Metsä Board, January-June 2017 results presentation

26

Metsä Board Half Year Report 1 − 6/2017 Presentation material

-

Upload

metsa-board -

Category

Investor Relations

-

view

1.631 -

download

0

Transcript of Metsä Board, January-June 2017 results presentation

Metsä BoardHalf Year Report 1−6/2017Presentation material

• Good demand for high-quality paperboardscontinued

• Stable or rising market price levels• Metsä Board’s paperboard deliveries up by 11%

from Q1 2017• The average price of folding boxboard was

burdened by Husum’s geographic sales mix• Steady working capital despite the strong sales

growth• New extrusion coating line in Husum started up

2017 Half Year Report2

Q2 2017 in summary

All-time high in paperboard deliveries

204 213 224 224 227 250 266 245 265 304

130 141 137 131 142148 148

143163

173

0

100

200

300

400

500

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

Folding boxboard White fresh fibre linerboard

1,00

0 to

nnes

Growth in total paperboarddeliveries:

+11% Q2/17 vs. Q1/17

+18% H1/17 vs. H1/16

+12% FY16 vs. FY15

3 2017 Half Year Report

FY 2015:1.4m tonnes

FY 2016:1.6m tonnes

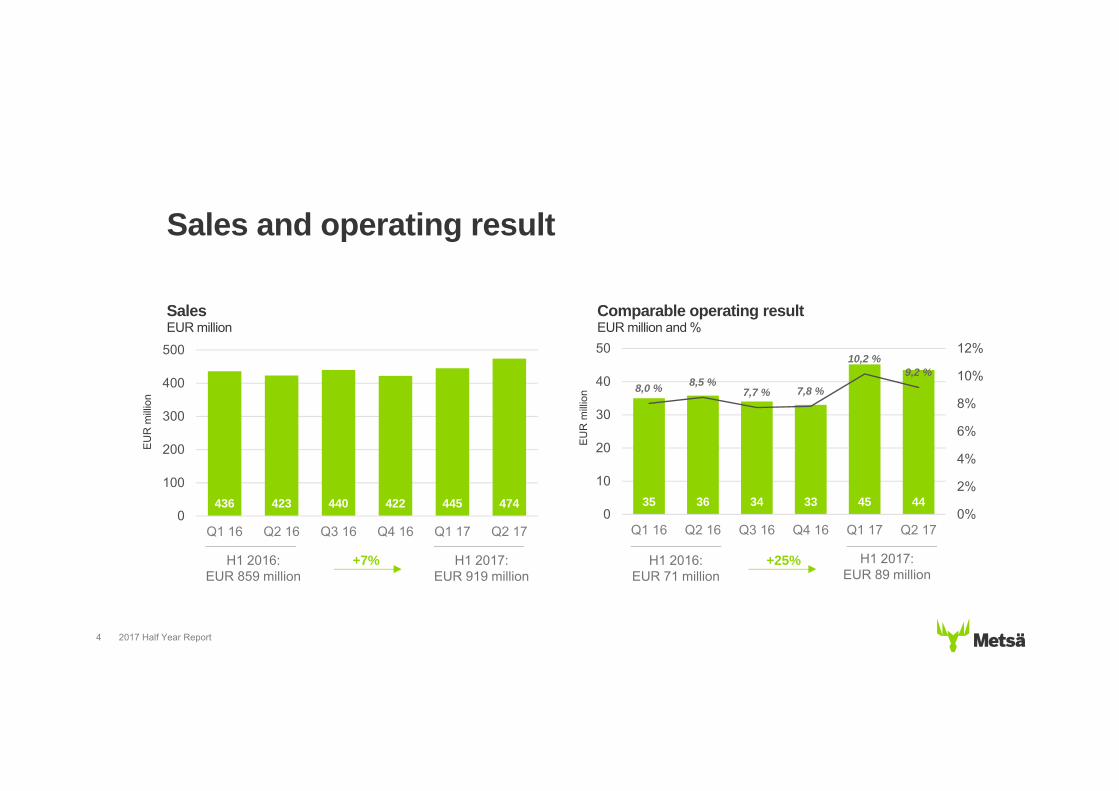

Sales and operating result

SalesEUR million

436 423 440 422 445 4740

100

200

300

400

500

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17

+7%

35 36 34 33 45 44

8,0 % 8,5 %7,7 % 7,8 %

10,2 %9,2 %

0%

2%

4%

6%

8%

10%

12%

0

10

20

30

40

50

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17

+25%

2017 Half Year Report4

Comparable operating resultEUR million and %

H1 2016:EUR 859 million

EU

R m

illio

n

EU

R m

illio

n

H1 2017:EUR 919 million

H1 2016:EUR 71 million

H1 2017:EUR 89 million

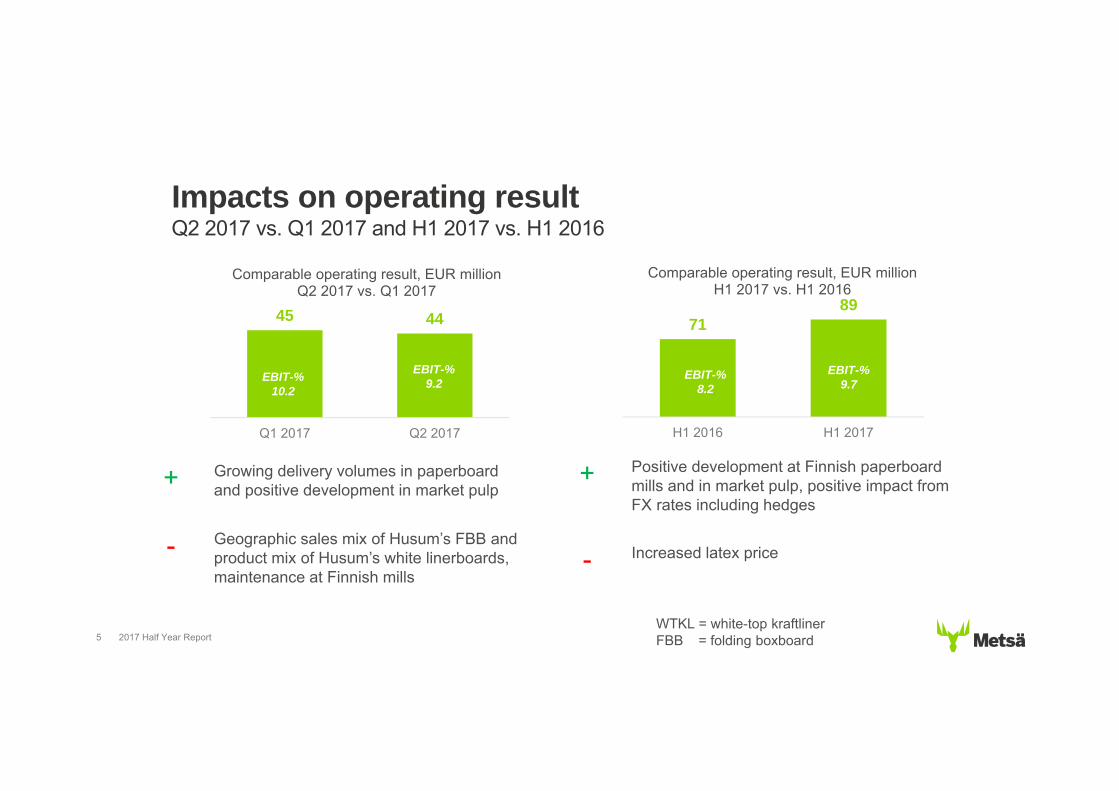

45 44

01020304050

Q1 2017 Q2 2017

Comparable operating result, EUR millionQ2 2017 vs. Q1 2017

2017 Half Year Report5

Impacts on operating resultQ2 2017 vs. Q1 2017 and H1 2017 vs. H1 2016

7189

0102030405060708090

H1 2016 H1 2017

Comparable operating result, EUR millionH1 2017 vs. H1 2016

+ Growing delivery volumes in paperboardand positive development in market pulp

- Geographic sales mix of Husum’s FBB and product mix of Husum’s white linerboards, maintenance at Finnish mills

+ Positive development at Finnish paperboardmills and in market pulp, positive impact fromFX rates including hedges

- Increased latex price

EBIT-%8.2

EBIT-%9.7EBIT-%

10.2

EBIT-%9.2

WTKL = white-top kraftlinerFBB = folding boxboard

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

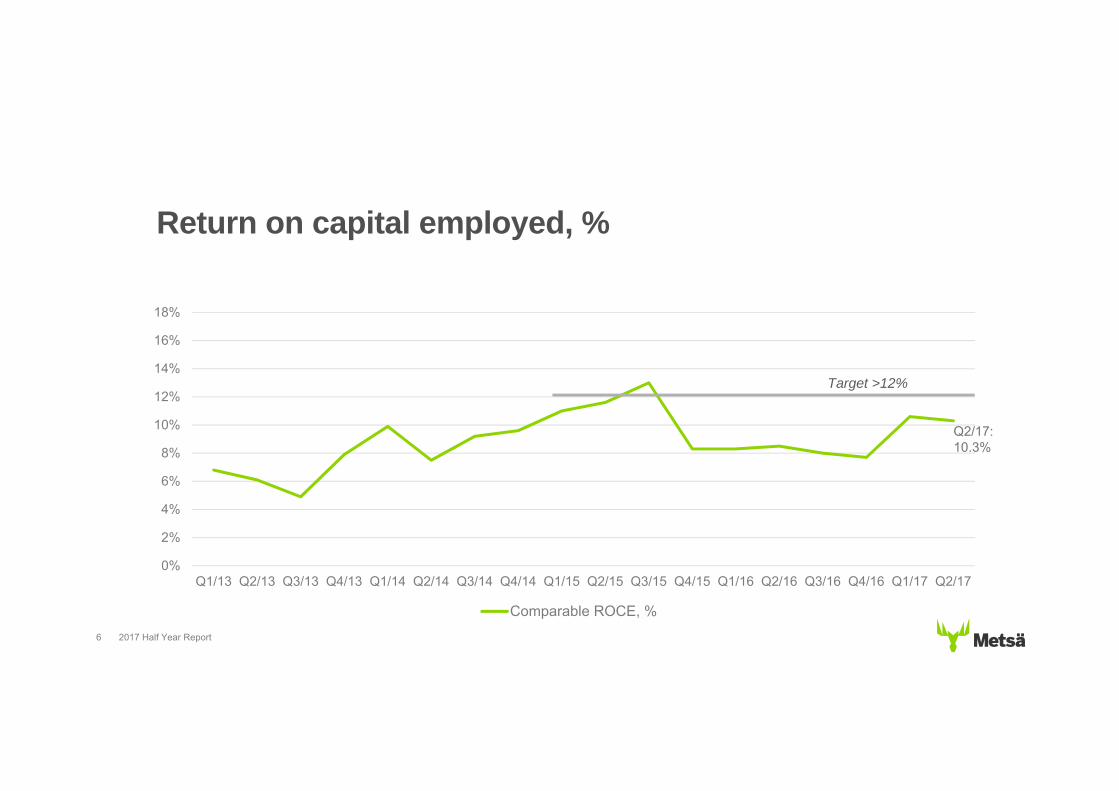

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

Comparable ROCE, %

2017 Half Year Report6

Return on capital employed, %

Target >12%

Q2/17:10.3%

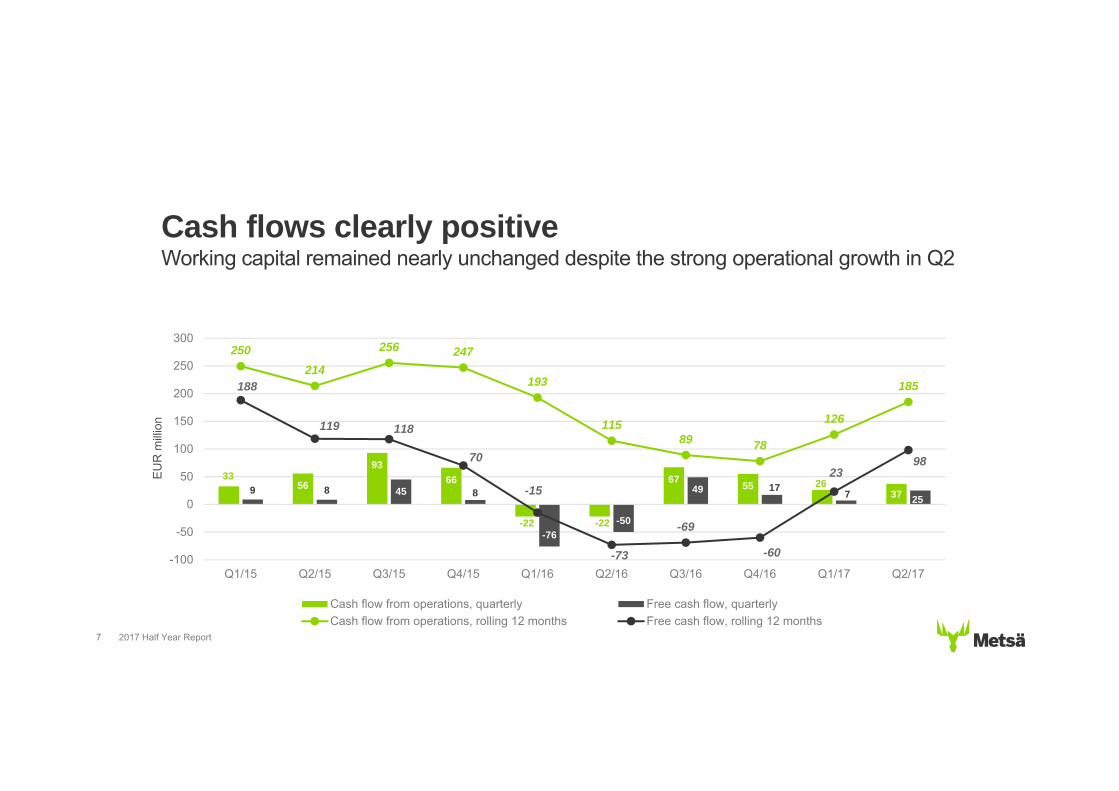

Cash flows clearly positiveWorking capital remained nearly unchanged despite the strong operational growth in Q2

3356

9366

-22 -22

67 55 26379 8 45 8

-76-50

49 17 7 25

250214

256 247

193

11589 78

126

185188

119 118

70

-15

-73

-69

-60

2398

-100

-50

0

50

100

150

200

250

300

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17

Cash flow from operations, quarterly Free cash flow, quarterlyCash flow from operations, rolling 12 months Free cash flow, rolling 12 months

EUR

milli

on

7 2017 Half Year Report

Stable balance sheet

333 464 541 488 464 458 495

1,2

2,0 2,1 2,1 2,0 1,9 2,0

0,0

1,0

2,0

3,0

0

200

400

600

2015 2016 6/16 9/16 12/16 3/17 6/17

Interest-bearing net debt, EUR millionInterest-bearing net debt / EBITDA (rolling 12-month)

Interest-bearing net debt / comparable EBITDA

333 464 541 488 464 458 495

32%

44%

54%49%

44% 44% 45%

0

0,1

0,2

0,3

0,4

0,5

0,6

0

200

400

600

2015 2016 6/16 9/16 12/16 3/17 6/17

Interest-bearing net debt, EUR millionNet gearing, %

Net gearing, %

8 2017 Half Year Report

Financial target: <2.5x

9

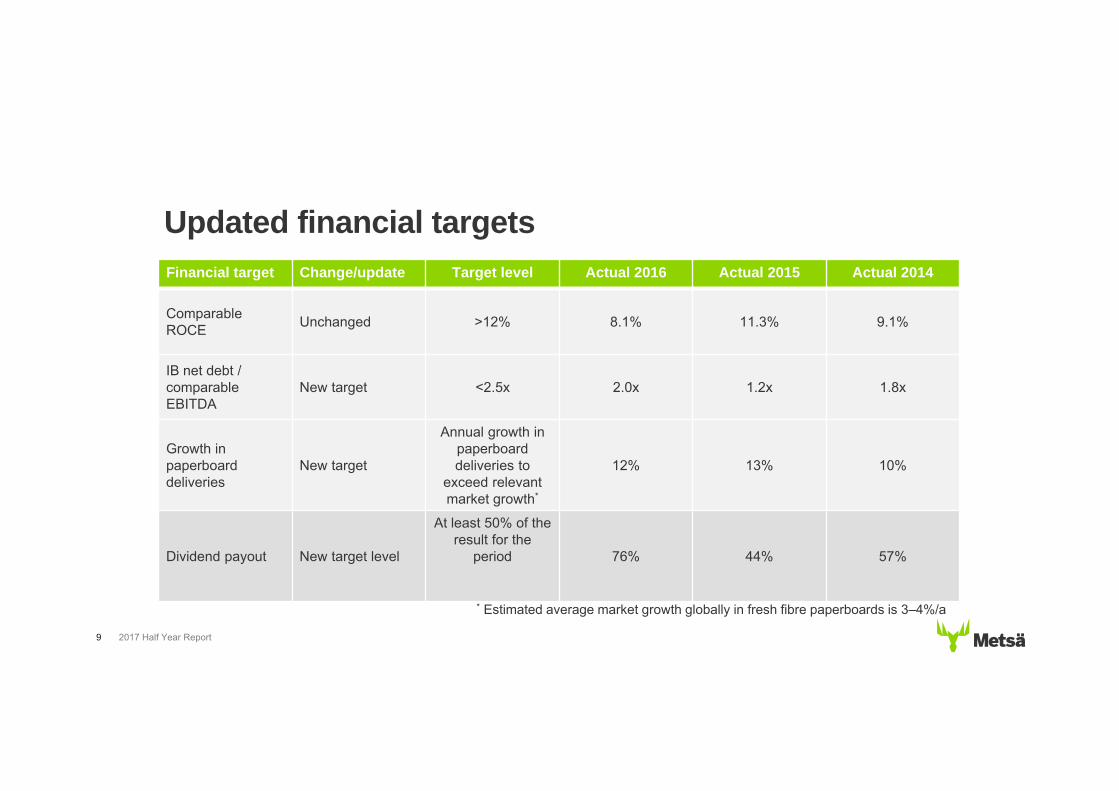

Updated financial targetsFinancial target Change/update Target level Actual 2016 Actual 2015 Actual 2014

ComparableROCE Unchanged >12% 8.1% 11.3% 9.1%

IB net debt / comparableEBITDA

New target <2.5x 2.0x 1.2x 1.8x

Growth in paperboarddeliveries

New target

Annual growth in paperboarddeliveries to

exceed relevant market growth*

12% 13% 10%

Dividend payout New target level

At least 50% of theresult for the

period 76% 44% 57%

* Estimated average market growth globally in fresh fibre paperboards is 3–4%/a

2017 Half Year Report

• Capacity utilisation rate during H1 2017 was 70%– In June, both production and deliveries were over 85% of

monthly capacity – The target of having the capacity in full use by end of 2018

is intact

• Production costs per tonne still higher compared to Finnish mills

• Geographic sales mix burdened the average price• Deliveries of own PE-coated paperboards to customers

have started

2017 Half Year Report10

Update on Husum’s foldingboxboard

11

Potential to improve profitability of HusumAt least EUR 100 million EBIT improvement from 2016 to 2019

2016 2019

+ EUR

25 million+ EUR

5 million+ EUR

>70 million

120,000 tonnesof pulp

productionlost in 2016

Restructuring:

Efficiency improvementprogramme

FBB capacityutilisation rate

>95% withnormal sales

price

2017 Half Year Report

Better consumer experiences with less environmental impact

Metsä Board approach for challenges of today

Betterwith Less

2017 Half Year Report12

2017 Half Year Report13

Near-term outlook

• Price levels in FBB are expected to be stable, several linerboard producers have announced price increases. Pulp market expected to remain in balance

• Metsä Board’s Q3 paperboard delivery volumes are expected to stay flat compared to Q2

• Focus on improving the geographic sales mix of Husum’s folding boxboard and to increase the share of North American sales, in particular

• Start-up phase of Metsä Fibre’s new bioproduct mill is expected to have only a minor negative impact on Metsä Board’s result

Metsä Board's comparable operating result for the third quarter of 2017 is expected to improve slightly compared to the second quarter of 2017.

2017 Half Year Report14

Profit guidance

• Good demand in high-qualitypaperboards is continuing

• Metsä Board’s paperboard deliveryvolumes grew strongly during H1 2017

• The target of having the currentpaperboard capacity in full use by theend of 2018 is intact

• Renewed key messages and unifiedproduct portfolio support sales growth

2017 Half Year Report15

Summary

Appendix

2017 Half Year Report17

Key financialsQ2/17 Q1/17

ChangeQ2/17

vs. Q1/17H1/17 H1/16

ChangeH1/17

vs. H1/162016

Sales EUR, m 474 445 +7% 919 859 +7% 1,720

EBITDA* EUR, m 68 69 -1% 136 119 +14% 231

Operating result* EUR, m 44 45 -2% 89 71 +25% 138

% of sales % 9.2 10.2 9.7 8.2 8.0

Result before taxes* EUR, m 37 40 -8% 77 57 +35% 107

Earnings per share EUR 0.09 0.10 -10% 0.19 0.13 +46% 0.25

ROCE* % 10.3 10.6 10.3 8.4 8.1

Capex EUR, m 12 19 -37% 31 103 -70% 162

Cash flow from operations EUR, m 37 26 +42% 63 -45 77

IB Net debt, at end of period EUR, m 495 458 +8% 495 541 -9% 464*comparable

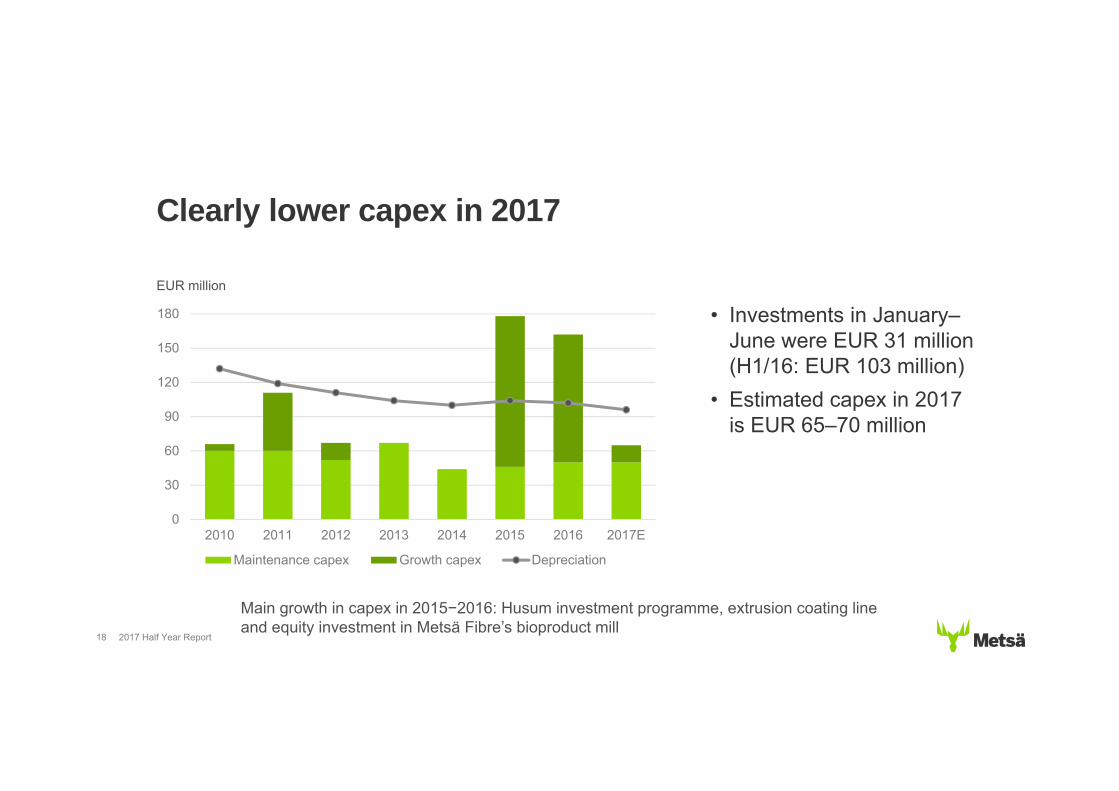

• Investments in January–June were EUR 31 million (H1/16: EUR 103 million)

• Estimated capex in 2017 is EUR 65–70 million

Clearly lower capex in 2017

0

30

60

90

120

150

180

2010 2011 2012 2013 2014 2015 2016 2017E

Maintenance capex Growth capex Depreciation

EUR million

18 2017 Half Year Report

Main growth in capex in 2015−2016: Husum investment programme, extrusion coating line and equity investment in Metsä Fibre’s bioproduct mill

Impact of FX rate changes including hedges– Q2 2017 vs. Q1 2017: EUR -1.5 million– H1 2017 vs. H1 2016: EUR 11 million

FX exposure and sensitivities

58 %35 %

5 %2 %USD

SEK

GBP

Othercurrencies

Annual transaction exposureEUR 1.1 billion

FX sensitivities excluding hedges

10% strengthening of foreign currency vs. EUR will have an impact on Metsä Board’s EBIT of

Currency Next 12 months

USD, $ EUR +70 million

SEK EUR -40 million

GBP, £ EUR +7 million

19 2017 Half Year Report Hedging policy: 100% of balance sheet position and 50% of annual net FX flows

Debt structure and liquidity30 June 2017

223

149111

23

134

Bonds

Loans fromfinancial institutions

Pension loans

Finance leases andother loans

Other short-termloans

141

100

102

Cash and cashequivalentsRevolving creditfacilityUnraised pensionloans

Interest-bearing debt, total EUR 640 million

Available liquidity, total EUR 343 million

Average maturity of long-term loans on 30 June 2017 was 2.0 years. 20 2017 Half Year Report

Long-term debt and financial costs

Net financial costs (EUR million) and average interest rate (%)

Maturity schedule in long-term IB debtEUR million

8242

258

174

1 2

100 102

0

50

100

150

200

250

300

2017 2018 2019 2020 2021 >2022

Long-term interest bearing liabilities, EUR million

Committed undrawn credit facilities, EUR million

21 2017 Half Year Report

56 39 32 31 12

4,6

4,2

3,8

3,3 3,3

3,0

3,5

4,0

4,5

5,0

0

15

30

45

60

2013 2014 2015 2016 H1/2017

Net financial costs, EUR million

Average interest rate at the end of period, %

500

600

700

800

900

1000

1100

1200

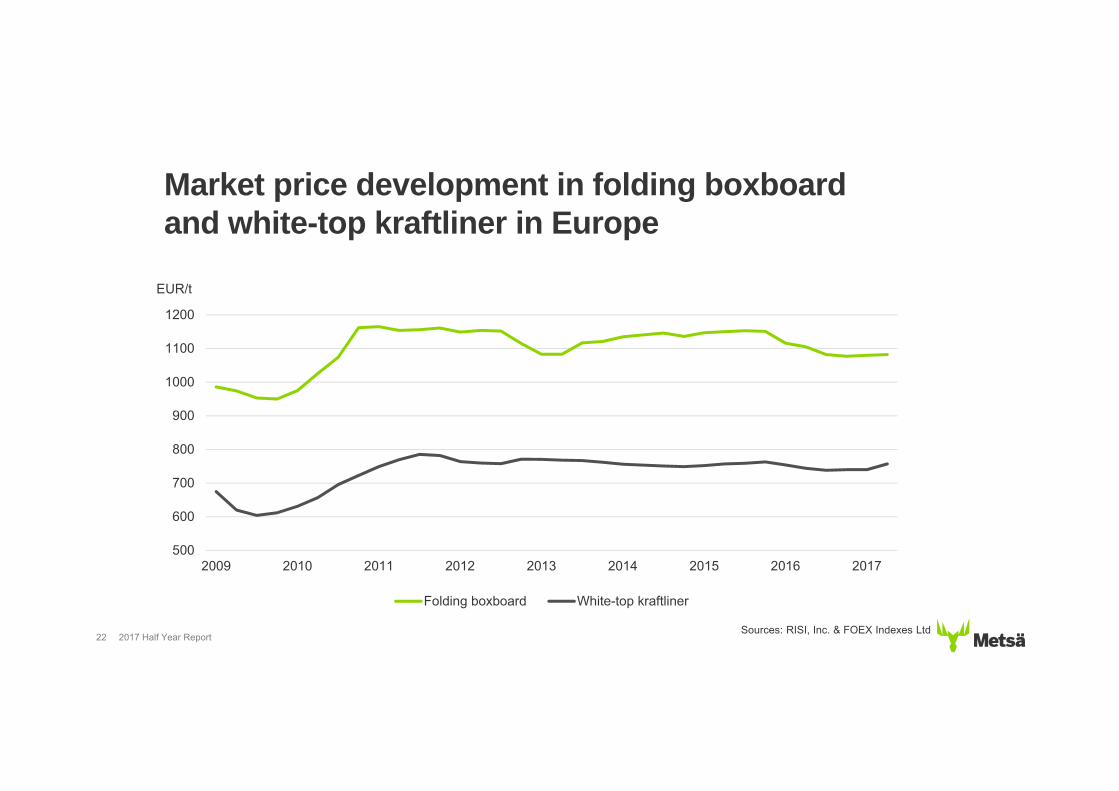

2009 2010 2011 2012 2013 2014 2015 2016 2017

Folding boxboard White-top kraftliner

2017 Half Year Report22

Market price development in folding boxboard and white-top kraftliner in Europe

EUR/t

Sources: RISI, Inc. & FOEX Indexes Ltd

Source: Foex Indexes Ltd

Softwood, USD

Softwood, EUR

Hardwood, EUR

Hardwood, USD

USDEUR

Pulp price development (PIX)

23

350400450

500550600650

700750800850900

95010001050

'10 '11 '12 '13 '14 '15 '16 '17350400450

500550600650

700750800850900

95010001050

2017 Half Year Report

• Metsä Board’s dividend payout target is at least 50% of the result for the financial period

• Dividend for 2016:– EUR 0.19 per share– Totalling EUR 68 million– Corresponds to 76% of EPS 0

0,1

0,2

0,3

0,4

0,5

2012 2013 2014 2015 2016

Earnings per share Dividend per share

2017 Half Year Report24

Steadily growing dividends

EUR

Market cap and foreign owners30 June 2017

Ownership distribution30 June 2017

Market cap and ownership distribution

0

4

8

12

16

20

24

0

500

1 000

1 500

2 000

2 500

2012 2013 2014 2015 2016 1-6/2017

Market cap, EUR million

Share of foreign owners, %

42 %

22 %

18 %

18 % MetsäliittoCooperative

Domestic institutionalinvestors

Domestic privateinvestors

Foreign owners

EUR million

* Metsäliitto Cooperative has 61% of voting rights

*

25

%

2017 Half Year Report

In Q2 2017, a total of 8,969 Metsä Board A shares were converted to B shares. After the conversion, the amount of A-shares is 35,886,682 and the amount of B-shares 319,626,064.