Melrose Industries PLC · A proposed final dividend of 3.4 pence per share (2018: 3.05 pence) is...

33

Strictly private and confidential Buy Improve Sell Melrose Industries PLC Year ended 31 December 2019 5 March 2020 Full Year Results GKN ePowertrain Nortek StatePoint ®

Transcript of Melrose Industries PLC · A proposed final dividend of 3.4 pence per share (2018: 3.05 pence) is...

BuyImproveSell

Strictly private and confidential

BuyImproveSell

Melrose Industries PLC

Year ended 31 December 20195 March 2020

Full Year Results

GKN ePowertrain Nortek StatePoint®

BuyImproveSell

Contents

1 Highlights

2 The results

3 Businesses – investment & improvement

4 Appendices

1The revenue and profit numbers included in this presentation are shown in round millions. Margin calculations are calculated using unrounded numbers

Highlights

2

BuyImproveSell

BuyImproveSell

Highlights

3

The results for 2019 were comfortably ahead of the Board’s expectations for both profit and cash generation

Adjusted1 diluted earnings per share (“EPS”) were 14.3 pence, up 13% on last year (statutory EPS: 0.9 pence) and adjusted free cashflow3 was £591 million, up 72%4 on an annualised like-for-like basis

Group net debt and leverage have both been improved and were reduced to £3.28 billion and 2.25x respectively

Net trade working capital in the Group was reduced by £95 million (5%) in the year, with adjusted profit conversion to cash1 of 104%.More progress in net trade working capital to come, in line with achieving the previously announced £400 million target within theMelrose ownership period

Loss-making contracts have been improved materially with the losses from 2018 reducing by 11% in 2019. In addition, c.25% of theremaining provision has been released (as previously stated this release is not included in adjusted1 operating profit) due toimprovements implemented by management this year. These improvements impact future trading in GKN positively

The GKN UK defined benefit pension schemes are significantly better funded, aided by over £240 million5 of cash contributions fromthe Group so far during Melrose ownership, fully in line with the plan agreed with the Trustees. Along with better investment returns, theremaining contributions required to make these schemes well funded has reduced from up to £1 billion at acquisition to c.£500 million

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Results for 2018 include GKN for 8 months only and have been restated for discontinued operations3. Adjusted free cash flow excludes the special one-off pension contributions and restructuring spend4. Calculated compared to 2018 annualised adjusted free cash flow, excluding the previously announced £150 million cash outflow from unwinding creditor stretch

in 2018. 2018 annualised adjusted free cash flow includes 12 months of GKN ownership5. Including the contribution paid on 6 January 2020

Continuing operations2

Adjusted1 results Statutory results

2019£m

2018£m

2019£m

2018£m

Revenue 11,592 8,645 10,967 8,152

Operating profit/(loss) 1,102 813 318 (387)

Profit/(loss) before tax 889 672 106 (542)

Diluted earnings per share 14.3p 12.7p 0.9p (11.8)p

BuyImproveSell 4

Highlights

A proposed final dividend of 3.4 pence per share (2018: 3.05 pence) is 11% up on last year, giving a full year dividend of 5.1 pence pershare (2018: 4.6 pence) up 11%

During 2019, a record total level of investment has been made in new product development; technology; environmental, social &governance (ESG); and capital and restructuring projects - all designed to improve the quality of the businesses and their futureperformance

The effects of the COVID-19 outbreak are not fully known at present. Approximately 10% of Group sales are manufactured in China, ofwhich 5% is sold in China, with GKN Automotive having the largest exposure through its 50% joint venture – all except one site areoperational after the new year break. Whilst there will clearly be some impact, the opportunities to improve GKN in 2020 and beyondposition Melrose well to deliver positive returns for shareholders in the future

The Automotive and Aerospace businesses are now totally separate from a head office, legal, tax and pensions perspective. Melrosewill be holding an Investor Day for Automotive in New York in October this year to update the markets on its future strategy

Melrose has appointed advisers to explore the strategic options for Nortek Air Management, although clearly recent events may havesome bearing on timing. In the event of a significant disposal, a further reduction to net debt would be made along with an exceptionalrepayment to shareholders and a further contribution to the GKN UK defined benefit pension schemes

Justin Dowley, Chairman of Melrose Industries PLC, today said:

“We are delighted with the Melrose performance in 2019 and the substantial value that is being unlocked. Notwithstanding anyimplications of the COVID-19 outbreak, the bedrock has now been built for the GKN businesses to attain results which were not previouslyachievable, and, in addition, the shareholder value built up in our longer held assets is closer to being realised. This shows, once more,that the Melrose model thrives by investing properly in businesses and giving management the entrepreneurial freedom to succeed. Thisis just the start of what is possible for GKN.”

BuyImproveSell

The results

5

BuyImproveSell

BuyImproveSell

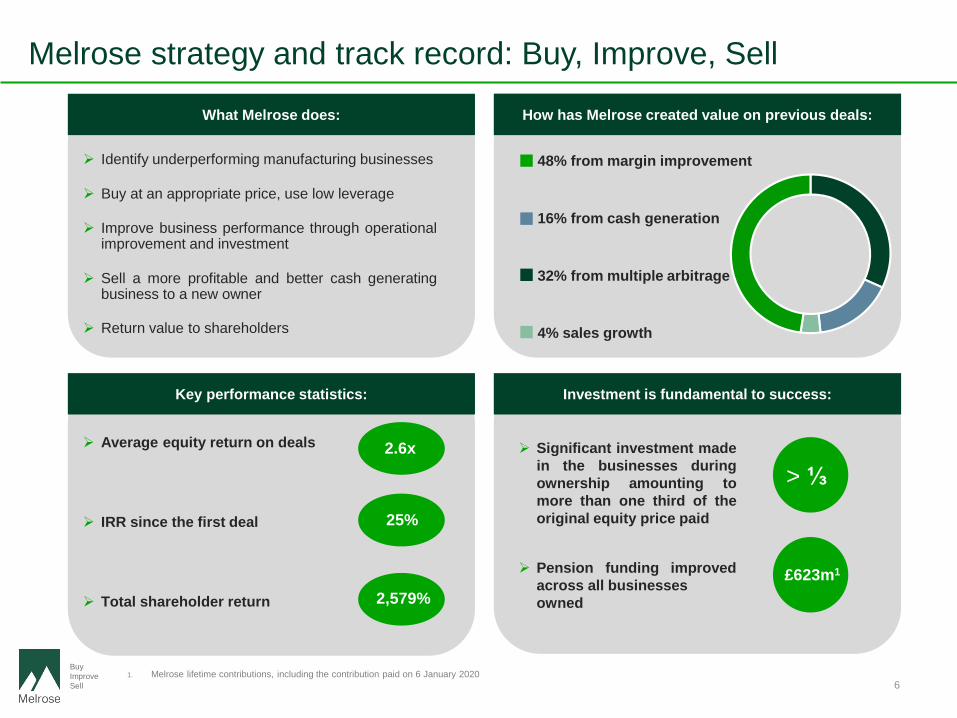

Melrose strategy and track record: Buy, Improve, Sell

6

Identify underperforming manufacturing businesses

Buy at an appropriate price, use low leverage

Improve business performance through operationalimprovement and investment

Sell a more profitable and better cash generatingbusiness to a new owner

Return value to shareholders

What Melrose does:

Average equity return on deals

IRR since the first deal

Total shareholder return

2.6x

25%

2,579%

Key performance statistics:

48% from margin improvement

16% from cash generation

32% from multiple arbitrage

4% sales growth

How has Melrose created value on previous deals:

Significant investment madein the businesses duringownership amounting tomore than one third of theoriginal equity price paid

Pension funding improvedacross all businessesowned

Investment is fundamental to success:

£623m1

1. Melrose lifetime contributions, including the contribution paid on 6 January 2020

> ⅓

BuyImproveSell

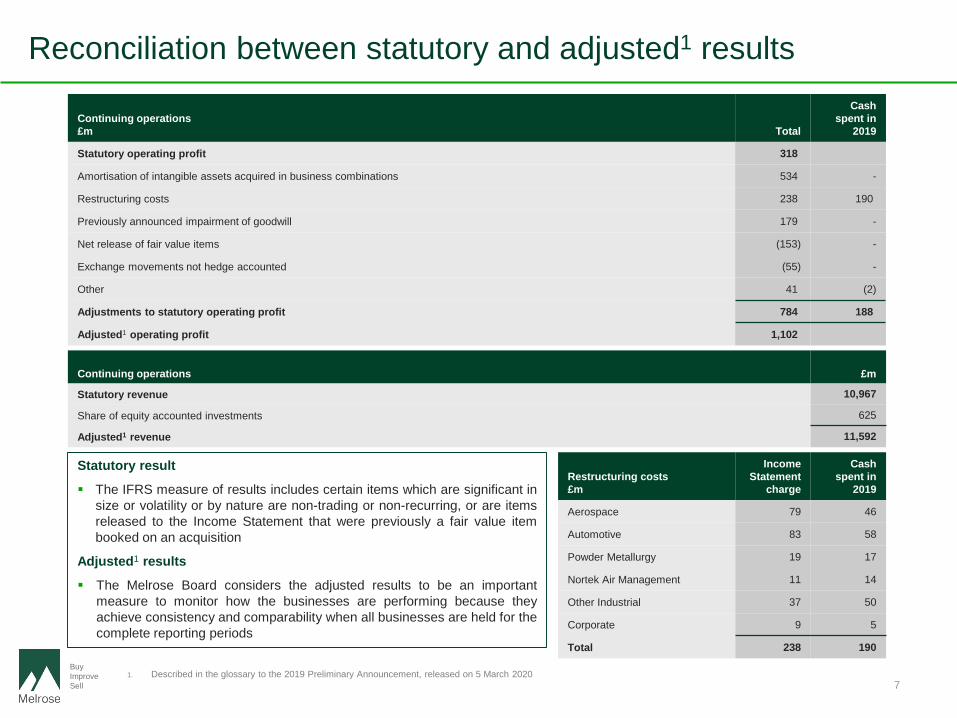

Reconciliation between statutory and adjusted1 results

7

Statutory result

The IFRS measure of results includes certain items which are significant insize or volatility or by nature are non-trading or non-recurring, or are itemsreleased to the Income Statement that were previously a fair value itembooked on an acquisition

Adjusted1 results

The Melrose Board considers the adjusted results to be an importantmeasure to monitor how the businesses are performing because theyachieve consistency and comparability when all businesses are held for thecomplete reporting periods

Restructuring costs£m

Income Statement

charge

Cash spent in

2019

Aerospace 79 46

Automotive 83 58

Powder Metallurgy 19 17

Nortek Air Management 11 14

Other Industrial 37 50

Corporate 9 5

Total 238 190

Continuing operations £m

Statutory revenue 10,967

Share of equity accounted investments 625

Adjusted1 revenue 11,592

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 2020

Continuing operations£m Total

Cash spent in

2019

Statutory operating profit 318

Amortisation of intangible assets acquired in business combinations 534 -

Restructuring costs 238 190

Previously announced impairment of goodwill 179 -

Net release of fair value items (153) -

Exchange movements not hedge accounted (55) -

Other 41 (2)

Adjustments to statutory operating profit 784 188

Adjusted1 operating profit 1,102

BuyImproveSell

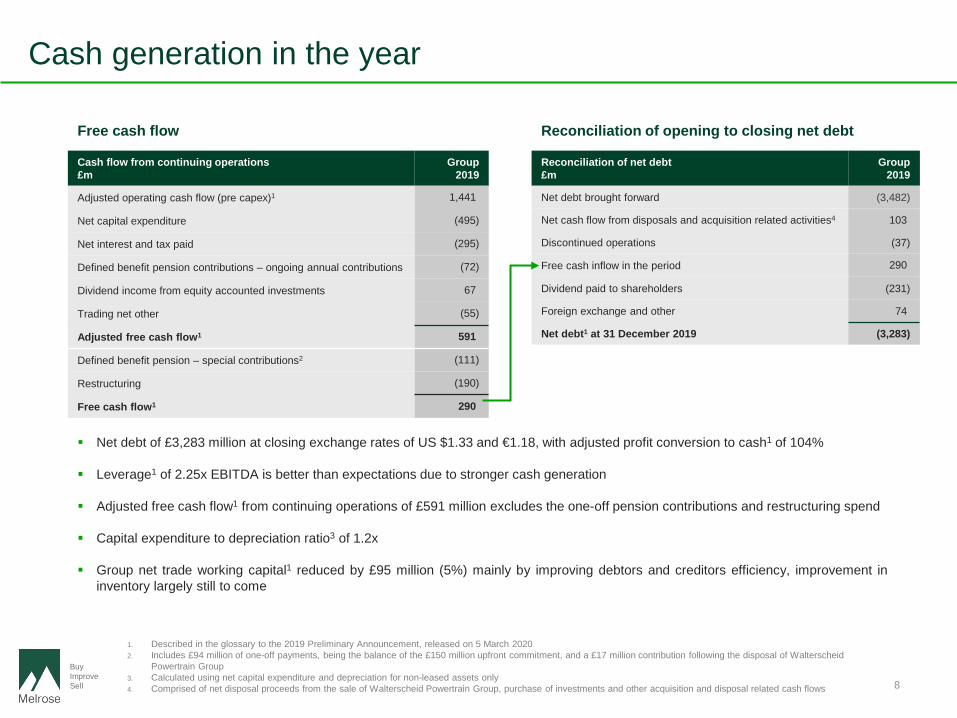

Cash generation in the year

8

Cash flow from continuing operations£m

Group2019

Adjusted operating cash flow (pre capex)1 1,441

Net capital expenditure (495)

Net interest and tax paid (295)

Defined benefit pension contributions – ongoing annual contributions (72)

Dividend income from equity accounted investments 67

Trading net other (55)

Adjusted free cash flow1 591

Defined benefit pension – special contributions2 (111)

Restructuring (190)

Free cash flow1 290

Reconciliation of net debt£m

Group2019

Net debt brought forward (3,482)

Net cash flow from disposals and acquisition related activities4 103

Discontinued operations (37)

Free cash inflow in the period 290

Dividend paid to shareholders (231)

Foreign exchange and other 74

Net debt1 at 31 December 2019 (3,283)

Free cash flow Reconciliation of opening to closing net debt

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Includes £94 million of one-off payments, being the balance of the £150 million upfront commitment, and a £17 million contribution following the disposal of Walterscheid

Powertrain Group3. Calculated using net capital expenditure and depreciation for non-leased assets only4. Comprised of net disposal proceeds from the sale of Walterscheid Powertrain Group, purchase of investments and other acquisition and disposal related cash flows

Net debt of £3,283 million at closing exchange rates of US $1.33 and €1.18, with adjusted profit conversion to cash1 of 104%

Leverage1 of 2.25x EBITDA is better than expectations due to stronger cash generation

Adjusted free cash flow1 from continuing operations of £591 million excludes the one-off pension contributions and restructuring spend

Capital expenditure to depreciation ratio3 of 1.2x

Group net trade working capital1 reduced by £95 million (5%) mainly by improving debtors and creditors efficiency, improvement ininventory largely still to come

BuyImproveSell

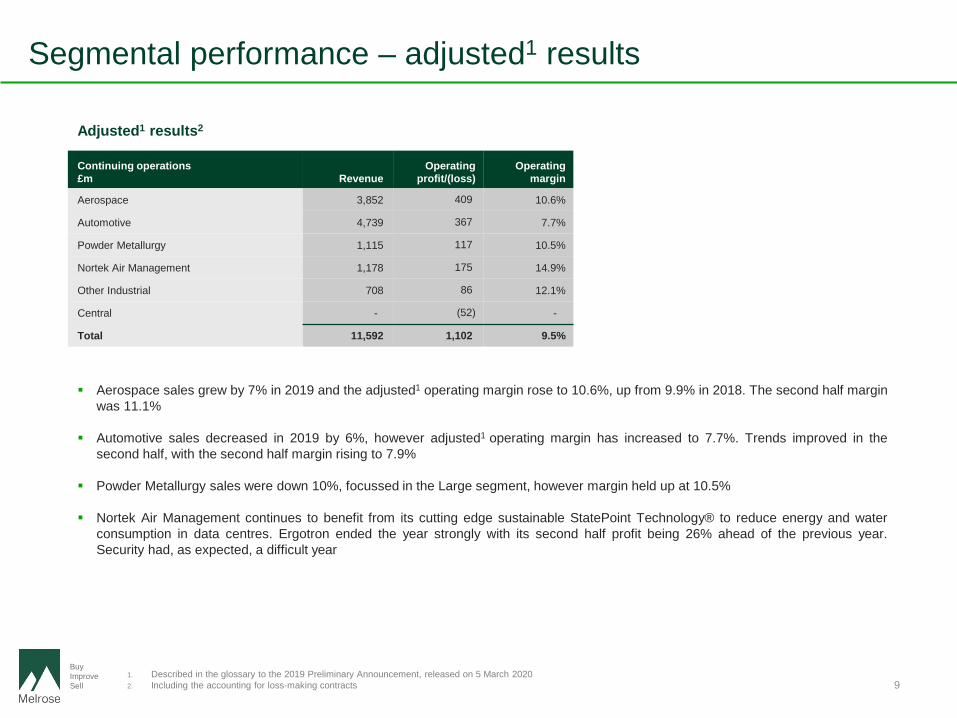

Segmental performance – adjusted1 results

9

Continuing operations£m Revenue

Operating profit/(loss)

Operating margin

Aerospace 3,852 409 10.6%

Automotive 4,739 367 7.7%

Powder Metallurgy 1,115 117 10.5%

Nortek Air Management 1,178 175 14.9%

Other Industrial 708 86 12.1%

Central - (52) -

Total 11,592 1,102 9.5%

Adjusted1 results2

Aerospace sales grew by 7% in 2019 and the adjusted1 operating margin rose to 10.6%, up from 9.9% in 2018. The second half marginwas 11.1%

Automotive sales decreased in 2019 by 6%, however adjusted1 operating margin has increased to 7.7%. Trends improved in thesecond half, with the second half margin rising to 7.9%

Powder Metallurgy sales were down 10%, focussed in the Large segment, however margin held up at 10.5%

Nortek Air Management continues to benefit from its cutting edge sustainable StatePoint Technology® to reduce energy and waterconsumption in data centres. Ergotron ended the year strongly with its second half profit being 26% ahead of the previous year.Security had, as expected, a difficult year

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Including the accounting for loss-making contracts

BuyImproveSell

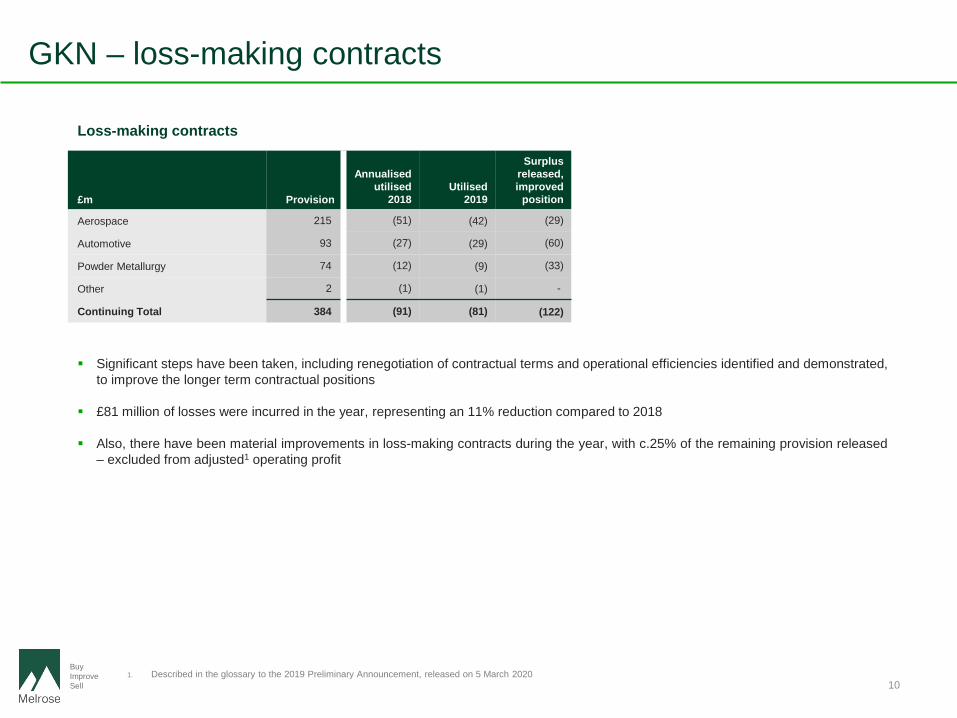

GKN – loss-making contracts

10

£m Provision

Aerospace 215

Automotive 93

Powder Metallurgy 74

Other 2

Continuing Total 384

Loss-making contracts

Significant steps have been taken, including renegotiation of contractual terms and operational efficiencies identified and demonstrated,to improve the longer term contractual positions

£81 million of losses were incurred in the year, representing an 11% reduction compared to 2018

Also, there have been material improvements in loss-making contracts during the year, with c.25% of the remaining provision released– excluded from adjusted1 operating profit

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 2020

Annualised utilised

2018Utilised

2019

Surplus released, improved

position

(51) (42) (29)

(27) (29) (60)

(12) (9) (33)

(1) (1) -

(91) (81) (122)

BuyImproveSell

Pensions and tax

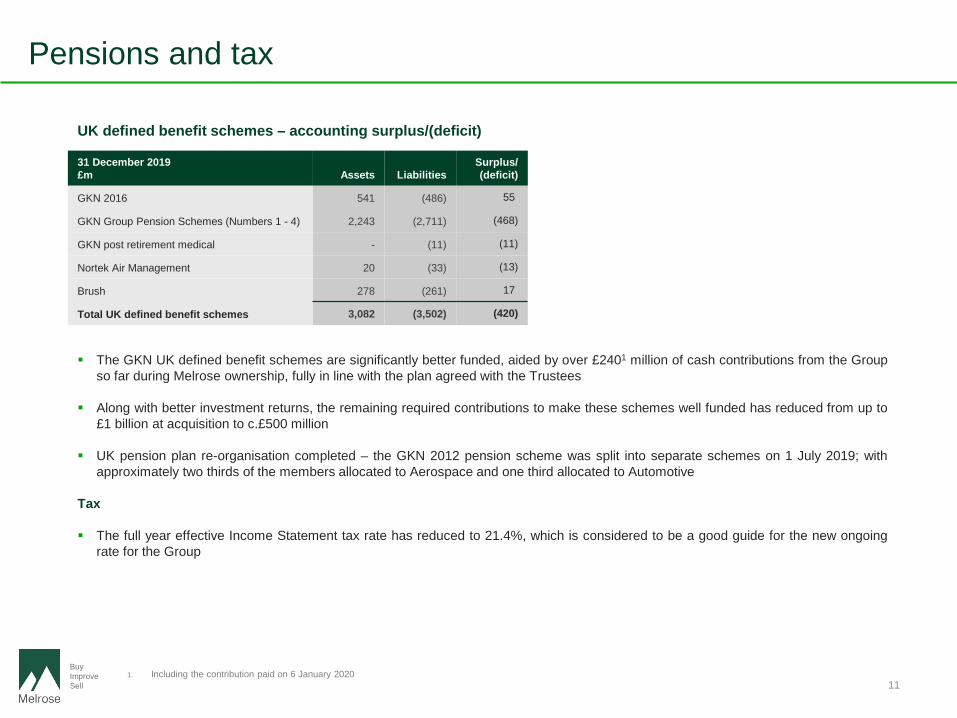

11

The GKN UK defined benefit schemes are significantly better funded, aided by over £2401 million of cash contributions from the Groupso far during Melrose ownership, fully in line with the plan agreed with the Trustees

Along with better investment returns, the remaining required contributions to make these schemes well funded has reduced from up to£1 billion at acquisition to c.£500 million

UK pension plan re-organisation completed – the GKN 2012 pension scheme was split into separate schemes on 1 July 2019; withapproximately two thirds of the members allocated to Aerospace and one third allocated to Automotive

Tax

The full year effective Income Statement tax rate has reduced to 21.4%, which is considered to be a good guide for the new ongoingrate for the Group

UK defined benefit schemes – accounting surplus/(deficit)

31 December 2019£m Assets Liabilities

Surplus/ (deficit)

GKN 2016 541 (486) 55

GKN Group Pension Schemes (Numbers 1 - 4) 2,243 (2,711) (468)

GKN post retirement medical - (11) (11)

Nortek Air Management 20 (33) (13)

Brush 278 (261) 17

Total UK defined benefit schemes 3,082 (3,502) (420)

1. Including the contribution paid on 6 January 2020

BuyImproveSell

Businesses – investment & improvement

12

BuyImproveSell

BuyImproveSell

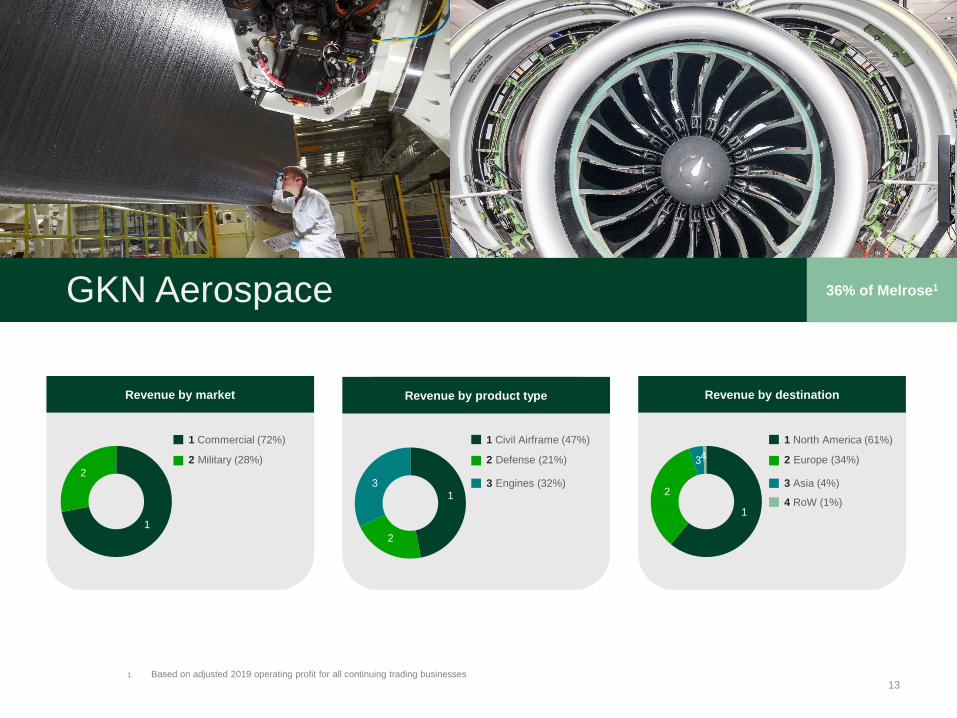

GKN Aerospace

13

36% of Melrose1

1. Based on adjusted 2019 operating profit for all continuing trading businesses

1

2

Revenue by market

1 Commercial (72%)

2 Military (28%)

4 RoW (1%)

1

2

3

Revenue by destination

1 North America (61%)

2 Europe (34%)

3 Asia (4%)

4

1

2

3

Revenue by product type

1 Civil Airframe (47%)

3 Engines (32%)

2 Defense (21%)

4 RoW (1%)

BuyImproveSell 14

Aerospace – highlights

Highlights

Adjusted1 operating profit up 25%, adjusted1 operating margin up 1.4 percentage points

Second half performance stronger than the first half, adjusted1 operating margin reaching 11% in the second half

New “One Aerospace” structure being implemented to better serve customers and generate further efficiencies

Major new operational improvement programme commenced to drive sustainable gains in quality, delivery and cost

North American Aerostructures business generated a small profit; only two years ago this part of Aerospace made a £43 million loss

Record year of investment in technology, construction underway on the new Global Technology Centre in Bristol, UK, which isexpected to open in 2020

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Growth is calculated at constant currency against 2018 annualised results, excluding the impact of loss-making contracts and IFRS 16 in both periods for consistency

£m2019

Adjusted1 results Growth2

H1 2019 Adjusted1

results

H2 2019 Adjusted1

results

H2 2019 Year on Year

Growth2

Revenue 3,852 7% 1,904 1,948 7%

EBITDA 579 17% 276 303 16%

EBITDA margin % 15.0% +1.2 ppts 14.5% 15.6% +1.2 ppts

Operating profit 409 25% 192 217 23%

Operating margin % 10.6% +1.4 ppts 10.1% 11.1% +1.3 ppts

BuyImproveSell 15

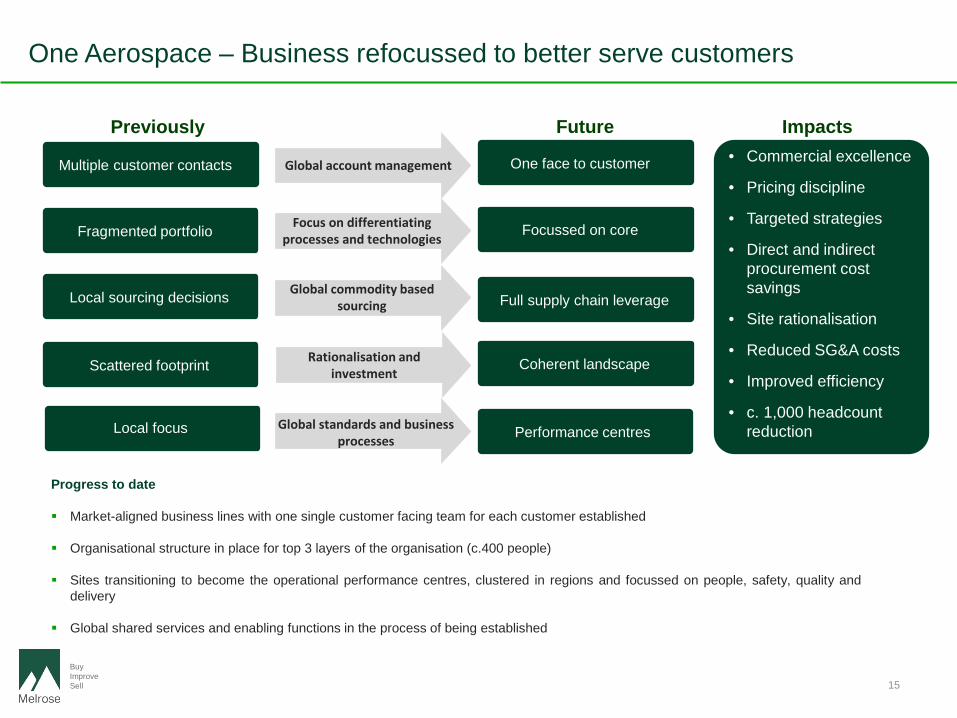

One Aerospace – Business refocussed to better serve customers

Previously Future Impacts

Multiple customer contacts

Fragmented portfolio

Local sourcing decisions

Scattered footprint

Local focus

One face to customer

Focussed on core

Full supply chain leverage

Coherent landscape

Performance centres

Global account management

Focus on differentiating processes and technologies

Rationalisation and investment

Global commodity based sourcing

Global standards and business processes

• Commercial excellence

• Pricing discipline

• Targeted strategies

• Direct and indirect procurement cost savings

• Site rationalisation

• Reduced SG&A costs

• Improved efficiency

• c. 1,000 headcount reduction

Progress to date

Market-aligned business lines with one single customer facing team for each customer established

Organisational structure in place for top 3 layers of the organisation (c.400 people)

Sites transitioning to become the operational performance centres, clustered in regions and focussed on people, safety, quality anddelivery

Global shared services and enabling functions in the process of being established

BuyImproveSell 16

Aerospace – markets, investment, technology and environment

Markets

Civil aerospace has a healthy backlog; long-term civil aerospace market remains in line with acquisition assumptions

Boeing 737 MAX position being monitored closely with required mitigating actions being taken – GKN Aerospace has an approximateshipset value of up to £400k for each aircraft

Military market is strong and could increase the balance of military versus commercial sales in the future

Investment and restructuring

Creation of “One Aerospace”; major new operational excellence programme commenced, focussed on serving customers better

Delivery, quality and customer relationships all continue to improve, working capital improvement plans being implemented

Good progress being made on resolving loss-making contracts – financial benefits expected to follow

Closure of two loss-making sites underway, full exit expected during 2020

Significant capital investment injected into previously underinvested parts of the business and in to new growth areas

Technology and ESG

Record investment in technology – focussed on improving efficiency, weight and emissions of aircraft:

– Construction of the new Global Technology Centre in Bristol, UK is underway, expected to open in 2020– World leading additive manufacturing pilot production cell at Oak Ridge National Laboratory, US– Technology centre in the Netherlands to focus on thermoplastic components– Manufactured first components for the Wing of Tomorrow programme

– Additive technologies being developed to significantly reduce waste material from production processes

Substantial research and development project into zero-emission hydrogen power systems planned for 2020 – decarbonisationopportunity leading to cleaner air

BuyImproveSell

GKN Automotive

17

32% of Melrose1

1. Based on adjusted 2019 operating profit for all continuing trading businesses

Revenue by product type

1

2

341 Driveline (72%)

3 eDrive (2%)2 All Wheel Drive (25%)

4 Cylinder Liners (1%)

Revenue by destination

1

2

3

41 Europe (35%)

3 Asia (26%)2 North America (34%)

4 RoW (5%)

BuyImproveSell 18

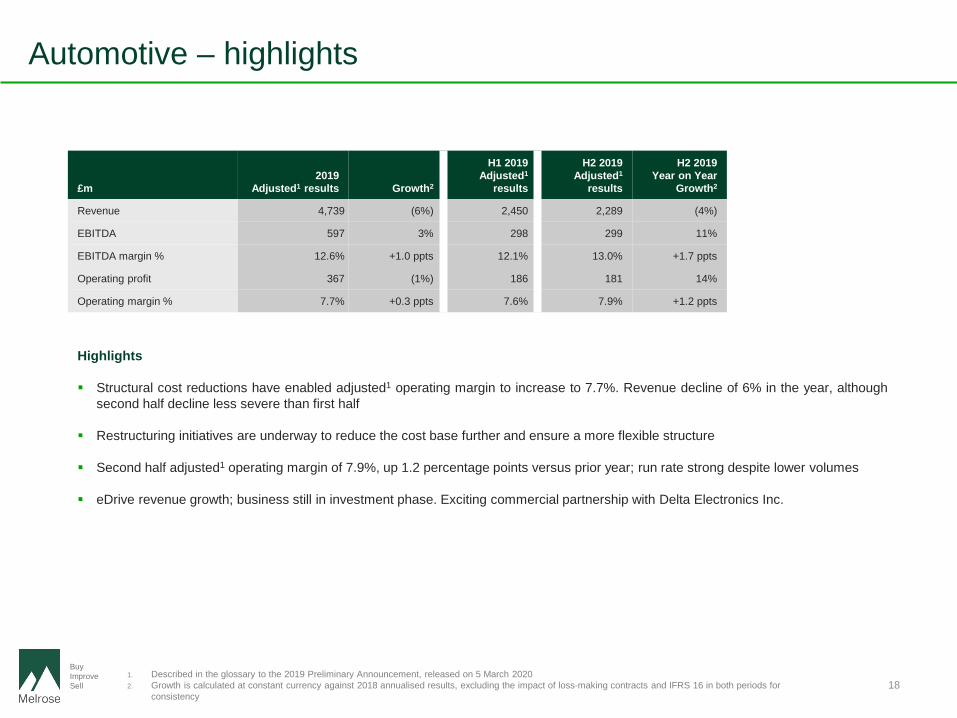

Automotive – highlights

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Growth is calculated at constant currency against 2018 annualised results, excluding the impact of loss-making contracts and IFRS 16 in both periods for

consistency

£m2019

Adjusted1 results Growth2

H1 2019 Adjusted1

results

H2 2019 Adjusted1

results

H2 2019 Year on Year

Growth2

Revenue 4,739 (6%) 2,450 2,289 (4%)

EBITDA 597 3% 298 299 11%

EBITDA margin % 12.6% +1.0 ppts 12.1% 13.0% +1.7 ppts

Operating profit 367 (1%) 186 181 14%

Operating margin % 7.7% +0.3 ppts 7.6% 7.9% +1.2 ppts

Highlights

Structural cost reductions have enabled adjusted1 operating margin to increase to 7.7%. Revenue decline of 6% in the year, althoughsecond half decline less severe than first half

Restructuring initiatives are underway to reduce the cost base further and ensure a more flexible structure

Second half adjusted1 operating margin of 7.9%, up 1.2 percentage points versus prior year; run rate strong despite lower volumes

eDrive revenue growth; business still in investment phase. Exciting commercial partnership with Delta Electronics Inc.

BuyImproveSell 19

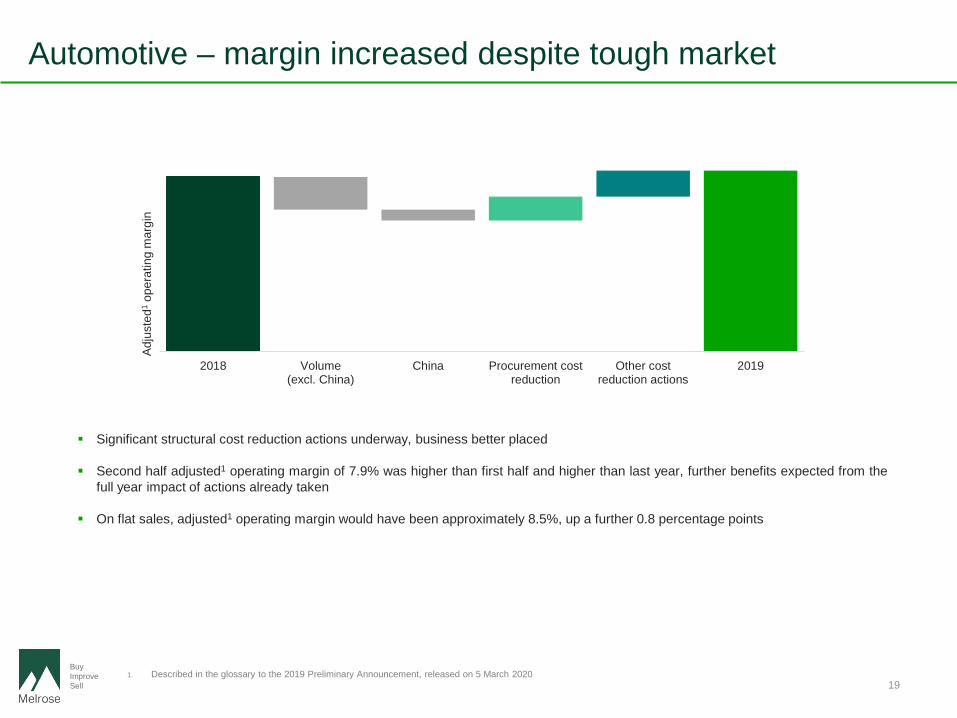

Automotive – margin increased despite tough market

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 2020

Significant structural cost reduction actions underway, business better placed

Second half adjusted1 operating margin of 7.9% was higher than first half and higher than last year, further benefits expected from thefull year impact of actions already taken

On flat sales, adjusted1 operating margin would have been approximately 8.5%, up a further 0.8 percentage points

2018 Volume(excl. China)

China Procurement costreduction

Other costreduction actions

2019

Adju

sted

1op

erat

ing

mar

gin

BuyImproveSell 20

Automotive – investments, technology and environment

Investment and restructuring

Significant restructuring programmes underway:

− Layers of management removed− Structural reductions in fixed costs− Early retirement programmes at several plants− Footprint reduction taking place – two site closures completed− Consolidation of back office service functions underway

Focus on improving production, material and inter-factory flows

Structural improvements in procurement, yielding direct and indirect savings

Good progress being made on resolving loss-making contracts – release of corresponding provision

Working capital improvement plan being implemented

Technology and ESG

Electric vehicle powertrain solutions enable low-carbon vehicles – eDrive becoming increasingly important with capital investments to increase specific eDrive manufacturing capacity

Strategy to make electric propulsion more affordable – using standardised electric drive systems and highly integrated inverters and motors

Strategic collaboration with power electronics specialist, Delta Electronics Inc., joint development should accelerate delivery of next generation 3-in-1 eDrive systems – a key step towards scaling greener powertrain solutions

BuyImproveSell

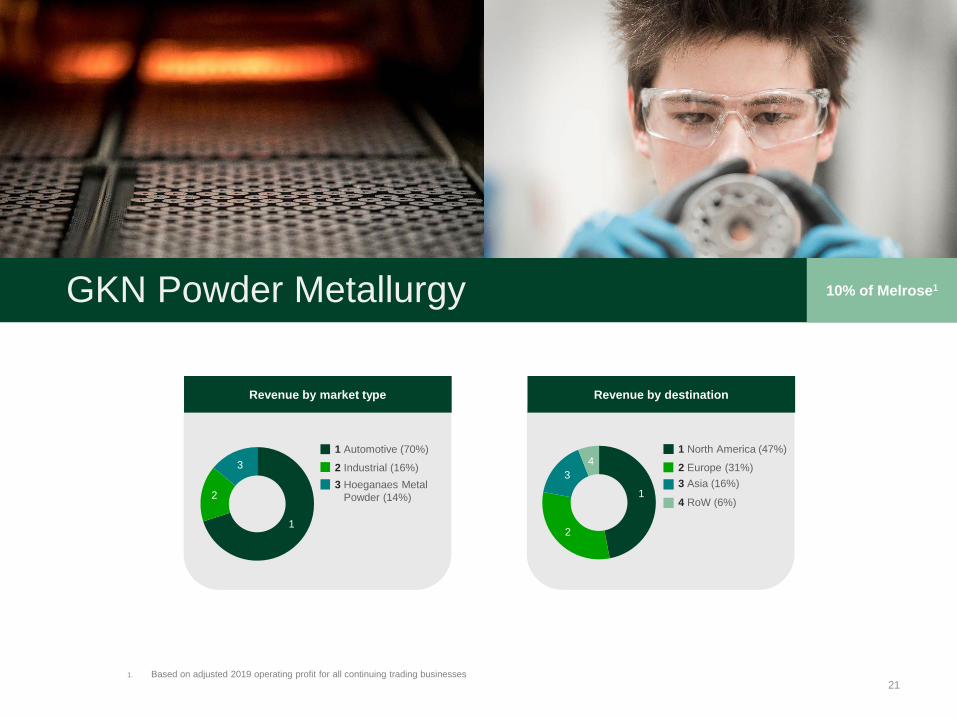

GKN Powder Metallurgy

21

10% of Melrose1

1. Based on adjusted 2019 operating profit for all continuing trading businesses

Revenue by market type

1

2

31 Automotive (70%)

3 Hoeganaes Metal Powder (14%)

2 Industrial (16%)

Revenue by destination

1

2

34

1 North America (47%)

3 Asia (16%)2 Europe (31%)

4 RoW (6%)

BuyImproveSell 22

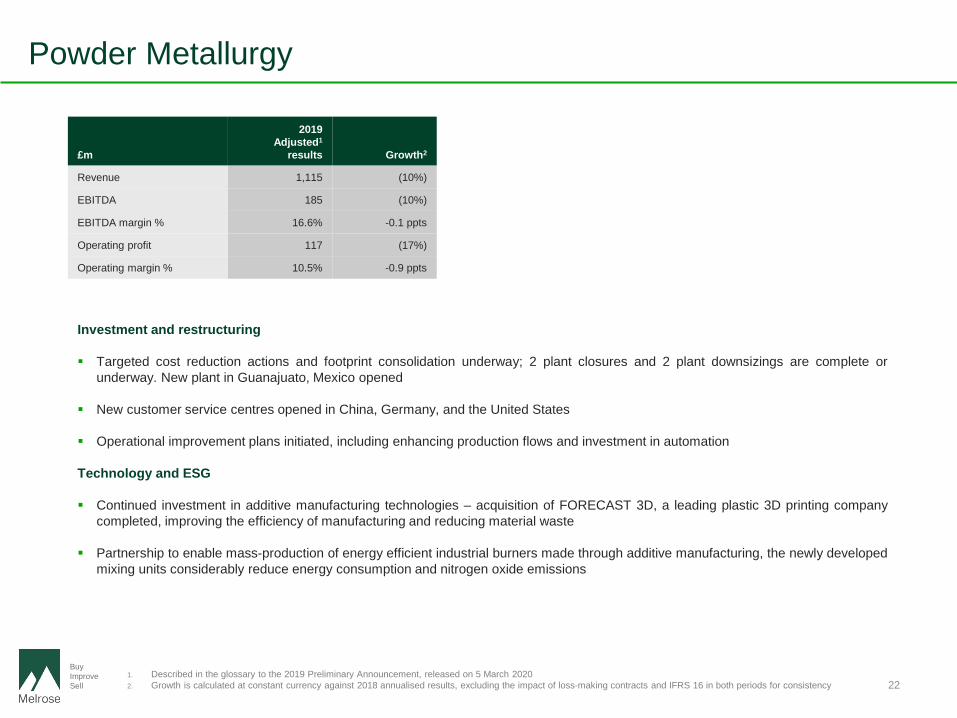

Powder Metallurgy

Investment and restructuring

Targeted cost reduction actions and footprint consolidation underway; 2 plant closures and 2 plant downsizings are complete orunderway. New plant in Guanajuato, Mexico opened

New customer service centres opened in China, Germany, and the United States

Operational improvement plans initiated, including enhancing production flows and investment in automation

Technology and ESG

Continued investment in additive manufacturing technologies – acquisition of FORECAST 3D, a leading plastic 3D printing companycompleted, improving the efficiency of manufacturing and reducing material waste

Partnership to enable mass-production of energy efficient industrial burners made through additive manufacturing, the newly developedmixing units considerably reduce energy consumption and nitrogen oxide emissions

£m

2019 Adjusted1

results Growth2

Revenue 1,115 (10%)

EBITDA 185 (10%)

EBITDA margin % 16.6% -0.1 ppts

Operating profit 117 (17%)

Operating margin % 10.5% -0.9 ppts

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Growth is calculated at constant currency against 2018 annualised results, excluding the impact of loss-making contracts and IFRS 16 in both periods for consistency

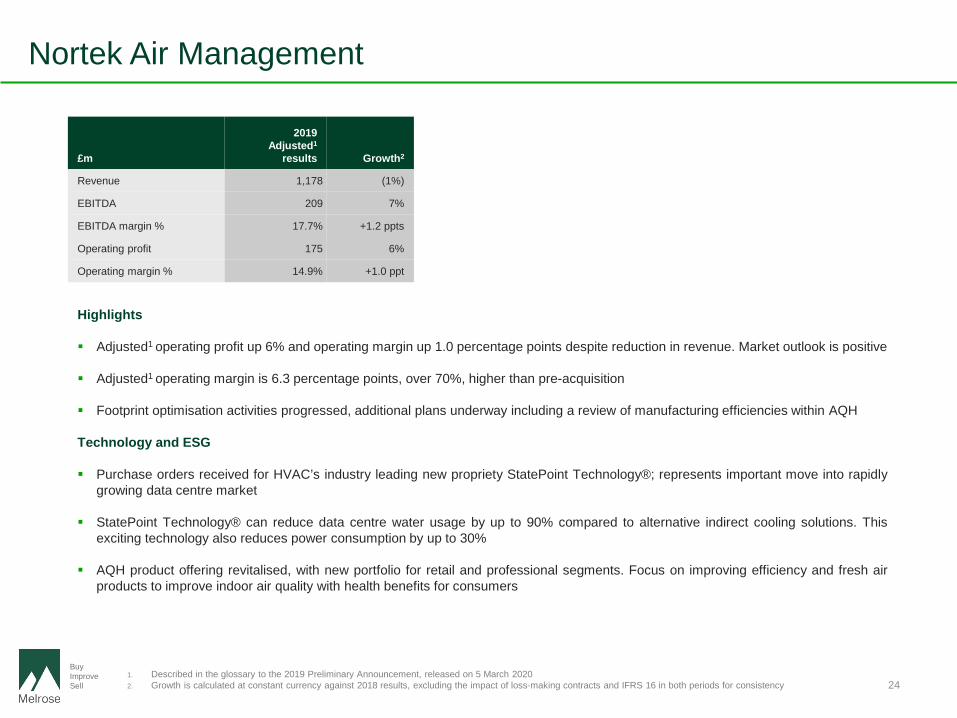

Nortek Air Management

23

15% of Melrose1

1. Based on adjusted 2019 operating profit for all continuing trading businesses

1

2 31 North America (94%)2 Europe (4%)

Revenue by destination

3 Asia (2%)

Revenue by market

12

3 4 51 Home (61%)

3 Health (5%)2 Work (28%)

4 Education (4%)5 Aftermarket (2%)

1

2

Revenue by business

1 AQH (41%)2 HVAC (59%)

BuyImproveSell 24

Nortek Air Management

Highlights

Adjusted1 operating profit up 6% and operating margin up 1.0 percentage points despite reduction in revenue. Market outlook is positive

Adjusted1 operating margin is 6.3 percentage points, over 70%, higher than pre-acquisition

Footprint optimisation activities progressed, additional plans underway including a review of manufacturing efficiencies within AQH

Technology and ESG

Purchase orders received for HVAC’s industry leading new propriety StatePoint Technology®; represents important move into rapidlygrowing data centre market

StatePoint Technology® can reduce data centre water usage by up to 90% compared to alternative indirect cooling solutions. Thisexciting technology also reduces power consumption by up to 30%

AQH product offering revitalised, with new portfolio for retail and professional segments. Focus on improving efficiency and fresh airproducts to improve indoor air quality with health benefits for consumers

£m

2019 Adjusted1

results Growth2

Revenue 1,178 (1%)

EBITDA 209 7%

EBITDA margin % 17.7% +1.2 ppts

Operating profit 175 6%

Operating margin % 14.9% +1.0 ppt

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Growth is calculated at constant currency against 2018 results, excluding the impact of loss-making contracts and IFRS 16 in both periods for consistency

Other Industrial

25

1

2

3 41 Europe (20%)

3 Asia (8%)2 North America (69%)

4 RoW (3%)

Revenue by destinationRevenue by business

1

2

3

1 Ergotron (35%)

3 Security & SmartTechnology (41%)

2 Brush (24%)

7% of Melrose1

1. Based on adjusted 2019 operating profit for all continuing trading businesses

BuyImproveSell 26

Other Industrial

£m2019

Adjusted1 results Growth2

Revenue 708 (9%)

EBITDA 103 (20%)

EBITDA margin % 14.5% -1.8 ppts

Operating profit 86 (21%)

Operating margin % 12.1% -1.8 ppts

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. Growth is calculated at constant currency against 2018 results, excluding the impact of loss-making contracts and IFRS 16 in both periods for consistency

Investment and restructuring

Ergotron market impacted by US tariffs on Chinese goods. Adjusted1 operating profit higher than last year on reduced revenue. Newproducts gaining traction

Brush margins expanding following completion of successful restructuring. Operational footprint consolidated into product-specificfacilities and dedicated service centres. Enhanced focus on growing services market

Security & Smart Technology moved from Nortek Air & Security to Other Industrial following the Board’s decision to consider strategicoptions for Nortek Air Management and Security & Smart Technology separately

Security market remains challenging, partly due to the impact of US tariffs, increased competition and technological changes, however,operations have been restructured to move production out of China

Wheels & Structures business made a small adjusted1 operating loss and is classified as held for sale at 31 December 2019

Appendices

27

BuyImproveSell

BuyImproveSell

Impact of loss-making contracts

28

Continuing operations£m Revenue

Operating profit/(loss)pre-positive

impact of loss-making

contracts

Positiveimpact of

loss-making contracts

Operating profit/(loss)

post-positive impact of

loss-makingcontracts

Operating margin

Pre-positive impact of

loss-making contracts

Post-positive impact of

loss-making contracts

Aerospace 3,852 367 42 409 9.5% 10.6%

Automotive 4,739 338 29 367 7.2% 7.7%

Powder Metallurgy 1,115 108 9 117 9.7% 10.5%

Nortek Air Management 1,178 175 - 175 14.9% 14.9%

Other Industrial 708 85 1 86 11.9% 12.1%

Central - (52) - (52) - -

Total 11,592 1,021 81 1,102 8.8% 9.5%

Adjusted1 results

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 2020

BuyImproveSell 29

Aerospace future potential cash profile

Over £10 billion of cash expected from existing RRSP1 arrangements

1. Risk and revenue sharing partnership

0

50

100

150

200

250

300

350

400

450

2020 2025 2030 2035 2040 2045 2050 2055 2060

£m p

er a

nnum

Indicative cash flows from RRSP1 portfolio

BuyImproveSell 30

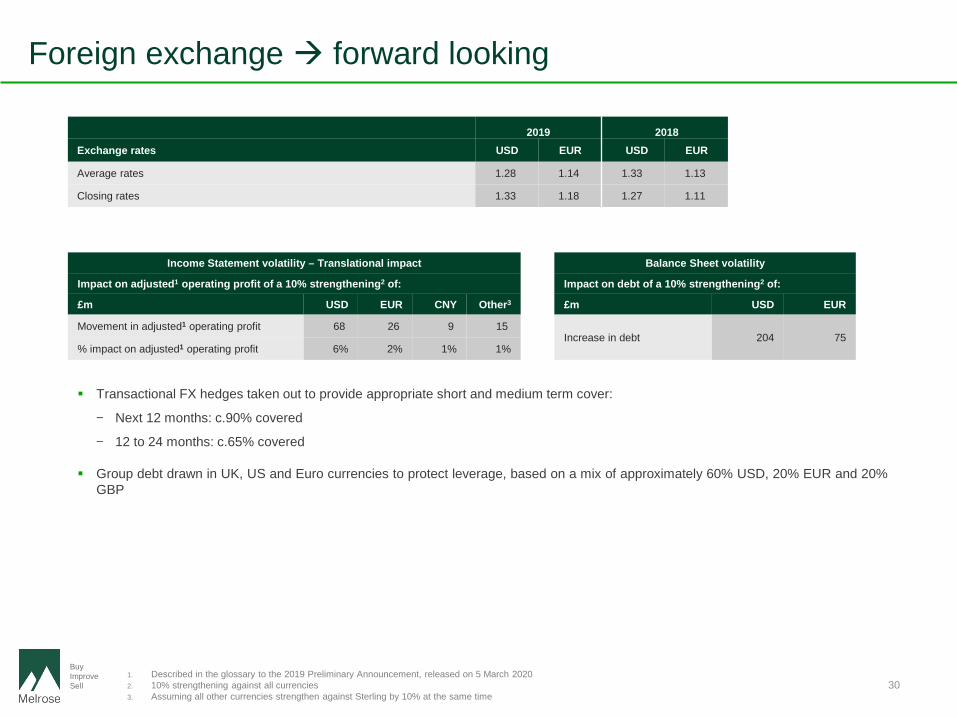

Foreign exchange forward looking

Transactional FX hedges taken out to provide appropriate short and medium term cover:

− Next 12 months: c.90% covered

− 12 to 24 months: c.65% covered

Group debt drawn in UK, US and Euro currencies to protect leverage, based on a mix of approximately 60% USD, 20% EUR and 20%GBP

2019 2018Exchange rates USD EUR USD EUR

Average rates 1.28 1.14 1.33 1.13

Closing rates 1.33 1.18 1.27 1.11

Income Statement volatility – Translational impact

Impact on adjusted1 operating profit of a 10% strengthening2 of:

£m USD EUR CNY Other3

Movement in adjusted1 operating profit 68 26 9 15

% impact on adjusted1 operating profit 6% 2% 1% 1%

Balance Sheet volatility

Impact on debt of a 10% strengthening2 of:

£m USD EUR

Increase in debt 204 75

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 20202. 10% strengthening against all currencies3. Assuming all other currencies strengthen against Sterling by 10% at the same time

BuyImproveSell

Interest

31

Interest

£m Facility size

At 31 December

2019

IncomeStatement

rate Cash rate

Bonds

2022 5.375% unsecured bond 450 450 2.9% 5.4%

2032 4.625% unsecured bond 300 300 4.4% 4.6%

Cross-currency swaps (2022 bonds) 74

750 824

Bank debt1

2021 term loan 824 824 3.8% 3.6%

2023 revolving credit facility 3,031 1,865 3.8% 3.4%

Cross-currency swaps 6

3,855 2,695

Other facilities 81 81

Total facilities / Gross debt 4,686 3,600 3.7% 3.6%

Cash (317)

Net debt2 3,283

1. Bank debt is presented net of £30 million of unamortised arrangement fees and includes £6 million cross-currency swaps valuation at 31 December 2019. Headroom on the Group’s committed bank facility at 31 December 2019 was £1,136 million

2. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 2020

Interest

Approximately 70% of interest exposure fixedon projected gross debt

Significant committed facility headroom

Effective average Income Statement interestrate of 3.7% on gross debt and cash rate of3.6%

2019 bond and associated cross-currencyswaps repaid in October 2019 usingcommitted bank debt

2021 term loan amended to include, atMelrose’s option, the right to extend thematurity date to April 2024

BuyImproveSell

Some helpful data for 2019

32

1. Described in the glossary to the 2019 Preliminary Announcement, released on 5 March 2020 2. IFRS 16 was effective from 1 January 2019, it increased the finance cost by £21 million (with a partially balancing uplift to operating profit) 3. £426 million of depreciation of owned property, plant and equipment and amortisation of owned computer software and depreciation of £72 million of leased assets as

described in the glossary to the 2019 Preliminary announcement released on 5 March 20204. Including the contribution paid on 6 January 20205. Includes £94 million of one-off payments, being the balance of the £150 million upfront commitment, and £17 million contribution following the disposal of Walterscheid

Powertrain Group

Continuing operations Income Statement Cash Flow

Item 2019 adjusted1 results 2019 adjusted1 results

Operating profit £1,102 million £1,102 million

Positive impact of loss-making contracts included above (£81 million) N/A

Central costs £52 million (includes a GKN LTIP charge of £20 million) (£32 million)

Adjusted free cash flow1 N/A £591 million

Finance costs2:- Bank and loan related- Amortisation of debt arrangement costs- Pension interest- Other

(£143 million) (£11 million)(£31 million)(£28 million)

(£178 million)2

Tax 21.4%(of adjusted1 profit before tax)

(£117 million)(13% of adjusted1 profit before tax)

Depreciation (£498 million)3 £498 million3

Capital expenditure N/A (£495 million)

Pension payments – ongoing contributions (global) N/A (£102 million)4

(£65 million UK, £37 million overseas)

Pension payments – special contributions N/A (£111 million) in 20195

(£56 million) in 2018

Restructuring costs (£238 million) (£190 million)

Annual dividend 5.1 pence per share (£231 million)

Non-controlling interest £6 million N/A

Number of shares in issue 4,858 million(average number of shares) N/A

![2003 annual [Read-Only]/media/Files/R/RBS... · Slide 4 Dividends 2003 2002 Dividend per ordinary share 50.3 pence 43.7 pence Dividend growth +15% +15% AVS dividend 55.0 pence 30.0](https://static.fdocuments.in/doc/165x107/5f7e0968c930365d39560b1b/2003-annual-read-only-mediafilesrrbs-slide-4-dividends-2003-2002-dividend.jpg)