MBA Strategy: Session One Michaelmas...

286

MBA Strategy: Session One Michaelmas 2006 Introduction to Strategy Christopher McKenna Thomas Powell

Transcript of MBA Strategy: Session One Michaelmas...

MBAStrategy: Session One

Michaelmas 2006

Introduction to Strategy

Christopher McKennaThomas Powell

Strategic Management

Course Objectives

The ability to apply strategy theory and frameworks to the analysis and diagnosis of strategy problems

Understanding how organizations align internal resources and capabilities with external conditions to produce business and corporate strategies

The capacity to formulate and defend arguments in support of strategy proposals, using theory and evidence

Course Structure

1. Introduction to Strategy

2. Competitive Advantage

3. Industry Strategy

4. Strategy and Change

5. Diversification

6. Global Strategy

7. Managing the Multibusiness Company

8. Strategy Process

Text Books and Readings

Main:

Grant R. (2005), Contemporary Strategy Analysis, Blackwell (5th Edition).

Supplements:

Johnson G, Scholes K and Whittington (2004), Exploring Corporate Strategy, Prentice Hall (7th Edition).

Besanko D, Dranove D, Shanley M. and Schaeffer S. (2004) Economics of Strategy, Wiley (3rd Edition)

Also: Selected classic articles

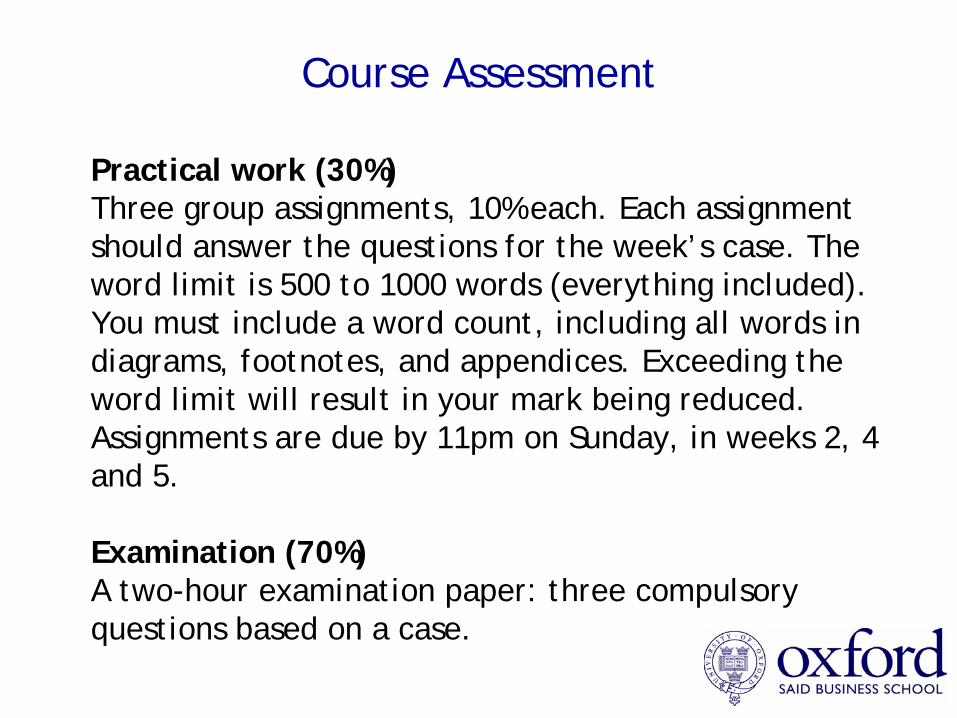

Course Assessment

Practical work (30%)Three group assignments, 10% each. Each assignment should answer the questions for the week’s case. The word limit is 500 to 1000 words (everything included). You must include a word count, including all words in diagrams, footnotes, and appendices. Exceeding the word limit will result in your mark being reduced. Assignments are due by 11pm on Sunday, in weeks 2, 4 and 5.

Examination (70%)A two-hour examination paper: three compulsory questions based on a case.

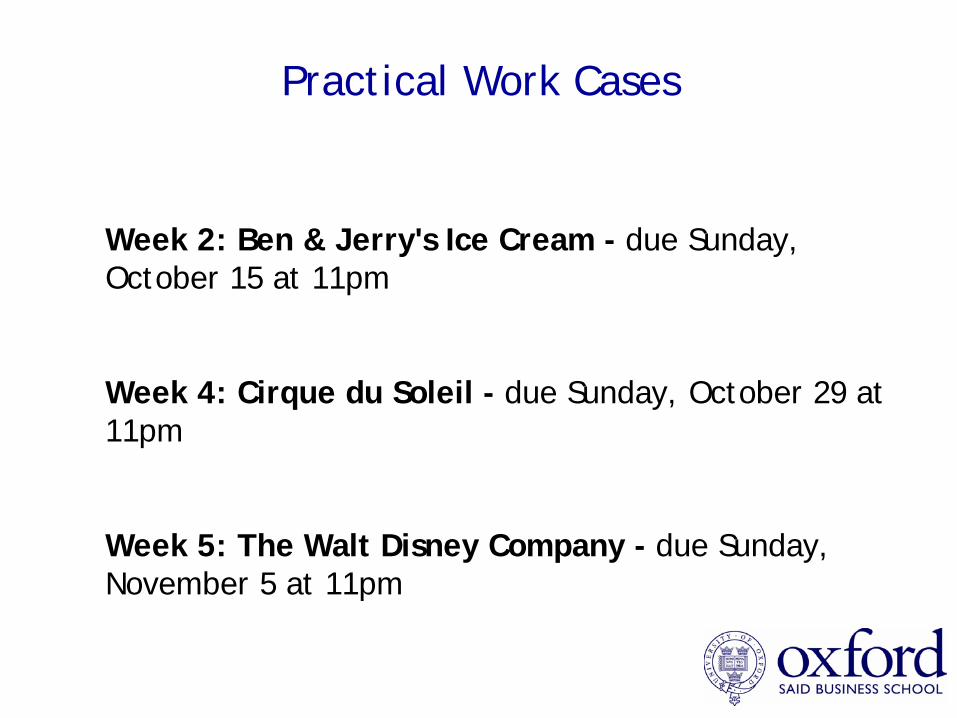

Week 2: Ben & Jerry's Ice Cream - due Sunday, October 15 at 11pm

Week 4: Cirque du Soleil - due Sunday, October 29 at 11pm

Week 5: The Walt Disney Company - due Sunday, November 5 at 11pm

Practical Work Cases

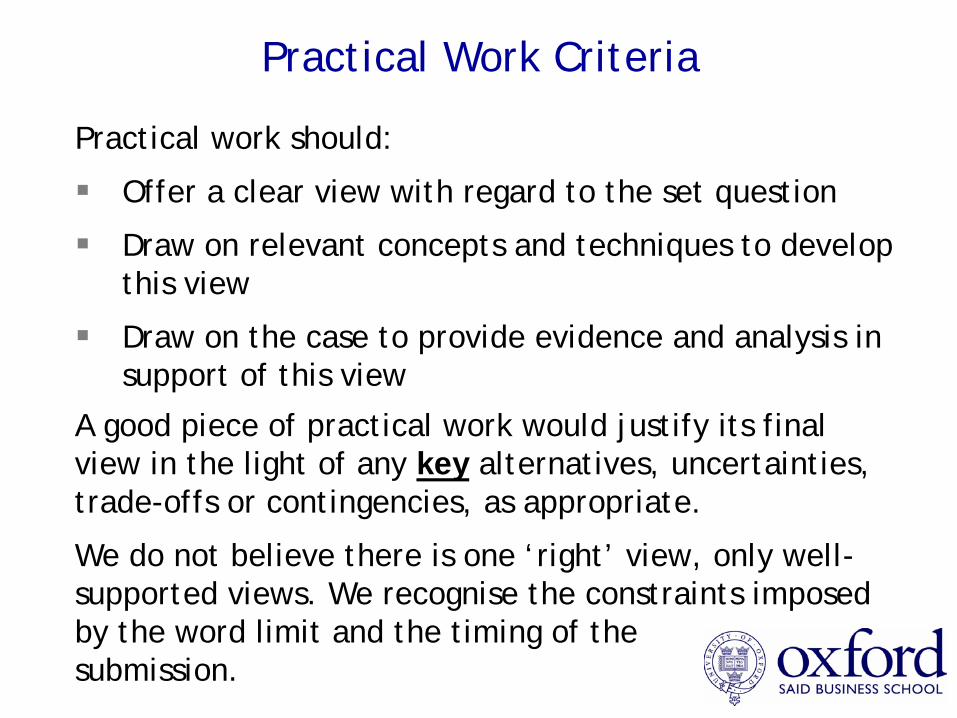

Practical Work Criteria

Practical work should:

Offer a clear view with regard to the set question

Draw on relevant concepts and techniques to develop this view

Draw on the case to provide evidence and analysis in support of this view

A good piece of practical work would justify its final view in the light of any key alternatives, uncertainties, trade-offs or contingencies, as appropriate.

We do not believe there is one ‘right’ view, only well- supported views. We recognise the constraints imposed by the word limit and the timing of thesubmission.

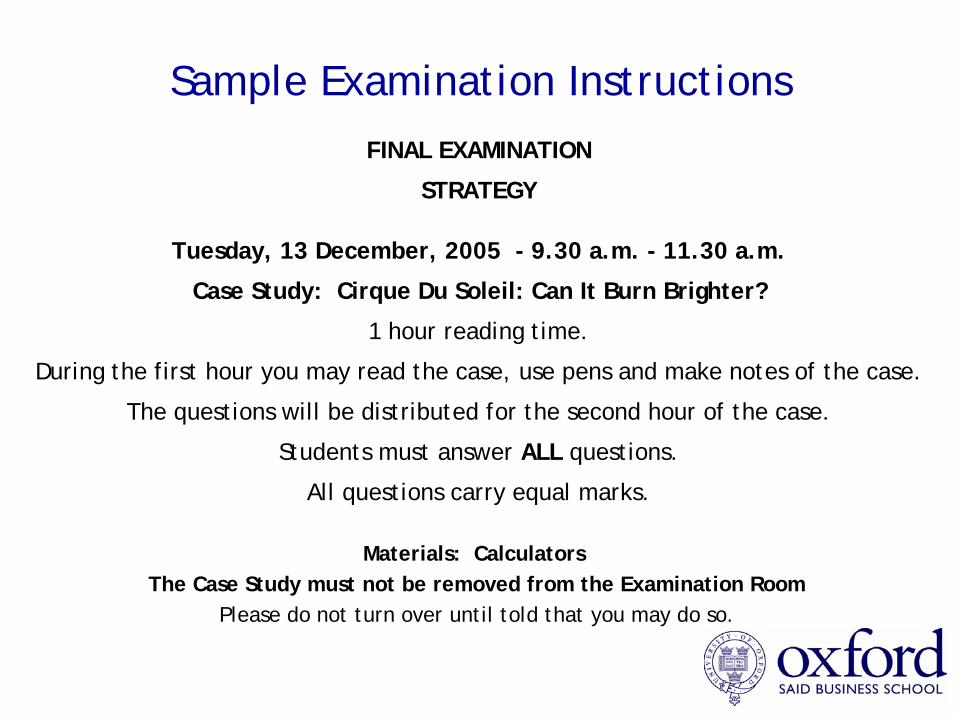

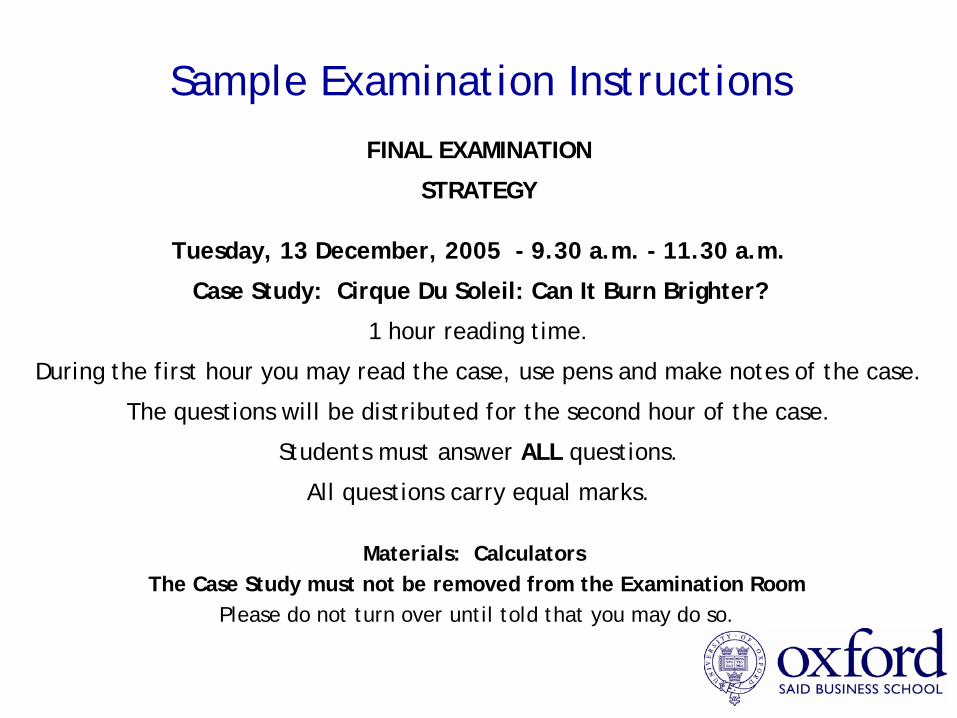

FINAL EXAMINATION

STRATEGY

Tuesday, 13 December, 2005 - 9.30 a.m. - 11.30 a.m.

Case Study: Cirque Du Soleil: Can It Burn Brighter?

1 hour reading time.

During the first hour you may read the case, use pens and make notes of the case.

The questions will be distributed for the second hour of the case.

Students must answer ALL questions.

All questions carry equal marks.

Materials: CalculatorsThe Case Study must not be removed from the Examination Room

Please do not turn over until told that you may do so.

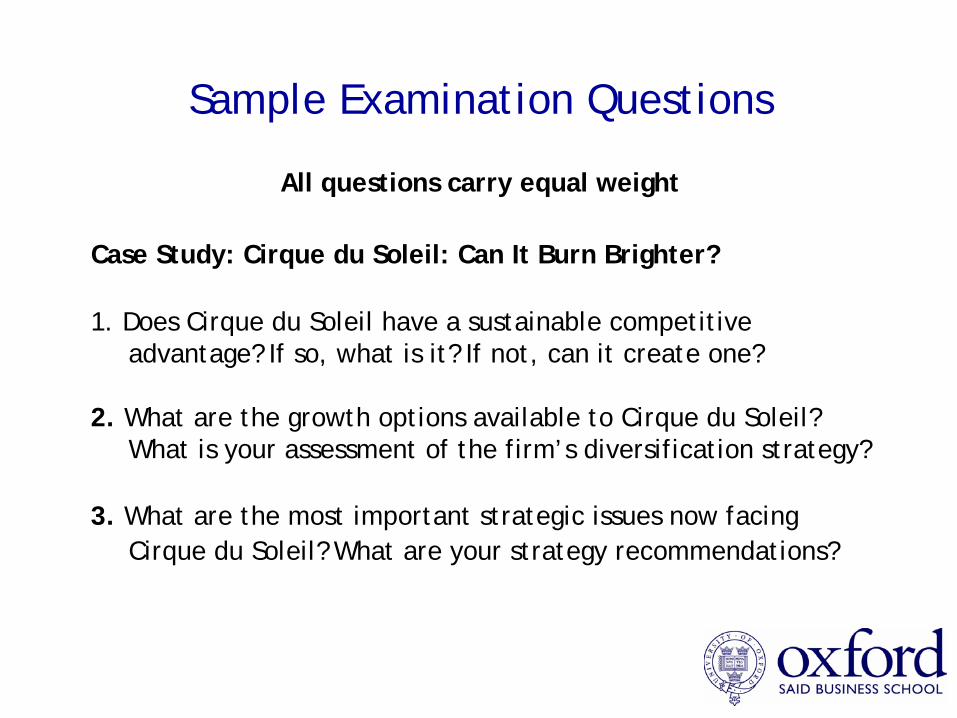

Sample Examination Instructions

All questions carry equal weight

Case Study: Cirque du Soleil: Can It Burn Brighter?

1. Does Cirque du Soleil have a sustainable competitive advantage? If so, what is it? If not, can it create one?

2. What are the growth options available to Cirque du Soleil? What is your assessment of the firm’s diversification strategy?

3. What are the most important strategic issues now facing Cirque du Soleil? What are your strategy recommendations?

Sample Examination Questions

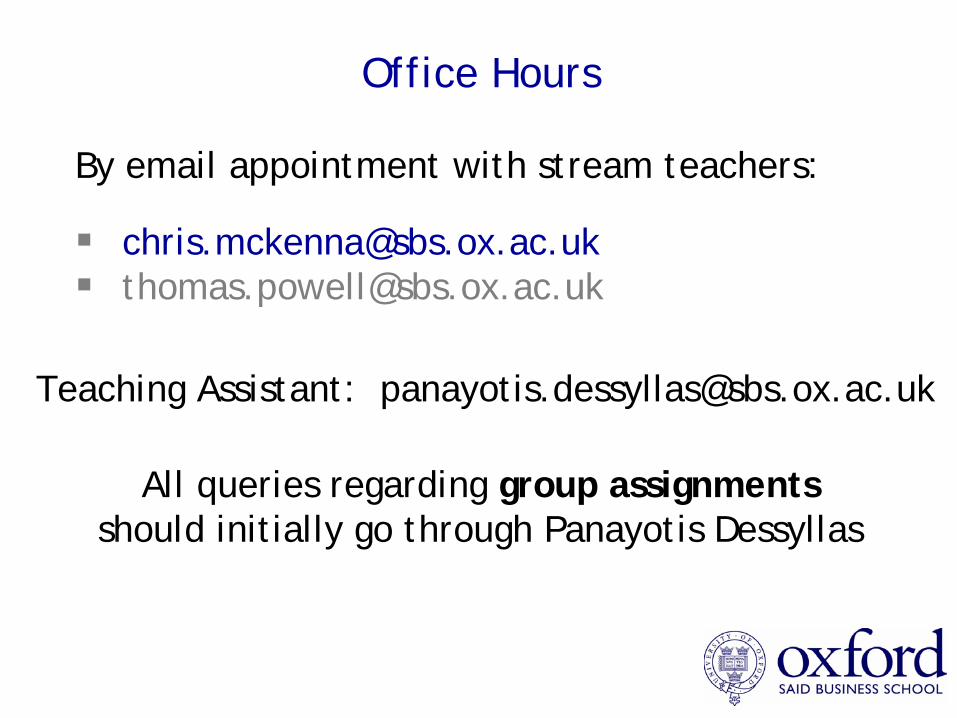

Office Hours

By email appointment with stream teachers:

[email protected]@sbs.ox.ac.uk

All queries regarding group assignments should initially go through Panayotis Dessyllas

Teaching Assistant: [email protected]

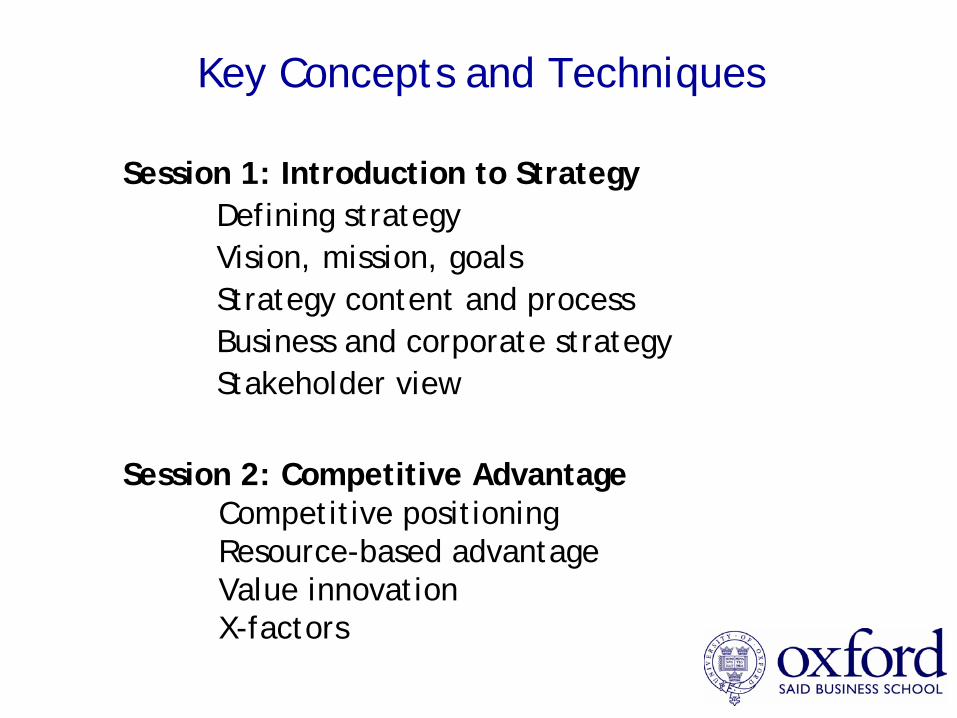

Key Concepts and Techniques

Session 1: Introduction to Strategy Defining strategyVision, mission, goalsStrategy content and process Business and corporate strategyStakeholder view

Session 2: Competitive AdvantageCompetitive positioningResource-based advantageValue innovationX-factors

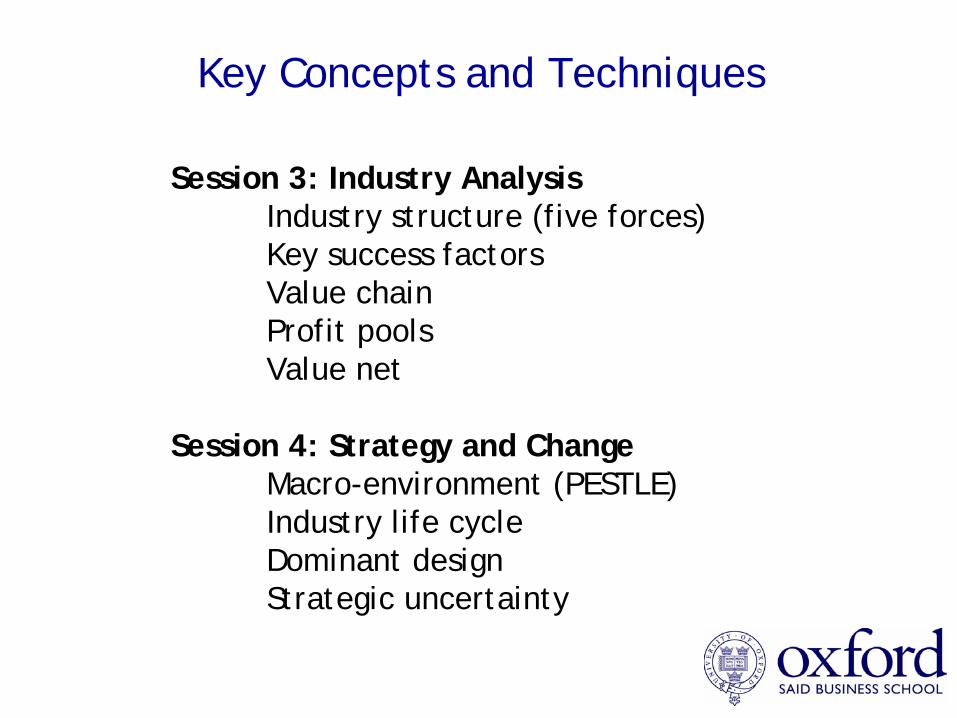

Key Concepts and Techniques

Session 3: Industry AnalysisIndustry structure (five forces)Key success factorsValue chainProfit poolsValue net

Session 4: Strategy and ChangeMacro-environment (PESTLE)Industry life cycleDominant designStrategic uncertainty

Key Concepts and Techniques

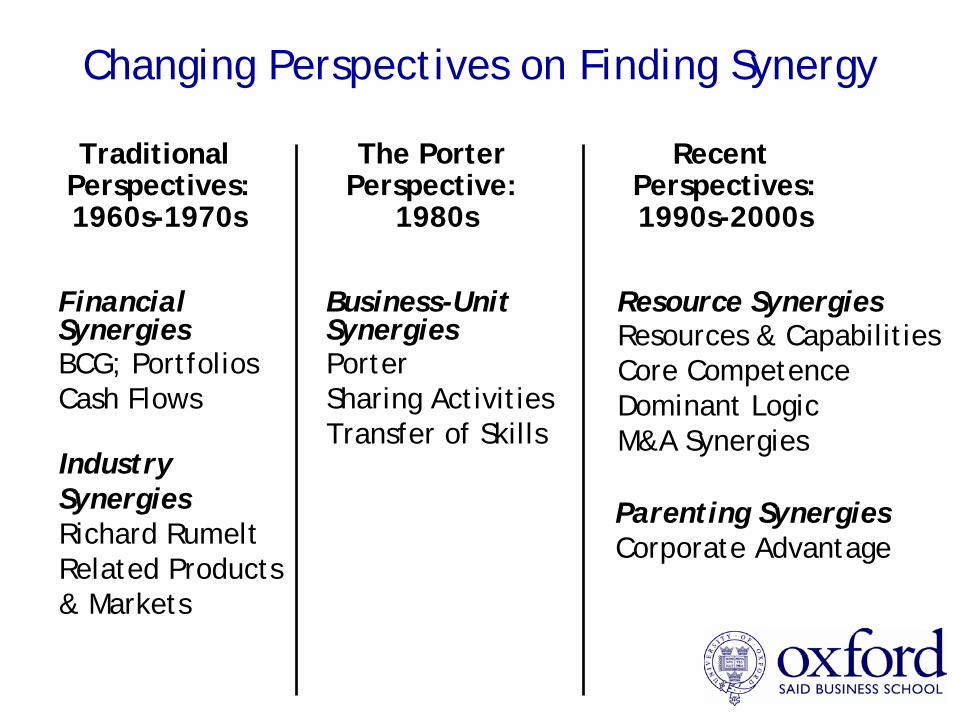

Session 5: DiversificationHierarchy of growthPortfolio modelsSynergyRelated diversificationCore competence

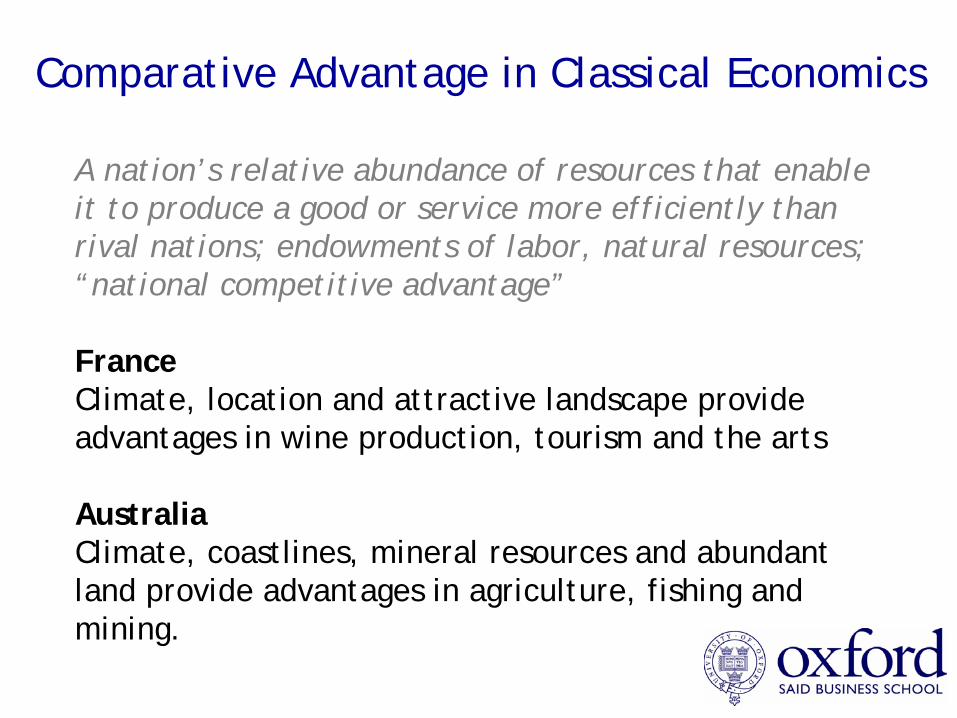

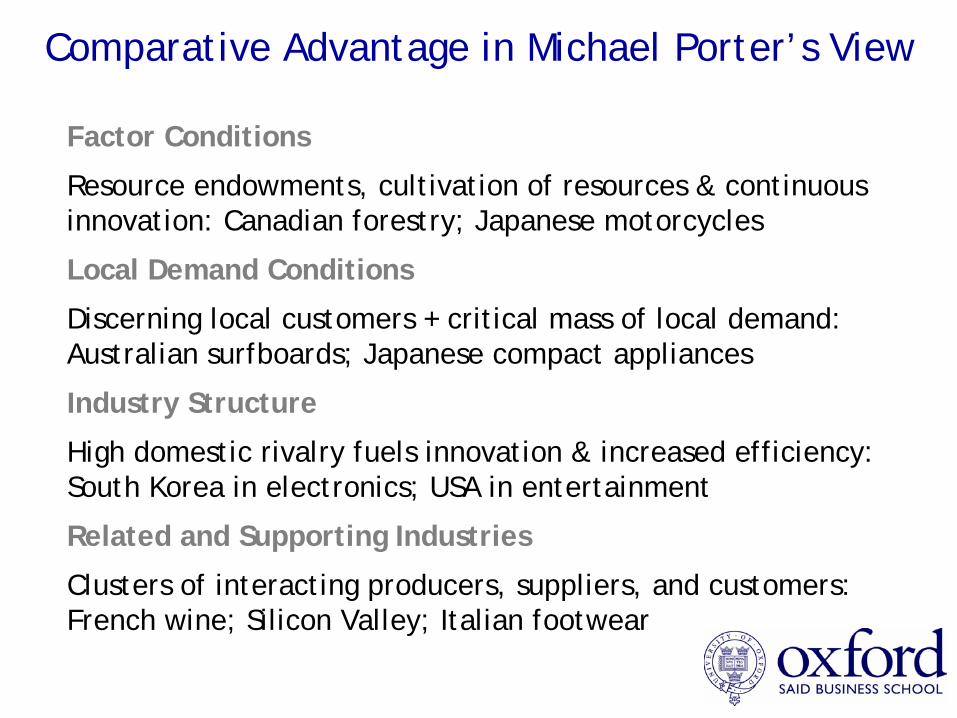

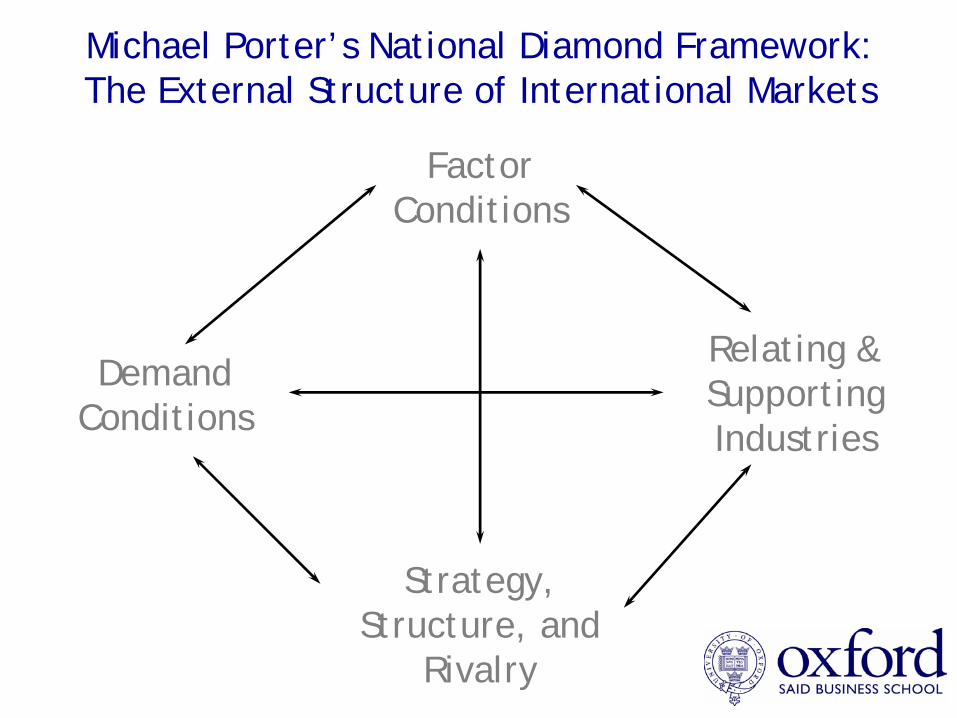

Session 6: Global StrategyModes of international expansionGlobal productsDiamond of national advantage

Key Concepts and Techniques

Session 7: Managing the Multibusiness CompanyDominant logic Corporate parentingMerger & acquisition integration

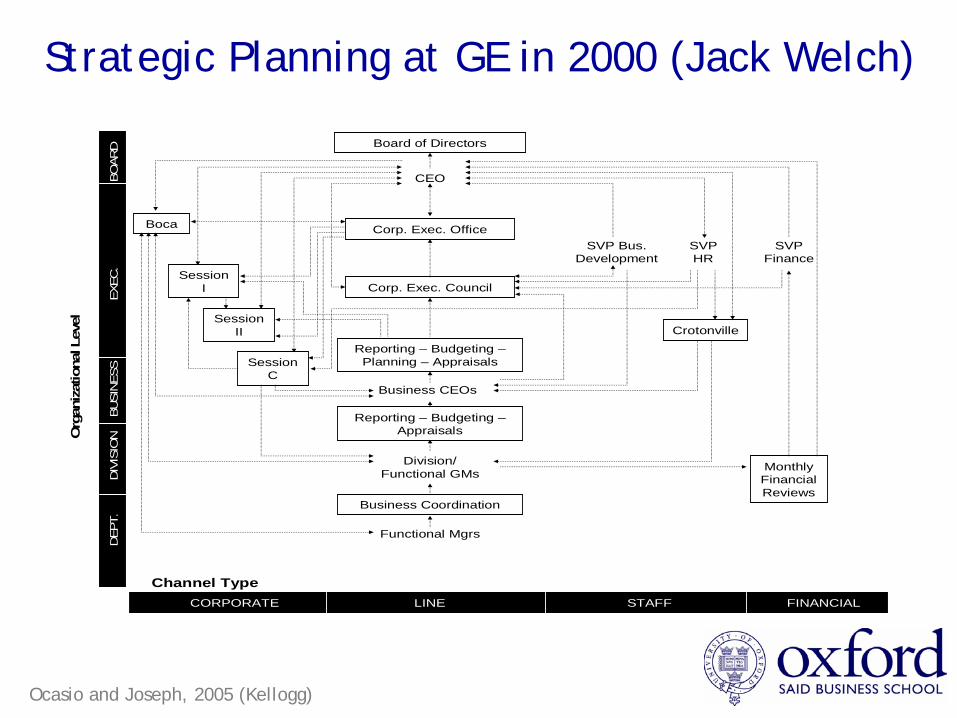

Session 8: Strategy ProcessStrategic planningEmergent strategyLogical incrementalism

SEIB

Strategy

Entrepreneurship

InternationalBusiness

STRATEGY, ENTREPRENEURSHIP & INTERNATIONAL BUSINESS (SEIB)

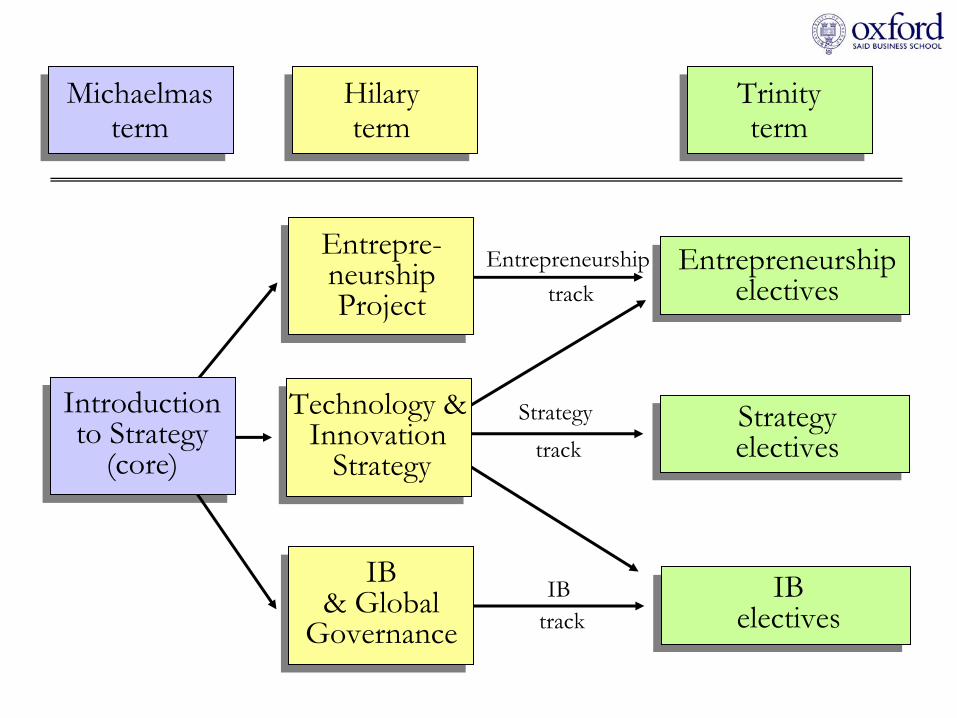

Michaelmasterm

Entrepreneurshipelectives

IBelectives

Strategyelectives

Technology & Innovation

Strategy

Strategy track

Entrepreneurship track

IB track

Introduction to Strategy

(core)

Hilaryterm

Trinityterm

Entrepre-neurshipProject

IB& Global

Governance

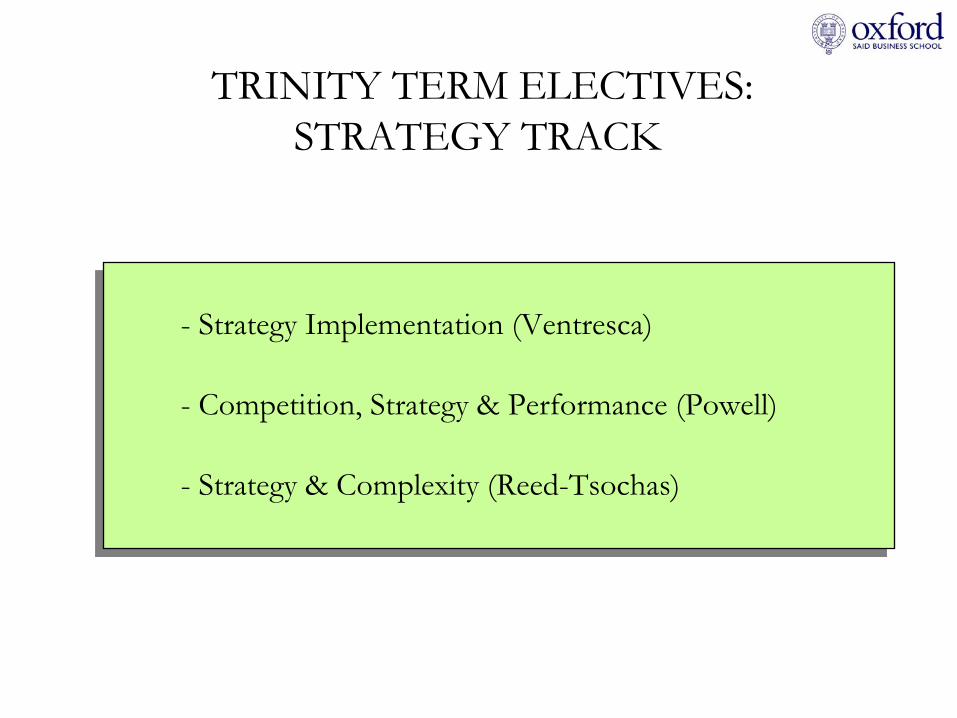

TRINITY TERM ELECTIVES:STRATEGY TRACK

- Strategy Implementation (Ventresca)

- Competition, Strategy & Performance (Powell)

- Strategy & Complexity (Reed-Tsochas)

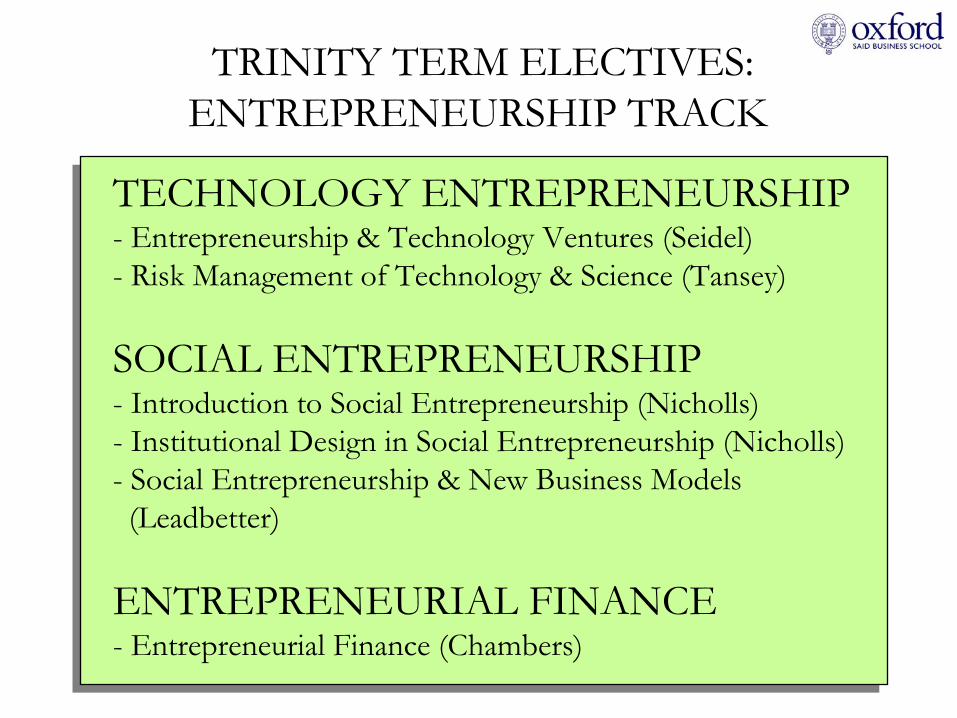

TRINITY TERM ELECTIVES:ENTREPRENEURSHIP TRACK

TECHNOLOGY ENTREPRENEURSHIP- Entrepreneurship & Technology Ventures (Seidel)- Risk Management of Technology & Science (Tansey)

SOCIAL ENTREPRENEURSHIP-

Introduction to Social Entrepreneurship (Nicholls)

- Institutional Design in Social Entrepreneurship (Nicholls)- Social Entrepreneurship & New Business Models (Leadbetter)

ENTREPRENEURIAL FINANCE-

Entrepreneurial Finance (Chambers)

TRINITY TERM ELECTIVES:INTERNATIONAL BUSINESS TRACK

-

Business in China (Thun)

-

Global Production in Emerging Markets(Brown, Sako, Thun)

- Corporate Responsibility (McBarnet)

-

Managing Business-State Relations and Political Risk (Brown)

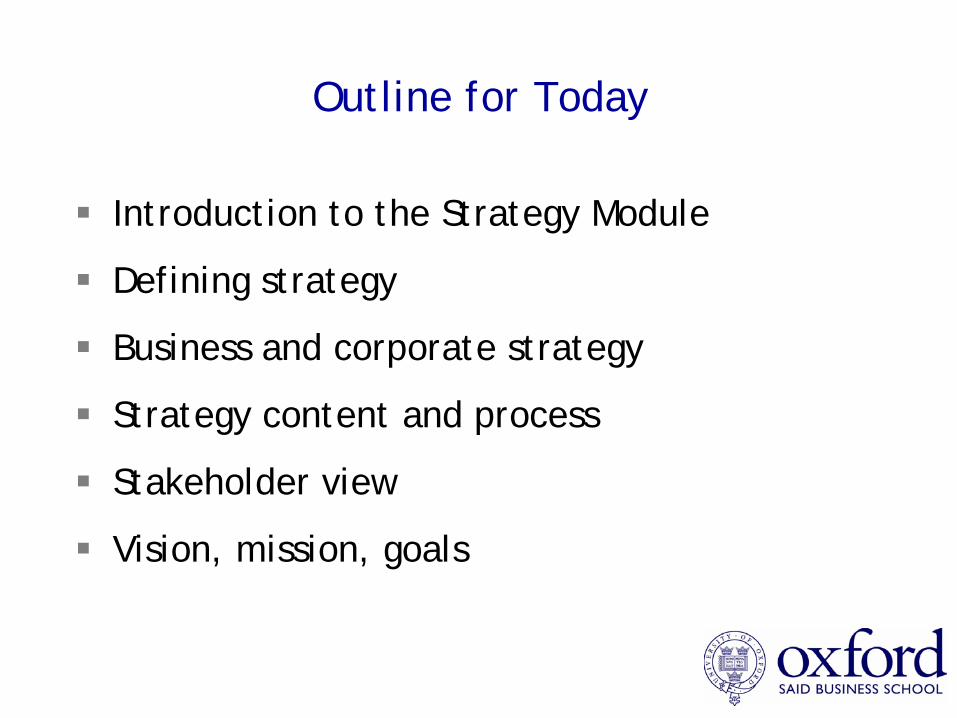

Outline for Today

Introduction to the Strategy Module

Defining strategy

Business and corporate strategy

Strategy content and process

Stakeholder view

Vision, mission, goals

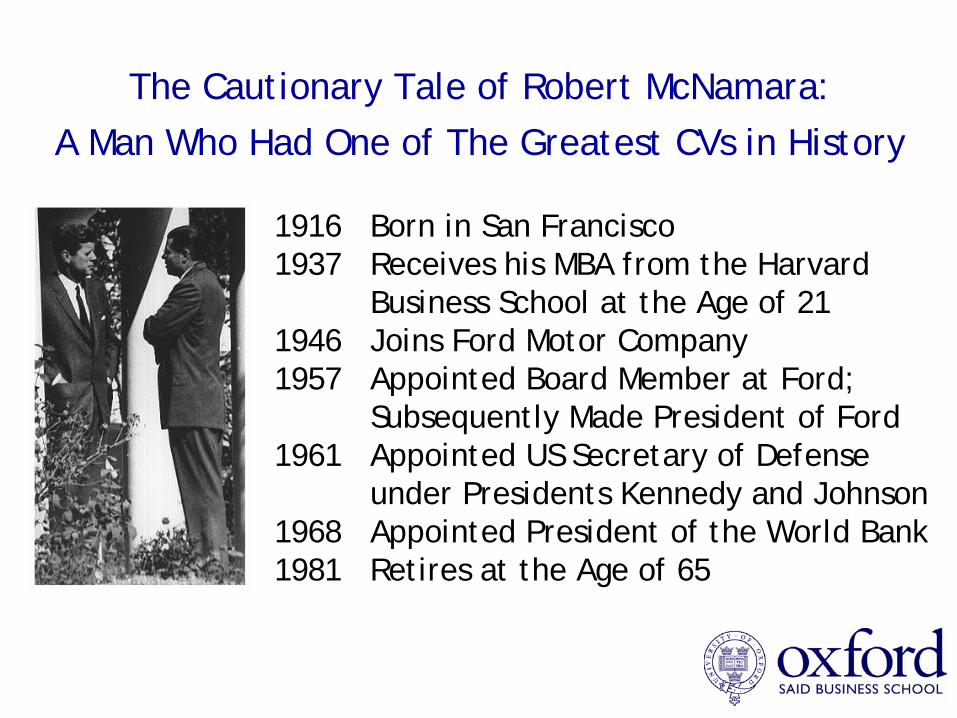

The Cautionary Tale of Robert McNamara: A Man Who Had One of The Greatest CVs in History

1916 Born in San Francisco1937 Receives his MBA from the Harvard

Business School at the Age of 211946 Joins Ford Motor Company1957 Appointed Board Member at Ford;

Subsequently Made President of Ford1961 Appointed US Secretary of Defense

under Presidents Kennedy and Johnson1968 Appointed President of the World Bank1981 Retires at the Age of 65

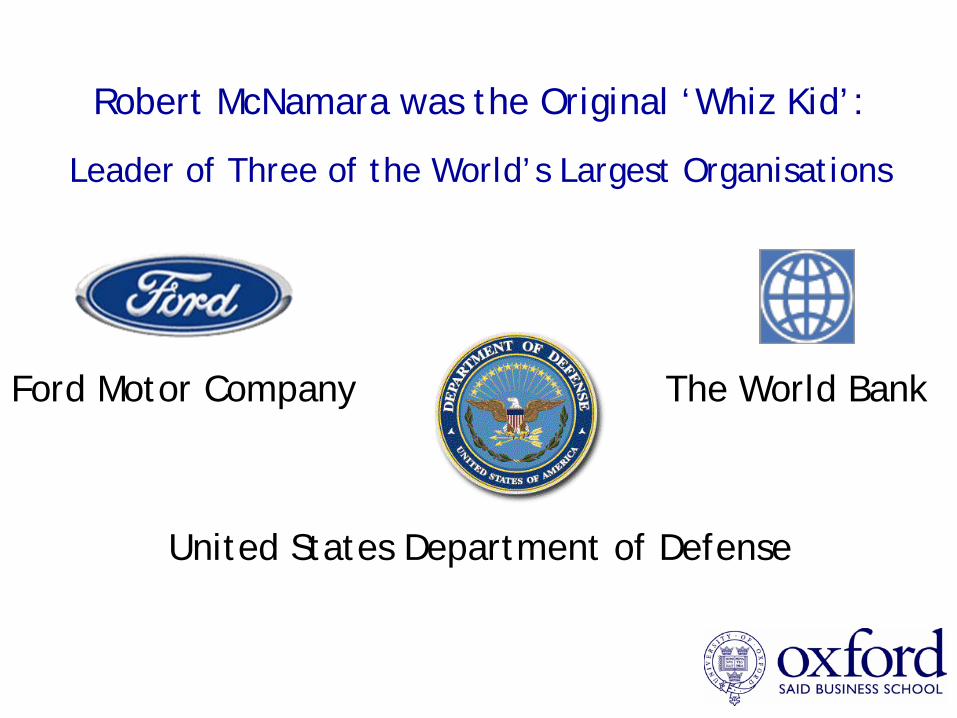

Robert McNamara was the Original ‘Whiz Kid’:

Leader of Three of the World’s Largest Organisations

Ford Motor Company The World Bank

United States Department of Defense

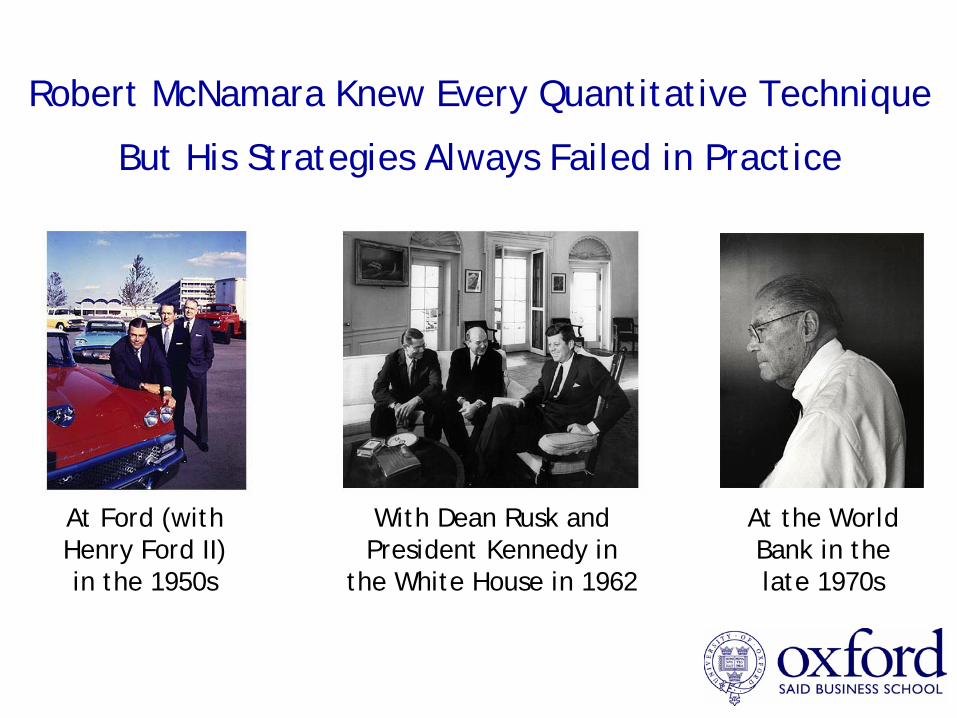

Robert McNamara Knew Every Quantitative Technique

But His Strategies Always Failed in Practice

At Ford (with Henry Ford II) in the 1950s

With Dean Rusk and President Kennedy in

the White House in 1962

At the World Bank in the late 1970s

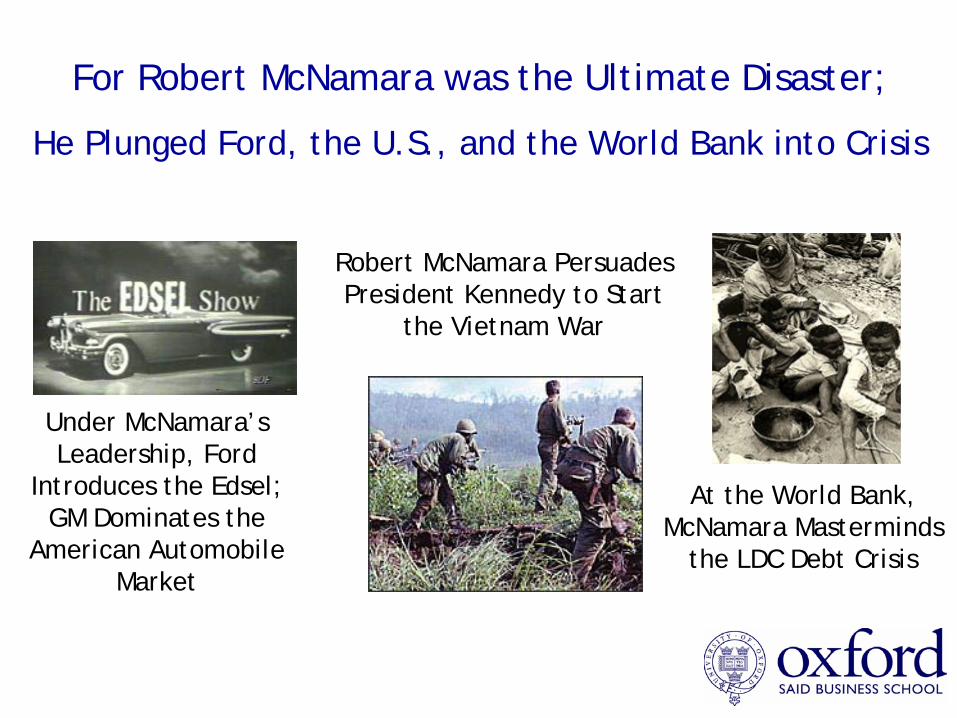

For Robert McNamara was the Ultimate Disaster;

He Plunged Ford, the U.S., and the World Bank into Crisis

Under McNamara’s Leadership, Ford

Introduces the Edsel;GM Dominates the

American Automobile Market

Robert McNamara Persuades President Kennedy to Start

the Vietnam War

At the World Bank,McNamara Masterminds

the LDC Debt Crisis

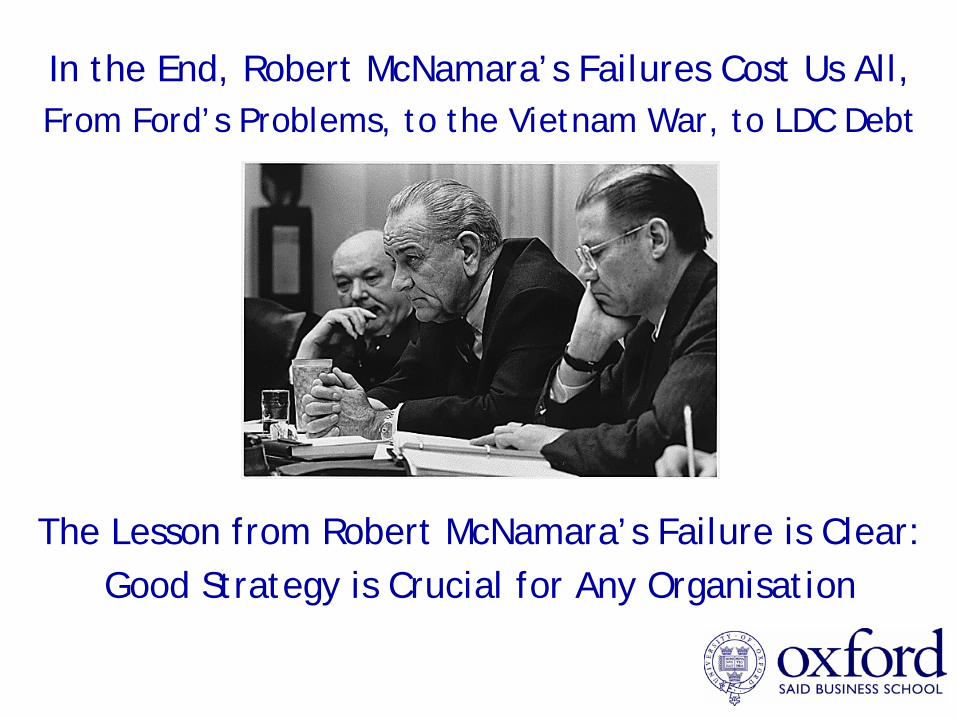

In the End, Robert McNamara’s Failures Cost Us All,From Ford’s Problems, to the Vietnam War, to LDC Debt

The Lesson from Robert McNamara’s Failure is Clear:Good Strategy is Crucial for Any Organisation

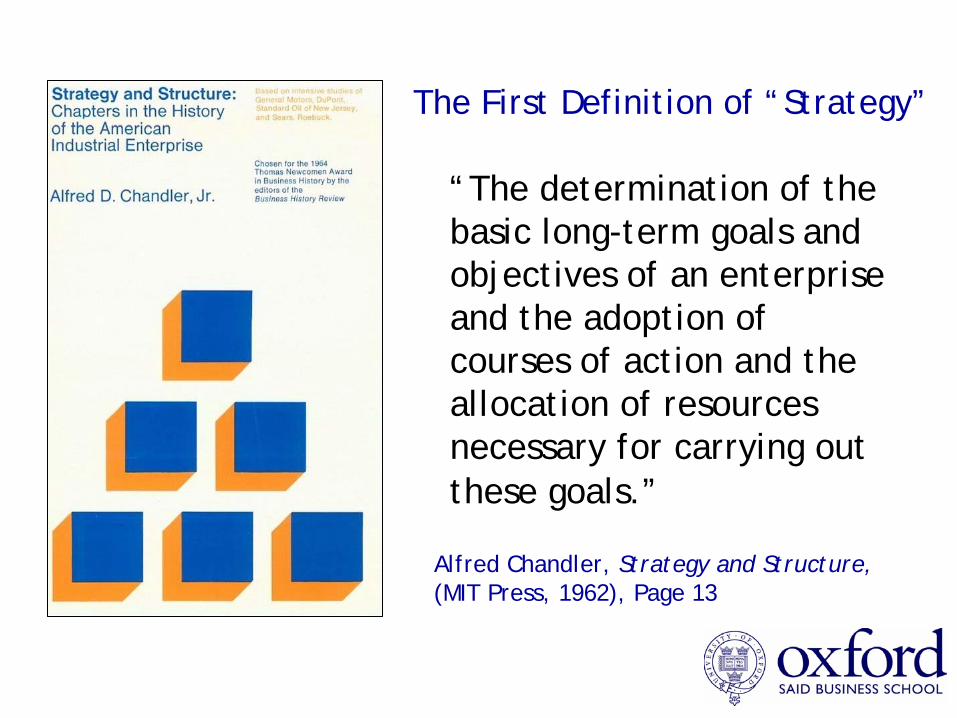

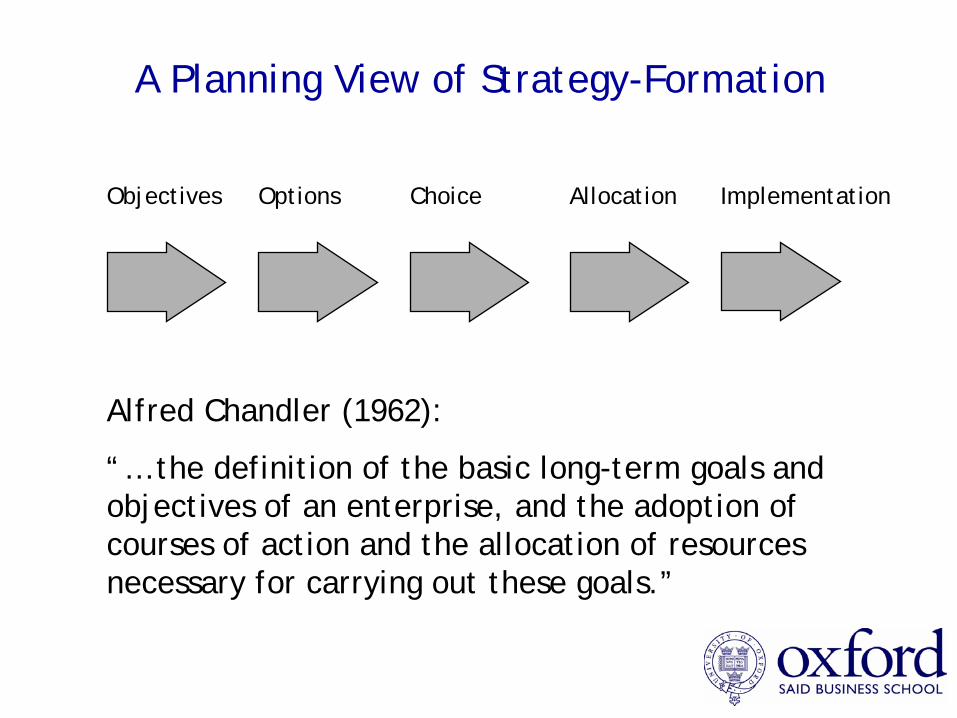

A Definition of “Strategy”

“The determination of the basic long-term goals and objectives of an enterprise and the adoption of courses of action and the allocation of resources necessary for carrying out these goals.”

Alfred Chandler, Strategy and Structure, (MIT Press, 1962), Page 13.

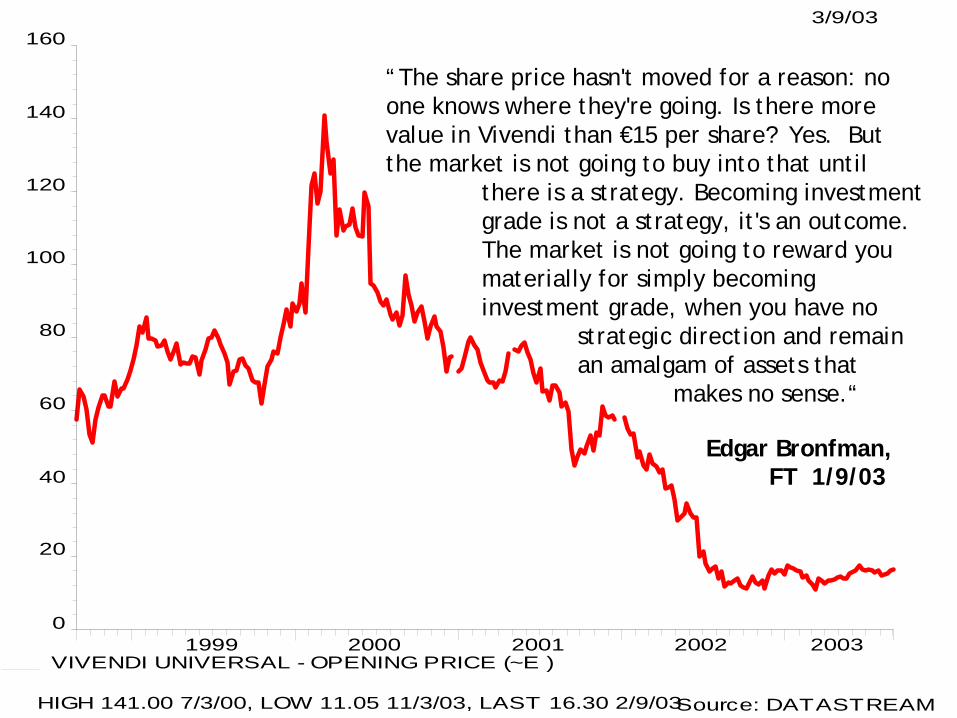

3/9/03

1999 2000 2001 2002 20030

20

40

60

80

100

120

140

160

VIVENDI UNIVERSAL - OPENING PRICE (~E )

HIGH 141.00 7/3/00, LOW 11.05 11/3/03, LAST 16.30 2/9/03Source: DATASTREAM

“The share price hasn't moved for a reason: no one knows where they're going. Is there more value in Vivendi than €15 per share? Yes. But the market is not going to buy into that until

there is a strategy. Becoming investment grade is not a strategy, it's an outcome. The market is not going to reward you materially for simply becoming investment grade, when you have no

strategic direction and remain an amalgam of assets that

makes no sense.“

Edgar Bronfman, FT 1/9/03

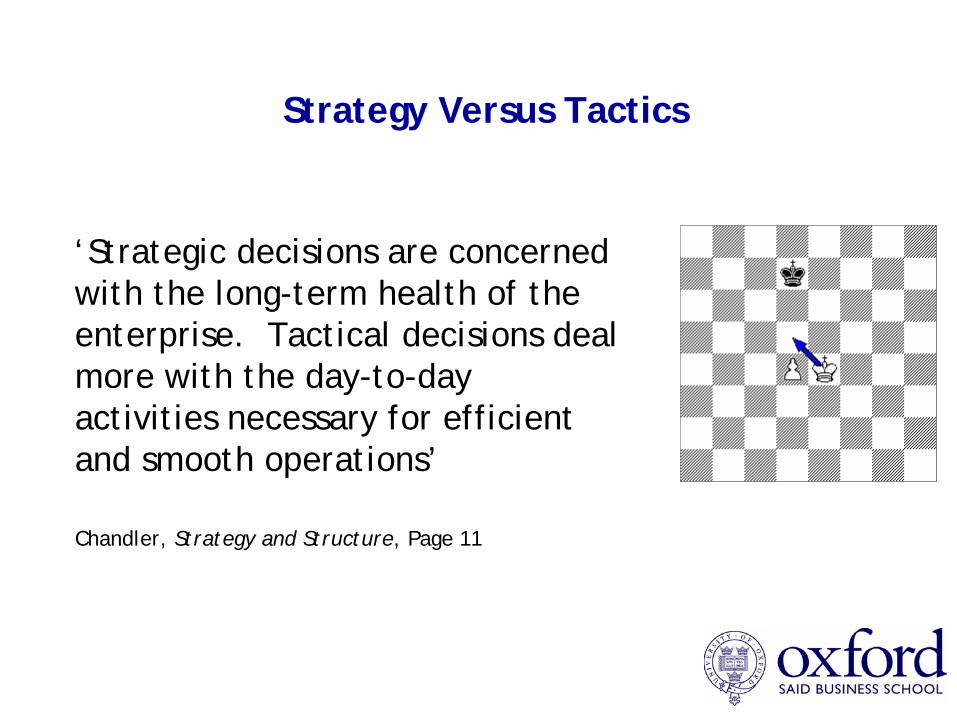

Strategy Versus Tactics

‘Strategic decisions are concerned with the long-term health of the enterprise. Tactical decisions deal more with the day-to-day activities necessary for efficient and smooth operations’

Chandler, Strategy and Structure, Page 11

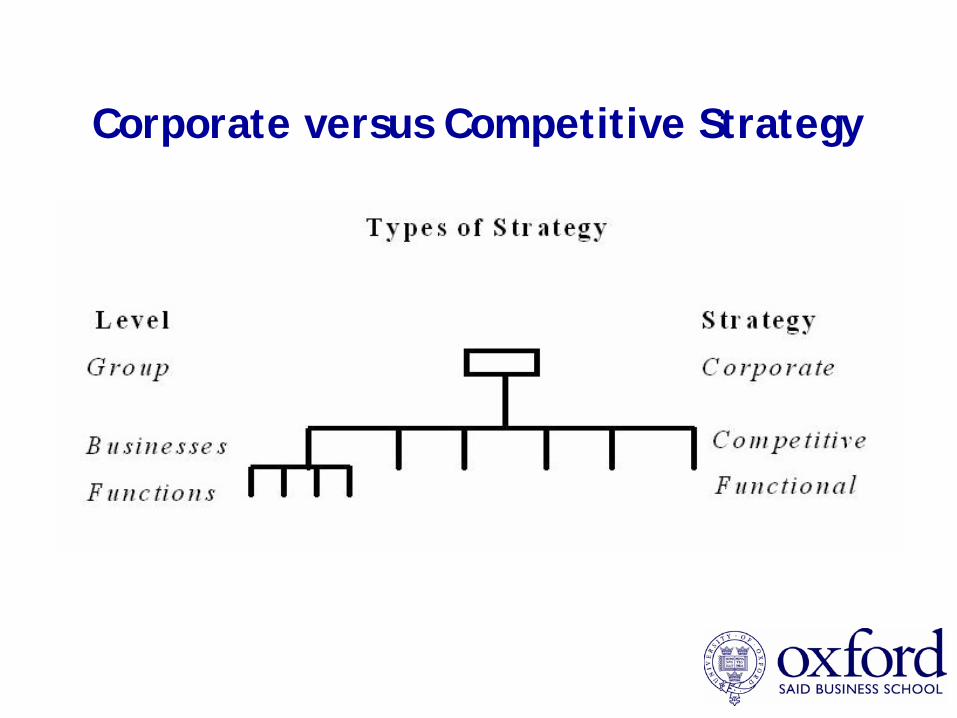

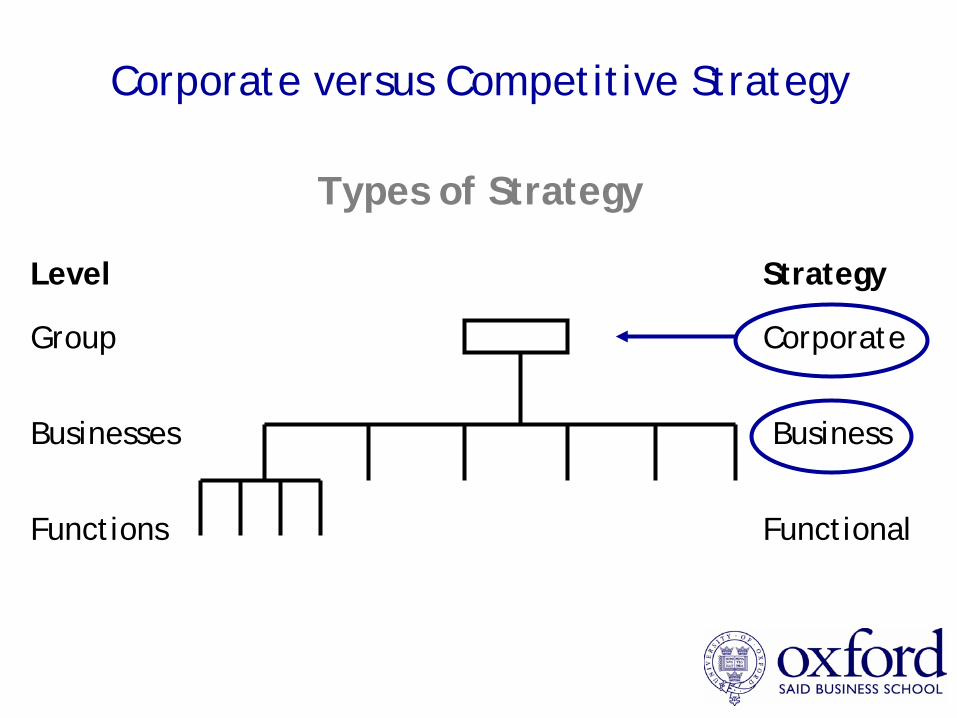

Corporate versus Competitive Strategy

Competitive and Corporate Strategy

Competitive (Business) Strategy• How should a business compete in its industry?

Corporate StrategyWhat businesses should be included in the corporate portfolio?How should these businesses relate to one another?How should these businesses relate to the corporate parent?

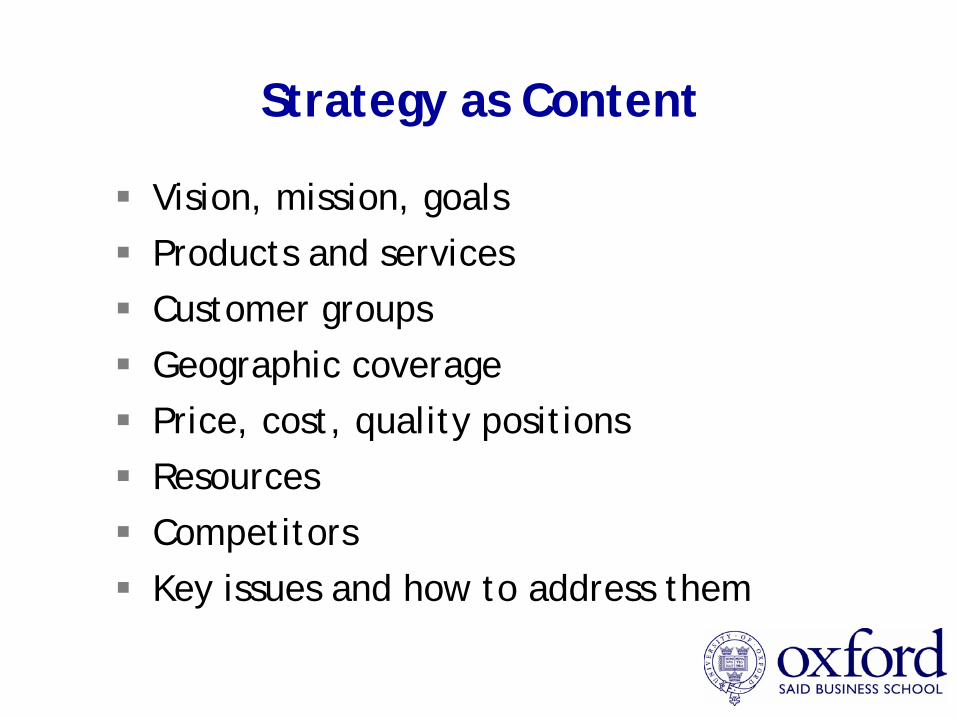

Strategy as Content

Vision, mission, goalsProducts and servicesCustomer groups Geographic coveragePrice, cost, quality positionsResourcesCompetitorsKey issues and how to address them

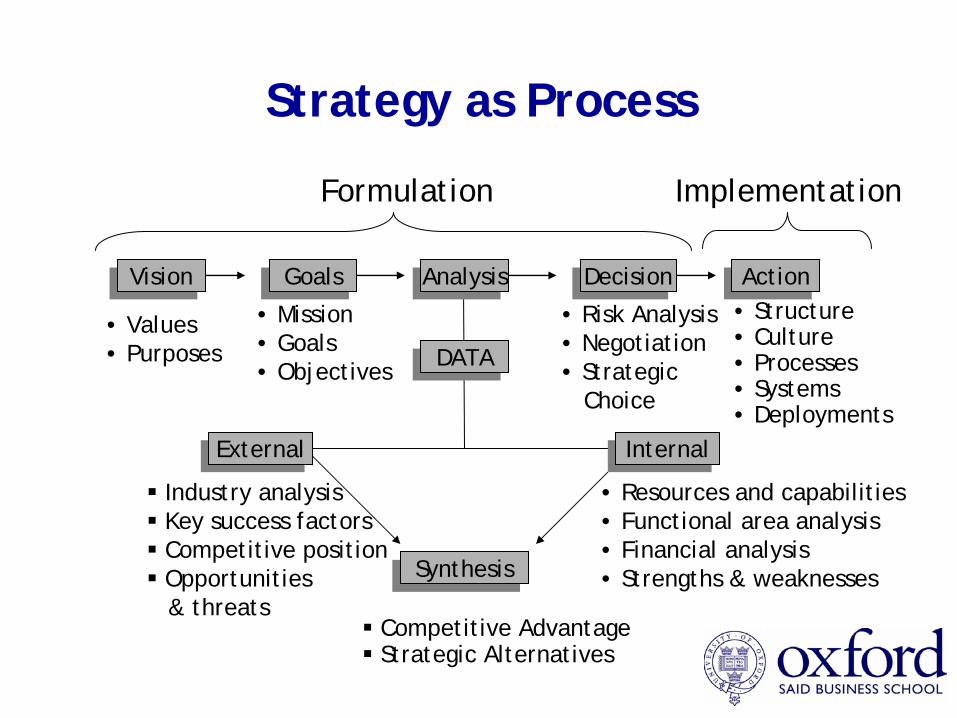

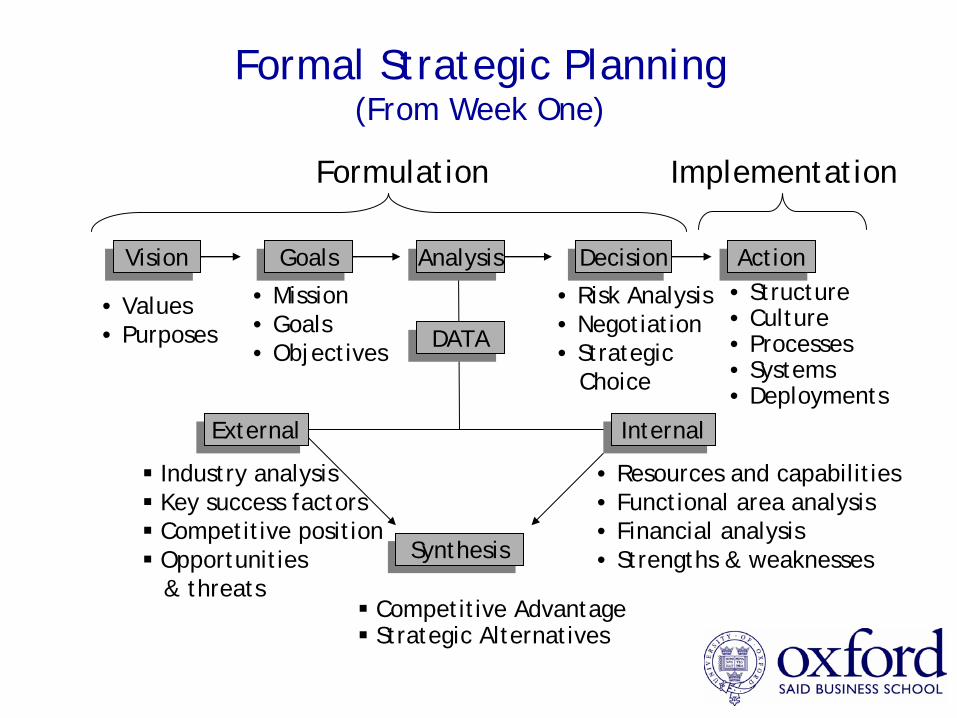

Strategy as Process

VisionVision GoalsGoals AnalysisAnalysis DecisionDecision ActionAction

ExternalExternal InternalInternal

SynthesisSynthesis

• Values• Purposes

• Mission• Goals• Objectives

Industry analysisKey success factorsCompetitive positionOpportunities & threats

• Resources and capabilities• Functional area analysis• Financial analysis• Strengths & weaknesses

• Risk Analysis• Negotiation• Strategic

Choice

• Structure• Culture• Processes• Systems• Deployments

Competitive AdvantageStrategic Alternatives

DATADATA

Formulation Implementation

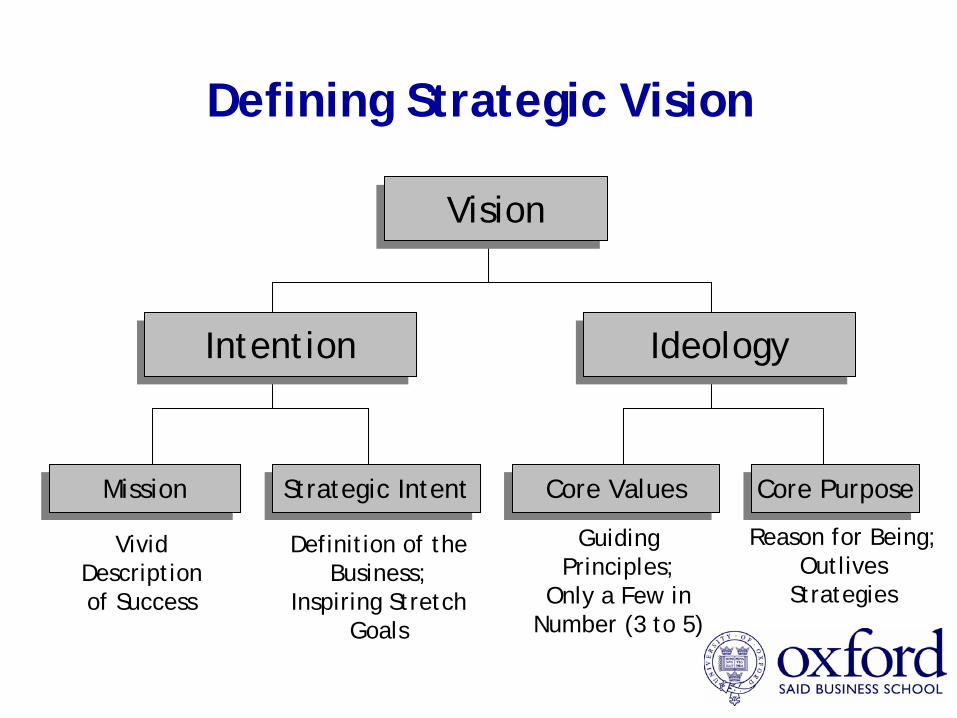

Defining Strategic Vision

VisionVision

IdeologyIdeologyIntentionIntention

Core PurposeCore PurposeCore ValuesCore ValuesStrategic IntentStrategic IntentMissionMission

Guiding Principles;

Only a Few in Number (3 to 5)

Reason for Being;Outlives

Strategies

Definition of the Business;

Inspiring Stretch Goals

Vivid Description of Success

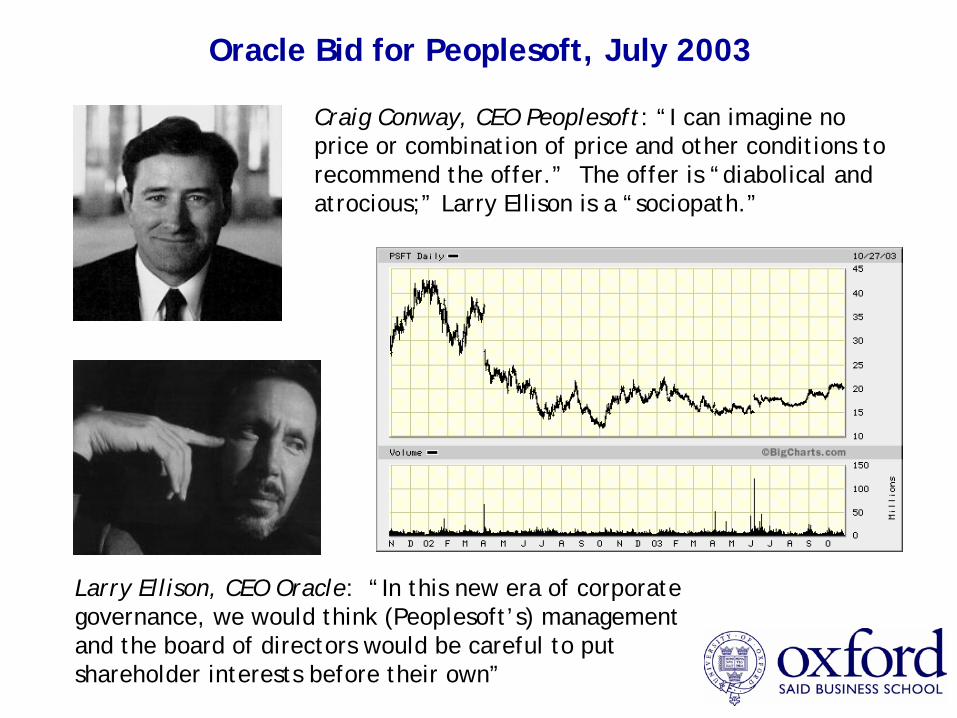

Craig Conway, CEO Peoplesoft: “I can imagine no price or combination of price and other conditions to recommend the offer.” The offer is “diabolical and atrocious;” Larry Ellison is a “sociopath.”

Larry Ellison, CEO Oracle: “In this new era of corporate governance, we would think (Peoplesoft’s) management and the board of directors would be careful to put shareholder interests before their own”

Oracle Bid for Peoplesoft, July 2003

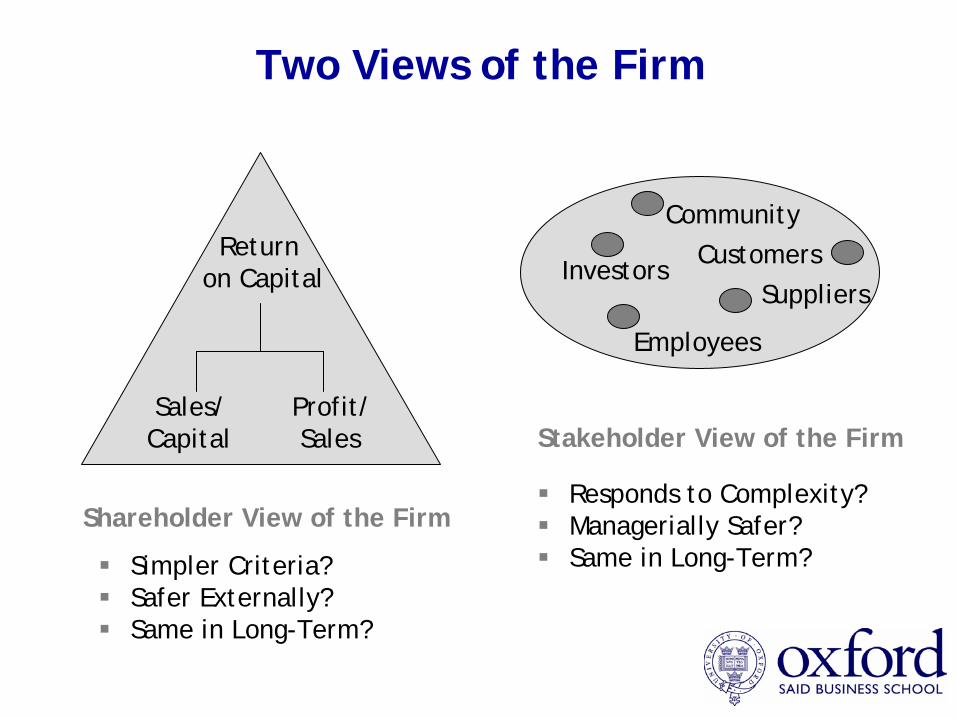

Two Views of the Firm

Return on Capital

Sales/Capital

Profit/Sales

Investors

Employees

Suppliers

CommunityCustomers

Shareholder View of the Firm

Simpler Criteria?Safer Externally? Same in Long-Term?

Responds to Complexity?Managerially Safer?Same in Long-Term?

Stakeholder View of the Firm

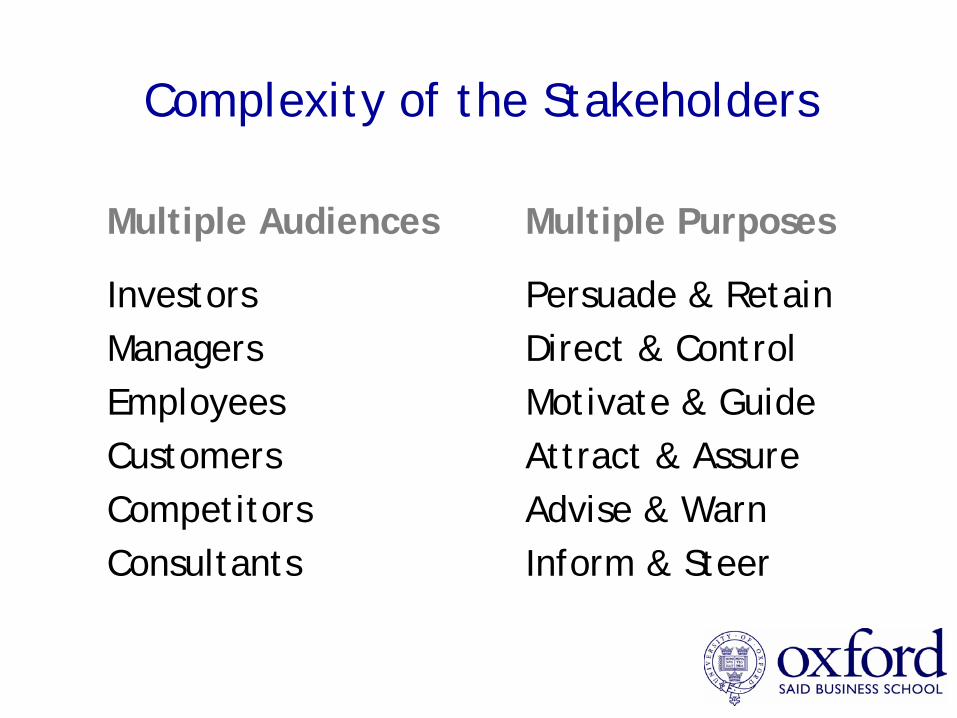

Complexity of the Stakeholders

Multiple Audiences Multiple Purposes

Investors Persuade & RetainManagers Direct & ControlEmployees Motivate & GuideCustomers Attract & AssureCompetitors Advise & WarnConsultants Inform & Steer

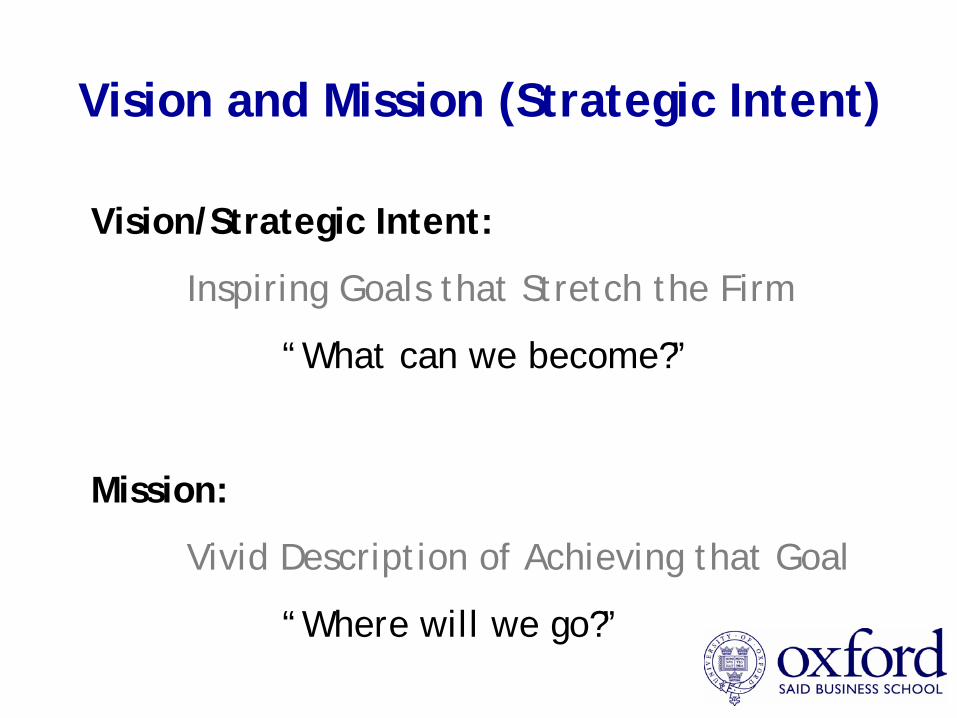

Vision and Mission (Strategic Intent)

Vision/Strategic Intent:

Inspiring Goals that Stretch the Firm

“What can we become?”

Mission:

Vivid Description of Achieving that Goal

“Where will we go?”

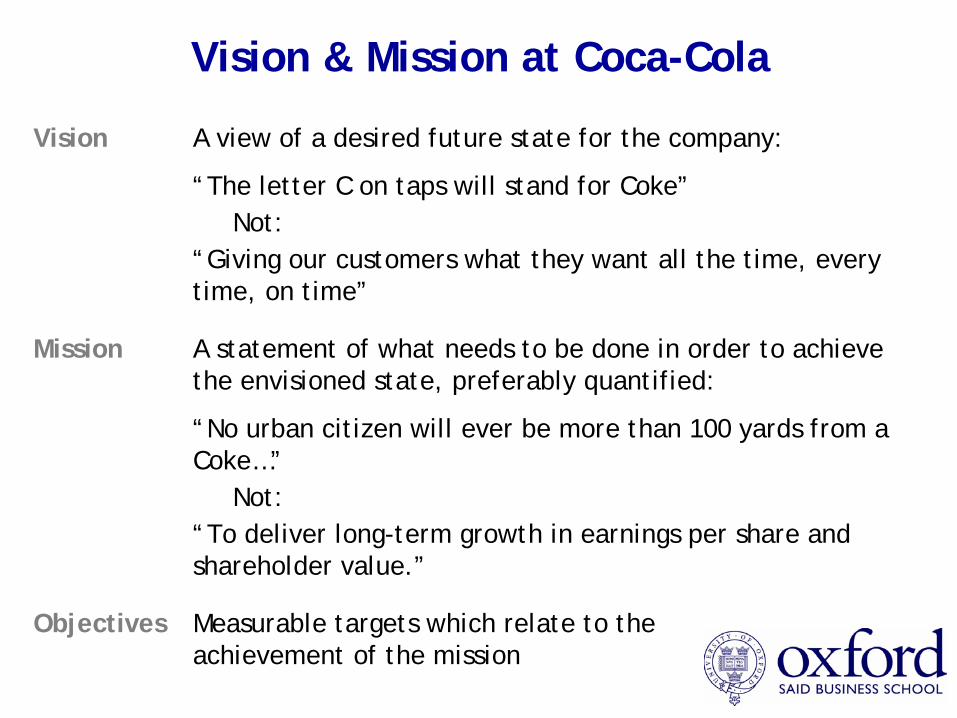

Vision & Mission at Coca-Cola

Vision A view of a desired future state for the company:

“The letter C on taps will stand for Coke”Not:

“Giving our customers what they want all the time, every time, on time”

Mission A statement of what needs to be done in order to achieve the envisioned state, preferably quantified:

“No urban citizen will ever be more than 100 yards from a Coke…”

Not:“To deliver long-term growth in earnings per share and shareholder value.”

Objectives Measurable targets which relate to the achievement of the mission

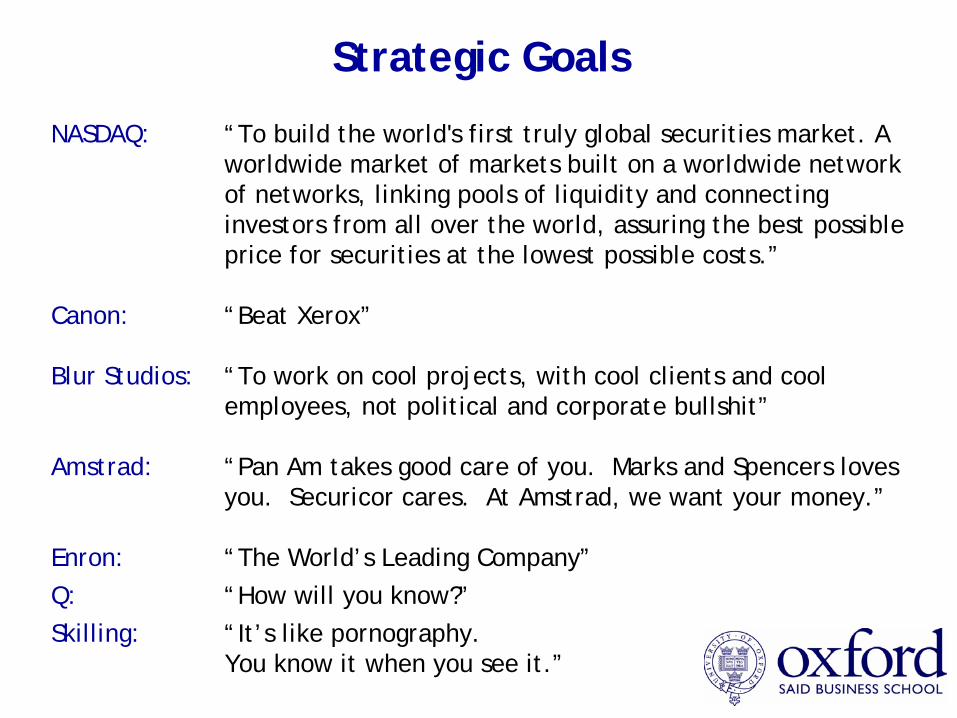

NASDAQ: “To build the world's first truly global securities market. A worldwide market of markets built on a worldwide network of networks, linking pools of liquidity and connecting investors from all over the world, assuring the best possible price for securities at the lowest possible costs.”

Canon: “Beat Xerox”

Blur Studios: “To work on cool projects, with cool clients and cool employees, not political and corporate bullshit”

Amstrad: “Pan Am takes good care of you. Marks and Spencers loves you. Securicor cares. At Amstrad, we want your money.”

Enron: “The World’s Leading Company”Q: “How will you know?”Skilling: “It’s like pornography.

You know it when you see it.”

Strategic Goals

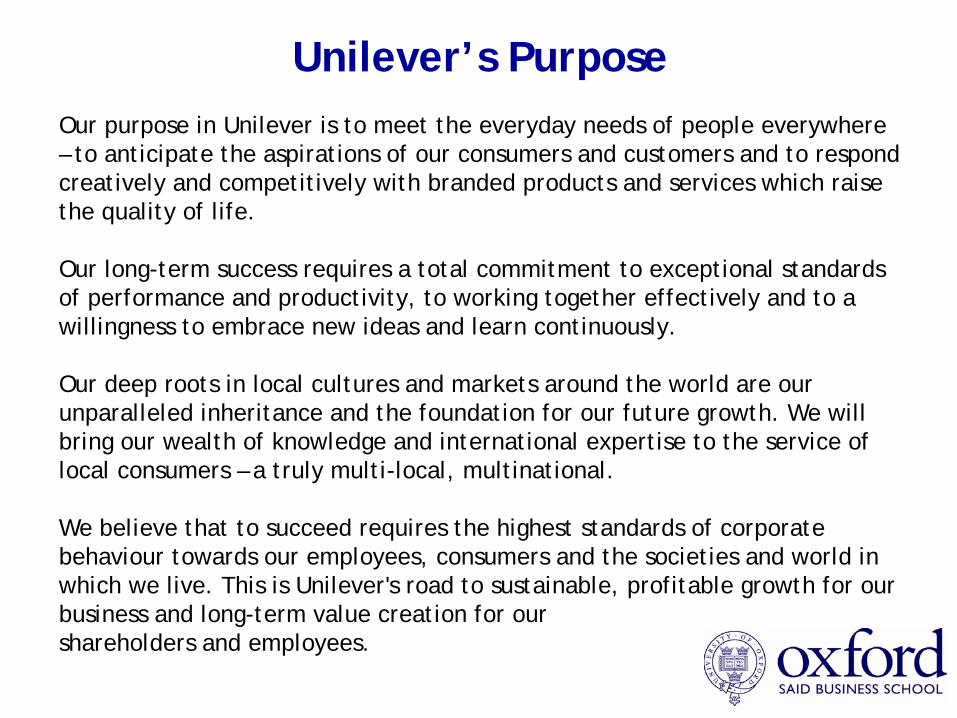

Unilever’s PurposeOur purpose in Unilever is to meet the everyday needs of people everywhere – to anticipate the aspirations of our consumers and customers and to respond creatively and competitively with branded products and services which raise the quality of life.

Our long-term success requires a total commitment to exceptional standards of performance and productivity, to working together effectively and to a willingness to embrace new ideas and learn continuously.

Our deep roots in local cultures and markets around the world are our unparalleled inheritance and the foundation for our future growth. We will bring our wealth of knowledge and international expertise to the service of local consumers – a truly multi-local, multinational.

We believe that to succeed requires the highest standards of corporate behaviour towards our employees, consumers and the societies and world in which we live. This is Unilever's road to sustainable, profitable growth for our business and long-term value creation for our shareholders and employees.

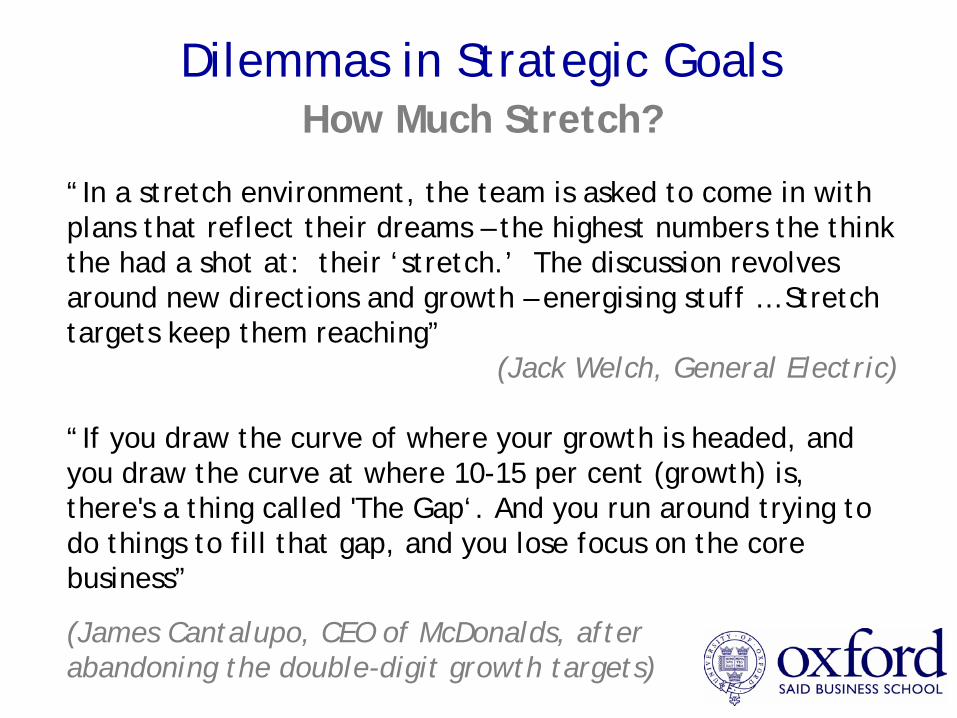

Dilemmas in Strategic GoalsHow Much Stretch?

“In a stretch environment, the team is asked to come in with plans that reflect their dreams – the highest numbers the think the had a shot at: their ‘stretch.’ The discussion revolves around new directions and growth – energising stuff … Stretch targets keep them reaching”

(Jack Welch, General Electric)

“If you draw the curve of where your growth is headed, and you draw the curve at where 10-15 per cent (growth) is, there's a thing called 'The Gap‘. And you run around trying to do things to fill that gap, and you lose focus on the core business”

(James Cantalupo, CEO of McDonalds, after abandoning the double-digit growth targets)

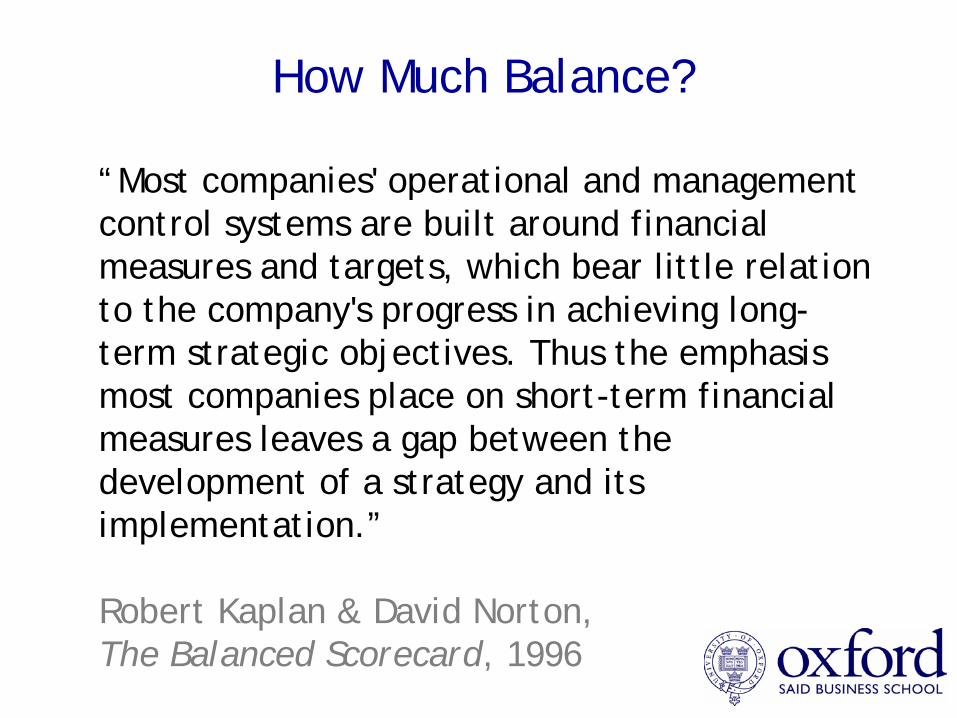

How Much Balance?

“Most companies' operational and management control systems are built around financial measures and targets, which bear little relation to the company's progress in achieving long- term strategic objectives. Thus the emphasis most companies place on short-term financial measures leaves a gap between the development of a strategy and its implementation.”

Robert Kaplan & David Norton, The Balanced Scorecard, 1996

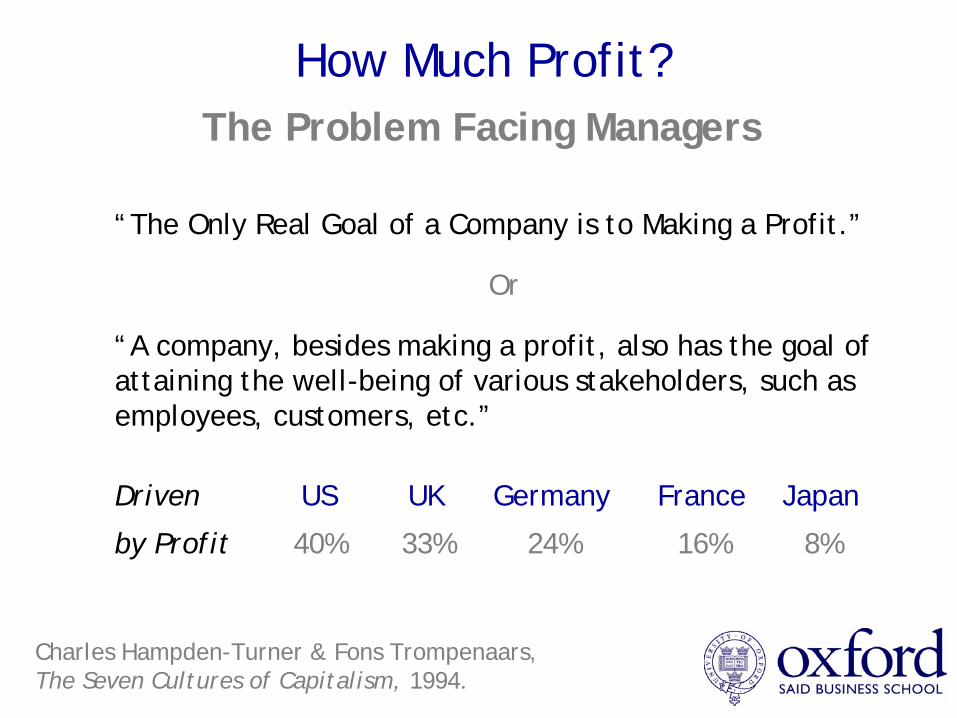

How Much Profit?

“The Only Real Goal of a Company is to Making a Profit.”

Or

“A company, besides making a profit, also has the goal of attaining the well-being of various stakeholders, such as employees, customers, etc.”

Driven US UK Germany France Japan

by Profit 40% 33% 24% 16% 8%

The Problem Facing Managers

Charles Hampden-Turner & Fons Trompenaars, The Seven Cultures of Capitalism, 1994.

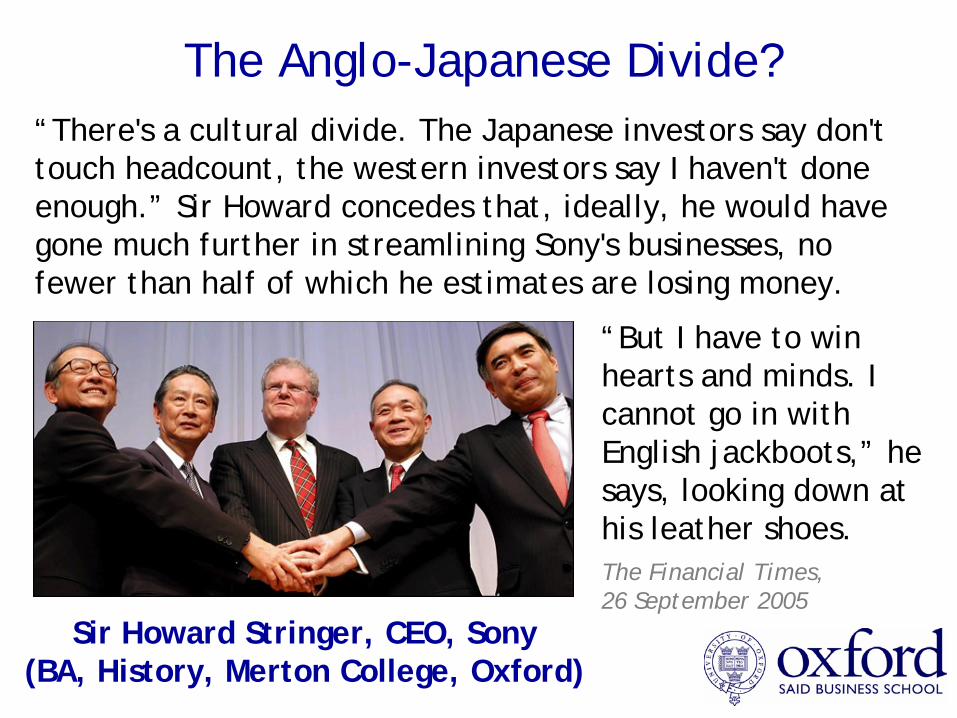

The Anglo-Japanese Divide?

The Financial Times, 26 September 2005

Sir Howard Stringer, CEO, Sony(BA, History, Merton College, Oxford)

“There's a cultural divide. The Japanese investors say don't touch headcount, the western investors say I haven't done enough.” Sir Howard concedes that, ideally, he would have gone much further in streamlining Sony's businesses, no fewer than half of which he estimates are losing money.

“But I have to win hearts and minds. I cannot go in with English jackboots,” he says, looking down at his leather shoes.

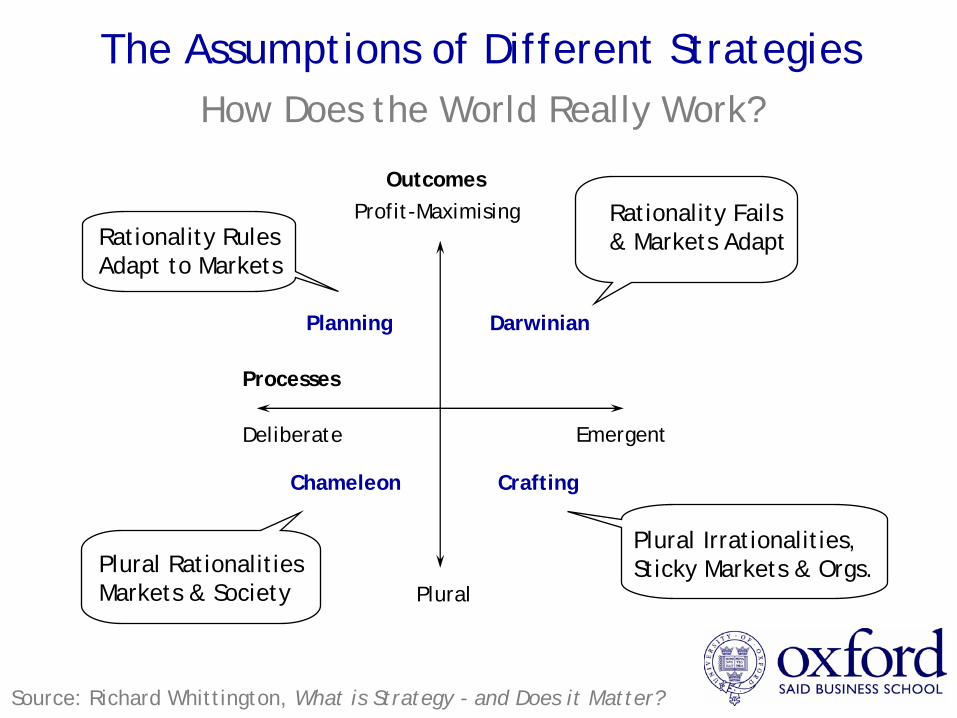

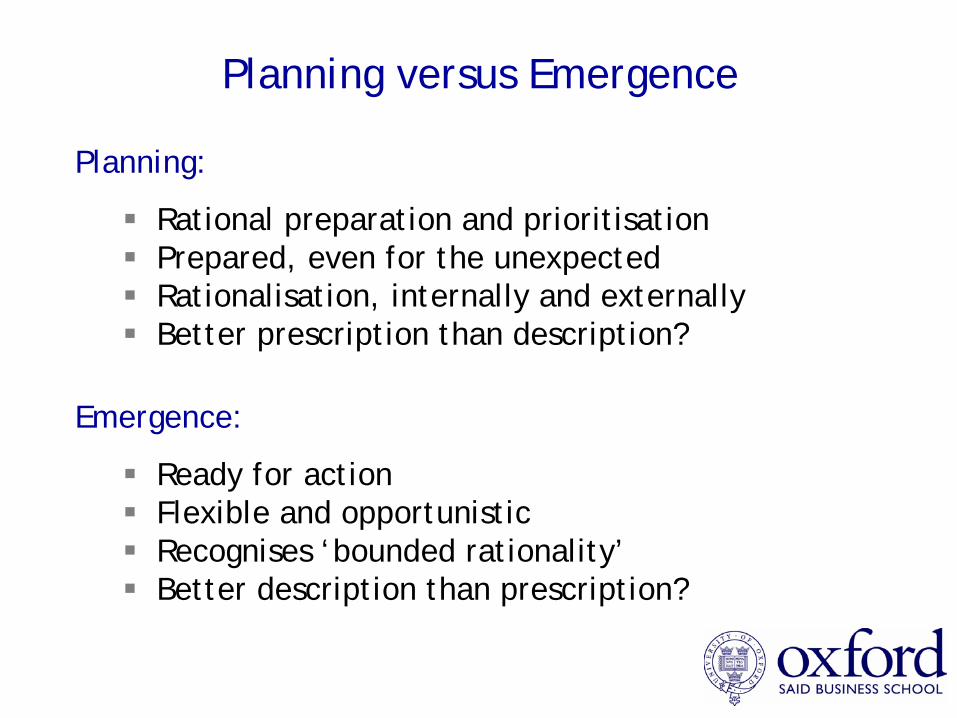

The Assumptions of Different Strategies

Planning Darwinian

Chameleon Crafting

Outcomes

Processes

Profit-Maximising

Deliberate Emergent

Plural

Rationality RulesAdapt to Markets

Rationality Fails& Markets Adapt

Plural RationalitiesMarkets & Society

Plural Irrationalities,Sticky Markets & Orgs.

How Does the World Really Work?

Source: Richard Whittington, What is Strategy - and Does it Matter?

Key Topics for Today

Defining strategy

Business and corporate strategy

Strategy content and process

Stakeholder view

Vision, mission, goals

Competitive Advantage

Christopher McKenna

MBAStrategy: Session Two

October 2006

Course Structure

1. Introduction to Strategy

2. Competitive Advantage

3. Industry Strategy

4. Strategy and Change

5. Diversification

6. Global Strategy

7. Managing the Multibusiness Company

8. Strategy Process

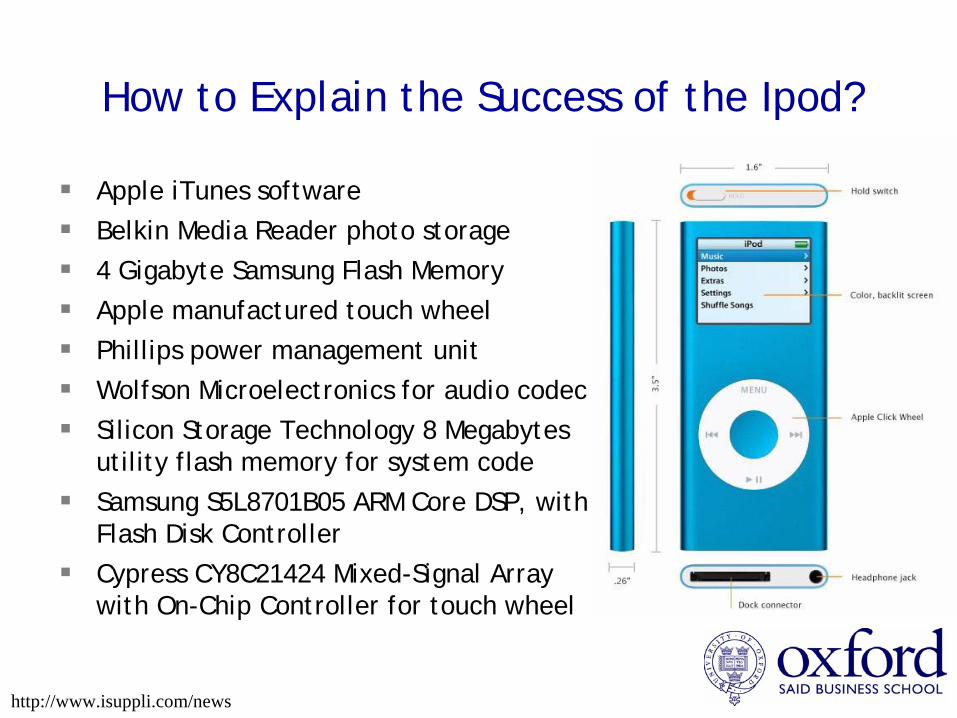

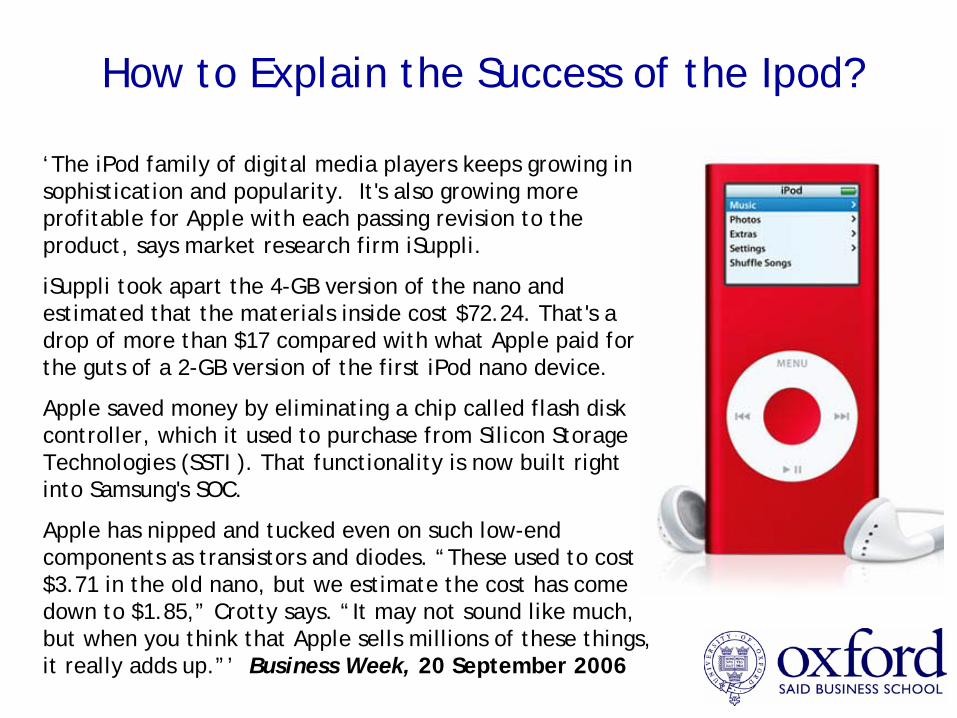

How to Explain the Success of the Ipod?

Apple iTunes softwareBelkin Media Reader photo storage4 Gigabyte Samsung Flash Memory Apple manufactured touch wheel Phillips power management unit Wolfson Microelectronics for audio codecSilicon Storage Technology 8 Megabytes utility flash memory for system codeSamsung S5L8701B05 ARM Core DSP, with Flash Disk ControllerCypress CY8C21424 Mixed-Signal Array with On-Chip Controller for touch wheel

http://www.isuppli.com/news

Key Concepts & Techniques

Competitive Positioning

Resource-Based Advantage

Value Innovation

X-Factors

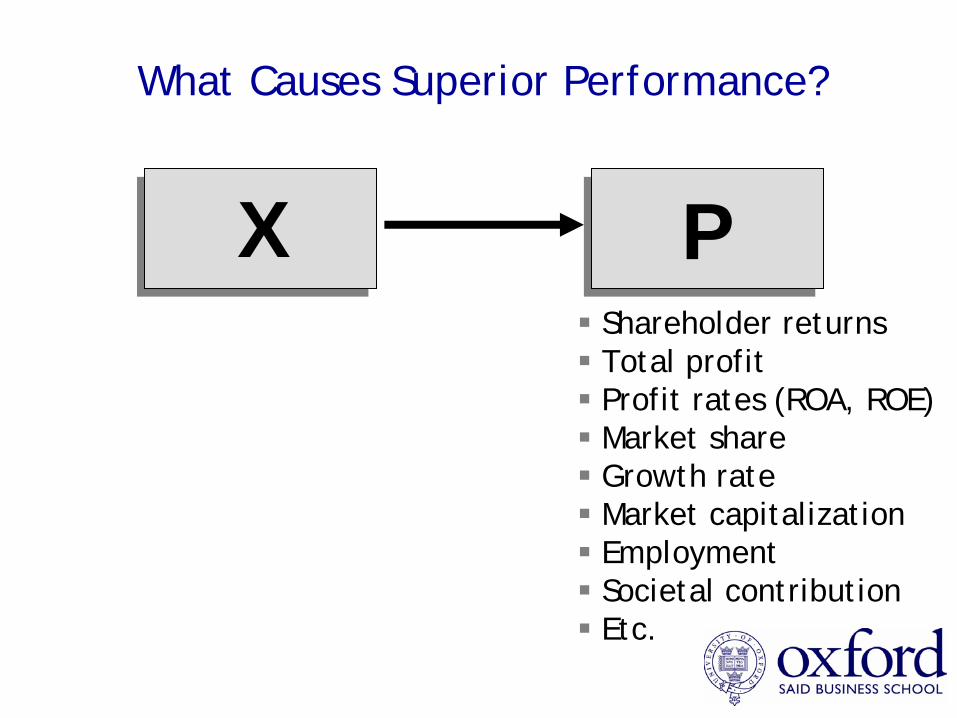

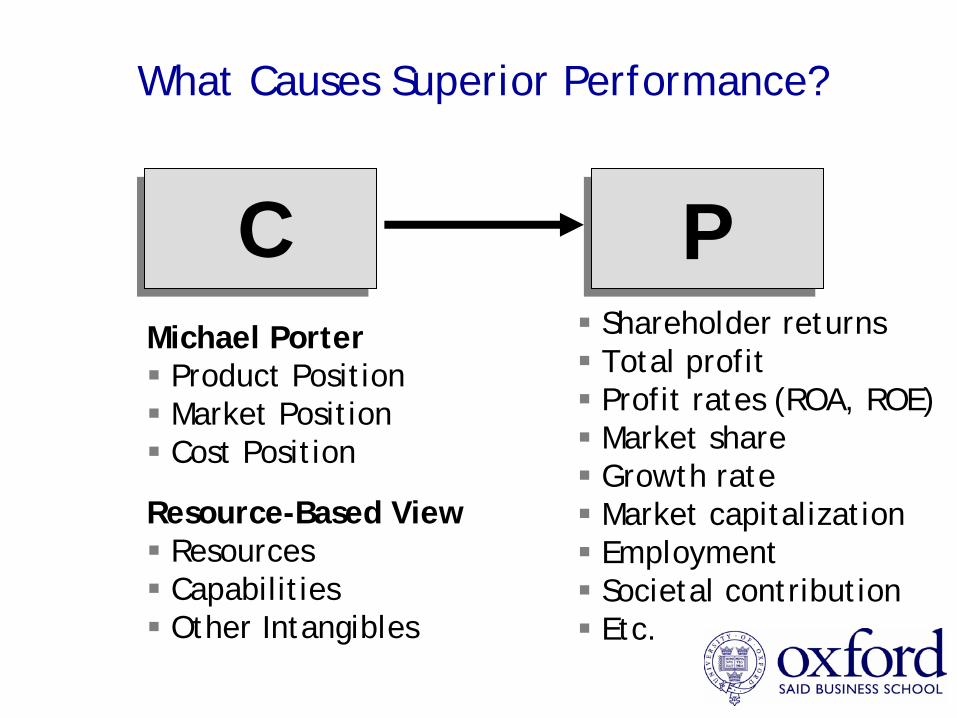

What Causes Superior Performance?

X PShareholder returnsTotal profitProfit rates (ROA, ROE)Market shareGrowth rateMarket capitalizationEmploymentSocietal contributionEtc.

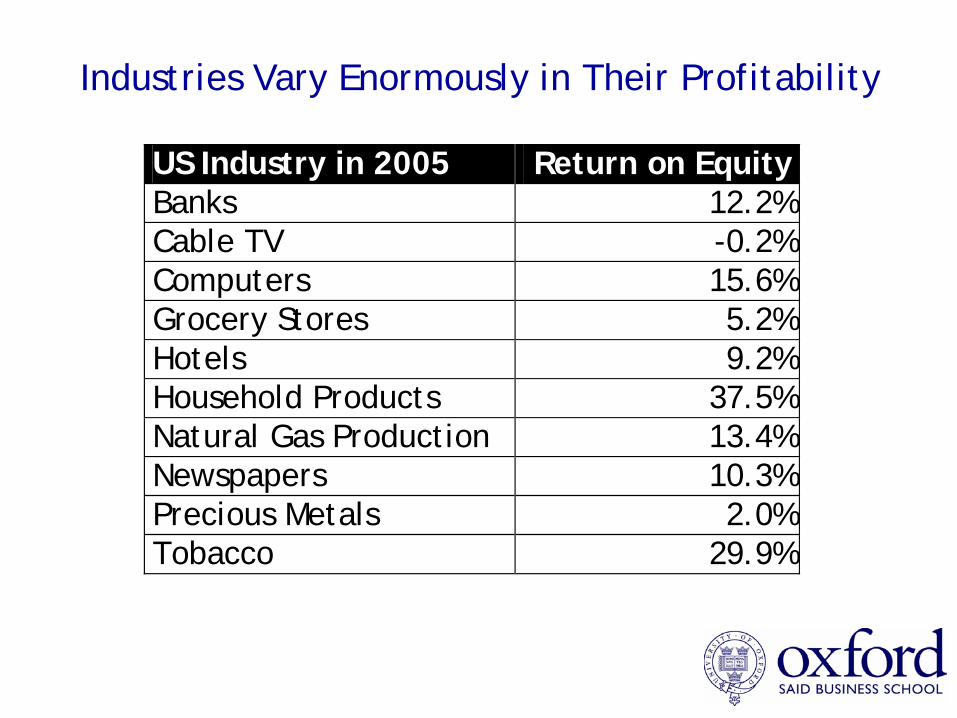

US Industry in 2005 Return on Equity Banks 12.2% Cable TV -0.2% Computers 15.6% Grocery Stores 5.2% Hotels 9.2% Household Products 37.5% Natural Gas Production 13.4% Newspapers 10.3% Precious Metals 2.0% Tobacco 29.9%

Industries Vary Enormously in Their Profitability

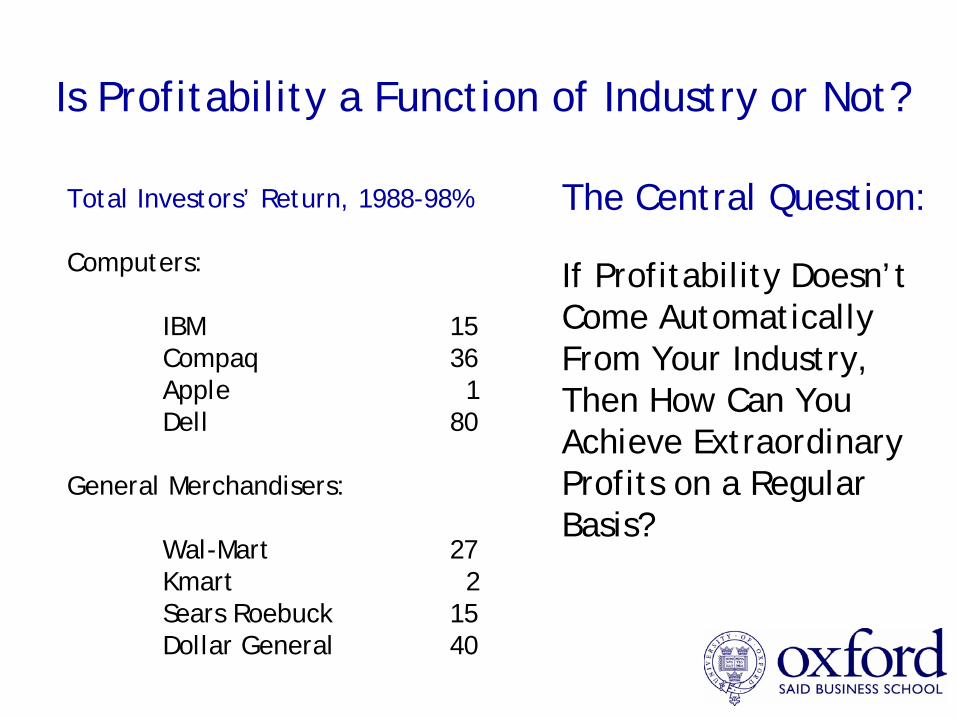

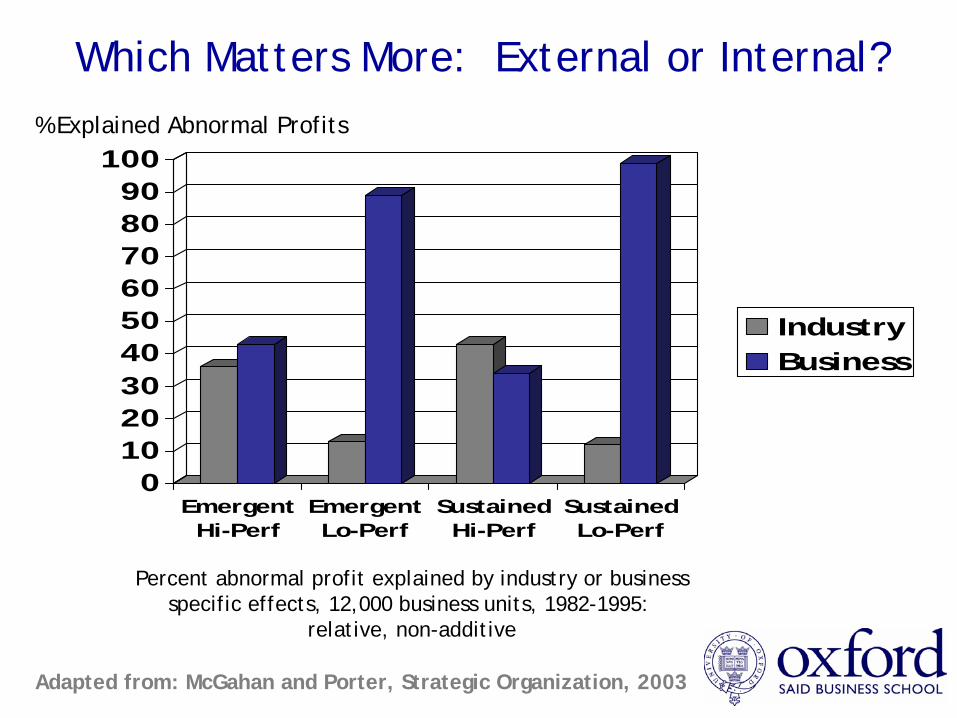

Is Profitability a Function of Industry or Not?

Total Investors’ Return, 1988-98%

Computers:

IBM 15Compaq 36Apple 1Dell 80

General Merchandisers:

Wal-Mart 27Kmart 2Sears Roebuck 15Dollar General 40

If Profitability Doesn’tCome AutomaticallyFrom Your Industry,Then How Can You Achieve ExtraordinaryProfits on a RegularBasis?

The Central Question:

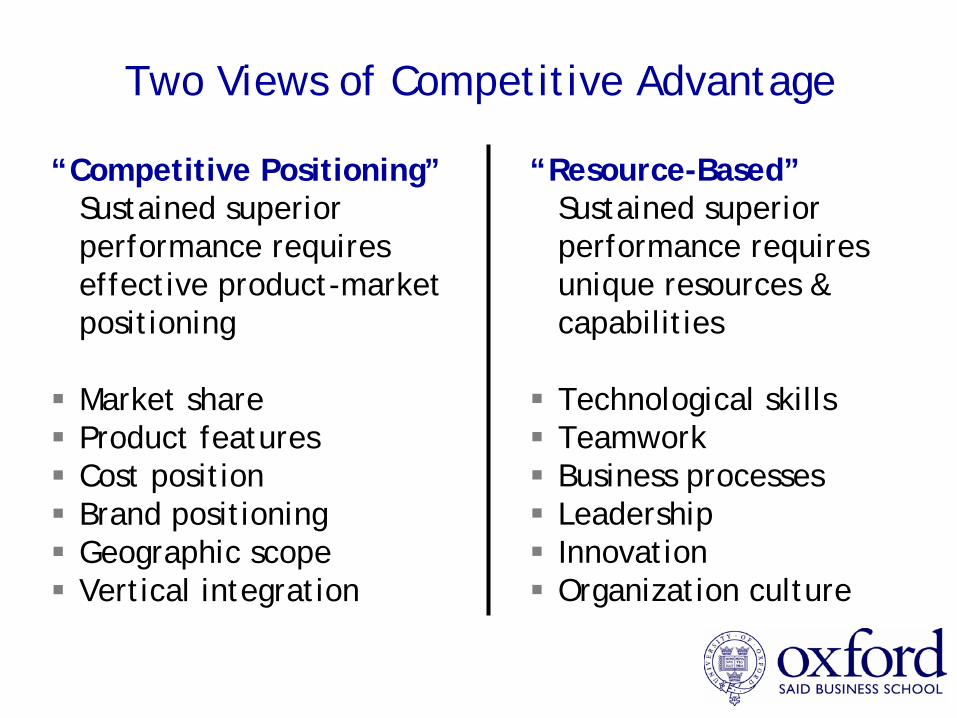

Two Views of Competitive Advantage

“Competitive Positioning”Sustained superior performance requires effective product-market positioning

Market shareProduct featuresCost positionBrand positioningGeographic scopeVertical integration

“Resource-Based”Sustained superior performance requires unique resources & capabilities

Technological skillsTeamworkBusiness processesLeadershipInnovationOrganization culture

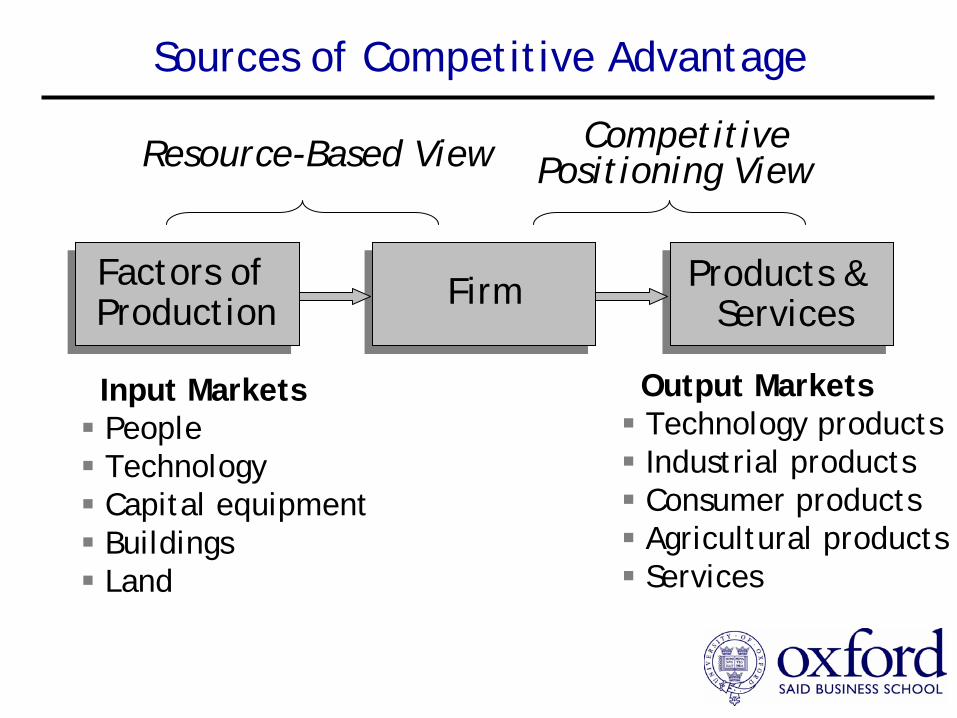

Sources of Competitive Advantage

FirmFactors of Production

Products & Services

Output MarketsTechnology productsIndustrial productsConsumer productsAgricultural productsServices

Resource-Based View

Input MarketsPeopleTechnologyCapital equipment BuildingsLand

Competitive Positioning View

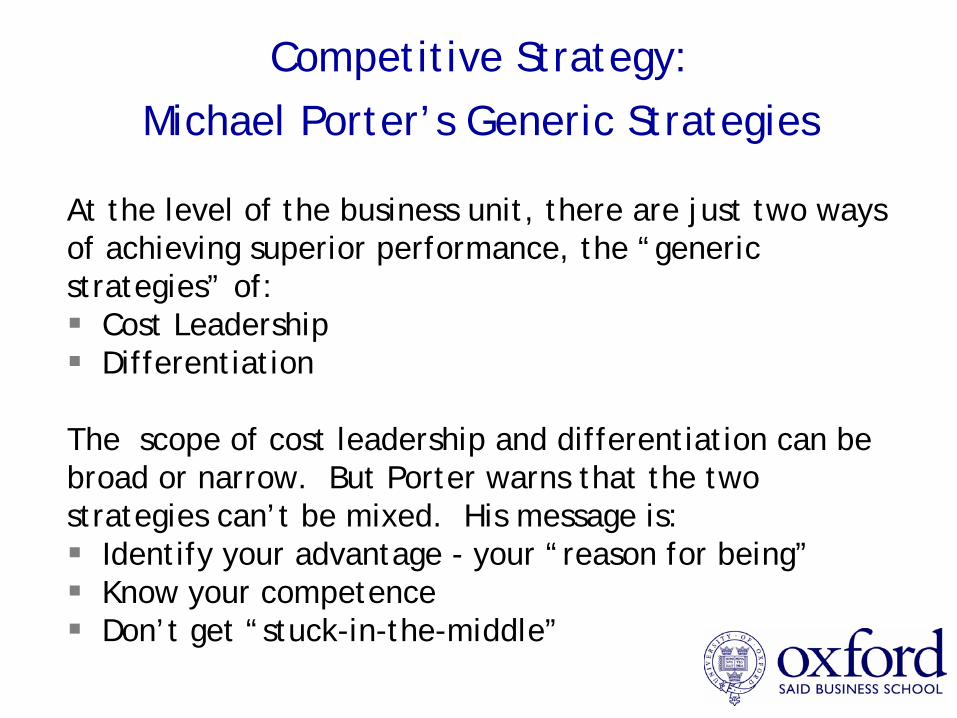

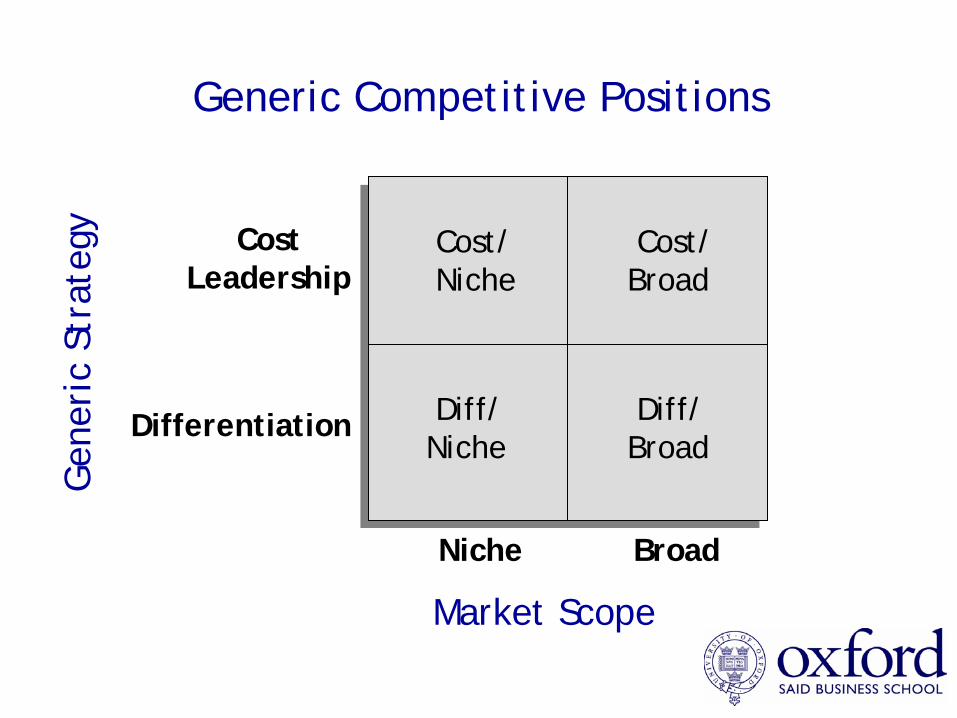

Competitive Strategy: Michael Porter’s Generic Strategies

At the level of the business unit, there are just two ways of achieving superior performance, the “generic strategies” of:

Cost LeadershipDifferentiation

The scope of cost leadership and differentiation can be broad or narrow. But Porter warns that the two strategies can’t be mixed. His message is:

Identify your advantage - your “reason for being”Know your competenceDon’t get “stuck-in-the-middle”

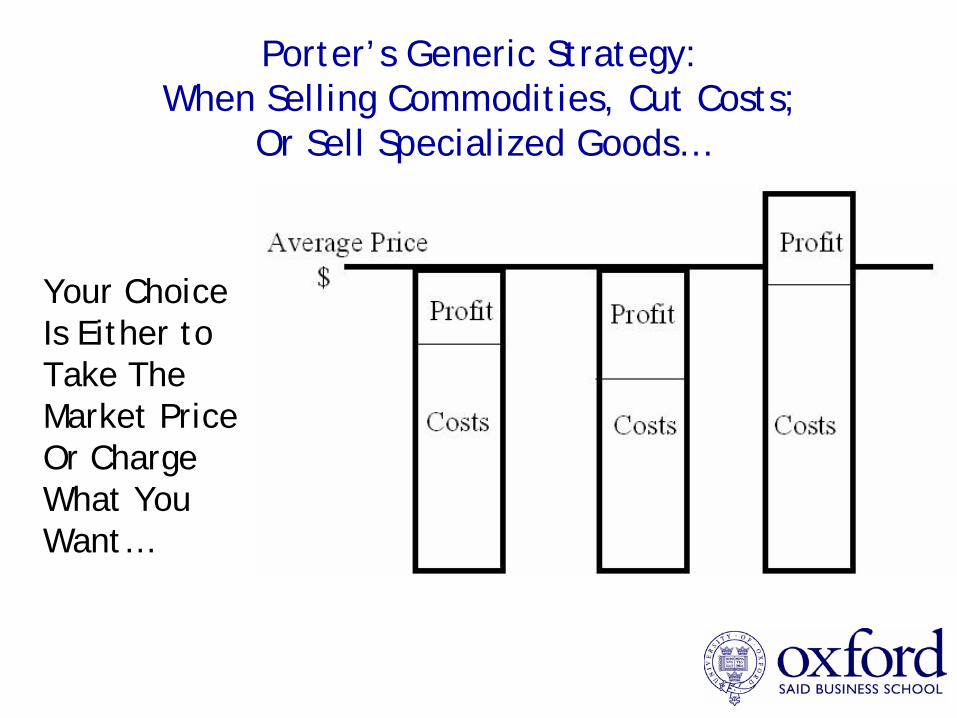

Porter’s Generic Strategy:When Selling Commodities, Cut Costs;

Or Sell Specialized Goods…

Your ChoiceIs Either to Take The Market PriceOr Charge What You Want…

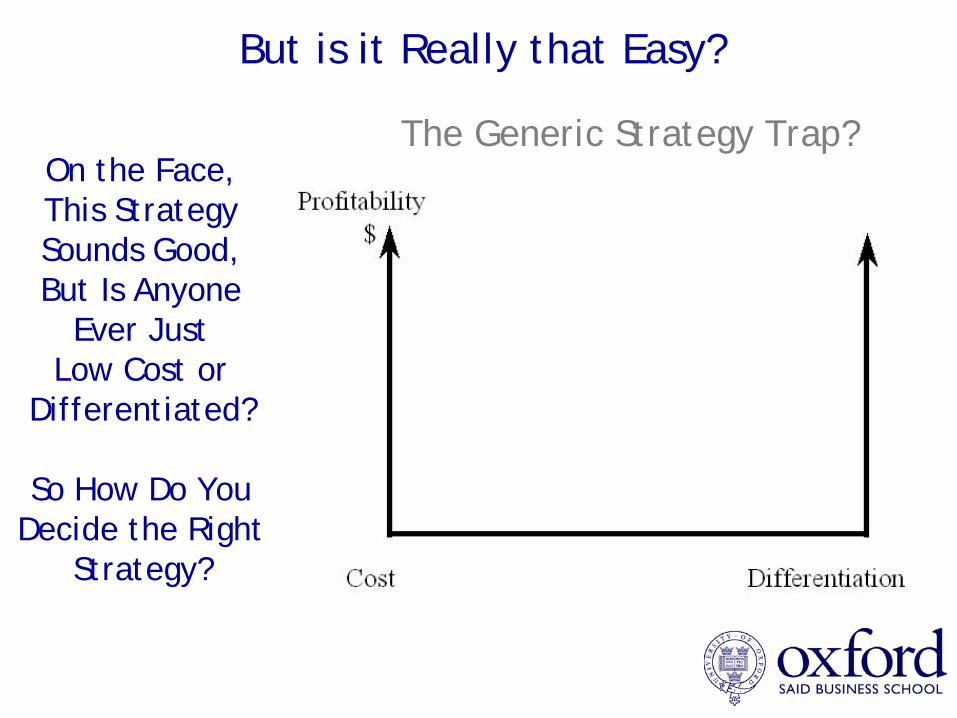

But is it Really that Easy?

The Generic Strategy Trap?On the Face, This Strategy Sounds Good, But Is Anyone

Ever Just Low Cost or

Differentiated?

So How Do You Decide the Right

Strategy?

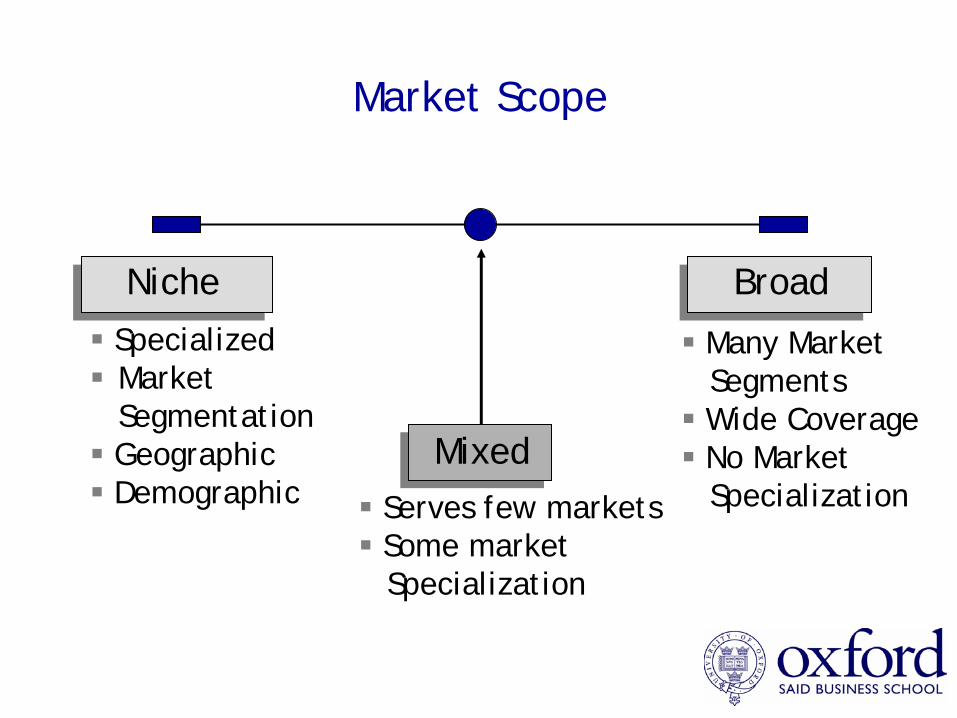

Market Scope

Niche Broad

Many Market SegmentsWide CoverageNo Market Specialization

SpecializedMarket SegmentationGeographicDemographic

MixedServes few marketsSome market Specialization

Generic Competitive Positions

Cost Leadership

Differentiation

Niche Broad

Cost/Niche

Diff/Niche

Diff/Broad

Cost/Broad

Market Scope

Gen

eric

Str

ateg

y

Instead of Generic, Be Specific.

In This Industry, What is the Basis of Competition?

Access to CapitalCost StructureCustomer ServiceDistribution ChannelsEnvironmental AwarenessGeographic BreadthInnovationMarket Segments ServedMarket ShareNovelty/Fashion Parent Company Affiliation

PriceProduct FeaturesProduct Line BreadthQualityReputationSocial ConsciousnessTechnologyTime/ConvenienceVertical Integration

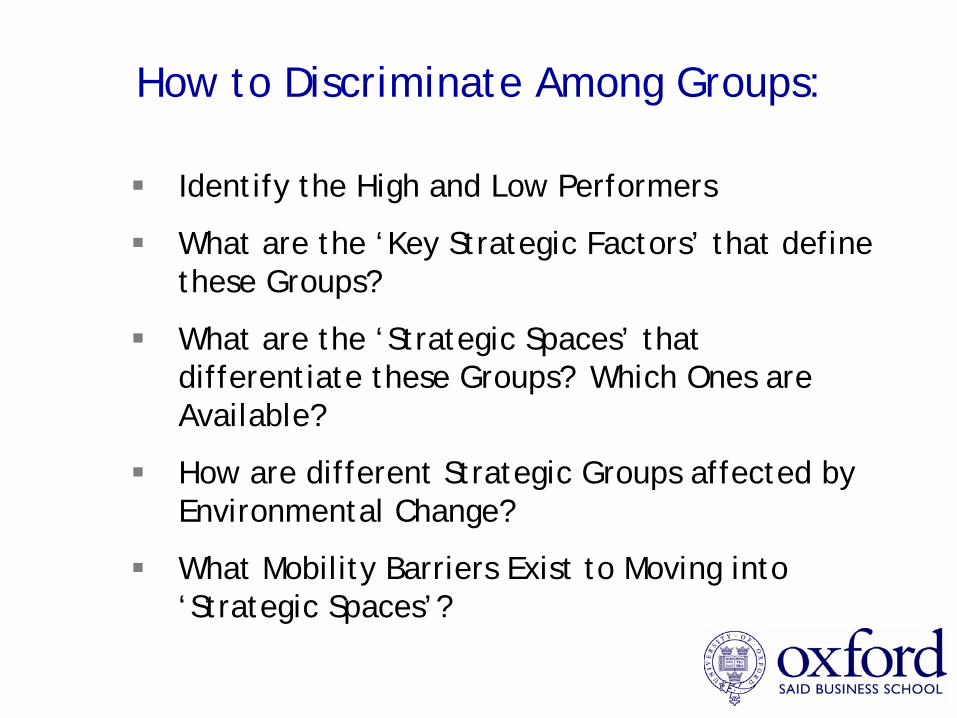

How to Discriminate Among Groups:

Identify the High and Low Performers

What are the ‘Key Strategic Factors’ that define these Groups?

What are the ‘Strategic Spaces’ that differentiate these Groups? Which Ones are Available?

How are different Strategic Groups affected by Environmental Change?

What Mobility Barriers Exist to Moving into ‘Strategic Spaces’?

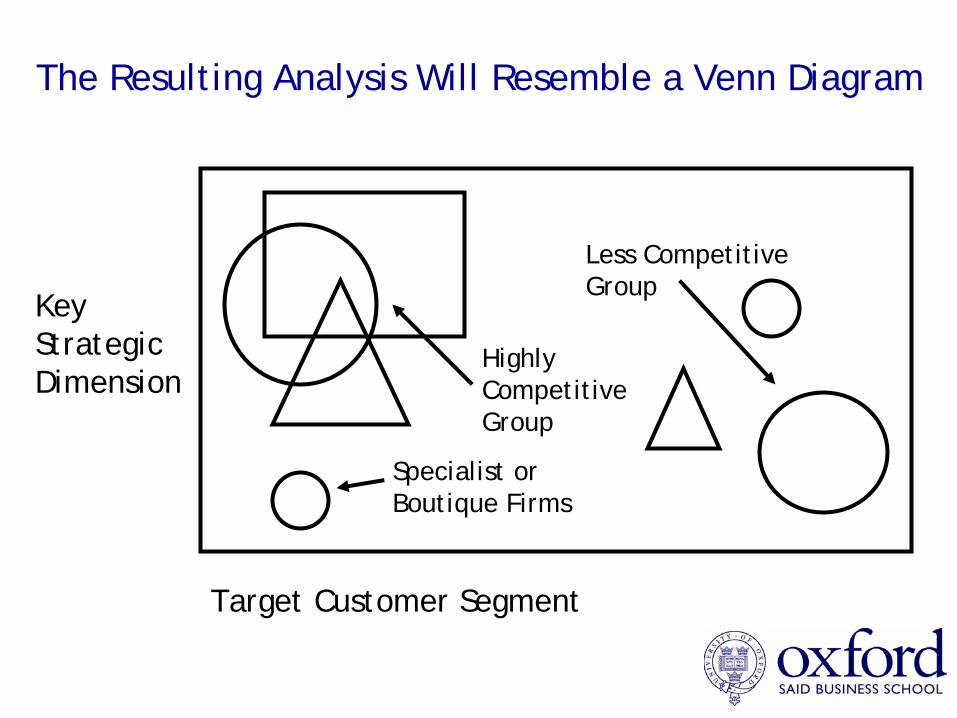

The Resulting Analysis Will Resemble a Venn Diagram

Target Customer Segment

KeyStrategicDimension

Less Competitive Group

Specialist orBoutique Firms

Highly CompetitiveGroup

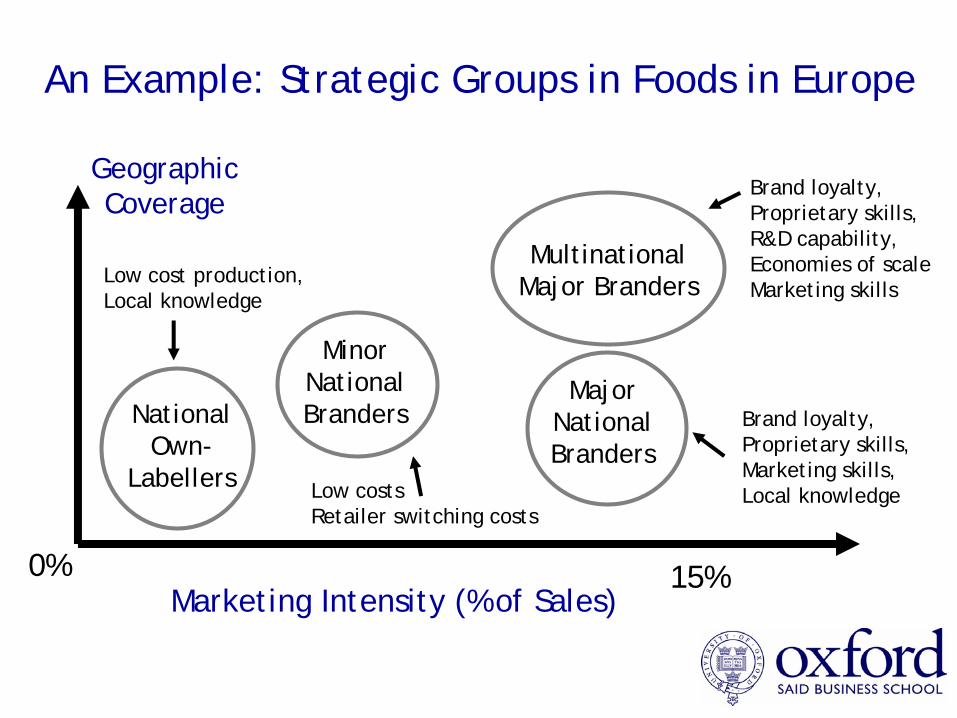

An Example: Strategic Groups in Foods in Europe

MultinationalMajor Branders

MajorNationalBranders

MinorNationalBrandersNational

Own-Labellers

Marketing Intensity (% of Sales)15%0%

GeographicCoverage

Low cost production,Local knowledge

Low costsRetailer switching costs

Brand loyalty,Proprietary skills,R&D capability,Economies of scaleMarketing skills

Brand loyalty,Proprietary skills,Marketing skills,Local knowledge

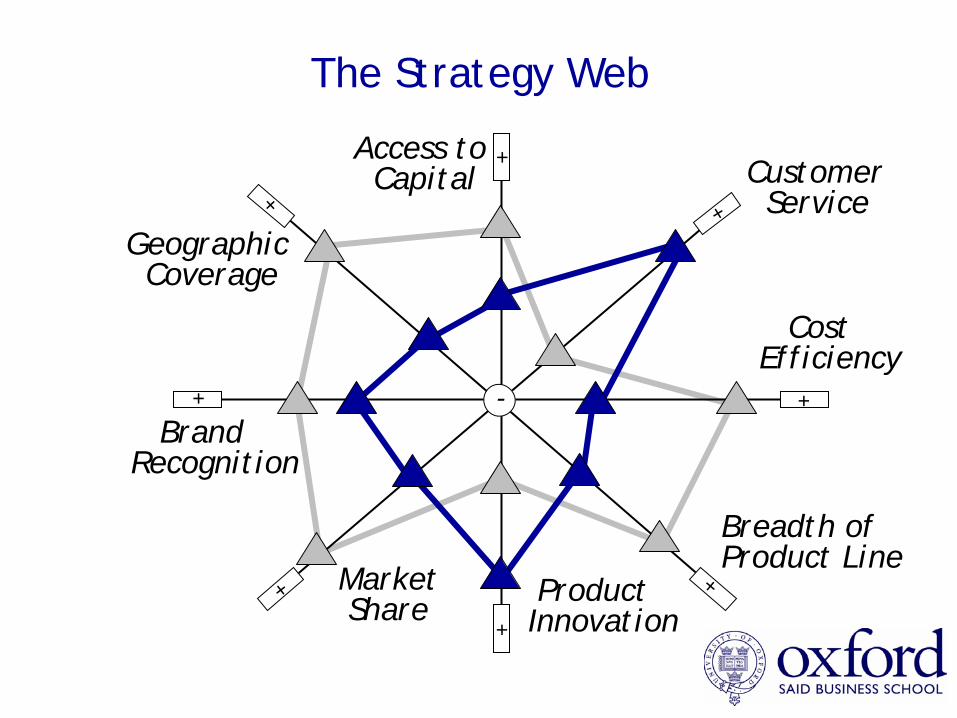

The Strategy Web

Access toCapital

CostEfficiency

Customer Service

Breadth of Product Line

Product Innovation

Market Share

Brand Recognition

GeographicCoverage

+

-

+

+

+

+

+

+

+

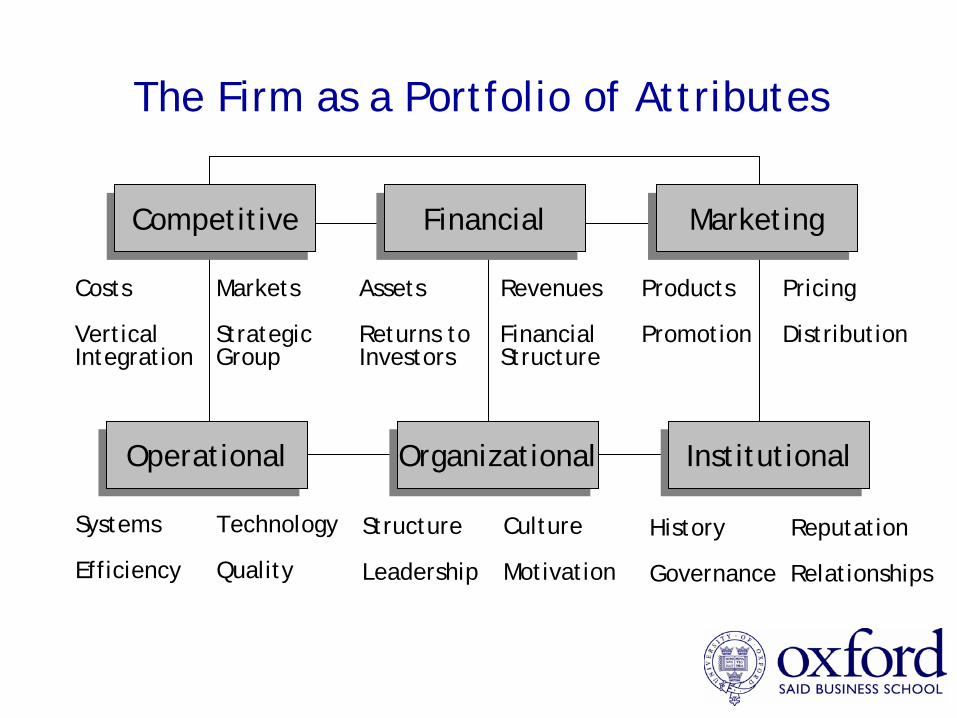

The Firm as a Portfolio of Attributes

OperationalOperational

CompetitiveCompetitive

OrganizationalOrganizational

FinancialFinancial

InstitutionalInstitutional

MarketingMarketing

Costs Markets

Vertical Strategic Integration Group

Assets Revenues

Returns to Financial Investors Structure

Products Pricing

Promotion Distribution

Systems Technology

Efficiency Quality

Structure Culture

Leadership Motivation

History Reputation

Governance Relationships

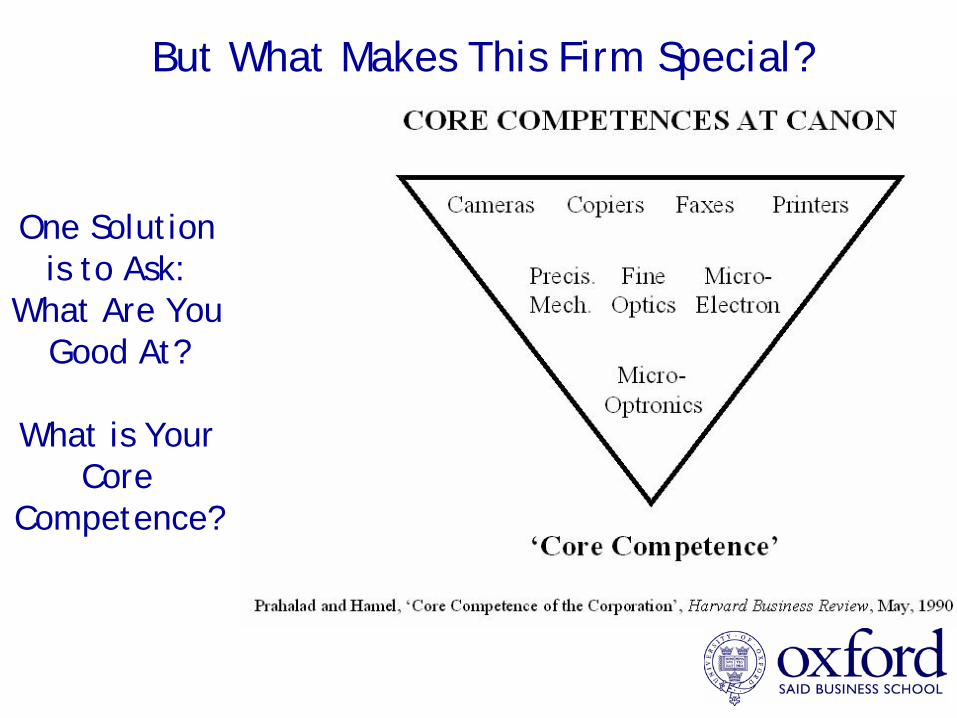

But What Makes This Firm Special?

One Solution is to Ask:

What Are You Good At?

What is Your Core

Competence?

Defining Core Competences

A ‘core competence’ is:

A bundle of skills and technologiesOf fundamental customer benefitCompetitively uniqueA gateway to new markets

The notion shifts strategy from a battle of market position, towards a mastery of skills and capabilities.

The key question is:

What are you best at?

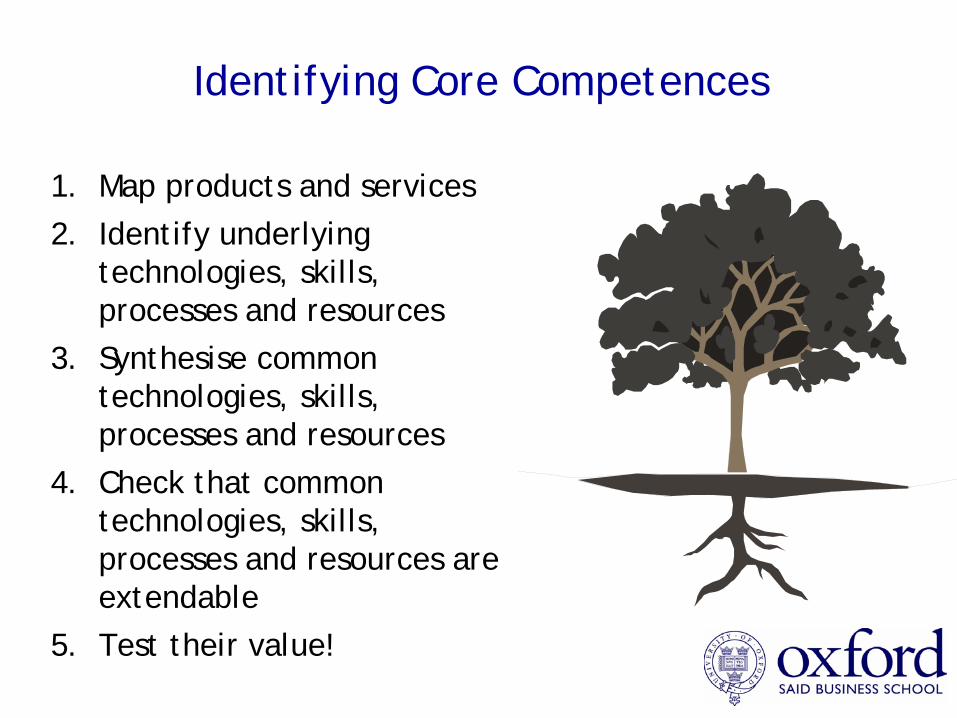

Identifying Core Competences

1. Map products and services2. Identify underlying

technologies, skills, processes and resources

3. Synthesise common technologies, skills, processes and resources

4. Check that common technologies, skills, processes and resources are extendable

5. Test their value!

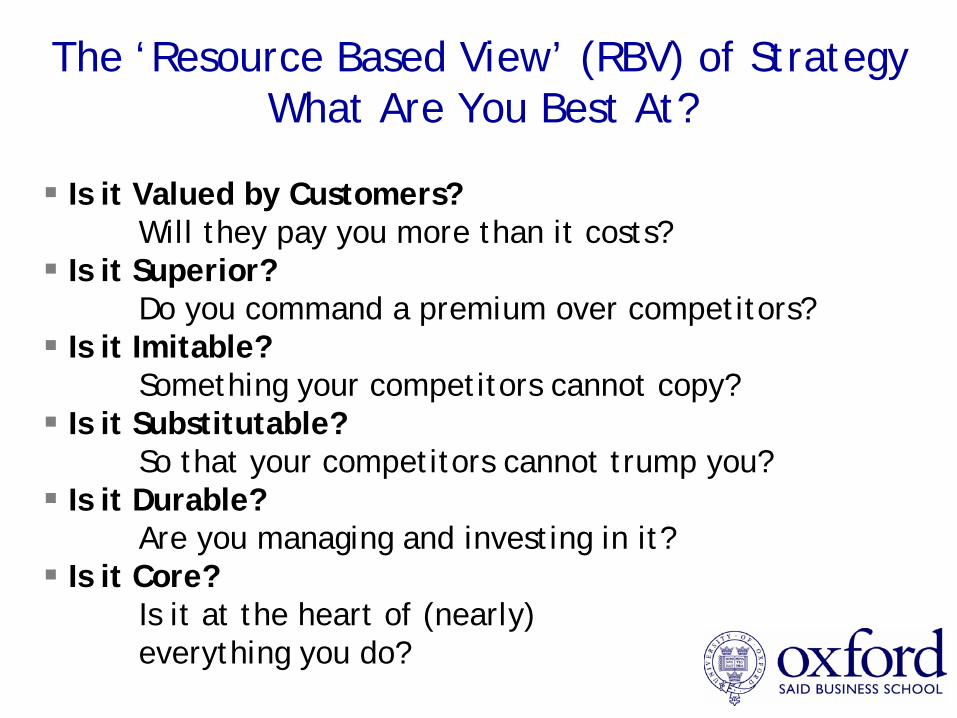

The ‘Resource Based View’ (RBV) of StrategyWhat Are You Best At?

Is it Valued by Customers?Will they pay you more than it costs?

Is it Superior?Do you command a premium over competitors?

Is it Imitable?Something your competitors cannot copy?

Is it Substitutable?So that your competitors cannot trump you?

Is it Durable?Are you managing and investing in it?

Is it Core?Is it at the heart of (nearly) everything you do?

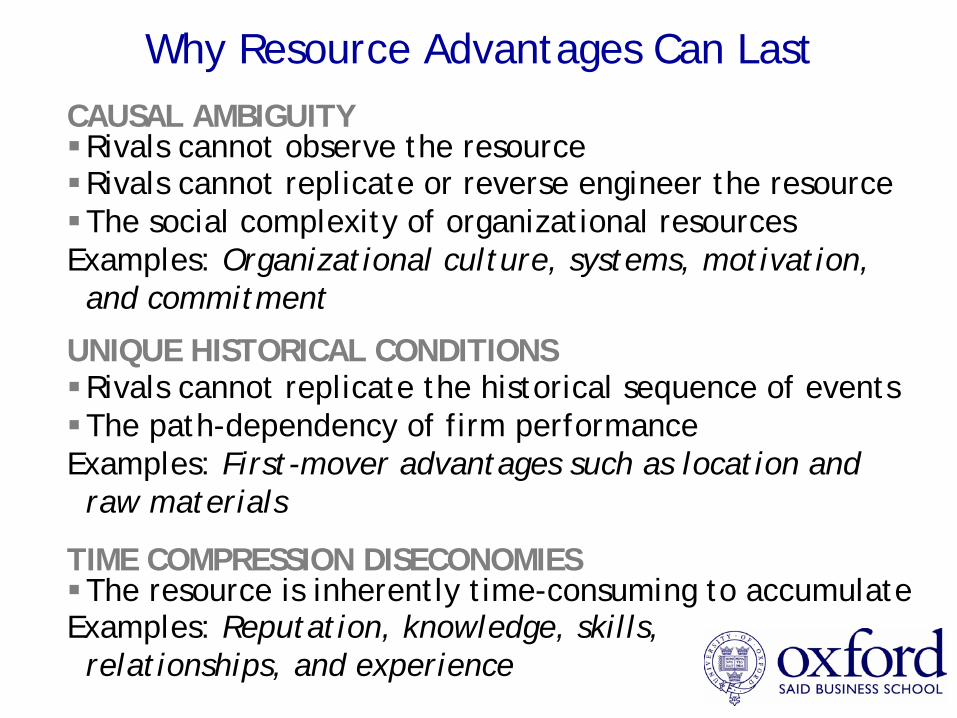

Why Resource Advantages Can LastCAUSAL AMBIGUITYRivals cannot observe the resourceRivals cannot replicate or reverse engineer the resourceThe social complexity of organizational resources

Examples: Organizational culture, systems, motivation, and commitment

UNIQUE HISTORICAL CONDITIONSRivals cannot replicate the historical sequence of events The path-dependency of firm performance

Examples: First-mover advantages such as location and raw materials

TIME COMPRESSION DISECONOMIESThe resource is inherently time-consuming to accumulate

Examples: Reputation, knowledge, skills, relationships, and experience

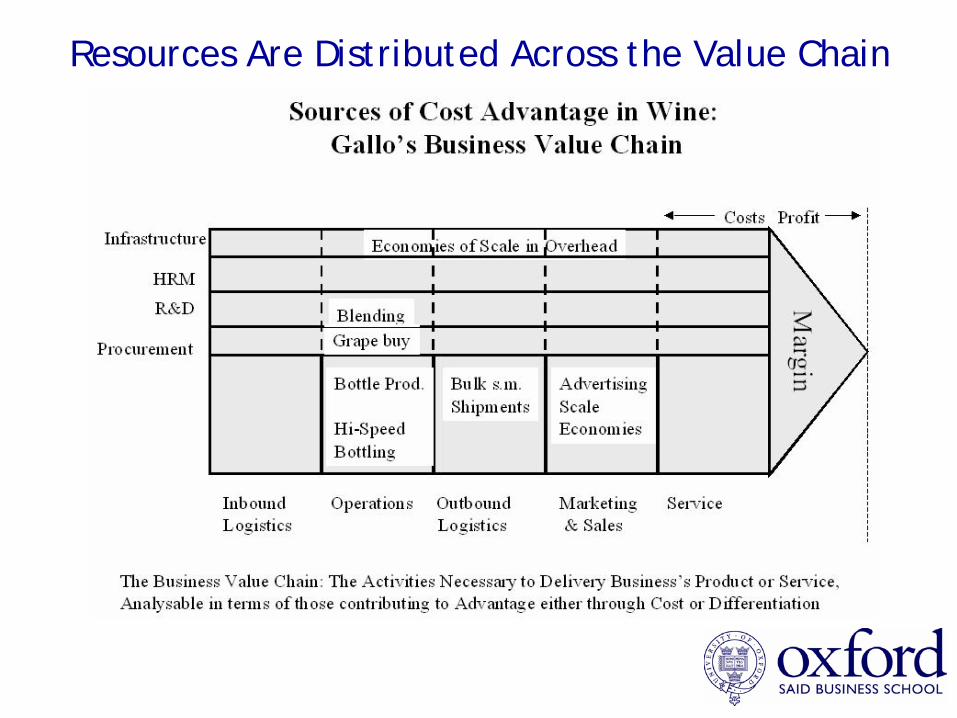

Resources Are Distributed Across the Value Chain

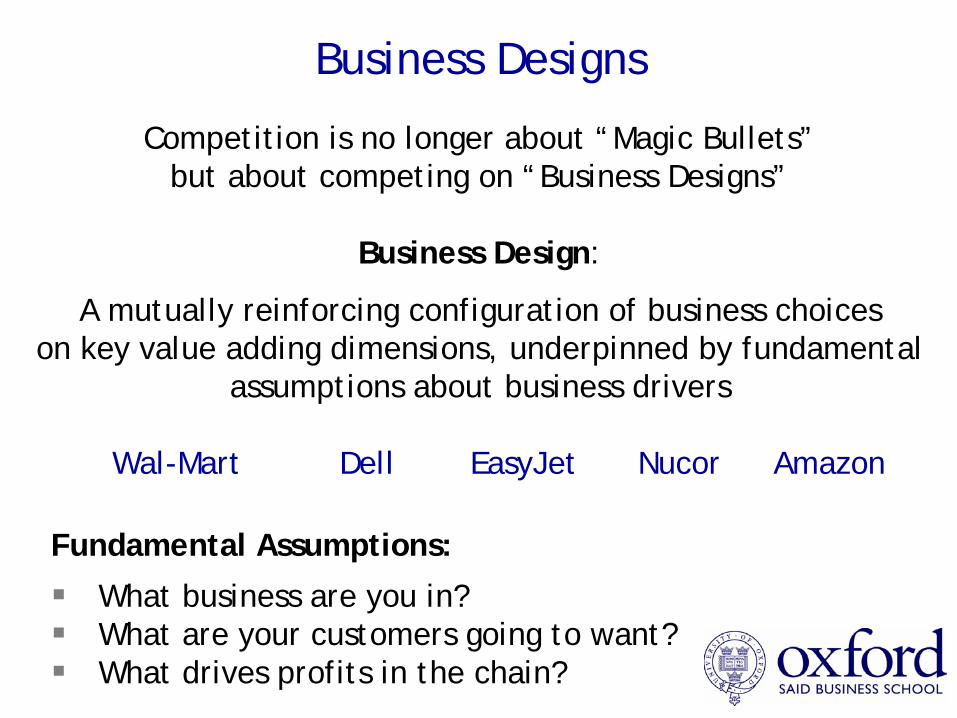

Business Designs

Competition is no longer about “Magic Bullets”but about competing on “Business Designs”

Business Design:

A mutually reinforcing configuration of business choices on key value adding dimensions, underpinned by fundamental

assumptions about business drivers

Wal-Mart Dell EasyJet Nucor Amazon

Fundamental Assumptions:

What business are you in?What are your customers going to want?What drives profits in the chain?

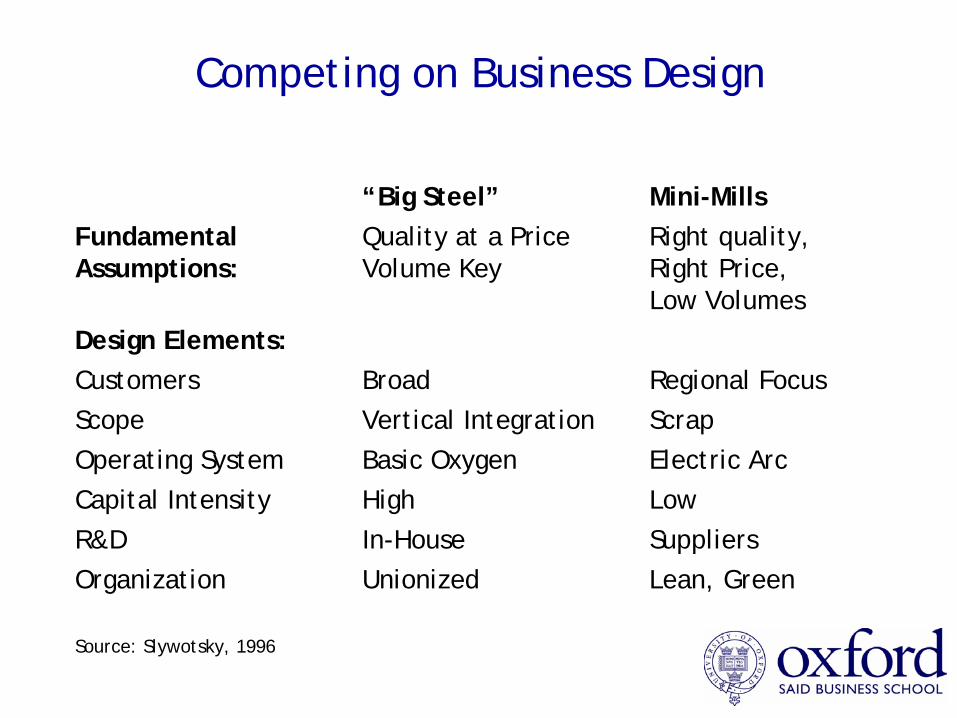

Competing on Business Design

“Big Steel” Mini-MillsFundamental Quality at a Price Right quality, Assumptions: Volume Key Right Price,

Low VolumesDesign Elements:Customers Broad Regional FocusScope Vertical Integration ScrapOperating System Basic Oxygen Electric ArcCapital Intensity High LowR&D In-House SuppliersOrganization Unionized Lean, Green

Source: Slywotsky, 1996

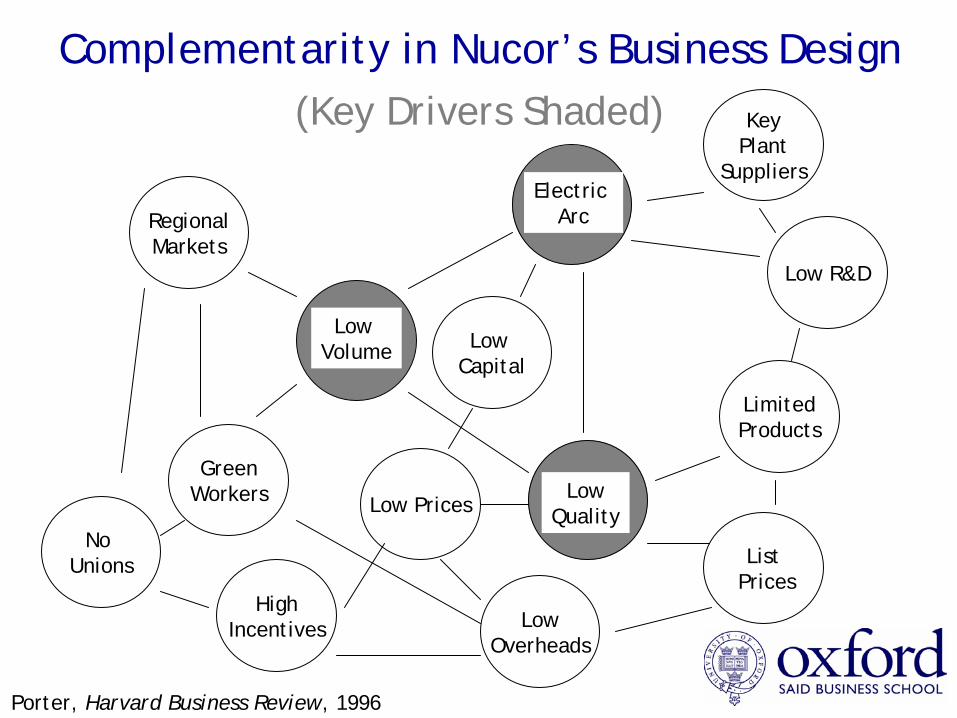

Complementarity in Nucor’s Business Design

Electric Arc

Low Volume

LowQuality

GreenWorkers

RegionalMarkets

Low R&D

KeyPlant

Suppliers

LowOverheads

HighIncentives

Low Prices

No Unions

Low Capital

ListPrices

LimitedProducts

Porter, Harvard Business Review, 1996

(Key Drivers Shaded)

Which Matters More: External or Internal?

0102030405060708090

100

EmergentHi-Perf

EmergentLo-Perf

SustainedHi-Perf

SustainedLo-Perf

IndustryBusiness

Percent abnormal profit explained by industry or businessspecific effects, 12,000 business units, 1982-1995:

relative, non-additive

% Explained Abnormal Profits

Adapted from: McGahan and Porter, Strategic Organization, 2003

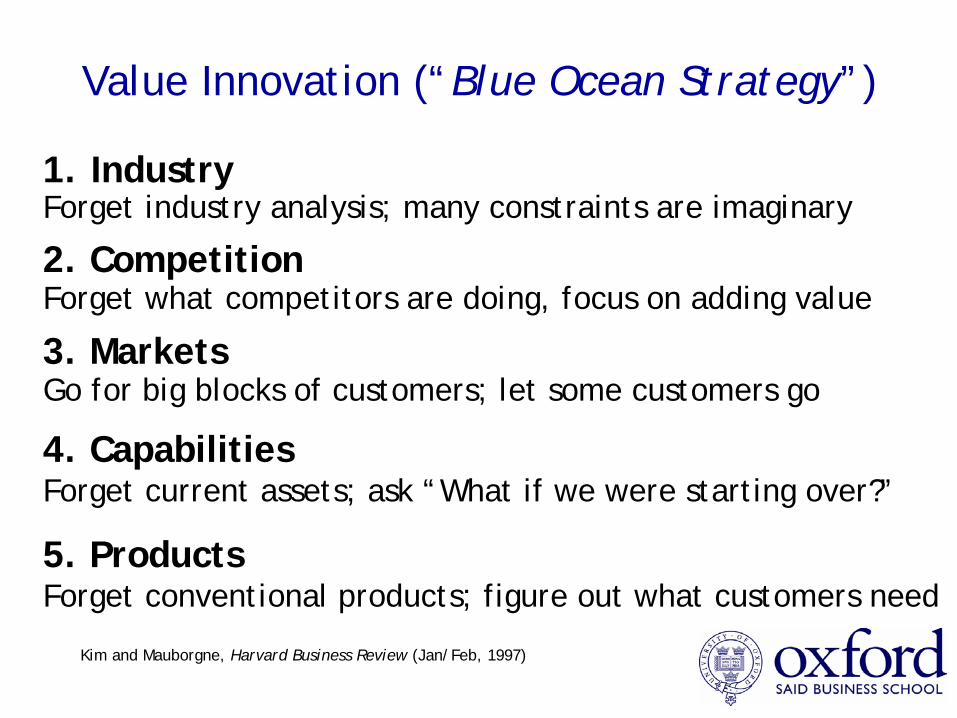

Value Innovation (“Blue Ocean Strategy”)

1. IndustryForget industry analysis; many constraints are imaginary

2. CompetitionForget what competitors are doing, focus on adding value

3. MarketsGo for big blocks of customers; let some customers go

4. CapabilitiesForget current assets; ask “What if we were starting over?”

5. ProductsForget conventional products; figure out what customers need

Kim and Mauborgne, Harvard Business Review (Jan/Feb, 1997)

Value Curve for a “Blue Ocean Strategy”

Din

ing

Aest

heti

cs

Loun

ge

Room

siz

e

Avai

labl

ere

cept

ion

Furn

ishi

ngs

Bed

qual

ity

Hyg

iene

Qui

et r

oom

Pric

e

Low

Hig

h

One-star hotel

Two-star hotel

Blue Ocean

Kim and Mauborgne, Harvard Business Review (Jan/Feb, 1997)

Is Performance Entirely Due to Competitive Advantages?

Is There Any Way to Achieve Sustained Performance Beyond Competitive Position, Resource

Advantages, and Industry Forces?

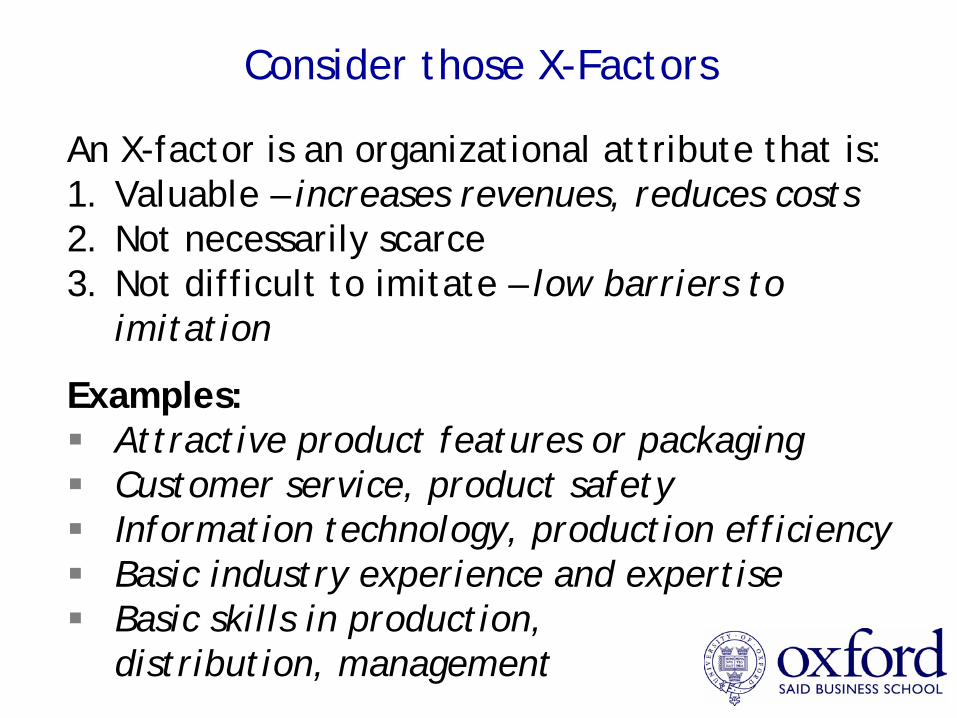

Consider those X-Factors

An X-factor is an organizational attribute that is:1. Valuable – increases revenues, reduces costs2. Not necessarily scarce3. Not difficult to imitate – low barriers to

imitation

Examples:Attractive product features or packagingCustomer service, product safetyInformation technology, production efficiencyBasic industry experience and expertiseBasic skills in production, distribution, management

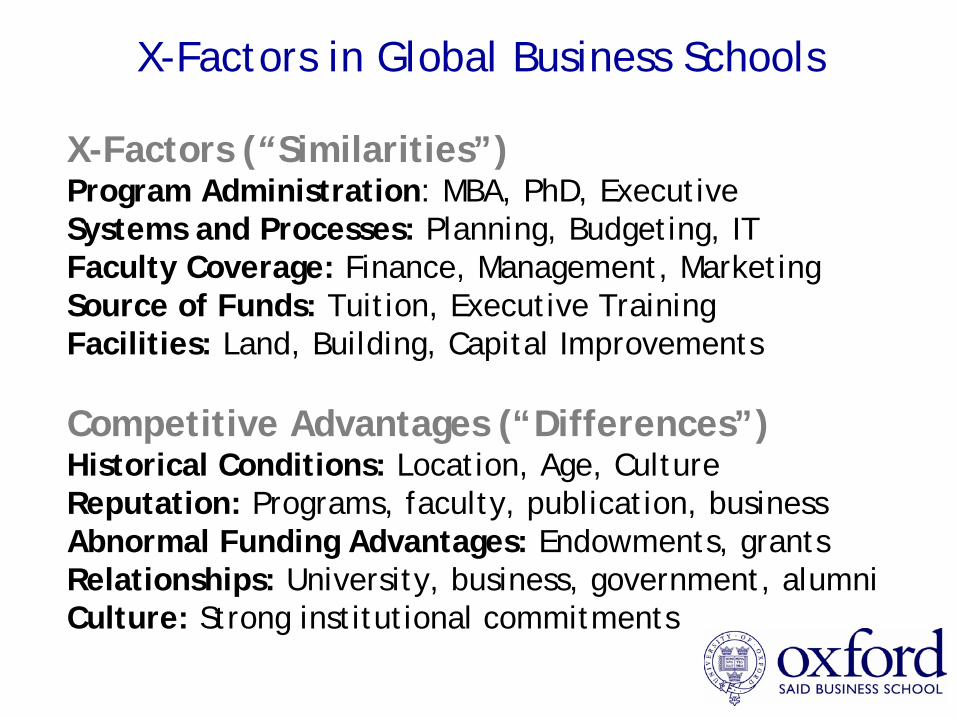

X-Factors in Global Business Schools

X-Factors (“Similarities”)Program Administration: MBA, PhD, Executive Systems and Processes: Planning, Budgeting, IT Faculty Coverage: Finance, Management, MarketingSource of Funds: Tuition, Executive TrainingFacilities: Land, Building, Capital Improvements

Competitive Advantages (“Differences”)Historical Conditions: Location, Age, CultureReputation: Programs, faculty, publication, businessAbnormal Funding Advantages: Endowments, grantsRelationships: University, business, government, alumniCulture: Strong institutional commitments

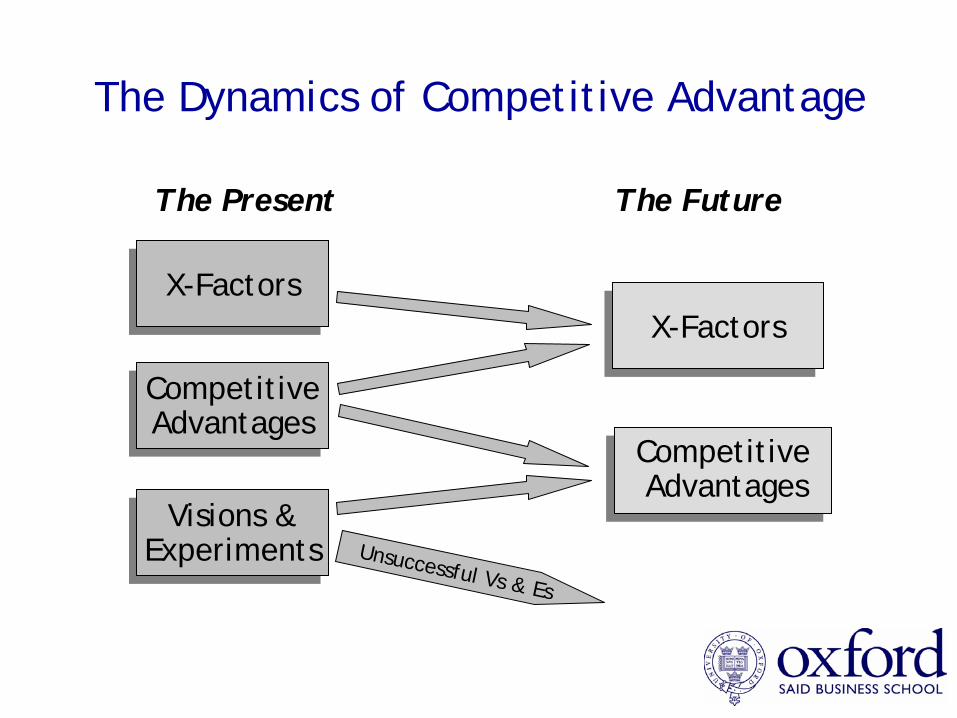

The Dynamics of Competitive Advantage

CompetitiveAdvantagesCompetitiveAdvantages

X-FactorsX-Factors

The Present The Future

CompetitiveAdvantages

Unsuccessful Vs & Es

X-FactorsX-Factors

Visions &Experiments

Visions &Experiments

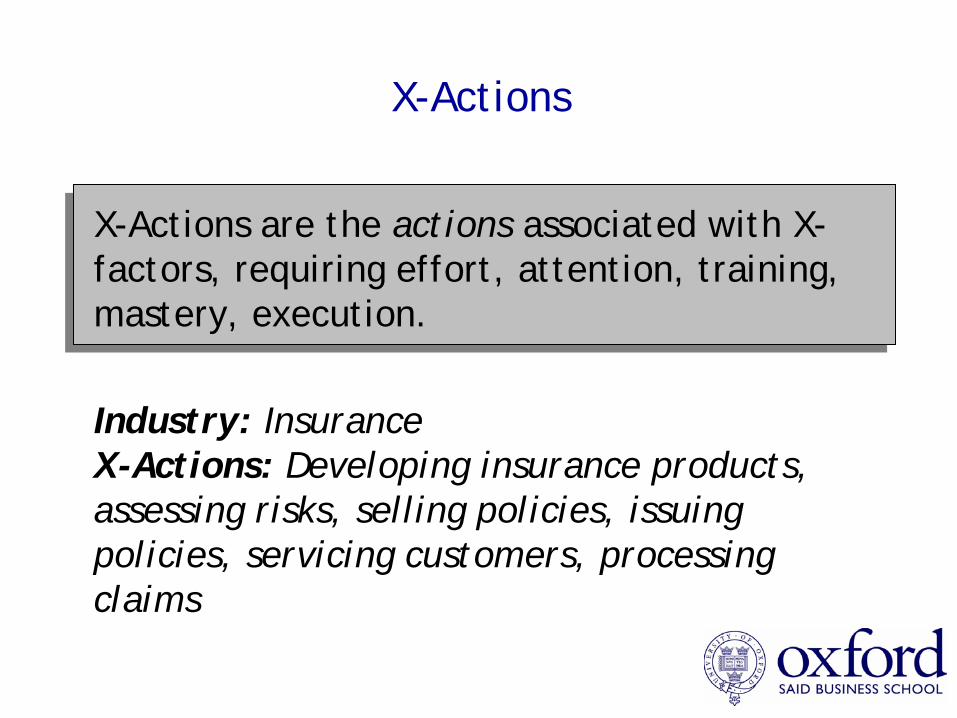

X-Actions

X-Actions are the actions associated with X- factors, requiring effort, attention, training, mastery, execution.

Industry: InsuranceX-Actions: Developing insurance products, assessing risks, selling policies, issuing policies, servicing customers, processing claims

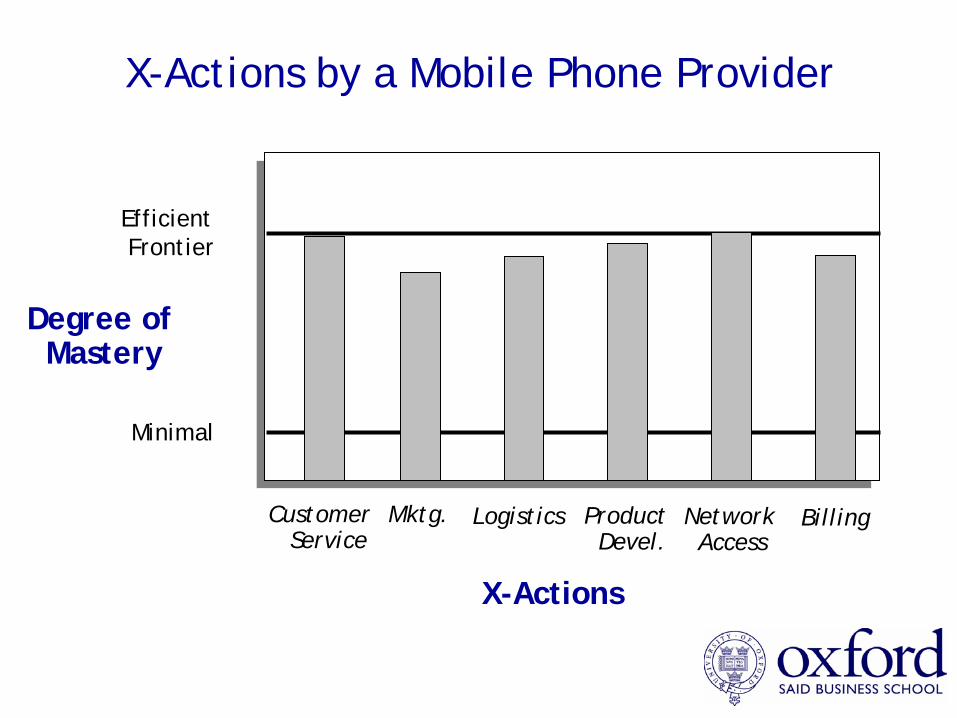

X-Actions by a Mobile Phone Provider

CustomerService

Mktg. Logistics ProductDevel.

NetworkAccess

X-Actions

Degree of Mastery

Minimal

Billing

EfficientFrontier

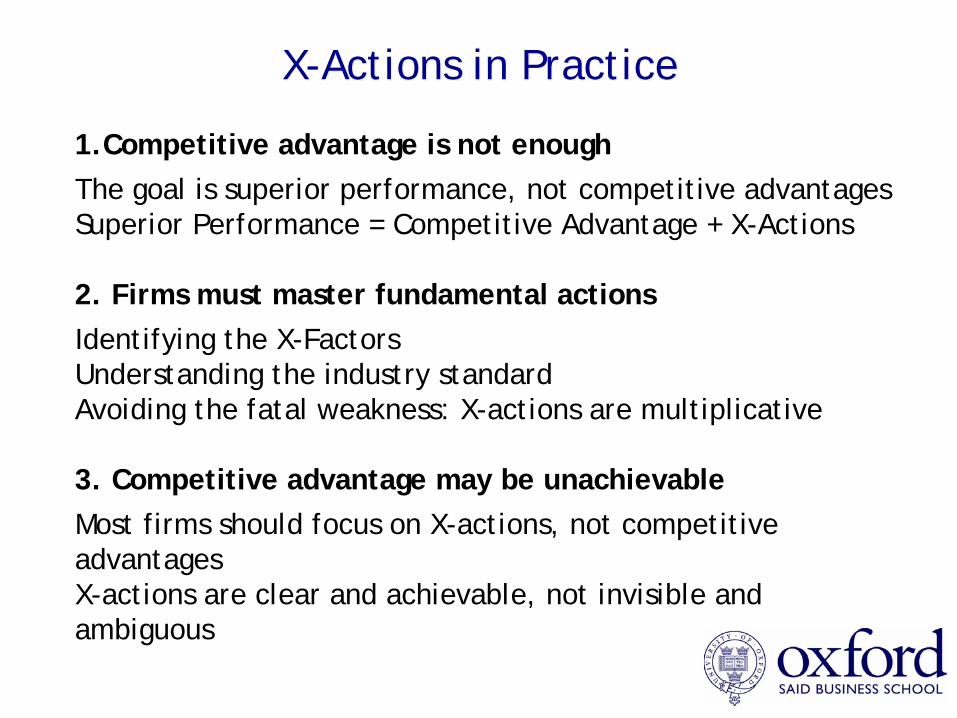

X-Actions in Practice

1.Competitive advantage is not enoughThe goal is superior performance, not competitive advantagesSuperior Performance = Competitive Advantage + X-Actions

2. Firms must master fundamental actions Identifying the X-Factors Understanding the industry standard Avoiding the fatal weakness: X-actions are multiplicative

3. Competitive advantage may be unachievableMost firms should focus on X-actions, not competitive advantages X-actions are clear and achievable, not invisible and ambiguous

How to Explain the Success of the Ipod?

‘The iPod family of digital media players keeps growing in sophistication and popularity. It's also growing more profitable for Apple with each passing revision to the product, says market research firm iSuppli.

iSuppli took apart the 4-GB version of the nano and estimated that the materials inside cost $72.24. That's a drop of more than $17 compared with what Apple paid for the guts of a 2-GB version of the first iPod nano device.

Apple saved money by eliminating a chip called flash disk controller, which it used to purchase from Silicon Storage Technologies (SSTI ). That functionality is now built right into Samsung's SOC.

Apple has nipped and tucked even on such low-end components as transistors and diodes. “These used to cost $3.71 in the old nano, but we estimate the cost has come down to $1.85,” Crotty says. “It may not sound like much, but when you think that Apple sells millions of these things, it really adds up.”’ Business Week, 20 September 2006

Firm Performance and Managerial Control

Impact on Performance

Controllability

Low

High

Low

CompetitivePosition

Resource- Based

Advantages

X-Actions

IndustryForces

High

What Causes Superior Performance?

C PShareholder returnsTotal profitProfit rates (ROA, ROE)Market shareGrowth rateMarket capitalizationEmploymentSocietal contributionEtc.

Michael PorterProduct PositionMarket PositionCost Position

Resource-Based ViewResourcesCapabilities Other Intangibles

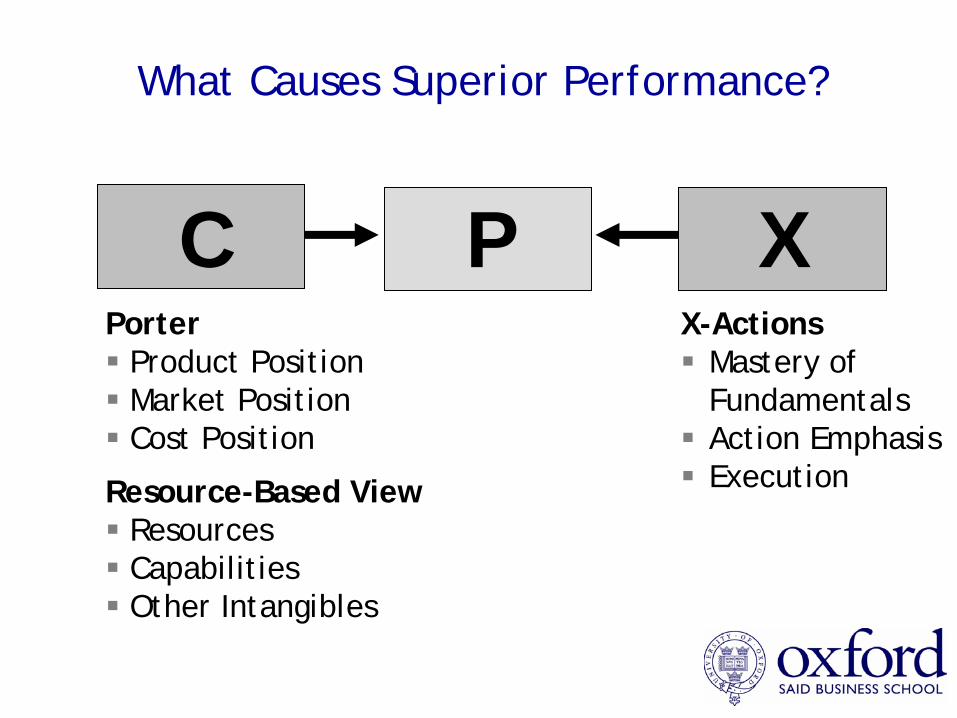

What Causes Superior Performance?

CX-Actions

Mastery ofFundamentalsAction EmphasisExecution

PorterProduct PositionMarket PositionCost Position

Resource-Based ViewResourcesCapabilitiesOther Intangibles

P X

Key Concepts & Techniques

Competitive Positioning

Resource-Based Advantage

Value Innovation

X-Factors

Industry Analysis

Christopher McKenna

MBAStrategy: Session Three

Michaelmas 2006

Outline for This Session

Industry Structure (Five Forces)

Key Success Factors

Value Chain

Profit Pools

Value Net

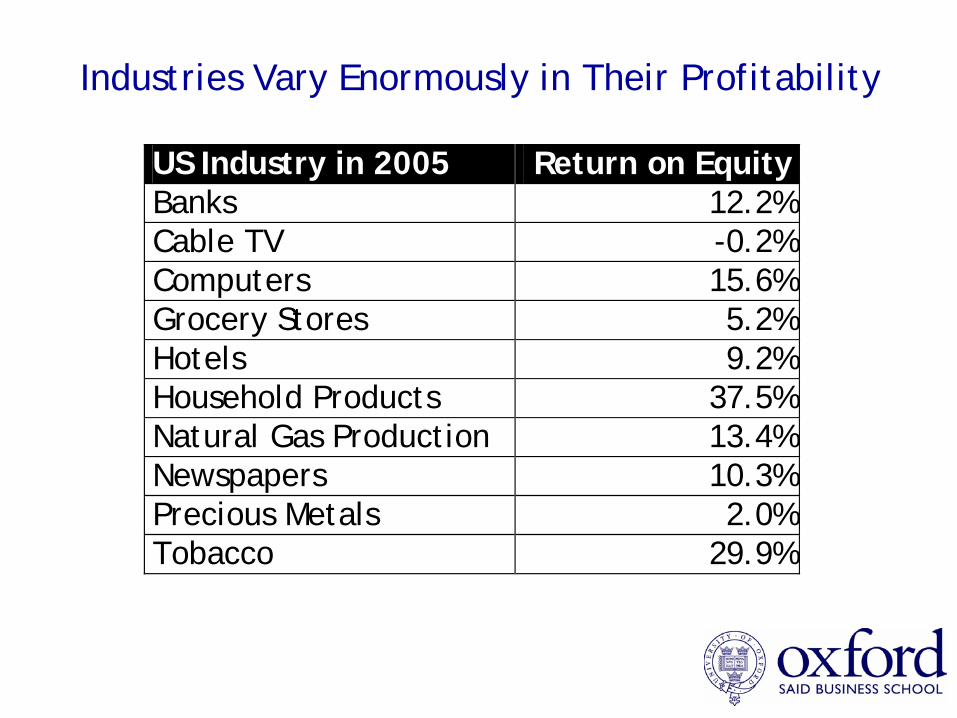

US Industry in 2005 Return on Equity Banks 12.2% Cable TV -0.2% Computers 15.6% Grocery Stores 5.2% Hotels 9.2% Household Products 37.5% Natural Gas Production 13.4% Newspapers 10.3% Precious Metals 2.0% Tobacco 29.9%

Industries Vary Enormously in Their Profitability

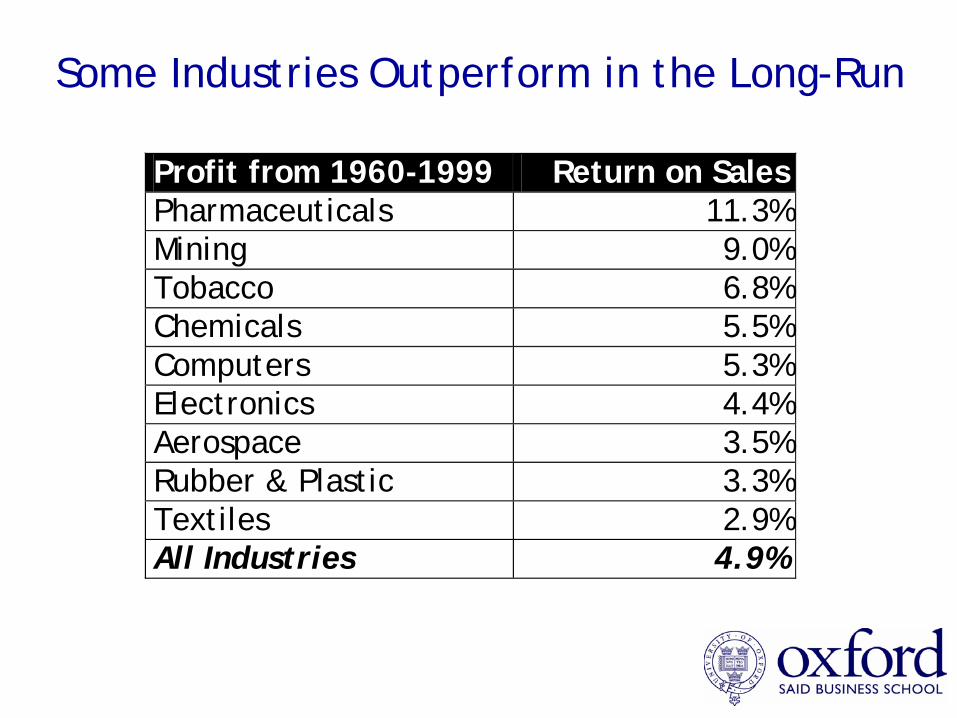

Some Industries Outperform in the Long-Run

Profit from 1960-1999 Return on Sales Pharmaceuticals 11.3% Mining 9.0% Tobacco 6.8% Chemicals 5.5% Computers 5.3% Electronics 4.4% Aerospace 3.5% Rubber & Plastic 3.3% Textiles 2.9% All Industries 4.9%

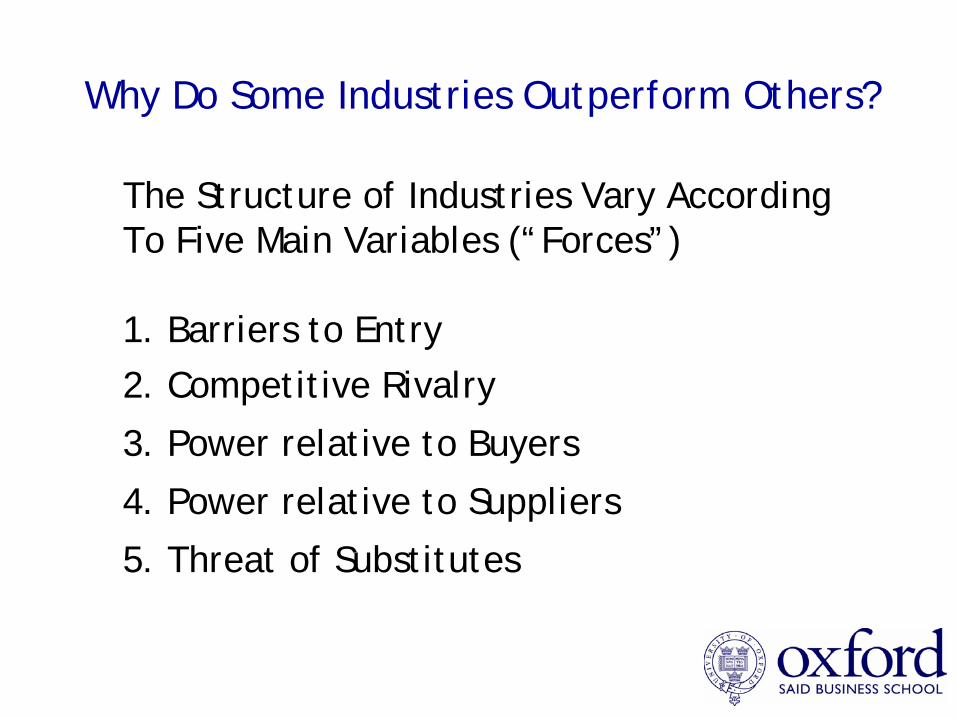

Why Do Some Industries Outperform Others?

The Structure of Industries Vary AccordingTo Five Main Variables (“Forces”)

1. Barriers to Entry2. Competitive Rivalry

3. Power relative to Buyers

4. Power relative to Suppliers

5. Threat of Substitutes

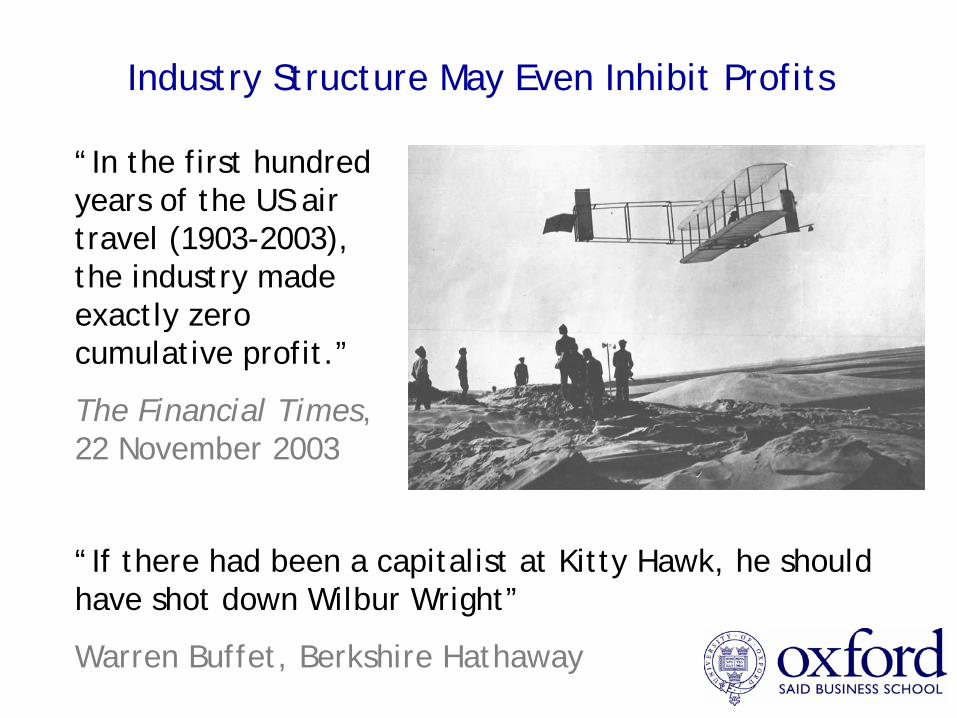

“In the first hundred years of the US air travel (1903-2003), the industry made exactly zero cumulative profit.”

The Financial Times, 22 November 2003

Industry Structure May Even Inhibit Profits

“If there had been a capitalist at Kitty Hawk, he should have shot down Wilbur Wright”

Warren Buffet, Berkshire Hathaway

Industry Structure Analysis

The Analysis of Profit Potential in an Industry

Is this a good industry to be in?

Why is it a good industry and will this change?

How can we manage this change?

Remember, as Karl Marx famously said:

“One capitalist kills many”

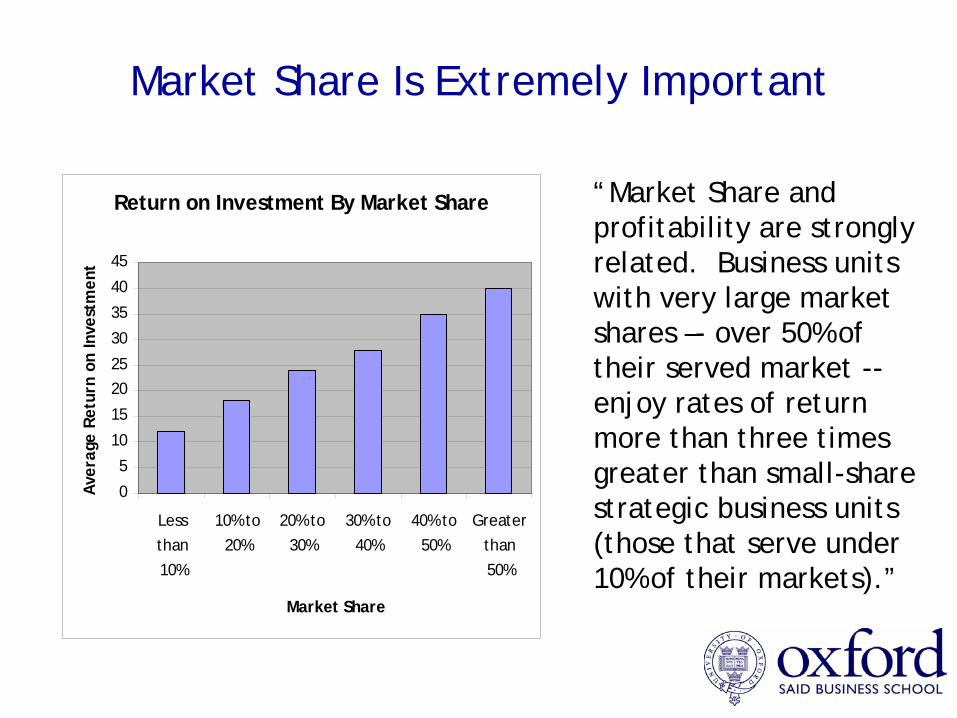

Market Share Is Extremely Important

Return on Investment By Market Share

0

5

10

15

2025

30

35

40

45

Lessthan10%

10% to20%

20% to30%

30% to40%

40% to50%

Greaterthan50%

Market Share

Aver

age

Ret

urn

on In

vest

men

t

“Market Share and profitability are strongly related. Business units with very large market shares –- over 50% of their served market -- enjoy rates of return more than three times greater than small-share strategic business units (those that serve under 10% of their markets).”

Market Share: The Top Prizes Available

Market Leader Market Share

PC Operating Systems Microsoft 96%

HIV Drugs GSK 45%

Diapers Kimberley-Clark 45% (North America)

Soft Drinks Coca-Cola 44% (North America)

Mobile Phones Nokia 39%

Databases IBM 36%

Servers IBM 30%

CDs Universal 30% (North America)

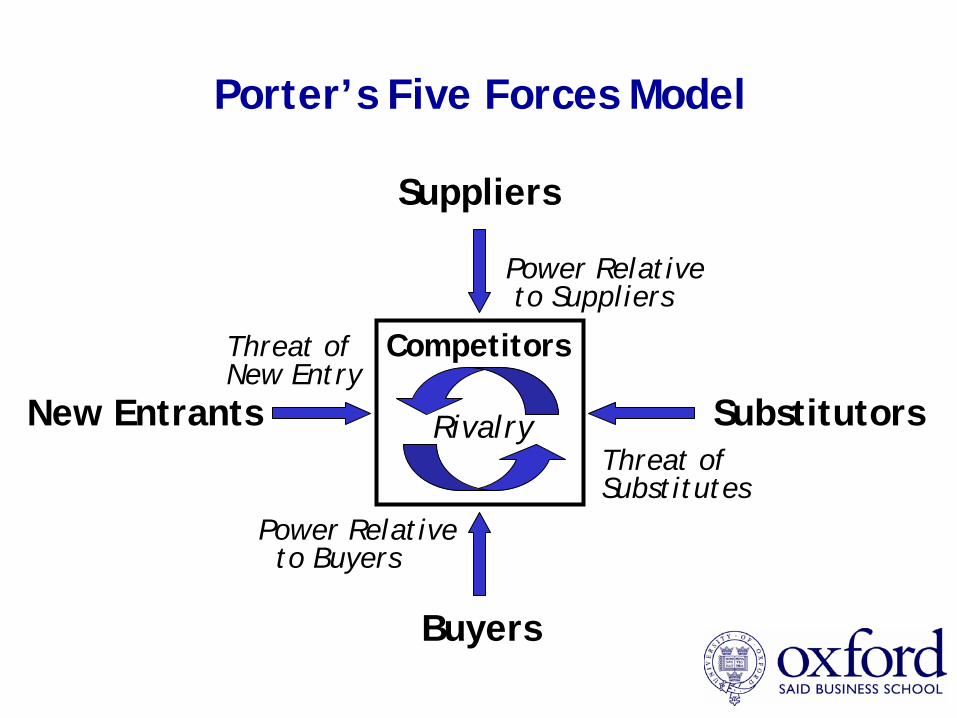

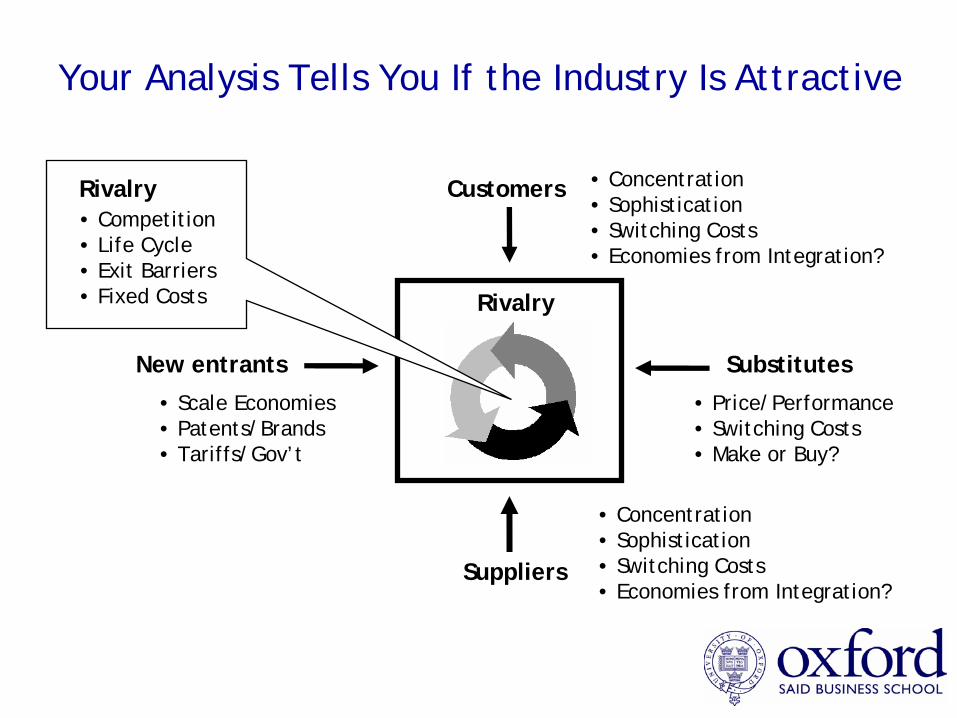

Porter’s Five Forces Model

Competitors

Buyers

Suppliers

New Entrants Substitutors

Power Relative to Suppliers

Power Relative to Buyers

Threat of Substitutes

Threat of New Entry

Rivalry

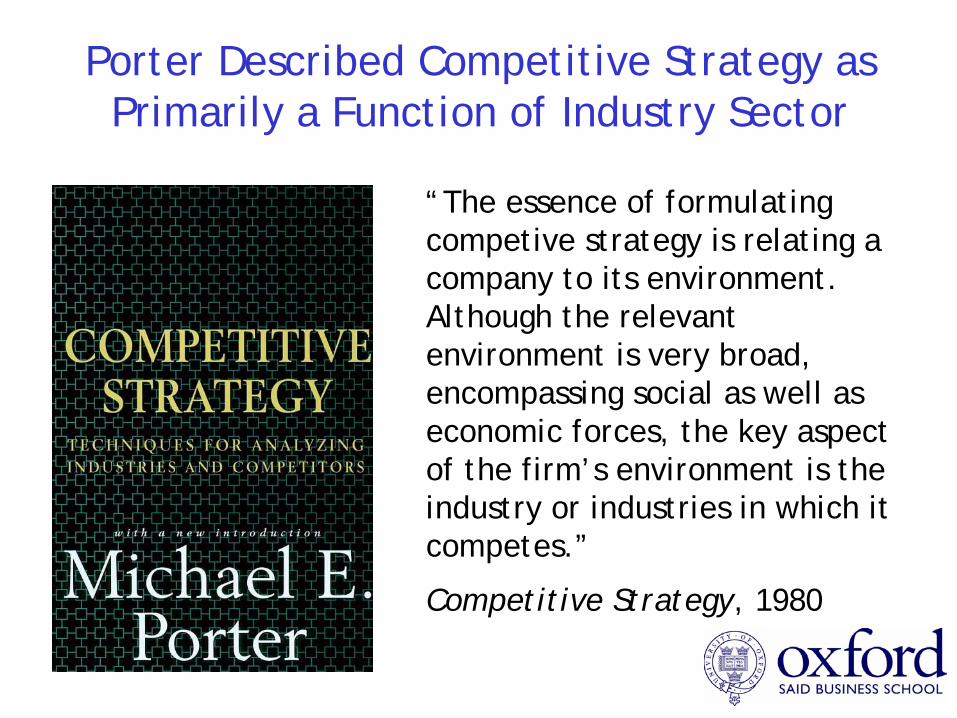

Porter Described Competitive Strategy as Primarily a Function of Industry Sector

“The essence of formulating competive strategy is relating a company to its environment. Although the relevant environment is very broad, encompassing social as well as economic forces, the key aspect of the firm’s environment is the industry or industries in which it competes.”

Competitive Strategy, 1980

Rivalry

Customers

Substitutes

Suppliers

New entrants

• Scale Economies• Patents/Brands• Tariffs/Gov’t

• Price/Performance• Switching Costs• Make or Buy?

• Concentration• Sophistication• Switching Costs• Economies from Integration?

• Concentration• Sophistication• Switching Costs• Economies from Integration?

Your Analysis Tells You If the Industry Is Attractive

Rivalry• Competition• Life Cycle• Exit Barriers• Fixed Costs

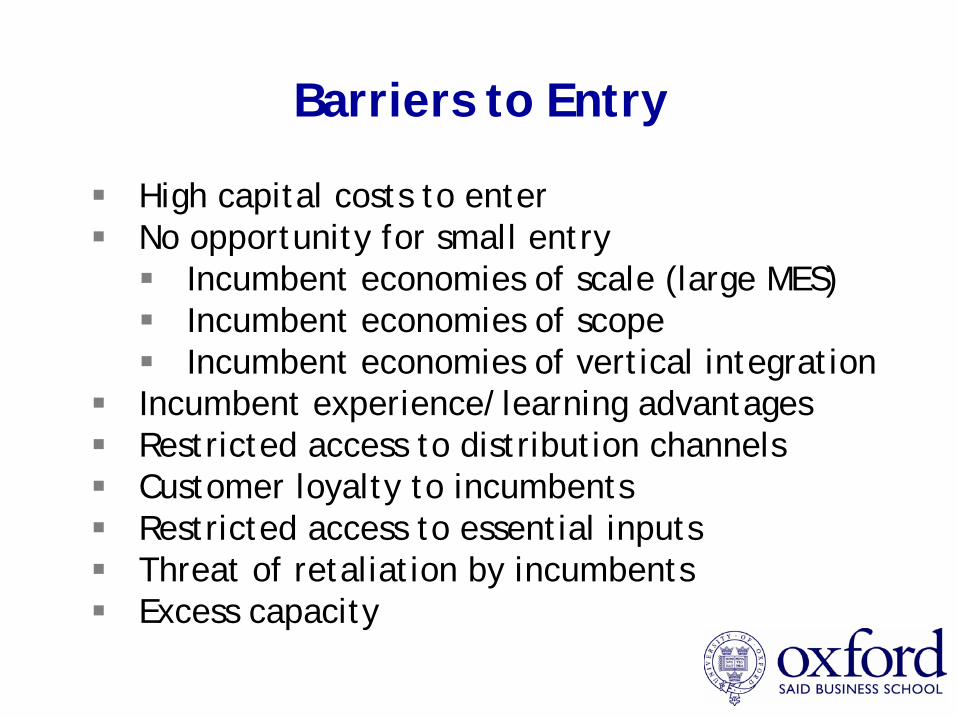

Barriers to Entry

High capital costs to enterNo opportunity for small entry

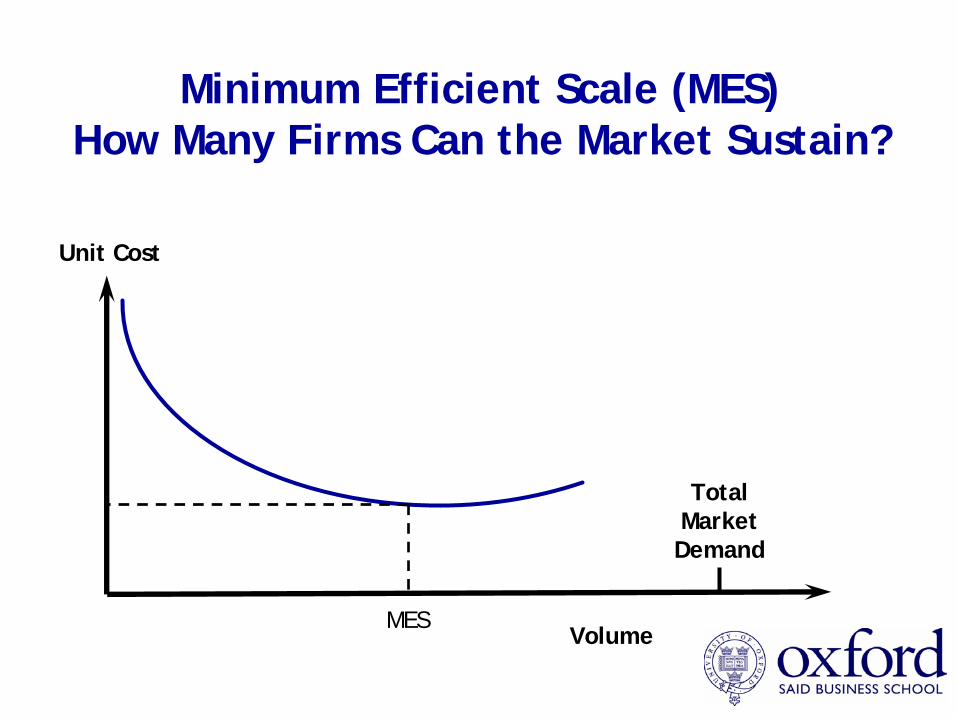

Incumbent economies of scale (large MES)Incumbent economies of scopeIncumbent economies of vertical integration

Incumbent experience/learning advantagesRestricted access to distribution channelsCustomer loyalty to incumbents Restricted access to essential inputsThreat of retaliation by incumbentsExcess capacity

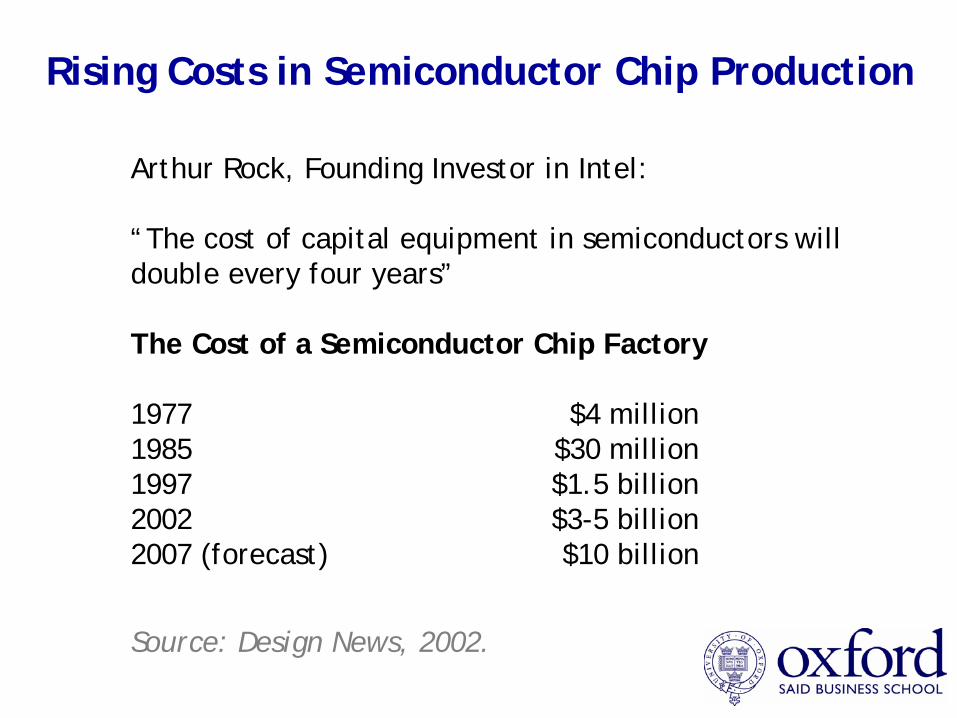

Rising Costs in Semiconductor Chip Production

Arthur Rock, Founding Investor in Intel:

“The cost of capital equipment in semiconductors will double every four years”

The Cost of a Semiconductor Chip Factory

1977 $4 million1985 $30 million1997 $1.5 billion2002 $3-5 billion2007 (forecast) $10 billion

Source: Design News, 2002.

Minimum Efficient Scale (MES)How Many Firms Can the Market Sustain?

Unit Cost

VolumeMES

Total MarketDemand

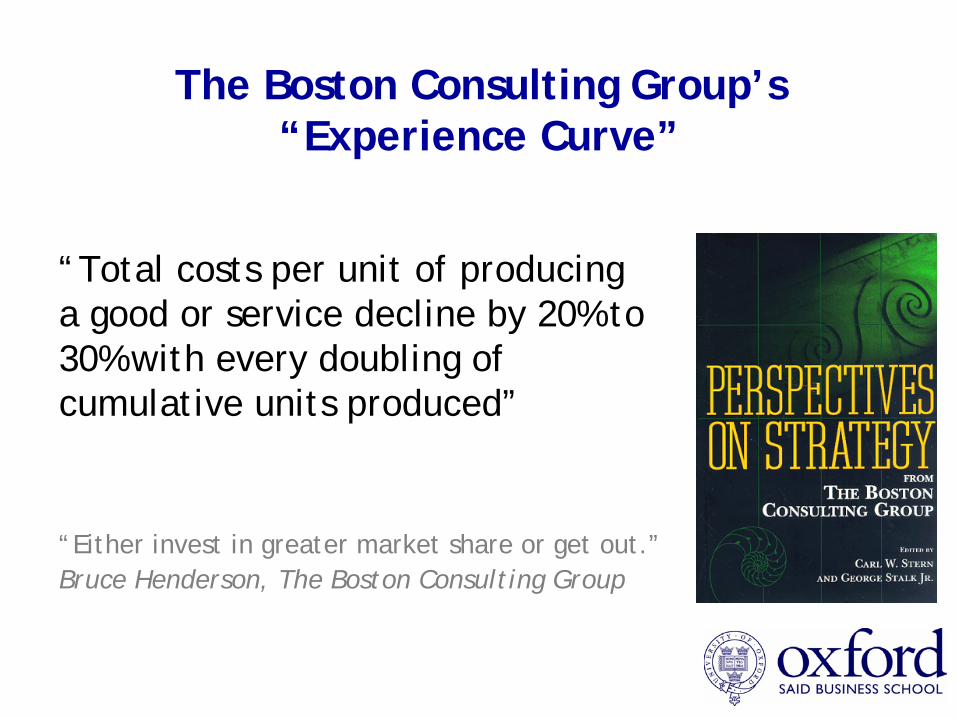

The Boston Consulting Group’s “Experience Curve”

“Either invest in greater market share or get out.”Bruce Henderson, The Boston Consulting Group

“Total costs per unit of producing a good or service decline by 20% to 30% with every doubling of cumulative units produced”

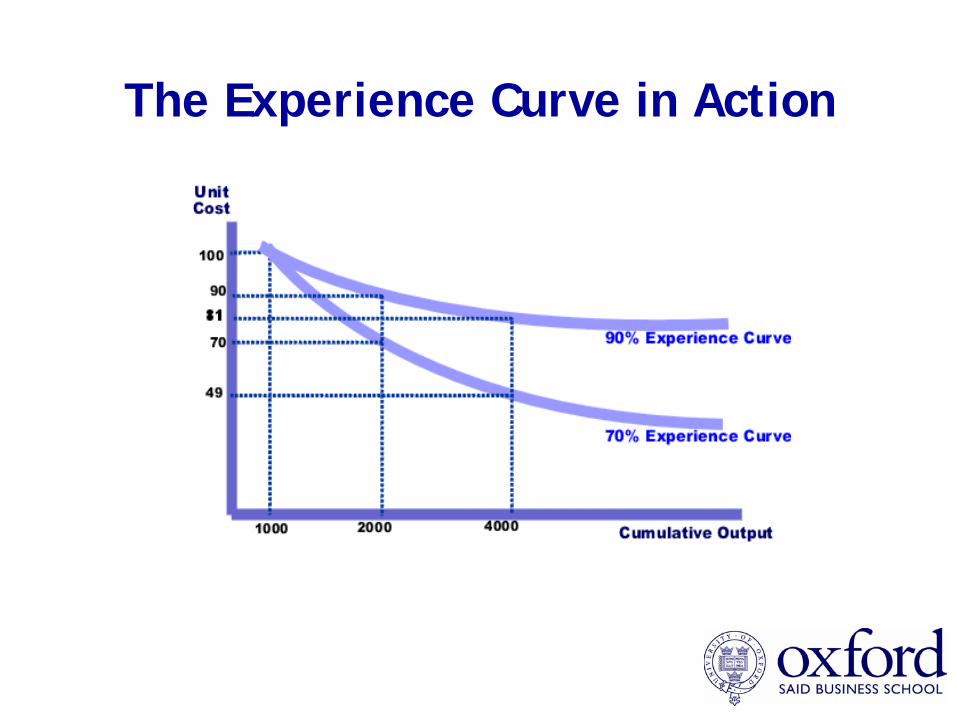

The Experience Curve in Action

Competitive Rivalry

Low industry growthCommodity products & servicesLow brand loyaltyLow switching costsExcess capacityHigh exit barriers

To What Extent Does the Industry Have?

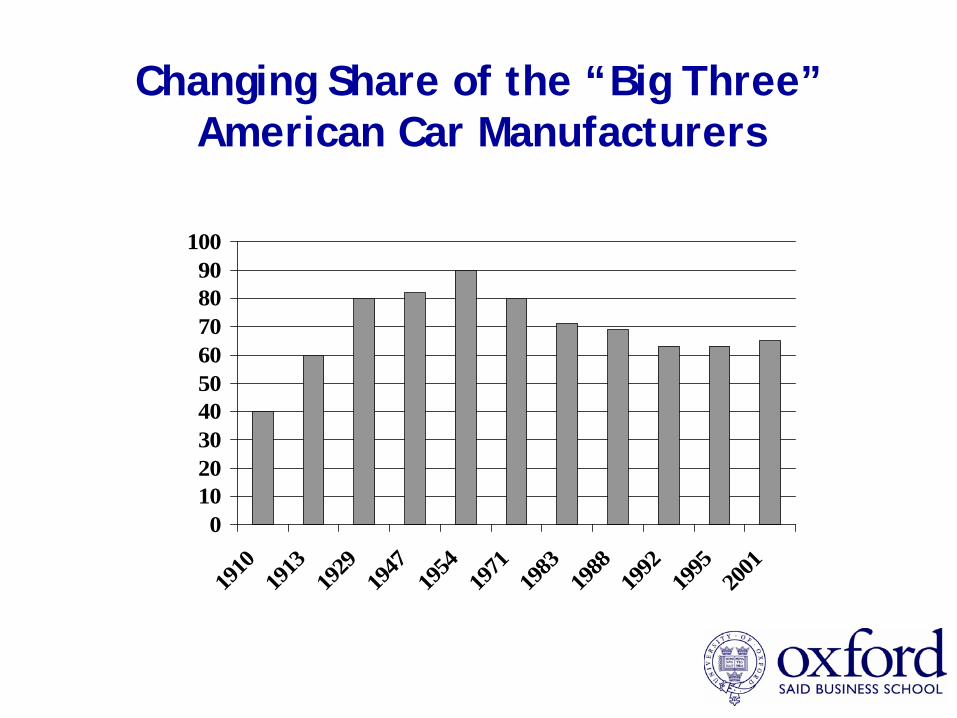

Changing Share of the “Big Three”American Car Manufacturers

0102030405060708090

100

1910

1913

1929

1947

1954

1971

1983

1988

1992

1995

2001

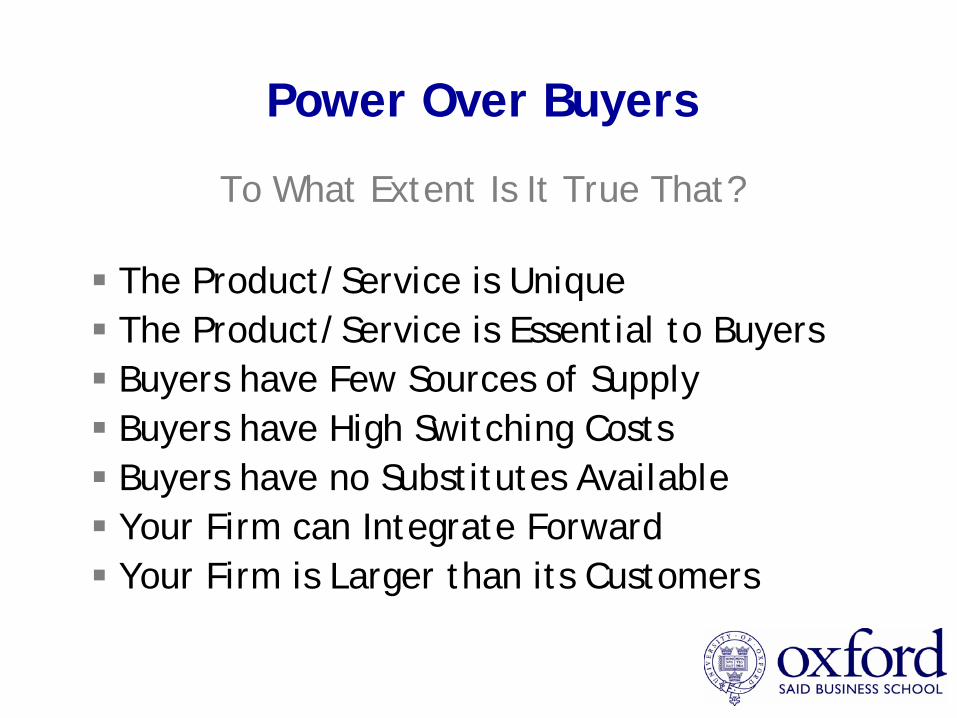

Power Over Buyers

The Product/Service is Unique The Product/Service is Essential to Buyers Buyers have Few Sources of SupplyBuyers have High Switching CostsBuyers have no Substitutes Available Your Firm can Integrate ForwardYour Firm is Larger than its Customers

To What Extent Is It True That?

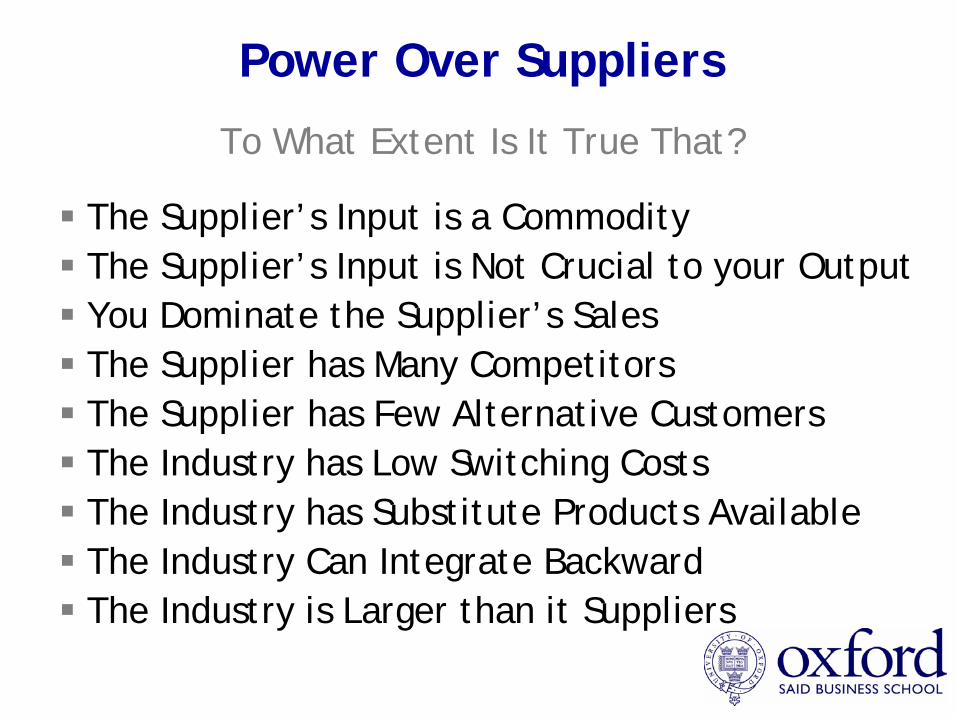

Power Over Suppliers

The Supplier’s Input is a CommodityThe Supplier’s Input is Not Crucial to your OutputYou Dominate the Supplier’s SalesThe Supplier has Many CompetitorsThe Supplier has Few Alternative CustomersThe Industry has Low Switching CostsThe Industry has Substitute Products AvailableThe Industry Can Integrate BackwardThe Industry is Larger than it Suppliers

To What Extent Is It True That?

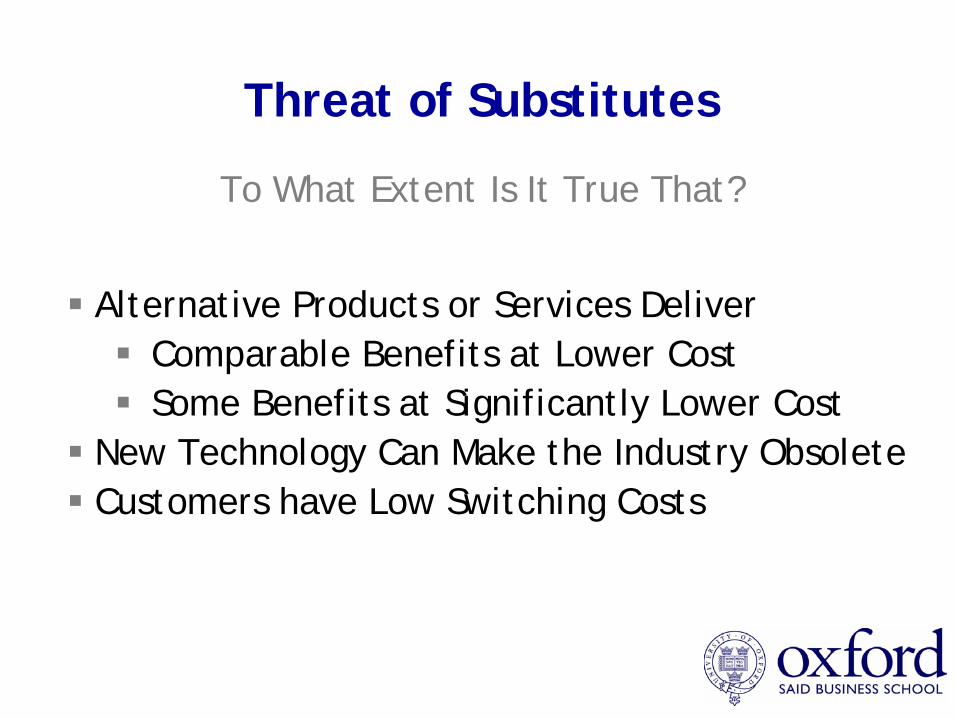

Threat of Substitutes

Alternative Products or Services DeliverComparable Benefits at Lower CostSome Benefits at Significantly Lower Cost

New Technology Can Make the Industry ObsoleteCustomers have Low Switching Costs

To What Extent Is It True That?

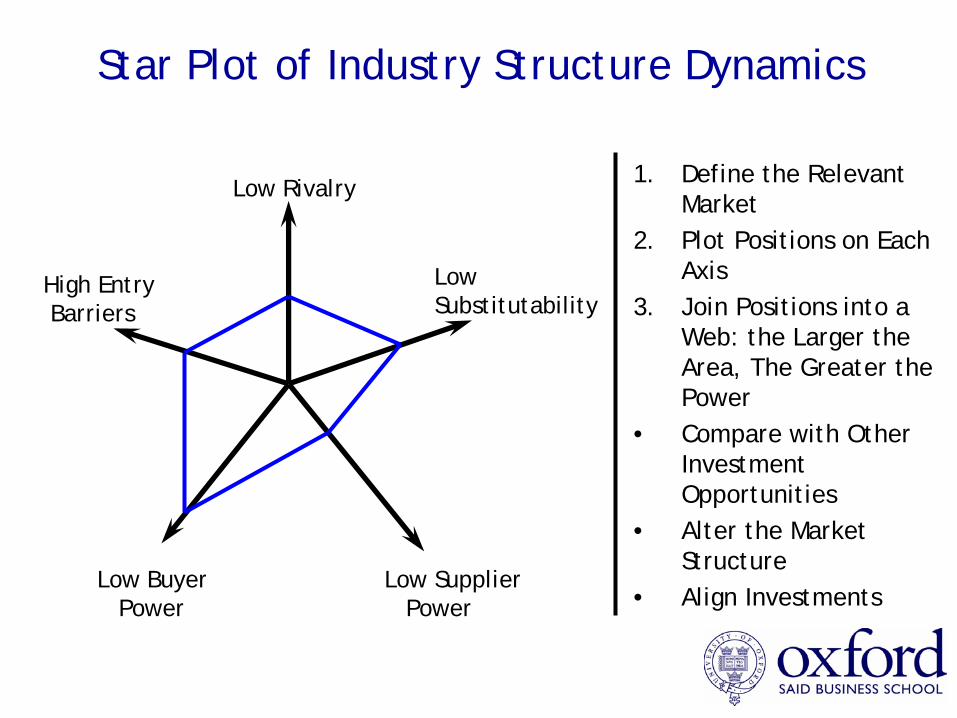

Star Plot of Industry Structure Dynamics

Low Rivalry

High EntryBarriers

LowSubstitutability

Low Buyer Power

Low SupplierPower

1. Define the Relevant Market

2. Plot Positions on Each Axis

3. Join Positions into a Web: the Larger the Area, The Greater the Power

• Compare with Other Investment Opportunities

• Alter the Market Structure

• Align Investments

Key Success Factors

Competitive ImperativesTechnological ImperativesFinancial ImperativesMarketing ImperativesOrganizational ImperativesOperational Imperatives

What Are the Requirements for Industry Success?

Global Strategy Consulting IndustryWhat Is Necessary for Success?

Competitive: Innovation, Uniqueness, Reputation

Technological: Leading-Edge Knowledge, Expertise

Financial: Capital, Pricing, Remuneration

Marketing: Products, Propositions, Customer Base

Organizational: Recruiting, Culture, Knowledge

Operational: Client Management, Global Systems

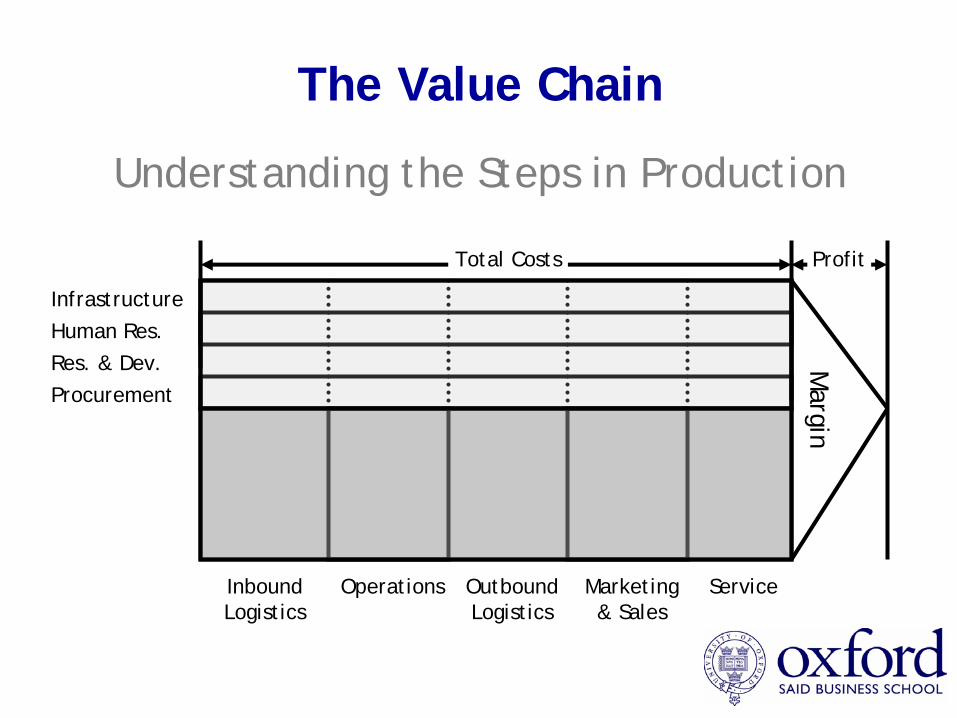

The Value Chain

Understanding the Steps in Production

InfrastructureHuman Res.Res. & Dev.Procurement

InboundLogistics

Operations OutboundLogistics

Marketing& Sales

Service

Total Costs

Margin

Profit

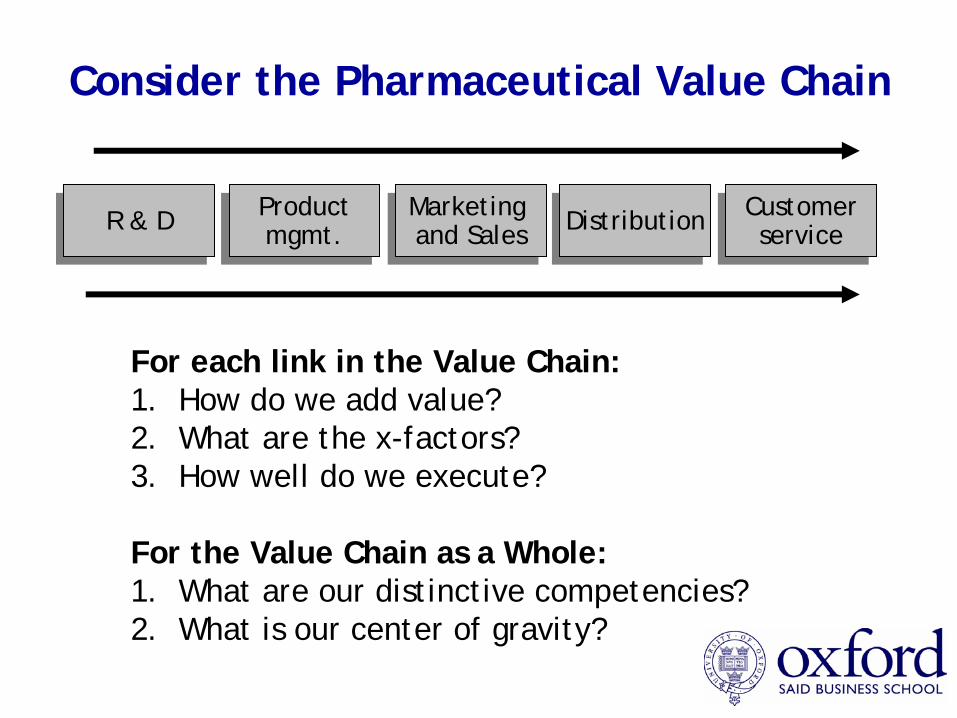

Consider the Pharmaceutical Value Chain

R & DR & D Productmgmt.Productmgmt.

Marketing and SalesMarketing and Sales DistributionDistribution Customer

serviceCustomerservice

For each link in the Value Chain:1. How do we add value?2. What are the x-factors?3. How well do we execute?

For the Value Chain as a Whole:1. What are our distinctive competencies?2. What is our center of gravity?

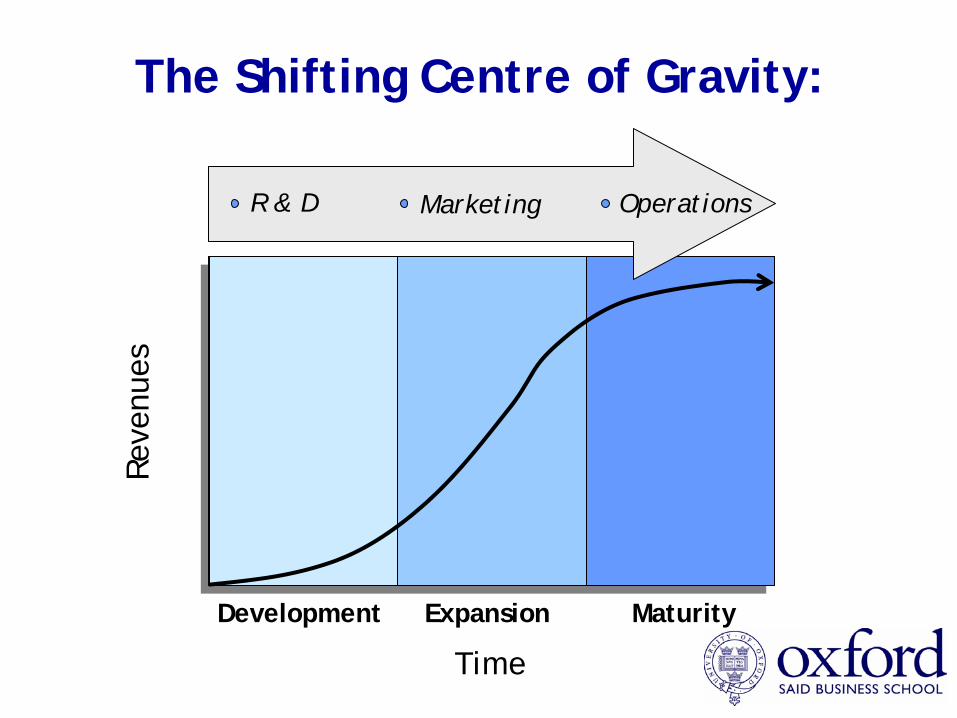

The Shifting Centre of Gravity:Re

venu

es

Time

Development MaturityExpansion

R & D Marketing Operations

Check the Revenue Along the Value Chain

Check the Profit Along the Value Chain

What is the Centre of Gravity?

Choke Points for Profitability

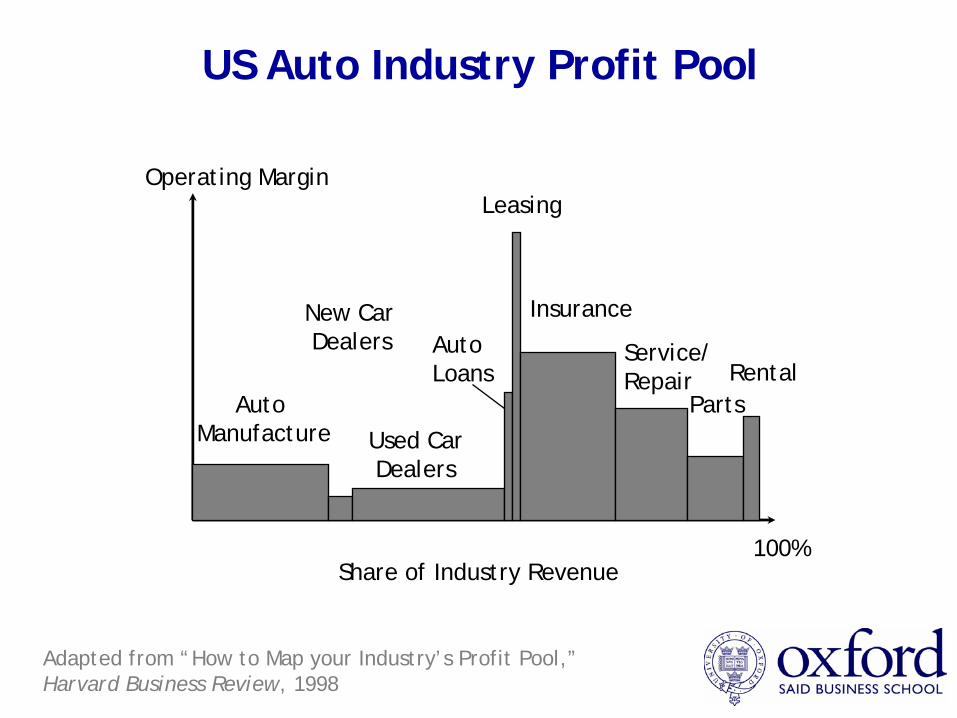

Profit Pool Analysis

US Auto Industry Profit Pool

100%

Operating Margin

Share of Industry Revenue

Auto Manufacture

New CarDealers

Used CarDealers

Auto Loans

Leasing

Insurance

Service/Repair

PartsRental

Adapted from “How to Map your Industry’s Profit Pool,”Harvard Business Review, 1998

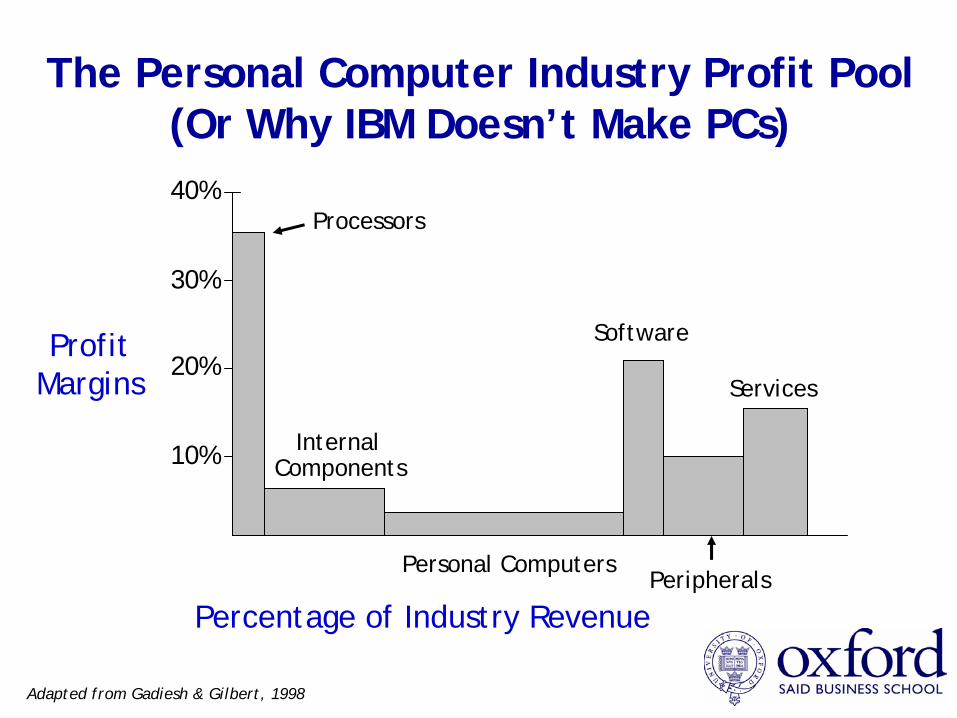

The Personal Computer Industry Profit Pool(Or Why IBM Doesn’t Make PCs)

ProfitMargins

10%

Percentage of Industry Revenue

20%

30%

40%Processors

InternalComponents

Personal Computers

Software

Peripherals

Services

Adapted from Gadiesh & Gilbert, 1998

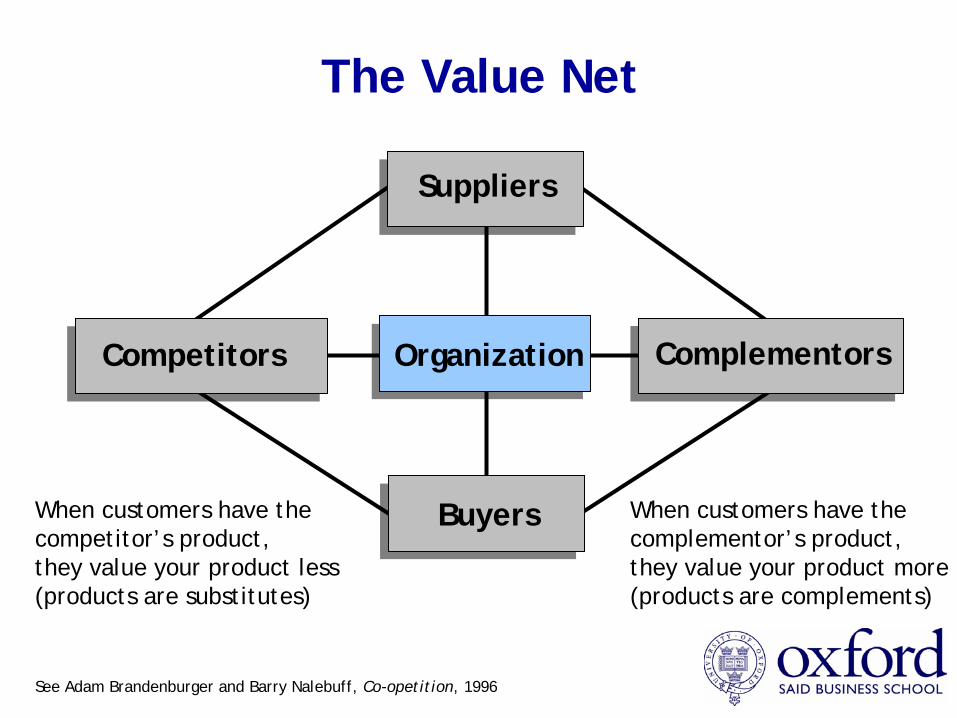

The Value Net

Organization

Buyers

Suppliers

Competitors Complementors

See Adam Brandenburger and Barry Nalebuff, Co-opetition, 1996

When customers have the complementor’s product, they value your product more(products are complements)

When customers have the competitor’s product, they value your product less(products are substitutes)

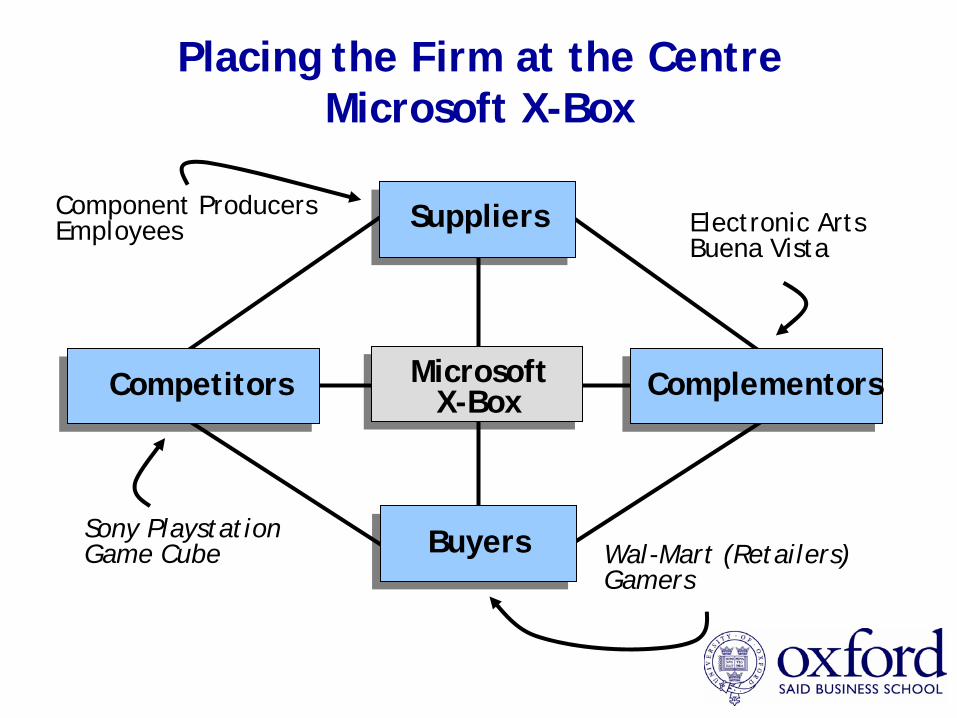

Placing the Firm at the CentreMicrosoft X-Box

MicrosoftX-Box

Buyers

Suppliers

Competitors Complementors

Component ProducersEmployees

Wal-Mart (Retailers)Gamers

Sony PlaystationGame Cube

Electronic ArtsBuena Vista

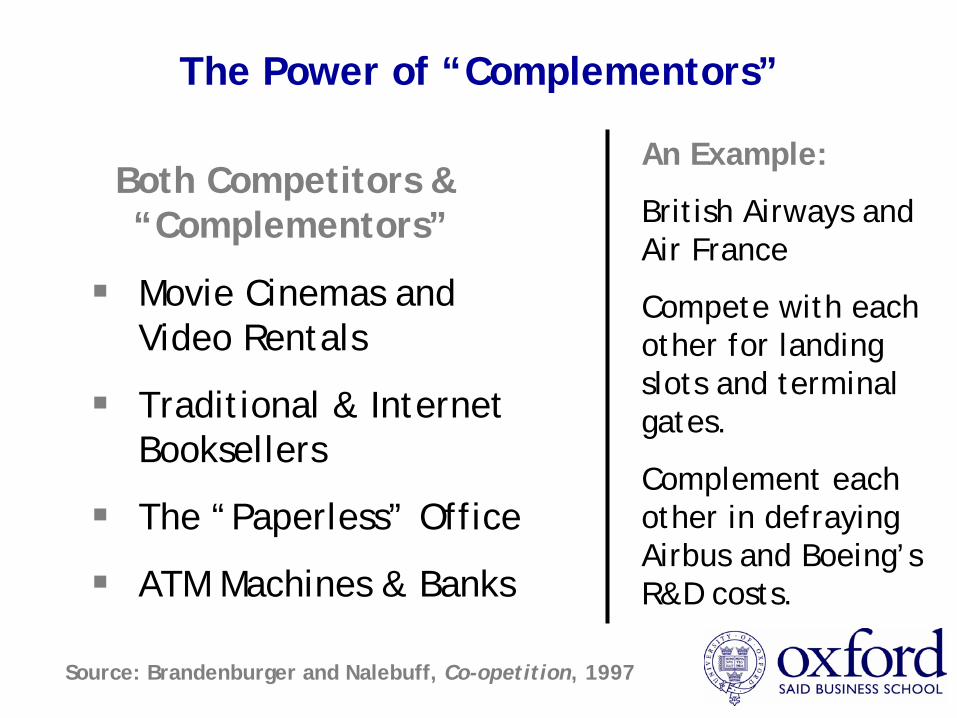

The Power of “Complementors”

An Example:

British Airways and Air France

Compete with each other for landing slots and terminal gates.

Complement each other in defraying Airbus and Boeing’s R&D costs.

Movie Cinemas and Video Rentals

Traditional & Internet Booksellers

The “Paperless” Office

ATM Machines & Banks

Both Competitors & “Complementors”

Source: Brandenburger and Nalebuff, Co-opetition, 1997

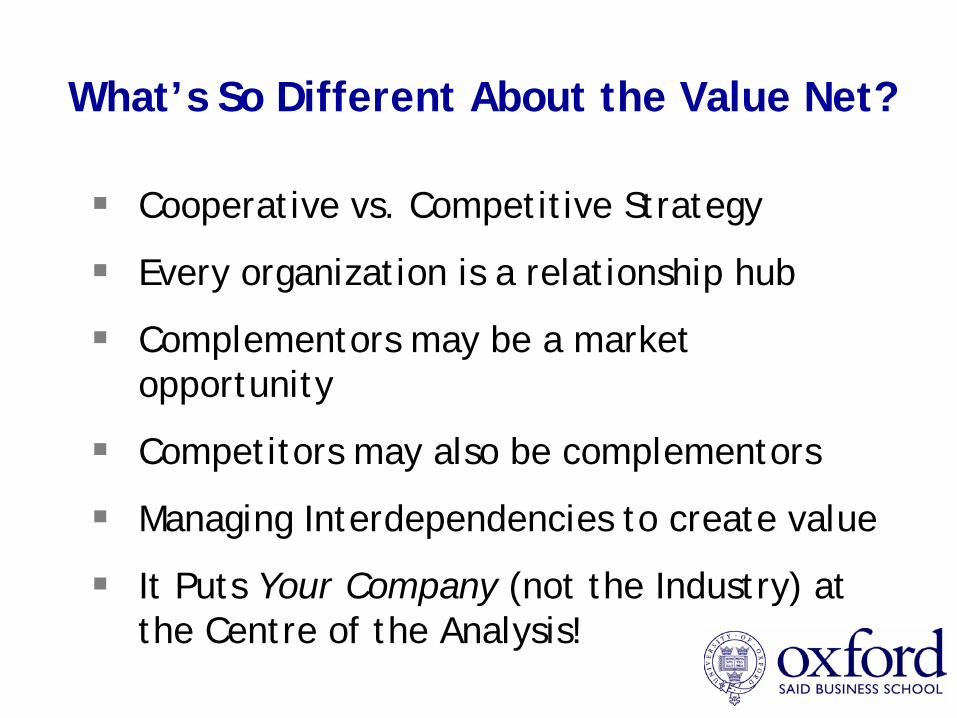

Cooperative vs. Competitive Strategy

Every organization is a relationship hub

Complementors may be a market opportunity

Competitors may also be complementors

Managing Interdependencies to create value

It Puts Your Company (not the Industry) at the Centre of the Analysis!

What’s So Different About the Value Net?

Develop Competitive AdvantagesDefine unique cost position, differentiation, market segments Cultivate firm-specific resources & capabilities

Change the Industry StructureManage the Five Forces (raise entry barriers, reduce rivalry, etc)Manage the value chain, profit pools, complementarities

Move into Attractive IndustriesManage corporate growth; the corporate portfolioDiversification strategy; merger & acquisition; synergies

How to Improve Firm Performance

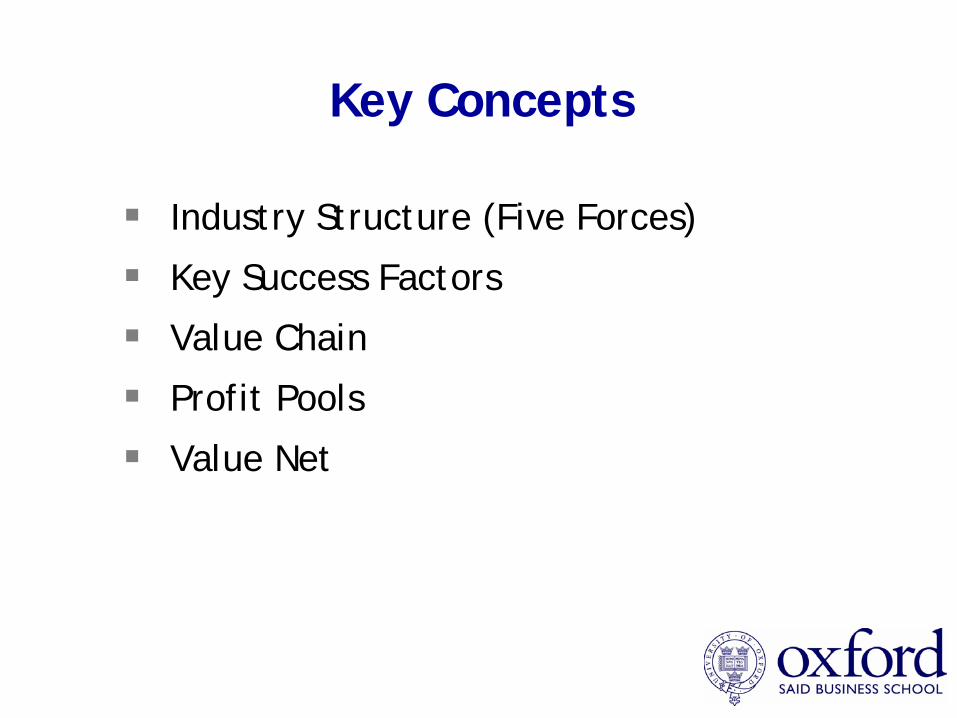

Key Concepts

Industry Structure (Five Forces)

Key Success Factors

Value Chain

Profit Pools

Value Net

Strategy & Change

Christopher McKenna

MBAStrategy: Session Four

Michaelmas 2006

Outline for This Session

Industry Life Cycle

Dominant Design

Macro-Environment (PESTLE)

Strategic Uncertainty

The Poetics of Uncertainty

“As we know, there are known knowns; these also are things we know we know.

We also know there are known unknowns; that is to say, there are some things we know we do not know.

But there are also unknown unknowns – the ones we don’t know we don’t know.”

Donald Rumsfeld, U.S. Defence Secretary, speaking in 2003, & the Winner of the Plain English Campaign’s “Foot in the Mouth Trophy.”

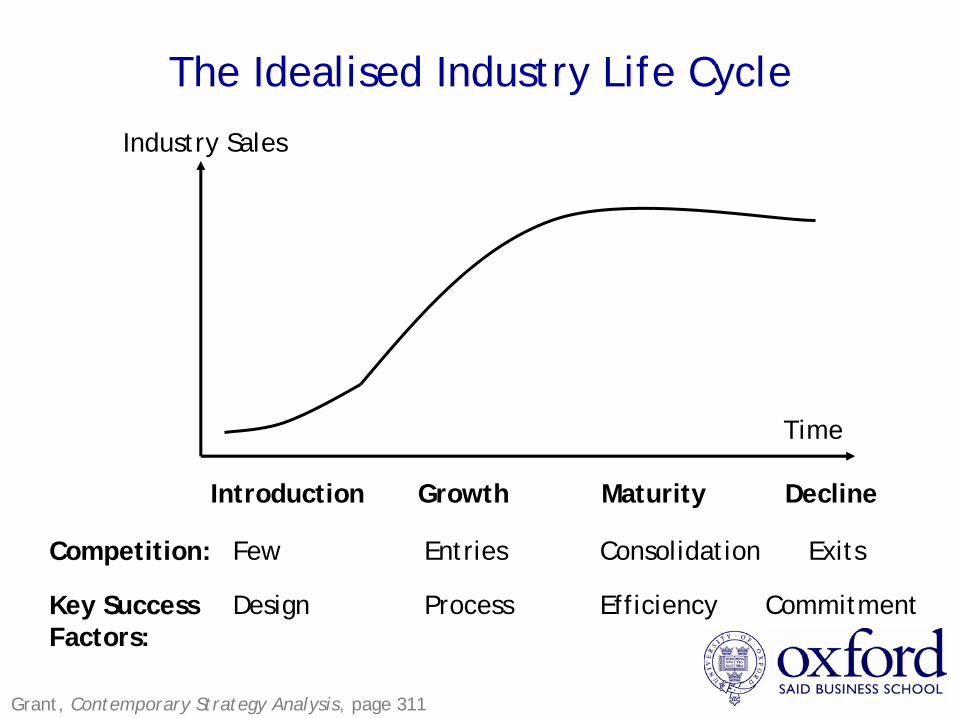

Industry Sales

Time

Competition:

Key Success Factors:

Introduction Growth Maturity Decline

The Idealised Industry Life Cycle

Grant, Contemporary Strategy Analysis, page 311

Few Entries Consolidation Exits

Design Process Efficiency Commitment

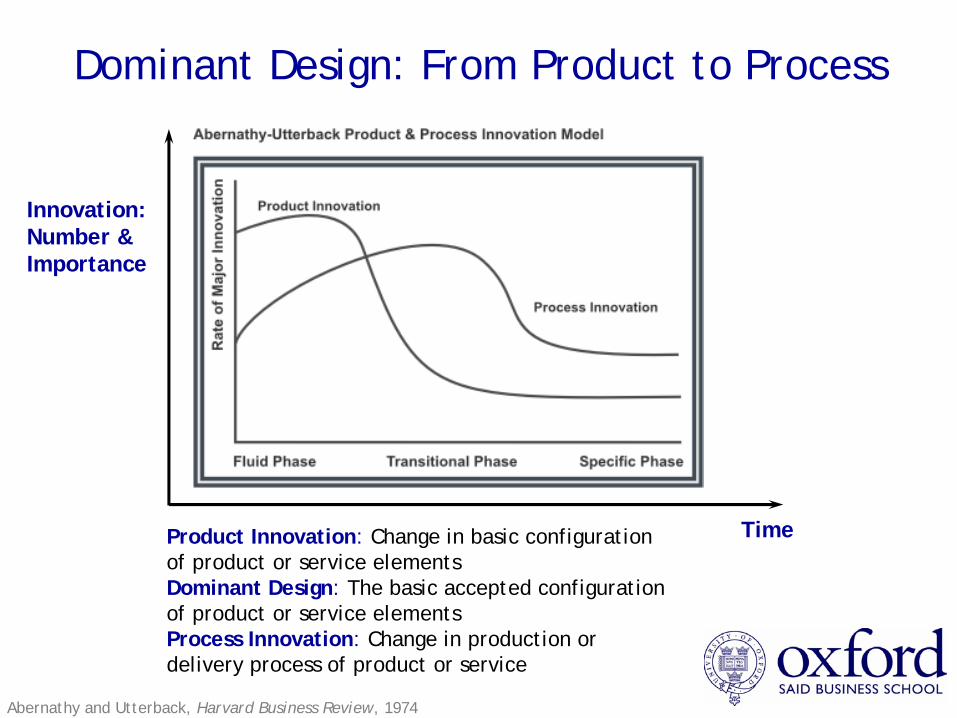

Dominant Design: From Product to Process

Time

Innovation:Number &Importance

Abernathy and Utterback, Harvard Business Review, 1974

Product Innovation: Change in basic configurationof product or service elementsDominant Design: The basic accepted configurationof product or service elements Process Innovation: Change in production or delivery process of product or service

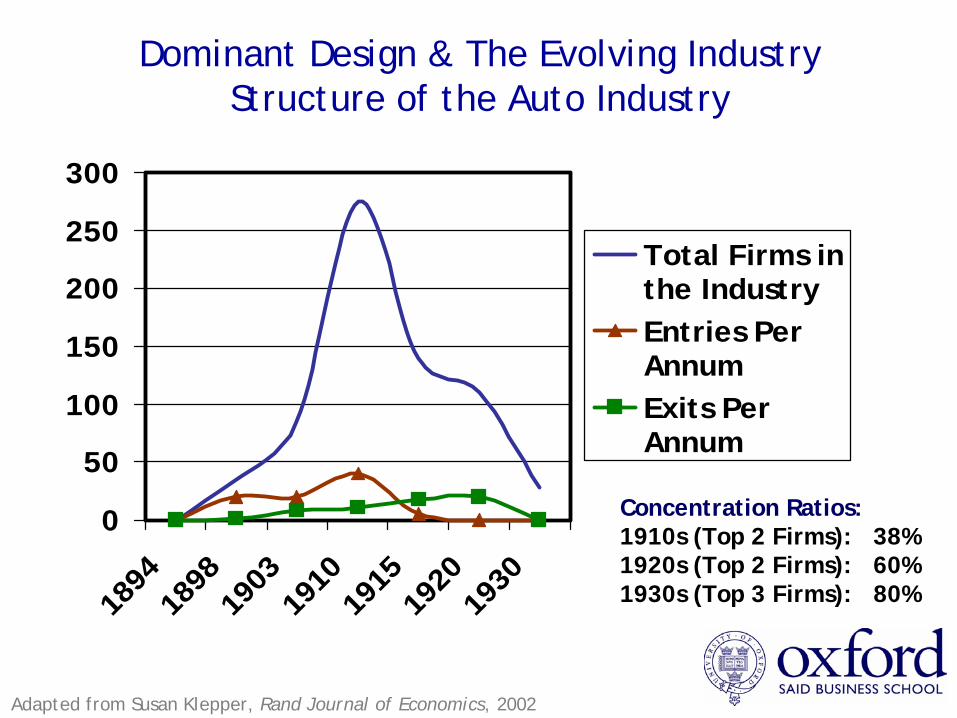

Dominant Design & The Evolving Industry Structure of the Auto Industry

0

50

100

150

200

250

300

1894

1898

1903

1910

1915

1920

1930

Total Firms inthe IndustryEntries PerAnnumExits PerAnnum

Concentration Ratios:1910s (Top 2 Firms): 38%1920s (Top 2 Firms): 60%1930s (Top 3 Firms): 80%

Adapted from Susan Klepper, Rand Journal of Economics, 2002

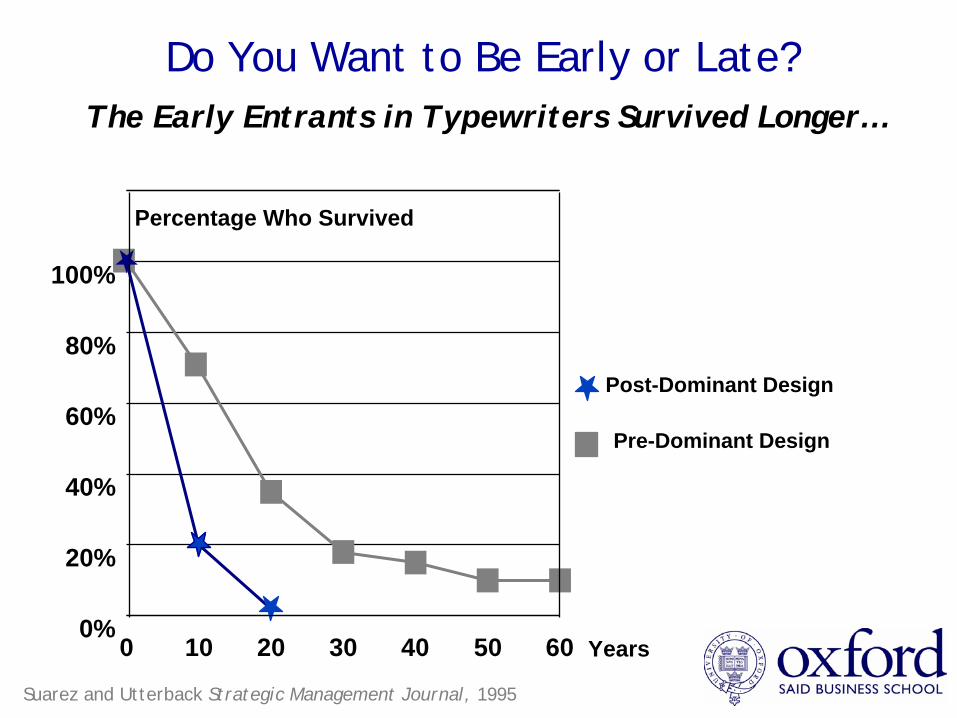

Do You Want to Be Early or Late?The Early Entrants in Typewriters Survived Longer…

Suarez and Utterback Strategic Management Journal, 1995

0 10 20 30 40 50 600%

20%

40%

60%

80%

100%

Post-Dominant Design

Pre-Dominant Design

Percentage Who Survived

Years

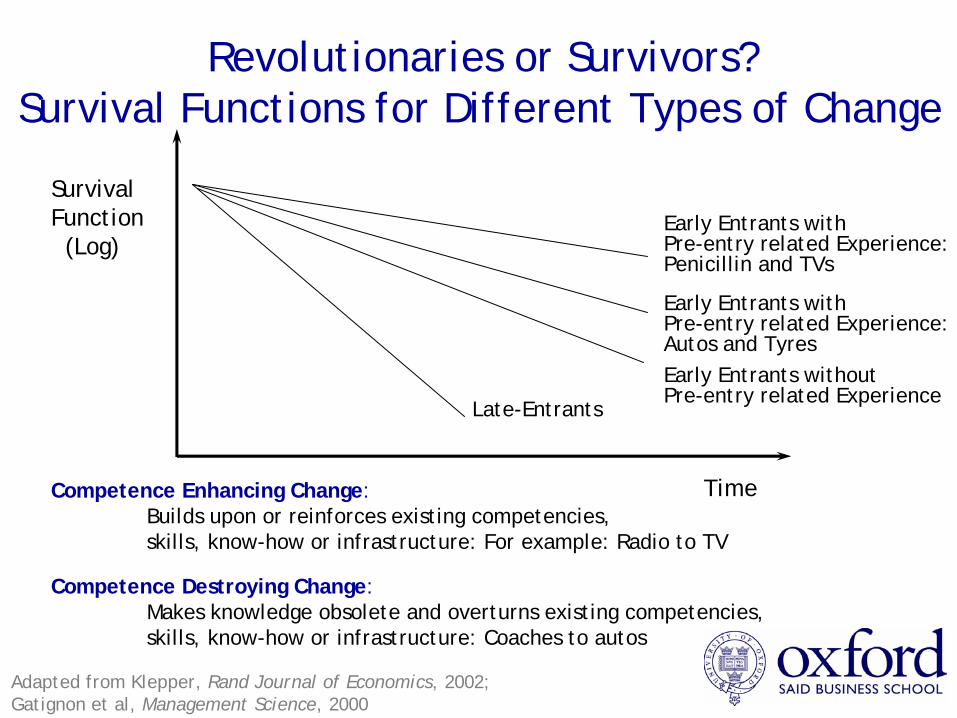

Revolutionaries or Survivors?Survival Functions for Different Types of Change

Competence Enhancing Change: Builds upon or reinforces existing competencies,skills, know-how or infrastructure: For example: Radio to TV

Competence Destroying Change:Makes knowledge obsolete and overturns existing competencies,skills, know-how or infrastructure: Coaches to autos

Survival Function(Log)

Time

Early Entrants with Pre-entry related Experience:Penicillin and TVs

Early Entrants with Pre-entry related Experience:Autos and TyresEarly Entrants without Pre-entry related Experience

Late-Entrants

Adapted from Klepper, Rand Journal of Economics, 2002; Gatignon et al, Management Science, 2000

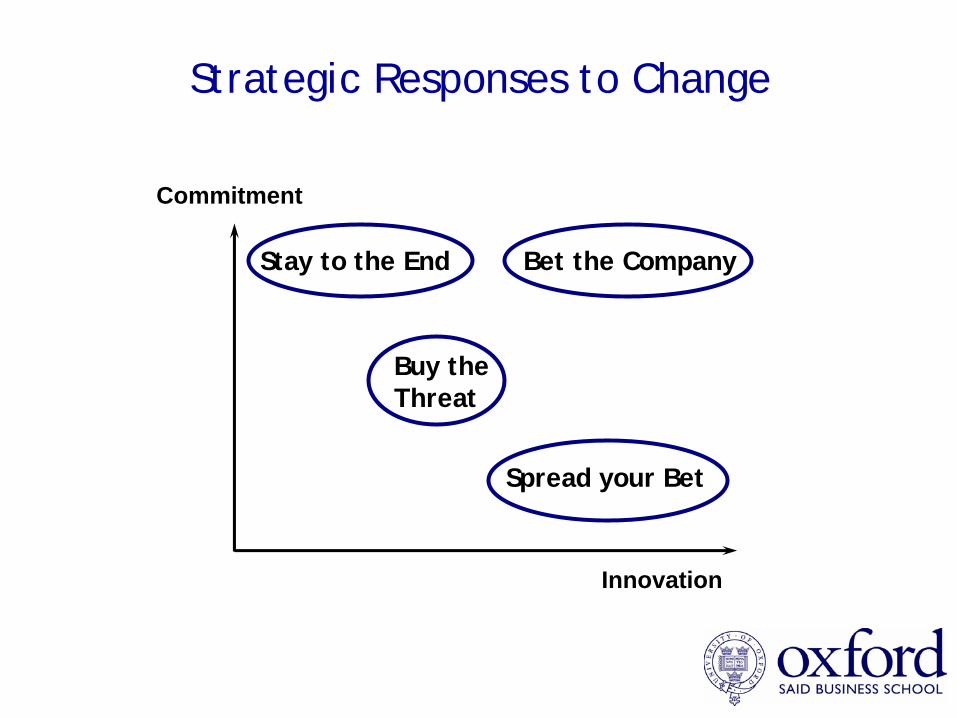

Strategic Responses to Change

Innovation

Commitment

Stay to the End

Buy theThreat

Spread your Bet

Bet the Company

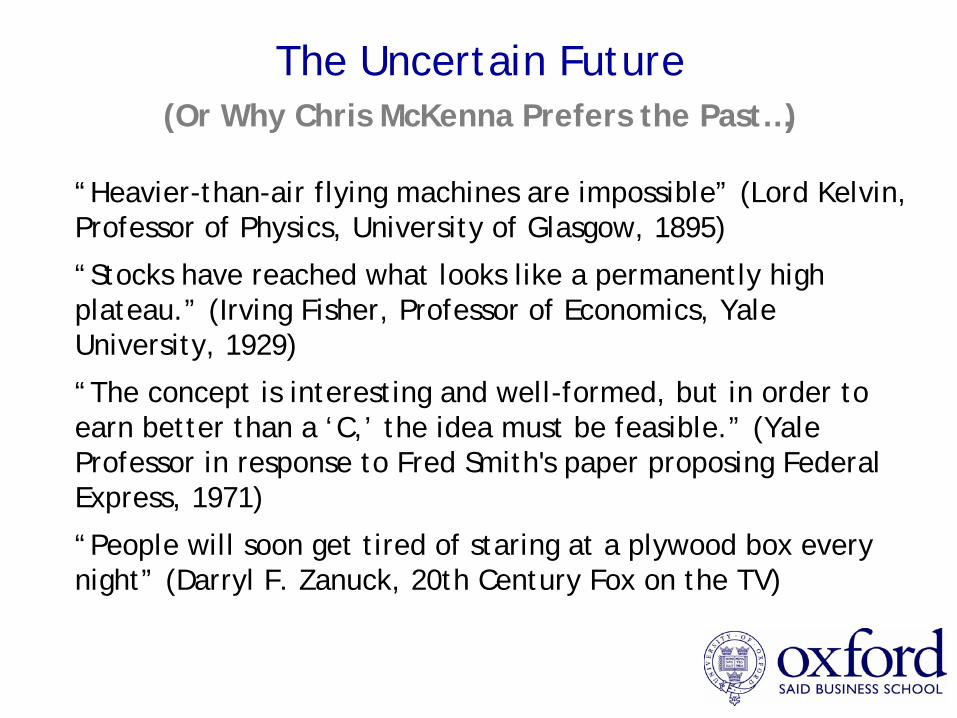

The Uncertain Future (Or Why Chris McKenna Prefers the Past…)

“Heavier-than-air flying machines are impossible” (Lord Kelvin, Professor of Physics, University of Glasgow, 1895)

“Stocks have reached what looks like a permanently high plateau.” (Irving Fisher, Professor of Economics, Yale University, 1929)

“The concept is interesting and well-formed, but in order to earn better than a ‘C,’ the idea must be feasible.” (Yale Professor in response to Fred Smith's paper proposing Federal Express, 1971)

“People will soon get tired of staring at a plywood box every night” (Darryl F. Zanuck, 20th Century Fox on the TV)

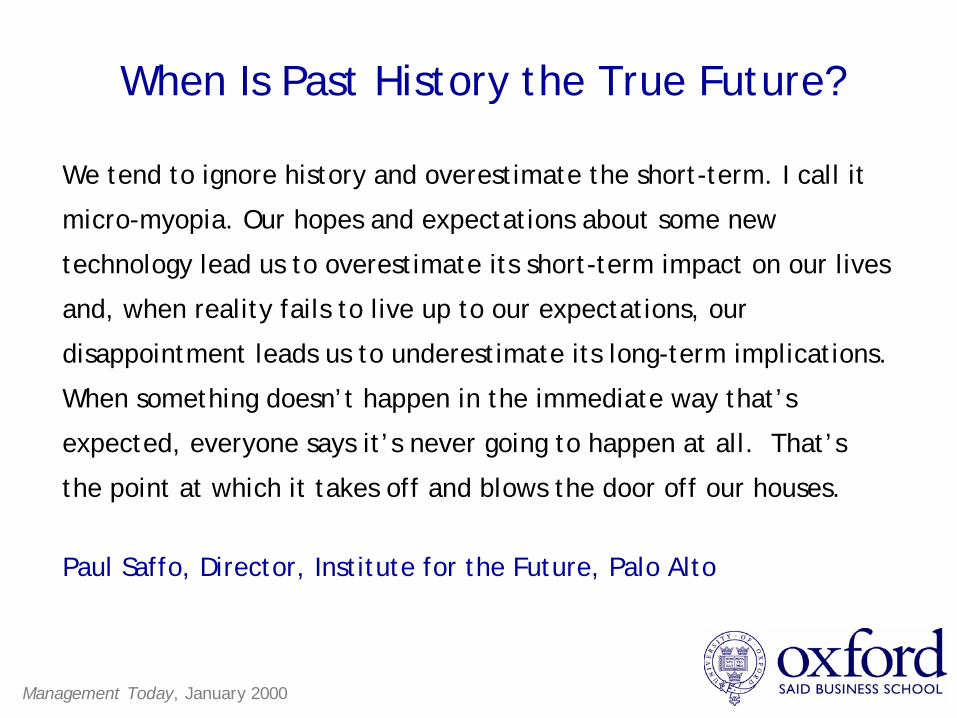

When Is Past History the True Future?

Management Today, January 2000

We tend to ignore history and overestimate the short-term. I call it

micro-myopia. Our hopes and expectations about some new

technology lead us to overestimate its short-term impact on our lives

and, when reality fails to live up to our expectations, our

disappointment leads us to underestimate its long-term implications.

When something doesn’t happen in the immediate way that’s

expected, everyone says it’s never going to happen at all. That’s

the point at which it takes off and blows the door off our houses.

Paul Saffo, Director, Institute for the Future, Palo Alto

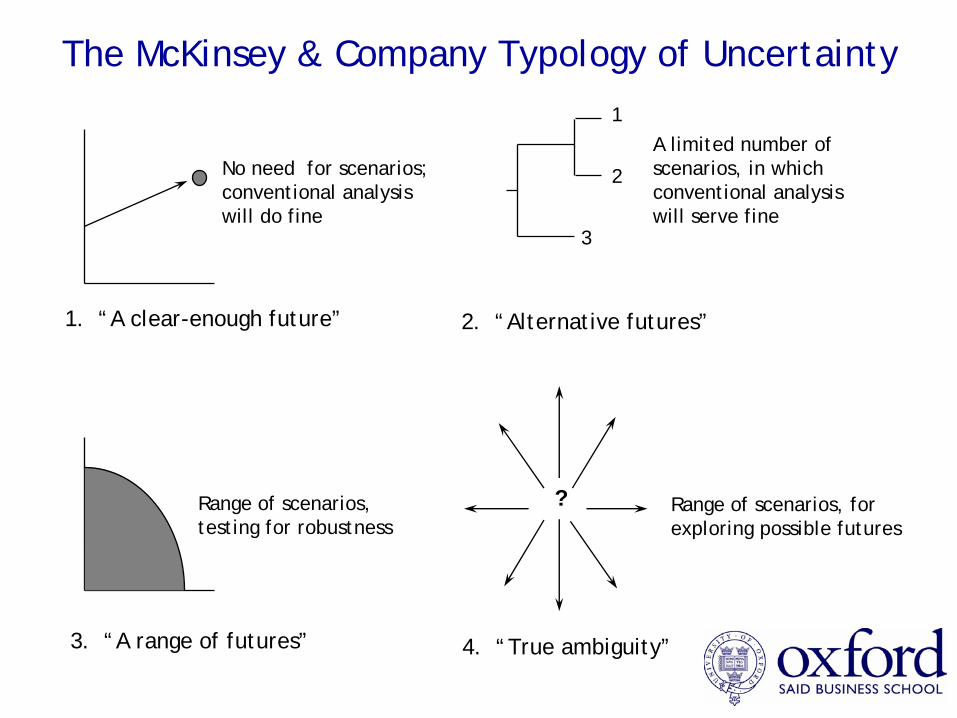

The McKinsey & Company Typology of Uncertainty

?

1

2

3

1. “A clear-enough future” 2. “Alternative futures”

3. “A range of futures” 4. “True ambiguity”

No need for scenarios;conventional analysis will do fine

A limited number of scenarios, in which conventional analysis will serve fine

Range of scenarios, testing for robustness

Range of scenarios, for exploring possible futures

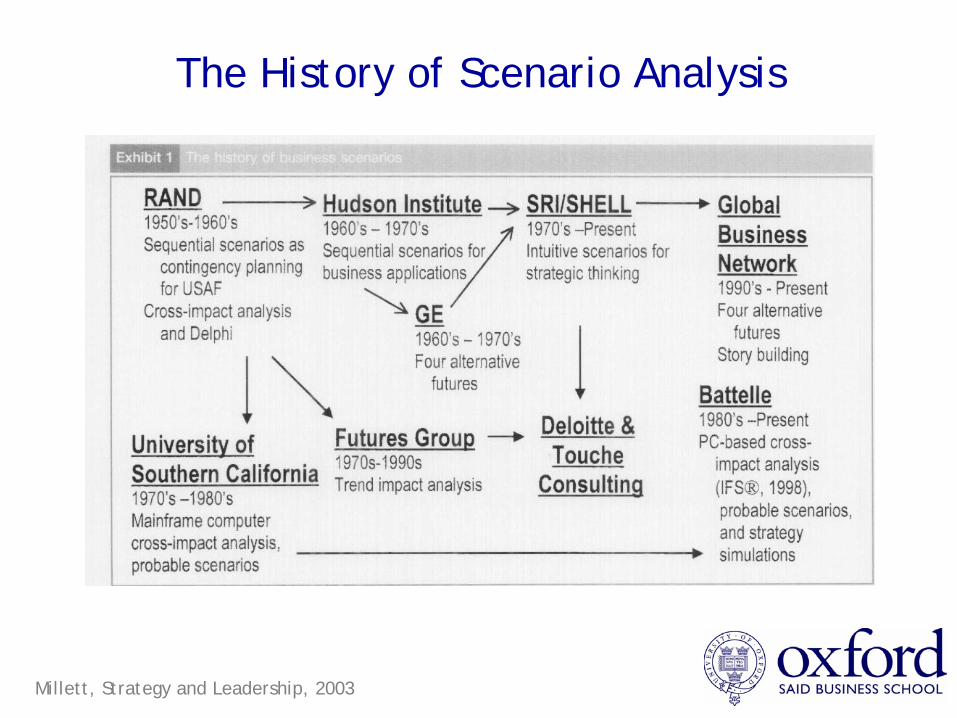

The History of Scenario Analysis

Millett, Strategy and Leadership, 2003

Scenario Analysis

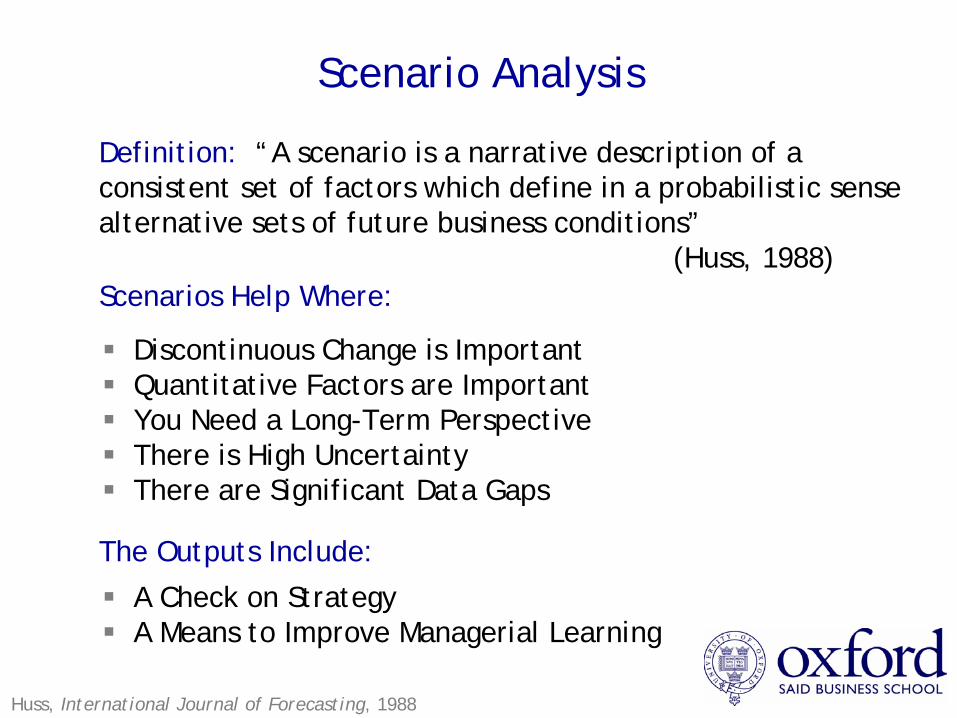

Huss, International Journal of Forecasting, 1988

Definition: “A scenario is a narrative description of a consistent set of factors which define in a probabilistic sense alternative sets of future business conditions”

(Huss, 1988)Scenarios Help Where:

Discontinuous Change is ImportantQuantitative Factors are ImportantYou Need a Long-Term PerspectiveThere is High UncertaintyThere are Significant Data Gaps

The Outputs Include:

A Check on StrategyA Means to Improve Managerial Learning

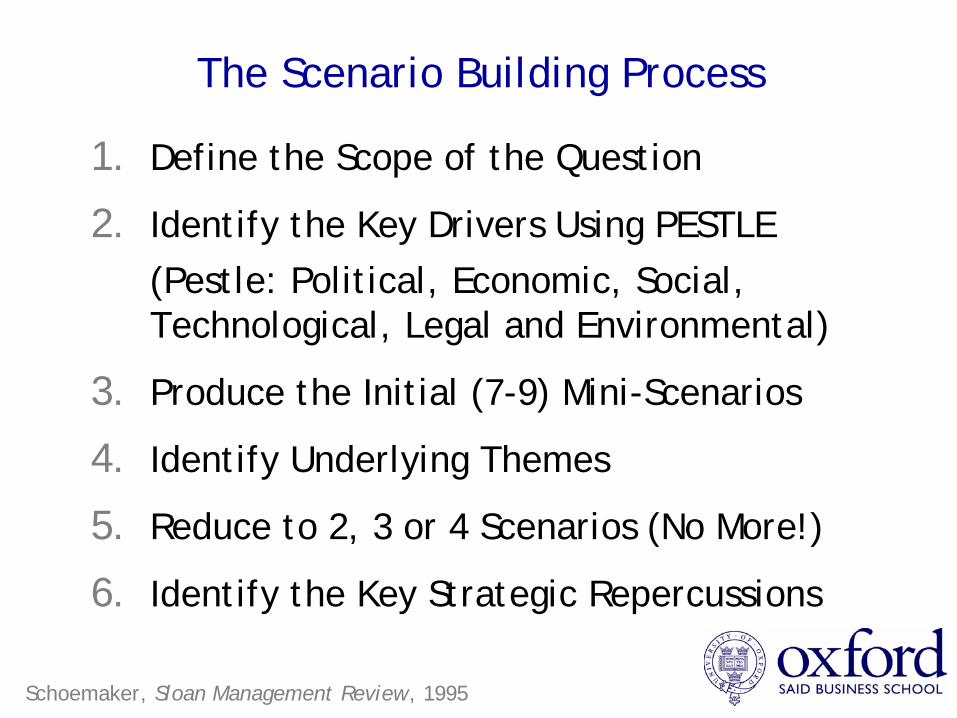

The Scenario Building Process

1. Define the Scope of the Question

2. Identify the Key Drivers Using PESTLE(Pestle: Political, Economic, Social, Technological, Legal and Environmental)

3. Produce the Initial (7-9) Mini-Scenarios

4. Identify Underlying Themes

5. Reduce to 2, 3 or 4 Scenarios (No More!)

6. Identify the Key Strategic Repercussions

Schoemaker, Sloan Management Review, 1995

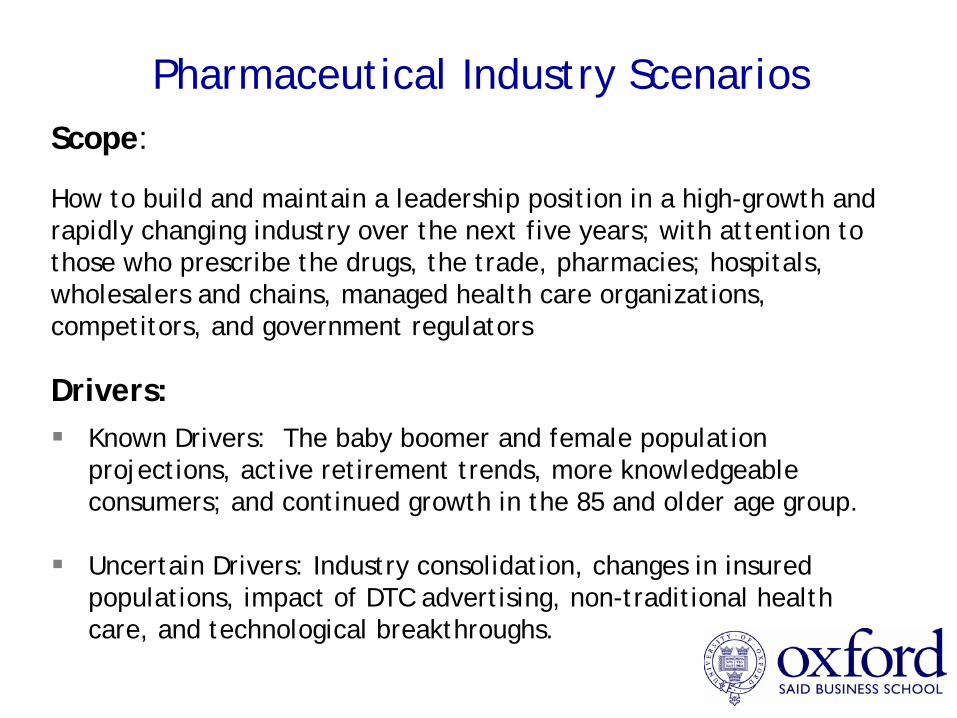

Pharmaceutical Industry ScenariosScope:

How to build and maintain a leadership position in a high-growth and rapidly changing industry over the next five years; with attention to those who prescribe the drugs, the trade, pharmacies; hospitals, wholesalers and chains, managed health care organizations, competitors, and government regulators

Drivers:Known Drivers: The baby boomer and female population projections, active retirement trends, more knowledgeable consumers; and continued growth in the 85 and older age group.

Uncertain Drivers: Industry consolidation, changes in insured populations, impact of DTC advertising, non-traditional health care, and technological breakthroughs.

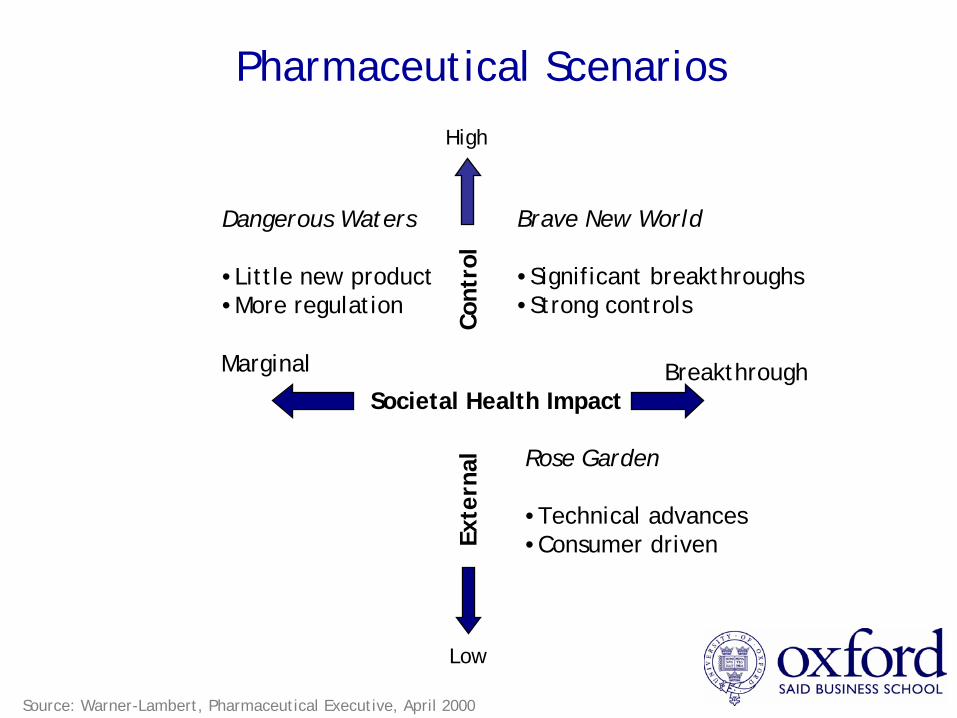

Pharmaceutical Scenarios

Societal Health Impact

Exte

rnal

C

ontr

ol

Dangerous Waters

•Little new product•More regulation

Brave New World

•Significant breakthroughs•Strong controls

Rose Garden

•Technical advances•Consumer driven

Low

High

Marginal Breakthrough

Source: Warner-Lambert, Pharmaceutical Executive, April 2000

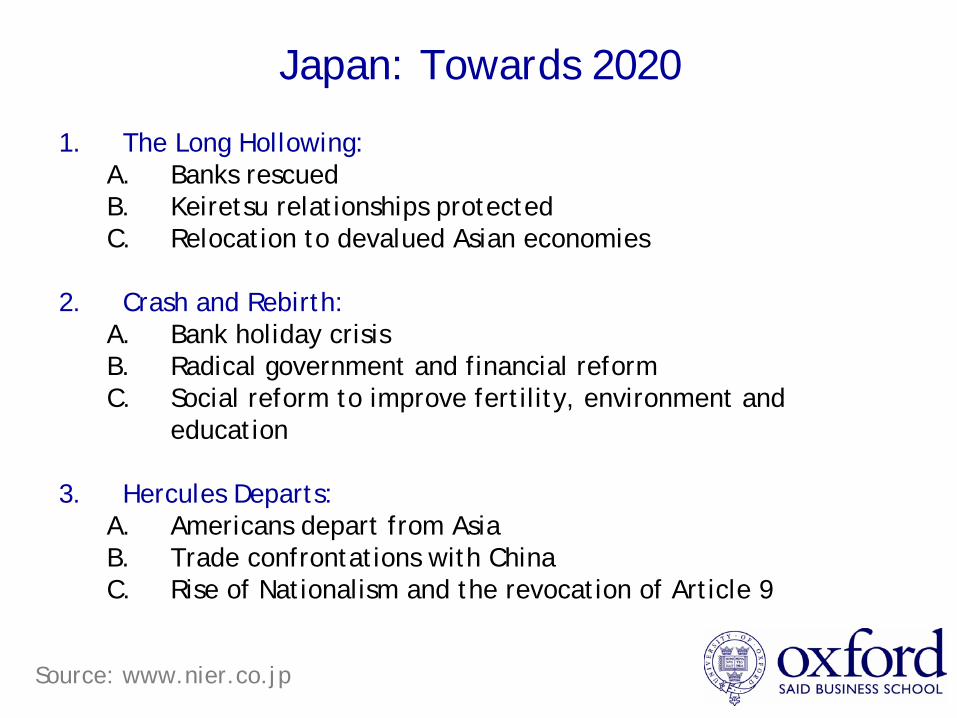

Japan: Towards 2020

Source: www.nier.co.jp

1. The Long Hollowing:A. Banks rescuedB. Keiretsu relationships protected C. Relocation to devalued Asian economies

2. Crash and Rebirth: A. Bank holiday crisisB. Radical government and financial reformC. Social reform to improve fertility, environment and

education

3. Hercules Departs:A. Americans depart from AsiaB. Trade confrontations with ChinaC. Rise of Nationalism and the revocation of Article 9

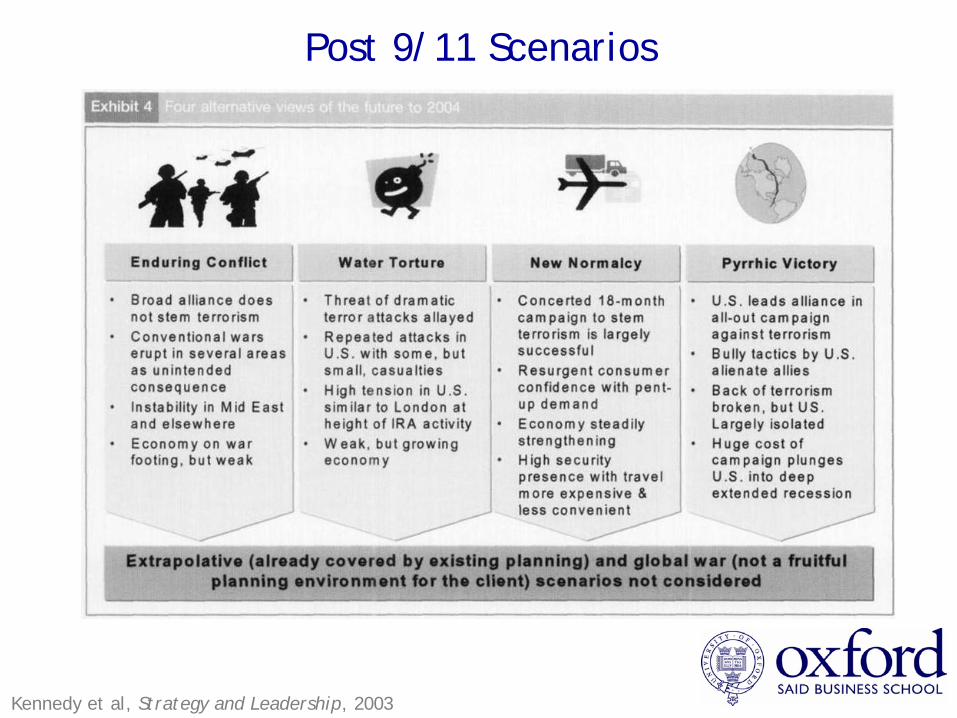

Post 9/11 Scenarios

Kennedy et al, Strategy and Leadership, 2003

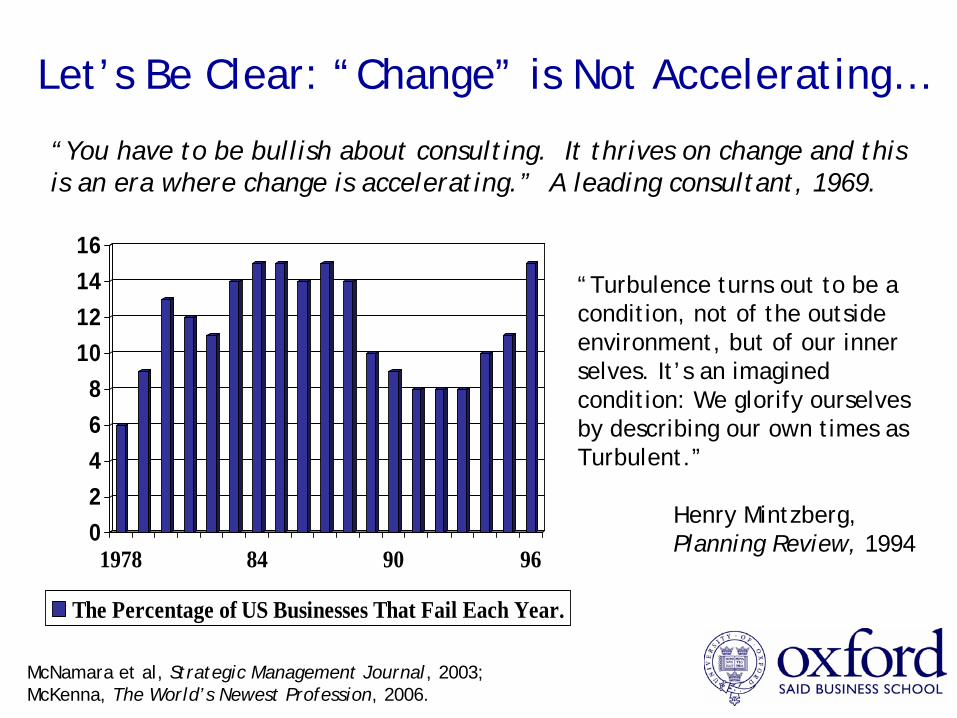

Let’s Be Clear: “Change” is Not Accelerating…

02468

10121416

1978 84 90 96

The Percentage of US Businesses That Fail Each Year.

McNamara et al, Strategic Management Journal, 2003;McKenna, The World’s Newest Profession, 2006.

“Turbulence turns out to be acondition, not of the outsideenvironment, but of our innerselves. It’s an imagined condition: We glorify ourselvesby describing our own times asTurbulent.”

Henry Mintzberg, Planning Review, 1994

“You have to be bullish about consulting. It thrives on change and this is an era where change is accelerating.” A leading consultant, 1969.

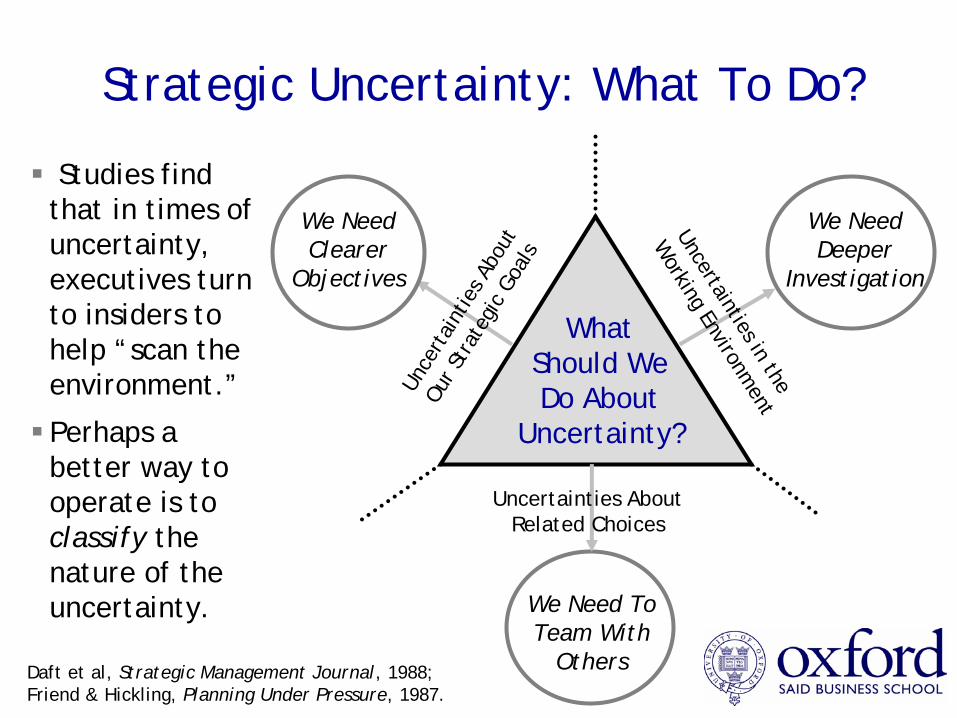

Strategic Uncertainty: What To Do?

Daft et al, Strategic Management Journal, 1988;Friend & Hickling, Planning Under Pressure, 1987.

We Need Clearer

Objectives

We Need Deeper

Investigation

WhatShould WeDo About

Uncertainty?

We Need To Team With

Others

Uncertainties in the

Working Environm

ent

Unce

rtai

ntie

s Abo

ut

Our S

trat

egic

Goa

lsUncertainties About

Related Choices

Studies find that in times of uncertainty, executives turn to insiders to help “scan the environment.”

Perhaps a better way to operate is to classify the nature of the uncertainty.

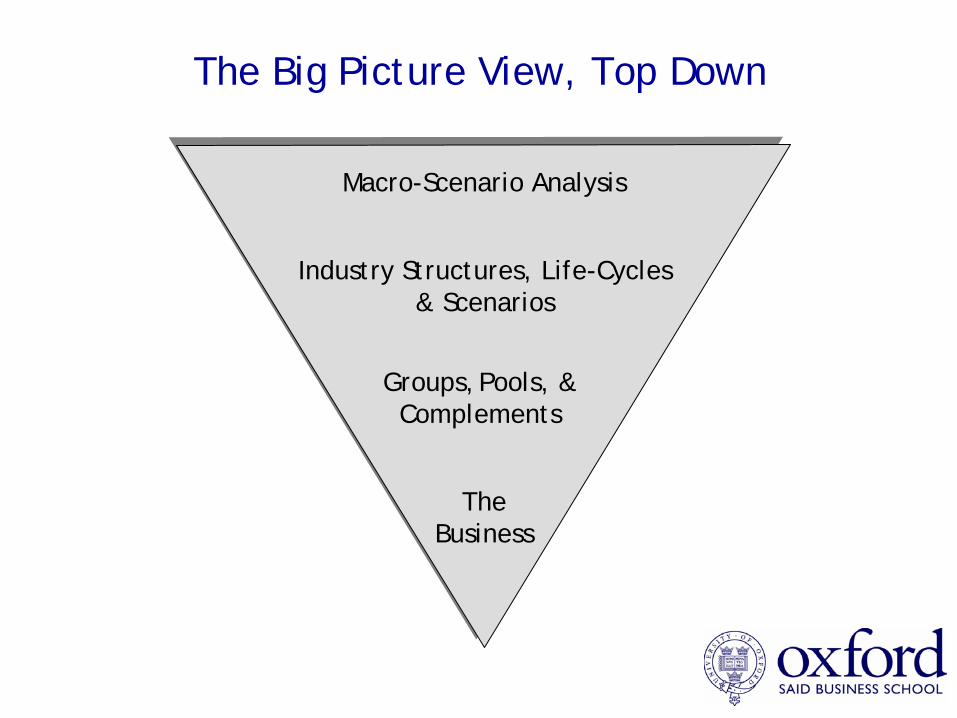

The Big Picture View, Top Down

Macro-Scenario Analysis

Industry Structures, Life-Cycles& Scenarios

Groups,Pools, & Complements

The Business

Industry Life Cycle

Dominant Design

Macro-Environment (PESTLE)

Strategic Uncertainty

Key Concepts

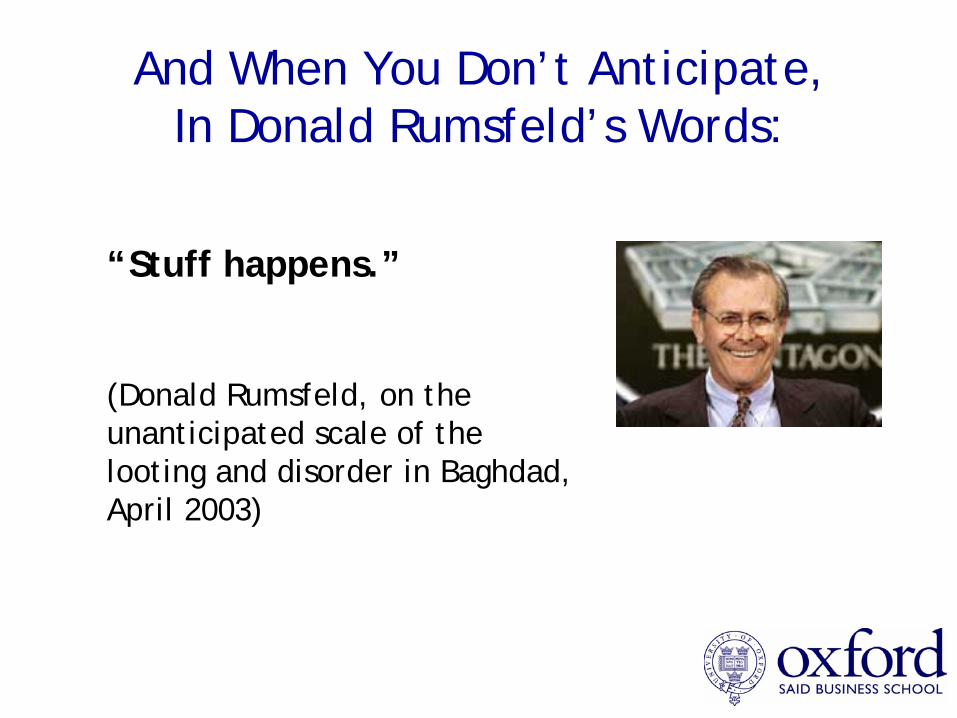

And When You Don’t Anticipate, In Donald Rumsfeld’s Words:

“Stuff happens.”

(Donald Rumsfeld, on theunanticipated scale of the looting and disorder in Baghdad, April 2003)

Understanding Diversification

Christopher McKenna

MBAStrategy: Session Five

Michaelmas 2005

Key Concepts and Techniques

Hierarchy of Growth

Related Diversification

Portfolio Models

Synergy

Core Competence

Corporate versus Competitive Strategy

Level

Group

Businesses

Functions

Strategy

Corporate

Business

Functional

Types of Strategy

Competitive and Corporate Strategy

Competitive (Business) StrategyHow should a business compete in its industry?

Corporate StrategyWhat businesses should be included in the corporate portfolio?How should these businesses relate to one another?How should these businesses relate to the corporate parent?

The First Definition of “Strategy”

“The determination of the basic long-term goals and objectives of an enterprise and the adoption of courses of action and the allocation of resources necessary for carrying out these goals.”

Alfred Chandler, Strategy and Structure, (MIT Press, 1962), Page 13

The Hierarchy of Growth

Revamp Packaging, Pricing, Promotions

Expand into New Domestic Territories

Develop New, Related Products and Services

Export Current Products Abroad

Acquire a Competitor

Expand Internationally

Acquire in a Related, Growing Industry

Integrate Vertically – Acquire a Supplier or Customer

Acquire in an Unrelated, Growing Industry

Early Strategies

Late Strategies

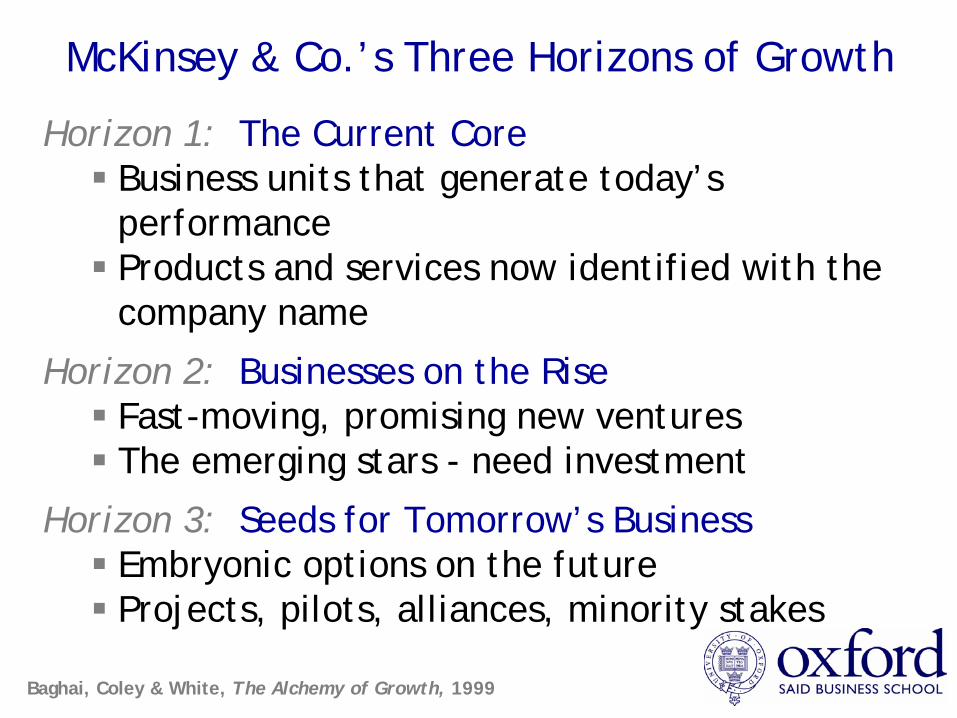

McKinsey & Co.’s Three Horizons of Growth

Horizon 1: The Current Core Business units that generate today’s performance Products and services now identified with the company name

Horizon 2: Businesses on the Rise Fast-moving, promising new venturesThe emerging stars - need investment

Horizon 3: Seeds for Tomorrow’s BusinessEmbryonic options on the futureProjects, pilots, alliances, minority stakes

Baghai, Coley & White, The Alchemy of Growth, 1999

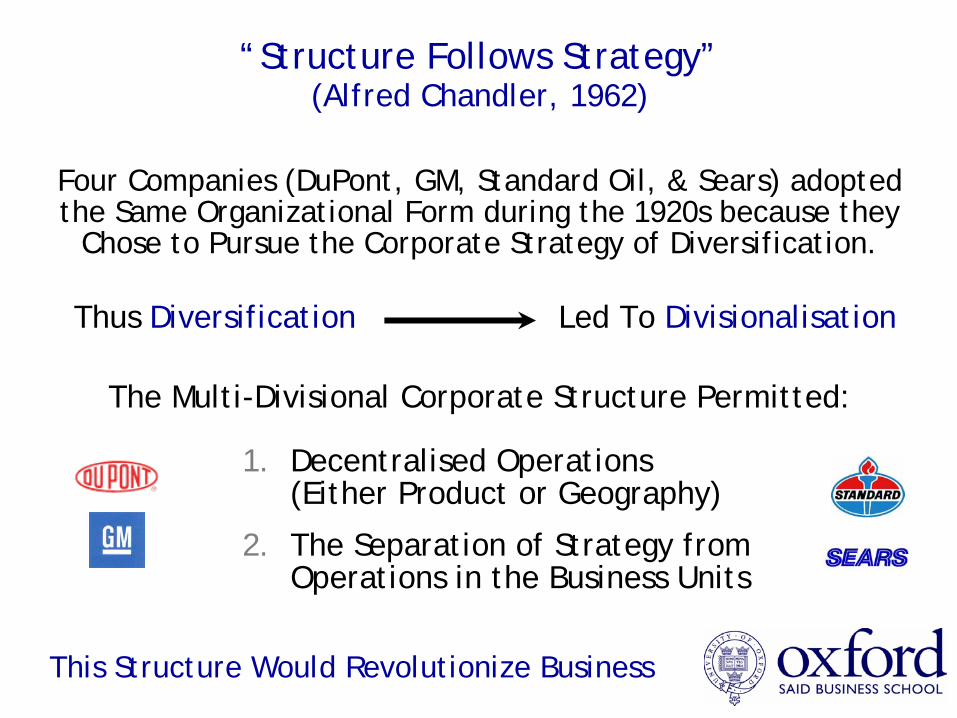

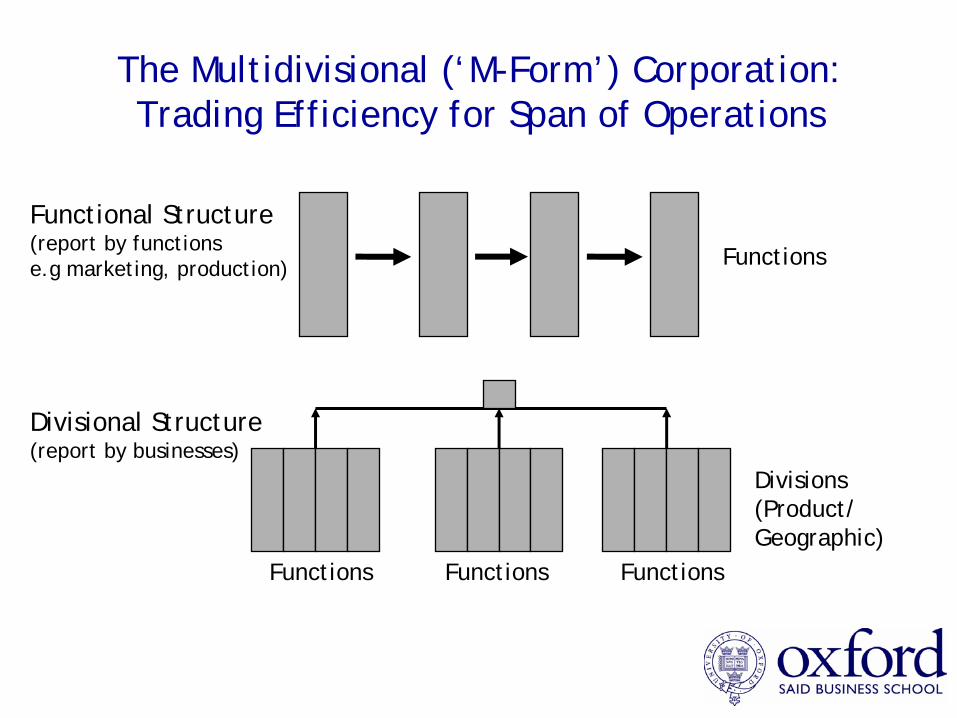

“Structure Follows Strategy”(Alfred Chandler, 1962)

Thus Diversification Led To Divisionalisation

The Multi-Divisional Corporate Structure Permitted:

1. Decentralised Operations (Either Product or Geography)

2. The Separation of Strategy from Operations in the Business Units

Four Companies (DuPont, GM, Standard Oil, & Sears) adopted the Same Organizational Form during the 1920s because they

Chose to Pursue the Corporate Strategy of Diversification.

This Structure Would Revolutionize Business

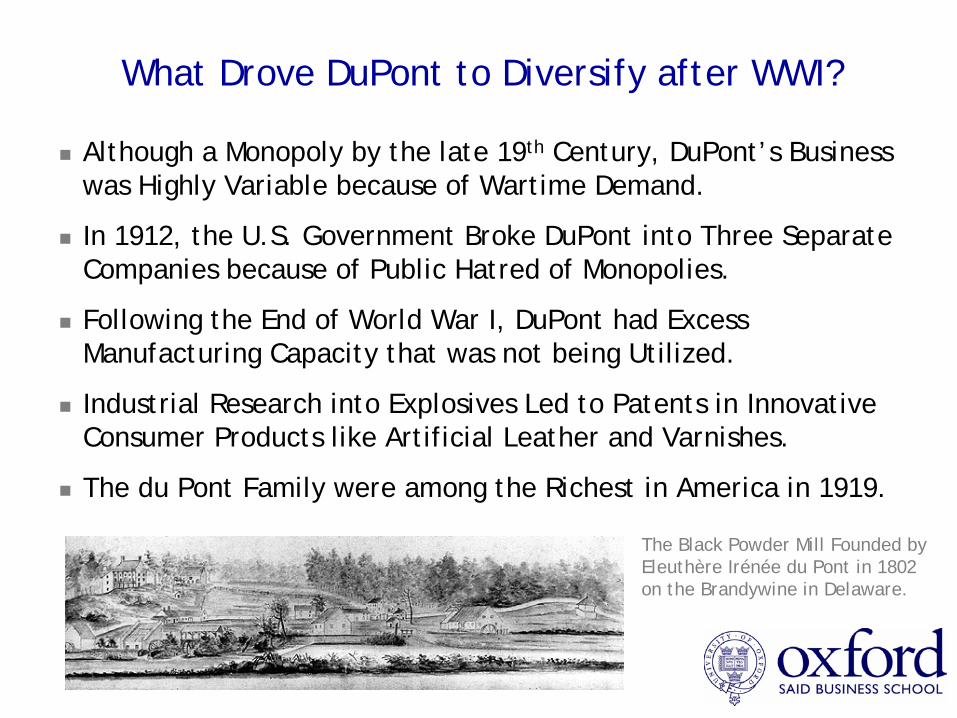

What Drove DuPont to Diversify after WWI?

The Black Powder Mill Founded by Eleuthère Irénée du Pont in 1802 on the Brandywine in Delaware.

Although a Monopoly by the late 19th Century, DuPont’s Business was Highly Variable because of Wartime Demand.

In 1912, the U.S. Government Broke DuPont into Three Separate Companies because of Public Hatred of Monopolies.

Following the End of World War I, DuPont had Excess Manufacturing Capacity that was not being Utilized.

Industrial Research into Explosives Led to Patents in InnovativeConsumer Products like Artificial Leather and Varnishes.

The du Pont Family were among the Richest in America in 1919.

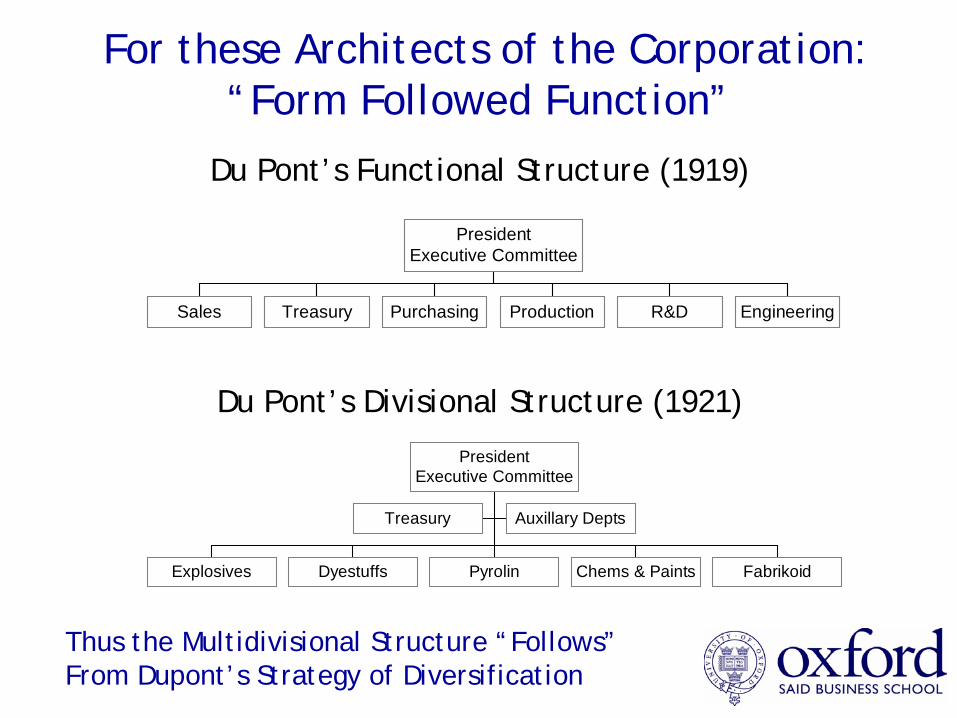

Sales Treasury Purchasing Production R&D Engineering

PresidentExecutive Committee

Treasury Auxillary Depts

Explosives Dyestuffs Pyrolin Chems & Paints Fabrikoid

PresidentExecutive Committee

Du Pont’s Functional Structure (1919)

Du Pont’s Divisional Structure (1921)

For these Architects of the Corporation: “Form Followed Function”

Thus the Multidivisional Structure “Follows”From Dupont’s Strategy of Diversification

Divisions(Product/Geographic)

Functions

Functional Structure(report by functionse.g marketing, production)

Divisional Structure(report by businesses)

Functions FunctionsFunctions

The Multidivisional (‘M-Form’) Corporation:Trading Efficiency for Span of Operations

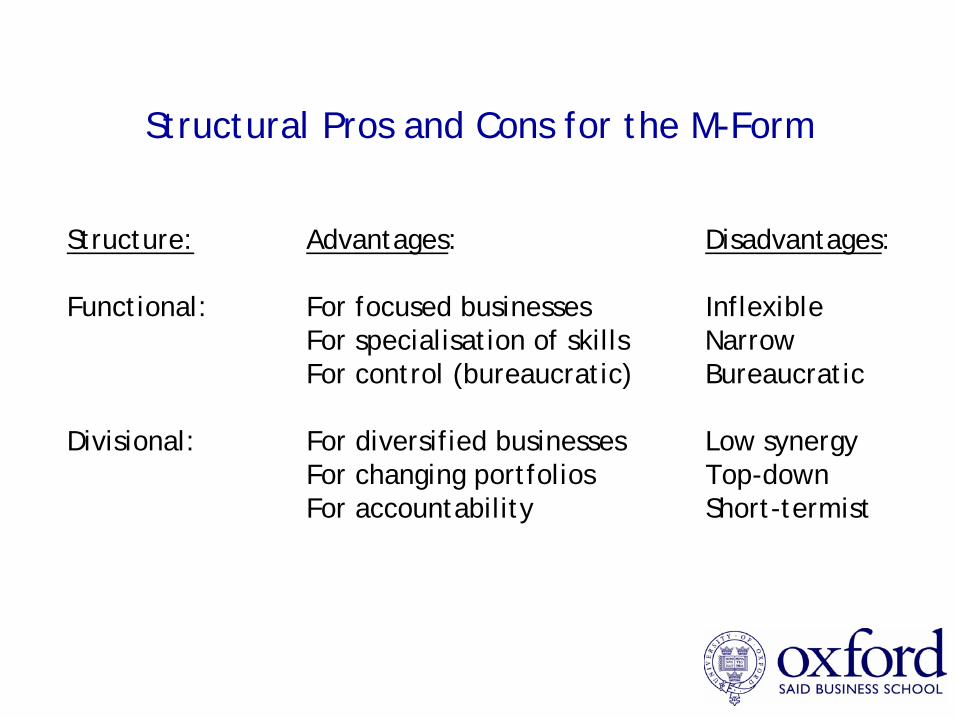

Structure: Advantages: Disadvantages:

Functional: For focused businesses InflexibleFor specialisation of skills NarrowFor control (bureaucratic) Bureaucratic

Divisional: For diversified businesses Low synergy For changing portfolios Top-down For accountability Short-termist

Structural Pros and Cons for the M-Form

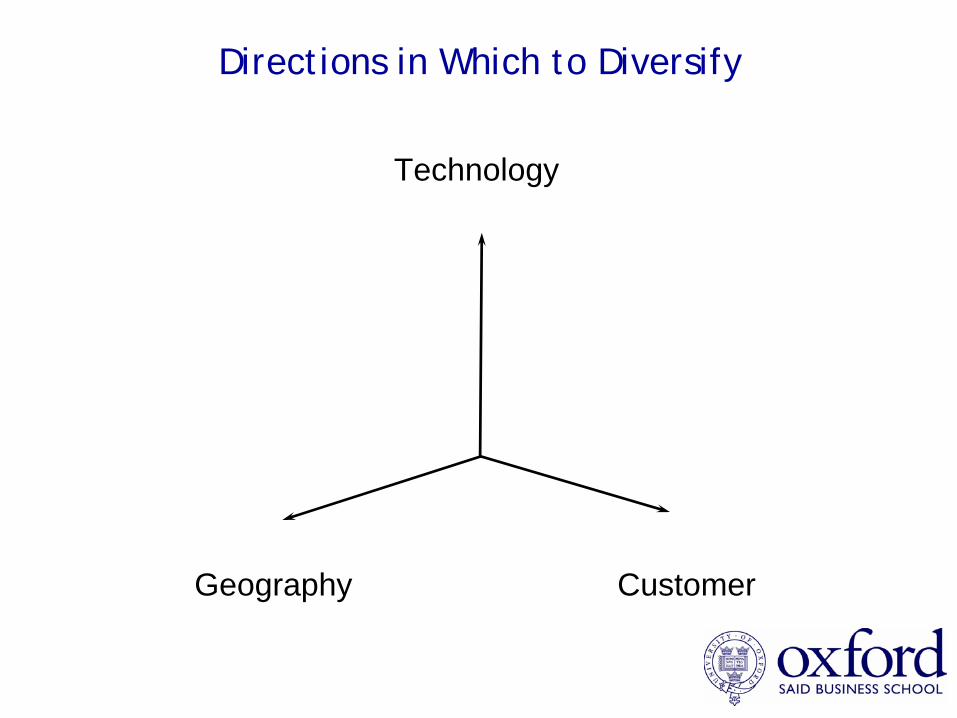

Directions in Which to Diversify

Technology

Geography Customer

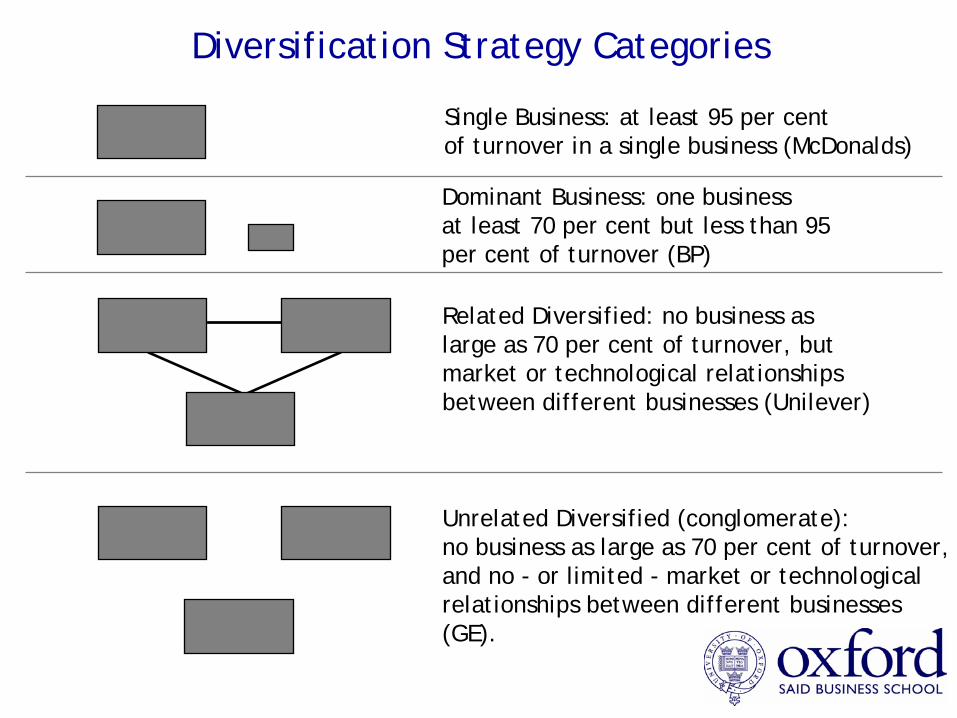

Diversification Strategy Categories

Single Business: at least 95 per centof turnover in a single business (McDonalds)

Dominant Business: one business at least 70 per cent but less than 95per cent of turnover (BP)

Related Diversified: no business as large as 70 per cent of turnover, but market or technological relationshipsbetween different businesses (Unilever)

Unrelated Diversified (conglomerate): no business as large as 70 per cent of turnover,and no - or limited - market or technological relationships between different businesses (GE).

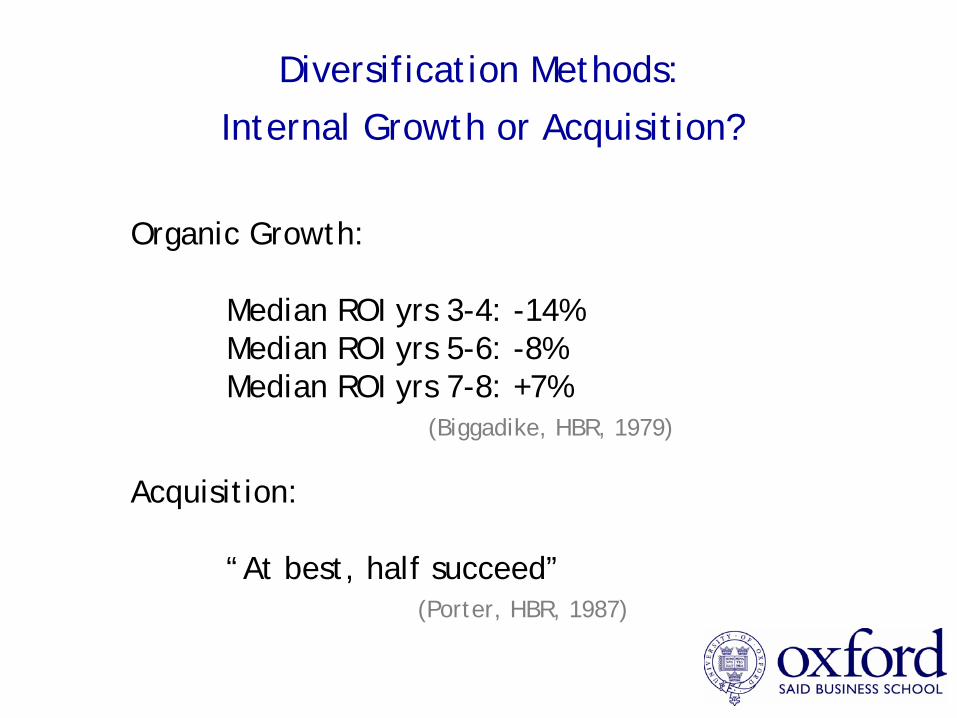

Diversification Methods:

Internal Growth or Acquisition?

Organic Growth:

Median ROI yrs 3-4: -14%Median ROI yrs 5-6: -8%Median ROI yrs 7-8: +7%

(Biggadike, HBR, 1979)

Acquisition:

“At best, half succeed”(Porter, HBR, 1987)

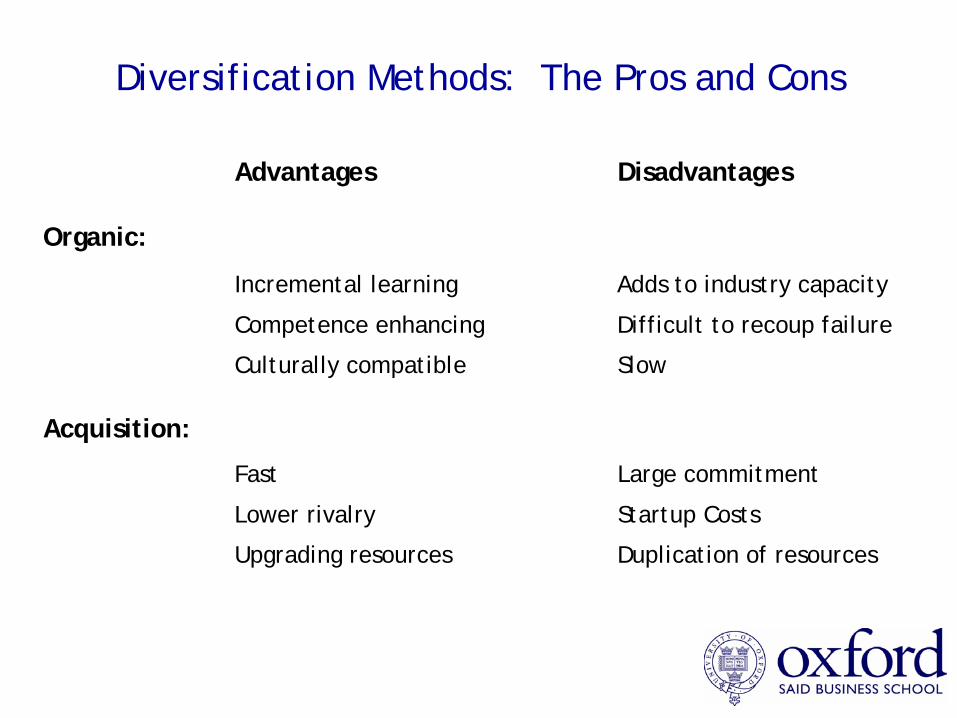

Diversification Methods: The Pros and Cons

Advantages Disadvantages

Organic:

Incremental learning Adds to industry capacity

Competence enhancing Difficult to recoup failure

Culturally compatible Slow

Acquisition:

Fast Large commitment

Lower rivalry Startup Costs

Upgrading resources Duplication of resources

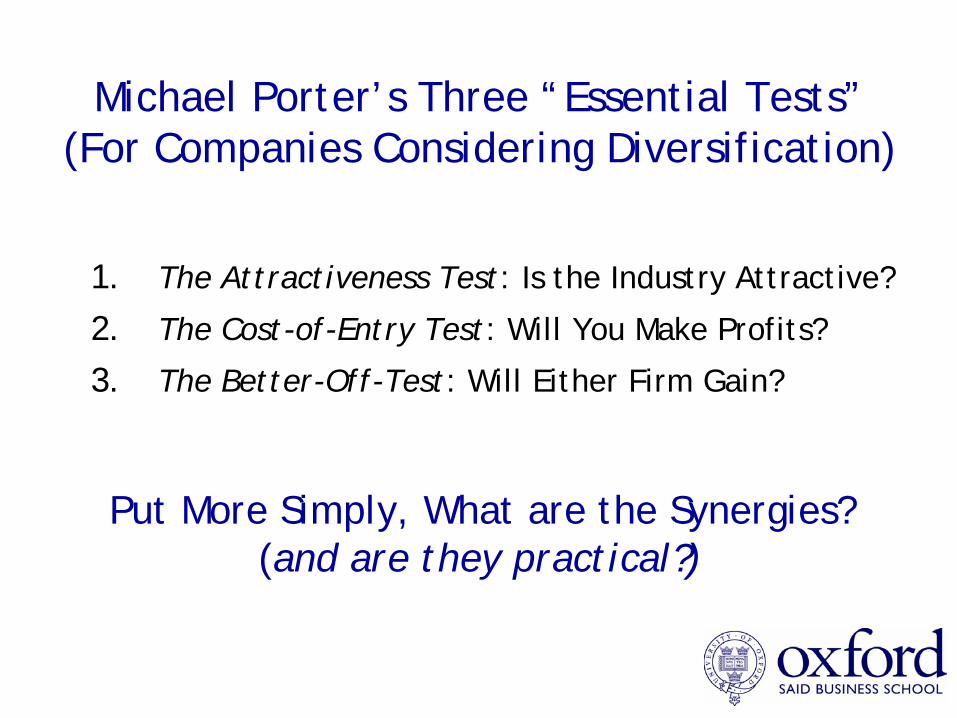

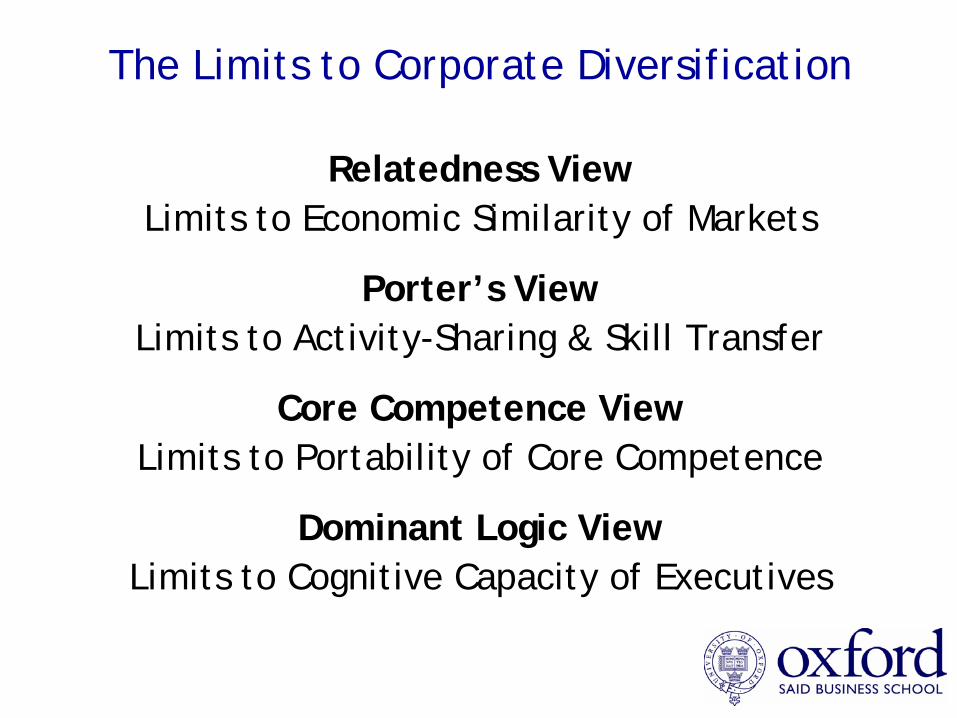

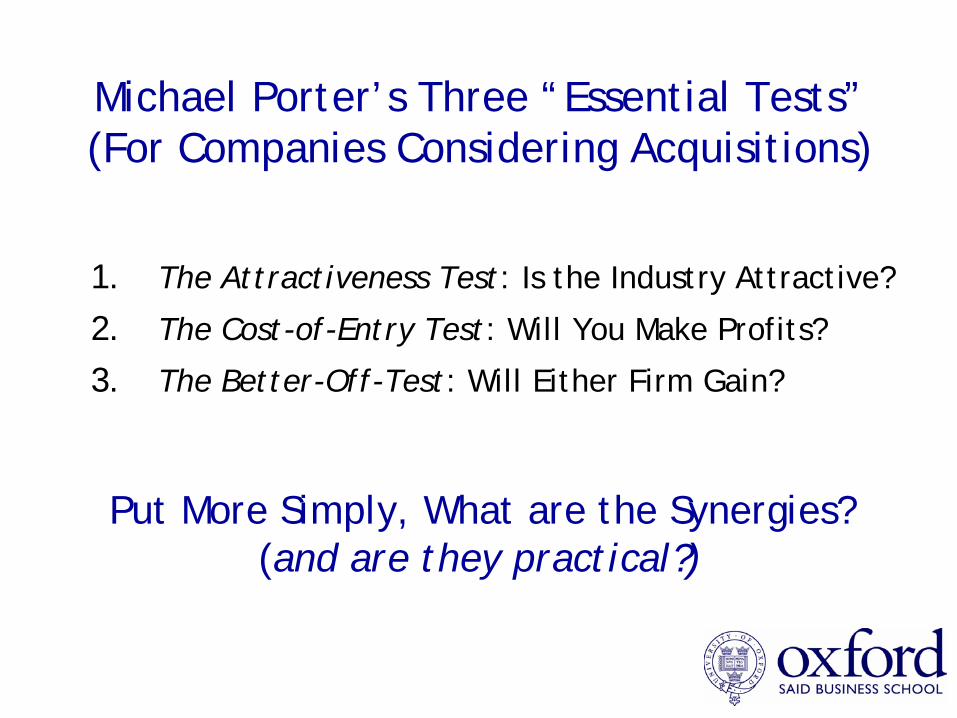

Michael Porter’s Three “Essential Tests”(For Companies Considering Diversification)

1. The Attractiveness Test: Is the Industry Attractive?

2. The Cost-of-Entry Test: Will You Make Profits?

3. The Better-Off-Test: Will Either Firm Gain?

Put More Simply, What are the Synergies?(and are they practical?)

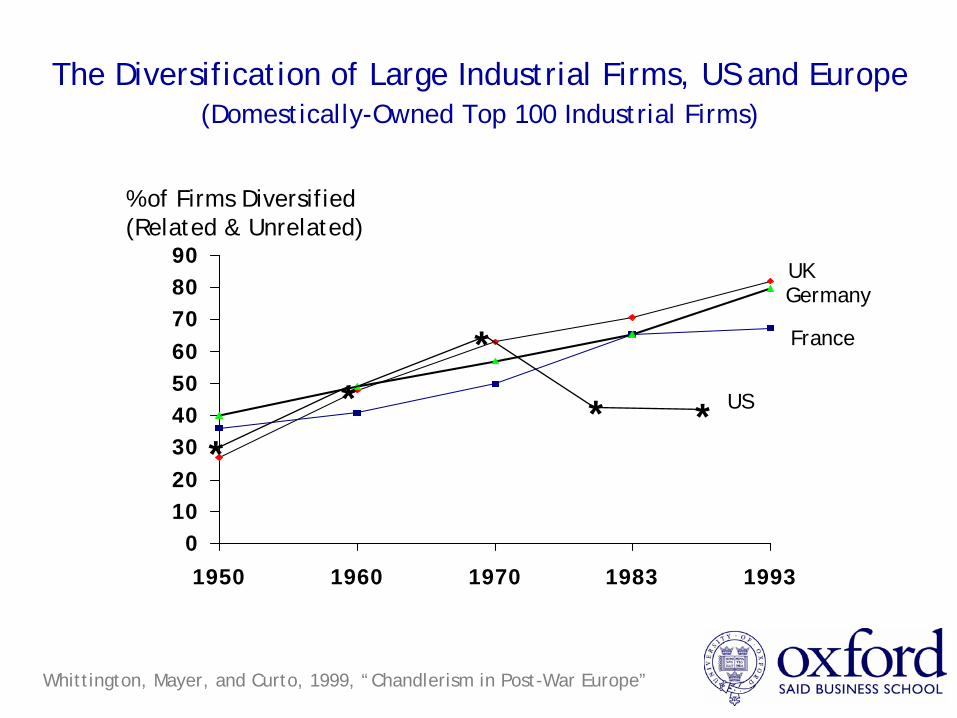

0102030405060708090

1950 1960 1970 1983 1993

**

*

* *

% of Firms Diversified(Related & Unrelated)

The Diversification of Large Industrial Firms, US and Europe

US

France

GermanyUK

(Domestically-Owned Top 100 Industrial Firms)

Whittington, Mayer, and Curto, 1999, “Chandlerism in Post-War Europe”

Management Consultants

At Work in 1957.

The Bulk of Consultants Work in the 1950s and 1960s

was to Install the Multidivisional

Structure.

Consulting Firms like McKinsey Carried the Structure to Europe

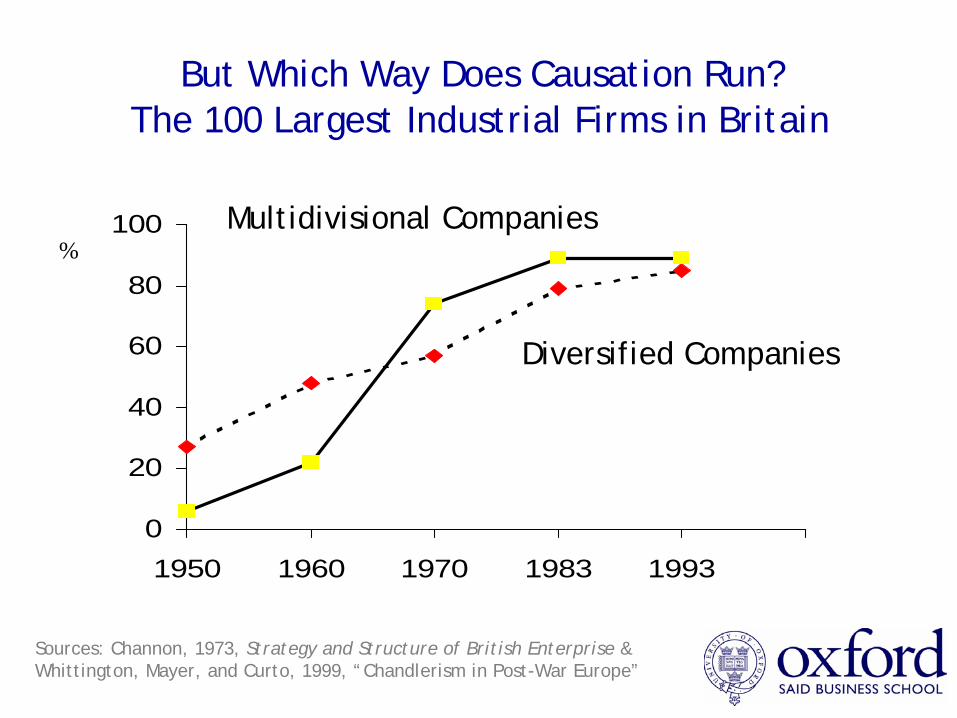

But Which Way Does Causation Run? The 100 Largest Industrial Firms in Britain

0

20

40

60

80

100

1950 1960 1970 1983 1993

%

Sources: Channon, 1973, Strategy and Structure of British Enterprise & Whittington, Mayer, and Curto, 1999, “Chandlerism in Post-War Europe”

Diversified Companies

Multidivisional Companies

The Context for Conglomerates The Geology & Geography of Conglomeration

Definition: Derived from Geology, a Conglomerate is a firm whose growth comes through the acquisition of other firms whose products are largely unrelated.

Origins: Pioneered in American by Royal Little at Textron in the 1950s, Conglomerates quickly became the darlings of stockmarkets in the 1960s before being dismantled in the 1980s.

ExamplesAmerica: GE, ITT, Gulf + Western Europe: Hanson, Virgin, VivendiAsia: Hutchison Whampoa, Hyundai

“Conglomerates are so 1970s. It was thought then that commercial power, brand strength, and management expertise could be leveraged by engaging in several different lines of business, creating a company that was greater than its myriad constituents could be on their own. Now the fashion is to concentrate on core operations, one or a few related activities, and shed the rest. Conglomerates are seen as cumbersome, inefficient, Byzantine corporate structures. Disco may have made a comeback, but based on the opinions of several portfolio managers, retro-chic is unlikely to extend to an appreciation of conglomerates. ‘I never wore flared trousers the first or the second time around, and I have the same attitude on conglomerates,’ says Liam Pagliaro, head of European research for Gartmore.”

The Anglo-American View of Conglomerates

“Conglomerates: Once a Rage, Now a Relic ”International Herald Tribune

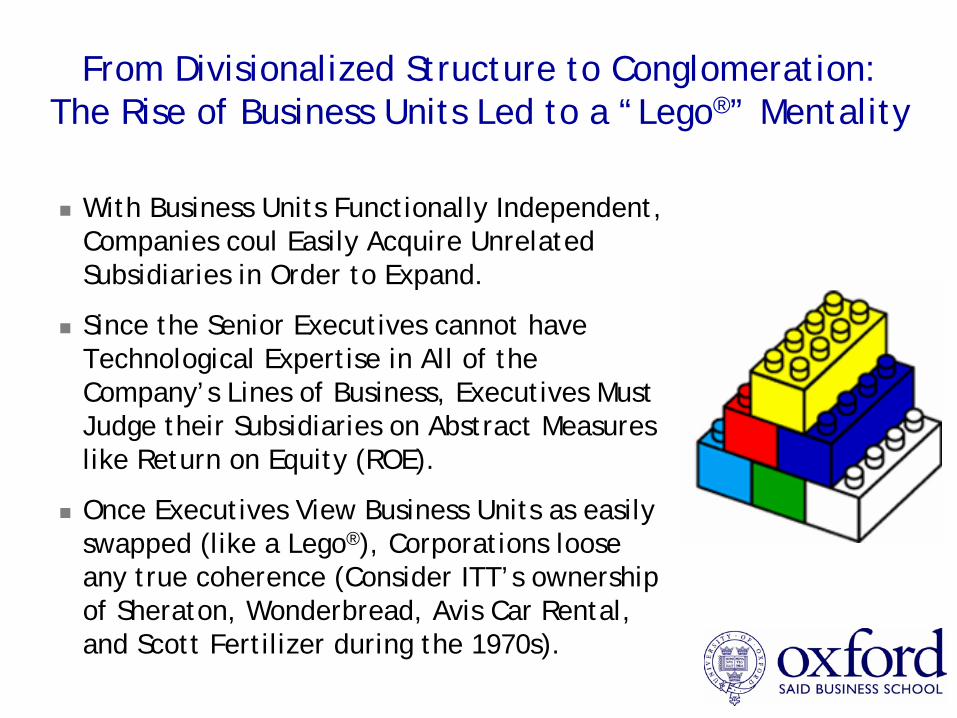

From Divisionalized Structure to Conglomeration:The Rise of Business Units Led to a “Lego®” Mentality

With Business Units Functionally Independent, Companies coul Easily Acquire Unrelated Subsidiaries in Order to Expand.

Since the Senior Executives cannot have Technological Expertise in All of the Company’s Lines of Business, Executives Must Judge their Subsidiaries on Abstract Measures like Return on Equity (ROE).

Once Executives View Business Units as easily swapped (like a Lego®), Corporations loose any true coherence (Consider ITT’s ownership of Sheraton, Wonderbread, Avis Car Rental, and Scott Fertilizer during the 1970s).

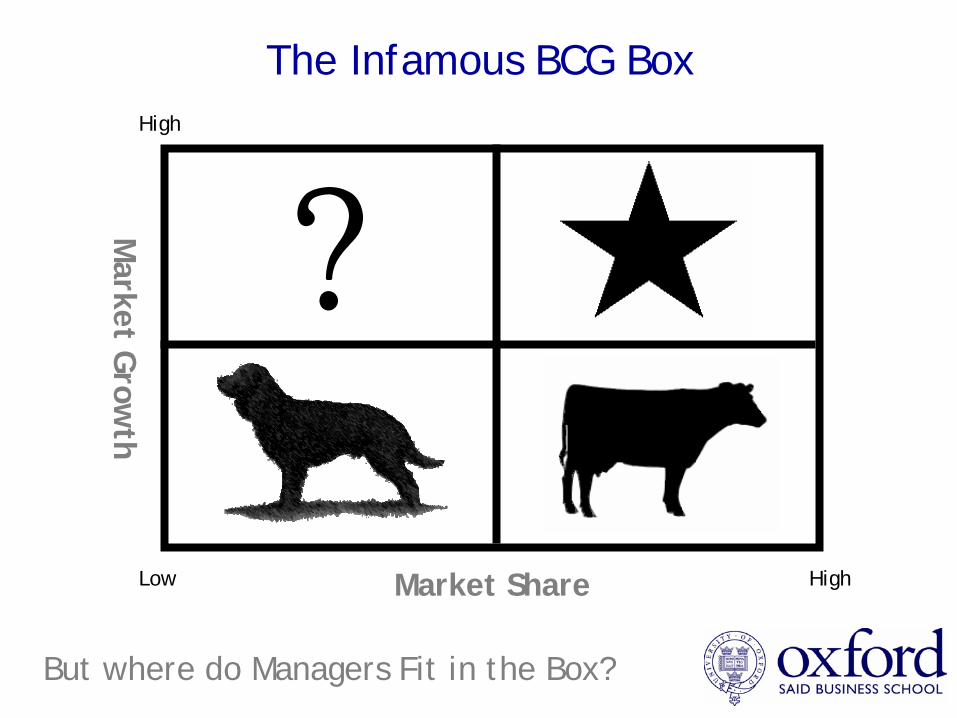

?Market G

rowth

Market Share HighLow

High

The Infamous BCG Box

But where do Managers Fit in the Box?

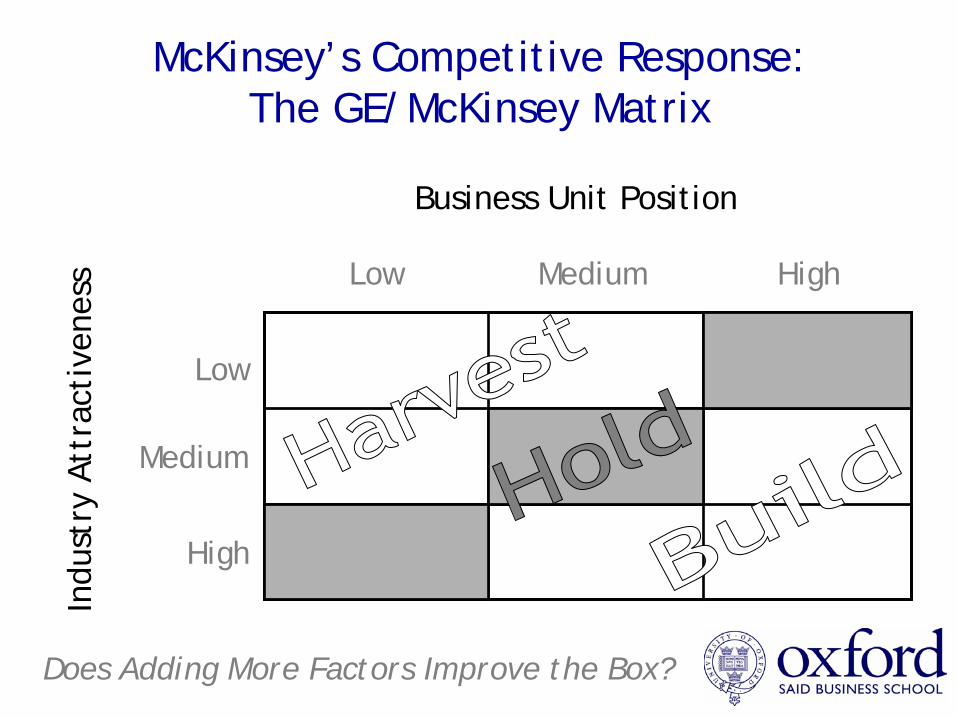

McKinsey’s Competitive Response: The GE/McKinsey Matrix

MediumLow High

Medium

Low

High

Business Unit Position

Indu

stry

Att

ract

iven

ess

Does Adding More Factors Improve the Box?

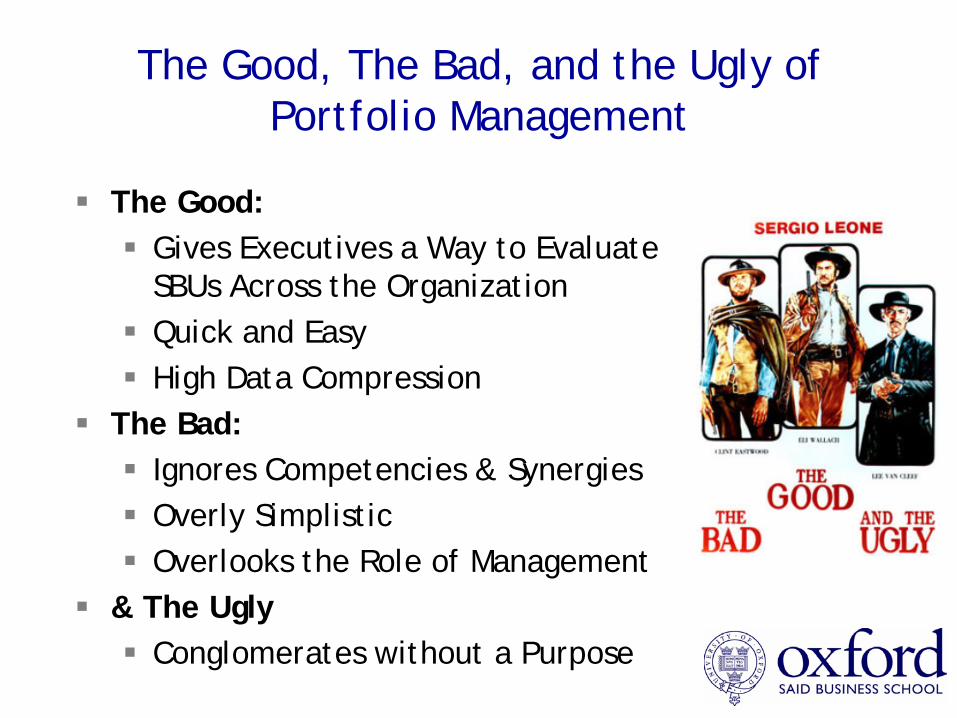

The Good, The Bad, and the Ugly of Portfolio Management

The Good:Gives Executives a Way to Evaluate SBUs Across the OrganizationQuick and EasyHigh Data Compression

The Bad:Ignores Competencies & SynergiesOverly SimplisticOverlooks the Role of Management

& The UglyConglomerates without a Purpose

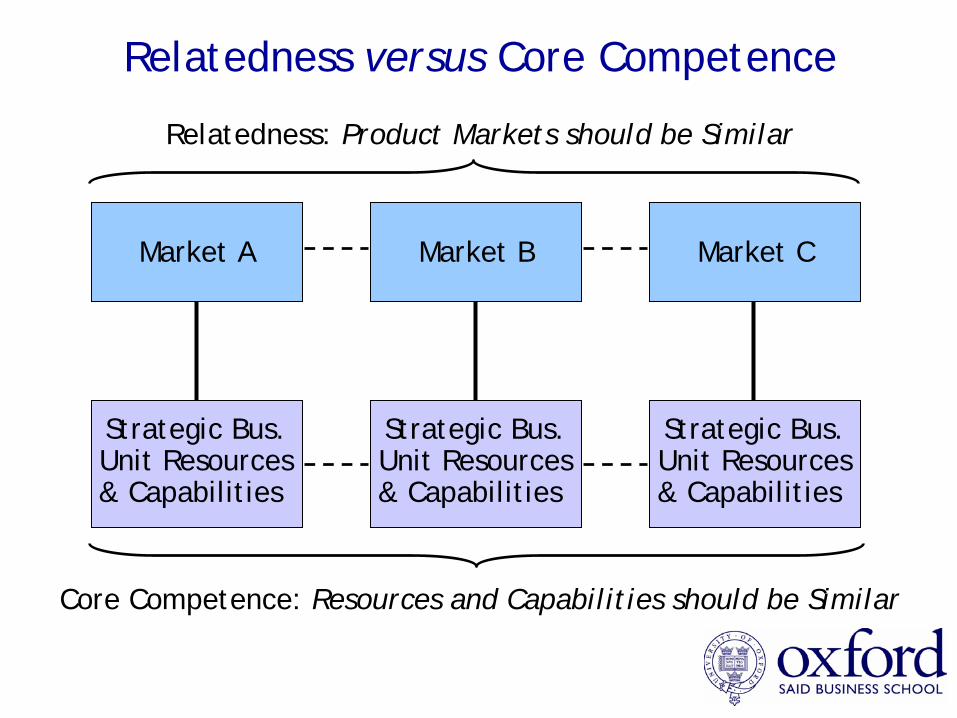

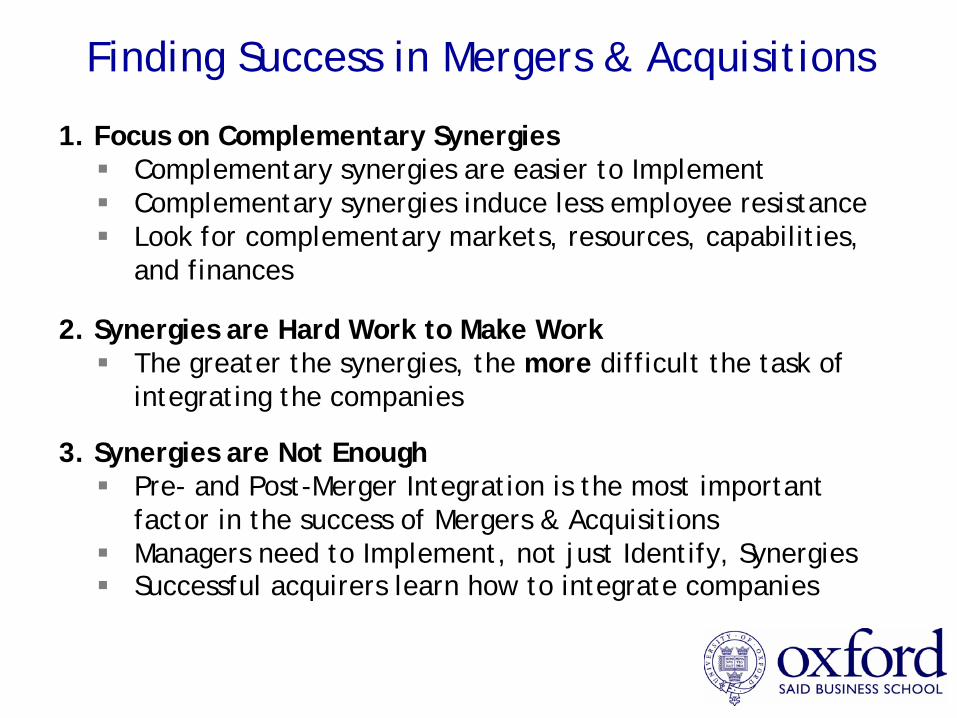

Synergies (or Economies of Scope)

Potential to Employ Your Assets in Other Markets Synergies can be Found in Assets that are Managerial, Industrial, Marketing, or Brand Related.Too Often Used to Justify Mergers and Conglomerates whether or not such synergies exist...

We can all Identify Economies of Scale, But where are there Economies of Scope?

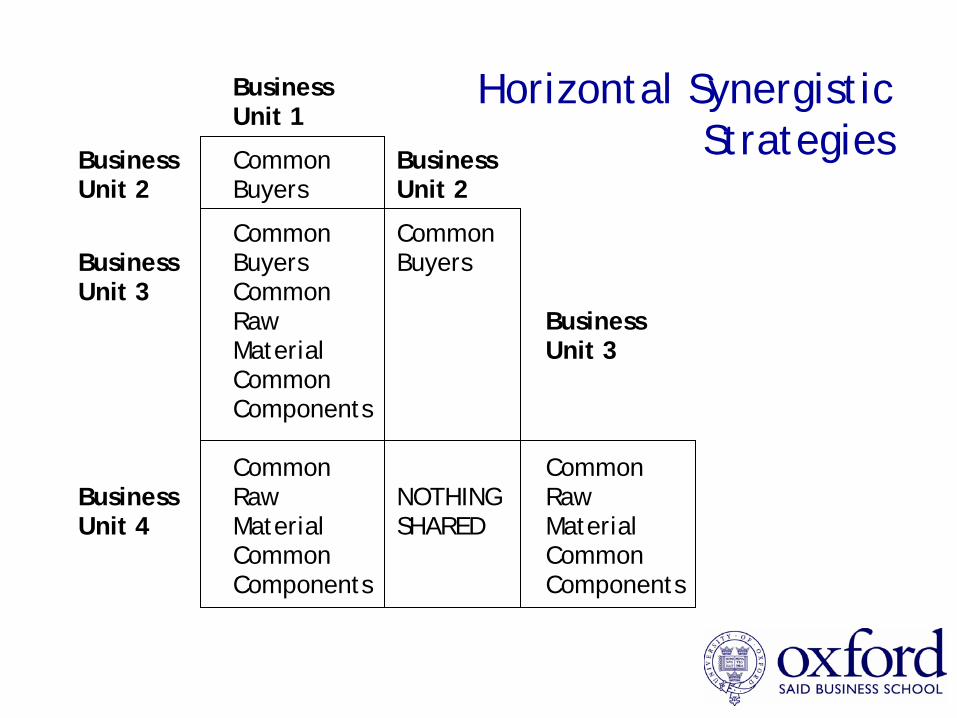

Horizontal Synergistic Strategies

Business Unit 1

Business Unit 2

Common Buyers

Business Unit 2

Business Unit 3

Common Buyers Common Raw Material Common Components

Common Buyers

Business Unit 3

Business Unit 4

Common Raw Material Common Components

NOTHING SHARED

Common Raw Material Common Components

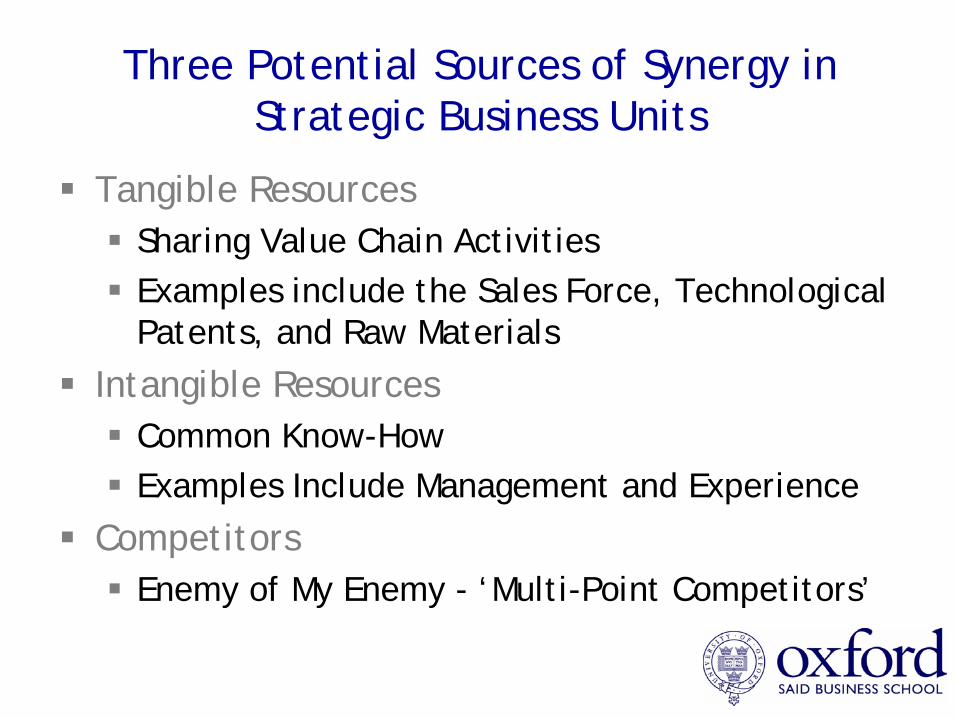

Three Potential Sources of Synergy in Strategic Business Units

Tangible ResourcesSharing Value Chain ActivitiesExamples include the Sales Force, Technological Patents, and Raw Materials

Intangible ResourcesCommon Know-HowExamples Include Management and Experience

CompetitorsEnemy of My Enemy - ‘Multi-Point Competitors’

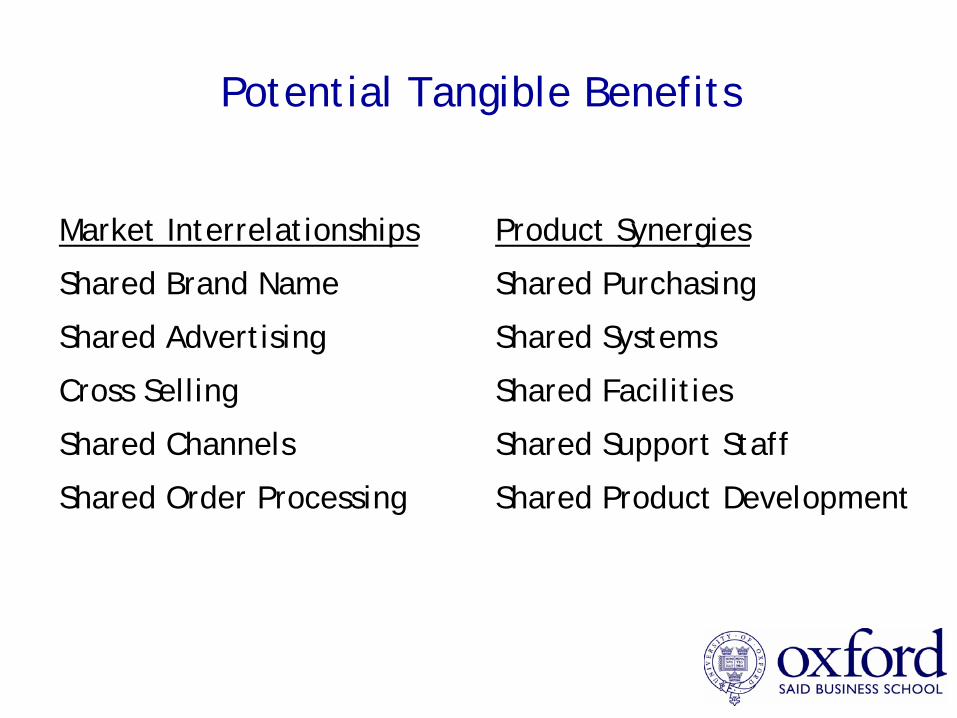

Potential Tangible Benefits

Market Interrelationships

Shared Brand Name

Shared Advertising

Cross Selling

Shared Channels

Shared Order Processing

Product Synergies

Shared Purchasing

Shared Systems

Shared Facilities

Shared Support Staff

Shared Product Development

Intangible Synergies

Transfer of Skills Among Activities

But Intangible Synergies are often Difficult...

Know-How Transfer Expensive

Individuals Lack Motivation to Help

Hard to Retain within the Organization

Potential Liabilities in Trying to Find Synergies

Lost Specialization in Product Segments

Coordination Costs Rise

Diffused Responsibility

Synergies are so Problematic that Financial Analysts Frequently Discount Them in Acquisitions…

“A study of diversification trends amongst Fortune 500 companies during the 1980s by Costas Markides found only a small decline in the proportion of conglomerates…

The outlook for the conglomerate in Europe is even rosier. Taking the long-view, my own research suggests there is a powerful post-war trend towards the building of more conglomerates among the top 100 domestically-owned French, German and British industrial companies. In Britain and Germany, at least, the restructuring of the 1980s and the early 1990s made no difference to the trend, so that by 1993 about a quarter of large industrial companies were conglomerates.”

In Contrast: A European View of Conglomerates

“In Praise of the Evergreen Conglomerate”The Financial Times (1 November 1999), By Richard Whittington

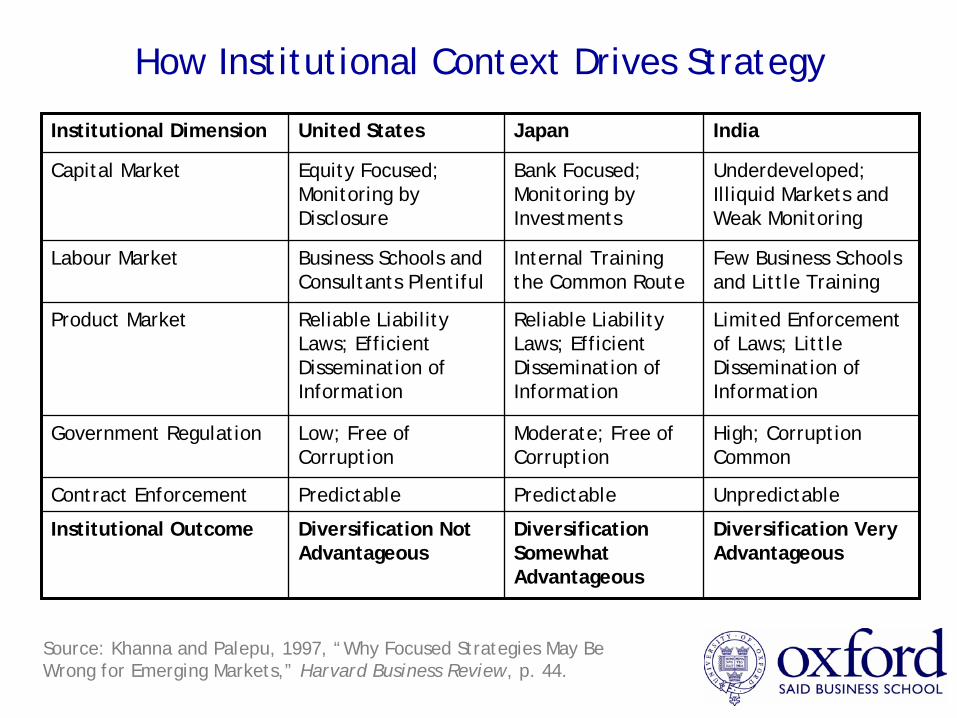

How Institutional Context Drives Strategy

Institutional Dimension United States Japan India

Capital Market Equity Focused; Monitoring by Disclosure

Bank Focused; Monitoring by Investments

Underdeveloped; Illiquid Markets and Weak Monitoring

Labour Market Business Schools and Consultants Plentiful

Internal Training the Common Route

Few Business Schools and Little Training

Product Market Reliable Liability Laws; Efficient Dissemination of Information

Reliable Liability Laws; Efficient Dissemination of Information

Limited Enforcement of Laws; Little Dissemination of Information

Government Regulation Low; Free of Corruption

Moderate; Free of Corruption

High; Corruption Common

Contract Enforcement Predictable Predictable Unpredictable

Institutional Outcome Diversification Not Advantageous

Diversification Somewhat Advantageous

Diversification Very Advantageous

Source: Khanna and Palepu, 1997, “Why Focused Strategies May Be Wrong for Emerging Markets,” Harvard Business Review, p. 44.

Consider Virgin’s Synergies (and Context)…

“We are involved in planes, trains, finance, soft drinks, music, mobile phones, holidays, cars, wines, publishing, bridal wear - the lot! What tie all these businesses together are the values of our brand and the attitude of our people. We have created over 200 companies worldwide, employing over 25,000 people. Our total revenues around the world exceed £4 billion (US$7.2 billion).”

www.virgin.com.uk

Defining Core Competences

A ‘core competence’ is:

A bundle of skills and technologiesOf fundamental customer benefitCompetitively uniqueA gateway to new markets

The notion shifts strategy from a battle of market position, towards a mastery of skills and capabilities.

The key question is:

What are you best at?

Identifying Core Competences

1. Map products and services2. Identify underlying

technologies, skills, processes and resources

3. Synthesise common technologies, skills, processes and resources

4. Check that common technologies, skills, processes and resources are extendable

5. Test their value!

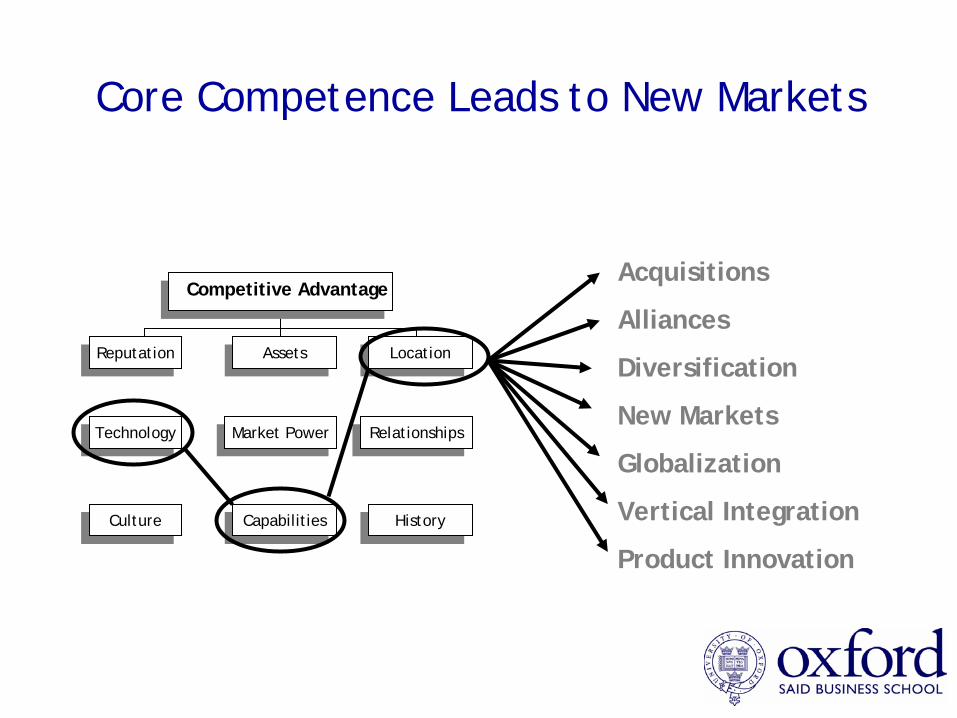

Core Competence Leads to New Markets

ReputationReputation

TechnologyTechnology

AssetsAssets

Market PowerMarket Power

CapabilitiesCapabilities

RelationshipsRelationships

CultureCulture HistoryHistory

LocationLocation

Competitive AdvantageAcquisitions

Alliances

Diversification

New Markets

Globalization

Vertical Integration

Product Innovation

Virgin’s Core Competence?(And its Relationship to Conglomeration?)

“We look for opportunities where we can offer something better, fresher and more valuable, and we seize them. We often move into areas where the customer has traditionally received a poor deal, and where the competition is complacent. And with our growing e-commerce activities, we also look to deliver 'old' products and services in new ways. We are pro-active and quick to act, often leaving bigger and more cumbersome organisations in our wake.”

www.virgin.com.uk

Key Concepts

Hierarchy of Growth

Related Diversification

Portfolio Models

Synergy

Core Competence

Global Strategy

Christopher McKenna

MBAStrategy: Session Six

Michaelmas 2006

Key Concepts and Techniques

Modes of International Expansion

Global Products

Diamond of National Advantage

Globalization is Popularly Linked with Multinationals(And Particularly the Dominance of American Culture)

The Growth in International TradeIncome Inequality Across the GlobeThe Power of Business over the StateThe Spread of CapitalismPolicies of Free Trade & LiberalisationFlows of International CapitalHomogeneity of Consumer CultureThe Spread of Multinational Business

“Globalization” Used to Described:

In this Lecture, We are Concerned with the Best Strategies for “Going Global.”

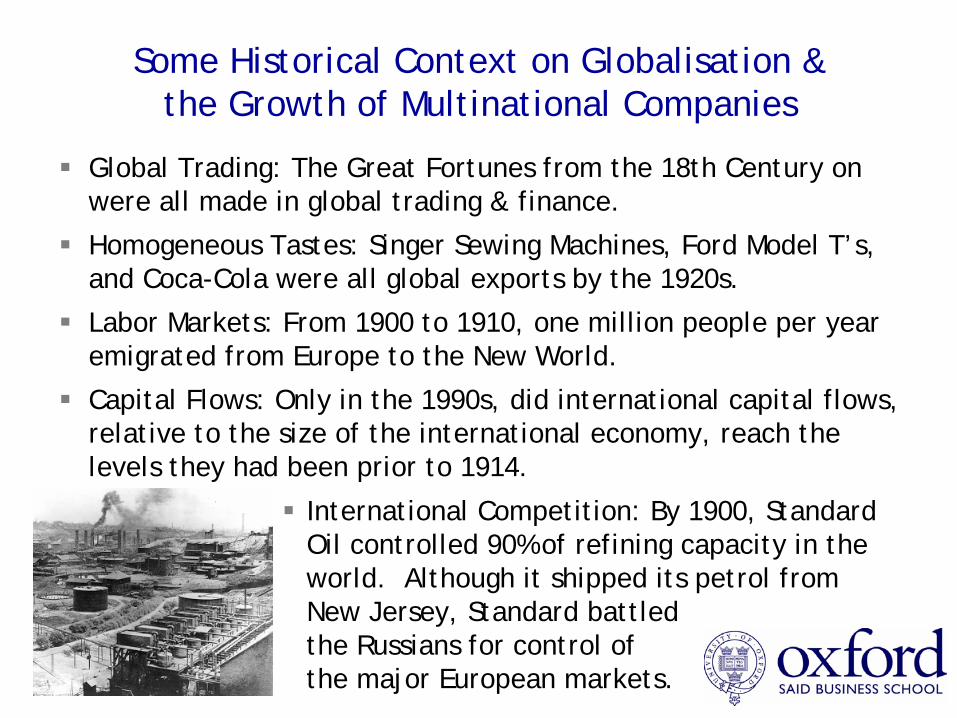

Some Historical Context on Globalisation & the Growth of Multinational Companies

Global Trading: The Great Fortunes from the 18th Century on were all made in global trading & finance.

Homogeneous Tastes: Singer Sewing Machines, Ford Model T’s, and Coca-Cola were all global exports by the 1920s.

Labor Markets: From 1900 to 1910, one million people per year emigrated from Europe to the New World.

Capital Flows: Only in the 1990s, did international capital flows, relative to the size of the international economy, reach the levels they had been prior to 1914.

International Competition: By 1900, Standard Oil controlled 90% of refining capacity in the world. Although it shipped its petrol from New Jersey, Standard battled the Russians for control of the major European markets.

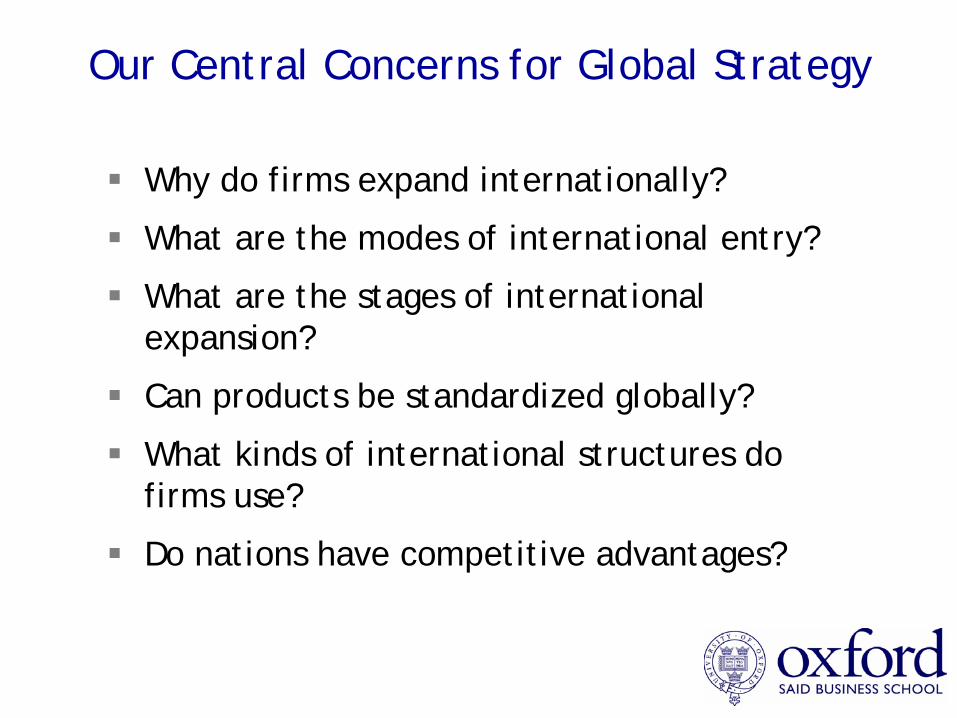

Our Central Concerns for Global Strategy

Why do firms expand internationally?

What are the modes of international entry?

What are the stages of international expansion?

Can products be standardized globally?

What kinds of international structures do firms use?

Do nations have competitive advantages?

The Five Myths of Global Strategy

Distance and National Borders No Longer MatterConsider the World after the 9-11 AttackDeveloping Countries are the Best New MarketsDeveloped Countries remain the largest marketsManufacture Where the Labor is CheapestKnowledge, Infrastructure, and Shipping Costs CrucialGlobalization will Last ForeverThe Global Economy has Contracted BeforeGovernments No Longer MatterRegulations and Nationalisation can Trump the Plans of any Corporation…

Source: Rangan, FT: Mastering Strategy, 2000

The Hierarchy of Growth

Revamp Packaging, Pricing, Promotions

Expand into New Domestic Territories

Develop New, Related Products and Services

Export Current Products Abroad

Acquire a Competitor

Expand Internationally

Acquire in a Related, Growing Industry

Integrate Vertically – Acquire a Supplier or Customer

Acquire in an Unrelated, Growing Industry

Early Strategies

Late Strategies

Why Do Firms Expand Internationally?

ACCESS TO OUTPUT MARKETSSatisfies demands for growthDomestic markets saturated; overseas markets largeScale economies; location or distribution platformsA way to expand without diversifying and still based up the firm’s core competence

ACCESS TO INPUT MARKETSAccess to low-cost labor or materialsAccess to the best knowledge, skills, & workersAccess to technology, best practices, & external capital markets

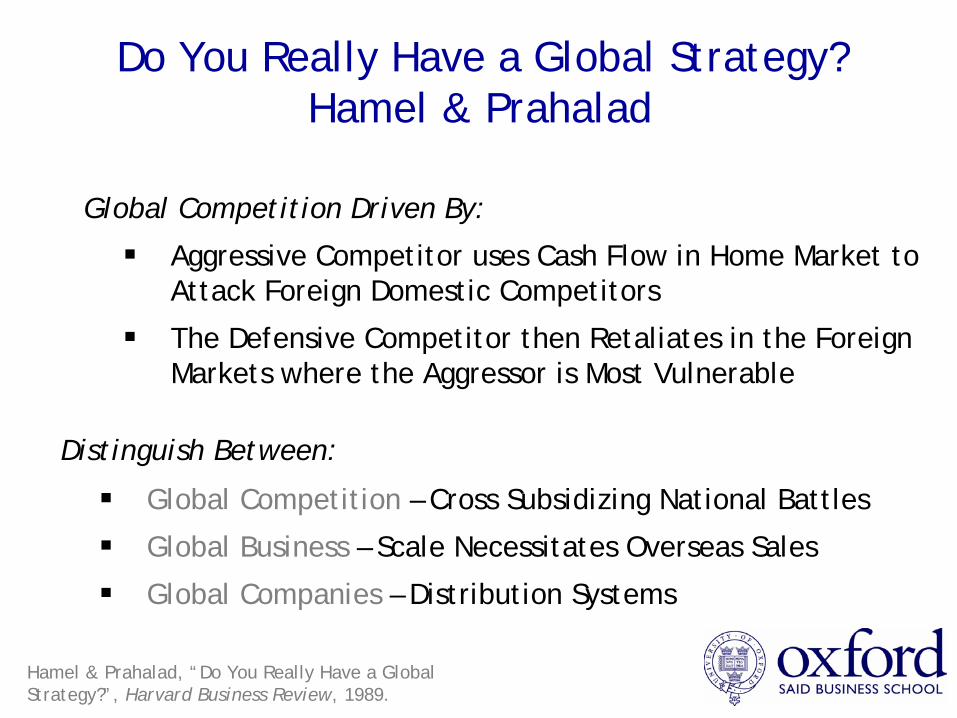

Do You Really Have a Global Strategy?Hamel & Prahalad

Global Competition Driven By:

Aggressive Competitor uses Cash Flow in Home Market to Attack Foreign Domestic Competitors

The Defensive Competitor then Retaliates in the Foreign Markets where the Aggressor is Most Vulnerable

Distinguish Between:

Global Competition – Cross Subsidizing National Battles

Global Business – Scale Necessitates Overseas Sales

Global Companies – Distribution Systems

Hamel & Prahalad, “Do You Really Have a Global Strategy?”, Harvard Business Review, 1989.

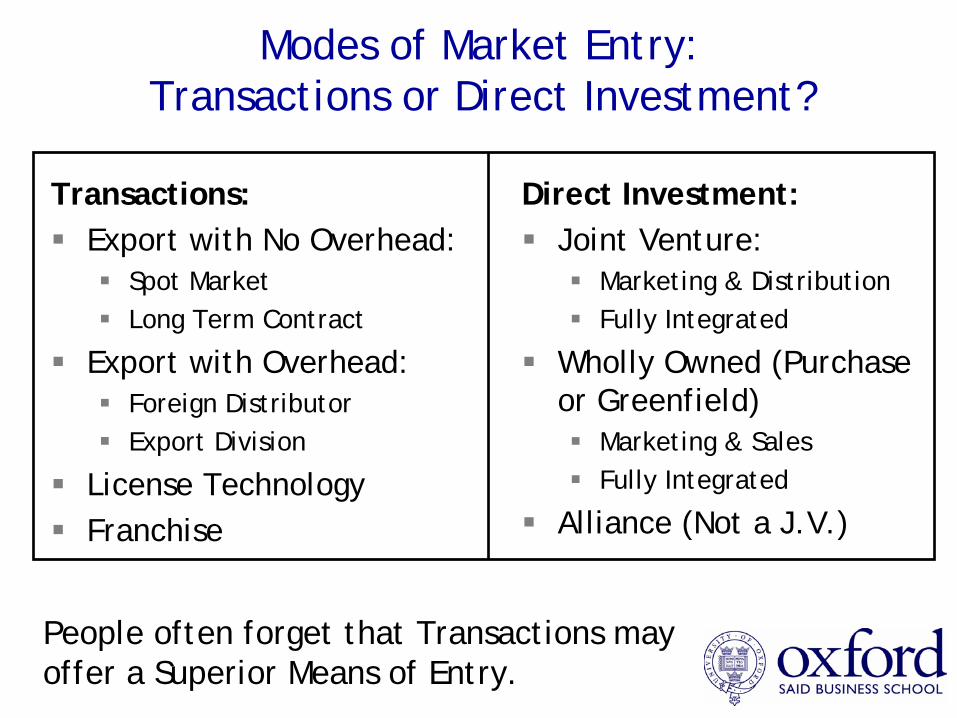

Modes of Market Entry: Transactions or Direct Investment?

Transactions:Export with No Overhead:

Spot Market Long Term Contract

Export with Overhead:Foreign DistributorExport Division

License TechnologyFranchise

Direct Investment:Joint Venture:

Marketing & DistributionFully Integrated

Wholly Owned (Purchase or Greenfield)

Marketing & SalesFully Integrated

Alliance (Not a J.V.)

People often forget that Transactions may offer a Superior Means of Entry.

Moving from Domestic to Global Competition

Stage 1: Domestic CompetitorMore than 80% of sales within home country; limited exports, licensing, outsourcing, franchising: Sainsbury’s

Stage 2: International CompetitorMore than 20% of sales outside the home country; mainly alliances or exports to large markets, some direct investment (FDI): Airbus, Apple

Stage 3: Multinational CompetitorMajority of sales outside of home country; exports, outsourcing, alliances, FDI, host country staffing: KPMG, Coca-Cola

Stage 4: Global CompetitorRevenues globally balanced; significant alliances, FDI, large commitments in host countries: Toyota, Unilever

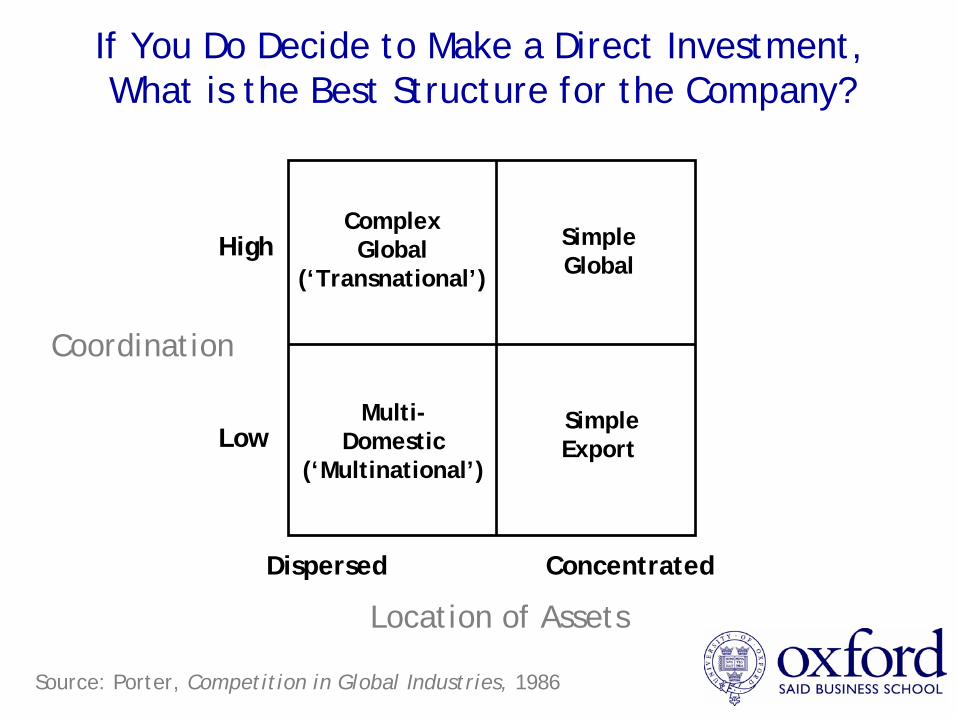

If You Do Decide to Make a Direct Investment,What is the Best Structure for the Company?

Source: Porter, Competition in Global Industries, 1986

Coordination

Location of Assets

High

Low

Dispersed Concentrated

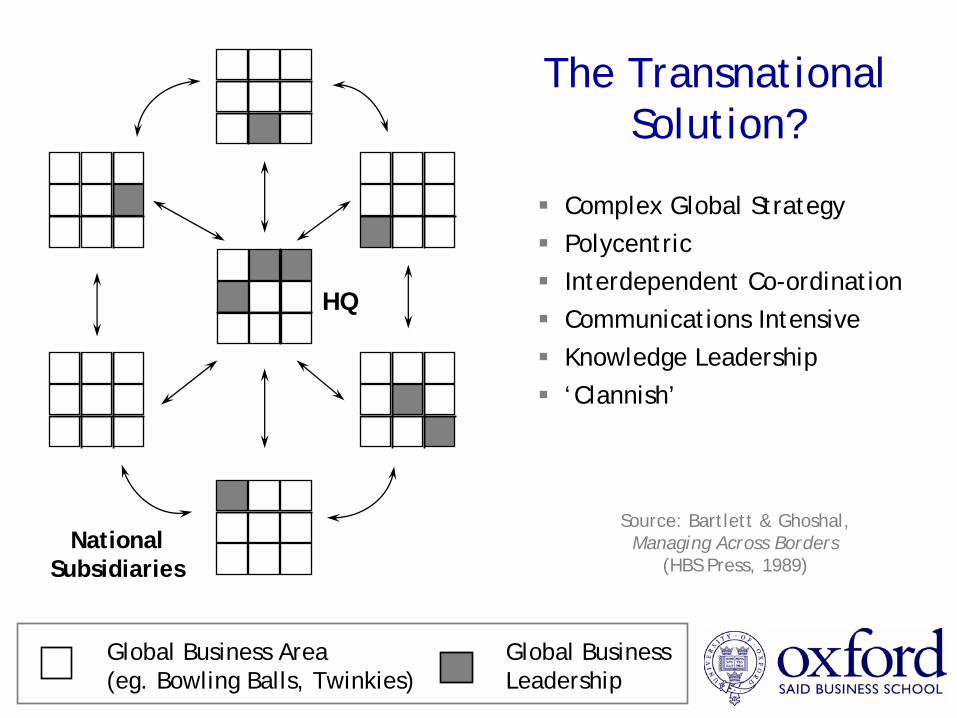

ComplexGlobal

(‘Transnational’)

SimpleExport

Multi-Domestic

(‘Multinational’)

SimpleGlobal

Margins

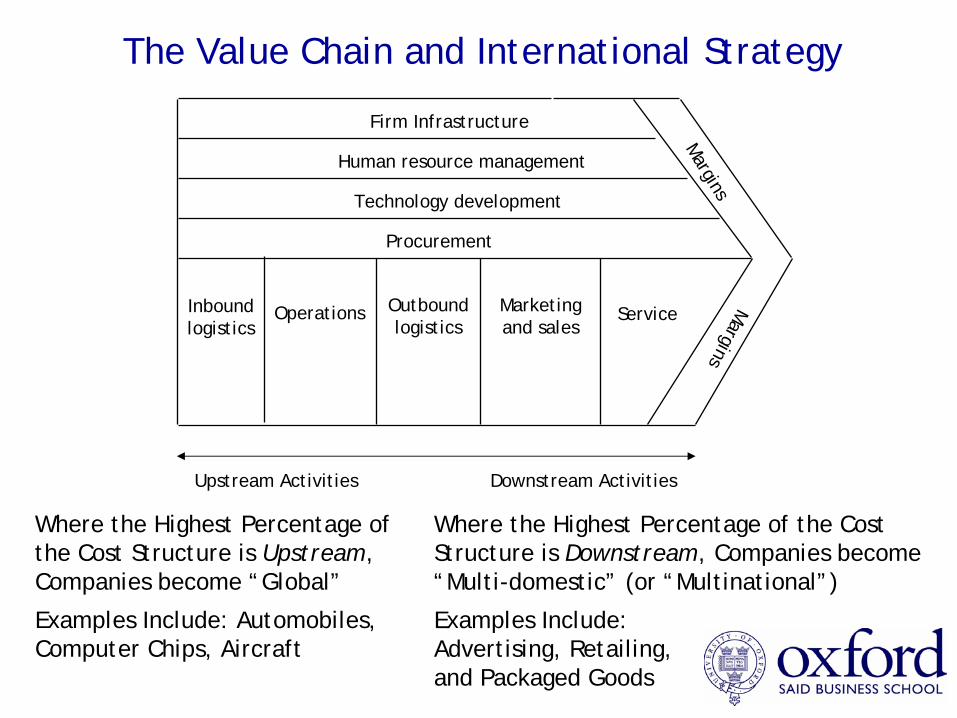

Firm Infrastructure

Human resource management

Technology development

Procurement

Inbound logistics

Operations Outbound logistics

Marketing and sales

Service

Margins

The Value Chain and International Strategy

Upstream Activities Downstream Activities

Where the Highest Percentage of the Cost Structure is Downstream, Companies become “Multi-domestic” (or “Multinational”)

Examples Include: Advertising, Retailing, and Packaged Goods

Where the Highest Percentage of the Cost Structure is Upstream, Companies become “Global”

Examples Include: Automobiles, Computer Chips, Aircraft

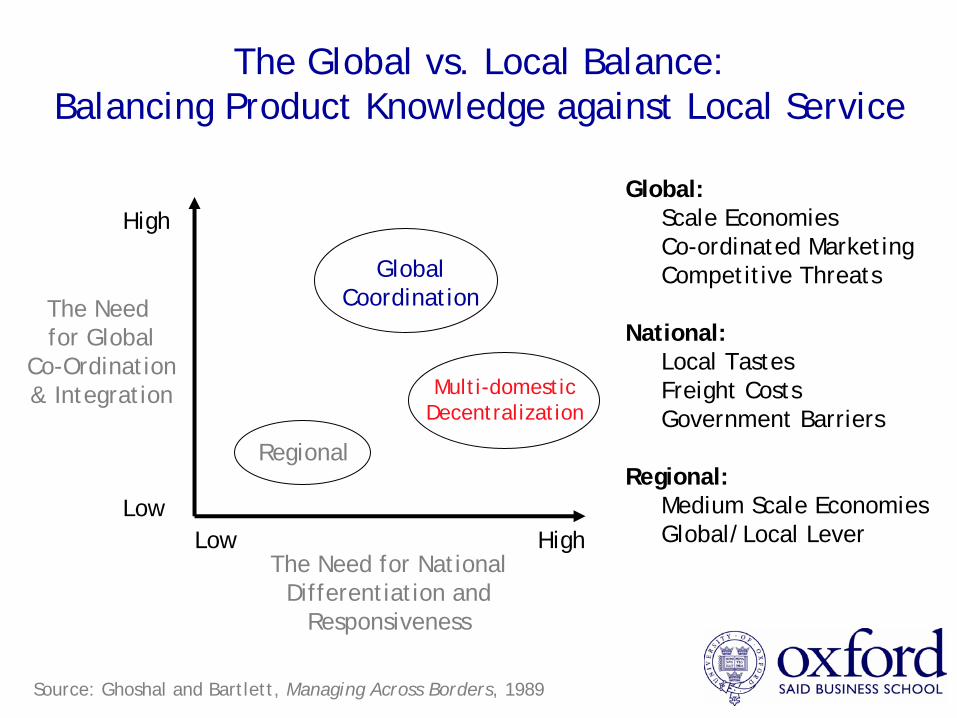

The Need for Global

Co-Ordination& Integration

The Need for NationalDifferentiation and

Responsiveness

High

LowLow High

The Global vs. Local Balance:Balancing Product Knowledge against Local Service

Global:Scale Economies Co-ordinated MarketingCompetitive Threats

National: Local TastesFreight CostsGovernment Barriers

Regional:Medium Scale EconomiesGlobal/Local Lever

Source: Ghoshal and Bartlett, Managing Across Borders, 1989

Multi-domesticDecentralization

GlobalCoordination

Regional

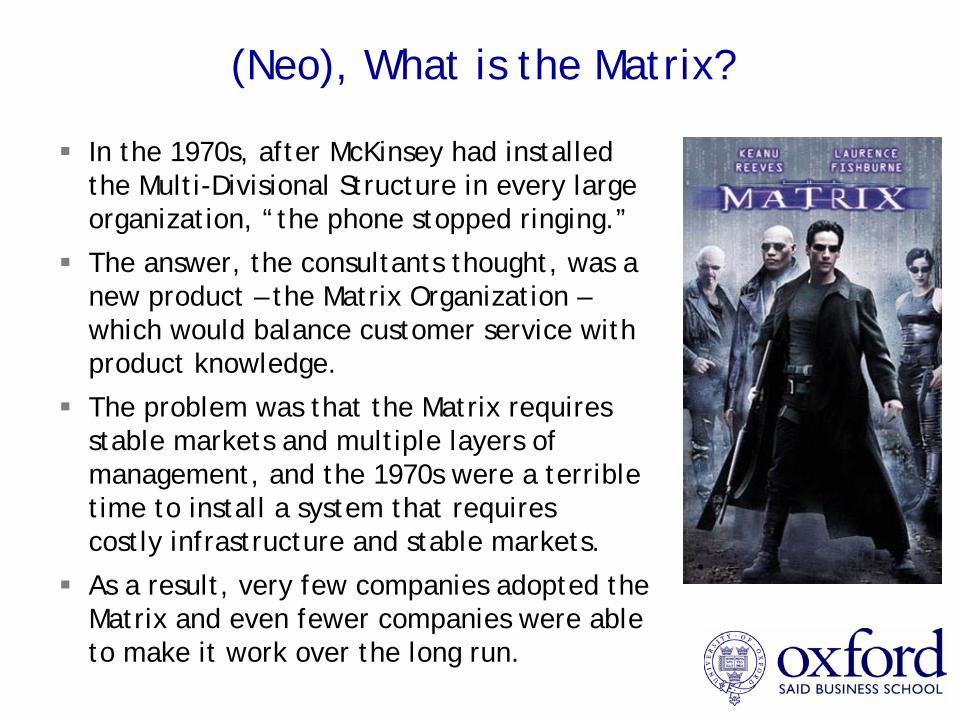

(Neo), What is the Matrix?

In the 1970s, after McKinsey had installed the Multi-Divisional Structure in every large organization, “the phone stopped ringing.”

The answer, the consultants thought, was a new product – the Matrix Organization –which would balance customer service with product knowledge.

The problem was that the Matrix requires stable markets and multiple layers of management, and the 1970s were a terrible time to install a system that requires costly infrastructure and stable markets.

As a result, very few companies adopted the Matrix and even fewer companies were able to make it work over the long run.

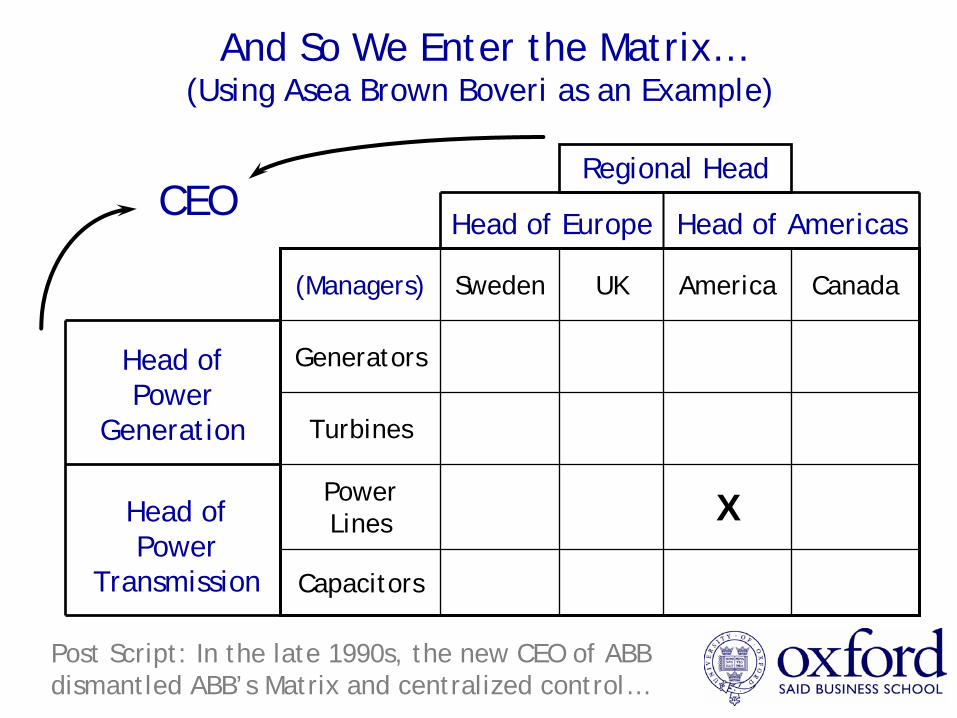

And So We Enter the Matrix…(Using Asea Brown Boveri as an Example)

(Managers) Sweden UK America Canada

Generators

Turbines

Power Lines X

Capacitors

Head of Europe Head of Americas

Head of Power

Generation

Head of Power

Transmission

Regional HeadCEO

Post Script: In the late 1990s, the new CEO of ABB dismantled ABB’s Matrix and centralized control…

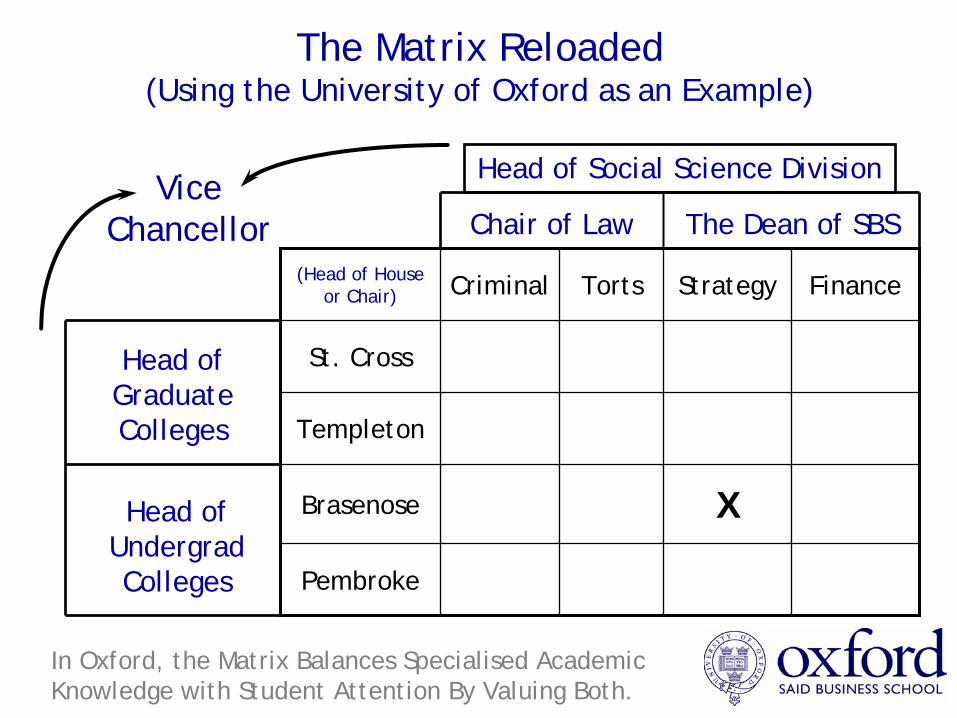

The Matrix Reloaded(Using the University of Oxford as an Example)

(Head of House or Chair) Criminal Torts Strategy Finance

St. Cross

Templeton

Brasenose X

Pembroke

Chair of Law The Dean of SBS

Head of Graduate Colleges

Head of Undergrad Colleges

Head of Social Science DivisionVice

Chancellor

In Oxford, the Matrix Balances Specialised Academic Knowledge with Student Attention By Valuing Both.

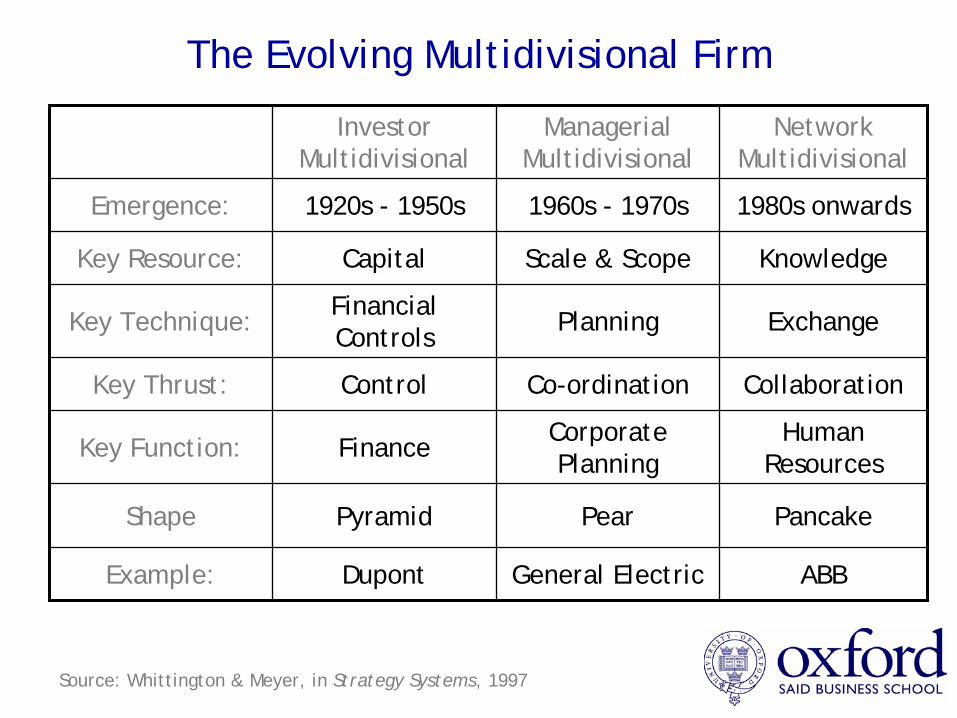

Investor Multidivisional

Managerial Multidivisional

Network Multidivisional

Emergence: 1920s - 1950s 1960s - 1970s 1980s onwards

Key Resource: Capital Scale & Scope Knowledge

Key Technique: Financial Controls

Planning Exchange

Key Thrust: Control Co-ordination Collaboration

Key Function: Finance Corporate Planning

Human Resources

Shape Pyramid Pear Pancake

Example: Dupont General Electric ABB

The Evolving Multidivisional Firm

Source: Whittington & Meyer, in Strategy Systems, 1997

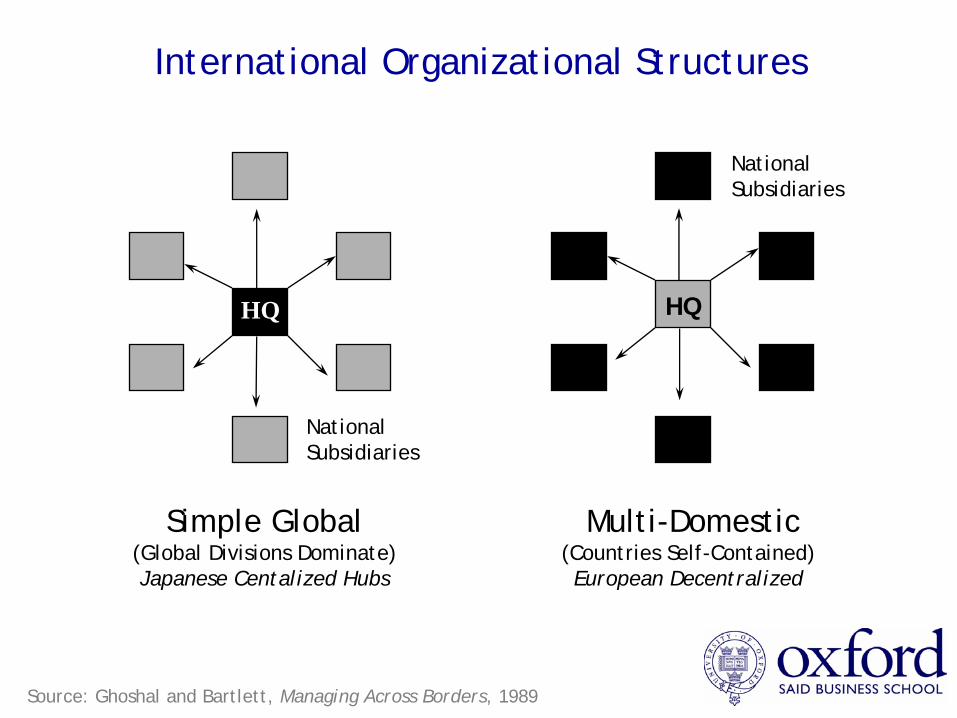

Multi-Domestic(Countries Self-Contained)European Decentralized

International Organizational Structures

National Subsidiaries

HQ

Simple Global(Global Divisions Dominate)Japanese Centalized Hubs

National Subsidiaries

HQ

Source: Ghoshal and Bartlett, Managing Across Borders, 1989

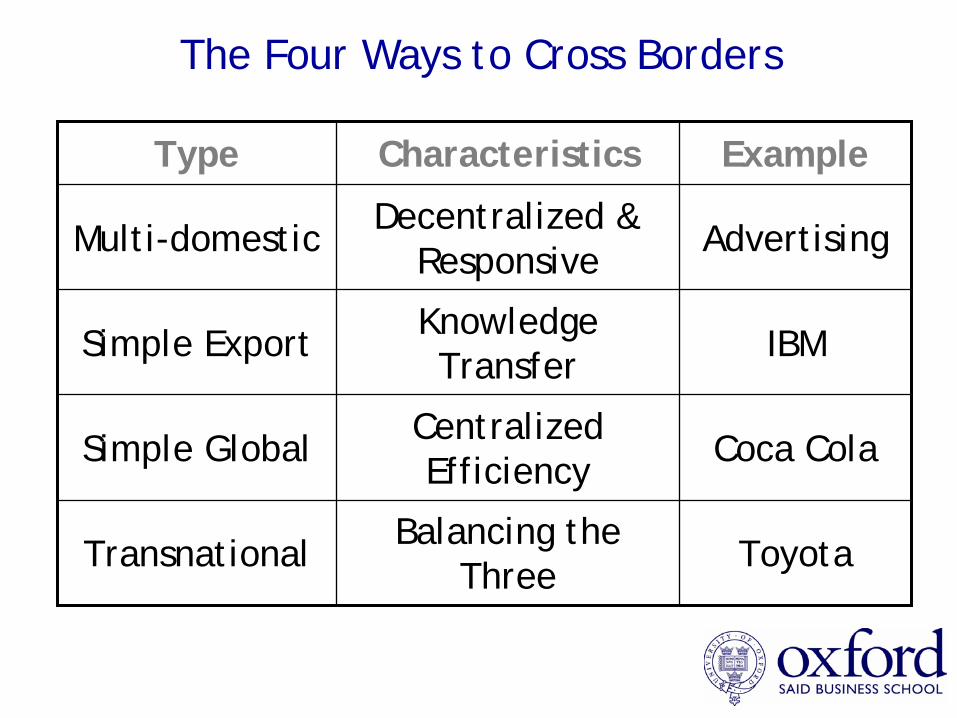

The Four Ways to Cross Borders

Type Characteristics Example

Multi-domestic Decentralized & Responsive Advertising

Simple Export Knowledge Transfer IBM

Simple Global Centralized Efficiency Coca Cola

Transnational Balancing the Three Toyota