Measurin g r A Note on T ransitory Shocks - CEMLA

59

g r * r *

Transcript of Measurin g r A Note on T ransitory Shocks - CEMLA

Measuring r ∗: A Note on Transitory Shocks

Kurt F. Lewis Francisco Vazquez-Grande

Federal Reserve Board

Lewis & Vazquez-Grande (FRB) Measuring r∗ 1 / 24

Federal Reserve Disclaimer

The analysis and conclusions set forth are those of the authors and donot indicate concurrence by other members of the research sta� or

the Board of Governors.

Lewis & Vazquez-Grande (FRB) Measuring r∗ 2 / 24

Chair Yellen, March 15, 2017

�That's based on our view that the neutral nominal federal funds rate...is

currently quite low by historical standards. That means that the federal funds

rate does not have to rise all that much to get to a neutral policy stance.�

Lewis & Vazquez-Grande (FRB) Measuring r∗ 3 / 24

Main Results

Main Results

We incorporate fully the uncertainty on r∗ embedded in the data, we �nd:

a more prociclycal r∗ in the benchmark model.

evidence of transitory shocks to r∗.

Lewis & Vazquez-Grande (FRB) Measuring r∗ 4 / 24

The Model

Baseline model (Holston, Laubach and Williams 2016)

yt = yt − y∗t

yt = ay ,1yt−1 + ay ,2yt−2 +ar2

2∑j=1

(rt−j − r∗t−j

)+ εy ,t

πt = bππt−1 + (1− bπ)πt−2,4 + bY yt−1 + επ,t

y∗t = y∗t−1 + gt−1 + εy∗,t

gt = gt−1 + εg ,t

r∗t = gt + zt

zt = zt−1 + εz,t

Lewis & Vazquez-Grande (FRB) Measuring r∗ 5 / 24

The Model

Extended model

yt = yt − y∗t

yt = ay ,1yt−1 + ay ,2yt−2 +ar2

2∑j=1

(rt−j − r∗t−j

)+ εy ,t

πt = bππt−1 + (1− bπ)πt−2,4 + bY yt−1 + επ,t

y∗t = y∗t−1 + gt−1 + εy∗,t

gt = µg + ρz(gt−1 − µg ) + εg ,t

r∗t = gt + zt

zt = ρzzt−1 + εz,t

Lewis & Vazquez-Grande (FRB) Measuring r∗ 6 / 24

The Model

Model estimation: MLE

pileup problem (Stock 1994)

Solution proposed by Laubach and Williams 2003

based on medium unbiased estimator from Stock and Watson 1998:

λg ≡σgσy∗

, λz ≡arσzσy

.

LW Method:

Step 1 Simplify model, estimate λg .

Step 2 Fix λg value, use alternative simpli�cation, estimate λz .

Step 3 Fix λg and λz , estimate remaining parameters.

Lewis & Vazquez-Grande (FRB) Measuring r∗ 7 / 24

The Model

Model estimation: MCMC

pileup problem? (DeJong and Whiteman 1993, Kim and Kim 2017)

We use standard Bayesian methods (random walk MC, FFBS).

Flat priors.

Imposing HLW λg and λz , we replicate HLW.

Lewis & Vazquez-Grande (FRB) Measuring r∗ 8 / 24

The Model

Priors

Name Domain Density Parameter 1 Parameter 2

a1 R Normal 0 2

a2 R Normal 0 2

ar R− Normal 0 2

b1 [0, 1] Uniform 0 1

bY R+ Normal 0 2

ρg R Normal 1 12

µg R Normal 0 2

ρz R Normal 1 12

σ1 [0, 5] Uniform 0 5

σ2 [0, 5] Uniform 0 5

σ3 [0, 5] Uniform 0 5

σ4 [0, 5] Uniform 0 5

σ5 [0, 5] Uniform 0 5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 9 / 24

The Model

MLE vs Bayesian: the di�erence in λ′s

λg λz

Lewis & Vazquez-Grande (FRB) Measuring r∗ 10 / 24

The Model

Models Considered

We estimate the key parameters ρg , µg and ρz of the extended model.

We consider four alternatives:

Model I ρg = 1, ρz = 1, (only di�erent estimation technique)

Model II ρg and µg estimated, ρz = 1

Model III ρg = 1, ρz estimated

Model IV ρg , µg and ρz estimated

Lewis & Vazquez-Grande (FRB) Measuring r∗ 11 / 24

The Model

Models Considered

We estimate the key parameters ρg , µg and ρz of the extended model.

We consider four alternatives:

Model I ρg = 1, ρz = 1, (only di�erent estimation technique)

Model II ρg and µg estimated, ρz = 1

Model III ρg = 1, ρz estimated

Model IV ρg , µg and ρz estimated

ρg , µg and ρz estimated

Lewis & Vazquez-Grande (FRB) Measuring r∗ 11 / 24

Estimation Results

Model I: ρg = 1, ρz = 1

Smoothed r∗ Draws in Model I (Shaded 10th to 90th Percentile)

Lewis & Vazquez-Grande (FRB) Measuring r∗ 12 / 24

Estimation Results

Model II: ρg and µg estimated, ρz = 1

Smoothed r∗ Draws in Model II

Lewis & Vazquez-Grande (FRB) Measuring r∗ 13 / 24

Estimation Results

Model II: ρg and µg estimated, ρz = 1

Figure: ρg

-0.5 0 0.5 1 1.50

0.5

1

1.5

2

2.5

3

3.5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 14 / 24

Estimation Results

Model III: ρg = 1, ρz estimated

Smoothed r∗ Draws in Model III

Lewis & Vazquez-Grande (FRB) Measuring r∗ 15 / 24

Estimation Results

Model I: ρg = 1, ρz = 1

Smoothed z in Model I

Lewis & Vazquez-Grande (FRB) Measuring r∗ 16 / 24

Estimation Results

Model III: ρg = 1, ρz estimated

Smoothed z in Model III

Lewis & Vazquez-Grande (FRB) Measuring r∗ 17 / 24

Estimation Results

Model III: ρg = 1, ρz estimated

Posterior Distribution of ρz in Model III

-0.5 0 0.5 1 1.50

0.5

1

1.5

2

2.5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 18 / 24

Model Comparison

Model I vs. Model III

The di�erence between the median path of r∗ in Model I and Model II

doesn't seem large.

Model III looks di�erent than Model I (in terms of the median path).

The only di�erence between the models is that Model I has a

degenerate prior on ρz ≡ 1.

Model Comparison

Bayes Factor for nested models reduces to the Savage-Dickey density

ratio (Dickey, 1971).

BIII ,I =pr(Y |MIII )

pr(Y |MI )=

pIII (ρz = 1)

pIII (ρz = 1|Y )

Lewis & Vazquez-Grande (FRB) Measuring r∗ 19 / 24

Model Comparison

Savage-Dickey Density Ratio

Figure: Prior and Post. ρz

0 0.2 0.4 0.6 0.8 1 1.20

0.5

1

1.5

2

2.5

Figure: Area around ρz = 1

0.95 1 1.050

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

BIII ,I =pIII (ρz = 1)

pIII (ρz = 1|Y )= 8.4

Lewis & Vazquez-Grande (FRB) Measuring r∗ 20 / 24

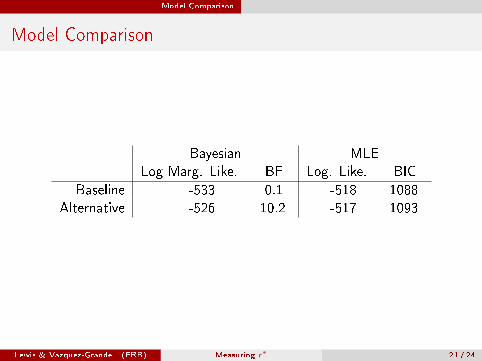

Model Comparison

Model Comparison

Bayesian MLE

Log Marg. Like. BF Log. Like. BIC

Baseline -533 0.1 -518 1088

Alternative -526 10.2 -517 1093

Lewis & Vazquez-Grande (FRB) Measuring r∗ 21 / 24

Discussion Thinking about zt

Connection to Theory

The r∗ equation is a linearized euler equation, we can denote the

stochastic discount factor (SDF) by S :

e−r∗t = Et [St+1]

Consider an SDF that di�ers from that of log-utility by an extra term

(Z ) as in Campbell and Cochrane, Epstein-Zin, etc. Then we have

r∗t = log Et

[Ct+1

CtZt+1

]= log Et

[egt+1+zt+1

]≈ Et [gt+1 + zt+1]

zt can be interpreted as an asset pricing term that measures the

separation from log-utility of the SDF. We can give z this �headwinds�

interpretation.

Lewis & Vazquez-Grande (FRB) Measuring r∗ 22 / 24

Discussion Thinking about zt

Headwinds

Frequently, �headwinds� are cited as a reason for why the level of r∗ is

still so low.

�...lingering sense of caution on the part of households and businessesin the wake of the trauma of the Great Recession.� (Yellen, 3/3/17)

zt is the �special sauce� (Williams, 2015 Brookings), it is all the thingsthat are not economic growth.

There is nothing that says the components have to be stationary orpersistent.In the current version of the model, there is no data speci�cally aimedat estimating zt .zt soaks up the variation in the rate gap that doesn't appear to belinked to growth.Headwinds seem like they should be temporary

Lewis & Vazquez-Grande (FRB) Measuring r∗ 23 / 24

Conclusion

Conclusion

Single-step Bayesian estimation with less informative priors shows

deeper drops and subsequent recoveries after recessions, in contrast to

multi-step MLE results.

When z is not assumed to be a random walk, we estimate a greater

recovery of r∗ since the lows of the great recession, reaching closer to

2% at the end of 2016Q3.

Our conclusion is that permanent shocks to z (and thus, in our minds,

the SDF) are needed to produce a persistent low level of r∗ after the

great recession.

The dynamics of z are hard to estimate with this data.

More structure around z may be helpful.

Lewis & Vazquez-Grande (FRB) Measuring r∗ 24 / 24

APPENDIX

Lewis & Vazquez-Grande (FRB) Measuring r∗ 1 / 34

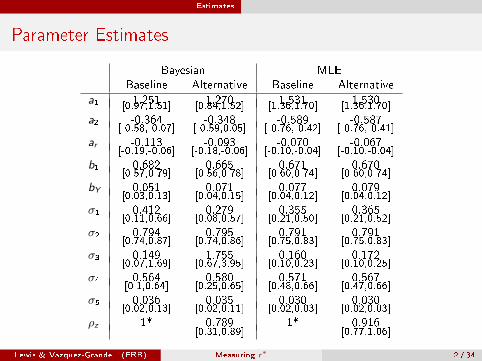

Estimates

Parameter Estimates

Bayesian MLE

Baseline Alternative Baseline Alternative

a1 1.251 1.270 1.531 1.530[0.97,1.51] [0.84,1.52] [1.36,1.70] [1.36,1.70]

a2 -0.364 -0.348 -0.589 -0.587[-0.58,-0.07] [-0.59,0.05] [-0.76,-0.42] [-0.76,-0.41]

ar -0.113 -0.093 -0.070 -0.067[-0.19,-0.06] [-0.18,-0.06] [-0.10,-0.04] [-0.10,-0.04]

b1 0.682 0.665 0.671 0.670[0.57,0.79] [0.56,0.78] [0.60,0.74] [0.60,0.74]

bY 0.051 0.071 0.077 0.079[0.03,0.13] [0.04,0.15] [0.04,0.12] [0.04,0.12]

σ1 0.412 0.279 0.355 0.365[0.11,0.66] [0.08,0.57] [0.21,0.50] [0.21,0.52]

σ2 0.794 0.795 0.791 0.791[0.74,0.87] [0.74,0.86] [0.75,0.83] [0.75,0.83]

σ3 0.149 1.755 0.160 0.172[0.07,1.69] [0.67,3.95] [0.10,0.23] [0.10,0.25]

σ4 0.564 0.580 0.571 0.567[0.1,0.64] [0.25,0.65] [0.48,0.66] [0.47,0.66]

σ5 0.036 0.035 0.030 0.030[0.02,0.13] [0.02,0.11] [0.02,0.03] [0.02,0.03]

ρz 1* 0.789 1* 0.916[0.31,0.89] [0.77,1.06]

Lewis & Vazquez-Grande (FRB) Measuring r∗ 2 / 34

Laubach-Williams Methodology

Laubach-Williams 3-part Estimation

Step 1 Hold g constant, drop real rate gap from model, then:

- Get estimate of potential output, y∗, compute ∆y∗

- λg is equal to Andrews and Ploberger (1994)

exponential Wald statistic for the test of a structural

break at unknown date in ∆y∗.

Step 2 Impose λg value from Step 1, include real rate gap, but hold

z constant, then:

- Estimate the simpli�ed model

- λz is equal to Wald statistic for the test of a shift in the

intercept of the IS equation.

Step 3 Impose λg from Step 1 and λz from Step 2, and estimate the

remaining parameters by MLE.

Back

Lewis & Vazquez-Grande (FRB) Measuring r∗ 3 / 34

Laubach-Williams Methodology

HLW replication

One-sided Bayesian estimate (blue) and HLW results (red)

back

Lewis & Vazquez-Grande (FRB) Measuring r∗ 4 / 34

Getting Around the �pile-up� problem

DeJong and Whiteman (1993)

Monte Carlo exercise where the true parameter value is 0.85, T = 100

Sample distribution of MLE estimate (left) and posterior distribution (right)

back

Lewis & Vazquez-Grande (FRB) Measuring r∗ 5 / 34

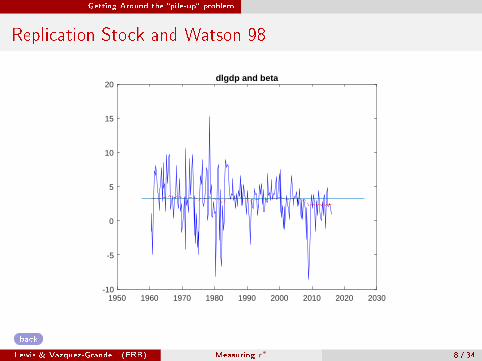

Getting Around the �pile-up� problem

Stock and Watson '98

Our estimation technique does not su�er from the pile-up problem.

To illustrate this: Consider Stock and Watson 1998 local level model of log

GDP growth.

∆yt = βt + ut

βt = βt−1 +λ

Tηt

ut = a1ut−1 + a2ut−2 + a3ut−3 + a4ut−4 + εt

Lewis & Vazquez-Grande (FRB) Measuring r∗ 6 / 34

Getting Around the �pile-up� problem

Replication Stock and Watson 98

0 5 10 15 200

20

40

60

80

100

120

140Histogram of draws of lambda

Lewis & Vazquez-Grande (FRB) Measuring r∗ 7 / 34

Getting Around the �pile-up� problem

Replication Stock and Watson 98

1950 1960 1970 1980 1990 2000 2010 2020 2030-10

-5

0

5

10

15

20dlgdp and beta

back

Lewis & Vazquez-Grande (FRB) Measuring r∗ 8 / 34

Key Posterior Estimates

Key Posterior Estimates From Each Model

Lewis & Vazquez-Grande (FRB) Measuring r∗ 9 / 34

Key Posterior Estimates Model I

Model I: ρg = 1, ρz = 1

Smoothed output gap

Lewis & Vazquez-Grande (FRB) Measuring r∗ 10 / 34

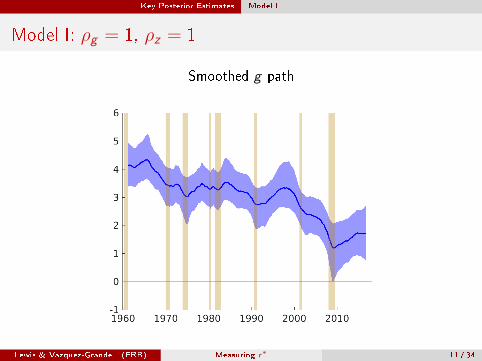

Key Posterior Estimates Model I

Model I: ρg = 1, ρz = 1

Smoothed g path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 11 / 34

Key Posterior Estimates Model I

Model I: ρg = 1, ρz = 1

Smoothed z path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 12 / 34

Key Posterior Estimates Model I

Model I: ρg = 1, ρz = 1

Posterior of σr∗

-2 0 2 4 60

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Lewis & Vazquez-Grande (FRB) Measuring r∗ 13 / 34

Key Posterior Estimates Model II

Model II: ρg and µg estimated, ρz = 1

Smoothed output gap

Lewis & Vazquez-Grande (FRB) Measuring r∗ 14 / 34

Key Posterior Estimates Model II

Model II: ρg and µg estimated, ρz = 1

Smoothed g path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 15 / 34

Key Posterior Estimates Model II

Model II: ρg and µg estimated, ρz = 1

Smoothed z path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 16 / 34

Key Posterior Estimates Model II

Model II: ρg and µg estimated, ρz = 1

Posterior of σr∗

-2 0 2 4 60

0.2

0.4

0.6

0.8

1

1.2

1.4

Lewis & Vazquez-Grande (FRB) Measuring r∗ 17 / 34

Key Posterior Estimates Model II

Model II: ρg and µg estimated, ρz = 1

Posterior of ρg

-0.5 0 0.5 1 1.50

0.5

1

1.5

2

2.5

3

3.5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 18 / 34

Key Posterior Estimates Model II

Model II: ρg and µg estimated, ρz = 1

Posterior of µg (Quarterly)

0 0.5 1 1.50

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 19 / 34

Key Posterior Estimates Model III

Model III: ρg = 1, ρz estimated

Smoothed output gap

Lewis & Vazquez-Grande (FRB) Measuring r∗ 20 / 34

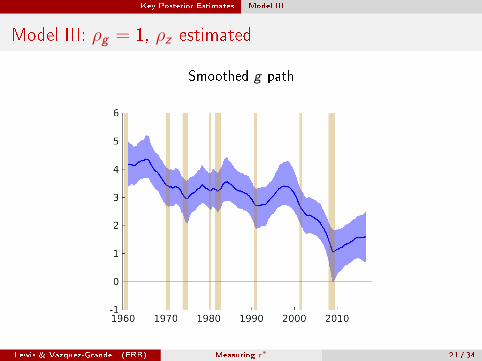

Key Posterior Estimates Model III

Model III: ρg = 1, ρz estimated

Smoothed g path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 21 / 34

Key Posterior Estimates Model III

Model III: ρg = 1, ρz estimated

Smoothed z path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 22 / 34

Key Posterior Estimates Model III

Model III: ρg = 1, ρz estimated

Posterior of σr∗

-2 0 2 4 60

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Lewis & Vazquez-Grande (FRB) Measuring r∗ 23 / 34

Key Posterior Estimates Model III

Model III: ρg = 1, ρz estimated

Posterior of ρz

-0.5 0 0.5 1 1.50

0.5

1

1.5

2

2.5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 24 / 34

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Smoothed output gap

Lewis & Vazquez-Grande (FRB) Measuring r∗ 25 / 34

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Smoothed g path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 26 / 34

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Smoothed z path

Lewis & Vazquez-Grande (FRB) Measuring r∗ 27 / 34

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Posterior of σr∗

-2 0 2 4 60

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Lewis & Vazquez-Grande (FRB) Measuring r∗ 28 / 34

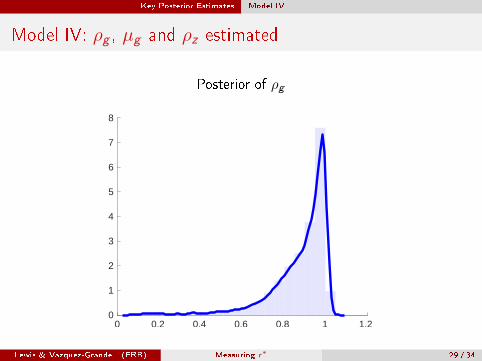

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Posterior of ρg

0 0.2 0.4 0.6 0.8 1 1.20

1

2

3

4

5

6

7

8

Lewis & Vazquez-Grande (FRB) Measuring r∗ 29 / 34

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Posterior of µg (Quarterly)

-1 -0.5 0 0.5 1 1.5 20

0.5

1

1.5

2

2.5

3

3.5

Lewis & Vazquez-Grande (FRB) Measuring r∗ 30 / 34

Key Posterior Estimates Model IV

Model IV: ρg , µg and ρz estimated

Posterior of ρz

-0.5 0 0.5 1 1.50

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Lewis & Vazquez-Grande (FRB) Measuring r∗ 31 / 34

Key Posterior Estimates Other parameters of interest

Model IV: ρg , µg and ρz estimated

Posterior of ar

-0.3 -0.2 -0.1 0 0.10

2

4

6

8

10

12

14

Lewis & Vazquez-Grande (FRB) Measuring r∗ 32 / 34

Key Posterior Estimates Other parameters of interest

Model IV: ρg , µg and ρz estimated

Posterior of bY

0 0.1 0.2 0.3 0.40

2

4

6

8

10

12

Lewis & Vazquez-Grande (FRB) Measuring r∗ 33 / 34

Key Posterior Estimates Other parameters of interest

Model IV: ρg , µg and ρz estimated

Posterior of b1

0.2 0.4 0.6 0.8 10

1

2

3

4

5

6

7

Lewis & Vazquez-Grande (FRB) Measuring r∗ 34 / 34