Micro Ch 16

30

Chapter 16 The Economics of Information © 2015 Pearson Education, Inc.

-

Upload

mrbagzis -

Category

Economy & Finance

-

view

59 -

download

1

Transcript of Micro Ch 16

© 2015 Pearson Education, Inc.

Chapter 16 The Economics of Information

© 2015 Pearson Education, Inc.

16 The Economics of Information

Chapter Outline

16.1 Asymmetric Information16.2 Hidden Actions: Markets with Moral Hazard16.3 Government Policy in a World of Asymmetric Information

© 2015 Pearson Education, Inc.

16 The Economics of Information

Key Ideas

1. In many markets buyers and sellers have different information, which can lead to market inefficiencies.

2. Asymmetry in information is either due to hidden characteristics or hidden actions.

© 2015 Pearson Education, Inc.

16 The Economics of Information

Key Ideas

3. In cases with hidden characteristics, agents can use their private information to decide whether to participate in a transaction or a market, causing adverse selection.4. In cases with hidden actions, an agent can take an action that adversely affects another agent, causing moral hazard.

© 2015 Pearson Education, Inc.

16 The Economics of Information

Key Ideas

5. There are both private and government solutions to reduce the effects of adverse selection and moral hazard.

© 2015 Pearson Education, Inc.

16 The Economics of Information

Evidence-Based Economics Example:

Why do new cars lose considerable value the minute they are driven off the lot?

© 2015 Pearson Education, Inc.

16.1 Asymmetric Information

Asymmetric information

Information available to buyers and sellers differs

Hidden characteristicsOne side observes something about the good

being transacted that is both relevant for and not observed by the other party

© 2015 Pearson Education, Inc.

16.1 Asymmetric Information

Hidden actions

One side takes actions that are relevant for, but not observed by, the other party

© 2015 Pearson Education, Inc.

16.1 Asymmetric InformationHidden Characteristics: Adverse Selection in the Used Car

Market

Peach or lemon?

© 2015 Pearson Education, Inc.

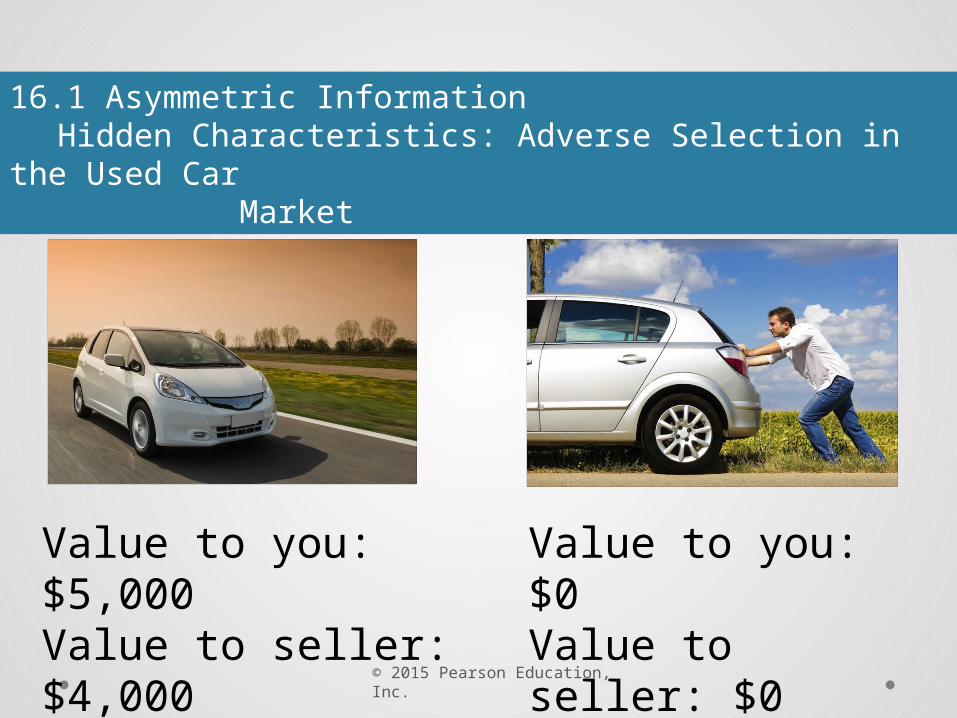

16.1 Asymmetric InformationHidden Characteristics: Adverse Selection in the Used Car

Market

Value to you: $5,000Value to seller: $4,000

Value to you: $0Value to seller: $0

© 2015 Pearson Education, Inc.

16.1 Asymmetric InformationHidden Characteristics: Adverse Selection in the Used Car

Market

For any given car, how much would you be willing to offer?

© 2015 Pearson Education, Inc.

16.1 Asymmetric InformationHidden Characteristics: Adverse Selection in the Used Car

Market

Expected value = .5($5,000) + .5($0) = $2,500

If you offer $2,500 to the seller, would he/she accept the offer?

© 2015 Pearson Education, Inc.

16.1 Asymmetric InformationHidden Characteristics: Adverse Selection in the Used Car

Market

Adverse selection

One agent in a transaction knows about a hidden characteristic of a good and decides whether to participate in the transaction on the basis of this information

© 2015 Pearson Education, Inc.

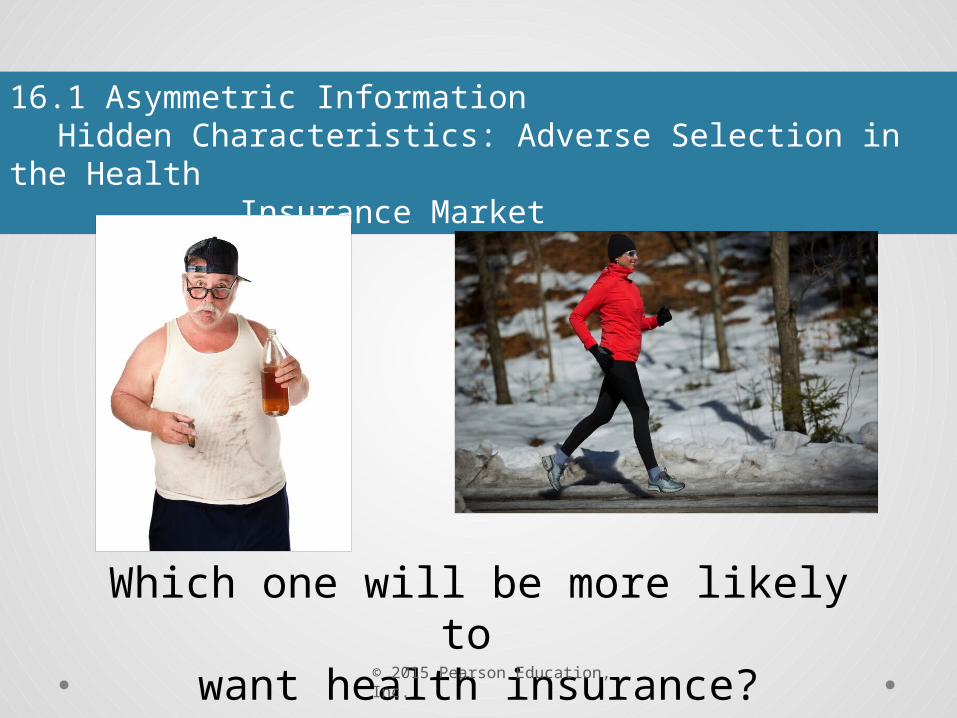

16.1 Asymmetric InformationHidden Characteristics: Adverse Selection in the Health

Insurance Market

Which one will be more likely to want health insurance?

© 2015 Pearson Education, Inc.

16.1 Asymmetric InformationMarket Solutions to Adverse Selection: Signaling

Signaling

An action that an individual with private information takes in order to convince others about his information

© 2015 Pearson Education, Inc.

16.1 Asymmetric Information

Evidence-Based Economics Example:

Why do new cars lose considerable value the minute they are driven off the lot?

© 2015 Pearson Education, Inc.

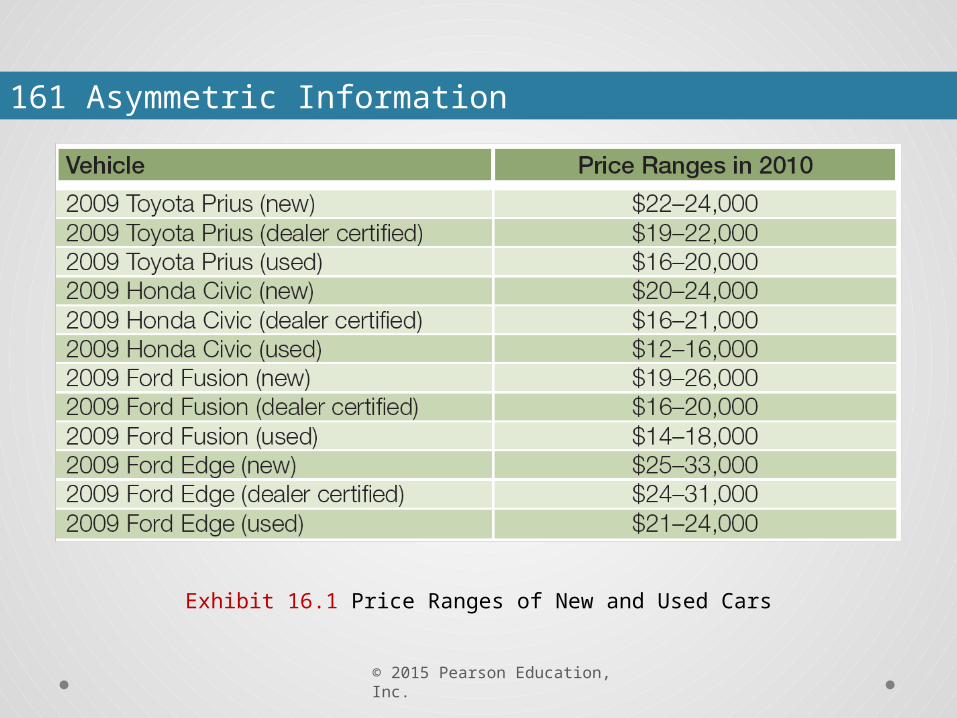

161 Asymmetric Information

Exhibit 16.1 Price Ranges of New and Used Cars

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral Hazard

Moral hazard

Actions that are taken by one party but are relevant for and not observed by the other party in the transaction

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral Hazard

People with air bags in their cars are more likely to get into accidents.

Why? Two explanations1. Adverse selection—if you know that you are a

bad driver, you are more likely to choose a car that has air bags.

2. Moral hazard—if you are protected from some of the risk of driving, you are more likely to drive recklessly.

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral Hazard

Principal-agent relationship

The principal designs a contract specifying the payments to the agent as a function of his or her performance, and the agent takes an action that influences performance and thus the payoff of the principal

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral Hazard

In other words, one party (the principal) provides incentives for another party (the agent) to work to the principal’s benefit.

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral Hazard

“There’s no ‘I’ in ‘team’”

Who is he playing for?

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral HazardMarket Solutions to Moral Hazard in the Labor Market:

Efficiency Wages

What would make this agent wake up?

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral HazardMarket Solutions to Moral Hazard in the Labor Market:

Efficiency Wages

Efficiency wages

Wages above the lowest pay that workers would accept; employers use them to increase motivation and productivity

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral HazardMarket Solutions to Moral Hazard in the Insurance Market:

“Putting Your Skin in the Game”

1. Deductibles

2. Co-payments

3. Coinsurance

© 2015 Pearson Education, Inc.

16.2 Hidden Actions: Markets with Moral HazardMarket Solutions to Moral Hazard in the Insurance Market:

“Putting Your Skin in the Game”

Evidenced-Based Economics Example:

Why is private health insurance so expensive?

© 2015 Pearson Education, Inc.

16.3 Government Policy in a World of Asymmetric Information

© 2015 Pearson Education, Inc.

16.3 Government Policy in a World of Asymmetric InformationGovernment Intervention and Moral Hazard

The ACA (Affordable Care Act) could lead to a moral hazard problem as risk behavior increases because of insurance coverage. In response, the government could

• Tax risky behavior• Subsidize healthy behavior• Have deductibles or copayments

© 2015 Pearson Education, Inc.

16.3 Government Policy in a World of Asymmetric InformationThe Equity-Efficiency Trade-off

How do unemployment benefits create a moral hazard problem?

© 2015 Pearson Education, Inc.

16.3 Government Policy in a World of Asymmetric InformationCrime and Punishment as a Principal-Agent Problem

Is this a principal-agent problem?