Michigan’s Capital Outlay ProcessMichigan’s . Capital Outlay Process. Prepared by . Ben Gielczyk...

42

7 Michigan’s Capital Outlay Process Prepared by Ben Gielczyk Senior Fiscal Analyst Mary Ann Cleary, Director February 2015

Transcript of Michigan’s Capital Outlay ProcessMichigan’s . Capital Outlay Process. Prepared by . Ben Gielczyk...

7

Michigan’s

Capital Outlay Process

Prepared by

Ben Gielczyk Senior Fiscal Analyst

Mary Ann Cleary, Director February 2015

HOUSE FISCAL AGENCY GOVERNING COMMITTEE

Al Pscholka Harvey Santana Kevin Cotter Tim Greimel Aric Nesbitt Sam Singh

MICHIGAN HOUSE OF REPRESENTATIVES APPROPRIATIONS COMMITTEE

Al Pscholka, Chair Phil Potvin

Chris Afendoulis Rob VerHeulen

John Bizon Roger Victory

Jon Bumstead, Vice Chair Harvey Santana, Minority Vice Chair

Edward Canfield Brian Banks

Laura Cox Brandon Dillon

Cindy Gamrat Fred Durhal

Larry Inman Jon Hoadley

Nancy Jenkins Jeff Irwin

Tim Kelly Kristy Pagan

Michael McCready Sarah Roberts

Aaron Miller Sam Singh

Paul Muxlow Henry Yanez

Dave Pagel Adam Zemke

Earl Poleski

STATE OF MICHIGAN HOUSE OF REPRESENTATIVES

HOUSE FISCAL AGENCY

MARY ANN CLEARY, DIRECTOR

P.O. BOX 30014 LANSING, MICHIGAN 48909-7514

PHONE: (517) 373-8080 FAX: (517) 373-5874 www.house.mi.gov/hfa

GOVERNING COMMITTEE

AL PSCHOLKA, CHAIR KEVIN COTTER, VC

ARIC NESBITT HARVEY SANTANA, MVC

TIM GREIMEL SAM SINGH

February 2015 TO: Members of the House of Representatives Michigan’s public universities and community colleges requesting state financial support for a building project must follow exacting procedures and standards. This publication will define and summarize the Michigan capital outlay process for those projects requiring State Building Authority financing, describe the responsibilities and functions of the Joint Capital Outlay Subcommittee, and explain the process used by the State Building Authority to finance capital outlay projects. The Appendix to this report provides a detailed listing of all major (over $1 million) projects authorized and appropriated for by the Legislature since FY 1992-93. Very little state building activity was accomplished prior to FY 1992-93 due to severe budgetary constraints. Hence, FY 1992-93 is considered the beginning of the state’s building boom. Ben Gielczyk, Senior Fiscal Analyst, is the author of this report. Please do not hesitate to call if you have questions or comments. Mary Ann Cleary Director

TABLE OF CONTENTS

INTRODUCTION ........................................................................................................................ 1 PROCESS .................................................................................................................................. 3 Five-Year Master Plans ................................................................................................... 3 Review for Planning Authorization ................................................................................... 3 Planning Costs ................................................................................................................ 5 Review of Submitted Planning Documents ...................................................................... 7 Authorization Enactments and Final Design/Bids ............................................................ 7 Project Management ....................................................................................................... 8 JOINT CAPITAL OUTLAY SUBCOMMITTEE (JCOS) ............................................................... 9 PROJECT FINANCING ............................................................................................................ 11 CONCLUSION .......................................................................................................................... 15 APPENDIX Department of Corrections Projects ............................................................................... 19 Other State Agency Projects ......................................................................................... 20 University Projects ......................................................................................................... 21 Community College Projects ......................................................................................... 27

FIGURES Figure 1 Michigan Capital Outlay Process ......................................................................... 6 Figure 2 SBA Financing Process ..................................................................................... 12 Figure 3 SBA Rent GF/GP Appropriations ....................................................................... 13

TABLES Table 1 History of Capital Outlay Planning Authorization Legislation ................................ 7 Table 2 State Building Authority (SBA) Bond Limits ........................................................ 13

INTRODUCTION

The Michigan capital outlay process is defined as:

The budgetary and administrative functions devoted to planning and financing for the acquisition, construction, renovation, remodeling, repair, and maintenance of facilities used by state agencies, State-supported public universities, or State-supported community colleges.

The purpose of this document is to define and summarize the Michigan capital outlay process for those projects requiring State Building Authority (SBA) financing, describe the responsibilities and functions of the (legislative) Joint Capital Outlay Subcommittee (JCOS), and explain how the SBA finances state building projects. This document does not include highway and bridge construction projects, which are covered by other administrative and legislative procedures. Additionally, appropriations for capital outlay projects and special maintenance that are supported with federal, state restricted, and general funds are generally included in the annual budgets for state departments (Agriculture; Corrections; Education; Licensing and Regulatory Affairs; Military and Veterans Affairs; Natural Resources; Technology, Management, and Budget; and Transportation) and will not be discussed at length in this document. General operational practices and procedures for capital outlay are contained in the following: Management and Budget Act (1984 PA 431)

State Building Authority Act (1964 PA 183)

Annual appropriation acts including capital outlay projects

General Government appropriations act

Formal policies of JCOS

Public Act 431 of 1984 establishes the administrative framework for all state government functions, including the capital outlay process. It also establishes the specific oversight roles of the Department of Technology, Management, and Budget (DTMB) and JCOS. The capital outlay process has been in a continual state of refinement over the past 40 years, both administratively and statutorily. In 2012, the Legislature enacted 2012 PA 430 and 2012 PA 519 which made substantial revisions to streamline and standardize the process for capital outlay projects and state leases of private property. This legislation envisioned a capital outlay process that was competitive and used objective evaluation of the project requests. Major revisions to the SBA-financed capital outlay process included the following: A reduction, from three to two, in the number of legislative actions required for state-funded

capital outlay projects by requiring SBA financing to be approved in an appropriation bill at the same time as the construction authorization instead of in a separate and subsequent concurrent resolution.

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 1

Requiring biannual self-funded university and community college project reporting for projects

over $1.0 million. A revised construction contract award requirement to the “responsive and responsible best

value bidder.” Revised five-year master plan requirements to include electronic submission and submission to

JCOS. Requiring DTMB and JCOS Chair and Vice Chair to review, evaluate, and score capital outlay

project requests by March 1 of each year and specified 10 factors that must be considered in scoring process (explained in more detail later in the document).

Requiring cost and scope changes to be established or revised through specific reference in

appropriation acts. Revised planning and construction authorization time frames: a planning authorization would

last for 24 months beyond the last day of the fiscal year in which the planning authorization was made and a construction authorization would last for 36 months following the last day of the fiscal year in which the authorization was made.

Since 1964 PA 183, there have been 344 SBA-financed projects authorized by law: 95 for community colleges, 137 for universities, and 112 for state agencies. The total SBA (State) share for these projects has exceeded $5.6 billion. The appendix to this report provides a detailed listing of all SBA-financed projects authorized and appropriated for by the Legislature since FY 1992-93. Very little building activity was accomplished prior to FY 1992-93 due to budgetary constraints. Beginning in FY 1992-93, there was a significant increase in SBA-financed capital outlay projects. The following terms and abbreviations are used throughout this publication: DTMB — Department of Technology, Management, and Budget

HFA — House Fiscal Agency

JCOS — Joint Capital Outlay Subcommittee

SBA — State Building Authority

SFA — Senate Fiscal Agency

Planning Authorization — Allows an agency/institution to professionally develop initial project

planning documents (Phase 200/300 Program Statement/Schematic Design) to determine project scope/costs. Also referred to as a “placeholder,” it is accomplished by a $100 GF/GP appropriation in a budget bill. Approval of a planning authorization does not guarantee construction authorization.

Construction Authorization — Final legislative action to allow a project to move to final design

and construction. The project’s scope, total authorized cost, and sources of financing are also established in this action. Appropriation of the estimated first-year SBA rent payment, conveyance of property to SBA, and legislative lease approval are also included in this step.

THE CAPITAL OUTLAY PROCESS PAGE 2 HOUSE FISCAL AGENCY: FEBRUARY 2015

PROCESS

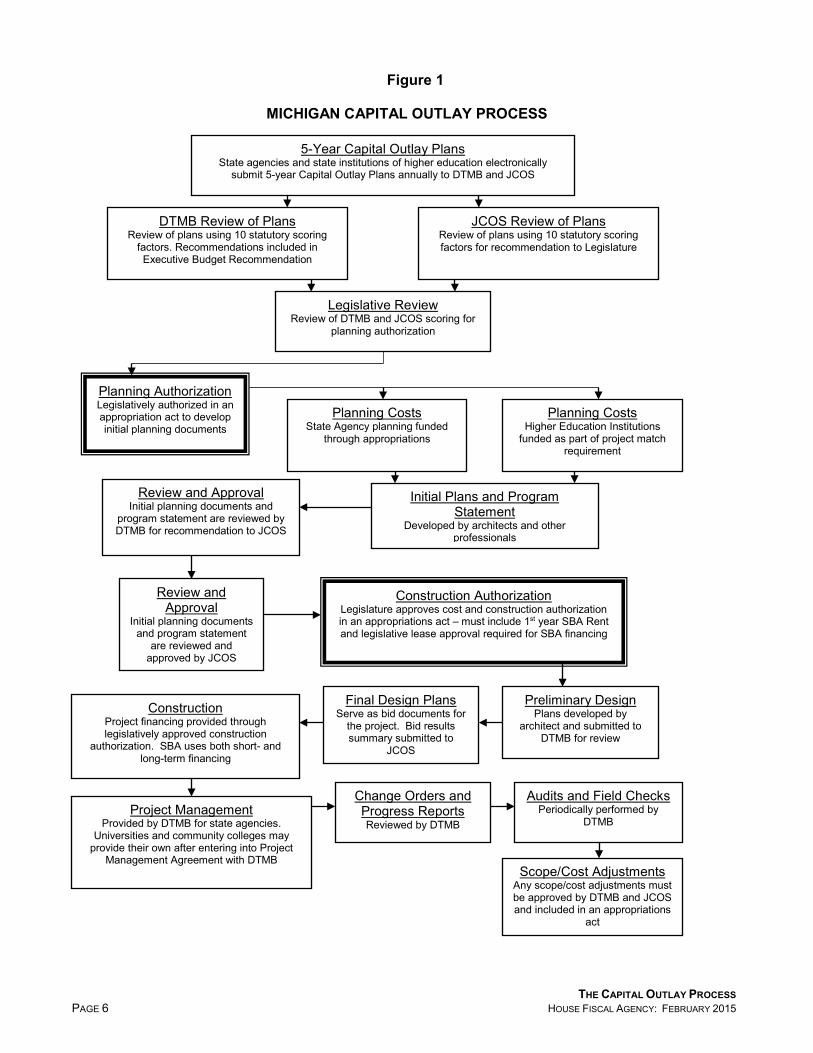

Practical application of the capital outlay process tends to be complex and highly technical, and is sometimes viewed as inconsistent due to variances of the appropriations process. However, the various reviews and approvals which are part of the process serve as checks and balances for state policymakers, enabling them to better understand all aspects of a project (e.g., need, purpose, scope, and cost) before an authorization is finalized. Thus, the capital outlay process helps ensure that public monies are spent on functional and necessary facilities. The following are summaries of the steps a successful project must complete. Figure 1 (page 6) provides a process flow chart of the steps described below:

Five-Year Master Plans Under Section 242 of 431 PA 1984 (MCL 18.1242), state agencies, universities, and community colleges must submit, in electronic format, rolling five-year capital outlay plans to DTMB, JCOS, HFA, and SFA for review not later than November 1 of each year. Each plan must include prioritized state-funded project requests and special maintenance needs, as well as an inventory of current facilities with a professional assessment of their respective conditions in light of current programming efforts and anticipated programming changes. The plan shall include both self-funded projects as well as future projects for which state cost sharing may be requested. According to DTMB budget instruction letters submitted to universities and community colleges, the following represent the required plan components: A description of the overall mission of the institution. A listing and description of the current academic programs and major academic initiatives. An account of staffing and enrollment trends. A professionally developed facilities assessment that identifies and evaluates the overall

condition, age, and use pattern of capital facilities under the institutions control. A schedule for addressing capital deficiencies at the institution.

State agency five-year master plans incorporate analogous requirements with modifications to accommodate state agency characteristics. Review for Planning Authorization Under Section 242 of 1984 PA 431, DTMB and JCOS are required to review, evaluate, and prioritize requests for state-funded projects by March 1 of each year. As part of the 2012 capital outlay process reforms, Section 242 requires that the following items be considered when reviewing and evaluating the state-funded priority project requests (items are not listed in order of importance)1:

1 FY 2014-15 State Budget Office state-funded priority project rankings can be found at http://www.michigan.gov/documents/budget/G_446686_7.pdf.

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 3

Investment in existing facilities and infrastructure Life and safety deficiencies Occupancy and utilization of existing facilities Integration of sustainable design Estimated cost Institutional support Estimated operating costs Impact on tuition Impact on job creation in this state History of prior appropriations received by the institution through the capital outlay process

DTMB and JCOS may include additional factors if either deem them necessary to the evaluation and scoring process. For example, DTMB included the following three criteria for the FY 2014-15 project requests: Impact on core mission of the institution; Focus of project on single, stand-alone facility; and History of compliance with JCOS and DTMB project requirements.

While statute doesn’t designate an order, in practice DTMB reviews, evaluates, and scores priority projects prior to JCOS due to the earlier release of the Executive Budget Recommendation. Once DTMB has reviewed, evaluated, and scored the requests, DTMB includes any recommended requests in the Executive Budget Recommendation. JCOS is also required to review, evaluate, and score the submitted priority projects. Due to the timing of the Executive Budget Recommendation, the JCOS review would likely include an examination of the DTMB priority project scoring. An affirmative vote by JCOS is required for a project to receive consideration for planning authorization in an appropriation bill before the full Legislature. Once the Legislature has reviewed DTMB and JCOS scoring evaluations, the Legislature determines which projects should receive consideration for planning authorization in an appropriation bill. Agency/institution priority projects selected for planning authorization by the Legislature shall appear as $100 line item appropriations in an enacted appropriation bill.2 The planning authorization line item in the appropriation act delineates the intended total project cost, the financing share to be borne by the state, and the financing share to be borne by the institution.

2 Prior to the 2012 Capital Outlay Reforms, state agency projects commonly skipped the planning authorization and went straight to construction authorization.

THE CAPITAL OUTLAY PROCESS PAGE 4 HOUSE FISCAL AGENCY: FEBRUARY 2015

An agency/institution granted a project planning authorization in an appropriation act has 24 months following the last day of the fiscal year in which the planning authorization was approved to receive authorization for final design and construction. Planning Costs Planning costs include architects and other professionals to develop the initial program and schematic planning documents required for submission prior to receiving construction authorization. The purpose of these documents is to develop details of the purpose, scope, and size of the project with reliable cost estimates. While planning costs for authorized state agency projects are provided through appropriations acts, institutions of higher education must fund planning costs as part of their project match requirement. Planning costs are considered an allowable cost if the project receives construction authorization. Prior to the legislatively authorized construction authorization, the institution of higher education assumes the risk of planning costs since a planning authorization provides no guarantee of construction authorization. The standard match rate for an SBA-financed project is 50% from community college funds and 25% from university funds. Recently, a maximum State share of $30.0 million has been implemented which requires higher community college and university match rates for larger projects. Community colleges are required to contribute a higher match rate due to their ability to levy local millages to support college operations.

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 5

Figure 1

MICHIGAN CAPITAL OUTLAY PROCESS

5-Year Capital Outlay Plans

State agencies and state institutions of higher education electronically submit 5-year Capital Outlay Plans annually to DTMB and JCOS

DTMB Review of Plans Review of plans using 10 statutory scoring

factors. Recommendations included in Executive Budget Recommendation

JCOS Review of Plans Review of plans using 10 statutory scoring factors for recommendation to Legislature

Legislative Review Review of DTMB and JCOS scoring for

planning authorization

Planning Authorization Legislatively authorized in an appropriation act to develop initial planning documents

Planning Costs State Agency planning funded

through appropriations

Planning Costs Higher Education Institutions

funded as part of project match requirement

Initial Plans and Program Statement

Developed by architects and other professionals

Review and Approval Initial planning documents and

program statement are reviewed by DTMB for recommendation to JCOS

Review and Approval

Initial planning documents and program statement

are reviewed and approved by JCOS

Construction Authorization Legislature approves cost and construction authorization in an appropriations act – must include 1st year SBA Rent and legislative lease approval required for SBA financing

Preliminary Design Plans developed by

architect and submitted to DTMB for review

Final Design Plans Serve as bid documents for

the project. Bid results summary submitted to

JCOS

Construction Project financing provided through legislatively approved construction

authorization. SBA uses both short- and long-term financing

Project Management Provided by DTMB for state agencies.

Universities and community colleges may provide their own after entering into Project

Management Agreement with DTMB

Change Orders and Progress Reports Reviewed by DTMB

Audits and Field Checks Periodically performed by

DTMB

Scope/Cost Adjustments Any scope/cost adjustments must be approved by DTMB and JCOS and included in an appropriations

act

THE CAPITAL OUTLAY PROCESS PAGE 6 HOUSE FISCAL AGENCY: FEBRUARY 2015

It is important to note that a planning authorization does not guarantee that a project will receive construction authorization. After review of the initial planning documents, the project may not be advanced if the Legislature deems the project without merit or too costly. However, it is very rare for a project to receive planning authorization and not receive construction authorization. Table 1 provides a 10-year history of capital outlay legislation that included new planning authorizations.

Table 1 History of Capital Outlay Planning Authorization Legislation

FY 2004-05 to FY 2013-14

Capital Outlay Legislation # of Planning Authorizations State Share PA 10 of 2005 22 $198.3 million PA 278 of 2008 16 $216.1 million PA 329 of 2010 20 $311.3 million PA 102 of 2013 6* $ 24.7 million*

*Includes $100,000 planning grant for the Marshall State Police Post (state agency project) Review of Submitted Planning Documents When the planning authorization documents (program statement and schematic planning documents) are completed, they are submitted to DTMB for review and analysis. Adjustments recommended by DTMB staff may occur at this point. These may include scope reductions in order to bring the project cost down or scope alterations to fit administration priorities. After the planning authorization documents are deemed acceptable to DTMB, DTMB makes a recommendation to JCOS for review and approval. If JCOS agrees that the project has merit through an affirmative vote, the documents will be approved and a construction authorization must be included in an appropriation bill. Similar to planning authorizations, construction authorizations appear as $100 line item appropriations in an enacted appropriation bill. The construction authorization delineates the total project cost, the financing share to be borne by the state, and the financing share to be borne by the institution. In addition to the construction authorization, the 2012 reforms require the appropriation bill to include an appropriation for annual projected SBA rent payments associated with the projects authorized for construction, the conveyance to SBA, and the legislative lease approval required for SBA financing. By combining the construction authorization and the SBA financing, conveyance, and lease approval in one step, the capital outlay process shifted from a three-step to a two-step legislative process. Subsequent to receiving construction authorization, any scope and/or cost adjustments requested by the state agency or institution of higher education must be submitted for approval to DTMB. Upon approval, DTMB submits a letter to JCOS recommending approval. If JCOS agrees that the scope and/or cost change is warranted through an affirmative vote, the scope and/or cost change must be included in an appropriation bill. Authorization Enactments and Final Design/Bids Enactment of a construction authorization allows a project to move to the preliminary planning phase. Preliminary plans are developed by an architect and are more detailed than the schematic plans submitted after receiving a planning authorization. Once the preliminary plan is complete, it is submitted to DTMB for review and approval. If DTMB determines that the project still complies with the legislatively-authorized purpose, scope, and cost, the project moves to final design. Final

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 7

design plans, often referred to as bid documents, are used by construction contractors to submit bids on the project. Construction bids may be managed by universities and community colleges for their respective projects. DTMB manages construction bids for state agency projects. In all cases, bid results are submitted to both DTMB and JCOS. Project Management Universities and community colleges may elect to take responsibility for project management of their respective projects. DTMB handles project management for state agency projects. If a university or community college does not have the internal capability to manage its own construction project, it may contract with a private vendor or with DTMB. As a means of ensuring state oversight, DTMB may require universities and community colleges self-managing a construction project to enter into an agreement with DTMB in which the university or community college agrees to construct the project within the authorized cost, design, and scope as established by the Legislature. DTMB retains the authority and fiduciary responsibility to maintain the public’s financial and policy interests relative to the state-financed project. If the public’s financial and policy interests are in jeopardy and there is a failure on the part of the university or community college to adhere to the requirements of Public Act 431 of 1984, the director of DTMB may take appropriate action to bring the capital outlay project to conclusion. Public Act 431 of 1984 requires that all contract change orders and monthly progress reports be submitted to DTMB on any project not managed directly by DTMB. Also, DTMB is empowered to conduct periodic field checks and audits on all projects.

Up to the start of construction, all planning costs are funded either through the planning appropriation in the case of state agency projects or by the university or community college managing the project. Universities and community colleges are required to spend their portion of the project cost before any state funds are released. Once construction begins, project financing is provided by SBA through the legislatively-approved construction authorization. Initially, short-term commercial paper financing is used. Once enough projects can be grouped together, SBA sells long-term bonds. More information about project financing is available later in this report.

THE CAPITAL OUTLAY PROCESS PAGE 8 HOUSE FISCAL AGENCY: FEBRUARY 2015

JCOS

Direct, ongoing legislative participation and oversight in the capital outlay process are provided through JCOS of the House and Senate Appropriations Committees. JCOS is the only subcommittee that has specific duties and responsibilities defined by statute (1984 PA 431), some of which have already been mentioned. Fourteen members (seven from each chamber), appointed by the chairperson of each respective appropriations committee, constitute JCOS. The chairperson of JCOS alternates between chambers on two-year terms, with a member from the other chamber serving as vice chair. JCOS meets throughout the year to review and approve various capital outlay documents, lease agreements, and other issues, as required by law. Although it is designated as an appropriations subcommittee, JCOS functions more like a regular standing committee due to the size of the committee and the nature of its business. A quorum consists of eight members with each chamber represented by at least four members. Approval of an agenda item requires an affirmative vote of a majority of the members serving (eight affirmative votes). A formal policy of the 2013-2014 subcommittee requires a two-week notice for agenda items proposed by DTMB, a state agency, or an institution of higher education, to JCOS, HFA, and SFA. However, this rule can be waived by the JCOS chairperson. JCOS has the following special duties and responsibilities: Adopt formal subcommittee policies and procedures

Prioritize future state agency, university, and community college building projects

Provide planning authorization for a project through an appropriations act

Approve/disapprove project program statements and schematic planning documents

Provide construction authorization and establish a project’s total authorized cost and financing

sources and convey property to the SBA and approve leases for bonded facilities among the SBA, the state, and user agencies through an appropriations act

Approve/disapprove state agency leases of non-state-owned spaces in which the base cost exceeds $500,000 per year

Review and approve Michigan Natural Resources Trust Fund (MNRTF) projects JCOS deliberates and acts upon numerous policy issues regarding the capital outlay process and capital outlay projects. Some of these issues are the sole discretion of JCOS (e.g., subcommittee policies, program statement approvals, lease approvals), while others are recommendations to the appropriations standing committees and subsequently to the House of Representatives and Senate (e.g., budget bills authorizing planning, construction, and financing, or appropriating funds for MNRTF projects).

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 9

PROJECT FINANCING

There are three ways the State of Michigan can fund capital outlay construction projects: pay-as-you-go, lease-purchase, and bond issuance. Under the pay-as-you-go method, appropriations are made to either meet project costs as they come due or finance the entire project with a lump sum. The lump sum method of funding occurs for a number of smaller, restricted fund projects (e.g., special maintenance, MDOT facilities, most Department of Natural Resources projects). Most often, these projects are funded through appropriations in individual department appropriation acts. The SBA finances nearly all (major) state-owned facility renovations and new construction projects from bond proceeds. The state leases a vast number of facilities across the state. Most of the leases for larger office buildings contain an option to purchase. This is how the state acquired the Lottery Building, the Grand Tower, and Constitution Hall—all in Lansing. In another example of a lease-purchase, the state enters into a long-term contractual lease arrangement with a developer and then receives the building at lease end for a nominal fee. This method is commonly referred to as the certificate of participation (COP) program. The SBA was created by 1964 PA 183 and is governed by a five-member Board of Trustees appointed by the Governor with the advice and consent of the Senate. By statute, SBA’s purpose is to construct, acquire, improve, enlarge, and lease facilities for use by the state, a university, or a community college. Unrelated acquisitions of furnishings and equipment for state agencies may also be financed by the SBA. Local school districts and Intermediate School Districts are specifically precluded from the use of SBA monies. Pursuant to 1964 PA 183, in order to initiate SBA financing, the State Building Authority Board, the State Administrative Board, the Attorney General, the governing body of the university or community college, and the Legislature must approve the conveyance of the property to SBA and the lease back to the State or institution of higher education. Once the Legislature has enacted a project cost authorization including language to convey the subject property to the SBA and approve the lease among the SBA, State, and institution, SBA can issue short- and long-term debt to finance the project. Conveyance of the property is an important aspect of the ability of the SBA to finance a project. If SBA cannot secure clear title to the property, it will be unable to sell bonds to finance the construction. During the construction phase, short-term debt in the form of commercial paper is issued to cover construction cash-flow requirements. Once the facility is complete, a long-term, tax-exempt revenue bond will be issued. Several projects are usually bundled together into one single bond issue. Figure 2 depicts the financing process. All SBA debt obligations are limited obligations of the SBA itself and are not considered general obligations of the state. Therefore, SBA has its own bond rating. Moody’s, Fitch, and Standard and Poor’s all currently rate SBA bonds one step below the state’s general obligation rating: Aa3, AA-, and A+, respectively. SBA debt obligations are not backed by the “full faith and credit of the state.” Rather, the annual SBA rent payment appropriated in annual appropriations acts serves as the guaranteed revenue stream. When the Legislature approves the SBA lease, it is contractually committing to pay the annual rent until THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 11

the SBA debt obligations are satisfied. Under the 2012 reforms, the Legislature is required to appropriate an estimated SBA rent amount for the project being approved at the same time that the construction authorization and SBA lease is authorized. While the appropriation for SBA rent payments is not needed until construction of the facility is complete, meaning that the funds will lapse back to the General Fund in that year, this requirement helps ensure that sufficient funds can be built into the state budget on an ongoing basis.

Figure 2

SBA FINANCING PROCESS Statute requires the SBA rent amount to be a “true market” rate, which is established when construction is complete and the facility has been independently appraised. Depending on the appraisal and other market conditions, the lease will be in effect for approximately 15 to 17 years. The amount of annual rent payment to the SBA is based on the value of the facility and not on debt service costs. Debt service costs determine the length of the lease. Once an obligation for a specific project is retired, the property is conveyed back to the state or institution, and rent payments terminate. Figure 3 shows a ten-year history of GF/GP appropriations for SBA rent payments. Growth in appropriations has been relatively modest as costs for new projects have been offset by savings from rent payments for previous projects being refunded or ending. Rent appropriations are anticipated to remain relatively stable over the next several years. The actual trend will depend on how many new projects are authorized, whether the current bond cap remains the same, and conditions of the general construction and bond markets.

Lease and Conveyance of Land and Facility

Lease agreed to by SBA and user. Lease and conveyance to SBA approved by the Legislature via

boilerplate of an appropriations act. Estimated first year of SBA debt

service is appropriated

Bids for construction are awarded

Short-Term Financing Commercial paper notes issued by SBA to fund

construction cash flow needs

Completion and Occupancy of Facility

Long-Term Financing Bonds issued by SBA to fund

project (usually bundle projects into one single bond issue)

JCOS is notified of the bond sale

Annual SBA Rent Appropriations

Legislature appropriates facility’s true market rent to SBA to cover

debt obligations (GF/GP)

Debt obligation is

retired

Land and Facility Reverts back to the State or

Institution of Higher Education

THE CAPITAL OUTLAY PROCESS PAGE 12 HOUSE FISCAL AGENCY: FEBRUARY 2015

Figure 3

$236.9 $232.7 $225.3 $230.3 $235.4 $241.9$256.9 $256.9

$234.6$254.6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

SBA Rent GF/GP Appropriations(in millions)

The SBA Act limits the maximum allowable amount of SBA debt obligations which can be outstanding at any point in time. This statutory limit is currently set at $2.7 billion which excludes issuing costs and refunding bonds. Table 2 shows the history of statutory SBA bond cap ceilings since the SBA was created. A large number of SBA-financed projects authorized from FY 1993 onward led to the large bond cap increase from 1993 to 1997. The available bond capacity is a constantly fluctuating number, but an important one. The planning, construction, and financing schedules of each individual project affect the bond cap projection. The timing of principal payments on SBA debt is also crucial. Policymakers must have reliable information on how debt obligations compare to the bond cap when considering whether to approve capital outlay projects. Calculating debt obligations is not an exact science as estimates have to be made two to three years in advance of when an authorized project will come online. As of October 31, 2014, based on a $2.7 billion bond cap, SBA estimates that the current available bond capacity is approximately $1.2 billion.

Table 2 State Building Authority Bond Limits

Public Act Amount (millions) PA 183 of 1964 $400.0 PA 206 of 1985 775.0 PA 119 of 1987 1,350.0 PA 35 of 1993 2,000.0 PA 127 of 1997 2,700.0

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 13

CONCLUSION

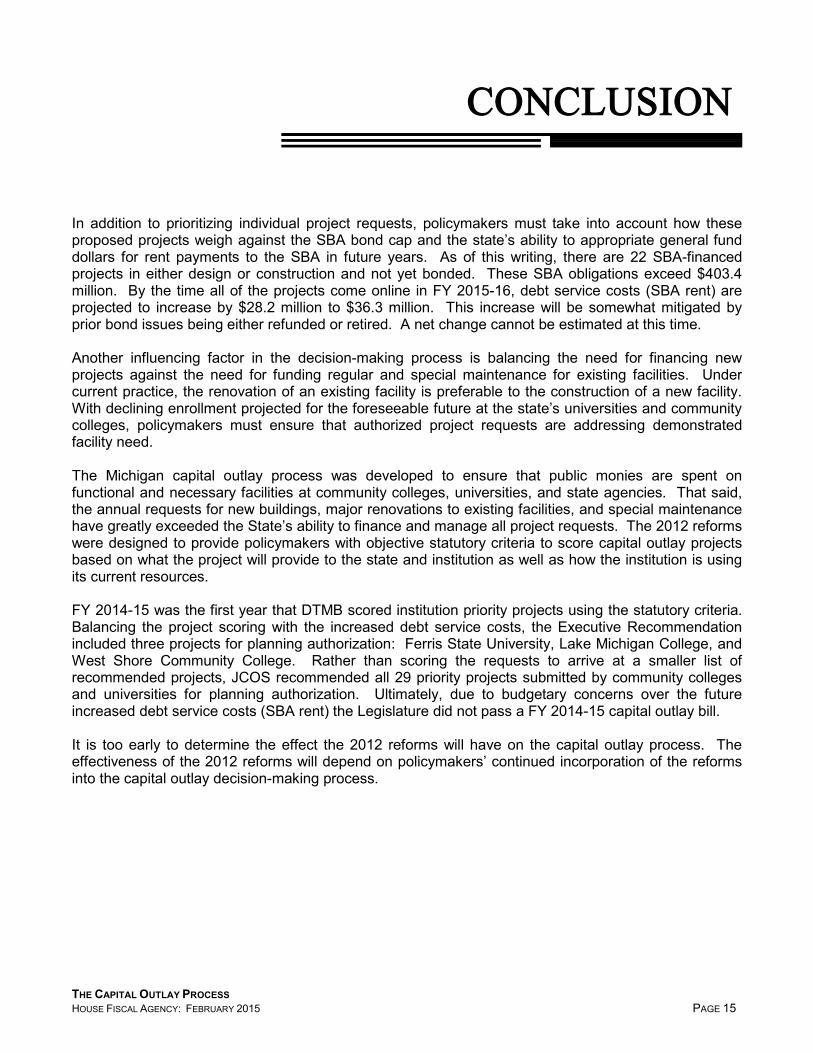

In addition to prioritizing individual project requests, policymakers must take into account how these proposed projects weigh against the SBA bond cap and the state’s ability to appropriate general fund dollars for rent payments to the SBA in future years. As of this writing, there are 22 SBA-financed projects in either design or construction and not yet bonded. These SBA obligations exceed $403.4 million. By the time all of the projects come online in FY 2015-16, debt service costs (SBA rent) are projected to increase by $28.2 million to $36.3 million. This increase will be somewhat mitigated by prior bond issues being either refunded or retired. A net change cannot be estimated at this time. Another influencing factor in the decision-making process is balancing the need for financing new projects against the need for funding regular and special maintenance for existing facilities. Under current practice, the renovation of an existing facility is preferable to the construction of a new facility. With declining enrollment projected for the foreseeable future at the state’s universities and community colleges, policymakers must ensure that authorized project requests are addressing demonstrated facility need. The Michigan capital outlay process was developed to ensure that public monies are spent on functional and necessary facilities at community colleges, universities, and state agencies. That said, the annual requests for new buildings, major renovations to existing facilities, and special maintenance have greatly exceeded the State’s ability to finance and manage all project requests. The 2012 reforms were designed to provide policymakers with objective statutory criteria to score capital outlay projects based on what the project will provide to the state and institution as well as how the institution is using its current resources. FY 2014-15 was the first year that DTMB scored institution priority projects using the statutory criteria. Balancing the project scoring with the increased debt service costs, the Executive Recommendation included three projects for planning authorization: Ferris State University, Lake Michigan College, and West Shore Community College. Rather than scoring the requests to arrive at a smaller list of recommended projects, JCOS recommended all 29 priority projects submitted by community colleges and universities for planning authorization. Ultimately, due to budgetary concerns over the future increased debt service costs (SBA rent) the Legislature did not pass a FY 2014-15 capital outlay bill. It is too early to determine the effect the 2012 reforms will have on the capital outlay process. The effectiveness of the 2012 reforms will depend on policymakers’ continued incorporation of the reforms into the capital outlay decision-making process.

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 15

APPENDIX

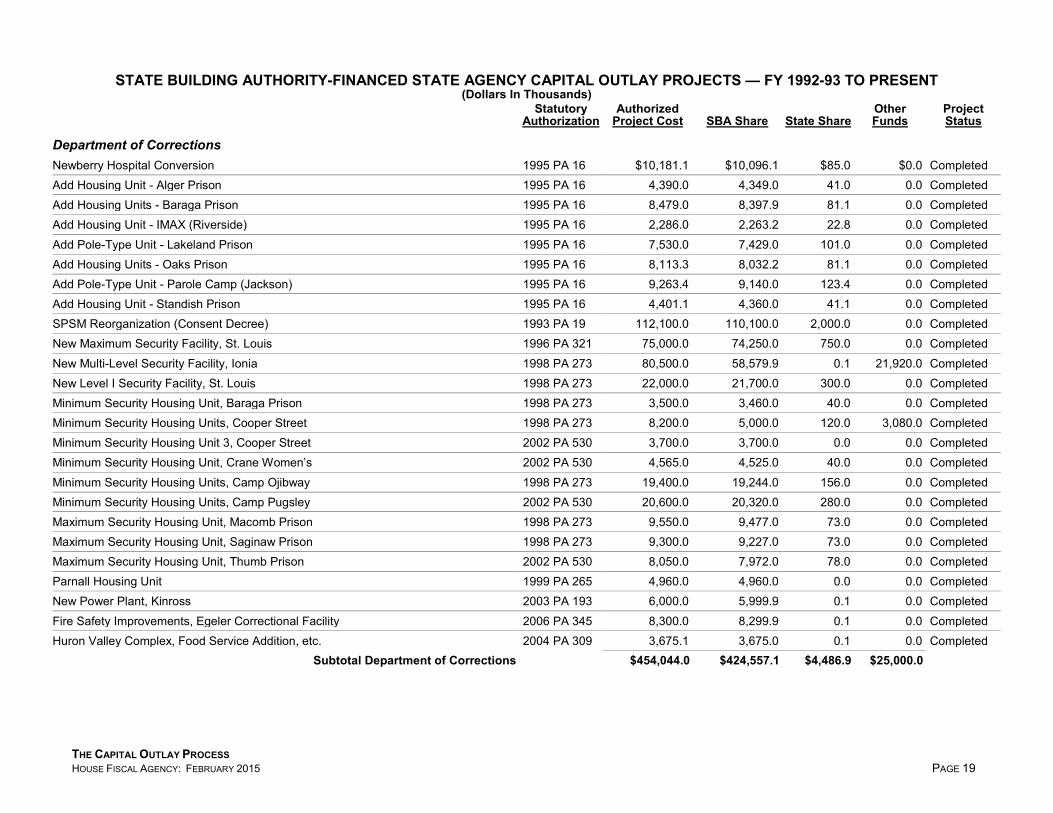

STATE BUILDING AUTHORITY-FINANCED STATE AGENCY CAPITAL OUTLAY PROJECTS — FY 1992-93 TO PRESENT (Dollars In Thousands)

Statutory

Authorization Authorized

Project Cost SBA Share State Share Other Funds

Project Status

Department of Corrections Newberry Hospital Conversion 1995 PA 16 $10,181.1 $10,096.1 $85.0 $0.0 Completed Add Housing Unit - Alger Prison 1995 PA 16 4,390.0 4,349.0 41.0 0.0 Completed Add Housing Units - Baraga Prison 1995 PA 16 8,479.0 8,397.9 81.1 0.0 Completed Add Housing Unit - IMAX (Riverside) 1995 PA 16 2,286.0 2,263.2 22.8 0.0 Completed Add Pole-Type Unit - Lakeland Prison 1995 PA 16 7,530.0 7,429.0 101.0 0.0 Completed Add Housing Units - Oaks Prison 1995 PA 16 8,113.3 8,032.2 81.1 0.0 Completed Add Pole-Type Unit - Parole Camp (Jackson) 1995 PA 16 9,263.4 9,140.0 123.4 0.0 Completed Add Housing Unit - Standish Prison 1995 PA 16 4,401.1 4,360.0 41.1 0.0 Completed SPSM Reorganization (Consent Decree) 1993 PA 19 112,100.0 110,100.0 2,000.0 0.0 Completed New Maximum Security Facility, St. Louis 1996 PA 321 75,000.0 74,250.0 750.0 0.0 Completed New Multi-Level Security Facility, Ionia 1998 PA 273 80,500.0 58,579.9 0.1 21,920.0 Completed New Level I Security Facility, St. Louis 1998 PA 273 22,000.0 21,700.0 300.0 0.0 Completed Minimum Security Housing Unit, Baraga Prison 1998 PA 273 3,500.0 3,460.0 40.0 0.0 Completed Minimum Security Housing Units, Cooper Street 1998 PA 273 8,200.0 5,000.0 120.0 3,080.0 Completed Minimum Security Housing Unit 3, Cooper Street 2002 PA 530 3,700.0 3,700.0 0.0 0.0 Completed Minimum Security Housing Unit, Crane Women’s 2002 PA 530 4,565.0 4,525.0 40.0 0.0 Completed Minimum Security Housing Units, Camp Ojibway 1998 PA 273 19,400.0 19,244.0 156.0 0.0 Completed Minimum Security Housing Units, Camp Pugsley 2002 PA 530 20,600.0 20,320.0 280.0 0.0 Completed Maximum Security Housing Unit, Macomb Prison 1998 PA 273 9,550.0 9,477.0 73.0 0.0 Completed Maximum Security Housing Unit, Saginaw Prison 1998 PA 273 9,300.0 9,227.0 73.0 0.0 Completed Maximum Security Housing Unit, Thumb Prison 2002 PA 530 8,050.0 7,972.0 78.0 0.0 Completed Parnall Housing Unit 1999 PA 265 4,960.0 4,960.0 0.0 0.0 Completed New Power Plant, Kinross 2003 PA 193 6,000.0 5,999.9 0.1 0.0 Completed Fire Safety Improvements, Egeler Correctional Facility 2006 PA 345 8,300.0 8,299.9 0.1 0.0 Completed Huron Valley Complex, Food Service Addition, etc. 2004 PA 309 3,675.1 3,675.0 0.1 0.0 Completed

Subtotal Department of Corrections $454,044.0 $424,557.1 $4,486.9 $25,000.0

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 19

STATE BUILDING AUTHORITY-FINANCED STATE AGENCY CAPITAL OUTLAY PROJECTS — FY 1992-93 TO PRESENT (Dollars In Thousands)

Statutory

Authorization Authorized

Project Cost SBA Share State Share Other Funds

Project Status

Other State Agency - Project Agriculture - Geagley Laboratory 1996 PA 480 $12,000.0 $11,900.0 $100.0 $0.0 Completed DCH - Ypsilanti Forensic Center (adjusted in PA 81 of 2001 and HCR 67 of 2004) 1999 PA 265 109,900.0 109,899.9 0.1 0.0 Completed DHAL - Warehouse Facility Acquisition 2008 PA 278 9,890.0 9,889.9 0.1 0.0 Completed DOE - School for the Deaf and Blind, Housing Facilities 1996 PA 480 1,500.0 1,485.0 15.0 0.0 Completed FIA - Camp Nokomis Renovation 1992 PA 149 3,900.0 3,500.0 400.0 0.0 Completed FIA - U.P. Detention Center (adjusted in PA 192 of 1989 and PA 253 of 1990) 1992 PA 149 4,255.0 4,212.5 42.5 0.0 Completed FIA - Maxey Training Center Renovation 1995 PA 128 37,607.0 37,231.0 376.0 0.0 Completed DIT - Public Safety Communications System, Critical Platform Upgrades 2005 PA 10 13,525.5 13,525.4 0.1 0.0 Completed Judiciary - Hall of Justice/Underground Parking Ramp 1998 PA 538 87,800.0 87,799.9 0.1 0.0 Completed DMB - Allegan Street Parking Ramp 1993 PA 19 21,000.0 20,790.0 210.0 0.0 Completed DMB - Purchase of Grand Tower Building (Lansing) 2001 PA 45 42,988.0 42,988.0 0.0 0.0 Completed DMB - Roosevelt Parking Facility 2001 PA 45 6,506.5 6,506.4 0.1 0.0 Completed DMB - Secondary Complex Warehouse 1999 PA 265 45,000.0 44,999.9 0.1 0.0 Completed DMB - Capitol Complex Renovations 2003 PA 237 27,563.3 27,563.2 0.1 0.0 Completed DMB - Purchase of Constitution Hall (Lansing) 2004 PA 360 122,363.2 122,363.2 0.0 0.0 Completed DMB - State Facility Preservation Projects, Phase I 2005 PA 10 56,220.0 56,219.9 0.1 0.0 Completed DMB - State Facility Preservation Projects, Phase II 2005 PA 297 70,000.0 69,999.9 0.1 0.0 Completed DMB - State Facility Preservation Projects, Phase III 2008 PA 278 42,221.0 42,220.9 0.1 0.0 Construction DTMB - State Facility Preservation Projects, Phase IV 2010 PA 329 35,000.0 34,999.9 0.1 0.0 Construction DTMB - State Emergency Operations Center (adjusted in PA 34 of 2014) 2013 PA 102 22,099.5 16,944.4 655.1 4,500.0 Construction DNR - State Fish Hatcheries Renovations (adjusted in PA 116 of 1997) 1998 PA 273 23,300.0 20,000.0 3,300.0 0.0 Completed State Police - Forensic Sciences Laboratory 1996 PA 480 23,500.0 23,325.0 175.0 0.0 Completed State Police - Metro North/South Posts 1993 PA 19 4,320.0 4,293.0 27.0 0.0 Completed State Police - Public Safety Communications System (bonded as through 5 phases) 1995 PA 128 234,157.2 212,726.0 21,431.2 0.0 Completed State Police - Bay City State Police Post 2008 PA 278 3,700.0 3,699.9 0.1 0.0 Completed State Police - New Headquarters (lease acquisition) 2009 PA 133 52,000.0 52,000.0 0.0 0.0 Completed State Police - Detroit Crime Lab 2010 PA 329 15,000.0 14,999.9 0.1 0.0 Completed

Subtotal Other State Agencies $1,127,316.2 $1,096,083.1 $26,733.1 $4,500.0 Grand Total All State Agencies $1,581,360.2 $1,520,640.2 $31,220.0 $29,500.0

THE CAPITAL OUTLAY PROCESS PAGE 20 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR STATE UNIVERSITIES — 1992 TO PRESENT

University - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

University Share*

Project Status

Central Michigan - Music Building PA 19 of 1993 $20,995,000 $20,995,000 $0 Completed Central Michigan - Primary Electrical System PA 19 of 1993 3,200,000 3,200,000 0 Completed Central Michigan - Park Library Addition/Remodeling PA 480 of 1996 50,000,000 37,500,000 12,500,000 Completed Central Michigan - Health Professions Building PA 515 of 1998 PA 291 of 2000 50,000,000 37,500,000 12,500,000 Completed Central Michigan - Education Building PA 10 of 2005 PA 345 of 2006 50,000,000 37,500,000 12,500,000 Completed Central Michigan - Bio-Science Building PA 329 of 2010 PA 192 of 2012 89,420,000 30,000,000 59,420,000 Construction CMU Subtotal $263,615,000 $166,695,000 $96,920,000 Eastern Michigan - Library Renovation/Office Relocation PA 19 of 1993 $57,668,000 $54,668,000 $3,000,000 Completed Eastern Michigan - Health and Human Services Building PA 480 of 1996 20,417,000 15,312,700 5,104,300 Completed Eastern Michigan - Pray Harrold Hall Renovations PA 278 of 2008 PA 64 of 2009 42,000,000 31,500,000 10,500,000 Completed EMU Subtotal $120,085,000 $101,480,700 $18,604,300 Ferris State - Arts and Sciences Building PA 19 of 1993 $31,225,000 $31,000,000 $225,000 Completed Ferris State - Elastomer Institute PA 321 of 1996 6,650,000 4,650,000 2,000,000 Completed Ferris State - Library Addition and Remodeling PA 480 of 1996 50,000,000 37,500,000 12,500,000 Completed Ferris State - Engineering and Technical Center PA 291 of 2000 PA 506 of 2000 18,000,000 13,500,000 4,500,000 Completed Ferris State - Instructional Resource Center PA 10 of 2005 PA 297 of 2005 8,500,000 5,625,000 2,875,000 Completed Ferris State - Center for Collaborative Health Education PA 278 of 2008 PA 64 of 2009 26,900,000 20,175,000 6,725,000 Completed Ferris State - College of Pharmacy - Grand Rapids PA 329 of 2010 8,800,000 6,600,000 2,200,000 Completed FSU Subtotal $150,075,000 $119,050,000 $31,025,000

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 21

CAPITAL OUTLAY PROJECTS FOR STATE UNIVERSITIES — 1992 TO PRESENT

University - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

University Share*

Project Status

Grand Valley State - Life Sciences Building PA 19 of 1993 $40,790,400 $39,900,000 $890,400 Completed Grand Valley State - School of Business and Grad Library PA 480 of 1996 52,650,000 37,525,000 15,125,000 Completed Grand Valley State - Fresh Water Research Center PA 137 of 1999 1,000,000 1,000,000 0 One-time grant Grand Valley State - Health Professions Building PA 265 of 1999 PA 291 of 2000 53,000,000 37,100,000 15,900,000 Completed Grand Valley State - Padnos College of Engineering PA 10 of 2005 PA 297 of 2005 16,000,000 12,000,000 4,000,000 Completed Grand Valley State - Science Laboratory, Classroom, and

Office Building PA 329 of 2010 PA 192 of 2012 55,000,000 30,000,000 25,000,000 Construction

GVSU Subtotal $218,440,400 $157,525,000 $60,915,400 Lake Superior State - Library Addition PA 19 of 1993 $10,900,000 $10,900,000 $0 Completed Lake Superior State - Crawford Hall Addition/Remodeling PA 480 of 1996 23,000,000 17,250,000 5,750,000 Completed Lake Superior State - Arts Classroom Building PA 538 of 1998 PA 291 of 2000

PA 193 2003 15,300,000 11,475,000 3,825,000 Completed

Lake Superior State – Infrastructure, Technology, Equipment, and Maintenance

PA 468 of 2004 192,700 192,700 0 One-time grant

Lake Superior State - Special Maintenance PA 10 of 2005 PA 10 of 2005 163,100 163,100 Completed Lake Superior State - School of Business Building PA 329 of 2010 PA 102 of 2013 12,000,000 9,000,000 3,000,000 Design LSSU Subtotal $61,555,800 $48,980,800 $12,575,000 Michigan State - Animal and Agricultural Facilities PA 19 of 1993 $69,651,000 $66,651,000 $3,000,000 Completed Michigan State - Crop and Soil Sciences Building PA 19 of 1993 3,100,000 3,100,000 0 Completed Michigan State - Biomedical Science Building PA 480 of 1996 93,000,000 69,750,100 23,249,900 Completed Michigan State - Animal Health Diagnostic Laboratory PA 265 of 1999 PA 291 of 2000 58,000,000 58,000,000 0 Completed Michigan State - Chemistry Building/Cooling Towers PA 10 of 2005 PA 297 of 2005 28,344,500 20,000,000 8,344,500 Completed Michigan State - Bio-Engineering Facility PA 329 of 2010 PA 192 of 2012 57,700,000 30,000,000 27,700,000 Construction MSU Subtotal $309,795,500 $247,501,100 $62,294,400

THE CAPITAL OUTLAY PROCESS PAGE 22 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR STATE UNIVERSITIES — 1992 TO PRESENT

University - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

University Share*

Project Status

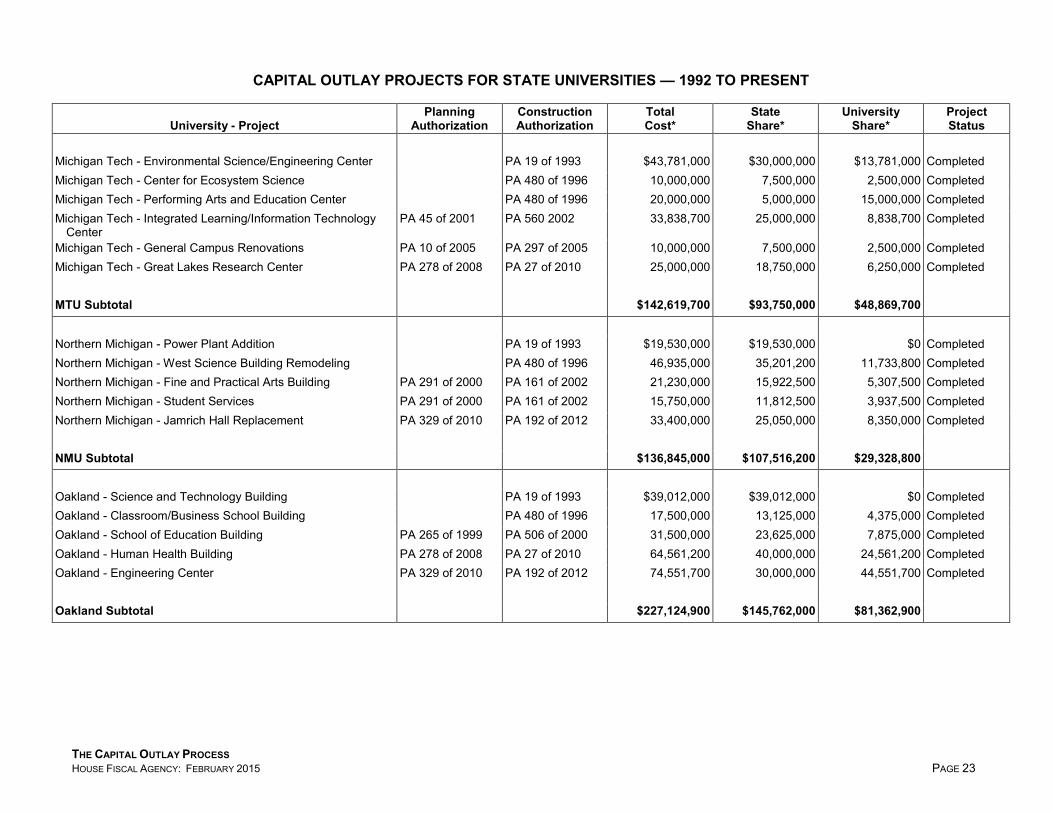

Michigan Tech - Environmental Science/Engineering Center PA 19 of 1993 $43,781,000 $30,000,000 $13,781,000 Completed Michigan Tech - Center for Ecosystem Science PA 480 of 1996 10,000,000 7,500,000 2,500,000 Completed Michigan Tech - Performing Arts and Education Center PA 480 of 1996 20,000,000 5,000,000 15,000,000 Completed Michigan Tech - Integrated Learning/Information Technology

Center PA 45 of 2001 PA 560 2002 33,838,700 25,000,000 8,838,700 Completed

Michigan Tech - General Campus Renovations PA 10 of 2005 PA 297 of 2005 10,000,000 7,500,000 2,500,000 Completed Michigan Tech - Great Lakes Research Center PA 278 of 2008 PA 27 of 2010 25,000,000 18,750,000 6,250,000 Completed MTU Subtotal $142,619,700 $93,750,000 $48,869,700 Northern Michigan - Power Plant Addition PA 19 of 1993 $19,530,000 $19,530,000 $0 Completed Northern Michigan - West Science Building Remodeling PA 480 of 1996 46,935,000 35,201,200 11,733,800 Completed Northern Michigan - Fine and Practical Arts Building PA 291 of 2000 PA 161 of 2002 21,230,000 15,922,500 5,307,500 Completed Northern Michigan - Student Services PA 291 of 2000 PA 161 of 2002 15,750,000 11,812,500 3,937,500 Completed Northern Michigan - Jamrich Hall Replacement PA 329 of 2010 PA 192 of 2012 33,400,000 25,050,000 8,350,000 Completed NMU Subtotal $136,845,000 $107,516,200 $29,328,800 Oakland - Science and Technology Building PA 19 of 1993 $39,012,000 $39,012,000 $0 Completed Oakland - Classroom/Business School Building PA 480 of 1996 17,500,000 13,125,000 4,375,000 Completed Oakland - School of Education Building PA 265 of 1999 PA 506 of 2000 31,500,000 23,625,000 7,875,000 Completed Oakland - Human Health Building PA 278 of 2008 PA 27 of 2010 64,561,200 40,000,000 24,561,200 Completed Oakland - Engineering Center PA 329 of 2010 PA 192 of 2012 74,551,700 30,000,000 44,551,700 Completed Oakland Subtotal $227,124,900 $145,762,000 $81,362,900

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 23

CAPITAL OUTLAY PROJECTS FOR STATE UNIVERSITIES — 1992 TO PRESENT

University - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

University Share*

Project Status

Saginaw Valley - Professional Development Center PA 149 of 1992 $33,500,000 $33,500,000 $0 Completed Saginaw Valley - Energy Loop PA 321 of 1996 3,500,000 3,500,000 0 Completed Saginaw Valley - Classroom Facility PA 480 of 1996 28,500,000 18,750,000 9,750,000 Completed Saginaw Valley - Instructional Facility Number 4 PA 265 of 1999 PA 45 of 2001 40,000,000 30,000,000 10,000,000 Completed Saginaw Valley - Pioneer Hall Renovations/Addition PA 10 of 2005 PA 297 of 2005 16,000,000 12,000,000 4,000,000 Completed Saginaw Valley - Health Sciences Facility PA 278 of 2008 HCR 104 of 2008 28,000,000 21,000,000 7,000,000 Completed Saginaw Valley - Wickes Hall Renovations PA 102 of 2013 PA 34 of 2014 8,000,000 6,000,000 2,000,000 Construction SVSU Subtotal $157,500,000 $124,750,000 $32,750,000 U of M Ann Arbor - Central Campus Renovations I PA 19 of 1993 $32,500,000 $32,500,000 $0 Completed U of M Ann Arbor - Integrated Technology Center PA 19 of 1993 58,350,000 57,000,000 1,350,000 Completed U of M Ann Arbor - Central Campus Renovations II PA 480 of 1996

PA 137 1999 PA 193 2003

88,000,000 59,250,000 28,750,000 Completed

U of M Ann Arbor - Dana Building Renovations PA 538 of 1998 PA 265 of 1999 17,700,000 11,250,000 6,450,000 Completed U of M Ann Arbor - Student Activities Building PA 10 of 2005 PA 153 of 2006 8,500,000 5,751,700 2,748,300 Completed U of M Ann Arbor - Observatory Lodge PA 10 of 2005 PA 297 of 2005 11,500,000 7,820,000 3,680,000 Completed U of M Ann Arbor - Phoenix Laboratory Renovations PA 10 of 2005 PA 345 of 2006 9,500,000 6,428,300 3,071,700 Completed U of M Ann Arbor - G.G. Brown Memorial Laboratories

Renovation PA 329 of 2010 PA 192 of 2012 47,000,000 30,000,000 17,000,000 Construction

U of M Ann Arbor Subtotal $273,050,000 $210,000,000 $63,050,000

THE CAPITAL OUTLAY PROCESS PAGE 24 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR STATE UNIVERSITIES — 1992 TO PRESENT

University - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

University Share*

Project Status

U of M Dearborn - Campus Renovations II PA 19 of 1993 $16,200,000 $14,000,000 $2,200,000 Completed U of M Dearborn - Campus Renovations III PA 480 of 1996 46,900,000 35,175,000 11,725,000 Completed U of M Dearborn - Science Building Renovations PA 265 of 1999 PA 530 of 2002 9,600,000 7,200,000 2,400,000 Completed U of M Dearborn - Engineering Building PA 265 of 1999 PA 530 of 2002 12,600,000 9,450,000 3,150,000 Completed U of M Dearborn - Ford Fairlane Building Acquisition PA 265 of 1999 PA 530 of 2002 32,800,000 24,600,000 8,200,000 Completed U of M Dearborn - Science and Computer Information Science

Building Renovations PA 329 of 2010 PA 192 of 2012 51,000,000 30,000,000 21,000,000 Construction

U of M Dearborn Subtotal $169,100,000 $120,425,000 $48,675,000 U of M Flint - Professional Studies and Classroom Building PA 480 of 1996 $35,623,000 $25,942,200 $9,680,800 Completed U of M Flint - Northbank Center Renovations PA 515 of 1998 3,000,000 3,000,000 0 One-time grant U of M Flint - French Hall/Murchie Hall PA 10 of 2005 PA 345 of 2006 9,350,000 7,000,000 2,350,000 Completed U of M Flint - Murchie Science Laboratory Building Renovations PA 329 of 2010 PA 192 of 2012 22,170,000 16,627,500 5,542,500 Construction U of M Flint Subtotal $70,143,000 $52,569,700 $17,573,300 Wayne State - Old Main Renovations PA 19 of 1993 $45,845,000 $42,845,000 $3,000,000 Completed Wayne State - Undergraduate Library PA 19 of 1993 32,000,000 26,000,000 6,000,000 Completed Wayne State - Pharmacy Building Replacement PA 480 of 1996 66,600,000 48,225,000 18,375,000 Completed Wayne State - Welcome Center PA 538 of 1998 PA 291 of 2000 18,500,000 13,875,000 4,625,000 Completed Wayne State - Engineering Development Center PA 10 of 2005 PA 345 of 2006 27,350,000 15,000,000 12,350,000 Completed Wayne State - Multidisciplinary Bio-Medical Research Building PA 329 of 2010 PA 192 of 2012 90,414,700 30,000,000 60,414,700 Construction WSU Subtotal $280,709,700 $175,945,000 $104,764,700

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 25

CAPITAL OUTLAY PROJECTS FOR STATE UNIVERSITIES — 1992 TO PRESENT

University - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

University Share*

Project Status

Western Michigan - Power Plant PA 149 of 1992 $25,282,000 $22,668,000 $2,614,000 Completed Western Michigan - Science Facility PA 19 of 1993 42,400,000 38,000,000 4,400,000 Completed Western Michigan - Engineering Building PA 480 of 1996 72,500,000 37,500,000 35,000,000 Completed Western Michigan - Health and Human Services Building PA 265 of 1999 PA 45 of 2001 48,170,800 36,128,100 12,042,700 Completed Western Michigan - Lake Michigan Southwest Center PA 265 of 1999 PA 45 of 2001 8,486,000 6,364,500 2,121,500 Completed Western Michigan - Brown Hall Renovations/Addition PA 10 of 2005 PA 297 of 2005 14,800,000 9,500,000 5,300,000 Completed Western Michigan - Sangren Hall Replacement PA 278 of 2008 PA 111 of 2010 60,000,000 30,000,000 30,000,000 Completed WMU Subtotal $271,638,800 $180,160,600 $91,478,200

Total $2,852,297,800 $2,052,111,100 $800,186,700

* Figures are based on appropriation authorizations and do not reflect actual expenditures for final project costs. Actual expenditures are provided in the Annual State Building

Authority Project Cost Summary Report, which can be obtained at: http://www.michigan.gov/treasury/0,4679,7-121-1753_66271---,00.html.

THE CAPITAL OUTLAY PROCESS PAGE 26 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

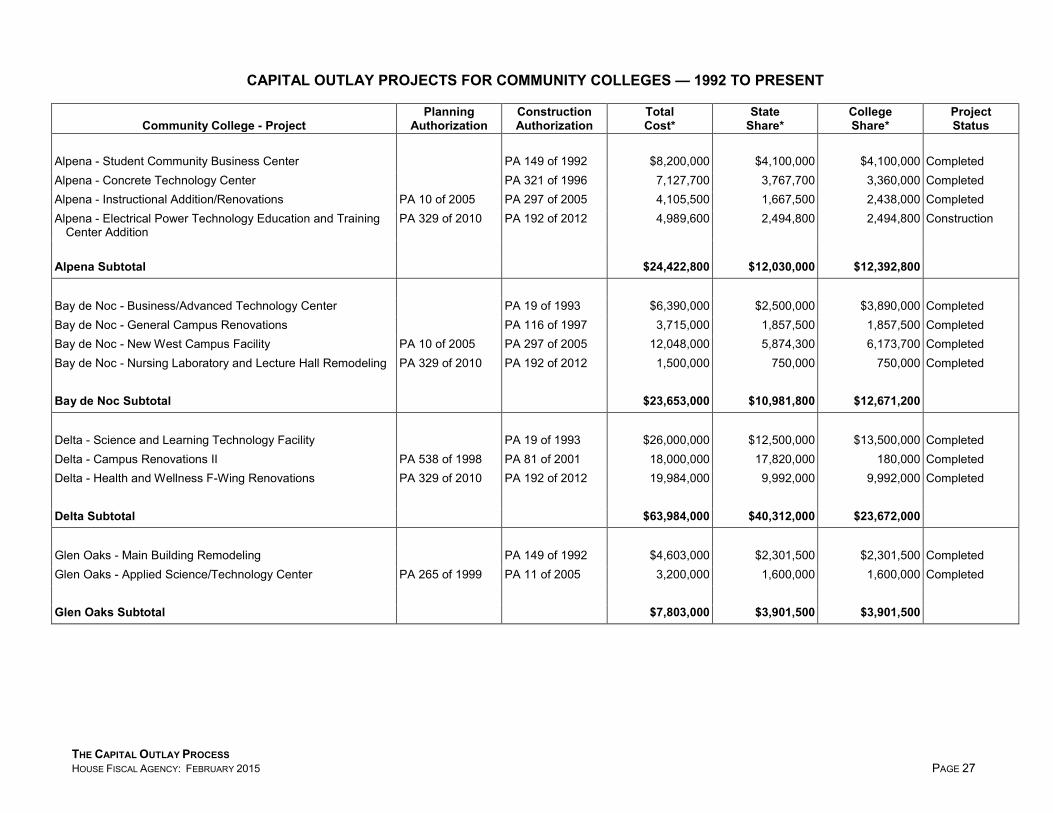

Alpena - Student Community Business Center PA 149 of 1992 $8,200,000 $4,100,000 $4,100,000 Completed Alpena - Concrete Technology Center PA 321 of 1996 7,127,700 3,767,700 3,360,000 Completed Alpena - Instructional Addition/Renovations PA 10 of 2005 PA 297 of 2005 4,105,500 1,667,500 2,438,000 Completed Alpena - Electrical Power Technology Education and Training

Center Addition PA 329 of 2010 PA 192 of 2012 4,989,600 2,494,800 2,494,800 Construction

Alpena Subtotal $24,422,800 $12,030,000 $12,392,800 Bay de Noc - Business/Advanced Technology Center PA 19 of 1993 $6,390,000 $2,500,000 $3,890,000 Completed Bay de Noc - General Campus Renovations PA 116 of 1997 3,715,000 1,857,500 1,857,500 Completed Bay de Noc - New West Campus Facility PA 10 of 2005 PA 297 of 2005 12,048,000 5,874,300 6,173,700 Completed Bay de Noc - Nursing Laboratory and Lecture Hall Remodeling PA 329 of 2010 PA 192 of 2012 1,500,000 750,000 750,000 Completed Bay de Noc Subtotal $23,653,000 $10,981,800 $12,671,200 Delta - Science and Learning Technology Facility PA 19 of 1993 $26,000,000 $12,500,000 $13,500,000 Completed Delta - Campus Renovations II PA 538 of 1998 PA 81 of 2001 18,000,000 17,820,000 180,000 Completed Delta - Health and Wellness F-Wing Renovations PA 329 of 2010 PA 192 of 2012 19,984,000 9,992,000 9,992,000 Completed Delta Subtotal $63,984,000 $40,312,000 $23,672,000 Glen Oaks - Main Building Remodeling PA 149 of 1992 $4,603,000 $2,301,500 $2,301,500 Completed Glen Oaks - Applied Science/Technology Center PA 265 of 1999 PA 11 of 2005 3,200,000 1,600,000 1,600,000 Completed Glen Oaks Subtotal $7,803,000 $3,901,500 $3,901,500

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 27

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

Gogebic - Building Renovations PA 265 of 1999 PA 291 of 2000 $1,400,000 $1,400,000 $0 Completed Gogebic - Special Maintenance Projects PA 10 of 2005 1,000,000 1,000,000 0 Completed Gogebic - Building Renovations PA 329 of 2010 PA 192 of 2012 1,500,000 750,000 750,000 Completed Gogebic Subtotal $3,900,000 $3,150,000 $750,000 Grand Rapids - Science Facility PA 19 of 1993 $30,080,800 $15,040,400 $15,040,400 Completed Grand Rapids - Building Renovations PA 265 of 1999 PA 506 of 2000 6,000,000 3,000,000 3,000,000 Completed Grand Rapids - Cook Academic Hall Renovations PA 329 of 2010 PA 192 of 2012 15,656,700 5,000,000 10,656,700 Completed Grand Rapids Subtotal $51,737,500 $23,040,400 $28,697,100 Henry Ford - Patterson Technology Center PA 149 of 1992 $15,985,000 $6,150,000 $9,835,000 Completed Henry Ford - Learning Resource Center/Health Care Education

Center PA 19 of 1993 25,144,800 10,448,400 14,696,400 Completed

Henry Ford - Building Renovations PA 265 of 1999 PA 506 of 2000 9,856,000 4,928,000 4,928,000 Completed Henry Ford - Science Building Improvements PA 278 of 2008 PA 329 of 2010 15,000,000 7,500,000 7,500,000 Completed Henry Ford Subtotal $65,985,800 $29,026,400 $36,959,400 Jackson - Lenawee Extension Center PA 480 of 1996 $4,400,000 $1,500,000 $2,900,000 Completed Jackson - Health Program Expansion PA 10 of 2005 PA 297 of 2005 18,100,000 7,500,000 10,600,000 Completed Jackson - Whiting Hall Renovation PA 278 of 2008 PA 64 of 2009 21,900,000 10,950,000 10,950,000 Completed Jackson - Bert Walker Hall Renovations PA 329 of 2010 PA 192 of 2012 15,200,000 7,600,000 7,600,000 Design Jackson Subtotal $59,600,000 $27,550,000 $32,050,000

THE CAPITAL OUTLAY PROCESS PAGE 28 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

Kalamazoo Valley - Technological Center/Downtown Center PA 149 of 1992 $14,350,000 $6,500,000 $7,850,000 Completed Kalamazoo Valley - Arcadia Commons Campus Phase II PA 480 of 1996 22,400,000 11,200,000 11,200,000 Completed Kalamazoo Valley - Texas Township Campus Expansion PA 278 of 2008 PA 64 of 2009 11,988,000 5,994,000 5,994,000 Completed Kalamazoo Valley - Healthy Living Campus** PA 102 of 2013 PA 34 of 2014 25,625,200 6,000,000 19,625,200 Design Kalamazoo Valley Subtotal $74,363,200 $29,694,000 $44,669,200 Kellogg - Computer Technology and Academic Center PA 321 of 1996 $16,517,000 $6,000,000 $10,517,000 Completed Kellogg - Career Development Center/Science Building

Renovations PA 291 of 2000 PA 530 of 2002 3,750,000 1,875,000 1,875,000 Completed

Kellogg - Roll Building Renovations PA 746 of 2002 PA 237 of 2003 5,000,000 1,625,000 3,375,000 Completed Kellogg Subtotal $25,267,000 $9,500,000 $15,767,000 Kirtland - Academic Building, Art/Maintenance and

Administration PA 128 of 1995 $7,234,000 $3,617,000 $3,617,000 Completed

Kirtland - Campus Well Water System Upgrades PA 278 of 2008 1,005,000 502,500 502,500 Completed Kirtland Subtotal $8,239,000 $4,119,500 $4,119,500 Lake Michigan - South Campus Facility/Student Services PA 19 of 1993 $8,761,200 $4,380,600 $4,380,600 Completed Lake Michigan - Van Buren Center PA 81 of 2001 PA 560 of 2002 7,800,000 3,900,000 3,900,000 Completed Lake Michigan Subtotal $16,561,200 $8,280,600 $8,280,600 Lansing - Academic Service Facility PA 19 of 1993 $25,570,000 $12,785,000 $12,785,000 Completed Lansing - University Center PA 10 of 2005 PA 297 of 2005 11,000,000 5,000,000 6,000,000 Completed Lansing - Arts and Sciences Building Renovations PA 329 of 2010 PA 192 of 2012 19,950,000 9,975,000 9,975,000 Completed Lansing Subtotal $56,520,000 $27,760,000 $28,760,000

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 29

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

Macomb - General Classroom Building PA 19 of 1993 $8,900,000 $4,450,000 $4,450,000 Completed Macomb - University Center at Central Campus PA 480 of 1996 13,000,000 6,500,000 6,500,000 Completed Macomb - Emergency Services Training Facility PA 265 of 1999 PA 45 of 2001 8,683,000 3,272,500 5,410,500 Completed Macomb - Health Science/Technology Building PA 10 of 2005 PA 297 of 2005 12,000,000 6,000,000 6,000,000 Completed Macomb - Health Science/Technology Building, Phase II PA 329 of 2010 0 0 0 Withdrawn Macomb - South Campus C-Building Renovation PA 102 of 2013 PA 34 of 2014 8,500,000 4,250,000 4,250,000 Design Macomb Subtotal $51,083,000 $24,472,500 $26,610,500 Mid-Michigan - Mount Pleasant Campus PA 165 of 1993 $3,350,000 $1,675,000 $1,675,000 Completed Mid-Michigan - Student Community Center PA 165 of 1993 3,500,000 1,750,000 1,750,000 Completed Mid-Michigan - Student Assessment Center PA 81 of 2001 PA 530 of 2002 3,165,000 1,582,500 1,582,500 Completed Mid-Michigan - Science and Technology Center PA 10 of 2005 PA 297 of 2005 16,475,000 8,237,500 8,237,500 Completed Mid-Michigan - Mt. Pleasant Campus Unification PA 329 of 2010 PA 192 of 2012 17,704,600 8,852,300 8,852,300 Completed Mid-Michigan Subtotal $44,194,600 $22,097,300 $22,097,300 Monroe County - Health Education Building PA 19 of 1993 $6,900,000 $3,450,000 $3,450,000 Completed Monroe County – Business and Technology Center, Library and

Welding Project PA 538 of 1998 PA 69 of 1999 2,500,000 1,250,000 1,250,000 Completed

Monroe County - Performing Arts and Education Building PA 291 of 2000 PA 530 of 2002 12,000,000 6,000,000 6,000,000 Completed Monroe County - Technology Center Construction PA 278 of 2008 PA 329 of 2010 17,000,000 8,500,000 8,500,000 Completed Monroe County Subtotal $38,400,000 $19,200,000 $19,200,000

THE CAPITAL OUTLAY PROCESS PAGE 30 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

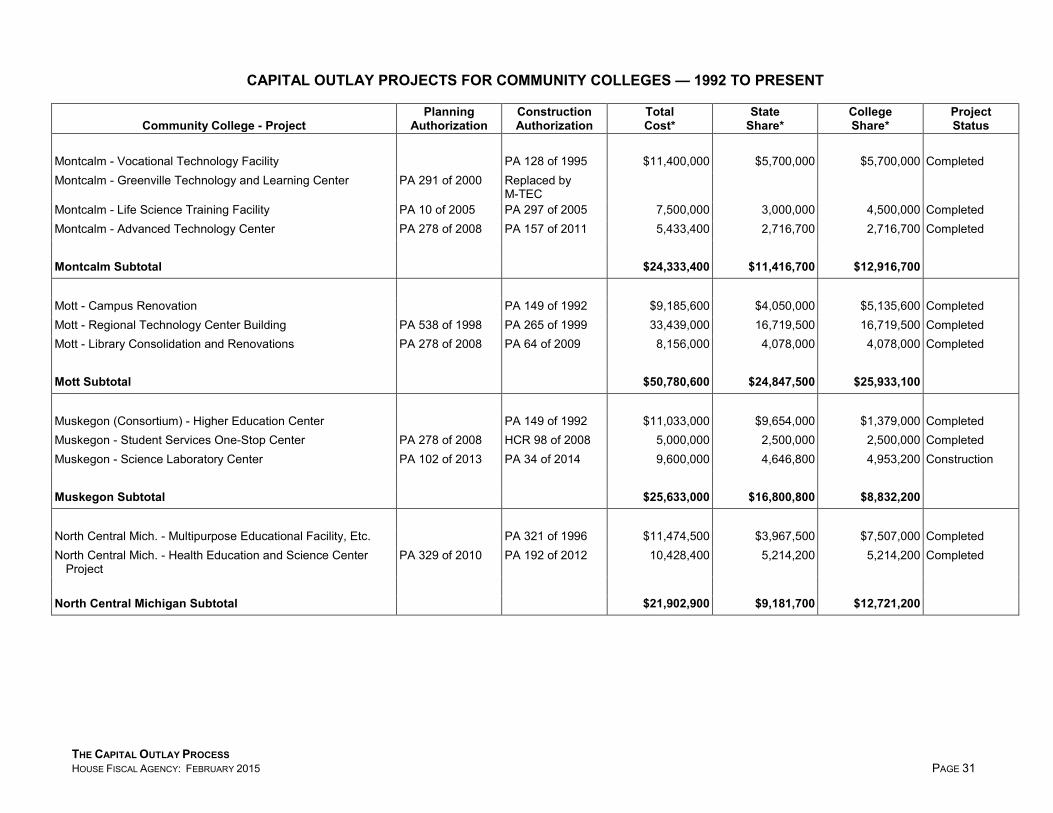

Montcalm - Vocational Technology Facility PA 128 of 1995 $11,400,000 $5,700,000 $5,700,000 Completed Montcalm - Greenville Technology and Learning Center PA 291 of 2000 Replaced by

M-TEC

Montcalm - Life Science Training Facility PA 10 of 2005 PA 297 of 2005 7,500,000 3,000,000 4,500,000 Completed Montcalm - Advanced Technology Center PA 278 of 2008 PA 157 of 2011 5,433,400 2,716,700 2,716,700 Completed Montcalm Subtotal $24,333,400 $11,416,700 $12,916,700 Mott - Campus Renovation PA 149 of 1992 $9,185,600 $4,050,000 $5,135,600 Completed Mott - Regional Technology Center Building PA 538 of 1998 PA 265 of 1999 33,439,000 16,719,500 16,719,500 Completed Mott - Library Consolidation and Renovations PA 278 of 2008 PA 64 of 2009 8,156,000 4,078,000 4,078,000 Completed Mott Subtotal $50,780,600 $24,847,500 $25,933,100 Muskegon (Consortium) - Higher Education Center PA 149 of 1992 $11,033,000 $9,654,000 $1,379,000 Completed Muskegon - Student Services One-Stop Center PA 278 of 2008 HCR 98 of 2008 5,000,000 2,500,000 2,500,000 Completed Muskegon - Science Laboratory Center PA 102 of 2013 PA 34 of 2014 9,600,000 4,646,800 4,953,200 Construction Muskegon Subtotal $25,633,000 $16,800,800 $8,832,200 North Central Mich. - Multipurpose Educational Facility, Etc. PA 321 of 1996 $11,474,500 $3,967,500 $7,507,000 Completed North Central Mich. - Health Education and Science Center

Project PA 329 of 2010 PA 192 of 2012 10,428,400 5,214,200 5,214,200 Completed

North Central Michigan Subtotal $21,902,900 $9,181,700 $12,721,200

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 31

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

Northwestern Mich. - University Center PA 19 of 1993 $5,900,000 $2,400,000 $3,500,000 Completed Northwestern Mich. - Integrated Sci. and Tech. Learning Center PA 116 of 1997 14,100,000 7,050,000 7,050,000 Completed Northwestern Mich. - West Bay Campus Reconstruction PA 81 of 2001 PA 161 of 2002 16,249,200 8,124,200 8,125,000 Completed Northwestern Mich. - Oleson Center Renovations PA 10 of 2005 PA 297 of 2005 1,300,000 650,000 650,000 Completed Northwestern Michigan Subtotal $37,549,200 $18,224,200 $19,325,000 Oakland - Renovation of Building “F” PA 19 of 1993 $10,500,000 $5,250,000 $5,250,000 Completed Oakland Subtotal $10,500,000 $5,250,000 $5,250,000 St. Clair County - University Center/Learning Resource Center PA 128 1995 $0 $0 $0 Terminated St. Clair County - General Campus Renovations PA 291 of 2000 PA 530 of 2002 13,000,000 4,500,000 8,500,000 Completed St. Clair County Subtotal $13,000,000 $4,500,000 $8,500,000 Schoolcraft - Student Services Facility PA 149 of 1992 $7,846,000 $3,923,000 $3,923,000 Completed Schoolcraft - Business Information Center PA 265 of 1999 PA 506 of 2000 27,916,500 13,369,000 14,547,500 Completed Schoolcraft - Technical Services Facility PA 10 of 2005 PA 153 of 2006 12,700,000 5,019,900 7,680,100 Completed Schoolcraft Subtotal $48,462,500 $22,311,900 $26,150,600 Southwestern Mich. - Business Dev. and Student Support Ctr. PA 19 of 1993 $5,000,000 $2,500,000 $2,500,000 Completed Southwestern Mich. - South County Extension Center PA 480 of 1996 3,100,000 1,370,000 1,730,000 Completed Southwestern Mich. - Instructional Resources Center PA 81 of 2001 PA 161 of 2002 2,500,000 1,250,000 1,250,000 Completed Southwestern Mich. - Information Tech. Center Renovations PA 10 of 2005 PA 297 of 2005 5,047,700 2,250,000 2,797,700 Completed Southwestern Mich. - Technology Building Renovation and

Expansion PA 278 of 2008 PA 64 of 2009 3,200,000 1,600,000 1,600,000 Completed

Southwestern Mich. - Science and Allied Health Labs, Classrooms, and Related Renovations

PA 102 of 2013 PA 34 of 2014 8,600,000 3,750,000 4,850,000 Construction

Southwestern Michigan Subtotal $27,447,700 $12,720,000 $14,727,700

THE CAPITAL OUTLAY PROCESS PAGE 32 HOUSE FISCAL AGENCY: FEBRUARY 2015

CAPITAL OUTLAY PROJECTS FOR COMMUNITY COLLEGES — 1992 TO PRESENT

Community College - Project Planning

Authorization Construction Authorization

Total Cost*

State Share*

College Share*

Project Status

Washtenaw - Business Education Center PA 19 of 1993 $6,000,000 $3,000,000 $3,000,000 Completed Washtenaw - Technology and Education Building PA 480 of 1996 21,121,600 10,500,000 10,621,600 Completed Washtenaw - Plumbers/Pipefitters Facility PA 265 of 1999 PA 530 of 2002 4,741,000 2,000,000 2,741,000 Completed Washtenaw - Technical Industrial Building Renovations PA 10 of 2005 PA 297 of 2005 13,985,000 3,000,000 10,985,000 Completed Washtenaw - Skilled Trades Training Program Renovations PA 278 of 2008 PA 27 of 2010 14,800,000 7,400,000 7,400,000 Completed Washtenaw Subtotal $60,647,600 $25,900,000 $34,747,600 Wayne County - General Campus Renovations PA 116 of 1997 $0 $0 $0 Terminated Wayne County - Northwest Campus Replacement Construction PA 278 of 2008 42,000,000 21,000,000 21,000,000 Completed Wayne County Subtotal $42,000,000 $21,000,000 $21,000,000 West Shore - Industrial Skills Center PA 149 of 1992 $3,986,000 $1,068,000 $2,918,000 Completed West Shore - New Student Learning Center PA 10 of 2005 PA 153 of 2006 7,899,400 3,949,700 3,949,700 Completed West Shore - Arts and Sciences Center/Remodeling and

Additions PA 278 of 2008 PA 64 of 2009 6,900,000 3,450,000 3,450,000 Completed

West Shore Subtotal $18,785,400 $8,467,700 $10,317,700

Total $996,756,400 $475,736,500 $521,019,900

* Figures are based on appropriation authorizations and do not reflect actual expenditures for final project costs. Actual expenditures are provided in the Annual State Building

Authority Project Cost Summary Report, which can be obtained at: http://www.michigan.gov/treasury/0,4679,7-121-1753_66271---,00.html.

**State share includes $2.0 million appropriated in FY 2014 MSF budget.

THE CAPITAL OUTLAY PROCESS HOUSE FISCAL AGENCY: FEBRUARY 2015 PAGE 33

Mary Ann Cleary, Director Kyle I. Jen, Deputy Director

Agriculture and Rural Development ......................................................................... William E. Hamilton Capital Outlay ...............................................................................................................Benjamin Gielczyk Community Colleges ..................................................................................................... Marilyn Peterson Community Health: Medicaid, Physical and Behavioral Health .......................... Kevin Koorstra; Steve Stauff; Kyle I. Jen Public Health/Aging/Departmentwide Services............................................................... Susan Frey Corrections ........................................................................................................................ Robin R. Risko Education (Department) ........................................................................................... Samuel Christensen Environmental Quality ........................................................................................................... Austin Scott General Government: Attorney General/Civil Rights/State (Department)/ Technology, Management, and Budget ........................................................................... Perry Zielak Executive Office/Legislature/Legislative Auditor General/ Lottery/Michigan Strategic Fund/Treasury ............................................................Benjamin Gielczyk Higher Education ........................................................................................................... Marilyn Peterson Human Services (Department) .......................................................................................... Viola Bay Wild Insurance and Financial Services ........................................................................................Paul Holland Judiciary ............................................................................................................................ Robin R. Risko Licensing and Regulatory Affairs ........................................................................................Paul Holland Military and Veterans Affairs ................................................................................................. Perry Zielak Natural Resources ................................................................................................................. Austin Scott School Aid .................................................................................... Bethany Wicksall; Samuel Christensen State Police ...........................................................................................................................Paul Holland Transportation ........................................................................................................... William E. Hamilton Economic/Revenue Forecast; Tax Analysis .......................................... Jim Stansell; Adam Desrosiers Revenue Sharing ............................................................................................. Jim Stansell; Ben Gielczyk Legislative Analysis .............................................................................................................. Chris Couch Edith Best; Joan Hunault; Josh Roesner; Sue Stutzky Fiscal Oversight, Audit, and Litigation ......................................................................... Mary Ann Cleary Legislative Transfers ......................................................................................................... Viola Bay Wild Retirement ................................................................................................... Bethany Wicksall; Kyle I. Jen Supplementals ......................................................................................................................... Kyle I. Jen Administrative Assistant ............................................................................................... Kathryn Bateson Budget Assistant /HFA Internet ...........................................................................................Tumai Burris Front Office Coordinator ..................................................................................................... Katie Eitniear

February 2015

P.O. Box 30014 Lansing, MI 48909-7514 (517) 373-8080

www.house.mi.gov/hfa