Meeting the Challenge: Maintaining System Reliability While Meeting Both Economic System Performance...

29

NOVEMBER 4, 2014 | LAS VEGAS, NV Michael I. Henderson DIRECTOR, REGIONAL PLANNING & COORDINATION Transmission & Distribution Summit Improving Transmission Reliability in a Highly Changing Marketplace

-

Upload

marcus-evans -

Category

Business

-

view

166 -

download

1

Transcript of Meeting the Challenge: Maintaining System Reliability While Meeting Both Economic System Performance...

N O V E M B E R 4 , 2 0 1 4 | L A S V E G A S , N V

Michael I. Henderson D I R E C T O R , R E G I O N A L P L A N N I N G & C O O R D I N A T I O N

Transmission & Distribution Summit

Improving Transmission Reliability in a Highly Changing Marketplace

About ISO New England

2

• Private not-for-profit

• Regulated by the federal government

• Independent of companies doing business in market

• Primary Responsibilities – Operate the regional power system – Administer wholesale electricity markets – Power system planning

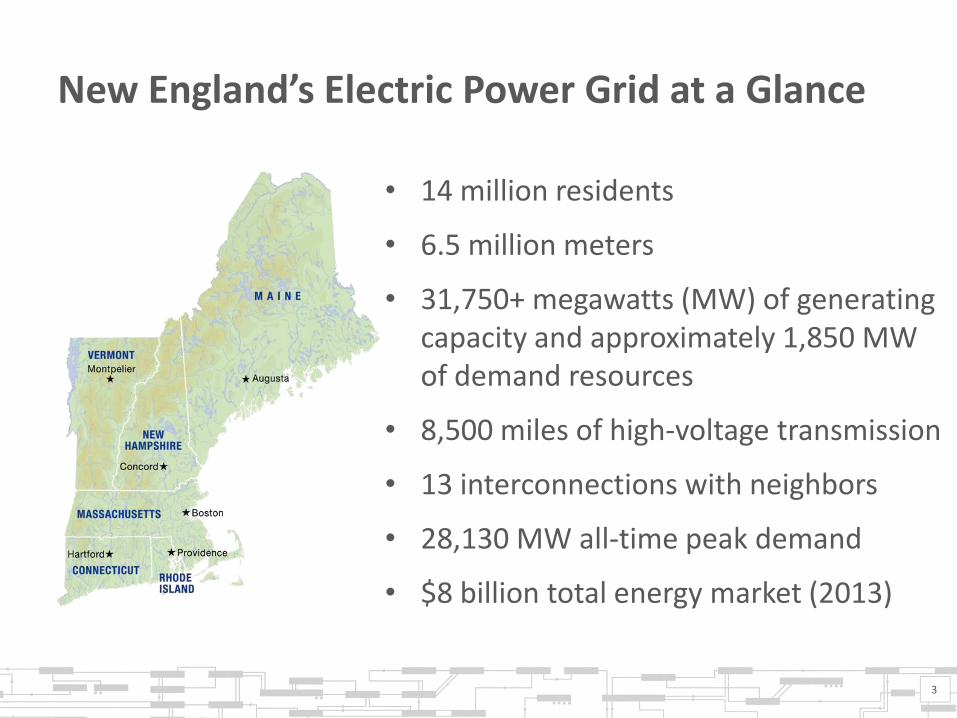

New England’s Electric Power Grid at a Glance

• 14 million residents

• 6.5 million meters

• 31,750+ megawatts (MW) of generating capacity and approximately 1,850 MW of demand resources

• 8,500 miles of high-voltage transmission

• 13 interconnections with neighbors

• 28,130 MW all-time peak demand

• $8 billion total energy market (2013)

3

Outline

• Order 1000

• Recent transmission investment

• Cost allocation

• Renewable policies and generator interconnection queue

• Challenges for the development of transmission in remote area (such as in Maine for wind)

• Illustration of elective transmission projects

• Reliance on natural gas

• Retirements

• Strategic Transmission Analysis

4

Order 1000 Process – Awaiting Final FERC Order

• New England region conducted numerous stakeholder meetings to discuss compliance with new requirements

2012-2013

• Addressed interregional planning requirements

• ISO built on the Planning Coordination Protocol

• Interregional cost allocation

July 10, 2013 Compliance Filing

• States that the region must “identify” and “consider” transmission plans in response to state and federal public policies, which may drive the need for transmission

• Removes arrangements that protect the right of first refusal (ROFR) in federal documents for incumbent transmission providers

November 15, 2013 Compliance Filing

5

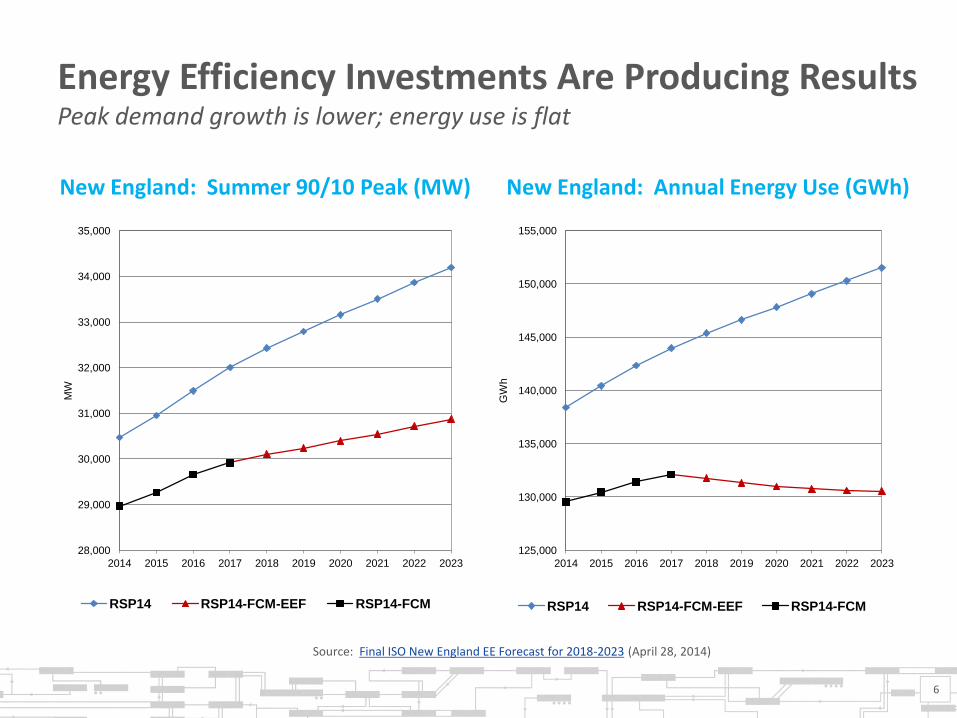

Energy Efficiency Investments Are Producing Results Peak demand growth is lower; energy use is flat

New England: Annual Energy Use (GWh) New England: Summer 90/10 Peak (MW)

Source: Final ISO New England EE Forecast for 2018-2023 (April 28, 2014)

28,000

29,000

30,000

31,000

32,000

33,000

34,000

35,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

MW

RSP14 RSP14-FCM-EEF RSP14-FCM

125,000

130,000

135,000

140,000

145,000

150,000

155,000

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

GW

h

RSP14 RSP14-FCM-EEF RSP14-FCM

6

Transmission Upgrades in New England

Generally Funded by

Entity Proposing Project

Funded by Region,

Localized Costs

Excluded

EXISTING

Generation Interconnection 100%

Elective Transmission 100%

Merchant Transmission 100%

Local Benefit Upgrades/ Localized Costs 100%

Regional Benefit Upgrades (Reliability & Market Efficiency) 100%

PROPOSED

Regional Benefit Upgrades (Public Policy)* *Order 1000 Compliance Filing Pending

30% 70%

7

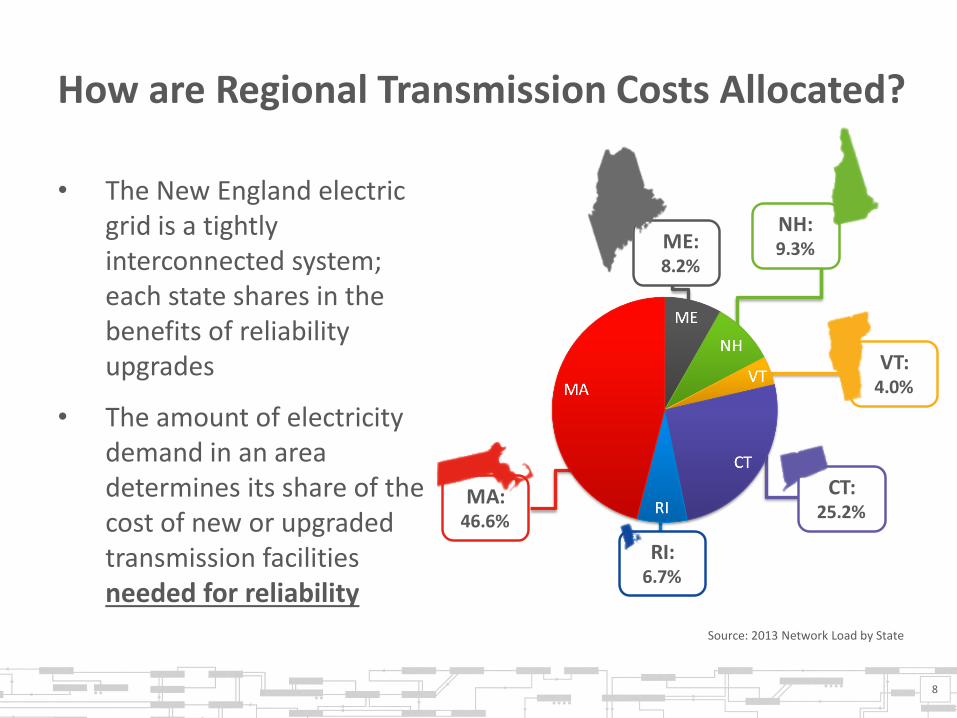

How are Regional Transmission Costs Allocated?

8

• The New England electric grid is a tightly interconnected system; each state shares in the benefits of reliability upgrades

• The amount of electricity demand in an area determines its share of the cost of new or upgraded transmission facilities needed for reliability

Source: 2013 Network Load by State

ME:8.2%

RI:6.7%

MA:46.6%

NH:9.3%

VT:4.0%

CT:25.2%

9

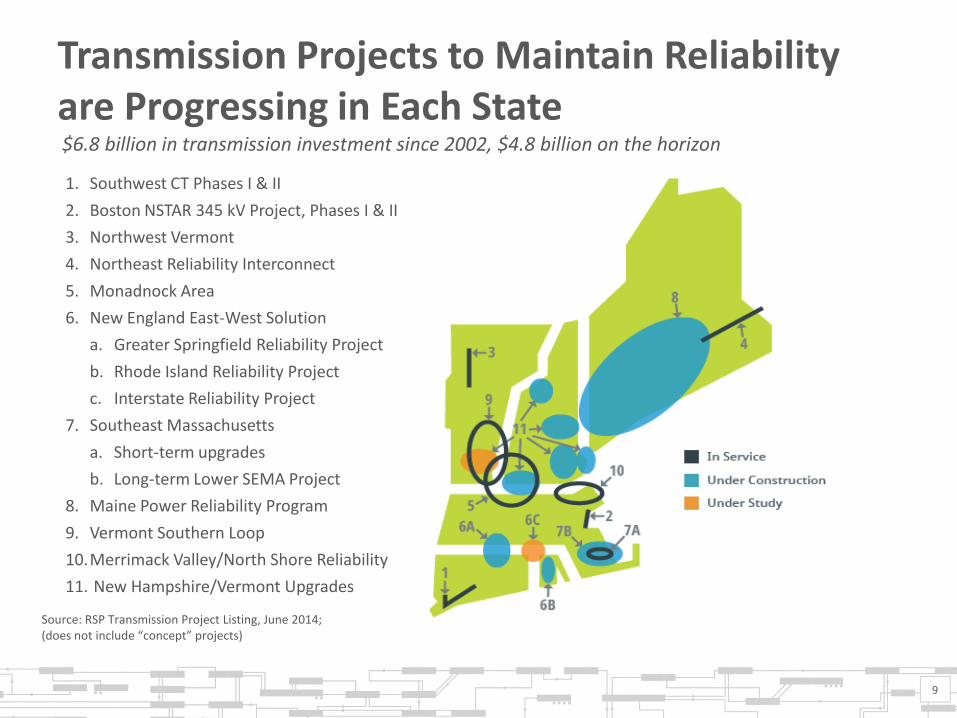

1. Southwest CT Phases I & II

2. Boston NSTAR 345 kV Project, Phases I & II

3. Northwest Vermont

4. Northeast Reliability Interconnect

5. Monadnock Area

6. New England East-West Solution

a. Greater Springfield Reliability Project

b. Rhode Island Reliability Project

c. Interstate Reliability Project

7. Southeast Massachusetts

a. Short-term upgrades

b. Long-term Lower SEMA Project

8. Maine Power Reliability Program

9. Vermont Southern Loop

10.Merrimack Valley/North Shore Reliability

11. New Hampshire/Vermont Upgrades

Transmission Projects to Maintain Reliability are Progressing in Each State $6.8 billion in transmission investment since 2002, $4.8 billion on the horizon

Source: RSP Transmission Project Listing, June 2014; (does not include “concept” projects)

Region Has Seen Growth in Wind Development

• Aggressive renewable portfolio standards and public policies have helped stimulate wind development

• 800 MW of large scale wind have begun commercial operation

• Additional efforts underway to: – Improve wind power forecasting tools – Allow negative bidding in energy market

(December 2014)

10

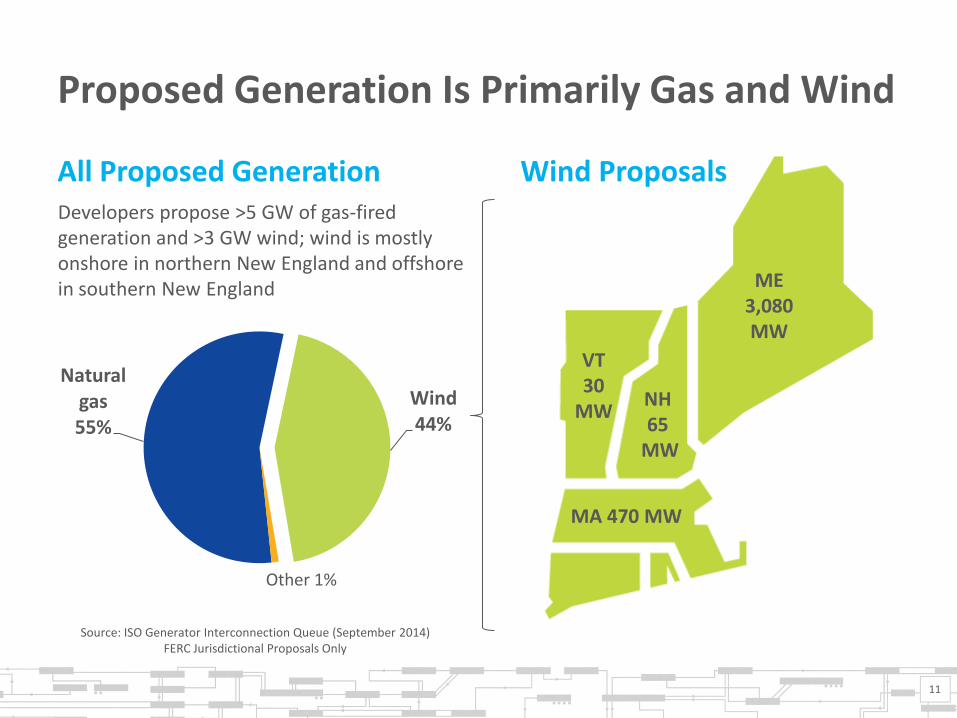

MA 480 MW

ME 3,080 MW

NH 65

MW

VT 30

MW

All Proposed Generation

11

Developers propose >5 GW of gas-fired generation and >3 GW wind; wind is mostly onshore in northern New England and offshore in southern New England

Wind Proposals

Proposed Generation Is Primarily Gas and Wind

Source: ISO Generator Interconnection Queue (September 2014) FERC Jurisdictional Proposals Only

ME 3,080 MW

NH 65

MW

VT 30

MW

MA 470 MW

Natural gas 55%

Wind 44%

Other 1%

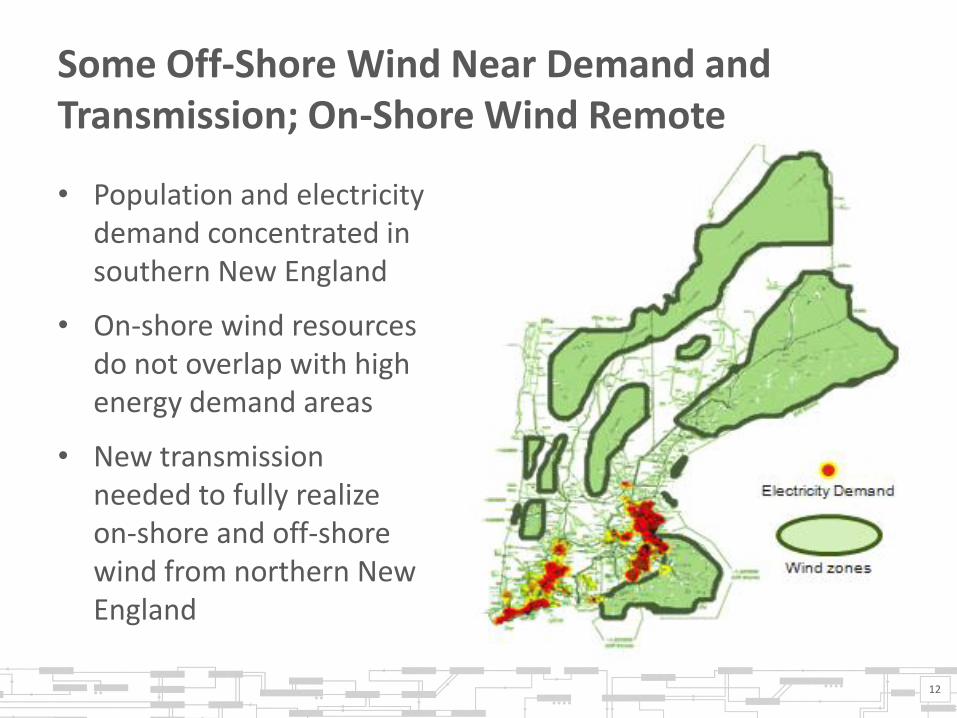

Some Off-Shore Wind Near Demand and Transmission; On-Shore Wind Remote

• Population and electricity demand concentrated in southern New England

• On-shore wind resources do not overlap with high energy demand areas

• New transmission needed to fully realize on-shore and off-shore wind from northern New England

12

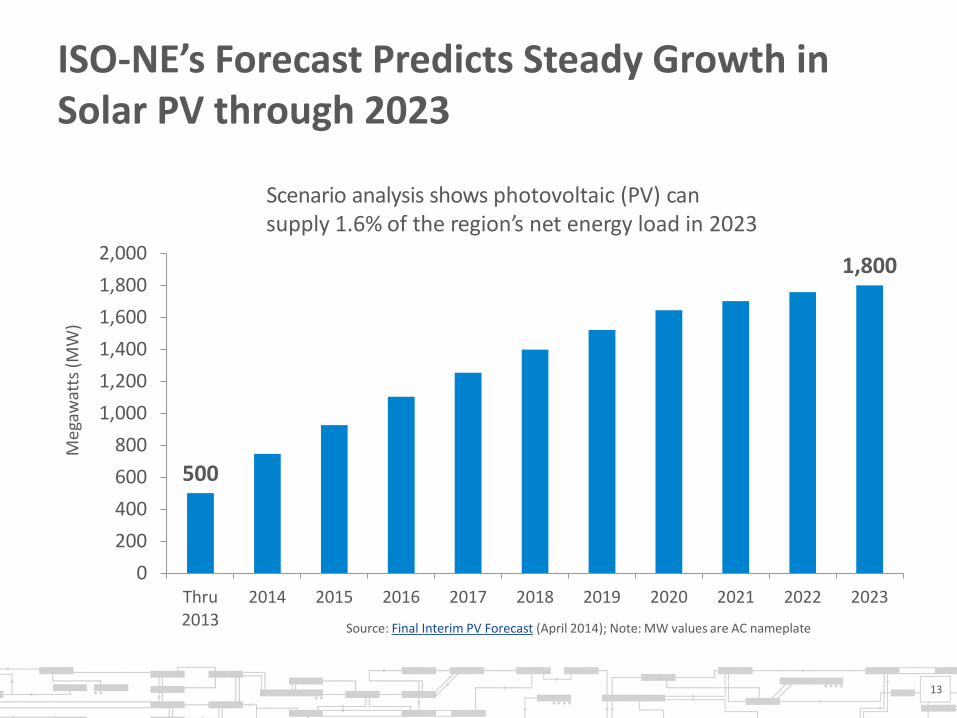

ISO-NE’s Forecast Predicts Steady Growth in Solar PV through 2023

500

1,800

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Thru 2013

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Meg

awat

ts (

MW

)

Source: Final Interim PV Forecast (April 2014); Note: MW values are AC nameplate

13

Scenario analysis shows photovoltaic (PV) can supply 1.6% of the region’s net energy load in 2023

Current State PV Interconnection Standards Pose Potential Reliability Concerns

• ISO is working with stakeholder groups to recommend changes to these standards to allow for: – Voltage ride-through – Frequency ride-through – Voltage support – Ramp rates – Soft-start capability

• All of these functionalities could be achieved with minor changes to existing inverter technology

14

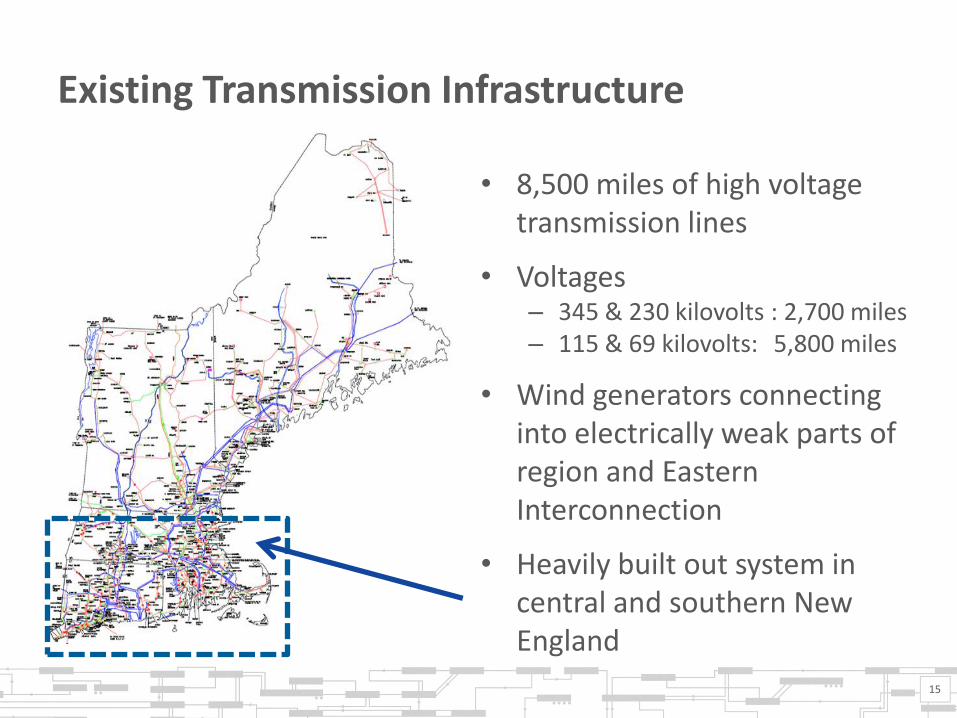

Existing Transmission Infrastructure

• 8,500 miles of high voltage transmission lines

• Voltages – 345 & 230 kilovolts : 2,700 miles – 115 & 69 kilovolts: 5,800 miles

• Wind generators connecting into electrically weak parts of region and Eastern Interconnection

• Heavily built out system in central and southern New England

15

Distances to New England Hub

• Greater distances require greater investment to get power to hub

• Off-shore wind resources in southern New England have shorter distances than resources in northern New England to get power to load

16

450 miles

250 miles

100 miles

17

a. Northern Pass – Hydro Quebec/Northeast Utilities

b. Northeast Energy Link – Emera Maine/National Grid

c. Green Line – New England ITC

d. Bay State Offshore Wind Transmission System – Anbaric Transmission

e. Northeast Energy Corridor – Maine/New Brunswick/Irving

f. Muskrat Falls/Lower Churchill – Nalcor Energy

g. Maine Yankee–Greater Boston h. Maine–Greater Boston i. Northern Maine–New England j. Plattsburgh, NY–New Haven, VT k. New England Clean Power Link – TDI New England

Representative Projects and Concept Proposals

November 2013: Publicly available information

On- and Off-shore Transmission Proposals are Vying to Move Renewable Energy to New England Load Centers

New England Flexible Alternating Current Transmission Systems (FACTS)

18

HVDC VSC HVDC

A Highgate

D Cross Sound Cable B Comerford (Retired)

C Sandy Pond (Phase II)

SVC STATCOM

E Chester G Essex

F Barnstable H Glenbrook

DVAR Synchronous Condensor

I Stony Hill (2) M Granite (4)

J Bates Rock Planned Dynamic Devices

Generators in Northern VT and Western Maine

K Kibby (2)

L Granite Wind

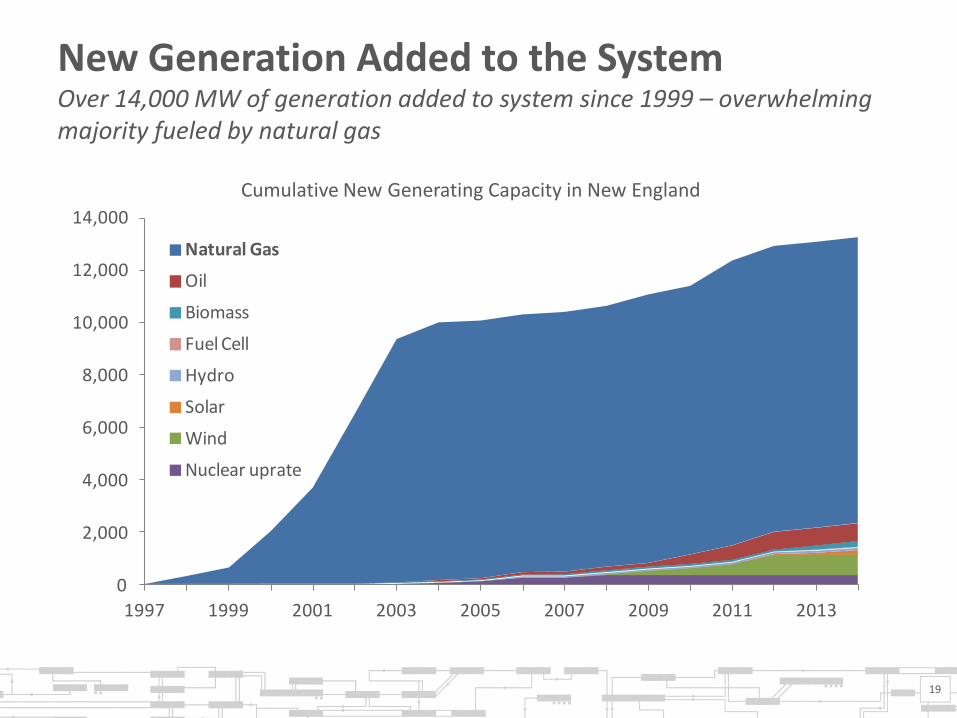

New Generation Added to the System Over 14,000 MW of generation added to system since 1999 – overwhelming majority fueled by natural gas

19

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1997 1999 2001 2003 2005 2007 2009 2011 2013

Natural Gas

Oil

Biomass

Fuel Cell

Hydro

Solar

Wind

Nuclear uprate

Cumulative New Generating Capacity in New England

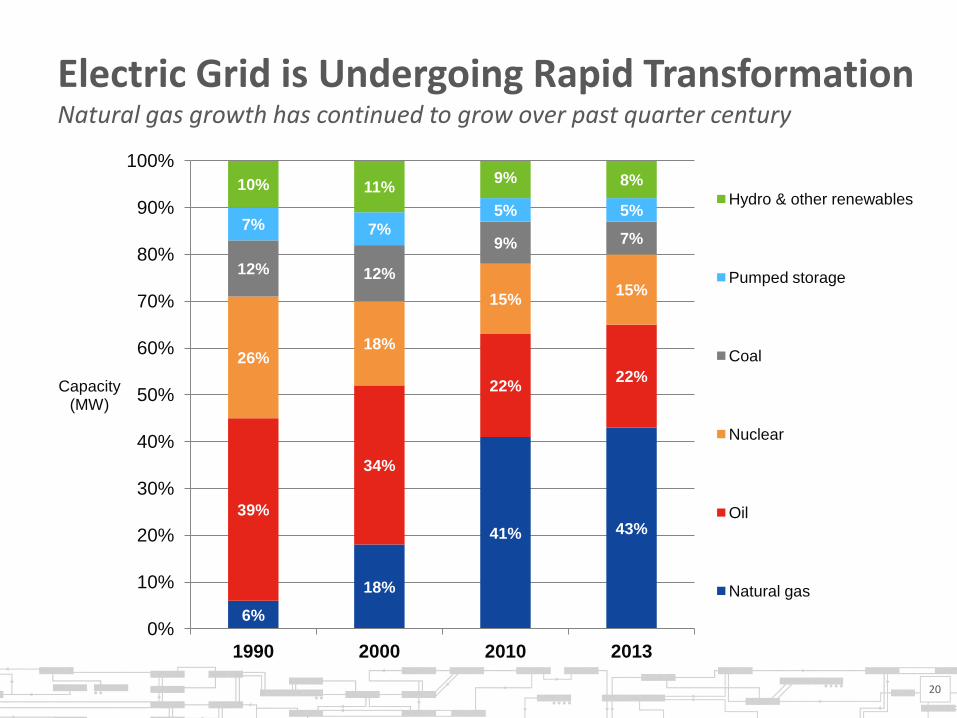

Electric Grid is Undergoing Rapid Transformation Natural gas growth has continued to grow over past quarter century

20

6%

18%

41% 43%

39%

34%

22% 22%

26% 18%

15% 15%

12% 12%

9% 7% 7% 7%

5% 5%

10% 11% 9% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 2000 2010 2013

Capacity (MW)

Hydro & other renewables

Pumped storage

Coal

Nuclear

Oil

Natural gas

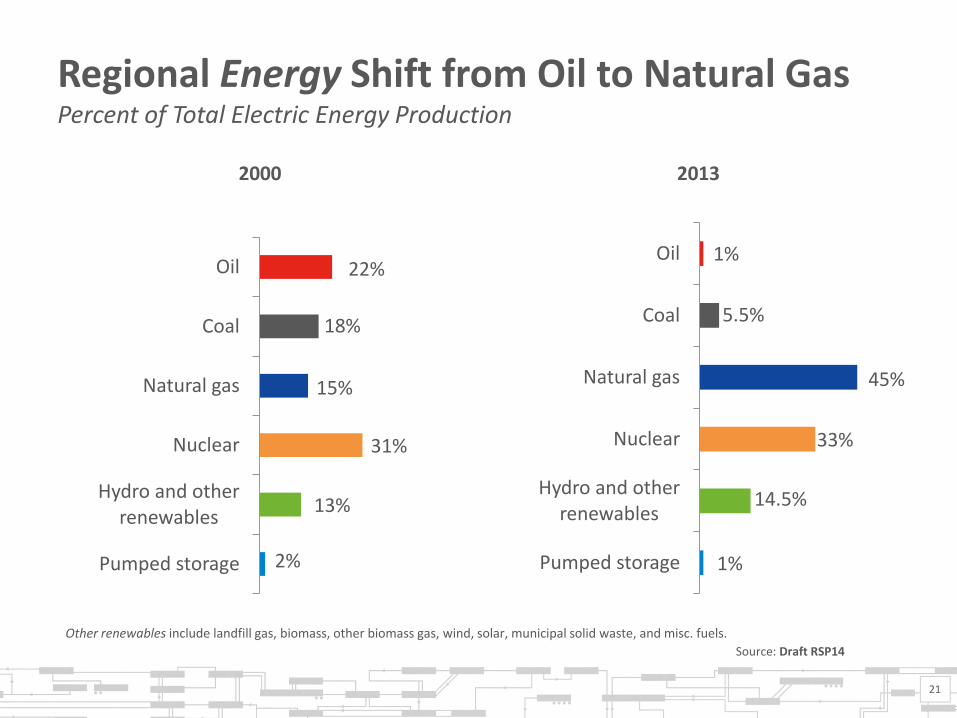

Regional Energy Shift from Oil to Natural Gas Percent of Total Electric Energy Production

2%

13%

31%

15%

18%

22%

Pumped storage

Hydro and other renewables

Nuclear

Natural gas

Coal

Oil

2000

1%

14.5%

33%

45%

5.5%

Pumped storage

Hydro and other renewables

Nuclear

Natural gas

Coal

Oil

2013

21

Other renewables include landfill gas, biomass, other biomass gas, wind, solar, municipal solid waste, and misc. fuels.

Source: Draft RSP14

1%

Pipeline Constraints into New England Cause High Prices and Reliability Issues

22

Source: The Hartford Courant, December 2013

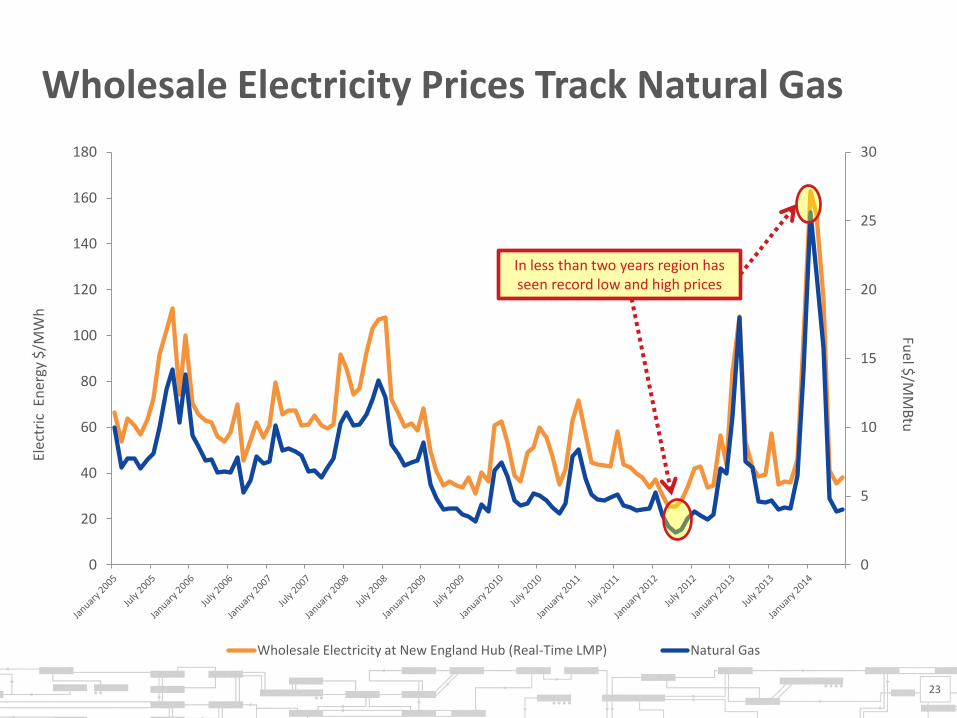

Wholesale Electricity Prices Track Natural Gas

23

0

5

10

15

20

25

30

0

20

40

60

80

100

120

140

160

180

Wholesale Electricity at New England Hub (Real-Time LMP) Natural Gas

Ele

ctri

c E

ner

gy $

/MW

h

Fuel $

/MM

Btu

In less than two years region has seen record low and high prices

Environmental Issues and Renewable Integration

24

• Challenges facing new and existing generation

– Over the past decade, average and marginal emissions rates have declined, in part due to the region’s increased use of natural gas

– Higher operating costs, reduced capacity or energy production

– Additional capital improvements and resource retirements

– Increased use of natural-gas-fired generation is likely

– Relicensing of nuclear and hydro facilities could reduce output and flexibility

• Public policy and regulation are driving the development of renewable resources, energy efficiency, and distributed generation

• Wind projects that interconnect to weak portions of the system are at risk of curtailment unless the transmission system is expanded

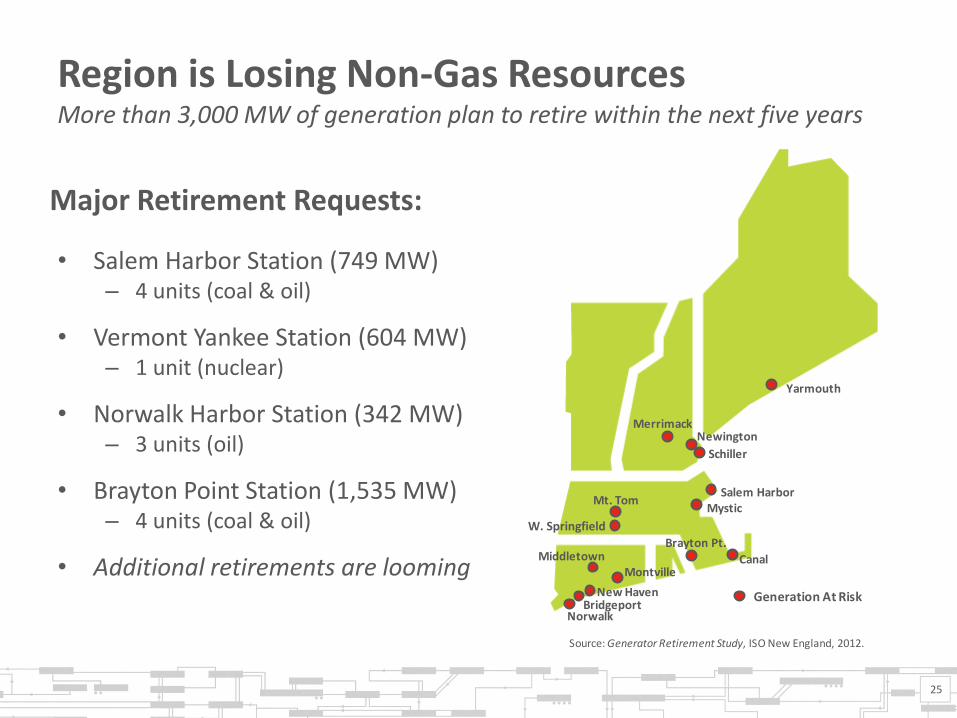

Region is Losing Non-Gas Resources More than 3,000 MW of generation plan to retire within the next five years

• Salem Harbor Station (749 MW) – 4 units (coal & oil)

• Vermont Yankee Station (604 MW) – 1 unit (nuclear)

• Norwalk Harbor Station (342 MW) – 3 units (oil)

• Brayton Point Station (1,535 MW) – 4 units (coal & oil)

• Additional retirements are looming

Major Retirement Requests:

25

Generation At Risk

Source: Generator Retirement Study, ISO New England, 2012.

Yarmouth

Newington

Schiller

Merrimack

Mt. Tom

Brayton Pt.

Canal

MysticSalem Harbor

BridgeportNorwalk

New Haven

MiddletownMontville

Generation At Risk

Source: Generator Retirement Study, ISO New England, 2012.

W. Springfield

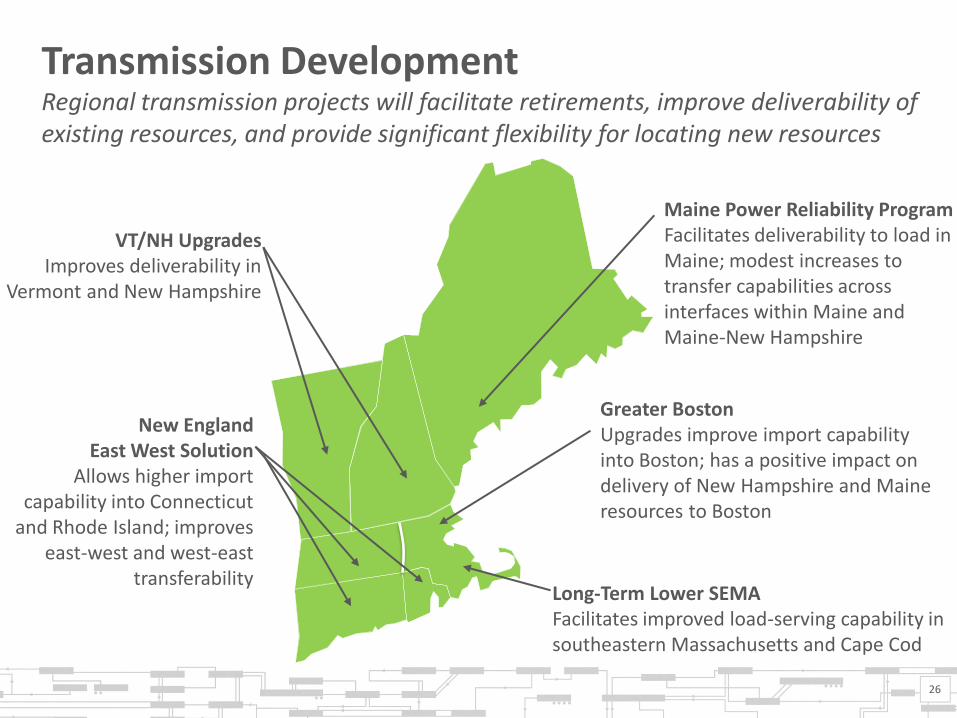

VT/NH Upgrades

Improves deliverability in Vermont and New Hampshire

Long-Term Lower SEMA Facilitates improved load-serving capability in southeastern Massachusetts and Cape Cod

Greater Boston Upgrades improve import capability into Boston; has a positive impact on delivery of New Hampshire and Maine resources to Boston

Maine Power Reliability Program Facilitates deliverability to load in Maine; modest increases to transfer capabilities across interfaces within Maine and Maine-New Hampshire

Transmission Development Regional transmission projects will facilitate retirements, improve deliverability of existing resources, and provide significant flexibility for locating new resources

New England East West Solution

Allows higher import capability into Connecticut

and Rhode Island; improves east-west and west-east

transferability

26

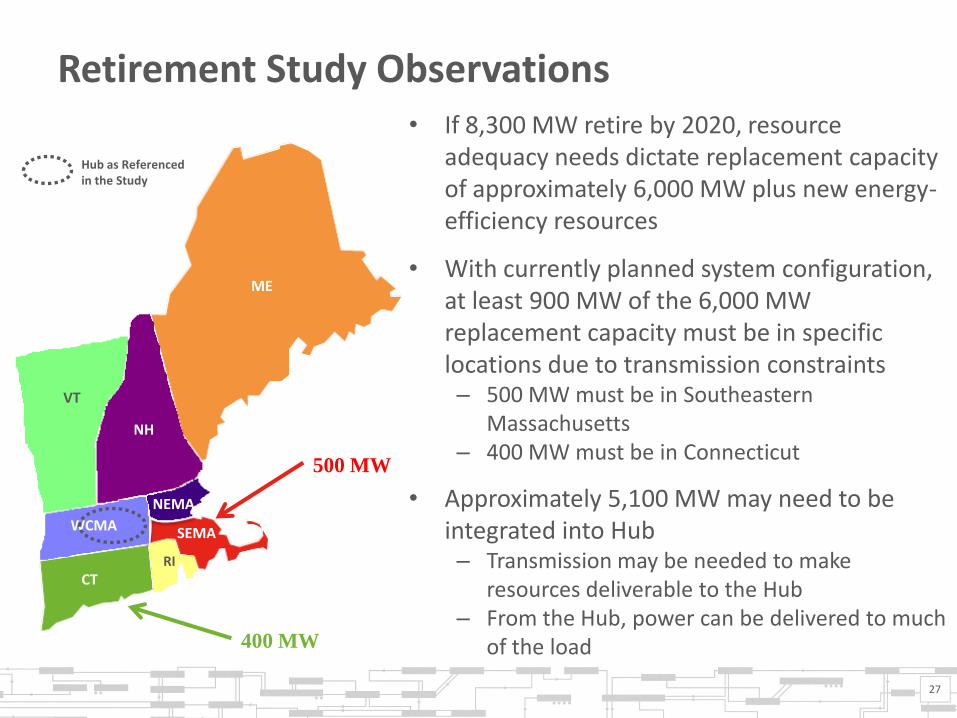

Retirement Study Observations • If 8,300 MW retire by 2020, resource

adequacy needs dictate replacement capacity of approximately 6,000 MW plus new energy-efficiency resources

• With currently planned system configuration, at least 900 MW of the 6,000 MW replacement capacity must be in specific locations due to transmission constraints – 500 MW must be in Southeastern

Massachusetts – 400 MW must be in Connecticut

• Approximately 5,100 MW may need to be integrated into Hub – Transmission may be needed to make

resources deliverable to the Hub – From the Hub, power can be delivered to much

of the load

27

VT

NH

ME

NEMA

CT

SEMA WCMA

RI

500 MW

400 MW

Hub as Referenced in the Study

Interregional Planning and Coordination Activities

28

U.S. Department of Energy

Congestion Study

Eastern Interconnection

Planning Collaborative (EIPC)

Electric Reliability Organization (ERO)

Northeast Power Coordinating

Council (NPCC)

ISO/RTO Council (IRC)

Northeastern ISO/RTO Planning

Coordination Protocol

29