Michal Radvan EU Tax Policy vs. National Sovereignty of Member States Michal Radvan.

56

EU Tax Policy vs. National Sovereignty of Member States Michal Radvan Michal Radvan

-

Upload

posy-walsh -

Category

Documents

-

view

216 -

download

1

Transcript of Michal Radvan EU Tax Policy vs. National Sovereignty of Member States Michal Radvan.

EU Tax Policy vs. National Sovereignty of Member States

Michal RadvanMichal Radvan

www.law.muni.cz

Aim of the Contribution Level of tax harmonization Taxes to be harmonized

2

www.law.muni.cz

Tax harmonization One of the most discussed issues in EU Proponents point to the need for uniform rules in

connection with the growth of international trade (increasing number and importance of multinational companies and their subsidiaries, the movement of capital and people - residents of one country working in another country). This leads to a conflict of individual tax systems that have been around for decades or even centuries built primarily with regard to national traditions, economic status, political and social developments and also taking into account the natural conditions, religion, etc.

Advocates of national interest: fiscal policy should remain the full responsibility of individual EU Member States - a loss of competitive advantage especially in CEE countries

www.law.muni.cz

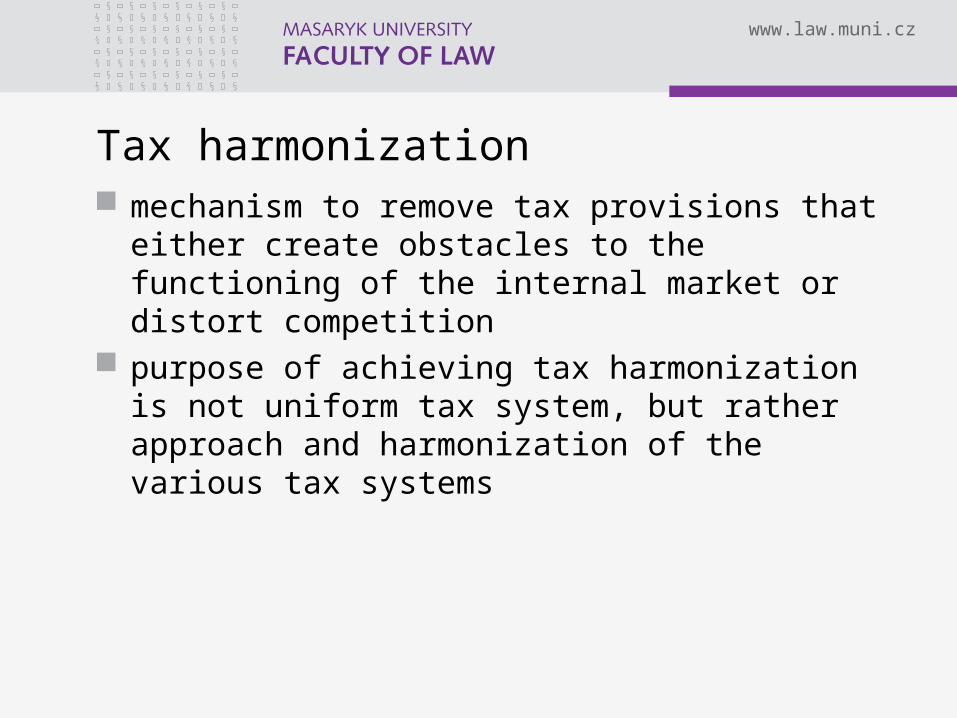

Tax harmonization mechanism to remove tax provisions that either

create obstacles to the functioning of the internal market or distort competition

purpose of achieving tax harmonization is not uniform tax system, but rather approach and harmonization of the various tax systems

www.law.muni.cz

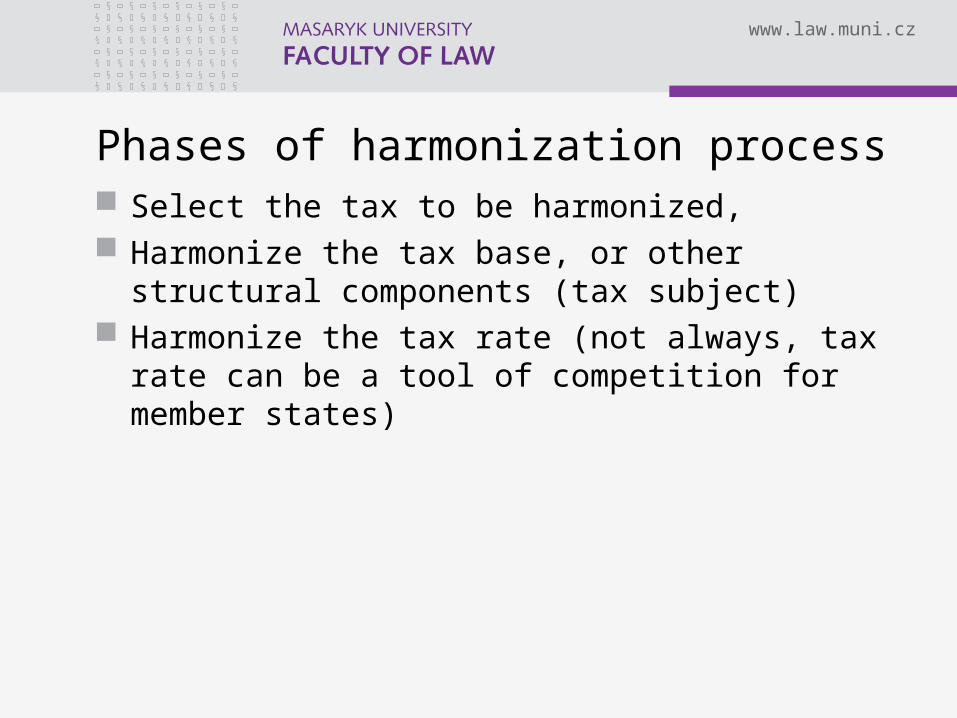

Phases of harmonization process Select the tax to be harmonized, Harmonize the tax base, or other structural

components (tax subject) Harmonize the tax rate (not always, tax rate

can be a tool of competition for member states)

www.law.muni.cz

Tax harmonization in EU tool leading to the ultimate objective of creating a single

market. Important obstacles to the single market are: the tax burden on the free movement of persons and

especially corporates and on the free cross-border movement of goods, services, capital and revenues,

different tax treatment of domestic and imported goods and services,

substantial differences between national tax legislation, which lead to market distortions,

difference in tax treatment between residents and non-residents, and domestic and foreign investments and incomes (in particular the double taxation of incomes from sources outside the country)

Tax harmonization is not just a goal - a final state, but the process itself.

www.law.muni.cz

Tax harmonization as a process Positive harmonization - the process of approximation of

national tax systems through the implementation of the EU directives, regulations and other legislative instruments; the result (assuming the proper implementation of the directives into national legislation) is where all states have the same rules

Negative harmonization - the result of the activities of the European Court of Justice, where national jurisdictions - tax systems taking steps based on the tax case law of the Court; does not create the same rules for all Member States, as the case law is focused only on Member State which is a party in proceedings; ECJ case law, however, may be a good interpretive guide

www.law.muni.cz

Negatives of harmonization Higher tax rates Slower economic growth Does not prevent the excessive expansion of

the public sector It interferes with national sovereignty of

member countries May jeopardize the revenue of public budgets The loss of fiscal autonomy of member states

www.law.muni.cz

Income tax harmonizationIncome tax harmonization Stagnation of the harmonization process Exchange of information Avoidance of double taxation The fight against tax havens

www.law.muni.cz

Start Good conditions - in all countries, there were

personal income tax and corporate income tax (excluding Italy)

Emphasis on corporate taxes (remove barriers of the common market functioning, mobility of capital, labor immobility)

www.law.muni.cz

Sad facts Limiting fiscal sovereignty - the unwillingness The unanimous adoption of directives Differences in accounting systems (tax vs.

Anglo-Saxon) Differences in structural components - social

aspects (children, disability - from tax base or tax), rate (bands, progressivity), application of losses, investment incentives, depreciation

Luxembourg - 17 zones The only rate - BLR, LAT, LTH, ROM, SVK Denmark - up to 59% Romania - 10%

www.law.muni.cz

4 possibilities Taxation in the home country - optional taxation

in each country or just in home country Common Consolidated Tax Base - based on

choice (CCCTB) European corporate tax - for large multinational

companies, at EU level, uniform rate Mandatory harmonized tax base - mandatory,

even for companies operating in only one Member State

www.law.muni.cz

Common Consolidated Tax Base The only rules within the EU for the determination of the

tax base, which would subsequently be divided into subsidiaries and the national tax rate is to be applied

Transparent effective rate and fair tax competition Removing obstacles to cross-border mergers Reduce costs Elimination of problems with transfer pricing Losses in one country and gain in another country - tax

neutrality

Not for non-european small companies

www.law.muni.cz

Taxation in the home country The tax base of all companies in the group

would be set as a consolidated tax base under the laws of the State of management, then divided by the subsidiaries and the national tax rate should be applied

For small companies Effective and cheap It is not harmonization, but rather the possibility

for competition

www.law.muni.cz

The Merge Directive

The main consequence is the possibility of deferral of tax liability that arises from capital gains in case of merger or division of a company, transfer of assets or exchange of shares

The aim is to prevent the taxation of profit, which may arise during the merger because of the difference between the value of the transferred assets and liabilities and their accountings amounts

www.law.muni.cz

The Parent-Subsidiary Directive

The aim of the Directive is to eliminate the double taxation of corporate profits paid by group companies resident in a Member State to the parent company located in another Member State. At least, parent company can deduct the tax paid by the daughter in another country from the tax base.

www.law.muni.cz

The Savings Directive

The aim is to prevent tax evasion to individuals who derive interest income from other Member States

Not applicable to payment of dividend

www.law.muni.cz

The Interest and Royalties Directive

It introduces a unified system of taxation of interest income and royalties between related parties, if they are paid over national borders

www.law.muni.cz

Conclusion It is very likely that there will not be any deepen

fiscal harmonization in the field of direct taxation in the near future

Member States have no will to give up more of their sovereign power

There must be unanimous agreement of all Member States in case of adoption of tax issues

www.law.muni.cz

VAT harmonization Almost finished with the exemption of tax rates

www.law.muni.cz

Start 2 systems of indirect taxation

France: VAT - a general consumption tax, imposed on the added value

Other countries: cumulative cascade system of turnover tax - a tax imposed on the gross value of production; the number of production stages affects the size of the resulting tax; this system causes distortion of the market environment, as the tax burden is increased in proportion to the length of the production / distribution chain; it is necessary for manufacturers to integrate; does not cover services (lawnmower vs. gardening services)

www.law.muni.cz

VAT VAT is the only way The principle of the country of destination, as

the principle of the country of origin assumes a uniform rate

www.law.muni.cz

Directive no. 77/388/EEC (6th Directive) Basic rules Rules for tax base Territory Subjects Rates – basic 15%, reduces 5%

Amended by directive no. 2006/112/EC (7th. Dir.)

www.law.muni.cz

Conclusion Structural harmonization is completed, there is a single

system of indirect taxation Incomplete issue of tax rates harmonization (interference

with national interests, instrument of fiscal policy, the budget revenue, unwillingness to enforce the implementation of the EC Directives, national traditions)

US various sales tax in each country, do not cause market distortions

The minimum amount of the reduced rate is not respected

It maintains the principle of the country of destination, as the country of origin principle would require tax rate unification, but this has proven very effective

www.law.muni.cz

Excise taxes harmonization fiscal plans, political aspects, regulation of

consumption, permanent consumption, luxury, harmfulness

Harmonized: tobacco and tobacco products, alcoholic beverages (spirits, beer, wine), mineral oils, energy

Non-harmonized: cars, fur products, guns, playing cards, roulette, etc.

www.law.muni.cz

Harmonization process Very advanced Efforts to unify rates (favoring domestic

producers is limited, resp. impossible) resulted in at least minimum rates

It relies on spontaneous harmonization process - a country with high rates will have to reduce rates to the level in other countries

The principle of the country of destination (country of origin is impossible with respect to different rates)

www.law.muni.cz

Directive 72/43/EEC System od excise taxes (mineral oils, tobacco, spirit,

beer, wine) abolish other excise taxes, except taxes that do

not need border controls or additional costs of international trade

www.law.muni.cz

Directive 92/12/EEC Horizontal directive Single Customs Tariff to identify the product admits other indirect taxes such as for

environmental reasons - eg taxation of waste (Sweden, Denmark), emissions (Italy, Lithuania), fertilizers (Sweden, Denmark) and air transport (UK, France)

Replaced by Directive 2008/118/EC

www.law.muni.cz

Structural directives Tax bases

www.law.muni.cz

Directive on the rates approximation Minimal rates

www.law.muni.cz

Conclusion Structural harmonization is completed, there is a single

system of indirect taxation Incomplete issue of harmonization of tax rates (national

interests, instrument of fiscal policy, the budget revenue, unwillingness to enforce the implementation of the EC Directives, national traditions)

The principle of the country of destination maintains, as the country of origin principle would require tax rates unification (hard to determine where purchased goods was made), but this has proven very effective

www.law.muni.cz

Taxes on motor vehicles Not in USA Europe, Japan

Registration tax (to be abolished) Regular tax – ones in EU, eco tax? Fuel tax, Vignettes, Toll systems

www.law.muni.cz

„Eurovignette“ Directive For all vehicles above 3,5 tons modifies somewhat broader than only toll (performance

fee) and the user (time) fee generally controls the regular tax on motor vehicles requirement to collect tax only in the Member State in

which the vehicle is registered minimum tax rate tolls and time-based charges may be levied only for the

use of multi-lane highways or roads for motor vehicles for the use of bridges, tunnels and mountain passes

maximum rates for tolls and time-based charges

www.law.muni.cz

Interoperability Directive the obligation to use in the implementation of

toll systems only satellite technology, GSM, or microwave

Preferred mobile technology GSM and GPS satellite due to their intended use within the system Galileo

www.law.muni.cz

Other taxes Tax on Air tickets? Property tax (tax on immovables) – is there any

need to unify? Transfer taxes (on sales, gift tax, inheritance

tax)

www.law.muni.cz

Local vs. State Taxes municipalities (not only in the Czech Republic) have

enough legal competences and sufficient privileges to influence their local taxes revenue?

36

www.law.muni.cz

Challenges for our region From central planning to markets => new

public finance system From State hegemony to local self government Local self governments need stable and

predictable financing To provide mandated services and duties Continued urbanization puts more strain on

urban infrastructure European integration encourages local gov’ts Growing role of subnational governments and

their financing37

www.law.muni.cz

State Taxes More stable Definite income VAT, PIT and CIT, Excises

38

www.law.muni.cz

Economic Autonomy of Municipalities

Article 8 Czech Constitution: There is a self-government of the self-government units

Article 101(3) Czech Constitution: Self-government units are public corporations with the right to own property and the right to manage with their budget.

www.law.muni.cz

Economic Autonomy and ECLSGRules from European Charter of Local Self-Government: Local communities have right fot their own incomes. Part of these incomes are local taxes. Local self-

government can set up these taxes. State must discuss the amount of money send to the

municipalities.

The last two are not valid for the Czech Republic!!! We have no legal act on local taxes!!!

www.law.muni.cz

Own Tax Incomes of the Municipalities

Real estate tax: cca 5 % Local fees and administrative fees:

cca 4 %

www.law.muni.cz

Other Tax Incomes of the Municipalities

VAT: 35 % Personal Income Tax from dependent activity:

19 % Personal Income Tax from business: 8 % Corporate Income Tax without tax paid by

municipalities: 15 % Corporate Income Tax paid by municipalities:

12 %

www.law.muni.cz

43

Local Taxes in General one of the most important revenues of local

budgets suitable instrument for local self-government

units to influence the revenue according to the needs of municipalities, regions, etc.

self-government units have usually rights to impose or abolish local taxes, they can set the tax base and the tax rate, create exemptions and other correction components

to adopt, change, or abolish local law is usually much easier and quicker than to do the same with legal acts at the national level

www.law.muni.cz

Local Taxes ??? Personal income taxes (shared or surcharge) Corporate income taxes (shared) User charges Business registration taxes Visitor taxes Property taxes Gross receipt and turnover taxes Transfer taxes Registration fees Local excise and sales taxes Local wage taxes Building permits, planning permissions etc. Dog taxes Other

44

www.law.muni.cz

Local Tax by Radvan a financial levy, determined to municipal

budget that can be influenced (talking about tax base, tax rates or one of the correction elements) by the municipality; it is not crucial whether the taxpayer obtains from the municipality any consideration or if it is a regular or a single levy – local taxes include the tax in the strict sense, so the charges (fees)

the catalogue of local taxes in the Czech Republic includes tax on immovable property and local charges

45

www.law.muni.cz

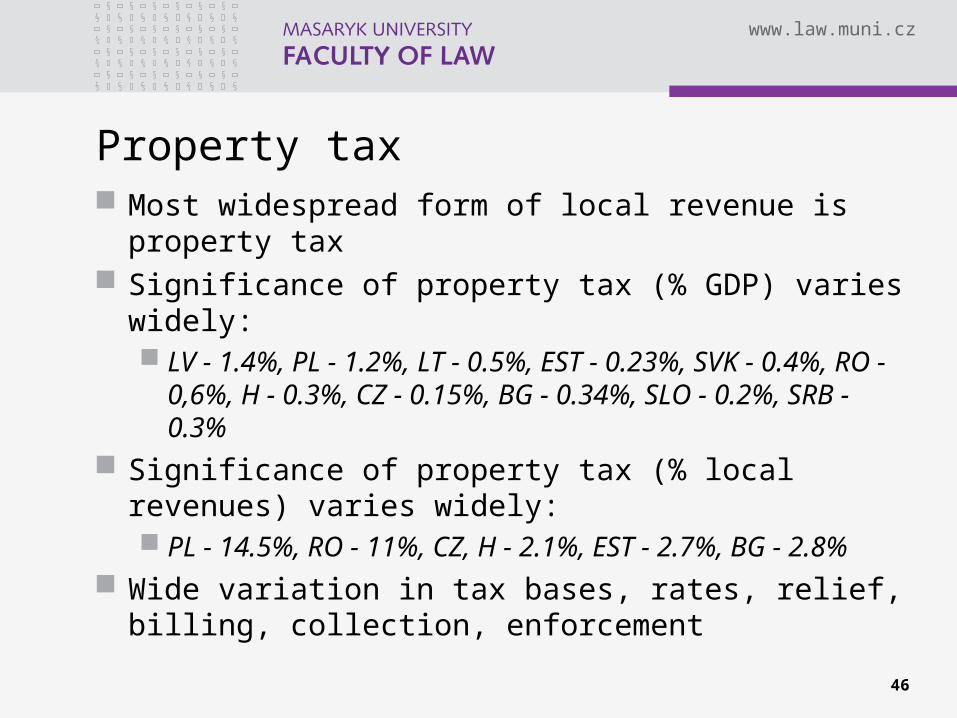

Property tax Most widespread form of local revenue is property

tax Significance of property tax (% GDP) varies widely:

LV - 1.4%, PL - 1.2%, LT - 0.5%, EST - 0.23%, SVK - 0.4%, RO - 0,6%, H - 0.3%, CZ - 0.15%, BG - 0.34%, SLO - 0.2%, SRB - 0.3%

Significance of property tax (% local revenues) varies widely: PL - 14.5%, RO - 11%, CZ, H - 2.1%, EST - 2.7%, BG -

2.8% Wide variation in tax bases, rates, relief, billing,

collection, enforcement

46

www.law.muni.cz

Tax on immovable property municipalities in the Czech Republic can

influence tax in two ways: exemptions

exemption of real estate attached by natural disaster

exemption of agricultural lands possibilities to apply or change coefficients that

can influence the tax rate location rentmunicipal coefficient local coefficient

47

www.law.muni.cz

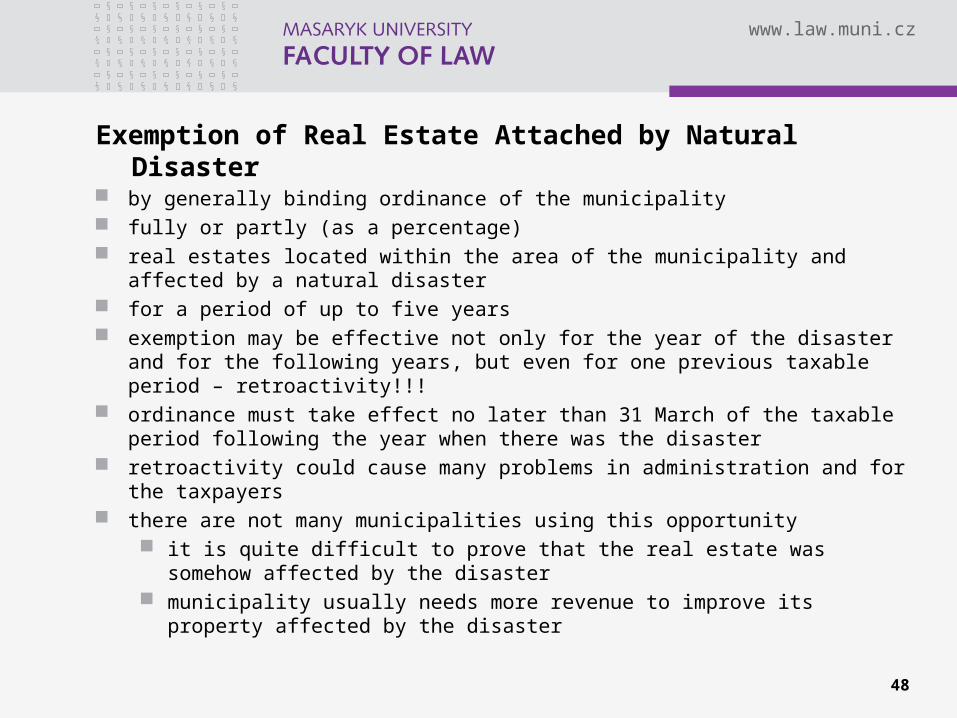

Exemption of Real Estate Attached by Natural Disaster

by generally binding ordinance of the municipality fully or partly (as a percentage) real estates located within the area of the municipality and affected by a

natural disaster for a period of up to five years exemption may be effective not only for the year of the disaster and for

the following years, but even for one previous taxable period – retroactivity!!!

ordinance must take effect no later than 31 March of the taxable period following the year when there was the disaster

retroactivity could cause many problems in administration and for the taxpayers

there are not many municipalities using this opportunity it is quite difficult to prove that the real estate was somehow affected

by the disaster municipality usually needs more revenue to improve its property

affected by the disaster

48

www.law.muni.cz

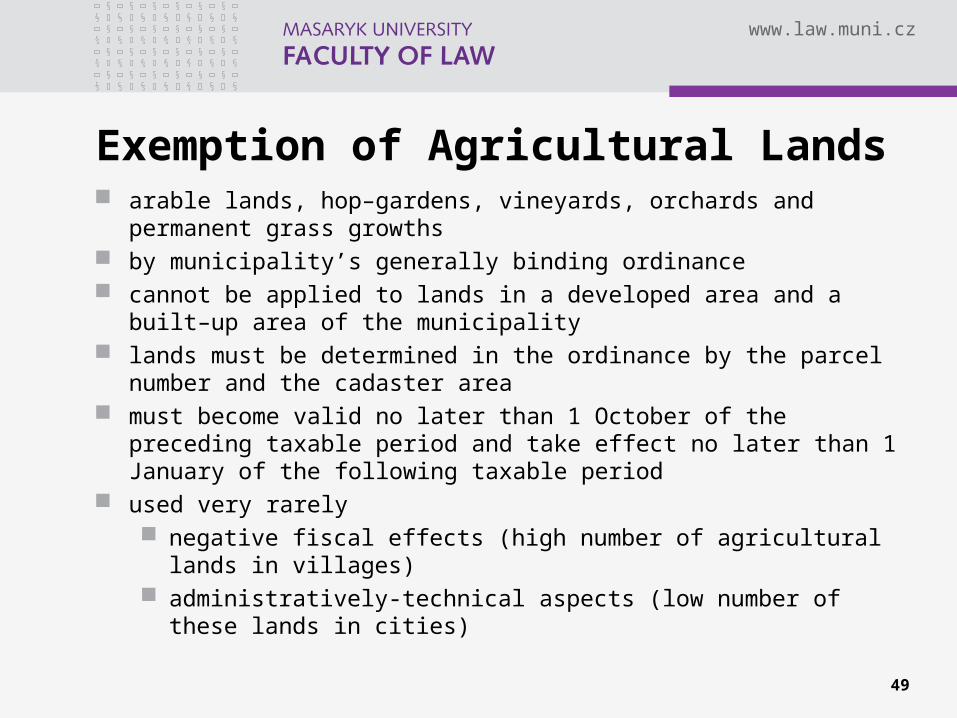

Exemption of Agricultural Lands arable lands, hop–gardens, vineyards, orchards and permanent

grass growths by municipality’s generally binding ordinance cannot be applied to lands in a developed area and a built–up

area of the municipality lands must be determined in the ordinance by the parcel

number and the cadaster area must become valid no later than 1 October of the preceding

taxable period and take effect no later than 1 January of the following taxable period

used very rarely negative fiscal effects (high number of agricultural lands in

villages) administratively-technical aspects (low number of these

lands in cities)

49

www.law.muni.cz

Location Rent coefficient according to the number of inhabitants for development lands, residential buildings, other

structures that provide facilities for residential buildings, flats and non–residential premises not used for the running of businesses and as garages

multiplies the standard tax rate basic value of the coefficient is set in the act (between

1.0 and 4.5) municipalities have the right to increase (up to one level)

or reduce (down to three levels) a basic coefficient by a generally binding ordinance

must become valid no later than 1 October of the preceding taxable period and take effect no later than 1 January of the following taxable period

50

www.law.muni.cz

Municipal Coefficient for houses and family houses used for individual

recreation, other structures that provide facilities for houses and family houses used for individual recreation, garages, structures for business activities, non–residential premises used for business activities and as garages

municipalities have the right to set this coefficient by their generally binding ordinance for particular types of structures

value of the coefficient is at 1.5 and it multiplies standard tax rate

must become valid no later than 1 October of the preceding taxable period and take effect no later than 1 January of the following taxable period

51

www.law.muni.cz

Local Coefficient multiplies the tax duty of the taxpayer for particular kinds

of lands, buildings, non–residential premises and flats at 2, 3, 4 or 5 by a generally binding ordinance for all real estates in their area, excluding agricultural lands must become valid no later than 1 October of the

preceding taxable period and take effect no later than 1 January of the following taxable period

only 7 % of municipalities in the Czech Republic are using this option political reasons some municipalities argue that they do not want to increase

the tax for all real estate, especially residential one

52

www.law.muni.cz

Local Charges I every municipality has a possibility to levy local

charges (local fees) by the generally binding ordinance

catalogue set by Local Charges Act includes following local charges: dog charge charge for spa and recreation stay charge for using public places charge on entrance (admission) charge for housing capacity charge on communal waste charge for permission to enter selected places by motor

vehicle charge on the evaluation of building land

53

www.law.muni.cz

Local Charges II list is comprehensive and the municipality cannot levy

any other charge municipality can define conditions for levying, the charge

rate, charge maturity, eventual exemptions, etc. the ordinance may not exceed the conditions defined by

the Local Charges Act (for example absolute charge rate or the definition of taxpayer)

no conditions when the ordinance must become valid and take effect, but especially for those charges with the taxable period of one calendar year (dogs and communal waste) I strongly recommend effectiveness to 1 January of the taxable period

ordinances must not be retroactive

54

www.law.muni.cz

Conslusion local taxes in the Czech Republic have minor role in the self-

government units financing real estate tax approx. 5 % local charges approx. 5 % very depends on number of inhabitants

several possibilities for municipalities to influence their budget incomes through local taxes, but none options like that for regions

local self-government units are dependent on the transfers of shared taxes (PIT, CIT, VAT) from central budget in drawing up their budgets

I have to reject the hypothesis that municipalities in the Czech Republic have enough legal competences and sufficient privileges to influence their local taxes revenue

shared taxes are the base for local budgeting PIT and richmen?

55

www.law.muni.cz

Thank you for your attention