MBA VTU Project on VOLVO Group in India

166

worlD ToGeTher we MoVe The The VolVo Group annual reporT 2011

-

Upload

lakshmish-gopal -

Category

Documents

-

view

222 -

download

0

Transcript of MBA VTU Project on VOLVO Group in India

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 1/166

worlD

ToGeTher we MoVe The

The VolVo Group

annual reporT 2011

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 2/166

ToGeTher we

MOVE THE WORLD

This report contains ‘for ward-looking statements’. Such statements reect management’s current expectations with respect to cer tain future events and

potential nancial performance. Although the Company believes that the expectations reected in such forward looking statements are reasonable, noassurance can be given that such expectations will prove correc t. Such statements are subject to risk and uncer tainties and such future events and nancialperformance could differ materially from those set out in the forward looking statements as a result of, among other factors, (i) changes in economic, marketand competitive conditions, (ii) success of business and operating initiatives , (iii) changes in the regulatory environment and other government actions, (iv)uctuations in exchange rates and (v) business risk management.

This report does not imply that the company has undertaken to revise these forward looking statements beyond what is required under the company’s

Without the products and services of the Volvo Group the societies

where many of us live would not function. Like lifeblood, our trucks,

buses, engines, construction equipment and aircraft components are

involved in many of the functions that most of us rely on every day.

For instance, one in seven meals eaten in Europe reaches the con-

sumers thanks to trucks from the Volvo Group rolling on the roads of the

continent. Buses are the most common type of public transportation in

the world, helping many people to reach work, school, vacations, friends

and family. And if all the Volvo buses in the world were to start at the

same time, they would transport more than 10 million people.

Every year, the population on earth produces billions of tons of gar-

bage. In the US alone, the garbage removed by refuse trucks from the

Volvo Group every week could form a line of full garbage cans that

would reach the moon.

These are just a few examples. In this Annual Report, you can learn

more about the Volvo Group – Together we move the world.

A global group

2 CEO comment

4 Vision, values and wanted position

6 Financial targets8 Volvo Group new organization

10 Global strength

12 Development by continent – Europe

16 Development by continent – North America

20 Development by continent – South America

24 Development by continent – Asia

28 Overall challenges

30 Challenge – Bus Rapid Transit

34 Challenges – Intelligent Transport Solutions

38 Brands

40 The Volvo Group’s product offering

42 World-class services

44 Industrial structure

Board of Directors’ report

46 Sustainable development

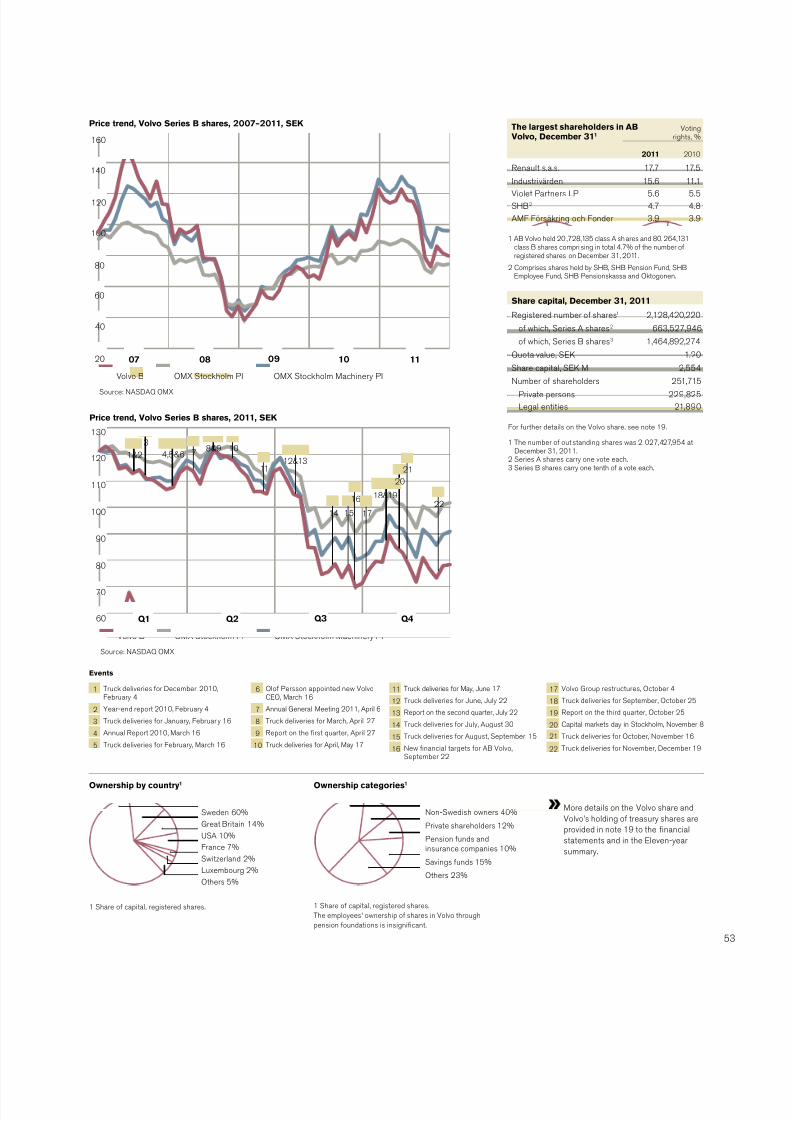

52 The share

54 Signicant events

56 Trucks

58 Construction Equipment

60 Buses

62 Volvo Penta

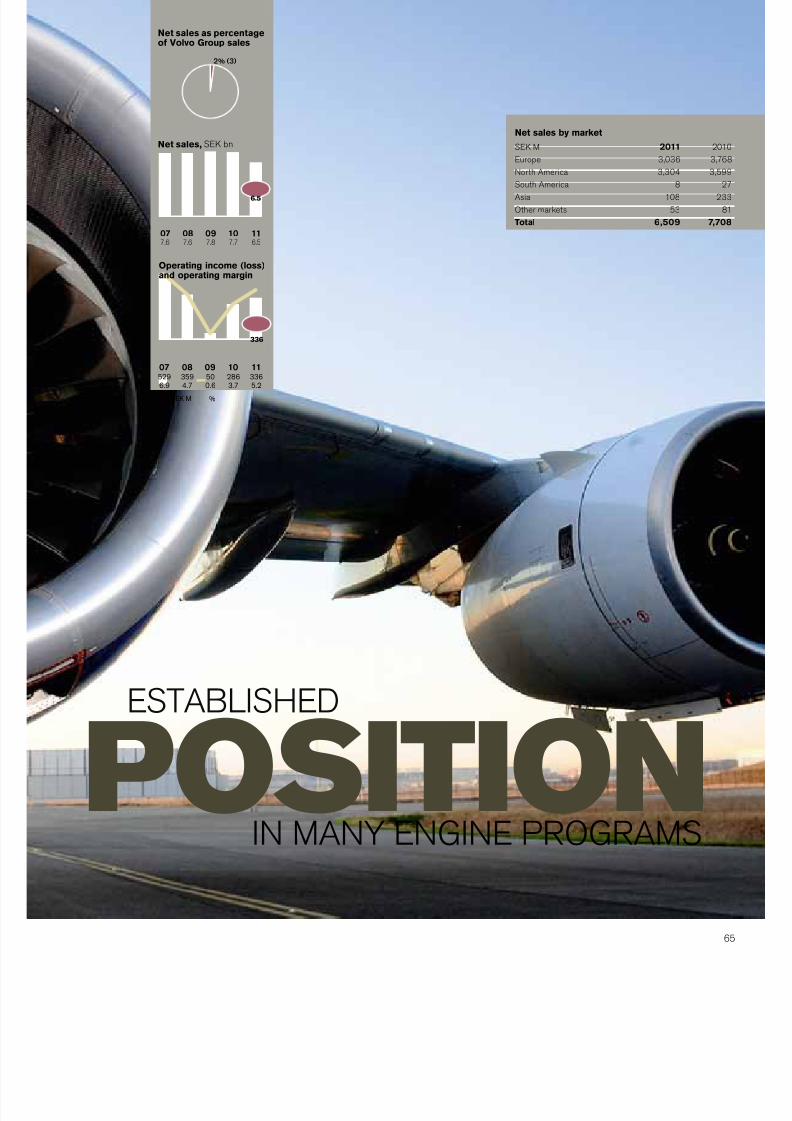

64 Volvo Aero

66 Volvo Financial Services

68 Financial strategy

69 Risks and uncertainties Financial information

71 Financial information 2011

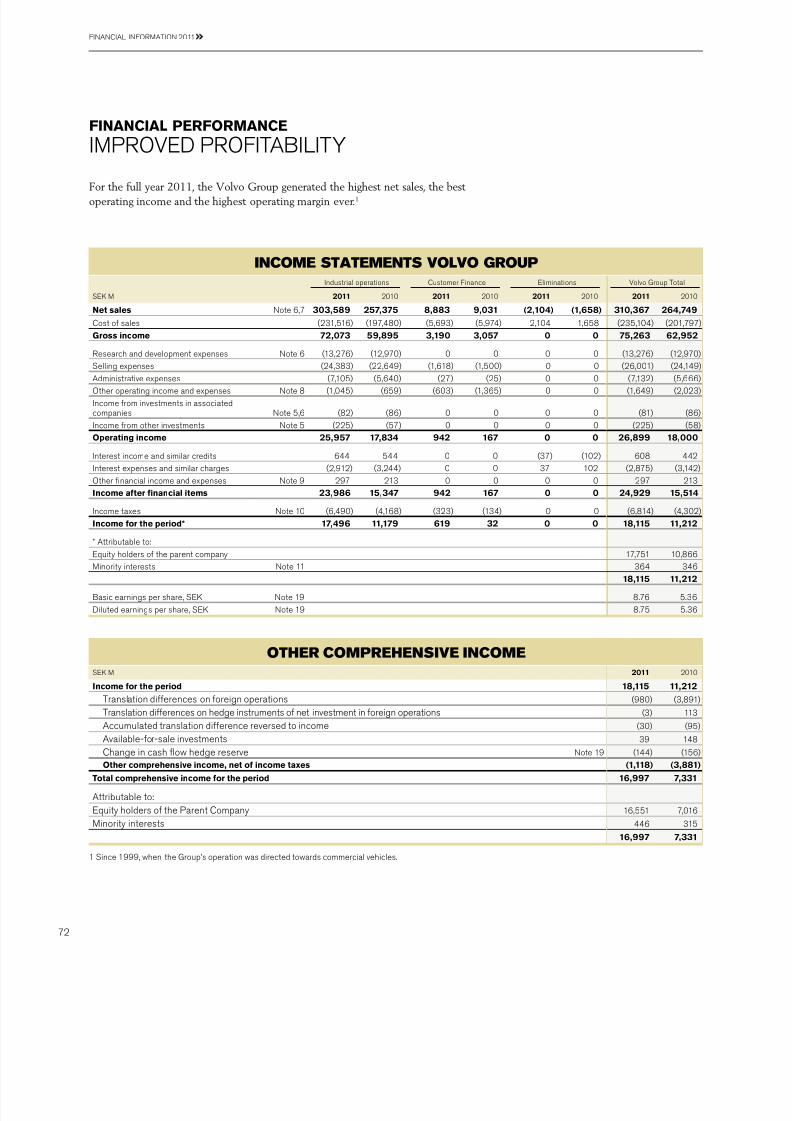

72 Financial performance

72 Consolidated income statement andOther comprehensive income

76 Financial position

76 Consolidated balance sheet

78 Consolidated cash-ow statements

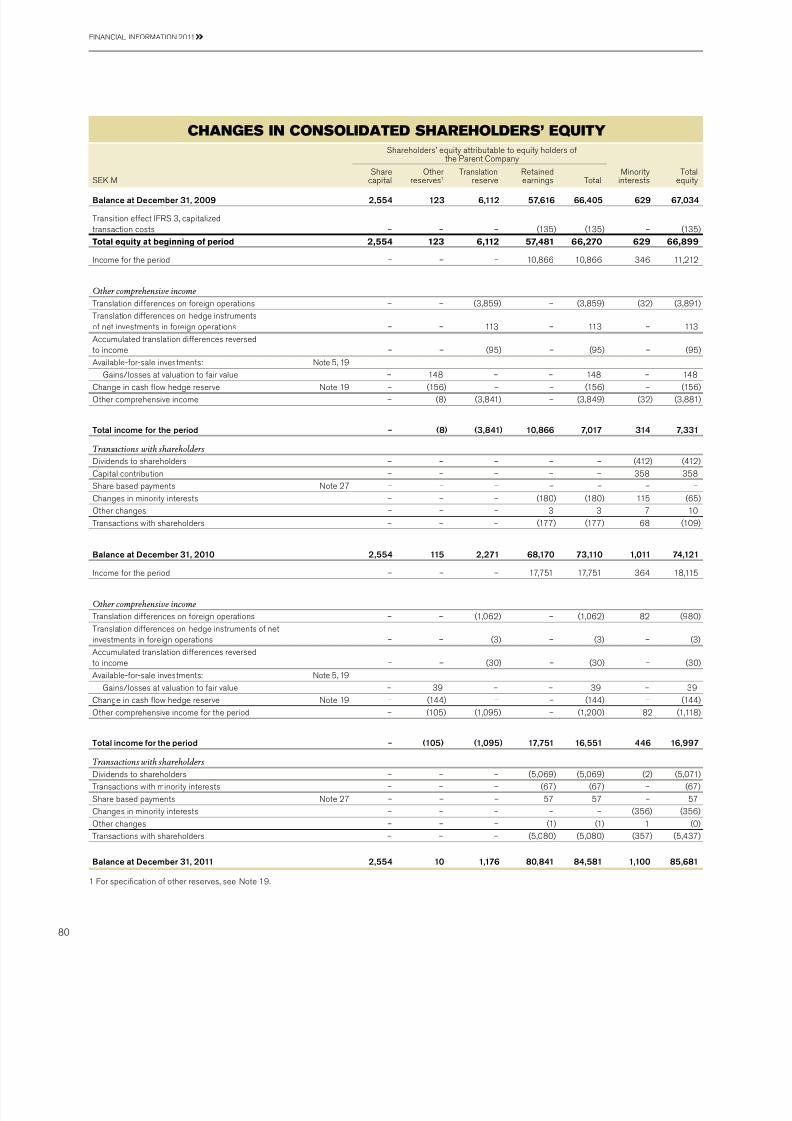

80 Changes in consolidatedShareholders’ equity

81 Notes to the consolidated nancialstatements

126 Parent Company AB Volvo

138 Proposed remuneration policy

139 Proposed disposition of unappropriated

earnings140 Audit Report for AB Volvo

141 Eleven-year summary

Corporate Governance Report

150 Group Management

152 Board of Directors and Auditors

154 Corporate Governance Report

Fold-out Denitions

Annual General Meeting

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 3/166

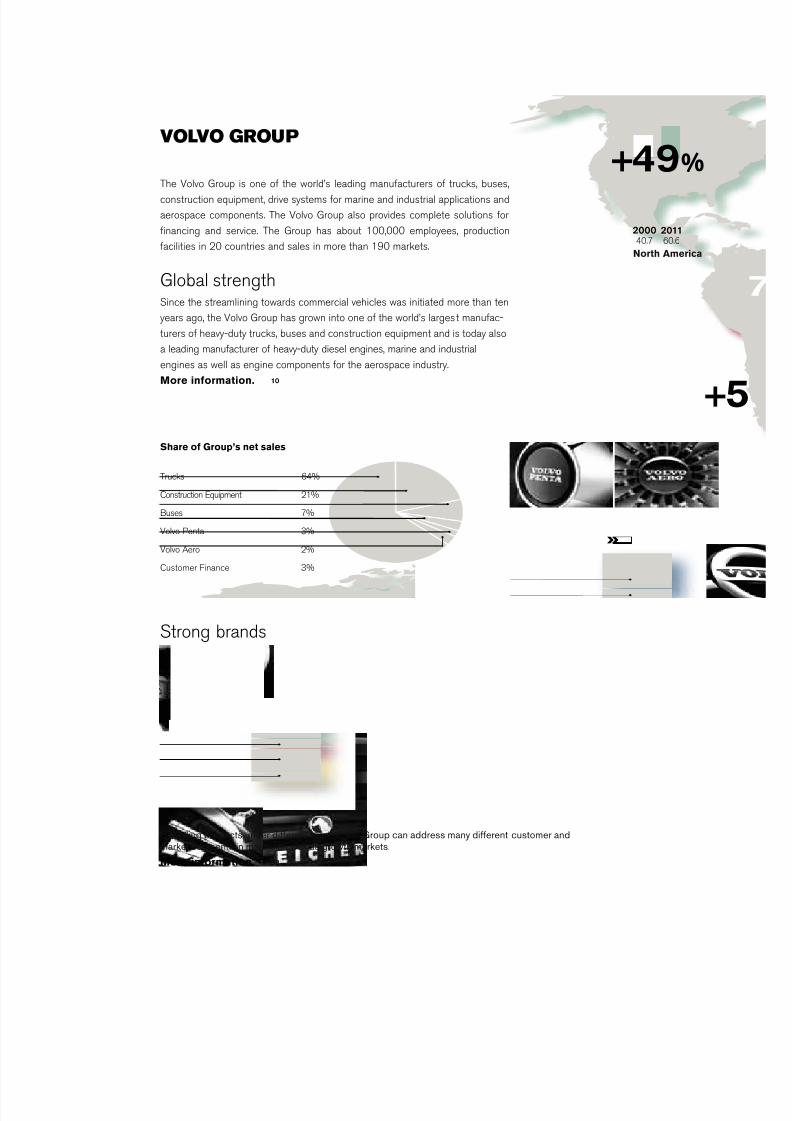

VolVo Group

The Volvo Group is one of the world’s leading manufacturers of trucks, buses,construction equipment, drive systems for marine and industrial applications and

aerospace components. The Volvo Group also provides complete solutions for

nancing and service. The Group has about 100,000 employees, production

facilities in 20 countries and sales in more than 190 markets.

Global strengthSince the streamlining towards commercial vehicles was initiated more than ten

years ago, the Volvo Group has grown into one of the world’s largest manufac-

turers of heavy-duty trucks, buses and construction equipment and is today also

a leading manufacturer of heavy-duty diesel engines, marine and industrial

engines as well as engine components for the aerospace industry.More information. 10

Europe, 39%

North America, 19%

South America, 11%

Asia, 24%

Rest of the world, 7%

Share of Group’s net sales by geographyShare of Group’s net sales

Trucks 64%

Construction Equipment 21%

Buses 7%

Volvo Penta 3%

Volvo Aero 2%Customer Finance 3%

Strong brands

By selling products under different brands , the Group can address many different customer andmarket segments in mature as well as growth markets.

More information. 38

North America

+

20112000

60.640.7

+49%

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 4/166

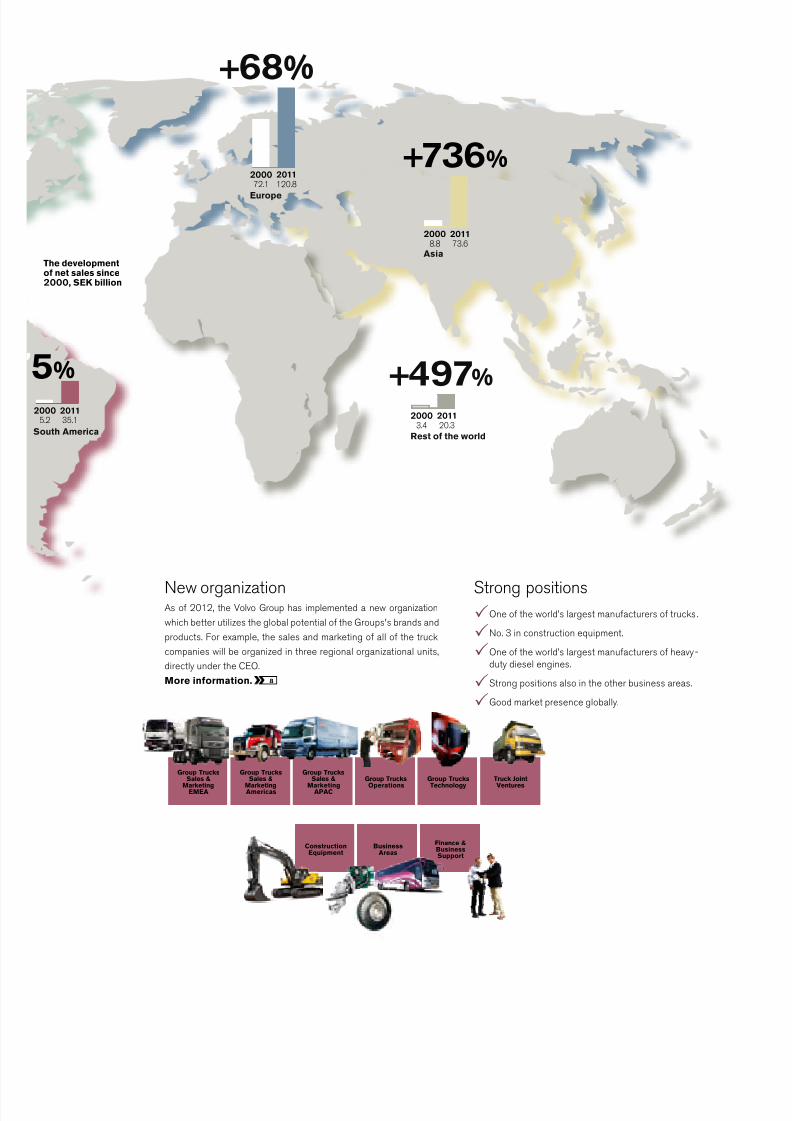

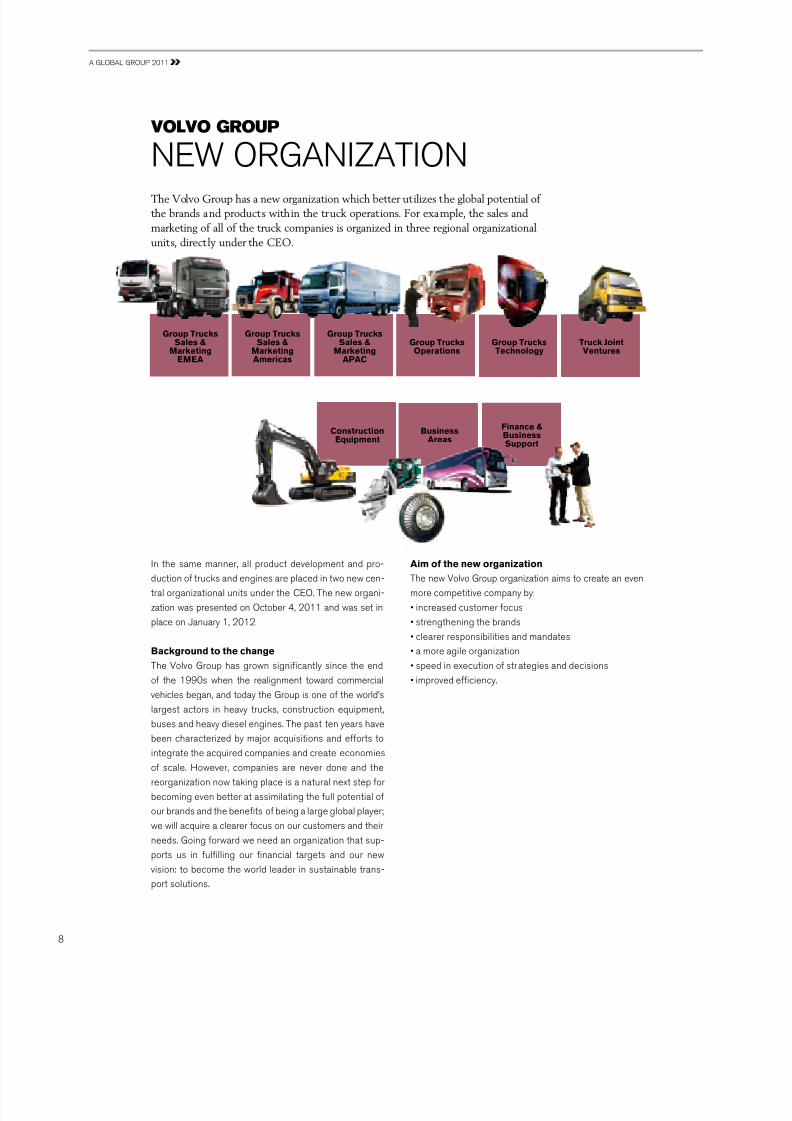

New organizationAs of 2012, the Volvo Group has implemented a new organization

which better utilizes the global potential of the Groups's brands and

products. For example, the sales and marketing of all of the truck

companies will be organized in three regional organizational units,

directly under the CEO.

More information. 8

Strong positions

One of the world’s largest manufacturers of trucks .

No. 3 in construction equipment.

One of the world’s largest manufacturers of heavy-

duty diesel engines.

Strong positions also in the other business areas.

Good market presence globally.

e developmentnet sales since00, SEK billion

Asia

Rest of the world

Group TrucksSales &

MarketingEMEA

Group TrucksSales &

MarketingAmericas

Group TrucksSales &

MarketingAPAC

Group TrucksOperations

Group TrucksTechnology

Truck JointVentures

ConstructionEquipment

BusinessAreas

Finance &BusinessSupport

20112000

73.68.8

+736%

%

20112000

20.33.4

+497%

20112000

120.872.1

+68%

20110

35.1

h America

Europe

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 5/166

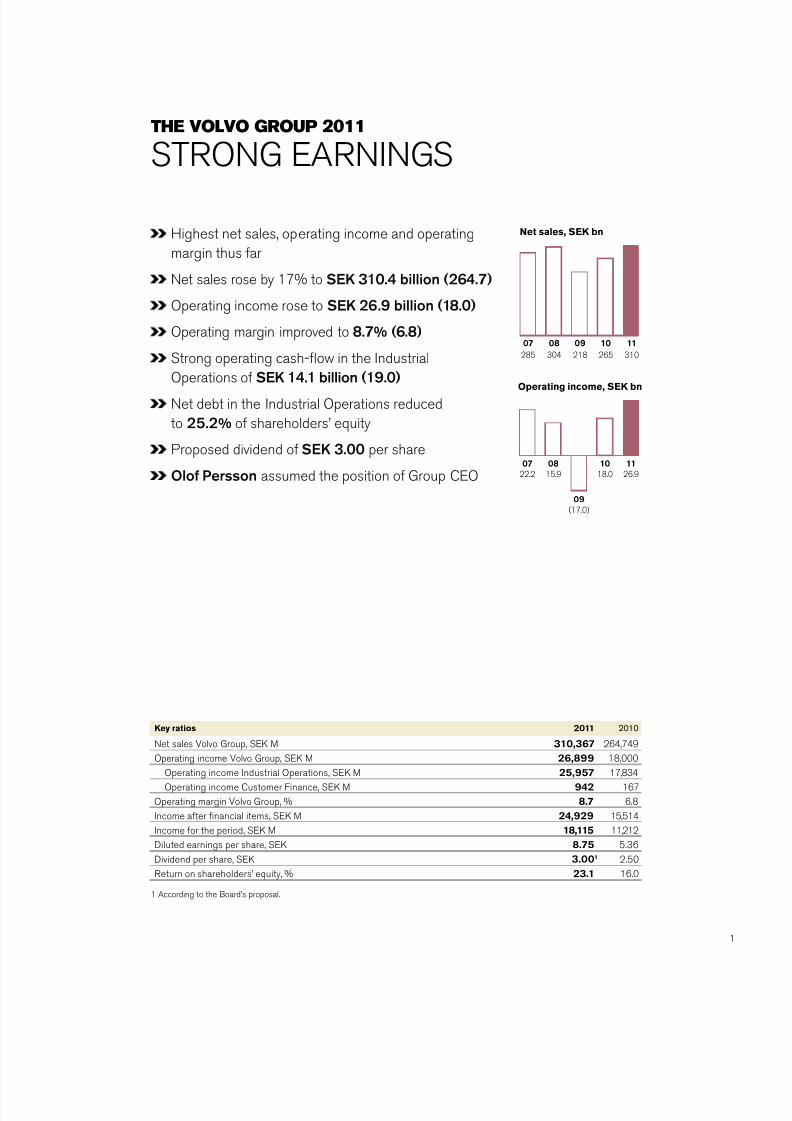

The VolVo group 2011

Sg gS

Key ratios 2011 2010

et sales Volvo group, SK M 310,367 264,749

peratin income Volvo group, SK M 26,899 18,000

peratin income ndustrial perations, SK M 25,957 17,834

peratin income Customer Finance, SK M 942 167

peratin marin Volvo group, % 8.7 6.8

ncome after nancial items, SK M 24,929 15,514

ncome for the period, SK M 18,115 11,212

Diluted earnins per share, SK 8.75 5.36

Dividend per share, SK 3.001 2.50

eturn on shareholders’ equity, % 23.1 16.0

1 ccordin to the Board’s proposal.

Hihest net sales, operatin income and operatin

marin thus far

et sales rose by 17% to SEK 310.4 billion (264.7)

peratin income rose to SEK 26.9 billion (18.0)

peratin marin improved to 8.7% (6.8)

Stron operatin cash-ow in the ndustrial

perations of SEK 14.1 billion (19.0)

et debt in the ndustrial perations reduced

to 25.2% of shareholders’ equity

Proposed dividend of SEK 3.00 per share

Olof Persson assumed the position of group C

Net sales, SEK bn

1110090807

310265218304285

Operating income, SEK bn

080807

09

(17.0)

15,915.922.2

11

26.9

10

18.0

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 6/166

gB gP 2011

A record year. That is one way of summing up 2011. We put the best

year ever under our belt and I can proudly state that all the hard work of

the Volvo Group’s employees to deliver the best products, services and

after-sales serv ice generated results.

Ceo CommenT

BS V

For the full-year 2011, the Volvo group enerated the

hihest net sales, the best operatin income and the

hihest operatin marin to date. et sa les rose to SK

310 billion (265), operatin income improved to SK 26.9

billion (18.0) and the operatin marin was 8.7% (6.8). t

the same time, return on operatin capital in the ndus-

trial perations rose to 28.8% and

return on shareholders’ equity in the

group to 23.1%.

Success in many ways

Success can be measured in

numerous ways; sales, orders

received or market shares. n par-

ticular, believe market shares pro-

vide a rapid and key indication of our

customers’ true opinions of our prod-

“We have now taken the rst steps on a journey which will

be full of challenges, but I am convinced that there is poten-

tial to increase sales and improve protability over time.”

ucts and how we compare to the competition. Market

shares comprise a clear acknowledement that we are

doin the riht thins.

et me provide a couple of examples from the past

year. t is wor th notin that enault rucks maintained its

market share in urope despite weak demand in its his-

toric stron markets in Southern urope. he Volvo brand

reaped reat success and in the heavy-duty sement in

urope increased its market share to a record 16.0%.

he uropean market weakened somewhat towards

the end of the year but after that stabilized on the new,

slihtly lower level.

Market shares in orth merica also increased. n

the .S., Volvo and Mack had a combined 19.8% of the

market for heavy-duty trucks. fter a number of slow years,

the situation is startin to appear very positive in orth

merica where we have made breakthrouhs with our

own enines and transmissions, an unbeatable

combination with a fuel-consumption that is

praised by our customers.

n Brazil, our market share rose to

17.1% for heavy-duty trucks and, for

the rst time, Volvo is the leader at the

top of the heavy-duty truck sement.

n the short-term, the Brazilian market

will be impacted by the transition to

new emission standards that took

place at the turn of the year, but we

have a positive view on the lon-term

development in Brazil and the other

markers in South merica.

2

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 7/166

world’s larest manufacturers of commercial vehicles

with stron positions in mature markets and with an

increasinly important presence in rowth markets. s a

step in further streamlinin the Volvo group towards

commercial vehicles, durin the year we initiated a pro-cess aimed at divestin Volvo ero.

Financially strong Group

Driven by improved protability and the ood cash ow,

the net nancial debt in the industrial operation was

down to 25% of shareholders’ equity at year-end, which

means that the group is nancially stron in an environ-

ment that in the beinnin of 2012 is characterized by

turmoil in the nancial markets and uncertain macro-

economic trends.

he Board of Directors proposes a dividend of SK

3.00 per share for 2011, up SK 0.50 per share com-

pared with the precedin year.

Reorganization to increase sales and proftability

We have a new vision – to become the world leader in

sustainable transport solutions. We shall fulll this by

creatin value for our customers and by pioneerin the

development in our industries. We have new nancial tar-

ets, a new oranization and a number of new manae-

ment teams in place. n January 1, 2012, we introduced

the new oranization which was put in place to better

capitalize on the lobal potential in our products and

brands and to improve the group’s efciency.

With the recent very positive trends in the group’s

development, we are in a favorable position. However,

this does not mean that everythin will run on rails.

reat deal of work remains. We have now taken the rst

steps on a journey which will be full of challenes, but

am convinced that there is potential to increase sales and

improve protability over time. his is a journey that am

very much lookin forward to.

lof PerssonPresident and C

Volvo Construction quipment (Volvo C) has also

strenthened its positions in several rowth markets

worldwide. n China our brands Volvo and SDg ained

the position as market leader within wheel loaders and

excavators. SDg recently launched new models of exca-vators, so we have hopes that the success in this iant

market will continue.

would also like to mention our hybrid buses that are

attractin an increasin amount of interest around the

world.

Increased proftability

good market conditions in the main and increasin market

shares driven by competitive products translated into us

deliverin some 238,000 trucks durin 2011 – an increase

of 32% compared to the precedin year. et sales in the

truck operations surpassed SK 200 billion and prot-

ability improved to an operatin marin of 9.1%.Volvo C increased its deliveries by almost 30% to the

new record level of 84,000 machines. he year was

intense with the launch of many new products and a con-

tinued expansion in rowth markets. Despite a stron

headwind from the weak dollar, Volvo C delivered an

operatin income of SK 6.7 billion and an operatin

marin of 10.2%.

From a historic perspective, Volvo Buses had a ood

year, both in terms of volumes and protability. his was

achieved by successful efforts to row in emerin mar-

kets, which offset the continued weak markets in urope

and the .S. peratin income increased to SK 1 billion

and operatin marin improved to 4.6%, which is below the

group averae but ood when compared to competitors.

Volvo Penta was impacted by a continued weak market

for marine enines and towards the end of the year also

for industrial enines, but despite this, achieved an oper-

atin income of almost SK 800 M with an operatin

marin of 8.8%.

For our Customer Finance perations, the trend pointed

in the riht direction, with portfolio rowth and lower

credit losses.

Volvo ero also had to strule with a sinicant

headwind from currency. Despite this, Volvo ero’s oper-

atin marin amounted to 5.2%.Durin my predecessor eif Johansson’s 14 years as

C, the Volvo group established itself as one of the

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 8/166

gB gP 2011

Vision

wanTedposiTion

Values

gB gP 2011

4

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 9/166

Our vision

he Volvo group’s vision is to become the world leader in sustainable transport solutions by:

• creatin value for customers in selected sements

• pioneerin products and services for the transport and infrastructure industries

• drivin quality, safety and environmental care

• workin with enery, passion and respect for the individual.

Volvo Group wanted position 2020

We are amon the most protable in our industry

We are our customers’ closest business par tners

We have captured protable rowth opportunities

We are proven innovators of enery-efcient transport solutions

We are a lobal team of hih performin people

Our values

he Volvo group views its corporate culture as a unique asset, since it is difcult for competitors to copy. By applyin and

strenthenin the expertise and culture we have built up over the years, we can achieve our vision.

Quality, safety and environmental care are the values that form the Volvo group’s common base and are important

components of our corporate culture. he values have a lon tradition and permeate our oranization, our products and

our way of workin. ur oal is to maintain a leadin position in these areas.

Environmental care

We believe that it is self-evident that our

products and our operations shall have

the lowest possible adverse impact on

the environment. We are workin to fur-

ther improve enery efciency and to

reduce emissions in all aspects of our

business, with particular focus on the

use of our products. ur oal is for the

Volvo group to be ranked as a leader in

environmental care within our industry.

o achieve this oal, we strive for a holistic

view, continuous improvement, technical

development and efcient resource utili-

zation.

Saety

Safety pertains to how our products are

used in society. We have had a leadin

position in issues reardin safety for a

lon time; our oal is to maintain this

position. focus on safety is an interal

part of our product development work.

ur employees are hihly aware of

safety issues, and the knowlede ained

from our internal crash investiations is

applied in product development. ur

oal is to reduce the risk of accidents

and mitiate the consequences of any

accidents that may occur as well as to

improve the personal safety and thework environment of the drivers of our

vehicles and equipment. ur lon-term

vision is zero accidents.

Quality

Quality is an expression of our oal to

offer reliable products and services. n

all aspects of our operations, from product

development and production to delivery

and customer support, the focus shall

be on customers’ needs and expecta-

tions. ur oal is to meet or exceed their

expectations. With a customer focus

based on everyone’s commitment and

participation, our aim is to be number

one in customer satisfaction. his is

based on a culture in which all employees

are responsive and aware of what must

be accomplished to be the best busi-ness partner.

new

new

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 10/166

gB gP 2011 gB gP 2011

The Volvo Group’s previous nancial goals were established by the Board in September 2006.

The Board focused on three goals comprising growth, operating margin and capital structure

for the Group’s Industrial Operations.

Growth

he rowth taret was that net sales should increase by a

minimum of 10% annually. Durin 2007–2011, the averae

rowth rate was 2.1% annually.

Operating margin

he Volvo group’s protability taret was that operatin marin

for the ndustrial operations was to exceed an averae of 7%

annually over a business cycle. he averae annual operatin

marin for the Volvo group’s ndus trial perations was 4.1%

from 2007 to 2011.

Capital structure

he capital structure taret is set to a net debt includin

provisions for post-employment benets for the ndustrial

operations of a maximum of 40% of shareholders’ equity

under normal conditions. s of December 31, 2011, the

Volvo group’s ndustrial operations had a net nancial debt

position correspondin to 25.2% of shareholders’ equity.

he taret for Customer Finance is a return on shareholders’

equity of 12–15% and an equit y ratio above 8%. he averae

annual return on shareholders’ equity for 2007–2011

amounted to 6%. t year end 2011 the equit y ratio was 9.1%.

1

2

34

FinanCial TargeTs

21

10

18

11

10

07

(30)

0

6

08

(28)

09

10

Target: above 10%

Net sales growth, %

6.9

10

8.6

11

7.8

07

0

5.2

08

(7.8)

09

10

(10)

Target: above 7%

Operating margin, %

37.4

10

25.2

11

5.7

07

0

(20)

(40)

39.7

08

70.9

09

40

20

80

60

N

e t c a s h

N e t d e b t

Target: below 40%

Net fnancial debt as percentageo shareholders’ equity, %

0.4

10

7.3

11

15.9

07(10)

0

12.6

08

(6.2)

09

15

10

5

(5)

Target: 12–15

Return on shareholders’ equity, %

Financial goals or Industrial Operations

Financial goals or Customer Finance Operations

2011

6

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 11/166

In September 2011 the Board of Directors of AB Volvo decided to implement new nancial

targets for the Volvo Group starting in 2012. The new targets have been set in order to enable

the growth and protability of the various operations to be measured and benchmarked annually

against competitors.

Transparent comparison with competitors

Volvo’s nancial tarets have included a focus on rowth

since the end of the 1990s and the Board of Directors

expects rowth to remain important in the future, but is

now addin a continuous benchmarkin of the rowth

and protability of the various operations aainst a

number of selected competitors.

o facilitate comparisons, the truck operations will be

measured jointly with the bus operations and the con-

struction equipment operations will be measured jointly

with Volvo Penta. n 2012, the comparisons will be made

in accordance with the table below:

Trucks and buses Volvo CE and Volvo Penta

Daimler Brunswick

veco C

M CH

avistar Cummins

Paccar Deere

Scania Hitachi

Sinotruk Komatsu

erex

The targets are ollowed up annually

• he annual oranic sales rowth for the truck, bus and

construction equipment operations, as well as Volvo

Penta, shall be equal to or exceed a weihted-averae

for comparable competitors.

• ach year, the operatin marin for the truck, bus and

construction equipment operations, as well as Volvo

Penta, shall be ranked amon the top two companies

when benchmarked aainst relevant competitors.

• For Customer Finance perations, the existin tarets

of 12–15% return of equity () and an equity ratio

exceedin 8% stand rm.

• Volvo ero has an taret of 15–25%. When calcu-

latin the , Volvo ero will be assined the

same equity ratio as that for the group’s ndustrial

perations.

• he capital structure taret is set to a net debt, includin

provisions for post-employment benets, for the ndus-

trial perations of a maximum of 40% of shareholders’

equity under normal conditions.

W gS FM2012

“Following the Group’s successfulgeographic and volume expansion, we have the prerequisites in place to compete successfully in our various product segments and it is with this in mind that the Boardhas now decided to introduce newnancial targets.”

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 12/166

gB gP 2011

n the same manner, all product development and pro-

duction of trucks and enines are placed in two new cen-

tral oranizational units under the C. he new orani-

zation was presented on ctober 4, 2011 and was set in

place on January 1, 2012.

Background to the change

he Volvo group has rown sinicantly since the end

of the 1990s when the realinment toward commercial

vehicles bean, and today the group is one of the world’s

larest actors in heavy trucks, construction equipment,

buses and heavy diesel enines. he past ten years have

been characterized by major acquisitions and efforts tointerate the acquired companies and create economies

of scale. However, companies are never done and the

reoranization now takin place is a natural next step for

becomin even better at assimilatin the full potential of

our brands and the benets of bein a lare lobal player;

we will acquire a clearer focus on our customers and their

needs. goin forward we need an oranization that sup-

ports us in fulllin our nancial tarets and our new

vision: to become the world leader in sustainable trans-

port solutions.

The Volvo Group has a new organization which better utilizes the global potential of

the brands and products within the truck operations. For example, the sales and

marketing of all of the truck companies is organized in three regional organizational

units, direct ly under the CEO.

VolVo group

W g

Group TrucksSales &

MarketingEMEA

Group TrucksSales &

MarketingAmericas

Group TrucksSales &

MarketingAPAC

Group TrucksOperations

Group TrucksTechnology

Truck JointVentures

ConstructionEquipment

BusinessAreas

Finance &BusinessSupport

Aim o the new organization

he new Volvo group oranization aims to create an even

more competitive company by:

• increased customer focus

• strenthenin the brands

• clearer responsibilities and mandates

• a more aile oranization

• speed in execution of strateies and decisions

• improved efciency.

8

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 13/166

ew oranization FQ

1. What will the new organization bring that is

so much better?

governance will become clearer and more efcient with

a clearer focus on brands and customers. Branded com-

panies in the truck business previously operated as both

independent units and part of a wider group structure.

he branded companies’ operations, product plannin,

product development and manufacturin are now coordi-

nated centrally, directly under the C, with a clear divi-

sion of responsibilities and minimum overlaps.

2. What happens to Volvo Trucks, Renault

Trucks, Mack and UD Trucks?

Sales and marketin of all of the truck companies is

oranized in three reional oranizational units. group

rucks Sales and Marketin mericas (comprisin all of

orth and South merica) with lobal responsibility for

the Mack brand, under the leadership of Dennis Slale.

group rucks Sales and Marketin M (comprisin

urope, the Middle ast and frica) with lobal responsi-

bility for the Volvo and enault brands, under the leader-

ship of Peter Karlsten. group rucks Sales & Marketin

PC (comprisin sia and Pacic) with lobal responsi-

bility for the D rucks brand, D, under the leadership of

Joachim osenber. ll product development and pro-

duction of trucks and enines is oranized in two new

central units: group rucks echnoloy and group rucksperations. here are no chanes to the nancial external

reportin – truck companies report their earnins com-

bined as previously.

3. What happens with Volvo CE?

he oranization remains intact. he Head of Volvo C,

Pat lney, continues to report directly to the C, lof

Persson. With respect to nancial external reportin, there

is no chane – the business areas report their results as in

the past.

4. What happens with Volvo Buses, Volvo Penta

and Volvo Aero?

he companies are oranized under Business reas,

headed by Håkan Karlsson. Per Carlsson has assumed

the position as new Head of Volvo Buses. göran gummeson

remains Head of Volvo Penta until pril 1, 2012 when he

is succeeded by Björn nemansson, but he no loner

reports directly to the C. Staffan achrisson remains

Head of Volvo ero but does not any loner report

directly to the C. With respect to nancial external

reportin, there is no chane – the business areas report

their results as in the past.

5. What happens with Volvo Financial Services?

he company is oranized under Finance and Business

Support headed by the new CF nders sber. Mar tin

Weissbur continues to head Volvo Financial Services

but does not any loner report directly to the C. With

respect to nancial external reportin, there is no chane

– the business areas report their results as in the past.

6. What happens with the dierent

business units?

Production is oranized under group rucks perations

headed by Mikael Bratt, while product development is

under group rucks echnoloy headed by orbjörn Holm-

ström. Volvo Parts has been divided into various units

based on their specic operations. he loistics portion

of Parts, as well as emanufacturin, falls under group

rucks perations. Purchasin is oranized under group

rucks echnoloy, where all other purchasin acti vities

are collected.

Volvo oistics falls under group perations, where all

loistics are handled.

Volvo Business Services, Volvo and Volvo group

eal state are oranized under Finance and Business

Support.

Volvo echnoloy and on-automotive Purchasin (P)

are oranized under group rucks echnoloy.

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 14/166

gB gP 2011

The Volvo Group’sacquisitions and

divestments

Durin this time, a number of acquisitions have been

made, which have brouht economies of scale and

increased eoraphical reach.

Volvo group has durin this time also successfully

established itself outside its historical markets of urope

and orth merica and ained a stron foothold in the

rowin markets of astern urope, South merica and

sia. Dur in 2011, the markets outside of Western urope

and orth merica accounted for for 49% of the ndustrial

perations’ total sales, compared to 17% in 2000.

n the followin paes there is more information

about the development on important markets and on

some of the Volvo group’s investments and successes on

them.

Long-term growth

he recovery that started in the group’s mature markets

in 2010 continued in Western urope and orth merica

durin 2011, with some tendencies towards a weakenin

in urope towards the end of the year. verall, demand in

the group’s rowth markets continued its stron devel-

opment, but also here demand weakened somewhat

towards the end of the year.

n the lon-term, demand for freiht capacit y, and thus

many of the group’s products, is closely linked to the

gDP trend. he extent of investment in infrastructure,

which drives demand for buildin and construction equip-

ment, is also closely linked to the gDP trend. n the

somewhat shorter-term, demand is affected by a number

of factors includin fuel prices, the implementation of

new emission reulations, interest rates, etc.

Since the streamlining towards commercial vehicles was initiated more than

ten years ago, the Volvo Group has grown into one of the world’s largest

manufacturers of heavy-duty trucks, buses and construction equipment and

is today also a leading manufacturer of heavy-duty diesel engines, marine and

industrial engines as well as eng ine components for the aerospace industry.

1998AcquisitionoftheexcavatoroperationsofSamsungHeavyIndustries.

1999SaleofVolvoCarstoFord.

2001Acquisitionofthetruckmanu-facturersMackandRenaultVI.

2003AcquisitionofBilia’sEuro-peantruckandconstructionequipmentdealers.

2004Saleofaxle-manufacturingoperationstoArvinMeritor.

2004Acquisitionofremaining50%oftheCanadianbusmanufacturerPrévost.

global sTrengTh

CHgg WD

gB gP 2011

10

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 15/166

Volvo Group net sales, SK bn

02 03 04 05 06 07 08 09 10 0

75

150

225

300

Economic growth in the U.S., Europeand Brazilnnual gDP-rowth, %

Source: ConsensusEconomics

1110090807

1.61.9(4.1)0.63.1 EU2.97.5(0.3)5.26.1 Brazil

1.7 USA3.0(3.5)(0.3)1.9

Economic growth in Asia, %nnual gDP-rowth, %

1110090807

4.47.11.93.87.2 Asia/Pacific*

7.08.58.06.89.0 India

(0.9) Japan4.5(5.5)(1.1)2.3

* China, Hong Kong, South Korea, Taiwan, Indonesia,Malaysia, Singapore, Thailand, Phillippines, Vietnam,Australia, New Zealand, India, Japan, Sri Lanka

9.2 China10.49.29.614.2

Source: ConsensusEconomics

AccordingtoConseEconomics,globalgrewby2.9%duri2011comparedwi4.3%in2010.GDtheEUgrewby1.6(1.9%),intheUSb1.7%(3.0%).JapaGDPfellby0.9%ahavingrisenby4.5%2010.GrowthincotriessuchasBrazil,andChinawasdamenedcomparedtohighlevelsof20102012,globalGDPexpectedtogrowb2.6%.Thefast-groeconomiesprimariAsiaandLatinAmecontinuetobethemarygrowthengin

2005SaleoftheservicecompanyCeleroSupport.

2006AcquisitionofJapanese

NissanDiesel(NowUDTrucks).Com-pletedin2007.

2007AcquisitionofChinesewheelloadermanufacturerLingong.

2007AcquisitionofIngersollRand’sroaddevelopmentdivision.

2008JointventurewithEicherMotorsofIndiawithintrucksandbuses.

growTh

Strong positions

ne of the world’s larest manufacturers of trucks.

o. 3 in construction equipment.

ne of the world’s larest manufacturers of heavy-dutydiesel enines.

Stron positions also in the other business areas.

good market presence lobally.

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 16/166

gB gP 2011

Growing markets

n 2011 the heavy-duty truck market in urope 29 (’s 27

member states, orway and Switzerland) increased by

35% to 242,400 trucks compared to 179,200 in the pre-

cedin year. n 2012, the total market for heavy-duty

trucks in urope 29 is expected to experience a moderate

decline to a level of about 220,000 trucks. he start of

the year is expected to be slow with a radual pick-up in

demand as customers start to renew their eets ahead of

the new emission reulation in 2014.

he construction equipment market increased substan-

tially in 2011 compared to the weak 2010. When measured

in number of units, the total market increased by 31%.

Despite the stron increase, the market is far from the

record levels of 2007. he uropean market for construction

equipment is expected to row by 10–20% durin 2012.

he uropean bus market was weak durin the year

with erce competition. Demand for marine enines was

characterized by a wait-and-see approach amon boat

buyers and the development was aumented by the lobal

turmoil in nancial markets. he nancial concern also

impacted the market for industrial enines, where

demand declined from hih levels.

Increased market shares in Europe

he group’s truck business ained market share in many

markets durin the year. n urope 29 the group’s combined

market share increased to 26.3% (24.4), primarily driven by

the Volvo brand.

New city bus given global premiere

t the end of ctober, Volvo Buses’ new city bus, the Volvo

7900, was iven its world premiere, when it was presented

at the lare international bus fair, Busworld, in Kortrijk in

Belium. Busworld is a lare and important fai r for the bus

industry and attracts visitors from all over the world. he

Volvo 7900 is a lowoor bus that has been desined to be

lihter, more fuel efcient and to take more passeners.

t the fair Volvo Buses also presented its hybrid version

of the Volvo 7900. he already very low fuel consumption

in Volvo’s hybrid bus will be even lower. Fuel consumption

will be up to 37% lower than a diesel bus, compared with up

to 35% in current hybrid buses.

However, the hybrid version is only one of the options

with respect to the new Volvo 7900. he bus is offered

with enines for diesel/biodiesel and natural as/bioas.

t is available as 12-meter bus or 18-meter articulated bus.

Environmentally-adapted products

n May, Volvo rucks launched the new Volvo FM Methane-

Diesel truck, a as-powered truck for lon-haul opera-

tions enhancin its focus on alternative fuels.

his truck can be powered by up to 75%

as and if run on bioas, emissions

of carbon dioxide from fossil

fuel could be cut by up to

70% compared with a

conventional diesel

enine.

During 2011, the European market accounted for SEK 121 billion,corresponding to 39%, of Group net sales. Europe is the historical

home market for both Volvo and Renault Trucks. In Europe, the

Group has a considerable industrial structure with a relatively large

share of its manufacturing and sizeable exports.

deVelopmenT by ConTinenT

P – H gS MK

gB gP 2011

1212

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 17/166

he world’s most powerful hybrid truck was launchedby Volvo rucks in the rst quarter. he Volvo F Hybrid,

the rst parallel hybrid from Volvo rucks, uses techniques

able to reduce fuel consumption and carbon dioxide emiss-

ions by up to 20%, and it makes the truck much more

silent. his is a very competitive solution for heavy distri-

bution and waste disposal in urban areas.

enault ruck has delivered the rst serial enault

Premium Distribution hybrid truck (Hybrys ech). enault

rucks also continued to extend its offerin of fully-electric

vehicles, and in ctober a fully-electric 16-ton enault

Midlum was delivered to the French retail chain Carrefour.

he truck is to be used for deliveries to supermarkets in

downtown yon, France. enault rucks also launched asystem called ptiroll for the enault Premium oute

ptifuel truck. ptiroll reduces fuel consumption even

further.

Volvo has taken the lead in introducin environmentally

friendly ier 4 nterim/Stae B-compliant products in

orth merica and urope, with the successful launch of

complete new enerations of machines affected by the

leislation. he company’s new V-C enine systems

have the hallmarks of lower emissions, better performance,

improved operational economy and hiher quality. s well

as advanced enine monitorin and control, the new Volvo

system uses an advanced exhaust after-treatment system

that reduces particulate matter by 90% compared to the

previous machine series.

Market development, heavy-duty trucks , Europe

housands

1110090807

242179165319328

242

Market development, construction equipment, Europe

housands

1110090807

1249476173217

124

Market shares in Europe, heavy-duty trucks %

11101110

10.310.216.014.2

Volvo Renault

VolVo FmMHDS

Volvo Group in Europe

• Net sales: SK 120,828 M (102,947)

• Share o Group sales: 39%

• Number o employees: 55,121

• Share o Group employees: 56%

• Largest markets: France, Sweden,great Britain, germany and ussia.

37%

Bus that lowers fuel

consumption by as much as

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 18/166

gB gP 2011

Russia back on the growth track

Durin 2011, the total market for trucks over 12 tons was

approximately 106,200 vehicles in ussia, considerably

more than the 61,500 that were sold durin 2010 and a

vast increase compared to the bottom in 2009 when thetotal market amounted to 37,100 trucks.

Volvo is the biest imported brand in ussia with a

total population of more than 55,000 heavy-duty trucks

in the country. population that has been built-up durin

a lon period of time. he population of enault trucks is

approximately 20,000 heavy-duty trucks. Durin 2011,

Volvo delivered 5,300 trucks (2,800) and enault trucks

delivered 1,300 trucks (800) in ussia.

n January 2009, the group opened a factory for the

assembly of trucks in Kalua, approximately 200 kilo-

meters south of the capital Moscow. lon-term con-

dence in the ussian market’s rowth prospects and to

come inside the duties and fees that apply to imported

trucks were important reasons for the establishment.

here are a number of other forein truck and auto makers

established in Kalua. t maximum capacit y, the plant in

Kalua can assemble 10,000 Volvo and 5,000 enaulttrucks annually. n 2011, 3,800 Volvo and 1,400 enault

trucks were manufactured in the plant.

Volvo Construction Equipment invests in Russia

Volvo Construction quipment will invest SK 350 M to

build a 20,660 m2 excavator plant in Kalua, ussia,

hihlihtin the company’s continued commitment to the

ussian market.

he new factory is part of the on-oin expansion in

developin markets. he plant will be built on the 15 hec-

tares of land that Volvo acquired in 2007. he Kalua plant

will initially manufacture ve models of Volvo excavators

FoCus

SS

After a considerable drop in connection with the nancial crisis, theRussian market has recovered.

gB gP 2011

1414

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 19/166

The market or trucks over 12 tons in Russia

o. of trucks, thousands

00

44

01

51

02

46

03

52

04

58

05

67

06

90

07

116

08

110

09

37

10

62

11

106

10

Volvo Group net sales in Russia, SK bn

00 11

8.9

0.2

Russia

• Area: 17,075,000 km2 (the larest country in the world)

• Population: 141.8 milli on

• Capital: Moscow with 10.2 million inhabitants (2008)

• Other big cities: St Petersbur (4.6), ovosibirisk (1.4),Jekaterinbur (1.3), izjnij ovoorod (1.3)

• GDP per capita: SD 10,522 (2010)

Volvo Group in Russia

• Number o employees: 1,644

• Production: ruck factory in Kalua. xcavator factoryunder construction in the same city

• Net sales: SK 8,895 M, 3% of group sales

• Volvo – the larest eet of Western trucks consistin ofmore than 55,000 vehicles

includin the Volvo C210, C240, C290, C360 and

C460, with production planned to bein in the rst quarter

of 2013.

“he new investment in ussia is part of our stratey to

build machines where they are sold and thanks to a stronpartnership with our ussian dealer, Ferronordic, our cus-

tomer base is rowin sinicantly in the country,” says

Head of Volvo Construction quipment, Pat lney.

t the same time, the distributor Ferronordic Machines

is implementin substantial investments in the distribution

network in the vast country. Ferronordic Machines plans

to invest in the reion of 100 M in the expansion of

its reional distribution network and will open as many as

60 new branches in the country by the end of 2015. his

will provide for a presence in all of ussia – from the Baltic

Sea to the Pacic cean.

141.8millioninhabitants

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 20/166

gB gP 2011

16

Growing truck market

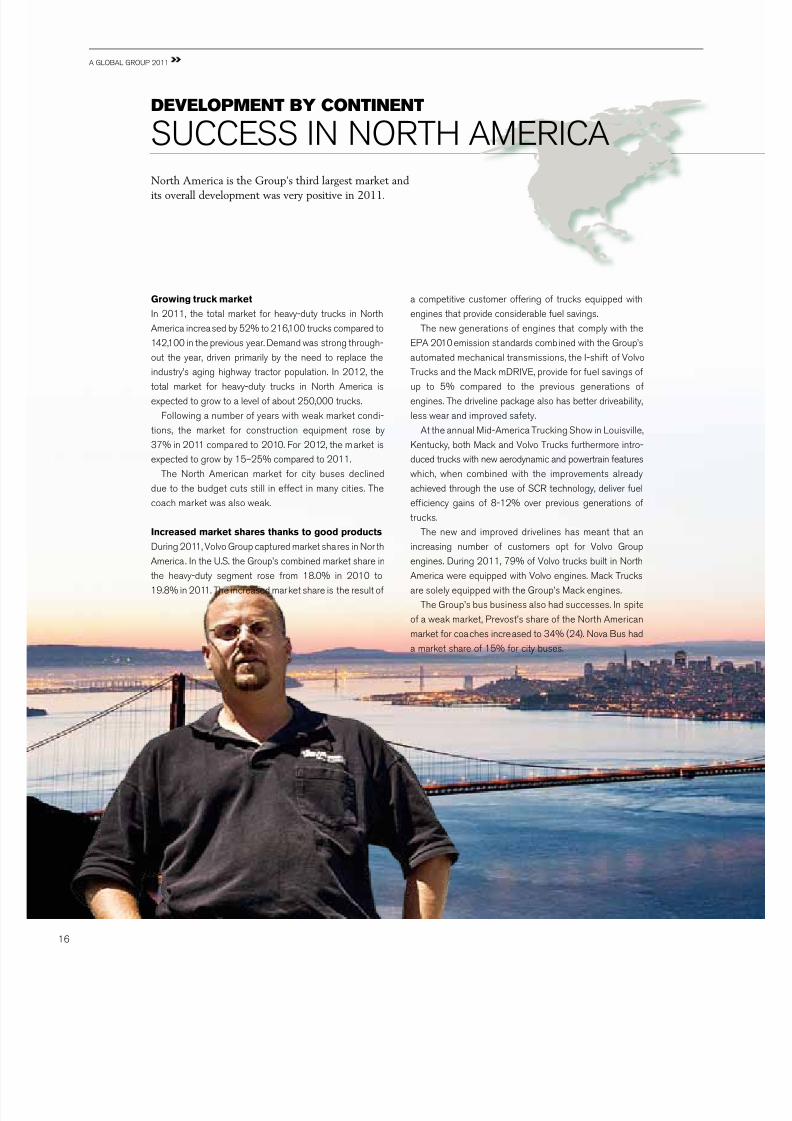

n 2011, the total market for heavy-duty trucks in orth

merica increased by 52% to 216,100 trucks compared to

142,100 in the previous year. Demand was stron throuh-

out the year, driven primarily by the need to replace the

industry’s ain hihway tractor population. n 2012, the

total market for heavy-duty trucks in orth merica is

expected to row to a level of about 250,000 trucks.

Followin a number of years with weak market condi-

tions, the market for construction equipment rose by

37% in 2011 compared to 2010. For 2012, the market is

expected to row by 15–25% compared to 2011.

he orth merican market for city buses declined

due to the budet cuts still in effect in many cities. he

coach market was also weak.

Increased market shares thanks to good products

Durin 2011, Volvo group captured market shares in or th

merica . n the .S. the group’s combined market share in

the heavy-duty sement rose from 18.0% in 2010 to

19.8% in 2011. he increased market share is the result of

a competitive customer offerin of trucks equipped with

enines that provide considerable fuel savins.

he new enerations of enines that comply with the

P 2010 emission standards combined with the group’s

automated mechanical transmissions, the -shift of Volvo

rucks and the Mack mDV, provide for fuel savins of

up to 5% compared to the previous enerations of

enines. he driveline packae also has better driveability,

less wear and improved safety.

t the annual Mid-merica ruckin Show in ouisville,

Kentucky, both Mack and Volvo rucks furthermore intro-

duced trucks with new aerodynamic and powertrain features

which, when combined with the improvements already

achieved throuh the use of SC technoloy, deliver fuel

efciency ains of 8-12% over previous enerations of

trucks.

he new and improved drivelines has meant that an

increasin number of customers opt for Volvo group

enines. Durin 2011, 79% of Volvo trucks built in orth

merica were equipped with Volvo enines. Mack rucks

are solely equipped with the group’s Mack enines.

he group’s bus business also had successes. n spite

of a weak market, Prevost’s share of the orth merican

market for coaches increased to 34% (24). ova Bus had

a market share of 15% for city buses.

North America is the Group’s third largest market andits overall development was very positive in 2011.

gB gP 2011

deVelopmenT by ConTinenT

SCCSS H MC

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 21/166

I-shit to be produced in the U.S.

s a result of the stron demand for the group’s auto-

mated mechanical transmissions, the company in June

announced that production of the Volvo -Shift and Mack

mDV earboxes will start at its .S. enine plant in

the third quarter of 2012.

Volvo rucks introduced its -Shift transmission on the

orth merican market in 2007. Durin 2011, 45% of

trucks with Volvo enines in orth merica were

equipped with -Shift and customers continue to report

sinicant fuel economy improvements with the auto-

shift transmission. Since -Shift is only available toether

with Volvo enines, this also helps promote sales of the

company’s own enines. -Shift incorporates a host of

fuel-savin and productivity-enhancin features into a

reliable, durable, and lihtweiht desin.

he transmission is currently assembled in Köpin, Swe-

den, and then sent to the S production plant in Haers-

town, Maryland for adaptation to orth merican market

requirements. he company is now investin SD 7 M in

Haerstown to build a new assembly line, install new

equipment and toolin, and train its employees. he

new assembly line is primarily intended to supply

the orth merican market.

Market development, heavy-duty trucks , North America

housands

1110090807

216142118185208

216

Market development, construction equipment, North America

housands

1110090807

1128268137173

112

Volvo Group in North America

• Net sales: SK 60,560 M (47,922)

• Share o Group sales: 19%

• Number o employees: 15,427

• Share o Group employees: 16%

• Largest markets: S, Canada and Mexico.

19.8%

Volvo Group’s market share in the heavy-duty

segment increased from 18.0% in 2010 to

in 2011

i-shiFT

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 22/166

gB gP 2011

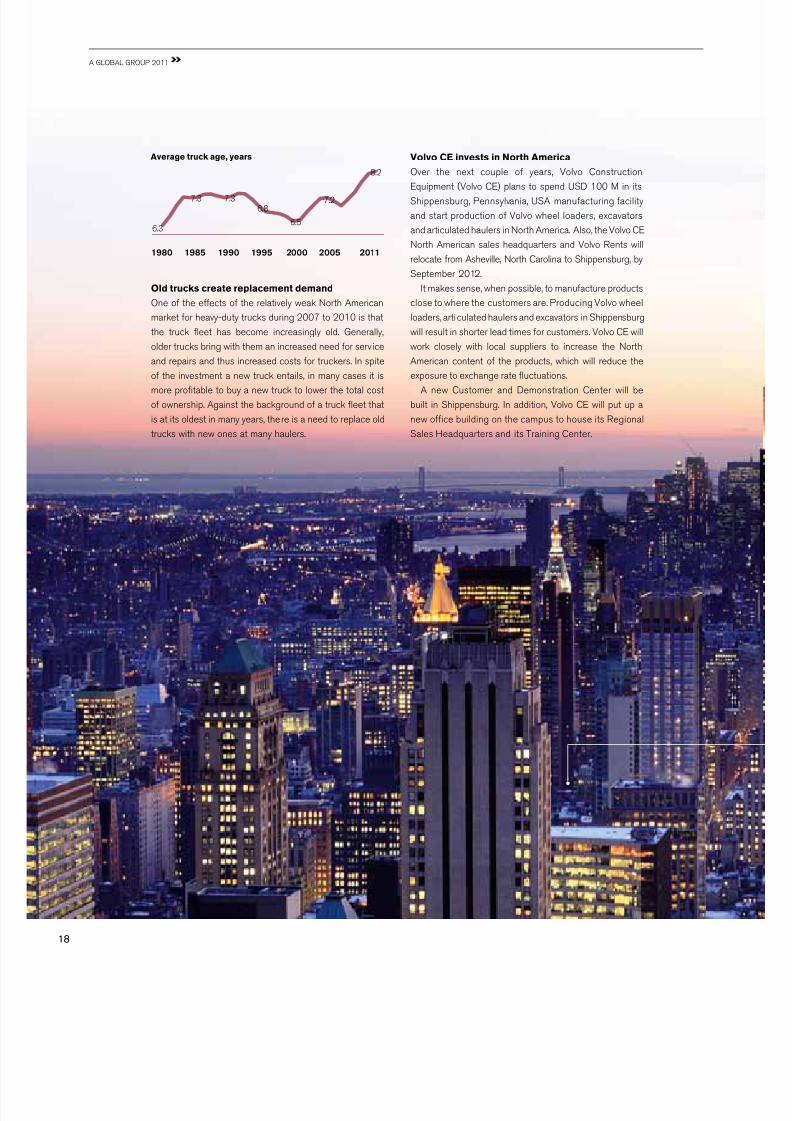

Old trucks create replacement demand

ne of the effects of the relatively weak orth merican

market for heavy-duty trucks durin 2007 to 2010 is that

the truck eet has become increasinly old. generally,

older trucks brin with them an increased need for serv ice

and repairs and thus increased costs for truckers. n spite

of the investment a new truck entails, in many cases it is

more protable to buy a new truck to lower the total cost

of ownership. ainst the backround of a truck eet that

is at its oldest in many years, there is a need to replace old

trucks with new ones at many haulers.

Volvo CE invests in North America

ver the next couple of years, Volvo Construction

quipment (Volvo C) plans to spend SD 100 M in itsShippensbur, Pennsylvania, S manufacturin facility

and start production of Volvo wheel loaders, excavators

and articulated haulers in orth merica. lso, the Volvo C

orth merican sales headquarters and Volvo ents will

relocate from sheville, orth Carolina to Shippensbur, by

September 2012.

t makes sense, when possible, to manufacture products

close to where the customers are. Producin Volvo wheel

loaders, articulated haulers and excavators in Shippensbur

will result in shorter lead times for customers. Volvo C will

work closely with local suppliers to increase the orth

merican content of the products, which will reduce the

exposure to exchane rate uctuations.

new Customer and Demonstration Center will be

built in Shippensbur. n addition, Volvo C will put up a

new ofce buildin on the campus to house its eional

Sales Headquarters and its rainin Center.

Average truck age, years

1980

6.3

7.3 7.3

6.8

6.5

7.2

8.2

1985 1990 1995 2000 2005 2011

gB gP 2011

1818

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 23/166

noVa busin newyorK CiTy

Since the acquisition of the Shippensbur facility in

2007, Volvo Construction quipment has continuously

invested in the existin plant. n June 2010, a 18,580 m2,

SD 30 M expansion of the facility was nalized, to improve

manufacturin ow and increase production space to

incorporate the production of Volvo motor raders.

Manufacturin Volvo wheel loaders, articulated haulers

and excavators in Shippensbur, P will have no sini-

cant impact on the current production in other Volvo loca-

tions. t will, however, further improve the competitiveness

and protability of the total business.

Multi-million dollar contract or Volvo Buses

in New York City

n June 2011, Volvo Buses secured an order for 328articulated buses for ew ork City throuh its subsidiary

ova Bus. he order is valued at SK 1.5 billion.

he order applies to 328 ova FS articulated buses.

he client, M ew ork City ransit, has a eet of more

than 6,000 buses, the larest bus eet amon all local

transport companies in orth merica and one of the lar-

est in the world. n the past year, M tested 90 of ova’s

articulated buses, includin on ine M15 in Manhattan.

hey are the rst buses in ew ork City with three doors

and low oors throuhout the bus, which contribute to

more rapid and comfortable boardin and alihtin.

he buses functioned very well durin the test and

contributed to the new major order. he 328 new buses

will be delivered from uust 2011 to pril 2013. ne

prerequisite for sellin city buses in the S is that a lare

portion of the manufacturin must also occur in the

country. he buses for ew ork City are manufactured

in the ova Bus plant in Plattsburh, in the northern part

of ew ork State.

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 24/166

gB gP 2011

Strong market

he South merican market for heavy-duty trucks rose

by 7% to 148,000 trucks in 2011 compared to 138,800

the year before.

Brazil is the larest market by far in South merica.

With 111,500 heavy-duty trucks in 2011 (109,800) Brazil

accounted for approximately 75% of the total market in

the reion. he Brazilian market was primarily driven by

the positive economic development in the country.

ainst the backround that Brazil moved directly from

the uro emission standard to uro V on January 1,

2012 order intake is expected to be relatively weak in the

beinnin of the year. he total market for heavy-duty

trucks in Brazil is expected to record a sliht decline and

reach a level of about 105,000 trucks for the full year

2012.

he construction equipment market rose by 18% in

2011 compared to the stron 2010. he South merican

market for construction equipment is expected to row

by 0–10% durin 2012.

he South merican bus market was stron durin the

year and is estimated to have rown by more than 30%.

he total bus market in Brazil increased by 25% to 4,900

buses, driven by prebuys ahead of the chaneover to

uro V and by many procurements of B-systems (Bus

apid ransit) in the cities. Volvo Buses increased its

market share to 23%.

The South American market has had high growth rates in recent years withBrazil as the engine. The fundamentals are in place for this development to

continue.

deVelopmenT by ConTinenT

SH MC CS S

gB gP 2011

2020

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 25/166

Increased market shares in heavy-duty trucks

Volvo rucks reaped success in the Brazilian market in

2011. Competitive products and a stron dealer network

provided for bi strides forward in the market. he market

share within heavy-duty trucks increased to 17.1% (14.8).

Market development, heavy-duty trucks, South America

housands

1110090807

1481398611791

148

Market development, construction equipment, South America

housands

1110090807

4235213325

42

Volvo Group in South America

• Net sales: SK 35 ,142 M (29,013)

• Share o Group sales: 11%

• Number o employees: 5,234

• Share o Group employees: 5%

• Largest markets: Brazil, Chile and Peru.

30%

The South American bus

market increased by more than

5,200employees

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 26/166

gB gP 2011

ven thouh the lobal nancial crisis a few years ao

led to a recession also in Brazil, the economy there

rebounded faster than in many other parts of the world.

Durin 2008 gDP rew by 5.2%, followed by a fall of

0.3% in 2009 but it turned around stronly and rose by

7.5% durin 2010 and by 2.9% in 2011, accordin to

Consensus conomics.

New products

Durin the year, Volvo rucks was the rst manufacturer to

launch trucks that comply with the new emission reulation

accordin to uro V that took effect on January 1, 2012.

he year also saw the launch of the all-new medium-

duty truck Volvo VM, which is produced specically for

the South merican market. he truck is adapted to

applications such as reional and city distribution.

n order to meet the increasin demand for buses in

the front enine sement, which in South merica

amounts to as many as 16,000 buses annually, Volvo

Buses launched a new front enine bus that was well-

received when it was introduced.

Success at Fenatran

Volvo do Brasil brouht toether 250 journalists from

Brazil and other atin merican countries for a press

conference with head of Volvo do Brasil, oer lm, at

FoCus

B

The Brazilian economy has had a very good growth since the beginning of the 21st century thanks to increased private

consumption and measures to reduce poverty.

the openin of the 18th nternational

ransportation Fair – Fenatran 2011.

Fenatran is the larest trade fair of

the transport sement in atin merica

and took place in São Paulo from

ctober 24 to 28, 2011. he outcome of the fair was ver y

positive for Volvo do Brasil with lare interest from cus-

tomers and more than 10,000 visitors to the Volvo stand.

lso, durin the fair a lare number of orders were sined,

of which more than half were for the new uro V trucks.

Increased production

Durin the year, Volvo do Brasil started the production of

the automated mechanical earbox -Shift. Volvo also

started local production of 11-liter enines. Previously,

components for the -Shift were imported from urope

and assembled locally. he earboxes will equip the

Volvo FH and Volvo FM.

“he -Shift earbox has been ettin outstandin

acceptance in Brazil and in all the other countries of

South merica. t already equips about 80% of the Volvo

FH and Volvo FM trucks and over 90% of the hihway

buses which leave our assembly line in Curitiba”, says

head of Volvo do Brasil, oer lm.

he success of the electronic earbox is mainly due to

the noticeable consumption reduction that it allows –

gB gP 2011

2222

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 27/166

Brazil

• Area: 8,547,404 km2

• Population: 195 million (2010 estimate)

• Capital: Brasilia with 2.5 million inhabitants (2010 estimate)

• Other big cities (2010 estimates): São Paulo (10.4),io de Janeiro (6.3), Salvador de Bahia (3.0) and Fortaleza (2.6)

• GDP per capita: SD 10,471 (2010)

Volvo Group in Brazil

• Number o employees: 4,546

• Production: Curitiba (trucks and buses) andPederneiras (construction equipment)

• Net sales: SK 26,056 M, 8% of group sales

• Best employer 2011

up to 5% compared to vehicleswith manual equipment. Besides,

it provides more durability to the clutch,

less tire wear, and increases the comfort and safety levels

for the driver.

With the 11-liter enine nationalization, the Curitiba

Volvo factory increases its portfolio of locally manufactured

products. he enines line is exible and now both 13-liter

and 11-liter enines are manufactured in the country.

Best employer in Brazil

For the second time, Volvo do Brasil was chosen as the

best employer in Brazil. he survey is conducted by the

Você S/ and xame maazines and comprises 504companies in different sectors. t ranks the best 150

employers in Brazil. Volvo do Brasil has 3,900 employees

and headquarters in Curitiba and it has always been

ranked in the top ten. n the 2011 survey, Volvo do Brasil

obtained excellent results in all cateories.

Volvo CE moves ahead

Volvo Construction quipment (Volvo C) moves ahead

in Brazil. n accordance with the stratey to support the

development in rowth economies, the factory in Peder-

neiras has started to manufacture three excavator models.

Volvo C has also introduced its Chinese brand SDg

with reat success in Brazil. he machines are imported

from China and reach new customer sements where

Volvo C has had a hard time

competin in the past.

Surverys show that as

many as 90% of SDg

customers have pre-

viously not been in contact with the Volvo group reardin

construction equipment.

Largest contract or hybrid buses

n July 2011, Volvo Buses received its larest hybrid bus

order thus far. he city of Curitiba in Brazil ordered 60

buses that enerate up to 35% less fuel consumption.

“Several of the larest cities in Brazil and the rest of

South merica tested a Volvo 7700 Hybrid in 2010 and

at the beinnin of this year,” says uis Carlos Pimenta,

head of Volvo Buses in atin merica. “he tests were

very successful and contributed to this rst order, which

we believe will be followed by additional orders from other

cities.”

Consequently, Volvo Buses has decided to commence

manufacturin hybrid buses in Curitiba. t will involve the

same hybrid technoloy used in Volvo’s hybrid buses and

trucks in urope and which is currently the world’s most

efcient for heavy vehicles.

Volvo Group net sales in Brazil

SK bn

00 11

26.1

3.6

i-shiFT

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 28/166

gB gP 2011

Growing markets

Sales in sia accounted for 24% of group net sales dur-

in 2011. n 2000 the correspondin ure was 7%. he

sharp increase has primarily been achieved by the acqui-

sitions of D rucks of Japan (which was named issan

Diesel at the time of the acquisition), the majority in inon

of China and throuh the joint venture VCV in ndia, but

also throuh substantial oranic rowth in many markets.

hrouh the brands D rucks, Volvo, enault rucks

and icher, the Volvo group has stron positions in

Japan, ndia, Korea and all of Southeast sia.

n Japan the heavy-duty truck market rew by 1% to

24,800 vehicles durin 2011. he rst half of the year

was weak, primarily as an effect of the earthquake and

ensuin tsunami that hit the country on March 11.

owards the end of the year, there were sins of a recovery

in the market, amon other thins aainst the backdrop

of the work to rebuild devastated reions beinnin to et

underway. For 2012, the Japanese market for heavy-duty

trucks is expected to row to approximately 30,000 vehicles.

n China the larest part of net sales stem from con-

struction equipment. he Chinese market slowed some-

what durin the latter part of 2011 after a number of years

of stron rowth. n total, the market rew by 7% durin the

year. he Volvo group strenthened its position as leader

in the sement for wheel loaders and excavators. n sia

outside of China, the market for construction equipment

rew by 28%. n 2012 the Chinese market is expected to

be on the same level as in 2011. sia excludin China is

expected to row by 10–20%.

Volvo CE number 1 in China

With a volume totalin 405,000 machines, the Chinese

market for construction equipment is the world’s larest.

When measured in number of units, it is in fact almost as

lare as the rest of the world put toether. nd the Volvo

group is number 1 in wheel loaders and excavators in

China. Durin 2011 Volvo Construction quipment’s both

brands Volvo and SDg had a combined market share of

12% within wheel loaders and excavators. hat made

them market leaders in China, ahead of all domestic manu-

facturers and with a ood marin to the other lobal

manufacturers. Contributin to the success was the fact

that SDg started sellin a rane of four excavators, a

product they previously lacked. n January 2012, SDg’s

new excavator plant in inyi, China was inauurated and at

the same time four updated versions of the excavators

were launched, n addition, the product rane was

extended with one excavator.

Through both acquisitions and organic growth, the Volvo Group has

created a good position from which to develop fur ther in the dynamic

and fast-growing markets in Asia. With increased wealth and the asso-

ciated needs for transport and with substantia l investments in infra-

structure, the region is of large and growing importance to the Group.

deVelopmenT by ConTinenT

S gWg MPC

gB gP 2011

2424

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 29/166

Growth plans or DND

hrouh D rucks, the Volvo group has a joint venture

for trucks toether with Donfen of China. fact

unknown to many. he joint venture, DD, manufactures

heavy-duty D trucks in a factory in Hanzhou in Southern

China. DD was included in the acquistion of D rucks

in 2007 and ave the group access to domestic production

in China.

number of uropean manufacturers are tryin to et

into China, and some have shares in domestic companies

producin Chinese brands, but the Volvo group is the

only Western manufacturer makin trucks under its own

brand, D, in the country.

China is the world’s larest truck market with reistra-tions of 899,000 heavy-duty trucks in 2011. DD had a

volume of 900 trucks in 2011, and the Volvo group is

toether with its joint venture partner examinin different

possibilities to expand the cooperation in order to row

the sales volumes within the DD framework. n addition

to the D trucks bein manufactured by DD, the group

also sells some 1,000 Volvo trucks annually. hese trucks

are built in urope and shipped to China. With those

volumes, Volvo has a stron position in the uropean

sement of the market.

New Condor

Durin the year, D rucks

launched its new medium-duty

truck Condor, which had under-

one a full model chane. he

new trucks have a new cab

desin that conveys the impres-

sion of a unied family identity with the Quon heavy-duty

truck series. hey also feature various advanced techno-

loies accumulated on the company’s heavy-duty trucks

to deliver outstandin fuel economy, improved environ-

mental and aerodynamic performance and safety.

Technology Center in Jinan

part of the increased focus on rowth markets is the

development of products aimed par ticularly at those mar-

kets. Volvo C’s new technoloy center in Jinan, China is

part of these efforts and covers both the Volvo and the

SDg brand. Jinan is the capital of Shandon province

where inon has its manufacturin. he center entails

an investment of SK 300 M, and when fully complete in

2013 it will have 200 employees and cover an area of

50,000 square meters.

Market development, heavy-duty trucks, Japan

housands

1110090807

2525193543

25

Market development, construction equipment, China

housands

1110090807

399371230251203

399

Volvo Group in Asia

• Net sales: SK 73,586 M (65,487)

• Share o Group sales: 24%

• Number o employees: 19,924

• Share o Group employees: 20%

• Largest markets: China, Japan, ndia and South Korea.

Volvo CE and SDLG had

a combined market share of

12% in China

New company or electric and hybrid drivelines

in China

n pril 2011, Volvo Bus and SC Motors of China

areed to form a new joint venture company in China for

driveline systems for electric and hybrid buses. he new

company is 60% owned by SC and 40% owned by Volvo.

Volvo invests C 40 million and SC C 60 million

in the new company, Shanhai green Bus Drive System

Co, based in Shanhai. he new company will industria lize

SC Motors and Volvo Buses research and development

projects within electric and hybrid drivelines for buses.

Since the beinnin of the 21st century, Volvo and SC

toether operate Sunwin Bus, which is one of the larest

city bus manufacturers in China.

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 30/166

gB gP 2011

Exciting development in VECV

he Volvo group’s joint venture company V Commercial

Vehicles (VCV) comprises the entire icher Motors

truck and bus operations and the Volvo group’s ndian

sales operations in the truck sement as well as the serv -

ice operations for trucks and buses. he joint venture was

formed in 2008.

he ndian market for heavy-duty trucks rew by 12% to

237,000 trucks in 2011 compared to 212,000 vehicles in

2010. he market for liht and medium-duty trucks rew by

19% to 103,000 vehicles (87,000).

With 11% of the total ndian market for commercial

vehicles, i.e. heavy-duty, medium-duty and liht-duty trucks

as well as buses, icher is ndia’s third larest manufacturer

of commercial vehicles. he position is especially stron in

the liht and medium-duty sement in which icher durin

2011 had a market share of 30.5% (30.5). n heavy-duty

trucks the market share is developin in the riht direction,

althouh from low levels, since icher durin 2011 launched

its, new heavy-duty truck proram based on the coopera-

tion in VCV. Durin 2011, icher had 3.1% of the market in

the heavy-duty sement compared to 2.0% the yearbefore. he ambition is to row within heavy-duty trucks in

the comin years.

India to become center or new

medium-duty engine

VCV’s facility in Pithampur is home to a rapid expansion.

Part of the new construction takin place is the SK 480 M

investment in the production of the Volvo

group’s new lobal medium-duty enine.

he investment ives the Volvo group a complete

facility in ndia for processin and assemblin the new

medium-duty enine, which will be introduced in the

group’s trucks and buses worldwide in the next few

years.

hrouh this investment, it will be possible for the

Volvo group to locate most of its production of medium-

duty enines to VCV’s plant in Pithampur. VCV has an

established supplier base in ndia and efcient purchas-

in channels and already today, VCV produces about

40,000 enines per year in the existin plant. he group

will now have an enine platform that combines the latest

in Japanese technoloy with ndia’s hihly competitive

production cost. he investment in Pithampur will result

in an annual production capacity of an additional 85,000

new medium duty base enines.

t the same time, the Volvo group will invest an addi-

tional SK 460 M in the group’s production plants for

enines in eo, Japan and Venissieux, France. hrouh

this investment, the group will, amon other thins, havean annual nal assembly capacity for 30,000 medium-duty

base enines for the uropean market.

Development of the new medium-duty enine has

been led by Volvo Powertrain in eo and the enine has

been desined to meet current and future exhaust require-

ments in urope, the S and Japan.

n addition to production of the base enine itself, the

FoCus

D

The Indian market is in an exciting growth phase withgrowing prosperity and increasing investments in infrastructure.

2626

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 31/166

Volvo Group sales in India, SK bn

00 11

6.0

0.3

India

• Area: 3,288,000 km2

• Population: 1,171 million (2010)

• Capital: ew Delhi with 242,000 inhabitants (stimate 2010.ew Delhi is a part of the Delhi metropolitan area)

• Other big cities: Mumbai (Bombay 13.8 million), Delhi (12.6), Banalore (5.4),Kolkata (Calcutta 5.1)

• GDP per capita: SD 1,176 (2010)

Volvo Group in India

• Number o employees: 3,919

• Production: Pithampur (icher – enines, earboxes,axles, trucks, bus chassis) and Banalore (Volvo –assembly of trucks, buses and construction equipment)

• Net sales: SK 6,007 M, 2% of group sales

• hird larest commercial vehicle manufacturer in ndiathrouh the VCV joint venture toether with icherMotor imited

facility in Pithampur will also conduct nal assembly ofenines for ndia and all of Volvo group’s lobal markets

with uro and uro V emission requirements. Production

and nal assembly of the enines for the Japanese market

will be in eo, while nal assembly of the enines for the

uropean market will take place in Venissieux.

By atherin base enine production in ndia, it will be

possible for us to meet the group’s need for cost-ef-

cient medium-duty enines in sia, while also contributin

to an increase in our competitiveness in the medium-duty

sement in other markets.

Production of the group’s new medium-duty enine

proram started in eo in 2010 for the Japanese and

.S. markets. he production of medium-duty enines inPithampur starts in 2012.

Excavator production in India

n ovember, the rst excavator rolled out of Volvo C’s

new excavator plant in Banalore, ndia. he production of

excavators will increase substantially durin 2012. he

plant will continue to manufacture road machinery. he

new excavator line is part of a SK 144 M investment to

uprade the plant. he local production of excavators will

mean reater machine availability for ndian customers, as

well as shorten delivery lead times and respond to cus-

tomer requirements more quickly.

Full speed ahead or Volvo Buses

n the eve of its 10th year in ndia, Volvo Buses announced

SK 500 M investment plans for the next ve years. n the

rst phase the company will expand its current industrial

establishment and introduce a rane of new products.

ver the last decade the company has emered as a

leader in its class with a dominant market presence and

in the process re-dened how people see buses. he

ndian market has witnessed a paradim shift in the bus

business. While earlier, coaches built on truck chassiswere the norm of the day, the entry of Volvo Buses intro-

duced the concept of a true-bus chassis with rear enines.

Volvo Buses also brouht in the idea of B, efcient,

bus-based public transport systems.

Mr kash Passey, head of Volvo Buses in ndia, said,

“he need for buses as sustainable transport solutions is

hih in ndia and we aim to row multifold in the years to

come. From 1,000 buses to 5,000. From 1,000 people to

5,000 people and be a billion dollar company.”

he ambition is to be there by 2015. By this time Volvo

aims to export 20–25% of its volumes not only in South

sia but to markets beyond.

Volvo Buses today has over 70% market share in the

luxury inter-city coach sement and over 50% market

share in the low oor air-conditioned city bus sement

respectively.

owards the end of the year, Volvo Buses launched

three new city buses and coaches in ndia and thus

increased the product rane to encompass ten buses.

11%of the total Indian market

7/29/2019 MBA VTU Project on VOLVO Group in India

http://slidepdf.com/reader/full/mba-vtu-project-on-volvo-group-in-india 32/166

oVerall Challenges

F SP DS

In 2012, the Volvo Group celebrates 85 years. In 1927, the rst series-produced Volvo car rolled

off the production line at the Gothenburg plant. For 85 years, Volvo has developed pioneering

products and serv ices.

Much has happened since 1927. Volvo has developed from

a small local industry to one of the world’s larest manufac-

turers of trucks, buses and construction equipment with

more than 100,000 employees, production facilities in 20

countries and sales in more than 190 countries.

t is crucial to keep pace in a rapidly chanin world.