Meso-finance in developing countries - · PDF filesegment above microfinance (loans to...

27

-

Upload

nguyenhanh -

Category

Documents

-

view

218 -

download

1

Transcript of Meso-finance in developing countries - · PDF filesegment above microfinance (loans to...

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.2

‐‐‐‐ POSITION PAPER ‐‐‐‐

Meso‐finance

filling the financial service gap for small businesses

in developing countries

September 2006 Authors: Thierry Sanders NCDO Editor Carolien Wegener Pro‐Ideal Researcher

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.3

CONTENTS

1. Introduction.................................................................................................................................. 4

2. The Relevance of SMEs in Developing Economies .................................................................. 5

3. The Missing Middle and Meso-Finance ...................................................................................... 7

4. The Issues .................................................................................................................................... 9

5. Stakeholders ............................................................................................................................... 12

6. Existing business models & pioneers...................................................................................... 17

7. Opportunities and solutions for meso-finance........................................................................ 20

Further Reading .............................................................................................................................. 24

Organisations invited to the Meso-finance seminar (* participants)......................................... 26

Acknowledgements We wish to thank Klaas Molenaar and David Wood for their expert comments on this paper. And are grateful to In Return, CMI, Gexsi, Cordaid, SOVEC, The Blue Link and Judith Brandsma for sharing their experience and knowledge with us.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.4

1. Introduction The aim of this paper is to prepare participants for the BiD Seminar on “Meso‐Finance for development” to be held at d.o.b. foundation on September 13th, 2006. The definitions, players and market issues will hopefully bring all participants up to speed on the issues of financing small businesses in developing countries. This will help all participants to start the session at a similar level. The focus and scope of this paper and the seminar are the financing needs of small and medium sized entertprises (SMEs) in developing countries. The focus here is: ‐ ‘Meso‐Finance’ – an unofficial term for financial needs of small businesses ranging between

€5,000 and €500,000. That is roughly the financial needs above the microfinance level and below the commercial and subsidized international finance level;

‐ The size of the SME businesses are anywhere between 2 to 250 employees. Again this is the segment above microfinance (loans to enterprising individuals, sometimes to ‘businesses’) and below large companies with more than 250 employees;

Summary The ultimate objective of promoting meso‐finance in developing countries is to improve small business performance. This in turn will influence higher economic growth and employment, reduce poverty and meet social development objectives. Meso‐Finance is only one means to these ends. Access to meso‐finance requires many ingredients, such as a policy environment conducive to enterprise competitiveness, access to financial and non‐financial services, and expanding markets for small business products and services.1 SME researchers at IFC, World Bank and others emphasize the crucial importance of SMEs for economic development. SMEs are the source of dynamism for local market development. They create (embryonic) supply chains and employ a majority of the workforce. In countries where markets and government agencies function reasonably well SMEs will represent over 80% of all companies in the economy, they employ over 60% of the workforce. SMEs, formal and informal, form the backbone of the economy. However, SMEs face many obstacles. In Congo, Dominican Republic, Venezuela and Indonesia it takes at least 100 days to start a business. These starting entrepreneurs are often poorly equipped or trained to start their business. They lack the legal papers to prove their collateral to back their requests for credit. The central question here is how access to finance can be improved so as to stimulate SME growth. This growth will generate the jobs, income, self‐esteem and entrepreneurial dynamism needed for economic growth and poverty reduction. This is our challenge!

1 Committee of Donor Agencies for Small Enterprise Development – ‘Business Development Services for small enterprises’ – 2001 – SME Dept. World Bank.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.5

2. The Relevance of SMEs in Developing Economies 2.1 Small Business or Small and Medium Sized Enterprises (SMEs) Small businesses vary in size from country to country. In large economies like the US and EU SMEs are considered to be companies with less than 500 employees. In smaller economies (less than) 100 or 250 employees is the going definition2. The IFC SME database uses the following definitions3: Micro business 0 ‐ 4 employees Small business 5 ‐ 49 employees Medium business 50 ‐ 250 employees In this paper we use the term small business and SMEs interchangeably to describe businesses with 2 to 250 employees. 2.2 Development impact Small businesses play a central role in any economy in terms of employment, income, innovation and the development of local markets and supply chains. In developing countries the social value and economic role of SMEs are even more significant. In developing economies employment and higher income effects translate directly to fulfilment of basic human needs like health services, education, better homes, buffers for risk, etc. SMEs use a combination of innovation, improvisation to develop local products and services for local needs using local resources. Their impact on the poorer in the community is greater simply due to their local activity radius through employment, procurement and sales. Small businesses often succeed in transforming informal activities into formal ones, directly contributing to economic health of the market environment. Studies on the macro‐economic effect of development programmes reveal that the dynamics in the economy depend on the small enterprise sector rather than the micro enterprise sector4. 2.3 Small business characteristics Small businesses make inventive use of knowledge, experience, resources and simple technologies to turn local market conditions into business opportunities. They are creative, fast moving and able to serve niche market segments often left out by larger businesses. A vibrant private sector generates jobs, raises incomes, and makes better, cheaper goods and services available. Small businesses build and strengthen local supply chains and rural production lines. They can offer security, education and relative high incomes to poor often unskilled people. Studies on the development impact of investment in small business confirm these characteristics: • In many developing countries 95% of all companies have less than 50 employees. If the aim is to

stimulate private sector development there is a clear demand to cater for specific needs of small businesses5;

• Every dollar invested in a small enterprise generated an average ten dollars of economic activity in the local economy6;

2 Tylor Biggs; Is Small Beautiful and Worthy of Subsidy? Literature Review –

http://rru.worldbank.org/Documents/PapersLinks/TylersPaperonSMEs.pdf 3 MSME database – IFC http://rru.worldbank.org/Documents/other/MSMEdatabase/msme_database.htm 4 K. Molenaar; Business Development Services, a key issue too often forgotten; FACET BV 2006 5 Source: People – plans – profit for poverty reduction, a publication of the Business in Development Challenge

2005, NCDO. 6 SEAF - The Development Impact of Small and Medium Enterprises - 2005

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.6

• A greater share of benefits go to employees7: – Two thirds of those employed are poor or low‐skilled workers, whose salaries increase by

28% on average; – Large investments are made in training their employees; – The stability of employment stimulates employees to pay for their children’s education,

health and social security services. • Small businesses have the span of influence to connect local, regional and (inter)national markets

as well as rural and urban markets; • Expanding small businesses are an important tax income for (local) governments, hopefully

catalysing investment in business enabling environments; • Small businesses are an integral part of communities; they contribute actively to community and

environmental development. 2.4 Small businesses in the emerging market environment Cross‐country studies on SME development in emerging economies find that financially more developed countries tend to have larger firms. This suggests that financial development eases financial constraints on successful firms and allows them to grow. Various studies show that restrained access to inputs, especially finance, results in a bi‐modal firm size distribution with small firms growing less and large firms growing faster than in developed economies8.

MSME's Contributions to GDP and Em ploym ent

0

10

20

30

40

50

60

High income countries Upper middle income Low er middle income

SME employment as %employmentSME contribution to GDP

The graph indicates a relation between countries income level and the share and functioning of micro, small and medium enterprises (SME’s) in the country. Lower middle income countries clearly lag behind in the SME contribution to GDP and employment. This indicates the presence of market constraints cutting back their potential growth and impact. The next chapter investigates the particular issues of influence to small business start‐up, development and growth in emerging markets.

7 Source first five bullet points: SEAF (www.seaf.com), 2004 case study on SME investment 8 Beck, Demirguc-Kunt, Levine ; SMEs, Growth, and Poverty: Cross-Country Evidence – Worldbank & University

of Minnesota, 2003

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.7

> $ 2 millionInternational commercial finance

> $ 500,000Local banks & subsidisedinternational finance

> $ 5,000Local banks, loansharks & personal loans

> $ 0Microfinance, loansharks & personal loans

Largecompanies

Medium sizedbusinesses

100-250 employees

Small business1-100 employees

Micro business1 employee

Number of companies

Company size

“The Missing Middle” Small companies lack

access to finance

Amount of finance

available

Finance size& source

“The Missing Middle”Finance is available for large and

micro businesses, but is limited for the smallin developing countries

Source: Thierry Sanders, NCDO

ILLUSTRATIVE

3. The Missing Middle and Meso-Finance Small businesses are the backbone of most developing and developed economies. They outnumber large companies and they employ the majority of the working population. However, in developing countries large companies have access to finance. Also micro‐entrepreneurs are getting access to the growing volume of microfinance. In the meantime small businesses in developing countries seem to be off the mainstream financial radar screens. This financing gap for the middle segment of companies is often called the ‘Missing Middle’. The generalised figure to the right visualises this gap.

Currently the most common way of financing the start or growth of a small businesses in a developing country is through family capital9. Money lenders and commission agents –often called ‘loan sharks’‐ are a second source of finance. Their nickname points to the exuberant interest rates and the stringent terms they operate upon. 3.1 Meso‐finance ‘Meso‐finance’ is not a generic financial term, but is a useful description of the financial services one level up from micro‐finance. We define meso‐finance as the financial services (loans, equity, guarantees) offered to small businesses in developing countries. These financial services cover the financial needs of small businesses from $5,000 up to $500,000. This financial range defines the scope of this paper and the seminar.

9 After bank finance borrowing from family and friends is the chief source of funds for new business start-ups in

many countries – source: Basu & Parker Family finance and new business start-ups

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.8

3.2 Meso‐finance and the business life cycle The classical definition of the business life cycle contains the stages of start‐up, survival, growth, expansion, and maturity/ decline. Meso‐finance in emerging markets typically targets businesses in the first three stages of the life cycle10. Differences in access to finance in developed and developing markets are most crucial in the survival and growth stage. Businesses in developed countries generally replace family and venture funding by banking services in those stages. Immature financial markets in transition economies are characterised by lack of such services. They fail to offer adequate financial services to make small businesses grow.

10 Based on PWC Diagnostic Chart – business growth stages - http://www.pwcglobal.com/nz/eng/ins-

sol/publ/pcs/DiagnosticChart.pdf

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.9

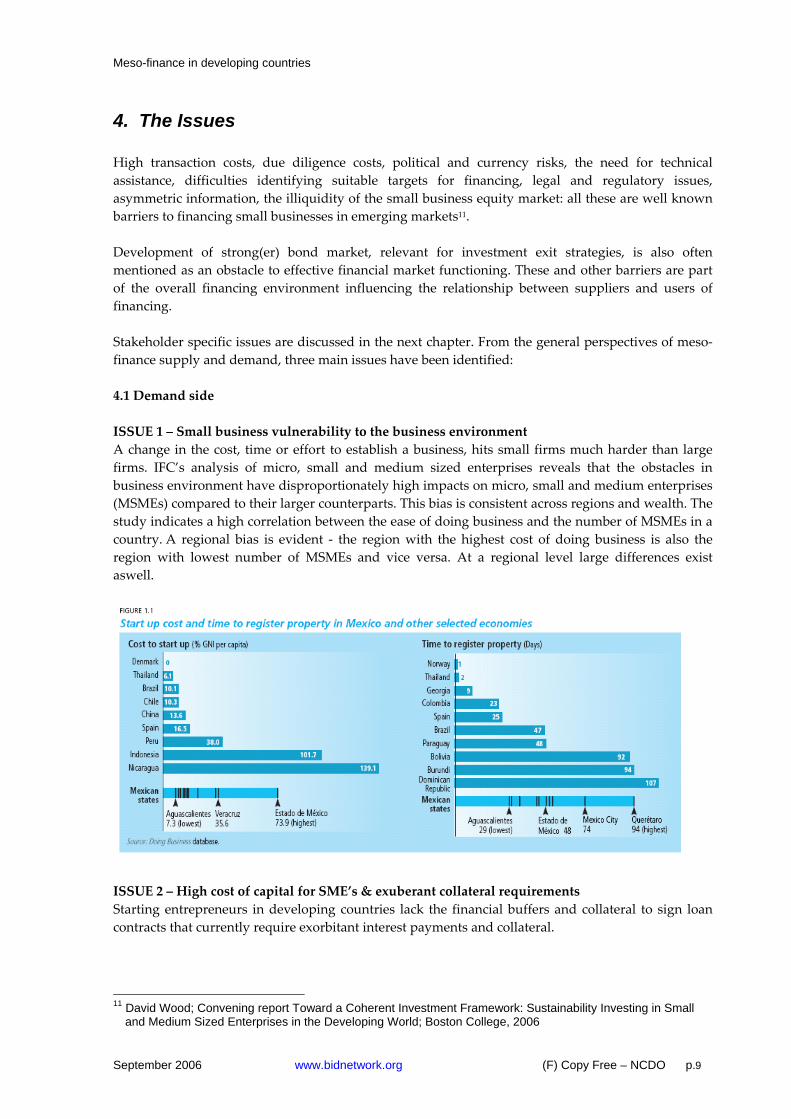

4. The Issues High transaction costs, due diligence costs, political and currency risks, the need for technical assistance, difficulties identifying suitable targets for financing, legal and regulatory issues, asymmetric information, the illiquidity of the small business equity market: all these are well known barriers to financing small businesses in emerging markets11. Development of strong(er) bond market, relevant for investment exit strategies, is also often mentioned as an obstacle to effective financial market functioning. These and other barriers are part of the overall financing environment influencing the relationship between suppliers and users of financing. Stakeholder specific issues are discussed in the next chapter. From the general perspectives of meso‐finance supply and demand, three main issues have been identified: 4.1 Demand side ISSUE 1 – Small business vulnerability to the business environment A change in the cost, time or effort to establish a business, hits small firms much harder than large firms. IFC’s analysis of micro, small and medium sized enterprises reveals that the obstacles in business environment have disproportionately high impacts on micro, small and medium enterprises (MSMEs) compared to their larger counterparts. This bias is consistent across regions and wealth. The study indicates a high correlation between the ease of doing business and the number of MSMEs in a country. A regional bias is evident ‐ the region with the highest cost of doing business is also the region with lowest number of MSMEs and vice versa. At a regional level large differences exist aswell.

ISSUE 2 – High cost of capital for SME’s & exuberant collateral requirements Starting entrepreneurs in developing countries lack the financial buffers and collateral to sign loan contracts that currently require exorbitant interest payments and collateral.

11 David Wood; Convening report Toward a Coherent Investment Framework: Sustainability Investing in Small

and Medium Sized Enterprises in the Developing World; Boston College, 2006

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.10

The lack of financial intermediaries servicing the SME segment and the lack of competition between them increases the price of financial services, i.e. the interest rate. The upward pressure is compounded by the higher risk of doing business as an SME and the lack of financial information. An informal sector SME has no (or limited) legal collateral – so a bank loan is out of the question. Currently, formal sector SMEs in many developing countries are often required to put up private collateral in addition to business estate collateral to banks. In some cases the collateral requirements are three times the loan value. This obviously restricts borrowing capacity of the firm12. ISSUE 3 – Lack of knowledge, education and market information A large number of small business owners do not have the know‐how to meet the business requirements set by banks to get bank loans and other forms of external financing. The major obstacle here is education and, accessibility to information on local market policies and business regulations13. Even if we dismiss the requirements of banks, the small business owners lack basic financial administration and regulation know‐how to successfully run their firm. 4.2 Supply side ISSUE 1 – Underdeveloped financial institution structure SMEs are omnipresent. Yet retail banking outlets are not. A shopkeeper in a rural village. A laundry service near a station. A metal workshop in a slum. A printing press in a small town. Where is their local bank? The owners of these businesses do not have the time to travel to the capital to get a loan. In Africa the problem is greatest. The African banking systems is the smallest in the world. Consequently African banks enjoy very little competition and few economies of scale. This again is reflected in very uncompetitive interest rates and a lack of distributional capacity14. This is exacerbated by governments restricting the entry of foreign banks. In such countries the state‐banks will often ‘crowd out’ more efficient private owned institutions.15 ISSUE 2 – Distorted lending infrastructure Many developing countries have poor lending infrastructure which also forms an obstacle to SME financing. For example: poor accounting standards may restrict financial statement lending; small business credit is restricted because the sharing of credit history information is restricted; asset‐based lending is limited by a weak legal system that cannot enforce commercial law or guarantee collateral rights; and poorly‐designed creditor rights and judicial enforcement of these rights may limit most types of lending16. ISSUE 3 – Lack of information Lack of market information affects not only interest rates, but also the diversity of SME credit services offered by a financial institution, as argued by Berger and Udell. For example the lack of information on payment and credit history results in poor risk assessment, higher credit risk and therefore higher interest rates. Countries with better information sharing capability lend more as a % of GDP. Also countries that are better at sharing credit information have better country‐level credit risk17. In the financial markets targeting SMEs the gathering of information costs more time and effort. So it is not

12 Jan Mulder, representative CIDRE, non-regulated financial NGO, Bolivia, 2005 13 Vanel Beuns; How to Improve Access to Finance for Small Firms? - Discussion topic Worldbank Private Sector

Development 14 Making finance work for Africa, A preview of the World Bank Report - to be published in late 2006 15 In Bolivia f.e. non-regulated financial NGO’s are legally restricted in attracting private commercial funding and

place equity investments 16 Berger, Udell; A More Complete Conceptual Framework for SME Finance - Worldbank 2004 17 Jappelli, Pagano; The European Experience with Credit Information Sharing - Journal of Banking and Finance,

2001

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.11

surprising that this is the least developed of type of financial information in less developed credit markets18.

18 Tylor Biggs; Is Small Beautiful and Worthy of Subsidy? Literature Review – published on WB.org

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.12

5. Stakeholders This chapter deals with meso‐finance stakeholders. Their role, their barriers to entry in the meso‐finance market and their needs are summarised. The demand side stakeholder is the SME entrepreneur themselves – they are omitted from this section as they are the object of this paper. 5.1 Supply‐Side Stakeholders Commercial retail banks Role Commercial retail banks can operate locally, downscale services and customise or localise

their financial services. In order to keep their corporate risk profiles to acceptable levels they can choose to co‐finance small businesses and share risk with a second party. They are distributor and administrator and cooperate with a small business development expert to fill the ‘local experience gap’. They are financial market and banking expert, provider of existing branch networks, administrator, distributor, co‐investor

Obstacles to entry They have a limit on minimum loan size. They lack equity financing expertise. They

perceive SME risk as too high. Their operational costs are too high. This makes expansion of their business model difficult.

What is needed to enter the meso‐finance market? Equity financing expertise. Risk leveraging facilities. Clear risk‐reward incentives. Rules of

thumb to cover for the lack of information on SMEs. Wholesale banks Role Wholesale banks can push for financial market development. They can lobby the

government for better SME policies and regulations and they can provide technical assistance for retail banks and financiers of SMEs. They can bring together organisations operating at the local and retail banking level to share information and experience.

Obstacles to entry Lack of awareness on missing middle/ meso‐finance issues, lack of meso‐finance retail

network, bureaucracy.

What is needed to enter the meso‐finance market? Marketing the relevance of the issue, clearly defining role and input, retail development of

meso‐finance, decentralised decision making power. Micro finance institutions (MFI’s) Role Micro finance institutions have strong networks at the local level. Their experience in

dealing with micro entrepreneurs can be useful to dealing with SMEs. The replacement of legal‐collateral for peer‐pressure collateral in micro finance could be applied to SMEs.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.13

Many clients of MFIs will eventually become too large for the MFI portfolio and will evolve into SME businesses. This means that MFIs have credit history, have ways of assessing risk, know how to deal with SMEs and have outreach in areas with no retail banking system.

Obstacles to entry There is a limit to the maximum size of of loans. They lack of equity financing expertise,

due diligence and monitoring methods. The business model is different. SME financing requires higher transaction costs per client compared to fast and standardised operations for micro finance.

What is needed to enter the meso‐finance market? Equity financing expertise, credit and investment management expertise, risk

management tools, financial product development, ways of dealing with transaction costs.

Non‐ Governmental Organisations (NGO’s) Role NGOs have networks in place where others have no networks. Some NGOs have well

established relationships with the local small business segment. If they don’t have the SME networks they are often capable of mobilising SMEs through other means. NGOs like the Dutch Agriterra and Indian Dhan Foundation help organise farmers into more professional businesses. Most of todays microfinance institutions have been built by NGOs. Also religious movements can be valuable in this sense and as a potential financial source. In summary: NGOs have small business development expertise, deal flow generation, promoting capacity building and favourable government regulation, local market presence, business support services, co‐investment

Obstacles to entry Lack of commercial insight and professional business management skills. Lack of

financing expertise, few of connections with local financial markets.

What is needed to enter the meso‐finance market? By working closely with a financial/commercial partner the NGO can act as a distribution

channel, network builder and preparing agent.

Domestic VC and PE funds Role Local venture capital and private equity funds like Tuninvest and Databank identify SME

investment opportunities, they assess them, invest, manage and help grow the SMEs. These VC funds have a wealth of local venture finance experience. They are flexible enough to change and try different business models. The fact that various pioneers have recently been starting meso‐finance activities with a VC approach is partial proof of their ability to serve the ‘missing middle’. They are entrepreneurial and have a market driven approach.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.14

Obstacles to entry Transaction costs. relative high risk/low return business. Remote location. Fragmented

markets. Cultural differences. Initial investment size, many SMEs are a hassle in comparison with larger deals.

What is needed to enter the meso‐finance market? Investor awareness and demand; creative solutions to legal issues and transaction costs;

risk hedging facilities; combined economic and social drive; Ability to exit from an SME, i.e. market liquidity.

(Western) VC and PE funds Role The overall tendency of investment in emerging markets is favourable. Emerging Market

Private Equity Association (EMPEA) estimates that 2005 fundraising for emerging markets private equity topped US$21 billion; fundraising for the asset class tripled. For private investors, meso‐finance can be the ‘social responsibility factor’ in their portfolio allocation. They are important for mobilising capital to developing countries. Acting like “wholesale” VC funds as it were. Expertise on entrepreneurship and sector expertise. They bring social networks and contacts with aid agencies with them but often not for the developing country context.

Obstacles to entry Lack of (contacts for) quality deal flow. Few channels for investment. Illiquidity of SME

finance market. Psychological paradox of ‘doing good’ and making profits. Lack of market information. High perceived risks/ ‘cowboy image’ of emerging market finance.

What is needed to enter the meso‐finance market? Appropriate channels and deal flow for investment. Liquidity of the SME finance market.

Understanding the successes and failures of meso‐finance business models. Simpler and cheaper due diligence methods. Risk hedging strategies.

5.3 Facilitating Stakeholders Local governments Role Governments of developing countries are very much aware of the importance and

catalysing effect of a strong private sector. They benefit from the ability of small businesses to enhance social return through access to new or growing markets for energy efficiency, biodiversity, clean technology and fair labour production19. A strong private sector is the stepping stone to generating market activity, attracting foreign investment and economic development.

19 Derived from David Wood; Convening report Toward a Coherent Investment Framework: Sustainability

Investing in Small and Medium Sized Enterprises in the Developing World; Institute for Responsible Investment, Boston College, 2006

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.15

Local governments fulfill the roles of facilitator, stimulator and beneficiary of private sector development

Obstacles to improved facilitation Fragmented market. Lack an understanding of the needs of meso‐finance stakeholders.

Poor market information to help enable business climate policy.

What is needed to facilitate the meso‐finance market? Policies that improve the business climate. Less regulation that cause delays and costs.

Better understanding of meso‐finance needs. Better local market information.

Governments and international regulators Role Create an enabling business environment. Improve the financial institution structures.

Improve legal frameworks. Deregulate or financial markets more efficient. Promote foreign investment. Co‐developing guarantee facilities.

Obstacles to better facilitation Lack of an integrated approach toward small business financing. Lack of market‐oriented

approach. Adherence to subsidies as a development tool. Lack of understanding of the ‘missing middle’ issues.

What is needed to facilitate the meso‐finance market? Recognition of meso‐finance opportunities. Formation of a ‘meso‐finance market’. Policy

and regulation that is conducive to SME development.

Small business experts/ sector organisations Role Local sector organisations like Trade and Investment centers or like the US Small Business

Administration and Chambers of commerce as well as business incubators are essential to SMEs. These organisations have direct contact with the larger SME entrepreneurs. So they are well positioned identify needs, pass on market information and alert financial stakeholders to the financing needs of SMEs. These centers can operate as a joint voice for the small business sector. Provider of business support services. Financing opportunity development. Local market expertise. Standardisation and facilitation of assessment procedures. They can match make investors and investees.

Obstacles to better facilitation Lack of funding. Lack of financing expertise from the investor’s perspective. Often poor

design of business support services. Insufficient use of partnership structures.

What is needed to facilitate the meso‐finance market? (Public) funding. Training in facilitation and small business needs. Standardisation.

Incentive based partnerships. Improved business support services. Better understanding of the matchmaking.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.16

Consultants Role For consultants an important role is the one of facilitator/ mediator between different

market parties. Many stakeholders acknowledge the fact that cooperation is key to meso‐finance. Differences in background, (organisational) culture, vision, business approach and way of working are all factors they have to deal with in closing partnerships. Roles: mediator, facilitator, advice on partnership design, business coaching, connector of market parties, interpreter and translator of intentions and ambitions.

Obstacles to entry Lack of market awareness on the ‘missing middle’ and its potential. Conservative market

approach by stakeholders. Willingness to pay for services.

What is needed to enter the meso‐finance market? Stakeholder recognition of meso‐finance market opportunities. Recognition of the value of

consultants as a broker, coach, facilitator.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.17

6. Existing business models & pioneers 6.1 Current forms of small business finance Currently the most common way of financing the start or growth of a small businesses in a developing country is through family capital20. Money lenders and commission agents –often called ‘loan sharks’‐ are a second source of finance. Their nickname points to the exuberant interest rates and the stringent terms they operate upon. They are able to do so because they operate in low competition and poorly informed environments based on high demand versus lack of supply of financial services in often desolated areas. In India the interest paid by farmers for this type of lending is generally between 18% and 36% (> 6x average market rate). The share of informal moneylenders and traders in farmersʹ outstanding debts remain as high as 43.3 % at the national level up to 81.9 % at regional level21. Local banks will offer loans to entrepreneurs if there is sufficient collateral (i.e. ≥100%) and credit records to back the loan. In Kenya, exuberant collateral obligations create the perverse situation that banks get richer by their lenders going bankrupt than by them succeeding in paying back their loans. Trade credit is another popular form of financing trading activities of small businesses in developing countries. As pointed out in the “Issues chapter” above, there is a severe lack of competition in the SME financing market – there are too few parties involved. Small entrepreneurs lack alternatives to turn to; they therefore either are constrained in business growth, or, they go for disadvantageous financing deals. 6.2 Pioneers in small business finance Several pioneering initiatives operate in and around the field of meso‐finance. They attempt to offer competitive financial services for small businesses. The famous microfinance pioneer, the Grameen Bank was one of the first to fill up the venture capital gap for ventures that promises good return on equity investments as well as direct and indirect benefits for the rural poor. The aim of their Grameen SME Fund is to provide equity finance to entrepreneurs with promising business and poverty alleviation potential, but with insufficient capital or collateral for their start‐ups. This fund focusses on ICTs and bio‐engineering22. Woman World Banking (WWB) and K‐Rep, both operating in Kenya. Both pioneer to extend their products out of the micro‐finance spectrum serving SMEs in the missing middle segment. WWB has acted as an intermediary with the commercial banking industry through their initiative the Global Network for Banking Innovation. This network of 24 organisations from 16 countries aims to stimulate cooperation between the commercial banking sector and the micro‐finance industry. This has spurred new product‐market combinations in micro and small business finance23. Some international equity funds acknowledge the presence of opportunities in the SME segment, but have as yet ‘hovered’ around the middle rather than financing in it. IFC for example, has invested in approximately 100 private equity funds which have together funded over 1,000 companies. Of these, about 500 are SMEs with an enterprise value of below $4 million. 100 SMEs have enterprise values below $500,000. Therefore only 10% targets the ‘missing middle’ segment. 20 After bank finance borrowing from family and friends is the chief source of funds for new business start-

ups in many countries – source: Basu & Parker Family finance and new business start-ups 21 Source: Rural credit: local lending still rules the roost – Punjab Agricultural University - 2006 22 http://www.grameen-info.org/grameen/gfund/index.html 23 http://www.swwb.org/spanish/1000/gnbi/gnbi_members_sp.htm

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.18

SEAF and AUREOS are relevant examples of internationally operating, non‐sectoral commercial funds active just ‘above’ the $ 500,000 level. They both focus on businesses underserved for reasons like investment size, remote location, cultural differences, or fragmentation within regional markets. SEAF has a portfolio with over $100 million invested in SMEs in Europe, Latin America, and Asia. The fund has managed 18 funds, targeting public investors, through which it has invested in over 200 companies, typically with $ 1‐5 million deals. AUREOS operates 16 funds, with some $ 380 million assets under management, placed with 169 investments with a typical deal size of $ 500,000 to $ 5 million. Business Partners Limited operates a similar business model in South Africa. CMI, In Return, SOVEC, Gexsi, The Blue Link and Cordaid are all developing their own commercial funds for serving the missing middle segment. They all operate with a commercial fund structure. They differ slightly in terms of fund size, sector and regional focus, partnership structure and investment policy. The fact that these initiatives have all been started over the last two years indicates that the SME financing market has been identified as a commercial opportunity. NCDO’s Guide for Venture Capital and Private Equity finds for development list 260 funds targetting developing countries. However, less than 10% of these funds target SME’s below the $ 500,000 investment level. 5.3 A note on subsidies and market distortions It is clear that MFIs and pioneering VC funds are entering the SME finance market. However, the development of this market, as with the development of many new markets in developing countries creates a substantial flow of subsuidies, technical assistance, soft loans, etc. Subsidy intervention in emerging economies is often criticised as a ‘medicine being worse than the disease’24. The is sufficient evidence of subsidized players ‘crowding out’ the budding or long established local businesses. There are also many examples of subsidized businesses collapsing once the donor finance is withdrawn. The adjacent micro finance industry is now coping with the challenging task of disentanglement from mass‐subsidization. These examples should serve as a warning that development of the SME market should focus only on commercially viabile market development25. Subsidies can be beneficial if used to improve the conditions needed for an SME finance market. These conditions aim to help facilitation and not the financing itself. i.e.the business climate, regulation, market information, business support or legal frameworks. At the business level, pro‐SME subsidisation policies could actually distort firm size and create economic inefficiencies. Beck, Demirguc‐Kunt, Levine argue that most subsidies to SMEs have unclear or unsecified results and performance targets like what an extra dollar of subsidy would bring in sterms of social and economic benefits26. These findings support a commercial approach of meso‐finance activities. At the market level things might deserve some modification. According to David Wood of Boston College, subsidies will be needed to bring the meso‐finance up from its current underdeveloped state to one that is fully commercial. Discovering ways to lower the transaction costs for SME finance as well as the development of risk abatement strategies which make subsidies necessary in the short to

24 Source: http://www.globalpolicy.org/socecon/bwi-wto/criticsindx.htm 25 Represents the line of thought of players now active in meso-finance funding – interview data, Pro Ideal 2006 26 Beck, Demirguc-Kunt, Levine ; SMEs, Growth, and Poverty: Cross-Country Evidence – Worldbank & University

of Minnesota, 2003

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.19

medium term. Wood’s key question is: How best can we structure the range of investments in sustainable SMEs so as to enable maturation of the market27? An interesting example aimed at developing this market commercially was launched by ACCION International, a leading microfinance player. ACCION recently created the Gateway MicroFinance Infrastructure Fund (GMI) to invest in technology and information service companies. The fund’s goal is to accelerate development of those companies whose goods and services can help the microfinance industry achieve greater scale and efficiency. Novib and AN Bank’s Triple Jump and ICCO’s Terrafina offer similar services. Although these services are aimed at the MFIs they are equally useful to SME finance organisations. These initiatives help create the right enabling environment for growth, without drawing energy away from core business activities28.

27 David Wood; Toward a Coherent Investment Framework: Sustainability Investing in Small and Medium Sized

Enterprises in the Developing World; Convening report, Boston College 2006 28 Source: http://www.accion.org/media_press_releases_detail.asp_Q_NEWS_E_265

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.20

7. Opportunities and solutions for meso-finance As a reminder, the analysis above identifies the following key issues for the development of a meso‐finance market:

1. Small firms are disproportionately vulnerable to the business environment 2. High cost of capital for SME’s & exuberant collateral requirements 3. Lack of knowledge, education and appropriate market information 4. Underdeveloped financial institution structure 5. Distorted lending infrastructure 6. Lack of market information

Generic issues include: ‐ high transaction costs (relative to investment size) ‐ political and cuurency risks ‐ high due diligence costs (relative to investment size) ‐ need for business support services ‐ identification of quality SME investment opportunities (information problem)

Possible Solutions 7.1 An Integrated approach Money alone is not the answer. SMEs need support from various angles. Better government policies, regulatory environment, business climate, legal framework, business support services, market information plus finance are all ingrediants needed to grow SMEs and the meso‐finance market. In the area of services most parties emphasise a need to focus on mixed financial service offerings. These include equity, quasi equity, partially secured loans with royalty payments attached. Improved financial services don’t come alone. SEAF states that, in many cases, the management of small enterprises requires adequate training and assistance as much as it needs capital29. All the pioneers in the previous chapter, offer integrated business support services in their business models. Technical assistance, network development and training and education are therefore offered along with finance. At the level of financial market regulation, SME’s report many more obstacles than access to finance alone30. The overall business environment facing both large and small firms – as measured by the ease of firm entry and exit, sound property rights, and contract enforcement – influences economic growth31. Being able to issue shares and certificates in SMEs in a country positively correlated to the level of foreign portfolio investment in a country32.

29 Source: http://www.seaf.com/support.htm 30 T. Beck & A. Demirguc-Kunt - How to Improve Access to Finance for Small Firms? - Discussion topic

Worldbank Private Sector Development 31 Beck, Demirguc-Kunt, Levine ; SMEs, Growth, and Poverty: Cross-Country Evidence – Worldbank & University

of Minnesota, 2003 32 April M. Knill; Can Foreign Portfolio Investment Bridge the Small Firm Financing Gap around the World? -

Worldbank group, 2005

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.21

7.2 Strategic partnerships An obvious result derived from the above and pointed out in the stakeholder chapter are the need for strategic partnerships. Combining expertise could well favour successful implementation of meso‐finance from the grassroot level to a national level. For example Business Partners South Africa took its business model to other African countries, beginning with Madagascar in tandem with a new IFC‐funded SME Solution Center. In this way they created a model that involves providing SMEs with integrated packages of financing, technical assistance, and market information. All of the pioneers have built their business models around similar partnerships constructs. The ‘information’ issue, i.e. market information, credit histories, sectoral/industry rsiks can largely be overcome through partnerships and information disclosure between local market stakeholders. 7.3 Business Support services Small business entrepreneurs need to develop their skills. They need to be able to present their business case to potential financiers. They need to do financial administration, manage personnel. They may need to diversify their products and services – at times without the have to bank‐roll their companies’ expansion33. The development of SMEs and the coaching of entrepreneurs falls under the umbrella term of Business Support Services. This valuable service is necessary in parrallel with finance. So‐called Small Business Information Centers (SBICs), can play an invaluable role here as a one‐stop shop for training, advice and market information. 7.4 Structured finance Structured finance means tailored financial product combinations to serve companies with unique financing needs. In terms of meso‐finance the focus is on tailoring financial products to the needs of SMEs. Structured finance can add a lot of value in terms of risk abatement, hedging of business environment characteristics and reinforcing financial product effectiveness. 7.5 Guarantees IFC and IDA provide a joint risk‐sharing ‘guarantee facility’ with the Republic of Madagascar and two local banks to make loans available to owners of small and medium enterprises34. Guarantees like these help mobilise local currency financing and encourage more lending to small businesses. Government guarantee facilities are often part of pro‐active foreign investment policy. In Colombia up to 50% of SME foreign investment is backed by the government under certain conditions35. 7.6 Leasing Leasing, though relatively new in this context, can provide a solution to financing of machinery, land and equipment for SMEs36. Among its many benefits: • Leasing functions in places where capital markets are less developed. The leased asset is the

collateral of the loan therefore security arrangements are simpler. • The pressure on SME cashflows is spread evenly over the lease period. Allowing the lessee to

save cash for working capital purposes. 33 Vanel Beuns; How to Improve Access to Finance for Small Firms? - Discussion topic Worldbank Private Sector

Development 34 Source: http://www.noticias.info/asp/aspComunicados.asp?nid=188107&src=0 35 Bancoldex – Pro Export http://www.proexport.com.co 36 More on the subject of leasing: Fletcher, Freeman, e.a.: Leasing in development – guidelines for emerging

markets – IFC 2005 - http://www.ifc.org/ifcext/sme.nsf/AttachmentsByTitle/Leasing_in_Dev_Nov05.pdf/$FILE/Leasing_in_Dev_Nov05.pdf

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.22

• Tax incentives related to leasing make it an interesting financing method. • Leasing promotes investment in capital equipment, increases competition in the financial sector,

and facilitates the transfer of new technology 7.7 (Reverse) factoring Factoring is a service which provides an SME with money now for a percentage of the invoices still due to the SME. i.e. financing of a company’s accounts receivable. Therefore the accounts receivable play the role of collateral. Ordinary factoring has in general not been profitable in emerging markets however. Firstly, because credit histories are unavailable or difficult to verify. Secondly, developing countries have weak enforcement procudres for invoice and debt collection. This poses a large risk to the factoring organisation. Thirdly, fraud is a big problem in this industry. One solution to these barriers to factoring is the technology often referred to as ‘Reverse Factoring’. In this case, the lender purchases accounts receivables only from high‐quality buyers (e.g. any receivable from a specific informationally transparent buyer). The factor only needs to collect credit information and calculate the credit risk for a few selected buyers (such as a large, internationally accredited firm). The main advantage of reverse factoring is that the credit risk is equal to the default risk of the high‐quality customer, and not the risky SME. This arrangement allows creditors in developing countries to factor ‘without recourse’ and provide low‐risk loans to high‐risk suppliers. 7.8 Capturing current trend in Socially Responsible Investment (SRI) Similar to microfinance, meso‐finance holds the opportunity for investment with the promise of social and financial returns. In this way the Meso‐finance market potentially offers a much larger financial market for SRI investors. It offers a way of diversifying SRI funds from their standard portfolios which often include ‘western sustainable’ companies like MicroSoft, Procter and Gamble, ABN Amro Bank and others. From the investors perspective this investment strategy could, like micro finance, bring the hedging benefits such as negative correllations with the regular financial market. 7.9 Using existing networks There is potential for financial operators to expand their core business into meso‐finance. This can be achieved by filling their expertise gaps through partnerships and existing networks. Making smart use of local, often informal, financial service networks may be a key to meso‐finance success. Rural Mexico has many examples. There are non‐bank depository institutions like Sociedades de Ahorro y Préstamo, SAPs and postal savings systems. There are formally licensed and informal institutions such as cooperativas de ahorro y crédito and cajas solidarias. Also rotating savings and credit associations (tandas), moneykeepers, savings groups and personal lenders, as well as loan sharks. These all form an unstructured yet effective and demand driven financing ecosystem. These players possess a competitive advantage hard to come by for outsiders: they know the local economic and social codes of conduct for assessing and dealing with small businesses. If enrolled in an integral approach of meso‐finance and given incentives to team up and cooperate, local market knowledge and the level of market penetration of even loan sharks can be of significant value in deal flow generation, managing key market information and distribution and monitoring of meso‐finance activities.

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.23

7.11 Reduced or simpler due diligence requirements Proper due diligence is expensive. In the meso‐finance segment ($5000 ‐ $500,000) it is often more expensive than the financing amount itself. It may in some cases make financial sense to do no or little due diligence at all. This situation arises once there is better insight into SME risk and banrupcy. If for example SME failure rate is 40%, but the total sum of due diligence costs is greater or equal to 40% of the invested amounts, it is wiser to invest the money in the SME and support services rather than spend it on consultants and accountants. 7.12 Creative application of existing financing models A critical success factor in the micro‐finance sector is the group lending method. The leading principle behind it is shared responsibility of all group members for loan repayment. This peer‐pressure works very well. If transposed and adapted to SMEs, this principle could well be one of the solutions for meso‐finance. Cooperatives already do exactly this. The key to making this work for SMEs is by clustering them in ways that are logical. A cluster comprising of a supply chain of SMEs or with similar or complementary activities. Small business ‘clusters’ could reduce risk, help increase specialisation, increase production capacity and increase market outreach. These factors combined could well make meso‐finance attractive. Countries like Taiwan, Hong Kong, and Italy have shown that SME clustering can be an effective approach to compete directly in export markets. Working through industry‐based clusters, SME exporters in these countries have created competitive niches in world markets and prospered. The ability to develop competitive industry clusters is strongly related to family based social networks particular to these countries though. These clusters have shown to reduce transaction costs substantially through the provision of shared‐services, like back‐office administration or common sales representation, which are needed in day‐to‐day operations37. For this SME cluster approach to work a good understanding of local social‐network dynamics is required as well as strong organisational skills.38.

37 Tylor Biggs; Is Small Beautiful and Worthy of Subsidy? Literature Review – 38 Source: Bianchi, Miller, Bertini; The Italian SME experience and possible lessons for emerging countries –

1997, www.unido.org

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.24

Further Reading • April M. Knill; Can Foreign Portfolio Investment Bridge the Small Firm Financing Gap around the World? ‐Worldbank group, 2005

• Basu, A. and S.C. Parker; Family Finance and New Business STart‐Ups ‐ 1999/ 2000 www.rdg.ac.uk/Econ/Econ/workingpapers/emdp419.pdf

• Beck, Demirguc‐Kunt, Levine; SMEs, Growth, and Poverty: Cross‐Country Evidence – Worldbank & University of Minnesota, 2003 http://www.worldbank.org/research/bios/tbeck/sme.pdf

• Berger, Udell; A More Complete Conceptual Framework for SME Finance ‐ Worldbank 2004 http://www.worldbank.org/research/projects/sme/Financing_Framework_berger_udell.pdf

• Bianchi, Miller, Bertini; The Italian SME experience and possible lessons for emerging countries – 1997

• Committee of Donor Agencies for Small Enterprise Development; Business Development Services for small enterprises – 2001 – SME Dept. World Bank.

• Cull, Davis, Lamoureaux; Historical Financing of Small‐ and Medium Size Enterprises – Worldbank http://www.worldbank.org/research/projects/sme/Historical_financing_of_SMEs.pdf

• David Wood; Convening report Toward a Coherent Investment Framework: Sustainability Investing in Small and Medium Sized Enterprises in the Developing World ‐ Boston College, 2006

• Diaz Villeda, Hansel; The Missing Link in the Value Chain: Financing for Rural Farmers and Microentrepreneurs; Strategic Alliances for Financial Services and Market Linkages in Rural Areas – The SEEP network, 2005

• Fletcher, Freeman, e.a.; Leasing in development – guidelines for emerging markets – IFC 2005 http://www.ifc.org/ifcext/sme.nsf/AttachmentsByTitle/Leasing_in_Dev_Nov05.pdf/$FILE/Leasing_in_Dev_Nov05.pdf

• Jappelli, Pagano; The European Experience with Credit Information Sharing ‐ Journal of Banking and Finance, 2001

• Leora Klapper; The role of reverse factoring for financing small and medium enterprises – Worldbank 2005 http://www.worldbank.org/external/default/WDSContentServer/IW3P/IB/2005/05/15/000090341_20050515140836/Rendered/PDF/wps3593.pdf

• MSME database – IFC http://rru.worldbank.org/Documents/other/MSMEdatabase/msme_database.htm

• NCDO; Venture Capital and private Equity Funds for Development – index 2005 http://www.bidnetwork.org/artefact‐12005‐en.html

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.25

• NCDO, FACET BV; Venture capital and private equity as a means to promote sustainable entrepreneurship in Africa – 2005 http://www.facetbv.nl/

• NCDO; People – plans – profit for poverty reduction, a publication of the Business in Development Challenge ‐ 2005 http://www.bidnetwork.org/artefact‐13709‐en.html

• Punjab Agricultural University ‐ Rural credit: local lending still rules the roost –2006 • PWC Diagnostic Chart – business growth stages http://www.pwcglobal.com/nz/eng/ins‐sol/publ/pcs/DiagnosticChart.pdf

• SEAF ‐ The Development Impact of Small and Medium Enterprises ‐ 2005 • Tylor Biggs; Is Small Beautiful and Worthy of Subsidy? Literature Review – http://rru.worldbank.org/Documents/PapersLinks/TylersPaperonSMEs.pdf

Meso-finance in developing countries

September 2006 www.bidnetwork.org (F) Copy Free – NCDO p.26

Organisations invited to the Meso-finance seminar (* participants)

360 responsibility* ABN AMRO* African Humanitarian* AIDEnvironment* Anthos Aqua for all Argidius Foundation ASN bank* ATA International Stichting* Atlas Ventures Atradius CBI Chairman* CMI* Cordaid* Cross Lines Foundation* d.o.b foundation* DDE DGIS DOEN Foundation* Dun and Bradstreet* E+Co Ecosecurities EIM EMF* EVD* Extent Ex‐VU FACET BV* Fair Ventures* FMO* Fortis* GEXSI‐Global Exchange for Social Investment* GITTS International* Grameen Fund* Het Groene Woud Hivos HPC ICCO* IFC IHE DELFT ILO TURIJN IMK advies In Return Capital Indian Scool of Business* ING InReturn BV* Institute for Responsible Investment, Boston College* Intent Interpolis ISS Kamer van Koophandel Rotterdam

KIT K‐Rep Bank* Life Sciences group MDF Mesics* Ministry of Economic Affairs Ministry of Foreign Affairs* NCDO* NEI NFX* Oiko Credit Nederland* ONDERNEMERSHUIS ZUID OOST OXFAM NOVIB People Planet Profit Magazine* PH Visie Planet Capital PRIVE ADRES OP INTENT Pro Ideal* PSOM / EVD PUM* Rabobank / Schretlen & Co* Rabobank Foundation* SEAF* Send money home Shell Livewire SME Solutions Center Kenya, International Finance Corporation* SNS REAAL Waterfonds N.V.* SOVEC* Steve co Steveco int. BV* Stichting Beheer Oikocredit Nederland Fonds* Stichting Doen Stichting Het Groene Woudt* Stichting IntEnt* Stimulans TBL Invest BV* Tendris Terrafina* The Blue Link Triodos Triple Jump UNDP UNESCO‐IHE* Universiteit Maastricht Valentus BV* VC F 4 Africa Vodafone Woord en Daad XSML*