Measuring Risk Risk Management Prof. Ali Nejadmalayeri, Dr N a.k.a. “Dr N”

16

Measuring Risk Measuring Risk Risk Management Prof. Ali Nejadmalayeri, a.k.a. “ Dr N Dr N”

-

Upload

rudolf-roberts -

Category

Documents

-

view

215 -

download

3

Transcript of Measuring Risk Risk Management Prof. Ali Nejadmalayeri, Dr N a.k.a. “Dr N”

Measuring RiskMeasuring Risk

Risk Management

Prof. Ali Nejadmalayeri,

a.k.a. “Dr NDr N”

Risk & Return of Securities

• Assuming that current price is P0 and the security can be sold for P1, then:

• If this return is random, then over time, we can see what is its distributiondistribution. The central tendency of the distribution is meanmean. If this distribution is true and stable, then this mean is our measure of expected value, E[expected value, E[rr]]. One measure of variation of our random return is variancevariance, E[E[r – r – E[E[rr]]]]22.

• Another measure of volatility is standard standard deviationdeviation which squared root of the variance.

10

1 P

Pr

Probability & Distribution

• Given that we know the distribution of returns, then we can compute cumulative probabilities of returns being below certain thresholds!

Excel & CDFs

• Imagine, IBM has an average return of 10% and standard deviation of 30%. What is probability of a loss?– Use NORMDIST function in Excel

• Enter

CDF vs. PDF

• Cumulative Distribution Functions represent probability of up to an outcome whereas Probability Density Functions represent probability of one outcome!

Portfolio Return

• Imagine N assets with returns, ri, are combined such that wi fraction of total funds is invested in each of the assets, then the portfolio’s return is:

• Then for expected return of the portfolio, we have:

N

iiip rwr

1

N

iiip rEwrE

1

][][

Portfolio Variance

• Imagine that each pair of assets in a portfolio with N assets with returns, ri, and asset weight, wi, has a correlation of ρij, then the variance of the portfolio is:

N

jijjiji

N

i

N

iiip

rVarrVarww

rVarwrVar

1

5.05.0

1

1

2

][][

][][

Diversification

• Unlike return, variance of a portfolio is also related to correlations. So if these correlations different from ONE, then there can be some risk saving!

Efficient Frontier

• When assets are combined, the possible return-risk outcomes form an efficient frontier on which best return for any level risk or vice versa lowest risk for any level return is obtained!

Risk & Asset Pricing

• If idiosyncratic risk can be removed by creating well-diversified portfolios, then only correlations with market risk should matter for determining return!

• Then return on each asset is given by:

M

imiim

M

iiimmm rrCovwrrwCovrrCovrVar

11

],[,],[][

][

],[

m

mii

fmifi

rVar

rrCov

rrErrE

Valuation & CAPM

• Assume a firm generates E[C] of cash flows. If the firm is all equity financed, then value of the firm is defined by:

fmifi rrEr

CE

rE

CEV

1

Risk Management & Value

• If risk management reduces risk, then value can increase; lower discount rate!– By prudent diversification schemes,

idiosyncratic risk can be eliminated• In perfect markets, both investors and firms can do

this, so the shouldn’t be reward associated with risk management in perfect markets

– By taking short or offsetting positions, systematic risk can be eliminated

• In perfect markets, both investors and firms can do this, so the shouldn’t be reward associated with risk management in perfect markets

Why Manage Risk?

• Hedging Irrelevance Proposition:Hedging Irrelevance Proposition:– When the cost of bearing risk is same for firms

and individuals, hedging cannot add value!

• Risk management is only beneficial only if firms can perform hedging at lower cost than their shareholders.

A Helicopter View

• Uncertainty is a fact of life, so there is no crystal ball! But risk can be managed!

Indentify Risk Exposures

Measure and Estimate Risk Exposures

Find Instruments & Facilities to Shift or Trade Risk

Asset Effects of Exposures Assess Costs & Benefits of Instruments

From a Risk Mitigation Strategy:Avoid, Transfer, Mitigate, Keep

Evaluate Performance

Topology of Risk

RisksLegal &

Regulatory Risk

Operational Risk

Liquidity Risk

Credit Risk

Market Risk

Strategic Risk

Reputation Risk

Business Risk

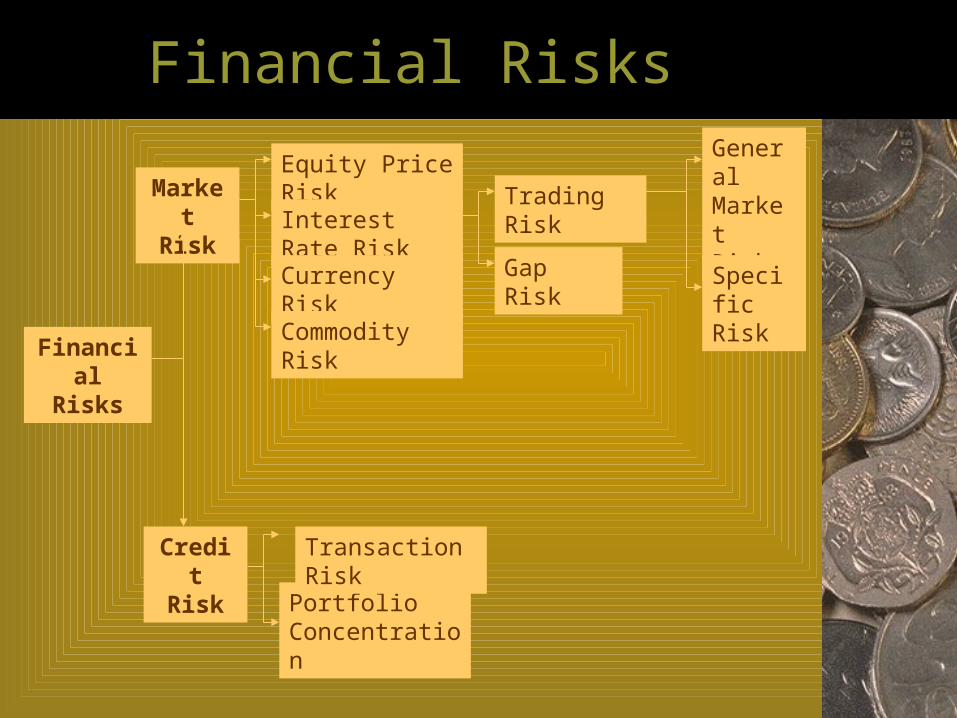

Financial Risks

Financial Risks

Market Risk

Credit Risk

Equity Price Risk

Interest Rate Risk

Currency Risk

Commodity Risk

Trading Risk

Portfolio Concentration

Transaction Risk

Gap Risk

General Market Risk

Specific Risk