Megatrends - iron ore, metallurgical coal and scrap 2 - CRU - OECD-SA Dec 2014.pdf · Megatrends -...

25

Megatrends - iron ore, metallurgical coal and scrap Prepared for: OECD/South Africa Workshop on Steelmaking Raw Materials 11 th December 2014 Prepared by: Laura Brooks, Senior Consultant

Transcript of Megatrends - iron ore, metallurgical coal and scrap 2 - CRU - OECD-SA Dec 2014.pdf · Megatrends -...

Megatrends - iron ore, metallurgical coal and scrap

Prepared for:

OECD/South Africa Workshop on Steelmaking Raw Materials

11th December 2014

Prepared by: Laura Brooks, Senior Consultant

Agenda • Summary of trade flows • Recent trends for the bulks – why have prices collapsed? • Forecast – 3 megatrends to watch for • What are our expectations for the scrap market? • Conclusions

3

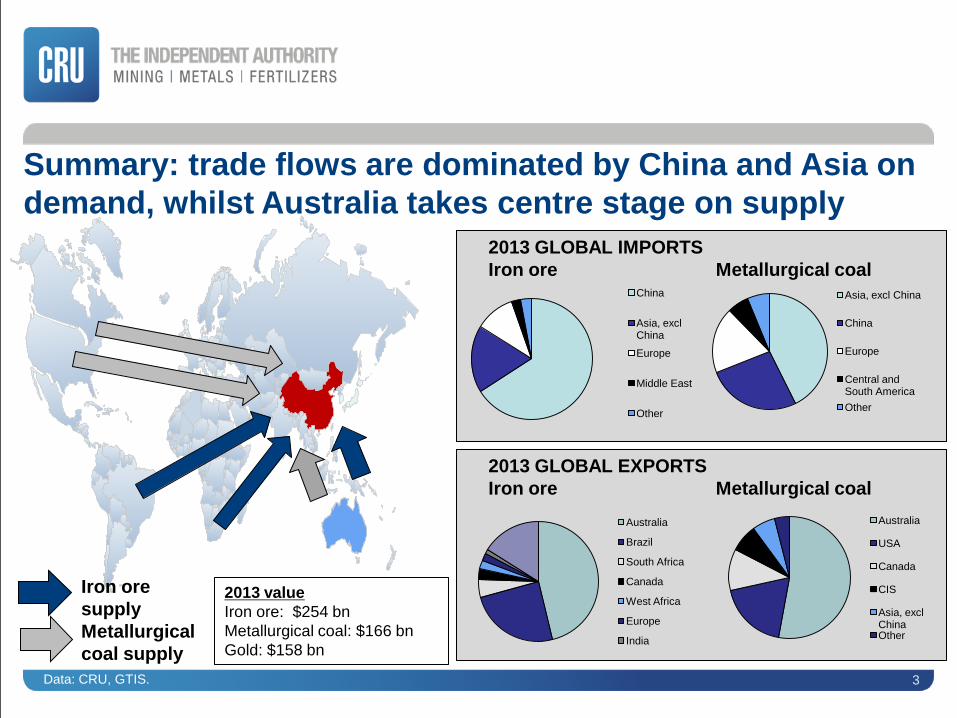

Summary: trade flows are dominated by China and Asia on demand, whilst Australia takes centre stage on supply

China

Asia, excl China

Europe

Middle East

Other

Asia, excl China

China

Europe

Central and South America Other

2013 GLOBAL IMPORTS Iron ore Metallurgical coal

2013 GLOBAL EXPORTS Iron ore Metallurgical coal

Australia

Brazil

South Africa

Canada

West Africa

Europe

India

Australia

USA

Canada

CIS

Asia, excl China Other

2013 value Iron ore: $254 bn Metallurgical coal: $166 bn Gold: $158 bn

Iron ore supply Metallurgical coal supply

Data: CRU, GTIS.

Agenda • Summary of trade flows • Recent trends for the bulks – why have prices collapsed? • Forecast – 3 megatrends to watch for • What are our expectations for the scrap market? • Conclusions

5

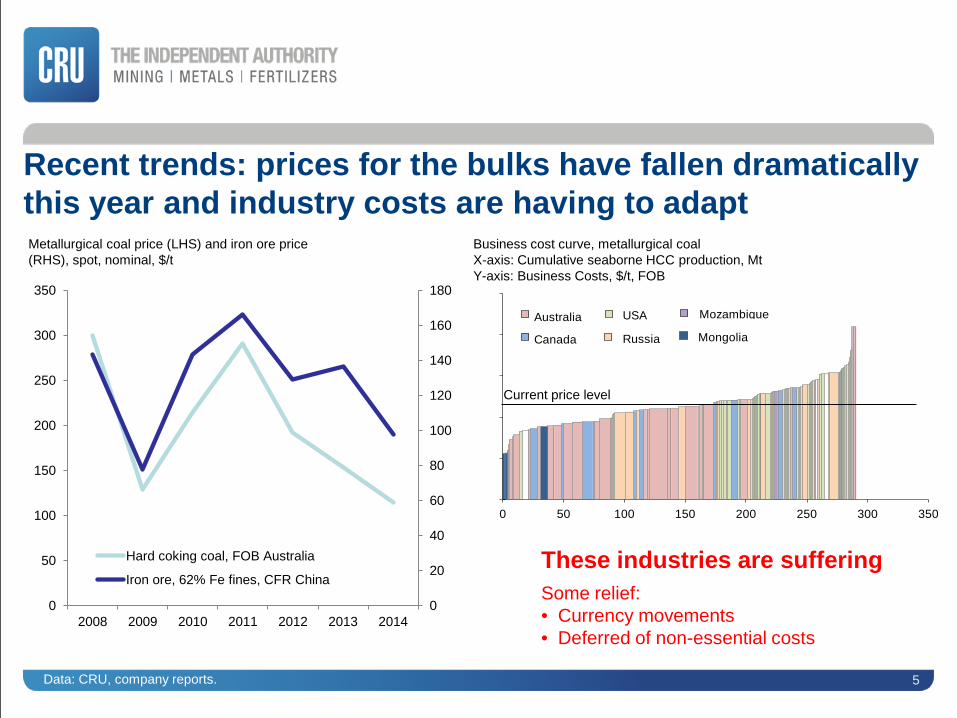

Recent trends: prices for the bulks have fallen dramatically this year and industry costs are having to adapt

0

20

40

60

80

100

120

140

160

180

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014

Hard coking coal, FOB Australia

Iron ore, 62% Fe fines, CFR China

Metallurgical coal price (LHS) and iron ore price (RHS), spot, nominal, $/t

0

50

100

150

200

250

0 50 100 150 200 250 300 350

Cos

ts ($

/t)

Cumulative production (mt)

0

50

100

150

200

250

0 50 100 150 200 250 300 350

Australia USA

Canada Russia

Mozambique

Mongolia

Business cost curve, metallurgical coal X-axis: Cumulative seaborne HCC production, Mt Y-axis: Business Costs, $/t, FOB

These industries are suffering

Some relief: • Currency movements • Deferred of non-essential costs

Current price level

Data: CRU, company reports.

6

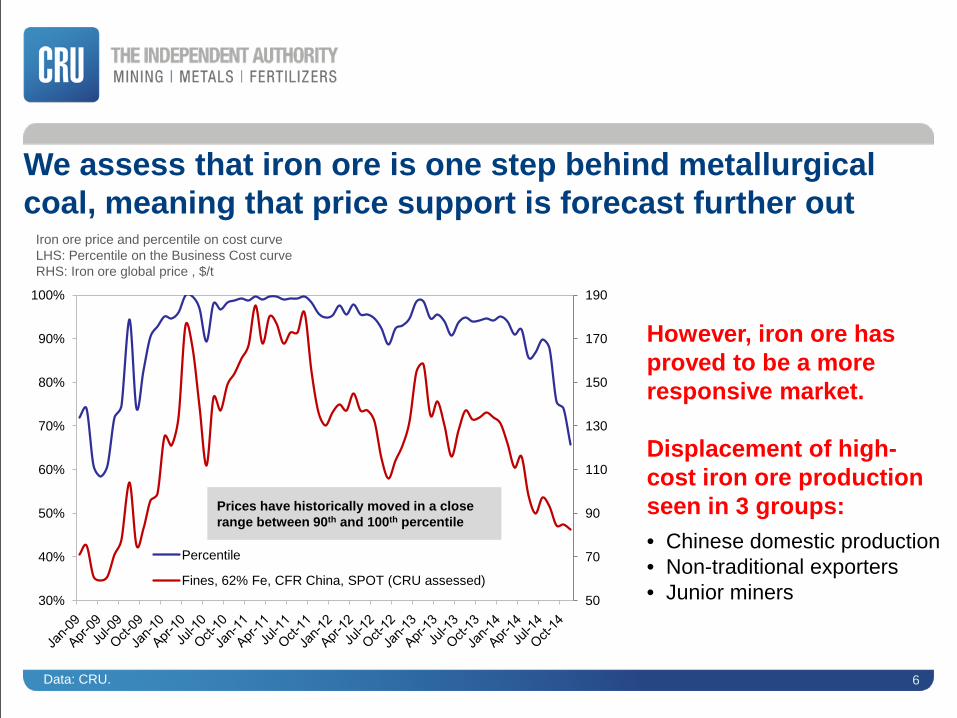

We assess that iron ore is one step behind metallurgical coal, meaning that price support is forecast further out

However, iron ore has proved to be a more responsive market. Displacement of high- cost iron ore production seen in 3 groups:

• Chinese domestic production • Non-traditional exporters • Junior miners

50

70

90

110

130

150

170

190

30%

40%

50%

60%

70%

80%

90%

100%

Percentile

Fines, 62% Fe, CFR China, SPOT (CRU assessed)

Iron ore price and percentile on cost curve LHS: Percentile on the Business Cost curve RHS: Iron ore global price , $/t

Prices have historically moved in a close range between 90th and 100th percentile

Data: CRU.

7

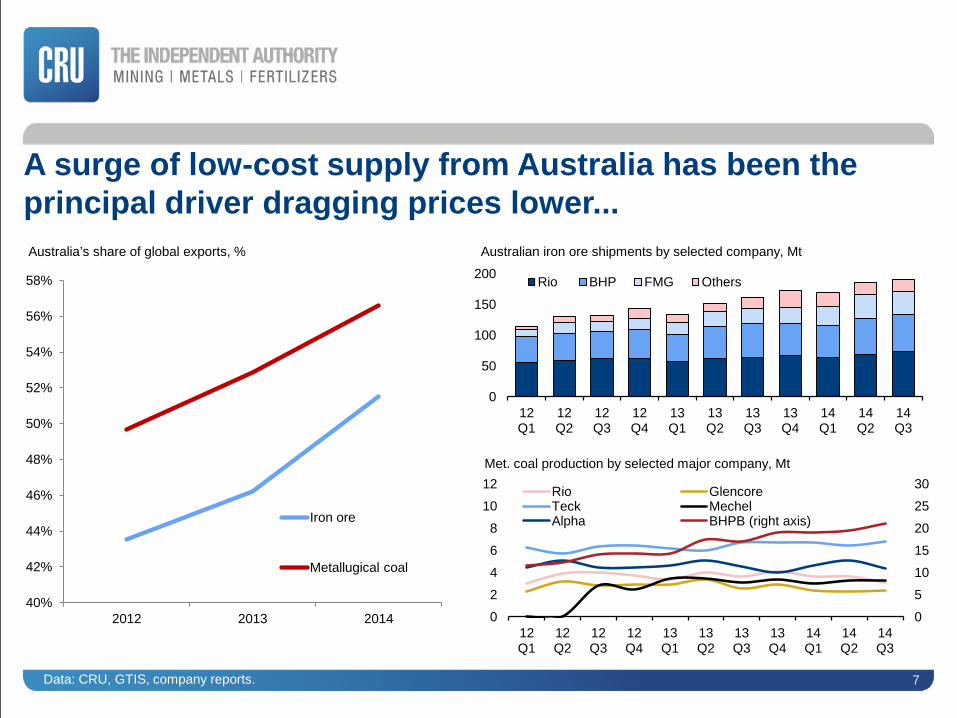

A surge of low-cost supply from Australia has been the principal driver dragging prices lower...

0

50

100

150

200

12 Q1

12 Q2

12 Q3

12 Q4

13 Q1

13 Q2

13 Q3

13 Q4

14 Q1

14 Q2

14 Q3

Rio BHP FMG Others

Australian iron ore shipments by selected company, Mt

0

5

10

15

20

25

30

0

2

4

6

8

10

12

12 Q1

12 Q2

12 Q3

12 Q4

13 Q1

13 Q2

13 Q3

13 Q4

14 Q1

14 Q2

14 Q3

Rio Glencore Teck Mechel Alpha BHPB (right axis)

Met. coal production by selected major company, Mt

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

2012 2013 2014

Iron ore

Metallugical coal

Australia’s share of global exports, %

Data: CRU, GTIS, company reports.

8

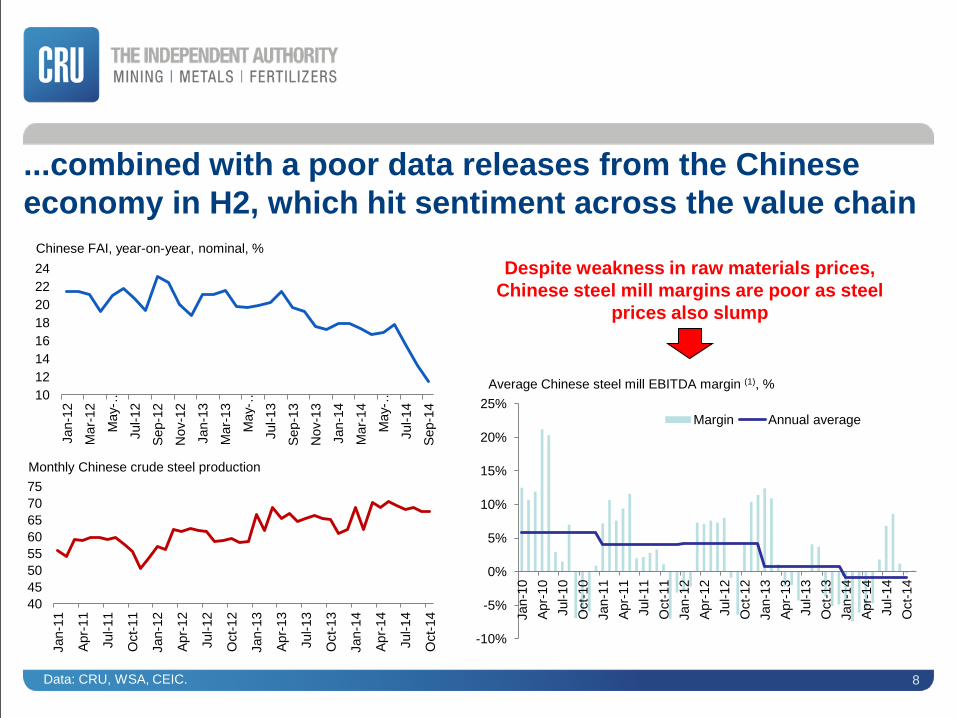

...combined with a poor data releases from the Chinese economy in H2, which hit sentiment across the value chain

40 45 50 55 60 65 70 75

Jan-

11

Apr-

11

Jul-1

1

Oct

-11

Jan-

12

Apr-

12

Jul-1

2

Oct

-12

Jan-

13

Apr-

13

Jul-1

3

Oct

-13

Jan-

14

Apr-

14

Jul-1

4

Oct

-14

Monthly Chinese crude steel production

10 12 14 16 18 20 22 24

Jan-

12

Mar

-12

May

-…

Jul-1

2

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-…

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-…

Jul-1

4

Sep-

14

Chinese FAI, year-on-year, nominal, %

-10%

-5%

0%

5%

10%

15%

20%

25%

Jan-

10

Apr-

10

Jul-1

0 O

ct-1

0 Ja

n-11

Ap

r-11

Ju

l-11

Oct

-11

Jan-

12

Apr-

12

Jul-1

2 O

ct-1

2 Ja

n-13

Ap

r-13

Ju

l-13

Oct

-13

Jan-

14

Apr-

14

Jul-1

4 O

ct-1

4

Margin Annual average

Despite weakness in raw materials prices, Chinese steel mill margins are poor as steel

prices also slump

Average Chinese steel mill EBITDA margin (1), %

Data: CRU, WSA, CEIC.

Agenda • Summary of trade flows • Recent trends for the bulks – why have prices collapsed? • Forecast – 3 megatrends to watch for • What are our expectations for the scrap market? • Conclusions

10

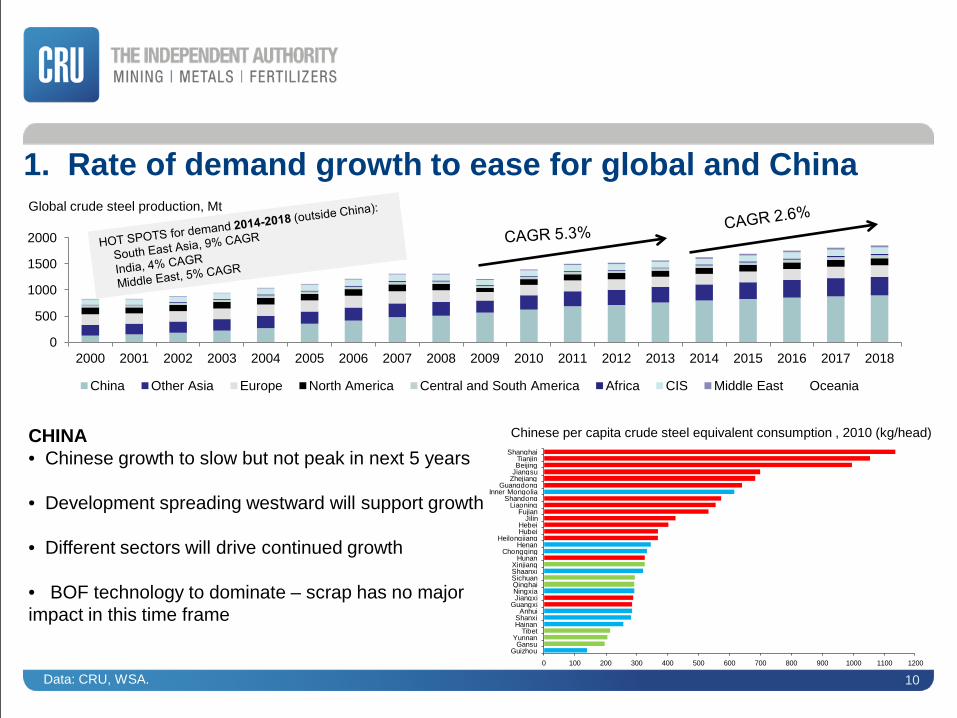

1. Rate of demand growth to ease for global and China

0 100 200 300 400 500 600 700 800 900 1000 1100 1200

GuizhouGansu

YunnanTibet

HainanShanxi

AnhuiGuangxiJiangxiNingxiaQinghaiSichuanShaanxiXinjiang

HunanChongqing

HenanHeilongjiang

HubeiHebei

JilinFujian

LiaoningShandong

Inner MongoliaGuangdong

ZhejiangJiangsuBeijingTianjin

Shanghai

Chinese per capita crude steel equivalent consumption , 2010 (kg/head)

0

500

1000

1500

2000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

China Other Asia Europe North America Central and South America Africa CIS Middle East Oceania

Global crude steel production, Mt

CHINA • Chinese growth to slow but not peak in next 5 years • Development spreading westward will support growth

• Different sectors will drive continued growth

• BOF technology to dominate – scrap has no major impact in this time frame

Data: CRU, WSA.

11

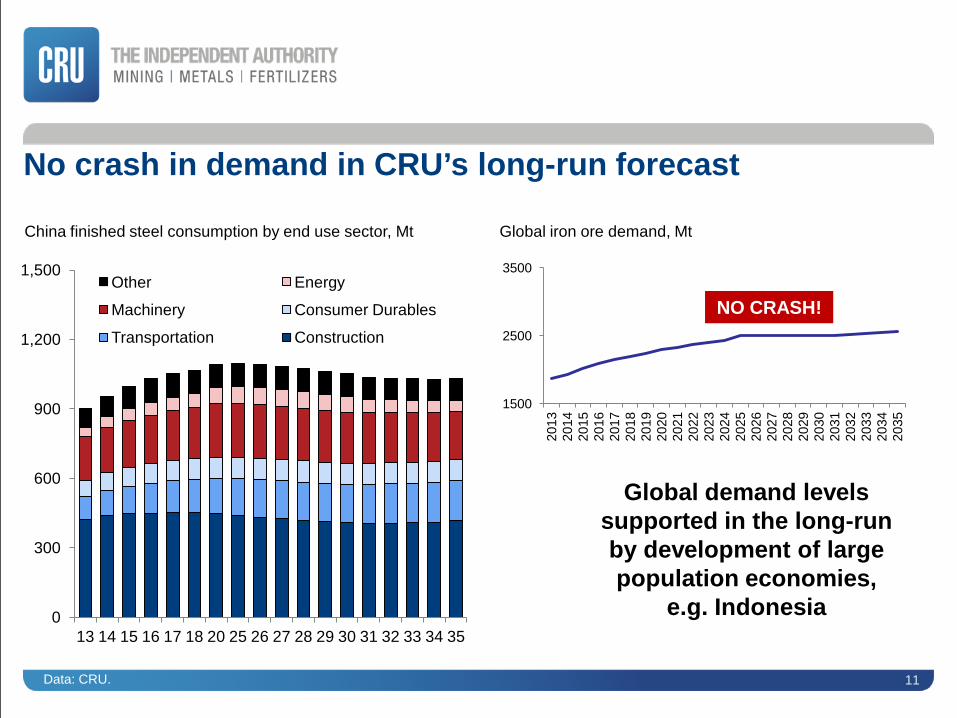

No crash in demand in CRU’s long-run forecast

0

300

600

900

1,200

1,500

13 14 15 16 17 18 20 25 26 27 28 29 30 31 32 33 34 35

Other Energy

Machinery Consumer Durables

Transportation Construction

China finished steel consumption by end use sector, Mt

1500

2500

3500

2013

20

14

2015

20

16

2017

20

18

2019

20

20

2021

20

22

2023

20

24

2025

20

26

2027

20

28

2029

20

30

2031

20

32

2033

20

34

2035

Global iron ore demand, Mt

Global demand levels supported in the long-run by development of large population economies,

e.g. Indonesia

NO CRASH!

Data: CRU.

12

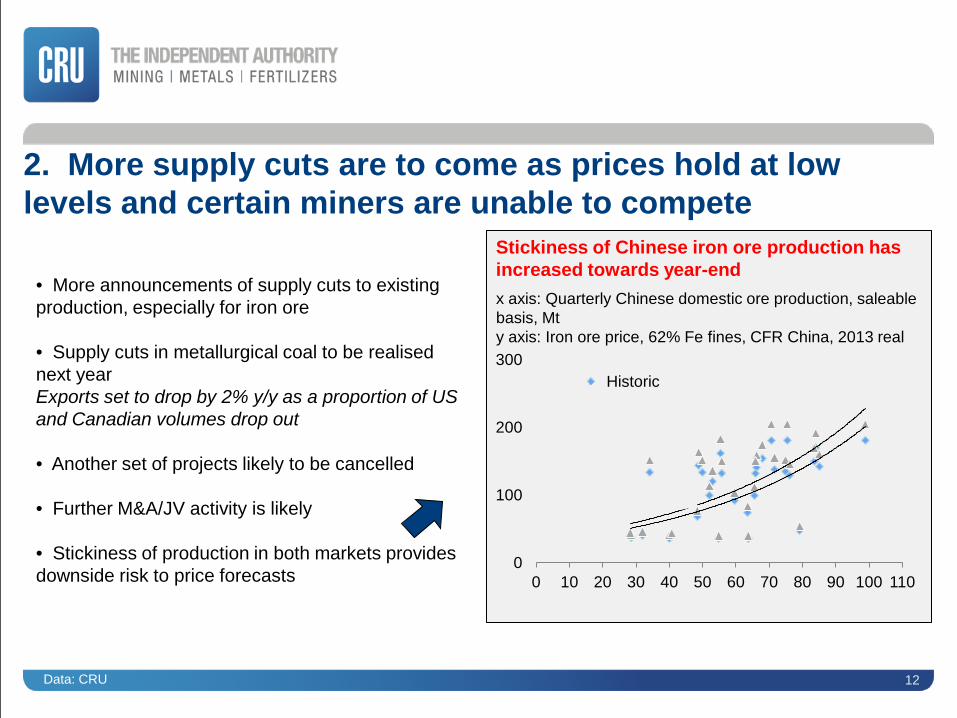

2. More supply cuts are to come as prices hold at low levels and certain miners are unable to compete

• More announcements of supply cuts to existing production, especially for iron ore

• Supply cuts in metallurgical coal to be realised next year Exports set to drop by 2% y/y as a proportion of US and Canadian volumes drop out • Another set of projects likely to be cancelled

• Further M&A/JV activity is likely

• Stickiness of production in both markets provides downside risk to price forecasts

0

100

200

300

0 10 20 30 40 50 60 70 80 90 100 110

Historic

x axis: Quarterly Chinese domestic ore production, saleable basis, Mt y axis: Iron ore price, 62% Fe fines, CFR China, 2013 real

Stickiness of Chinese iron ore production has increased towards year-end

Data: CRU

13

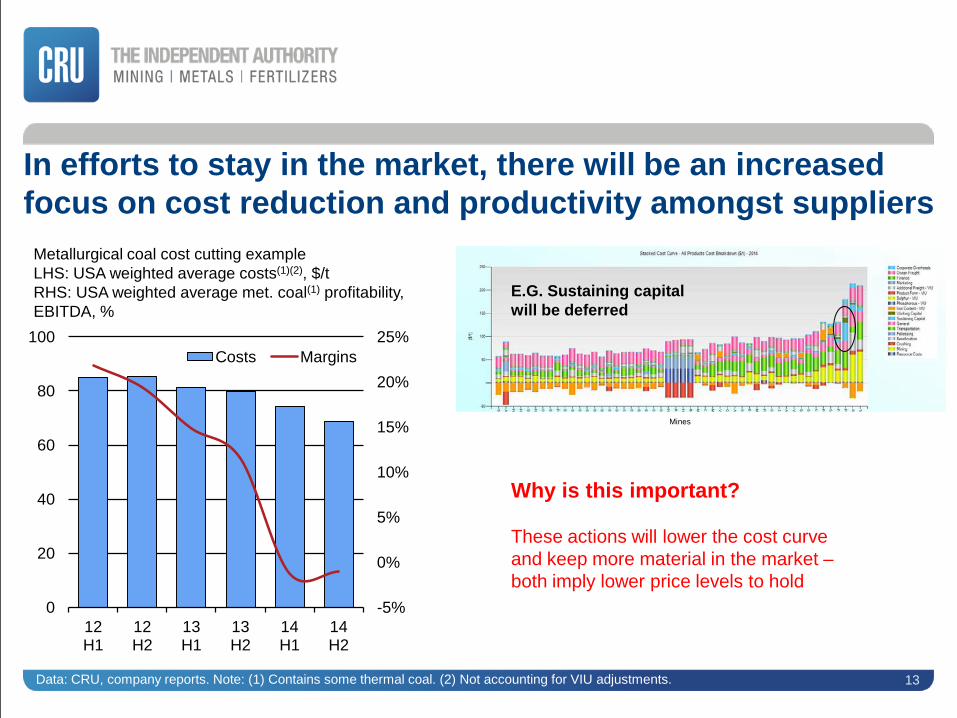

In efforts to stay in the market, there will be an increased focus on cost reduction and productivity amongst suppliers

-5%

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

12 H1

12 H2

13 H1

13 H2

14 H1

14 H2

Costs Margins

Metallurgical coal cost cutting example LHS: USA weighted average costs(1)(2), $/t RHS: USA weighted average met. coal(1) profitability, EBITDA, %

Data: CRU, company reports. Note: (1) Contains some thermal coal. (2) Not accounting for VIU adjustments.

E.G. Sustaining capital will be deferred

Mines

Why is this important? These actions will lower the cost curve and keep more material in the market – both imply lower price levels to hold

14

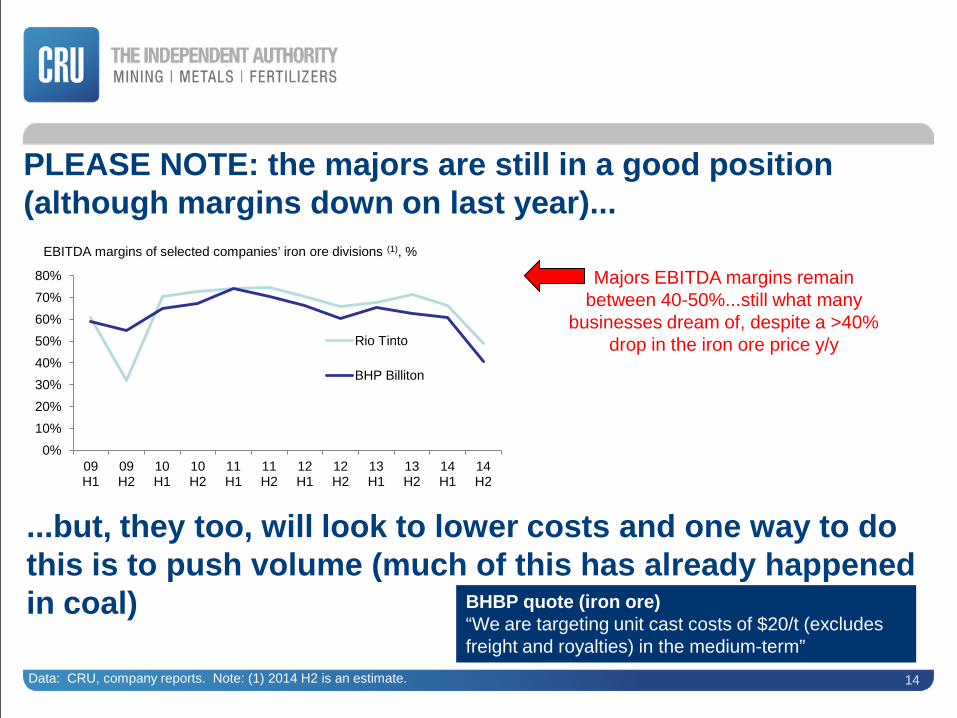

PLEASE NOTE: the majors are still in a good position (although margins down on last year)...

...but, they too, will look to lower costs and one way to do this is to push volume (much of this has already happened in coal) BHBP quote (iron ore)

“We are targeting unit cast costs of $20/t (excludes freight and royalties) in the medium-term”

0% 10% 20% 30% 40% 50% 60% 70% 80%

09 H1

09 H2

10 H1

10 H2

11 H1

11 H2

12 H1

12 H2

13 H1

13 H2

14 H1

14 H2

Rio Tinto

BHP Billiton

Majors EBITDA margins remain between 40-50%...still what many

businesses dream of, despite a >40% drop in the iron ore price y/y

EBITDA margins of selected companies’ iron ore divisions (1), %

Data: CRU, company reports. Note: (1) 2014 H2 is an estimate.

15

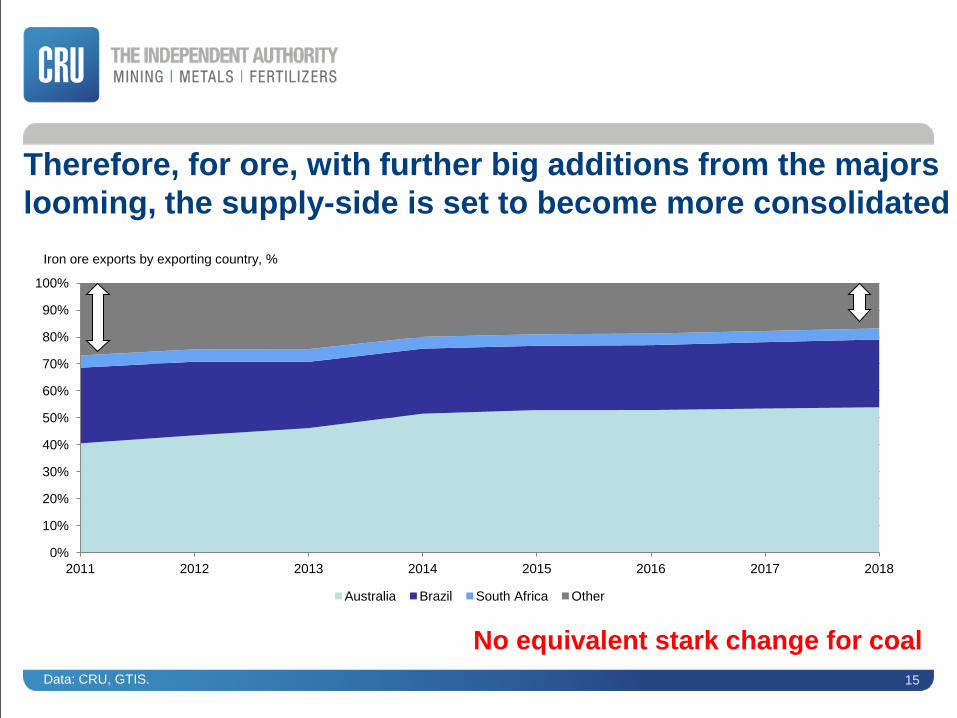

Therefore, for ore, with further big additions from the majors looming, the supply-side is set to become more consolidated

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 2017 2018

Australia Brazil South Africa Other

Iron ore exports by exporting country, %

No equivalent stark change for coal Data: CRU, GTIS.

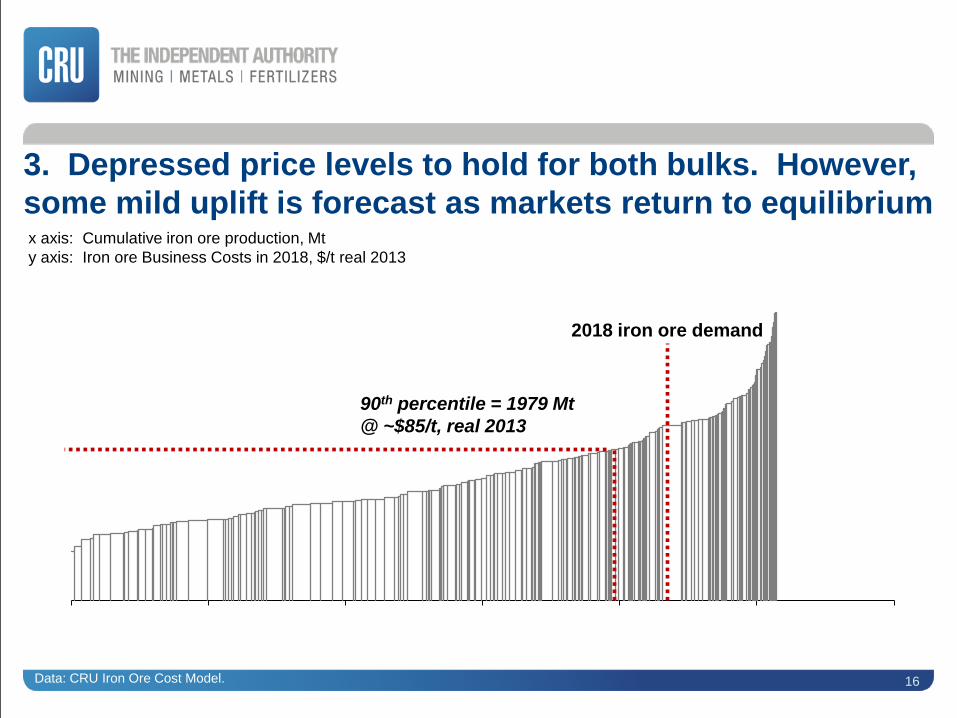

3. Depressed price levels to hold for both bulks. However, some mild uplift is forecast as markets return to equilibrium

Data: CRU Iron Ore Cost Model.

x axis: Cumulative iron ore production, Mt y axis: Iron ore Business Costs in 2018, $/t real 2013

0

20

40

60

80

100

120

140

160

180

0 500 1,000 1,500 2,000 2,500 3,000

2018 iron ore demand

90th percentile = 1979 Mt @ ~$85/t, real 2013

16

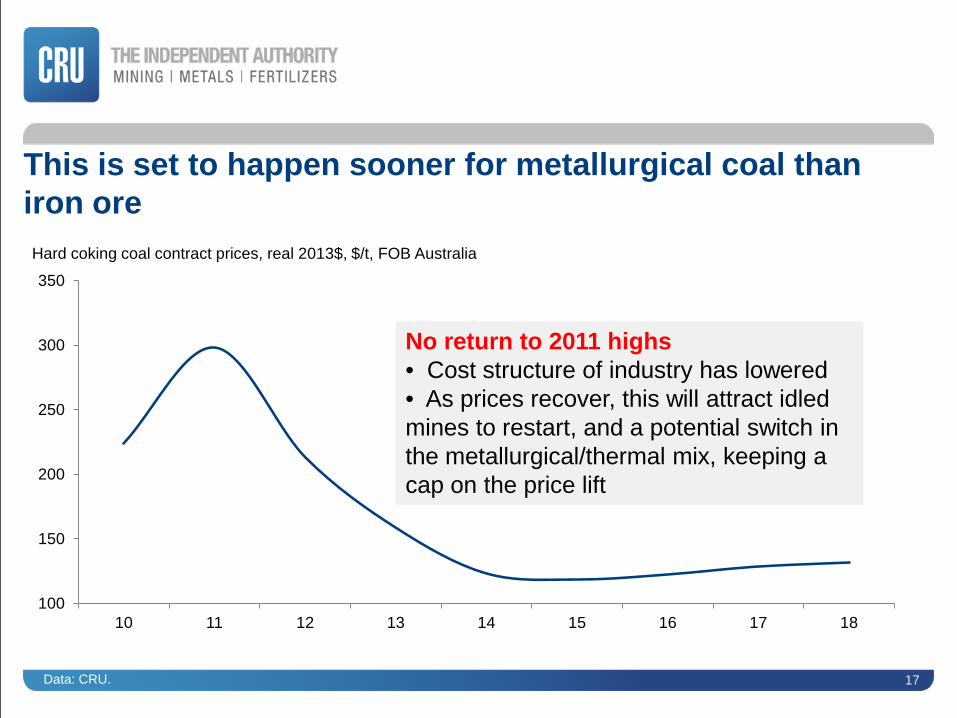

This is set to happen sooner for metallurgical coal than iron ore

17

100

150

200

250

300

350

10 11 12 13 14 15 16 17 18

Hard coking coal contract prices, real 2013$, $/t, FOB Australia

No return to 2011 highs • Cost structure of industry has lowered • As prices recover, this will attract idled mines to restart, and a potential switch in the metallurgical/thermal mix, keeping a cap on the price lift

Data: CRU.

18

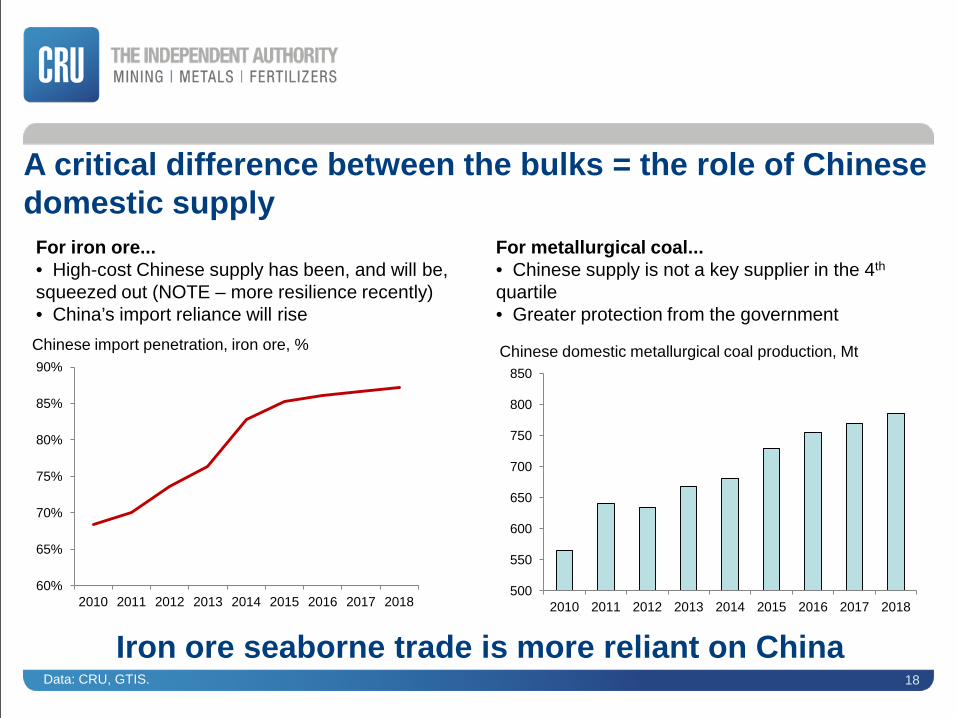

A critical difference between the bulks = the role of Chinese domestic supply

For iron ore... • High-cost Chinese supply has been, and will be, squeezed out (NOTE – more resilience recently) • China’s import reliance will rise

For metallurgical coal... • Chinese supply is not a key supplier in the 4th quartile • Greater protection from the government

Iron ore seaborne trade is more reliant on China

60%

65%

70%

75%

80%

85%

90%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Chinese import penetration, iron ore, %

500

550

600

650

700

750

800

850

2010 2011 2012 2013 2014 2015 2016 2017 2018

Chinese domestic metallurgical coal production, Mt

Data: CRU, GTIS.

Agenda • Summary of trade flows • Recent trends for the bulks – why have prices collapsed? • Forecast – 3 megatrends to watch for • What are our expectations for the scrap market? • Conclusions

20

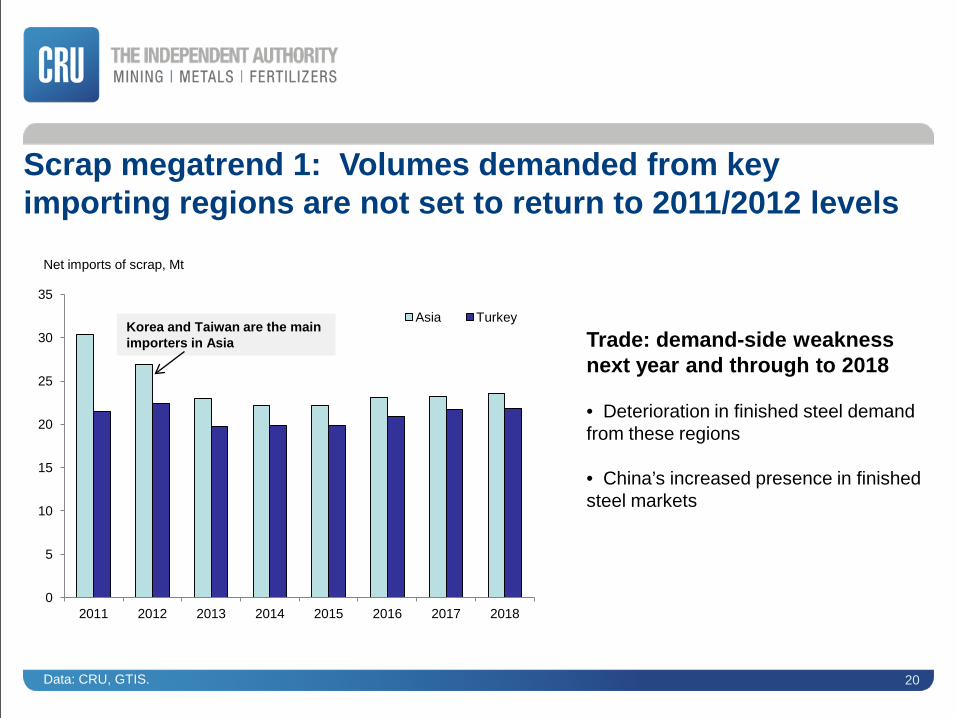

Scrap megatrend 1: Volumes demanded from key importing regions are not set to return to 2011/2012 levels

Net imports of scrap, Mt

0

5

10

15

20

25

30

35

2011 2012 2013 2014 2015 2016 2017 2018

Asia Turkey Korea and Taiwan are the main importers in Asia Trade: demand-side weakness

next year and through to 2018 • Deterioration in finished steel demand from these regions • China’s increased presence in finished steel markets

Data: CRU, GTIS.

21

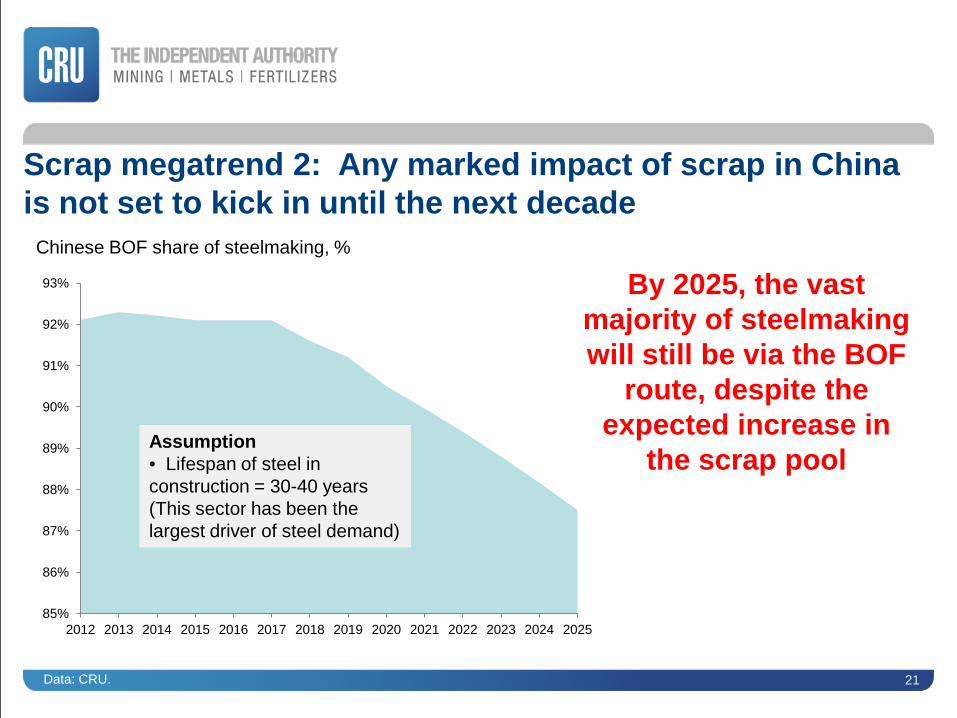

Scrap megatrend 2: Any marked impact of scrap in China is not set to kick in until the next decade

Chinese BOF share of steelmaking, %

85%

86%

87%

88%

89%

90%

91%

92%

93%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

By 2025, the vast majority of steelmaking will still be via the BOF

route, despite the expected increase in

the scrap pool Assumption • Lifespan of steel in construction = 30-40 years (This sector has been the largest driver of steel demand)

Data: CRU.

Agenda • Summary of trade flows • Recent trends for the bulks – why have prices collapsed? • Forecast – 3 megatrends to watch for • What are our expectations for the scrap market? • Conclusions

Conclusions what megatrends in the next 5 years?

1. Steel demand to continue to grow but at a slower rate 2. More supply cuts for the bulks – those in coal to come sooner 3. Increased focused amongst producers on cost control 4. Today’s lower price range is the new norm 5. Import demand in scrap markets to remain weaker than recent history

Thank you for your attention

Laura Brooks

Senior Consultant – Steel Raw Materials

T: +44 (0)20 7903 2239

Please address any questions or comments relating to this presentation to:

25