Michael Cueva Andrew Dartez Audrey...

127

1 Michael Cueva Andrew Dartez Audrey Guazzone Dylan Mclaughlin

-

Upload

duongkhanh -

Category

Documents

-

view

216 -

download

1

Transcript of Michael Cueva Andrew Dartez Audrey...

1

Michael Cueva Andrew Dartez

Audrey Guazzone Dylan Mclaughlin

2

Table of Contents Executive Summary 4

Industry Analysis 5

Accounting Analysis 6

Financial Analysis, Forecast Financials, and Cost of Capital Estimation 7

Valuations 9

Southwest Airlines and the Airline Industry 10

Company Overview 11

Industry Overview 13

Industry Analysis: five factors model 16

Rivalry amongst existing firms 17

Threat of new Entrants 27

Threat Of Substitutes 30

Bargaining Power of Customers 33

Bargaining Power of Suppliers 37

Value Chain Analysis 40

Firm Competitive Advantage 43

Accounting Analysis 46

Key Accounting Policies 47

Potential Accounting Flexibility 51

Actual Accounting Strategy 55

Quality of Disclosure 57

Qualitative Analysis of Disclosure 60

Potential Red Flags 69

Accounting Distorsions 72

Financial Analysis, Forecasting Financials and Cost of Capital Estimation 73

Financial Analysis 73

Liquidity Ratio Analysis 73

3

Profitability Ratio Analysis 79

Capital Structure Analysis 86

Internal Growth Rate and Sustainable Growth Rate Analysis 90

Financial Statement Forecasting 93

Cost of Capital Estimation 104

Intrinsic Valuations 109

Appendices 117

References 127

4

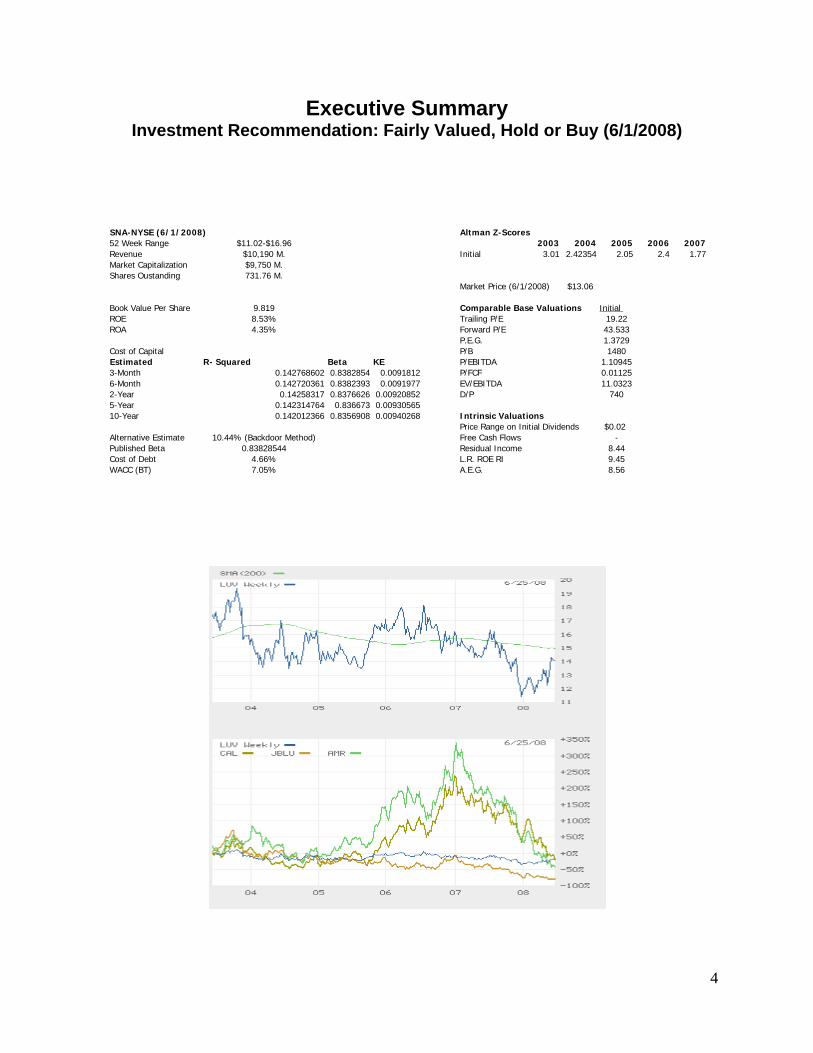

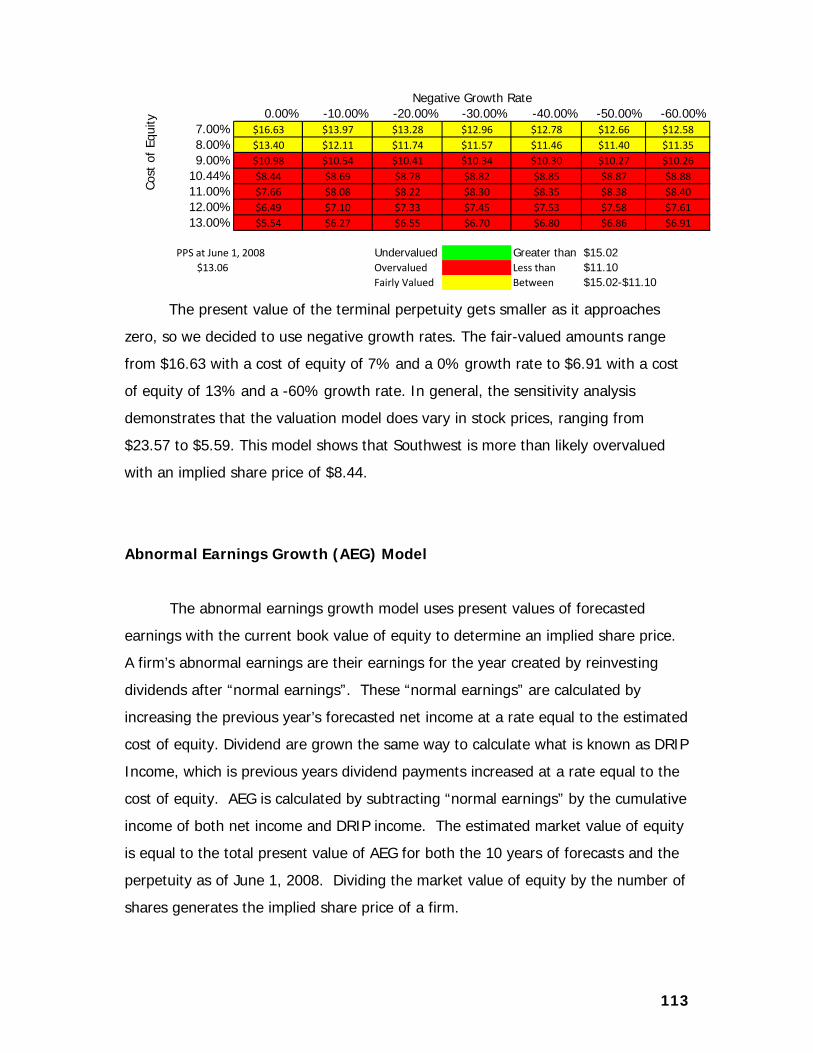

Executive Summary Investment Recommendation: Fairly Valued, Hold or Buy (6/1/2008)

SNA-NYSE (6/1/2008) Altman Z-Scores52 Week Range $11.02-$16.96 2003 2004 2005 2006 2007Revenue $10,190 M. Initial 3.01 2.42354 2.05 2.4 1.77Market Capitalization $9,750 M.Shares Oustanding 731.76 M.

Market Price (6/1/2008) $13.06

Book Value Per Share 9.819 Comparable Base Valuations Initial ROE 8.53% Trailing P/E 19.22ROA 4.35% Forward P/E 43.533

P.E.G. 1.3729Cost of Capital P/B 1480Estimated R- Squared Beta KE P/EBITDA 1.109453-Month 0.142768602 0.8382854 0.0091812 P/FCF 0.011256-Month 0.142720361 0.8382393 0.0091977 EV/EBITDA 11.03232-Year 0.14258317 0.8376626 0.00920852 D/P 7405-Year 0.142314764 0.836673 0.0093056510-Year 0.142012366 0.8356908 0.00940268 Intrinsic Valuations

Price Range on Initial Dividends $0.02Alternative Estimate 10.44% (Backdoor Method) Free Cash Flows -Published Beta 0.83828544 Residual Income 8.44Cost of Debt 4.66% L.R. ROE RI 9.45WACC (BT) 7.05% A.E.G. 8.56

5

Industry Analysis

Southwest Airlines Company is a major domestic airline that provides point to

point, low fare service. Southwest is headed by Gary C Kelly. It employs a relatively

simple fare structure, featuring low, unrestricted, unlimited, everyday coach fares, as

well as lower fares available on a restricted basis. Southwest currently flies to 64

destinations throughout the United States with more than 3,300 flights a day. The firm

is the primary example of an airline that still uses the point to point transit model.

Currently, however, Southwest Airlines actually uses a hybrid system, flying point to

point routes, but also connecting passenger through several smaller hubs. The company

and its third-party maintenance providers are subject to the jurisdiction of the Federal

Aviation Administration with respect to maintenance and operations.

Southwest was incorporated in Texas in 1967 but obtained the right to fly after a

three year legal battle, which is considered by many to be the beginning of deregulation

in the airline industry. Southwest commenced Customer Service on June 18, 1971, with

three Boeing 737 aircraft serving three cities- Dallas, Houston and San Antonio.

Southwest turned its first annual profit in 1973, and has done so every year since.

Southwest has used financial techniques such as fuel hedging to bolster its profitability

and counteract many of the fiscal disadvantages of operating an airline.

Existing firms compete in an almost cost control industry with a minimal level of

differentiation. The success and profitability of Southwest’s overall cost leadership

strategy led to a common trend being named the Southwest Effect. Indeed, Southwest

entered the airline market, and the market itself changed. The number of customers

augmented significantly. Direct competitors of Southwest Airlines include JetBlue,

American Airlines and Continental.

The airline industry is extremely competitive. Rivalry is intense. The U.S. airline

industry has been in a chaotic state for a number of years. It is now a stagnant industry

6

where the concentration is changing according to the recent mergers and alliances.

Companies face increased exposure to the raw oil market every year. This is not a good

sign for the airlines, which are also facing tough competition for US legacy carriers that

have lowered cost through bankruptcy. With the market already over-saturated,

operating limits, and the start up costs being high, the threat of new entrants is low.

However, the threat of substitutes is medium because advantages like speed, service,

and routes provided by planes seem to be considerable compared to substitutes.

However, the relative price performance of trains could be a major threat in a decade

for regional airlines. Buyers’ power is medium/high due to low switching costs, price

sensitivity, standard product, information access, a large number of buyers and low

volume purchases. Finally, suppliers’ power is very high because only Boeing and Airbus

provide planes, and the oil price is increasing.

To be successful, an airline must be effective in three general areas. They need

to attract customers and the ticket price is by far the most significant factor in

attractiveness. Managing its fleet with a cost efficiency control system is essential.

Finally airlines have to be very innovative to try to differentiate themselves from their

competitors.

Accounting Analysis

In order to evaluate a company properly, it is important to look meticulously at

the company’s financial statements. To provide a precise valuation, it is essential to

question how transparent these financials are. The degree of disclosure by the company

is important when evaluating the financial statements. Full disclosure will give a more

accurate picture of the company. Many companies try to hide key information in order

to make the company more appealing to potential investors. There are many ways a

company can manipulate their financials even though they are regulated by the SEC.

This practice makes it complicated for investors or shareholders to have a clear

accurate view of the company. It also makes it difficult for an analyst to have a clear

outlook of the firm in order to make a fair valuation of it.

7

Southwest had a high-level of disclosure when it came to their information on

their 10k. They key accounting policies for Southwest Airlines include: revenue

recognition, fuel hedging, capital and operating leases, and retirement and pension

plans. Accounting policies that directly correlate with the identified success factors are

revenue recognition, fuel hedging practices, capital and operating leases, and

retirement and pension plans. Southwest recorded unearned revenue as air traffic

liabilities on the balance sheet before it records it as passenger revenue on the income

statement. It is finally allocated when the passenger is on the plan and the plane has

taken off. Southwest along with many of its competitors practice this accounting when

recording unearned revenue. This accounting practice is in accordance with GAAP, but

can be distorted by managers in order to make their financials look attractive. They

accounted for rising price of fuel in their fuel hedging analysis. They stated their prices

and how they were going to deal with them now and in the future. In the case of

capital and operating leases, it is straight forward; 86 of the 95 planes Southwest leases

are classified as operating leases while the other 9 are classified with capital leases.

The overall accounting strategy for Southwest’s financial statements was fairly

conservative. The accounting had little or no room for any discrepancies leaving no

information out. They explained why they placed line items on their financials.

Financial Analysis, Forecast Financials, and Cost of Capital Estimation

Financial Analysis

When analyzing a firm, potential shareholders look at three main areas to predict

the strength of any given firm. These areas include: a firm’s liquidity, profitability, and

capital structure. With applying useful ratios and trends that can be determined from

past as well as current transactions, the potential shareholder can therefore be able to

make a better and well informed decision on his/her upcoming investment.

8

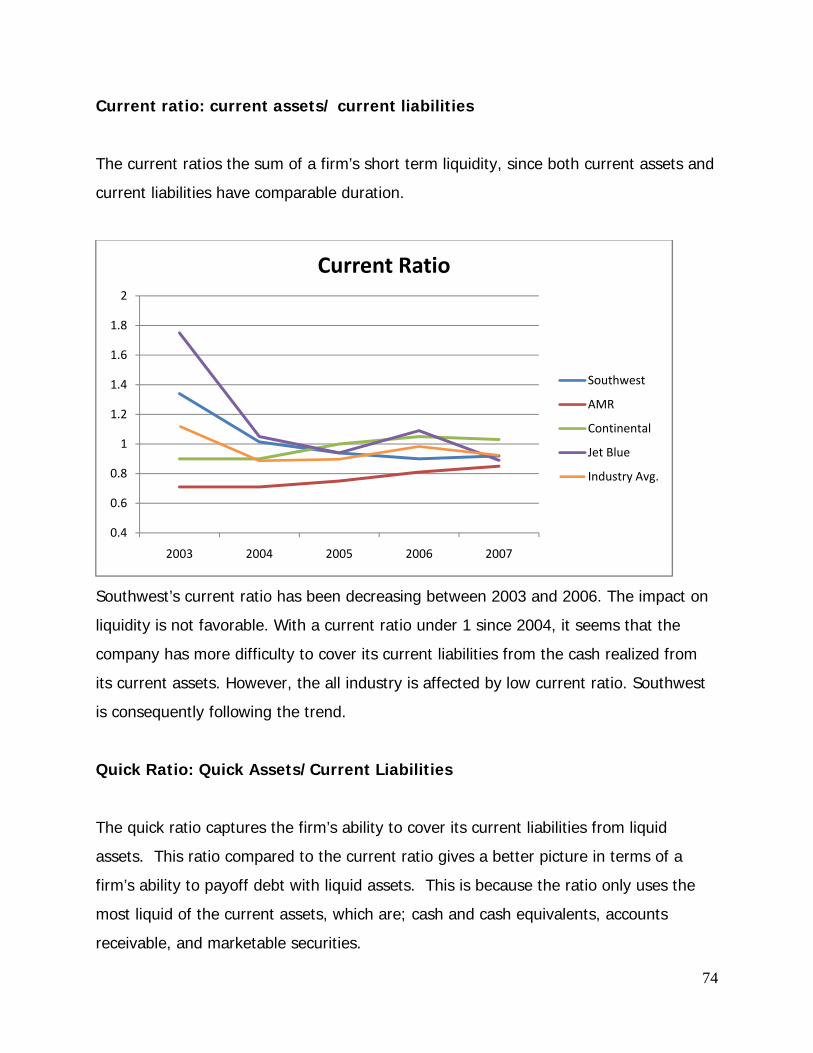

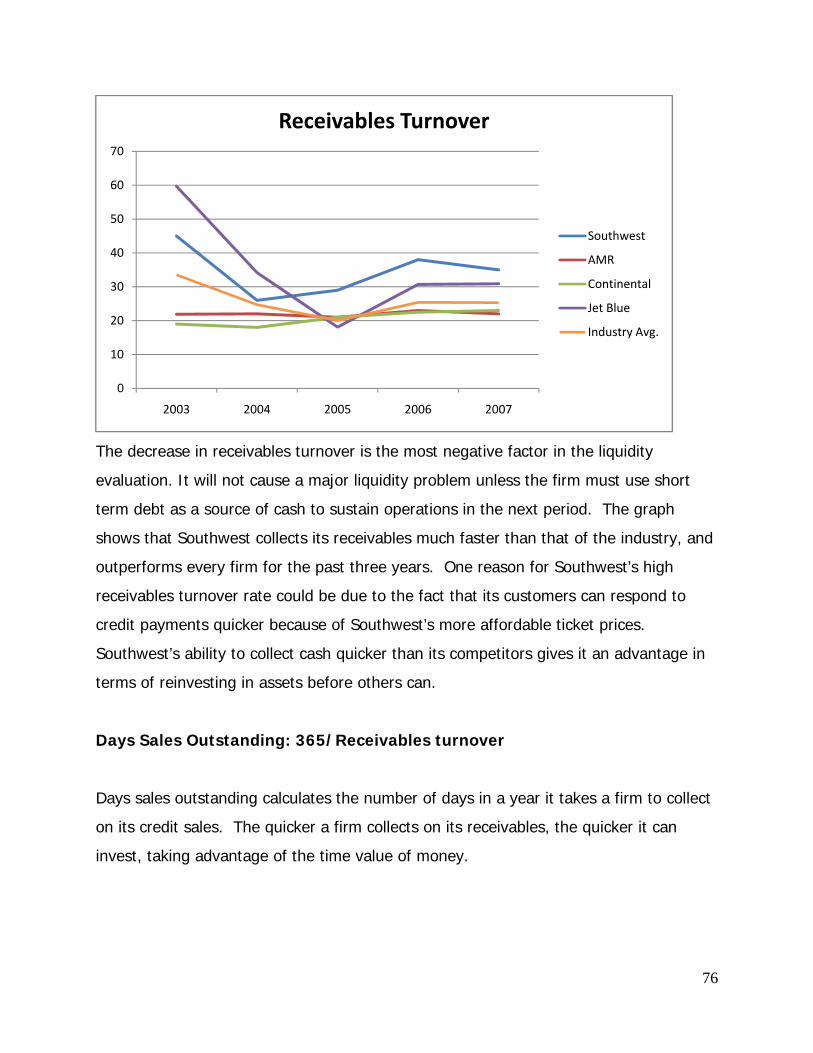

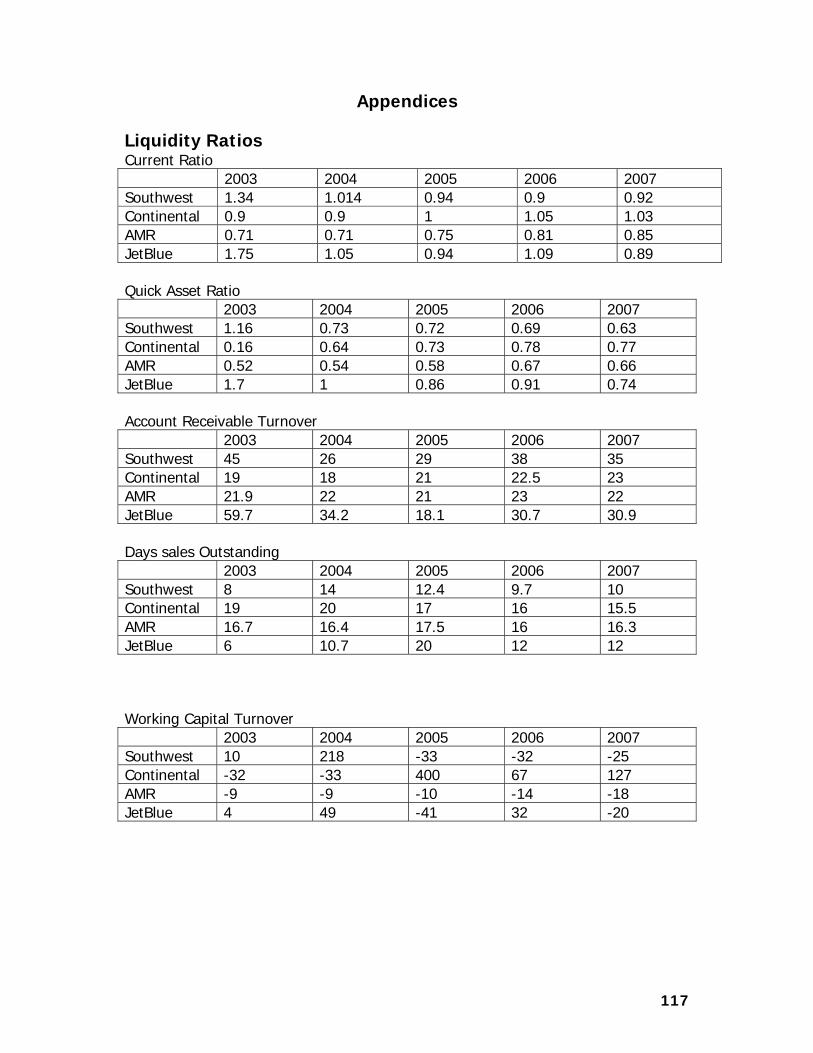

Liquidity

Southwest’s current ratio and quick ratio have been decreasing since 2006. The

impact on liquidity is not favorable. With a current ratio of less than 1 and a quick ratio

of .63 it seems that the company has more difficulty covering its current liabilities from

the cash realized on the current asset account. However, the entire industry is affected

by low current and quick ratios, but Southwest seems to stand alone by having a higher

365/receivables turnover which helps it receive cash realized on credit accounts faster

than its competitors.

Profitability

Like the liquidity ratios, the airline industry all follows the same trends in

profitability ratios. The Net profit margin, gross profit margin, and the operating profit

margin are all very low. However, Southwest seems to always stay on top of the

competition by their superior operating efficiency. The reason they continually best the

other competitors in the industry is due to their primary focus on cost reduction.

Keeping costs down creates the potential for greater profit margins, which is

Southwest’s main competitive advantage.

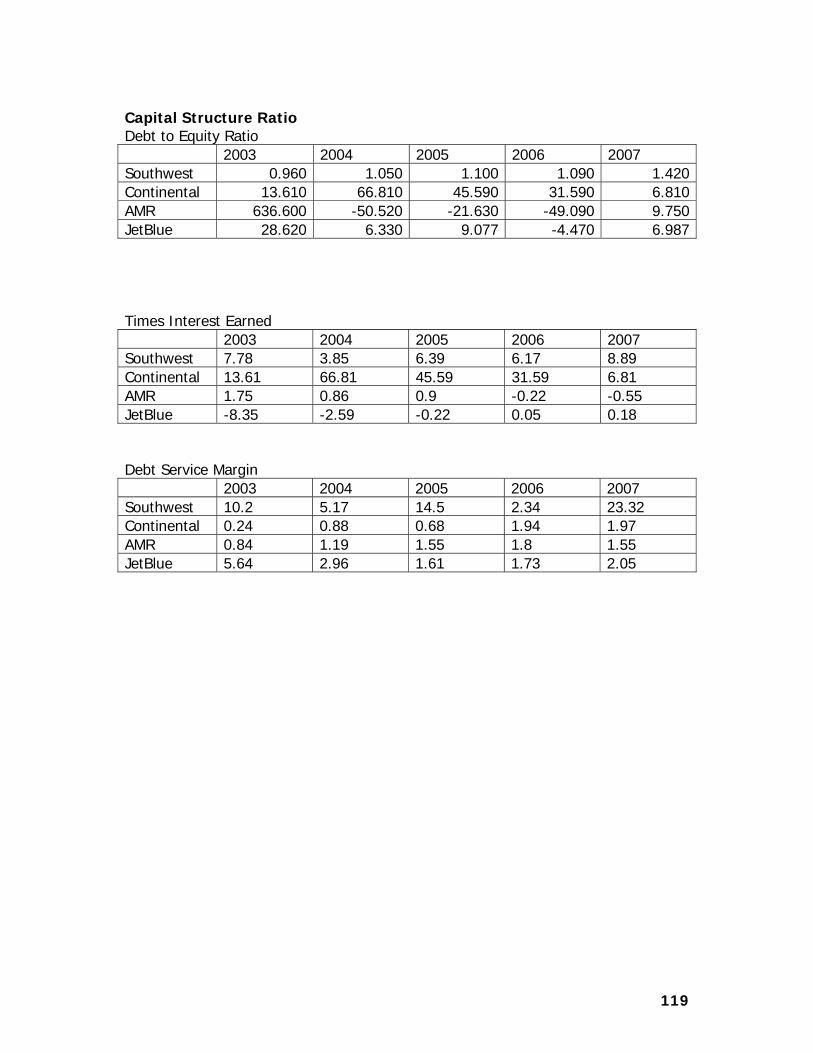

Capital Structure

The three capital structure ratios that Southwest was evaluated on were the debt to

equity ratio, times interest earned, and the debt service margin. Overall, Southwest

usually tends to follow the industry average when it comes to these ratios as pertaining

too closely relating its financial activities through debt and equity outsourcing. However,

they by far exceed their competition in the debt to equity category by generating large

surpluses of cash (from operations) than needed to cover their liabilities.

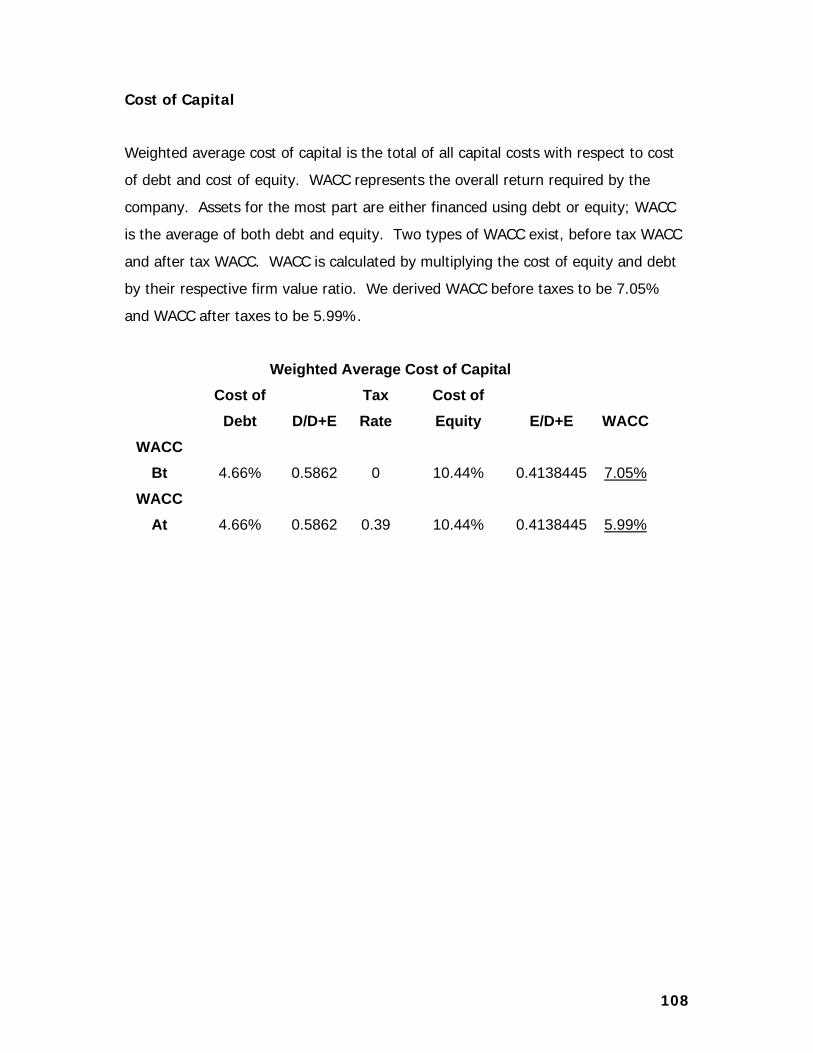

Forecast Financials/Cost of Capital Estimation

9

To forecast Southwest’s financial accounts for the following ten years ending in

2017, we used our financial ratios, industry averages and trends, and growth rates

within the company pertaining to patterns that we saw fit. Along with these three

forecasting techniques, we used our extensive knowledge of the company’s future

strategies pertaining to cost efficiency tactics and fuel hedging techniques. This

information also played a vital role in our predictions of forecasting growth stunts and

rapid expansions.

To find the cost of equity we used an alternative method which resulted

in10.44% for both before and after taxes. We then calculated the cost of debt to be

4.66% for both before and after taxes. In secession we concluded the weighted

average cost of capital before tax to be 7.05% and after tax to be 5.99%.

Valuations

The purpose of an equity valuation is to value a company’s stock price,

determining if it is under, over, or fairly valued. By using financial ratios, accounting

skills and an exquisite knowledge of the industry to be possibly invested in, potential

stockholders can help better their chances of profitable investments.

After valuing Southwest Airlines through the use of intrinsic valuation models, we

determined there were three particular models that were appropriate for the valuation

of the company. The models used were; the residual income model, the long-term

residual income, and the abnormal earnings growth model. Through the use of these

models we were able to value Southwest’s share price with the respective models as

follows; $8.44, $9.45, and $8.56. Each of Southwest’s share prices was determined

using a cost of equity of 10.44% and a 0% perpetuity growth rate. Comparing the

values of the intrinsic valuations models to the June 1, 2008 share price of $13.06 it can

be concluded that Southwest Airlines is overvalued, and the option is to sell.

10

Southwest Airlines and the Airlines Industry

Southwest Airlines (LUV) is a Dallas, Texas based airlines. The airline was

established in 1971by Rollin King and Herb Kelleher with the notion of cheap, no-frills

flights. The airlines had originally three destinations; San Antonio, Houston, and Dallas.

Southwest’s objective market was and still is medium to high frequency business

travelers (grabers.com). Southwest operates in the national category of the Airline

industry, which means it only flies nationally not internationally. Southwest’s home

base is still Dallas, Texas; it has not changed from the 1970’s. Southwest flies to 64

destinations in 32 states and has a fleet of 532 planes, 95 of which are leased.

Competitors of Southwest are American Airlines, Continental, and JetBlue. The

rivalry amongst firms is high for this industry. Firms are competing for brand image

whether it be cheaper flights, state of the art planes, or faster check-in time. The airline

industry has a very high level of competition between existing firms with low or no

switching costs for the customer. Threat of new entrants is low for this industry

because of large economies of scale with low or no exit barriers. Price drives customers

in this industry, this leads to high threat of substitute products. The firms try to create

competitive advantages over one another in order to be number one.

Southwest has had to focus on numerous tactics in order to stay a competitor in

this industry. They looked at their customer base, which is mostly made up of one day

business travelers, and thought what was most important to them. After giving it some

thought, Southwest came to realize that convenience is a very important factor to its

travelers, so they felt it was important to implement that in their airports and on their

website. Now a customer can check-in online so they can avoid the checking lines, pay

a little extra and get seated first on the plane, or even charge their mp3 player while

waiting to board their plane. It also helps that Southwest puts a huge of emphases on

price, which helps them stay ahead of the curve. Southwest is trying to build a

11

competitive advantage so it can distinguish itself easily from other firms in the airline

industry.

Company Overview

Southwest Airlines (LUV) is a competitor in the National airline industry. “Based

on the most recent data available from the U.S. Department of Transportation (“DOT”),

Southwest is the largest air carrier in the United States, as measured by the number of

originating passengers boarded and the number of scheduled domestic departures

(Southwest 10K).” Southwest is a Texas-Based airline that was developed in the late

1960’s on the grounds of offering customers discounted flights. Rollin King and Herb

Kelleher founded Southwest Airlines, the airline had originally been named Air

Southwest but changed shortly after in 1970. In the early days, the airline only flew to

and from three cities in Texas; Dallas, Houston, and San Antonio. The airline offered a

no frill, short flight to three destinations, this business approach has helped with the

continuing growth of Southwest. Today, Southwest flies to and from 64 cities in 32

states, with a fleet size of 532. In 2007 Southwest has recommenced service to and

from San Francisco. However, Southwest has recently slowed their growth plan in 2008

because of the rising fuel costs.

(www.wikinvest.com/stock/southwest_airlines)

12

The total sales growth of southwest for 2007 was 8.5% (AOL Finance).

(In Thousands) 2002 2003 2004 2005 2006 2007

Assets

8,954.00

9,878.00

11,337.00

14,218.00

13,460.00

16,772.00

Sales

5,522.00

5,937.00

6,530.00

7,584.00

9,086.00

9,816.00

Stock Price

13.90

16.14

16.28

16.43

15.31

12.20

Southwest competes with many other companies in the airline industry. Competitors

with southwest include American Airlines (AMR), Continental (CAL), and JetBlue (JBLU).

Southwest competes more directly with JetBlue because both airlines are more regional

than international. Both are similar when it comes to flight destinations.

13

Industry Overview

The airline industry changed the way people traveled the world. The airline industry is

made up of four different types of categories. These categories include

• International - 130+ seat planes that have the ability to take passengers just

about anywhere in the world. Companies in this category typically have annual

revenue of $1 billion or more.

• National - Usually these airlines seat 100-150 people and have revenues

between $100 million and $1 billion.

• Regional - Companies with revenues less than $100 million that focus on short-

haul flights.

• Cargo - These are airlines whose main purpose is to transport goods

This industry exists in a highly competitive market (Investopedia.com). The airline

industry is also affected by other factors. These factors can range from bad weather to

the rising costs of fuel, to government regulations on safety or noise pollution.

Southwest competes for the most part in the national category of the airline industry.

The international category would classify airlines similar to American Airlines and United

Airlines. The regional category would classify airlines similar to JetBlue. The cargo

category would classify companies similar to FedEx and UPS. All of these categories that

classify the airline industry are highly competitive with themselves and with each other.

They each intertwine with each other in way or another.

14

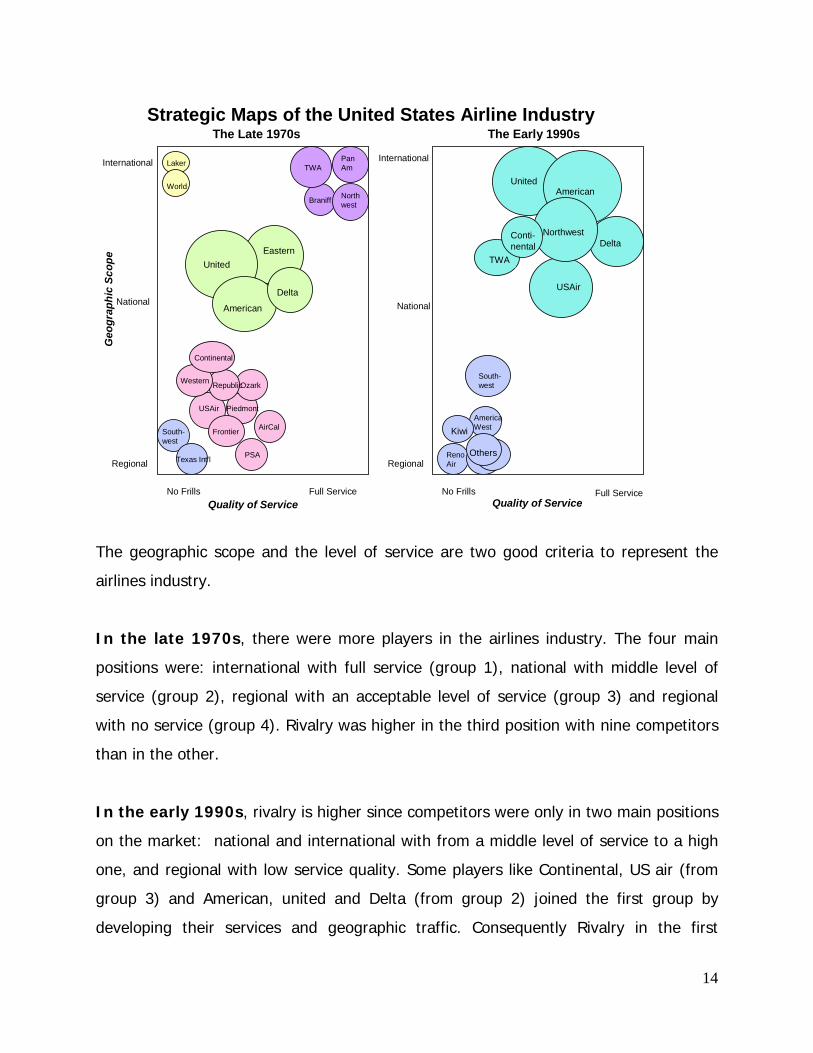

The geographic scope and the level of service are two good criteria to represent the

airlines industry.

In the late 1970s, there were more players in the airlines industry. The four main

positions were: international with full service (group 1), national with middle level of

service (group 2), regional with an acceptable level of service (group 3) and regional

with no service (group 4). Rivalry was higher in the third position with nine competitors

than in the other.

In the early 1990s, rivalry is higher since competitors were only in two main positions

on the market: national and international with from a middle level of service to a high

one, and regional with low service quality. Some players like Continental, US air (from

group 3) and American, united and Delta (from group 2) joined the first group by

developing their services and geographic traffic. Consequently Rivalry in the first

Strategic Maps of the United States Airline Industry

Braniff

TWA

EasternUnited

American

Delta

Western RepublicOzark

USAir Piedmont

Frontier AirCal

PSA

South-west

Texas Int’l

United

South-west

AmericaWest

International International

National National

Regional Regional

No Frills No FrillsFull Service Full ServiceQuality of Service Quality of Service

Geo

grap

hic

Scop

e

The Late 1970s The Early 1990s

RenoAir

Continental

PanAm

Northwest

Laker

World American

TWA

Delta

USAir

NorthwestConti-nental

Kiwi

Others

15

position became higher with a total of seven players. Some players disappeared from

the 70s to the 90s. Western airlines was purchased by Delta Air Lines in 1986 and after

the merger, Delta released the name Western airlines. Another example is Texas Air

Corporation which had been spilt up with parts sold to Scandinavian Airlines System,

Ross Perot's EDS (Electronic Data Systems), and an Air Canada-led investment group.

New players also, like Kiwi travel international Airlines, came in the industry. Rivalry in

the second group in the 90s became also very strong. Cost leadership was the main

strategy for those firms that provided short air travels. Southwest airlines tried to create

a gap with a more expanded network geographically and a higher level of service than

the group 2 competitors. It was this same strategy that made the firm able to join the

group 2 in the early 90s. In fact, differences in management styles, skills set and

strategic perspectives create advantages and disadvantages. Southwest airlines has

become phenomenally successful and an industry leader. For year q it went virtually

unchallenged. But Southwest costs have crept up, and now start up airlines such as jet

blue are challenging the industry leader with their own low cost strategies. This is

indicative of the competitive dynamic cycle.

16

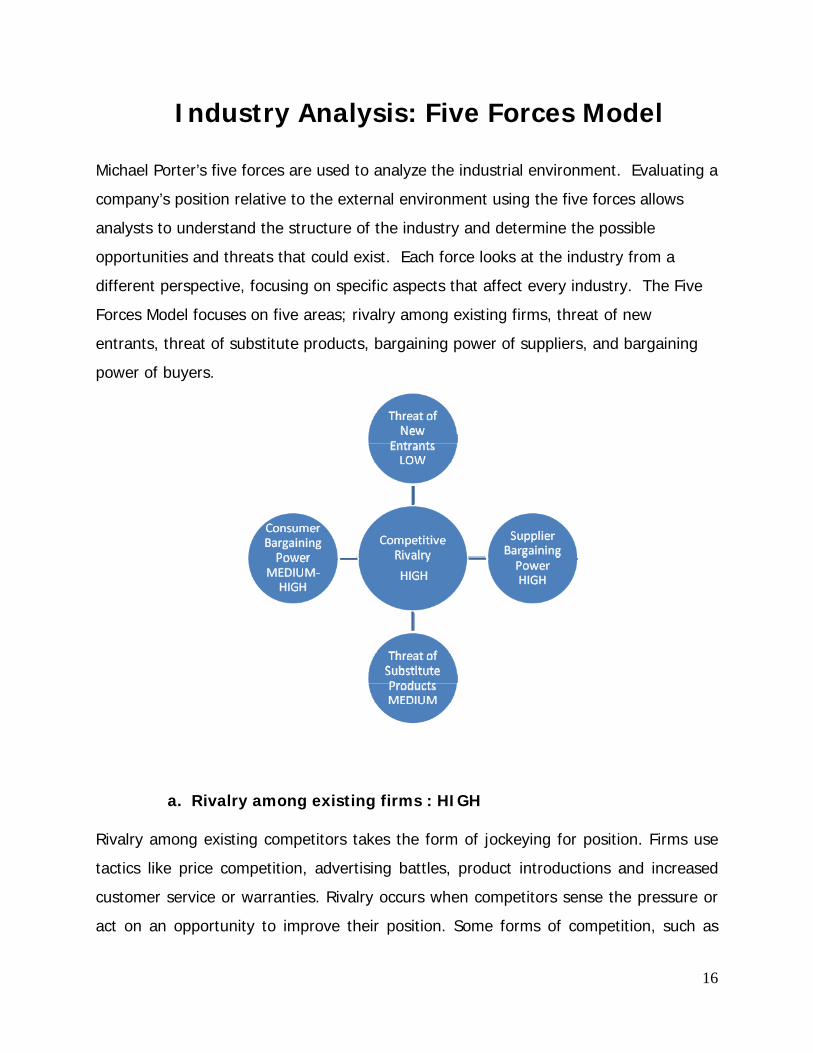

Industry Analysis: Five Forces Model Michael Porter’s five forces are used to analyze the industrial environment. Evaluating a

company’s position relative to the external environment using the five forces allows

analysts to understand the structure of the industry and determine the possible

opportunities and threats that could exist. Each force looks at the industry from a

different perspective, focusing on specific aspects that affect every industry. The Five

Forces Model focuses on five areas; rivalry among existing firms, threat of new

entrants, threat of substitute products, bargaining power of suppliers, and bargaining

power of buyers.

a. Rivalry among existing firms : HIGH Rivalry among existing competitors takes the form of jockeying for position. Firms use

tactics like price competition, advertising battles, product introductions and increased

customer service or warranties. Rivalry occurs when competitors sense the pressure or

act on an opportunity to improve their position. Some forms of competition, such as

17

price competition, are typically highly destabilizing and are likely to erode the average

level of profitability in an industry. Rivals easily match price cuts, an action that lowers

profits for all firms. On the other hand, advertising battles expand overall demand or

enhance the level of profit differentiation for the benefit of all firms in the industry.

The US airline industry is a highly competitive and sensitive market. Recently the

merger between Delta and Northwest airlines has heightened the level of

competition in the fight for market share. Competition in the industry has also been

altered by the creation of larger airplanes, a slowing economy and the demand for

cheaper airfare, as well as developing technology, including onboard Wi-Fi internet

access (WSJ 2008). Competitive rivalry is affected by many different factors, these

include: Industry growth, level of concentration, differentiation, switching costs,

economies of scale, fixed and variable costs, excess capacity, and exit barriers.

Industry Growth

The level of industry growth determines whether or not a firm must seek to obtain

market share or not. The airline industry in the United States has grown to become

one of the major modes of transportation for many Americans. According to the

Bureau of Transportation Statistics, there were 735 million passengers on US

domestic flights, up 11.4% from the previous year. With such a large increase in

the number of passengers each year revenues have also increased.

18

The chart above shows a constant growth in sales revenues for the past five years.

Each year has been greater than the next, which is a good indicator of growth

within the industry. While the number of flights is increasing, the relative growth in

sales has not increased at such a strong rate.

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2003 2004 2005 2006 2007

Airline Industry Operating Revenue (millions)

0

2

4

6

8

10

12

2003 2004 2005 2006 2007

Industry Sales Growth (%)

19

Industry revenues have increased by an average of 7.67% each year for the last 5

years. While each company’s increase varies from year to year the average rate of

increase has started to slow. However the overall growth rates are still strong and

there has been no sign that sales will start declining. Although revenues increase

over recent years so have expenses.

Expenses across the industry over the past 4 years have increased by an average

9.9% per year. With operating expenses increasing at the same rate as operating

revenues creating increased profits is made difficult. As expenses increase the

industry looks toward cost cutting methods in order to increase profit potential.

With jet fuel prices on the rise expenses for airlines are increasing drastically. Just

this year the price of jet fuel has increased from $850 per metric ton to $1300.

With such a large increase in price jet fuel is the second largest expense for most

airline companies, consisting of an average 34% of all expenses (WSJ 2008).

With high ticket prices and a dismal economy, airliners are looking at alternative

ways to cut cost rather than just making the consumer pay for the difference.

20

Recently UAL announced that it will be cutting 70 jetliners from its fleet in lou of

the jet fuel price increase. UAL also announced that it would be cutting routes that

it deemed no longer profitable, a strategy that AMR Corp. already acted upon (WSJ

2008).

With expenses so high, losses in the airline industry are expected to hit $2.3 billion

(Dallas Morning News 2008). Such loses aren’t uncharacteristic in the airline

industry.

In the case of most airlines profits have occurred with similar frequency to losses.

Such an industry could only be described as stagnant. The graph above shows an

income curve that is virtually horizontal, meaning that the level of growth in the

industry is very small. With the exception of Southwest Airlines, every airline

company has reported a loss at year end in a least one of the past 5 years. With

such unstable earnings it makes it hard for an industry to strive. Such factor lead to

price wars, these have been evident in the airline industry for quite some time.

Recent mergers are evidence that the industry is stagnant also, because they

21

intend to take market share, the only way to grow in such an industry.

Concentration

Concentration within an industry compares the number of firms in an industry as

well as their relative size to the market. The concentration level in the Domestic

airline industry is reasonably low; market share is divided by many different

companies, neither having any considerable control over the majority. The result is

high price competition because there are a large number of competitors all

competing for the same customers.

The information above reveals that there are four dominant companies in the

industry; Delta and Northwest (after merger), AMR (American), Southwest, and

UAL (United). These four companies only control about 56% of the market, which

only goes to show how fragmented the industry really is. Another indicator of the

22

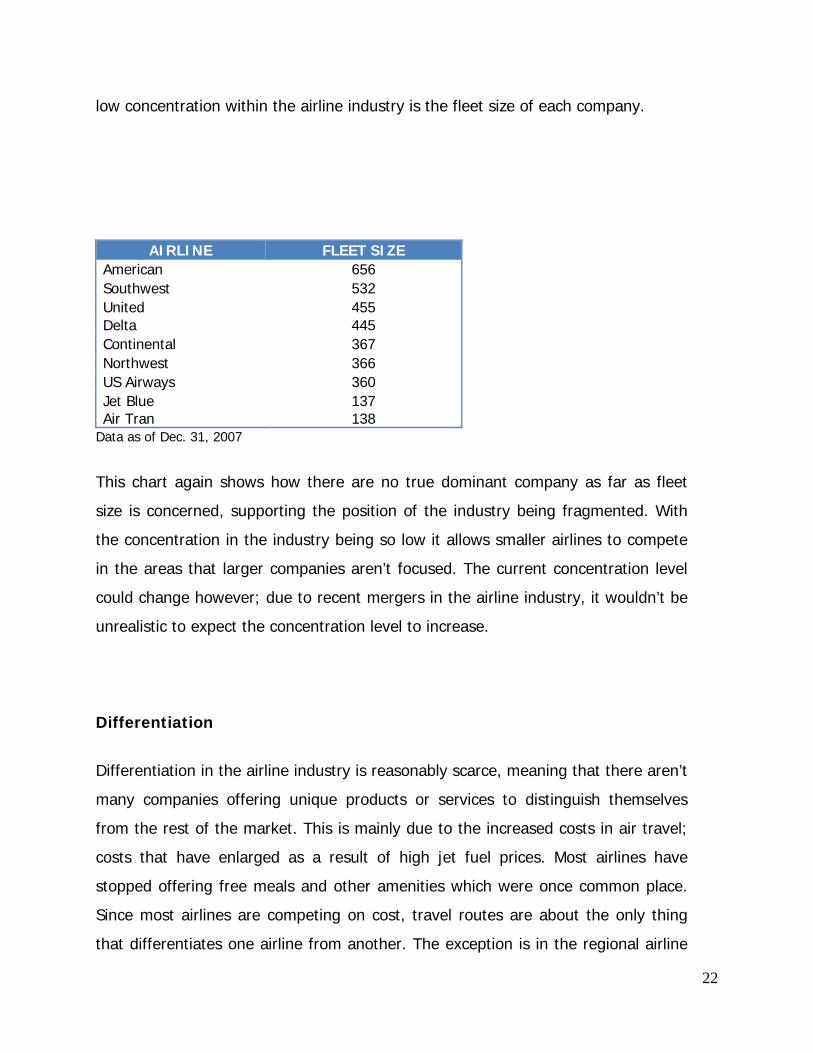

low concentration within the airline industry is the fleet size of each company.

AIRLINE FLEET SIZEAmerican 656Southwest 532United 455Delta 445Continental 367Northwest 366US Airways 360Jet Blue Air Tran

137138

Data as of Dec. 31, 2007

This chart again shows how there are no true dominant company as far as fleet

size is concerned, supporting the position of the industry being fragmented. With

the concentration in the industry being so low it allows smaller airlines to compete

in the areas that larger companies aren’t focused. The current concentration level

could change however; due to recent mergers in the airline industry, it wouldn’t be

unrealistic to expect the concentration level to increase.

Differentiation

Differentiation in the airline industry is reasonably scarce, meaning that there aren’t

many companies offering unique products or services to distinguish themselves

from the rest of the market. This is mainly due to the increased costs in air travel;

costs that have enlarged as a result of high jet fuel prices. Most airlines have

stopped offering free meals and other amenities which were once common place.

Since most airlines are competing on cost, travel routes are about the only thing

that differentiates one airline from another. The exception is in the regional airline

23

industry: Many of these airlines provide unique travel routes not offered by some of

the major airlines. Other examples of the differentiation offered by some of these

airlines include: First come first served seating, offered by Southwest, Jet Blue

offers personal entertainment and data systems for every passenger, and Frontier

Airlines goes one step beyond by offering satellite TV. One form of differentiation

which is now almost an industry standard is the offering of rewards for

accumulated miles flown on a certain airline, as well as the purchase of items on a

credit card affiliated by an airline. Overall the airline industry competes in an almost

pure cost control industry with a very minimal level of differentiation.

Switching Costs

Switching cost refers to the degree of ease a company can produce a different

product using the current resources of the company. The cost of one Boeing 737

can range from $50-85 million, making switching costs in the airline industry

incredibly high. Another factor making the switching cost in the airline industry so

high, is that it is almost impossible to use an airplane for anything else than flying

passengers. The only exception would be switching into the cargo freight industry;

however most commercial airlines already transport cargo and is factored into their

operating revenues. Therefore switching costs are barely diminished. This means

that companies within the airline industry are “stuck” with high competitive

pressures.

Economies of Scale

Economies of scale result due to the relative size of a company and its ability to

purchase large amounts of product at cheaper prices, creating an advantage over

smaller companies. Companies with large economies of scale should be able to sell

their commodity at a lower price than any competitor. As discussed in the

concentration section, there isn’t any single dominant market share holder and

therefore it would make it hard for any large economies of scale to exist in the

24

industry. Also the fact that there are so many airlines with a large number of

planes, that it doesn’t give any one airline a great advantage in terms of economies

of scale.

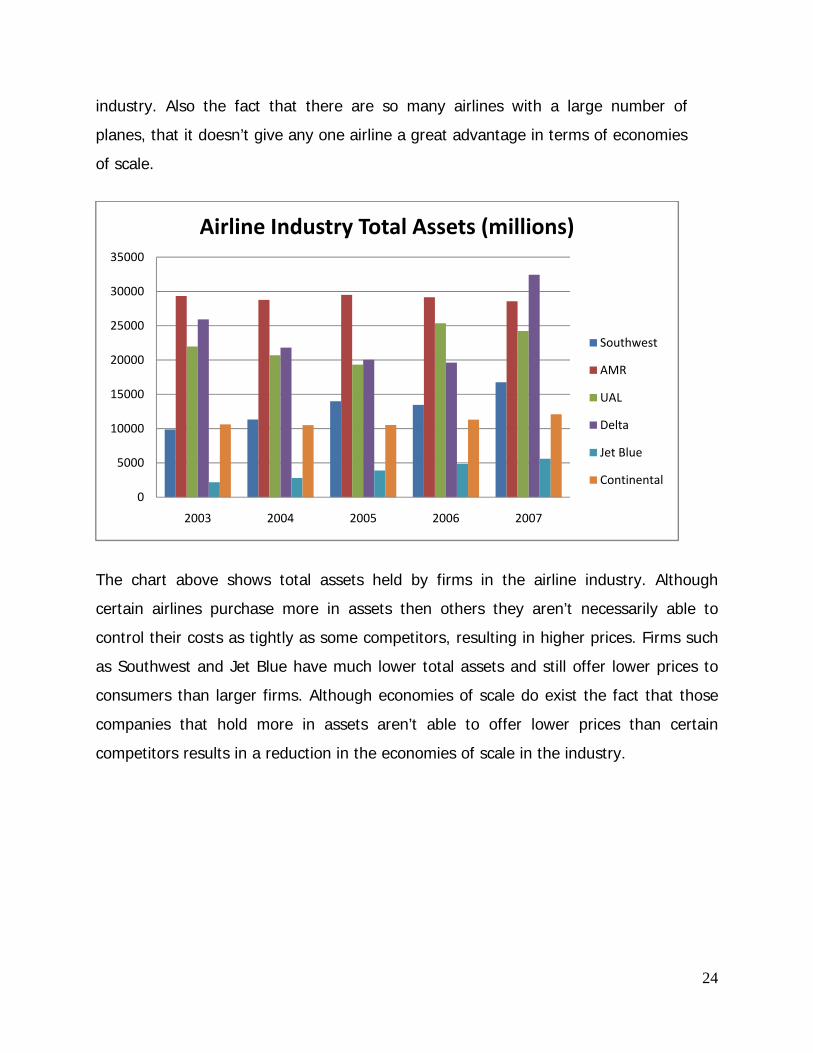

The chart above shows total assets held by firms in the airline industry. Although

certain airlines purchase more in assets then others they aren’t necessarily able to

control their costs as tightly as some competitors, resulting in higher prices. Firms such

as Southwest and Jet Blue have much lower total assets and still offer lower prices to

consumers than larger firms. Although economies of scale do exist the fact that those

companies that hold more in assets aren’t able to offer lower prices than certain

competitors results in a reduction in the economies of scale in the industry.

0

5000

10000

15000

20000

25000

30000

35000

2003 2004 2005 2006 2007

Airline Industry Total Assets (millions)

Southwest

AMR

UAL

Delta

Jet Blue

Continental

25

Fixed-Variable Costs

The relation between fixed cost and variable cost defines how a firm goes about pricing

items in relation to competition. The higher the fixed-variable cost ratio, the higher the

level of price competition. Because airlines fixed costs are so great compared to most

other industries, each company must compete at a higher level to gain customers in

order to pay off its sunk costs with the goal of making a profit

The graph above illustrates Southwest’s fixed-variable cost relationship, a ratio which is

quite consistent across the industry. Fixed cost in the airline industry are high mainly

because the costs of owning and/or renting aircrafts are extremely high. Even if the

aircraft is leased, contracts are often for 15 to 20 years, resulting in an expense

whether the planes are flying or not. Recent surges in the cost of jet fuel as well as

increased maintenance costs have led to increasing variable costs. With already high

fixed costs, and ever increasing variable costs, competition between airlines becomes

increasingly important.

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

2003 2004 2005 2006 2007

Axis Title

Southwest's Operating Expenses per ASM (¢)

Variable Costs

Fixed Costs

26

Excess Capacity

Excess capacity relates to the rule of supply and demand. With excess capacity, supply

is greater than demand and in order to reach equilibrium, prices must decrease, thus

filling capacity. Excess capacity in the airline industry is a result in high prices charged

by companies battling the increased fuel costs, as well as the inability of airlines to fill

their planes do to high route frequency.

The chart above shows the average capacity load function for each airline over five

years. Capacity load function is equal to the revenue passenger miles (RPM) divided by

available seat miles (ASM); this function provides the average percentage capacity of

operation for each airline. Filling excess capacity is made hard in the airline industry

because each plane is limited to a certain size and number of passengers. The

relatively similar excess capacity that exists across the industry is evident to the high

degree of price competition that exists, in companies both large and small.

71.75 74.57 78 78.85 79.12

28.25 25.43 22 21.15 20.88

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2006 2007

Airline Industry Capcity Load Factor (%)

Excess Capacity

Occupancy Load

27

Exit Barriers

Exit barriers refer to the degree of difficulty a firm faces when trying to exit an industry.

Barriers are increased when the assets owned by the firm are costly and/or specialized.

Exit barriers in the airline industry are extremely high. Airplanes are highly specialized

pieces of equipment and cannot be sold easily. Due to the tremendous exit barriers of

the airline industry companies are forced to become even more competitive in order to

survive.

Conclusion

The rate of rivalry amongst existing firms in the airline industry is high, creating an

industry that is extremely competitive and sensitive. Most companies with the

exception of only a few share very similar changes in profit. These similarities are due

to a very low growth rate, low concentration, very little differentiation within the

industry, high switching costs, moderate economies of scale, high fixed costs, and high

exit barriers. High rivalry keeps the airlines industry dynamic and creates pressure on all

firms to improve and innovate.

b. Threat of new Entrants: LOW

The threat of new entrants refers to the possibility that the profits of the established

firms in the airline industry may be eroded by new competitors. The extent of the

threats depends upon existing barriers to entry and the combined reactions from

existing competitors. The more new airlines that enter the market, the more saturated

it becomes for everyone.

28

Deregulation of the airline industry has eased the establishment of new airlines such as

low cost carriers. The increased use of the internet has made it easier for new

companies to find distribution channels and to sell their tickets over the Internet.

Upstart Jet Blue and Southwest Airlines were among the few to earn a profit in recent

years. However, there are several barriers to potential entrants.

Hubs and landing slots

Hubs and landing slots are a barrier to entry in the airline industry. Researches, from

the General Accounting Office (GAO), show that ticket prices at airports dominated by a

single airline are higher than at more competitive airports. Opportunities for establishing

new service continue to be limited in some airports by restrictive gate leases. These

leases permit an airline exclusive right to use most of an airport’s gates over a long

period of time, commonly 20 years. To gain access to an airport in which most gates

are exclusively leased, a company must sublet gates from the incumbent airlines, often

at none preferred times and at a higher cost than the incumbent. This system leads to a

low threat of new entrants in the airline industry.

Federal restrictions

Federal restrictions prevent foreign ownership of US airlines and block foreign airlines

from offering connecting service between US cities.

Economies of scale

Perhaps the most important barrier to entry is economies of scale. If a firm’s minimum

efficient scale is relatively large compared to industry output, then only a few firms are

needed to satisfy industry demand. To compete with existing airlines companies, a new

entrant must sell enough air tickets to reach a competitive scale of operation.

29

The high cost of entry in a competitive industry

The total investment needed to reach the minimum efficient size is gigantic. High start

up costs and established brand names create substantial barriers to entry. The fact that

the new carriers don’t have a well known name and don’t have any long term

relationships with companies which can offer them loyal business consumers could

make it hard for the new actors to grow. The prospect of such losses discourages many

potential entrants.

Another barrier to entry would be the intense competition a starter company would

face. With most potential customers already loyal to their airline of their choice,

whether through lower prices, reward programs, or differentiated quality, it would be

almost impossible for a new company to come in and find a niche that could steal these

customers from the airlines of choice. For example, the biggest airlines fly more

national and international routes, so they offer more opportunities both to accumulate

frequent flyer miles and to use them. Thus, the biggest airlines have the most attractive

programs.

Thus, operating limits in the form of slot controls, scarce hubs and gates, and

restrictions against foreign competition create barriers to entry in the airline industry.

Likewise, several marketing strategies, including special incentives for travel agents and

frequent flyer programs, give an advantage to the established carriers. These strategies

continue to deter new airlines from entering the market. Seven airlines account for

over 80 percent of all passenger service; the threat of new entrants is consequently

low.

30

c. Threat Of Substitutes : MEDIUM

All firms within an industry compete with industries producing substitute products and

services. Substitutes limit the potential returns of an industry by placing a ceiling on the

prices that firms in that industry can profitably charge. The more attractive the

price/performance ratio of substitute products, the tighter the lid on an industry’s

profits. The existence of close substitute products increases the propensity of customers

to switch to alternatives in response to price increases (high elasticity of demand).

Substitutes

Travel services, like train and private transportation (cars), are substitutes because they

perform the same function. People who need to travel can choose between those

different travel means. As digital technology has improved and wireless and other forms

of telecommunication have become more efficient, new substitutes have become a

viable substitute for business travel for many executives. Videoconferencing and

groupware allow two or more locations to interact simultaneously via two way video

and audio transmissions. There are consequently two main types of substites,

transportation providers and high technology telecommunication products.

Relative price and performance

Teleconferencing can be a very important threat. It can save both time and money and

affect the number of business travellers. The rate of improvement in the price-

performance relationship of the substitute product is high.

Trains are not a good substitute for airlines because they don’t provide enough routes

in the US to provide a good transportation system. However, with airports and

highways more congested than ever, there are now plenty of plans for next-generation

passenger rail, from upgrading existing lines to building super-high tech tracks. Given

31

the expense, the technical challenges and the political complexity of these projects,

trains have the potential to substitute airplanes in at least a decade.

popularmechanics.com

In this map, we can see the proposed North American High Speed Train Project. The

threat to the airlines here yet but it will be soon when it comes to travel over medium

distances. Regional airlines would be the first affected because soon most of the train

routes would provide fast transportation between cities adjoining states very fast,

particularly on the east coast. The threat looks lower when it comes to large distances

in the US. Even if it would be possible to travel by train from Boston to Houston, we

don’t imagine a lot of people doing that. Airplanes will be always more time and money

efficient. Moreover, the major connections between the east and west coasts would be

still via airlines. On the map, we can’t see any routes crossing the entire country.

As for trains in more than a decade, cars are already a reliable substitute for regional

airplanes, when it comes to short distances. In an attempt to provide a long term

perspective in this report, we will assume that the project mapped above will be

implemented and consequently we will compare the time and energy required for all

travel options within a 400 mile trip. A 400 mile trip is appropriate to evaluate the

highest threat of substitutes, which is, as we said before, regional airlines. A 400 mile

trip corresponds to the distance from Boston to Baltimore.

High-Speed Rail Amtrak (Diesel)Travel time: 2 hours, 54 minutes (maglev); 4 hours, 35 minutes (steel-wheel)

Travel time: 7 hours, 5 minutesEnergy used per passenger mile: 2709

32

Energy used per passenger mile: 1180 Btu* (maglev); 1200 Btu (steel-wheel) CO2 emissions per passenger mile: 0.47 pounds (maglev); 0.48 pounds (steel-wheel)

Btu CO2 emissions per passenger mile: 0.46 pounds

Airplane CarTravel time: 2 hours, 20 minutes (including 1-hour check-in time) Energy used per passenger mile: 3264 Btu CO2 emissions per passenger mile: 1.06 pounds

Travel time: 7 hours, 6 minutesEnergy used per passenger mile: 3445 Btu CO2 emissions per passenger mile: 0.77 pounds

*Btu stands for British thermal unit. One gal. of gasoline yields about 114,000 Btu.

Trains are a significant threat for airplanes because there is only a 30 minute time

difference between an airplane and a maglev (a train that suspends, guides, and

propels vehicles, using electromagnetic force). The energy used per passenger mile is

lower for trains which represents therefore a lower cost for trains than for airplanes.

Contrary to airplanes or cars, high-speed trains draw power from the electrical grid,

which is fueled primarily by domestically produced energy sources, such as coal.

However, it seems that cars are not a key threat due to the time difference. It is

imperative that airlines take into account the cost of automobile travel in order to fix

their prices and discourage people from driving. Furthermore, with oil cracking $130 a

barrel, driving has become very expensive.

Buyers’ willingness to switch

Air transport is traditionally very reliable for people. But it’s apparent that, in some

areas, this system is reaching capacity. For example, for short distances, air travellers

are spending more time in security lines and waiting on the runway before they ever

get into the air. According to the Department of Transportation, 2007 was the worst

year in the past decade for airport delays, with 25 percent of flights arriving late.

According to these facts, buyers’ propensity to substitute could increase significantly,

particularly with the emergence of reliable train routes. Key criteria for customers are

the amount of money people are willing to spend to travel. As a consequence, such

substitutes are easy to counter by determining airline ticket prices according to the

33

equivalent price of the substitute product. For the same amount of money, people

prefer to fly in general. But, since trains will be cheaper and more environmentally

friendly, people may adopt the train instead of the car. They will value the fact that

they don’t need to wait for planes or for luggage, they don’t have to go through the

security or they can still use their cell phones.

However, it seems that customers perceive a higher level of service for airlines and

travel more comfortably in a plane than in a car or a train. Differentiation is also high

when we consider the highest number of routes for airlines.

Currently, the threat of substitutes for airlines is medium. Advantages like speed,

service, and routes provided by planes seem to be considerable compared to

substitutes. However, the relative price performance of trains could be a major threat in

a decade for regional airlines. Airlines need to define themselves as transportation

providers in order to avoid marketing myopia.

d. Bargaining Power of Customers : MEDIUM / HIGH

The power of buyers is the impact that customers have on a producing industry. This is

how much pressure customers can place on business. Customers threaten an industry

by forcing down prices, bargaining for higher quality or more services, and playing

competitors against each other. These actions erode industry profitability.

The largest proportion of revenue is derived from regular and business passengers. For

this reason, it is important that one takes consumer and business confidence into

account on top of the regular factors that one should consider. Main customers in the

airline industry are: Travel Agents, Business Travellers, Federal Government, Pleasure

Travellers, Charter Service, the US military.

34

Switching costs.

It’s very easy for customers to switch to another product and company because they

are extremely price sensitive. For example, travelers will choose to drive if they consider

it cheaper than flying. Students, for example almost always adopt this kind of behavior.

Some customers, in general, can do without flying for a period of time if they think that

prices are too high. In times of economic uncertainty or sharp decline in consumer

confidence, one can expect the number of leisure travelers to decline.

Even business travellers become more sensitive to prices, according on the Business

Travel News’ Corporate Travel 100 Report. This year, 22 percent of more than 60

companies that spend a total of more than $44 million in U.S.-booked air travel said

they are seeking air savings by becoming more restrictive in business class policies. Last

year, 28 percent did so. Moreover, these companies don’t have a preference in a

particular airline. They will choose the best price.

However, in some case, consumers value speed more than saving. For example,

Business travellers can’t waste time driving when they can fly. Business travellers are

important to airlines because they are more likely to travel several times throughout the

year and they still tend to purchase the upgraded services that have higher margins for

the airline.

Ticket Price

Also, buyers tend to buy a round trip ticket only, so they can’t negotiate discount for

their purchase volume. Fares are going up and will continue to grow. Average published

airfares next year will rise 6 to 10 percent from 2007 levels, said Bob Brindley, vice

president for the Americas for BCD Travel's consulting subsidiary Advito. However, the

demand should remain at least stable since the airlines tend to give customers some

discounts. Phil Dunphy. director of global travel, said: "If the airlines raise fares 5

percent, they'll give you back 3 percent, but they still net that additional 2

35

percent.”(www.btnonline.com) Obviously, discounts may not be sufficient to recover

airline’s previous price but this practice would not decrease demand fundamentally.

Also, airlines product is highly perishable. Once an airplane takes off, the empty seats

lose all value, so airlines need to do what they can to fill them. That means that airlines

companies need to decrease ticket prices daily depending up how full the flights are.

Number of buyers

As American Airlines senior vice president of global sales David Cush said, travel

demand and corporate spending remain robust this year: "I think less about what

people are saying and more about what they're doing. What they're doing is continuing

to travel at a very strong level," he said. "Our July figures for corporate travel show no

decrease in demand there and forward-looking bookings look very strong, so everything

we see points to a robust travel market." It seems that the airlines industry would have

to wait to see "the fallout from some of this financial market turmoil," but international

travel remains strong. Indeed companies have globalized, and they can't just stop

travelling internationally. International demand is going to remain strong. Consequently,

it appears that individual buyers don’t have a lot of power.

Differentiation

Customers appreciate services and airlines companies have to improve them as much

as they can. Indicators that are used in survey such as the “BTN annual airline survey

2007” are flexibility in negotiating pricing; flexibility in negotiating services and

amenities; availability of timely; accurate contract performance data; complaint problem

resolution; quality of airline communication; value of relationships with managers; sales

representatives; quality of customer service; and overall price value. However, it is

quite hard to compete on service. Consumers realize that there is now virtually no

differentiation between airlines in terms of product, even in the upper travel classes. Air

36

travel is mostly standard and there is little opportunity for sustainable differentiation. Is

the seat in one airline more comfortable than another? Probably not, unless you are

analyzing a luxury liner like the Concord Jet.

Airlines try to differentiate travel but the problem is that there is simply not enough

product differentiation to go around. Product packages, like air ticket and hotel or car,

used to work; they no longer always do because they can more often be copied or

improved by competitors at an increasing speed. For example, in the mid 1980s, AMR (

American Airlines) introduced AAvantage. This differentiating concept was a great

success until most other competitors realized that they could do likewise. As a

differentiator, the effective life-cycle of frequent flyer miles/points and their

differentiating power were much shorter than the airlines originally anticipated.

Access to information

Another key element of high buyer power is that buyers have access to information.

They can easily compare online hours, prices, connections to decide which flight they

want and therefore the company they want to choose. Tickets can be purchased

through common online venues like Orbitz and Travelocity or are issued directly by

airlines over the phone or through the company’s website. A minority are booked

through travel agents. In the Economist, published June 14th 2007, we find that: “The

web has made it possible for passengers to be their own travel agents by comparing

fares and schedules and booking flights—and at prices much lower than a decade ago.”

The access to information increase buyers’ power.

In conclusion, buyers’ power is medium/high due to low switching costs, price

sensitivity, a standard product, information access, a large number of buyers and low

volume purchases.

37

e. Bargaining Power of Suppliers : HIGH The bargaining power of suppliers is how much pressure suppliers can place on a

business. Suppliers can exert bargaining power over participants in an industry by

threatening to raise prices or reduce quality of purchased goods and services. If one

supplier has a large enough impact to affect a company's margins and volumes, then

they hold substantial power.

The airline industry is extremely sensitive to costs such as fuel, labor and borrowing

costs. The airline industry’s main suppliers are aircraft manufacturers, aircraft leasing

companies, labor unions, food service companies, fuel companies, airports, the federal

Aviation Administration (FAA), hotels.

Aircraft makers

The airline supply business is mainly dominated by Boeing and Airbus. For this reason,

there isn't a lot of cutthroat competition among suppliers. As a consequence aircraft

makers are powerful. Even if there is an intensive war between Airbus and Boeing (cf:

graph) gain a higher percentage of the world market, prices are comparable for similar

planes, which allow no breathing space for airlines. Furthermore, aircraft makers’ power

could be higher in the future because they won’t offer identical aircrafts. Indeed,

Boeing’s strategy now is to focus more on small aircrafts for regional lines whereas

Airbus’s strategy is more oriented towards big international planes. The negotiation with

suppliers would be harder to airlines companies. Suppliers’ products are an important

input to the buyers business. Airlines company need to renew their fleet regularly and

Boeing and Airbus are the only providers. Without sufficient planes, an airlines company

loses power. Plane investments are critical and airlines firms don’t have any substitute

products to offer.

The only element that tends to reduce supplier power is that the airlines industry is an

important customer and that the rivalry between Boeing and Airbus is very high.

38

Labor supply power (labor unions)

The initial changes in the airline industry created by the Airline Deregulation Act of 1978

seem to have increased union bargaining power. Airline unions have considerable strike

threat power, but are constrained by the financial health of carriers. Since airline

deregulation, compensation has waxed and waned in response to the industry’s

economic environment. Airline workers capture sizable rents following good times and

provide concessions following lean times. Evidence from the CPS for 1995-2006 shows

that wage premiums for airline industry workers remain, particularly for pilots, with

existing premiums almost entirely a union phenomenon. Because unions retain

bargaining power at the major carriers, wages are likely to head upward as carriers’

financial health returns. Such wage levels may or may not be sustainable in the

inevitable next downturn.

Fuel suppliers

Fuel suppliers are very powerful. Indeed, some of the major players in the airline

industry attribute 10-20% of their costs to jet fuel. Fuel prices have been known to

fluctuate 5-10% or more on a monthly basis, so paying close attention to these costs is

crucial. That’s why airlines companies had been interested in reducing the volatility of

oil prices. For example, Southwest Airlines has a long-time program to hedge fuel

prices. It has purchased fuel options years in advance to smooth out fluctuations in fuel

costs. The use of these hedges helped airlines maintain their profitability during oil

shocks like the Iraq War and Hurricane Katrina. However, the rapid increase in fuel

prices this year has a strong impact on airlines profits. Record jet-fuel prices are making

50-seat regional jets unprofitable to fly. For example, with fuel prices at $3.15 a gallon,

the Embraer ERJ-145’s total operating cost has increased 39%, making it, a money-

loser on its routes.

39

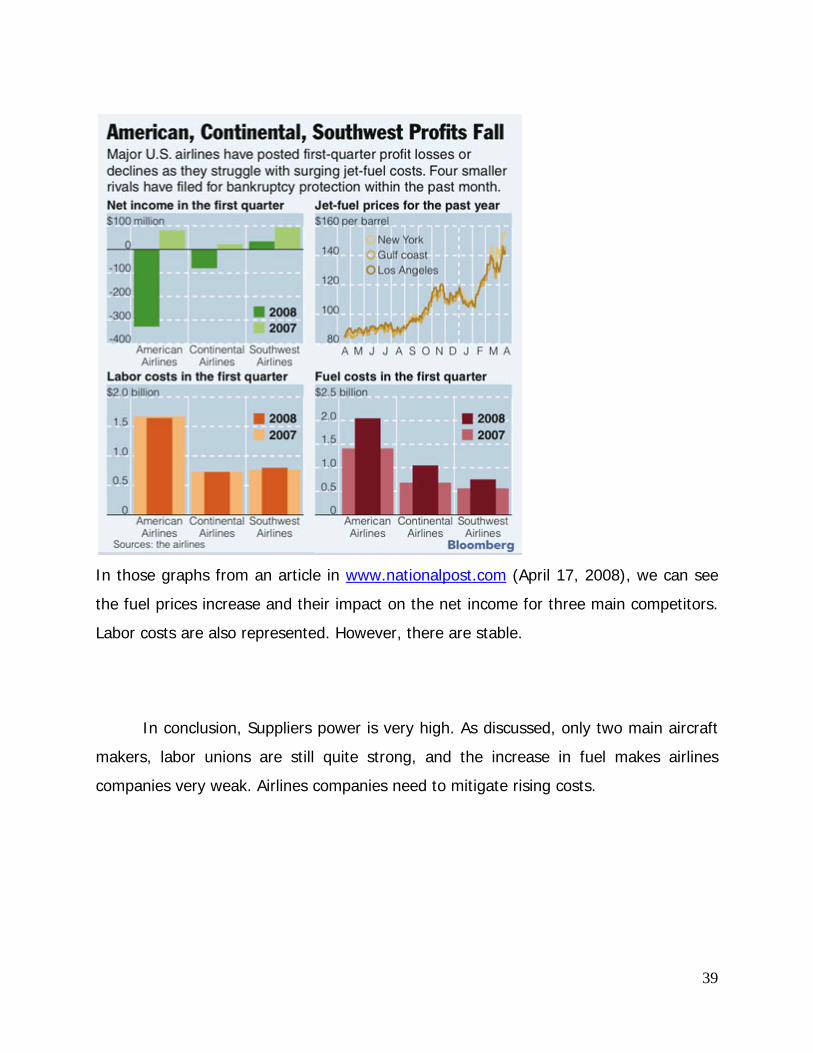

In those graphs from an article in www.nationalpost.com (April 17, 2008), we can see

the fuel prices increase and their impact on the net income for three main competitors.

Labor costs are also represented. However, there are stable.

In conclusion, Suppliers power is very high. As discussed, only two main aircraft

makers, labor unions are still quite strong, and the increase in fuel makes airlines

companies very weak. Airlines companies need to mitigate rising costs.

40

Value Chain Analysis

Competitive strategies-

The airline industry firmly believes that the three main areas of competition is

Cost Control/ Efficiency, frequency and convenience of schedules/routes, and ultimately

fares. With highly competitive price wars, each firm must use its own competitive

advantage to try to increase profitability. Each firm uses its own economies of scale

and cost structures to try to establish the maximum share of the market it can obtain.

Cost Control/Efficiency

Unlike Southwest, the 9/11 aftermath has sent many of the airline firms into

bankruptcy. Recently some of the firms have just climbed out of this negative profit

whole by cutting costs by renegotiating labor, supply, and financial contracts. Through

new deals with labor unions, fuel suppliers, and insurance companies, each firm is

finding new ways to become more cost efficient in day-to-day activities. In addition to

cutting costs through the above stated new venture, many of the other airline

companies are beginning to form new “alliances” to help spread efficiency. Ones such

alliance is Continental’s train-to-plane alliance with Amtrak. (Continental’s 2007 Annual

Report) This alliance allows an easily accessible eight-minute shuttle service for

commuters from Manhattan to Continental’s New York Liberty hub. Other alliances

include SkyTeam, which allows all of its members to share airport lounge

accommodations and helps offer greater destination coverage, as well as an ever

expanding network alliance with various travel agencies to help promote sales of the

individual airline’s ticket sales. These ways are all important in cutting costs to try to

find a competitive advantage in the domestic travels, but as for Southwest’s main

competitors, they have to find additional and alternative strategies to try to help control

cost in their international travels. Along with domestic factors the competitors must face

41

additional factors such as currency exchange, war difficulties, and different weather

patterns in international territories.

Frequency and convenience of schedules/routes

Before 9/11 the airline industry seemed to have two main market-share seeking

strategies. One of which was Southwest’s, in seeking the most efficient way of

optimizing domestic route patterns and cost control, and the alternate used by almost

all of Southwest’s competitors, of having a larger fleet to increase route frequency

domestically and internationally, as well as increasing route volume by establishing

codesharing alliances, and obtaining brand recognition. After the terrorist attacks of

9/11, the entire industry had to incur higher fuel prices and a lesser volume of willing

flyers. Southwest continued to maintain its competitive advantage with a smaller and

efficient fleet, but almost all other airlines had to shrink capacity, cut labor, and cease

certain operations.

Fares

All of the airline companies fiercely compete in price competition of lowering their

individual fares. However, each company must face its own factors that deal with the

adjusting of these fares. Besides the main differences of international travel vs domestic

travel and large fleet vs small fleet, each airline must face the same economic and other

conditions that could possibly have them adjust their prices. Some of these conditions

include: fuel prices, union problems, threatened political instability, environmental

issues, changes in consumer preferences, and potential problems in the air traffic

control system. One such factor that had a substantial increase in individual fare prices

were the terrorist attacks of 9/11. This event caused all TSA (Transportation Security

Administration) to increase personnel in all U.S. domicile airports. For example,

Continental’s per enplanement ticket tax went from a $10 per passenger roundtrip cap

to an $18 per passenger roundtrip cap. (Continental’s 2007 Annual Report)

42

Along with these factors, the entire airline industry is also faced with competition

from surface transportation, pertaining to shorter travel. In economic regressions, this

form of travel could seem more appropriate.

43

Firm Competitive Advantage

Economies of Scale-

Southwest Airlines Co. focuses on targeting a very simplistic market segment. It

focuses principally on customers that are traveling on shorter-route trips that want low-

fares and non-stop frequent flights. These types of customers range from the everyday

traveling businessman to possibly vacationing families. Southwest achieves reaching

these arrays of customers by its efficient cost-structure, differentiated strategies, and

future goal setting techniques.

Cost Efficiency/Control System

Southwest’s main competitive advantage is its superb cost structure. This low

cost-structure is reached through only using one type of aircraft, efficient route

structures, and high moral employees.

By using only one aircraft type, the Boeing 737, Southwest is able to simplify

scheduling, maintenance, flight operations, and training activities. This in turn greatly

reduces costs of having to hire additional workers/trainers that would have to require

additional skill sets.

Southwest’s main low-cost driver would be its efficient route-structure. “Point-to-

point service allows for more direct nonstop routing than the hub and spoke system,

minimizing connections, delays, and total trip time.” (Southwest’s 2007 Annual Report)

As of this year, Southwest now has over 400 nonstop city pairs. Also helping in

Southwest’s efficient routing schedule are conveniently located downtown and

secondary airports. These airports are generally less crowded and congested, which

helps minimize the time the aircraft has to stay on the ground. This asset utilization

helps reduce costs by avoiding flying time in the air waiting too land, and cabbing time

waiting to depart in crowded airports. This reduction in aircraft usage also helps add

44

additional routes to increase profitability. Another cost reduction strategy to

compensate for the raising of fuel prices is eliminating shorter less profitable flights to

help utilize the already existing fleet in more profitable ventures. This in turn keeps the

company from expensing additional aircraft and fuel, while increasing its turnover.

Differentiation strategies

-Fare Structure-

“Southwest was the first major airline to introduce a Ticketless travel option,

eliminating the need to print and then process a paper ticket altogether, and the first to

offer Ticketless travel through the Company’s website at www.southwest.com”

(Southwest’s 2007 Annual Report) This innovative strategy helped bring new clientele

that did not want to have to wait in airport terminals to receive their travel vouchers. At

the end of 2007 over 90 % of all Southwest customers chose the ticketless confirmation

method. In addition to this fare distribution channel, Southwest is better trying to reach

the everyday businessman traveler by adding on to its fare distribution web. To help

show available fares in the future, Southwest announced an expansion of its Global

Distribution System to help with corporate travel. Also, to help better compensate these

frequent flyers, Southwest has recently created their rapid rewards frequent flyer

program. This program is based on the number of trips the customer has taken rather

than the mileage flown. For every 16 credits (flights) within 24 months, the flyer will

receive one free round-trip award to any destination on Southwest.

-Enhanced Boarding Method and Updated Gate Design-

To help with efficient boarding, Southwest has created a method that greatly

reduces customer wait time standing in line at the gate. In addition to adding their

“Business Select” class, which basically means frequent flyers that automatically receive

A class status upon arrival at the gate, the new method arranges customers in a fashion

45

of A, B, and C boarding groups with assigned numbers. This boarding method allows for

the flyer to have a reserved spot in line, depending on when he/she checked in

electronically or at the terminal, as early as 24 hours in advance. With this new

boarding method, Southwest updated its gate design to have columns with letters and

numbers to help facilitate the order in which to board. Along with these columns, to

help indulge the Southwest experience, they included “(i) a business focused area with

padded seats, tables with power outlets, power stations with stools, and a flat screen

television for news programming; and (ii) a family area with smaller tables and chairs,

“kid friendly” programming on a flat screen television, and power stations for charging

electrical devices.”

Looking into the future

To help become more efficient and to help differentiate itself from its

competitors, Southwest plans to replace its existing Ticketless system and revenue

accounting system with new technology. This new technology will help create easier

data flow, which will in turn increase operational efficiencies and Customer Service

capabilities.

As a member of the low concentration airline industry, Southwest engages in

high price competition with its rivals. With having very closely related rival firms, to

emerge successful a firm must have excellent cost-efficiency strategies. By creating a

superior cost-efficient structure, innovative differentiated strategies, and implementing

useful future goal setting techniques, Southwest seems to be able to sustain its top of

the industry status.

46

Accounting Analysis

The purpose of performing an accounting analysis on this firm is to analyze the

firms accounting practices. The analysis will also highlight if the firm, in fact, exercised

acceptable accounting practices that mirror accurate information about the firm. The

degree of financial reporting is regulated in the United States by GAAP, Generally

Accepted Accounting Principles. The Security Exchange commission (SEC) requires

managers of firms to follow GAAP in order to provide a clear picture of the company for

their shareholders and potential investors. GAAP give managers numerous alternative

options in accounting so they can show how their company succeeds or falls short; also

how it competes within its industry. GAAP provides a degree of flexibility to the

managers of the firms rather than using accounting principles that do not represent

accurate conditions of the company and its industry. This accounting flexibility has good

intentions, but accounting can still be manipulated by management.

Structuring an accounting analysis begins with identifying the company’s key

accounting policies that deal directly with its key success factors. Also to look at would

be important information on the financial statements as well. Information like capital

and operating leases, pension plans, and fuel hedging costs should be investigated for

possible manipulation. Assessing the degree of accounting flexibility will help determine

if the firm’s managers distorted the financials in some way to make the company look

financially sound. The accounting strategy phase of the accounting analysis process

allows us to evaluate the accounting policies the company used. From there we need to

compare them with the industry norm and identify if there are any irregularities in our

firm or that of any of the competitors. During the accounting analysis; we will have to

assess the quality of information we are disclosed in the company’s 10K. After

completing the analysis, we will be able to determine how transparent this firm’s

financial statements are. If there are any inconsistencies with reporting, we must

47

identify the potential “Red Flags” or other abnormalities. Lastly, we must then undo any

abnormalities in the firm’s accounting in order to properly value the firm.

Key Accounting Policies

The initial step in Accounting Analysis is to identify the firm’s key accounting

policies. In order to analyze this, Southwest’s key accounting policies must be directly

related to its key success factors. These factors include industry growth, level of

concentration, differentiation, switching costs, economies of scale, fixed and variable

costs, excess capacity, and exit barriers. “The airline industry is highly competitive. The

company believes the principal competitive factors in the industry are, fares, customer

service, costs, frequency and convenience of scheduling, frequent flyer benefits, and

Efficiency and productivity, including effective selection and use of aircraft (Southwest

10K)”. This allows Southwest to help differentiate itself, allowing it to have some

competitive advantage over other airlines in the industry. Every firm wants the

advantage to differ itself from the competition in one way or another to have the upper

hand in the industry. We found in draft one that Southwest’s key success factors are

price competition, differentiated strategies, and future goal setting techniques. The firm

can clearly present these factors, or give their own account of their competitive

advantages.

Southwest also utilizes GAAP when they prepare their financial statements. This

allows Southwest’s management to make assumptions and estimations that affect

amounts stated on their Consolidated Financial Statements. “The Company’s estimates

are based on historical experience and changes in the business environment (Southwest

10K).” Southwest’s assumptions are most important when it comes to the portrayal of

the company’s financial condition; they require the best judgment from managers. The

accounting policies that are directly linked to Southwest’s key success factors are the

following: revenue recognition, fuel hedging, operating leases, and retirement and

pension plans.

48

Revenue Recognition

In the airline industry companies like JetBlue, American, Continental, and

Southwest emphasize the importance of price competition, but also have to follow

GAAP’s policies in recording such entries accordingly. The SEC instructs all U.S. based

companies to use GAAP when preparing their financials. Price competition is important

to southwest because it enables them to be the “low cost leader” in the airline industry.

How they maintain low prices in an uncertain economy is a big question. Southwest

achieves this by adjustments made first on the balance sheet, that then affect the

income statement. Southwest like many of its competitors use revenue recognition

when estimating revenue. Southwest initially records all ticket sales to the “Air Traffic

Liability” line of the balance sheet before it allocates the sale to the “Passenger

Revenue” line on the income statement. The air plane has to actually take off before

the sale is adjusted on the Income Statement. An argument can be made that the ticket

sale should be viewed as a revenue not a liability, and have line for doubtful accounts.

Other airlines face the same disadvantage when recording revenues from ticket sales.

Air traffic liability accounted for $931 million in 2007 versus $799 million in 2006.

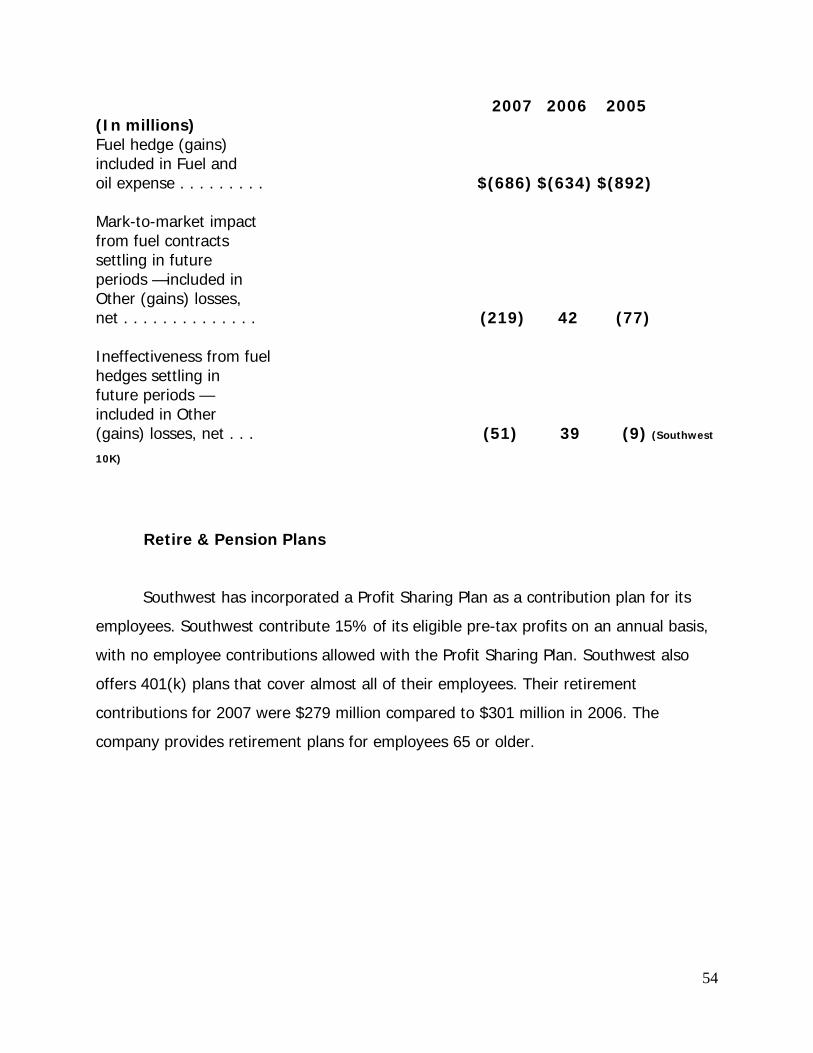

Fuel Hedging

”Southwest is a pioneer when it comes to the low-cost business model, but high

oil prices are a growing threat (Morningstar.com).” Southwest Airlines has incurred

more costs in 2007 because of rising fuel costs, but those are not the only costs

Southwest has. “Southwest’s business is dependent on the price and availability of

aircraft fuel. Continued periods of high fuel costs and/or significant disruptions in the

supply of fuel could adversely affect the Company’s results of operations (Southwest

10K)”. Fuel cost have risen from $2,119,520 in 2006 to $2,539,600 in 2007, the

average cost per gallon of jet fuel has risen from $1.53 in 2006 to $1.70 in 2007 with

the expected rate to be in the $2.60 to $2.65 range.

49

2007 2006

(In millions)

Mark-to-market impact from fuel contracts settling in future periods — included in

Other (gains) losses, net . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $(219) $ 42

Ineffectiveness from fuel hedges settling in future periods —included in Other (gains)

losses, net . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (51) 39

Realized ineffectiveness and mark-to-market (gains) or losses — included in Other

(gains) losses, net . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (90) 20

Premium cost of fuel contracts included in Other (gains) losses, net . . . . . . . . . . . . . . 58 52

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 (2)

$(292) $151

(Southwest 10K)

Southwest’s profit for 2007 was $645 million compared to 2006 with $499 million, a

29.3% increase (Southwest 10K). “Jet fuel and oil consumed for fiscal 2007 and 2006

represented approximately 28 percent and 26 percent of Southwest’s operating

expenses, respectively (Southwest 10)”.

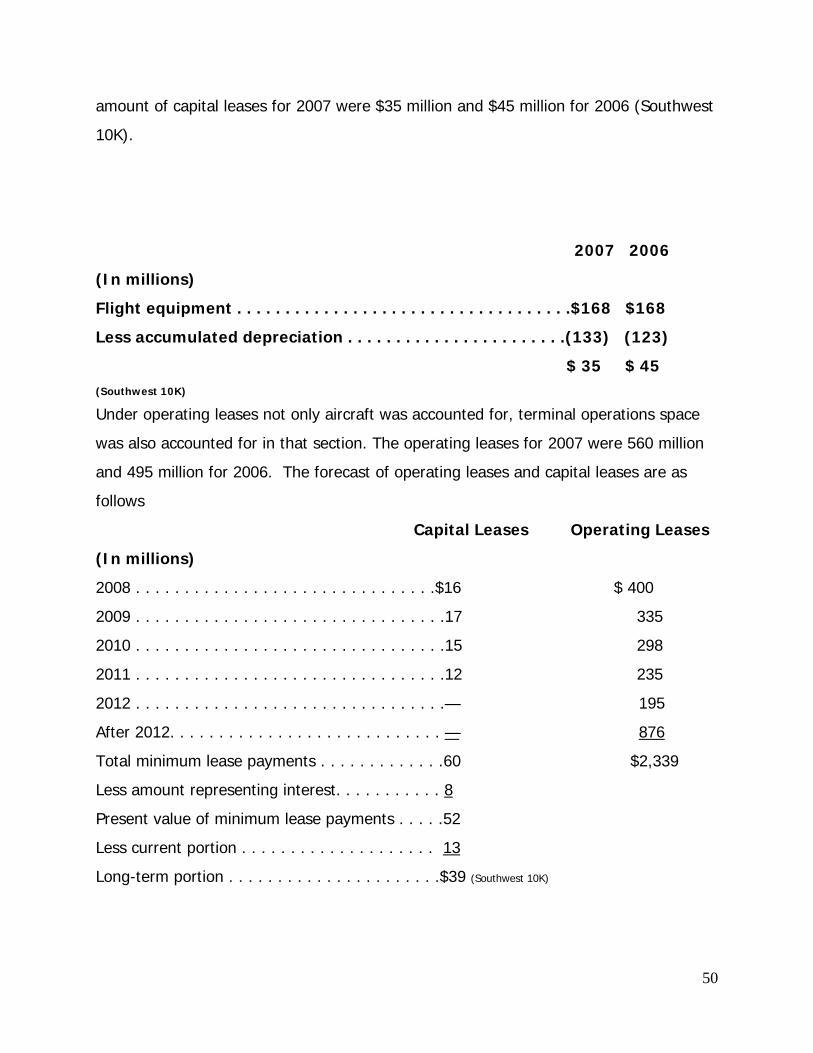

Capital and Operating Leases

Southwest believes that having a single type of aircraft, Boeing 737, contributes

to its low cost structure. Some believe that having a single type of aircraft can be

damaging to the firm. The maker of the aircraft may at sometime not be able to provide

adequate assistance to the aircraft. However, Southwest believes that the advantages

outweigh the negative risks when it comes to having a single aircraft strategy

(Southwest 10K). Out of Southwest’s fleet of 520 planes 95 of them are leased, 86 were