MICRO SAVINGS AND MICROINSURANCE IN INDIA Presented by: Manoj K. Sharma.

19

MICRO SAVINGS AND MICROINSURANCE IN INDIA Presented by: Manoj K. Sharma

-

Upload

maurice-baker -

Category

Documents

-

view

221 -

download

5

Transcript of MICRO SAVINGS AND MICROINSURANCE IN INDIA Presented by: Manoj K. Sharma.

MICRO SAVINGS AND MICROINSURANCE IN INDIA

Presented by:

Manoj K. Sharma

FINANCIAL INCLUSION SCENARIO

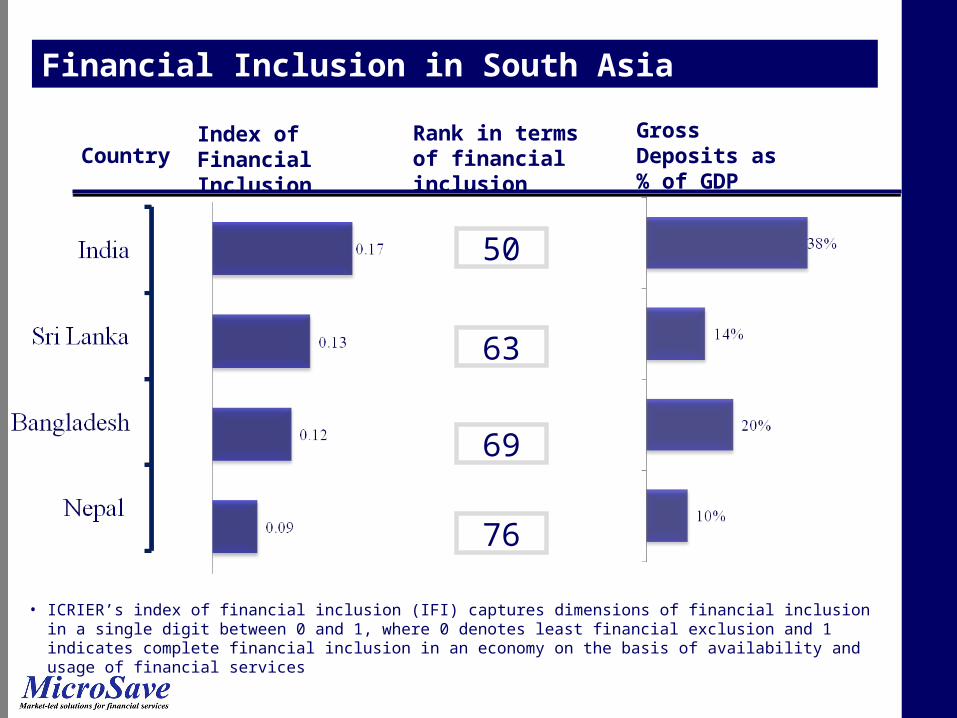

Financial Inclusion in South Asia

CountryIndex of Financial Inclusion

Rank in terms of financial inclusion

Gross Deposits as % of GDP

50

63

69

76

• ICRIER’s index of financial inclusion (IFI) captures dimensions of financial inclusion in a single digit between 0 and 1, where 0 denotes least financial exclusion and 1 indicates complete financial inclusion in an economy on the basis of availability and usage of financial services

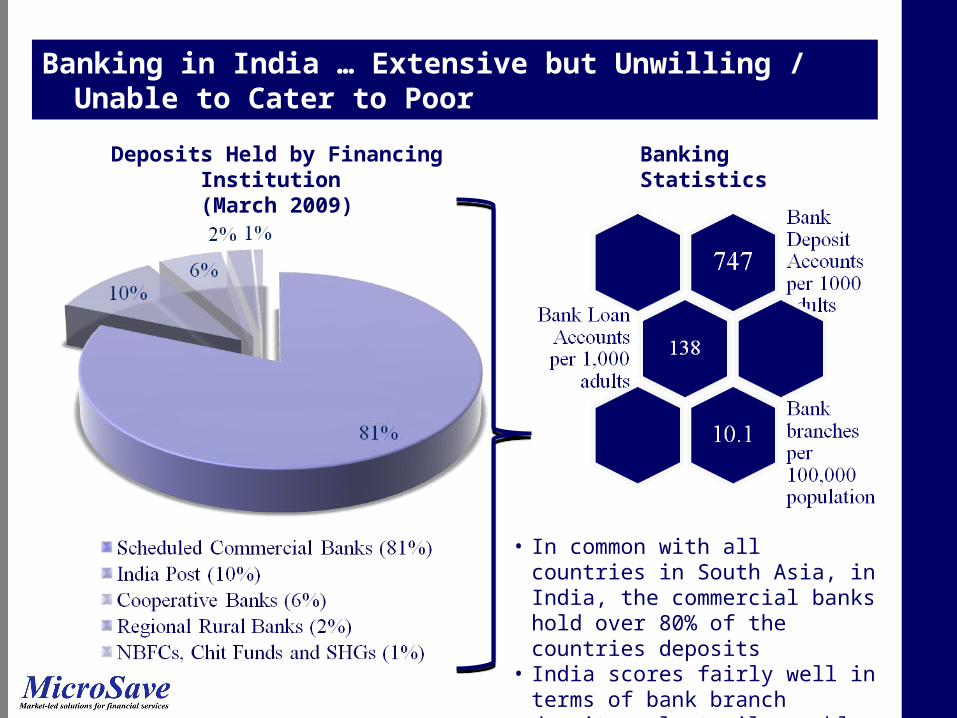

Banking in India … Extensive but Unwilling / Unable to Cater to Poor

Deposits Held by Financing Institution (March 2009)

Banking Statistics

• In common with all countries in South Asia, in India, the commercial banks hold over 80% of the countries deposits

• India scores fairly well in terms of bank branch density – last mile problem is solved but banks don’t perceive poor as worthy customer

PERCEPTION OF THE POOR: GLIMPSES FROM MARKET RESEARCH

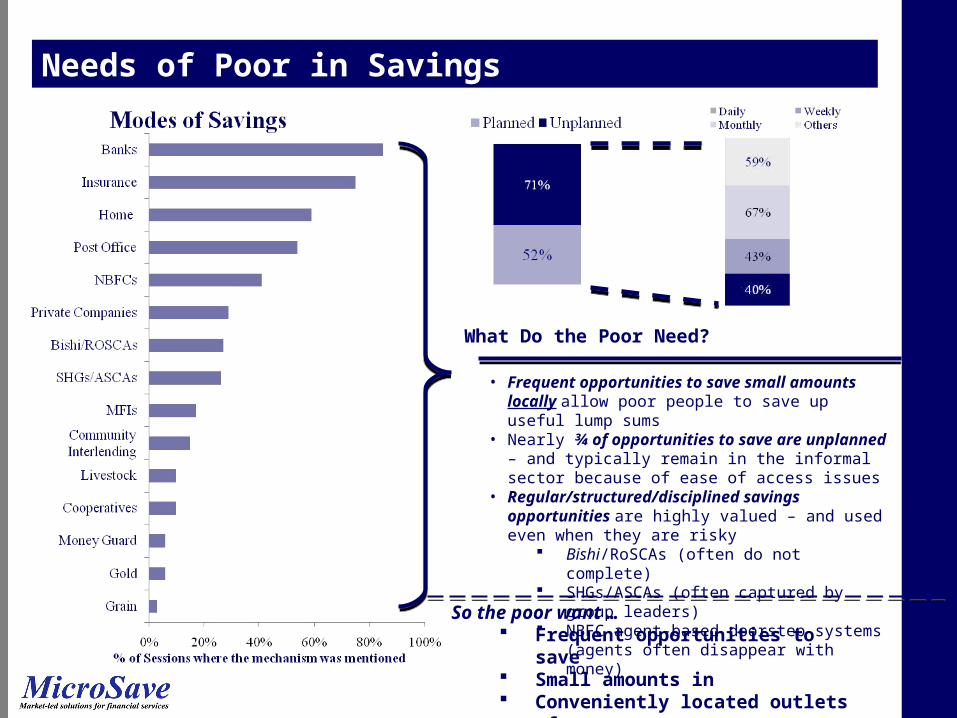

Needs of Poor in Savings

• Frequent opportunities to save small amounts locally allow poor people to save up useful lump sums

• Nearly ¾ of opportunities to save are unplanned – and typically remain in the informal sector because of ease of access issues

• Regular/structured/disciplined savings opportunities are highly valued – and used even when they are risky

Bishi/RoSCAs (often do not complete) SHGs/ASCAs (often captured by group leaders) NBFC agent-based doorstep systems (agents often

disappear with money)

So the poor want … Frequent opportunities to save Small amounts in Conveniently located outlets of Trustworthy/secure institutions

What Do the Poor Need?

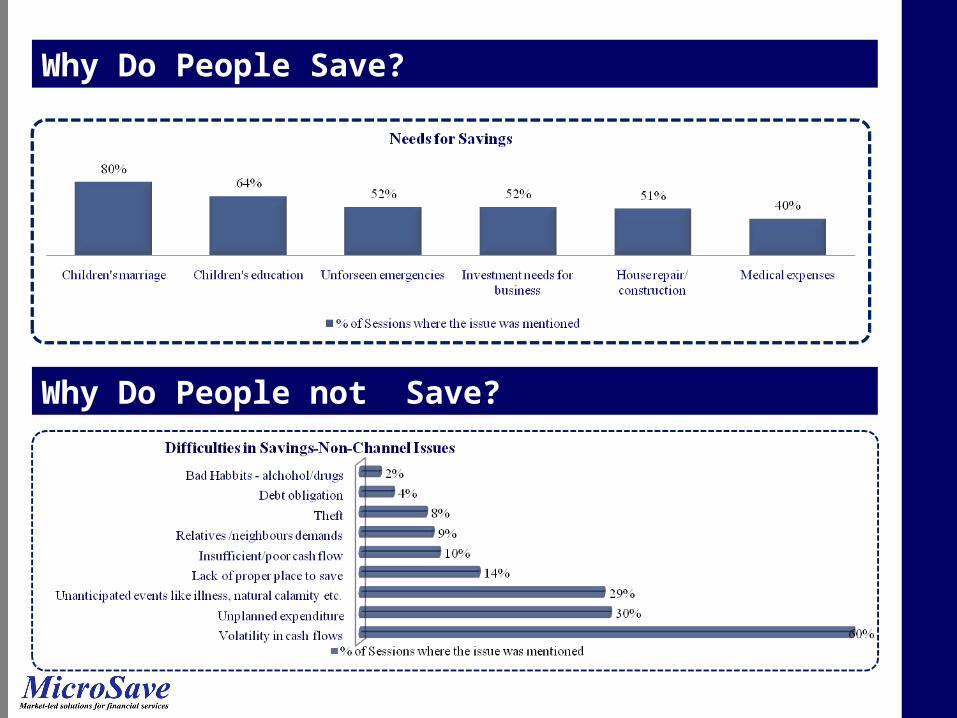

Why Do People Save?

Why Do People not Save?

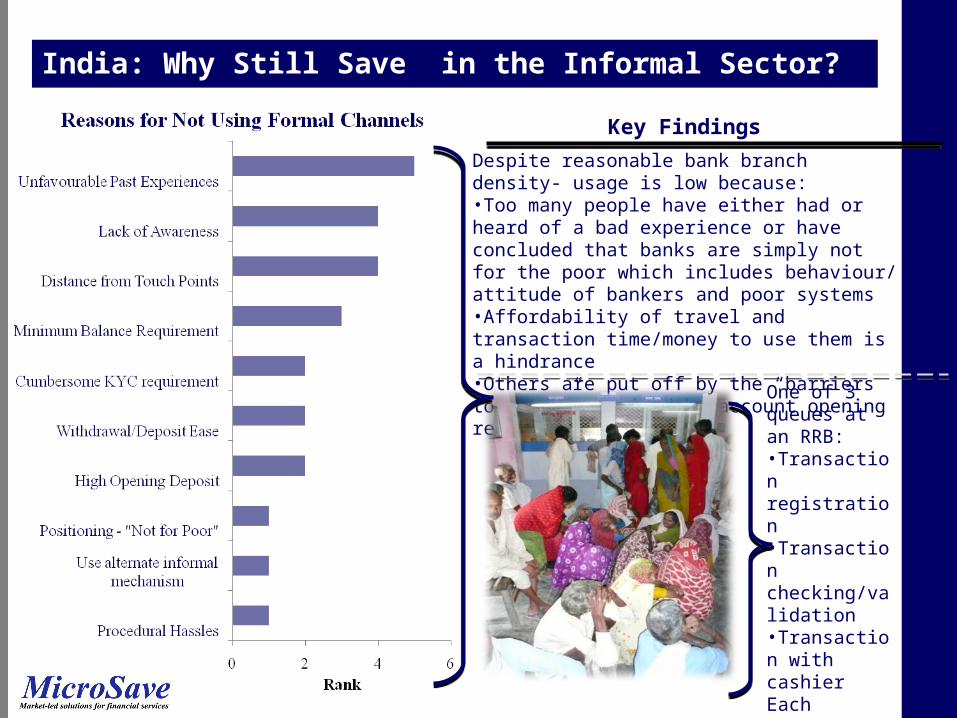

India: Why Still Save in the Informal Sector?

Despite reasonable bank branch density- usage is low because:•Too many people have either had or heard of a bad experience or have concluded that banks are simply not for the poor which includes behaviour/ attitude of bankers and poor systems•Affordability of travel and transaction time/money to use them is a hindrance•Others are put off by the “barriers to entry” provided by account opening requirements

One of 3 queues at an RRB:•Transaction registration•Transaction checking/validation•Transaction with cashierEach queue/process takes about 45 -60 minutes – total process: nearly 3 hours.

Key Findings

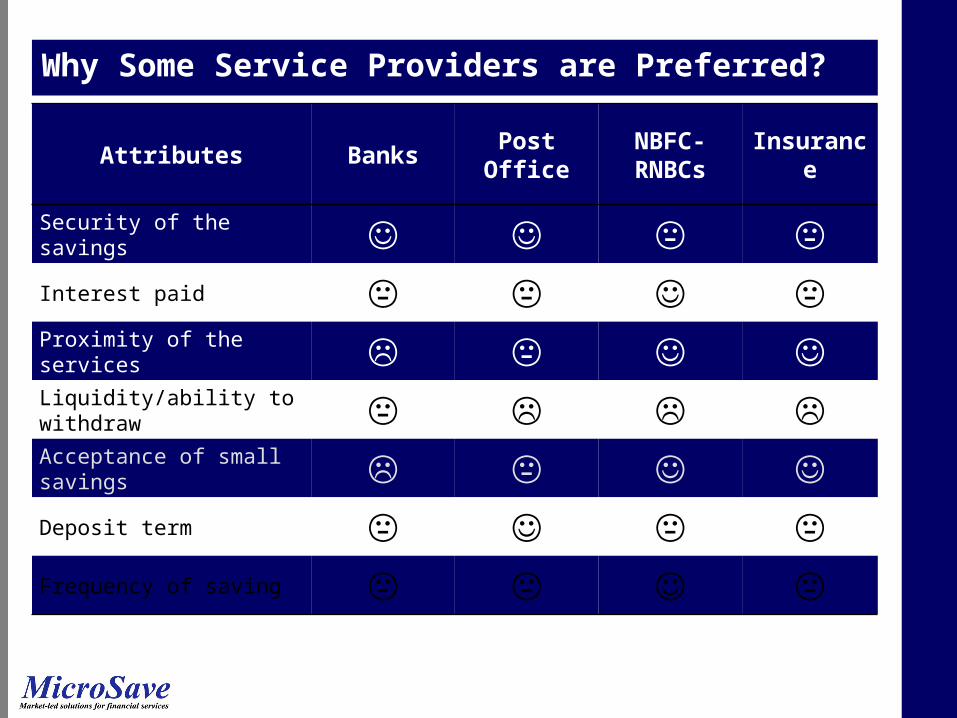

Why Some Service Providers are Preferred?

Attributes Banks Post OfficeNBFC-RNBCs

Insurance

Security of the savings Interest paid Proximity of the services Liquidity/ability to withdraw Acceptance of small savings Deposit term Frequency of saving

Preferred Attributes in Savings

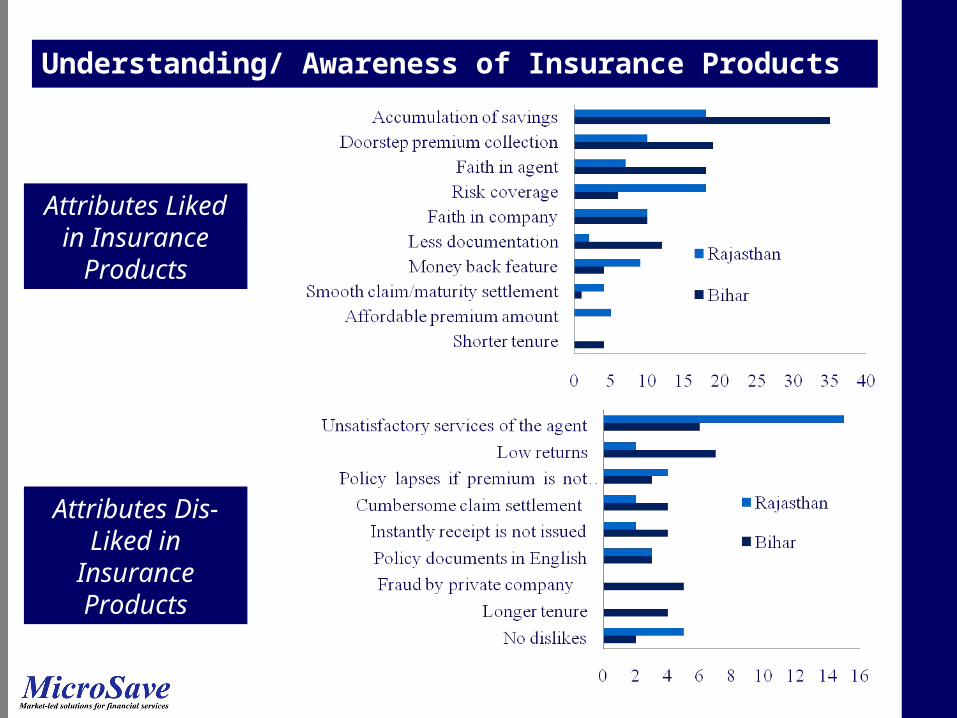

Understanding/ Awareness of Insurance Products

Attributes Liked in Insurance Products

Attributes Dis-Liked in Insurance

Products

ISSUES AND PROSPECT: BANK ACCOUNTS

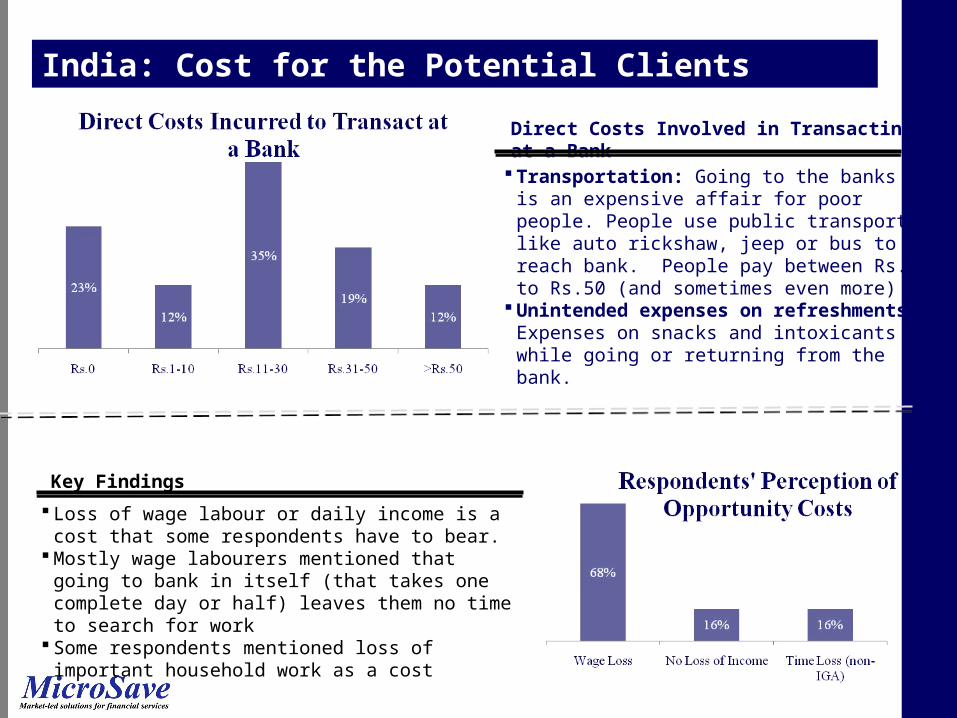

Transportation: Going to the banks is an expensive affair for poor people. People use public transport like auto rickshaw, jeep or bus to reach bank. People pay between Rs.1 to Rs.50 (and sometimes even more)

Unintended expenses on refreshments: Expenses on snacks and intoxicants while going or returning from the bank.

Direct Costs Involved in Transacting at a Bank

Loss of wage labour or daily income is a cost that some respondents have to bear.

Mostly wage labourers mentioned that going to bank in itself (that takes one complete day or half) leaves them no time to search for work

Some respondents mentioned loss of important household work as a cost

Key Findings

India: Cost for the Potential Clients

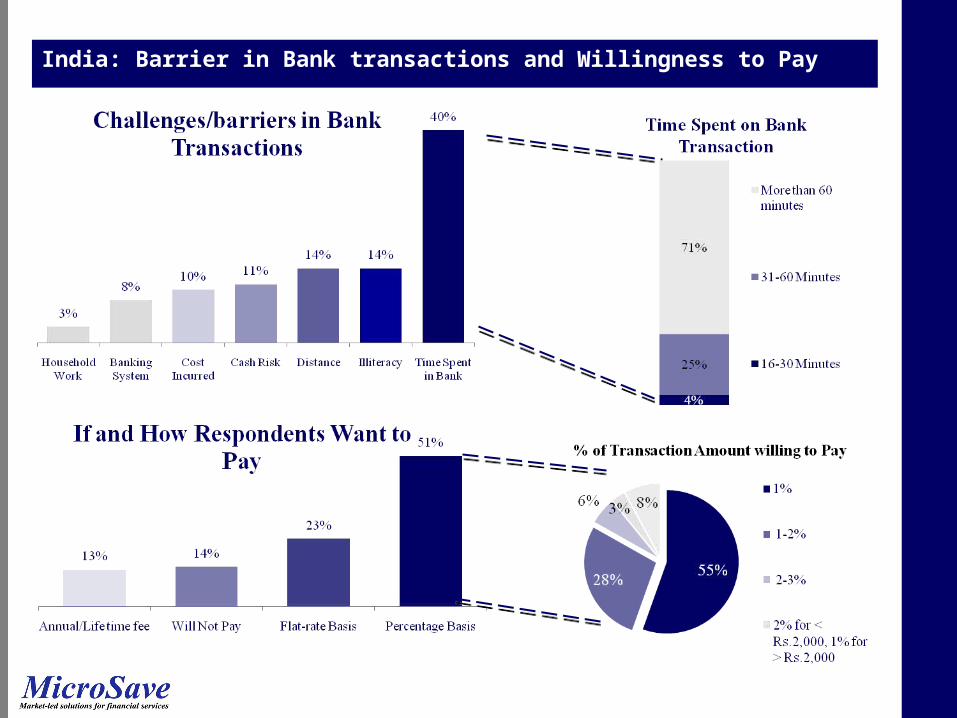

India: Barrier in Bank transactions and Willingness to Pay

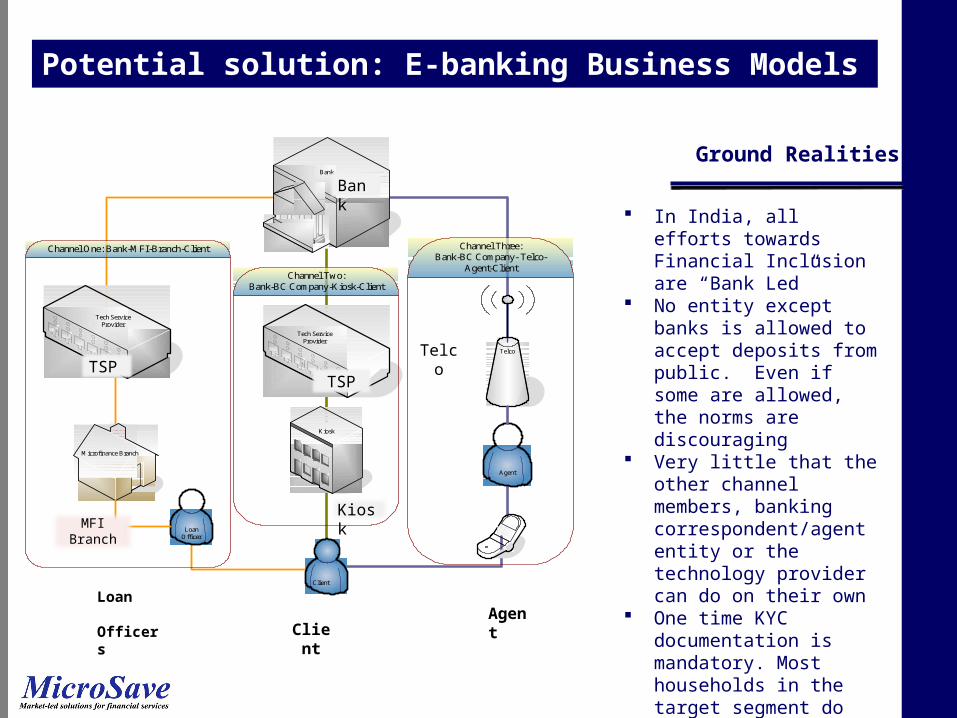

FINANCIAL INCLUSION TOOLS: AGENT BANKING AND M BANKING

Channel One: Bank-MFI-Branch-Client

Tech Service Provider

Microfinance Branch

LoanOfficer

Client

Kiosk

Channel Two: Bank-BC Company-Kiosk-Client

Tech Service Provider

Agent

Telco

Bank

Channel Three: Bank-BC Company- Telco-

Agent-Client

Bank

TSPTSP

MFI BranchKiosk

Telco

Client

Loan Officers Agent

Ground Realities

In India, all efforts towards Financial Inclusion are “Bank Led”

No entity except banks is allowed to accept deposits from public. Even if some are allowed, the norms are discouraging

Very little that the other channel members, banking correspondent/agent entity or the technology provider can do on their own

One time KYC documentation is mandatory. Most households in the target segment do not have the basic documents required

Logistics is a key challenge, especially managing the agent network and cash involved

Potential solution: E-banking Business Models

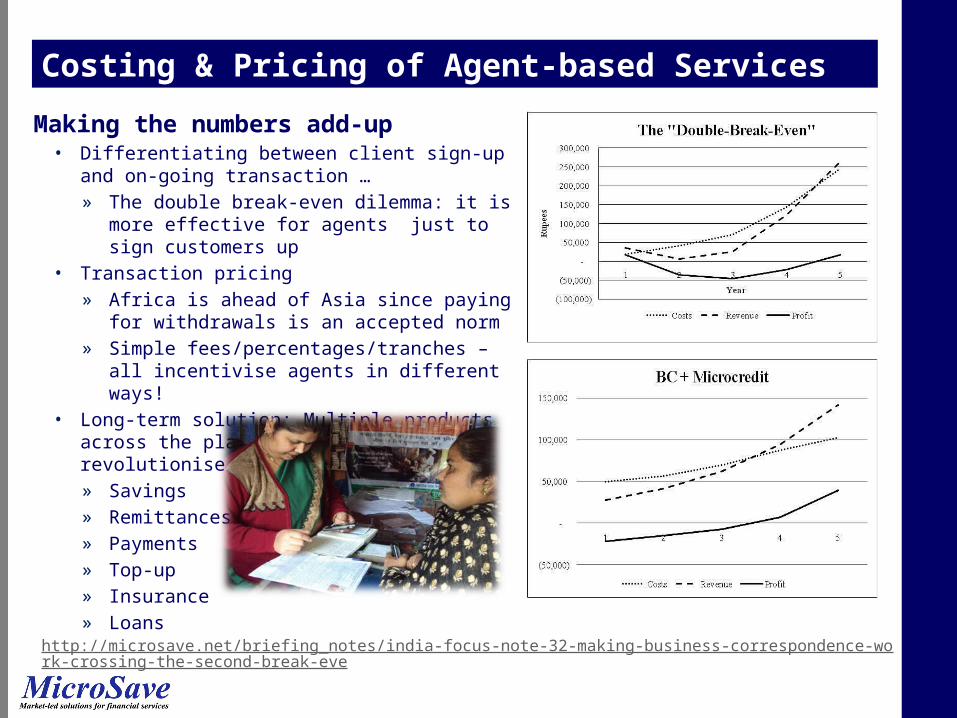

Making the numbers add-up• Differentiating between client sign-up and on-going

transaction … » The double break-even dilemma: it is more effective

for agents just to sign customers up• Transaction pricing

» Africa is ahead of Asia since paying for withdrawals is an accepted norm

» Simple fees/percentages/tranches – all incentivise agents in different ways!

• Long-term solution: Multiple products across the platform – will revolutionise microfinance» Savings» Remittances» Payments» Top-up» Insurance» Loans

http://microsave.net/briefing_notes/india-focus-note-32-making-business-correspondence-work-crossing-the-second-break-eve

Costing & Pricing of Agent-based Services

Key Take-Aways

• Poor people have rich and complicated financial lives• Managing the basics• Coping with risks• Raising lump sums

• Poor people use a wide variety of instruments to save • Each financial tool is linked to a specific need• Mostly informal in nature • Mostly subject to the risk of loss

• To design savings (and indeed other) services for the poor, we need to understand their needs, perceptions, aspirations and current financial behaviour

• Key drivers are (usually):• Trust/security• Proximity/convenience/access• Interest rates/returns • Liquidity/illiquidity preferences

• Get the products and delivery systems right … and the demand can be overwhelming

• The poor want … • Frequent opportunities to save • Small amounts at• Conveniently located outlets of• Trustworthy/secure institutions

• E-/M-banking solutions look like a high potential option but challenges remain• Driving adoption and usage• Developing and managing agent

networks• Costing and pricing

THANK YOU