Methane Emission Management Emission... · Presentation at the KMG III Annual General Directors HSE...

12

Methane Emission Management: Regional and international experiences Presentation at the KMG III Annual General Directors HSE Leadership forum «GREAT SAFETY LEADERSHIP» Astana 28 th June 2017 Torleif Haugland , Carbon Limits

Transcript of Methane Emission Management Emission... · Presentation at the KMG III Annual General Directors HSE...

Methane Emission Management: Regional and international experiences

Presentation at the KMG III Annual General Directors HSE Leadership forum

«GREAT SAFETY LEADERSHIP»

Astana 28th June 2017

Torleif Haugland , Carbon Limits

Carbon Limits – Methane and Gas flaring experience

CARBON LIMITS – METHANE AND GAS FLARING PROJECTS

- Consulting company based in Oslo

- 10 years + experience on GHG emissions in the

oil and gas sector in 20 + countries

- Provide a number of services including emission

reduction project identification and assessment

- Worked on methane emissions for the last 5

Years

SOME OF OUR CURRENT CLIENTS AND PARTNERS

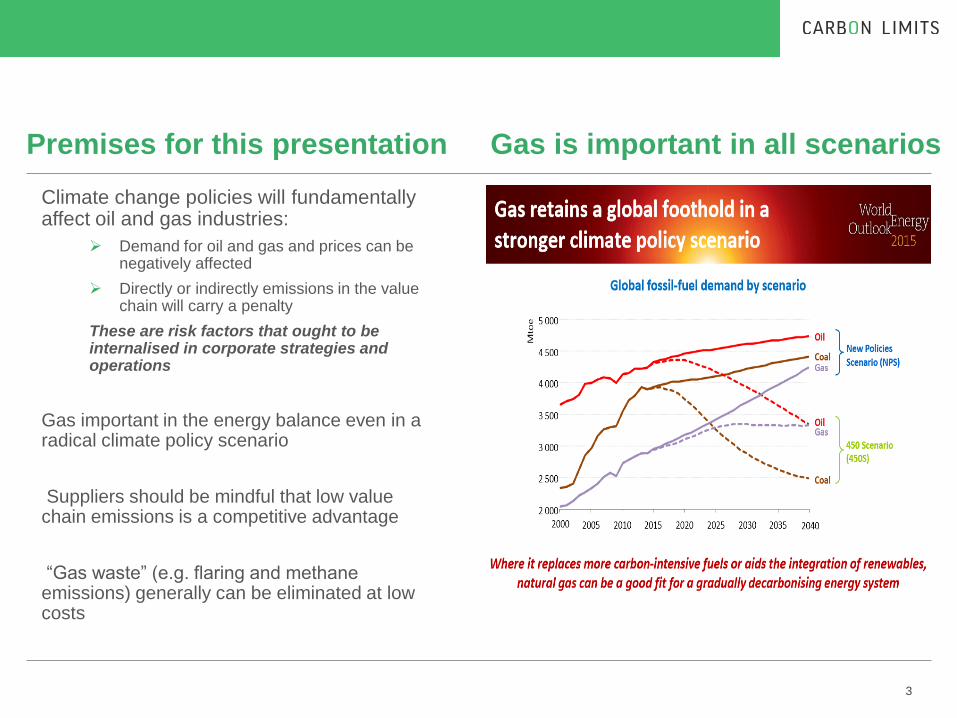

Gas is important in all scenarios

3

Premises for this presentation

Climate change policies will fundamentally affect oil and gas industries:

Demand for oil and gas and prices can be negatively affected

Directly or indirectly emissions in the value chain will carry a penalty

These are risk factors that ought to be internalised in corporate strategies and operations

Gas important in the energy balance even in a radical climate policy scenario

Suppliers should be mindful that low value chain emissions is a competitive advantage

“Gas waste” (e.g. flaring and methane emissions) generally can be eliminated at low costs

0

200

400

600

800

1000

1200

1400

1600

1800

Gas flaring Venting and Fugitiveemissions

But much gas is wasted and creates environmental pressures

4

Wasted energy: 250 bcm/year

4% of global greenhouse gas emissions

Direct emissions of methane:

equals Norway’s production of natural gas, worlds 7th largest producer

30 billion US$ per annum in lost revenues

Direct methane

emissions

Mill

ion

t C

O2

eq

Gas does not always have lower emissions than coal

5

Factors that matter:

Distance to end use markets

Efficiency of compressors and

other upstream

Leak rates

Current methane

emissions by region

6

However current methane emissions

are uncertain due to the lack of

measurement data in a number of

regions

0

50

100

150

200

250

300

350

400

450

Russia Caspian US EU

MtC

O2eq

(G

WP

100 y

ears

)

2012 2020 2030

Reducing emissions

is cost-effective

0% 20% 40% 60% 80% 100%

Canada

Mexico

Kazakhstan

US

Economic abatement potential Other abatement potential

Past studies have demonstrated that a large

share of the abatement potential is economic

or low abatement cost (<10 USD/tCO2eq).

Main opportunities are country specific but

include:

• Liquid storage tanks

• Repairs of fugitives leaks

• Compressors seals,

• …

* Caspian includes Kazakhstan,

Azerbaijan and Turkmenistan

** Kazakhstan contributes to around

35% - 40% of the caspian methane

Methane Mitigation Opportunities at KMG

7

Methane Mitigation Opportunity

In total, KMG’s mitigation opportunity is

~132 MM m3/year, or

~2.3 million tons of CO2/year,

in global warming potential.

Major Identified Sources for KMG

MM m3/y tCO2eq/y

Leaks (A) 15,6 250 000

Storage tanks (B) 34 610 000

Centrif. Compress. (C) 25,4 450 000

Blowdown sources (D) 45,7 830 000

Others 11,5 160 000

Total 132 2 300 000

Methane emission reduction

projects for KMG

8

Project type

A - Leak detection and repair (LDAR)

B - Vapor Recovery Units Storage Tanks

By project By KMG total By project By KMG total

Capex range Less than

200kUS$

1,3 million US$

(~ 10 companies x

$120

kUSD/equipment

set)

200k to 1 million

US$

per tank farm

8 million US$

(~ 40 tank farms x

$200k/tank farm)

Payback time A few months 2 years 1 to 4 years 4 years

EP, KTG, KTO, RM EP, RM

MM m3/y tCO2eq/y

Leaks (A) 15,6 250 000

Storage tanks (B) 34 610 000

Centrif. Compress. (C) 25,4 450 000

Blowdown sources (D) 45,7 830 000

Others 11,5 160 000

Total 132 2 300 000

Methane emission reduction

projects for KMG

9

Project type

C - Wet Seal Compressors

D -Mobile Compressors

By

project By KMG total By project By KMG total

Capex range

100k to 1 million

US$

per compressor

2,7 million US$

(~109K USD x

25 KC)

6 million per unit

60 million US$

(10 mobile compressor

stations X $6M USD/MCS) -

to avoid blowdown during

the 5 pipeline repairs per

year

Payback

time 1 to 5 years 3 years 10 to 12 years 12 years

KTG KTG

MM m3/y tCO2eq/y

Leaks (A) 15,6 250 000

Storage tanks (B) 34 610 000

Centrif. Compress. (C) 25,4 450 000

Blowdown sources (D) 45,7 830 000

Others 11,5 160 000

Total 132 2 300 000

10

0

200

400

600

800

1000

1200

LDAR,1 MMm3 saved

VRU,1.3 MMm3 saved

Wet seal degassing,1 MMm3 saved

Net p

rese

nt va

lue

, th

ou

sa

nd

US

D

IRR

66% IRR

45%

IRR

38%

CAPEX

Project returns

Add returns with 5

USD/tonne CO2e

Based on CL measurements and assessment of sites in Kazakhstan

Even with modest valuation, GHG benefits are substantial

compared to the value of recoverable gas. Project cases in Kazakhstan.

Value of natural gas versus value of GHG benefits at US$ 5 per tonne CO2e in methane emission reduction

projects.

Old and new opportunities for selling “carbon credit off-sets”

2020 2012 2019 2021 2029

Offsets (CDM or ISO) to be sold at voluntary

market or into national ETS schemes

Voluntary offset schemes

Paris Agreement Article 6 schemes UERs

Article 6 of the Paris Agreement: Two schemes

Article 6.4 - a project based mechanism, probably with similarities to the CDM, but modified and possibly

simplified. Still, with approval and issuance procedures managed by UNFCC.

Article 6.2 – “Internationally Transferable Mitigation Outcomes” (ITMOs). Bilateral agreements on

transactions between countries (Paris Agreement Parties). General oversight by UNFCCC to ensure

environmental integrity and that “double counting” does not occur. “Bottom-up” approach.

UERs: Carbon credits under the EU Fuel Quality Standards.

Fuel supplier in the EU are obliged to reduce carbon intensity by 6% from 2010 to 2020. They can blend in bio-fuel

and use hydrogen and electricity, and /or they can obtain carbon credits from upstream projects

Final remarks

12

International climate policy will fundamentally

impact framework conditions for oil and gas sector

operations. Creates risks and opportunities

End use consumers will increasingly consider

supply chain emissions of the products they buy.

There will be a call for documentation of carbon

footprint of oil and gas supplies.

KMG has ample opportunities for supply chain

emission reductions, of which a large part can be

done at no net-costs.

Opportunities exist for monetizing emission

reductions, and documentation of emission

reduction efforts have considerable reputational

value.