MCR_2012_web

228

-

Upload

iulia-vedislav -

Category

Documents

-

view

301 -

download

2

Transcript of MCR_2012_web

2012

MAJORCOMPANIESIN ROMANIA

MCR CONTENTS

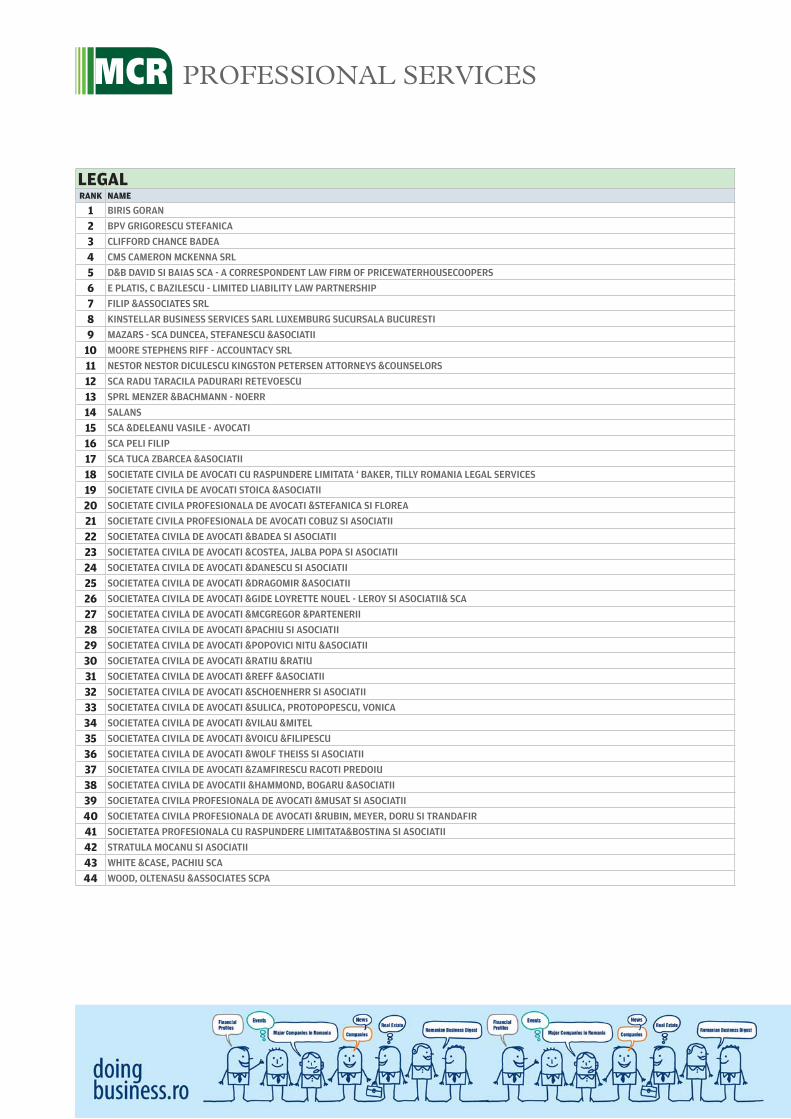

7 FROM THE EDITOR8 FOREWORD - Tracing the excellence pattern in Romanian industries - Bogdan Ion, Country Managing Partner, Ernst&Young Romania9 MCR RANKING METHODOLOGY11 TOP 300 MAJOR COMPANIES IN ROMANIA23 BANKING & FINANCE Banking in 2012 towards a more regulated market – Gabriela Bratu, Senior, Assurance& Advisory Business Services, Ernst&Young Doing Business In Romania – Steven van Groningen, President Raiffeisen Bank Romania, President Foreign Investors Council TOP Banking 2012 on the Merger and Acquisition market in the insurance sector – The re-launching year? – Cristina Cerbu, Manager, Transaction Advisory Services, Ernst&Young 2012, a year of challenges in insurance market – Violeta Ciurel, President & CEO, AXA Life Insurance TOP Insurance Financial leasing companies target – survival – Cristina Cerbu, Manager, Transaction Advisory Services, Ernst&Young TOP Financial Leasing Solid reasons to grow – Shane Dowling, General Manager, ALD Automotive TOP Operational Leasing TOP Pension Funding and TOP Capital Market Intermediation TOP Fund Management43 ENERGY Shining future for solar power – Andreea Stanciu, Senior Manager, Transaction Advisory Services, Ernst & Young, Mihaela Cuturescu, Senior Consultant, Transaction Advisory Services, Ernst & Young The right way? The Green way – Adrian Borotea, Member of the Board, CEZ Romania TOP Electric power generation and distribution TOP Oil & gas extraction and distribution TOP Whole sale of electricity and fuels TOP Retail trade of gas - gas stations53 CHEMICALS On way from politics to ECOnomics – Iulian Ernst, Freelance Analyst TOP Manufacture of basic chemicals TOP Wholesale of chemical products TOP Manufacture of rubber and plastic products - except tires TOP Manufacture of paints, varnishes and similar coatings, printing inks and mastics TOP Waste Management61 PHARMACEUTICALS Pharmaceutical Market – Reaping the fruits of past - Bogdan Tenu, Senior Manager, Transaction Advisory Services, Ernst & Young Invest in Romania - Dragos Damian, CEO Terapia Ranbaxy TOP Manufacture of basic pharmaceuticals TOP Retail trade of pharmaceuticals TOP Wholesale of pharmaceuticals69 GLASS & CERAMICS An industry war – Magda Munteanu, Freelance Journalist TOP Manufacture of glass and glass products TOP Manufacture of ceramic products

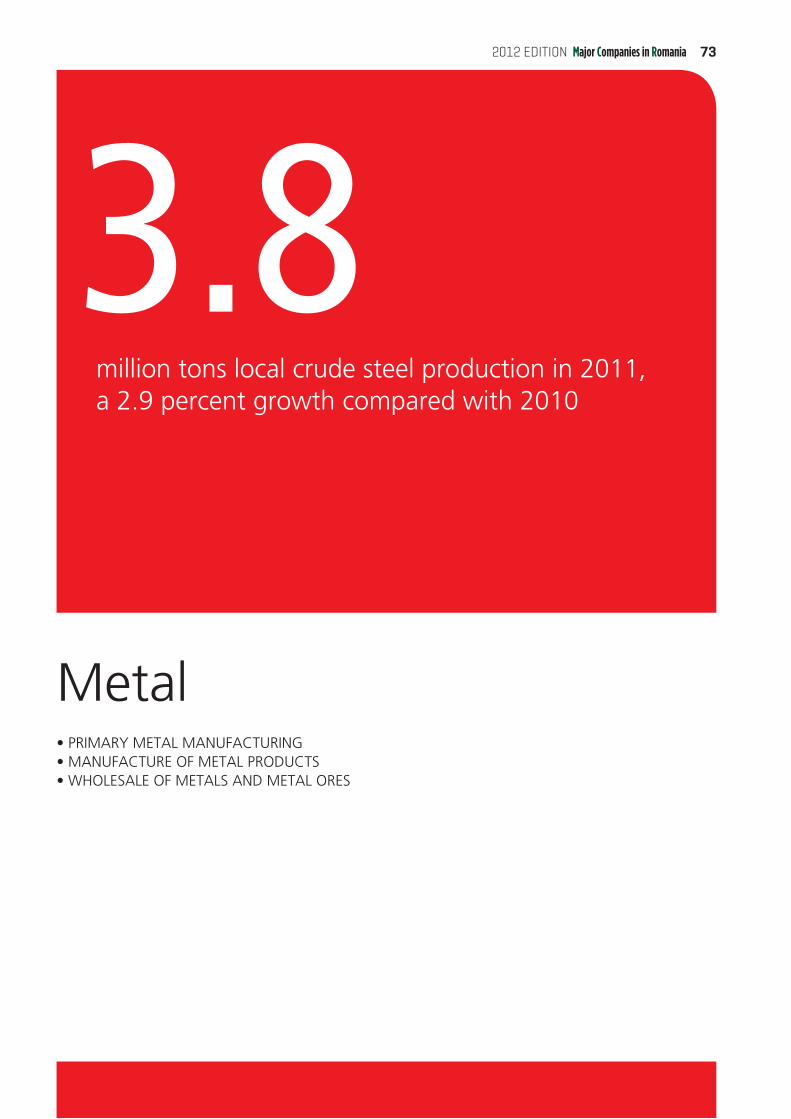

73 METAL Metal Industry faces bleak perspectives – Magda Munteanu, Freelance Journalist TOP Primary metal manufacturing TOP Manufacture of metal products TOP Wholesale of metals and metal ores81 MACHINERY Better than expected – Magda Munteanu, Freelance Journalist Let’s invest in skilled workforce – Alexandru Blemovici, General Manager, Schaeffler Romania TOP Manufacture of machinery, industrial equipment, ships and aircraft TOP Wholesale of machinery, industrial equipment, ships and aircraft89 ELECTRIC & ELECTRONIC EQUIPMENT Moderate raise keeps market afloat – Corina Mica, Freelance Journalist TOP Manufacture of electrical and electronic equipment TOP Trade of electrical and electronic equipment Manufacture of domestic appliances95 IT&C The mobile maze: when communication goes digital – Mirela Calota, Manager, Transaction Advisory Services, Ernst & Young In pursuit of a robust IT market – Carmen Dobre, Senior Manager, Transaction Advisory Services, Ernst & Young Growth comes from innovations – Jean - François Fallacher, CEO Orange Romania TOP Telecommunications TOP Communication equipment TOP Computer programming, consultancy and related activities TOP Manufacture and sale of computers and peripheral equipment105 INDUSTRIAL ENGINEERING Project Rush – Magda Purice, Journalist TOP Industrial engineering109 CONSTRUCTIONS Building industry’s performance returns on upward path, after two years of double-digit decline – Diana Macovei, Freelance Analist How to predict the unpredictable – Daniel Bach, CEO, Holcim Romania TOP Construction of residential & industrial buildings TOP Building materials TOP Construction of roads, railways, bridges and tunnels TOP Construction of electric sites TOP Construction of utility projects for fluids and related services TOP Hydro-technical constructions TOP Electrical, plumbing and other construction installation activities TOP Manufacture of equipment for construction industry119 REAL ESTATE The real state of real estate in Romania – Andreas Hadjidamianou, Partner, Assurance & Advisory Business Services, Ernst & Young Low appetite in real estate sight – Adrian Crivii FRICS, MAA, CEO, Darian DRS SA TOP Real estate evaluation companies TOP Real estate agencies TOP Real estate project developers TOP Property & facility management TOP Real estate asset managers

3Major Companies in Romania 2012 EDITION Major Companies in Romania

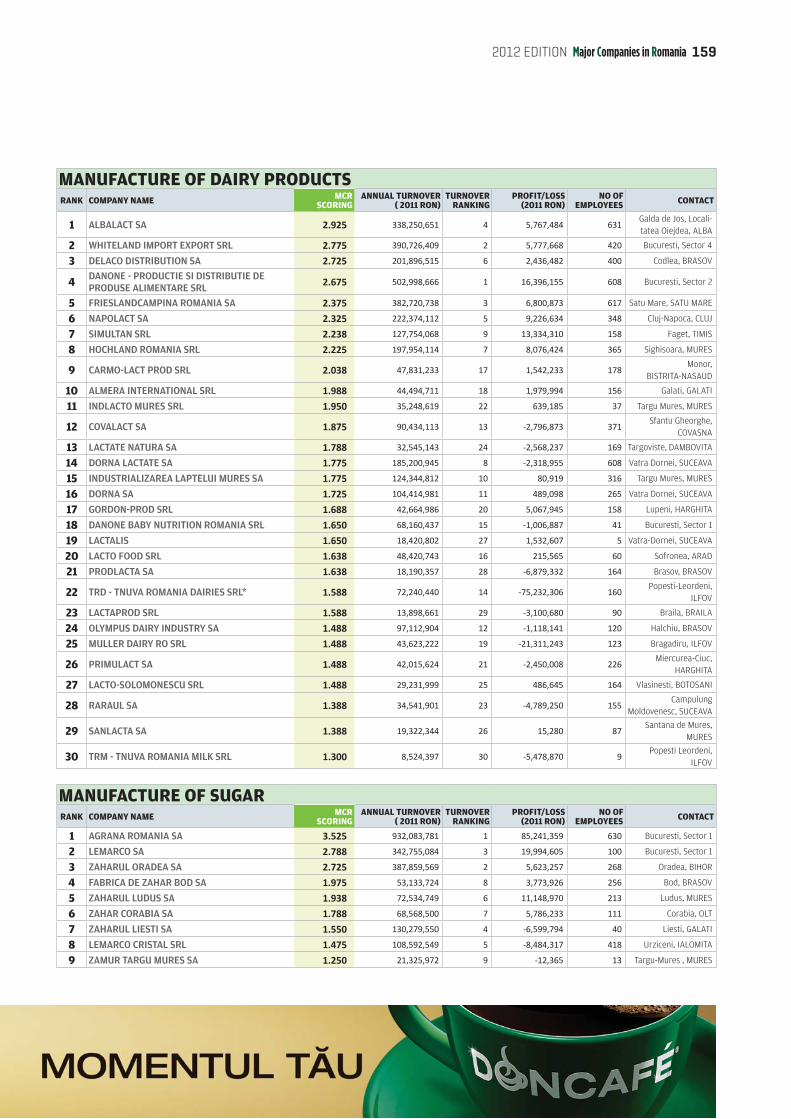

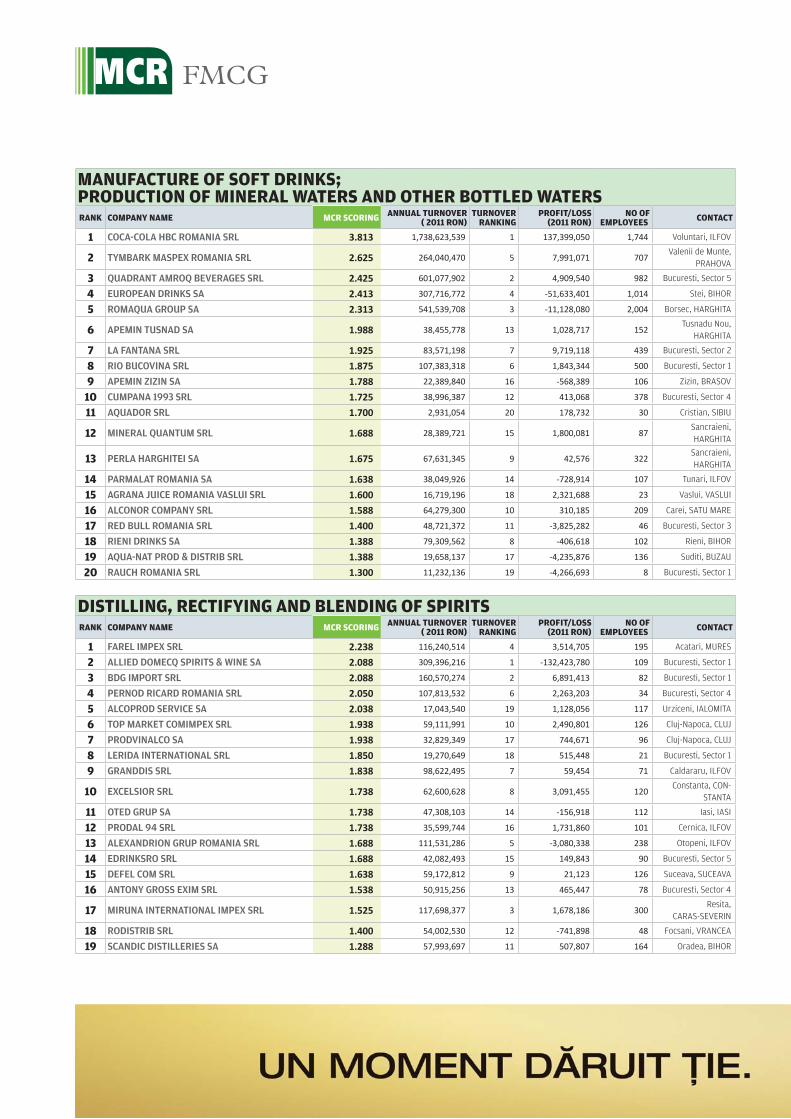

129 WOOD, PAPER & FURNITURE New investments need Government support – Corina Mica, Freelance Journalist A louder voice for Romanian design brands – Camelia Sucu, President, Class Leaving TOP Manufacture of wood and wooden products TOP Manufacture of furniture TOP Retail trade of furniture, carpets and lighting equipment TOP Manufacture of paper and paper products137 TEXTILE & LEATHER Production of textiles recovers slowly after the 2009 plunge – Diana Macovei, Freelance Analyst TOP Manufacture of wearing apparel TOP Preparation of textile fibers and textiles manufacture TOP Retail trade of clothing in specialised stores TOP Manufacture of footwear and leather goods TOP Retail trade of footwear and leather goods145 AGRICULTURE Romania’s eternal and fascinating promise – Iulian Ernst, Freelance Analyst Traders face unpredictable weathers – Angelo Nicolae, General Manager AgriBusiness at BriseGroup Constanta TOP Growing and trading agricultural raw materials TOP Growing and trading fruit and vegetables TOP Farming and meat processing153 FMCG How fast are consumer goods moving? – Corina Mica, Freelance Journalist X-Raying the Romanian coffee market – Marius Melesteu, General Manager Strauss Romania TOP Processing of tea and coffee TOP Manufacture of condiments and seasonings TOP Manufacture of tobacco products TOP Manufacture of cocoa, chocolate and confectionery TOP Manufacture of dairy products TOP Manufacture of sugar TOP Manufacture of grain mill products and starches TOP Manufacture of vegetable and animal oils and fats TOP Manufacture of wine from grape TOP Manufacture of beer TOP Manufacture of soft drinks; production of mineral waters and other bottled waters TOP Distilling, rectifying and blending of spirits TOP Home and personal care165 TRADE With a slow economic recovery ahead, retailers cannot afford to think short term – Marius Boatca, Manager, Transaction Advisory Services, Ernst & Young TOP Cash & Carry TOP Hypermarkets TOP Supermarkets TOP Do-it-yourself TOP Discount TOP Malls & Shopping centers

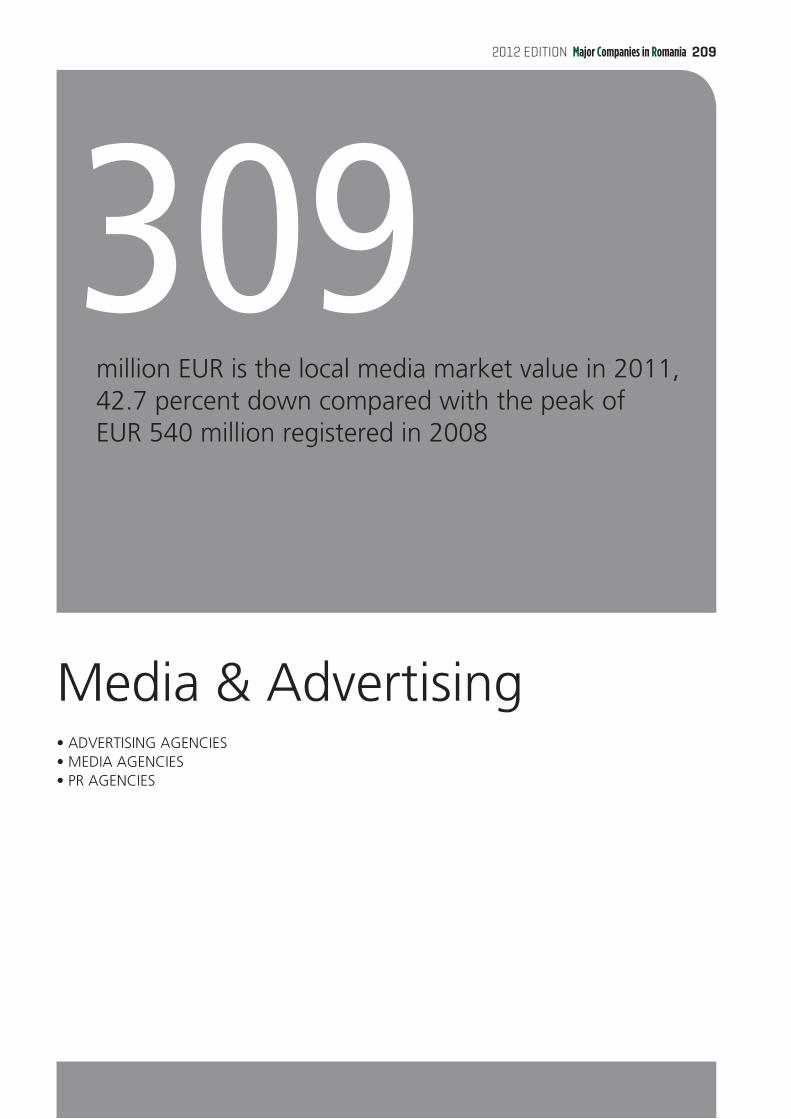

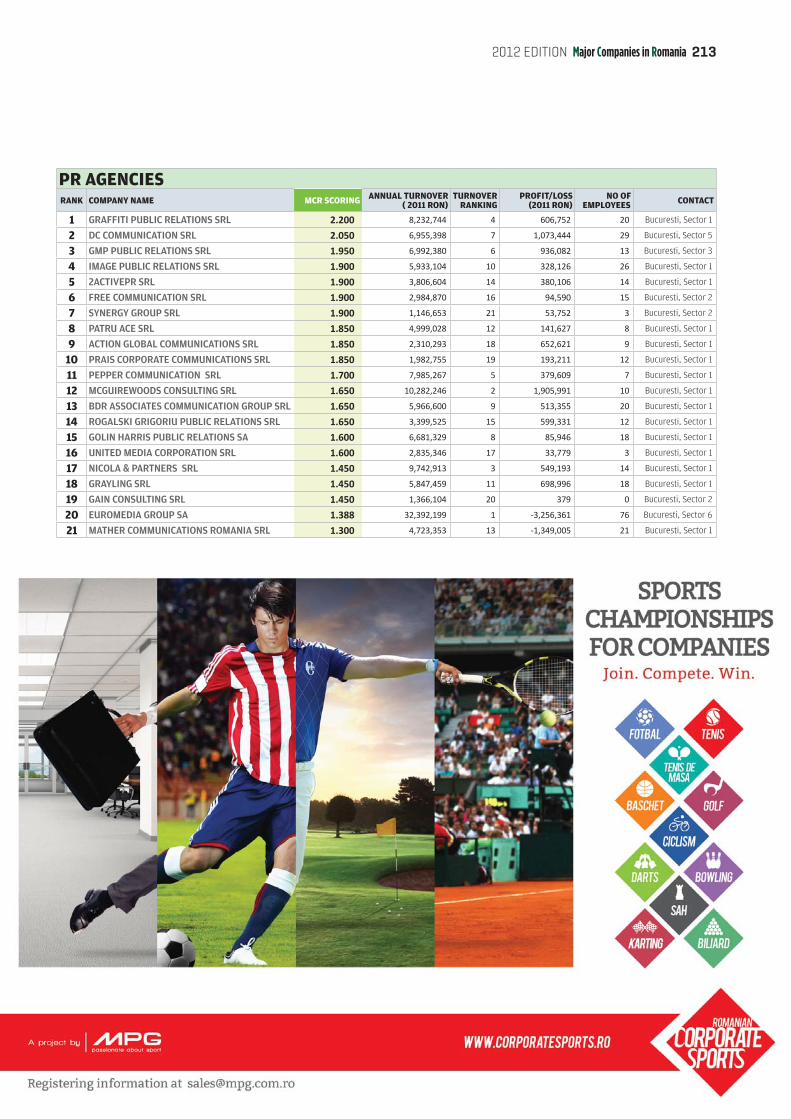

171 TRANSPORT & CARGO Long Road to effectiveness – Magda Purice, Journalist Getting into gear – Sergiu Iordache, Managing Director, DSV Solutions TOP Road transport TOP Maritime & river transport TOP Air transport TOP Rail transport TOP Freight transport TOP Postal and courier activities179 AUTOMOTIVE The Romanian automotive industry: changing gear or changing lanes? – Ariadna Oslobeanu, Senior Manager, Assurance & Advisory Business Services, Ernst & Young TOP Automotive producers & importers Back in 2000? – Dana Cortina, General Manager, Porsche Inter Auto Romania TOP Car dealers TOP Automotive parts producers TOP Automotive parts distributors 191 PROFESSIONAL SERVICES Circle of trust: relying on the right partner – Corina Mica, Freelance Journalist TOP Legal TOP Accounting, audit, FAS & tax TOP Business Process Outsourcing TOP Management consulting companies TOP Executive search, recruitment and HR management TOP Training companies TOP Market research companies203 BUSINESS SERVICES Tourism, not a walk in the park – Magda Purice, Journalist TOP Travel agencies TOP Security companies TOP Hotels and similar accommodation TOP Printing services209 MEDIA & ADVERTISING How to survive on a shrinking market – Corina Mica, Freelance Journalist TOP Advertising agencies TOP Media agencies TOP PR agencies215 HEALTH CARE The two-headed healthcare system – the dinosaur and the phoenix – Mihai A. Pop, MBA, Manager, Transaction Advisory Services, Ernst & Young The urge of threating with good will – Mihai Marcu, President, Medlife TOP Medical centers TOP Dental centers

MCR CONTENTS

MAJORCOMPANIESIN ROMANIA

doingbusiness.ro

Dumitru Ion

Roxana Neacsu

Madalina AthanasiuMirela BobeNicolae IonMagda Purice

Iulian ErnstDiana Macovei Corina MicaMagda MunteanuBogdan Preda

Raluca Butnariu

Marian CaramihaiIlie Toader

Carmen Popescu

Teodora DanciuCatalin LucaRamona RaicuElena VijoliCatalin Zaf iu

Edited by:

General Manager:

Project Manager:

Project team:

Contributors:

IT & Web Development:

DTP & Grafic design:

Production:

Sales:

Copyright © 2012doingbusiness.ro

Strada Prof. Ion Bogdannr. 4-6, etaj 4,

sector 1, BucureştiPhone: +40 21 528 0408

Fax: +40 21 528 0409E-mail: [email protected]

www.doingbusiness.ro

The Publisher cannot, under any circumstances, assume responsibility for any kind of damages supposing to be resulted from the use of the information provided by this publication. The information included into printed edition of Major Companies of Romania, was provided by sources we considered to be reliable: Trade Register, National Bank of Romania, Bucharest Stock Exchange, The Insurance Supervisory Commission, The Romanian Pension Funds' Association, Romanian Association of Fund Managers, Ministry of Finance, companies themselves. However the Publisher cannot take responsibility for the information accuracy.

* the companies from TOPs, marked this way, were, based on our information, on the moment of our analysis under the incidence of the law 85/2006 – insolvency.

No part of this publication may be reproduced, copied or distributed in any form or by any means, electronic or printed, without mentioning the source, respectively the publisher or the contributor.

Distribution: Major Companies in Romania is distributed for free. Copy available only free of charge, not for sale.

Printed byTipografia Everest 2001

7

Major Companies in Romania

This note is not about detailed techniques or complicated numbers. It’s about what prompted us (again) to prepare the new edition of Major Companies in Romania.

In good times and bad times alike we feel we need to know who has remained strong, who is struggling to become stronger and who is fighting to avert weaknesses. That’s because we want to share these findings with you. We want to be the most qualified tellers of corporate performance criteria because this will also make you the happy users of the data, and equally more qualified critics and observers of the business environment.

Knowing all these is not as simple as drawing tables or punching in numbers such as turnovers, revenues or net incomes into a computer. We believe that wouldn’t be enough and, above all, wouldn’t be relevant. At least not as far as we’re concerned. That’s because this is ultimately about helping you not only with knowing business but also with doing business in Romania. And that’s also why we called in our partners in this project, the experts at Ernst & Young Romania to help us again produce this edition by making a real difference with their unparalleled knowledge.

We genuinely believe that the product we developed together with Ernst & Young has become one of a kind in Romania as far as the truly relevant enterprise rankings and scoring algorithms are concerned. Firstly, that’s because we believe no one else uses so many quantitative and qualitative indicators as we do. Then again, and equally important, because we bring in experts and observers to tell the story behind each and every industry that we assess in our Major Companies in Romania. Additionally, we’ve also added some of the most qualified opinions for more than half of the industries and sectors that we’re presenting in this issue. Last but not least, we believe that making all this data available online will turn our work into a truly helpful database that all of you can access from everywhere, at anytime without having to carry the print version with you at all times.

MCR From the editor

Major Companies in Romania - Turning into a MAJOR habit

2012 EDITION Major Companies in Romania

The Editorial Team

We happen to know and to understand that the harsher the economic times are or shall be, the more important it is that our readers get the right picture about what is, was, or is about to happen. We’ve already predicted in our latest separate publication (the Romanian Business Digest) that Romania is now heading for The Real Crossroad, a junction point that’s going to determine the way business will be carried forward for the next few years to come. Therefore, we feel our current X-ray of the Major Companies in Romania needs to be as accurate and as real as it can get.

As such, we’ve first selected 5,000 companies from among which we analyzed, scored and ranked more than 2,400 from 23 different industries and sectors in Romania, with the primary data obtained from the Trade Registry and the Finance Ministry. In the case of financial entities and banks, we used the primary data from the National Bank of Romania and the Romanian Insurance Supervisory Commission.

We’re happy to also offer you the rankings of the top 300 companies in Romania (bar the banking and financial institutions that are treated separately due to their specifics) and 23 chapters that altogether reveal another 100 rankings.

It has been a real effort on our side, and yet we hope a useful one for you.

We therefore hope you’ll enjoy reading and using this product. As of now, it belongs to you.

Creating value. Achieving potential.

It is four years since many countries around the world have been struggling with what we used to call the economic crisis. We are seeing paradox evolutions of many economies in Europe, with various industries acting differently from one region to another and from one moment to another.

In Romania, 2012 has been a challenging year for all players in the market. They faced the contagious impact of evolutions in Europe, while the local political uncertainty hampered the competitiveness of our economy.

Drawing closer to the end of the year, it is crucial to identify and acknowledge the reference players and the industry landmarks that are driving value creation in today’s market. By looking at the performance footprint of industry leaders, we can map the industry hot spots and the attractiveness drivers of the local economy.

It is why the Ernst & Young Transaction Advisory team has contributed to this year’s edition of Major Companies in Romania. As a global company, tapping into 140 diverse economies all over the world, at Ernst & Young, we support a wide range of companies, enabling us to draw specific insights from every market where we are present. This year, we mark a great milestone, by celebrating 20 years of continuous achievements in Romania. In this context, we have committed to developing and sharing a comprehensive insight into the Romanian economic environment.

Together with the doingbusiness.ro team, we have designed a multifaceted methodology capturing all the qualitative and quantitative aspects that make the profile of the strongest, most competitive major companies on the market. We pursued this unique project with the goal to build a reference instrument that can assist potential foreign investors, local firms as well as entrepreneurs, when looking at the business landscape in Romania.

Through Major Companies in Romania, we bring forward a general ranking of the most performing 100 companies in the country, highlighting how positive results are distributed in the economy today. But even more importantly, through our methodology, we have put together specific analysis of 24 Romanian industry sectors, bringing a unique outline of market trends and predictions.

MCR Foreward

Tracing the excellence pattern in Romanian industries

BOGDAN ION,Country Managing Partner,Ernst & Young Romania

This overview book that concludes our research for 2012 is more than a collection of rankings and industry outlooks. It is in a sense a White Paper of the Romanian economy that can assist top executives in planning their strategy for 2013. Emerging countries, such as Romania, are not only economically significant at the moment, but will be the growth engine for the global economy going forward. Business leaders across Central and Eastern Europe are still cautious about their investments in the region, but many see reasonable business potential in Romania, expecting it to act as a regional power-house.

Romania has a long way to go in building a strong competitive market. The foundation is however here, boasting promising perspectives for the post-recession years. It is clear that nobody will step up and put the pieces together if the business community doesn’t take the lead. We need to drive the Romanian market into the regional and global competition, if we want to turn its promising opportunities into reality.

92012 EDITION Major Companies in Romania

doingbusiness.ro and Ernst & Young developed the present study by analyzing a composite mix of indicators based on the results reported by companies registered in Romania for 2011. Ernst & Young, together with doingbusiness.ro, have put together an in-depth assessment algorithm, which balances the most relevant business performance indicators, factoring in the particular conditions of today’s economic context. The ranking methodology includes a scoring system by which each company is assessed, based on turnover, financial and non-financial aspects, all considered by separate weights which reflect our insights regarding the specifics of doing business in the local market.

The most important criteria taken into consideration by our methodology was the turnover reported by the companies in 2011. This was further weighted alongside other financial and non-financial performance aspects. The indicators included in this methodology are computed based on public information disclosed either by authorized bodies and institutions or by the companies themselves.

The analysis of non-financial indicators was applied to aspects such as average number of employees, type of company (listed, unlisted), corporate social responsibility and environmental initiatives developed in Romania as well as the contribution to developing a local brand.

The financial indicators were computed based on information extracted from annual financial statements as at 31 December 2011. A number of financial indicators were

selected, such as Earnings before Interest, Taxes, Amortization and Depreciation (EBITDA) growth, Current Ratio, Return on Equity Ratio, Debt to Equity Ratio and Interest Coverage Ratio.

Each indicator has been assessed based on a scoring grid from 1 to 5 allotted for specific value intervals, 1 being the value assigned for the lowest performance and 5 being assigned for the highest performance.

This year, we have also developed a separate methodology for the banking sector. Apart from Total Assets, which represent the major size measure, we have considered other indicators such as the Net Banking Income growth, Return on Equity and Loans/Deposits Ratio.

With this revised approach, Major Companies in Romania looks at the performance of companies registered in Romania that have filed the financial statements for the year ended 31 December 2011 with the Trade Register. Companies that have not submitted their financial statements for 2011 were not included in this analysis. Ernst & Young was pleased to bring its contribution to Major Companies in Romania drawing upon its significant experience in serving leading companies and investors across various industry sectors. Our 20 years of experience on the local market allowed us to thoroughly customize the research algorithm in order to reflect the particular aspects of doing business in Romania.

MCR MCR Methodology

Ranking methodology for Major Companies in Romania Developed by Ernst & Young Romania and doingbusiness.ro

Top 300 Major Companies in RomaniaACTIVE AND PROFITABLE IN 2011

626,604 REGISTERED ACTIVE COMPANIES 360,333 COMPANIES POSTED PROFITS (58 PERCENT) 266,274 COMPANIES POSTED LOSSES (42 PERCENT) 623,231 PRIVATE-HELD COMPANIES 772 STATE-OWNED COMPANIES

112012 EDITION Major Companies in Romania

6thRomania’s ranking as the most attractive European country for investments over the next 3 years

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

1 OMV PETROM SA 4.950 16,565,465,973 1 3,685,607,226 22,052 Bucuresti, Sector 1

2 AUTOMOBILE DACIA SA 4.500 13,177,841,584 3 275,111,397 13,652 Mioveni, ARGES

3 BRITISH AMERICAN TOBACCO (ROMANIA) TRADING SRL

4.475 6,051,829,824 7 317,054,628 299 Bucuresti, Sector 1

4 SOCIETATEA NATIONALA DE GAZE NATURALE ROMGAZ SA

4.400 4,211,149,514 13 1,031,748,972 5,779 Medias, SIBIU

5 OMV PETROM MARKETING SRL 4.375 13,684,564,230 2 125,396,136 356 Bucuresti, Sector 1

6 KAUFLAND ROMANIA SCS 4.350 5,586,202,967 8 167,624,061 10,493 Bucuresti, Sector 2

7 METRO CASH & CARRY ROMANIA SRL 4.300 4,963,012,603 10 95,208,230 6,003 Bucuresti, Sector 3

8 CARREFOUR ROMANIA SA 4.300 4,031,266,685 16 133,799,794 6,951 Bucuresti, Sector 6

9 AZOMURES SA 4.263 1,625,577,204 55 365,196,441 2,688 Tg. Mures, MURES

10 ROMPETROL RAFINARE SA 4.213 10,174,808,952 4 -735,847,584 1,103 Navodari,

CONSTANTA

11 COMPANIA NATIONALA DE TRANSPORT AL ENERGIEI ELECTRICE - TRANSELECTRICA SA

4.163 3,113,142,778 22 90,913,316 2,197 Bucuresti, Sector 1

12 ALRO SA 4.163 2,241,390,928 33 228,309,982 2,513 Slatina, OLT

13 DEDEMAN SRL 4.063 2,016,376,729 39 205,670,978 4,646 Bacau, BACAU

14 PIRELLI TYRES ROMANIA SRL 4.013 1,501,679,442 63 94,411,056 1,890 Slatina, OLT

15 GDF SUEZ ENERGY ROMANIA SA 3.975 4,090,867,846 15 209,555,220 740 Bucuresti, Sector 4

16 ROMPETROL DOWNSTREAM SRL 3.963 7,645,953,049 5 -108,229,346 2,499 Bucuresti, Sector 1

17 NOKIA ROMANIA SRL 3.963 4,103,613,593 14 -8,770,342 1,866 Cluj-Napoca, CLUJ

18 HOLZINDUSTRIE SCHWEIGHOFER SRL 3.913 1,589,521,923 56 312,866,728 1,267 Sebes, ALBA

19 TAKATA ROMANIA SRL 3.913 1,522,320,748 62 46,228,727 4,230 Arad, ARAD

20 MEGA IMAGE SRL 3.913 1,221,043,229 78 13,097,320 4,277 Bucuresti, Sector 1

21 ARCELORMITTAL GALATI SA 3.900 4,663,330,401 11 -620,130,335 8,755 Galati, GALATI

22 INTERAGRO SA 3.875 2,741,108,028 27 162,792,694 257 Bucuresti, Sector 2

23 FARMEXPERT DCI SA 3.875 1,821,368,650 46 86,369,568 623 Bucuresti, Sector 6

24 COFICAB EASTERN EUROPE SRL 3.875 1,133,672,090 84 63,538,680 378 Arad, ARAD

25 LUKOIL ROMANIA SRL 3.863 5,458,206,353 9 -115,201,885 3,460 Bucuresti, Sector 1

26 ELECTRICA FURNIZARE SA 3.863 1,751,474,401 48 84,527,445 1,156 Bucuresti, Sector 2

27 SILCOTUB SA 3.863 1,442,409,942 65 107,588,856 1,348 Zalau, SALAJ

28 POLISANO SRL 3.825 1,245,539,397 76 42,157,465 639 Sibiu, SIBIU

29 CELESTICA ( ROMANIA ) SRL 3.813 2,357,993,685 31 12,519,199 1,163 Bors, BIHOR

30 AUTOLIV ROMANIA SRL 3.813 1,911,619,925 42 160,959,700 3,101 Brasov, BRASOV

31 COCA-COLA HBC ROMANIA SRL 3.813 1,738,623,539 50 137,399,050 1,744 Voluntari, ILFOV

32 SOCIETATEA COMERCIALA COMPLEXUL ENERGETIC TURCENI SA

3.813 1,529,901,979 61 55,567,882 4,496 Turceni, GORJ

33 SOCIETATEA NATIONALA DE TRANSPORT GAZE NATURALE TRANSGAZ SA

3.813 1,343,321,806 71 379,571,465 4,951 Medias, SIBIU

34 BILLA ROMANIA SRL 3.813 1,127,473,002 85 5,222,261 2,734 Bucuresti, Sector 2

35 HEINEKEN ROMANIA SA 3.813 1,042,285,902 97 182,888,969 1,198 Bucuresti, Sector 1

36 OMV PETROM GAS SRL 3.800 3,110,115,994 23 137,804,129 45 Bucuresti, Sector 2

37 SAMSUNG ELECTRONICS ROMANIA SRL 3.788 1,530,472,159 60 31,852,822 90 Voluntari, ILFOV

38 PETROTEL - LUKOIL SA 3.775 6,625,679,238 6 -391,609,120 556 Ploiesti, PRAHOVA

39 EON ENERGIE ROMANIA SA 3.775 4,261,045,806 12 -191,719,192 559 Targu Mures, MURES

40 MEDIPLUS EXIM SRL 3.775 2,700,529,658 28 56,231,206 900 Mogosoaia, ILFOV

41 ORANGE ROMANIA SA 3.763 3,981,959,733 17 805,637,899 2,707 Bucuresti, Sector 1

42 VODAFONE ROMANIA SA 3.763 3,399,602,653 20 425,484,737 2,951 Bucuresti, Sector 1

43 ARABESQUE SRL 3.763 1,715,508,601 52 34,635,851 2,530 Galati, GALATI

44 ROMANIA HYPERMARCHE SA 3.763 1,378,385,595 69 39,962,988 3,665 Bucuresti, Sector 3

45 DISTRIGAZ SUD RETELE SRL 3.763 1,099,691,738 92 135,369,392 3,112 Bucuresti, Sector 4

132012 EDITION Major Companies in Romania

MCR TOP 300

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

46 HIDROCONSTRUCTIA SA 3.750 1,002,178,651 101 50,428,795 6,528 Bucuresti, Sector 1

47 SELGROS CASH & CARRY SRL 3.713 3,408,091,410 19 86,702,217 4,248 Brasov, BRASOV

48 COMPLEXUL ENERGETIC CRAIOVA SA 3.713 1,228,075,942 77 795,421 2,175 Craiova, DOLJ

49 MECHEL TARGOVISTE SA 3.713 1,099,750,708 91 -133,495,504 2,250 Targoviste,

DAMBOVITA

50 SOCIETATEA COMERCIALA COMPLEXUL ENERGETIC ROVINARI SA

3.713 1,017,710,306 99 33,385,699 4,380 Rovinari, GORJ

51 REGIA NATIONALA A PADURILOR ROMSILVA RA

3.700 1,204,391,260 80 20,787,107 18,601 Bucuresti, Sector

52 JT INTERNATIONAL (ROMANIA) SRL 3.675 2,375,824,912 29 6,030,690 577 Bucuresti, Sector 2

53 EUROPHARM HOLDING SA 3.675 1,024,526,005 98 11,236,244 344 Brasov, BRASOV

54 CONTINENTAL AUTOMOTIVE PRODUCTS SRL 3.650 2,224,673,603 34 202,239,107 - Timisoara, TIMIS

55 DELPHI PACKARD ROMANIA SRL 3.650 1,700,702,239 53 34,612,356 9,812 Sannicolau Mare,

TIMIS

56 COMPANIA NATIONALA DE AUTOSTRAZI SI DRUMURI NATIONALE DIN ROMANIA SA

3.650 1,008,605,903 100 246,292,679 5,867 Bucuresti, Sector 1

57 PHILIP MORRIS TRADING SRL 3.625 2,362,448,641 30 14,966,343 270 Otopeni, ILFOV

58 DAEWOO-MANGALIA HEAVY INDUSTRIES SA 3.613 1,725,406,261 51 -72,788,618 3,065 Mangalia,

CONSTANTA

59 OLTCHIM SA 3.613 1,533,016,194 59 -278,342,623 3,447 Ramnicu Valcea,

VALCEA

60 ARCTIC SA 3.613 1,073,231,988 95 42,149,099 2,532 Gaesti, DAMBOVITA

61 TMK-ARTROM SA 3.613 856,313,578 116 67,503,261 1,141 Slatina, OLT

62 WIEE ROMANIA SRL 3.600 1,104,270,989 90 -21,896,147 7 Bucuresti, Sector 1

63 PROCTER & GAMBLE DISTRIBUTION SRL 3.600 1,253,875,543 75 22,697,889 45 Bucuresti, Sector 2

64 OSCAR DOWNSTREAM SRL 3.588 2,250,309,163 32 26,778,021 240 Bucuresti, Sector 6

65 TINMAR - IND SA 3.588 1,402,890,170 67 21,539,140 52 Bucuresti, Sector 1

66 AGRO-CHIRNOGI SA 3.575 1,124,597,971 86 20,812,621 574 Chirnogi, CALARASI

67 ELECTROCENTRALE BUCURESTI SA 3.563 2,180,397,722 36 106,854,822 3,100 Bucuresti, Sector 6

68 MICHELIN ROMANIA SA 3.563 2,146,783,116 37 44,927,593 2,657 Bucuresti, Sector 1

69 RCS & RDS SA 3.550 2,028,873,472 38 -12,542,312 6,910 Bucuresti, Sector 5

70 PORSCHE ROMANIA SRL 3.538 1,798,618,534 47 114,723,266 150 Voluntari, ILFOV

71 AGRANA ROMANIA SA 3.525 932,083,781 109 85,241,359 630 Bucuresti, Sector 1

72 REWE (ROMANIA) SRL 3.513 1,750,171,052 49 5,145,553 2,493Stefanestii de Jos,

ILFOV

73 SCHAEFFLER ROMANIA SRL 3.513 1,481,631,232 64 7,417,486 3,267 Comuna Cristian,

BRASOV

74 ENEL ENERGIE MUNTENIA SA 3.475 1,842,264,078 45 -1,297,079 257 Bucuresti, Sector 1

75 SOCIETATEA NATIONALA NUCLEARELECTRICA SA

3.463 1,588,353,753 57 95,036,272 2,167 Bucuresti, Sector 1

76 DELPHI DIESEL SYSTEMS ROMANIA SRL 3.463 1,317,523,227 72 47,686,003 2,070 Bratuleni, IASI

77 PROFI ROM FOOD SRL 3.463 934,039,541 107 13,222,420 2,476 Timisoara, TIMIS

78SOCIETATEA COMERCIALA DE PRODUCERE A ENERGIEI ELECTRICE IN HIDROCENTRALE &HIDROELECTRICA&SA

3.450 3,020,591,574 24 6,444,266 5,243 Bucuresti, Sector 2

79 COMPANIA NATIONALA POSTA ROMANA SA 3.450 1,264,810,799 73 -182,932,177 32,124 Bucuresti, Sector 2

80 SOCIETATEA NATIONALA DE TRANSPORT FEROVIAR DE MARFA - CFR MARFA - SA

3.450 1,107,684,939 89 -93,452,745 9,145 Bucuresti, Sector 1

81 EXPUR SA 3.425 781,211,255 130 106,983,324 473 Urziceni, IALOMITA

82 COMPANIA NATIONALA “LOTERIA ROMANA” SA

3.413 1,160,084,883 81 81,659,837 2,709 Bucuresti, Sector 4

83 SOCIETATEA NATIONALA DE TRANSPORT FEROVIAR DE CALATORI CFR CALATORI SA

3.400 2,189,750,845 35 1,522,533 13,924 Bucuresti, Sector 1

84 BUNGE ROMANIA SRL 3.388 1,377,067,121 70 -232,841 237 Buzau, BUZAU

MCR TOP 300

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

85 REMAT SA 3.388 749,609,421 137 10,710,524 133 Calarasi, CALARASI

86 COSMOTE ROMANIAN MOBILE TELECOMMUNICATIONS SA

3.363 1,944,725,623 41 -30,803,300 1,234 Bucuresti, Sector 6

87 LIDL DISCOUNT SRL 3.363 1,678,989,043 54 -283,414,839 2,325 Nedelea, PRAHOVA

88 JOHNSON CONTROLS ROMANIA SRL 3.363 1,119,868,177 87 -10,661,767 3,350 Mioveni, ARGES

89 URSUS BREWERIES SA 3.363 1,108,012,643 88 -57,660,007 1,440 Bucuresti, Sector 1

90 DUCTIL STEEL SA 3.363 1,047,689,527 96 -141,648,777 1,507 Buzau, BUZAU

91 COMPANIA NATIONALA DE CAI FERATE CFR SA

3.350 1,149,704,461 82 -708,455,012 23,839 Bucuresti, Sector 1

92 CARGILL AGRICULTURA SRL 3.338 2,897,665,343 26 31,583,472 249 Bucuresti, Sector 1

93 SANOFI-AVENTIS ROMANIA SRL 3.338 848,148,293 118 19,095,940 187 Bucuresti, Sector 5

94 AUCHAN ROMANIA SA 3.313 1,578,059,613 58 -7,152,681 3,289 Bucuresti, Sector 1

95 ALTEX ROMANIA SRL 3.313 882,765,222 113 29,575,030 1,435 Piatra Neamt,

NEAMT

96 TRW AUTOMOTIVE SAFETY SYSTEMS SRL 3.313 878,392,258 114 23,484,769 2,788 Timisoara, TIMIS

97 REGIA AUTONOMA PENTRU ACTIVITATI NUCLEARE RA

3.313 715,991,743 144 37,774,933 3,659 Drobeta Turnu

Severin, MEHEDINTI

98 PROSPECTIUNI SA 3.313 315,293,527 345 30,981,821 1,604 Bucuresti, Sector 1

99 real,- HYPERMARKET ROMANIA SRL 3.300 3,008,864,542 25 -120,760,658 5,771 Bucuresti, Sector 3

100 MOL ROMANIA PETROLEUM PRODUCTS SRL 3.288 3,137,003,249 21 -13,397,874 176 Bucuresti, Sector 1

101 ROCHE ROMANIA SRL 3.288 1,090,313,389 93 149,697 225 Bucuresti, Sector 2

102 MERCEDES-BENZ ROMANIA SRL 3.288 764,704,445 132 26,137,904 136 Bucuresti, Sector 1

103 ENEL ENERGIE SA 3.275 1,897,153,560 43 -43,137,204 412 Bucuresti, Sector 1

104 ROMPETROL PETROCHEMICALS SRL 3.275 1,077,761,809 94 -151,271,747 471 Navodari,

CONSTANTA

105 GLAXOSMITHKLINE (GSK) SRL 3.275 723,741,502 142 21,173,671 300 Bucuresti, Sector 1

106 CONTINENTAL AUTOMOTIVE SYSTEMS SRL 3.263 1,264,430,015 74 -104,789,414 1,577 Sibiu, SIBIU

107 REGIA AUTONOMA DE DISTRIBUTIE A ENERGIEI TERMICE BUCURESTI RADET RA

3.263 1,208,837,877 79 -904,421,089 4,281 Bucuresti, Sector 3

108 CONTINENTAL AUTOMOTIVE ROMANIA SRL 3.263 1,139,142,245 83 -150,597,676 3,461 Timisoara, TIMIS

109 EON GAZ DISTRIBUTIE SA 3.263 800,458,510 124 230,492,490 3,747 Targu Mures, MURES

110 GRUP FEROVIAR ROMAN SA 3.263 761,053,345 134 28,920,981 2,386 Bucuresti, Sector 1

111SOCIETATEA COMERCIALA DE DISTRIBUTIE SI FURNIZARE A ENERGIEI ELECTRICE - ELECTRICA SA

3.238 1,438,037,720 66 7,148,124 247 Bucuresti, Sector 1

112 LAFARGE CIMENT (ROMANIA) SA 3.225 764,608,960 133 180,109,955 502 Bucuresti, Sector 1

113 FARMACEUTICA REMEDIA SA 3.225 203,467,822 527 4,077,449 395 Deva, HUNEDOARA

114 EATON ELECTRO PRODUCTIE SRL 3.213 814,087,797 120 35,083,922 1,829 Sarbi, MARAMURES

115 CEZ DISTRIBUTIE SA 3.213 809,391,603 122 130,458,811 1,345 Craiova, DOLJ

116 ARCELORMITTAL TUBULAR PRODUCTS ROMAN SA

3.213 748,109,975 138 -26,449,686 1,149 Roman, NEAMT

117 CEZ VANZARE SA 3.200 1,395,974,833 68 -31,316,430 48 Craiova, DOLJ

118 SEWS ROMANIA SRL 3.200 905,507,808 111 5,699,559 6974 Deva, Hunedoara

119 ALFRED C TOEPFER INTERNATIONAL (ROMANIA) SRL

3.188 1,848,711,705 44 -17,460,690 138 Bucuresti, Sector 2

120 LLK LUBRICANTS ROMANIA SRL 3.188 870,188,203 115 12,085,649 98 Ploiesti, PRAHOVA

121 JT INTERNATIONAL MANUFACTURING SA 3.175 1,979,436,255 40 -12,647,951 318 Bucuresti, Sector 2

122 MECHEL SERVICE ROMANIA SRL 3.175 816,528,524 119 14,770,336 365 Bucuresti, Sector 3

123 ADM FARM SRL 3.175 781,828,812 129 8,883,553 556 Pantelimon, ILFOV

124 SIEPCOFAR SA 3.163 755,620,215 136 6,830,066 1,300 Popesti-Leordeni,

ILFOV

125 RENAULT INDUSTRIE ROUMANIE SRL 3.150 3,944,561,044 18 1,048,546 1 Mioveni, ARGES

126 PLANOIL SRL 3.150 721,535,851 143 3,716,261 20 Bucuresti, Sector 1

152012 EDITION Major Companies in Romania

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

127 FARMEXIM SA 3.125 972,471,927 102 10,316,324 549 Bucuresti, Sector 2

128 CARPATCEMENT HOLDING SA 3.125 812,746,577 121 142,116,730 814 Bucuresti, Sector 1

129 COMPA SA 3.113 475,420,370 223 17,369,837 1,782 Sibiu, SIBIU

130 ANTIBIOTICE SA 3.113 281,847,455 391 20,298,909 1,450 Iasi, IASI

131 MAIRON GALATI SA 3.075 883,323,141 112 29,629,929 367 Galati, GALATI

132 ALUM SA 3.075 574,237,971 184 32,562,133 719 Tulcea, TULCEA

133 ROPHARMA SA 3.075 385,169,835 283 10,687,756 756 Brasov, BRASOV

134 ELECTROCENTRALE DEVA SA 3.063 778,330,788 131 2,499,075 1,506 Mintia, HUNEDOARA

135 ENEL DISTRIBUTIE MUNTENIA SA 3.063 705,878,691 146 50,470,639 1,302 Bucuresti, Sector 1

136 ERICSSON TELECOMMUNICATIONS ROMANIA SRL

3.063 543,675,580 193 26,220,612 1,433 Bucuresti, Sector 1

137 STX RO OFFSHORE BRAILA SA 3.063 375,914,905 291 50,378,911 1,815 Braila, BRAILA

138 ARA SHOES ROMANIA SRL 3.063 220,667,632 483 7,114,881 1,548 Valea lui Mihai,

BIHOR

139 HOLCIM (ROMANIA) SA 3.025 943,855,284 105 74,029,255 948 Bucuresti, Sector 1

140 FILDAS TRADING SRL 3.025 935,162,376 106 24,596,603 499 Pitesti, ARGES

141 LAMINORUL SA 3.025 933,973,827 108 -132,867,299 667 Braila, BRAILA

142 DAN STEEL GROUP BECLEAN SA 3.025 278,347,307 393 5,058,202 684 Beclean,

BISTRITA-NASAUD

143 STIROM SA 3.025 207,570,716 515 19,462,703 421 Bucuresti, Sector 3

144 SENSIBLU SRL 3.013 920,786,955 110 1,166,452 2,133 Mogosoaia, ILFOV

145 ADMINISTRATIA ROMANA A SERVICIILOR DE TRAFIC AERIAN ROMATSA RA

3.013 742,857,431 140 45,403,645 1,545 Bucuresti, Sector 1

146 GENPACT ROMANIA SRL 3.013 220,997,557 482 26,277,385 1,571 Bucuresti, Sector 2

147 CRH ROMANIA SRL 2.975 383,968,466 286 29,874,301 550 Jimbolia, TIMIS

148 GREENFIBER INTERNATIONAL SA 2.975 310,406,128 353 21,457,151 533 Buzau, BUZAU

149 DALKIA TERMO PRAHOVA SRL 2.975 236,541,218 451 27,868,421 429 Ploiesti, Prahova

150 DOMO RETAIL SA 2.963 701,019,798 147 -27,515,191 1,575 Targu Secuiesc,

COVASNA

151 CONTITECH FLUID AUTOMOTIVE ROMANIA SRL

2.963 509,780,658 211 40,536,731 1,230 Carei, SATU MARE

152 ORACLE ROMANIA SRL 2.963 427,871,180 250 25,598,720 1,715 Bucuresti, Sector 1

153 KROMBERG & SCHUBERT ROMANIA SRL 2.963 360,789,334 302 5,492,288 1,955 Timisoara, TIMIS

154 CONFIND SRL 2.963 218,829,078 486 29,715,977 1,124 Campina, PRAHOVA

155 SPEDITION UMB SRL 2.950 791,456,834 127 161,456,607 33 Bacau, BACAU

156 AMIGO & INTERCOST SRL 2.925 213,184,227 498 7,982,487 488Odorheiu Secuiesc,

HARGHITA

157 TMK - RESITA SA 2.925 804,234,037 123 50,412,602 782 Resita,

CARAS-SEVERIN

158 AD AUTO TOTAL SRL 2.925 438,504,261 241 20,289,510 722 Bucuresti, Sector 4

159 AVICOLA CREVEDIA SA 2.925 395,973,057 268 2,256,188 428 Crevedia,

DAMBOVITA

160 TITAN SA 2.925 338,268,130 322 8,287,814 872 Pantelimon, ILFOV

161 ALBALACT SA 2.925 338,250,651 323 5,767,484 631 Galda de Jos, Locali-tatea Oiejdea, ALBA

162 CROMSTEEL INDUSTRIES SA 2.925 251,843,625 429 21,560,799 331 Targoviste,

DAMBOVITA

163 MW ROMANIA SA 2.925 231,000,062 464 25,479,269 337 Dragasani, VALCEA

164 TEHNOSTRADE SRL 2.913 572,444,536 186 124,714,073 1,293 Bacau, BACAU

165 APA NOVA BUCURESTI SA 2.913 493,644,646 217 85,732,079 1,951 Bucuresti, Sector 5

166 ROSKO TEXTIL SRL 2.913 332,469,063 328 21,491,773 1,207 Curtici, ARAD

167 COMPANIA ROMPREST SERVICE SA 2.913 267,590,738 414 14,912,162 2,920 Bucuresti, Sector 1

168 RULMENTI SA 2.913 261,601,928 423 18,959,099 2,339 Barlad, VASLUI

MCR TOP 300

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

169 ALPIQ ROMENERGIE SRL 2.900 715,416,545 145 26,422,338 12 Bucuresti, Sector 1

170 UNILEVER SOUTH CENTRAL EUROPE SA 2.875 727,113,466 141 -66,077 279 Bucuresti, Sector 1

171 PORSCHE INTER AUTO ROMANIA SRL 2.875 636,456,271 161 5,915,195 521 Tunari, ILFOV

172 ELECTROMAGNETICA SA 2.875 495,195,622 216 15,075,281 535 Bucuresti, Sector 5

173 CORD ROMANIA SRL 2.875 383,708,042 287 18,823,477 458 Slatina, OLT

174 TIMKEN ROMANIA SA 2.875 351,791,919 309 86,447,728 852 Ploiesti, PRAHOVA

175 AEDIFICIA CARPATI SA 2.875 310,916,205 351 24,486,956 729 Bucuresti, Sector 5

176 ARGUS SA 2.875 231,042,645 463 7,930,422 291 Constanta,

CONSTANTA

177 REGIOTRANS SRL 2.875 225,505,914 472 8,669,801 760 Brasov, BRASOV

178 PREH ROMANIA SRL 2.875 216,340,379 493 9,736,777 324 Ghimbav, BRASOV

179 CHIPITA ROMANIA SRL 2.875 212,667,390 500 15,464,874 555 Clinceni, ILFOV

180 SIVECO ROMANIA SA 2.875 204,985,381 525 14,971,311 964 Bucuresti, Sector 1

181 COMPANIA NATIONALA DE TRANSPORTURI AERIENE ROMANE TAROM SA

2.863 946,315,772 104 -262,224,490 2,286 Otopeni, ILFOV

182 LEONI WIRING SYSTEMS RO SRL 2.863 664,314,181 154 16,838,477 3,413 Bistrita,

BISTRITA-NASAUD

183 CONTITECH ROMANIA SRL 2.863 646,344,364 158 106,239,205 1,554 Timisoara, TIMIS

184 YAZAKI ROMANIA SRL 2.863 612,330,127 169 15,317,650 3,489 Ploiesti, PRAHOVA

185 LEONI WIRING SYSTEMS ARAD SRL 2.863 510,879,742 210 14,249,600 2,999 Arad, ARAD

186 STRACO GRUP SRL 2.863 372,590,194 294 4,240,589 1,029 Bucuresti, Sector 5

187 ASESOFT DISTRIBUTION SRL 2.838 853,231,813 117 2,942,581 146 Bucuresti, Sector 2

188 BRISEGROUP SRL 2.838 544,497,306 192 12,813,660 128 Constanta,

CONSTANTA

189 AMEROPA GRAINS SA 2.838 483,949,128 220 11,351,261 200 Constanta,

CONSTANTA

190 CORTUBI SRL 2.838 431,773,722 248 5,322,664 122 Mioveni, ARGES

191 TRUST MOTORS SRL 2.838 248,839,423 436 10,898,148 75 Bucuresti, Sector 6

192 EURO AUTO PLASTIC SYSTEMS SRL 2.825 436,829,312 244 35,942,357 667 Mioveni, ARGES

193 TRANS BITUM SRL 2.825 314,694,139 346 7,039,912 280 Bucuresti, Sector 1

194 IBM ROMANIA SRL 2.825 311,815,348 350 55,891,208 806 Bucuresti, Sector 1

195 ZES ZOLLNER ELECTRONIC SRL 2.825 231,786,310 460 13,346,129 832 Satu Mare,

SATU MARE

196FILIALA DE DISTRIBUTIE A ENERGIEI ELEC-TRICE - ELECTRICA DISTRIBUTIE MUNTENIA NORD SA

2.813 685,740,287 151 67,414,812 2,078 Ploiesti, PRAHOVA

197SOCIETATEA COMERCIALA FILIALA DE DIS-TRIBUTIE A ENERGIEI ELECTRICE - ELEC-TRICA DISTRIBUTIE TRANSILVANIA NORD SA

2.813 535,412,637 199 29,100,621 2,016 Oradea, BIHOR

198 RENAULT TECHNOLOGIE ROUMANIE SRL 2.813 534,872,284 200 18,550,524 1,988 Voluntari, ILFOV

199 COMPANIA NATIONALA AEROPORTURI BUCURESTI SA

2.813 474,335,158 225 52,608,755 1,099 Otopeni, ILFOV

200 KOYO ROMANIA SA 2.813 231,283,959 461 4,551,725 1,345 Alexandria,

TELEORMAN

201 KROMBERG & SCHUBERT ROMANIA ME SRL 2.813 224,843,874 473 4,571,667 1,824 Medias, SIBIU

202 FAN COURIER EXPRESS SRL 2.813 222,633,218 477 43,993,292 1,137 Bucuresti, Sector 2

203 METALROM SRL 2.800 242,779,829 445 2,253,653 25 Bucuresti, Sector 1

204 BRIDGESTONE ROMANIA SRL 2.800 201,801,702 531 7,527,102 12 Bucuresti, Sector 2

205 AROMET SA 2.788 397,865,426 267 2,310,909 187 Buzau, BUZAU

206 COMFERT SRL 2.788 388,851,148 275 9,151,592 190 Bacau, BACAU

207 ENERGOBIT SRL 2.788 386,956,309 281 42,078,764 184 Cluj-Napoca, CLUJ

208 MHS TRUCK & BUS SRL 2.788 376,513,172 290 14,112,199 135 Bucuresti, Sector 6

209 DONALAM SRL 2.788 284,986,507 383 55,464,566 174 Calarasi, CALARASI

172012 EDITION Major Companies in Romania

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

210 JOHNSON CONTROLS FABRICS ROMANIA SRL 2.788 252,556,381 428 16,277,185 123 Timisoara, TIMIS

211 AGRICOVER SRL 2.788 236,750,800 450 6,605,172 116 Voluntari, ILFOV

212 GRUP ROMET SA 2.788 624,090,512 164 3,843,537 79 Buzau, BUZAU

213 LS TRAVEL RETAIL ROMANIA SRL 2.788 264,051,362 419 5,268,709 139 Bucuresti, sector 1

214 KRONOSPAN SEBES SA 2.775 972,230,274 103 -31,620,157 442 Sebes, ALBA

215 HELLA ROMANIA SRL 2.775 592,357,122 174 31,240,868 928 Sannicolau Mare,

TIMIS

216 LINDE GAZ ROMANIA SRL 2.775 437,597,916 243 64,734,733 437 Timisoara, TIMIS

217 EUROPHARM SA 2.775 407,769,055 258 25,704,364 258 Brasov, BRASOV

218 TCE 3 BRAZI SRL 2.775 402,400,692 262 49,741,849 912 Piatra Neamt,

NEAMT

219 WHITELAND IMPORT EXPORT SRL 2.775 390,726,409 273 5,777,668 420 Bucuresti, Sector 4

220 HELP NET FARMA SA 2.775 350,442,551 313 12,580,059 993 Bucuresti, Sector 2

221 KATHREIN ROMANIA SRL 2.775 288,759,340 379 20,997,753 860 Timisoara, TIMIS

222 BOROMIR IND SRL 2.775 264,813,069 418 4,972,163 827 Ramnicu Valcea,

VALCEA

223 ARDEALUL SA 2.775 222,340,428 480 29,744,158 282 Carei, SATU MARE

224 EMERSON SRL 2.775 205,770,924 521 28,392,323 698 Cluj-Napoca, CLUJ

225 UNICARM SRL 2.763 635,301,465 163 13,781,420 2,688 Vetis, SATU MARE

226 MARQUARDT SCHALTSYSTEME SCS 2.763 518,218,340 207 32,441,032 1,048 Sibiu, SIBIU

227 DELTA ANTREPRIZA DE CONSTRUCTII SI MONTAJ 93 SRL

2.763 407,736,320 259 49,802,964 1,214 Bucuresti, Sector 3

228 VEGA 93 SRL 2.763 361,214,554 300 28,790,208 2,087 Galati, GALATI

229 ALCATEL - LUCENT ROMANIA SA 2.763 328,377,251 333 27,522,541 1,486 Timisoara, TIMIS

230 GLOBAL E-BUSINESS OPERATIONS CENTRE SRL

2.763 274,220,700 399 27,755,616 2,594 Bucuresti, Sector 2

231 AEM SA 2.763 258,532,296 426 22,915,111 1,370 Timisoara, TIMIS

232 GRANI COMERT SRL 2.750 374,804,985 292 7,656,500 49 Constanta,

CONSTANTA

233 ENERGY HOLDING SRL 2.738 747,454,302 139 -34,583,954 53 Bucuresti, Sector 1

234 CARMISTIN SRL 2.738 384,794,152 284 3,214,146 525 Voluntari, ILFOV

235 FLANCO RETAIL SA 2.725 482,000,196 221 95,848,848 667 Cluj-Napoca, CLUJ

236 TERAPIA SA 2.725 421,239,266 253 95,848,848 667 Cluj-Napoca, CLUJ

237 ARCELORMITTAL HUNEDOARA SA 2.725 388,082,736 277 -19,811,164 683 Hunedoara,

HUNEDOARA

238 ZAHARUL ORADEA SA 2.725 387,859,569 279 5,623,257 268 Oradea, BIHOR

239 ELGEKA - FERFELIS ROMANIA SA 2.725 282,092,710 389 1,887,738 400 Bucuresti, Sector 3

240 CUMMINS GENERATOR TECHNOLOGIES ROMANIA SA

2.725 265,401,137 416 3,012,892 707 Craiova, DOLJ

241 ZARA BUCURESTI SRL 2.725 262,871,579 421 44,040,102 491 Bucuresti, Sector 3

242 VALROM INDUSTRIE SRL 2.725 246,466,069 441 14,140,879 340 Bucuresti, Sector 6

243 ZENTIVA SA 2.725 235,648,166 453 33,857,309 555 Bucuresti, Sector 3

244 INTRAROM SA 2.725 221,672,458 481 1,440,302 412 Bucuresti, Sector 2

245 ARCELORMITTAL TUBULAR PRODUCTS IASI SA

2.725 218,094,258 490 -35,611,590 547 Iasi, IASI

246 TERAPLAST SA 2.725 209,359,979 509 -14,642,198 449 Bistrita,

BISTRITA-NASAUD

247 DELACO DISTRIBUTION SA 2.725 201,896,515 530 2,436,482 400 Codlea, BRASOV

248 RAJA SA 2.713 206,825,742 520 12,112,477 2553Constanta, CON-

STANTA

249 FORD ROMANIA SA 2.713 797,674,088 125 -471,350,988 3,501 Craiova, DOLJ

250 LISA DRAXLMAIER AUTOPART ROMANIA SRL 2.713 295,424,439 368 8,831,594 3,515 Pitesti, ARGES

251 LEMARCO SA 2.700 342,755,084 317 19,994,605 - Bucuresti, Sector 1

MCR TOP 300

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

252 MARIA CEREALE SRL 2.700 316,630,800 343 5,619,256 14 Constanta,

CONSTANTA

253 AIR BP SALES ROMANIA SRL 2.700 288,719,992 380 6,230,480 1 Otopeni, ILFOV

254 AUTOCORA SRL 2.700 276,022,388 397 9,484,310 42 Alexandria,

TELEORMAN

255 ROREX TRADER SRL 2.700 205,400,638 523 832,152 10 Constanta,

CONSTANTA

256 ROMPETROL GAS SRL 2.688 784,405,200 128 -2,760,637 171 Bucuresti, Sector 1

257 UNICOM HOLDING SA 2.688 758,778,507 135 -19,280,605 141 Voluntari, ILFOV

258 GENERAL ELECTRIC INTERNATIONAL INC - WILMINGTON SUCURSALA ROMANIA

2.688 694,710,373 148 11,638,925 98 Bucuresti, Sector 1

259 IPSO SRL 2.688 369,638,427 296 21,063,687 238 Mogosoaia, ILFOV

260 3M ROMANIA SRL 2.688 267,863,415 412 43,900,023 70 Bucuresti, Sector 1

261 PUNCTUAL COMIMPEX SRL 2.688 249,260,965 435 1,520,548 62 Cluj-napoca, CLUJ

262 WRIGLEY ROMANIA SRL 2.688 213,525,542 497 30,201,909 196 Bucuresti, Sector 1

263 GRUP SERVICII PETROLIERE SA 2.675 796,938,787 126 -307,319,833 434 Constanta,

CONSTANTA

264 CAMERON ROMANIA SRL 2.675 677,011,157 152 51,853,430 845 Campina, PRAHOVA

265 KRAFT FOODS ROMANIA SA 2.675 563,555,504 189 26,064,691 262 Ghimbav, BRASOV

266 DANONE - PRODUCTIE SI DISTRIBUTIE DE PRODUSE ALIMENTARE SRL

2.675 502,998,666 214 16,396,155 608 Bucuresti, Sector 2

267 SIEMENS SRL 2.675 475,386,469 224 19,781,890 469 Bucuresti, Sector 6

268 AVON COSMETICS (ROMANIA) SRL 2.675 444,432,678 239 56,435,043 315 Oiejdea, ALBA

269 TRANSAVIA SA 2.675 357,681,199 305 26,299,438 913 Oiejdea, ALBA

270 EURO CONSTRUCT TRADING 98 SRL 2.675 354,497,745 308 37,930,724 780 Bucuresti, Sector 6

271 COMPANIA NATIONALA IMPRIMERIA NATIONALA SA

2.675 342,553,292 319 32,645,355 474 Bucuresti, Sector 1

272 CARGILL OILS SA 2.675 313,656,544 347 -2,839,381 277 Bucuresti, Sector 1

273 BOS AUTOMOTIVE PRODUCTS ROMANIA SCS 2.675 304,484,903 358 16,333,470 855 Arad, ARAD

274 AGRISOL INTERNATIONAL RO SRL 2.675 231,060,622 462 8,441,745 953 Boldesti-Scaeni,

PRAHOVA

275 ANTENA TV GROUP SA 2.675 222,617,199 478 6,248,649 520 Bucuresti, Sector 1

276SOCIETATEA COMERCIALA FILIALA DE DIS-TRIBUTIE A ENERGIEI ELECTRICE - ELEC-TRICA DISTRIBUTIE TRANSILVANIA SUD SA

2.663 598,510,775 173 19,569,602 1,813 Brasov, BRASOV

277 ROMSTRADE SRL 2.663 539,727,094 197 10,881,044 1,623 Adunatii Copaceni,

GIURGIU

278 TMUCB 2.663 284,624,365 384 5,230,113 1,599 Bucuresti, Sector 1

279 SUCCES NIC COM SRL 2.663 273,925,545 400 2,470,789 1,431 Targu Jiu, GORJ

280 SANTIERUL NAVAL DAMEN GALATI SA 2.663 273,123,588 402 13,581,756 1,573 Galati, GALATI

281 COMPANIA LOCALA DE TERMOFICARE COLTERM SA

2.663 208,532,946 512 6,844,761 1,051 Braila, BRAILA

282 BRAICONF SA 2.663 33,123,548 1,835 1,959,082 1,046 Braila, BRAILA

283 TRANSENERGO COM SA 2.650 551,836,290 190 4,721,041 24 Bucuresti, Sector 5

284 ARELCO DISTRIBUTIE SRL 2.650 450,128,844 237 1,970,347 12 Bucuresti, Sector 1

285 GOODYEAR DUNLOP TIRES ROMANIA SRL 2.650 391,829,339 272 5,459,887 38 Bucuresti, Sector 1

286 ROMSPEED SRL 2.650 276,478,458 395 668,976 8 Constanta,

CONSTANTA

287 REMATHOLDING CO SRL 2.638 578,389,137 180 11,303,473 198 Braila, BRAILA

288 COMISION TRADE SRL 2.638 432,010,493 247 4,337,501 136 Braila, BRAILA

289 BULROM GAS IMPEX SRL 2.638 321,546,949 341 3,125,023 122 Bucuresti, Sector 1

290 CAN-PACK ROMANIA SRL 2.638 289,642,596 377 19,151,136 157 Bucuresti, Sector 4

291 COLGATE-PALMOLIVE (ROMANIA) SRL 2.638 248,723,770 437 5,933,337 100 Bucuresti, Sector 2

192012 EDITION Major Companies in Romania

TOP 300 MAJOR COMPANIES IN ROMANIARANK COMPANY NAME MCR SCORING ANNUAL TURNOVER

2011TURNOVER

RANKING PROFIT/LOSS 2011 NO OF EMPLOYEES CONTACT

292 VIVANI SALUBRITATE SA 2.638 205,510,109 522 10,448,441 191 Slobozia, Ialomita

293 BV MCCANN ERICKSON SRL 2.638 201,713,544 533 7,577,453 92 Bucuresti, Sector 1

294 ICME ECAB SA 2.625 652,464,236 157 13,084,487 563 Bucuresti, Sector 3

295 DANTE INTERNATIONAL SA 2.625 621,423,342 166 5,104,301 338 Voluntari, ILFOV

296 STRABAG SRL 2.625 585,828,064 176 6,436,998 448 Bucuresti, Sector 5

297 HENKEL ROMANIA SRL 2.625 542,369,628 194 30,414,936 459 Bucuresti, Sector 2

298 PETROM LPG SA 2.625 513,028,100 209 11,501,793 274 Otopeni, ILFOV

299 PRUTUL SA 2.625 489,975,996 219 2,362,422 416 Galati, GALATI

300 ENEL DISTRIBUTIE DOBROGEA SA 2.625 458,996,729 234 108,851,221 995 Constanta,

CONSTANTA

MCR TOP 300

232012 EDITION Major Companies in Romania

21CEE lending institutions active in Romania, the largest presence of region's major banks

Total assets of Romanian banking system is worth RON 353,91 billion in 2011

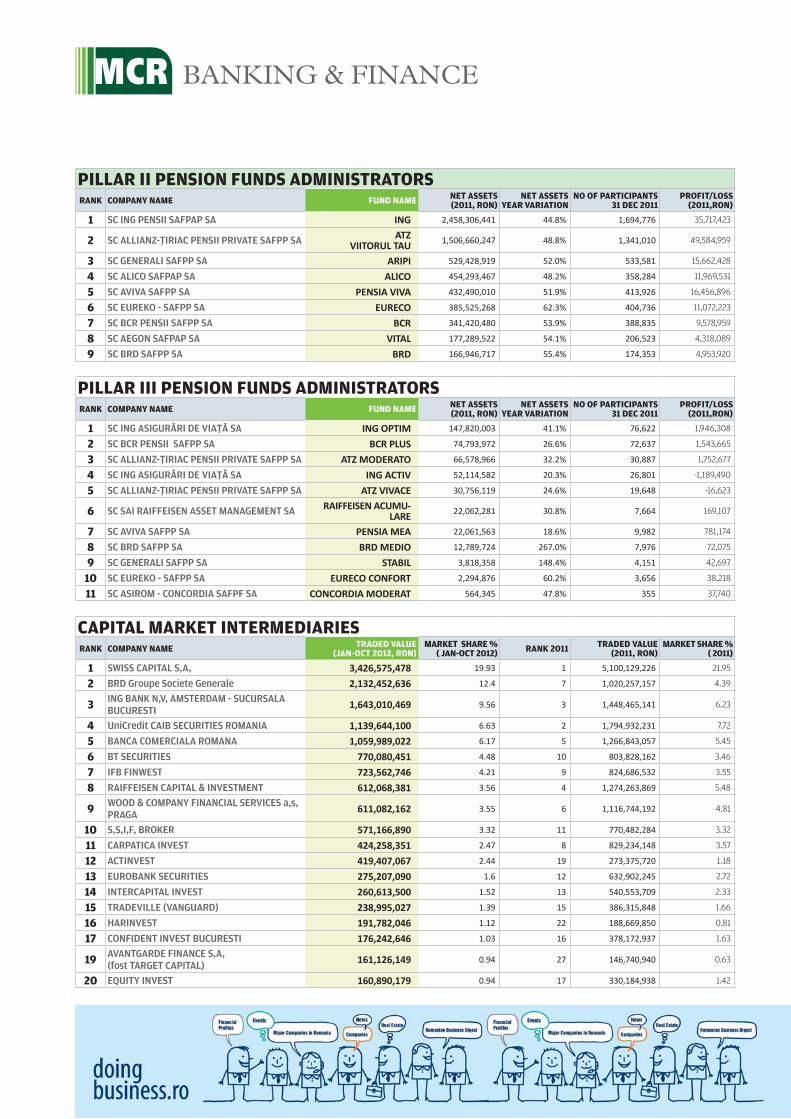

Banking & Finance BANKING INSURANCE FINANCIAL LEASING OPERATIONAL LEASING PENSION FUNDS ADMINISTRATORS FUND MANAGEMENT CAPITAL MARKET INTERMEDIARIES

Two of the most significant events in the banking sector in 2012 were the introduction of the International Financial Reporting Standards (IFRS) starting with 1 January 2012 and the legislative framework of the bridge-bank concept. These measures converge to the common purpose of the national and European authorities to have a unified view over the globalised banking sector as well as to re-enforce their role in financial stability. These changes were due to the commitment of the Romanian Authorities to a new preventive finance arrangement with the European Union, IMF and World Bank. Also, in 2012, the enforcement of the cooperation and harmonization framework in a new collaboration step under the Viena European Initiative for Banking Coordination 2.0 was set as a primary goal for national regulators. This initiative sets up a better cooperation between the regulators in the origin European countries and those in host-countries for the purpose of preventing erratic financial dealing.

The IFRS transition was guided by the National Bank of Romania (NBR) in such a way as to prevent any irregularities in computing prudential indicators. The International Standards assume that the allowances for loans are to be recorded as a consequence of a default event, while the former national regulations imposed that allowances were recorded based on expected losses. This used to lead to the ex ante recognition of losses in the financial statements, i.e: a decrease in annual profits. The concern was that, with the transition to IFRS, banks would increase their profits and thus improve their own funds position in the calculation of capital adequacy ratios. This was prevented by the NBR through the Order 26 issued in December 2011, which sets the framework for reporting of prudential filters, starting with January 2012. Based on the analysis performed on financial reporting as at 31 December 2011 and 31 March 2012, NBR decided to maintain prudential filters after 1 January 2013 as well.

Additional measures taken by NBR were targeted to the monitoring of correct capitalization of risks in the Romanian banking sector. Capitalization was, in 2012 like in previous periods, assured by the shareholders. Other capitalization movements referred to the take-over of Emporiki Bank Romania by the French group Credit Agricole and the recent takeover by Piraeus Bank of the good assets of ATE Bank (including the Romanian branch). These restructurings did not affect the capitalization ratios and did not assume state intervention. The net increases in the social capital of banks

reached EUR 550 million in the first semester of 2012. The solvency ratio reached a level of 14.7 in June 2012 (EU minimum level required: 8%).

The banks’ biggest problem was in 2012 the same as in the previous 2 years: the quality of the loan portfolio. The level of non-performing loans (NPLs) continued to grow in 2012 rising from a level of 14.3% in December 2011 to 16.8% in June 2012. The growth is due, in part, to the introduction of IFRS, whereby banks are obliged to recognize losses from loans previously recognized off-balance sheets. Also, in 2012, banks re-valued the performance of customers whose loans they had re-structured in previous years.

The transition to IFRS has been followed-up by the National Bank through the requirement of prudential filters, whereby banks are required to compute solvency ratios based on recognition criteria that are stricter than the ones required by IFRS. The latest stress-testing results show, that on a two years horizon, the Romanian banking entities have the capacity to overcome strong macro-economic shocks. These tests show that in the adverse scenario case where Romania re-enters the recession and the national currency incur heavy devaluation against foreign currencies, the solvency ratio would drop to 12.3%, maintaining an acceptable level.

In 2012, banks continued to record a majority of mortgage loans in their balance sheet. The mortgage loans granted to individuals in 2012 grew by RON 13 billion between January 2011 and June 2012. This was mainly due to the “First House” program. During this period, the program contributed with 53% to the total mortgage loans, in approximately 30,500 guarantees. These loans are, though, responsible for a significant increase in the NPL ratios, as the non-performing mortgage loans granted to individuals raised by 60% in the period to June 2012. Out of these loans, the most risky ones are the so-called “American Mortgages”: loans for personal needs, with real estate collaterals, as opposed to Housing Loans - loans used for the construction/acquisition of a real estate property. A similar situation occurs for mortgage loans granted to companies. The non performing loans have increased by 66.1% by June 2012. These movements in non-performing loans cannot be entirely imposed to the bank’s decision to invest, but more to the market trends between June 2011 and June 2012. The National Statistics Institute reported a drop of 15% in prices of real estate properties for the above mentioned period.

MCR BANKING & FINANCE

Banking in 2012:towards a more regulated market

Gabriela Bratu, Senior, Assurance & Advisory Business Services, Ernst & Young

Thus, the loan-to-value indicator (“LTV”) deteriorated in this period, by increasing from 71% to 78% for retail loans and from 70% to 75% for corporate loans.

This drop in real estate prices also worsened the banks’ exposure towards real estate companies. The NPL ratio for these loans rose from 18% in December 2010 to 28.4% in July 2012. Banks continue to support this sector by re-scheduling and restructuring the loans granted to developers. This year, 12% of total restructured loans were represented by loans

granted to the real estate sector. Banks continue also to grant new finance to this sector, as they believe that the market was not fully matured at the inception of the economic crisis, and it could re-start from where it has left, back in 2009-2010. Their beliefs is consolidated by the numbers in the construction and real-estate industry where there has been a raise in volume of work as well as an increase in number of employees and investment projects. Other analysts state, however, that this sector is still to fall, as construction authorizations have decreased in the previous 18 months.

The other major event in 2012 was the set-up of the legislative framework of the bridge bank. This is an instrument used by NBR to intervene promptly when one of the banks faces problems that might spread to the entire banking system. If such an event occurs, the NBR will immediately suspend the mandates of the problem-bank management and transfer all assets and liabilities to a newly formed entity – the bridge bank. This entity will have a two-tier administration board, the members of the Board being elected by NBR. The unique shareholder of this new entity will be the Banks Deposits Guarantee Fund who will also finance this new bank from its own private resources. Public funding could also be provided in the form of loans granted by the Ministry of Finance to the Fund. The new entity will function for a period of two years when the NBR should be able to find a new investor willing to take-over the assets and liabilities. This period could be prolonged if no such investor is found by the end of the two-year period. The troubled bank from which the assets and liabilities are taken over will be liquidated, as NBR will annul its authorization.

The legal framework that describes the functionality of the bridge-bank also brings forward new roles of NBR. The Romanian Banking regulator will be able from 2012, to suspend the banks’ shareholders’ right to vote , if it considers that their decision can endanger the prudential administration of the respective financial entity. Also, NBR is free to intervene whenever it observes a current or possible future “significant deterioration” of prudential indicators and conclude that the shareholders are not taking appropriate measures to improve these indicators.

With regards to the solvency ratios, NBR is also taking a more pro-active role, as it will be obliged to constitute special administration for banks whose capital adequacy ratios will fall lower than 75% of the minimum required level.

These set of measures are meant to strengthen the regulators’ role, as well as to improve the confidence level of foreign investors in the Romanian financial system. Once the world economy will start to recover from the outcome of the financial crisis, the investors will begin to look for new investment opportunities, but with a keener eye to regulated markets. Also, by functioning in this new regulatory framework, the banks themselves will re-educate their investment choices and will perhaps learn to identify and finance those healthy sectors of the real economy.

252012 EDITION Major Companies in Romania

Main prudential indicators Dec-10 Jun-11 Dec-11 Mar-12 Jun-12 Capital adequacy ratio 15.02% 14.19% 14.87% 14.63% 14.66% Leverage ratio 8.11% 7.79% 8.07% 8.60% 8.42% Loans to clients (% of total assets) 58.64% 59.86% 59.24% 61.42% 60.93% NPL ratio 11.85% 13.35% 14.33% 15.88% 16.76% Total number of overdue clients 218,370 240,097 224,599 239,571 244,820

Source: NBR

The moderate recovery in Emerging Europe is still threatened by continued uncertainty and recession in the Eurozone. Romania still has difficulties in boosting growth due to the overall uncertain international economic situation, along with the internal uncertainties. The political turmoil has diminished Romania’s credibility on the financial markets and in the eyes of potential investors. Because the private sector is directly confronted with the effects of the political turmoil and the deterioration of the economic environment, our voice will be stronger in expressing our worry with regard to the future of the business we make in Romania.

In this context, the business community in Romania announced the creation of a coalition for the economic growth and stability that gathers AmCham, The Council for Foreign Investors or the business bilateral chambers of commerce (Dutch, British, Canadian, Irish, Finnish, Danish) and has the support of the diplomatic missions to Romania of some EU member states as well as of US and Canada. We call for a strategic dialogue with the Government to improve the business environment, to raise the competitiveness of Romania on a international plan and to rebuild the trust in the Romanian economy.

We are a strong voice that can no longer be avoided because we represent the majority of the foreign investors in Romania created and continue to create thousands of work places for the citizens

of Romania and contribute significantly to the state budget. Despite the political landscape, Romania is still a good business opportunity. According to the European Attractiveness Survey 2012 report (Ernst & Young’s survey over 840 business leaders) Romania will be the sixth most attractive European country for investment over the next three years1. This is encouraging news for the foreign investors and it is a call for action for the political class, which should have no other concern than end the political turmoil and stop doing more damage to the economy and the country’s credibility.

Considering the fact that the FDIs dropped last year to the lowest value since 2003, we realize it is crucial to push through further structural reforms if it is to boost competitiveness and enable economic sustainable growth. Here are some priorities for action which relates one to the other:

legislative and regulatory processes is vital for the investors. Without a stable, clear and predictable regulatory framework, investors' interest to invest in a market is limited;

challenges related to labor legislation if it wants to improve productivity. Romania has productivity by 57% lower than the EU average. Delaying long-awaited reforms will diminish the competitive advantage of the labor market

Doing business in Romania

STEVEN VAN GRONINGEN,President Raiffeisen Bank Romania,President of Foreign Investors Council (FIC) in Romania

payments (113 payments are required during the course of a year which takes 222 hours (9 days) to make) - most of them relates to labor taxes and the fact that currently Romania has no functional electronic payment system available for companies. Therefore, rationalizing and simplifying the tax system should be a priority;

revitalize economy’s financing through capital markets; Romania still need to work hard to improve its capital markets, which remain less developed than those in other accession countries.

Romania has been ranked 77 out of 142 countries in the 2011-2012 Global Competitiveness Index Report issued by the World Economic Forum (WEF) - Romania lost 10 positions from the previous report. According to WEF, the most problematic factors for doing business in Romania: access to financing, tax rates, policy instability, tax regulations, inefficient government 38 bureaucracy, inadequate supply of infrastructure, corruption (based on average ranking in the last three Global Competitiveness Reports, 2009-2011). From now on, the Romanian government should give special attention to those measures that help rebuild the country’s credibility and contribute to sustainable economic growth.

1 The top five countries in the ranking are Germany, Poland, the United Kingdom, Russia and France. The study is based on methodology that includes an analysis of the number of foreign investment projects in 2011 and a soft analysis of the perception of the attractiveness of European countries for foreign investment. The country outperforms the Czech Republic, Turkey, Switzerland, the Netherlands, Italy, Spain and Sweden.

MCRMCR Opinion

BANKINGRANK COMPANY NAME MCR SCORING AT 2011 MARKET SHARE PROFIT/LOSS

RON 2011

PEERS MORE THAN 5% MARKET SHARE

1 RAIFFEISEN BANK SA 4.250 23,690,300,000 7% 320,068,972

2 BANCA TRANSILVANIA S.A. 4.000 25,745,200,000 7% 131,870,976

3 VOLKSBANK ROMANIA SA 3.750 17,728,100,000 5% -698,881,415

4 BRD - GROUPE SOCIETE GENERALE S.A. 3.500 48,027,700,000 14% 465,265,368

5 CEC BANK SA 3.500 24,815,600,000 7% 67,445,929

6 UNICREDIT TIRIAC BANK SA 3.500 22,346,500,000 6% 103,062,227

7 ALPHA BANK ROMANIA S.A. 3.500 16,544,100,000 5% -117,707,116

8 BANCA COMERCIALA ROMANA SA 3.250 71,054,800,000 20% -510,818,823

PEERS 1% - 4% MARKET SHARE

9 ING BANK N.V. AMSTERDAM SUCURSALA BUCURESTI 4.500 14,509,900,000 4% 129,611,734

10 RBS BANK (ROMANIA) SA 3.500 5,793,300,000 2% 100,068,925

11 BANCPOST S.A. 3.250 12,274,100,000 3% -11,016,904

12 GARANTI BANK SA 3.250 6,189,500,000 2% -79,438,040

13 CITIBANK EUROPE PLC, DUBLIN - SUCURSALA ROMANIA

3.250 5,752,400,000 2% 117,119,398

14 BANCA ITALO ROMENA SPA ITALIA VOLPAGO DEL MONTELLO SUCURSALA BUCURESTI

3.250 4,220,100,000 1% 30,683,869

15 PIRAEUS BANK ROMANIA S.A. 3.125 8,166,600,000 2% 42,057,757

16 BANK OF CYPRUS PUBLIC COMPANY LIMITED NICOSIA SUCURSALA ROMANIA

3.000 2,297,500,000 1% 24,929,252

17 BANCA DE EXPORT IMPORT A ROMANIEI (EXIMBANK) S.A.

2.500 4,174,500,000 1% 59,431,557

18 BANCA ROMANEASCA SA MEMBRA A GRUPULUI NATIONAL BANK OF GREECE

2.750 7,418,200,000 2% -122,611,967

19 CREDIT EUROPE BANK (ROMANIA) S.A. 2.750 4,751,600,000 1% -62,961,948

20 OTP BANK ROMANIA S.A. 2.750 3,745,900,000 1% -21,063,973

21 MARFIN BANK (ROMANIA) S.A 2.750 2,635,000,000 1% -15,162,761

22 BANCA COMERCIALA INTESA SANPAOLO ROMANIA S.A.

2.625 3,964,700,000 1% -254,956,765

23 BANCA COMERCIALA CARPATICA S.A. 2.250 3,787,100,000 1% -31,989,275

24 BANCA MILLENNIUM S.A. 2.250 2,087,800,000 1% -104,040,129

PEERS LESS THAN 1%

25 PROCREDIT BANK S.A. 2.750 1,126,600,000 0% 18,149,547

26 BCR BANCA PENTRU LOCUINTE S.A. 2.750 950,600,000 0% 11,983,539

27 CAIXABANK SA (BARCELONA) - SUCURSALA ROMANIA 2.500 564,500,000 0% 2,074,100

28 CREDIT AGRICOLE BANK ROMANIA S.A 2.250 1,104,800,000 0% -37,679,814

29 BANCA C.R. FIRENZE ROMANIA S.A 2.250 706,800,000 0% 1,039,889

30 BLOM BANK FRANCE SA PARIS SUCURSALA ROMANIA 2.250 626,800,000 0% 3,420,610

31 LIBRA INTERNET BANK S.A. 2.250 595,400,000 0% 10,180,829

32 ATE BANK ROMANIA SA 1.750 1,599,400,000 0% -204,792,307

33 BANK LEUMI ROMANIA S.A 1.750 1,128,100,000 0% -24,051,333

34 NEXTEBANK SA 1.750 1,122,700,000 0% -101,940,963

35 FORTIS BANK SA/NV BRUXELLES SUCURSALA BUCUR-ESTI

1.750 406,200,000 0% -147,758

36 PORSCHE BANK ROMANIA S.A. 1.750 384,800,000 0% 5,813,123

37 ROMANIAN INTERNATIONAL BANK S.A. 1.250 515,900,000 0% -13,498,368

38 RAIFFEISEN BANCA PENTRU LOCUINTE S.A. 1.250 323,700,000 0% 22,219

39 BANCA COMERCIALA FEROVIARA S.A 1.250 176,400,000 0% -17,096,788

SOURCE: NATIONAL BANK OF ROMANIA, TRADE REGISTER, MINISTRY OF FINANCE

272012 EDITION Major Companies in Romania

According to the results notified by the ISC President, Mr. Constantin Buzoiuanu within FIAR, the first quarter of 2012 brought a slight increase (0.55%) on the Romanian insurance market, for the first time since 2009. Is this the sign of a re-launching of the insurance industry? In spite of the uncertainties and the volatility which are the current features of the economic environment in the European Union and not only?

A study concerning the perspectives of the European insurance market published this January by Ernst & Young indicates 2012 to be the year of strategic decisions in an economic environment dominated by stagnation and even recession.

What have these three years of decline meant to the insurance industry? First of all, losses, especially for the companies providing general insurance, but also a trend of market consolidation, materialized in the three mergers that have rearranged the classifications in the Romanian specialized market.

The first important merger during this period took place in 2009 between Asiban and BT Asigurari – recently purchased by the French from Groupama. The French company has chosen to renounce to the two well-known local brands and to promote its own brand, unknown on the Romanian market until that time. The purchase of Asiban was a top transaction in 2008, having a value of above Euro 350 million. Even though, at that time, the effects of the crisis were not yet felt, we can say that Groupama had a vision and they moved fast towards integration and, by doing so, towards making potential synergies, especially in the cost area, but not only there. The French strategy seems to have worked, Groupama Asigurari ranking fourth in the general classification of insurance companies according to the gross premiums subscribed in 2011.

2010 was quiet from the merger and acquisition perspective, the only remarkable event being the entry of another French company on the Romanian market – AXA – by purchasing Omniasig Life, a small-sized insurer exclusively on the life insurance market. The transaction value was much lower this time - approx. Euro 5 million.

However, 2011 was fruitful from the perspective of the mergers between insurance companies belonging to the same

international group and being present on the Romanian market, with two announced mergers - one between Ardaf and Generali, both belonging to the Italian group Generali, which was closed in October 2011 and one between the two general insurance companies held by the Austrian group Vienna Insurance Group - BCR Asigurari and Omniasig, concluded at the end of April 2012.

What is the catalyst causing these international groups to regroup on the local markets and rethink and rationalize the "corporate” structure? The reasons must be searched, first of all, in the current economic situation. We refer here to the extended recession, combined with the worsening of the capitalization requirements (and not only), caused by the implementation of the Solvency II regulations.

The international groups which, until recently, were present on the local market with three or four companies having more or less similar strategies and objectives, have reanalyzed their position and strategic choices and reached the conclusion that cost cuttings, as well as the capitalization requirements that could result from merging the activity into a single legal entity, are not at all negligible.

Strictly from the legal perspective such a merger is neutral and its impact on the market is not considered to be an economic concentration, but merely group reorganization. However, from a competitive point of view, the resulting company is usually better placed on the market than the ones it derives from, and this not only as a result of elementary arithmetic 1+1=2, but also from making the synergies between the merged companies happen.

From the perspective of mergers and acquisitions in the insurance sector, 2012 started with the announcement of the MetLife takeover of the operations of Aviva Romania, Czech Republic and Hungary (the total value of the amount USD 75.3 million or about Euro 57 million at the exchange rate valid on the date of transaction announcement), which was the first transaction of this kind between life insurance companies on the Romanian market. The transaction was closed at the end of August and the next logical expected move is the group structure rationalization and the merger between the two entities. Another but less important transaction on the market of general insurance was announced in March – the takeover of the

MCR BANKING & FINANCE

2012 On the Merger and Acquisition market in the insurance sector – The re-launching year?

Cristina Cerbu, Manager, Transaction Advisory Services, Ernst & Young

majority stock (98.57%) of ABC Asigurari by the businessman Nelu Iordache for Euro 6.7 million.

The Germans from Gothaer also entered the Romanian market by purchasing the majority stock (67%) in another small-sized general insurance company – Platinum Asigurari – Reasigurari (one of the main charter members of the Insurance Pool Against Natural Disasters [PAID] with a 15% shareholding - the maximum legal threshold). The transaction was also finalized in March 2012. These transactions prove there is an appetite for acquisitions on the Romanian market and also available funding, but we consider it to be rather premature to speak about a trend in this regard.

At least two of the insurance companies on the Romanian market – Alico (MeLife) and AXA – have publicly stated their interest for growth by way of acquisitions, to the extent the market provides interesting opportunities. According to a past statement, Allianz does not exclude acquisitions as an instrument for portfolio extension on the Romanian market, either.

However, the fact that the performance of other transactions in the period to come depends greatly also on the existence of quality assets/target companies on the market must be mentioned.

Such a target company is ING Asigurari de Viata – the company ranking first in the classification of Romanian life insurers – given the Dutch financial group has recently confirmed they intended to sell the insurance divisions in Europe, North America and Asia, as a part of the restructuring process agreed with the Dutch State.

The insurance companies with Greek majority shareholding are also potential targets for mergers and acquisitions on the background of the problems currently faced by the Greek State, which are obviously impacting on the financial institutions in this area and not only on them. If there are interested investors, the shareholders of these companies could become very motivated in selling their interests in the companies held in Romania in order to generate cash.

These recent developments aim at confirming the conclusions of another Ernst & Young study Global Capital Confidence Barometer - 5th edition. They foresee a paradigm change, namely, the mergers and acquisitions coexisting with volatility in the economic and financial environment, because the large players have learned to run their businesses under volatility conditions and have developed their ability and ambition to perform strategic transactions in the current circumstances.

292012 EDITION Major Companies in Romania

Although compared to Western Europe, the Romanian insurance market is still underdeveloped, there is no doubt that it has a significant growth potential on medium and long term, if we consider the low level of insurance penetration and the higher competition in the last few years. Yet, in the current crisis context, there are factors that are slowing its growth.

Overall, insurers have been less directly exposed to the international financial crisis, due to conservative investment policies, provisions and restrictions imposed by the Romanian legislation on the investment of assets, portfolio diversification, the interdiction or limitation of alternative investment instruments. The profitability of insurance business decreased due to the crisis, mainly in life insurance sector, by a poor performance of the investments due to falling of the stock market indices and financial market volatility.

The reasons are largely related to the lack or the inadequacy of fiscal incentives, lack of financial resources, bad understanding of the need for insurance policies, lack of tradition in life insurance system plus motivations related to the economic crisis and the worsening economic activities, to the high debt accumulated by the population along the pre-crisis years, the negative growth of the credit institution, low income levels and uncertainty about financial security and even a decreasing level of trust in the insurance concept.

The downfall of the Romanian insurance market was also triggered by the decrease of the corporate sector spending. The straight focused effects of the crisis on companies have also been influenced by the financial statement of the clients. The decreasing of incomes, thus of disposable reserves dedicated to achieving insurance products and the changes in financial priorities contributed to a significant negative growth of sales. Besides the facts listed above, the uncertain political environment, as well as the situation in the Euro Zone, also contributed to a reluctance of companies and individuals towards acquiring a life insurance. However, there were also short- term positive effects of the crisis on the insurance business as the companies learned to survive and continue their business. The offer of insurance products has kept on growing; the insurers have launched new products meant to exploit their opportunities for expansion, offsetting the poor demand for traditional insurance products with a fast development of more flexible and less costly products for their clients. The

Opinion

2012, a year of challenges in insurance marketVIOLETA CIUREL,

President and CEO,AXA Life Insurance

diversification of the distribution channels, more focused on on-line sales, communication and higher quality services for clients with lower costs and increased flexibility are therefore positive effects of the crisis.

Acquisitions and mergers have started, and it is possible to continue in the coming years, leading to a higher consolidation of the market. As I mentioned before, there is a high potential for the growth of the life insurance industry on the Romanian market. The level of insurance penetration for Romania is under 2% compared with an 8% average at European level. Last year, the entire Romanian insurance market was about 1.7 mld EUR with less than 20% life insurance. I anticipate a stagnation on the overall market for the next year mainly because of the global economic environment, Euro crisis, lower investment level and, because of the low level of the direct foreign investments. These influencing factors, as well as the very low degree of absorption of European funds add up to those already mentioned earlier.

MCR

“IN THE NEXT YEARS, THE ROMANIAN INSURANCE MARKET TARGETS THE INCREASE OF EFFICIENCY AND PERFORMANCE, THE REVIEW OF DISTRIBUTION CHANNELS AND THE MORE FREQUENT USE OF BANCASSURANCE, AS AN INSURANCE DISTRIBUTION CHANNEL.”

INSURANCERANK COMPANY NAME GWP 2011 GWP 2010 GWP GROWTH % PROFIT/LOSS 2011 CONTACT

1 OMNIASIG VIENNA INSURANCE GROUP SA 1,202,571,506 * 916,123,674 - -181,296,117 Sector 1, BUCURESTI

2 SOCIETATEA COMERCIALA DE ASIGURARE-REASIGURARE ASTRA SA

1,008,544,317 1,083,209,476 -6.9% 81,013,945 Sector 3, BUCURESTI

3 ALLIANZ - TIRIAC ASIGURARI S.A. 898,416,364 1,020,399,089 -12.0% 24,513,434 Sector 1, BUCURESTI