Merrill Lynch - Swiss Re

13

ab Merrill Lynch Banking & Insurance CEO Conference Jacques Aigrain Chief Executive Officer London, 4 October 2007 Slide 2 ab Merrill Lynch CEO Conference 4 October 2007 Today’s agenda “Delivering Growth in a Riskier World” Generate economic profit growth Reduce earnings volatility Enlarge market scope ILS - reduce risk and provide growth Summary and outlook

Transcript of Merrill Lynch - Swiss Re

abMerrill LynchBanking & Insurance CEO Conference

Jacques AigrainChief Executive Officer

London, 4 October 2007

Slide 2

ab

Merrill LynchCEO Conference4 October 2007

Today’s agenda

“Delivering Growth in a Riskier World”Generate economic profit growth Reduce earnings volatilityEnlarge market scope ILS - reduce risk and provide growth

Summary and outlook

Slide 3

ab

Merrill LynchCEO Conference4 October 2007

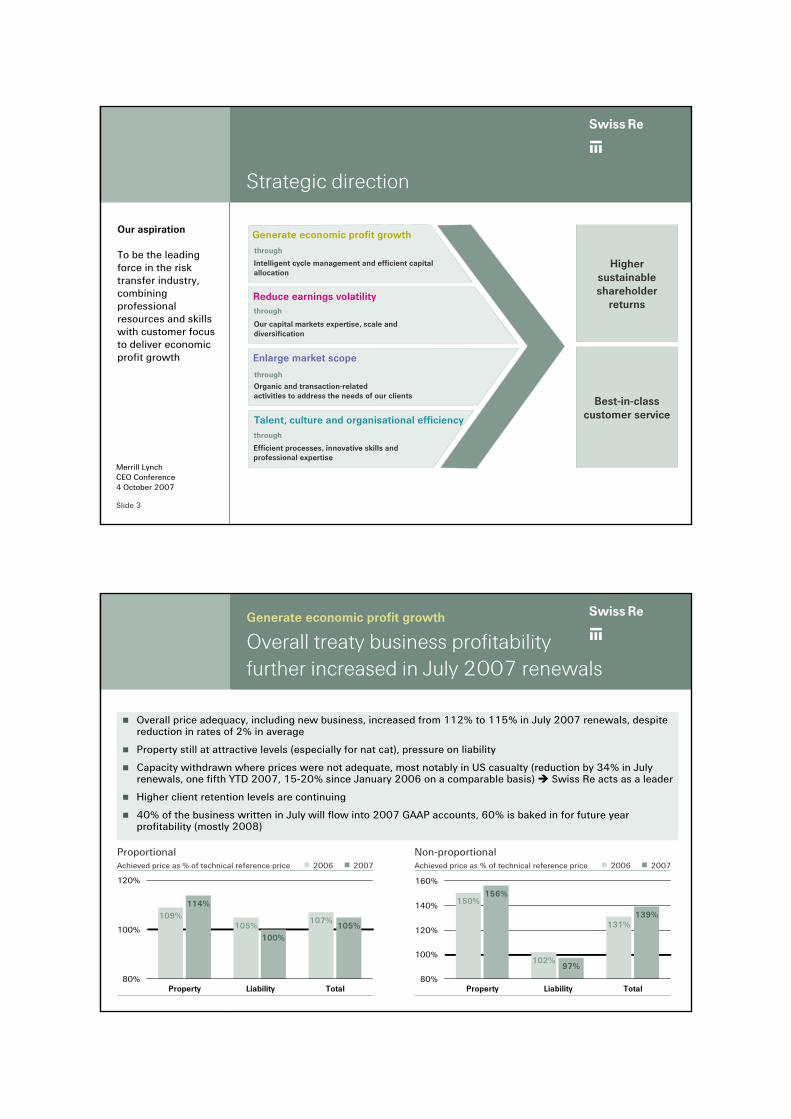

Strategic direction

Our aspiration

To be the leading force in the risk transfer industry, combining professional resources and skills with customer focus to deliver economic profit growth

Generate economic profit growth

Higher sustainable shareholder

returns

Best-in-classcustomer service

Reduce earnings volatility

Enlarge market scope

Our capital markets expertise, scale and diversification

Organic and transaction-related activities to address the needs of our clients

Efficient processes, innovative skills and professional expertise

Talent, culture and organisational efficiency

Intelligent cycle management and efficient capital allocation

through

through

through

through

Slide 4

ab

Merrill LynchCEO Conference4 October 2007

ProportionalAchieved price as % of technical reference price 2006 2007 Total

Overall treaty business profitability further increased in July 2007 renewals

Generate economic profit growth

Overall price adequacy, including new business, increased from 112% to 115% in July 2007 renewals, despite reduction in rates of 2% in average

Property still at attractive levels (especially for nat cat), pressure on liability

Capacity withdrawn where prices were not adequate, most notably in US casualty (reduction by 34% in July renewals, one fifth YTD 2007, 15-20% since January 2006 on a comparable basis) Swiss Re acts as a leader

Higher client retention levels are continuing

40% of the business written in July will flow into 2007 GAAP accounts, 60% is baked in for future year profitability (mostly 2008)

109%105%

107%

114%

100%105%

80%

100%

120%

Property Liability Total

Non-proportionalAchieved price as % of technical reference price 2006 2007

150%

102%

131%

156%

97%

139%

80%

100%

120%

140%

160%

Property Liability Total

Slide 5

ab

Merrill LynchCEO Conference4 October 2007

52 week renewals traditional portfolio

July 2006 to July 2007 renewalsGrowth at high quality point of cycle

All renewal figures are estimated and calculated at constant FX rates

Since July 2006 Swiss Re has grown its non-life reinsurance portfolio by 13%

Premium volume for “old” Swiss Re book at stable levels complemented by successful renewals of acquired Insurance Solutions business

Increase on renewed Swiss Re book includes 1% higher margins

Former Insurance Solutions business underwritten and priced on Swiss Re standards with improvement in underlying profitability

100%

78%

13% 113%-22% 4% 18%

0%

25%

50%

75%

100%

125%

Total renewable July 2006 to

July 2007

Cancelledor replaced

Renewed Increase on renewal

New business/replacement

Insurance Solutions

Estimated outcome

Represents 5% increase on the renewed block, comprising:Rates 1%Change in share 2%Exposure growth 2%

Generate economic profit growth

Slide 6

ab

Merrill LynchCEO Conference4 October 2007

Outlook January 2008 renewalsContinued bottom line focus – at expense of top line if necessary

Property Europe (incl. nat cat)

Casualty overall (excl. motor)

Casualty critical risks/products

Specialties

Property US (incl. nat cat)

Generate economic profit growth

Credit

Life and health

Motor

Expected development of reinsurance rates

Slide 7

ab

Merrill LynchCEO Conference4 October 2007

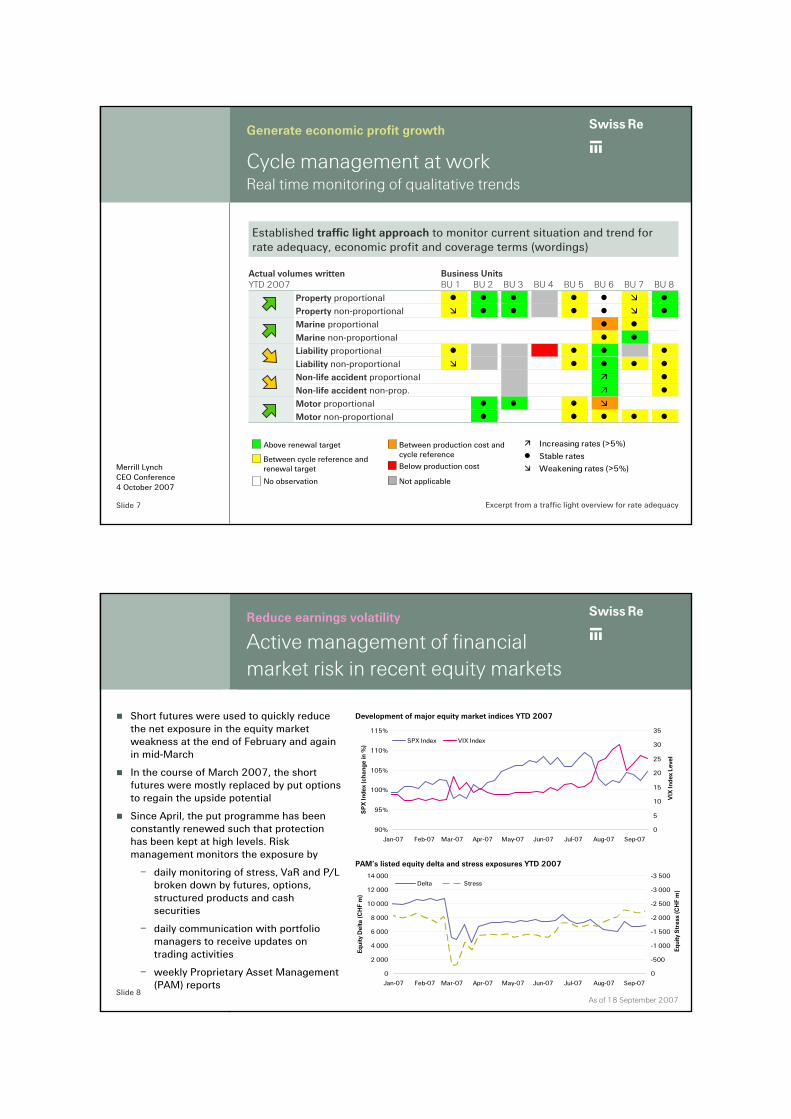

Cycle management at workReal time monitoring of qualitative trends

Established traffic light approach to monitor current situation and trend for rate adequacy, economic profit and coverage terms (wordings)

Excerpt from a traffic light overview for rate adequacy

Above renewal target

Between cycle reference and renewal target

Between production cost and cycle referenceBelow production cost

Increasing rates (>5%)Stable ratesWeakening rates (>5%)

Generate economic profit growth

BU 8BU 7BU 6BU 5BU 4BU 3BU 2BU 1YTD 2007Actual volumes written

Motor non-proportionalMotor proportionalNon-life accident non-prop.Non-life accident proportionalLiability non-proportionalLiability proportionalMarine non-proportionalMarine proportionalProperty non-proportionalProperty proportional

Business Units

No observation Not applicable

Slide 8

ab

Merrill LynchCEO Conference4 October 2007

Active management of financial market risk in recent equity markets

Short futures were used to quickly reduce the net exposure in the equity market weakness at the end of February and again in mid-March

In the course of March 2007, the short futures were mostly replaced by put options to regain the upside potential

Since April, the put programme has been constantly renewed such that protection has been kept at high levels. Risk management monitors the exposure by

– daily monitoring of stress, VaR and P/L broken down by futures, options, structured products and cash securities

– daily communication with portfolio managers to receive updates on trading activities

– weekly Proprietary Asset Management (PAM) reports

PAM’s listed equity delta and stress exposures YTD 2007

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Jul-07 Aug-07 Sep-07

Equi

ty D

elta

(CH

F m

)

-3 500

-3 000

-2 500

-2 000

-1 500

-1 000

-500

0

Equi

ty S

tres

s (C

HF

m)

Delta Stress

90%

95%

100%

105%

110%

115%

Jan-07 Feb-07 Mar-07 Apr-07 May-07 Jun-07 Jul-07 Aug-07 Sep-07

SP

X In

dex

(cha

nge

in %

)

0

5

10

15

20

25

30

35

VIX

Inde

x Le

vel

SPX Index VIX Index

Development of major equity market indices YTD 2007

As of 18 September 2007

Reduce earnings volatility

Slide 9

ab

Merrill LynchCEO Conference4 October 2007 0

500

1000

1500

2000

2500

Q2 06 Q3 06 Q4 06 Q1 07 Q2 07

Cre

dit S

prea

d S

tres

s Ex

posu

re(C

HF

m)

Gross Net

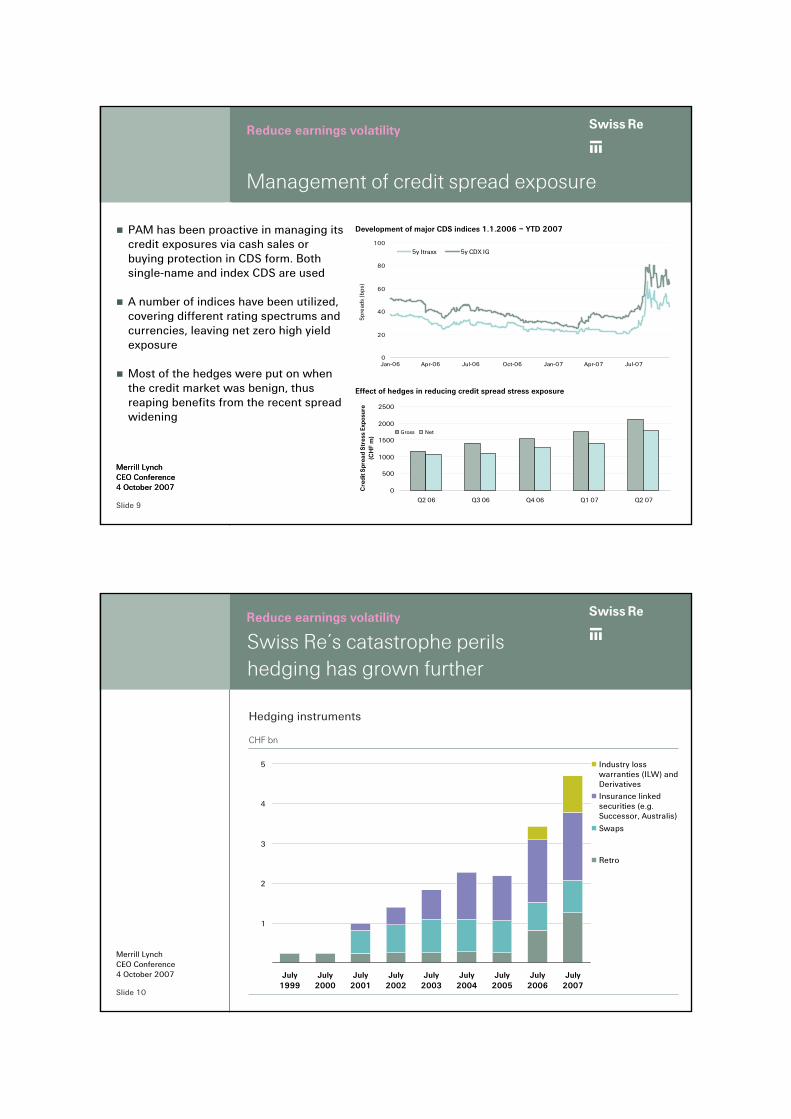

Management of credit spread exposure

PAM has been proactive in managing its credit exposures via cash sales or buying protection in CDS form. Both single-name and index CDS are used

A number of indices have been utilized, covering different rating spectrums and currencies, leaving net zero high yield exposure

Most of the hedges were put on when the credit market was benign, thus reaping benefits from the recent spread widening

0

20

40

60

80

100

Jan-06 Apr-06 Jul-06 Oct-06 Jan-07 Apr-07 Jul-07Sp

read

s (b

ps)

5y Itraxx 5y CDX IG

Development of major CDS indices 1.1.2006 – YTD 2007

Effect of hedges in reducing credit spread stress exposure

Merrill LynchCEO Conference4 October 2007

Reduce earnings volatility

Slide 10

ab

Merrill LynchCEO Conference4 October 2007

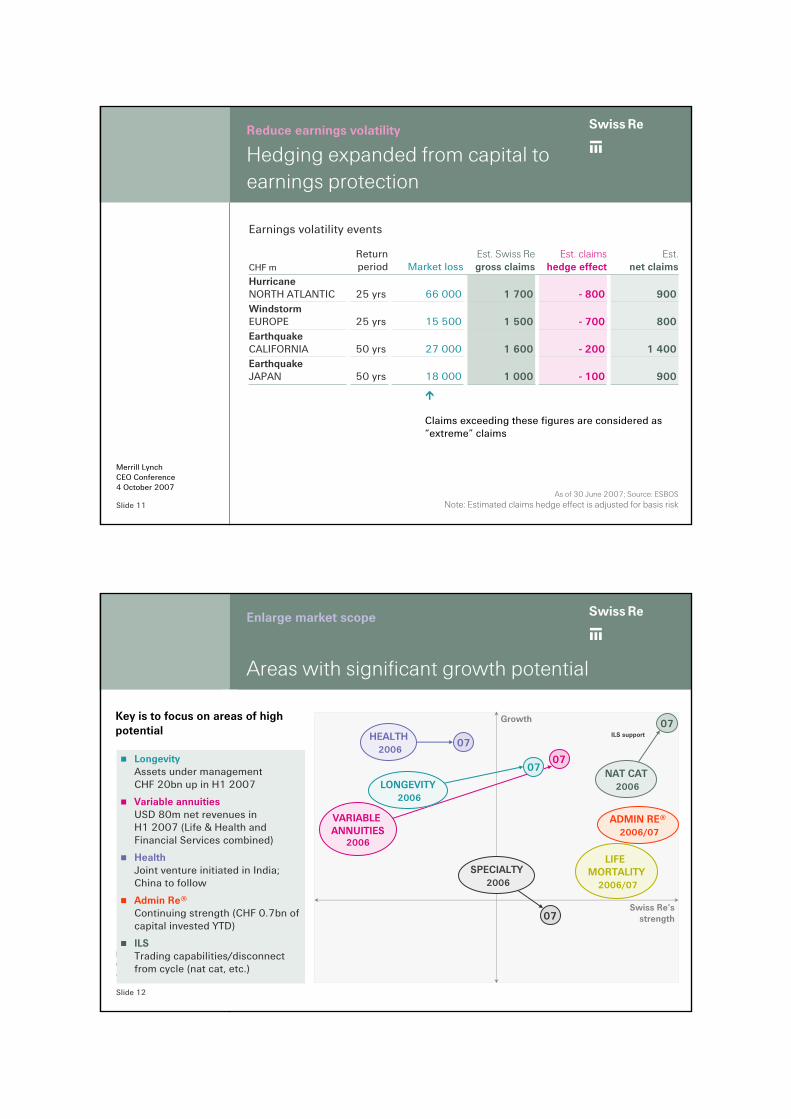

Swiss Re’s catastrophe perils hedging has grown further

1

2

3

4

5

July1999

July2000

July2001

July2002

July2003

July2004

July2005

July2006

July2007

Industry losswarranties (ILW) andDerivativesInsurance linkedsecurities (e.g.Successor, Australis)

Swaps

Retro

CHF bn

Hedging instruments

Reduce earnings volatility

Slide 11

ab

Merrill LynchCEO Conference4 October 2007

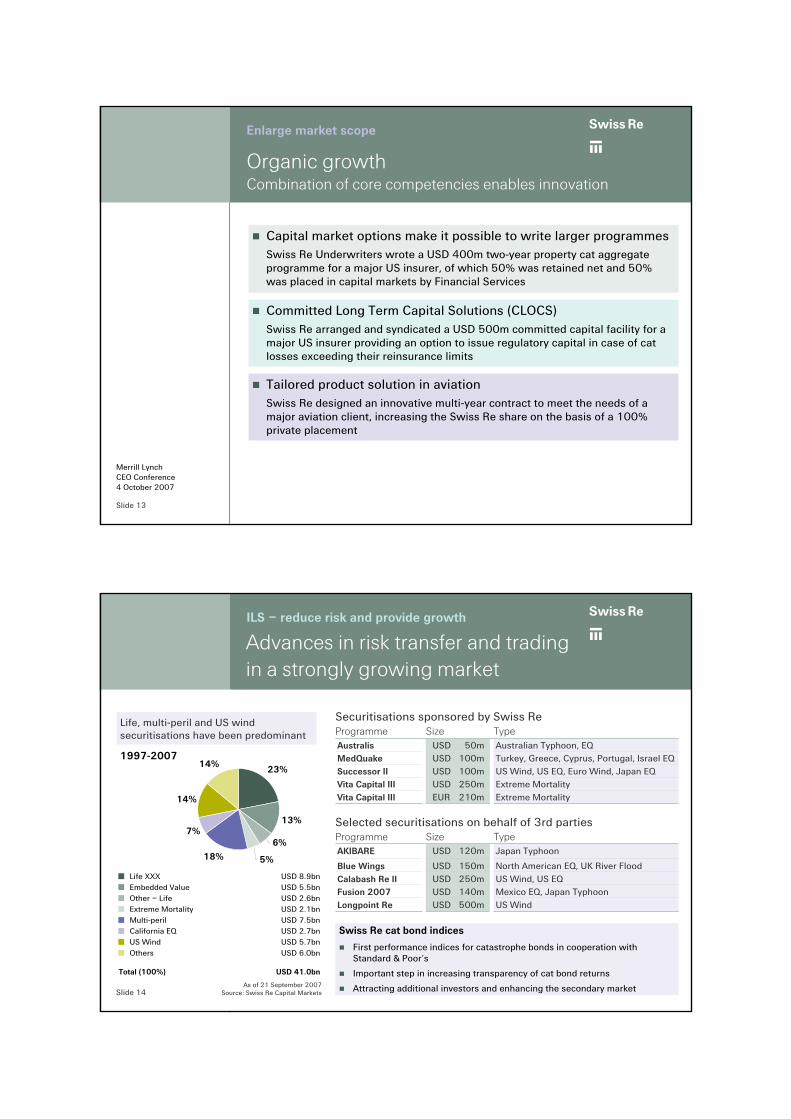

Hedging expanded from capital to earnings protection

Claims exceeding these figures are considered as “extreme” claims

CHF m

50 yrs

50 yrs

25 yrs

25 yrs

Return period

Earnings volatility events

18 000

27 000

15 500

66 000

Market loss

1 000

1 600

1 500

1 700

Est. Swiss Regross claims

- 100

- 200

- 700

- 800

Est. claimshedge effect

900

1 400

800

900

Est.net claims

EarthquakeJAPAN

EarthquakeCALIFORNIA

WindstormEUROPE

HurricaneNORTH ATLANTIC

As of 30 June 2007; Source: ESBOSNote: Estimated claims hedge effect is adjusted for basis risk

Reduce earnings volatility

Slide 12

ab

Merrill LynchCEO Conference4 October 2007

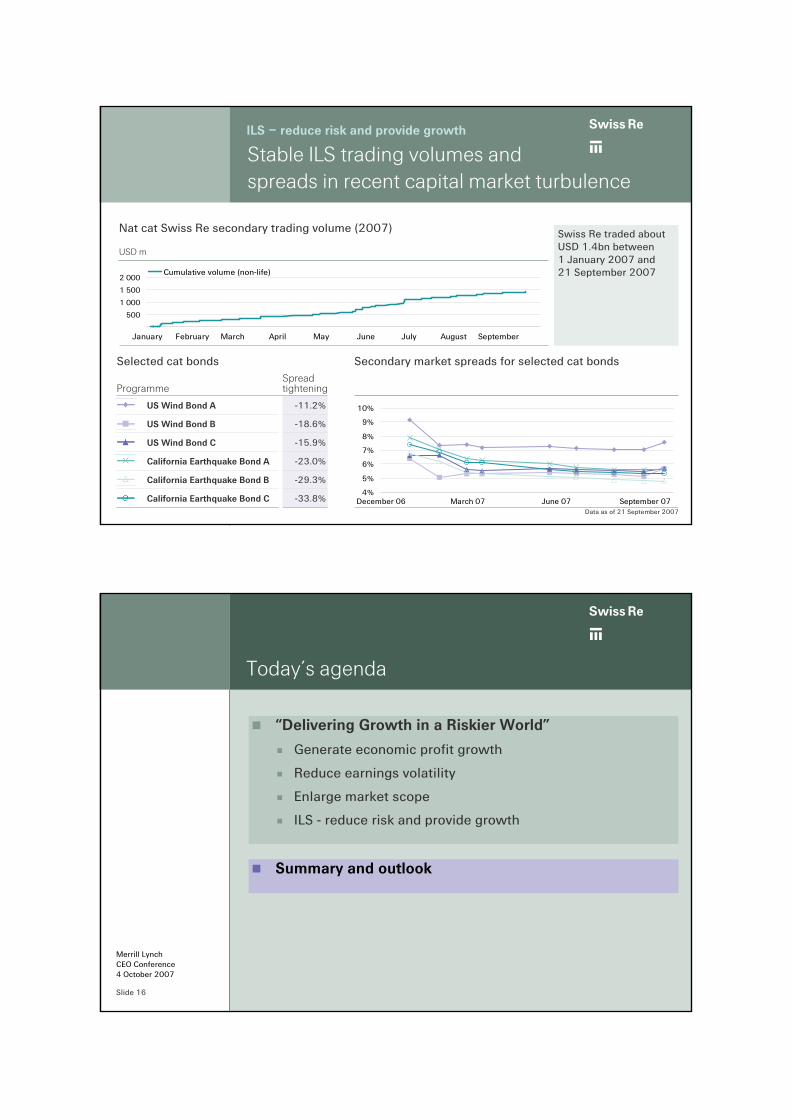

Key is to focus on areas of high potential

Growth

Swiss Re’s strength

07

07

07

07

07

ILS support

LIFE MORTALITY

2006/07

ADMIN RE®2006/07

LongevityAssets under management CHF 20bn up in H1 2007

Variable annuitiesUSD 80m net revenues in H1 2007 (Life & Health and Financial Services combined)

HealthJoint venture initiated in India; China to follow

Admin Re®Continuing strength (CHF 0.7bn of capital invested YTD)

ILSTrading capabilities/disconnect from cycle (nat cat, etc.)

Areas with significant growth potential

Enlarge market scope

SPECIALTY2006

NAT CAT2006

VARIABLE ANNUITIES

2006

LONGEVITY2006

HEALTH2006

Slide 13

ab

Merrill LynchCEO Conference4 October 2007

Committed Long Term Capital Solutions (CLOCS)Swiss Re arranged and syndicated a USD 500m committed capital facility for a major US insurer providing an option to issue regulatory capital in case of cat losses exceeding their reinsurance limits

Organic growth Combination of core competencies enables innovation

Capital market options make it possible to write larger programmesSwiss Re Underwriters wrote a USD 400m two-year property cat aggregate programme for a major US insurer, of which 50% was retained net and 50% was placed in capital markets by Financial Services

Enlarge market scope

Tailored product solution in aviationSwiss Re designed an innovative multi-year contract to meet the needs of a major aviation client, increasing the Swiss Re share on the basis of a 100% private placement

Slide 14

ab

Merrill LynchCEO Conference4 October 2007

23%

13%

6%

5%18%

7%

14%

14%

Advances in risk transfer and trading in a strongly growing market

As of 21 September 2007Source: Swiss Re Capital Markets

Life XXX

Multi-peril

US Wind

Other – Life

California EQ

Others

Embedded Value

Extreme Mortality

Life, multi-peril and US wind securitisations have been predominant

ILS – reduce risk and provide growth

Extreme MortalityUSD 250mVita Capital IIIExtreme MortalityEUR 210mVita Capital III

US Wind, US EQ, Euro Wind, Japan EQUSD 100mSuccessor II

Securitisations sponsored by Swiss Re

USD 100mUSD 50m

SizeAustralian Typhoon, EQAustralisTurkey, Greece, Cyprus, Portugal, Israel EQMedQuake

TypeProgramme

Mexico EQ, Japan TyphoonUSD 140mFusion 2007US WindUSD 500mLongpoint Re

US Wind, US EQUSD 250mCalabash Re II

Selected securitisations on behalf of 3rd parties

USD 150m

USD 120m

SizeJapan TyphoonAKIBARE

North American EQ, UK River FloodBlue Wings

TypeProgramme

USD 8.9bn

USD 7.5bn

USD 5.7bn

USD 2.6bn

USD 2.7bn

USD 6.0bn

USD 5.5bn

USD 2.1bn

Total (100%) USD 41.0bn

Swiss Re cat bond indices

First performance indices for catastrophe bonds in cooperation with Standard & Poor’s

Important step in increasing transparency of cat bond returns

Attracting additional investors and enhancing the secondary market

1997-2007

Slide 15

ab

Merrill LynchCEO Conference4 October 2007

Stable ILS trading volumes and spreads in recent capital market turbulence

-33.8%

-29.3%

-23.0%

-15.9%

-18.6%

-11.2%

Spread tightening

California Earthquake Bond B

California Earthquake Bond A

California Earthquake Bond C

US Wind Bond C

Selected cat bonds

US Wind Bond A

US Wind Bond B

Programme

Data as of 21 September 2007

4%

5%

6%

7%

8%

9%

10%

December 06 March 07 June 07 September 07

Secondary market spreads for selected cat bonds

ILS – reduce risk and provide growth

Swiss Re traded about USD 1.4bn between 1 January 2007 and 21 September 2007

USD m

Nat cat Swiss Re secondary trading volume (2007)

500

1 000

1 500

2 000

January February March April May June July August September

Cumulative volume (non-life)

Slide 16

ab

Merrill LynchCEO Conference4 October 2007

Today’s agenda

“Delivering Growth in a Riskier World”

Generate economic profit growth

Reduce earnings volatility

Enlarge market scope

ILS - reduce risk and provide growth

Summary and outlook

Slide 17

ab

Merrill LynchCEO Conference4 October 2007

PresentBuy and Hold

or Sell

PastBuy and Hold

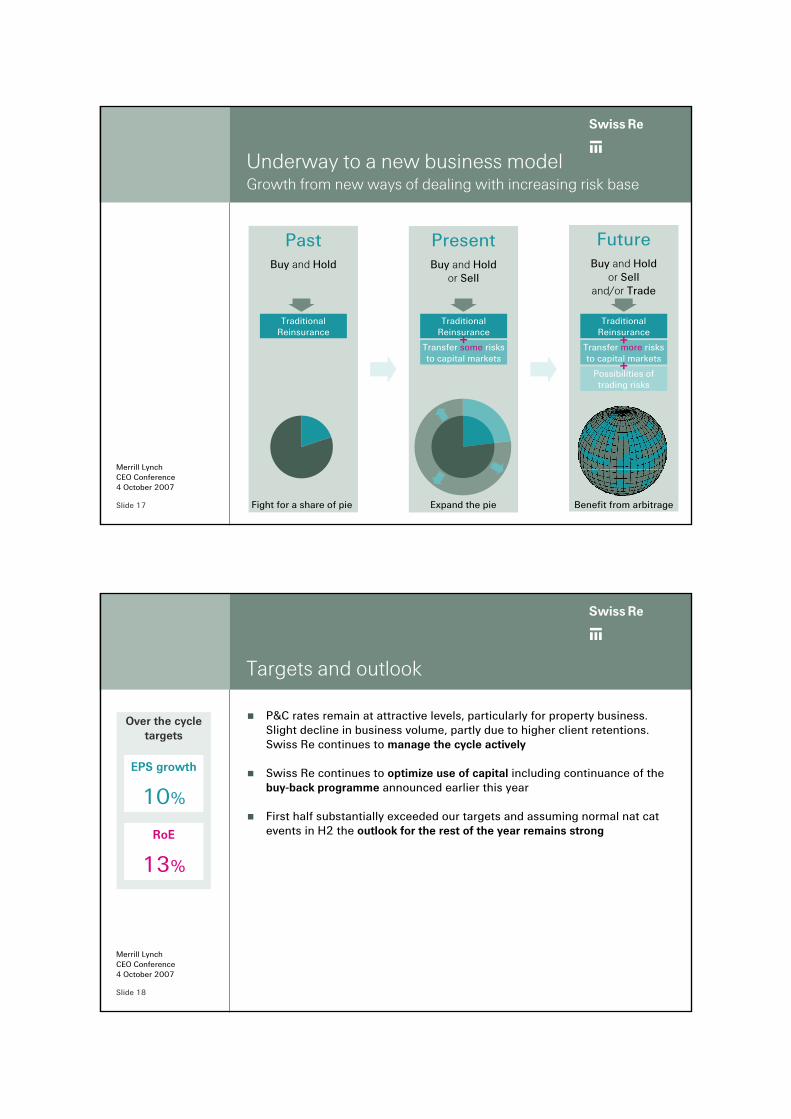

Underway to a new business model Growth from new ways of dealing with increasing risk base

FutureBuy and Hold

or Sell and/or Trade

Fight for a share of pie

Traditional Reinsurance

Transfer more risks to capital markets

Possibilities of trading risks

+

+

Traditional Reinsurance

Transfer some risks to capital markets

Traditional Reinsurance

+

Expand the pie Benefit from arbitrage

Slide 18

ab

Merrill LynchCEO Conference4 October 2007

Targets and outlook

P&C rates remain at attractive levels, particularly for property business. Slight decline in business volume, partly due to higher client retentions. Swiss Re continues to manage the cycle actively

Swiss Re continues to optimize use of capital including continuance of the buy-back programme announced earlier this year

First half substantially exceeded our targets and assuming normal nat cat events in H2 the outlook for the rest of the year remains strong

Over the cycle targets

EPS growth

10%

RoE

13%

Slide 19

ab

Merrill LynchCEO Conference4 October 2007

Swiss Re’s strategic priorities designed for “Delivering Growth in a Riskier World”

Our aspiration

To be the leading force in the risk transfer industry, combining professional resources and skills with customer focus to deliver economic profit growth

Generate economic profit growth

Higher sustainable shareholder

returns

Best-in-classcustomer service

Reduce earnings volatility

Enlarge market scope

Our capital markets expertise, scale and diversification

Organic and transaction-related activities to address the needs of our clients

Efficient processes, innovative skills and professional expertise

Talent, culture and organisational efficiency

Intelligent cycle management and efficient capital allocation

through

through

through

through

Slide 20

ab

Merrill LynchCEO Conference4 October 2007

Appendix

Slide 21

ab

Merrill LynchCEO Conference4 October 2007

OwnersProducts and Client Markets

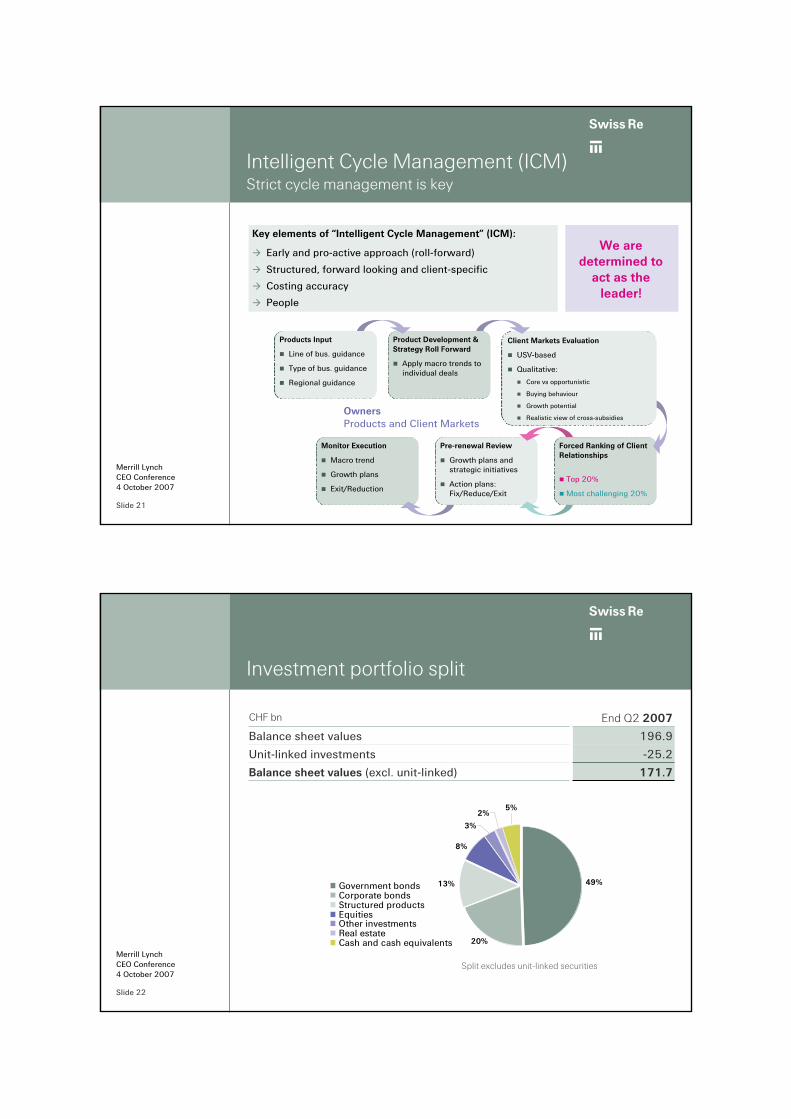

Intelligent Cycle Management (ICM)Strict cycle management is key

Monitor Execution

Macro trend

Growth plans

Exit/Reduction

Monitor Execution

Macro trend

Growth plans

Exit/Reduction

Key elements of “Intelligent Cycle Management” (ICM):

Early and pro-active approach (roll-forward)

Structured, forward looking and client-specific

Costing accuracy

People

We are determined to

act as the leader!

Pre-renewal Review

Growth plans and strategic initiatives

Action plans:Fix/Reduce/Exit

Pre-renewal Review

Growth plans and strategic initiatives

Action plans:Fix/Reduce/Exit

Forced Ranking of Client Relationships

Top 20%

Most challenging 20%

Forced Ranking of Client Relationships

Top 20%

Most challenging 20%

Client Markets Evaluation

USV-based

Qualitative:

Core vs opportunistic

Buying behaviour

Growth potential

Realistic view of cross-subsidies

Client Markets Evaluation

USV-based

Qualitative:

Core vs opportunistic

Buying behaviour

Growth potential

Realistic view of cross-subsidies

Product Development & Strategy Roll Forward

Apply macro trends to individual deals

Product Development & Strategy Roll Forward

Apply macro trends to individual deals

Products Input

Line of bus. guidance

Type of bus. guidance

Regional guidance

Products Input

Line of bus. guidance

Type of bus. guidance

Regional guidance

Slide 22

ab

Merrill LynchCEO Conference4 October 2007

Investment portfolio split

5%2%

8%

13% 49%

20%

3%

Government bondsCorporate bondsStructured productsEquitiesOther investmentsReal estateCash and cash equivalents

196.9Balance sheet values

-25.2Unit-linked investments

171.7Balance sheet values (excl. unit-linked)

End Q2 2007CHF bn

Split excludes unit-linked securities

Slide 23

ab

Merrill LynchCEO Conference4 October 2007

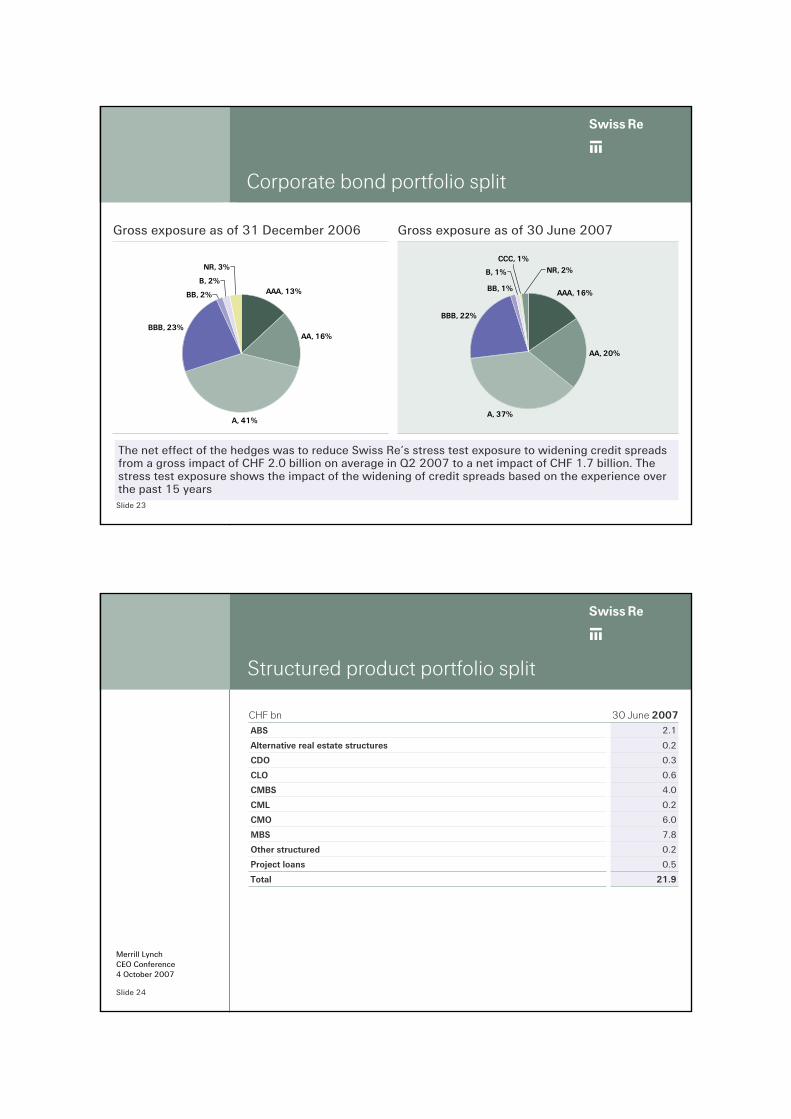

Gross exposure as of 30 June 2007

Corporate bond portfolio split

The net effect of the hedges was to reduce Swiss Re’s stress test exposure to widening credit spreads from a gross impact of CHF 2.0 billion on average in Q2 2007 to a net impact of CHF 1.7 billion. The stress test exposure shows the impact of the widening of credit spreads based on the experience over the past 15 years

Gross exposure as of 31 December 2006

AAA, 16%

AA, 20%

A, 37%

BBB, 22%

BB, 1%

B, 1%

CCC, 1%NR, 2%

AAA, 13%

AA, 16%

A, 41%

BBB, 23%

BB, 2%

B, 2%

NR, 3%

Slide 24

ab

Merrill LynchCEO Conference4 October 2007

Structured product portfolio split

0.6CLO

4.0CMBS

0.2CML

6.0CMO

7.8MBS

0.2Other structured

0.5Project loans

21.9

0.3

0.2

2.1

30 June 2007

Total

CDO

ABS

Alternative real estate structures

CHF bn

Slide 25

ab

Merrill LynchCEO Conference4 October 2007

Corporate calendar & contacts

Corporate calendar

3Q 2007 results (Conference Call) 06 November 2007

Investors’ day (London) 11 December 2007

Investor Relations contact

Hotline +41 43 285 4444

Susan Holliday +44 20 7933 3890Andreas Leu +41 43 285 5603Rolf Winter +41 43 285 9673Marc Habermacher +41 43 285 2637

E-mail [email protected]

Slide 26

ab

Merrill LynchCEO Conference4 October 2007

Cautionary note on forward-looking statements

Certain statements and illustrations contained herein are forward-looking. These statements and illustrations provide current expectations of future eventsbased on certain assumptions and include any statement that does not directly relate to a historical fact or current fact. Forward-looking statements typicallyare identified by words or phrases such as "anticipate", "assume", "believe", "continue", "estimate", "expect", "foresee", "intend", "may increase" and "mayfluctuate" and similar expressions or by future or conditional verbs such as "will", "should", "would" and "could". These forward-looking statements involveknown and unknown risks, uncertainties and other factors, which may cause Swiss Re's actual results, performance, achievements or prospects to bematerially different from any future results, performance, achievements or prospects expressed or implied by such statements. Such factors include, amongothers:

the impact of significant investments, acquisitions or dispositions, and any delays, unexpected costs or other issues experienced in connection with any such transactions, including, in the case ofacquisitions, issues arising in connection with integrating acquired operations; cyclicality of the reinsurance industry;changes in general economic conditions, particularly in our coremarkets;uncertainties in estimating reserves;the performance of financial markets;expected changes in our investment results as a result of the changed composition of our invested assets or changes in our investment policy;the frequency, severity and development of insured claim events;acts of terrorism and acts of war;

These factors are not exhaustive. We operate in a continually changing environment and new risks emerge continually. Readers are cautioned not to placeundue reliance on forward-looking statements. We undertake no obligation to publicly revise or update any forward-looking statements, whether as a resultof new information, future events or otherwise.

mortality and morbidity experience;policy renewal and lapse rates;changes in rating agency policies or practices;the lowering or withdrawal of one or more of the financial strength or credit ratings of one or more of our subsidiaries;changes in levels of interest rates;political risks in the countries in which we operate or in which we insure risks;extraordinary events affecting our clients, such as bankruptciesand liquidations;risks associated with implementing our business strategies;changes in currency exchange rates;changes in laws and regulations, including changes in accountingstandards and taxation requirements; andchanges in competitive pressures.

![[Merrill Lynch] Credit Derivatives Handbook](https://static.fdocuments.in/doc/165x107/55cf97e9550346d03394646c/merrill-lynch-credit-derivatives-handbook.jpg)