Microfinance Performance in SHG Project Report

55

A STUDY ON MICROFINANCE PERFORMANCE IN SELF HELF GROUP Project Report Submitted in partial fulfillment of the requirements for the award of the Degree of Of Bharathiar University, Coimbatore Submitted by (Reg. No) Under the guidance of

-

Upload

dinu05 -

Category

Economy & Finance

-

view

236 -

download

4

Transcript of Microfinance Performance in SHG Project Report

A STUDY ON MICROFINANCE PERFORMANCE IN

SELF HELF GROUP

Project Report

Submitted in partial fulfillment of the requirements for the award of the

Degree of

Of Bharathiar University, Coimbatore

Submitted by

(Reg. No)

Under the guidance of

DECLARATION

I hereby declare that the Project Report entitled “A STUDY ON

MICROFINANCE PERFORMANCE IN SELF HELP GROUP” submitted to

BHARATHIAR UNIVERSITY, Coimbatore, in partial fulfillment of the requirements for the

award of the Degree of is a record of original work done

by me, under the guidance of , during the period of my study, at

Place:

Date: _______ (Reg. No.)

This is to certify that the Project Report entitled “A STUDY ON MICROFINANCE

PERFORMANCE IN SELF HELP GROUP” is a bonafide record of work, submitted by

(Reg. No.) in partial fulfillment of the requirements for the award of the Degree of

--------------------------------------------- ------------------------------------------------------------

Faculty Guide Principal/Director

College seal ------------------

Viva-Voce Examination held on _________________

--------------------------------------------- ----------------------------------------------------------

Internal Examiner External Examiner

ABSTRACT

ABSTRACT

ACKNOWLEDGMENT

ACKNOWLEDGEMENT

I am greatly indebted to many personalities for their kind help,

encouragement and guidance for me to prepare and finish this project successfully.

I take this opportunity to thank all of them.

I would like to thank

for all encourage and inspiring support in completing the project.

I very much obliged and indebted to for his approval and valuable

suggestions to take up the project.

I am also thankful to dept.head Mrs for his

great support and suggestions during the project.

I am very pleased to express my deep sense of gratitude to (Assistant

professor and Guide) for her consistent encouragement. I shall forever cherish my

association with her for exuberant encouragement personnel approachability

absolute freedom of thought and action. I have enjoyed doing the course of the

project.

CONTENTS

TABLE OF CONTENT

CHAPTERS TITLE PAGE NO

CHAPTER – I INTRODUCTION AND DESIGN OF THE

STUDY

CHAPTER – II MICROFINANCE IN SELF HELP GROUP

CHAPTER – II1 DATA ANALYSIS AND

INTERPRETATION

CHAPTER – IV FINDINGS AND SUGGESTIONS

CHAPTER – V CONCLUSION

BIBLIOGRAPHY

LIST OF TABLES

LIST OF TABLES

TABLE

NO TITLES

PAGE

NO

A OVERALL PROGRESS UNDER SHG- BANK

LINKAGES

1 SHG SAVINGS WITH BANKS AS ON 31ST

MARCH

2 LOANS DISBURSED TO SHGs DURING THE

YEAR

3 LOANS OUTSTANDING AGAINST SHGs AS

ON 31ST MARCH

4 WOMEN SHGs SAVINGS WITH BANK AS ON

31ST MARCH

5 LOANS DISBURSED TO WOMEN’S SHGs

DURING THE YEAR

6 LOANS OUTSTANDING AGAINST WOMEN’S

SHGs AS ON 31ST MARCH

B PROGRESS UNDER MFI- BANK LINKAGE

PROGRAMME

7 LOANS DISBURSED BY BANKS TO MFIs

8 LOANS OUTSTANDING AGAINST MFIs AS

ON 31ST MARCH

C

PROGRESS UNDER MICROFINANCE

INSTITUTIONS

9 SAVINGS OF SHGs WITH BANK IN

TAMILNADU

10 BANK LOAN DISBURSED TO SHG DURING

THE YEAR 2011-12

11 BANK LOAN OUTSTANDING AGAINST SHG

IN TAMILNADU AS ON 31ST MARCH 2012

LIST OF CHARTS

LIST OF CHARTS

CHART

NO TITLE

PAGE

NO

A OVERALL PROGRESS UNDER SHG- BANK

LINKAGES

1 SHG SAVINGS WITH BANKS AS ON 31ST

MARCH

2 LOANS DISBURSED TO SHGs DURING THE

YEAR

3 LOANS OUTSTANDING AGAINST SHGs AS

ON 31ST MARCH

4 WOMEN SHGs SAVINGS WITH BANK AS ON

31ST MARCH

5 LOANS DISBURSED TO WOMEN’S SHGs

DURING THE YEAR

6 LOANS OUTSTANDING AGAINST WOMEN’S

SHGs AS ON 31ST MARCH

B PROGRESS UNDER MFI- BANK LINKAGE

PROGRAMME

7 LOANS DISBURSED BY BANKS TO MFIs

8 LOANS OUTSTANDING AGAINST MFIs AS

ON 31ST MARCH

C PROGRESS UNDER MICROFINANCE

INSTITUTIONS

9 SAVINGS OF SHGs WITH BANK IN

TAMILNADU

10 BANK LOAN DISBURSED TO SHG DURING

THE YEAR 2011-12

11 BANK LOAN OUTSTANDING AGAINST SHG

IN TAMILNADU AS ON 31ST MARCH 2012

CHAPTER- I

CHAPTER- l

INTRODUCTION AND DESIGN OF THE STUDY

1.1 INTRODUCTION:

The Indian microfinance sector witnessed tremendous growth over the last five years,

during which institutions were subject to little regulation. Micro credit programmes extend small

loans to poor people for self-employment projects that generate income, allowing them to care

for themselves and their families. Some microfinance institutions were subject to prudential

requirements; however no regulation addressed lending practices, pricing, or operations.

Micro credit has come to be recognized and accepted as one of the new development

paradigms for alleviating poverty through social and economic empowerment of the poor, with

focus on empowering women. Credit is usually provided to groups of individuals or village

organizations that use joint-liability to enforce loan repayment. Through group savings and

loans, poor people often increase their economic security and well being. Over the past two

decades micro credit programs have emerged as one of the leading strategies in the overall

movement to end poverty. Micro credit programmes have become a major tool of development

and found to be the only practical and most appropriate solution to alleviate poverty.

Micro credit programmes have been employed in developing countries for some years,

and their effectiveness in the development and poverty alleviation is increasingly acknowledged.

In many countries micro credit programmes have proved to be an effective tool in freeing people

from poverty and have helped to increase their participation in the economic and political

processes of society. The Asia-Pacific region is home to many micro credit institutions, and the

majority of programs are directed at women in rural areas. Targeting women as clients of micro

credit programs has been an effective method to ensure that the benefits of increased family

income are directed towards the general welfare of the family, and particularly the children. The

combination of minimal regulation and rapid sector growth led to an environment where

customers were increasingly dissatisfied with microfinance services, culminating in the Andhra

Pradesh crisis in the fall of 2010. For the purpose of this article, data published by National Bank

for Agriculture and Rural Development in India have been used.

1.2 STATEMENT OF THE PROBLEM

Microfinance needs a lot of regulation in the country as the experience with

private microfinance has not been very good, though the Andhra Pradesh Government was

extending microfinance to self-help groups at 3.5 per cent interest rate, private institutions were

charging between 20 and 25 per cent. “When a person is still fighting poverty, you cannot expect

him to pay high interest,” Microfinance was usually taken for onetime investments and though

the poor seek money for creating an asset and thereby economic activity, they generally end up

clearing previous debts or giving it away in dowry to their daughter’s marriage or paying

hospital bills. Microfinance is largely supporting to SHG’s, various banks are supporting for the

growth of microfinance. In order to find out the reason for the above said the researcher has

framed the objectives below.

1.3 OBJECTIVES

To study the Microfinance Performance in Tamilnadu

To examine the growth in microfinance

To study the women’s SHG performance in microfinance

To analyze the SHG’s outstanding loans

1.4 METHODOLOGY

The Study is conducted to assess and analyze “A Study on Microfinance Performance in

SHG with Special references to Tamilnadu”. The descriptive study conducted by using the

following methodology.

1.5 DATA AND SOURCES

Secondary Data: The data regarding Microfinance Performance in SHG were collected

through Research Papers, Conference Paper, Web Documents, and Books etc.

1.6 PERIOD OF THE STUDY

The study period covers from the year 2009-10 to 2011-12

1.7 TOOLS FOR ANALYSIS

Univariate summary statistics, graphical chart and percentage analysis

1.8 LIMITATIONS OF THE STUDY

This study was taken up with sincere effort to accomplish the objectives; there were

certain factors that hold back the satisfactory completion of the same. These factors include in

following,

The Microfinance gives loan only to poor people not to the moderate people.

SHG is mainly focusing only on woman.

Only government Microfinance is providing the low rate of interest.

1.9 CHAPTER SCHAME

The project is arranged into the following five chapters

Chapter I - Introduction & Design of the study

This chapter deals with introduction, statement of the problem, objectives, methodology

and limitations.

Chapter II - Microfinance and Self Help Group

This chapter deals with Microfinance in India, Models of Microfinance, Microfinance in

Tamilnadu, SHG and Microfinance, Scopes of Microfinance, Objectives of Microfinance,

Development of SHG, Formation of SHG, Characteristics of SHG.

Chapter III - Analysis & Interpretation

This chapter deals with the analyses of secondary data by using various statistical tools

like Graphical Charts and Percentage Analysis.

Chapter IV - Finding, Suggestion & Conclusion

This chapter brings oust the results of the study, findings, suggestions and conclusion.

BIBLIOGRAPHY

This chapter deals with bibliography of collecting materials from the different sources for

the study.

CHAPTER- II

CHAPTER- II

MICROFINANCE AND SELF HELP GROUP

2.1 MICROFINANCE IN INDIA

Microfinance sector has traversed a long journey from micro savings to micro credit and

then to micro enterprises and now entered the field of micro insurance, micro remittance and

micro pension. This gradual and evolutionary growth process has given a great opportunity to the

rural poor in India to attain reasonable economic, social and cultural empowerment, leading to

better living standard and quality of life for participating households. Financial institutions in the

country continued to play a leading role in the microfinance programme for nearly two decades

now. They have joined hands proactively with informal delivery channels to give microfinance

sector the necessary momentum. During the current year too, microfinance has registered an

impressive expansion at the grass root level.

NABARD has been instrumental in facilitating various activities under microfinance

sector, involving all possible partners at the ground level in the field. NABARD has been

encouraging voluntary agencies, bankers, socially spirited individuals, other formal and informal

entities and also government functionaries to promote and nurture SHGs. The focus in this

direction has been on training and capacity building of partners, promotional grant assistance to

Self Help Promoting Institutions (SHPIs), Revolving Fund Assistance (RFA) to MFIs, equity/

capital support to MFIs to supplement their financial resources and provision of 100 per cent

refinance against bank loans provided by various banks for microfinance activities.

2.2 MODELS OF MICROFINANCE

i. SHG - Bank Linkage Model: This model involves the SHGs financed directly by the

banks viz., CBs (Public Sector and Private Sector), RRBs and Cooperative Banks.

ii. MFI - Bank Linkage Model: This model covers financing of Micro Finance Institutions

(MFIs) by banking agencies for on-lending to SHGs and other small borrowers.

iii. Joint Liability Model: this is a comparatively newer model. These are small groups of

about 5 members and many such groups come together at the centre level.

iv. Lending to the individual by the banks or MFIs: in this the MFIs or the banks give loan to

the individuals who are then themselves responsible for the repayment of the loans.

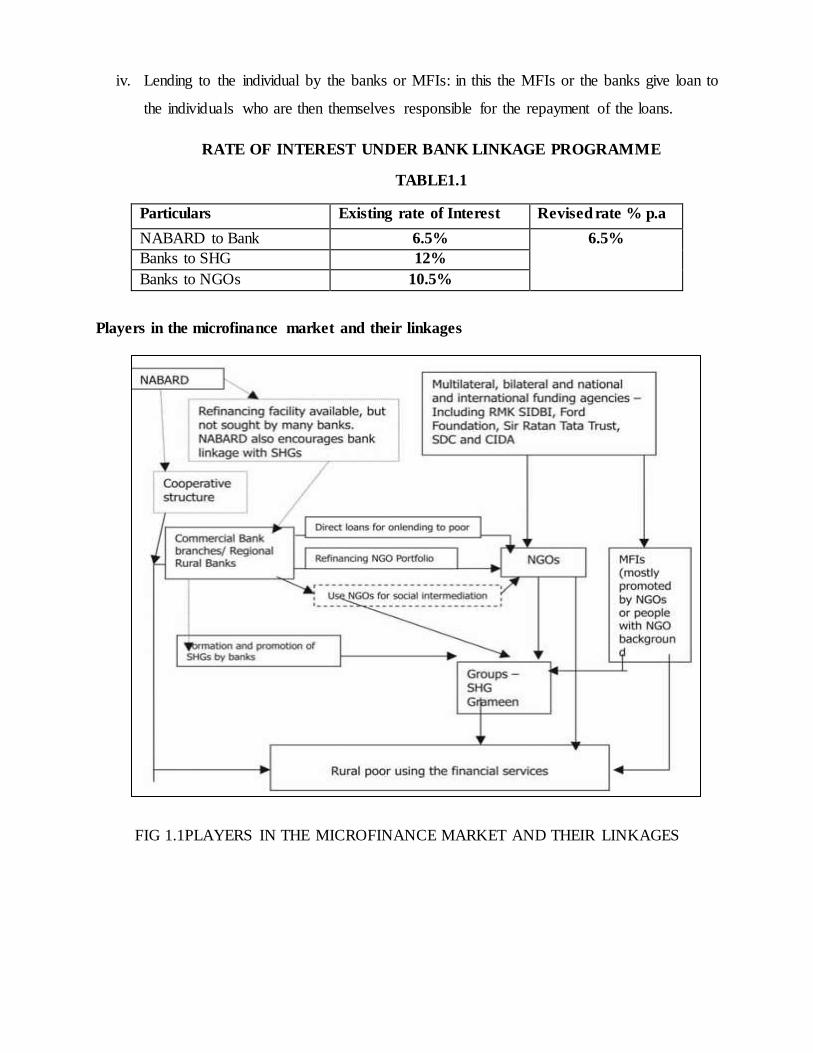

RATE OF INTEREST UNDER BANK LINKAGE PROGRAMME

TABLE1.1

Particulars Existing rate of Interest

p.a

Revised rate % p.a

NABARD to Bank

Refinance

6.5% 6.5%

Banks to SHG 12%

Banks to NGOs 10.5%

Players in the microfinance market and their linkages

FIG 1.1PLAYERS IN THE MICROFINANCE MARKET AND THEIR LINKAGES

2.3 MICROFINANCE IN TAMILNADU

Micro credit programs are successfully implemented in many countries. The principles

and procedures behind micro-credit are simple, but the system is widely effective. Small

business loans are provided to people who are not able to get loans from other institutions

because they have no credit history and the interest rates are enormous (regular interest rates in

Tamil Nadu on loans range from 36% to 120% from banks and private money lenders). Small

business loans are provided to groups of people (Self Help Groups) who trust each other and are

together responsible for the loan. By starting up small businesses with loans people are in charge

of their own future independent of the goodwill of others. Micro credit loans allow people the

opportunity and dignity to create a sustainable income for themselves. Besides that, loans

prepare the borrower also for the commercial world should their enterprise get big enough for the

formal business sector. The increase in income has a positive effect on the whole family, or even

the community. When the loan is repaid in full, people can look forward to a better overall and

financial future, while the returned funds can now provide the same opportunity and benefits to

another family. AID INDIA’s micro credit system is based on the principles of the famous

Grameen Bank (Bangladesh) micro credit system. We modified the micro credit program taking

into account the situations and laws of Tamil Nadu in the implementation of this program.

The District Central Cooperative Banks and Urban Cooperative Banks are implementing

this unique scheme to benefit marginalized small and petty merchants and street vendors

engaged in the business of selling flowers, vegetables, fruits and running petty shops. They are

the most vulnerable group for exploitation by usurious money lenders. Their credit requirements

are very small but critical. This scheme which was launched by this Government has been

amplified and streamlined over the years. Under the scheme the loan amount up to Rs.5000/- is

being provided without any security.

Madura Micro Finance Limited (MMFL) whose core business is providing financial

products i.e. credit, to the rural customer is poised for rapid growth in the next three years. A

clear strategy and the necessary systems have been put in place to propel the company to greater

heights. The primary customer for MMFL is women and together with self-help groups (SHG’s)

the company expects to touch a figure of 1.5 million members from the current 400,000 in the

next three years. MMFL is focused only in Tamilnadu and hopes to reach 20% of the rural

households in Tamilnadu.

Grama Vidiyal Micro Finance Ltd (GVMFL), the largest microfinance institution in

Tamil Nadu, will go for its second round of equity funding of about Rs 50 crore shortly.

GVMFL, which started off as an NGO trust to address the issues of poverty and women’s

empowerment, converted itself into an NBFC (non-banking financial company). Its loans to self-

help group (SHG) members are typically for six months to one year and range from Rs 1,000 to

Rs 7,000 a member in the first instance. Once their track record of regular repayment is

established, members become eligible to draw higher amounts.

In Tamilnadu microcredit is given to individuals but it mainly focused women

empowerment. There are so many microcredit/microfinance institutions in Tamilnadu is to help

raise the socio-economic status of women and children belonging to the weaker sections of

society and thus enabling them to become productive members of society. New Life, through its

community owned association structures known as Affinity Association of Self Help Groups

(AASHG), plays an active role in promoting and providing micro-credit. The AASHGs are

community based groups comprised of women leaders that manage the credit needs of the

individuals within that community. Community based affinity associations are one of the most

effective way in channeling the loans to the borrowers. The AASHGs are responsible for

gathering and validating the credit needs of the borrowers, and then New Life through its partner

organization seeks to fulfill these Credit needs.

2.4 MICRO-CREDIT BENEFITS THE POOR

There is clear evidence that MF benefits the poor by providing them savings

opportunities and credit. Barrowers often increase their incomes and improve their livelihood

because of micro-credit. The employment impact is, however more limited. MF leads to changes

in the use of technology only of the less poor as adoption of new technology is risky and the

poorer borrowers are more risk averse. The poor also benefit from mF a sense of involvement

and dignity. Where wide gender disparities abound, MF catering to women raises their sense of

participation and increases their empowerment. There is however little evidence that MF

succeeds in transforming a community from poverty to prosperity.

An economically poor individual gains strength as part of a group. Besides, financing

through SHGs reduces transaction costs for both lenders and borrowers. While lenders have to

handle only a single SHG account instead of a large number of small-sized individual accounts,

borrowers as part of a SHG cut down expenses on travel (to & from the branch and other places)

for completing paper work and on the loss of workdays in canvassing for loans.

2.5 SCOPE OF MICRO FINANCE

Micro finance usually refers to investments with more opportunity for high profits, and

also more risk: options, futures, currency trading, penny stocks, etc. Profits can be in the double

digit percentages per day! But so can losses, if you're not careful. Other short-term investments,

like money market funds, can be very conservative and designed to earn a little while keeping

your money safe in anticipation of some upcoming need, such as a down payment for a house in

a few weeks or months. Microfinance is a broad category of services, which includes

microcredit. Microcredit is provision of credit services to poor clients. Although microcredit is

one of the aspects of microfinance, conflation of the two terms is endemic in public discourse.

Critics often attack microcredit while referring to it indiscriminately as either 'microcredit' or

'microfinance'.

The sources of Micro financing include trade credit, bank loans, bankers acceptances,

finance company loans, commercial paper, receivable financing, and inventory financing. One

particular source may be more appropriate than another in a given circumstance; some are more

desirable than others because of interest rates or collateral requirements. Note: Banker`s`

acceptances is a time draft payable on a specified date and guaranteed by the bank.

2.6 SELF-HELP GROUPS AND MICRO-FINANCE

There is a welcome recognition in the Finance Minister's speech of the role MFIs have

played in catering to the credit needs of the poorer sections of rural society. This is a function

mainline bank in India and most other countries have been unable to do on their own. Since

February 2000 when the Reserve Bank of India gave priority sector status to loans provided by

banks to the MFIs, the activity has been mainstream. Experience of operating a micro-credit

model pioneered by the National Bank for Agriculture and Rural Development (NABARD)

during 1991-92 has shown that establishing a linkage between an SHG and a bank is the best

method for bringing SHGs into the ambit of formal banking especially because it infuses a

degree of professionalism into the services offered to the rural poor.

The budget has ambitious plans to extend the target of credit linking for 2005-06 from

200,000 self-help groups to 250,000. The Government hopes to enhance the beneficial role of the

MFIs as an intermediary between banks and rural borrowers. Commercial banks will be allowed

to appoint MFIs as their "banking correspondents" for providing a variety of services on their

behalf. That will vastly increase their reach and remove some of the intractable rigidities that

have stood in the way of the spread of rural banking. Close to 70 per cent of the rural poor do not

have a bank account and 87 per cent do not have access to credit from a formal source. The

proposal to appoint MFIs as agents for micro-insurance products will help spread the insurance

habit and enable them to earn a fee income. Another significant proposal is to let the eligible

MFIs seek equity support from the redesignated Micro Finance Development and Equity Fund,

which has a corpus of Rs. 200 crore.

Originally confined to the southern States, micro-finance is fast spreading to the rest of

India. For the banking system, the SHG linkage has been a winning proposition. It has resulted in

lower transaction costs, negligible defaults, and the generation of enormous goodwill. The MFIs

have been adept at providing customized solutions based on their understanding of local

conditions. However, a number of weaknesses remain. Banks have not yet standardized their

approach towards micro-lending. A lack of infrastructure and design facilities and also

worthwhile distribution channels for marketing the products has constrained growth. A number

of initiatives are needed to keep the micro-finance system on track. The goal is to make it a

dispenser not just of credit but of a variety of social goods and services to the rural poor.

2.7 MICRO-FINANCE AND ITS OBJECTIVES

The concept of microfinance is not new. Savings and credits groups that have operated

for centuries include the “susus” of Ghana, “chit funds” in India, “tandas” in Mexico, and

“pasanaku” in Bolivia, as well as numerous savings clubs and burial societies found all over the

world. One of the earlier and longer lived microcredit organizations was the Irish loan fund

system, initiated in the early 1700s. The term micro-finance is commonly used in addressing

issues related to poverty alleviation, financial support to micro-entrepreneurs and gender

development etc. Micro- finance can be defined as “provision of thrift, credit and other financial

services and products of very small amounts to the poor in rural, semi- urban or urban areas for

enabling them to raise their income levels and improve living standards “.

The term micro-finance sometimes is used interchangeably with the term micro-credit.

However, while micro-credit refers to purveyance of loans in small quantities, the term micro

finance has a broader meaning covering in its ambit other financial services like saving,

insurance etc.

The main benefits of micro-finance appear to be reduced vulnerability of the poor to

adverse circumstances, increased consumption in the same group and empowerment of women.

Fortunately, micro-finance practice in India like some other countries has much to offer to the

rural population. These include poverty alleviation, livelihood promotion, developing the local

economy, gender empowerment, building organizations and changing wider systems and

institutions within society.

2.8 DEVELOPMENT OF SHGS

Self Help Groups are considered as one of the most significant tools to adopt

participatory approach for the economic empowerment of women. It is an important institution

for improving the life of women on various social and economic components. The basic

objective of an SHG is that it acts as the forum for members to provide space and support to each

other and get financial sustainability through adopting micro-enterprises based on availability of

resources, prevalent skill and availability of markets for sale of products. Group entrepreneurship

is ideal for weaker sections of the society and it is an instrument which helps the poor women to

overcome their poverty. It gives employment opportunities for illiterates.

2.9 FORMATION OF SELF HELP GROUPS

An SHG both by definition and in practice is a group of individual members who by free

association come together for a common collective purpose. In practice SHG comprise

individual members known to each other coming from the same village, community and even

marketing neighborhood. That is they are homogeneous and have certain pre group social

binding factors. In the context of micro-finance, SHG are formed around the theme of savings

and credit.

Self-Help Groups don't start with credit; they start as savers groups, with regular weekly

for forthrightly saving targets. Each number of the group has to save a small amount per month.

The savings are deposited in a meeting on an appointed time every week, and the collected

saving are lent to members, with the decision on who gets the loan being taken by the group; in

many groups saving are entered in individual passbooks. Some groups pay interest on saving,

others pay dividends; but most have retained their earnings as part of their capital. An account is

opened with a mainline bank to deposit any surplus savings. After some six months, the bank

where the savings were deposited examines the performance of the group and issues loans to the

group. The SHG in turn increases its capacity to manage high amount of finance, develop

entrepreneurial and communication skills and logical ability, cooperative sense and finally

income and employment generating confidence.

The main objective of SHGs is to inculcate the habit of thrift, savings and banking

culture to gain economic prosperity through credit. The most important component of SHG is the

mobilization and organization of women towards the basic strength of solidarity, informality and

collective action. Self Help Group methodology is a novel approach in development of

economics. These groups can create a unique, alternative, need-based credit delivery mechanism

by pooling their insufficient resources for catering to their consumption and occupational

requirement.

3.0 CHARACTERISTICS OF A GOOD SELF HELP GROUP

Well-functioning SHG should have following structural features:

An ideal SHG comprises 15-20 members.

All the members should belong to the same socio-economic strata of society specifically

poor.

Group should have strong bond of affinity.

Rotational leadership should be encouraged for distribution of power and to provide

leadership opportunities to all the members.

Members should attend meetings, save and participate in all activities voluntarily.

To provide gainful employment and to involve the poor in productive activities.

An SHG should be socially viable institution.

The procedure of decision-making in SHG should be democratic in nature.

It should be non-partisan in nature.

The group is frames rules and regulations which are required for its effective functioning.

To involve women in decision making and to promote leadership qualities among them.

CHAPTER- III

CHAPTER- III

ANALYSIS AND I NTERPRETATION OF DATA

3.1 INTRODUCTION

To assess the Microfinance Performance in SHG were selected through the Reference

papers, Web Documents, and Books. And well structured data are prepared and collected the

required data from the sample. The analyses are made with the help of Statistical tools like

Graphical Charts and Percentage Analysis.

3.2 OVERALL PROGRESS UNDER SHG-BANK LINKAGES

The selected samples of SHG are classified into the Bank linkages. The

linkages of the SHG Savings with Bank is given in the Table 1.1

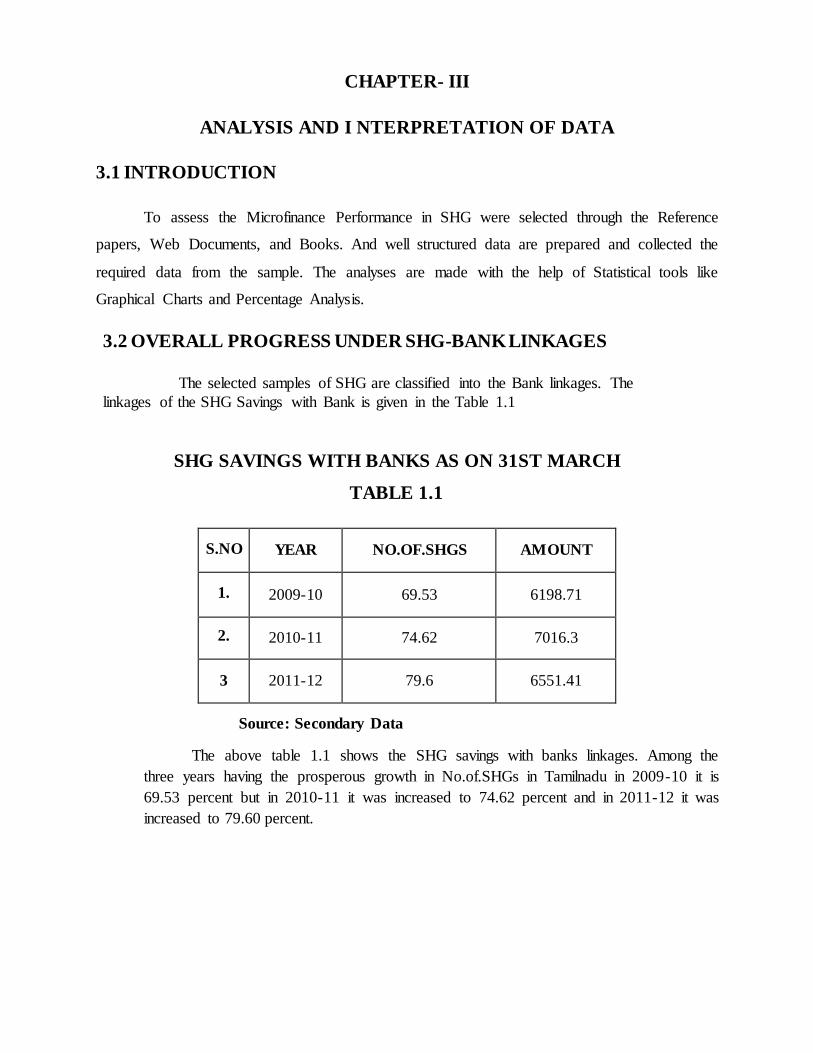

SHG SAVINGS WITH BANKS AS ON 31ST MARCH

TABLE 1.1

Source: Secondary Data

The above table 1.1 shows the SHG savings with banks linkages. Among the

three years having the prosperous growth in No.of.SHGs in Tamilnadu in 2009-10 it is

69.53 percent but in 2010-11 it was increased to 74.62 percent and in 2011-12 it was

increased to 79.60 percent.

S.NO YEAR NO.OF.SHGS AMOUNT

1. 2009-10 69.53 6198.71

2. 2010-11 74.62 7016.3

3 2011-12 79.6 6551.41

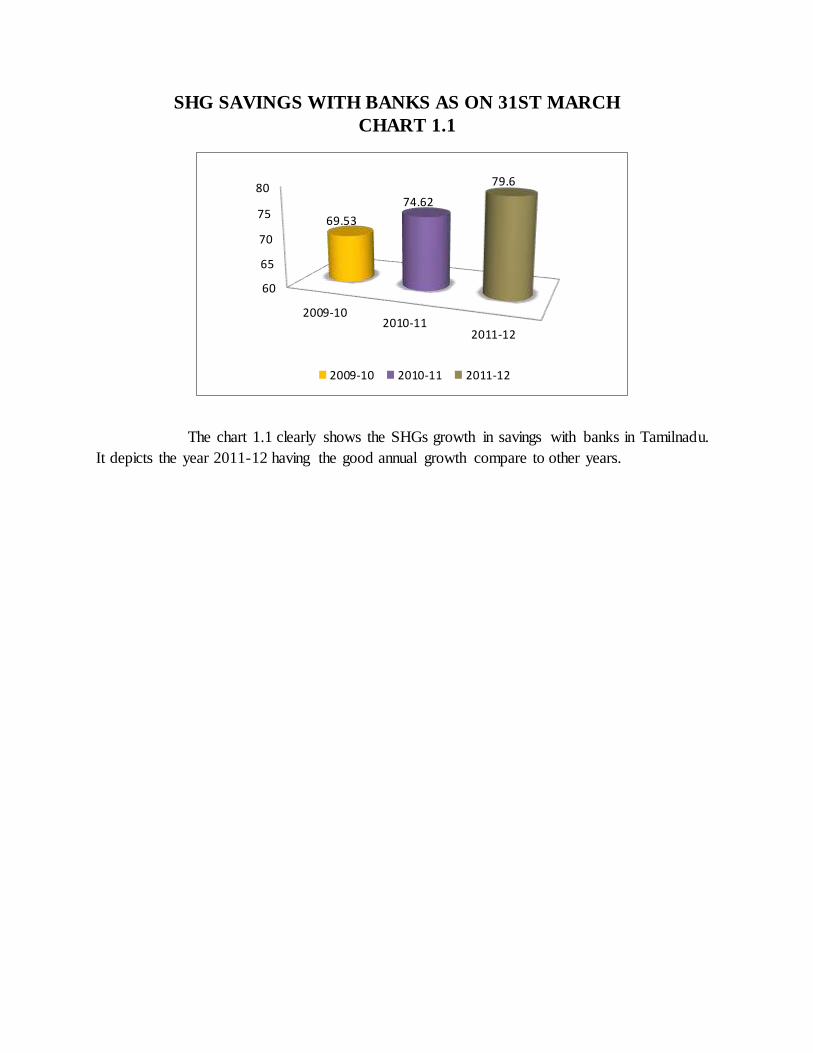

SHG SAVINGS WITH BANKS AS ON 31ST MARCH

CHART 1.1

The chart 1.1 clearly shows the SHGs growth in savings with banks in Tamilnadu.

It depicts the year 2011-12 having the good annual growth compare to other years.

60

65

70

75

80

2009-102010-11

2011-12

69.53

74.62

79.6

2009-10 2010-11 2011-12

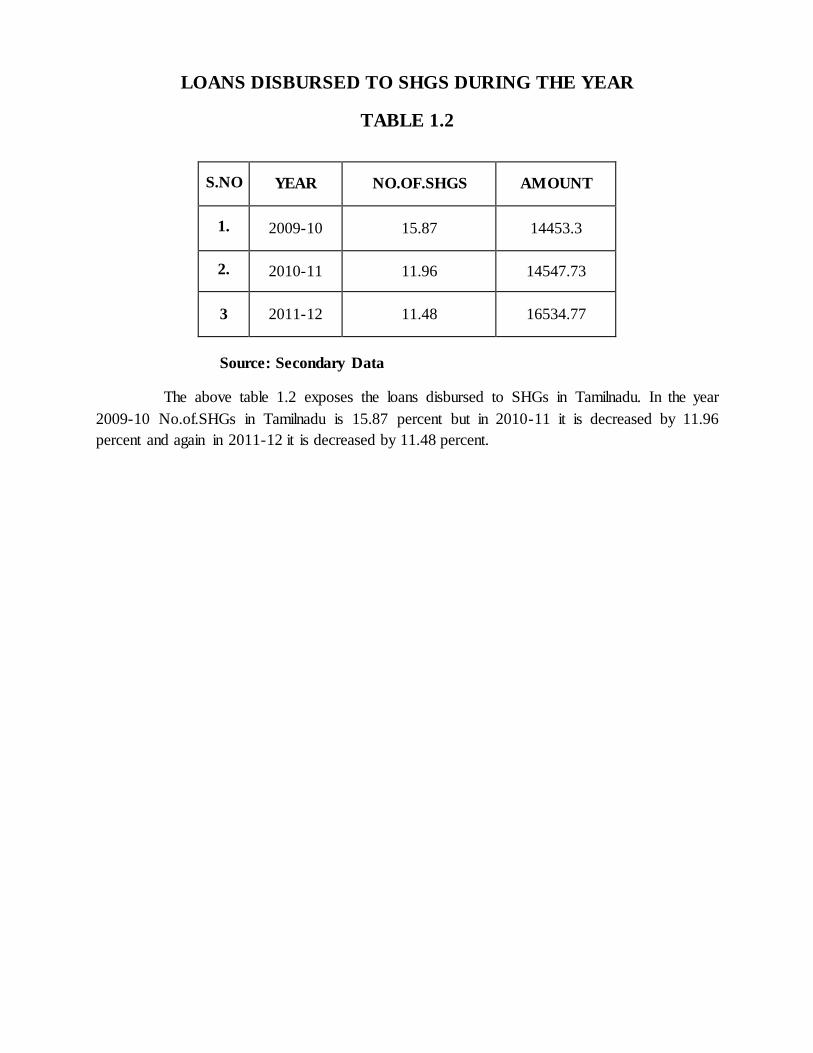

LOANS DISBURSED TO SHGS DURING THE YEAR

TABLE 1.2

Source: Secondary Data

The above table 1.2 exposes the loans disbursed to SHGs in Tamilnadu. In the year

2009-10 No.of.SHGs in Tamilnadu is 15.87 percent but in 2010-11 it is decreased by 11.96

percent and again in 2011-12 it is decreased by 11.48 percent.

S.NO YEAR NO.OF.SHGS AMOUNT

1. 2009-10 15.87 14453.3

2. 2010-11 11.96 14547.73

3 2011-12 11.48 16534.77

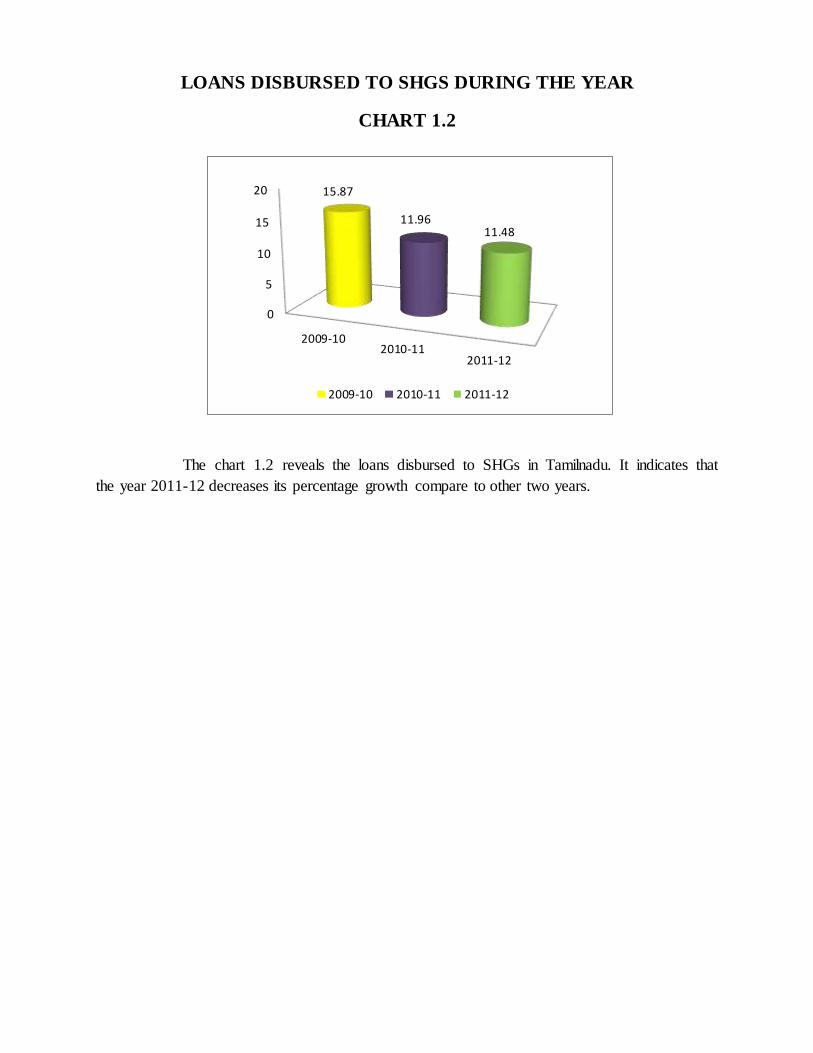

LOANS DISBURSED TO SHGS DURING THE YEAR

CHART 1.2

The chart 1.2 reveals the loans disbursed to SHGs in Tamilnadu. It indicates that

the year 2011-12 decreases its percentage growth compare to other two years.

0

5

10

15

20

2009-102010-11

2011-12

15.87

11.9611.48

2009-10 2010-11 2011-12

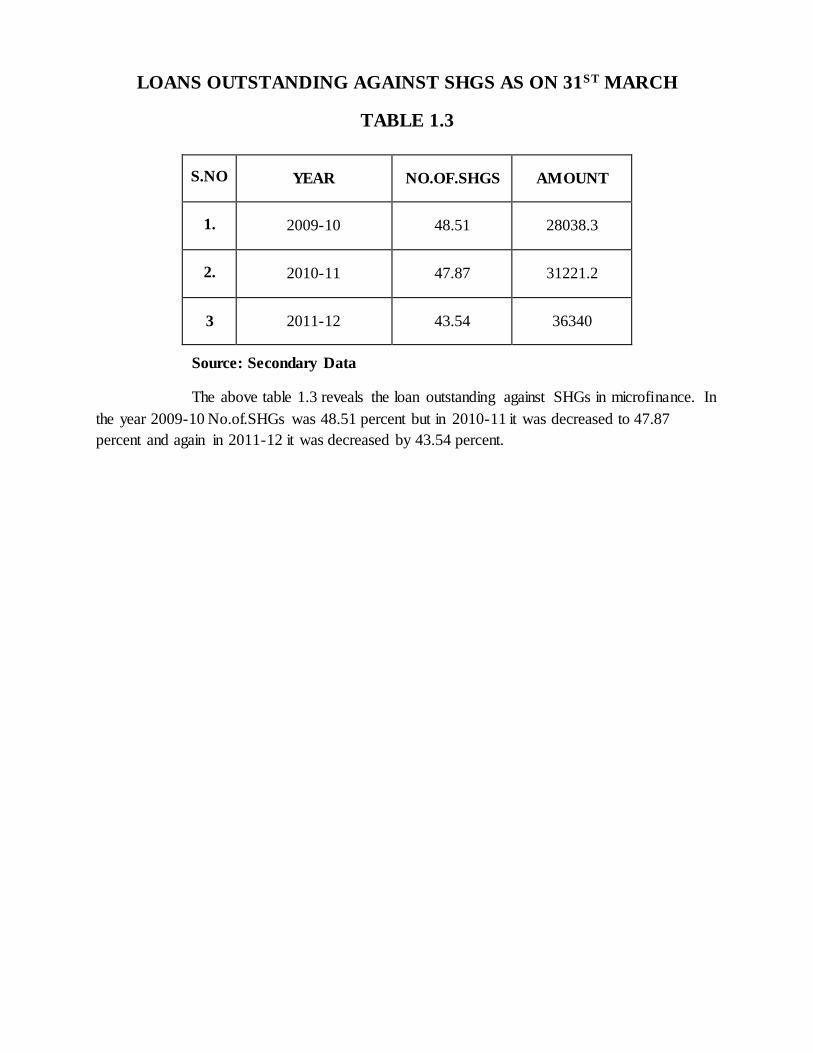

LOANS OUTSTANDING AGAINST SHGS AS ON 31ST MARCH

TABLE 1.3

Source: Secondary Data

The above table 1.3 reveals the loan outstanding against SHGs in microfinance. In

the year 2009-10 No.of.SHGs was 48.51 percent but in 2010-11 it was decreased to 47.87

percent and again in 2011-12 it was decreased by 43.54 percent.

S.NO YEAR NO.OF.SHGS AMOUNT

1. 2009-10 48.51 28038.3

2. 2010-11 47.87 31221.2

3 2011-12 43.54 36340

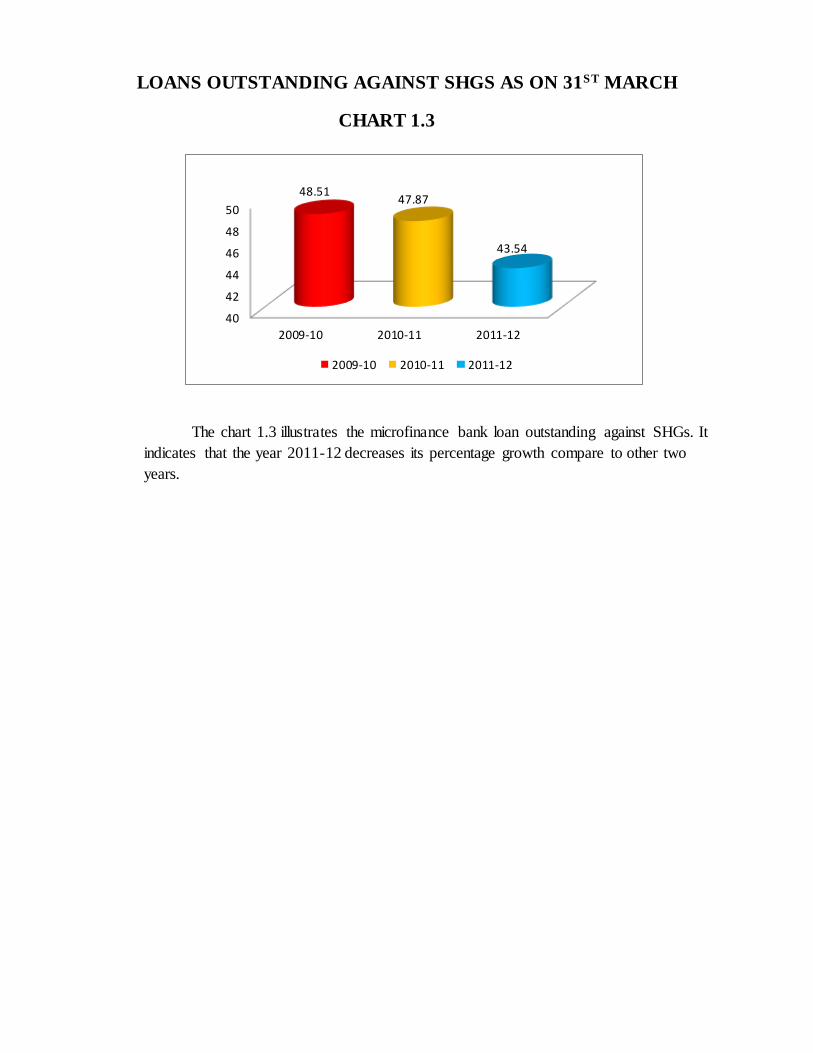

LOANS OUTSTANDING AGAINST SHGS AS ON 31ST MARCH

CHART 1.3

The chart 1.3 illustrates the microfinance bank loan outstanding against SHGs. It

indicates that the year 2011-12 decreases its percentage growth compare to other two

years.

40

42

44

46

48

50

2009-10 2010-11 2011-12

48.5147.87

43.54

2009-10 2010-11 2011-12

WOMAN SHGS SAVINGS WITH BANK AS ON 31ST MARCH

TABLE 1.4

S.NO YEAR NO.OF.SHGS AMOUNT

1. 2009-10 53.1 4498.66

2. 2010-11 60.98 5298.65

3. 2011-12 62.99 5104.33

Source: Secondary Data

The above table 1.4 shows the women’s SHGs saving with bank among the three

years having the prosperous growth in No.of.SHGs in Tamilnadu. In 2009-10 is 53.10 percent

and in 2010-11 it was increased to 60.98 percent and 2011-12 it was again increased to 62.99

percent.

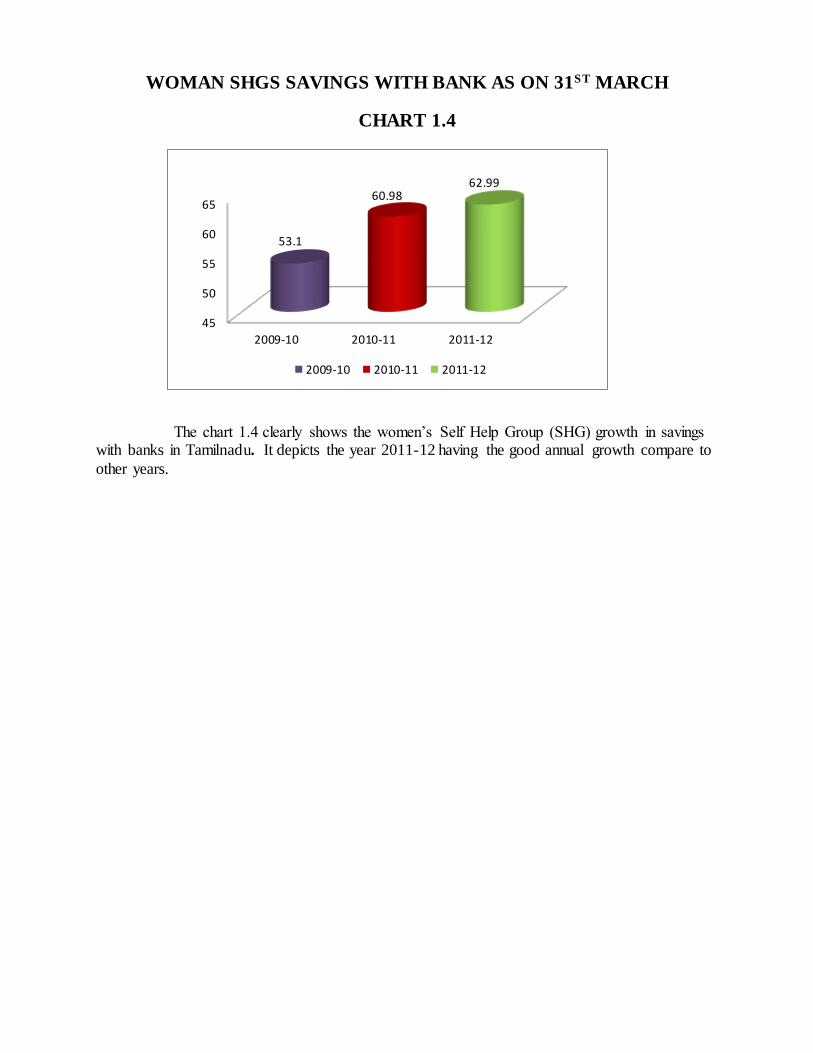

WOMAN SHGS SAVINGS WITH BANK AS ON 31ST MARCH

CHART 1.4

The chart 1.4 clearly shows the women’s Self Help Group (SHG) growth in savings with banks in Tamilnadu. It depicts the year 2011-12 having the good annual growth compare to

other years.

45

50

55

60

65

2009-10 2010-11 2011-12

53.1

60.9862.99

2009-10 2010-11 2011-12

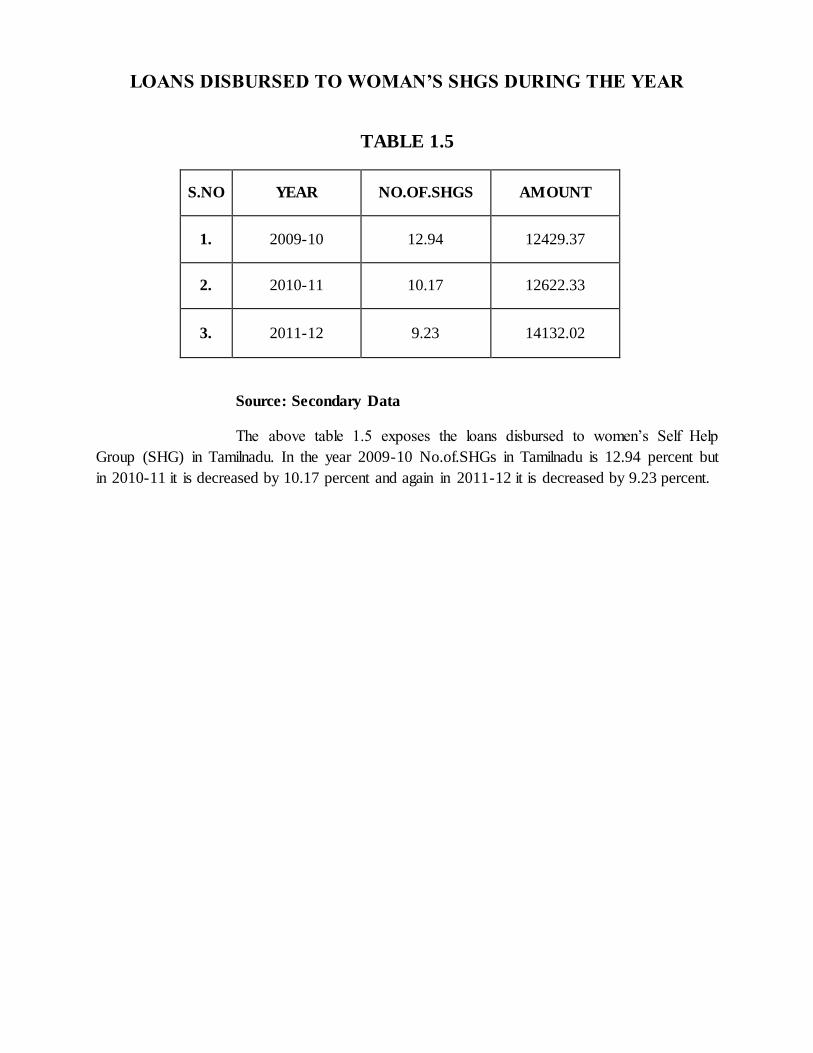

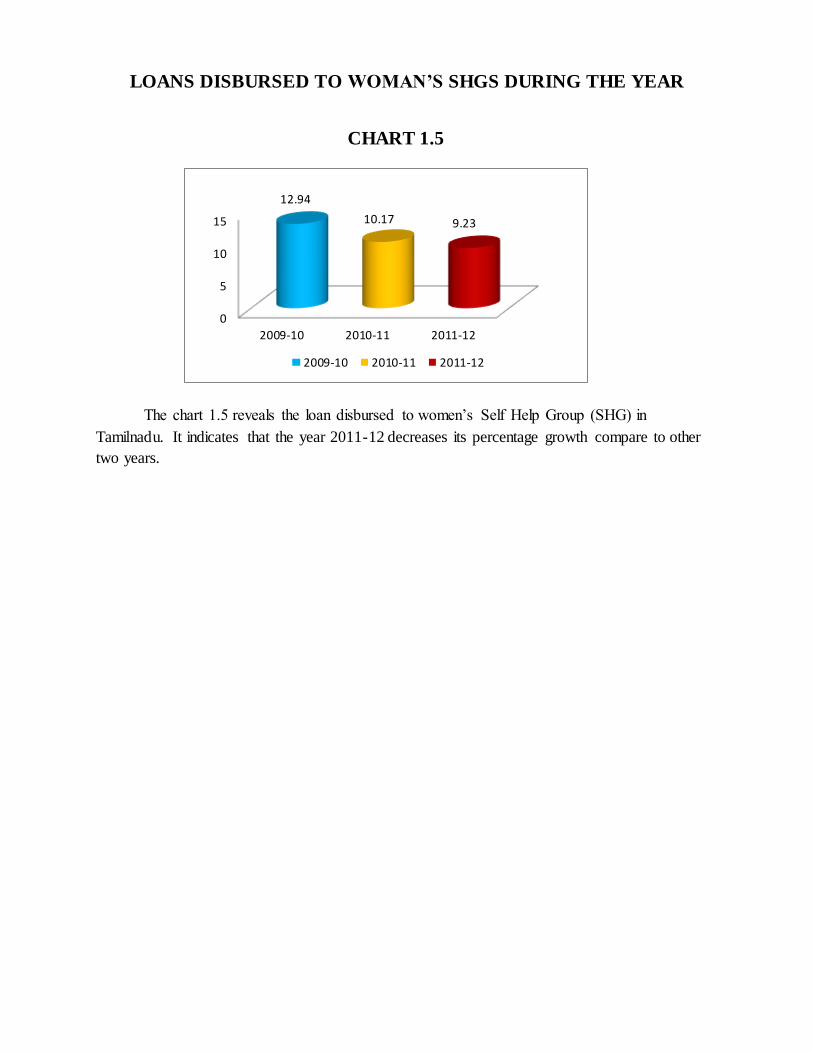

LOANS DISBURSED TO WOMAN’S SHGS DURING THE YEAR

TABLE 1.5

S.NO YEAR NO.OF.SHGS AMOUNT

1. 2009-10 12.94 12429.37

2. 2010-11 10.17 12622.33

3. 2011-12 9.23 14132.02

Source: Secondary Data

The above table 1.5 exposes the loans disbursed to women’s Self Help

Group (SHG) in Tamilnadu. In the year 2009-10 No.of.SHGs in Tamilnadu is 12.94 percent but

in 2010-11 it is decreased by 10.17 percent and again in 2011-12 it is decreased by 9.23 percent.

LOANS DISBURSED TO WOMAN’S SHGS DURING THE YEAR

CHART 1.5

The chart 1.5 reveals the loan disbursed to women’s Self Help Group (SHG) in

Tamilnadu. It indicates that the year 2011-12 decreases its percentage growth compare to other

two years.

0

5

10

15

2009-10 2010-11 2011-12

12.94

10.17 9.23

2009-10 2010-11 2011-12

LOANS OUTSTANDING AGAINST WOMAN’S SHGS AS ON 31ST

MARCH

TABLE 1.6

S.NO YEAR NO.OF.SHGS AMOUNT

1. 2009-10 38.98 23030.4

2. 2010-11 39.84 26123.8

3. 2011-12 36.49 30465.3

Source: Secondary Data

The above table 1.6 reveals the loan outstanding against women’s Self Help Group

(SHG) in microfinance. In the year 2009-10 No.of.SHGs was 38.98 percent but in 2010-11 it

was increased by 39.84 percent and in 2011-12 again it was decreased by 36.49 percent.

LOANS OUTSTANDING AGAINST WOMAN’S SHGS AS ON 31ST

MARCH

CHART 1.6

The chart 1.6 illustrates the microfinance bank loan outstanding against women’s Self

Help Group (SHG). It indicates that the year 2011-12 decreases its percentage growth compare

to other two years.

34

35

36

37

38

39

40

2009-10 2010-11 2011-12

38.98

39.84

36.49

2009-10 2010-11 2011-12

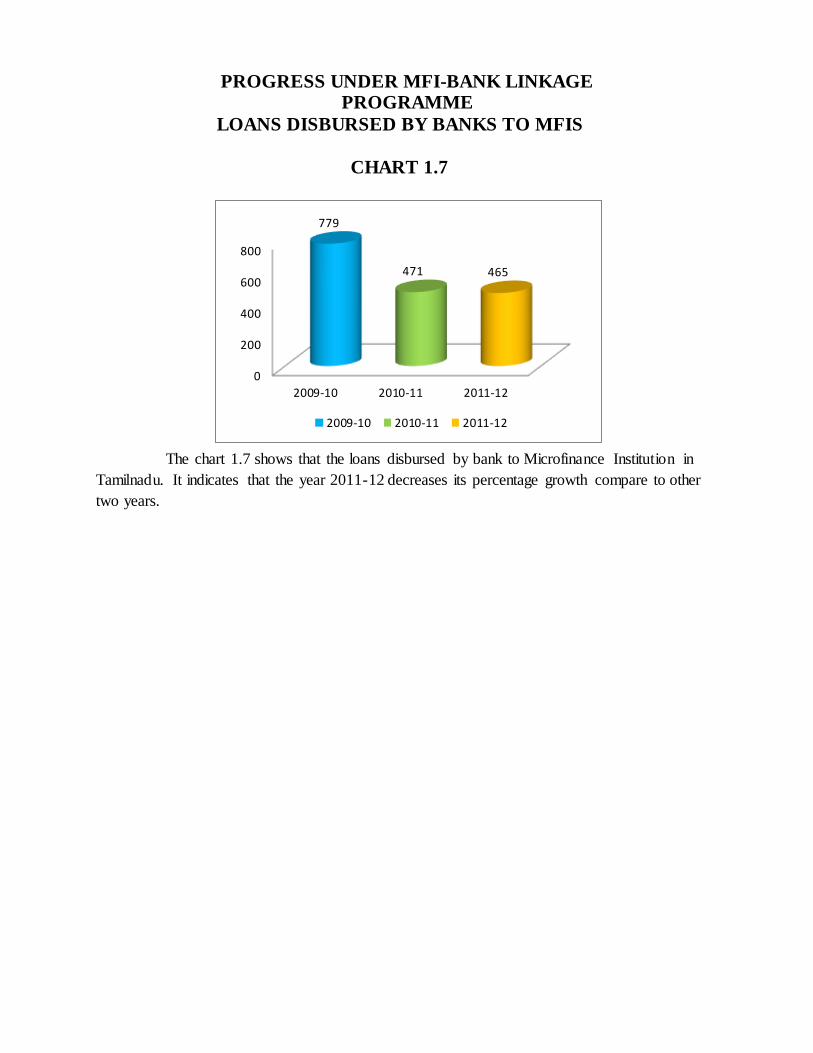

Source: Secondary Data

The above table 1.7 shows the progress under Microfinance Institution Bank

linkages programme with loans disbursed by banks to Microfinance Institutions. In the year

2009-10 No.of.MFIs in Tamilnadu were 779 percent and in 2011-12 it is decreased by 471 and in

2011-12 it is again decreased by 465 percent.

PROGRESS UNDER MFI-BANK LINKAGE PROGRAMME

LOANS DISBURSED BY BANKS TO MFIS

TABLE 1.7

S.NO YEAR NO.OF.MIFS AMOUNT

1. 2009-10 779 10728.5

2. 2010-11 471 8448.96

3. 2011-12 465 5205.29

The chart 1.7 shows that the loans disbursed by bank to Microfinance Institution in

Tamilnadu. It indicates that the year 2011-12 decreases its percentage growth compare to other

two years.

PROGRESS UNDER MFI-BANK LINKAGE PROGRAMME

LOANS DISBURSED BY BANKS TO MFIS

CHART 1.7

0

200

400

600

800

2009-10 2010-11 2011-12

779

471 465

2009-10 2010-11 2011-12

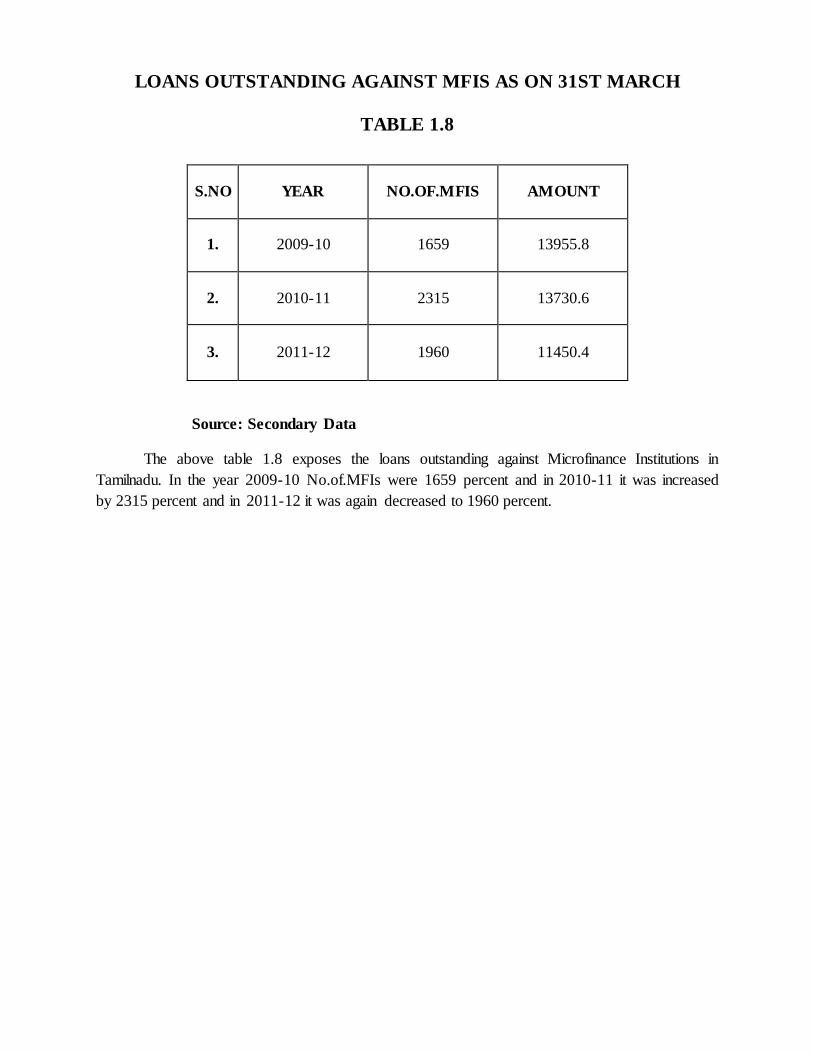

LOANS OUTSTANDING AGAINST MFIS AS ON 31ST MARCH

TABLE 1.8

Source: Secondary Data

The above table 1.8 exposes the loans outstanding against Microfinance Institutions in

Tamilnadu. In the year 2009-10 No.of.MFIs were 1659 percent and in 2010-11 it was increased

by 2315 percent and in 2011-12 it was again decreased to 1960 percent.

S.NO YEAR NO.OF.MFIS AMOUNT

1. 2009-10 1659 13955.8

2. 2010-11 2315 13730.6

3. 2011-12 1960 11450.4

LOANS OUTSTANDING AGAINST MFIS AS ON 31ST MARCH

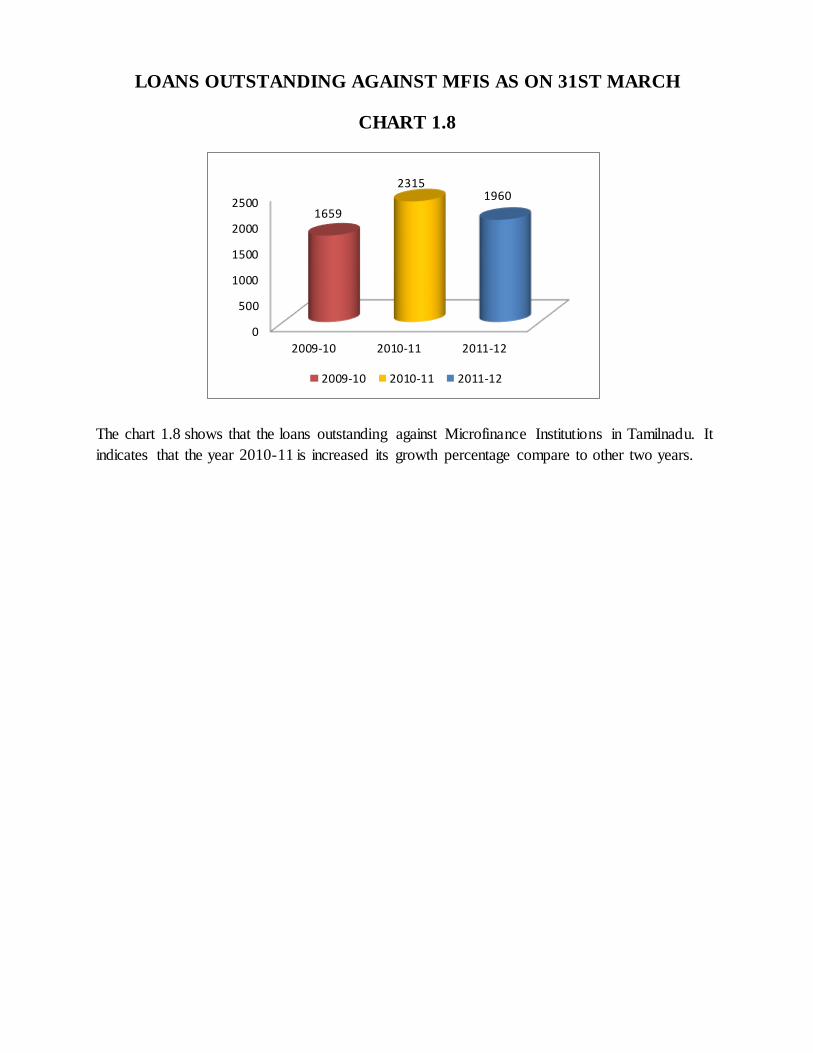

CHART 1.8

The chart 1.8 shows that the loans outstanding against Microfinance Institutions in Tamilnadu. It

indicates that the year 2010-11 is increased its growth percentage compare to other two years.

0

500

1000

1500

2000

2500

2009-10 2010-11 2011-12

1659

23151960

2009-10 2010-11 2011-12

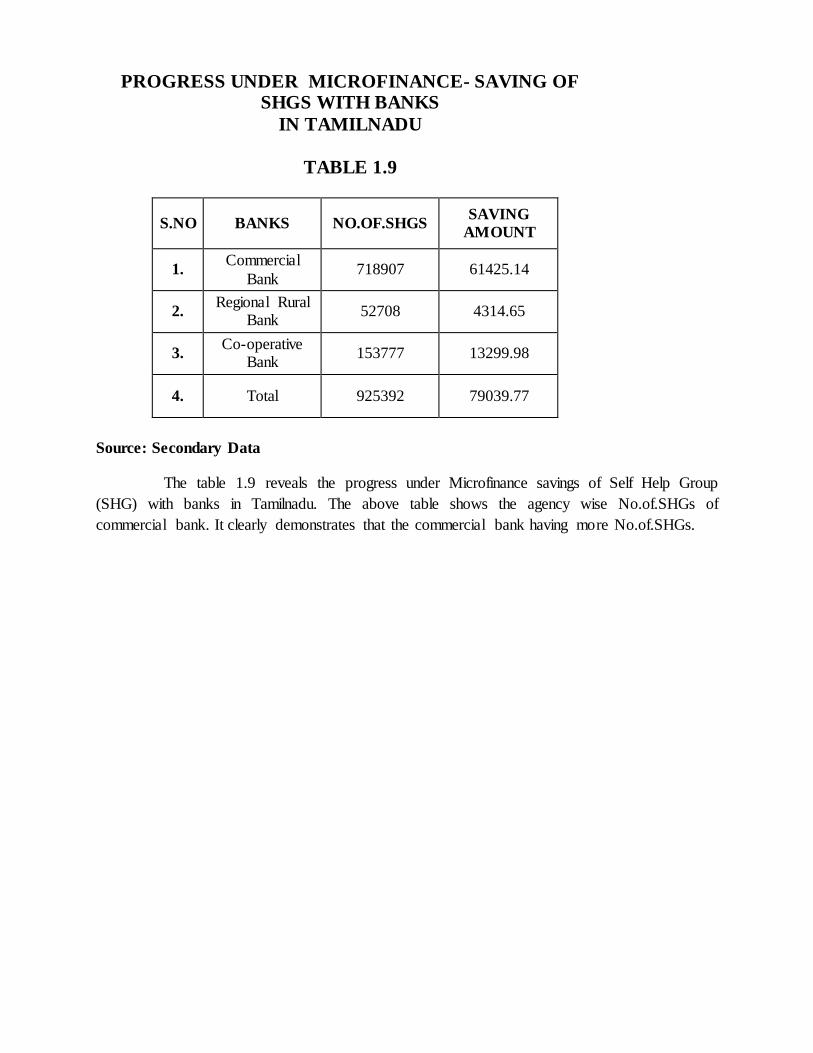

PROGRESS UNDER MICROFINANCE- SAVING OF SHGS WITH BANKS

IN TAMILNADU

TABLE 1.9

Source: Secondary Data

The table 1.9 reveals the progress under Microfinance savings of Self Help Group

(SHG) with banks in Tamilnadu. The above table shows the agency wise No.of.SHGs of

commercial bank. It clearly demonstrates that the commercial bank having more No.of.SHGs.

S.NO BANKS NO.OF.SHGS SAVING

AMOUNT

1. Commercial

Bank 718907 61425.14

2. Regional Rural

Bank 52708 4314.65

3. Co-operative

Bank 153777 13299.98

4. Total 925392 79039.77

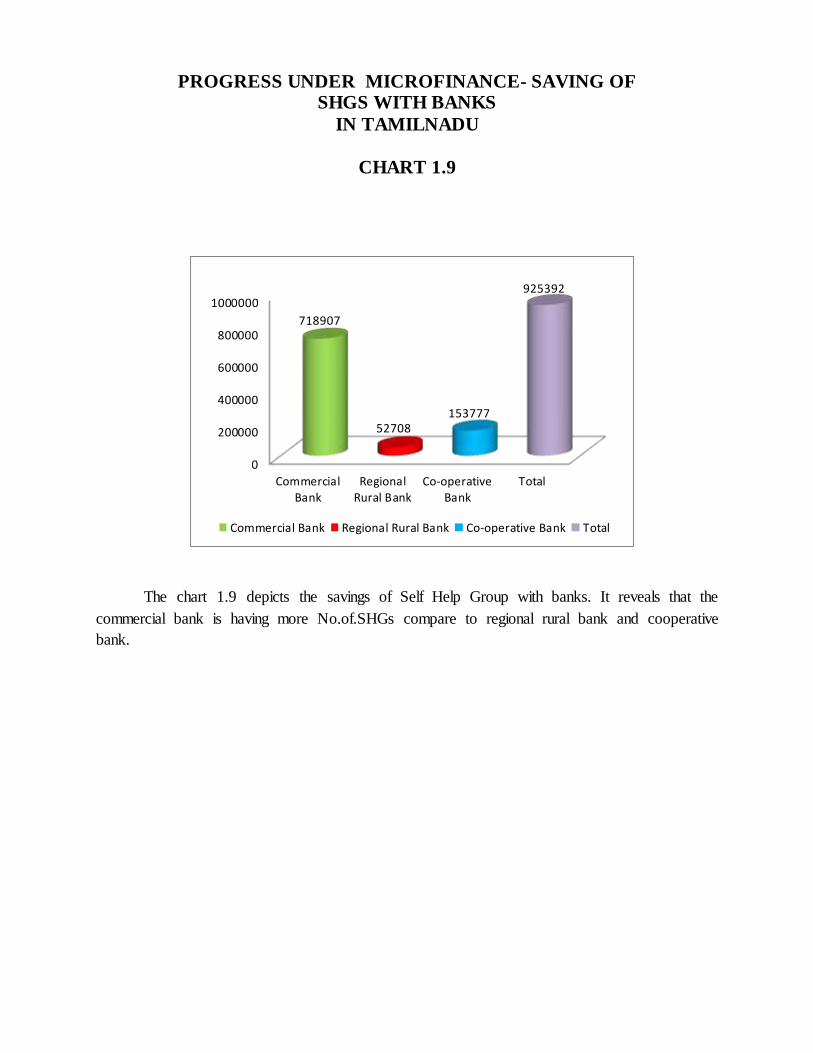

The chart 1.9 depicts the savings of Self Help Group with banks. It reveals that the

commercial bank is having more No.of.SHGs compare to regional rural bank and cooperative

bank.

PROGRESS UNDER MICROFINANCE- SAVING OF SHGS WITH BANKS

IN TAMILNADU

CHART 1.9

0

200000

400000

600000

800000

1000000

Commercial

BankRegional

Rural BankCo-operative

BankTotal

718907

52708153777

925392

Commercial Bank Regional Rural Bank Co-operative Bank Total

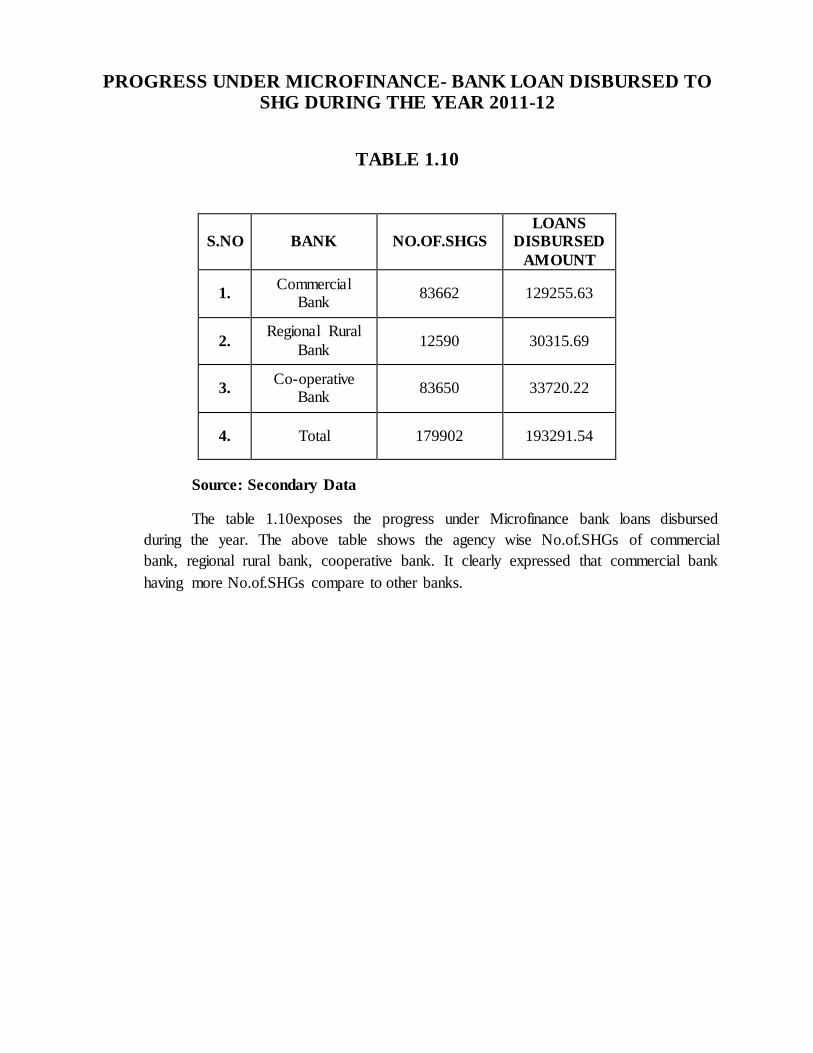

PROGRESS UNDER MICROFINANCE- BANK LOAN DISBURSED TO SHG DURING THE YEAR 2011-12

TABLE 1.10

Source: Secondary Data

The table 1.10exposes the progress under Microfinance bank loans disbursed

during the year. The above table shows the agency wise No.of.SHGs of commercial

bank, regional rural bank, cooperative bank. It clearly expressed that commercial bank

having more No.of.SHGs compare to other banks.

S.NO BANK NO.OF.SHGS

LOANS

DISBURSED

AMOUNT

1. Commercial

Bank 83662 129255.63

2. Regional Rural

Bank 12590 30315.69

3. Co-operative

Bank 83650 33720.22

4. Total 179902 193291.54

PROGRESS UNDER MICROFINANCE- BANK LOAN DISBURSED TO SHG DURING THE YEAR 2011-12

CHART 1.10

The chart 1.10 illustrates the bank loan disbursed during the year. Commercial bank

having the more No.of.SHGs compare to regional rural bank and cooperative bank.

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Commercial

Bank

Regional Rural

Bank

Co-operative

Bank

Total

83662

12590

83650

179902

Commercial Bank Regional Rural Bank Co-operative Bank Total

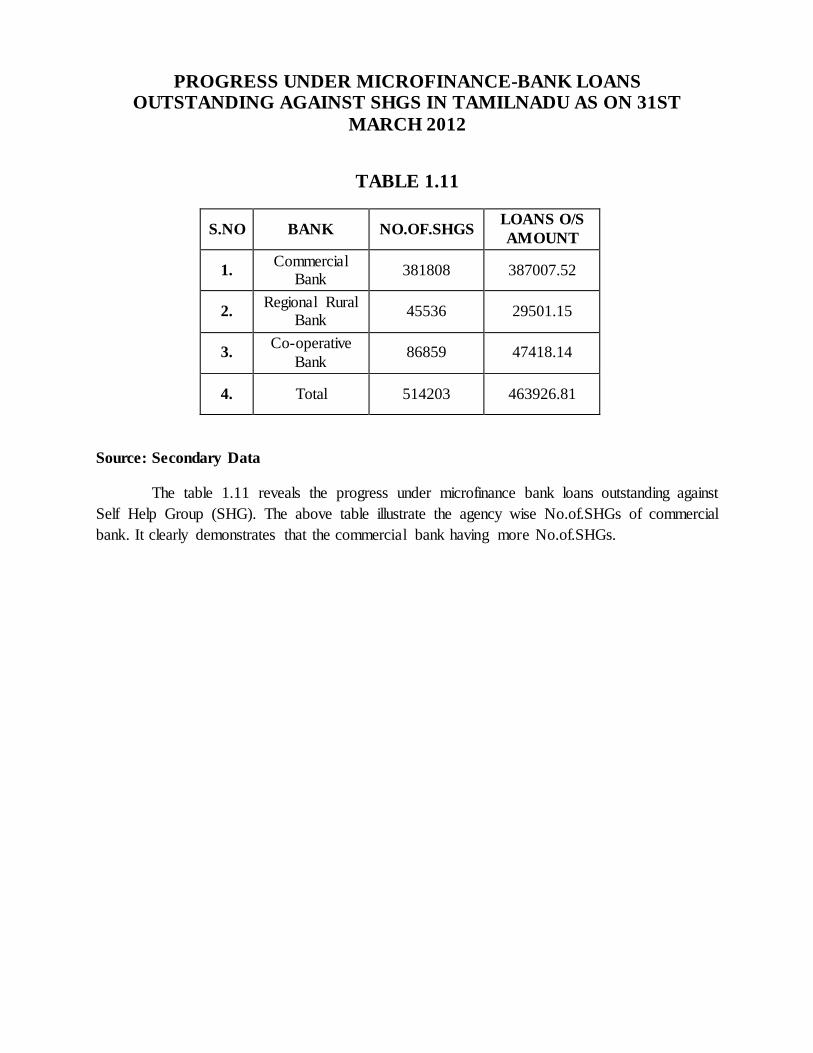

PROGRESS UNDER MICROFINANCE-BANK LOANS OUTSTANDING AGAINST SHGS IN TAMILNADU AS ON 31ST

MARCH 2012

TABLE 1.11

S.NO BANK NO.OF.SHGS LOANS O/S

AMOUNT

1. Commercial

Bank 381808 387007.52

2. Regional Rural

Bank 45536 29501.15

3. Co-operative

Bank 86859 47418.14

4. Total 514203 463926.81

Source: Secondary Data

The table 1.11 reveals the progress under microfinance bank loans outstanding against

Self Help Group (SHG). The above table illustrate the agency wise No.of.SHGs of commercial

bank. It clearly demonstrates that the commercial bank having more No.of.SHGs.

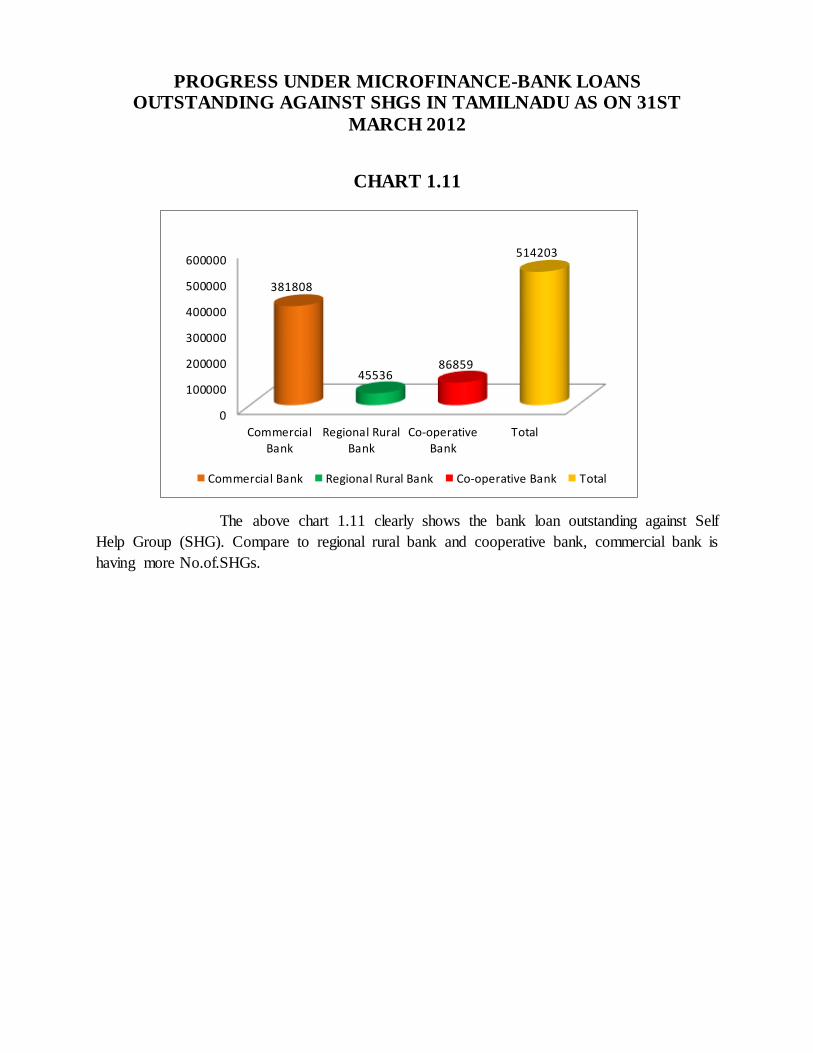

PROGRESS UNDER MICROFINANCE-BANK LOANS OUTSTANDING AGAINST SHGS IN TAMILNADU AS ON 31ST

MARCH 2012

CHART 1.11

The above chart 1.11 clearly shows the bank loan outstanding against Self

Help Group (SHG). Compare to regional rural bank and cooperative bank, commercial bank is

having more No.of.SHGs.

0

100000

200000

300000

400000

500000

600000

Commercial

BankRegional Rural

BankCo-operative

BankTotal

381808

4553686859

514203

Commercial Bank Regional Rural Bank Co-operative Bank Total

CHAPTER-IV

CHAPTER- IV

FINDINGS, SUGGESION AND CONCLUSION

4.1 FINDINGS

Self Help Group (SHG) bank linkage and saving with banks was increased by

No.of.SHGs in the year from 2009-12 by 79.60 percent.

Disbursement of loan to No.of.SHGs was gradually decreased in the year 2011-12

by 11.48 percent which compare to 2009-10.

Outstanding loans against No.of.SHGs was decreased from 2009-12 gradually to

43.54 percent.

Women’s savings with banks was increased by No.of.SHGs in the year 2009-12

by 62.99 percent.

Disbursed of loans to No.of.SHGs was gradually decreased in the year 2011-12

by 9.23 percent which compare to other years.

Outstanding loans against No.of.SHGs were increased in the year 2010-11 with

39.84 percent and it was decreased in the year 2011-12 with 36.49 percent.

Microfinance Institution with loans disbursed by bank to No.of.MFI decreased

gradually from the year 2009-12 by 465 percent.

Outstanding loans against Microfinance Institutions were increased in the year

2010-11 with 2315 and it was decreased in the year 2011-12 with 1960.

Savings of Self Help Group (SHG) with bank in Tamilnadu with total

No.of.SHGs was having a good growth in commercial bank.

Disbursement of bank loans to No.of.SHGs with commercial bank is having the

good growth than other two banks.

Bank loan outstanding against Self Help Group (SHG) in Tamilnadu is having the

tremendous growth in commercial bank which compare to regional rural bank and

cooperative bank.

CONCLUTION

The study reveals the microfinance programme has become an important tool to eradicate

poverty in Tamilnadu. It is gathering momentum to become a major force in Tamilnadu. The

Self Help Group (SHG) model with bank lending to groups of poor women without collateral has

become an accepted part of rural finance. Yearly base analysis was made over Tamilnadu to

know the performance of microfinance in Self Help Group (SHG). In 2011-12 there is a good

level of growth in No.of.SHGs with savings banks and women’s savings banks. Disbursement of

loan to SHGs and women’s SHGs was reduced in 2011-12. So it shows that the Tamilnadu

having good growth in SHGs and better repayment of loans to the government. Disbursement of

loans by banks to No.of.MFI is good in 2009-10 which compare to other two years. Outstanding

of loans against No.of.MFI is good in 2010-11 which compare to other two years. Microfinance

is a Bank which gives an interest to SHGs commercial bank has the tremendous growth in

No.of.SHGs in Tamilnadu which compare to other Banks. Disbursement of bank loans to Self

Help Group (SHG) in commercial bank has a good growth in microfinance in Tamilnadu. By

comparing other two banks. Outstanding of loans in Self Help Group (SHG) commercial bank

has the prosperous growth in No.of.SHGs of microfinance in Tamilnadu. The major crisis

happened in microfinance industry, the fact that private bank microfinance is in competition with

public bank Self Help Group (SHG) programme is itself a major reason for the crisis.