METHODOLOGY GUIDE- VALUING GRAIN ELEVATORS IN ONTARIO

18

METHODOLOGY GUIDE VALUING GRAIN ELEVATORS IN ONTARIO Valuation Date: January 1, 2016 AUGUST 2016

Transcript of METHODOLOGY GUIDE- VALUING GRAIN ELEVATORS IN ONTARIO

METHODOLOGYGUIDEVALUINGGRAINELEVATORSINONTARIO

ValuationDate:January1,2016

AUGUST2016

August22,2016

TheMunicipalPropertyAssessmentCorporation(MPAC)isresponsibleforaccuratelyassessingandclassifyingpropertyinOntarioforthepurposesofmunicipalandeducationtaxes.

InOntario’sassessmentsystem,MPACassessesyourpropertyvalueeveryfouryears.Thisyear,MPACisupdatingthevalueofeverypropertyintheprovincetoreflectthelegislatedvaluationdateofJanuary1,2016.MPACiscommittedtoprovideOntariopropertyowners,municipalitiesandallitsstakeholderswiththebestpossibleservicethroughtransparency,predictabilityandaccuracyinvalues.Aspartofthiscommitment,MPAChasdefinedthreelevelsofdisclosureofinformationinsupportofitsdeliveryofthisyear’sassessmentupdate.ThisMethodologyGuideisthefirstlevelofinformationdisclosure.ThisguideprovidesanoverviewofthevaluationmethodologyundertakenbyMPACwhenassessinggrainelevatorsforthisyear’supdateensuringthemethodologyforvaluingthesepropertiesiswelldocumentedandinalignmentwithindustrystandards.

Propertyownerscanaccessadditionalinformationabouttheirownpropertiesthroughaboutmyproperty.ca.Logininformationforaboutmyproperty.caisprovidedoneachPropertyAssessmentNoticemailedthisyear.AdditionalinformationaboutMPACcanbeaccessedatmpac.ca.

AntoniWisniowskiPresidentandChiefAdministrativeOfficer

RoseMcLean,M.I.M.A.ChiefOperatingOfficer

TableofContents

1.0INTRODUCTION................................................................................................................4

1.1PROPERTIESCOVEREDBYTHISMETHODOLOGYGUIDE......................................................................4

1.2LEGISLATION.............................................................................................................................5

1.3CLASSIFICATION.........................................................................................................................6

1.4THEUSEOFTHISMETHODOLOGYGUIDE.......................................................................................7

1.5CONSULTATIONANDDISCLOSURE.................................................................................................7

2.0THEVALUATIONPROCESS.................................................................................................9

2.1OUTLINE..................................................................................................................................9

2.2APPROACH.............................................................................................................................10

2.3DATACOLLECTION...................................................................................................................10

2.4DATAANALYSIS.......................................................................................................................12

2.5VALUATION............................................................................................................................12

2.6VALIDATINGTHERESULTS..........................................................................................................12

3.0THEVALUATION..............................................................................................................13

3.1COSTAPPROACHOVERVIEW......................................................................................................13

3.2LANDVALUATION....................................................................................................................14

3.3BUILDINGANDSITEIMPROVEMENTS............................................................................................14

3.4ESTABLISHINGCOSTNEW..........................................................................................................15

3.5DEDUCTINGDEPRECIATION/OBSOLESCENCE..................................................................................15

3.6MARKETVALUECONCLUSION....................................................................................................16

3.7CURRENTVALUEASSESSMENT...................................................................................................16

3.8QUALITYCONTROL...................................................................................................................17

3.9CONCLUSION..........................................................................................................................17

APPENDIX..............................................................................................................................18

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 4

1.0Introduction

TheMunicipalPropertyAssessmentCorporation(MPAC)–mpac.ca–isresponsibleforaccuratelyassessingandclassifyingpropertyinOntarioforthepurposesofmunicipalandeducationtaxation.

InOntario,propertyassessmentsareupdatedonthebasisofafour-yearassessmentcycle.Thenextprovince-wideAssessmentUpdatewilltakeplacein2016,whenMPACwillupdatetheassessmentsofOntario’snearlyfivemillionpropertiestoreflectthelegislatedvaluationdateofJanuary1,2016.Assessmentsupdatedforthe2016baseyearareineffectforthe2017–2020propertytaxyears.Ontario’sassessmentphase-inprogramprescribesthatassessmentincreasesarephasedinoverafour-yearperiod.Anydecreasesinassessmentareappliedimmediately.

Itisimportanttoensurethatthevaluationmethodologyappliediscapableofprovidingarealisticestimateofcurrentvalueattherelevantvaluationdate,which,inturn,enablesallstakeholderstounderstandthevaluationprocessandhaveconfidenceinthefairnessandconsistencyofitsoutcome.

ThisMethodologyGuidehasbeenpreparedforthebenefitofMPACassessors,propertyownersandtheirrepresentatives,municipalitiesandtheirrepresentatives,AssessmentReviewBoardmembers,provincialofficials,andthegeneralpublic.

Thisguideoutlinesthevaluationprocesstobefollowedbyanassessor,includingstepsthatrequireappraisaljudgment.Itisincumbentupontheassessortomakeinformeddecisionsthroughoutthevaluationprocesswhenarrivingatestimatesincurrentvalue.

1.1PropertiesCoveredbyThisMethodologyGuide

ThisMethodologyGuideappliesspecificallytofederallylicensedgrainelevatorsinOntario,andisnotintendedtobeusedforelevatorsthatdonotrequirelicensingwiththeCanadianGrainCommission.

Agrainelevatorisessentiallyatowercontainingabucketelevatororapneumaticconveyor,whichtransportsgrainfromalowerlevelanddepositsitinasiloorotherstoragefacility.Inthecontextofthisguide,theterm"grainelevator"coverstheentireelevatorcomplex,includingreceivingandtestingoffices,weighbridges,storagefacilities,etc.

InCanada,theterm"grainelevator"isusedtorefertoaplacewherefarmerssellgrainintotheglobalgraindistributionsystemand/oraplacewherethegrainismovedintorailcarsorocean-

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 5

goingshipsfortransport.Specifically,thereareseveraltypesofgrainelevatorsunderCanadianlaw,definedintheCanadaGrainAct,Section2,asfollows:

• Primaryelevators(called"countryelevators"before1971)receivegraindirectlyfromproducersforstorage,orforwarding,orboth.

• Processelevators(called"millelevators"before1971)receiveandstoregrainfordirectmanufactureorprocessingintootherproducts.

• Terminalelevatorsreceivegrainonorafterofficialinspectionandweighing,andtheyclean,store,andtreatgrainbeforemovingitforward.

AllcompaniesoperatingterminalelevatorsinCanadamustbelicencedbytheCanadianGrainCommission,whichmaintainsalistofalllicencedcompaniescurrentlyoperatinginthecountry.

TherearemanytypesandsizesofgrainelevatorsinOntario,rangingfromverylargefacilitieswithover350,000tonnescapacitytosmallerfacilitieswithaslittleas10,000tonnescapacity.

ThefollowingMPACpropertycodesareusedtocategorizethevarioustypesofgrainelevatorsinOntario:

• 522Grainelevators–GreatLakeswaterway

• 523Grainhandling–Primaryelevators

• 525Processelevators

Terminalgrainelevatorsaregiventhepropertycode522.

Itshouldbenotedthatthesearegeneralguidelinesthatvarydependingonthespecificcircumstancesofaparticularproperty.

AnassessormayalsomakereferencetoadditionalMethodologyGuidesforpropertiesthatdonotfallpreciselywithinthedescriptionofoneofthepropertycodeslistedabove.

1.2Legislation

ThemainlegislationgoverningtheassessmentofpropertiesinOntarioforpropertytaxpurposesiscontainedintheAssessmentAct.1

1AssessmentAct,R.S.O1990,cA.31:https://www.ontario.ca/laws/statute/90a31.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 6

TheActcontainsimportantdefinitionsandstatesthatallpropertyinOntarioisliabletoassessmentandtaxation,subjecttosomeexemptions.Section19(1)oftheActrequiresthatlandbeassessedatcurrentvalue,whichisdefinedtomean,inrelationtoland,“theamountofmoneythefeesimple,ifunencumbered,wouldrealizeifsoldatarm'slengthbyawillingsellertoawillingbuyer.”

Section17.1ofOntarioRegulation282/98definesa“grainelevator”tomean,“anelevatorusedtoreceive,store,clean,treatortransferfeedforlivestockorgrain.”2Section17.3oftheAssessmentActspecificallyprovidesthatSection33(1)oftheActdoesnotapplyforthe2012and2013taxationyears.Thismeansthatnoomittedassessmentsforgrainelevatorscanbemadeforthe2012or2013taxationyears.

1.3Classification

MPAC’sroleistoaccuratelyassessandclassifyallpropertiesinOntarioinaccordancewiththeAssessmentActandregulationsestablishedbytheGovernmentofOntario.

TheMinisterofFinancesignedOntarioRegulation257/14onDecember8,2014,toamendOntarioRegulation282/98byaddingsections17.1,17.2,17.3and44.2andrevokingsections6(2)4and14(2)3oftheregulation.

Priortothisamendment,Section6(2)4ofOntarioRegulation282/98specificallyprescribedthat“elevatorsusedtoreceive,store,clean,treatortransferfeedforlivestockorgrain”beplacedintheIndustrialPropertyClass.

Section17.2ofOntarioRegulation257/14nowprescribesthatagrainelevatoristobeincludedintheCommercialPropertyClass,subjecttocertainconditionsdescribedinparagraphs(2),(3),(4)and(6),whichwouldeitherincludethegrainelevatorintheFarmorResidentialPropertyClass.(Seetheappendix.)

Ifaportionofthepropertyisusedforotherpurposes,itmaybenecessarytovaluethosecomponentsseparatelyandsumthecomponentvaluestoachievethecorrecttotalcurrentvalue.Itmayalsobenecessarytoapportionthetotalvalueofthepropertybetweenthevarioususestoensurethattheappropriatetaxrateisappliedtotherelevantpartsoftheproperty.

2OntarioRegulation282/98,GENERAL:https://www.ontario.ca/laws/regulation/980282.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 7

1.4TheUseofThisMethodologyGuide

ThisMethodologyGuideisintendedto:

• EnsureMPAC’sassessedvaluesforthesepropertiesarefair,accurate,predictableandtransparent.

• Providedirectiontoassessorsandclearexplanationstomunicipalities,taxpayersandAssessmentReviewBoardmembers.

• EnsurethatMPAC’smethodologyforvaluingthesepropertiesiswelldocumentedandalignswithindustrystandards.

• Explainthethoughtprocess/decision-makingprocessthatanassessorshouldundertaketoapplythevaluationmethodology.

• Ensureaconsistentapproachtovaluingthesepropertytypes.

• SupportMPACassessorsinconductingtheirduediligencein:

Ø applyingOntario’slegislationandregulationsØ adheringtoindustrystandardsformarketvaluationinamassappraisal

environment

ItshouldbenotedthatthisMethodologyGuideisnotintendedtobeasubstituteforanassessor’sjudgmentinarrivingatamarketvalue–basedassessment(i.e.,currentvalue)foraparticularproperty.However,giventhattheMethodologyGuideexplainsindustrystandardsforpropertyassessment,conformstovaluationindustrynorms,andadherestoprovinciallegislationandregulation,MPACassessorsareexpectedtofollowtheproceduresintheMethodologyGuideandbeabletoclearlyandsatisfactorilyjustifyanydeviationsfromit.

1.5ConsultationandDisclosure

MPACiscommittedtoprovidingmunicipalities,taxpayersandallitsstakeholderswiththebestpossibleservicethroughtransparency,predictabilityandaccuracy.Insupportofthiscommitment,MPAChasdefinedthreelevelsofdisclosureaspartofitsdeliveryofthe2016province-wideAssessmentUpdate.

• Level1–MethodologyGuidesexplaininghowMPACapproachedthevaluationofparticulartypesofproperty

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 8

• Level2–MarketValuationReportsexplaininghowthemethodologyoutlinedinLevel1hasbeenappliedatthesectorlevelforthepurposesofeachassessment

• Level3–PropertySpecificValuationInformationavailabletopropertytaxpayers,theirrepresentativesandmunicipalities

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 9

2.0TheValuationProcess

Thevaluationprocessalwaysbeginswithadeterminationofthehighestandbestuseofthesubjectproperty.

Anyrelianceuponthisguideismadeonlyaftertheassessorhasdeterminedthatthehighestandbestuseofthesubjectpropertyisthatofafederallylicensedgrainelevator.

Assessorsdeterminethevalueofapropertyusingoneofthreedifferentapproachestovalue:

• thedirect(sales)comparisonapproach

• theincomeapproach

• thecostapproach

2.1Outline

Inthedirect(sales)comparisonapproach,valueisindicatedbyrecentsalesofcomparablepropertiesinthemarket.Inconsideringanysalesevidence,itiscriticaltoensurethatthepropertysoldhasasimilaroridenticalhighestandbestuseasthepropertytobevalued.

Intheincomeapproach(or,moreaccurately,theincomecapitalizationapproach),valueisindicatedbyaproperty’srevenue-earningpower,basedonthecapitalizationofincome.Thismethodrequiresadetailedanalysisofbothincomeandexpenditure,bothforthepropertybeingvaluedandothersimilarpropertiesthatmayhavebeensold,inordertoascertaintheanticipatedrevenueandexpenses,alongwiththerelevantcapitalizationrate.

Inthecostapproach,valueisestimatedasthecurrentcostofreproducingorreplacingimprovementsoftheland(includingbuildings,structuresandothertaxablecomponents),lessanylossinvalueresultingfromdepreciation.Themarketvalueofthelandisthenadded.

Thisapproachseparatelyvaluesimprovementsandlandtoproduceacurrentvaluefortheproperty.Thecostapproachforgrainelevatorshasthefollowingmainstepsforgrainelevatorbuildingsandstructures:

1. Determinereproductioncostnew(RCN).

2. Determinephysicaldepreciation.

3. Determinefunctionalobsolescence.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 10

4. Determineexternalobsolescence.

5. Determinenetimprovementvalue.

Theassessorthenfollowsthesamestepstodeterminethevalueoftheelevatorsiteimprovements(yardwork).

Finally,theassessordetermineslandvalueforthegrainelevatorcomplexandaddsthevaluesforotherpurposes(e.g.,excessland).Atthispoint,theassessorisreadytodeterminethecurrentvalueassessment.

2.2Approach

TherearethreemainphasesinthevaluationprocessusedbyMPAC:

• datacollection

• analysisofthedatacollected

• valuation

2.3DataCollection

Thedatarequiredforgrainelevatorvaluationscomefromanumberofsources:

• MPACconductsperiodicinspectionsofgrainelevators.

• MPACalsocollectsinformationaboutsalesandtransfersofgrainelevators.

• Thereareanumberofguidesandotherpublishedinformationaboutgrainelevatorsfromindustrysources,suchastheCanadianGrainCommissionandindustryandportauthoritywebsites.

MPACgenerallycollectsthefollowingtypesofdataforgrainelevators:

• landdata–includingcommercial,industrial,excesslandandotherland

• siteimprovementsdata–includinginteriorandexterioraccessroads,waterfrontfacilities,railfacilities,tunnelsandutilities(electrical,water,sewage,gas)

• buildingimprovementsdata–includingelevator,silos,workhouses,administrativeoffices,weighbridges,conveyors,walkways,workshops,securityfacilitiesandotherstoragefacilities

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 11

Thelandwillbemeasuredintermsofitssizeinacres.Buildingswillnormallybemeasuredinsquarefeet.Storagefacilitiesmaybemeasuredintermsof“bushelcapacity.”

Theassessorwillrecorddetailsnotonlyofthesizeandcapacityofthebuildingsandstructures,butalsotheirage,conditionanduse.

MPACwilleitherprepareaplanofthesiteandbuildingsorobtainonefromthesiteoperator.Thesiteplanwillidentifyallthedifferentbuildings,structuresandotherimprovementsbyareferencenumberforeaseofidentification.

Thesereferencenumberswillbeusedinthevaluationofthegrainelevatortoensurethatallpartsofthepropertyareproperlyincludedinthecurrentvalueassessment.

Confidentiality

Asoutlinedabove,itisimportanttobeawarethat,inordertoenableMPACtoproduceanaccuratevaluationofthepropertyconcerned,informationneedstobeobtainedfromavarietyofsources.

ThiswillincludeinformationfromMPAC’srecords,fromtheowneroroperatoroftheproperty,fromthemunicipalityinwhichthepropertyislocated,fromtheassessor’svisittotheproperty,andfromothersources.

AllstakeholdersinthepropertytaxsystemhaveaninterestinensuringthatthecurrentvalueprovidedbyMPACiscorrect;inordertoachievethis,itisnecessaryforallpartiestocooperateintheprovisionofinformation.

Itisappreciatedthatsomeoftheinformationoutlinedabovemaybeofacommerciallysensitivenature.MPACrecognizestheneedtoensurethatanyinformationprovidedtoitisproperlysafeguardedandonlyusedforthepurposeforwhichitissupplied.Assessorsmustappreciatethenatureofthisundertakingandensuredataistreatedaccordingly.

If,afteranappealhasbeenfiled,MPACreceivesarequestforthereleaseofactualincomeandexpenseinformation,orothersensitivecommercialproprietaryinformation,theusualpracticeistorequirethepersonseekingtheinformationtobringamotionbeforetheAssessmentReviewBoard(ARB),withnoticetothethirdparties,requestingthattheARBorderproductionoftherequestedinformation.ThereleaseofsuchinformationisatthediscretionoftheARBandcommonlyaccompaniedbyarequirementforconfidentiality.

TheAssessmentActoutlinesinsection53(2)thatdisclosedinformationmaybereleasedinlimitedcircumstances“(a)totheassessmentcorporationoranyauthorizedemployeeofthe

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 12

corporation;or(b)byanypersonbeingexaminedasawitnessinanassessmentappealorinaproceedingincourtinvolvinganassessmentmatter.”

2.4DataAnalysis

Havingcarriedoutthedatacollectionoutlinedpreviously,theassessorneedstoanalyzeitandreachaconclusionregardingtheappropriatevaluationmethodtouseandhowitshouldbeapplied.

Asalreadyindicated,forthepurposesofthisMethodologyGuide,itisassumedthattheassessorwillconcludethatthereisinsufficientevidenceavailabletoenableeitherthedirectcomparisonapproachorincomeapproachtobeadopted.Forthatreason,theassessorwillbeadoptingthecostapproachandusingthedatacollectedtoensurethatthecostapproachisproperlyapplied.

2.5Valuation

Havingundertakenthenecessarystepsoutlinedabove,theassessorshouldnowbeinapositiontoapplytheappropriatevaluationmodel.AdetailedwalkthroughofthevaluationprocessisincludedinSection3.

2.6ValidatingtheResults

Oncetheassessorhascompletedthevaluation,itisnecessarytocarryoutaseriesofcheckstoensurethatallrelevantpartsofthepropertyhavebeenincludedinthevaluation,therehasbeennodouble-countingofanyadjustmentsmadefordepreciation,theresultingvaluationhasbeencomparedwithanymarketevidencethatmaybeavailableinrelationtosimilarproperties,andthefinalvaluationisinlinewiththevaluationofothersimilarpropertiesinOntario.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 13

3.0TheValuation

3.1CostApproachOverview

Thetheorybehindthecostapproachtovaluefollowstheprincipleofsubstitution:thevalueofapropertyisequaltotheamountitwouldcosttoreplaceitwithasubstituteofequalutility.

Therearetwomaintasksinestimatingmarketvalueusingthecostapproach:valuethelandandvaluetheimprovements.

ValuetheLand

Theestimateforthecurrentvalueofthelandisusuallyestablishedthroughanalysisofcomparablemarketsalesdata.

ValuetheImprovements

Avaluationofimprovementsincludesthefollowingsteps:

1. Collectthephysicalanddescriptivedataaboutthegrainelevator.Inspectthebuildings,structuresandotherimprovements,quantifyareas,noteconditionsandanalyzetheirutility.

2. Quantifythebuildingareasfromplansandlayouts,or,ifnecessary,duringthepropertyinspection.

3. UsingMPAC’sautomatedcostsystem(ACS),estimatethereproductioncostnewoftheassessableimprovementsasofthevaluationdate.

4. Deductfromreproductioncostnewvalueanamountreflectingallformsofdepreciation.Thismayinclude:

• physicaldeterioration(age-lifedepreciation)

• functionalobsolescence(curableandincurable)

• externalobsolescence(economicandlocationalobsolescence)

Theresultingvaluewillbeanestimateofthecontributionoftheimprovementstothemarketvalueofthesubject,depreciatedforallcauses.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 14

FinalValue

Thesumoflandvalueplusdepreciatedimprovementvalueistheestimatedmarketvalueoftherealestateatthesubjectlocation.

3.2LandValuation

Essentialsourcesofinformationthatcanbeusedinthevaluationofgrainelevatorsinclude:assessmentrecords,municipalzoningbylaws,owners,realestateconsultantsandbrokers,realestatepublications,costmanuals(forsiteservicingcosts)andtitleregistrationoffices.Comparablesalesareutilizedindetermininglandvalueswheneverpossible.

Thefollowingtypesoflandusesmaybeassociatedwithafederallylicensedgrainelevatorsite:

• commercial

• industrial

• otheruse

• excessland

Theassessorwillnormallyassignaseparatevaluetoeachtypeoflanduse.

3.3BuildingandSiteImprovements

Variousbuildingandsiteimprovementsareessentialtothefunctioningofagrainelevator.Theymayinclude,butarenotlimitedto:

• elevator • walkways

• silos • workshops

• otherstoragefacilities • securityfacilities

• workhouses • washrooms

• administrativeoffices • canteen

• weighbridges • utilities(electrical,water,sewage,gas)

• conveyors • exterioraccessroads

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 15

• interioraccessroads • tunnels

• waterfrontfacilities • parking

• railfacilities

Theassessorwillobtainasmuchfactualinformationaspossibleaboutboththenatureoftheimprovementsandthewayinwhichtheyareused.Theassessorwilltalktotheoperatorofthegrainelevatortoobtainaproperunderstandingofthewayinwhichtheimprovementsareusedandtheirefficiency.

3.4EstablishingCostNew

Threeapproachescanbeusedtoestablishcostnew:

• historicalconstructioncost–actualcostsindexedtothevaluationdate,whichmaybeusefulforrelativelynewbuildingsorstructures(upto5to10years)

• reproductioncosttechniques–appliedinthevaluationofmostbuildingsorstructuresandobtainedfromcostmanualssuchastheAutomatedCostSystem(ACS)developedforMPAC

• replacementcosttechniques–maybeappliedwhenestimatingthecostofamodernfacilitythatisdifferenttotheexistinggrainelevatorandwhichmaybeusedinconnectionwithquantifyinganyfunctionalobsolescence

Dependingonthefunctionalutilityofthegrainelevatorinthemarket,theassessorwillselectthemostrelevantoptionforthesubjectproperty.Inmostcases,MPACwillusereproductioncostnew(RCN)asthestartingpointforthevaluation.

3.5DeductingDepreciation/Obsolescence

Depreciationmayincludephysicaldeteriorationduetoage,conditionand/oruseoftheproperty.Depreciationmayalsoincludeobsolescence.

Obsolescencereflectstheabnormaldepreciationthatarisesinsomepropertiesduetofunctionaland/orexternallygeneratedeconomicproblems.

Functionalobsolescencecanbetheresultofnumerousfactors,includingpoororoutdateddesigns,inadequateareas,excessoperatingcosts,etc.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 16

Obsolescenceisnotrelatedtotheageofthepropertybuttoitsabilitytoadequatelyperformitsintendedfunctions.

Whendeterminingwhetherobsolescenceexistsinaproperty,theassessorasks:“Couldtheexistingfacilitybereplacedwithamoremodern,efficientsubstitute,andifso,whatwouldconstitutethismodernfacility?”

Knowledgeofcurrenttrendsandbuildingdesignsforgrainelevatorsisimportantinrecognizingobsolescence.Functionalobsolescencecanusuallyberecognizedthroughpoordesignandlayout,poororinferiorconstruction,unusedareasandtheexistenceofexcessoperatingcosts.

Externalobsolescenceresultsfromachangeofcircumstancesoutsidethecontrolofthegrainelevatoroperator.Thiscouldbealarge-scalefactorsuchaseconomicrecessionandachangeintheprice/valueofgrainoramorelocalizedfactorsuchasachangeinthelocaltransportationinfrastructure,whichmakesthelocationofthegrainelevatorlessattractiveandlessvaluable.

Thereareavarietyofmethodsthatcanbeusedtoquantifydepreciation.Thedetailofthesemethodsisnotappropriateforthisguide.However,whileitisimportanttoquantifyallaspectsofdepreciation,itisequallyimportantnottodoublecountforthesameaspectofdepreciationwhileusingthevariousapproaches.

Aftertheamountanddegreeofdepreciationhavebeendeterminedandquantified(ifany),theendresultshouldreflectthereproductioncostnewofthebuildingandsiteimprovementslessanydepreciation(RCNLD)foundinthepresentimprovements.

3.6MarketValueConclusion

Theassessoraddsthevalueofthelandtothevalueofthedepreciatedbuildingandsiteimprovementsinordertoproducethemarketvalueofthepropertybasedonthecostapproach.

3.7CurrentValueAssessment

Thefinalstepintheprocessistoconsolidateacurrentvalueassessmentfortheproperty.Oncethedeterminationofvalueusingthecostapproachhasbeencompleted,theassessorwillconsiderwhetherthereisanyothervalueintherealestatethathasnotbeencapturedbytheanalysis.

©MunicipalPropertyAssessmentCorporation2016Allrightsreserved 17

AddOtherComponentsofValue

Theremaybegrainelevatorswherethevalueisnotentirelycapturedbytheapplicationofthecostapproach.Forexample,theremaybeexcesslandavailablethathasnotbeenincludedinthevaluationofthegrainelevator.

ExcessLand

Excesslandislandthatissurplustocurrentneeds.Thevalueofexcesslanddependsonitslocationwithinthesiteandhowwellitsuitsfuturedevelopments.Suchsurpluslandwouldhavetobevaluedseparatelyandaddedtothecurrentvalueassessmentarrivedatforthegrainelevator.

Beforearrivingatanexcesslandconclusion,asiteinspectionisrequiredtoensurethatadditionaldevelopmentwouldbepossible.Thedeterminationofexcesslandinvolvesareviewofcurrentzoningbylawsaswellasthecurrentcoverageandconfigurationoftheproperty.Theratetobeappliedtovalueexcesslandistypicallyderivedusingmarketsalesstudiesofvacantlandsites.

3.8QualityControl

Havingarrivedatthevalueofthegrainelevatorthroughtheaboveprocess,theassessorwillchecktheoutcomeofthevaluationtoensurenoerrorshavebeenmadeandthatthevalueisinlinewiththevaluationofothersimilargrainelevatorsinOntario.

Comparisonsbetweencurrentvalueassessmentsofgrainelevatorsmaybemadebyreferenceto“bushelcapacity”or“metrictonnes,”takingintoaccountlocationalandotherdifferencesbetweentheproperties.

3.9Conclusion

ThisguidesetsouthowMPACassessorsapproachthevaluationofgrainelevatorsforpropertyassessmentpurposes.

Althoughitoutlinesthegeneralapproachadopted,itdoesnotreplacetheassessor’sjudgmentandtheremaybesomecaseswheretheassessoradoptsadifferentapproachforjustifiablereasons.

ForfurtherinformationaboutMPAC’srole,pleasevisitmpac.ca.

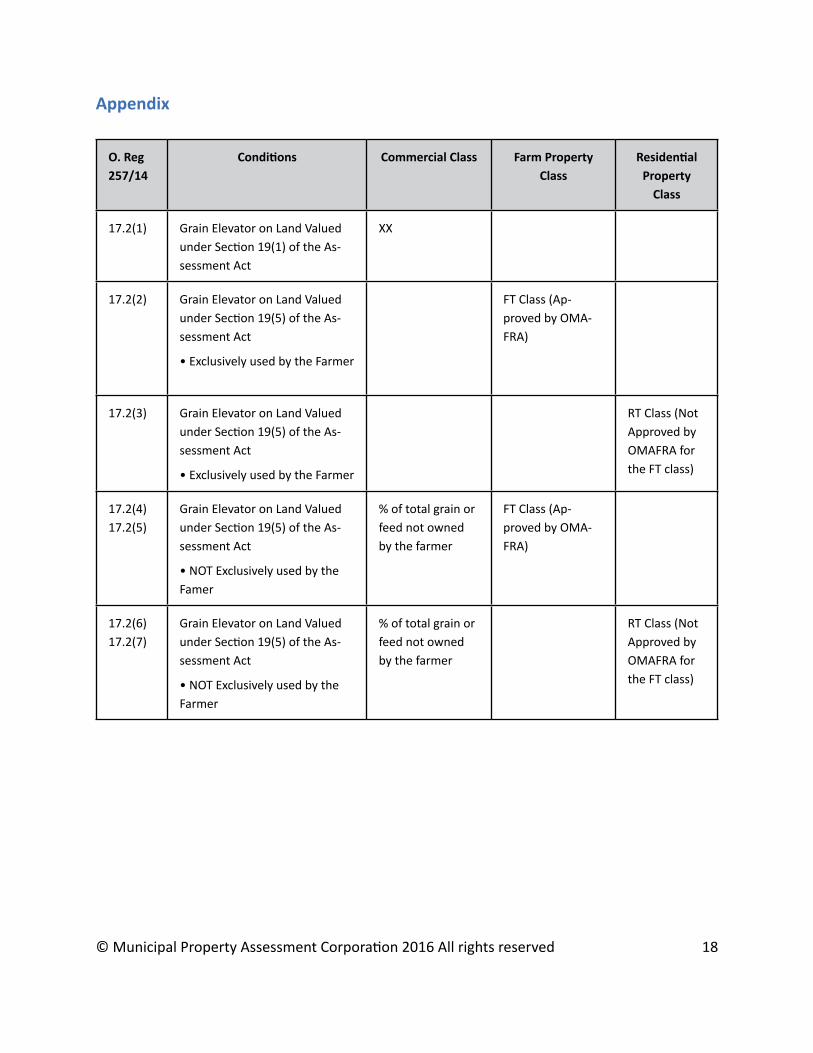

Appendix

O. Reg 257/14

Conditions Commercial Class Farm Property Class

Residential Property

Class

17.2(1) Grain Elevator on Land Valued under Section 19(1) of the As-sessment Act

XX

17.2(2) Grain Elevator on Land Valued under Section 19(5) of the As-sessment Act

• Exclusively used by the Farmer

FT Class (Ap-proved by OMA-FRA)

17.2(3) Grain Elevator on Land Valued under Section 19(5) of the As-sessment Act

• Exclusively used by the Farmer

RT Class (Not Approved by OMAFRA for the FT class)

17.2(4)17.2(5)

Grain Elevator on Land Valued under Section 19(5) of the As-sessment Act

• NOT Exclusively used by the Famer

% of total grain or feed not owned by the farmer

FT Class (Ap-proved by OMA-FRA)

17.2(6)17.2(7)

Grain Elevator on Land Valued under Section 19(5) of the As-sessment Act

• NOT Exclusively used by the Farmer

% of total grain or feed not owned by the farmer

RT Class (Not Approved by OMAFRA for the FT class)

© Municipal Property Assessment Corporation 2016 All rights reserved 18