Medical Facilities Corporation TSX: DR...9 Unemployment Rate (%)1 U.S. Arkansas Indiana Oklahoma...

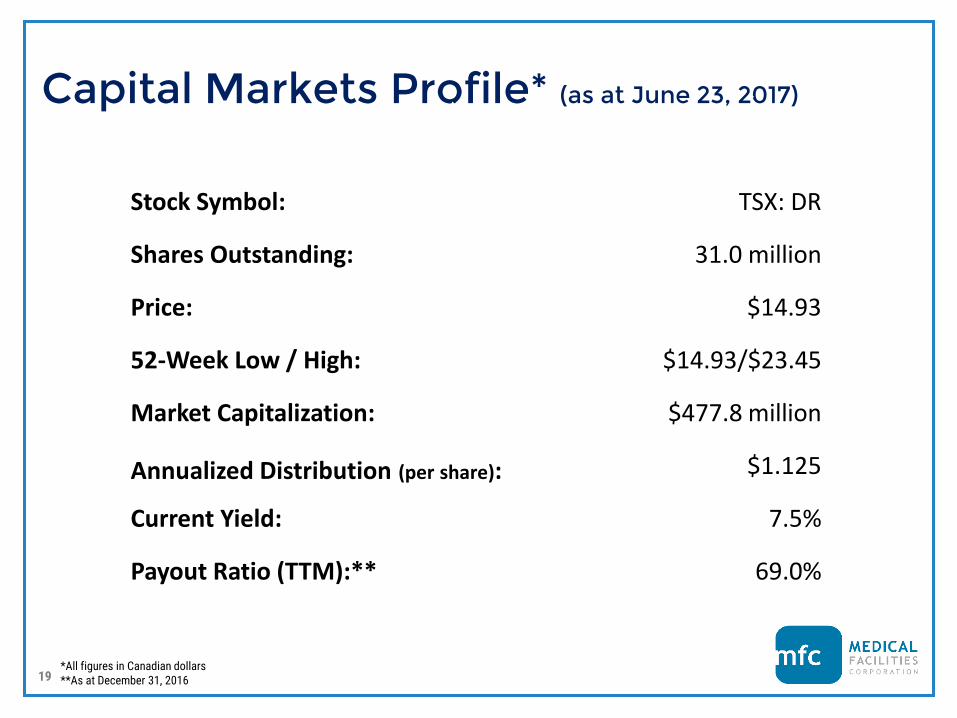

19

TSX: DR INVESTOR PRESENTATION JUNE 2017 Optimized. Enhanced.

Transcript of Medical Facilities Corporation TSX: DR...9 Unemployment Rate (%)1 U.S. Arkansas Indiana Oklahoma...

TSX: DR

INVESTOR PRESENTATION JUNE 2017

Optimized.Enhanced.

2

Forward-Looking Statements

This presentation may contain forward-looking statements within the meaning of certain securities laws, including the

“safe harbour” provisions of the Securities Act (Ontario) and other provincial securities law in Canada. These forward-

looking statements include, among others, statements with respect to our objectives, goals and strategies to achieve

those objectives and goals, as well as statements with respect to our beliefs, plans, objectives, expectations,

anticipations, estimates and intentions. The words “may”, “will”, “could”, “should”, “would”, “suspect”, “outlook”,

“believe”, “plan”, “anticipate”, “estimate”, “expect”, “intend”, “forecast”, “objective” and “continue” (or the negative

thereof), and words and expressions of similar import, are intended to identify forward-looking statements. Any such

statements are subject to risks and uncertainties that could cause actual results to differ materially from those

projected in these forward-looking statements. For more information on the risk factors related to these forward-

looking statements, please refer to the management’s discussion and analysis, annual information form and ongoing

quarterly filings of Medical Facilities Corporation available on SEDAR at www.sedar.com.

3

Transforming U.S. Healthcare Landscape

Acute Care Hospital

Specialty Surgical Hospital

Ambulatory Surgery Center

Urgent/Primary Care Center

MFC TODAY

Home Healthcare

Imaging Clinic

Other Specialty Clinic

(~5,500*)

(<300 physician-owned*)

(~5,500*)

* Estimated total U.S.

4

Multiple Payment Sources

Medicare20%

Medicaid18%

Other Government3%

Other Third Parties8%

Public Health and Investment

7%

Out of Pocket11%

Private Health Insurance33%

2015:

$3.2TRILLION

41% Public Health Insurance

Source: Kaiser Family Foundation

5

Growing Demand for Healthcare

DRIVERS:

Overall population growth

Aging population

Healthcare reform expanding coverage

Source: U.S. Census Bureau, 2010 based on National Population Projections 2008; 2015 & 2020 based on National Population Projections 2012Centers for Medicare & Medicaid Services, National Health Expenditure Projections 2011-2021

(millions) (US$ billion)

Po

pula

tio

n

Natio

nal Health Expenditure

0

1,000

2,000

3,000

4,000

5,000

0

100

200

300

400

2010 2015E 2020E

Under 45 years 45 to 64 years 65 years and over National Health Expenditure(US$ billion)

6

Changing Healthcare Industry Driving Acquisition Opportunities

Greater need for efficiency and scale among healthcare providers

Independent centers requiring scale to drive margin improvement

Portfolio rebalancing as a result of consolidation or service realignment makes attractive assets available

~940 healthcare transactions in 2016 ($72B)*

*Irving Levin Associates, cited by PRWeb, March 21, 2017

7

MFC: A Quality Healthcare Provider Well-Positioned for Growth

Majority ownership in five specialty surgical hospitals and one ambulatory surgery center • Specialty Surgical Hospitals: 48 operating rooms and 156 overnight rooms• Ambulatory Surgery Center: 2 operating rooms

2016 Revenue: US$339.5 million

2016 Income from Operations: US$68.1 million

8

MFC Specialty Surgical Hospitals

2

1 1

Specialty surgical hospitals have consistently demonstrated

HIGHER PATIENT SATISFACTIONratings resulting from

HIGHER QUALITY OF CARE RECEIVED

Our physician owned hospitals benefit from direct physician involvement in

facility management resulting inSUPERIOR PROCESSES AND EFFICIENCIES

1

FacilityOperating

SinceAcquired Operating Rooms Overnight Rooms Square Feet

Arkansas Surgical Hospital 2005 2012 11 41 126,000

Unity Medical and Surgical Hospital 2009 2016 6 29 50,000

Oklahoma Spine Hospital 1999 2005 7 25 61,000

Black Hills Surgical Hospital 1997 2004 11 26 75,000

Sioux Falls Specialty Hospital 1985 2004 13 35 76,000

9

Unemployment Rate (%)1 U.S. Arkansas Indiana Oklahoma South Dakota

2016 4.7 3.9 4.0 4.8 2.9

2015 5.0 4.3 4.6 4.6 2.8

65 and Over (% of population)2

2015 14.9 16.0 14.6 14.7 15.7

Situated in geographic regions that have proven to be resilient against challenging economic environments

MFC physicians and staff are integral part of our success, they provide patients with innovative treatments and optimal service

1 Source: The Bureau of Labor Statistics of the US Department of Labor.

2 Source: U.S. Census Bureau, U.S. Census Bureau, Population Division. Release Date: June 2016

Well-Situated in Current Markets

10

Strict Acquisition Criteria

Accretion, with growth available from a local strong provider base, attractive

demographics, and opportunities for operating enhancements

High quality and optimum clinical outcomes

Continued strong earnings and opportunity for growth

Controlling position by MFC

11

FinancialReview

12

Factors Driving Our Results

Revenues

Case Mix

Case Counts

Payor Mix

Ancillary Services

Levelof

Revenue

Operating Margins

Salaries & Benefits

Drugs & Supplies (incl. implants)

General & Administrative

13

Blue Cross/Blue Shield

Medicare/Medicaid

Workers’Compensation

Other Private Insurance

Other

MFC Payor Mix – 2016

34%

38%

7%

14%

7%

GROSS BILLINGS NET REVENUE

35%

29%

8%

20%

8%

14

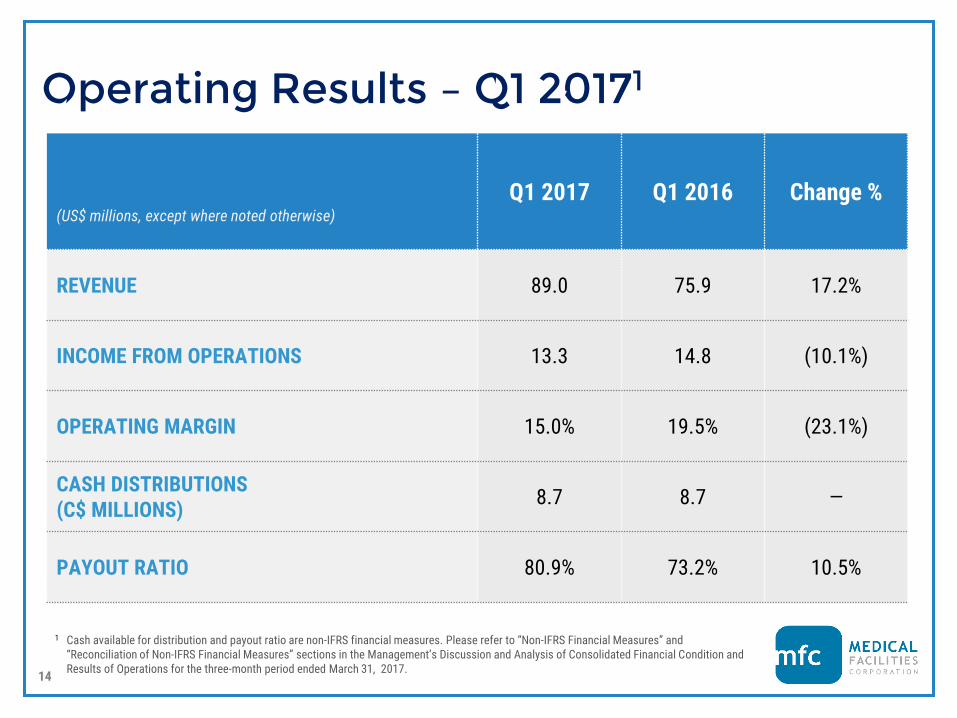

(US$ millions, except where noted otherwise)

Q1 2017 Q1 2016 Change %

REVENUE 89.0 75.9 17.2%

INCOME FROM OPERATIONS 13.3 14.8 (10.1%)

OPERATING MARGIN 15.0% 19.5% (23.1%)

CASH DISTRIBUTIONS (C$ MILLIONS)

8.7 8.7 —

PAYOUT RATIO 80.9% 73.2% 10.5%

Operating Results – Q1 20171

1 Cash available for distribution and payout ratio are non-IFRS financial measures. Please refer to “Non-IFRS Financial Measures” and “Reconciliation of Non-IFRS Financial Measures” sections in the Management’s Discussion and Analysis of Consolidated Financial Condition and Results of Operations for the three-month period ended March 31, 2017.

15

Well-Resourced for Growth

Cash and cash equivalents: $50.3 million

Current ratio: 2.4x

Net Debt/Equity: 50.0%

Subsidiary Debt Coverage (LTM): 1.4x

16

31.534.4 35.3 35.2 34.9

37.840.8 41.4

45.9

50.7

35.7

40.843.3

51.9 50.7

2012 2013 2014 2015 2016

69.02016

PAYOUT RATIO

%

83.3%

(C$ millions)

Distributions Cash Available for Distribution (including realized gains/losses on FX forward contracts)2

84.3%Payout Ratio2

1. Cash available for distribution and payout ratio are non-IFRS financial measures. Please refer to “Non-IFRS Financial Measures” and “Reconciliation of Non-IFRS Financial Measures” sections in the Management’s Discussion and Analysis of Consolidated Financial Condition and Results of Operations for the three-month period ended March 31, 2017.

2. Including realized gains/losses of FX forward contracts for years 2012-2015.

Strong Cash Flow1

Cash Available for Distribution (Excluding realized gains/losses on FX forward contracts)

85.2% 76.7% 69.0%

17

Key Strengths

• Well-located facilities providing stable cash flows

• Favorable industry growth drivers

• Experienced, entrepreneurial management team

• Resources in place to execute on growth strategy

18

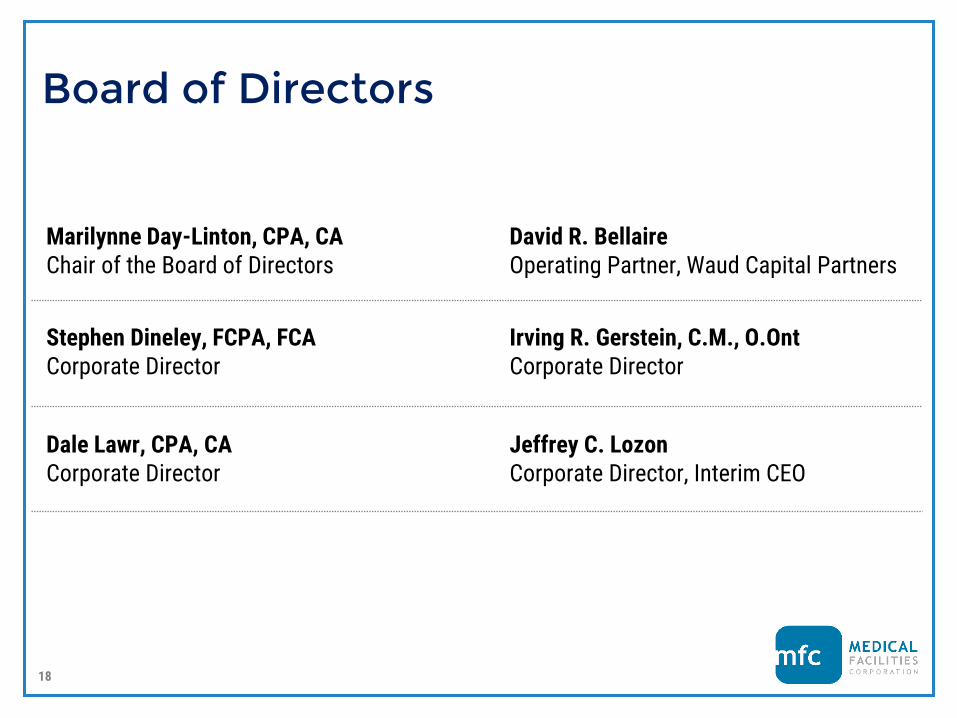

Board of Directors

Marilynne Day-Linton, CPA, CA Chair of the Board of Directors

Irving R. Gerstein, C.M., O.OntCorporate Director

David R. Bellaire Operating Partner, Waud Capital Partners

Dale Lawr, CPA, CACorporate Director

Stephen Dineley, FCPA, FCA Corporate Director

Jeffrey C. LozonCorporate Director, Interim CEO

19

Capital Markets Profile* (as at June 23, 2017)

Stock Symbol: TSX: DR

Shares Outstanding: 31.0 million

Price: $14.93

52-Week Low / High: $14.93/$23.45

Market Capitalization: $477.8 million

Annualized Distribution (per share): $1.125

Current Yield: 7.5%

Payout Ratio (TTM):** 69.0%

*All figures in Canadian dollars**As at December 31, 2016