpd)

Capital

(MM$ CDN)

EBITDA

(MM$ CDN)

Per yearStatus

Gas Plant Alberta 91 21 15 6.5 Operating

Total 91 21 15 6.5

GAS PLANT

90MM Scfd Sour Gas Plant with Sulfur Recovery

1 hour SW of Calgary

High replacement cost due to location

Letter of Interest (LOI) due January 26, 2016-completed

Acquisition Price $15 MM agreed by both parties

Adjusted Net Operating Income – Base case

2016 $6.5 MM / year

2.1-year payout / 2.3 x adjusted net operating income

Upside opportunities

20%+ additional acquired gas

50%+ additional fee gas

Adjusted Net Operating Income – High case

2016 $9.9MM / year

1.5-year payout / adjusted net operating income

Adjusted Net Operating Income – Low case

8 year payout at $1.50 / M Scf

12

GAS PLANT13

2012 2013 2014 2015

Capacity (MM Scfd) 90.5 90.5 90.5 90.5

Raw Gas (MM Scfd) 37 29 30 28

Sales Gas (MM Scfd) 27 19 20 21

NGL (bpd) 1850 1830 1810 590

Sulphur (ton/d) 115 75 93 68

Annual Fee ($MM) $13.5 $10.6 $10.9 $8.4

*Data is in development phase

RESERVERS14

Producer Field Formation Production Reserves

Mississippian 9.4 MMScfd 45 Bcf 1P

56 Bcf 2P

Mississippian 10.9 MMScfd tbd

Cardium 0.6 MM Scfd tbd

Gas Plant Background

Plant includes gas sweetening & sulphur

recovery and NGL mix recovery

FINANCIAL ASSUMPTIONS15

Base Case

Acquired resource production

9.4 MM Scfd (Sales)

590 bpd Natural Gas Liquids

68 t/d Sulphur

3% decline, 20 year reserve life

Fee Income Gas

0.7 MM Scfd @ $0.7/M Scf Crimson Oil & Gas (Raw)

10.9 MM Scfd @ $1.61M Scf Crescent Point (Raw)

Revenue Adjustments

Sproule 2014 commodity pricing

$0.15 / M Scf transportation cost

Operating expense Adjustments

$4.6 MM/year annualized turn around costs

$1 MM/ year abandonment fund

High Case

Add 2 MM Scfd shut-in from acquired resource

production

Add 5 MM Scfd shut-in from 3rd Party fee

income @ $1.00 / m Scf

Low Case

Aeco at $1.50 / M Scf

Fee Income Gas reduced by 25% due to

commodity prices, however AER regulations

would likely keep the wells flowing to avoid

significant suspension / abandonment costs

PRO FORMA –Base16

Acquisition:Capital Cost $15 million CDN

Capacity 91 MMScfd

Current 21 MMScfd

Economics:IRR (BT/AT) 77 / 54%

10% NPV $66 million CDN

Cum. Cash Flow $110 million CDN

Pay-Out 2.1 years

0.000

5.000

10.000

15.000

20.000

25.000

2016 2018 2020 2022 2024 2026 2028 2030

mm

cf/

d

year

Forecast

Crescent Point Crimson Oil & Gas Pengrowth Quirk Crk. - Gas

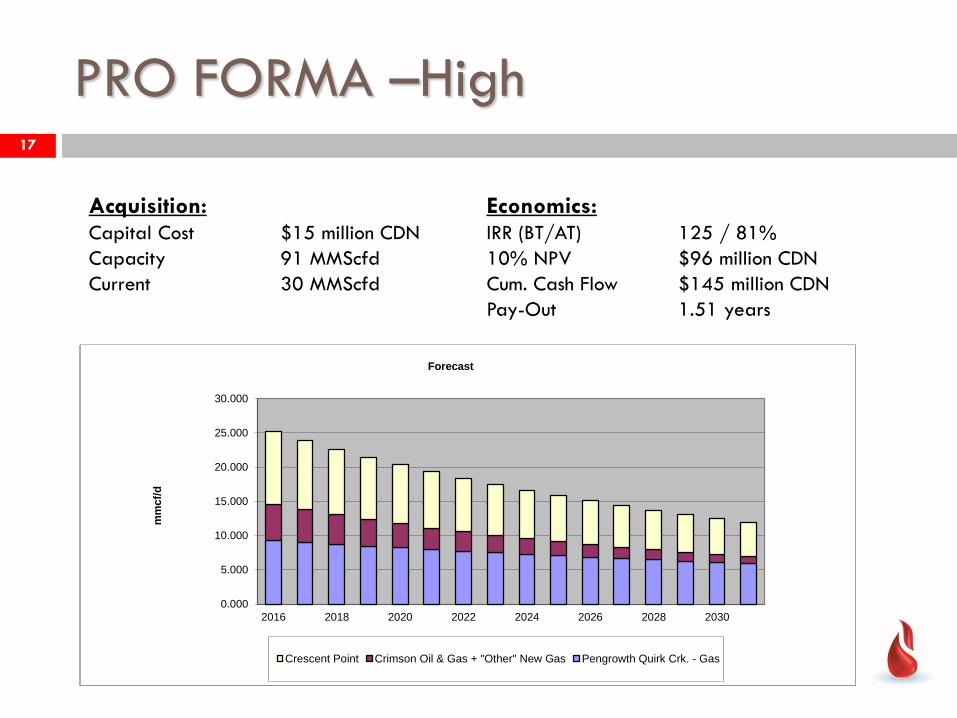

PRO FORMA –High17

Acquisition:Capital Cost $15 million CDN

Capacity 91 MMScfd

Current 30 MMScfd

Economics:IRR (BT/AT) 125 / 81%

10% NPV $96 million CDN

Cum. Cash Flow $145 million CDN

Pay-Out 1.51 years

0.000

5.000

10.000

15.000

20.000

25.000

2016 2018 2020 2022 2024 2026 2028 2030

mm

cf/

d

year

Forecast

Crescent Point Crimson Oil & Gas Pengrowth Quirk Crk. - Gas

0.000

5.000

10.000

15.000

20.000

25.000

30.000

2016 2018 2020 2022 2024 2026 2028 2030

mm

cf/

d

year

Forecast

Crescent Point Crimson Oil & Gas + "Other" New Gas Pengrowth Quirk Crk. - Gas

PRO FORMA –Low18

Acquisition:Capital Cost $15 million CDN

Capacity 91 MMScfd

Current 18 MMScfd

Economics:IRR (BT/AT) 0 / 0%

10% NPV $66 million CDN

Cum. Cash Flow NA

Pay-Out 8 years

0.000

5.000

10.000

15.000

20.000

25.000

2016 2018 2020 2022 2024 2026 2028 2030

mm

cf/

d

year

Forecast

Crescent Point Crimson Oil & Gas Pengrowth Quirk Crk. - Gas

0.000

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

20.000

2016 2018 2020 2022 2024 2026 2028 2030

mm

cf/

d

year

Forecast

Crescent Point Crimson Oil & Gas Pengrowth Quirk Crk. - Gas

MCL TEAM

Experienced Management Team

Strategic Relationships

BSG Engineering – EPCM

Construction being finalized

19

MANAGEMENT TEAM

Neeky Noor-Ali, P.Eng., President, Director

B.Sc. Mechanical Engineering, University of Calgary

20+years experience

Founder and President of BSG Engineering – EPC on over $500

million Surface Facilities projects in just over 7 years

Founder of Bitumen Energy – Heavy Oil Technology Solutions

TBC, Vice President Finance

B. Comm., University of Saskatchewan

25+ years experience

Director of Optimization, Director of Natural Gas Suncor Energy

Vice President Commodity Marketing, Trading and Risk Management

Deloitte

Ben VanRootselaar, P.Eng. Vice President Engineering

B.Sc. Mechanical Engineering, University of Alberta

35+ years experience

Development Engineer Talisman Midstream

Vice President Engineering Trafina Energy

Vice President Operations Tornado Resources

Senior Engineer Gas Department and Sothern Production Supervisor,

Reservoir Engineer, Joint Venture Coordinator Dome Petroleum

Sujit Sarkar, P.Eng., Vice President Operations

B.Sc. Mechanical Engineering, University of Newcastle-Upon Tyne

M.Sc. Material Engineering, Council of National Academic Awards

40+ years experience

Founder and President of ACS Engineering

Three new technologies Sulfire, BFU, Enhanced BFU

Technical Director of Process & Mechanical for Fluor Daniel

o Head of the Heat Transfer Group Worldwide

o Direct hands on engineering experience for 44 major clients

worldwide (including Suncor, Syncrude, Shell, Esso, CNRL,

Methanex) development of specifications, start-ups, shutdown

logics, feasibility and economic studies, process simulations,

design engineering, procurement, commissioning

Tony Kuehne, Vice President Business Development

B. Ma. Economics, University of Lethbridge

30+ years experience

VP Gas Marketing and Business Development Quicksilver Canada

Team Leader Strategic Development, Talisman Energy

Director Business Development/Transmission AltaGas

20

SUMMARY

Opportunity

Low Commodity Prices

De-Risk Full Cycle Hydrocarbon Resource Economics

Vision

Multi-billion dollar Market Cap Potential

Business Plan

Starter Kit with Immediate Cash Flow i.e. Return on Investment

Steady growth with repeatable business model

Experienced Team

Business Development

Finance

Engineering & Operations

21

Contact Information

Nèeky Noor-Ali, P.Eng., President

Tel: 403-630-4148

Email: [email protected]

Address:

400, 909 17 Avenue SW

Calgary, Alberta

T2T 0A4

22

APPENDIX

MIDSTREAM CANADA LTD.CREATING VALUE

APPENDIX - FINANCE

MIDSTREAM CANADA LTD.CREATING VALUE

APPENDIX - DEVELOPMENT PLAN

MIDSTREAM CANADA LTD.CREATING VALUE

APPENDIX – FOOTHILLS

MIDSTREAM CANADA LTD.CREATING VALUE

APPENDIX – METHANOL

MIDSTREAM CANADA LTD.CREATING VALUE

APPENDIX – Strategic Relationships

MIDSTREAM CANADA LTD.CREATING VALUE

MCL TEAM

Strategic Relationships

BSG Engineering – EPCM

Construction being finalized

29

EXPERIENCE MATRIX

NAME DICIPLINEYRS

of

EXP

Pip

elin

es

Natu

ral

Gas

Faci

lities

Oil F

aci

lities

Refi

nin

g

Ch

em

ical

/ P

etr

och

em

ical

Po

wer

Pla

nt &

Utilities

Pro

ject

Man

agem

en

t

Pro

cess

Desi

gn

Mech

an

ical

Equ

ipm

en

t

En

vir

on

men

tal

Sta

rt-u

p /

Co

mm

issi

on

ing

Pla

nt Safe

ty/O

ps

HA

SO

Ps

EU

/ N

A C

od

e S

tan

dard

s

Ele

ctri

cal

Desi

gn

Fo

un

datio

n/

Site P

rep

Co

gen

era

tio

n

Nu

mb

er

of

Majo

r C

lien

ts

S. Sarkar, P.Eng. Mechanical Engineer 35+ 44

N. Noor-Ali, P.Eng. Project Management 20+ 5

R. Langen, P.Eng. Project Management 35+ 8

S. Noor-Ali, P.Eng. Process Engineer 35+ 16

T. Morris, P.Eng. Process Engineer 35+ 18

P. Cechmanek, P.Eng. Mechanical Engineer 35+ 10

G. Silverberg Mechanical Engineer 35+ 9

L. Sobry, P.Eng. Electrical Engineer 30+ 17

E. McHeriuk, P.Eng. Electrical Engineer 35+ 14

J. Mellepurran Design 25+ 8

B. Gilbert Procurement 35+ 12

PROJECTS

Enhanced Oil Recovery

Kerrobert, Saskatchewan Water Flood Project

40,000 bbl/day water injection facilities

100+ wells tied in with more than 200km pipeline

Oil Treating Battery and Gas Plant Upgrade

Regulatory, Engineering, Procurement, Construction Management

Oil Production Facilities

100+ producing wells tied to Satellites and pipeline to Central Processing Facility

100km main truck pipeline

Standardized Design for efficient execution

Regulatory, Engineering, Procurement, Construction Management

Midstream Pipeline & Storage

8” 54 km Sales Oil Pipeline

10,000 bbl/day pumping station with sales meter

30,000 bbl tank farm

Internal & 3rd Party trucking facilities

Regulatory, Engineering, Procurement, Construction Management

Oil Treating Facility

Plato, Saskatchewan Oil Treating Battery

10,000 bbl/d capacity

Fast Track green field project

Regulatory, Engineering, Procurement, Construction Management

Expertise Provided with CoMmitment (EPCM)

Oilsands Steam Generation

Fort McMurray, Alberta Oilsands Project

30,000 bbl/day oil production facility

Trouble shooting Once Through Steam Generators for steam injection into the bitumen reservoir

Fertilizer Plant Upgrade

Carseland, Alberta

De-bottleneck and improve production by retrofitting equipment

Reformer simulation and modifications

Methanol Facility

Trinidad Grass Roots Facility

5,000 tone per day production

Engineering review and design

Methanol MTBE Facility

Umm Sa’id, Qatar

2,500 tone per day methanol and 1,630 tonne per day MTBE production

Front end engineering, design and procurement of long lead equipment

Facility design including utilities, offsites and infrastructure

Expertise Provided with CoMmitment (EPCM)

Consultant Specialist

PROJECTS

PROJECT LIFE-CYCLE

Expertise Provided with CoMmitment (EPCM)

SCOPE

• Simulation

• Concept Design

• Estimate

• Feasibility Studies

• Regulatory

• Site Planning

DESIGN

• Front End Engineering and Design

• Detail Engineering

• Project Controls

• Procurement

• Safety

CONSTRUCTION

• Cost Control

• Technical Support

• Contractors

• Equipment mobilization

• Material planning

• Quality Control

• HSE

START-UP

• Commissioning

• Systems check

• Turn over

OPERATIONS & MAINTENANCE

• Optimization

• Equipment Management

• Integrity Programs

• Maintenance Turn around

CLEAN UP/DISPOSAL

• Environmental remediation

• Decontamination

• Demolition