Mergers, Foreign Collaborations and Financial Innovations in a Global Economy International Tax...

38

Mergers, Foreign Collaborations and Financial Innovations in a Global Economy International Tax Conference on Cross Border Transactions Theme Presentation November 2005

-

Upload

cora-quinn -

Category

Documents

-

view

215 -

download

0

Transcript of Mergers, Foreign Collaborations and Financial Innovations in a Global Economy International Tax...

Mergers, Foreign Collaborations and Financial Innovations in a Global Economy

International Tax Conference on Cross Border Transactions

Theme Presentation

November 2005

2

Part I: India and the global economy

Part II: The trends

Part III: The Regulatory Framework

Part IV: The Tax Framework

Part V: Concluding Remarks

Agenda

3

Part I: India and the global economy

4

The Drivers of the Global Economy

GDP of BRIC countries, in 2003 US$bn, Source: Goldman Sachs BRIC report

Engines of growth US and Europe are expected to grow at 2-4%

Brazil, Russia, India and China are going to be the next big drivers of the global economy

In less than 40 years, the BRIC companies could be larger than the G6 in dollar terms

Among BRICs, India will be the fastest growing and will rank behind China and USA by 2033

The movement of capital Higher growth will lead to higher returns

Increased demand for capital will mean more fund flows in these countries

Accompanying shifts in spending would provide significant opportunities for global companies

Cumulative FDI InflowIndia has witnessed a strong inflow of FDI in the last 5 years

Source: Reserve Bank of India

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY

199

1

FY

199

2

FY

1993

FY

199

4

FY

1995

FY

199

6

FY

199

7

FY

199

8

FY

1999

FY

200

0

FY

200

1

FY

2002

FY

200

3

FY

2004

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000Cumulative FDI (USDmn) FDI (USDmn)

5

Why India ?

Sweeping reforms post liberalization

Cost competitiveness

Large scientific research capabilities

Reforms in key growth areas like infrastructure and power

Demographic changes

Indian companies are warming to the concept of shareholder value

6

India: Sweeping reforms post liberalization

Dismantling Protectionism

Average imports tariffs have reduced from 53% in 1988 to 18% In 2002

Strong Infrastructure

- Avoid direct government involvement- Allowing FDI- Sound regulatory framework (TRAI, CERC)- Introduction of competition

Disinvestment

- Major successes include VSNL, BALCO, CMC, Maruti Udyog, GAIL, ONGC, NTPC- Progress by state governments as well

Financial SectorReforms

- Sound regulatory base in banking, insurance and securities- Securitisation Act- Strengthening creditors’ rights, debt restructuring efforts

Fiscal Reforms- Removal of distortionary taxes- Migration to VAT regime- Simplicity and low cost of compliance

Globalisation- Reduced barriers to movement of goods and capital- Well-poised to exploit the Internet

The economic reforms process has been a key source of convergence among the

political parties, with every successive government taking the reforms forward

7

India: Cost competitiveness Increasing participation limits for FII and

FDI in different sectors

Lower custom tariffs leading to competition

and lower prices

More than half of cost diff between India &

China is on account of high tariffs and taxes

FTA with Thailand, CECA with SG, moving

towards pact with ASEAN

ChinaIndia Indirecttaxes

Interest costs

LabourProduc-tivity

Others**Import duties*

100 14-164-7 3-4 2-5 2-5

67-72

Price structure comparison between India and China: higher taxes main difference

Source: McKinsey Global Institute, CII

Source: Budget documents

10152025303540455055

FY

96

FY

97

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

%

Peak Import duty reduced to 15%

8

India: Large scientific research capabilities

More than 100 companies outsource R&D facilities from India

GE, Monsanto, Eli Lily, to name a few have largest facilities outside US, in India

Well established IT and ITES services market with CAGR of > 50% in last 5 yrs

IT exports touch US$ 22bn in 2004, form 20% of total exports (goods+services)

Skilled workforce: 0.36m engineers are certified every year

Source: GOI

0

200

400

600

800

1000

1200

1400

FY 98 FY 99 FY 00 FY 01 FY 02 FY 03

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4No of engineering colleges (LHS)

Annual enrollment, million (RHS)

Cisco announces US$1.1bn investment in R&D base

9

India: Key reforms in growth areas

Significant milestones in infrastructure developments over last 5 years

New Telecom Policy of 1999 led to rapid penetration of telephony

Government initiated NHDP at a cost of US$13.2bn (Phase 1&2) until 2008– Phase 3 to add another 10,000km by 2012

– Plans to extend further by another 26,000km

Electricity Act 2003 improves investment scenario in power sector– US$ 62bn of investments only in generation until 2012

– Additional investments in T&D and generation could push total to US$150bn

Development of new airports and upgradation of major airports

Private sector participation in ports

Increased investments in mining (oil & gas, coal, minerals)– NELP progressing well

– Private / Foreign participation in iron ore, coal into last lap of evolution

10

Source: India Census 2001

Age profile

India: Demographic changes have ….

Almost half the population is under 25 years Literacy levels among young significantly high Impact of mass media is potent Legacy savings nest of US$600bn+ Time to ditch the adage ‘Indians live poor but die rich’

% of population (2003) 2003 2002

15-19 10.6 84.3 76.1

20-24 10.0 76.9 70.2

25-34 17.1 67.9 57.4

35-44 12.8 58.6 46.9

45+ 18.3 45.2 36.9Source: NRS

Literacy levels

(%) Age group Popn (mn) (%)< 14 363.61 35.3%15-24 189.98 18.5%25-39 228.27 22.2%40-59 167.39 16.3%> 59 79.36 7.7%

11

… changed consumption patterns

Rising share of spend on ‘new services’ and lifestyle

Savings rate remains high @ 24%

Penetration of media, higher literacy and a nascent credit culture underpin the

transition

Rural

Other food22%

Vegetables6%

Milk & milk products

8%Cereals

18%

Fuel & light9%

Clothing & footw ear

8%

Other non-food29%

Urban

Other non-food42%

Clothing & footw ear

7%Fuel & light

9%

Cereals10%

Milk & milk products

8%

Vegetables4%

Other food20%

Source: NSS Report 2003, ICICI Securities Research Source: NSS Report 2003, ICICI Securities Research

Consumer expenditure pie

12

India: Unlocking shareholder value

Universal restructuring : Top 100…Midcap 200… down to SMEs

Relearned the mantra post liberalisation: ROCE > WACC !

Focus on de-gearing and free cash flows

Operating rates near peak – Cement, Automobiles, Steel, Mining, Electricity

Well positioned for modular, ‘high yield’ capex phase

Job creation - Manufacturing renaissance

– Textiles, Tourism, Pharma R&D, Ad industry joins IT/ITES in globalisation/ outsourcing

– PSUs : ‘employment boomers’ of 70s’ to retire over next 3-5 years

The ROCE transformation

Source: CMIE; Note: ex IT, Pharma & Banks (BSE 100)

-300

-200

-100

0

100

200

300

400

500

FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04

(Rs

bn)

0%

10%

20%

30%

40%

50%

60%

70%

80%FCF Net D/E (RHS) NWC/ Sales (RHS) Capex

Free cash flow mantra

Source: CMIE; Note: ex IT, Pharma & Banks (BSE 100)

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY03 FY04

RoCE WACC Rf

13

Part II: The trends

14

International Investors have reposed faith in the Indian Economy …

Source: RBI

Source: A T Kearney

FDI Confidence IndexIndia ranks 3rd in global FDI Confidence Index

As per a study conducted by AT Kearney, India ranks among the top 3 in global FDI Confidence Index

Growth opportunities in India have attracted global investors including VC funds and private equity investors

– PE Investments worth over

USD1.75bn in FY2005 (USD 1bn in

1HFY06) and exits of over

USD 545mn (USD 939mn in

1HFY06)

Cumulative FDI InflowIndia has witnessed a strong inflow of FDI in the last 5 years, USD mn

0 0.5 1 1.5 2 2.5

Japan

Italy

HK

Aus

France

Ger

UK

India

USA

China

0

2000

4000

6000

8000

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03 (R)

2003-04 (P)

2004-05 (P)

-5000

15000

35000

55000

75000

Cumulative FDI FDI

15

… which is reflected in bullish capital markets

Sources: SEBI, www.moneycontrol.com

Performance of Emerging Market Economies

India has delivered superior returns over the last year

Source: Bloomberg, Returns as on Oct 7, 2005

Country Y-o-Y Return PE RatioIndia 51.69% 16.38South Korea 50.38% 12.06Indonesia 15.76% 12.29Hong Kong 12.46% 13.82FTSE 11.91% 13.03Taiwan 6.83% 15.02Thailand 5.98% 10.89Dow Jones 2.36% 16.33Malaysia 1.30% 15.54

Total Equity Holdings of MFs and FIIs

Increased institutional buying in the stock markets

Source: AMFI, SEBI ; Mutual fund data for only pure equity funds

Strong rally in the market in spite of minor hiccups along the way

Superior returns attracting increased FII participation

– Nearly 800 registered FIIs with a

cumulative investment of over USD

39 bn Equity Mutual Funds have emerged

as strong players with AUM of about USD12 bn

-15000

-9000

-3000

3000

9000

15000

21000

Jan-05 Feb-05 Mar-05 Apr-05 May-05 Jun-05 Jul-05 Aug-05 Sep-05

4600

5100

5600

6100

6600

7100

7600

8100

8600FII Inflows MF Inflows Sensex

Stock Markets are Witnessing a Bull Run, USD mn

24.90%19.05%18.37%

75.10%

80.95%

81.63%

0

5

10

15

20

25

30

35

40

45

50

Aug-04 Feb-05 Aug-05USD bn

MF FII

16

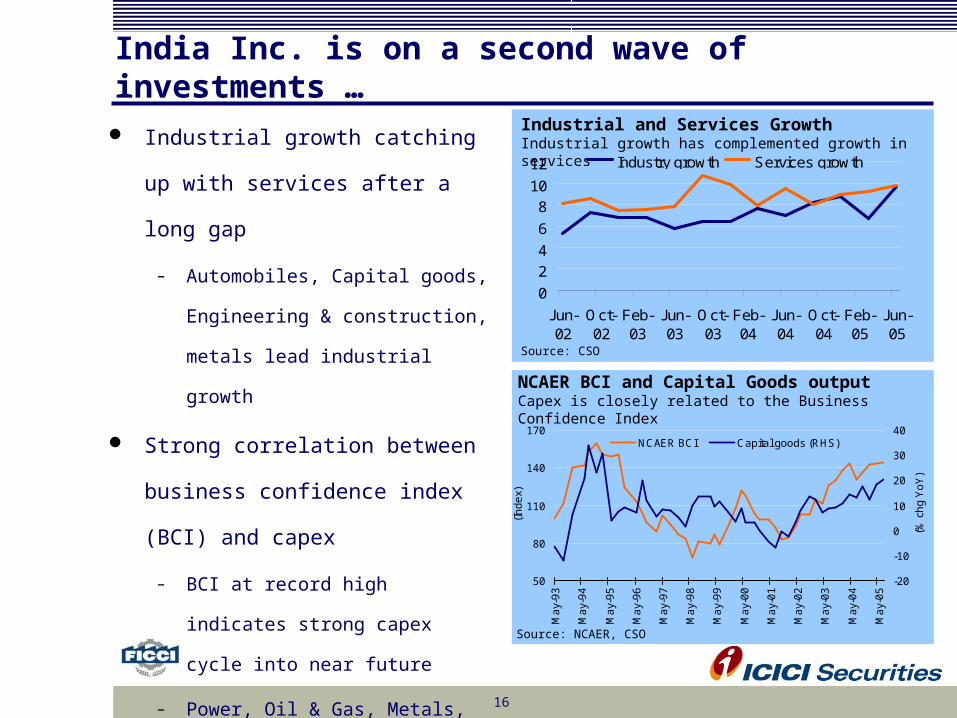

India Inc. is on a second wave of investments …

Source: CSO

Industrial and Services GrowthIndustrial growth has complemented growth in services

Source: NCAER, CSO

NCAER BCI and Capital Goods outputCapex is closely related to the Business Confidence Index

Industrial growth catching up with

services after a long gap

– Automobiles, Capital goods,

Engineering & construction, metals

lead industrial growth

Strong correlation between business

confidence index (BCI) and capex

– BCI at record high indicates strong

capex cycle into near future

– Power, Oil & Gas, Metals,

Automobiles, Textiles, Construction

driving investments

50

80

110

140

170

Ma

y-9

3

Ma

y-9

4

Ma

y-9

5

Ma

y-9

6

Ma

y-9

7

Ma

y-9

8

Ma

y-9

9

Ma

y-0

0

Ma

y-0

1

Ma

y-0

2

Ma

y-0

3

Ma

y-0

4

Ma

y-0

5

(In

de

x)

-20

-10

0

10

20

30

40

(% c

hg

Yo

Y)

NCAER BCI Capital goods (RHS)

0

2

4

6

8

10

12

Jun-02

Oct-02

Feb-03

Jun-03

Oct-03

Feb-04

Jun-04

Oct-04

Feb-05

Jun-05

Industry growth Services growth

17

…underpinned by domestic capital raising … Companies are tapping primary

equity markets for financing a

large number of expansion

projects

– A record USD 4.9 bn of equity

raised in FY 05 demonstrating

the depth of markets

– Virtuous cycle of larger IPOs

leading to increasing inflows

by QIBs; especially FIIs

– Primary markets remain active

with a total of USD 1.7 bn

equity raised by 35 companies

in first 6 months of 2005-06

– The primary market will

continue to remain active with

a strong pipeline of issues

expected to hit the market

Source: Prime Database * Data till September 30, 2005

568

4,087

4,915

1,690238232

0

1000

2000

3000

4000

5000

6000

FY 2001 FY 2002 FY 2003 FY 2004 FY 2005 FY 2006*

Issu

e A

mou

nt

0

10

20

30

40

50

No.

of

Issu

es

Issue Amount USD mn No: of issues

Primary Market IssuancesFirst half of 2006 has already witnessed issuances of over USD 1.6 bn with many more issues in the pipeline

18

… and overseas capital raising Overseas fund raising options

– GDR and FCCB gaining significant popularity

Break up of Equity Capital IssuancesSignificant international investor participation through DRs and FCCBs

Source: Prime Database (Excluding Sponsored ADR Issues) * Data till September 30, 2005

84.10%

55.33%

36.60%

3.00%

12.11%

22.77%

12.90%

32.56%40.63%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY 04 FY 05 FY 06*

IPO/FPO DR FCCB

19

Case Study 1: Reliance Industries Multi-currency Term Loan

US$ 350 mn multi-currency

loan

– Facility consists of a USD,

Euro and JPY tranche

– Syndicated with a consortium

of 34 banks across 13

countries

– Finest pricing among offshore

medium term loans

June 2005

Reliance Industries Limited

Syndication of term loan

USD 350,000,000

June 2005

Reliance Industries Limited

Syndication of term loan

USD 350,000,000

20

Case Study 2: Motherson Sumi’s FCCB

Asia’s first Euro denominated FCCB (deal size

EUR 50 mn)

– Conversion Premium of 50%

– 5 yr, Zero Coupon, Bullet deal with issue at par

– Redemption Premium of 126.77% ; YTM 4.8%

– Call Option after 3 years with 130% hurdle and

no greenshoe

Ideal from the Company’s standpoint

– Currency provides a better match for its cash

flows with nearly two thirds of production

exported

July 2005

Motherson Sumi

FCCB Offering

EUR 50,300,000

July 2005

Motherson Sumi

FCCB Offering

EUR 50,300,000

21

Growth Through Consolidation and Inorganic Expansion: Predatory India Inc Large number of companies in India are looking at achieving growth through

acquisition of companies in the US, Europe and Asia

– Key aspect of acquisition of the customers of the target

– Creation of value through usage of the manufacturing set up at a lower cost Indian

location

– Acquisition of a competency / technology

The potential Indian acquirers are evaluating the available opportunities on the

following criteria

– Reasonably large customer base including blue chip customers

– Established technology

– Reasonable size

– Flexibility towards shifting of operations to India, if required, and a willing management

22

Indian Corporates are Seeking International Acquisition Opportunities to Reach Global Size

Target Name Acquirer Name DateAnnounced Total

Value (USD mn)Industry

Television-tube Business Videocon International Ltd Jun 05 291 Manufacturing

Natsteel Asia Pte Ltd Tata Steel Ltd Aug o4 284 Steel

Flag Telecom Group Ltd Reliance Gateway Net Private Oct 03 191 Telecom

DSI Financial Solutions Pte HCL Technologies Ltd Nov 04 157 Software

Tyco Global Network Videsh Sanchar Nigam Ltd Nov 04 130 Telecom

Tata Daewoo Commercial

Vehicle Co. LtdTata Motors Ltd Nov 03 118 Auto

Trevira Gmbh Reliance Industries Limited Jun 04 97 Textile

23

International Companies are also Seeking a Foothold in the Growing Indian Market

Target Name Acquirer Name DateAnnounced Total Value (USD mn)

Industry

BPL Mobile Cellular Ltd Hutchison Telecommunications Nov 05 1,152 Telecom

I-flex Solutions Ltd Oracle Corp Aug 05 779 Software

Indian Phone Ventures Hutchison Telecommunications Feb 05 592 Telecom

ACC Holcim Jan 05 583 Cement

GECIS Global US Based Private Equity Firms Non 04 500 BPO

Aircel Televentures Ltd Afk Sistema Feb 05 450 Telecom

Flextronics Software Sys Ltd Flextronics Intl Ltd Jun 04 399 Software

Digital Globalsoft Ltd Hewlett-Packard Co Dec 03 304 Applications Software

24

Emerging Trends- M&A Cross-border M&A to continue

– In-bound M&A in sectors like IT/BPO, telecom and manufacturing

– Outbound M&A in pharmaceuticals, auto & auto ancillary, textiles, oil & gas

Buyouts driven by private equity funds expected to gain ground

Rs mn 2003 2004 2005

Deals Value Deals Value Deals Value

Inbound 24 581.7 12 116.3 21 455.6

Outbound 23 1338.4 21 668.1 30 1081.4

Total 47 1920.1 33 784.4 51 1537

Source: Bloomberg; includes only completed transactions; average size and range calculated on deal values that arePublicly announced

Predominantly cash transactions

– Stock is yet to see an emergence as a currency in cross border transactions

25

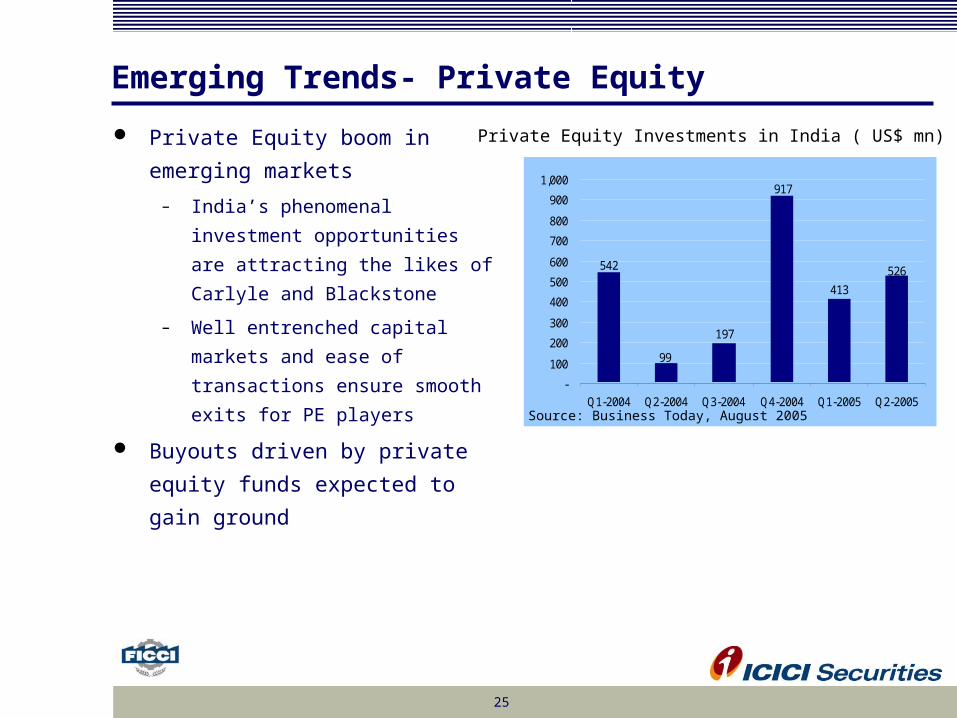

Emerging Trends- Private Equity

Private Equity boom in emerging

markets

– India’s phenomenal investment

opportunities are attracting the likes

of Carlyle and Blackstone

– Well entrenched capital markets

and ease of transactions ensure

smooth exits for PE players

Buyouts driven by private equity

funds expected to gain ground

526

413

917

197

99

542

-

100

200

300

400

500

600

700

800

900

1,000

Q1-2004 Q2-2004 Q3-2004 Q4-2004 Q1-2005 Q2-2005

Private Equity Investments in India ( US$ mn)

Source: Business Today, August 2005

26

Case Study 1: Tata Tea’s acquisition of Tetley

First Leveraged Buy-out ( Rs. 2,135 cr)

– Instant access to Tetley’s worldwide

operations, combined turnover at Rs 3,000 cr

Financial Innovation at its best

– SPV created to ring fence risk with equity

contributed by Tata Tea and Tata Tea Inc

– Debt of 235 mn pounds raised in the form of

long term debt and revolver; charge against

Tetley’s brand and assets

– Tata Tea’s exposure only to the extent of

equity component of 70 mn pounds

March 2000

Tata Tea Limited

Acquisition of 100% equity stake in Tetley Tea (UK)

INR 21,350,000,000

March 2000

Tata Tea Limited

Acquisition of 100% equity stake in Tetley Tea (UK)

INR 21,350,000,000

27

Case Study 2: Amtek Group’s Global StepsPhase I: Setting up a strong efficient base

Amtek Group is a leading player in auto ancillary

business manufacturing connecting rods,

crankshafts, gear shifter forks, etc

Phase II: Acquires Domain Expertise in a niche

Sets up a joint venture with Benda Kogyo,

Japan for manufacture of flywheel ring gears

and flexplates

Phase III: Acquires Smith Jones, Inc

Acquires Smith Jones, Inc., a leading

manufacturer of flywheel ring gears

– Present in the OEM and replacement market

– Market share of around 40% in the USA

Acquisition catapults Amtek Auto into number

three producer of ring gears in the world and

provides access to key OEM customers

December 2002

Amtek Auto Limited

Acquisition of 100% equity stake in Smith Jones, Inc. (USA)

Rs358,010,000

December 2002

Amtek Auto Limited

Acquisition of 100% equity stake in Smith Jones, Inc. (USA)

Rs358,010,000

28

Case Study 3: Vodafone enters India

Largest investment in the Indian telecom

sector by overseas player (Deal Size: Rs

6700 cr)

– India is the third-largest mobile with 65 mn

subscribers; growth of 54% Y/Y

– Bharti is the fastest-growing mobile market in

Asia with 14 mn subscribers

10% of Bharti at Rs 351/sh with 4.39%

indirectly from Bharti Enterprises and 5.61%

from Warburg Pincus

– Exit for Warburg Pincus who originally

invested US$ 300 mn for 18 % in 1999-2001

September 2005

Bharti Televentures

Sale of 10% equity stake to Vodafone Plc.

Rs 21,350,000,000

September 2005

Bharti Televentures

Sale of 10% equity stake to Vodafone Plc.

Rs 21,350,000,000

29

Part IV: The Regulatory framework

30

Investment in India – Alternatives

Portfolio Investment by institutional investors through Securities and Exchange Board of

India Regulations

– Requires registration with SEBI

Foreign Direct Investment is freely allowed in all sectors including the services sector,

except a few sectors where the existing and notified sectoral policy does not permit FDI

beyond a ceiling

FDI for virtually all items allowed through the automatic route under powers delegated to the

Reserve Bank of India (RBI) and for the remaining items through Government approval

– Government approvals are accorded on the recommendation of the Foreign Investment Promotion

Board (FIPB)

Approval Route – Through FIPB

Automatic Route – Through RBI

Foreign Direct Investment

Foreign Direct Investment

Portfolio InvestmentInvestment In India by

Foreigners

31

Investment in Existing Companies

If the investment is made in a listed entity, the Acquirer needs to comply with

various provisions of Securities and Exchange Board of India (Substantial

Acquisition of Shares and Takeovers) Regulations, 1997

Listed entity

Unlisted entity

Fair valuation of shares to be performed by a chartered accountant as per the

Guidelines issued by the Controller of Capital Issues

Listed entity

Unlisted entity

Investment in Existing Company

32

Easing of Government Approval Process

FDI limits being eased up

– 100% in all infrastructure projects, drugs and pharmaceuticals, hotels and tourism, etc

– Currently at 74% in banking, telecom services, exploration and mining

– 49% in civil aviation

– 26% in insurance

Foreign investment approval through FIPB route do not require any further clearance from RBI for the purpose of receiving inward remittance and issue of shares to foreign investors

– RBI Notification:

Notification by the company to the RBI within 30 days of receipt of inward remittances

Filing the required documentation within 30 days after issue of shares

33

Part V: The Tax framework

34

Tax Regime – Taxing the Corporate

Dividend Distribution Tax – 14.025%– DDT : 12.5% plus surcharge: 10% plus

cess: 2%

A minimum alternate tax under Section 115 JB(7.5% plus 2.5% plus 2.0%) is also imposed

Fringe Benefit Tax – 30.6% FBT: 30% plus cess: 2% on certain

percentages of expenditure

Foreign Company – 41.82%– Income tax: 40% plus surcharge: 2.5%

plus cess: 2%

The Indian

Corporate

Domestic Company – 33.66%

Income tax: 30% plus surcharge: 10%

plus cess: 2%

35

Tax Regime – Issues

Carry Forward of Losses Can be carried forward and set off

against future profits up to 8 years No carry backward of business

losses

Securities Transaction tax (STT)

STT levied at 0.02%

Abolition of long-term capital gains

Need to cover

– Share buy-back

– Shares transferred under open offer

– Sale/transfer of shares under SEBI

approved routes

Special Tax Treatment 100% Tax exemption for Export

Oriented Units (EOUs)

Facilitation of R&D

Weighted deduction benefit for

biotechnology, drugs and

pharmaceuticals

Tax advantage of 7-8% as against

35% in developed countries

36

Tax Regime: Taxing the Foreign Corporate

Non-residents Royalties, Fees from technical

services, Income from GDRs, dividends, interest, etc. taxed at variable rates

Applicability of MAT?

Foreign Dividends and Capital gains Dividends from foreign subsidiaries

taxed at 35% Profits from foreign subsidiaries

taxed at 20%

Controlled Foreign Corporations

(CFC)

Foreign Income in a country with a

tax rate lower than tax rate

applicable to resident shareholders

is classified CFC

CFC is taxed at the rate applicable to

resident shareholders

Cross Border M&A Transfer of shares in Indian

company to a foreign entity (share-swap) not tax-neutral

Embargo on carry forward of losses under certain conditions

Asset purchase transactions are not tax neutral

37

Part VI: Concluding Remarks

38

Recap

The borders in a global economy are becoming seamless

– India occupies a favorable place for foreign investment

– Indian corporates are looking at opportunities abroad

– Financial innovation has spawned a host of products

The Regulatory and the Tax framework

– Foreign Investment in the form of FII/FDI

– FII Investment requires SEBI registration

– FDI Investment through (a) approval and (b) automatic route

– Indian and Foreign corporates taxed differently

– Tax structure needs to be streamlined to facilitate cross border transactions