Media presentation H1 2018 results - rabobank.com · Dec 16. 43,729. Valuable progress on our...

17

Rabobank Media presentation H1 2018 results 16 August 2018

Transcript of Media presentation H1 2018 results - rabobank.com · Dec 16. 43,729. Valuable progress on our...

RabobankMedia presentation H1 2018 results

16 August 2018

Growing a better world together

Banking for the Netherlands Banking for Food

10 Strategic Top Priorities

• 100% Digital convenience in everything

• Top customer advice nearby

• Growth with innovation

• Top performance• Optimal balance sheet• Exceptionally good

execution

• Concrete socially responsible contribution

• Involved members and communities

• Inspired employees• One-Rabobank culture

Excellent customerfocus

Rock-solidbank

Empoweredemployees

Meaningful cooperative

Strategy overviewFocus on 10 top priorities for 2018-2020

2

Highlights H1 2018 (I)

3

Growth deposit base & loan book • Growth loan book by € 7.6bn • Deposit base increased by € 3.4bn

Excellent customer focus Meaningful cooperative

Most customer-friendly bank • 1st place by consumers as the most customer-friendly

bank in the Netherlands (Customer First Awards)• Sustained increase in domestic Net Promotor Scores

Strong progress in innovation• Rabobank innovation SurePay (IBAN name check) rolled

out to many Dutch banks and insurance companies• 1st Dutch bank to facilitate 3rd party payment initiation• Customers can check account balance or set a spending

alert using their voice via Google Assistant

Client-focused operating model• New client focused operating model for local Rabobanks

in the Netherlands as the foundation for a more effective and efficient banking operation

Industry leading in sustainability• Sustainalytics score: 86 + awarded ‘ESG Industry Leader’ • Oekom Prime: awarded ‘Industry Leader’ in 2017• RobecoSam: score 89 (11th worldwide)

First to launch ‘ESG Leader’ program• Rabobank was first to launch ESG Leader CP/CD program• Driven by Rabobank's 'ESG Industry Leader' status

Rabobank issues short term funding labelled as ESG investment

3rd Kickstart program launched (Food)• Launched Kickstart Waste to drive food waste reduction,

from stimulating innovations to financial support for farmers to improve replanting, logistics and storage

Driving energy efficient housing• Proprietary sustainability scan helps mortgage clients

identify sustainability improvements in their homes• Introduced Green Depot, a 2-year interest-free depot to

finance sustainable home improvements

Highlights H1 2018 (II)

4

Strong net profit• H1 net profit of € 1.7bn (+12%) supported by favorable

economic environment

Rock-solid bank Empowered employees

Comfortable capital position• Well positioned to absorb future

Basel IV and MREL requirements (30.96%)• Expected Non-Preferred Senior issuance in H2 2018

Continued strategic focus• Non-core domestic CRE portfolio divested with FGH Bank

portfolio sale• Repositioned BPD with focus on Dutch and German

market by divesting BPD France (expected closing: Q4)

Improved efficiency• Cost/Income ratio improved to 64.6% with further cost

reduction remaining a point of attention

#1 Employer in the Netherlands• Rabobank awarded #1 favorite employer to work for by

talents (university & higher vocational education)

Diversity strong and improving• Women well-represented in senior management

positions (33% overall, 40% in Managing Board)• Strong cultural diversity in our young talent pool (30%)

235 New start-up ideas generated• Employees from 13 countries generated 235 ideas for

start-ups through our innovation incubator program • Involved in 68 start-up communities and organizer of F&A

innovation events such as FoodBytes! and Terra

High employee mobility• 63% of the employees we had to let go found a job within

six months, which is above average for the banking sector in the Netherlands

+12%(€ 1.7bn)

CET1

Total Capital

15.8%

26.1%

64.6%(-3.0%-point)

Ongoing successful transformation in the Netherlands…Ready for the next phase

5

Phase 3 | Optimize service modelPhase 2 | Regionalize mid- & back officePhase 1 | Implement new governance

January 2016

• Efficiency improvement through process standardization and regionalization of customer call center and operational service centers

• Incorporated digitalization as an integral part of the strategy and change agenda

• Significantly reduced cost and FTE, while increasing Net Promotor Scores (NPS)

• Next step towards a more effective and efficient organization as per 1/1/2019

• Further optimization of omnichannel client service model

• 250 Market teams ensure customer intimacy through face-to-face contact, operating out of 90 banks supported by 14 regional teams

• Anticipating changing client demands and regulatory requirements

• Merger of 106 local Rabobanks with central entity to one legal entity with one banking license and one balance sheet

• More flexible, simple and adaptive structure supporting cooperative values

2016 -2018 June 2018

14 regions of 6-7

Rabobanks

…resulting in higher client appreciation and efficiency

6

37

60

33

56

21

52

Dec 15 Dec 16 Dec 17 Jun 18

NPS private banking customers

NPS retail customers

NPS business customers

Net Promotor Score (domestic market) FTE development Rabobank Group

* Including 1,255 FTEs due to the Athlon sale in 2016 ** This is the balance of -775 FTEs at DRB (of which ~400 FTEs transferred to the central

organization), and +669 FTEs at the other business segments

-106**

Dec 17

45,567

Ambition

43,623

38,500

Jun 18

-8,390*

52,013

Dec 15 Dec 16

43,729

Valuable progress on our financial targets

7

Jun 2017 Dec 2017 Jun 2018 Ambition 2020

Capital

Fully loaded CET1 ratio 14.7% 15.5% 15.8% >14%

Total capital ratio 25.5% 26.2% 26.1% >25%

Profitability

ROIC 7.8% 6.9% 8.8% >8%

C/I ratio 67.6% 71.3% 64.6%

53-54%

Underlying C/I ratio 63.9% 65.3% 62.9%

Funding Wholesale funding € 171bn € 160bn € 164bn < €150bn

Financial targets and results

Positive net profit development

8

In € mn H1 2017 H2 2017 H1 2018

Net interest income 4,454 4,389 4,274

Net fee & commission income 988 927 981

Other results 496 747 774

Total income 5,938 6,063 6,029

Operating expenses 3,755 4,299 3,611

Regulatory levies 258 247 284

Impairment charges -67 -123 -37

Operating profit before tax 1,992 1,640 2,171

Tax 476 482 473

Net profit 1,516 1,158 1,698

Profit & Loss account Net profit (in € mn)

1,522

997

692

1,027

1,158

1,5161,698

2015

2,214

2016

2,024

20182017

2,674H2

H1

Continued strong underlying performance

9

Exceptional items included in operating profit before tax Underlying profit before tax (in € mn)

In € mn H1 2017 H2 2017 H1 2018

Fair Value items -186 -127 -133

Restructuring costs -98 -61 -22

Provision RNA 0 -310 0

Derivatives framework 0 -51 0

Total effect -284 -549 -155

1,992

1,640

2,171

549

155284

H1 2017

2,1892,276

+2%

Operating profit before tax

Exceptional items

H1 2018

2,326

H2 2017

Total income slightly up despite challenging interest rate environment

10

Total income (in € mn)

4,389 4,274

927 981

874

4,454

988

907682

5,938

H1 2017

-186

6,190 6,162

6,029

6,124

6,063

Net fee and commission income

Net interest income

Other results

FV itemsH1 2018

-133

H2 2017

-127

Net interest income impacted by prolonged low interest rate environment

11

Net interest income (in € mn) and Net interest margin (in % of average balance sheet total)

NIM(12m-rolling average)

1.41%1.39%1.33%1.29%1.33%1.33%1.32%

4,657 4,375 4,368 4,454 4,389 4,2744,482

H1 2018H2 2017H1 2017H2 2016H1 2016H2 2015H1 2015

Multi-year transformation program is paying off

12

Operating expenses (in € mn)

H1 2017 H2 2017 H1 2018

C/I ratio 67.6% 75.0% 64.6%

Underlying C/I ratio 63.9% 66.6% 62.9%

2,206 2,266 2,127

1,4511,611

1,462

31061

51

H1 2017

3,755

4,299

3,589

H1 2018

Staff costs

Other Opex

H2 2017

3,657 3,877

Restructuringcosts 22

3,61198

Derivatives frameworkProvision RNA

Development cost/income ratio incl. regulatory levies

Asset quality continues to benefit from economic tail wind

13

Impairment charges (in € mn and in bps of average lending)

-2 bps-3 bps -6 bps

-43 -73

105

-103

41

65

-42

-156

-27

35

-3

H2 2017

-10

H1 2018

0

Domestic Retail

Other

Real Estate

Leasing

WRR

H1 2017

-2-14

-€ 37mn-€ 67mn -€ 123mn

Loan portfolio increased after a few years of slight contraction

14

Composition of private sector loan portfolio (in € bn)

193 193

23 22 2227 27 27

42 42 43

62 61 65

37 36 3727 27 29

192

Domestic Retail F&A

Domestic Retail other SMEs

WRR Wholesale (excl. CRE)

WRR Rural & Retail

Leasing

Jun 18

416

Jan 18

408

Dec 17

Domestic CRE

Domestic Retail mortgages

+2%

411

Deposits from customers and private sector lending (in € bn)

Loan-to-deposit ratio slightly improved

15

1.21 LtD ratio

229 229 235

28 28 25

84 86 87

411 408 416

343

WRR and Other

RaboDirect

347

DRB

341

Dec 17 Jan 18 Jun 18

1.20

Deposits from customersLending

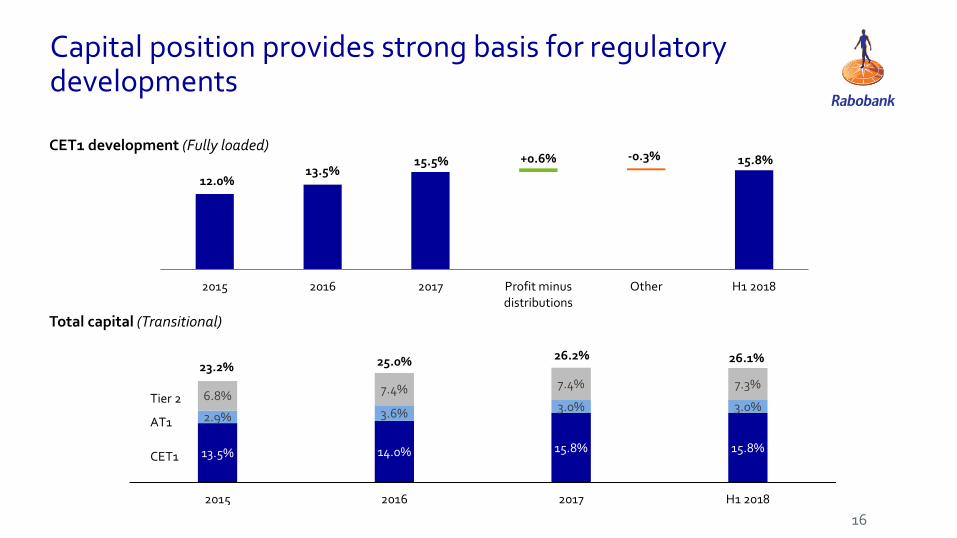

13.5% 14.0% 15.8% 15.8%

2.9% 3.6% 3.0% 3.0%6.8% 7.4% 7.4% 7.3%

2015 2016 2017 H1 2018

Tier 2

AT1

CET1

Capital position provides strong basis for regulatory developments

16

CET1 development (Fully loaded)

Total capital (Transitional)

25.0% 26.2% 26.1%23.2%

12.0%13.5%

15.5% 15.8%+0.6% -0.3%

2015 2016 2017 Profit minusdistributions

Other H1 2018

RabobankMedia presentation H1 2018 results

16 August 2018

![6,029(570$67(5’5,9(6 1iYRGNREVOX]HD~GUæE … · 6,029(570$67(5’5,9(6 0rwlrq&rqwuro 1iyrgnrevox]hd~guæe 0 qlþnplwrþwx $& $& ⁄nrpsdnwqts uryhghqt ⁄yhvwdyqpsuryhghqt 6w˝tgdþnplwrþwx](https://static.fdocuments.in/doc/165x107/5bec8a5509d3f2d6718b9c33/6029570675596-1iyrgnrevoxhdguaee-6029570675596-0rwlrqrqwuro.jpg)