Middle East Point of ViewAugust 2010 - Deloitte · IFIs (GIFI) and comes at a critical time of...

60

Middle East Published by Deloitte & Touche (M.E.) and distributed to thought leaders across the region. August 2010 Point of View The neglected essence of Islamic Finance Talent advancement Women in the public sector Any silver lining to this cloud? IFRS Looking ahead Tourism, Hospitality & Leisure Point of no return Human Resources One stop shop Public Sector

Transcript of Middle East Point of ViewAugust 2010 - Deloitte · IFIs (GIFI) and comes at a critical time of...

Middle EastPublished by Deloitte & Touche (M.E.)and distributed tothought leadersacross the region.

August 2010 PointofViewThe neglected essence of Islamic Finance

Talent advancementWomen in the public sector

Any silver lining to this cloud?IFRS

Looking aheadTourism, Hospitality &Leisure

Point of no returnHuman Resources

One stop shopPublic Sector

2 | August 2010 | A Middle East Point of View

August 2010Middle East Point of ViewPublished by Deloitte & Touche (M.E.)

www.deloitte.com

A Middle East Point of View | August 2010 | 3

A word from theeditorial team

'Islamic Finance' seems to be the new buzzword in business circlesthese days. And with good reason. With an estimated 1.8 billionpotential consumers, the Islamic world presents a huge potential forbusinesses worldwide. Banking is one industry that has taken advantageof this potential. Since the opening of the first commercial Islamic bankin 1975, Islamic finance assets have grown to an estimated USD 950billion in 2009, defying a recessive market.

But not all is well in the land of Takaful and Shari'a. The pressure now ison these financial institutions to maintain authenticity and integratefully into the mainstream global financial market. In this issue of MiddleEast Point of View ( ME PoV) we take an in-depth look at IslamicFinance and examine its need to invest in an asset it has sometimesbeen missing: thought leadership.

That is not all what is on offer in ME PoV. In our tradition of sharing theexpertise and independent views of our partners and practitioners, andhosting visiting authors, we offer you a select array of pieces on manyhot topics in the region, that include opinions on financial marketefficiencies, developments in the Middle East hospitality industry, an in-depth piece on the current unwinding of the global economy, an expertopinion on the protection of company data on informationsuperhighways, and an analysis of how the public sector in the GCC ismaking strides in providing services to its citizens.

Moreover and with talent related concerns uppermost on the minds ofregional leaders, we dedicated two articles on talent related topics.When it comes to gender equality, few achievements can compare withthe rising role of women in governments worldwide, so we share withyou a Deloitte study and recommendations on how the private sector inthe region can look at lessons from the public sector. But are theseenough? A close look at the Human Resource services in the regionpoint in one direction only: that of 'No Return'.

And lastly, will 2010 see the emergence of one language in financialreporting, that of IFRS? Or will the GCC region take to VAT? Probablynot but we will certainly continue to inform you about all the burningissues in, and of interest to, the region in what we aim to be a timely,though not time-constrained, publication.

We hope that this issue delivers on its promise of being both engagingand informative.

ME PoV editorial team

4 | August 2010 | A Middle East Point of View

In this issue

Thought leadership: the neglectedessence of Islamic FinanceHatim El Tahir

The long unwinding roadIra Kalish

Tourism, Hospitality & Leisure in the Middle East:ready to move to the next levelRobert O’Hanlon

IFRS: the ultimate choice of the accounting world orwill the “IASB” march to a different drummer?Abass Ali Mirza

Market efficiency in the GulfBen Moore

Have governments been quicker than corporationsto advance talented women?Rana Ghandour Salhab

6

10

18

22

26

28

Contents

A Middle East Point of View | August 2010 | 5

Trends in government services in the GCC countriesAbdelhamid Suboh

An introduction to VATJustin Whitehouse

The time to change is now: enhancing HRservice delivery across the Middle EastLinda Jarnhamn

Protecting what mattersFadi Mutlak

New thought leadership publications from Deloitte

32

38

42

50

56

Table of contents

A Middle East Point of View | August 2010 | 7

Islamic Finance

Thoughtleadership:the neglectedessence ofIslamic Finance

Have Islamic Financial Institutions(IFIs) around the world, including theGulf region, been so busy structuringproducts and services that they haveoverlooked the importance ofcommunicating the essence of IslamicFinance? This brief analysis suggeststhat investing in thought leadershipprograms, a hitherto neglected assetclass, is an essential tool for thecontinuity, practice synergy andimproved business performance of IFIs.However, past experience of IFI practicedifferences, regulatory discrepanciesand market divergences show thatpractice harmonisation has achallenging path ahead.

8 | August 2010 | A Middle East Point of View

Regulatory inconsistencies within some practice areas ofIslamic finance has inhibited industry growth andcreated performance gaps. More importantly, they haveslowed its expansion and integration into the worldfinancial market. It is evident that IFIs, largely driven bycommercial goals, have not done enough to conversethe fundamental nature of educating andcommunicating Islamic Finance’s social and economicvalue propositions.

This is an issue that is high on the agenda of several GulfIFIs (GIFI) and comes at a critical time of their history forthree reasons: since the early twenty first century, GIFIshave expanded by leaps and bounds both in marketcapitalization and cross-border investments. Secondly,they have developed important institutional regulatoryand industry frameworks designed to improve servicesand standardize practice. Thirdly, concerns about theirstructures, operations and practices pose specialchallenges for long-term sustainability.

Leverage on practice synergiesUndoubtedly, thought leadership in Islamic Finance isplaying an increasingly important role in many individualorganizations. What is missing is a more holistic andstrategic approach to identify and align industry leadersto develop, adapt and enforce a harmonized andstandardized set of best practices. The commonattributes for such an approach include developing acoherent code of practice that addresses the differentfinancial and Sharia governance and applicationmethods within the industry worldwide. Hence, athought leadership initiative becomes the lead advocate for this task, which will be aimed at measuring,

improving and adapting a Unified Code of Practice(UCOP) in Islamic Finance.

The process of aligning industry stakeholder practicesand the more ambitious goal of developing a unifiedcode of practice are of paramount importance.Nevertheless, the success of a thought leadershipinitiative relies on developing a workable, yet efficient,model to energize thought leadership programs in theindustry and benefit from the experience of differentpractices across the world.

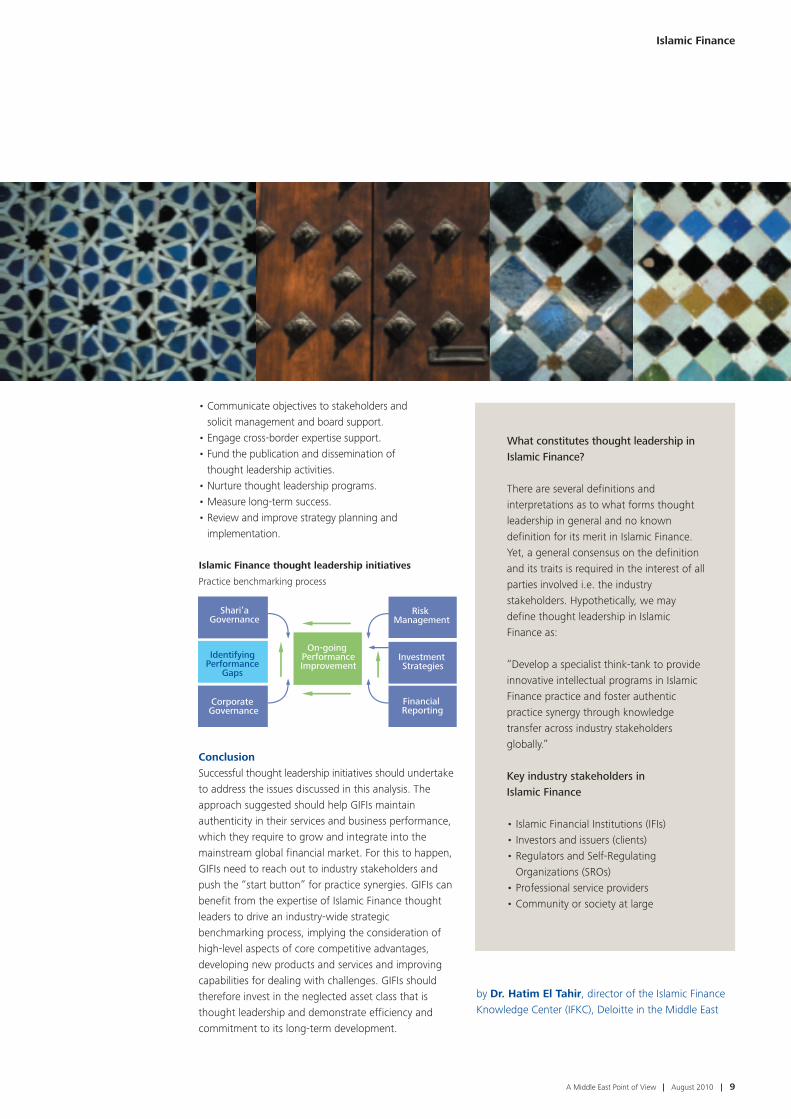

Strategic benchmarking in practiceA thought leadership initiative in Islamic Finance requiresthe collective efforts and support of its industrystakeholders. The factors underpinning its effectivenesslie in creating a sense of urgency and unified responsesto the challenges that impede its growth and prosperity.This can be achieved through a strategic benchmarkingprocess to identify best practices within the industry, forexample, the products and services created, offered anddelivered by GIFIs. The main objective of this process isto understand, evaluate and improve performance gapsand differences in practice. This is especially relevant forIFIs within the GCC countries, let alone practices in otherjurisdictions such as Malaysia or Europe.

There are five broad areas of thought leadershipproposals for benchmarking research, assessment andimprovement of practices. These are:• Shari’a Governance and Compliance• Liquidity Management Instruments• Risk Management and Development of Risk

Mitigating Tools (RMTs)• Investment and Capital Market Strategies • Financial Reporting Procedures• Corporate Governance Frameworks

The opposite chart draws the features of an IslamicFinance thought leadership initiative. It highlights theimportance of a strategic practice benchmarkingapproach. The process can be used to identifyperformance gaps within the industry practices indifferent aspects of organizations and operations. Thecrux of this process is the ongoing performanceimprovement to sustain best practices in Islamic Finance.

For this approach to work, industry stakeholders have toendorse, support and commit to the strategic long-termdevelopment of thought leadership initiatives. Thefollowing factors are largely desirable for a meaningful thought leadership initiative:• Identify thought leadership objectives and

strategic direction.

Thought leadership in IslamicFinance is playing an increasinglyimportant role in many individualorganizations. What is missing isa more holistic and strategicapproach to identify and alignindustry leaders to develop, adaptand enforce a harmonized andstandardized set of best practices.

A Middle East Point of View | August 2010 | 9

• Communicate objectives to stakeholders and solicit management and board support.

• Engage cross-border expertise support.• Fund the publication and dissemination of

thought leadership activities.• Nurture thought leadership programs.• Measure long-term success.• Review and improve strategy planning and

implementation.

Conclusion Successful thought leadership initiatives should undertaketo address the issues discussed in this analysis. Theapproach suggested should help GIFIs maintainauthenticity in their services and business performance,which they require to grow and integrate into themainstream global financial market. For this to happen,GIFIs need to reach out to industry stakeholders andpush the “start button” for practice synergies. GIFIs canbenefit from the expertise of Islamic Finance thoughtleaders to drive an industry-wide strategicbenchmarking process, implying the consideration ofhigh-level aspects of core competitive advantages,developing new products and services and improvingcapabilities for dealing with challenges. GIFIs shouldtherefore invest in the neglected asset class that isthought leadership and demonstrate efficiency andcommitment to its long-term development.

Islamic Finance

by Dr. Hatim El Tahir, director of the Islamic FinanceKnowledge Center (IFKC), Deloitte in the Middle East

IdentifyingPerformance

Gaps

Risk Management

Financial Reporting

Shari’aGovernance

Corporate Governance

Investment Strategies

On-going PerformanceImprovement

Islamic Finance thought leadership initiatives

Practice benchmarking process

What constitutes thought leadership in Islamic Finance?

There are several definitions andinterpretations as to what forms thoughtleadership in general and no knowndefinition for its merit in Islamic Finance.Yet, a general consensus on the definitionand its traits is required in the interest of allparties involved i.e. the industrystakeholders. Hypothetically, we maydefine thought leadership in IslamicFinance as:

“Develop a specialist think-tank to provideinnovative intellectual programs in IslamicFinance practice and foster authenticpractice synergy through knowledgetransfer across industry stakeholdersglobally.”

Key industry stakeholders in Islamic Finance

• Islamic Financial Institutions (IFIs)• Investors and issuers (clients)• Regulators and Self-Regulating

Organizations (SROs)• Professional service providers• Community or society at large

10 | August 2010 | A Middle East Point of View

In the decade prior to the current economic crisis,there was strong consumer spending growth inthe United States as well as in smaller economiessuch as the United Kingdom, Spain and Ireland.To simplify what happened, such growth wasfunded, in part, by borrowing against theincreased value of homes, itself the result of aflood of liquidity from surplus countries such asChina. This excessive consumer spending growthwas not only the principal source of economicgrowth in these countries, it also fueled export-driven growth in surplus countries such as China,Japan and Germany. In fact, the symbiosisbetween these “consuming” and “producing”groups of countries was the hallmark of theglobal economy in the first decade of the twenty-first century.

All that will now change.

The longunwindingroadSetting the stage

Global consumers and the economic imbalance

A Middle East Point of View | August 2010 | 11

12 | August 2010 | A Middle East Point of View

The global economic crisis of 2008-09 exposed the faultlines of the imbalanced global economy. When theinflated values of property-based assets peaked andthen collapsed, global financial institutions sufferedhuge losses. The resulting loss of confidence caused anear shutdown in global credit markets as investors fledto the safety of short-term government securities.Moreover, indebted consumers were forced todramatically shift gears. They increased savings, paid offdebts and ceased to spend with abandon. Of course thiscrisis, like all economic crises, will eventually end, andthe global economy will recover – indeed there aresignificant indications that recovery is now under way.Yet the global pattern of consumer spending of the pastdecade will not return.

In the coming decade, the countries that borrowedheavily to finance excessive consumer spending mayexperience slower consumer spending growth ashouseholds struggle to de-leverage, repair tatteredbalance sheets and accumulate wealth for futureretirement and other needs. More of the economicgrowth of these countries will likely be driven byexports, business investment and government spending.Conversely, those countries whose growth was fueledby exporting to borrowing countries will no longer beable to depend on such markets. The U.S. consumer willnot be able to sustain China’s export sector as it did inthe past. Consequently, countries such as China will shiftaway from export-oriented growth toward growthdriven by consumer spending. The degree to which thisadjustment takes place, and takes place smoothly, willdepend on the policies put in place by variousgovernments. Nevertheless, an adjustment of some sortwill definitely take place.

For those global companies that sell goods and servicesto consumers (such as those in retailing, consumerproducts, hospitality and even retail financial services)the next decade will entail a very different businessenvironment than that of the past decade. Not only willthe growth of consumer spending shift geographically,the nature of consumer spending will shift as well.

Why can’t the pattern of the past

continue indefinitely?

The answer is that the strength of consumer spending in

debtor nations was based on factors that cannot be

sustained. For example, U.S. consumer spending was

able to grow faster than consumer income because the

personal savings rate continuously declined until it was

close to zero. For obvious reasons, it cannot go below

zero in perpetuity. Hence, the growth of consumer

spending must necessarily slow down, even if

consumers don’t increase their savings. In addition, the

ability of consumers in the United States and the United

Kingdom to take on large debts was predicated on the

willingness of foreigners to lend to these countries. That

flow of capital cannot be taken for granted, especially as

those foreigners have suffered sizable capital losses

already. China, for example, has expressed serious

concern about the declining value of its dollar holdings.

During the past decade, the United States consumed

more than it produced and borrowed from the rest of

the world to make up the difference. This difference

was the U.S. current account deficit. At its peak, it was

roughly $700 billion, or over 6 percent of U.S. GDP. The

counterpart to this was a massive surplus in the rest of

the world, principally China, Japan and the oil exporting

countries of the Middle East. This massive imbalance in

the global economy was partly sustained by China’s

desire to maintain a low-valued currency. Hence, the

Chinese central bank purchased dollars in order to hold

down the value of the Chinese renminbi. In so doing, it

enabled its exports to remain inexpensive and many

Chinese workers to remain employed.

When China bought dollars, it represented a flow of

capital into the United States. The result was downward

pressure on U.S. long-term interest rates. This flow of

cheap capital, in turn, probably contributed to the

bubble in the U.S. housing market. The rising value of

property meant that consumers could achieve wealth

without saving, especially as it was easy for them to

borrow against the increasing value of their homes.

If this situation were to continue, it would require that

During the past decade, theUnited States consumed morethan it produced and borrowedfrom the rest of the world tomake up the difference. Thisdifference was the U.S. currentaccount deficit.

A Middle East Point of View | August 2010 | 13

the United States achieve a dangerous andunprecedented level of external debt (it is alreadyunprecedented). This would very likely lead investors toshy away from dollar denominated assets, therebyleading to a collapse in the value of U.S. assets.Something like this actually happened during the pastyear, but a continuation of global imbalances wouldprobably create an even greater problem.

RebalancingThe economist Herbert Stein once wrote that “ifsomething cannot go on forever, it will stop.” In someways, that describes the imbalance in the globaleconomy. It may not stop, but at least for the nearfuture it won’t get bigger and likely will get smaller.What is uncertain, however, is the manner in which theimbalance will be corrected. There are a number ofthings that could happen.

Reducing the imbalance means that the United Statesand other debtor countries like the United Kingdommust save more, import less and export more thanwould otherwise be the case. The path to this usuallyincludes currency depreciation (already under way),which would change the relative prices of traded goods,thereby stimulating exports and suppressing imports. ForChina, adjustment means undertaking measures tostimulate consumer spending. This could includeliberalizing consumer finance, improving the social safetynet so as to discourage saving, and allowing thecurrency to appreciate in value.

There are indications that China intends to move in thisdirection, but there are obstacles as well. First, China’sgovernment appears to be of two minds on the currency.On the one hand, it wants to encourage domesticdemand so that it need not accumulate more foreigncurrency reserves. On the other hand, it complains aboutthe potential capital loss on its existing reserves shouldthe dollar fall further. During the economic crisis, Chinastopped allowing the currency to appreciate lest it harmits export competitiveness. However, once globalrecovery is fully extant, China is likely to allow furtherrevaluation. The question is how much.

Second, China’s response to the crisis was to massivelystimulate investment in infrastructure and state-ownedcompanies. The result is an economy distorted byexcessive investment and insufficient consumer demand.If the consumer is to play a bigger role in the economygoing forward, China will have to adjust policyaccordingly. The degree to which this will take placeremains uncertain.

If China and the United States do all the right things,then adjustment in the global economy should gosmoothly. The growth of global consumer spending willshift away from the United States and toward China. Ifpolicymakers fail to act, however, then the road toadjustment could be bumpy. It could, for example, entailvolatility in financial markets especially currency markets that could have onerous consequences foreconomic growth.

How will U.S. adjustment take place?It is not sufficient to predict that American consumerswill simply decide to spend less in the future. Somethingwill compel them to do this, and there are several factors that will likely contribute to a significant shift inU.S. consumer behavior. First, the destruction of wealththat has transpired over the past two years (roughly $14trillion) will not be reversed quickly unless both theequity and property markets experience unusually rapidprice increases. Thus, consumers will feel the necessity torebuild wealth by saving, a process that has already begun.

Second, given the destruction of housing wealth, mostconsumers will no longer be in a position to borrowagainst increased property values. Thus, consumerspending will be constrained by income. Third, whilefinancial markets are showing signs of recovery, historysuggests that banks will remain cautious in their lendingbehavior for some time to come. Thus, consumer creditwill not be as readily available as in the recent past.

For those global companies thatsell goods and services toconsumers (such as those inretailing, consumer products,hospitality and even retailfinancial services) the next decadewill entail a very differentbusiness environment than thatof the past decade.

Global consumers and the economic imbalance

Moreover, prospective changes to the regulatoryenvironment will likely exacerbate this factor. If banksare forced to hold more capital, and if the market forsecuritization remains a shadow of its former self, therewill be less credit available for consumers.

Fourth, other areas of government policy may play a rolein restricting consumer spending. Increased taxes onupper income households will have a negative impacton spending. In addition, efforts to restrict emissions ofcarbon gases are likely to increase the price of energy,thus shifting consumer spending away from othergoods and services. Finally, there is the elusorypsychological factor. That is, the length and depth of therecent recession, the worst of the post-war era, mayhave a lasting impact on the willingness of consumers toengage in risky behavior. This may compel a permanentshift toward more frugal spending (fewer big ticketitems purchased, more discount shopping).

Is China big enough to make a difference?If China does all the right things to boost consumerspending and suppress export growth, will the Chineseconsumer alone be sufficient to offset the declininggrowth of U.S. consumer spending? The answer is thatit depends on what happens.

In 2008, for example, China’s consumer spending wasonly 15 percent of U.S. consumer spending whenmeasured at current exchange rates. Now, consider thefollowing plausible scenario for future growth. Supposethat, over the next decade, Chinese GDP grows 9percent per year and consumer spending grows 12percent per year. Also, suppose that U.S. GDP grows 3percent per year and consumer spending grows 2percent per year. Under this scenario, Chinese consumerspending rises from an unusually low 36 percent of GDPin 2008 to 50 percent of GDP in 2020. This wouldrepresent an increase in consumer spending in 2020 of$1.7 trillion above what it would have been with nochange in share of GDP. In the United States, consumerspending drops from 72 percent of GDP to 64 percentof GDP. This would represent a decline in consumerspending of $1.7 trillion below what it would have beenif consumer spending had remained 72 percent of GDP.Thus, the dollar value of the drop in consumer spendingas a share of GDP in the United States will ultimately beoffset by the dollar value of the increased share inChina, but not until 2020. This is a long adjustment.

In other words, even in an optimistic yet plausiblescenario, China’s boost to consumer spending takes a

Even in an optimistic yetplausible scenario, China’s boostto consumer spending takes along time to offset the decline inthe United States.

14 | August 2010 | A Middle East Point of View

A Middle East Point of View | August 2010 | 15

long time to offset the decline in the United States. Theimplication is that, for the global economy to adjust toa relatively quick shift in U.S. consumer spending,several large economies will have to boost consumerspending significantly. Otherwise, global growth couldbe stymied and currency markets could becomeexcessively volatile. The most likely candidates to playthat role are Japan and Germany, both huge economiesthat have been highly dependent on exports ratherthan consumer spending.

Yet consider the numbers. In Japan, where consumerspending is roughly 30 percent that of the UnitedStates, it is 58 percent of GDP, an historically highnumber already by Japanese standards. It is unlikely togo significantly higher, and Japan’s economy is unlikelyto grow significantly faster anytime soon. In Germany,consumer spending is less than 17 percent that of theUnited States. German consumer spending is 56 percentof GDP, a number that is unlikely to become significantlyhigher. In other words, it is hard to see how thesecountries can play a big role in offsetting a U.S.adjustment. Moreover, the degree to which Germanyand Japan will undertake policies necessary to achieve ashift is uncertain at best.

That leaves the rest of the world. The reality is that,given what is likely to take place in the United States,sizable shifts in economic structure will be necessaryin many countries, including many of the bigemerging markets.

What could go wrong?If U.S. consumer spending resumes growth at a levelsimilar to the past decade, or if other countries (such asChina) fail to sufficiently accelerate consumer spending,then the global economy could face problems. Either ofthese scenarios would entail continued large globalimbalances, with the U.S. borrowing massively fromoverseas and/or China and other countries running hugesurpluses with nowhere to invest them. If the U.S.continues to borrow excessively, financial markets willrespond by driving down the dollar and driving up U.S.interest rates thereby stifling growth, fuelling inflationand causing instability. If China and other countries runlarge surpluses then there will also be downwardpressure on the dollar, increased inflation in China andpotential political instability.

What could bring about such failure? Several thingscould do it. In the United States, these include largebudget deficits, failure to reform U.S. finance and failureto allow the dollar to gradually decline.

In China, problems could come about because ofsupport for the dollar, failure to reform financial services,failure to provide consumers with an adequate safetynet, and excessive government support for businessinvestment at the expense of consumer spending. Theproblem in China is that consumers save an inordinateshare of their income. Although there are strong culturalreasons for this, government policy could at least causeconsumers to switch to a more historical norm. After all,as recently as 1997, consumer spending in China wasroughly 47 percent of GDP compared to about 36percent today. Financial market liberalization could go along way toward encouraging consumers to take onmore debt rather than massively saving for every largepurchase, including homes. Yet previous efforts by thegovernment to discourage saving have not beenespecially successful.

Finally, problems could also arise from a Japanese and/orGerman failure to shift toward a more consumer-driveneconomy. Both giant economies have traditionally been

If U.S. consumer spendingresumes growth at a level similarto the past decade, or if othercountries (such as China) fail tosufficiently accelerate consumerspending, then the globaleconomy could face problems.

Global consumers and the economic imbalance

16 | August 2010 | A Middle East Point of View

dependent on exports rather than the domesticconsumer to drive growth. Yet if the markets to whichthey have exported are less prone to importing, thenthey will not achieve sufficient growth without adjustingto more consumer spending growth. The degree towhich they do this will depend on policy. This remainshighly uncertain, although the government in Japan andthe current coalition in Germany have both signaled aninterest in reforms.

What will the consumer world look like?In the next few years, a fundamental change in thestructure of the global economy will likely shift themanner in which consumer-oriented companies obtaingrowth. The U.S. consumer will be financiallyconstrained. As such, spending in the United States andother indebted countries such as the United Kingdomwill increase more slowly than in the past. Consumerswill be more value conscious, seeking low prices andavoiding some discretionary spending. Thus, companieswill obtain growth through market share gains ratherthan simply latching onto a growing market. Achieving this will entail good brand management, an improved customer experience and differentiationfrom competitors aimed at avoiding ruinous price competition.

During the economic crisis, there have been severalchanges in consumer behavior, many of which maypersist even when the economy recovers. These includea shift toward discount retail venues, a shift towarddiscounted private label products, a shift away fromeating out and toward eating at home, a decline in theshare of income spent on large discretionary items forthe home, and greater price sensitivity in general. Ifthese trends endure even partly, they will change therequirements for success on the part of consumer-oriented companies.

Meanwhile in China, retail sales have weathered theeconomic crisis quite well. The shock to the Chineseeconomy from the global crisis was concentrated onChina’s export sector. The drop in exports led to the lossof roughly 20 million jobs at coastal factories. Yetdespite this significant rise in joblessness, Chineseconsumer spending continued to grow rapidly.

There are several reasons. First, the newly jobless factoryworkers were low paid and did not contributesignificantly to overall retail spending. Rather, middle-class service workers in rich cities like Shanghai play a farlarger role in generating retail sales. Moreover, thesepeople have not lost their jobs. Second, China’sgovernment provided a massive stimulus to theeconomy, creating consumer income. This, combinedwith easier credit conditions, fueled consumer purchasesof homes and cars.

When the global economy is fully recovered, it is likelythat Chinese consumer spending will remain on a highgrowth path. As this happens, the number of middle-class consumers will continue to rise rapidly, especially inthe big coastal cities. That means rising discretionaryspending, increased spending on home-related

In the future, more innovation willtake place in emerging marketsand be aimed at the specific needs of consumers in emergingmarkets. While this is already starting to happen, thistrend will accelerate considerablyin the next few years.

A Middle East Point of View | August 2010 | 17

products, expanded awareness of global brands yetpride in high quality local brands, and increasedwillingness to eat outside the home. The latter will beespecially important as there will be a sizable increase inthe number of two-income, middle-class householdswho are highly time constrained. Still, China will remaina relatively poor country – as will the other big, fast-growing emerging markets such as India, Russia, Brazil,Indonesia and Turkey. That means relatively smallshopping baskets, a high degree of price sensitivity anda big market for discount shopping.

What should companies do?For global consumer-oriented companies, the newbusiness environment will have several implications:

The shift in global consumer spending growth awayfrom the United States toward big emerging marketsmeans that companies will shift their resources in thesame direction. Although rich countries like the United States will remain of critical importance, adisproportionate share of growth could come from theemerging world. As such, companies will invest moreheavily in brand management, product developmentand marketing in such markets. Of course a criticalcomponent of success for such companies is innovation.In the future, more innovation will take place inemerging markets and be aimed at the specific needs of consumers in emerging markets. While this is already starting to happen, this trend will accelerateconsiderably in the next few years.

For the United States and United Kingdom and otherrich but constrained markets, there will be a greaterfocus on offering consumers a sense of value. Thismeans innovation, marketing and brand managementaimed at attracting consumers who feel constrainedfinancially but remain interested in high qualityexperiences. It means shifting resources toward

discount formats, a focus on limiting costs, and arecognition that consumers will purchase fewer bigticket items or experiences and, perhaps, purchasemore accessory items.

The rise of China as a consumer market will come inconjunction with a rise in the currency and wages ofChina. Consequently, China will become a somewhatless attractive location for sourcing low-value-addedproducts, and therefore consumer goods companieswill diversify their supply chains. Less sourcing will takeplace in China’s big coastal cities. Instead, there will bean increase in sourcing from China’s interior cities (withfar lower wages) as well as other low wage countries(India, Vietnam, Central Europe, Central America) that,in some cases, are closer in location to the finalmarket. The latter fact will be important if there is asubstantial rise in transport costs associated with highenergy prices.

What about the longer term?The changes taking place in the global economy willrender a new economic structure that is likely to be withus until the next business cycle. Although the focus ofthis article is on the next few years, the trends discussedare likely to be sustained over a much longer time –perhaps as long as the next two decades. Consequently,consumer companies would be wise to keep this inmind when making long-term plans.

by Ira Kalish, director of consumer research for DeloitteResearch, Deloitte Services LP.

Reprinted from Deloitte Review, Issue 6: 2010.

Global consumers and the economic imbalance

Tourism, Hospitality & Leisure in the Middle East: ready to move to the next level

With world-class infrastructure and facilities and anexcellent geographic location on the world stage, theMiddle East is expected to emerge as one of theworld’s most competitive landscapes offering valuetourism and conference experiences to a worldwidecustomer base.

18 | August 2010 | A Middle East Point of View

A Middle East Point of View | August 2010 | 19

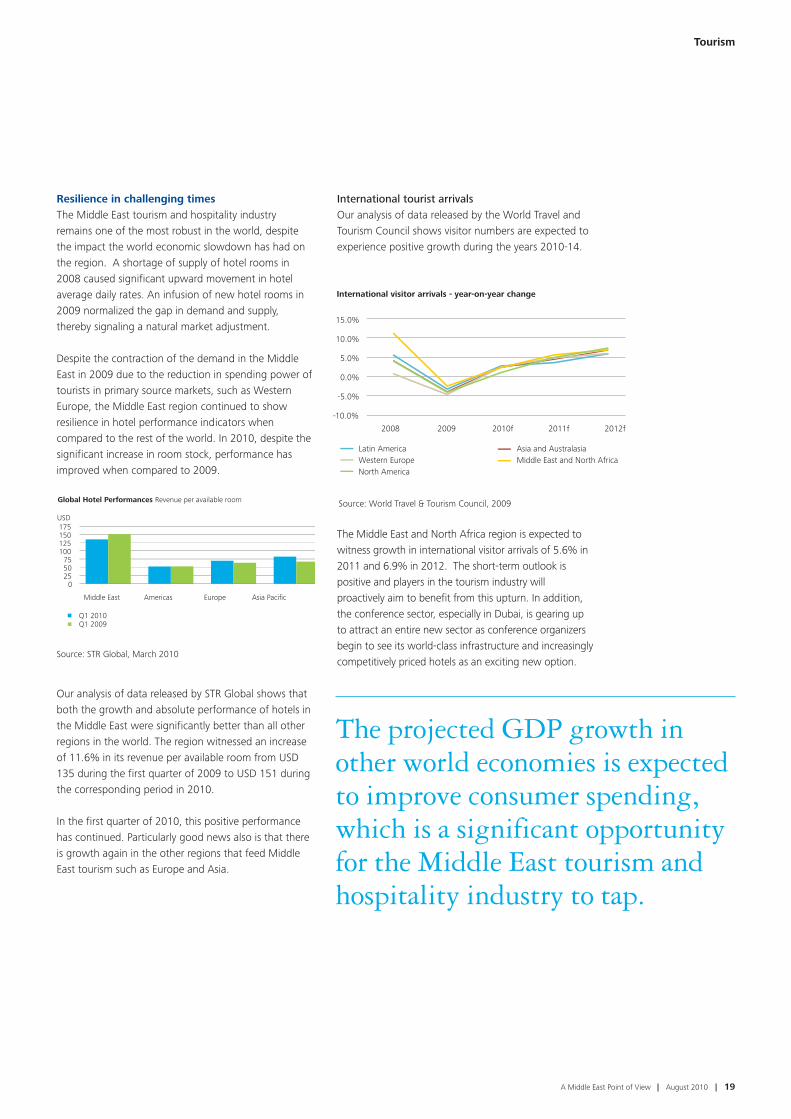

Resilience in challenging timesThe Middle East tourism and hospitality industryremains one of the most robust in the world, despitethe impact the world economic slowdown has had onthe region. A shortage of supply of hotel rooms in2008 caused significant upward movement in hotelaverage daily rates. An infusion of new hotel rooms in2009 normalized the gap in demand and supply,thereby signaling a natural market adjustment.

Despite the contraction of the demand in the MiddleEast in 2009 due to the reduction in spending power oftourists in primary source markets, such as WesternEurope, the Middle East region continued to showresilience in hotel performance indicators whencompared to the rest of the world. In 2010, despite thesignificant increase in room stock, performance hasimproved when compared to 2009.

Our analysis of data released by STR Global shows thatboth the growth and absolute performance of hotels inthe Middle East were significantly better than all otherregions in the world. The region witnessed an increaseof 11.6% in its revenue per available room from USD135 during the first quarter of 2009 to USD 151 duringthe corresponding period in 2010.

In the first quarter of 2010, this positive performancehas continued. Particularly good news also is that thereis growth again in the other regions that feed MiddleEast tourism such as Europe and Asia.

International tourist arrivalsOur analysis of data released by the World Travel andTourism Council shows visitor numbers are expected toexperience positive growth during the years 2010-14.

The Middle East and North Africa region is expected towitness growth in international visitor arrivals of 5.6% in2011 and 6.9% in 2012. The short-term outlook ispositive and players in the tourism industry willproactively aim to benefit from this upturn. In addition,the conference sector, especially in Dubai, is gearing upto attract an entire new sector as conference organizersbegin to see its world-class infrastructure and increasinglycompetitively priced hotels as an exciting new option.

0 25 50 75

100 125 150 175

Middle East Americas Europe Asia Pacific

Global Hotel Performances Revenue per available room

USD

Q1 2010Q1 2009

Source: STR Global, March 2010

Tourism

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

2008 2009 2010f 2011f 2012f

International visitor arrivals - year-on-year change

Latin America Asia and Australasia Western Europe Middle East and North Africa North America

Source: World Travel & Tourism Council, 2009

The projected GDP growth inother world economies is expectedto improve consumer spending,which is a significant opportunityfor the Middle East tourism andhospitality industry to tap.

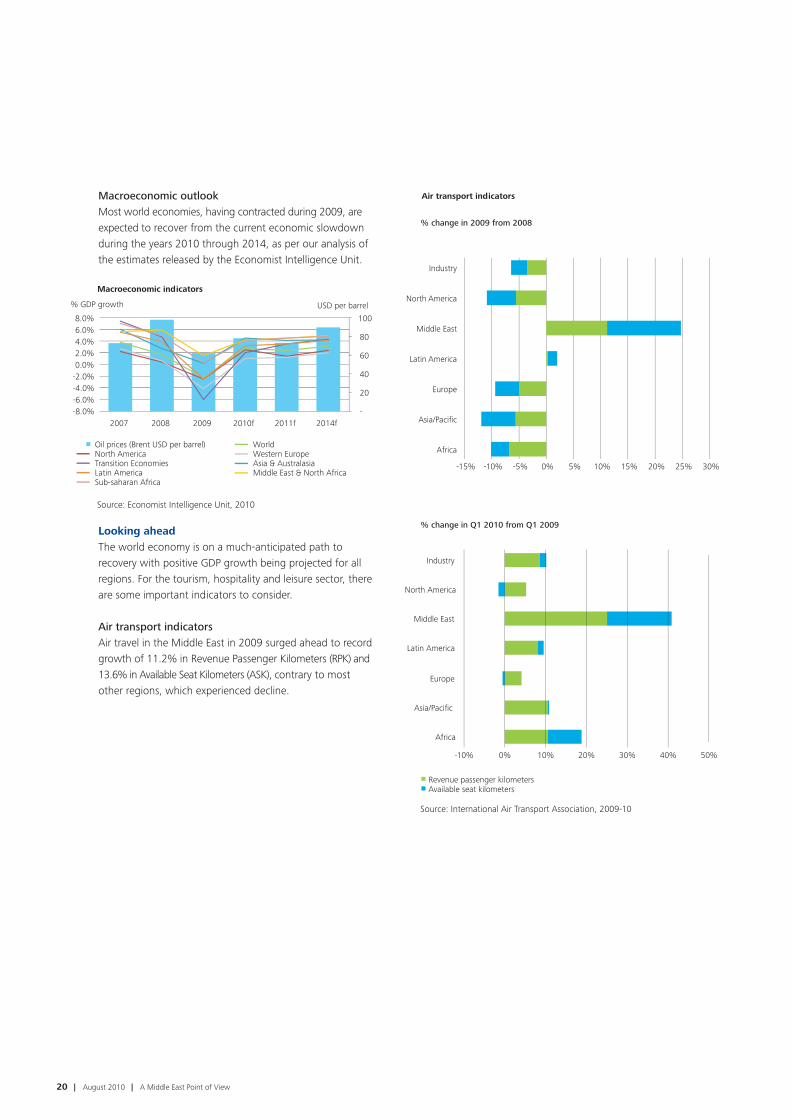

Macroeconomic outlook Most world economies, having contracted during 2009, areexpected to recover from the current economic slowdownduring the years 2010 through 2014, as per our analysis ofthe estimates released by the Economist Intelligence Unit.

Looking ahead The world economy is on a much-anticipated path torecovery with positive GDP growth being projected for allregions. For the tourism, hospitality and leisure sector, thereare some important indicators to consider. Air transport indicatorsAir travel in the Middle East in 2009 surged ahead to recordgrowth of 11.2% in Revenue Passenger Kilometers (RPK) and13.6% in Available Seat Kilometers (ASK), contrary to mostother regions, which experienced decline.

Source: International Air Transport Association, 2009-10

Africa

Asia/Pacific

Europe

Latin America

Middle East

North America

Industry

% change in 2009 from 2008

Africa

Asia/Pacific

Europe

Latin America

Middle East

North America

Industry

% change in Q1 2010 from Q1 2009

Revenue passenger kilometers Available seat kilometers

-15% -10% -5% 0% 5% 10% 15% 20% 25% 30%

-10% 0% 10% 20% 30% 40% 50%

Air transport indicators

20 | August 2010 | A Middle East Point of View

-

20

40

60

80

100

-8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0%

2007 2008 2009 2010f 2011f 2014f

Macroeconomic indicators

Oil prices (Brent USD per barrel) World North America Western Europe Transition Economies Asia & Australasia Latin America Middle East & North Africa Sub-saharan Africa

USD per barrel % GDP growth

Source: Economist Intelligence Unit, 2010

A Middle East Point of View | August 2010 | 21

Tourism

The GDP of the Middle East & North Africa region isexpected to expand by over 4% each year from 2010 to2014, while Western Europe, one of the primary sourcemarkets for the Middle East tourism industry, is expected towitness positive growth during these years. The projectedGDP growth in other world economies is expected toimprove consumer spending, which is a significantopportunity for the Middle East tourism and hospitalityindustry to tap.

Moving to the next levelThe world travel industry is currently witnessingsignificant changes due to the constantly changingglobal and regional economic landscape. Consumerspending levels are changing, and so are travelpreferences of value-conscious tourists.

Given the positive economic outlook and projectedincrease in tourist numbers, world regions, including theMiddle East, will invest heavily in marketing andpromotional efforts to attract the right customersthrough value packages.

The Middle East tourism industry will benefit from notonly constantly gauging its existing travelers’ choices,but also by exploring tourism demand from emergingeconomies such as China and India. Stakeholders in theMiddle East tourism industry will be striving to provide acompelling value proposition to its customers.

Robert O’Hanlon, partner in charge, Tourism, Hoteland Leisure (THL) industry, Deloitte in the Middle East &Hari Ram, supervisor & head of THL industry group analyses

22 | August 2010 | A Middle East Point of View

A Middle East Point of View | August 2010 | 23

With its recent issuance of a controversial ‘exposuredraft’ – a proposed standard – on ‘Financial Instruments,’the U.S. Financial Accounting Standards Board (FASB)has taken a vastly different approach to financialreporting to that taken by the International AccountingStandards Board (IASB). At the end of 2009, the IASBhad promulgated their own version of the revisedstandard on ‘Financial Instruments’ – a new standardentitled ‘IFRS 9’ – in response to a call by the financeministers and governors of central banks of the G20,representing the 20 most powerful economies of theworld. Some believe this latest move by the U.S. FASBdoes not fit well with the global ‘convergence’ initiativeand the various standard setters around the globe.

Several moot questions, including the ones set outbelow, are now plaguing the minds of the stakeholdersin the financial and accounting world, especially theregulators, financial statement users and preparers:

• Will the International Accounting Standards Board(IASB) toe the line and compromise with the way ofthinking of the FASB, the U.S. standard setter? Or,

• Is there still hope for the emergence of a universalstandard, an Esperanto of Accounting?

• In other words, will International FinancialReporting Standards (IFRS), the standardspromulgated by the IASB (an international standardsetting body with Board members from severalnations who are regarded as ‘best of breed’ fromacross the globe) be the ultimate choice of theaccounting and financial world?

Let us examine as to where it is all going in terms of theglobalization of financial reporting and the convergenceof standards worldwide. To comprehend it from alayman’s perspective, an oft-quoted verse fromShakespeare’s Romeo and Juliet perhaps best depictsthe point: “What’s in name? That which we call a roseby any other name would smell as sweet”. Can thesame be said of financial statements prepared indifferent jurisdictions of the globe? Not too far in thedistant past, countries and economic regional blocs,such as Europe, would not be swayed by the thought ofconverging to a single set of global accountingstandards and, due to such nationalistic approaches toaccounting standard setting, a financial statementissued in Japan (under the Japanese accountingstandards) used to be vastly different in terms of

IFRS

IFRS: theultimatechoice of theaccountingworld or willthe “IASB”march to adifferentdrummer?

24 | August 2010 | A Middle East Point of View

accounting treatments and disclosures compared to afinancial statement issued in other major parts of theworld, say, in Germany where German accountingstandards were used hitherto. In other words, the“name” did matter for several countries since theirnational standard setters strongly believed that theirown national accounting standards were suitable fortheir needs and were compatible to other globallypreferred accounting standards. However, due to theadvent of globalization, the falling of the erstwhileinsurmountable barriers between nations and morerecently, the much-awaited response to the globalfinancial crisis, things have changed dramatically interms of the preferred set of standards of accountingglobally. The accounting and financial world is nowseriously considering the notion of using a single set ofaccounting and financial reporting standards that wouldbe used by most, if not all, the nations around theglobe. In all likelihood the name of the globalaccounting standards may be “IFRS”!

The acceptance of IFRS around the world by more than100 countries, including global players that have eitheragreed to allow their standards to converge to IFRS orhave permitted the use of IFRS as their nationalstandards, is an extraordinary achievement for the IASB.The tidal wave of first-time adoptions of IFRS that sweptthrough Europe in 2005 as a result of the decision of theEuropean Union to require all listed companies in thismajor economic bloc to use IFRS for their consolidatedfinancial statements proved to be a significant turningpoint in the history of IFRS. The decision by the U.S.Securities and Exchange Commission (SEC) in November2007 to allow foreign private issuers to enter the U.S.capital market using IFRS-compliant financial statementswithout reconciling to U.S. GAAP (Generally AcceptedAccounting Principles) was yet another defining momentfor IFRS. Several major economies in the world(including global players such as Canada, China, India,South Korea and Brazil) have agreed to adopt IFRS in the(near) future. Commenting on how many morecountries are expected to adopt IFRS by 2011, Sir DavidTweedie, chairman of the IASB, remarked, "we reckonby about 2011, there'll be 150 — all the majoreconomies." (“Accountancy”, January 2008).

While the accounting world may have reason enough torejoice at the prospect of finally being able to sing the“one world, one music” accounting standards tune,there are some who still have doubts about thecommitment of the U.S. to allow that to happen soon.This is mainly due to the U.S. SEC’s announcement inNovember 2009 that it will alter its stand on IFRSacceptance by adding a new dimension in the U.S. – the“U.S. SEC Work Plan” which would assess if and whenwould be the right time for the U.S. to plunge into theIFRS stream. This move has evoked mixed emotionsinternationally about the U.S. SEC’s intentions.

Let us look at some viewpoints on this highly volatileissue/burning question: will the US accept internationalaccounting standards for domestic use, and, if so, whenwill the U.S. offer a favorable nod to these globalstandards, allowing them unconditional entry onto theU.S. domestic scene?

While the accounting worldmay have reason enough torejoice at the prospect of finallybeing able to sing the “oneworld, one music” accountingstandards tune, there are somewho still have doubts about thecommitment of the U.S. toallow that to happen soon.

A Middle East Point of View | August 2010 | 25

In a statement made at a presentation to the AnnualConference of the CFA Institute held on May 18, 2010in the U.S.by the U.S. SEC Chairman, Mary Schapirodebunked the below-listed “myths” about the U.S. SEC’sstand on International Financial Reporting Standards(IFRS) with a clear-cut “NO”:

Myth #1: The SEC’s commitment to global accountingstandards is not as strong as it should be.

Myth #2: The U.S. may be committed, but it is draggingits feet regarding adoption of IFRS.

Myth #3: The United States is fixated on process.

Myth #4: America is protecting its parochial interests.

Some believe that such an unambiguous public supportfor IFRS has not been offered by the U.S. hitherto andthey are right in this belief since the U.S. support forIFRS has usually been a bit lukewarm and never in clear-cut terms.

To understand why many in the accounting andfinancial world are skeptical about the U.S. SEC’scommitment towards acceptance of IFRS, let us examinethe specific areas of concern to be addressed in the U.S.SEC’s Work Plan. These include:

• Sufficient development and application of IFRS forthe U.S. domestic reporting system;

• The independence of standard setting for thebenefit of investors.Composition of the IFRSFoundation and the IASB;

• Investor understanding and education regarding IFRS;

• Examination of the U.S. regulatory environment that would be affected by a change in accounting standards;

• The impact on issuers, both large and small,including changes to accounting systems, changesto contractual arrangements, corporate governanceconsiderations and litigation contingencies; and

• Human capital readiness.

Looking at the afore-mentioned areas of concerns thatthe U.S. SEC is still wanting to address (while severalother global players have already publicly announcedtheir unequivocal support for IFRS) many in theaccounting and financial world are raising questionsabout the possibility of acceptance of IFRS by the U.S.for domestic use in the near future.

People are wondering whether there is any silver liningto this cloud. Questions are also being raised as to theextent of convergence of IFRS with U.S. GAAP and towhat extent the U.S. FASB is ready to move towardsIFRS. Yet another important question on everyone’smind is: if the U.S. SEC does finally accept IFRS fordomestic use, “when” can the world of accountingexpect to see light at the end of the tunnel? All theseremain unanswered questions and time will only tellwhether IFRS will win the coveted title of the GlobalAccounting Standards. Let us keep our fingers crossedthat it will happen soon!

by Abbas Ali Mirza, Audit partner, Deloitte in the Middle East

IFRS

26 | August 2010 | A Middle East Point of View

Perhaps one of the most discussed topics in corporatefinance is Efficient Market Hypothesis. In a developedmarket such as the United States, that discussion centerson the strength of market efficiency. But in emergingmarkets such as the Middle East, and the GulfCooperation Council (GCC) countries in particular, wherethe securities markets have not kept pace with thespectacular growth witnessed in the last few years, thequestion is more whether Efficient Market Hypothesisholds at all in the region.

Impeding factorsA major factor that impacts market efficiency in the GCCis ownership restrictions. All public joint stockcompanies listed on the Dubai Financial Market (DFM)and the Abu Dhabi Securities Exchange (ADX) forexample, have to be 51% owned by UAE nationals. Theremaining 49% are further subdivided among non-GCCArabs and non-Arabs. Of the total 69 companies listedon the ADX, 53 have an average foreign ownership(primarily Arab) of only 14%. The remaining 16companies do not have any foreign ownership at all.Considering that foreigners make up over 80% of theUnited Arab Emirate’s population of around 6.9 million,the prices quoted for a sizeable percentage of the stocksonly reflect the views of a small minority of thepopulation. Albeit, this may well be consistent withwhere the local wealth lies.

Another important factor prevalent in the GCC marketsand that is common to emerging markets, has to dowith the availability of financial and other relevantinformation. Pertinent information that is available in an efficient and timely manner is essential to the properfunctioning of the market as it provides investors withthe basis with which to form their decisions. An April2010 study by The National Investor (TNI), a UAE-basedinvestment bank, mentions that the majority ofcompanies in the GCC do not announce the releasedate of annual reports in advance. Furthermore, manyof them do not publish annual reports in English, often

How do the GCCmarkets compare withmore developedeconomies in terms ofmarket efficiency? Nottoo well, according tothis author, thoughrecent developments have been encouraging.

Market effic in the Gulf

A Middle East Point of View | August 2010 | 27

Valuation

the functional business language of most of the region.Another factor that impacts decision-making is the levelof analyst coverage and in the GCC, only 26% of listedcompanies have analyst coverage.

Impact on the marketsA direct consequence of these impeding factors couldbe the low trading volumes observed in a majority ofthe listed securities. Many companies trade only a fewdays a year, which can result in stale prices. Most majorexchanges have witnessed an increase in volumes overthe last few years, however exchanges in the MiddleEast have not, except in a limited number of stocks. Onthe DFM, by way of example, three stocks onlyaccounted for almost 53% of the total volume traded inQ1 2010, to which the real estate company Emaarcontributed 43% of the total traded value.

The volume of trade on the regional exchanges isfurther affected by the lack of short selling and equityderivative products. The use of such products has beenlimited to Kuwait, which has offered some derivativesfor years, and more recently in the UAE (2005) with theDubai Gold and Commodities Exchange, which offeredmetals and currency futures and options. The use ofshort selling and derivative products further incorporatesthe market’s view, thus leading to better pricing of thesecurities. The UAE regulators were consideringintroducing these features a couple of years backthough the global financial crisis put a hold on suchplans. There are now reports suggesting that theSecurities and Commodity Authority is considering these once again.

In addition to structural factors, a distinct characteristicof the GCC market is the demography with a significantproportion of the population made up of expatriates.Their “temporary” stay in the country leads to whatbehavioural finance terms as “home country bias”,wherein people are more comfortable investing insecurities with which they are familiar and comfortablei.e. those in their “home country”. This of course furtherimpacts demand and consequently, pricing.

If the basic tenet of efficient markets is that prices arethe result of the market’s view of a company’s risk andprospects based on all publicly available information,then there are several factors that lead one to suggest

that the Middle East markets have some way to gobefore they come into line with more developedmarkets around the world. However, the Middle Eastmarkets have already come a long way and with furtherdevelopments such as the recent announcement thatMubadala will look to IPO investments, albeit in 5 to 8years’ time, and with the continued focus on the development of transparency levels and the adoption ofIFRS, interesting times lie ahead for exchange markets as the Middle East continues to close the gap. In themeantime, from a valuation perspective, speculatorsneed to be as ever aware of these factors and apply agreater degree of subjectivity when dealing with thevaluation of regional companies.

by Ben Moore, managing director, Valuation services,Deloitte Corporate Finance Limited

ciency

A not too efficient market, but the Middle East

continues to close the gap.

28 | August 2010 | A Middle East Point of View

Have governmentsbeen quicker thancorporations to advancetalented women? Yes, but the Middle East stillhas a long way to go

A Middle East Point of View | August 2010 | 29

Debates on the value of diversity and the empowermentand advancement of women have raged for centuries,but when it comes to gender equality, few achievementscan compare with the rising role of women ingovernment worldwide.

Paths To Power, a March 2010 report by Deloitte andForbes Insights, reveals that women worldwide arerapidly advancing in the public sector, makinggovernment a leading example for businesses. The studyreported that women hold chief executive andpresidential positions in only 3% of the world's top1,000 companies, yet almost 10% of United Nationscountries now have women heads of state, a hugeincrease from the three female heads of state in 1975.Women also hold about 20% of parliamentary seatsworldwide, nearly double that of 1995's 11.3%.However, only 9.4% of all jobs than higher VicePresident at Fortune Global 500 companies are women.

Women are advancing faster in government than inbusiness, but some countries are advancing faster thanothers and the report makes clear that women continueto have a low political impact in most parts of the world.

A Middle East snapshotIn the Middle East, women’s gains and their leadershipon public sector platforms remain unrecognized anduneven although they are entering politics andgovernment in growing numbers. Despite their increasedrepresentation, they continue to be significantly under-represented in senior positions in politics as well as inthe private sector.

Women in the Middle East have been at the core ofgovernments’ development work for a number of years,a very needed focus as on average, only 28% of theadult female population in the Middle East is

economically active, the lowest rate in the world. Whilethis statistic is consternating, in nearly all Middle Easterncountries, women today are better represented and arebeginning to play a more prominent role in theworkplace than was the case in the year 2000. Thisappears to be the result of increased literacy andeducational opportunities, slowly changing culturalattitudes and in some countries, government policiesaimed at reducing dependence on foreign labor.

An 18-nation study, Women's Rights in the Middle Eastand North Africa, 2010, led by Freedom House, foundthat while on the whole, Middle Eastern women stillsuffer from a “substantial deficit in women’s rights”, 15of 18 Arab countries have seen increases in women’sliteracy rates and suffrage over the past five years. Thestudy noted that GCC countries have demonstrated thegreatest degree of improvement, shrinking the gapbetween them and the rest of the region on someissues. The most significant achievement occurred inKuwait, where women received the same political rightsas men in 2005, enabling them to vote and run foroffice and paving the way for the election of thecountry’s first female members of parliament in 2009. Inthe United Arab Emirates (UAE), eight women wereappointed and one secured election to the 40-memberFederal National Council (FNC), an advisory body to therulers of the seven emirates. In Bahrain and the UAE, thefirst women judges were appointed in 2006 and 2008,respectively. In other countries, such as Oman andBahrain, the government has appointed an increasingnumber of women to unelected positions, includingcabinet and diplomatic posts. In Egypt, to increasewomen’s representation in the legislature, a gender-based quota system for the lower house of parliamentwas passed in 2009 and is scheduled for implementationin 2010. A quota for women was introduced formunicipal elections in Jordan and Lebanon among other

Women in the public sector

“The best clue to a nation’sgrowth and developmentpotential is the status androle of women.”(i)David S. Landes

countries in the region. In general, women have becomemore visible participants in public life, education andbusiness throughout the region, including Saudi Arabia.

Progress is occurring, but at a pace that is still too slowand what looks like progress may actually be deceptiveas increased female participation in Middle Eastgovernments does not necessarily translate into more women in decision-making roles, where they have opportunity to advance, affect change andinfluence policy.

More progress in the public sector in the MiddleEast will serve as a model for the private sectorA critical mass of women in leadership begets morewomen in leadership. Evidence suggests that oncefemale representation reaches critical mass – commonlycited figures hover around one-third as the tipping point– their shared interests as women emerge. Countrieswhere efforts to include women at the highest levels ofgovernment have been most successful have reapedrewards in the private sector as well. The increasingnumber of women in public service creates a criticalmass essential to the continual empowerment andadvancement of women in their societies: simply put,women in power begets more women in power.

There is a need to harness and continue to minethe wealth of female talent to improve thecompetitiveness of Middle Eastern countriesTalent is the most important natural resource a nationcan possess and knowledge is the most valuablecurrency in the 21st century economy. Therefore, it iskey to continue to advance the most talented women todecision-making levels as women are rapidly matching,or overtaking, men in terms of education in many partsof the world. More women than men in many countriesin the Middle East are now likely to attend university, insome countries, by a wide margin. There are morewomen entrepreneurs, more women doctors, morewomen PhDs, and more women in universities than everbefore. However, substantial roadblocks remain forwomen pursuing careers. Participation by women insenior roles translates to greater financial rewards inboth public and private sectors: the top 500multinational firms, which had at least three women ontheir boards, saw a 16.7% return on equity whileaverage companies just saw an 11.5% return. Thegreater the number of women, the greater thedifference -- those with the greatest number of womenon their boards had 53 percent greater return on equitythan those with the fewest.

Organizations in the public sector in the MiddleEast can address gender disparity throughdifferent tools Recruitment rates, promotion rates, turnover rates,assignment and leadership appointments, are some ofthe critical metrics that can be adopted. Organizations inthe public and private sectors have to establish aninstitutional approach to the advancement and retentionof women. They can raise the profile of women throughestablished networks, where women get to meet andbe mentored by other women through organizednetworking and mentoring events. They can alsopromote work-life integration by helping women

Only 28% of the adult femalepopulation in the Middle East iseconomically active, the lowest rate in the world. While this statistic isconsternating, in nearly all MiddleEastern countries, women today arebetter represented and are beginningto play a more prominent role in theworkplace than was the case in theyear 2000.

Only 9.4% of alljobs higher thanVice-President at

Fortune 500companiesare women.

30 | August 2010 | A Middle East Point of View

A Middle East Point of View | August 2010 | 31

accommodate their public role with their demands athome by providing accessible childcare and othersupport networks.

Numbers are also crucial for the inclusion of women inthe public and private spheres. Introducing quotas forfemale representation has been often used as one of themost effective methods for increasing femalerepresentation in the public sector.

It is not enough to hold public officeCapacity-building for governance is essential not only forwomen but for men as well. It is not enough to beelected or to be appointed to government servicewithout the ability to exercise that responsibilityeffectively. To address this need, Middle Eastgovernments need to invest in programs to strengthenthe skills and leadership abilities of women and menparliamentarians and other elected officials.

Middle East governments as leading example forbusinessesWomen’s progress has vital implications for the healthand growth of companies, governments and nations.On the frontlines of moderation, women are often thestrongest advocates for positive political, economic,educational, legal and social reform. There are still fewfemale role models in our region to encourage youngergenerations and entry barriers like gender prejudice,cultural pressures and a lack of resources often stand inthe way.

In the final analysis, the struggle of women to reachsenior levels cannot be seen as simply a “women’sissue,” but rather one of talent and economicdevelopment: women’s progress has vital implicationsfor the health and growth of Middle East governments,companies, and countries.

Deloitte is not only a signatory of the UN GlobalCompact, the corporate code of conduct focusedexclusively on empowering, advancing and investing inwomen worldwide, but was also involved in aninternational multi-stakeholder consultation process forcrafting the UNIFEM’s and the UN Global Compact’s“Women’s Empowerment Principles - Equality Means

Business.”Organizations in both the public and privatesectors in the Middle East should review its principlesand recommendations in adopting appropriatestrategies to address gender disparity.

By Rana Ghandour Salhab, ME Talent partner, Deloitte in the Middle East

(i) Landes, David, The Wealth and Poverty of Nations: Why Some areSo Rich and Some So Poor. New York: W. W. Norton & CompanyInc., 1998.

Sources

• Paths to Power: Advancing Women in Government, published byForbes Insights and Deloitte, March 2010. Available at:www.deloitte.com/pathstopower.

• Freedom House, Women's Rights in the Middle East and NorthAfrica 2010 - March 2010, available at: http://www.unhcr.org.

• The Women's Empowerment Principles are a set of Principles forbusiness offering guidance on how to empower women in theworkplace, marketplace and community. They are the result of acollaboration between the United Nations Development Fund forWomen (UNIFEM) and the United Nations Global Compact. Thedevelopment of the Principles included an international multi-stakeholder consultation process, which was launched in March2009:http://www.unglobalcompact.org/Issues/human_rights/equality_means_business.html.

Women in the public sector

11%

3%of the 195 nations have female heads of state

of CEOs of top 1000 multinational companies are women

40% of the workforce is women

• Establish high-level corporate leadershipfor gender quality

• Treat all women and men fairly at work-respect and support human rights andnondiscrimination

• Ensure the health, safety and well-beingof all women and men workers

• Promote education, training andprofessional development for women

• Implement enterprise development,supply chain and marketing practicesthat empower women

• Promote equality through communityinitiatives and advocacy

• Measure and publicly report on progressto achieve gender equality

Women’s Empowerment Principles

32 | August 2010 | A Middle East Point of View

Trends in gover in the GCC cou

A Middle East Point of View | August 2010 | 33

Government services

In recent years, governments in the Gulf CooperationCouncil (Saudi Arabia, United Arab Emirates, Qatar,Bahrain, Oman and Kuwait) embarked on a largenumber of initiatives to enhance government servicesto citizens, residents and businesses both at thenational level and at the GCC level. One key trend isthe participation of the private sector in enhancinggovernment services through the formation of PublicPrivate Partnerships (PPPs).

rnment services untries

34 | August 2010 | A Middle East Point of View

Trends at the national level

At the national level, GCC governments haveconsistently increased their budget spending on keyservice sectors including Education and NationalEmployment, Healthcare, Infrastructure and e-Government. In fact these service sectors were amongthe top budget items consistently across the GCC inrecent years.

Education and national employment servicesTo enhance national talent and increase nationalemployment, GCC countries increased budget spendingon education including school education, highereducation and vocational training. GCC governmentsare building schools, universities and vocationalinstitutions. Furthermore, there are many initiatives toenhance curricula, teaching skills and tools. GCCgovernments are also spending more on scholarships forstudents studying at universities abroad both at theundergraduate and the graduate level.

Examples of these initiatives are: • Saudi Arabia is establishing many new schools and

universities across the country. • Education Management System initiative in Saudi

Arabia to introduce e-Learning and teaching tools. • The United Arab Emirates (UAE) is establishing

new universities and attracting leading international ones.

• Qatar Foundation attracted leading international universities.

The GCC governments are also engaging the privatesector in the education sector by forming Public PrivatePartnerships. The Abu Dhabi Education Counsel (ADEC)has engaged the private sector for its educationdevelopment program.

Another item on the agenda is the promotion ofnational employment in the private sector. Theseinitiatives focus on identifying and executing publicpolicy initiatives to promote national employment in theprivate sector as well as encouraging private sector-related initiatives. A good example of these initiatives isthe Abu Dhabi Tawteen Council.

But despite the increase in spending and the initiatives

GCC governments are embarking on to improveeducation services and national employment, there arestill many challenges. Talent and skill gaps are still wideand not meeting the market requirements. Furthermore,national employment in the private sector in the GCCremains very low, in some cases less than 5% of theprivate sector workforce.

Healthcare servicesTo enhance national healthcare services and reduce thecost of sending patients abroad, GCC countries haveincreased spending on this sector, including buildinghospitals and clinics, enhancing skills and services andencouraging private sector participation. Although thenumber of private hospitals and clinics is growing in theGCC, governments still own most of the healthcareinstitutions. For example, in Saudi Arabia, the largestGCC economy, the private healthcare sector providesless than 25% of overall healthcare services in thekingdom according to published material by the Ministry of Health.

GCC governments are also exploring Public PrivatePartnerships in the healthcare sector. For example, Ithmar,a private equity company announced recently a strategicequity partnership with Al Noor Medical Company, theleading private integrated healthcare operator in AbuDhabi. The Ithmar-Al Noor partnership will be aspringboard for Al Noor’s future expansion via PPP.

Recently, GCC governments also embarked on the e-Health initiatives focusing on implementing state-of-the-art Hospital Information Systems (HIS), Electronic HealthRecords and Health Information Exchanges. Theseinitiatives will enhance hospital services and allowhospitals and clinics across the country to exchange andshare patient information.

Examples of these initiatives include: • Dubai Healthcare city providing healthcare and an

integrated centre of excellence for clinical andwellness services, medical education and research.

• Sidra Medical and Research Center founded by Qatar Foundation.

• Wareed & HIS (e-Health) initiative in the UAEMinistry of Health.

• The e-Health initiative at the Saudi Ministry of Health.

Still, healthcare services in the GCC countries do notmeet the demand and the quality required by citizens,therefore, GCC governments still bear the cost ofsending patients abroad for treatment services theycannot provide in their own countries. The aboveinitiatives are still in infancy and must be carried throughand executed successfully to bear fruit and make apositive impact on the quality of healthcare in the GCC.

GCC governments still bear thecost of sending patients abroad fortreatment services they cannotprovide in their own countries.

A Middle East Point of View | August 2010 | 35

Infrastructure services GCC governments increased spending on nationalinfrastructure projects including water, electricity,housing, railway and telecommunications. They havebuilt the largest water desalination facilities in the worldto meet water demand.

New power generation facilities are also being built tomeet demand. Recent initiatives were launched to utilizenuclear energy to generate electricity in the UAE andSaudi Arabia.

Railway projects have also been launched. Dubaicompleted most of the first phase of its Metro project to reduce traffic congestion. The UAE government isalso planning a railway project to interconnect all the emirates. Saudi Arabia started large railway projects across the country. Qatar is also planning a railway project.

Furthermore, GCC governments built telecommunicationand broadband digital infrastructure enhancingadvanced Mobile, Internet, Telephone and Multimediaservices. This infrastructure also allowed thesegovernments to introduce their e-Services.

In recent years, GCC governments are encouragingprudent private investments in infrastructure projects.GCC Governments formed Public Private Partnerships tofund, build and operate power, water and urbanInfrastructure projects. For example, the Saudigovernment is embarking on the establishment ofEconomic and Industrial Cities engaging the privatesector and forming PPPs.

Affordable housing projects were launched by manyGCC governments, including the UAE and Saudi Arabia.Mortgage regulations are being developed and issued toenable more of their citizens to afford owning homes.

However, about 70% of Saudi citizens still do not owntheir own homes and cannot afford buying houses evenunder the initial mortgage regulations which are goingthrough amendment to allow more citizens to buyhouses. Furthermore, the latest floods in Jeddahrevealed significant issues in infrastructure qualitydespite huge investments by the Saudi government.Therefore, infrastructure initiatives must focus not onlyon capacity but also on quality.

E-Government servicesGCC governments initiated programs to streamlinegovernment services, launch e-Services and IntegratedGovernment Services.

The United Nations (UN) in its 2008 and 2010 e-Government Surveys showed GCC states improvingtheir e-Government Readiness: • Bahrain moved up from 53rd place in 2005 to 42nd in

2008, leaping to 13th place in 2010 and 3rd in Asiajust short of Singapore (11th globally and 2nd in Asia);

• UAE moved from 42nd place in 2005 to 32nd in 2008,to 49th in 2010, and 9th in Asia,

• Kuwait moved up from 75th place in 2005 to 57th in2008, 50th in 2010, and 10th in Asia,

• Saudi Arabia moved up from 80th in 2005, to 70th in2008, to 58th in 2010,

• Qatar moved from 62nd in 2005, to 53rd in 2008, to62nd in 2010,

• Oman moved up from 112th in 2005, to 84th in2008, to 82nd in 2010.

The strong performance by the GCC countries has beenattributed to heavy investments in deploying broadbanddigital infrastructure, coupled with increasedimplementation of e-Government applications for their citizens.

GCC governments have also initiated ServiceImprovement Programs similar to “Service Canada”.These programs will focus on developing Citizen-CentricServices where citizens’ feedback is solicited on ways toimprove government services. These programs will thenfocus on streamlining government services utilizingIntegrated Service Centers (ISCs) or One Stop Shopservice centers where citizens, residents, businesses andeven visitors can complete their governmenttransactions in one location, in simple, convenient andrapid fashion. Dubai government offers such ISCs in freezones and the Saudi Arabian General InvestmentAuthority (SAGIA) established a one stop shop forforeign companies and investors to rapidly establishcommercial registration in the Kingdom.

Despite the above accomplishments, GCC countries stillranked quite low in the 2009 Transparency Indexreleased by Transparency International. Although someimproved their rankings, others did not.

It is essential to carry out serious initiatives in this regardin order to improve government services, attract foreigninvestments and above all protect national wealth.

GCC governments still face challenges in solicitingfeedback from citizens and in increasing the usage of e-Government services by citizens. GCC governmentscan significantly develop their e-Government and ServiceImprovement Programs by both opening their data tocitizens and utilizing the developing Social Media to getcontinuous feedback from citizens on governmentservices and ways to improve these services.(i)

Government services

36 | August 2010 | A Middle East Point of View

At the GCC level, member states have started majorinitiatives to build closer economic cooperationincluding the establishment of a Common Market,Single Currency, GCC Railway and GCC Electricity Grid.These initiatives would strengthen GCC cooperation andenhance GCC government services to citizens, residentsand businesses.

GCC Single currency & common market Currently, GCC cross-border business requires payingsalaries and consolidating accounts in six differentcurrencies, which makes cross-border business complexand distracts from core business issues.

A GCC common currency will make cross-borderbusiness simpler, encouraging mergers and acquisitionsand creating large regional players that can competewith the multinationals aggressively entering the GCCmarket. A GCC common currency is a key enabler of theformation of cross-border companies with economies of

scale that will be more competitive and deliver extravalue to shareholders.

Citizens, residents and visitors can travel across the GCCwithout having to carry different currencies and worryabout exchange rates.

A single currency would be stronger and more stablecompared with the current national currencies in theGCC. It could allow the GCC to price Oil, Gas andPetrochemicals using a common currency rather thanstaying dependent on the U.S. Dollar. It would alsoallow pegging to a basket of currencies rather than thedeclining U.S. Dollar. Once well-established, it can befloated like other hard currencies.

Furthermore, the establishment of the Common Marketwill allow easier and cost-effective movement of citizensand goods in the GCC. This would allow the GCC toeconomically compete on the global level.