Medical with Life Cover - Opportunity for Advisers and Clients

18

Medical with Life Cover Opportunity for Advisers and Clients February 2015 Russell Hutchinson and Alan Rafe www.qpresearch.co.nz

-

Upload

quality-product-research-limited -

Category

Economy & Finance

-

view

111 -

download

1

Transcript of Medical with Life Cover - Opportunity for Advisers and Clients

Medical with Life Cover

Opportunity for Advisers and

Clients

February 2015

Russell Hutchinson and Alan Rafe

www.qpresearch.co.nz

Long-term Trend: Medical and LifeMore than 25 years ago the health and life markets were largely separate, then

this happened

• Sovereign bought Met Life

• TOWER Life bought AXA Health

• Club Life – now OnePath life

• Partners Life

• Fidelity Life and nib

Other insurers without health cover are interested. Even insurers with poorly

operating health books see the value of health insurance as a gateway product

to sales of more life, disability, and trauma insurance. In parallel we have seen:

• More mortgage cover

• More income protection

• More trauma cover

February 2015

Better Together: Joint QuotingNumber of Health only Quotes in June 2014 1,871

Number of quotes with health in (last crunch, 2-3 re-crunches is typical) 3,295

Proportion of quotes including health of any kind which are health only: 57%

Proportion of all advisers that have quoted health at least once: 66%

400

500

600

700

800

900

1000

1100

1200

Jul-14 Aug-14 Sep-14

Accuro AIA Fidelity / nib OnePath Partners Life Southern Cross Sovereign

February 2015

Benefit Combinations With Health

Benefit Combinations with Health in last crunch How many in June

Health 1,871

Health Life 330

Health Life Trauma 283

Health IP Life Trauma WOP 111

Health IP Life TPD Trauma WOP 100

Health Life Repayment Trauma WOP 73

Health Trauma 65

Health Life TPD Trauma 53

Health IP Life Repayment TPD Trauma WOP 47

Health IP Life Repayment Trauma WOP 32

Subtotal 2,965

Others 330

Total 3,295

February 2015

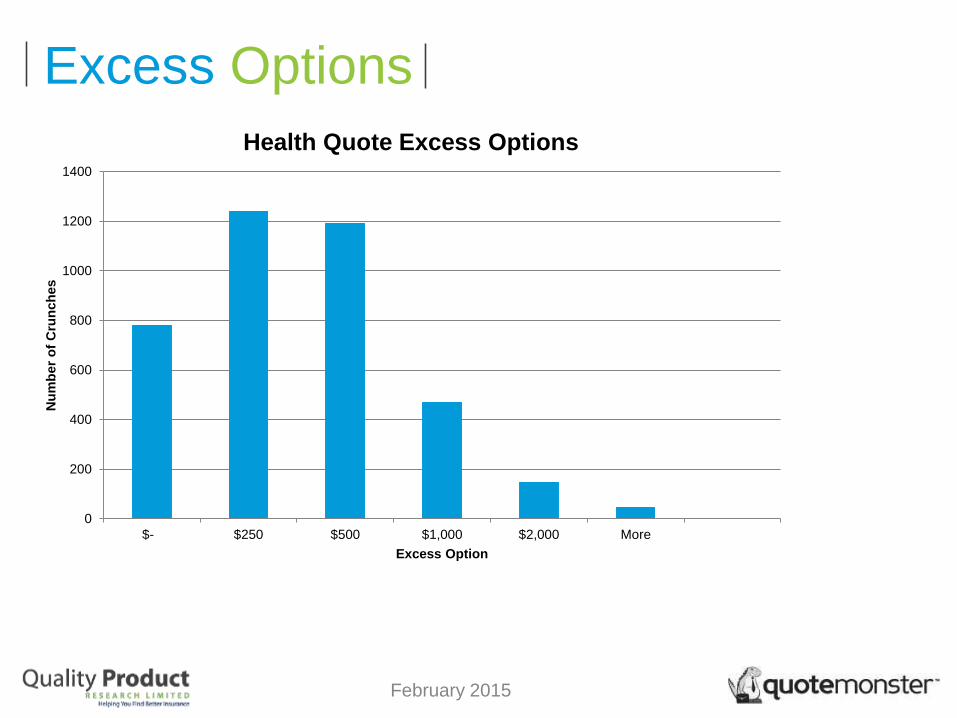

Excess Options

0

200

400

600

800

1000

1200

1400

$- $250 $500 $1,000 $2,000 More

Nu

mb

er

of

Cru

nch

es

Excess Option

Health Quote Excess Options

February 2015

Add-On Options

Basic32%

With Specialists68%

Health Quote Add-On Options

Note: Other combinations with GP and Dental too small to graph.

February 2015

Children in Health Quotes

0

500

1000

1500

2000

2500

0 1 2 3 4+

Nu

mb

er

of

Cru

nch

es

Number of Children

Number of Children Included in Health Quotes

February 2015

How Clients Use Medical CoverFull health Medical Trauma Disablement Death

Care free or

careless?

Specialists and

tests

Trauma add-

ons

Mortgage

cover

Terminal Illness

Basic medical Limited Trauma Income

protection

Life Cover

Fully featured

medical

insurance

Fully featured

trauma

Total and

Permanent

Disablement

Non-Pharmac

cover

International

Direct / “Everyday”

products

Doctors’ Visits etc.

Clients can see this

need first!

Choices are created by the financial assistance provided

February 2015

Competition: Making Products Better

• Stand alone specialists and tests sales

• ‘Best Doctors’ diagnosis tool

• Simple direct products – low cost, low benefit, high co-

payments

• Non-Pharmac drugs cover

• Loyalty rewards offering procedures outside scope of medical

cover e.g. Sterilisation, Breast Reduction & Bariatric Surgery.

• Extensive range of products and benefit variations on offer

prompted by new market entrants, where previously a couple

of providers held market monopoly.

February 2015

Advisers: Please Consider• Medical insurance has a role in the risk package

• Role of medical, IP, Trauma alongside state benefits

• Overseas treatment - International options

• Sales process innovations

• Bundling

• Health savings accounts

• Long-term care cover

• Screening programmes

February 2015

How Do You Compare Products?Risks

• “The One thing” to rule them all

• The “non-compliant” feature

Factors

• The whole product

• Price

• Service

• Claims

• Company Factors

Preference

• A Package View

February 2015

Overview• Medical is the next protection benefit clients can see the need for

• It is a great way to open up a constructive discussion about all the

other benefits

• Good advice acknowledges that it is part of a personal risk plan

• That risk plan isn’t alone: it exists in a context of personal wealth,

family, and state health and welfare provision

• An overview considering a range of factors rather than just one

factor is the right starting point for product selection

February 2015

Current Issues in Comparing

Medical• Guaranteed wordings

• Provides customer value in knowing wordings that cannot be altered

• Provides an option for unsustainable books

• Non-Pharmac

• We are seeing claims paid for Cancer related treatment

• Increased our weighting due to claims experience being higher

• Still working to understand the impact of non cancer related treatments

• Need to understand the impact of Chronic Condition exclusions

• Impact of out of hospital benefits

• Breast Reconstruction

• Cosmetic versus medically required

• Covered under main surgical benefit

• Including realignment, tattooing

• Exclusions

• Different excesses

February 2015

What We Compare on QuotemonsterCompany Basic Excess Options Specialist &

Tests Excess

Options

Saying Specialist

Excess

Used

Accuro$0, $250, $500, $1,000,

$2,000, $4,000

$0

$250

Nil excess on specialist & tests

no matter which base excess is

selected.

$0

AIA$0, $250, $500, $1,000,

$2,000

$100 $100 excess on specialist &

tests no matter which base

excess is selected.

$100

nib$0,$250, $500, $1,000,

$2,000, $4,000, $6,000

$0 Nil excess on specialist & tests

no matter which base excess is

selected.

$0

OnePath$0, $250, $500, $1,000,

$2,000, $5,000

$250 $250 excess on specialist &

tests no matter which base

excess is selected.

$250

Partners Life $0, $250, $500, $1,000,

$2,000, $5,000,

$10,000

$250 $250 excess on specialist &

tests no matter which base

excess is selected.

$250

Southern

Cross $0, $250, $500, $1,000

$0 Excess for specialist & tests is

matched to whichever base

excess is selected.

$0

Sovereign$0, $250, $500, $750,

$1,000, $2,000, $4,000

$0

$250

Nil excess on specialist & tests

no matter which base excess is

selected.

$250

February 2015

Getting it Right: Settings

February 2015

Rating Process

Definition Incidence Frequency Amount

Readability Impact

Better research to support recommendations, based

on: the meaningful differences between products, on

your client’s actual situation, and on real-world risks.

Based on actual

risks and

payment

Specific to each

client and

options

Low cost, easy

to update and

use

Male / Female

Employed / self-

employed

Age

Options

selected

Realistic claims

scenario

Each report

varied for each

quotation

February 2015

17

Thank You!Visit us at www.qpresearch.co.nz

Please remember that this material is

© Copyright – please use in your business but do

not distribute or re-sell

Information was current to 2 February 2015.

Rating Process

Definition Incidence Frequency Amount

Readability Impact

Better research to support recommendations, based

on: the meaningful differences between products, on

your client’s actual situation, and on real-world risks.

Based on actual

risks and

payment

Specific to each

client and

options

Low cost, easy

to update and

use

Male / Female

Employed /

self-employed

Age

Options

selected

Realistic

claims

scenario

Each report

varied for each

quotation