Mexico Sugar Annual Mexico Sugar Annual Report · 4/16/2015 · contracting mills. In exchange,...

12

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Date: GAIN Report Number: Approved By: Prepared By: Report Highlights: Mexican sugar production for marketing year 2015/16 is forecast to be at 6.5 million metric tons raw- value (MMT-RV), although there is not yet an official forecast. Sugar production for MY 2014/15 was revised downward to 6.4 MMT-RV. The sugar export forecast for MY 2015/16 is 1.8 MMT-RV. Post /New total sugar export estimate for MY 2014/15 is 1.6 MMT-RV, where exports to the United States under the suspension agreements are 1,383,969.68 MT-RV. The high fructose corn syrup (HFCS) import forecast for MY 2015/16 is expected to be similar to MY 2014/15 imports, as sugar prices remain low. Dulce Flores and Alicia Hernandez Lloyd Harbert Mexico Sugar Annual Report Sugar Annual Mexico MX5017 4/16/2015 Required Report - public distribution

Transcript of Mexico Sugar Annual Mexico Sugar Annual Report · 4/16/2015 · contracting mills. In exchange,...

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY

USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT

POLICY

Date:

GAIN Report Number:

Approved By:

Prepared By:

Report Highlights:

Mexican sugar production for marketing year 2015/16 is forecast to be at 6.5 million metric tons raw-

value (MMT-RV), although there is not yet an official forecast. Sugar production for MY 2014/15 was

revised downward to 6.4 MMT-RV. The sugar export forecast for MY 2015/16 is 1.8 MMT-RV. Post

/New total sugar export estimate for MY 2014/15 is 1.6 MMT-RV, where exports to the United States

under the suspension agreements are 1,383,969.68 MT-RV. The high fructose corn syrup (HFCS)

import forecast for MY 2015/16 is expected to be similar to MY 2014/15 imports, as sugar prices

remain low.

Dulce Flores and Alicia Hernandez

Lloyd Harbert

Mexico Sugar Annual Report

Sugar Annual

Mexico

MX5017

4/16/2015

Required Report - public distribution

MX5017 Mexico Sugar Annual Report Page 2

Commodities:

PRODUCTION

Sugar

The Mexican sugar industry expects sugar production levels for marketing year (MY) 2015/16

(October/September) to be close to 6.5 MMT-RV as appropriate cultivation practices, such as

application of fertilizers, pesticides, crop rotation, and pruning, have not been as expected due to lower

export expectations. Although there is not yet an official Mexican forecast for sugar production for MY

2015/16, the Post/New forecast is 6.5 MMT-RV. According to recent reports, renewal of cane fields

continues. Final production will depend on timely maintenance of sugar mills, appropriate cultivation

practices, weather throughout the growing season, and harvest conditions.

In March 2015, the Mexican National Committee for the Sustainable Development of Sugar Cane

(CONADESUCA) issued a second estimate of Sweeteners Production for MY 2014/15 setting sugar

production at 6.5 MMT-RV (6.15 MMT- Actual Weight). Nonetheless, due to weather issues and heavy

rainfall during March 2015, the Post/New estimate is at 6.4 MMT-RV. Mill yields are estimated at 11.1

percent.

According to the Advance Report # 22, from April 4, 2015, the harvest is advancing with respect to the

first estimate of 63 percent of area harvested, 68 percent of milled sugarcane, and 67 percent of sugar

production. However, there is an accumulated deficit of sugar production of 320,363 MT Actual

Weight (339,584 MT-RV) in the current output compared to the first estimate of sugar production (See

Table 1). Official production estimates in Mexico for MY 2013/14 remain unchanged from previous

estimates.

Table 1. Mexico -Sugar Production – Week 27

MY 2014/15 Area Harvested

(Has)

Milled cane

(MT)

Sugar production (MT-Actual

Weight) Mill

Yield

%

Current MY

2014/2015

514,936 37,586,491 4,179,641 11.12

1st. Estimate 2014/15 601,082 40,775,620 4,500,005 11.04

Source: CONADESUCA Report #22 for 2014/15 April 4, 2015

According to reports from CONADESUCA, fifty mills were operating throughout the country by April

2015 and CONADESUCA is expecting two more mills to begin processing soon. Due to rainfall,

Sugar

MX5017 Mexico Sugar Annual Report Page 3

harvesting of sugarcane has been slower than expected and is currently about eight percent behind the

first estimates for MY 2014/15. Some areas in northern Veracruz could slow down harvesting due to

the March rainfall.

Growers are organized within two major unions that represent over 95 percent of all cane growers.

These unions are the National Sugarcane Growers (affiliated with the CNC- a strong organization of

peasants/small agricultural producers that is very close to the ruling PRI Party) and the National

Association of Sugarcane Growers (CNPR). All growers operate with contracts to deliver their cane to

contracting mills. In exchange, they receive technical support and agrochemicals from the mills to grow

cane. The industry has been fostering better working relationships between mills and sugarcane grower

associations to better integrate overall sugar production.

Sugarcane Production

Although there is no official Mexican forecast for sugarcane production for MY 2015/16, based on past

performance, the Post/New forecast of cane to be processed is 55.0 MMT. This forecast is close to

Post’s cane production estimate for the current year, as market uncertainties are not encouraging

investments in cane production. Final production will depend on appropriate cultivation practices and

weather conditions throughout the growing season. Current price uncertainties may discourage best

management practices (e.g., less fertilizer applications) and expansion of production areas. The

Post/New estimate for sugarcane production to be processed for MY 2014/15 was revised downward

from previous estimates to 55.0 MMT. The industry estimates overall cane yields at 67.3 MT/hectare

(Ha) for MY 2014/15, slightly lower than MY 2013/14 yields of 68.7 MT/Ha. Sugarcane production for

MY 2013/14 remains unchanged.

As previously reported, virtually all sugarcane goes to the production of centrifugal sugar. Mills operate

between November and May to coincide with the cane harvest. Although there is no official Mexican

MY 2015/16 forecast for cane planted area, it is expected that area will continue at about the same or

836,000 Ha. According to the information service SAGARPA/SIAP, area planted data includes area

planted in past marketing years, as well as additional new areas, since the growing phase of this crop is

approximately 18 months. In addition to sugar prices, area expansion will depend on weather

conditions, production cost changes, and the level of continued investment by sugar mills. Post/New

estimate for MY 2014/15 for area planted was revised slightly downwards to 835,000 Ha and the

estimate for area harvested was revised upward to 816,000 Ha, based on CONADESUCA’s estimates.

The Post/New MY 2013/14 planted and harvested estimates remain unchanged.

Sugarcane Reference Price

Cane growers receive payment for their cane from sugar mills. The price is negotiated each year and is

based on a complex formula involving sugar prices and other domestic and international market

conditions. These factors are used to determine the Sugarcane Reference Price. According to Article 58

MX5017 Mexico Sugar Annual Report Page 4

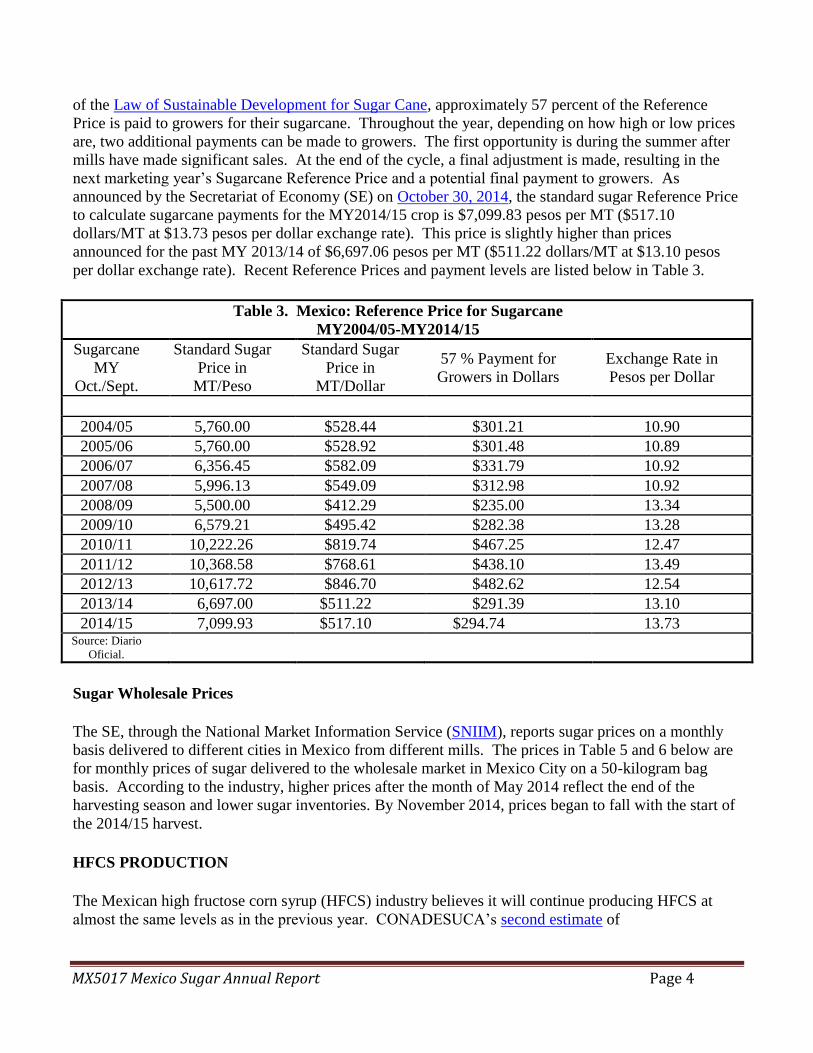

of the Law of Sustainable Development for Sugar Cane, approximately 57 percent of the Reference

Price is paid to growers for their sugarcane. Throughout the year, depending on how high or low prices

are, two additional payments can be made to growers. The first opportunity is during the summer after

mills have made significant sales. At the end of the cycle, a final adjustment is made, resulting in the

next marketing year’s Sugarcane Reference Price and a potential final payment to growers. As

announced by the Secretariat of Economy (SE) on October 30, 2014, the standard sugar Reference Price

to calculate sugarcane payments for the MY2014/15 crop is $7,099.83 pesos per MT ($517.10

dollars/MT at $13.73 pesos per dollar exchange rate). This price is slightly higher than prices

announced for the past MY 2013/14 of $6,697.06 pesos per MT ($511.22 dollars/MT at $13.10 pesos

per dollar exchange rate). Recent Reference Prices and payment levels are listed below in Table 3.

Table 3. Mexico: Reference Price for Sugarcane MY2004/05-MY2014/15

Sugarcane

MY

Oct./Sept.

Standard Sugar

Price in MT/Peso

Standard Sugar

Price in MT/Dollar

57 % Payment for

Growers in Dollars Exchange Rate in

Pesos per Dollar

2004/05 5,760.00 $528.44 $301.21 10.90

2005/06 5,760.00 $528.92 $301.48 10.89

2006/07 6,356.45 $582.09 $331.79 10.92

2007/08 5,996.13 $549.09 $312.98 10.92

2008/09 5,500.00 $412.29 $235.00 13.34

2009/10 6,579.21 $495.42 $282.38 13.28

2010/11 10,222.26 $819.74 $467.25 12.47

2011/12 10,368.58 $768.61 $438.10 13.49

2012/13 10,617.72 $846.70 $482.62 12.54

2013/14 6,697.00 $511.22 $291.39 13.10

2014/15 7,099.93 $517.10 $294.74 13.73 Source: Diario

Oficial.

Sugar Wholesale Prices

The SE, through the National Market Information Service (SNIIM), reports sugar prices on a monthly

basis delivered to different cities in Mexico from different mills. The prices in Table 5 and 6 below are

for monthly prices of sugar delivered to the wholesale market in Mexico City on a 50-kilogram bag

basis. According to the industry, higher prices after the month of May 2014 reflect the end of the

harvesting season and lower sugar inventories. By November 2014, prices began to fall with the start of

the 2014/15 harvest.

HFCS PRODUCTION

The Mexican high fructose corn syrup (HFCS) industry believes it will continue producing HFCS at

almost the same levels as in the previous year. CONADESUCA’s second estimate of

MX5017 Mexico Sugar Annual Report Page 5

Sweeteners Production for MY 2014/15 increased its HFCS domestic production estimate to 503,186

MT dry basis compared to 498,820 MT dry basis in MY 2013/14. This level is nearly at the industry’s

maximum capacity. Industry members indicate that there is no additional HFCS manufacturing

capacity being built or expanded in Mexico. Sources report that as long as HFCS prices remain

competitive, it is easier and more financially prudent to import the remainder of the HFCS demand.

The Mexican HFCS industry produces fructose with domestic and imported U.S. yellow corn.

According to IDAQUIM, the industry group that represents HFCS producers, this industry consumes

about two million tons of yellow corn of which 80 to 90 percent is imported. The Government of

Mexico continues to encourage forward contract purchases between Mexican farmers and yellow corn

buyers in an attempt to increase domestic production of yellow corn but it seems the results have not

been as optimistic as expected and domestic production of yellow corn remains small. Currently the

State of Chihuahua produces about 1.2 million tons of yellow corn and the State of Jalisco produces

about 400,000 tons of yellow corn. The United States will remain the main supplier of yellow corn to

Mexico.

CONSUMPTION

Sugar and HFCS

Assuming current pricing trends for sugar and fluctuating exchange rates, the sugar industry could

expect sugar consumption for MY 2015/16 to grow at a rate slower than last year. Therefore, the

Post/New forecast for domestic consumption for MY 2015/16 is 4.53 MMT-RV. Consumption will

also depend on the substitution of sugar by HFCS.

As reported in January 2014, a value added tax of $1.00 peso/liter (US $0.076/liter) was imposed on

artificially sweetened soft drinks. During the first quarter of 2014, soft drink sales dropped more than

five percent, followed by a four percent drop in sales the second quarter, and a two percent decline the

second half of the year. This decrease in soft drink consumption weakened demand for HFCS and

caused some soft drink producers to alter their recipes to use more sugar, which is currently cheaper

than HFCS. The Post/New estimate for domestic sugar consumption for MY 2014/15 was revised

upward accordingly based on recent official estimates to 4.50 MMT-RV. This increase is also a

consequence of the implementation of the suspension agreements, as less sugar will be exported to the

United States making more sugar available for consumption in the domestic market and pressuring

prices downward. (See Trade Section). The Post/New domestic sugar consumption estimate for MY

2013/14 remains unchanged from previous estimates.

Substitution between HFCS and sugar has been increasing in several industries, including soda bottling

(the largest user of HFCS), over the last few years. However, this change was not enough to increase

consumption as much as previously expected. Trends indicate that substitution between sugar and

HFCS will likely result in a 1.5 percent decrease in HFCS consumption in MY 2014/15 or 1.35 MMT

dry basis. This volume of HFCS represents about 23.5 percent of total domestic sweeteners

consumption. HFCS consumption depends on domestic sugar prices, imported corn prices, and more

importantly on current exchange rates.

Consumption of HFCS for MY 2013/14 remains at 1.37 MMT dry basis, lower than MY 2012/13

consumption of 1.5 MMT dry basis. Industry indicated that lower sugar prices led the soft drink

MX5017 Mexico Sugar Annual Report Page 6

industry to substitute more sugar for HFCS, thus reducing HFCS consumption in their products. This

trend could continue for MY 2015/16, as Mexico is exporting smaller quantities of refined sugar to the

United States, however, bottlers are limited in their ability to substitute sugar for HFCS by infrastructure

and soda formulas. Still, there is uncertainty on how consumption of HFCS will behave due to the sugar

suspension agreements and availability of domestic sugar (See Trade Section).

TRADE

Sugar

On October 28, 2014, the United States and Mexico came to an agreement to avoid antidumping (AD)

and countervailing duties (CVD) on U.S. sugar imports from Mexico. On December 19, 2014, both

governments signed these two suspension agreements. On January 8, 2015, two U.S. industry parties

filed a petition requesting that the U.S. International Trade Commission review the suspension

agreements to determine whether they completely eliminate the injury caused by the alleged dumping of

Mexican sugar. On January 16, 2015, these two parties filed another request with the Department of

Commerce to continue the AD and CVD investigations. Thursday March 19, 2015, ITC Commissioners

voted unanimously in favor of upholding the suspension agreements. The official opinion should be

released later. Meanwhile, Mexico is complying with the agreements to be able to export sugar to the

United States.

The Post/New sugar export forecast for MY 2015/16 is 1.8 MMT-RV. This number is tentative and will

tend to change depending on production, U.S. and international sugar and sweeteners (HFCS) prices,

and the degree to which the Mexican industry is able to comply with the sugar suspension agreements.

CONADESUCA indicates that for MY 2014/15 they are expecting sugar exports at 1.9 MMT-RV, even

though the sugar sector has been concerned about domestic surpluses, falling international prices, the

suspension agreements, and finding third-country markets for Mexican sugar. Therefore, Post/New

total sugar exports estimates for MY 2014/15 were revised downward to 1.6 MMT-RV, where exports

to the United States under the suspension agreements are 1,383,969.68 MMT-RV. The rest is expected

to be exported to third-country markets.

On February 11, 2015, Mexico announced the amount of the total quota of Mexican sugar derived from

sugarcane or beets to be exported to the United States from October 2014-September 2015. The amount

was 1,162,604.75 MT-RV. This announcement was published following a previous announcement of

the guidelines, on February 6, 2015, to request and receive sugar export licenses, in accordance with the

suspension agreements. On March 30, 2015, an adjustment to the quota to be exported to the United

States was published in the Diario Oficial for a total amount of 1,383,969.68 MMT-RV, in compliance

with Point 13 of the February 6, 2015 notification. This calculation was determined based on the March

2015 World Agricultural Supply and Demand Estimates (WASDE) and Mexico’s CONADESUCA data.

The SE is in charge of closely following sugar exports via licenses so that they do not exceed the

established quota to the United States.

According to data, through March, Mexico has exported 438,242 MT-RV of sugar, mostly to the United

States. Exports are substantially lower than previous years because Mexican exporters were holding

back shipments due to the uncertainty surrounding the suspension agreements and the fact that the

guidelines to obtain export licenses were not published until the first week of February. Mexico now has

to quickly export more sugar to the United States as domestic inventories are high. The total export

number is tentative and will tend to change depending on production and the extent of substitution

MX5017 Mexico Sugar Annual Report Page 7

between sugar and alternative domestic and imported sweeteners (HFCS), and total exports under the

suspension agreements. The Mexican sugar export estimate for MY 2013/14 was revised downward

based on official data.

The Post/New sugar import forecast for MY 2015/16 is estimated at 184,000 MT-RV, as domestic

supplies are expected to remain adequate. A large portion of these imports could be used to cover the

needs of the Mexican Sugar Re-export Program industries (IMMEX). The MY 2013/14 sugar import

estimate was revised upward and MY 2014/15 estimate was revised downward from previous estimates

as domestic supplies are expected to provide more sugar for the IMMEX program.

SE recently submitted a proposal to modify the IMMEX program to Mexico’s equivalent of the Office

of Management Budget, COFEMER. This proposal states that IMMEX-certified companies can only

import sugar if that sugar does not benefit from the U.S. Sugar Re-export Program. IMMEX regulations

require that this sugar be transformed into a product with an HTS code that is not included in the Annex

II-A list so that it does not count against Mexico’s sugar export limit to the United States, and then

exported within a specific timeframe. This proposal is intended to comply with the sugar suspension

agreements and is expected to become a final regulation by end of April 2015.

Sugar use under the “other disappearance” category is mainly for the IMMEX program. The Post/New

forecast for MY 2015/16 for sugar use under IMMEX is 343,000 MT-RV based on CONADESUCA’s

information. According to sources, the same industries will be using imported sugar for the processing

of their products. The Post/New estimates for sugar use under IMMEX for MY 2013/14 were revised

upward and MY 2014/15 estimates were revised downward from previous estimates as more domestic

sugar is being used for the IMMEX program. The Government of Mexico is reporting IMMEX sugar

use for MY 2014/15 under the consumption section, whereas before it was reported under the sugar

export section.

HFCS Imports

The HFCS import forecast for MY 2015/16 is expected to be similar to MY 2014/15 imports, as sugar

has continued to be accessible, and the U.S. dollar exchange rate versus the Mexican peso has increased,

thus making HFCS imports more expensive. According to CONADESUCA’s second estimate, imports

of HFCS for MY 2014/15 will be about 880,600 MMT dry basis compared to MY 2013/14 imports of

912,535 MMT dry basis. Imports of HFCS slowed down during 2014, especially the first semester, due

to lower consumption of soft drinks resulting from the special tax on calorically sweetened drinks (See

Consumption Section).

STOCKS

The Post/New sugar ending stock forecast for MY 2015/16 is 1.0 MMT-RV based on expected sugar

production. However, sugar prices and exports will determine the final data. Post/New stocks for MY

2014/15 are likely to end at 1.0 MT-RV based on lower than expected sugar exports. The Post/New

sugar ending stock estimate for MY2013/14 remains unchanged at 881,000 MT-RV.

Sugar stocks in Mexico are held by both government mills and private mills and traders.

MX5017 Mexico Sugar Annual Report Page 8

POLICY

Selling of State Owned Sugar Mills

On March 26, 2015, Mexico’s Service of Administration and Disposition of Assets (SAE) announced

the public tender of nine sugar mills that were administered by FEESA, a fund created in 2001 to

administer the government expropriated sugar mills. The mills are: El Potrero, El Modelo, Providencia,

San Cristobal, and San Miguelito from the State of Veracruz, Casasano and Emiliano Zapata from the

State of Morelos, Plan de San Luis in the State of San Luis Potosi, and finally Atencingo in the State of

Puebla. The mills will be offered in five packages. Additional information on the mills such as location,

production, general information of the sugar sector in Mexico, and how to participate in the tender, can

be found at the SAE’s page as follows: http://ingenios.sae.gob.mx/paginas/default.aspx

Ethanol Production

The Biofuels Law, which first passed the Mexican Congress on April 26, 2007, and was amended in

October 2007, was published in the Diario Oficial on February 1, 2008. The Law contains a

comprehensive biofuels policy that promotes ethanol production from different agricultural

commodities. According to the sugar mill industry, ethanol production from sugarcane in Mexico is

still not as profitable as producing sugar due to the high price of cane, the need for the vast majority of

production to be used for centrifugal sugar, and more importantly the lack of a domestic ethanol

market. There are, however, provisions within the Sugar Law that contain overall goals focused on the

possibility of producing ethanol. PEMEX published a public bid in September 10, 2014, to purchase

ethanol for blending into gasoline on a trial basis, and released results on March 19, 2015. Six

companies will be supplying ethanol to four PEMEX terminal plants; applications from two other

terminals were declared void. As a result of this bid, PEMEX will purchase a minimum amount of

$524.5 million dollars and a maximum of $751.2 million dollars of ethanol produced in Mexico,

through 10 year contracts, allowing a purchase of about 123 million liters per year. There is still no

clear information as to the selling price of ethanol as some sources indicate that the current price is

about $12 pesos/liter (USD$0.78/liter) and PEMEX could be buying at $8.50 pesos/liter

(USD$0.55/liter).

PEMEX indicates that in this first stage 60,000 barrels a day of gasoline blended with ethanol will be

sold in the states of Tamaulipas, San Luis Potosi, and Veracruz. The business model that has been

developed allows buying ethanol at a competitive price at the same time that PEMEX supports regional

producers of sugarcane in Veracruz and sorghum in Tamaulipas. Meanwhile, ethanol trials for blending

into gasoline have been successful in several places in Mexico including Nuevo Leon and Veracruz.

INFORMATION RESOURCES

The National Committee for the Sustainable Development of Sugar Cane (CONADESUCA)

The National Chamber for the Sugar and Alcohol Industries (CNIAA)

The National Service of Market Information (SNIIM-ECONOMIA)

STATISTICAL TABLES

Table 3. Mexico: Centrifugal Sugar PS&D

MX5017 Mexico Sugar Annual Report Page 9

Sugar, Centrifugal 2013/2014 2014/2015 2015/2016

Market Begin Year Oct 2013 Oct 2014 Oct 2016

Mexico USDA Official New post USDA Official New post USDA Official New post

Beginning Stocks 1,548 1,548 881 881 0 1,030

Beet Sugar Production 0 0 0 0 0 0

Cane Sugar Production 6,383 6,382 6,508 6,413 0 6,500

Total Sugar Production 6,383 6,382 6,508 6,413 0 6,500

Raw Imports 0 0 0 0 0 0

Refined Imp.(Raw Val) 137 183 229 184 0 184

Total Imports 137 183 229 184 0 184

Total Supply 8,068 8,113 7,618 7,478 0 7,714

Raw Exports 0 0 0 0 0 0

Refined Exp.(Raw Val) 2,644 2,545 1,779 1,600 0 1,800

Total Exports 2,644 2,545 1,779 1,600 0 1,800

Human Dom. Consumption 4,344 4,344 4,452 4,505 0 4,530

Other Disappearance 199 343 408 343 0 343

Total Use 4,543 4,687 4,860 4,848 0 4,873

Ending Stocks 881 881 979 1,030 0 1,041

Total Distribution 8,068 8,113 7,618 7,478 0 7,714

1000 MT

Table 4. Mexico: Sugar Cane for Centrifugal PS&D

Sugar Cane for Centrifugal 2013/2014 2014/2015 2015/2016

Market Begin Year Nov 2014 Nov 2015 Nov 2016

Mexico USDA Official New post USDA Official New post USDA Official New post

Area Planted 836 836 836 835 0 836

Area Harvested 790 790 790 816 0 800

Production 54,329 54,329 56,000 55,000 0 55,000

Total Supply 54,329 54,329 56,000 55,000 0 55,000

Utilization for Sugar 54,329 54,329 56,000 55,000 0 55,000

Utilization for Alcohol 0 0 0 0 0 0

Total Utilization 54,329 54,329 56,000 55,000 0 55,000

1000 HA, 1000 MT

Table 5. Mexico: Average Wholesale Sugar Prices in Mexico City MX Pesos per 50 Kilograms – Bulk (CIF Basis) Table 3. Mexico:in Mexico City

MX Pesos per 50 Kilograms – Bulk (CIF Basis) Month Standard Refined

2013 2014 Percent Change 2013 2014 Percent Change

January 371.63 380.75 2.45 434.17 430.42 (0.86)

February 393.50 345.50 (12.19) 450.83 416.83 (7.54)

March 391.00 343.25 (12.21) 458.75 422.83 (7.82) April 341.73 337.90 (1.12) 452.40 420.33 (7.08) May 309.63 362.38 17.03 410.58 426.67 3.91 June 343.13 432.50 26.04 400.17 466.25 16.51 July 337.80 422.70 25.13 393.80 462.85 17.53 August 366.92 438.75 19.57 398.75 470.00 17.86

September 349.25 457.50 30.99 391.00 487.06 24.56

MX5017 Mexico Sugar Annual Report Page 10

Table 5. Mexico: Average Wholesale Sugar Prices in Mexico City MX Pesos per 50 Kilograms – Bulk (CIF Basis) Table 3. Mexico:in Mexico City

MX Pesos per 50 Kilograms – Bulk (CIF Basis) October 310.10 456.50 47.21 379.67 493.84 30.00

November 365.50 431.00 17.92 379.59 509.92 34.33

December 399.73 397.80 00.13 435.70 525.93 21.16

Source: Servicio Nacional de Información de Mercados SNIIM-ECONOMIA

Table Table 6. Mexico: Average Wholesale Sugar Prices in Mexico City MX Pesos per 50 Kilograms – Bulk (CIF Basis) Table 4. Mexico: rams – Bulk (CIF

Basis) Month Standard Refined

2014 2015 Percent Change 2014 2015 Percent Change

January 380.75 387.25 1.70 430.42 498.42 15.79

February 345.50 378.50 9.55 416.83 492.92 18.61

March 343.25 370.60 7.96 422.83 486.07 14.95

April 337.90 385.00* 13.93 420.33 481.67* 14.59

May 362.38 426.67

June 432.50 466.25

July 422.70 462.85

August 438.75 470.00

September 457.50 487.06

October 456.50 493.84

November 431.00 509.92

December 397.80 525.93

Source: Servicio Nacional de Información de Mercados SNIIM-ECONOMIA

*Through 1st Week of April 2015

Table 7. Mexico: Monthly Exchange Rate

Averages for 2012-2015

MX Pesos per U.S. $1.00

2012 2013 2014 2015

January 13.46 12.71 13.20 14.68

February 12.79 12.69 13.28 14.92

March 12.75 12.54 13.22 15.21

April 13.05 12.21 13.29 15.02*

May 13.60 12.95 12.93

June 13.94 12.94 12.99

July 13.37 12.77 12.97

August 13.18 12.89 13.14

September 12.95 13.08 13.21

October 12.88 13.00 13.47

MX5017 Mexico Sugar Annual Report Page 11

November 13.08 13.07 13.59

December 12.86 13.00 14.44

Annual Avg 13.15 12.76 13.29

*As of 1st Week of April 2015 Source: Mexican Federal Register Note: Monthly rates are averages of daily exchange rates from the Banco de Mexico

Table 8. Mexico: Trade Matrices HFCS Trade

HFCS 1702460 Unit: Metric Tons Dry Basis

Exports for MY 2013/14 (Oct-Sept) to: Imports for MY 2013/14 (Oct-Sept) from:

U.S. 21,853 U.S. 824,821

Germany 3,689 Canada 2,793

Other 8,078 Other 0

TOTAL 33,620 TOTAL 827,614

SOURCE: Global Trade Information Services, Inc. Global Trade Atlas, Mexico Edition, December 2014

HFCS 1702440 Unit: Metric Tons Dry Basis

Exports for MY 2013/14 (Oct-Sept) to: Imports for MY 2013/14 (Oct-Sept) from:

U.S. 160 U.S. 56,254

Other 34 Other 26

TOTAL 194 TOTAL 56,280

SOURCE: Global Trade Information Services, Inc. Global Trade Atlas, Mexico Edition, December 2014

Other Relevant Reports Submitted by FAS/Mexico:

Report

Number Subject Date Submitted

MX 5013

Mexico Increases Maximum Sugar Export Limit to the U.S. 03/30/2015

MX 5012 Mexico Puts State-Owned Sugar Mills Up for Sale 03/30/2015

MX 5007

Mexico Announces Maximum Sugar Export Quota 02/11/2015

MX 5006 Mexico Announces Guidelines for Sugar Export Licenses 02/09/2015

MX 4076 Mexico Announces Sugar Cane Reference Prices 10/31/2014

MX 4067

Sugar Semi-Annual 09/30/2014

MX5017 Mexico Sugar Annual Report Page 12

For More Information

FAS/Mexico Web Site: We are available at http://www.mexico-usda.com.mx or visit the FAS

headquarters' home page at www.fas.usda.gov for a complete selection of FAS worldwide agricultural

reporting.

Useful Mexican Web Sites: Mexico's equivalent of the U.S. Department of Agriculture (SAGARPA)

can be found at www.sagarpa.gob.mx, the equivalent of the U.S. Department of Commerce (SE) can be

found at www.economia.gob.mx, and the equivalent of the U.S. Food and Drug Administration

(SALUD) can be found at www.salud.gob.mx. These web sites are mentioned for the reader's

convenience but USDA does NOT in any way endorse, guarantee the accuracy of, or necessarily concur

with, the information contained on the mentioned sites.