Mega Lifesciences PCL Investor Presentationmega.listedcompany.com/misc/PRESN/20140228-MEGA... ·...

41

We care Mega Lifesciences PCL Investor Presentation Financial Year 2013

Transcript of Mega Lifesciences PCL Investor Presentationmega.listedcompany.com/misc/PRESN/20140228-MEGA... ·...

We care

Mega Lifesciences PCLInvestor PresentationFinancial Year 2013

We care

Section 1Business Overview

3We care

Our history

1982

Incorporated

1985-86

1993-94

1995-96

20022012

•Received approval from Thai FDA for Samut Prakarnfacility in Thailand•Began manufacturing nifedipine for Berlin Pharmaceutical Industry Co. Ltd

•Expanded into Vietnam, Myanmar and Cambodia to sell branded products and operate distribution business

•Established manufacturing plant in Australia

•Market leading branded products in key Southeast Asian markets•Leading distributor of pharmaceutical and OTC products •Announced acquisition of Eugica

•Commenced branded products business •Acquired Medicrafts brand

We have evolved from an OEM player into a leading international consumer healthcare and pharmaceutical company

Started as an OEM manufacturer

Entered branded products and distribution business;

geographical expansion

Emerged as a leading branded and distribution company

2013

•Commissioning of new plant in Australia•Planned manufacturing expansion in Thailand• Successful IPO on SET

4We care

Distribution Business46.4% and 44.9 % of 2012 and 2013

operating revenues respectively

Branded Products Business 45.3% and 48.4% of 2012 and 2013

operating revenues, respectively

Mega at a glance

OEM Business8.3% and 6.7% of 2012 and 2013 operating revenues, respectively

2012 2013 Gr.%

Total Sales (THB mn) 2,700 3,403 26.0

Nutraceuticals 76.0% 76.1% 25.6

Prescription 19.9% 19.5% 22.9

OTC 4.1% 4.4% 35.3

2012 2013 Gr.%

Total Sales (THB mn) 498 473 (5.0)

Australia 52.4% 52.8% (4.3)

Thailand 30.9% 28.7% (11.7)

Others 16.7% 18.5% 5.4

1 2 3

65.9% and 72.8% of Gross Profit in 2012 and 2013, respectively

29.7% and 24.5% of Gross Profit in 2012 and 2013, respectively

4.5% and 2.7% of Gross Profit in 2012 and 2013, respectively

2012 2013 Gr.%

Total Sales (THB mn) 5,965 7,034 17.9

Mega Lifesciences PCL

2012 2013 Gr.%

Total Sales (THB mn) 2,767 3,157 14.1

Pharmaceuticals 75.8% 65.8% (0.9)

FMCG 20.1% 30.2% 71.2

Intersegment 4.1% 4.0% 11.6

5We care

Geographical overview of our operations – we derive majority of our revenue from Southeast Asia

Thailand, Vietnam and Myanmar are our key geographies which accounted for 75.7% of our operating revenue in 2013

1.Revenues exclude other income

Philippines

Indonesia

MalaysiaSingapore

Myanmar

Cambodia

VietnamThailand

Azerbaijan

Sri Lanka

Uzbekistan

YemenUnited Arab Emirates

Mongolia

Hong Kong

GhanaKenya

Nigeria

TanzaniaUganda

KazakhstanUkraine

Russia

Belarus

Peru

Denmark

Legend

Countries with sales of our branded products

Countries with manufacturing or product development capabilities

Ausralia

IndiaTrinidad

Rwanda

Kuwait

South East Asia 84.8%

Rest of World 15.2%

Southeast Asia accounts for majority of revenues1

Revenue Breakdown by Region (2013)

6We care

We sell nutraceuticals, prescription and OTC products within our branded business

Product Categories Description Key Brands

Nutraceutical Products

• Products which provide health benefits in addition to the basic nutritional value found in normal diet

• Regulation varies across jurisdictions but generally regulated for their manufacturing, safety, efficacy, labeling and marketing

Prescription Products

• Medicines only available for purchase by consumers with a medical prescription

• Strictly regulated by authorities as to their manufacturing, safety, efficacy, labeling and marketing

OTC Products • Medicines sold directly to consumer without a prescription from a healthcare professional

7We care

Our value-added distribution business model for pharmaceutical and FMCG products

Conventional distribution services (CDS)• Our integrated approach lends enhanced efficiency and quality control of our

products at every stage of our operations from procurement to delivery to our end consumers

• We purchase products from our principals, subject them to a quality control inspection, then warehouse the products in a climate-controlled environment until receipt of end customer orders. We arrange for logistics services and ensure the timely delivery of products

1

2

3

Sales and conventional distribution services (SCDS)• In addition to our conventional distribution services, we also provide sales support

to our principals• Our sales channels include pharmacies, hospitals and clinics for pharmaceutical

products and supermarkets, department stores, key accounts, wholesalers and dealers for FMCG products

Marketing, sales and conventional distribution services (MSCDS)• Our pharmaceutical and FMCG teams provide a complete package of marketing,

sales and distribution services tailored to our principals and their products• The teams market directly and engage in marketing activities through available

channels

Principals can choose from any of our three service models to help meet their distribution needs

8We care

Thailand manufacturing facilities: two manufacturing facilitiesFacility 1 – Soi 6, Samut Prakarn Facility 2 – Soi 8, Samut Prakarn

Description• Commenced

production in 1985• Planned upgrade to

3.8bn capsules p.a.1

• Manufactures:– Soft gels– Hard gels– Sachets

• Approved by German health authorities, the Thai FDA and the Australian TGA

1 Annual design capacity for soft gels will increase to 3.8 bn capsules when the addition of eight new production lines at the Soi 8 facility is completed,

Description• Commenced

production in 1985• Manufactures:

– Soft gels (after expansion)

– Hard gels– Tablets– Sachets

• Approved by German health authorities, the Thai FDA and the Australian TGA

9We care

Australian manufacturing facility: Pakenham facility

Overview

• Facility replaces the manufacturing facility established in Dandenong, Melbourne

• Commenced production in 2nd quarter 2013• Manufactures:• Hard capsules• Tablets• Powders

• Approved by Australian TGA

Pakenham facility

We care

Section 2Key investment highlights

11We care

Key investment highlights

Leading distributor of pharmaceutical and OTC products in frontier markets of Myanmar, Vietnam and Cambodia2

Focused on fast growing markets including a unique established and market leading presence in the Myanmar market3

High quality products manufactured in world-class manufacturing facilities accredited by international regulatory agencies

4

Strong product pipeline driven by an efficient and targeted product development strategy5

Proven track record of delivering growth and profitability6

Experienced management team instrumental in building the business is significantly invested in the Company7

Market leading own consumer health and pharmaceutical brands in fast growing developing markets1

12We care

Own Brand Rank Therapeutic Category (TC)

Nat C

#1 Vitamin C

Nat B

#1 Vitamin B Complex

Fish oil

#1 Anti-atheromaNatural

Gofen

#4 Anti-rheumatics Non-steroidal

Own Brand Rank Therapeutic Category (TC)

Ferrovit

#1 Haematinics

Enat

#1 Vitamin E

Calcivita

#1 Calcium Supplements

Livolin Forte

#1 Hepatoprotectant

Prenatal

#2 Prenatal

Nutrivita

#2 MVMM

Own Brand Rank Therapeutic Category (TC)

Enat

#1 Vitamin E

Eugica

#1 Herbal Cough Sedative

Acnotin

#2 Oral Anti-acne Preparation

Ferrovit

#5 Iron Combination Products

Giloba

#5Cerebral and

Peripheral Vascular

NNO

#3 Emollients and Protectives

Our market leading nutraceutical, branded generic and OTC brands

1

Source: IMS Health Sep 2013, Myanmar estimates based on Myanmar import customs data and Company assumptions

Thailand Vietnam Myanmar

Acnotin

#1 Oral Anti-acne Preparation

13We care

Science-based sales and marketing approach to build awareness of the safety and efficacy of our brands

“Science-based” sales and educational approach catering to medical customers

Overview

• Customers of branded products business include:

– Pharmacies

– Hospitals

– Clinics

– Health practitioners

– Physicians

• Direct promotion to these channels to strengthen market recognition and build brand loyalty

• Sales representatives and product consultants promote products through

– Educational seminars

– Trade shows

– Product information and promotional material

– Academic trainings

– Informational sessions for medical professionals

• Sales force includes members with a medical background

Sales and product consultants promoting Mega products

1

14We care

Leading distributor of pharmaceutical and OTC products in frontier marketsKey Distribution Markets Myanmar Vietnam Cambodia

Market Positioning

• Leading international distributor of pharmaceutical and OTC products

• Among top 2 distributors of FMCG products

• Leading international distributor of pharmaceutical and OTC products

• Leading international distributor of pharmaceutical and OTC products

Distribution Infrastructure

• 8 warehouses strategically located across Yangon, Mandalay, Mawlamyaing, Naypyidaw, Taungyyi and Lashio

• Distribute to 27,204 outlets representing c.85% geographical coverage

• 3 warehouses strategically located in Hanoi, Danang, Ho Chi Minh, with 2 feeder warehouses in Can Tho

• Distribute to 12,280 outlets across 48 out of 58 provinces

• 1 warehouse located in Phnom Penh

• Distribute to 5,700 outlets

% of Distribution Sales (2013) 63.0% 31.1% 5.8%

2

15We care

Advanced information technology systems provide valuable business intelligence for our principalsOverview

• Our advanced IT systems allow us to collect, analyse and derive business intelligence across each of our distribution markets

• We offer a broad range of value-added services, including:

– Inventory tracking systems

– Inventory management systems

– Access to valuable market data

– Real-time information sharing

• Our principals can leverage on the array of value-added services we offer in order to:

– Increase operational efficiency

– Reduce inventory cost, fulfillment cost and operational expenses

– Tailor their marketing activities to target their customers

– Improve overall efficiency of their businesses

• We believe this is a key competitive advantage and it strengthens the existing principal and customer relationships

Through our advanced IT systems we can provide value-added services to help our principals increase operational efficiency, reduce inventory cost, fulfillment cost and operational expenses, and tailor their marketing activities

Our teams collecting real time data on the field

We capture all aspects of our relationship

with customers,

providing us with current

market insights which

we use for effective sales & marketing

2

16We care

1.4%

1.8%

2.1%

2.3%

2.8%

3.5%

4.0%

19.9%

23.1%

32.7%

Philippines

Peru

Ukraine

Malaysia

Nigeria

Australia

Cambodia

Thailand

Vietnam

Myanmar

Revenue growth (‘12-’13)

We focus on fast growing developing markets…3

% Real GDP growth (‘12-’16)

6.7%

5.3%

4.6%

7.2%

3.1%

7.1%

2.4%

5.2%

6.1%

5.5%

Source: IMF, WEO Database, April 2013 | Countries with GDP growth < 5%Countries with GDP growth > 5%

28%

10%

20%

10%

(4%)

(11%)

36 %

4%

83%

45%

We have consistently grow

n faster than the markets w

e operate in

Note : Brand business in Nigeria grew by 21.0 % (‘12-’13)

17We care

58.9

23.8

6.0

ThailandVietnamMyanmar

…and Mega is well-positioned to capitaliseMyanmar’s GDP expected to witness significant growth…

Myanmar GDP at current prices in USD bns

…with a leading position in Myanmar, a key market with significant growth potential

3

53

73

2012E 2016E

…and expected to benefit a significantly underpenetrated health care market

Myanmar pharma and consumer health market size per capita (USD)

1995

10.3%

85%

8

9

63.0%

Source: IMF, WEO Database, April 2013, ADB Study 2012, Estimates based on Myanmar import customs data and Company assumptions| Note: (1) Suffix ‘E’ represents IMF estimate, (2) as at 31Dec 2013

1 1

Establishment date testament to our long-standing presence in the country

% of 2013 branded revenues (before inter-segment charges) generated in Myanmar

% of 2013 distribution revenues generated in Myanmar

# of our branded products ranked as leading brands in their respective therapeutic category

# of strategically located warehouses

Extensive distribution reach covering 85% of the country

Myanmar significantly lags behind Vietnam

and Thailand in healthcare spend

c.1,4502 # of employees in Myanmar

18We care

All of our products are made to high quality standards in world class manufacturing facilities

4

State of the art quality control laboratoryInternationally accredited manufacturing facilities

Manufacturing facilities in Australia and Thailand

These facilities are accredited and regularly inspected by:• German health authorities• Australian TGA• Thai FDA • Additional GMP

certifications from 12 countries

• Australian TGA approved since 1992• Amongst the few manufacturers globally,

who apply the same standards for the manufacturing of nutraceutical products as with pharmaceutical products

• Team of 151 professionals in our Quality Assurance and Quality Control teams to ensure our products comply with the highest quality standards

• State of the art QC laboratory with world class Quality Assurance (“QA”) systems and EU GMP standard manufacturing facilities make us amongst the leading such facility in its category in Thailand and in Southeast Asia

Internationally accredited facilities Sizeable and dedicated teams monitor quality Significant investment made into infrastructure

We manufacture our nutraceutical products to pharmaceutical standards

19We care

Product development strategy

Efficient and targeted product development strategy drives a strong product pipeline

5

Nutraceuticals

• Identify new clinically-effective and safe product candidates

• Create line extensions of existing established products

Prescription Pharmaceuticals

• Review effective pharmaceutical compounds which have been successful for major originator companies

• Products with expired or due to expire patents

OTC

• Develop products which offer the following: faster relief, are easy to use, have better formulations for self medication, and will be recommended by pharmacies

Our objective is to develop new products which offer consumers health and wellness benefits

Products - Key information as at 31 Dec 2013Existing:# of Unique formulations 195 # of Product registrations 681

Application for registrations:# of Unique formulations 71 # of Product registrations 398

# of unique product formulation under Development

75

# No of poroduct launches (Jan 2008 to Dec 2013) 103

20We care

Growing both top-line and bottom-line

CAGR (2010-2013)

Proven track record of delivering growth and profitability

6

Commentary

• Evolved from a contract manufacturer to a leading branded products and consumer health company

• Growth in branded products driven by strong brands across markets

• Growing volumes on the back of strong promotional activities

• Focus on building long term relationships with customers

• Leveraged on well established distribution infrastructure

• Increased focus on international principals

• Distribution business benefited from increased volumes from principals

19%

17%

19%

PATMI

EBIDTA

Sales

21We care

Management ably supported by other experienced in-country personnel and teams

Management1 team instrumental in building the business is significantly invested in the Company

7

Vivek DhawanChief Executive Officer and Chief coach• Joined Mega in 1986

Thomas AbrahamChief Financial Officer and

Head coach • Joined Mega in 1998

Duangnapa TongsiriPresident and Head coach, Mega We Care , Thailand

(excluding Manufacturing)• Joined Mega in 1993

Girish WadhwaPresident and Head coach,

Mega We Care and Maxxcare, Myanmar

• Joined Mega in 1997

Paramjit SinghPresident International and

Head coach ,Mega We Care and Maxxcare

(excluding Thailand , Myanmar and Manufacturing)Joined Mega in 1993

Management team has a collective history of over 100 years working with the Company

John FarleyManaging Director, Australia, 1989

Apichai ChancharusiriDirector Manufacturing, 1985

Pornchai WongpayakDirector Quality Control, 1990

1 Management designations have been changed w.e.f. 01-Jan-2014; approved in the Board meeting dated 25-Feb-2014 . SET filling in due course

22We care

Continue OEM• Helps service our long standing

customers and helps improve the productivity and efficiency of our manufacturing processes

Grow our market leading brands• Leverage brand strength and

recognition to increase demand• Expand specialised sales and

marketing team to increase our coverage of the market

Launch new branded products• Launch new products and line

extensions• Leverage on speed to market

competitive advantage

Expand distribution business• Strengthen relations with existing

principals, add new principals and invest in infrastructure

Enter new markets• Selectively enter new markets

where we can compete effectively• Identified new markets in Africa,

Middle East, CIS and South America as new frontier markets

Expand margins and profitability• Minimise manufacturing and

distribution cost inefficiencies • Improving yield on

manufacturing processes

Selective acquisitions• Selectively assess complimentary

acquisitions• For e.g. the Eugica acquisition

helped us add a leading brand to our portfolio

Future strategies

Our strategies for the branded and distribution business will drive future growth

23We care

Organization structure

The Company operates in 22 countries through 17 subsidiaries and an affiliate and 17 branch or representative offices

Mega Lifesciences Public Company Limited

(Thailand)

Mega Lifesciences Public Company Limited

(Thailand)

99.99% 99.99% 99.96%

99.99%99.99%

99.99%98.99%99.99%99.96% 99.99% 99.99%

99.99%99.99%99.99%99.99% 99.99% 49%

Natural Health Foods Ltd.

(Thailand)

Natural Health Foods Ltd.

(Thailand)

Mega Lifesciences Pty. Ltd.

(Thailand)

Mega Lifesciences Pty. Ltd.

(Thailand)

Mega We Care Ltd.(Thailand)

Mega We Care Ltd.(Thailand)

Mega Lifesciences Pty. Peru S.A.C.

(Peru)

Mega Lifesciences Pty. Peru S.A.C.

(Peru)

Mega Products (Mauritius) Ltd.

(Mauritius)

Mega Products (Mauritius) Ltd.

(Mauritius)

Mega Lifesciences Sdn. Bhd.

(Malaysia)

Mega Lifesciences Sdn. Bhd.

(Malaysia)

PT Mega Lifesciences(Indonesia)

PT Mega Lifesciences(Indonesia)

Mega Lifesciences Pty. Ltd.

(Cambodia)

Mega Lifesciences Pty. Ltd.

(Cambodia)

E-Sense Ltd.(Thailand)

E-Sense Ltd.(Thailand)

Mega Lifesciences Ltd.(Myanmar)

Mega Lifesciences Ltd.(Myanmar)

Mega Lifesciences(Vietnam) Ltd.

(Vietnam)

Mega Lifesciences(Vietnam) Ltd.

(Vietnam)

Mega LifesciencesNigeria Ltd.

(Nigeria)

Mega LifesciencesNigeria Ltd.

(Nigeria)

Mega Lifesciences Ghana Ltd.

(Ghana)

Mega Lifesciences Ghana Ltd.

(Ghana)

Mega Lifesciences Pte. Ltd.

(India)

Mega Lifesciences Pte. Ltd.

(India)

Mega Lifesciences Pte. Ltd.

(Singapore)

Mega Lifesciences Pte. Ltd.

(Singapore)

Mega Lifesciences(Australia) Pty. Ltd.

(Australia)

Mega Lifesciences(Australia) Pty. Ltd.

(Australia)

Mega Product Ltd.(Yemen)

Mega Product Ltd.(Yemen)

Note : As at 31 Dec 2013

24We care

Pre-IPO and post-IPO shareholding

7.06%20.44%0.96%58.92% 3.76% 8.86%

Existing Minority (Employees)

Existing Minority (Employees)ManagementManagementG. Prem Gee Pte.

Co., Ltd.G. Prem Gee Pte.

Co., Ltd.Unistretch

Company Ltd.Unistretch

Company Ltd.Globlex

Corporation Ltd.Globlex

Corporation Ltd. Shah FamilyShah Family

Existing Minority (Employees)

Existing Minority (Employees)ManagementManagementShah FamilyShah Family

25.00% 6.00%15.23%50.08% 0.02% 3.67%

New InvestorsNew Investors UnistretchCompany Ltd.

UnistretchCompany Ltd.

GloblexCorporation Ltd.

GloblexCorporation Ltd.

Mega Lifesciences PCLMega Lifesciences PCL

Mega Lifesciences PCLMega Lifesciences PCL

Pre – IPO shareholding

Post – IPO shareholding1

1. As at 31-Dec-2013

25We care

Our Board of Directors

10

1. Mr. Mechai Viravaidya - Chairman of the Board of Directors & Independent Director 6. Mr. Ishaan Shah – Director

2. Mr. Alan Kam - Director / Independent Director / Chairman of Audit Committee 7. Ms. Sameera Shah – Director

3. Mr. Manu SawangJaeng - Director / Independent Director / Audit Committee / Chairman of Remuneration and Nomination Committee 8 Mr. Shiraz Erach Poonevala – Director

4. Mr. Thor Santhisiri - Director / Independent Director / Audit Committee 9. Mr. Vivek Dhawan – Director / Remuneration and Nomination Committee

5. Mr. Kirit Shah - Director / Remuneration and Nomination Committee 10. Mr. Thomas Abraham – Director

1 2

34

5

67 8

9

We care

Section 3Financial OverviewFY 2013

27We care

Summarized Income Statement

1.Normalized for change in business model in Myanmar in 2012 and additional overheads in Australia in 2013.

2.Normalized for deferred tax and non- recurring expenses in 2013

All figures in THB mn 2013 2012

Operating Revenue 7,033.5 5,964.8 Gross Margin (GM) 2,959.4 2,633.3 % of GM to operating revenue 42.1% 44.1%

% of GM to operating revenue (Normalized) 142.5% 42.0%

Selling and Admin. exp (SGA) 2,235.8 1,980.0 % of SGA to operating revenue 31.8% 33.2%EBIDTA 884.5 798.3 Reported (PATMI) 624.0 577.7

Normalized2 PATMI before deferred tax adjustment 662.0 555.6

28We care

Strong growth in sales over time…

Branded products was the largest business segment

Revenue split by business segment

47.6% 47.3% 45.3% 48.4%

42.4% 43.6% 46.4% 44.9%

10.0% 9.1% 8.3% 6.7%

Brand Distribution OEM

2010 2011 2012 2013

Total revenues1 (THB mn)

4,159

4,857

5,965

7,034

2010 2011 2012 2013

1.Excludes Other Income

2.Thailand, Myanmar, Vietnam, Cambodia, Malaysia, Philippines, Indonesia and Singapore.

3 Thailand, Myanmar, Vietnam and Cambodia

Commentary

• The Company experienced growth in revenue with CAGR of 19.8% between 2010 and 2012 and a growth of 17.9% for 2013 over 2012

• Brand and distribution business continue to be major contributors to the Company’s revenue

• Southeast Asia2 and Indochina3 contribute 84.8% and 79.7% of the consolidated operating revenue in year 2013

29We care

…driven by growth in both branded products and..

Total branded products revenues1 (THB mn)

1,9782,297

2,700

3,403

2010 2011 2012 2013

Thailand is our largest market

Revenue split by geography

Commentary

• Thailand contributed the largest portion of revenue from brand business followed by Vietnam and Myanmar

• All key markets have continued to grow significantly in 2013. The low per capita consumption and penetration levels for our products in these markets as compared to developed markets enabled us to sustain the good growth rates by expanding the user base

• Indochina contributed approximately 69% of total brand business revenue for 2013

• Southeast Asia contributed approximately 79% of total brand business revenue for 2013

36.7% 35.8% 37.3% 37.0%

21.9% 18.8% 17.9% 19.2%

10.9% 14.6% 10.1% 9.6%

30.5% 30.8% 34.7% 34.2%

Thailand Vietnam Myanmar Others

2010 2011 2012 2013

1. After inter-segment charge (expense incurred by brand business for distribution of branded product, which will be booked as revenue under distribution business)

30We care

…distribution business revenues

Total distribution business revenues1 (THB mn)

1,765

2,117

2,767

3,157

2010 2011 2012 2013

Myanmar is our largest distribution market

Revenue split by geography

40.7%49.1% 55.0% 63.0%

45.5%41.5% 36.0%

31.1%

8.9% 6.8% 6.8% 5.9%4.9% 2.7% 2.1%

Myanmar Vietnam Cambodia Nigeria

2010 2011 2012 2013

Commentary

• All of Mega’s revenue from distribution business is derived from outside of Thailand• CAGR between 2010 and 2012 was 25.2% • Distribution revenue from Myanmar has experienced strong growth, with CAGR of over 45% between 2010 and 2012• The revenue growth of 14.1% between 2012 to 2013 is impacted by the change in distribution model with one of our principal in

Myanmar• Other factors which impacted growth in 2013 were that the revenue from new principals added is yet to stabilize and these incremental

revenues couldn’t fully compensate the discontinuance of certain principals in Nigeria & Vietnam

1.After inter-segment charge (expense incurred by brand business for distribution of branded product, which is booked as revenue under distribution business)

31We care

Commentary

• Normalized Gross margin in 2013 has moved in tandem with revenue growth

• Reported Gross margin slightly declined from 44.1% in 2012 to 42.1% in 2013 mainly due to the change in business model for one of our Principals in Myanmar as well as the additional overheads incurred in Australia due to the temporary stoppage of production for shifting to the newly constructed plant . Normalized for the above impact, Gross margins remained stable at 42% approximately.

• Comparison of PATMI before and after deferred tax impact and the normalized 1PATMI after adjusting for non-regular expenses are as follows

2,011

2,309

2,633

2,959

2010 2011 2012 2013

Profit after tax and minority interest (PATMI) (THB mn)

368

456

578624

2010 2011 2012 2013

Profits have grown in tandem with Sales

Gross Margin ( THB mn)

1. Normalized for deferred tax and non- recurring expenses in Australia (due to plant closure ) and IPO related expenses in 2013

All figures in THB mn 2013 2012 %Gr

Normalized1 PATMI before deferred tax

662.0 555.6 19.1%

PATMI before deferred tax adjustment 631.9 555.6 13.7%

Reported PATMI 624.0 577.7 8.0%

32We care

Branded products business – high and stable gross margins

468 529 592826

116152

202

216

117149

173

208

Raw Materials Direct Labor Overhead2010 2011 2012 2013

Gross Margin (THB mn) and margin (%) Commentary

• Growth in gross profits have tracked growth in sales – resulting in steady gross margins between c.63-65%

• Our steady gross margins reflect our ability to maintain the prices of our products while simultaneously controlling our costs

• Raw material costs contributed more than 60.0% of the total COGS and their proportion varies depending on product mix

1,2771,467

1,7342,154

64.5% 63.9% 64.2% 63.3%

0%

10%

20%

30%

40%

50%

60%

70%

0200400600800

1,0001,2001,4001,6001,8002,0002,2002,400

2010 2011 2012 2013

16.7% 16.6%

66.7%

17.9%

18.3%

63.8%

17.9%

20.9%

61.3%

16.6%

17.3%

66.1%

Note: Percentages denote respective item’s contribution as a % of total COGS

701

830966

1,249

Raw materials is the largest direct costCOGS break down (THB mn)

33We care

Distribution business – Gross margins have remained stable on a normalized basis

Profitability of our distribution business has remained stableGross Margin (THB mn)

623

733781

725

0

200

400

600

800

1,000

2010 2011 2012 2013

Commentary

• Reduction in Gross margin in absolute terms in 2013 is due to change in product/principal mix; however net margins as a % of fee earned remains steady

• Net margin (reflecting the gross fee earned by the distribution business net off distribution expenses) has remained steady over the years.

• Normalized Gross margin reflects the Gross fee earned by distribution business adjusted for the impact of change in business model for one of our principals in Myanmar. Change in normalized Gross margin reflects change in product/principal mix.

26.4% 25.4%23.0%

36.3% 35.4%

34.8%

0.0%

10.0%

20.0%

30.0%

40.0%

Reported gross margin Normalized gross margin Net Margin

2011 2012 2013

34We care

OEM business – financial overview

Raw materials is the largest direct cost element

COGS break down (THB mn)

Gross profit (THB mn) and margin (%)

185 193226 218

7490

107 1104651

47 64

Raw Materials Direct Labor Overhead

2010 2011 2012 2013

Total OEM revenues (THB mn)

15.1%

24.2%

60.8%

15.2%26.9%

12.3%

28.2%

59.4%

16.4%

28.1%

55.5%

Note: Percentages denote respective item’s contribution as a % of total COGSCommentary

• OEM revenue are mainly from customers in Thailand and Australia

• In 2013 Gross margin declined to 17.0% from 23.8% because of additional overheads incurred in Australia due to temporary stoppage of production for shifting to the newly constructed plant.

• Gross margin (post adjustment of additional overheads ) in 2013 was 23.4%.

112 109 118

81

26.8%24.7% 23.8%

17.0%

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

140

2010 2011 2012 2013

Decline due to relocation of plant

in Australia

417 443498 473

2010 2011 2012 2013

26.9%

57.9%

305334

379 392

Decline due to relocation of plant

in Australia

35We care

Selling and administrative expenses – benefitting from increased scale

S&A expense has reduced as a % of total sales

35.1% 36.1%33.2% 31.8%

19.7%22.3%

19.3% 19.5%

15.4% 13.9% 13.9%12.3%

Selling & Admin Expenses (% of Sales)Selling Expense (% of Sales)Admin Expense (% of Sales)

2010 2011 2012 2013

Advertising is the largest component of selling expenses

Selling expenses (THB mn)

529695 653

833

170

220 308

353

41

6489

86

80

103103

100

Advertising Personnel Freight expense Others

5.0%20.7%

64.5%

5.9%20.4%

64.2%

7.7%

26.7%

56.7%

6.3%

25.7%

60.7%

9.8%

9.5%8.9%

7.3%

820.4

1,082.21,153.0

1,372.6c.3.3%

reduction since 2010

Personnel costs is the largest component of admin expenses

Administrative expenses (THB mn)

289.9 350.3 423.3 418.6 47.9

59.7 113.9 118.0 303.1

263.6

289.9 326.6

Personnel Travel & Trans. Others

2010 2011 2012 2013

47.3%

7.5%

45.2%

39.1%

8.9%

52.0%

35.1%

13.8%

51.2%

37.8%

13.7%

48.5%

640.9 673.6

827.0 863.1

Commentary

• On an overall basis , selling and administrative has continuously declined reflecting economies of scale

• Advertising comprised the largest of all selling expenses

• In 2013, the Company spent THB 833.1 mn (as against to THB 653.3 mn in 2012) as advertising costs to expand the market and further business

• Approximately 20% - 27% of selling expenses are human resources expenses related to sale force

2010 2011 2012 2013

36We care

Balance sheet and capex summary – significant investments already incurred to boost capacity

Total liabilities and equity (THB mn)Total assets (THB mn)

101 330 3541,540929

1,386 1,288

1,724

688

904 1,442

1,685

362

368

733

970

141

301

515

617

Cash AR Inventories PPE Others

2010 2011 2012 2013

2,221

3,290

4,332

6,536

566 738 1,198 997480

787769 1,145

289446

654 702

885

1,318

1,710

3,693

Debt AP Other liabilities Equities

2010 2011 2012 2013

2,221

3,290

4,332

6,536

IBD/E 0.64x 0.56x 0.70x 0.27x

Commentary

• In 2013, the Company invested for expansion of manufacturing facilities in Thailand and Australia

• Rise in equities was driven by fresh issue of ordinary shares as part of IPO

• Mega’s current manufacturing capacity will be sufficient for its businesses for the next 3 – 5 years

Capital expenditure in THB mn

3080

439

352

2010 2011 2012 2013 Note : Balance sheets elements of previous years are based on restated financials

37We care

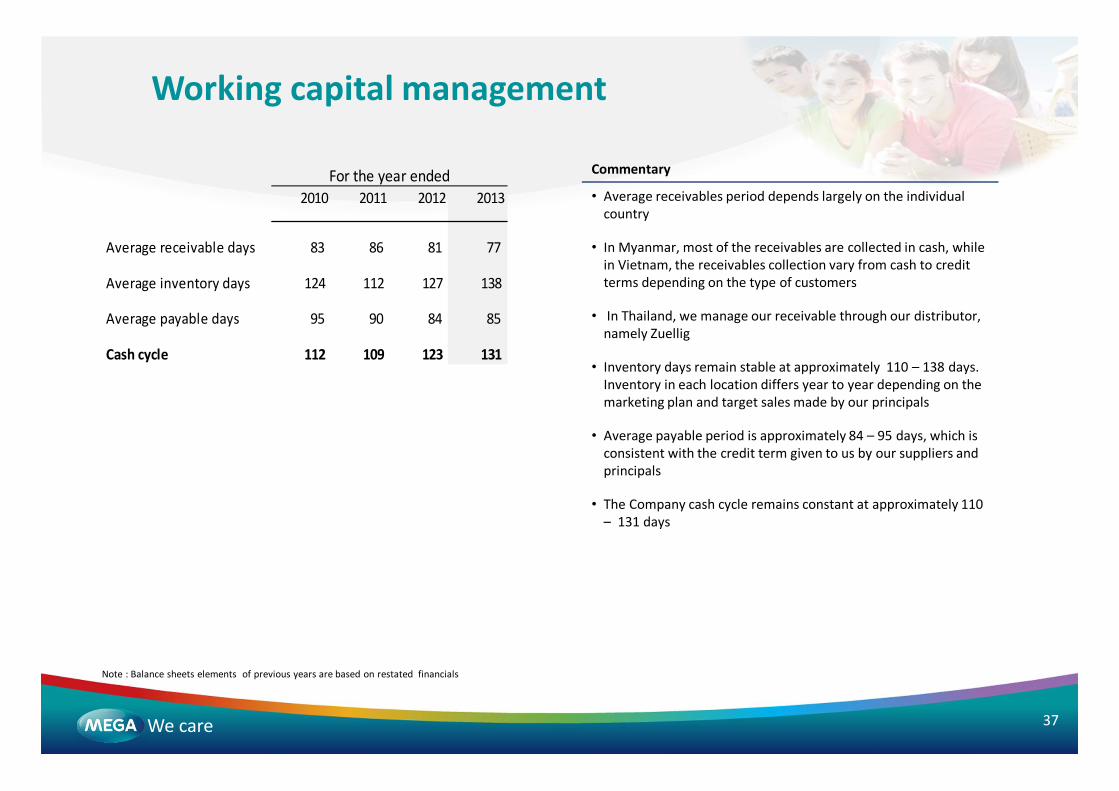

Working capital management

Commentary

• Average receivables period depends largely on the individual country

• In Myanmar, most of the receivables are collected in cash, while in Vietnam, the receivables collection vary from cash to credit terms depending on the type of customers

• In Thailand, we manage our receivable through our distributor, namely Zuellig

• Inventory days remain stable at approximately 110 – 138 days. Inventory in each location differs year to year depending on the marketing plan and target sales made by our principals

• Average payable period is approximately 84 – 95 days, which is consistent with the credit term given to us by our suppliers and principals

• The Company cash cycle remains constant at approximately 110 – 131 days

Note : Balance sheets elements of previous years are based on restated financials

2010 2011 2012 2013

Average receivable days 83 86 81 77

Average inventory days 124 112 127 138

Average payable days 95 90 84 85

Cash cycle 112 109 123 131

For the year ended

38We care

Strong operating cash flow generationCash flows from operations, investments and financing activities (THB mn)

Commentary

Operation continued to generate strong operating cash flows . Net cash from operations increased by 36.1% to THB 465.8 mn in 2013

In FY2013, net cash used in investing activities was THB 396.2 mm; the spent was driven by investment of THB 352.0 mn. in new property, plant, and equipment, which mainly include the expansion of production lines at our manufacturing facilities in Thailand which accounted for THB 256.7 million and the expansion of manufacturing facilities in Australia which accounted for THB 43.2 mn

In FY2013, net cash generated from financing activities was THB 1.10 billion, which mainly came from IPO issue of 129.79 mn ordinary shares of THB 17.5 per share amounting to THB 2.27 billion . Part of IPO proceeds were used for the repayment of term loans and working capital loans from financial institution amounting to THB 1.14 billion.

336 267

342 466

-37 -77

-626

-396(273)

40

304

1,103

26229

20

1,172

Operating cashflow Net cash from (used in) investing activities Net cash from (used in) financing activities Net change in cash

2010 2011 2012 2013

39We care

Taxation and BOI privileges

Board of Investment (“BOI”) privileges

• Exemption from corporate income tax on the net profits derived from the promoted activity (Manufacture of Drugs for Human use) in Thailand

• The amount of tax exemption is not to exceed 100 percent of the total investment (THB339.8 mn), excluding land costs and working capital ; THB 50.1 mn already used

• The period of exemption is for 5 years from the date such income is first derived (Aug 2012 to July 2017)

• Exemption from payment of imported duties on machinery as being approved by BOI and the import should be before Jan 2015

• Exemption from import duties on raw and essential materials imported for use in producing to export, for period of one year after the first import

• Exemption from import duties on items which are imported for re-export, period of one year after the first import

• Exemption from tax on dividend distributed from profits of promoted activity for a period of 5 years (Aug 2012 to July 2017)

Exemption from corporate income tax on profits from the manufacture of drugs in Thailand, for a period of 5 years and for a maximum amount of THB339.8mn (of which THB 59.3 mn has already been used)

(1) The company adopted Thai Accounting Standard for deferred tax (TAS 12) in 2013 with retrospective effect.

1

THB mn 2010 2011 2012 2013

Profit before tax 462.3 565.7 698.3 757.4

Current tax 92.6 107.4 141.2 125.5

Deferred tax - - (22.1) 7.9

Total tax expenses 92.6 107.4 119.1 133.4

Effective tax rate ( before deferred tax) 20.0% 19.0% 20.2% 16.6%

Effective tax rate ( after deferred tax) 20.0% 19.0% 17.1% 17.6%

For the year ended

40We care

Key financial elements

2010 2011 2012 2013

Return on assets (%) 15.8% 16.6% 15.2% 11.5%

Return on equity (%) 47.4% 41.6% 38.2% 23.1%

Debt to equity (times) 1.51 1.50 1.53 0.77

Interest bearing debt to equity (times) 0.64 0.56 0.70 0.27

Earning per share (THB)1 0.43 0.63 0.79 0.84

Note: Number of outstanding equity shares for 2010 ,2011 and 2012 have been adjusted for share split and issue of stock dividend made in 2013

41We care

927 1,093 1,280 1,361

10931,245

1,535 1,803 811

838

947 1,062

1819

23

27

Mega We Care Maxxcare Manufacturing Corporate/Others

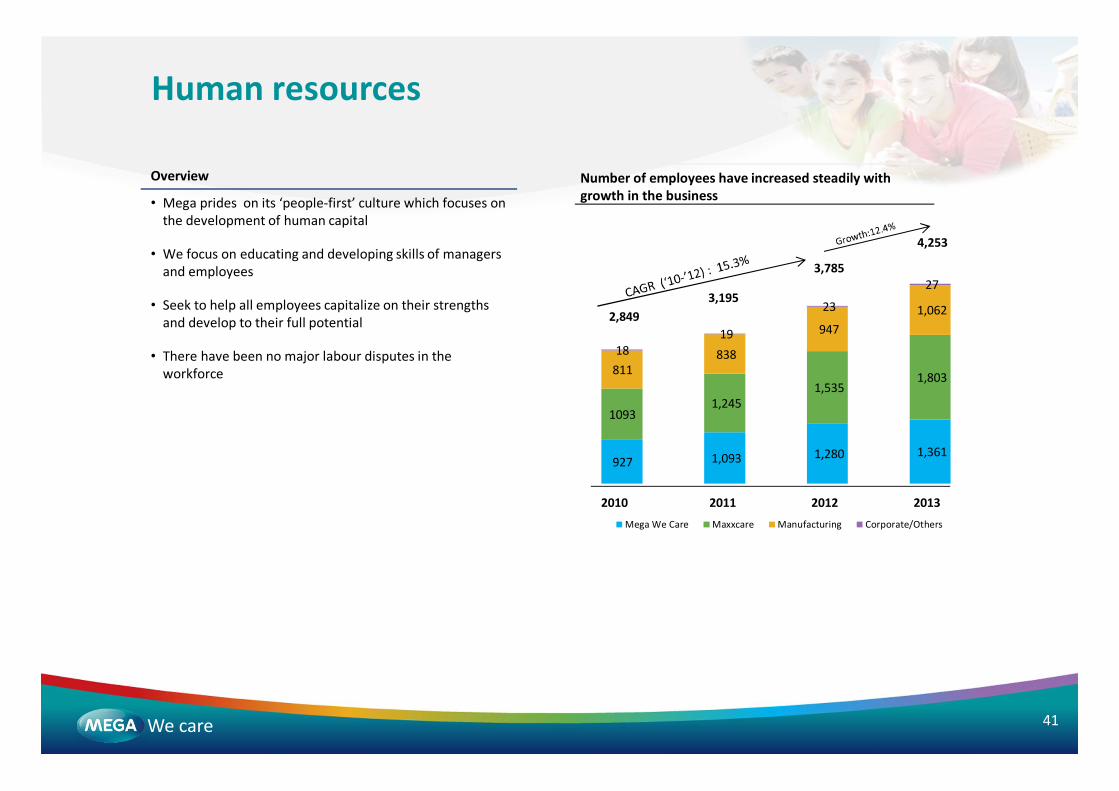

Number of employees have increased steadily with growth in the business

Human resources

Overview

• Mega prides on its ‘people-first’ culture which focuses on the development of human capital

• We focus on educating and developing skills of managers and employees

• Seek to help all employees capitalize on their strengths and develop to their full potential

• There have been no major labour disputes in the workforce

2,8493,195

3,785

4,253

2010 2011 2012 2013