Mba - Afm - Analysis of Financial Statements

100

ANALYSIS OF FINANCIAL STATEMENTS Unit III

-

Upload

vijayaraj-jeyabalan -

Category

Documents

-

view

215 -

download

0

Transcript of Mba - Afm - Analysis of Financial Statements

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 1/100

ANALYSIS OFFINANCIAL

STATEMENTS

Unit III

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 2/100

Syllabus

Analysis of FinancialStatements

Financial Ratio AnalysisCash Flow

(as per Accounting Standard 3)

Funds Flow Statement Analysis.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 3/100

Analysis of Financial

Statements

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 4/100

Financial StatementAnalysis

American Institute of certied public accountssays ! nancial statements are prepared forthe purpose of presenting a periodical re"iew

or report on the progress by the managementand dealt with

#he status of in"estment in the business and

#he result achie"ed during the period under

re"iew.A nancial statement is an organi$edcollection of data.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 5/100

Financial Statement

Types of Financial Statements

%rot and &oss account or

Income statement'alance Sheet or Statement of

nancial position

A surplus statement or retainedearnings statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 6/100

Financial Statement

Schedules to nancial statements

Schedule of ed assets

Schedule of debtorsSchedule of creditors

Schedule of in"estment

Statement of changes in woringcapital

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 7/100

Financial Statement

!ot and Loss account o! Income statement

It matches the re"enue and costs incurred in theprocess of earning re"enues and shows the net protearned or loss su*ered during a particular period.

"alance Sheet

It is the statement which shows the assets andliabilities of the business. It re+ects the nancialcondition of a business concern as re"ealed by the

accounting records. It shows the assets owned by theconcern and the source of funds used in theac,uisition of those assets.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 8/100

Financial Statement

Su!plus o! #etained ea!nin$s statement

It re+ects to ecess of prot o"er losses. Suchretained earnings are taen to balance sheet fromthe retained earnings statement. It is a lin betweenthe balance sheet and the income statement.

Supplementa!y schedules

&ists of schedules are used to supplement the dataand details contained in the balance sheet and prot

and loss account. #he schedules re considered to bepart and parcel of the nancial statements for thebenet of analysis and interpretation.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 9/100

-ature of nancialstatements

Financial statements are prepared tochec the nature of in"estment in abusiness and result achie"ed during the

specic time period. Financial statementsshows /

'ased on recorded facts

Accounting con"entions%ostulates (assumptions0suggestions)

%ersonal 1udgment

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 10/100

Financial Statement

Limitations

Information shown in nancial statements are notaccurate.

It is based on practical eperience andcon"entions

2o not disclose correct position of the business

2o not disclose the contribution of humanresource towards the eciency of the business

It is prepared by way of comparing two di*erentperiods

Record only monetary facts

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 11/100

Analysis and Interpretation

Analysis and Interpretation are inter/related.Interpretation re,uires Analysis4 while Analysis isuseless without interpretation.

Analysis means methodical classication of the data

gi"en in the nancial statements. Interpretationmeans eplaining the meaning and signicance of the

data so simplied0classied.

Analysis may be described as a critical eamination of

nancial transactions e*ected during a denite periodof time and Interpretation is drawing of inference(suggestion or conclusion) and stating what thegures in the nancial statement really mean.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 12/100

Analysis and Interpretation

According to 5ennedy and 6uller4 ! the analysis andinterpretation of nancial statements are anattempt to determine the signicance and meaningof the nancial statement data so that forecast may

be made of the prospects for future earnings4 abilityto pay interest and debt maturities andchance0probability of a sound di"idend policy7.

Interpretation includes many processes lie

arrangement4 analysis4 establishing relationshipbetween a"ailable fact and nally maingconclusions.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 13/100

8b1ecti"es

#o interpret the protability and eciency of"arious business acti"ities with the help of protand loss account.

#o determine the managerial eciency of therm.

#o measure short/term and long/term sol"ency ofthe business.

#o ascertain earning capacity in future period.

#o compare operational eciency.

#o determine protability of the concern.

#o measure the nancial stability of the business.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 14/100

Financial StatementAnalysis

Financial Statement Analysis isclassied below/

8n the basis of information used

9ternal Analysis Internal Analysis

8n the basis of modus operandi ofanalysis

:ori$ontal Analysis ;ertical Analysis

8n the basis of ob1ecti"es of analysis

&ong/term Analysis Short/term

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 15/100

Financial StatementAnalysis

8n the basis of information used

E%te!nal Analysis

It is made by those who do not ha"e access to

detailed record and depend on publishedstatements. Such type of analysis is made byin"estors4 credit agencies4 go"ernment agenciesand research scholars.

Inte!nal AnalysisIt is done on the basis of unpublished records bythe eecuti"es. It is "ery much useful andsignicant to employees and management.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 16/100

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 17/100

Financial StatementAnalysis

8n the basis of ob1ecti"es of analysis

Lon$)te!m Analysis

#his analysis is used for understanding the long/

term nancial stability4 sol"ency and li,uidity aswell as protability and earning capacity of aorgani$ation.

Sho!t)te!m Analysis

#his analysis is used to determine the short/termsol"ency of the business concern. Stability4li,uidity and earning capacity of the business isalso analy$ed.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 18/100

#echni,ues ofAnalysis and Interpretation.

Comparati"e statements

Common si$e statements

Fund +ow analysisCash +ow analysis

Ratio analysis

-et woring capital analysis #rend analysis

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 19/100

Comparati"estatement analysis

Compa!ati*e statement analysis

It is a techni,ue used to analy$e the nancialstatement. #his statement summari$es and presentsrelated data for a number of years.

#hese statements are prepared in a way so as topro"ide time prospecti"e to the consideration of"arious elements of nancial position embodied in suchstatements.

#hese statements normally contains comparati"ebalance sheet and comparati"e income statement.

Comparati"e balance sheet is a statement which shows

changes in total capital and changes in woring capital

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 20/100

Comparati"e Statements / specimen

a!ticula!s +,-, +,-- Inc!ease .ec!ease

Current Assets(a)

Fied Assets(b)

#otal Assets (a= b)

Current &iabilities(a)

&ong #erm &iabilities

(b)

#otal &iabilities (a= b)

Capital and Reser"es

Shareholders Funds( c )

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 21/100

Common Si$e Statements

Common si$e statements indicate the relationshipof "arious items with some common items. It shouldbe denoted in percentage of common items.

#hese statements normally contains common si$e

balance sheet and common si$e income statement.

a!ticula!s

+,-, / +,-- /

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 22/100

Funds Flow Statement

Funds +ow statement indicated the sources andapplication of funds. #he term funds refer tochanges in woring capital. Funds +owstatement clearly shows internal source andeternal source of woring capital and the wayfunds ha"e been used. Funds +ow is deri"edfrom analysis of changes which ha"e taenplace in assets and e,uities between twobalance sheets.

A statement of sources and application of fundsis a technical de"ice designed to analy$e the

changes in nancial position of a businessconcern between two eriods.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 23/100

Cash Flow Statement

Cash +ow statement shows thechanges in cash position. It re+ects thein+ows and out+ows of cash.

#his statement is prepared to nowclearly the "arious items of in+ow andout+ow of cash.

It is an essential tool for short/termnancial analysis and is "ery helpful inthe e"aluation of current li,uidity of

the business concern.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 24/100

Ratio Analysis

Ratio analysis refers to the numerical relationshipbetween two numbers.

An accounting ratio shows the relationshipbetween the two inter/related accounting guresas gross prot to sales4 current assets tocurrent liabilities4 loaned capital to owned capital.

Ratio analysis is the process of computing4determining and presenting the relationship ofitems. It also includes comparison andinterpretation of ratios and using them as basisfor the gure pro1ection.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 25/100

-etworing Capital Analysis

-ormally woring capital refers to the di*erencebetween current assets and current liabilities of thebusiness concern.

Current Assets are cash4 ban4 debtors4 bills

recei"able4 stoc4 prepaid epenses4 ad"ances andshort term in"estments.

Current &iabilities are sundry creditors4 bills payable4ban o"erdraft4 outstanding epenses4 pro"isions4

proposed di"idend etc.4-etworing capital statement or schedule changes inworing capital is prepared to disclose net changes inworing capital on two specic periods.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 26/100

#rend Analysis

#rend analysis is an important tool of hori$ontalnancial analysis. #his method plays a "ital roleto maing a comparati"e study of the nancialstatements of se"eral periods.

#rend analysis is carried out by calculating trendratio (>) and plotting the accounting data ongraph sheet or paper.

#rend analysis is signicant for forecasting andbudgeting. #rend analysis discloses the changesin nancial and operating data between specicperiods.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 27/100

&imitations ofFinancial Statement Analysis

:istorical nature of nancialstatements

Reliability of gures

'ased on past records

2i*erent interpretation

Change in accounting methods

Single year analysis is not much useful

%rice le"el changes

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 28/100

#atio Analysis

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 29/100

Ratio Analysis

Accounting ratios are relationships epressed inmathematical terms between gures which areconnected with each other in some manner.

Accounting ratios can be epressed as

A pure ratio

A rate

A percentage

Ratio analysis stands for the process of determining

and presenting the relationship of items and groupof items in the nancial statements. It is animportant method of nancial analysis.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 30/100

Ratio Analysis

Me!its

?seful in nancial position analysis

?seful in simplifying accounting gures

?seful in assessing the operationaleciency

?seful in forecasting purposes

?seful in locating the woring of thebusiness

?seful in comparison of performance

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 31/100

Ratio Analysis

Limitations

%ractical nowledge and eperience

Inter/relationship

-on/a"ailability of standards or norms

Accuracy of nancial information

Consistency in preparation of nancial

statement #ime delay

Change in price le"el

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 32/100

Ratio Analysis

Classication of #atios

Classication by Statements

'alance Sheet4 %rot and &oss A0c and Compositeratios

Classication by users

Ratios for 6anagement4 Creditors and Shareholders

Classication by relati"e importance

%rimary4 Secondary4 Creditors and @rowth ratiosClassication of ratios by purpose

%rotability4 #urno"er and Sol"ency ratios

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 33/100

Classication of Ratios by

Statements

F!om "alance Sheet

&i,uid Ratio4 Current Ratio4 Ade,uate &i,uid Ratio4%roprietary Ratio4 Fied Assets Ratio4 2ebt 9,uity Ratioand Capita @earing Ratio.

F!om !ot 0 Loss@ross %rot Ratio4 8perating %rot Ratio4 -et %rotRatio and 9penses Ratio.

Composite #atios

Return on in"estment4 Return on net worth4 Stoc #urno"er Ratio4 2ebtors #urno"er Ratio4 Creditors

#urno"er Ratio4 Fied Assets #urno"er Ratio4 9arning perShare Ratio and %ayout Ratio.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 34/100

Classication by ?sers#atios fo! Mana$ement

8perating Ratio4 Stoc #urno"er Ratio4 2ebtors #urno"er Ratio4 Fied Assets #urno"er Ratio4 Creditors #urno"er Ratio4 Boring Capital #urno"er Ratio4 -et%rot Ratio4 @ross %rot Ratio4 8perating %rot Ratio4

Short term Sol"ency Ratio and &ong term Sol"encyRatio.

#atios fo! C!edito!s

Fied charges co"er Ratio4 2ebt Ser"ice co"er Ratio4

&i,uid Ratio4 Current Ratio4 2ebt 9,uity Ratio4 Capital@earing Ratio4 Sol"ency Ratio and Creditors #urno"erRatio.

#atio fo! Sha!eholde!s

Return on Shareholders fund4 Shareholders fund4%ayout ratio4 2i"idend yield ratio4 2i"idend co"er ratio

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 35/100

2etailed Formulaefor Calculating Ratios

!ota1ility #atios#etu!n on In*estment

8perating %rot DD

Capital 9mployed#etu!n on Sha!eholde!s2 fund

-et %rot after ta and interest DD

Shareholders fund

#etu!n on E3uity Sha!eholde!s2 fund

-et %rot after ta and %ref. di"idend DD

9,uity Shareholders fund

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 36/100

2etailed Formulaefor Calculating Ratios

#etu!n on Total Assets

-et %rot after ta and interest DD

Shareholders fund

4!oss !ot #atio

@ross %rot DD

-et Sales

Ope!atin$ !ot #atio8perating %rot DD

-et Sales

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 37/100

2etailed Formulaefor Calculating Ratios

E%penses #atio

Specic epenses DD

-et Sales

Net !ot #atio

-et %rot DD

-et Sales

Ea!nin$ pe! sha!e 5ES6-et %rot after ta and %ref. di"idend DD

-o. of e,uity shares

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 38/100

2etailed Formulaefor Calculating Ratios

!ice Ea!nin$ #atio

6aret price per e,uity share

9arning per e,uity share

ayout #atio

9,uity 2i"idend DD

-et %rot after ta and %ref. di"idend

#etainin$ Ea!nin$s #atioRetained 9arnings DD

-et %rot after ta and %ref. di"idend

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 39/100

2etailed Formulaefor Calculating Ratios

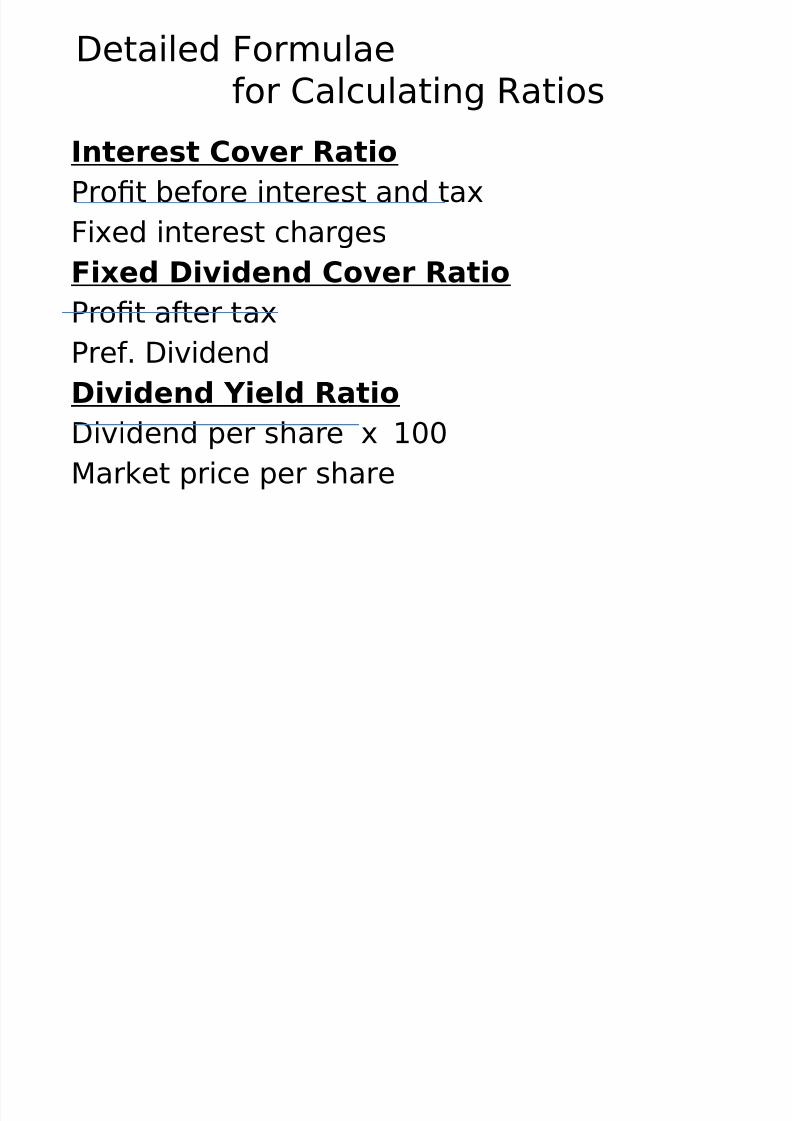

Inte!est Co*e! #atio

%rot before interest and ta

Fied interest charges

Fi%ed .i*idend Co*e! #atio

%rot after ta

%ref. 2i"idend

.i*idend Yield #atio2i"idend per share DD

6aret price per share

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 40/100

2etailed Formulaefor Calculating Ratios

Tu!no*e! #atiosIn*ento!y Tu!no*e! #atio

Cost of goods soldA"erage Stoc

.e1to!s Tu!no*e! #atio

-et Credit SalesA"erage recei"able

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 41/100

2etailed Formulaefor Calculating Ratios

C!edito!s2 Tu!no*e! #atio

-et credit purchase

A"erage accounts payable

7o!8in$ Capital Tu!no*e! #atio

Cost of Sales

-et Boring Capital(Boring Capital E Current Assets Current&iabilities)

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 42/100

2etailed Formulaefor Calculating Ratios

Fi%ed Assets Tu!no*e! #atio

Cost of Sales

-et Fied Assets

Capital Tu!no*e! #atioCost of Sales

Capital 9mployed

O9ned Capital Tu!no*e! #atioCost of Sales

Shareholders Fund

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 43/100

2etailed Formulaefor Calculating Ratios

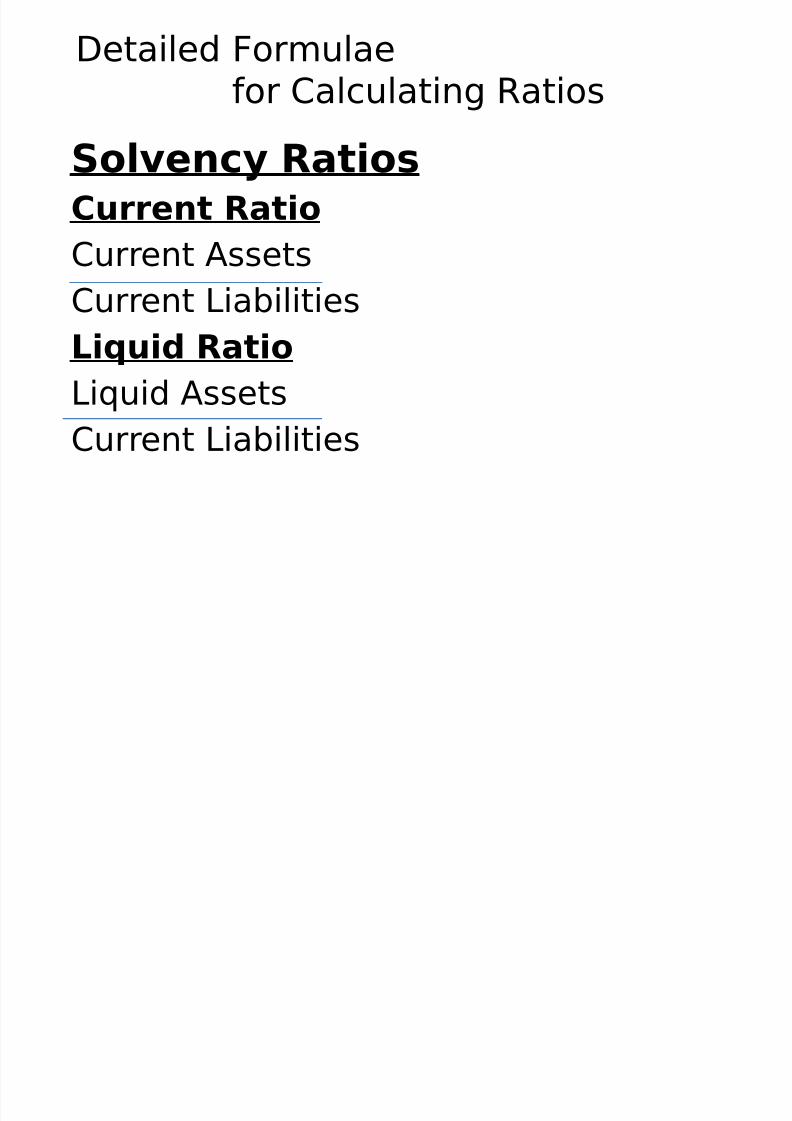

Sol*ency #atiosCu!!ent #atio

Current AssetsCurrent &iabilities

Li3uid #atio

&i,uid AssetsCurrent &iabilities

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 44/100

2etailed Formulaefor Calculating Ratios

A1solute Li3uid #atioCash = 'an = 6aretable securities

Current &iabilities

Fi%ed Assets #atio

Fied Assets

&ong term funds

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 45/100

2etailed Formulaefor Calculating Ratios

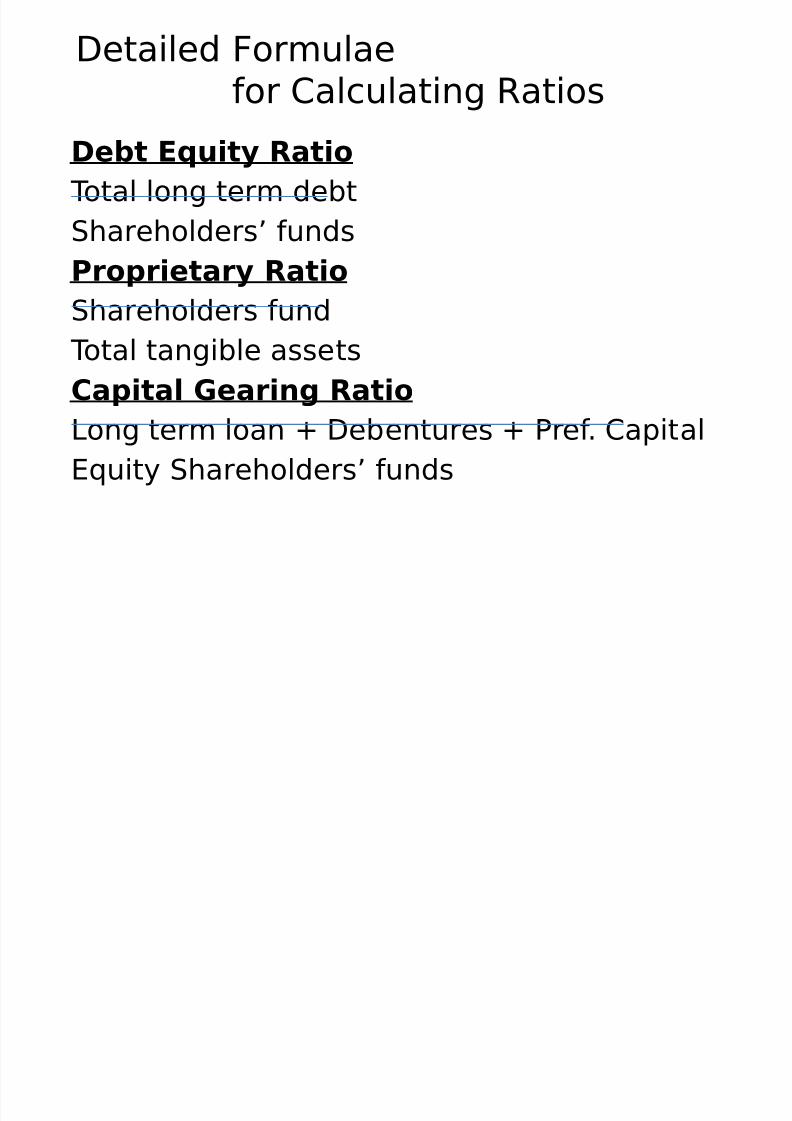

.e1t E3uity #atio

#otal long term debt

Shareholders funds

!op!ieta!y #atioShareholders fund

#otal tangible assets

Capital 4ea!in$ #atio&ong term loan = 2ebentures = %ref. Capital

9,uity Shareholders funds

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 46/100

%rotability Ratios

%rotability refers to the ability to mae moreprot from optimum utili$ation of resourcesby a business concern.

%rotability in"ol"es study of sales4 cost ofgoods sold4 analysis of gross margin onsales4 analysis of operating epenses4operating prot and analysis of prot in

relation to capital employed.%rots are the goals of e"ery business rm.

#hey indicate a rms progress.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 47/100

%rotability Ratios

%rotability Ratios are in two models/

!ot Ma!$in #atio

It shows the di*erence between protsand sales.

#ate of #etu!n #atio

It eplains the relationship betweenprot and capital.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 48/100

%rotability Ratios

4!oss !ot #atio

Refers to the relationship between gross prot and net sales.A higher ratio is preferable for showing higher protability.

Ope!atin$ #atio

Re+ects the di*erence between total operating epenses andnet sales. 8perating epenses includes cost of goods sold4administrati"e epenses and selling epenses but ecludesnance epenses. -et sales means sales sales returns.

Ope!atin$ !ot #atio

9plains the operating eciency of the rm and is a measureof the managements eciency in running the businessoperations.

8perating prot ratio E @ross prot operating epenses

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 49/100

%rotability Ratios

E%penses #atio

?seful to support operating ratio and indicates thee*ecti"eness of the business. @uides management toascertain the sa"ings or wastages in di*erent items of

epenses.Net !ot #atio

Also called as net prot to sale ratio. :igher the ratiobetter is the operational eciency of the business.

Ea!nin$ pe! sha!e 5ES6:ighlights the o"erall success of the business from

owners. It is calculated by di"iding the net prot afterta and pref. di"idend by number of e,uity shares.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 50/100

%rotability Ratios

!ice Ea!nin$s #atio

%09 ratio is important to prospecti"e in"estors to decidewhether to in"est in the e,uity shares of a company ata specic maret price or not. Shows earnings per

share re+ected by the maret price.Inte!est co*e! o! Fi%ed Cha!$es co*e! #atio

Re+ects the relationship between prot before interestand ta and ed interest charges.

.i*idend Yield #atio2i"idend yield ratio based on maret "alue of shares.

#he calculation of this ratio related with di"idend pershare and maret price per share.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 51/100

#urno"er Ratios

In*ento!y Tu!no*e! o! Stoc8 Tu!no*e! #atio

Also nown as stoc "elocity ratio. It is e*ecti"e to determinethe eciency of the in"entory. Shows relationship betweenthe cost of goods sold and a"erage in"entory.

Cost of goods sold means Sales @ross prot.e1to!s2 Tu!no*e! !atio

Also called as Account recei"able ratio or 2ebtors "elocityratio. #his ratio indicates the number of times the recei"ableare rotated in a year in terms of sales. It shows the eciency

of credit collection and credit policy.C!edito!s Tu!no*e! #atio

Also called as Account payable or Creditors "elocity.Indicates the number of times the payable rotate in a year.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 52/100

#urno"er Ratios

7o!8in$ Capital Tu!no*e! #atio

Boring capital means the relationship between current assetsand current liabilities. #his ratio measures the e*ecti"eutili$ation of woring capital and the relationship between costof sales and net woring capital.

Fi%ed Assets Tu!no*e! #atio

2etermines the eciency of utili$ation of ed assets andprotability of business concern. :igher ratio indicates eciencyin utili$ation and lower ratio indicates under utili$ation of edassets.

Capital Tu!no*e! #atio6anagerial eciency is calculated with the help of capitalturno"er ratio. It is the relationship between cost of sales andamount of capital in"ested in the business.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 53/100

Sol"ency Ratios

Cu!!ent #atio

#he ratio of current assets to current liabilities. #his ratioindicates the ability of a concern to meet its currentobligations as and when they are due for payments.

Current ratio E G Li3uid #atio

Also nown as <uic ratio or acid test ratio. It is calculatedby comparison of ,uic assets and current liabilities.

A1solute #atio

Also called cash position ratio or super ,uic ratio.It measures li,uidity in terms of cash and cash

e,ui"alents.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 54/100

Sol"ency Ratios

Fi%ed Assets #atio

9press the relationship between ed assetsand long term funds. #he benet of calculatingthis ratio is to ascertain the proportion of longterm funds in"ested in ed assets.

.e1t E3uity #atio

2etermining long term sol"ency position of a

company. 2ebt e,uity ratio is calculated inrelationship between eternal debt and internaldebt. Also called eternal internal ratio.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 55/100

Sol"ency Ratios

!op!ieta!y #atio

9presses the relationship between theproprietors funds and the total tangible assets. Itshows the soundness of the company. A high ratio

indicates safety to creditors and a low rate showsgreater ris to the creditors.

Capital 4ea!in$ #atio

It is used to analy$e the capital structure of therm. 9stablishes relationship between edinterest and di"idend bearing funds and e,uityshareholders fund.

Inter rm H Intra rm

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 56/100

Inter/rm H Intra/rmComparison

Inter/rm comparison refers to comparing two or morerms in the same rm or industry. #he main ob1ecti"eis to analy$e the features and e*ecti"eness of the rmto highlight the location of strength and weaness.

Inter rm comparison is a diagnostic tool whicheplains the e*ect of certain di*erences in thefeatures and practices of rms on their performance.

Intra rm comparison is a "oluntary4 condential andanonymous pooling of ey management data for thepurpose of pro"iding to the management of eachparticipating rm with data on its areas of strengthand weaness in relation to other similar rms.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 57/100

Cash Flo9 Analysis

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 58/100

Cash Flow Analysis

Cash +ow incudes cash in+ows and out+ows(cash receipts and cash payments) during aperiod. &i,uidity and short term sol"ency of a rmare dependent on its cash +ows.

A fundamental ob1ecti"e of nancial managementis to match the in+ows and out+ows of cash.

A cash +ow statement is a statement whichre+ects the changes in the cash position between

two accounting periods. It helps in taing shortterm nancial decision and also in the preparationof cash budget for the net period.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 59/100

Cash Flow Analysis

Cash +ow analysis can re"eal the causes fore"en highly protable rm eperiencingacute cash shortages.

An elaborate study of the sources of cashhelps to impro"e in+ow and analysis ofdi*erent application of cash helps to slowdown or decrease the out +ow of cash.

#he highest benet can be in getting a clearinsight into the method of matching thein+ows with the out+ows.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 60/100

Cash Flow Analysis

.enitions

Cash +ows are in+ows and out+ows of cash and cashe,ui"alents.

Cash e,ui"alents are short term4 high li,uid

in"estments that are readily con"ertible into nownamounts of cash and which are sub1ect to aninsignicant ris of changes in "alue.

Cash consists of cash on hand and demand deposit

with ban.In"esting acti"ities are the ac,uisition and disposal of

long term assets and other in"estment not includedin cash e,ui"alent.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 61/100

Cash Flow Analysis

"enets

:istorical analysis as guide to forecasting.

9*ecti"e cash management

Formulation of nancial policies%reparation of cash budgets

Short term nancial decision

&i,uidity positionRe"aluation

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 62/100

Cash Flow Analysis

Limitations

2iscloses in+ows and out+ows ofcash alone

Scope of cash +ow statement islimited

Can be easily altered or more +eible

in nature

-on/cash items of epenses andincomes are ecluded.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 63/100

Cash Flow Analysis

Cash and Cash E3ui*alents

Cash e,ui"alents are held for the purpose ofmeeting short term cash commitments

rather than for in"estment or other purposes.It must be readily con"ertible to a nownamount of cash and be sub1ected to aninsignicant ris of changes in "alue.

Cash management include the in"estment ofecess cash in cash e,ui"alents.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 64/100

Cash Flow Statement

Cash +ow statement should epresscash +ow during the period classiedby operating4 in"esting and nancing

acti"ities.Classication by acti"ity pro"idesinformation that allows users to assess

the impact of those acti"ities on thenancial position of the enterprise andthe amount of its cash and cash

e,ui"alents.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 65/100

Cash Flow Statement

Ope!atin$ Acti*ities

#he amount of cash +ows arising fromoperating transactions is a ey indicator to

the etent to which the operations of theenterprise ha"e increased sucient cash+ow to maintain the operating capacity ofthe enterprise4 pay di"idends4 repay loans

and mae new in"estments withoutrecourse to eternal source of nancing.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 66/100

Cash Flow Statement

In*estin$ Acti*ities

Represent the etent to which ependituresha"e been made for resources intended to

generate future incomes and cash +ow.Financial Acti*ities

Cash +ow arising from nancing acti"ities isimportant because it is useful indetermining claims on future cash +ow bypro"iders of funds to the enterprise.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 67/100

%reparation of Cash Flow Statement

Cash +ow statement is prepared on the basis ofsource and uses of cash. Also based on theopening and closing balance sheet4 prot and lossaccount and other rele"ant information.

Cash +ow statement begins with the cash andban balances at the commencement of theperiod. If there is ban o"erdraft and cashbalance4 the net cash balance or net ban

o"erdraft becomes the starting point. #he "arious sources of cash are added to theopening balance and the application of cash aresubtracted. #he balance represents cash or ban

balances at the end of the accounting period. If a

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 68/100

Sources of Cash

Cash f!om Ope!ations

Refers to a business generating cash in+owthrough its normal business operations which

is usually the most important and routinesource of cash.

Computation of Cash f!om Ope!ations

Bhen all transactions are cash transactions

Bhen all transactions are not cashtransactions

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 69/100

Sources of Cash

7hen all t!ansactions a!e casht!ansactions

Bhen all epenses4 incomes and

re"enues are recei"ed or paid in cash4the net prot ascertained by prot andloss account represents cash from

operations.-et loss represents cash out +ow onaccount of operations.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 70/100

Sources of Cash

7hen all t!ansactions a!e not cash t!ansactions

'asically income statements are prepared on accrual

basis4 se"eral non/cash items are duly accounted inthe statements.

In such situations4 cash from operations is ascertainedin two stages/

Calculation of funds from operations

#his is be dealt in the net topic !Fund Flow

Analysis7Calculation of cash from operations

Bill be discussed in detail in this topic

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 71/100

Calculation of Cash from 8perations

#he cash from operations is essentialto con"ert the "arious items a*ectingthe prot into cash basis.

2etermining funds from operations byadding bac to the net prot all non/cash epenses shown in the prot and

loss account and subtracting the non/cash incomes.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 72/100

Calculation of Cash from 8perations

E:ect of c!edit sales and de1to!s

Cash from operations E -et prot = opening

debtors closing debtors 5O!6

Cash from operation E -et prot = decrease indebtors increase in debtors

E:ect of c!edit pu!chases and c!edito!s

Cash from operations E -et prot = closing

creditors opening creditors 5O!6Cash from operation E -et prot = increase increditors decrease in creditors

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 73/100

Calculation of Cash from 8perations

E:ect of unsold $oods in stoc8 oncash ;o9

Cash from operation E -et prot =

8pening stoc Closing stoc 5o!6

Cash from operation E -et prot =decrease in stoc 5o!6

Cash from operation E -et prot /increase in stoc

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 74/100

Calculation of Cash from 8perations

E:ect of outstandin$ e%penses 0incomes !ecei*ed in ad*ance

Cash from operation E -et prot = closing

outstanding epenses and income recei"edin ad"ance / opening outstanding epensesand income recei"ed in ad"ance 5o!6

Cash from operation E -et prot = increase

in outstanding epenses and incomerecei"ed in ad"ance / decrease outstandingepenses and income recei"ed in ad"ance

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 75/100

Calculation of Cash from 8perations

E:ect of p!epaid e%penses andacc!ued incomes

Cash from operation E -et prot =

opening accrued incomes and prepaidepenses closing accrued incomesand prepaid epenses 5o!6

Cash from operation E -et prot =decrease accrued incomes and prepaidepenses increase accrued incomes

and prepaid epenses

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 76/100

Calculation of Cash from 8perations

#he changes during the accounting period incurrent assets and current liabilities other thancash and ban balances ha"e to be noted. #henthe amount of such changes should be added to

or subtracted from the funds from operations onthe basis of the following principle /

Increase in current liability / Increases cash

2ecrease in current liability / decreases cash

Increase in current asset / decreases cash

2ecrease in current asset / Increases cash

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 77/100

9ternal sources of cash

Fresh issue of shares

Issue of debentures or bonds

&ong term borrowings

Sale of ed assets and in"estment

Cash out+ow on account of operation

%urchase of ed assets and longterm in"estment

%ayment of ta and di"idend

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 78/100

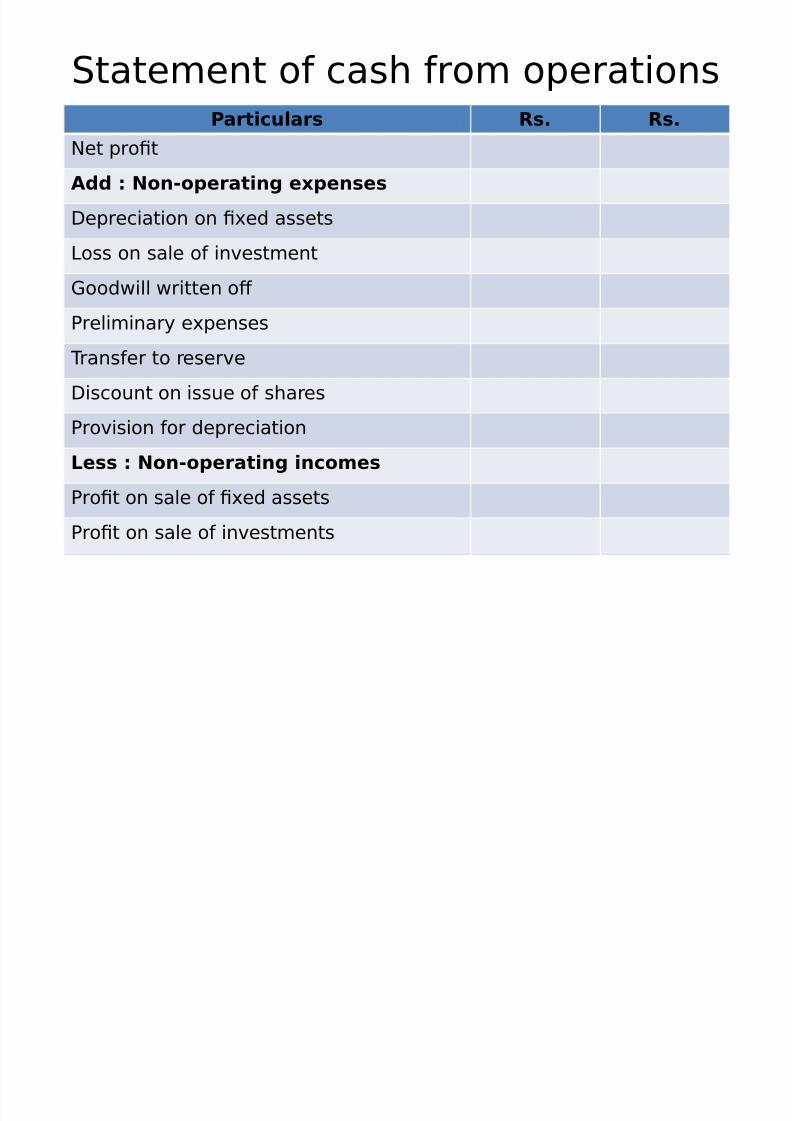

Statement of cash from operationsa!ticula!s #s< #s<

-et prot

Add = Non)ope!atin$ e%penses

2epreciation on ed assets

&oss on sale of in"estment

@oodwill written o*

%reliminary epenses

#ransfer to reser"e

2iscount on issue of shares%ro"ision for depreciation

Less = Non)ope!atin$ incomes

%rot on sale of ed assets

%rot on sale of in"estments

Ad1usted %rot and &oss

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 79/100

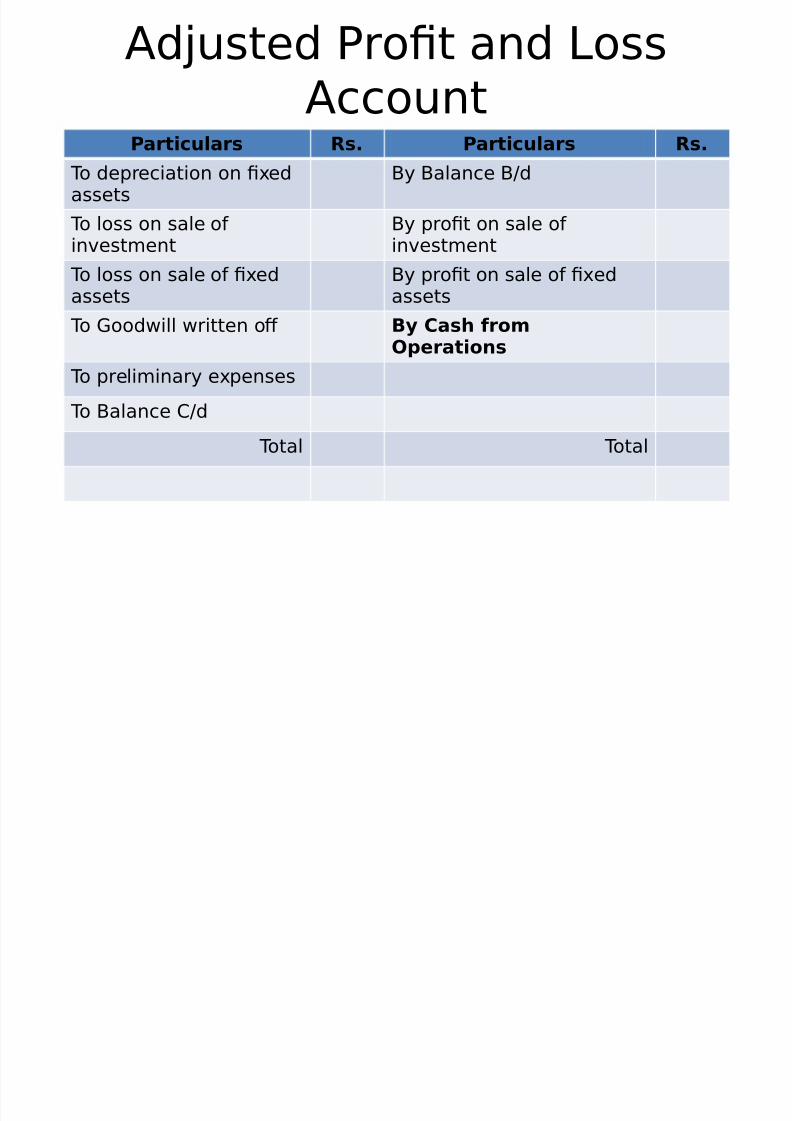

Ad1usted %rot and &ossAccount

a!ticula!s #s< a!ticula!s #s<

#o depreciation on edassets

'y 'alance '0d

#o loss on sale ofin"estment

'y prot on sale ofin"estment

#o loss on sale of edassets

'y prot on sale of edassets

#o @oodwill written o* "y Cash f!omOpe!ations

#o preliminary epenses

#o 'alance C0d

#otal #otal

Statement of cash from

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 80/100

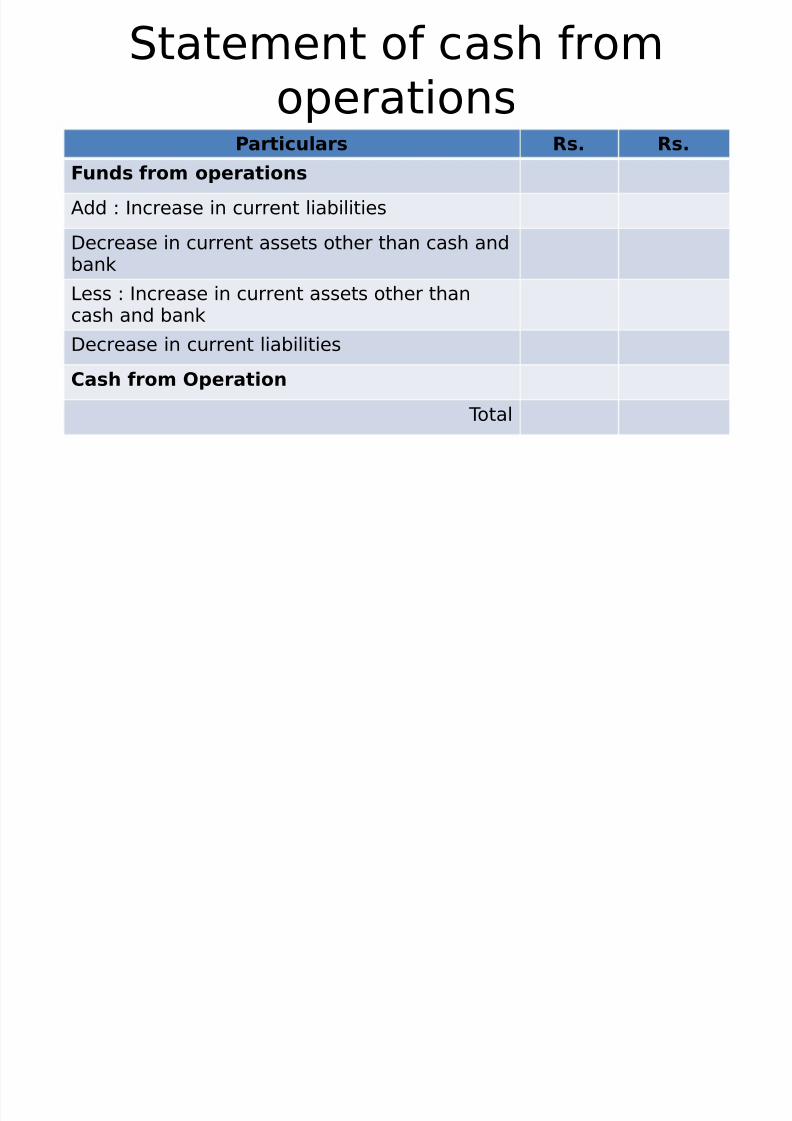

Statement of cash fromoperations

a!ticula!s #s< #s<

Funds f!om ope!ations

Add Increase in current liabilities

2ecrease in current assets other than cash and

ban&ess Increase in current assets other thancash and ban

2ecrease in current liabilities

Cash f!om Ope!ation

#otal

Cash Flow Statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 81/100

Cash Flow Statementfor the year ended .

a!ticula!s #s< #s<

Openin$ 1alances= Cash

"an8

Add = Sou!ces of Cash

Cash from operation

Issue of shares

Issue of debentures

Sale of ed assets

Sale of in"estment

Increase in current liabilities

&ong term loans taen

Cash Flow Statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 82/100

Cash Flow Statementfor the year ended .

a!ticula!s #s< #s<

Less = Application of cash

Redemption of preference shares

Redemption of debentures

&oan repaid

#a paid

2i"idend paid

2ecrease in current liabilities

Increase in current assets

&oss on sale of ed assets

&oss on sale of in"estment

Closin$ 1alances = Cash

"an8

C h Fl St t t

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 83/100

Cash Flow Statement

In;o9 o! Sou!cesof Cash

Amount

Out;o9 o! Application ofCash

Amount

8pening balance ofCash and 'an

JJ Redemption of %ref. shares JJ

Issue of shares JJ Repayment of 2ebenture JJ

Issue of debentures JJ Repayment of loans JJ

Raising of loans JJ %urchase of ed assets JJ

Sale of ed assets JJ 2i"idend paid JJ

2i"idends recei"ed JJ Income #a paid JJ

Share %remiumrecei"ed

JJ Cash from 8perations (&ossin operation)

JJ

Cash from 8perations JJ Closing balance of Cash and'an

JJ

JJ JJ

9 t di It

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 84/100

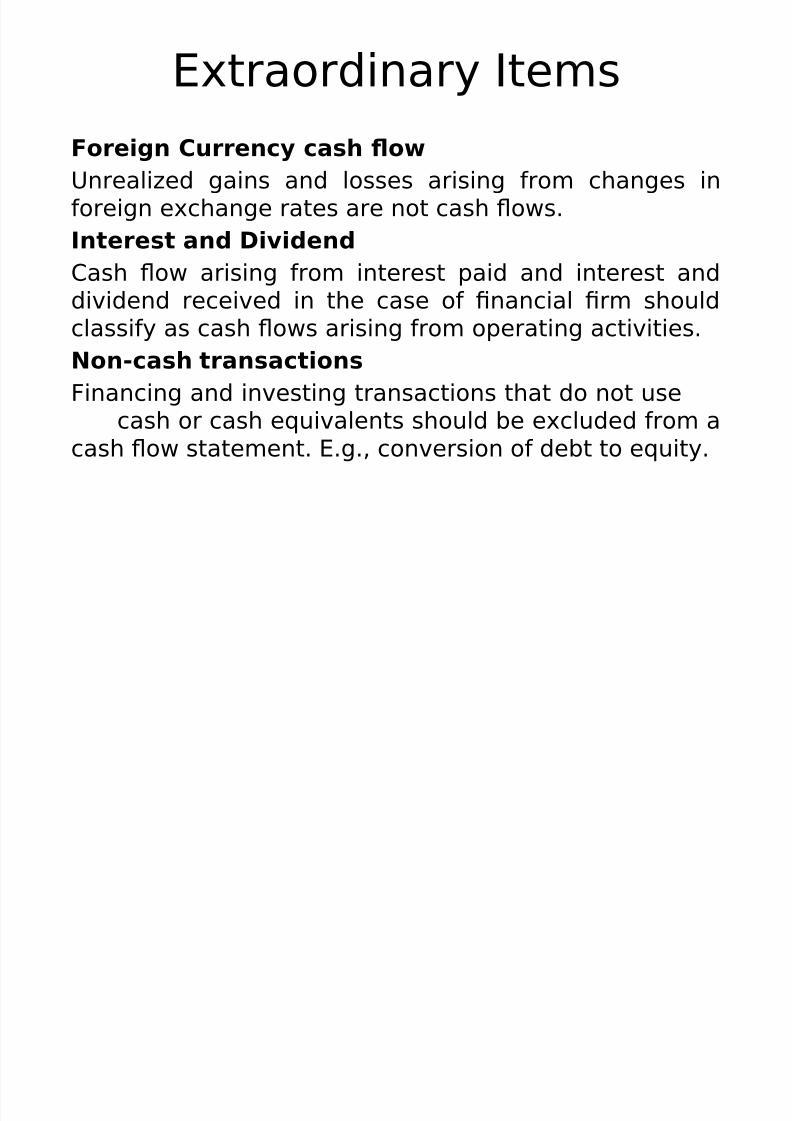

9traordinary Items

Fo!ei$n Cu!!ency cash ;o9?nreali$ed gains and losses arising from changes inforeign echange rates are not cash +ows.

Inte!est and .i*idend

Cash +ow arising from interest paid and interest anddi"idend recei"ed in the case of nancial rm shouldclassify as cash +ows arising from operating acti"ities.

Non)cash t!ansactions

Financing and in"esting transactions that do not usecash or cash e,ui"alents should be ecluded from a

cash +ow statement. 9.g.4 con"ersion of debt to e,uity.

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 85/100

Fund Flo9 Analysis

F d Fl A l i

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 86/100

Funds Flow Analysis

#he International Accounting Standard -o.Keplains Funds +ow as ! Statement of changes innancial position7. #he word fund refers to cashand cash e,ui"alents or to woring capital.

Concept of woring capital is di"ided into two/4!oss 9o!8in$ capital concept

It refers to the rms in"estment in current assets

Net 9o!8in$ capital concept

It refers to the ecess of current assets o"ercurrent liabilities.

F d Fl A l i

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 87/100

Funds Flow Analysis

Non)cu!!ent lia1ilities #hese liabilities are not re,uired to be payable within a yearand paid out of current assets.

Cu!!ent lia1ilities

#hese liabilities are payable within a year and paid out ofcurrent assets.

Non)cu!!ent assets

#hese assets are purchased in the business for use o"er along period of time for earning purpose.

Cu!!ent assets #hese assets are easily con"erted into cash and reasonablyreali$ed in cash or sold or consumed within a year.

F d Fl St t t

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 88/100

Funds Flow Statement

Funds +ow statement is a nancial statementwhich re"eals the methods by which the businesshas been nanced and how it has used its fundsbetween the opening and closing balance sheet

dates. #he funds +ow statement describes the sourcesfrom which additional funds were deri"ed andthe uses to which these funds were put.

It is also called as Statement of Sources andApplication of funds and Statement of Changesin Boring Capital.

F d Fl St t t

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 89/100

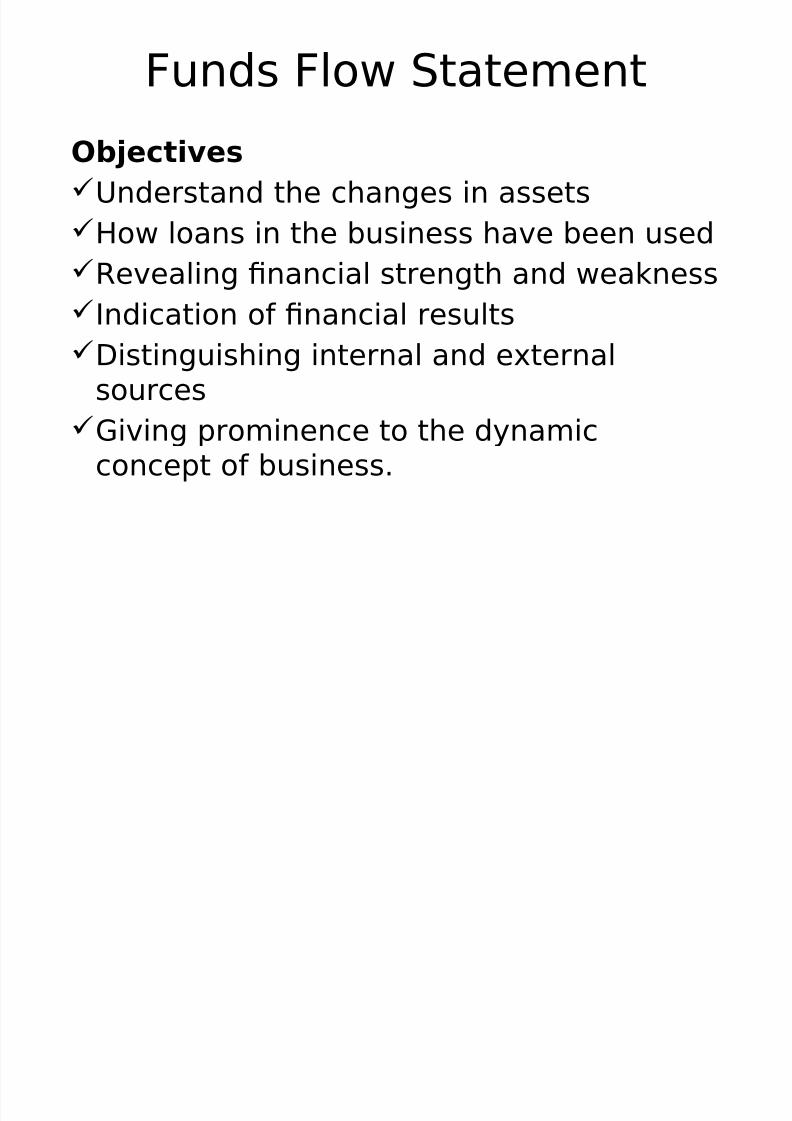

Funds Flow Statement

O1>ecti*es?nderstand the changes in assets

:ow loans in the business ha"e been used

Re"ealing nancial strength and weanessIndication of nancial results

2istinguishing internal and eternal

sources@i"ing prominence to the dynamic

concept of business.

Funds Flo Statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 90/100

Funds Flow Statement

Ad*anta$es %ro"ides detailed analysis and understanding

of changes in the distribution of nancialresources between two balance sheet dates.

Shows how funds were obtained and usedduring a period

Computation of cost of capital from sources offunds Indication of weaness and strength in

the nancial position of the rm Actuals compared with rele"ant budgets to

access usage

Formulating long term nancial plan and

olicies

Funds Flow Statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 91/100

Funds Flow Statement

Si$nicance #he sources4 amount and timing of

nance

?tili$ation of funds on priority basis

Amount of di"idends through aconsistent di"idend policy

Appropriate decisions regardingpurchase of assets

Funds Flow Statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 92/100

Funds Flow Statement

Limitations:istorical in nature

Shows only past happenings

Simply termed as secondary data

9*ect of current assets and liabilitiesnot shown

Ignores transactions between longterm assets and liabilities

Funds Flow Statement

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 93/100

Funds Flow Statement

!epa!ation of Funds ;o9statement

Statement of changes in woringcapital

Funds +ow statement

Funds from operationAd1usted prot and loss account

B i C it l St t t

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 94/100

Boring Capital Statement

Statement of chan$es in 9o!8in$ capitalIt is concerned with the current assets and currentliabilities only4 as they are shown in the balance sheet ofthe current year and the pre"ious year. -on/current assetsand non/current liabilities4 prot and losses4

additional information a"ailable are completely omitted.

Increase in current assets / Increases woring capital

2ecrease in current assets / 2ecreases woring capital

Increase in current liability / 2ecreases woring capital

2ecrease in current liability / Increases woring capital

Statement of changes

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 95/100

gin woring capital / specimen

Changes in Boring Capital

a!ticula!s Yea! Yea! Inc!ease

.ec!ease

Cu!!ent Assets

Cash 'alance

'an 'alance

Stoc

Sundry 2ebtors

#rading In"estment

%repaid epenses

'ills Recei"able

Total 5A6

Statement of changes

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 96/100

gin woring capital / specimen

Changes in Boring Capitala!ticula!s Yea! Yea! Inc!eas

e.ec!eas

e

Less= Cu!!ent Lia1ilities

Creditors'ills %ayable

8utstanding epenses

Short term loans

'an 8"erdraft

Total 5"6

7o!8in$ Capital

(Increase 0 2ecrease) 5A ?

"6

Funds Flow Statement /

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 97/100

specimenFunds ;o9 statement fo! the yea! endin$@@@@

Sou!ces of funds #s<

Issue of shares

Issue of debentures

Sale of ed assets

In"estment sold

Funds from operations

Total Sou!ces 5A6

Funds Flow Statement /

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 98/100

specimenApplication of funds #s<Repayment of long term loans

Redemption of preference shares

Redemption of debentures

%urchase of ed assets

#a paid

2i"idend paid

In"estment purchased

8ut +ow of funds

#otal Application (')

Increase 0 2ecrease in woring capital ( A ' )

Statement of Funds from

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 99/100

8perations

Ad>usted !ot 0 Loss Account #s< #s<Net !ot fo! the yea!

Add= Items 9hich do not dec!ease fundsf!om ope!ation

2epreciation on ed assets

&oss on sale of ed assets

&oss on sale of in"estment

@oodwill written o*

2iscount on debentures written o* %ro"ision for ta

%roposed 2i"idend

Total

Statement of Funds from

7/26/2019 Mba - Afm - Analysis of Financial Statements

http://slidepdf.com/reader/full/mba-afm-analysis-of-financial-statements 100/100

8perations

Ad>usted !ot 0 Loss Account #s< #s<Less= Items 9hich do not inc!ease fundsf!om ope!ations

%rot on sale of ed assets

%rot on sale of in"estment

Income from in"estment

Income ta refund

Funds from 8perations ('alancing gure)

Total