MFS Module 1

63

Management of Financial Services Let us know what is Financial System Financial system can be compared to nervous system – Blood circulation in nervous System - It deals with Money & monitory assets . Complex set up –, Institutions , Markets, services, instruments –claims and liabilities –money, credit ,Finance Economic Development needs good Financial system Ensure supply of Fin for production of goods and services Well-being – standard of living Responsibility of FS – mobilize savings and invest in productive ventures Promote free flow of funds in economy - liquidity Study complex structure under following heads:

-

Upload

farhasangolli -

Category

Documents

-

view

19 -

download

1

description

MFS Model 1

Transcript of MFS Module 1

Management of Financial Services Let us know what is Financial System Financial system can be compared to nervous system – Blood circulation in nervous System - It deals with Money & monitory assets . Complex set up –, Institutions , Markets, services,

instruments –claims and liabilities –money, credit ,Finance Economic Development needs good Financial system Ensure supply of Fin for production of goods and services Well-being – standard of living Responsibility of FS – mobilize savings and invest in

productive ventures Promote free flow of funds in economy - liquidity Study complex structure under following heads:

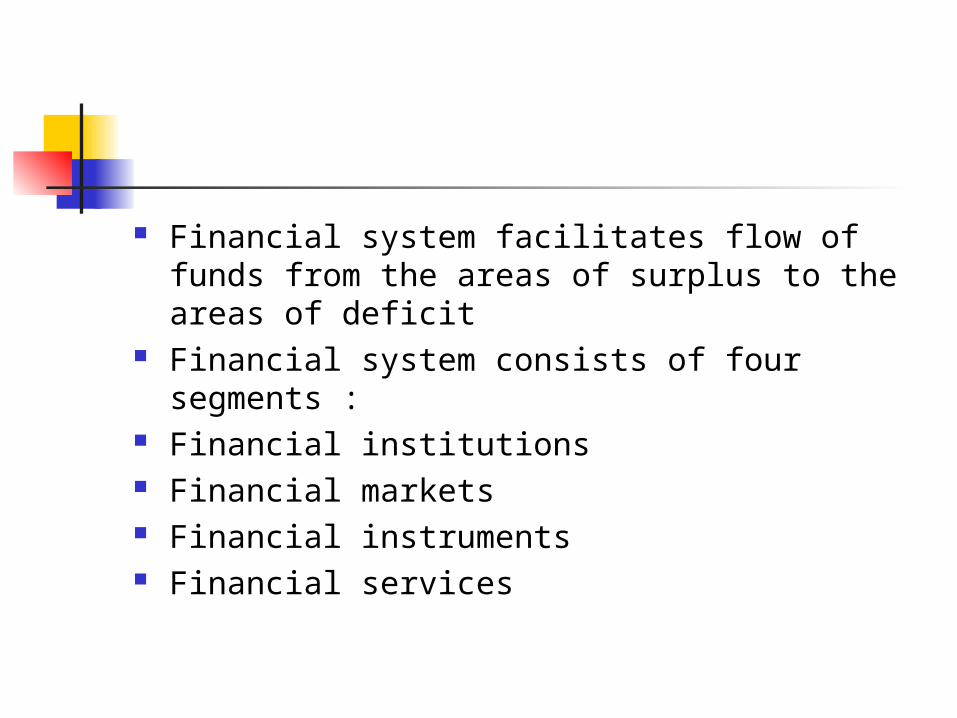

Financial system facilitates flow of funds from the areas of surplus to the areas of deficit

Financial system consists of four segments : Financial institutions Financial markets Financial instruments Financial services

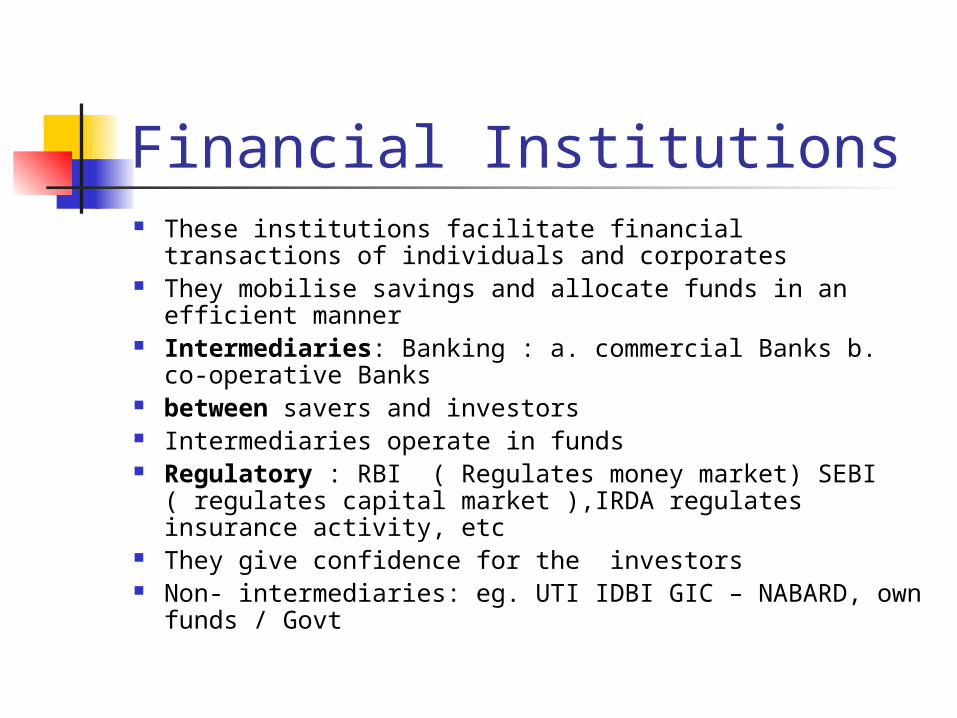

Financial Institutions These institutions facilitate financial transactions of

individuals and corporates They mobilise savings and allocate funds in an efficient

manner Intermediaries: Banking : a. commercial Banks b. co-

operative Banks between savers and investors Intermediaries operate in funds Regulatory : RBI ( Regulates money market) SEBI

( regulates capital market ),IRDA regulates insurance activity, etc

They give confidence for the investors Non- intermediaries: eg. UTI IDBI GIC – NABARD, own funds /

Govt

Financial Markets Place where buyer & seller meet Price determination Financial markets are the centers which facilitate buying

and selling of financial assets Organised Market has :it has standardised rules and

regulations for financial dealings Done under supervision of regulatory body like RBI Capital Market: deals with financial assets which has a

long and indefinite maturity –more than one year a. corporate securities market , b. Govt Securities market, c. Long term loans market

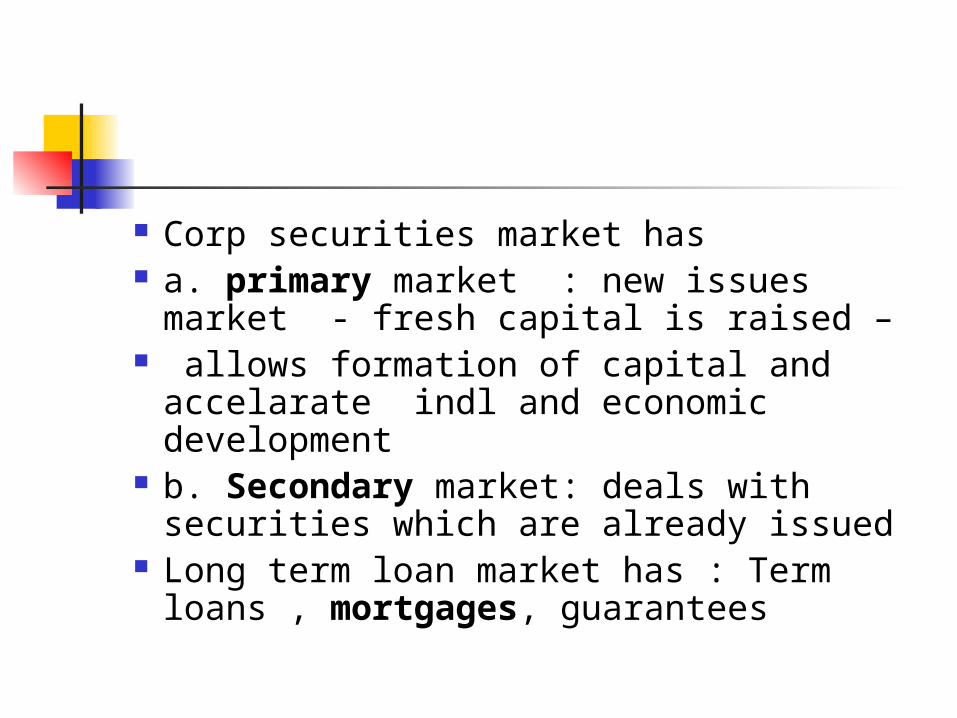

Corp securities market has a. primary market : new issues market -

fresh capital is raised – allows formation of capital and accelarate

indl and economic development b. Secondary market: deals with

securities which are already issued Long term loan market has : Term loans ,

mortgages, guarantees

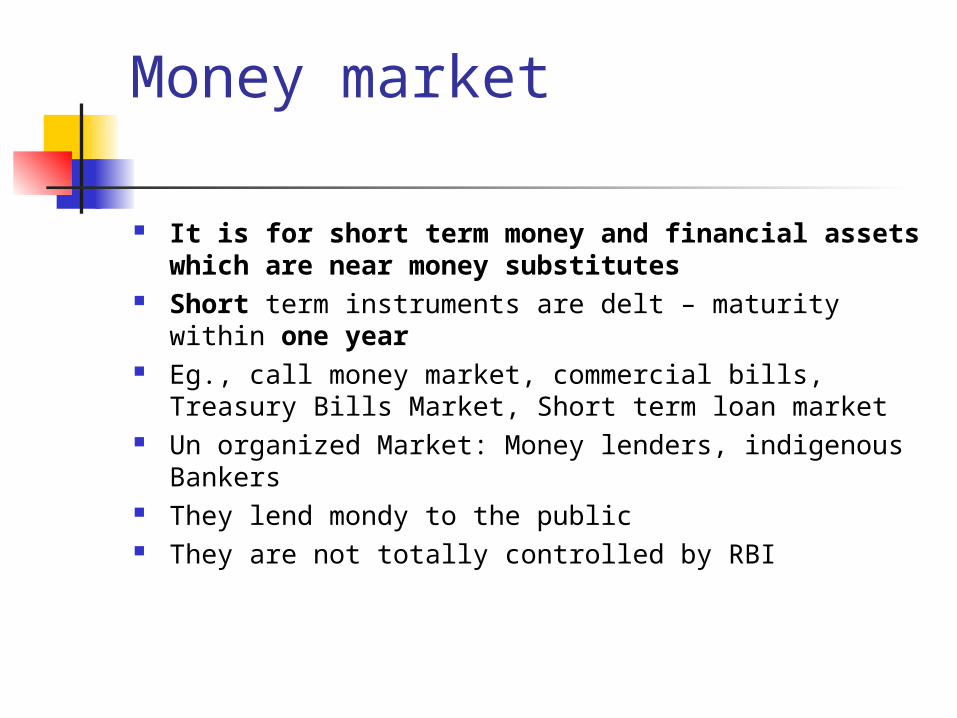

Money market

It is for short term money and financial assets which are near money substitutes

Short term instruments are delt – maturity within one year

Eg., call money market, commercial bills, Treasury Bills Market, Short term loan market

Un organized Market: Money lenders, indigenous Bankers

They lend mondy to the public They are not totally controlled by RBI

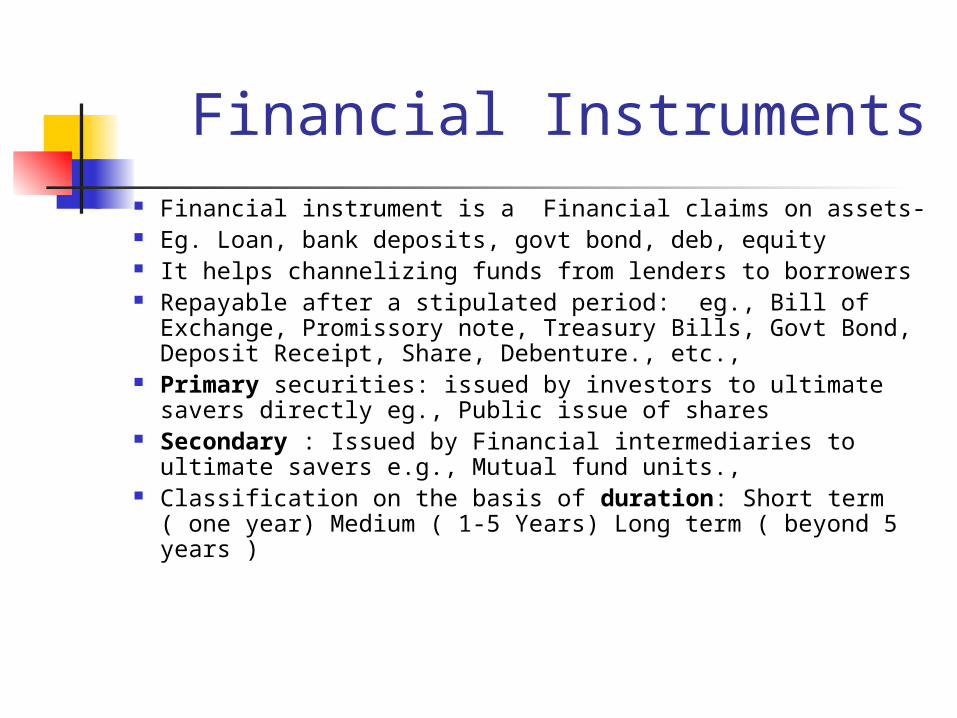

Financial Instruments Financial instrument is a Financial claims on assets- Eg. Loan, bank deposits, govt bond, deb, equity It helps channelizing funds from lenders to borrowers Repayable after a stipulated period: eg., Bill of

Exchange, Promissory note, Treasury Bills, Govt Bond, Deposit Receipt, Share, Debenture., etc.,

Primary securities: issued by investors to ultimate savers directly eg., Public issue of shares

Secondary : Issued by Financial intermediaries to ultimate savers e.g., Mutual fund units.,

Classification on the basis of duration: Short term ( one year) Medium ( 1-5 Years) Long term ( beyond 5 years )

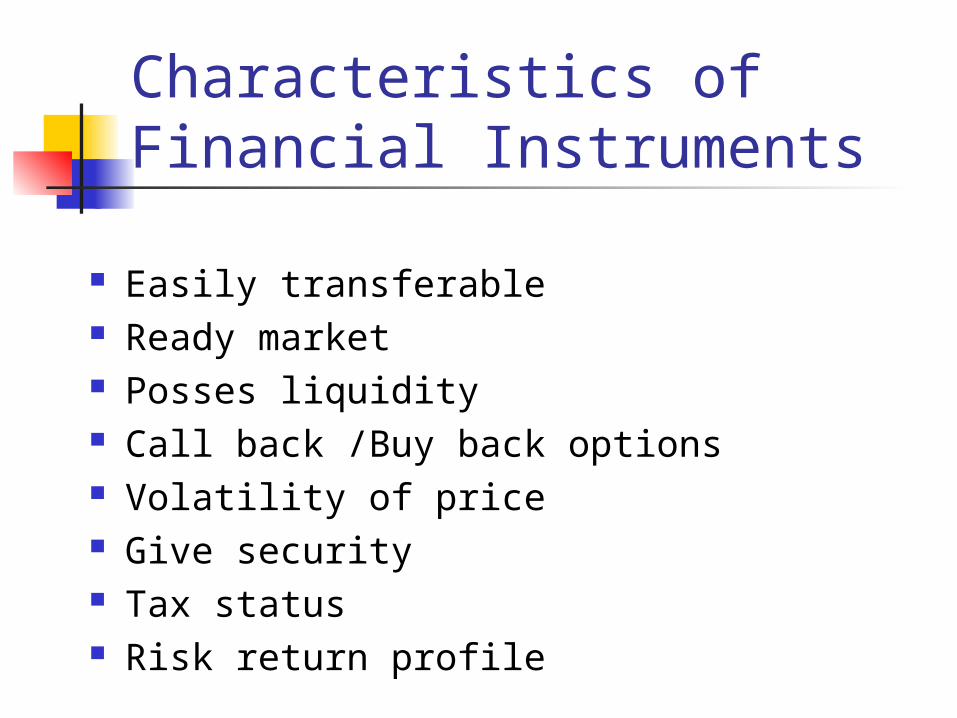

Characteristics of Financial Instruments

Easily transferable Ready market Posses liquidity Call back /Buy back options Volatility of price Give security Tax status Risk return profile

Financial Services

Banks Consultants Merchant Bankers Services which facilitate the flow of money and

monitory assets in the economy Examples: Portfolio Management Factoring Services Forfeiting NBFC Leasing & Hire purchase Credit Rating Venture capital services

Functions of Financial System Regulates dealings between various

Economic units – individuals, Institutions – in money and money assets

Provides Markets – organised and unorganised – Primary and secondary – platform for buying and selling goods and services

Provide Financial Institutions, Intermediaries, brokers, agents, dealers for flow of Money and financial assets and goods and services

Provide Financial Instruments – suit requirements of different entities

Functions of FS Aims to promote savings and investments by

offering financial assets of various qualities Aims to allocate savings to various channels of

investment It arranges for creation and distribution of

money, credit and finance throughout the economy

Promotes economic development by capital formation by offering suitable Financial assets. Larger the proportion of financial assets (money and monitory assets) to Real assets (Physical goods and services ) greater is the scope for economic growth.

Increase Standard of living of population.

Role of Financial Markets Provide Platform for buyers and sellers

to meet & transact Fin instruments & real assets

Provides for Price discovery Lays down systems and procedures –

Laws - settlement of transactions Provides Financial assets with different

varied features to suit requirement of different entitities and investors.

Market Perfection - efficiency There are large number of savers and

investors Operating in the market Savers and investors are rational Operators are well informed & info freely

available. There are no transaction costs Fin assets are infinitely divisible There are no TaxesUnder these ideal conditions Market attains

equilibrium – supply and demand are equal

Limitations of financial system Industrial finance dominated by development Banks –

but they do not mobilize savings Capital market is not very strong and dependable – lot

of scams and frauds – public do not have enough faith Govt owns many institutions – it also controls – hence

there is no much co-ordination between them Monopolistic structure : very large - not much of

compition – like LIC

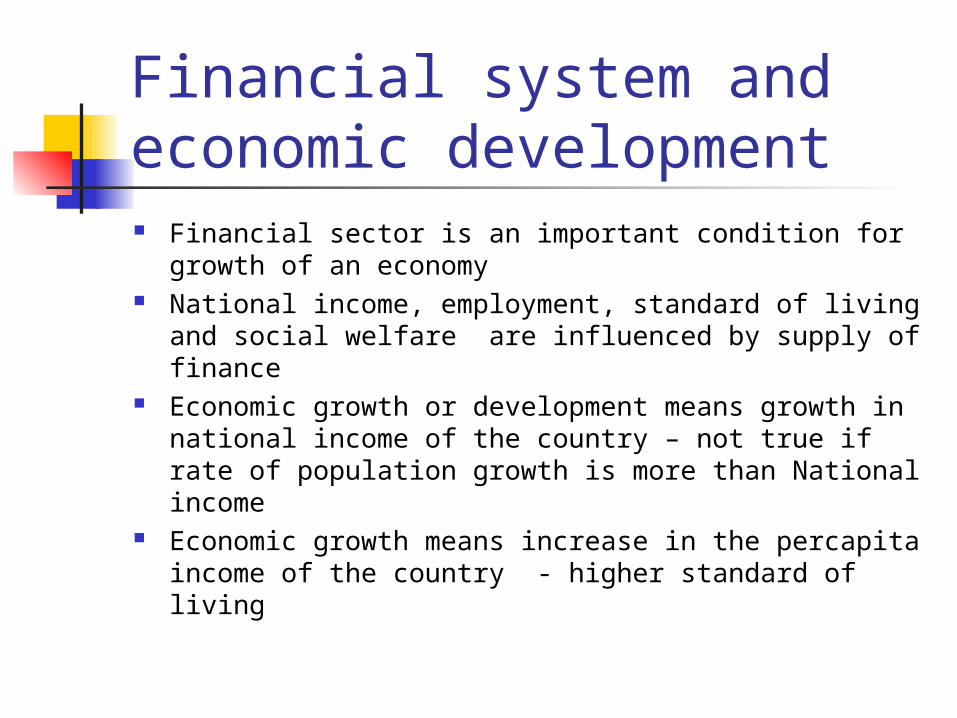

Financial system and economic development Financial sector is an important condition for growth of

an economy National income, employment, standard of living and

social welfare are influenced by supply of finance Economic growth or development means growth in

national income of the country – not true if rate of population growth is more than National income

Economic growth means increase in the percapita income of the country - higher standard of living

Stages of economic development There are three stages in economic development - according

to Prof Rostow: 1. preparatory stage : Long period or a century - when the precondition fro take off

are established In the matter of society’s attitude, political sovereignty, good

tax system, financial institutions, creation of infrastructure etc., 2. The take off period: It is abrief period - say two to three decades After this economic development takes place automatically 3. Period of self sustained growth : There is a good savings and investment – self generating

Effect of financial system on savings and investments Human capital and physical capital can be

bought and developed with money as input Money , credit and finance are the life blood of

the economic system The required technology also can be

developed for acclerating growth It also enlarges the markets – deepen and

widen - leads to efficiency in medium of exchange

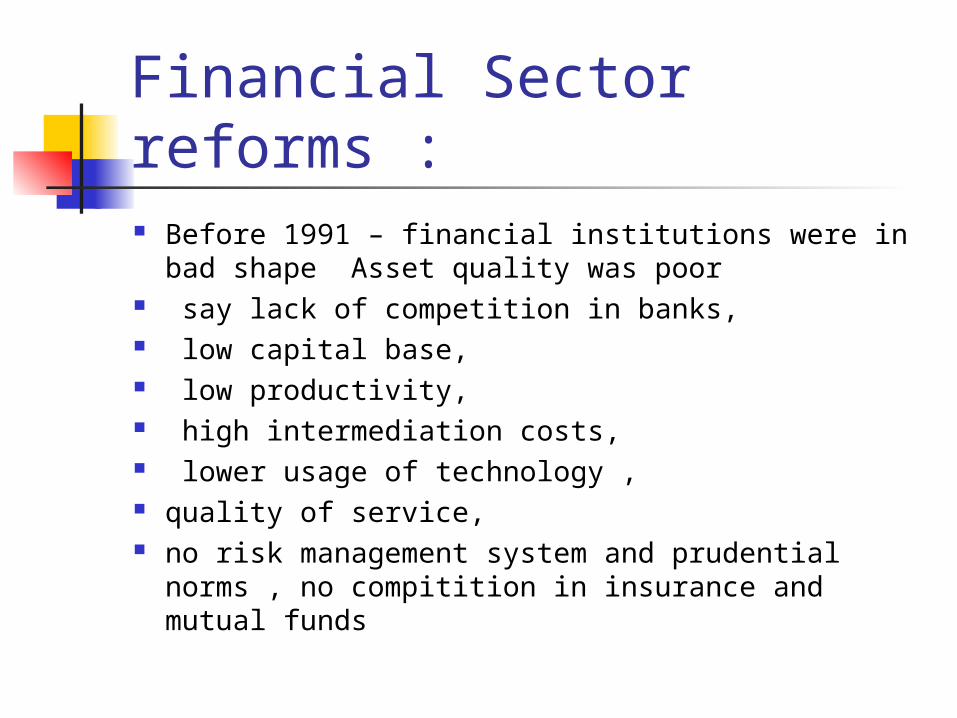

Financial Sector reforms : Before 1991 – financial institutions were in bad

shape Asset quality was poor say lack of competition in banks, low capital base, low productivity, high intermediation costs, lower usage of technology , quality of service, no risk management system and prudential norms

, no compitition in insurance and mutual funds

Financial markets were: Operated under controlled conditions There were barriers for entry Transaction costs were high Banks were running under loss or low profits Banks were unable to provide for defaults, and

build their capital High SLR and CRR Cross subsidization – low rates to priority sector

and high rates to larger borrowers

New Economic policy (NEP) was given a big thrust in India in 1991

Govt appointed a high power committee to examine structure, organization, function procedure of financial system

After its report lot of changes were introduced - as the financial institutions and markets were in bad shape

Objectives of financial reforms -1991 To develop market oriented competitive, world integrated

transparent financial system Allocate the savings properly, Promote growth in real sector Create accountability, profitability, efficiency, professionalism

and depoliticalisation in financial sector Promote competition – free entry and exit for players -in level

playing ground to them Rationalize interest rates - market determined – dismantle

administered system of interest rates Improve financial infrastructure, supervision credit , etc., Modernize instruments to make it suitable for conducting

monetary policy and control

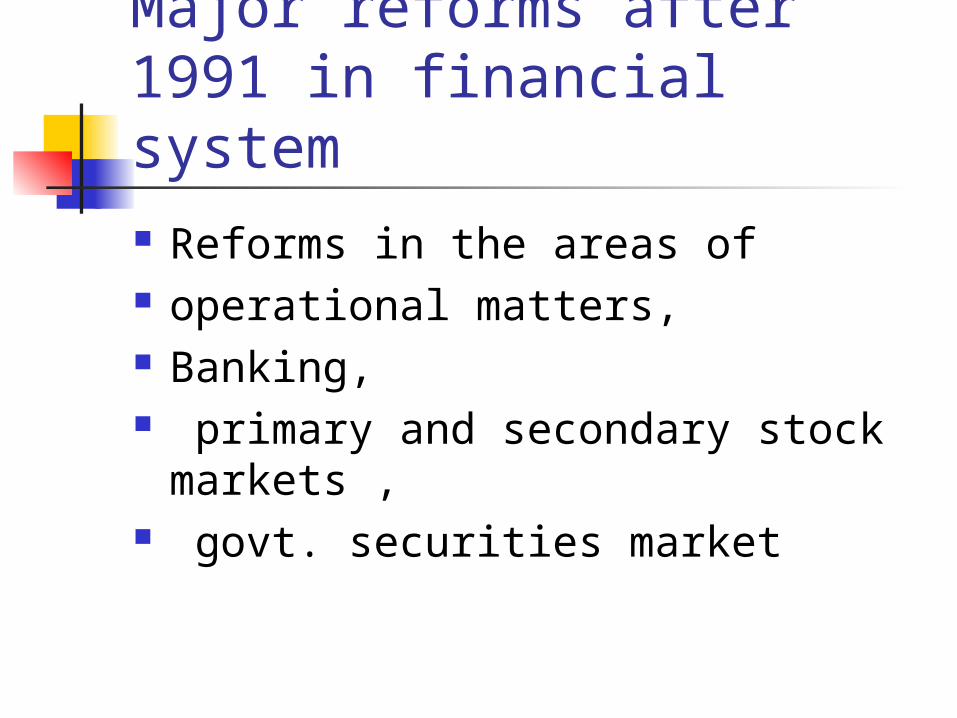

Major reforms after 1991 in financial system Reforms in the areas of operational matters, Banking, primary and secondary stock

markets , govt. securities market

Systemic and policy reforms Interest rates deregulated - market rates on G sec. – dismantle

administered interest rates SLR reduced from 38.5% of DTL to 23% now Capital adequacy norms introduced Board of financial supervision - dept in RBI was formed Recovery of debts by banks by special recovery tribunals Ad hoc treasury bills replaced by ways and means advances from

1997 Private sector was allowed to set up banks, Mutual funds,

insurance companies Office of CCI was abolished SEBI was formed to regulate capital market NBFC with above 25 laths Net owned fund should register with RBI OTC and NSE were formed to have nationwide trading and display

Some impt banking reforms are: Interest rates on deposits and advances deregulated SBI and nationalized banks allowed to access capital market for

debt and equity Introduce prudential norms for income recognition, classification

of assets and provisioning for bad debts Valuation of investments by banks - make it mark to market for

securities held by them Bank balance sheet to become fully transparant and adopt

international accounting standards Banks given freedom to open, shifit, or open extension counters Provided budgetory support for weak PSU Banks Banking ombudsman scheme 1995 was introduced Free to fix the FX open positon – subject to RBI approal

Primary and secondary market reforms Primary market allotment only through depository 100% book building for issues above 25 crores Payment of direct or indirect discount on shares prohibited Housing companies can raise money if they get refinance

from NHB Mutual funds allowed to underwrite the public issues Depositories act 1996 was passed - dmat of shares Stock lending scheme introduced – facilitate short sellers Stock exchanges modernised – introduce on line trading by

BSE Short and long sales are disclosed to stock exchange -

impose strict margins

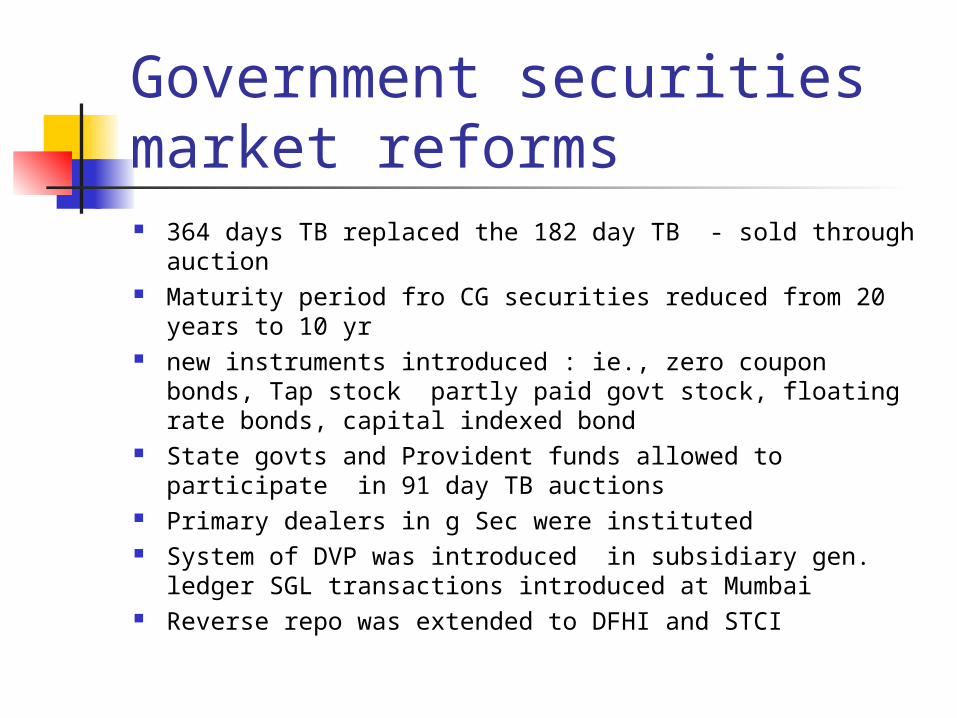

Government securities market reforms 364 days TB replaced the 182 day TB - sold through auction Maturity period fro CG securities reduced from 20 years to

10 yr new instruments introduced : ie., zero coupon bonds, Tap

stock partly paid govt stock, floating rate bonds, capital indexed bond

State govts and Provident funds allowed to participate in 91 day TB auctions

Primary dealers in g Sec were instituted System of DVP was introduced in subsidiary gen. ledger SGL

transactions introduced at Mumbai Reverse repo was extended to DFHI and STCI

External financial market reforms FIIs allowed to access Indian capital markets on

Regn with SEBI Indian companies permitted to access international

capial markets through various euro-equity issues FERA replacved by FEMA – 1997-98

NRIs and OCB’s are permitted to invest upto 24%in equities of Indian companies

RBI made single window agency for overseas investment by indian companies

Reserve Bank of India Money is medium of exchange Monitory system – role of RBI crucial Apex institution in Banking & fin System Partial shouldering of mgt of economy England –highly developed banking & central banking system Bankers bank, lender of last resort – maintain CRR – active

securities market Technical advisory service in fx, foster growth RBI set up in 1935 – as a body corporate -paid up Rs. 5 crores nationalized in 1949 – to control inflation and plan economic

programme and to fall in line with international trend Operates according to the provisions of RBI Act

Objectives of Central Bank 1. Maintain internal value of the currency 2. To preserve the external value of the

currency To secure reasonable price stability Promote economic development – raise

employment, output, etc.,

To facilitate external trade and payment To provide adequate quantity of currency notes

and coins in good quality

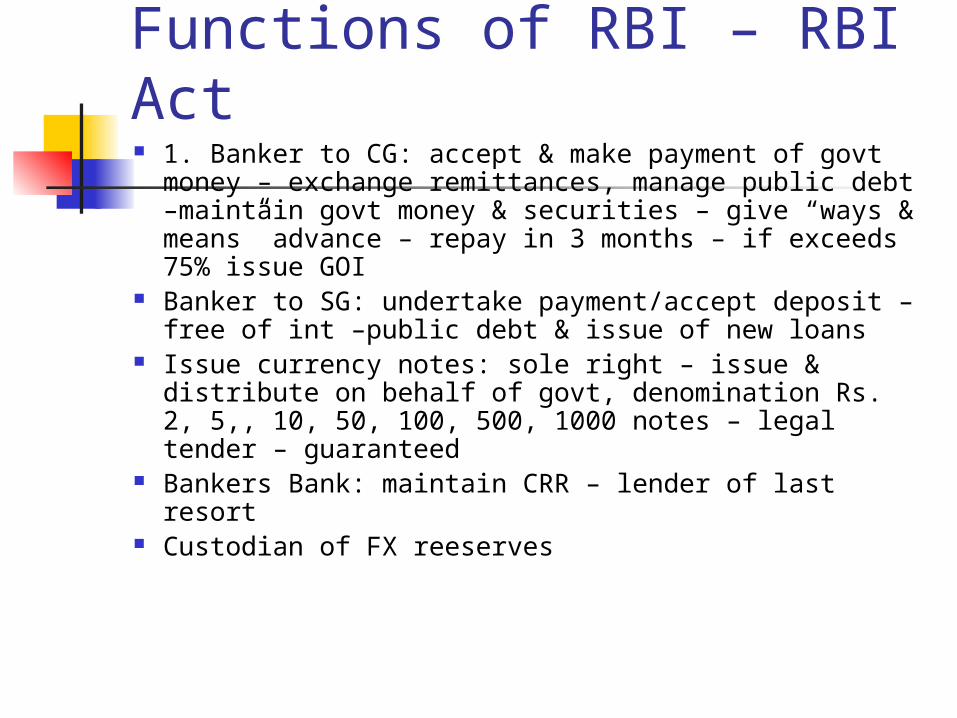

Functions of RBI – RBI Act 1. Banker to CG: accept & make payment of govt

money – exchange remittances, manage public debt –maintain govt money & securities – give “ways & means” advance – repay in 3 months – if exceeds 75% issue GOI

Banker to SG: undertake payment/accept deposit – free of int –public debt & issue of new loans

Issue currency notes: sole right – issue & distribute on behalf of govt, denomination Rs. 2, 5,, 10, 50, 100, 500, 1000 notes – legal tender – guaranteed

Bankers Bank: maintain CRR – lender of last resort Custodian of FX reeserves

Functions – contd Controller of credit : through OMO – selective

credit controls - regulation of banks – Bank send weekly report to RBI – inspect books of Bank

Sponsor top Banks: idbi, nabard, NHB Sit in boards of all banks Advise on CG& SG – monitory matters Keep CRR – 3% to 15%- send statemt Grant loans - security approved securities –

rediscount Bills Watch dog of entire financial system Indian RBI – one of the best

Organisation and mangement Central board : gen superintendence – a governor, not more

than 4 dy governors and 15 directors – nominated by CG Local Board : in 4 regional areas – mumbai, Kolkata, New Delhi,

and chennai.- perform the duties delegated by Central board Departments of RBI : Issue department Banking department Banking development - expansion , training banks etc Agricultural credit Exchange control Industrial finance Non Banking companies

Depts - contd Legal department Research and statistics Department of

planning and reorganization Economic department Inspection department Department of accounts and expn., RBI services board : HRD of RBI Department of supervision – of banks

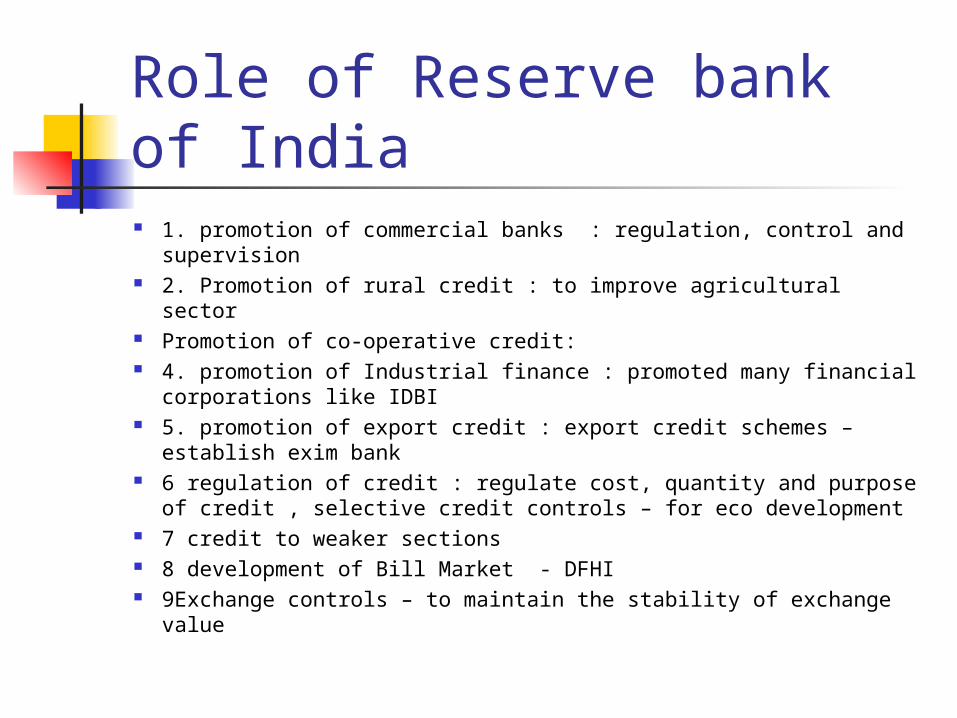

Role of Reserve bank of India 1. promotion of commercial banks : regulation, control and

supervision 2. Promotion of rural credit : to improve agricultural sector Promotion of co-operative credit: 4. promotion of Industrial finance : promoted many financial

corporations like IDBI 5. promotion of export credit : export credit schemes – establish

exim bank 6 regulation of credit : regulate cost, quantity and purpose of

credit , selective credit controls – for eco development 7 credit to weaker sections 8 development of Bill Market - DFHI 9Exchange controls – to maintain the stability of exchange value

Achievements of RBI Developed banking practices Managing public debt effectively Institutionalize savings – establish specialized agencies Promote co-operative credit Regulate credit to meet the requirement of trade and industry Provision of credit facilities to exporters and concessional rate –

refinance, Providing deposit insurance and credit guarantee DICGC Successfully develop bill culture in the country Providing information on different sectors – give publications Providing clearing house facilities Good management of FX by RBI Set up training colleges to difft banks Modernized through information technology

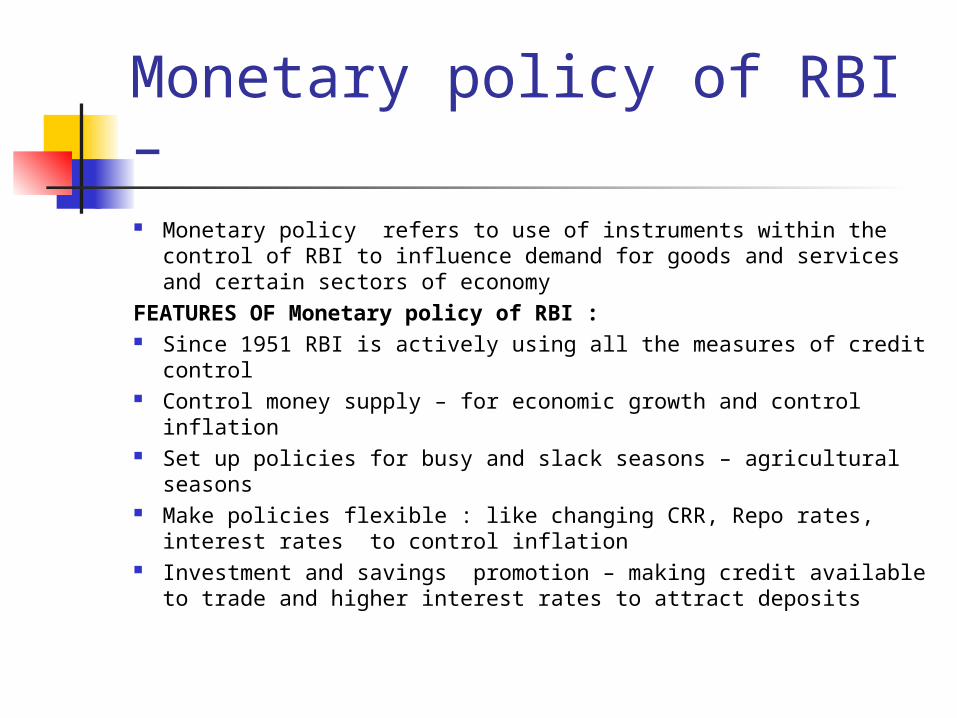

Monetary policy of RBI – Monetary policy refers to use of instruments within the control

of RBI to influence demand for goods and services and certain sectors of economy

FEATURES OF Monetary policy of RBI : Since 1951 RBI is actively using all the measures of credit

control Control money supply – for economic growth and control

inflation Set up policies for busy and slack seasons – agricultural seasons Make policies flexible : like changing CRR, Repo rates, interest

rates to control inflation Investment and savings promotion – making credit available to

trade and higher interest rates to attract deposits

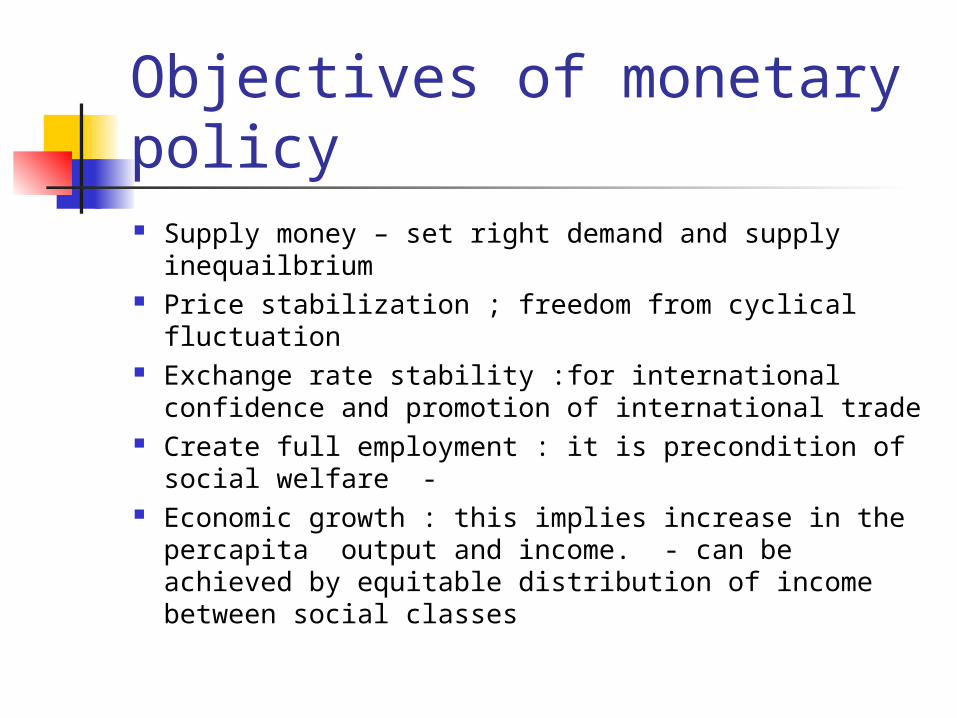

Objectives of monetary policy Supply money – set right demand and supply

inequailbrium Price stabilization ; freedom from cyclical fluctuation Exchange rate stability :for international confidence

and promotion of international trade Create full employment : it is precondition of social

welfare - Economic growth : this implies increase in the

percapita output and income. - can be achieved by equitable distribution of income between social classes

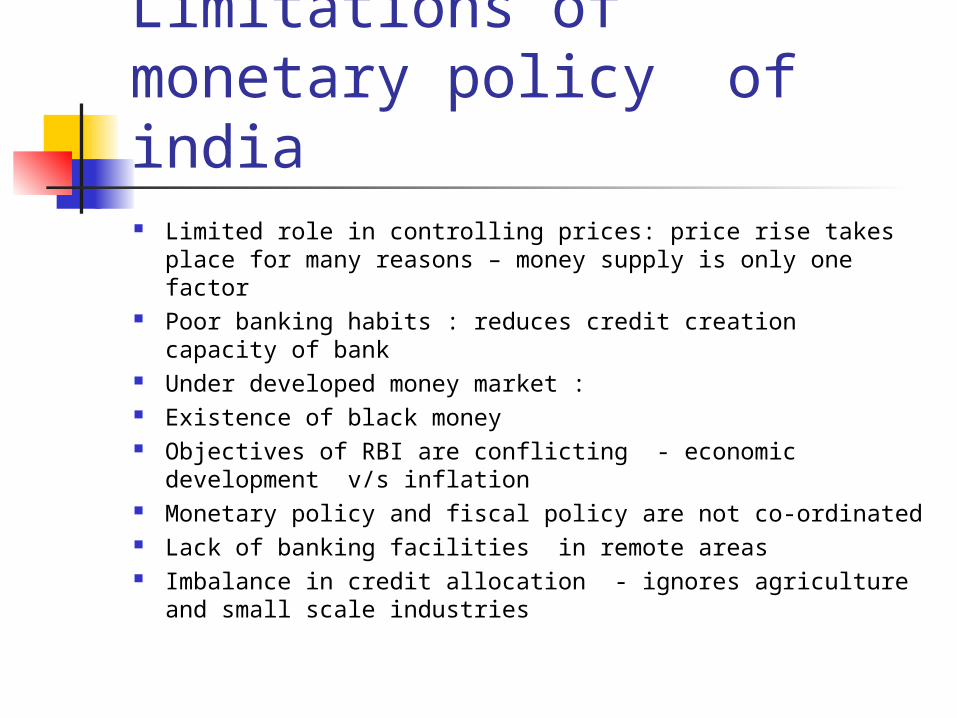

Limitations of monetary policy of india Limited role in controlling prices: price rise takes place for

many reasons – money supply is only one factor Poor banking habits : reduces credit creation capacity of

bank Under developed money market : Existence of black money Objectives of RBI are conflicting - economic development

v/s inflation Monetary policy and fiscal policy are not co-ordinated Lack of banking facilities in remote areas Imbalance in credit allocation - ignores agriculture and

small scale industries

Securities & exchange Board of India (SEBI)

•Regulatory Authority – over constitutuents of Capital Market• - constituted in 1988 – operational and autonomous in 1992•Vested with various powers like •Regulate Stock Exchanges•Intermediaries and mutual funds •Investor Education•Training of intermediaries •Establish SRO s•Prohibit Unfair trade practices and insider trading

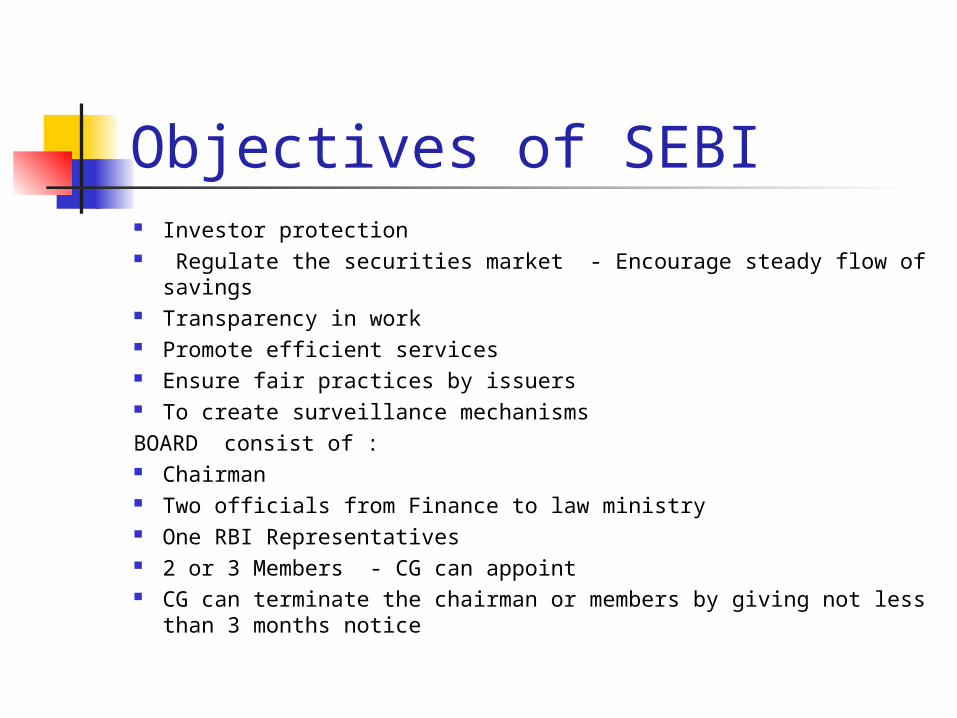

Objectives of SEBI Investor protection Encourage steady flow of savings Transparency in work Promote efficient services Ensure fair practices by issuers To create surveillance mechanisms BOARD consist of : Chairman Two officials from Finance to law ministry One RBI Representatives 2 or 3 Members - CG can appoint

Operational departments Primary Markets Dept Issue Management and intermediaries dept Secondary Markets Dept Institutional Dept Legal and investigation Dept - Headed by officials of ED

rank Two Advisory committees - Primary market Secondary markets

Note : Advisory committee members are selected from the players or eminent persons from the the capital market

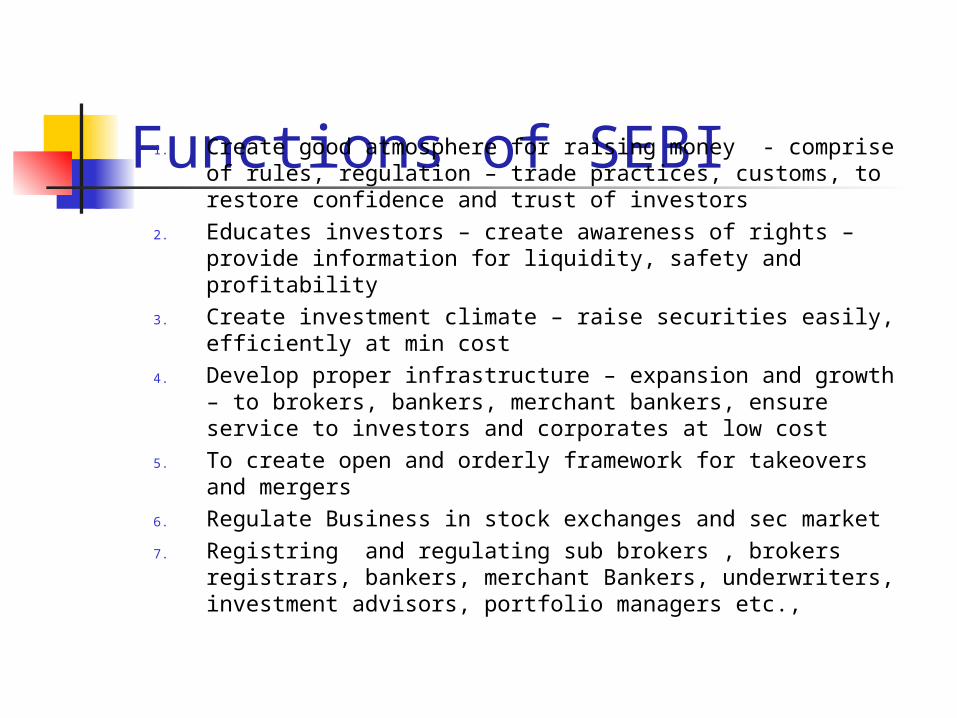

Functions of SEBI1. Create good atmosphere for raising money - comprise of rules,

regulation – trade practices, customs, to restore confidence and trust of investors

2. Educates investors – create awareness of rights – provide information for liquidity, safety and profitability

3. Create investment climate – raise securities easily, efficiently at min cost

4. Develop proper infrastructure – expansion and growth – to brokers, bankers, merchant bankers, ensure service to investors and corporate at low cost

5. To create open and orderly framework for takeovers and mergers6. Regulate Business in stock exchanges and sec market 7. Registering and regulating sub brokers , brokers registrars,

bankers, merchant Bankers, underwriters, investment advisors, portfolio managers etc.,

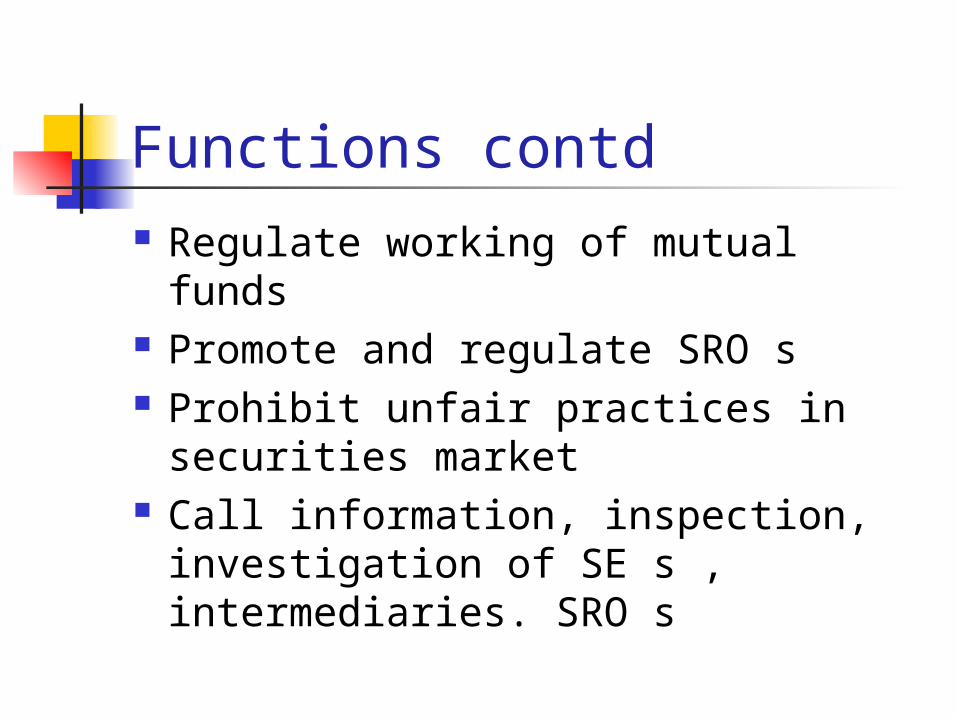

Functions contd Regulate working of mutual funds Promote and regulate SRO s Prohibit unfair practices in

securities market Call information, inspection,

investigation of SE s , intermediaries. SRO s

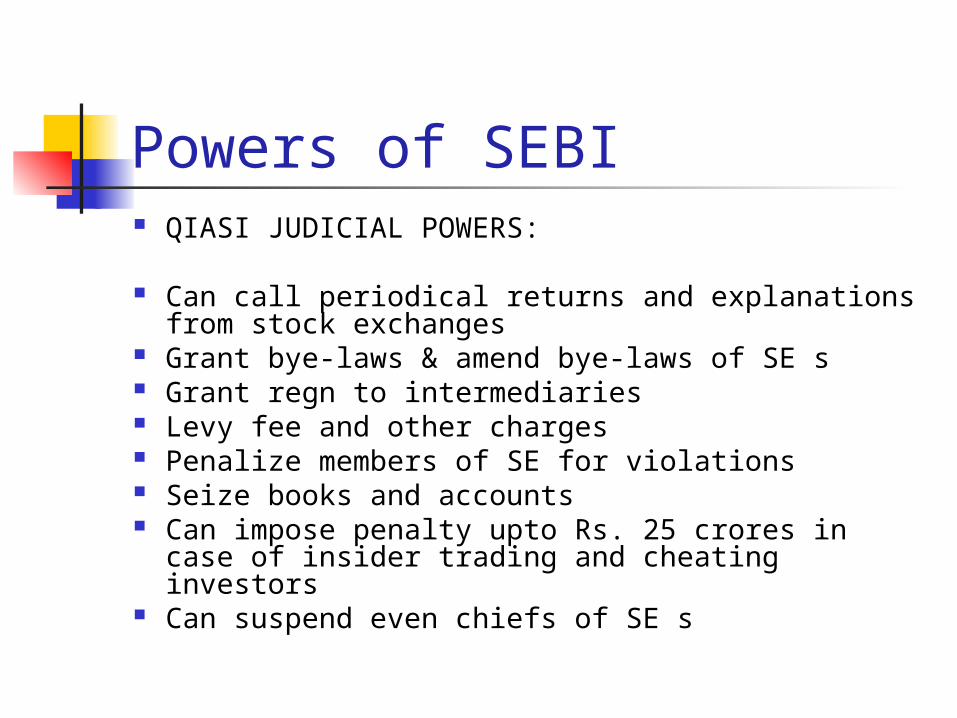

Powers of SEBI QIASI JUDICIAL POWERS:

Can call periodical returns and explanations from stock exchanges

Grant bye-laws & amend bye-laws of SE s Grant regn to intermediaries Levy fee and other charges Penalize members of SE for violations Seize books and accounts Can impose penalty upto Rs. 25 crores in case of

insider trading and cheating investors Can suspend even chiefs of SE s

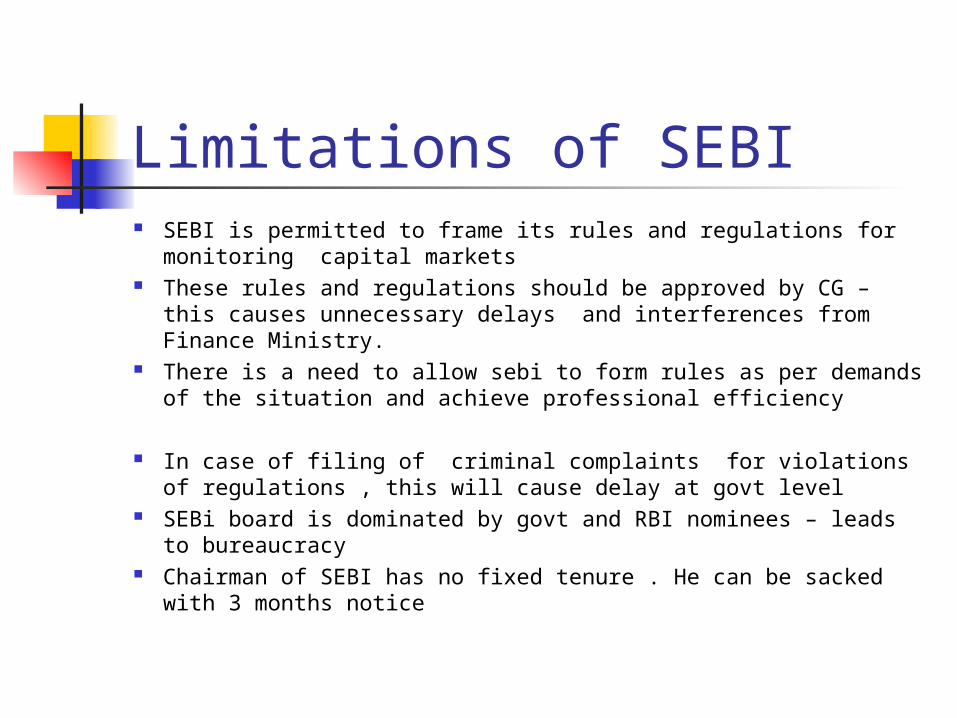

Limitations of SEBI SEBI is permitted to frame its rules and regulations for monitoring

capital markets These rules and regulations should be approved by CG – this

causes unnecessary delays and interferences from Finance Ministry.

There is a need to allow sebi to form rules as per demands of the situation and achieve professional efficiency

In case of filing of criminal complaints for violations of regulations , this will cause delay at govt level

SEBi board is dominated by govt and RBI nominees – leads to bureaucracy

Chairman of SEBI has no fixed tenure . He can be sacked with 3 months notice

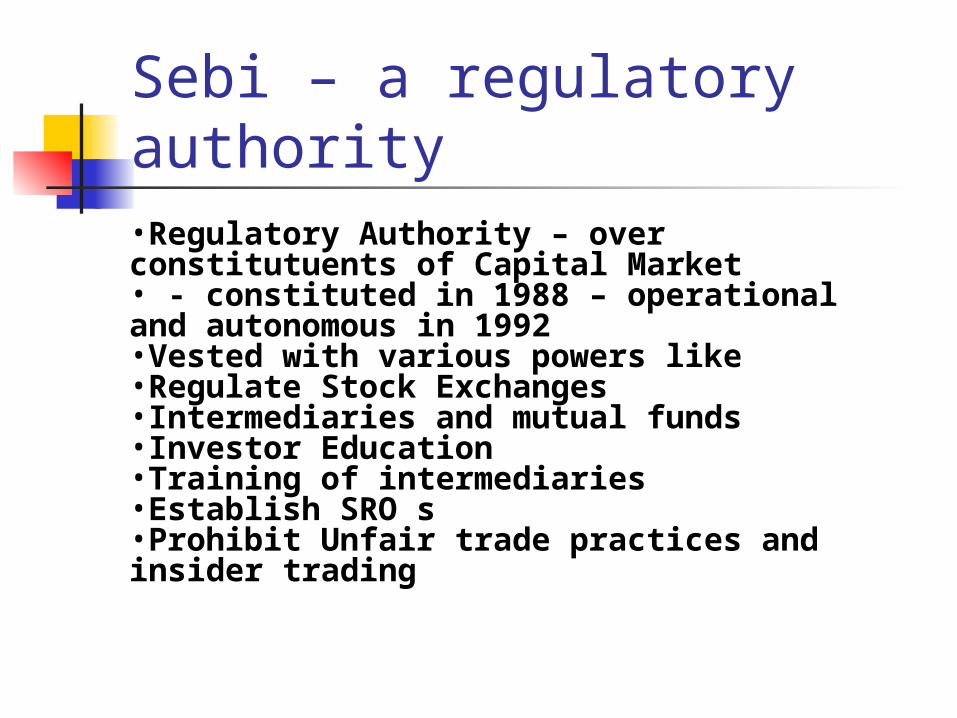

Securities & exchange Board of India

•Regulatory Authority – over constitutuents of Capital Market

•constituted in 1988 – operational and autonomous in 1992

•Vested with various powers like •Regulate Stock Exchanges

•Intermediaries and mutual funds •Investor Education

•Training of intermediaries •Establish SRO s

•Prohibit Unfair trade practices and insider trading

Sebi – a regulatory authority •Regulatory Authority – over constitutuents of Capital Market• - constituted in 1988 – operational and autonomous in 1992•Vested with various powers like •Regulate Stock Exchanges•Intermediaries and mutual funds •Investor Education•Training of intermediaries •Establish SRO s•Prohibit Unfair trade practices and insider trading

Objectives of SEBI Investor protection Regulate the securities market - Encourage steady flow of savings Transparency in work Promote efficient services Ensure fair practices by issuers To create surveillance mechanisms BOARD consist of : Chairman Two officials from Finance to law ministry One RBI Representatives 2 or 3 Members - CG can appoint CG can terminate the chairman or members by giving not less than

3 months notice

Operational departments Primary Markets Dept Issue Management and intermediaries dept Secondary Markets Dept Institutional Dept Legal and investigation Dept - Headed by officials of ED

rank Two Advisory committees - Primary market Secondary markets Note : Advisory committee members are selected from the

players or eminent persons from the the capital market

Functions of SEBI1. Create good atmosphere for raising money - comprise of rules, regulation – trade practices, customs, to restore confidence and trust of investors

2. Educates investors – create awareness of rights – provide information for liquidity, safety and profitability

3. Create investment climate – raise securities easily, efficiently at min cost

4. Develop proper infrastructure – expansion and growth – to brokers, bankers, merchant bankers, ensure service to investors and corporates at low cost

5. To create open and orderly framework for takeovers and mergers

6. Regulate Business in stock exchanges and sec market 7. Registring and regulating sub brokers , brokers registrars,

bankers, merchant Bankers, underwriters, investment advisors, portfolio managers etc.,

Functions contd Regulate working of mutual funds Promote and regulate SRO s Prohibit unfair practices in

securities market Call information, inspection,

investigation of SE s , intermediaries. SRO s

Powers of SEBI QIASI JUDICIAL POWERS:

Can call periodical returns and explanations from stock exchanges

Grant bye-laws & amend bye-laws of SE s Grant regn to intermediaries Levy fee and other charges Penalize members of SE for violations Seize books and accounts Can impose penalty upto Rs. 25 crores in case of

insider trading and cheating investors Can suspend even chiefs of SE s

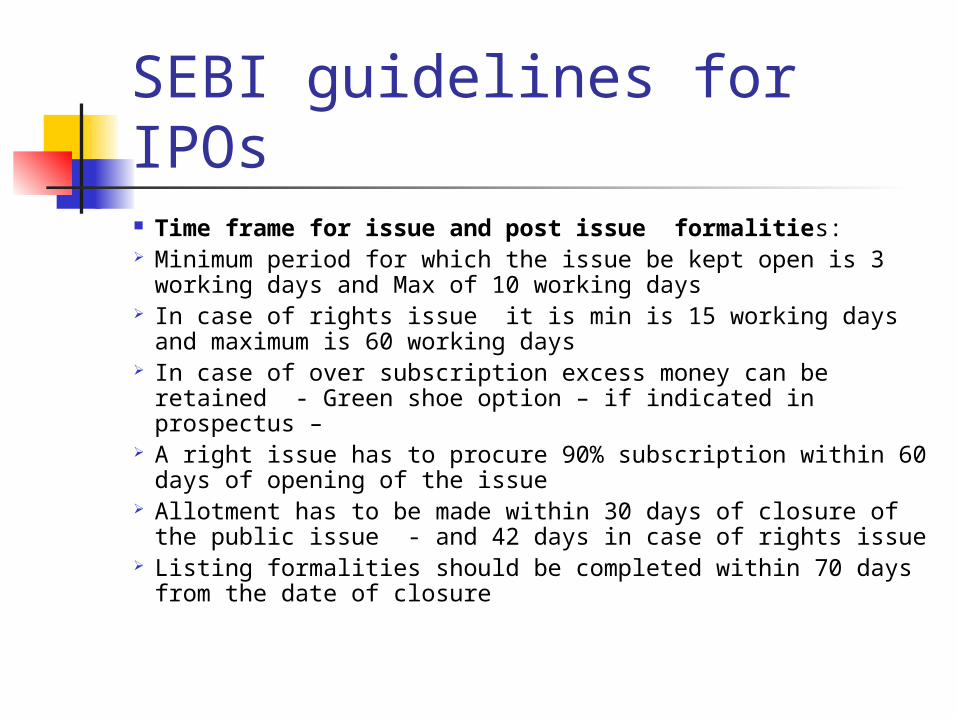

SEBI guidelines for IPOs Time frame for issue and post issue formalities: Minimum period for which the issue be kept open is 3

working days and Max of 10 working days In case of rights issue it is min is 15 working days and

maximum is 60 working days In case of over subscription excess money can be retained

- Green shoe option – if indicated in prospectus – A right issue has to procure 90% subscription within 60

days of opening of the issue Allotment has to be made within 30 days of closure of the

public issue - and 42 days in case of rights issue Listing formalities should be completed within 70 days

from the date of closure

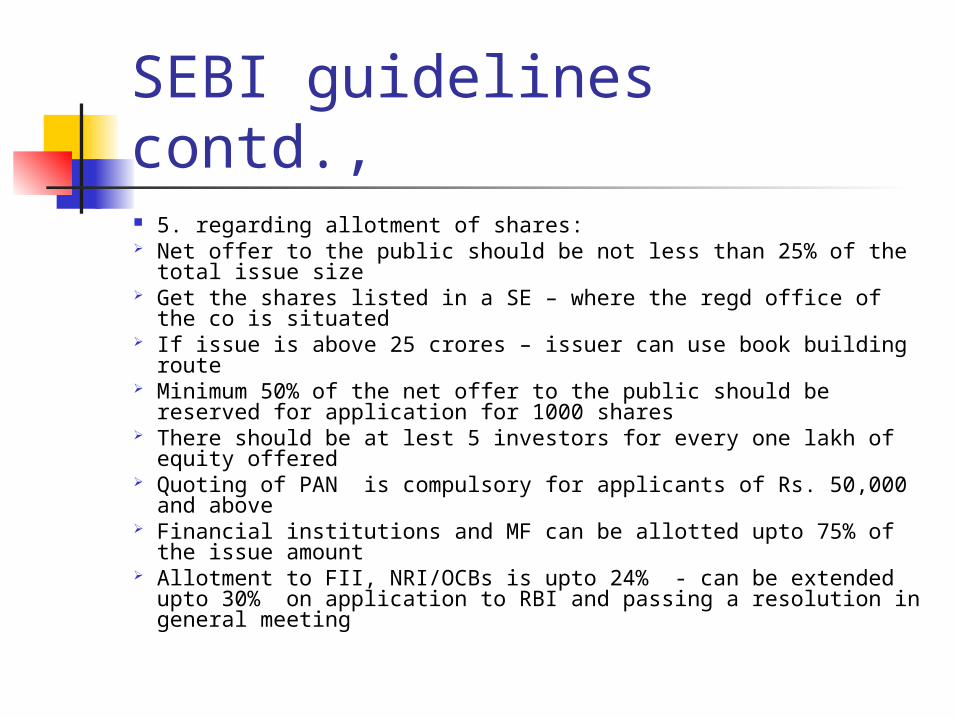

SEBI guidelines contd., 5. regarding allotment of shares: Net offer to the public should be not less than 25% of the total

issue size Get the shares listed in a SE – where the regd office of the co is

situated If issue is above 25 crores – issuer can use book building route Minimum 50% of the net offer to the public should be reserved for

application for 1000 shares There should be at lest 5 investors for every one lakh of equity

offered Quoting of PAN is compulsory for applicants of Rs. 50,000 and

above Financial institutions and MF can be allotted upto 75% of the issue

amount Allotment to FII, NRI/OCBs is upto 24% - can be extended upto

30% on application to RBI and passing a resolution in general meeting

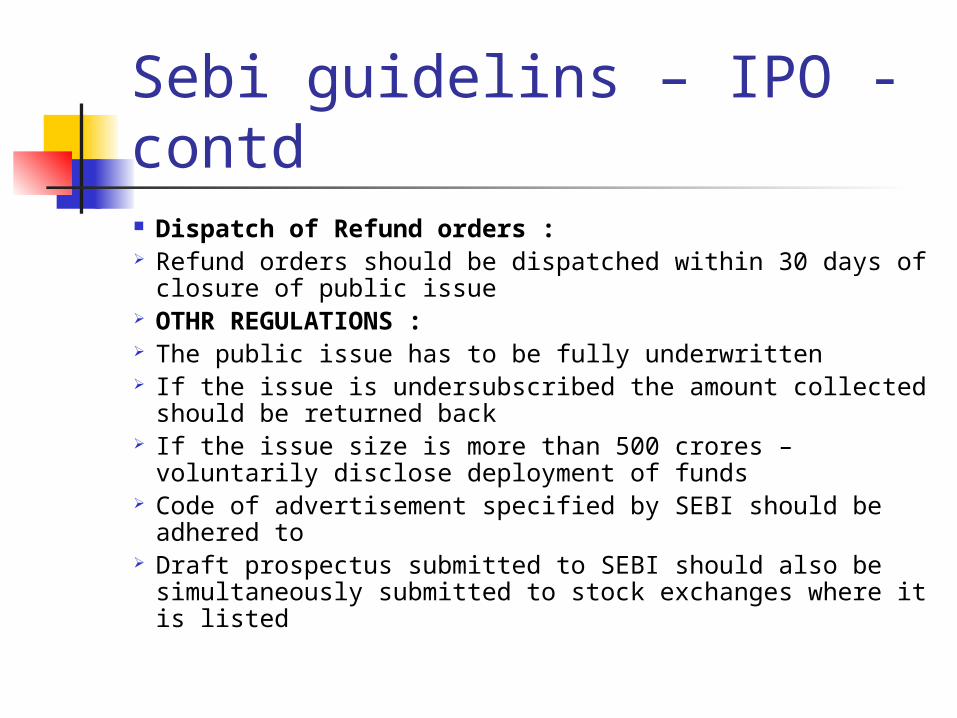

Sebi guidelins – IPO - contd Dispatch of Refund orders : Refund orders should be dispatched within 30 days of closure

of public issue OTHR REGULATIONS : The public issue has to be fully underwritten If the issue is undersubscribed the amount collected should

be returned back If the issue size is more than 500 crores – voluntarily disclose

deployment of funds Code of advertisement specified by SEBI should be adhered

to Draft prospectus submitted to SEBI should also be

simultaneously submitted to stock exchanges where it is listed

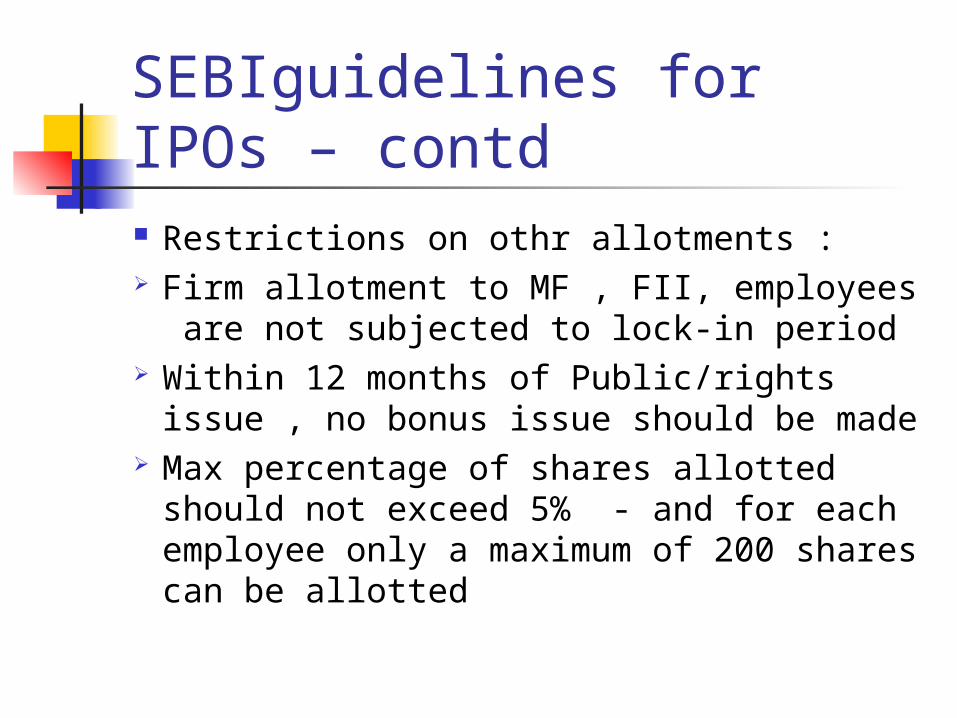

SEBIguidelines for IPOs – contd Restrictions on othr allotments : Firm allotment to MF , FII, employees are

not subjected to lock-in period Within 12 months of Public/rights issue ,

no bonus issue should be made Max percentage of shares allotted should

not exceed 5% - and for each employee only a maximum of 200 shares can be allotted

SEBI guidelines for rights issue - offer of shares to existing sh holdrs Ensure that the rights issue is within the authorized

capital of the co Ensure that draft prospectus is vetted by SEBI before

issued Appoint a merchant banker if the issue size exceeds Rs.

50 lakhs Ensure that issue is not kept open for more than 60 days Open separate bank account for keeping subscription

received under rights issue Convene a board meeting to decide the proportion in

which it should be issued Secretary to draft a explanatory statement and notices

of the meeting – explaining how the additional capital is proposed to be utilized .

SEBI guidelines on issue of Bonus shares by public companies - (note : there are not guidelines private and unlisted companies ) No company shall issue bonus shares pending conversion of

FCD/PCD unless a similar benefit is extended to FCD and PCD Out of free reserves : it can be issued only out of free reserves

or share premium collected in cash Revaluation reserve should not be used for issue of bonus

shares Declaration of bonus issue in place of dividend is not permitted The existing partly paid shares should be made fully paid

before issue of bonus shares There should not be default in payment of interest to

depositors or debentures Company should not have defaulted in payment of statutory

dues of employees - like PF, gratuity, etc., The decision of the board for issue of bonus shares can be

implemented within a period of 15 days - no need to share holders approval