May 2015 | 12th edition Capital Confidence...

39

64 respondents Capital Confidence Barometer May 2015 | 12th edition Real estate

Transcript of May 2015 | 12th edition Capital Confidence...

64 respondents

CapitalConfidenceBarometer

May 2015 | 12th edition

Real estate

Page 2Commentary provides analysisfor the global respondents.12th Capital Confidence Barometer

EY’s Capital Confidence Barometer is a regular survey of senior executivesfrom large companies around the world conducted by the EconomistIntelligence Unit (EIU).

The respondent community is comprised of an independent EIU panel ofsenior executives and select EY clients and contacts.

Our 12th Barometer provides a snapshot of our findings, gauges corporateconfidence in the economic outlook, and identifies boardroom trends andpractices in the way companies manage their Capital Agenda.

EIU panel of more than 1,600 executives surveyed in February and March 2015 | 64 executives

from Real estate | Companies from 54 countries | Respondents from 18 industry sectors | 855 CEO,

CFO and other C-level executives |

About the Barometer

Macroeconomic environment

Page 4Commentary provides analysisfor the global respondents.

60%

31%9%

53%

44%

3%

83%

14%

3%

Improving Stable Declining

57%

40%

3%

38%

61%

1%

76%

19%

5%

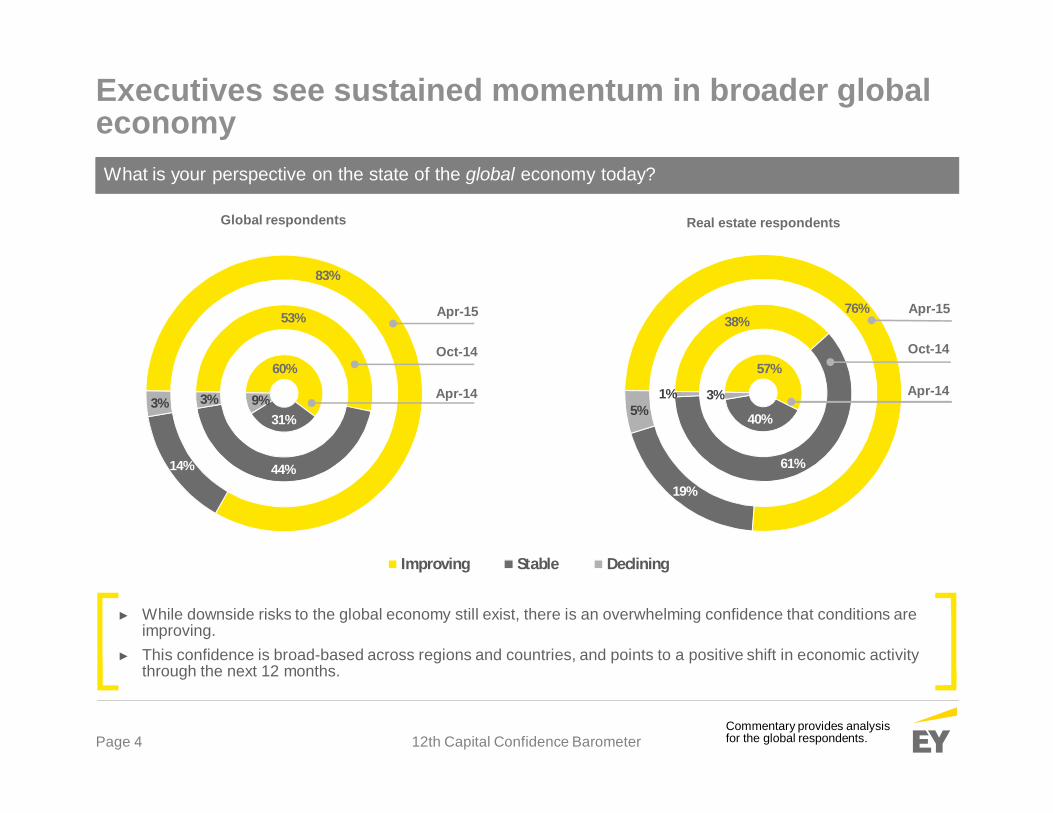

Executives see sustained momentum in broader globaleconomy

12th Capital Confidence Barometer

What is your perspective on the state of the global economy today?

Oct-14

Apr-14

Apr-15

Global respondents Real estate respondents

Oct-14

Apr-14

Apr-15

► While downside risks to the global economy still exist, there is an overwhelming confidence that conditions areimproving.

► This confidence is broad-based across regions and countries, and points to a positive shift in economic activitythrough the next 12 months.

Page 5Commentary provides analysisfor the global respondents.

Corporate earnings outlook and other leading marketindicators remain positive

12th Capital Confidence Barometer

Please indicate your level of confidence in the following at the global level:

72%

72%

69%

51%

77%

58%

64%

54%

65%

54%

54%

49%

Corporate earnings

Credit availability

Short-term marketstability

Equityvaluations/stockmarket outlook

Global respondents Real estate respondents

78%

66%

63%

53%

73%

72%

66%

52%

76%

57%

54%

41%

Corporate earnings

Credit availability

Short-term marketstability

Equity valuations/stockmarket outlook

Apr-15Oct-14Apr-14

► While earnings season in 2015 was very strong in the US and Europe, there has a been a downward trend inforward earnings, as the impact of cost savings achieved over the last five years have become the norm.

► Corporate earnings growth is still expected, but may have less upside than 2013-14.► Credit availability continues to be boosted by QE in Eurozone and Japan, and low interest rates elsewhere.

Page 6Commentary provides analysisfor the global respondents.

Geopolitical concerns persist, commodity and currencyvolatility rises

12th Capital Confidence Barometer

What do you believe to be the greatest economic risk to your business over the next 6–12 months?

37%

35%

10%

9%

7%

2%

Increased global andregional political instability

Increased volatility incommodities and currencies

Economic situation in theEurozone

Regulatory environment

Slowing growth in keyemerging markets

Deflation

Global respondents Real estate respondents

37%

30%

11%

11%

8%

3%

Increased volatility incommodities and currencies

Increased global and regionalpolitical instability

Economic situation in theEurozone

Slowing growth in key emergingmarkets

Regulatory environment

Deflation Apr-15

► Continuing geopolitical issues in Eastern Europe and the Middle East cause most concern around economic risk.► The sharp fall in commodity prices and increasing volatility of currencies make it more difficult to plan ahead.► Divergent monetary policies may impact currency fluctuations .

Page 7Commentary provides analysisfor the global respondents.

31%

52%17%

52%

41%

7%

29%

65%

6%

Create jobs/hire talent Keep current workforce size Reduce workforce numbers

29%

59%12%

61%

33%

6%

39%

55%

6%

Battle for talent heats up as companies look to recruitand retain

12th Capital Confidence Barometer

With regards to employment, which of the following does your organization expect to do in the next12 months?

Global respondents Real estate respondents

Oct-14

Apr-14

Apr-15

Oct-14

Apr-14

Apr-15

► As confidence returns to the global economic outlook, most companies are planning to retain or grow theirworkforce.

► Strong employment growth in the US and UK, and an improving situation in the Eurozone, validate this.► The desire to retain talent in an improving global economy is top of mind for many executives.

Page 8Commentary provides analysisfor the global respondents.

21%

38%

31%

1%

4%

5%

12%

11%

40%

6%

13%

18%

Digital future:Technology is disrupting all areas of enterprise, driving

myriad opportunities and challenges

Entrepreneurship rising:Entrepreneurship around the world is growing, driving the

need for more supportive ecosystems

Global marketplace:Economic power continues to shift east and south, driving

new patterns of trade and investment

Health reimagined:Technology and demographics converge to drive a once-in-

a-lifetime transformation of health services and provision

Resourceful planet:Growing demand and shifting supply are driving

innovation in the energy and resources space

Urban world:Effective infrastructure investment and sound planning

will make future cities competitive and resilient

Globalization, technology and rising entrepreneurshipcreating smaller business ecosystem

12th Capital Confidence Barometer

Which of the following will impact your core business and your acquisition strategy most in the next12 months?

Global respondents

► The continuing growth and economic power of China, India and the wider Asian economy is expected to havethe greatest impact on core business and acquisition strategies in the near term.

► The rise of entrepreneurship in many markets and sectors will play a key role in core business strategy, as thepace of innovation and the number of new market entrants increase.

33%

32%

22%

2%

0%

11%

19%

19%

24%

2%

11%

25%

Core businessAcquisition strategy

Real estate respondents

Corporate strategy

Page 10Commentary provides analysisfor the global respondents.

52%

40%

31%

31%

37%

54%

15%

17%

14%

2%

6%

1%

Apr-13

Apr-14

Apr-15

Growth Cost reduction and operational efficiency Maintain stability Survival

Intense cost scrutiny now an everyday feature ofcorporate strategy

12th Capital Confidence Barometer

Which statement best describes your organization’s focus over the next 12 months?

Global respondents Real estate respondents

58%

40%

41%

21%

40%

43%

18%

17%

16%

3%

3%

Apr-13

Apr-14

Apr-15

► Focus on costs is exacerbated by short-term pressures from commodity and currency fluctuations.► Low inflation makes it difficult to pass on any cost increases to customers, which will impact corporate margins.► This focus on lean operations has become part of the corporate DNA in the five years since the Global Financial

Crisis.

Page 11Commentary provides analysisfor the global respondents.

Intense cost scrutiny now an everyday feature ofcorporate strategy

12th Capital Confidence Barometer

Which of the following has been elevated on your boardroom agenda?

Global respondents Real estate respondents

40%

31%

18%

6%

3%

2%

Reducing costs/improvingmargins

Changing commodityprices

Acquisition

Returning cash toshareholders

Shareholder activism

Strategic divestment(Spin-off/IPO)

45%

22%

20%

8%

3%

2%

Reducing costs/improvingmargins

Changing commodityprices

Acquisition

Returning cash toshareholders

Shareholder activism

Strategic divestment(Spin-off/IPO)

Apr-15

► Focus on costs is exacerbated by short-term pressures from commodity and currency fluctuations.► Low inflation makes it difficult to pass on any cost increases to customers, which will impact corporate margins.► This focus on lean operations has become part of the corporate DNA in the five years since the Global Financial

Crisis.

Page 12Commentary provides analysisfor the global respondents.

Executives are looking to innovative organic strategiesto boost their potential market footprint

12th Capital Confidence Barometer

What is the primary focus of your company’s organic growth over the next 12 months?

Global respondents

19%

6%

24%

11%

30%

19%

More rigorous focus oncore products/existing

markets

New sales channels

Conventional

Real estate respondents

24%

20%

17%

14%

15%

17%

21%

12%

16%

12%

14%

9%

Exploiting technology to develop newmarkets/products

Increase R&D/product introductions

Changing mix of existing products andservices

Investing in new geographies/markets

Innovative

7%

0%

27%

0%

21%

14%

More rigorous focus on coreproducts/existing markets

New sales channels

Conventional

Apr-15Apr-14Apr-13

44%

21%

21%

7%

0%

7%

46%

20%

7%

14%

21%

23%

Exploiting technology to developnew markets/products

Changing mix of existing productsand services

Investing in newgeographies/markets

Increase R&D/product introductions

Innovative

► Increased R&D and innovative use of technology are seen as key routes to organic growth.► The focus on core operations is still a key driver, but after several years of emphasis, companies may find it can

no longer deliver growth – just support earnings.

M&A Outlook

Page 14Commentary provides analysisfor the global respondents.

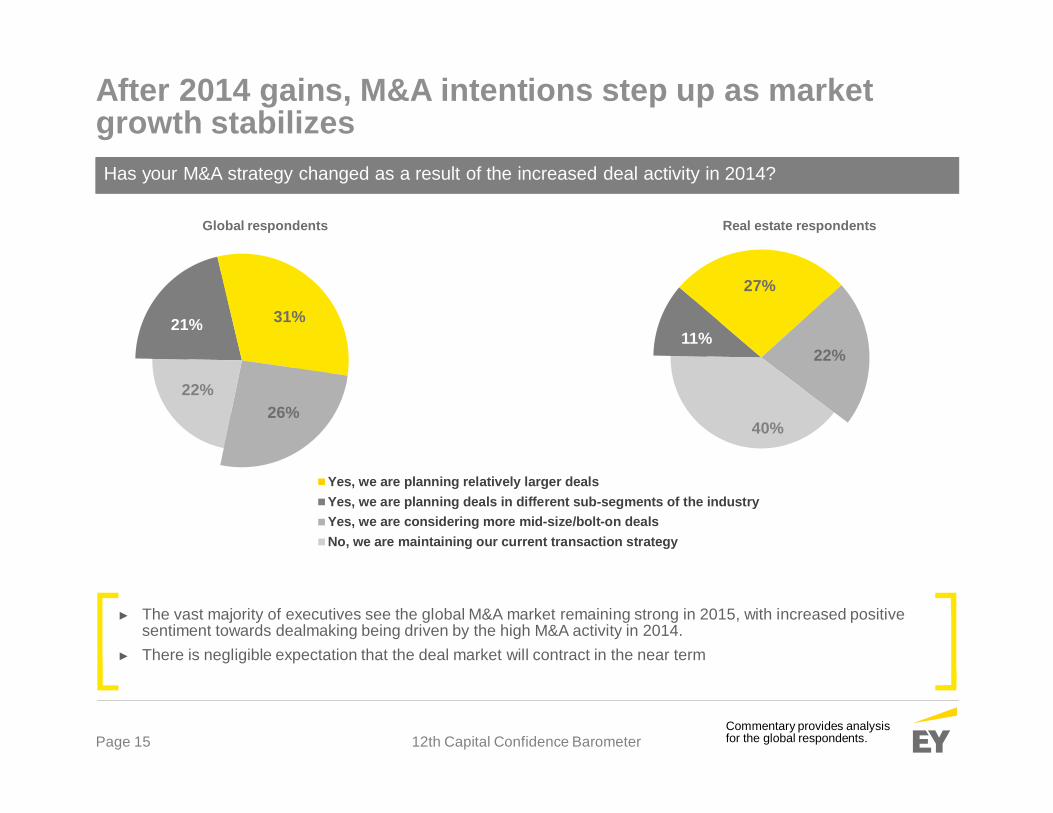

After 2014 gains, M&A intentions step up as marketgrowth stabilizes

12th Capital Confidence Barometer

What is your expectation for the M&A market in the next 12 months? – At global level

49%

49%

2%

58%

36%

6%

73%

23%

4%

Improving

Stable

Declining

Global respondents Real estate respondents

47%

50%

3%

45%

45%

10%

76%

21%

3%

Improving

Stable

Declining Apr-15Apr-14Apr-13

► The vast majority of executives see the global M&A market remaining strong in 2015, with increased positivesentiment towards dealmaking being driven by the high M&A activity in 2014.

► There is negligible expectation that the deal market will contract in the near term

Page 15Commentary provides analysisfor the global respondents.

Yes, we are planning relatively larger dealsYes, we are planning deals in different sub-segments of the industryYes, we are considering more mid-size/bolt-on dealsNo, we are maintaining our current transaction strategy

Real estate respondents

21% 31%

26%22%

After 2014 gains, M&A intentions step up as marketgrowth stabilizes

12th Capital Confidence Barometer

Has your M&A strategy changed as a result of the increased deal activity in 2014?

Global respondents

11%

27%

22%

40%

► The vast majority of executives see the global M&A market remaining strong in 2015, with increased positivesentiment towards dealmaking being driven by the high M&A activity in 2014.

► There is negligible expectation that the deal market will contract in the near term

Page 16Commentary provides analysisfor the global respondents.

Strong uptick in deal intentions driven by longer-termgrowth strategies

12th Capital Confidence Barometer

Do you expect your company to actively pursue acquisitions in the next 12 months?

Real estate respondentsGlobal respondents

37%

46%

69%

44%

51%

58%

32%

41%

51%

Likelihood ofclosing

acquisitions

Quality ofacquisition

opportunities

Number ofacquisition

opportunities

50%

55%

72%

55%

58%

62%

20%

33%

36%

Apr-15 Oct-14 Apr-14

29%

35%31% 40%

56%

30%

22%26%

42%

58%

Apr-13 Oct-13 Apr-14 Oct-14 Apr-15

Expectations to pursue an acquisition

Global respondents Real estate respondents

► Executives report a strong increase in expectations to pursue an acquisition in 2015.► Increasing numbers of opportunities are bolstered by improving quality of assets, supported by private equity

finally divesting long-held assets and private companies being attracted by relatively high valuations.► Likelihood of closing deals remains subdued – pointing to a disciplined approach to M&A.

Page 17Commentary provides analysisfor the global respondents.

Govt, public sectorInsurance

Life sciences

Mining and metalsOil and gas

Other sectors

Power and utilities

Provider care

Real estate

Technology

Telecommunications

Automotive andtransportation

Global M&A — relative performance by sector

12th Capital Confidence Barometer

(LTM to January 2015)

HIGHVOLUME

HIGHVALUE

LOWVALUE

LOWVOLUME Few deals, high value

Many deals, moderate valueMany deals, low value

Few deals, low value

Wealth and assetmanagement

Banking and capitalmarkets

Media andentertainment

Diversified industrialproducts

Consumer productsand retail

Aerospace and defense

Page 18Commentary provides analysisfor the global respondents.

77%

20%

3%

US$0 – US$250m US$251m – US$1b Greater than US$1b+

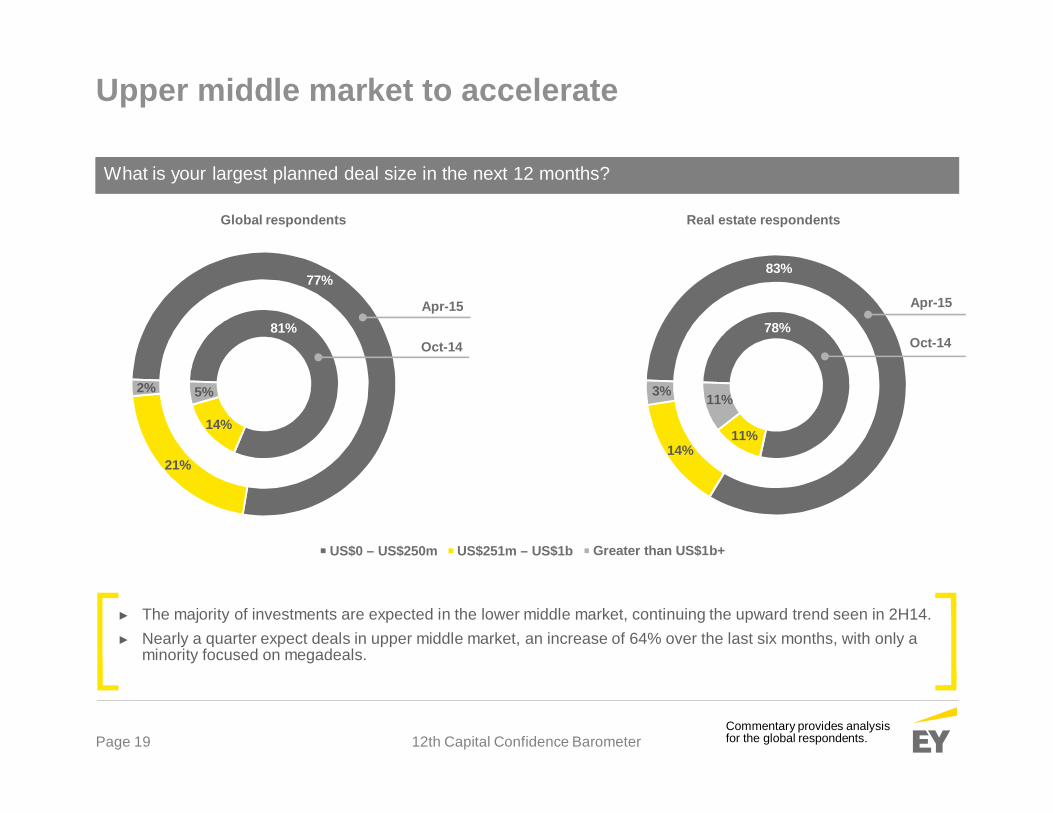

Upper middle market to accelerate

12th Capital Confidence Barometer

How much capital do you plan to allocate to acquisitions in the next 12 months?

Global respondents Real estate respondents

84%

11%

5%

► The majority of investments are expected in the lower middle market, continuing the upward trend seen in 2H14.► Nearly a quarter expect deals in upper middle market, an increase of 64% over the last six months, with only a

minority focused on megadeals.

Page 19Commentary provides analysisfor the global respondents.

81%

14%

5%

77%

21%

2%

US$0 – US$250m US$251m – US$1b Greater than US$1b+

78%

11%

11%

83%

14%

3%

Upper middle market to accelerate

12th Capital Confidence Barometer

What is your largest planned deal size in the next 12 months?

Global respondents Real estate respondents

Oct-14

Apr-15

Oct-14

Apr-15

► The majority of investments are expected in the lower middle market, continuing the upward trend seen in 2H14.► Nearly a quarter expect deals in upper middle market, an increase of 64% over the last six months, with only a

minority focused on megadeals.

Page 20Commentary provides analysisfor the global respondents.

Deal pipelines remain healthy and future deal intentionsare solid...

12th Capital Confidence Barometer

How many deals of all sizes do you have in your pipeline today?

24%

32%

19%

10%

15%

26%

30%

13%

8%

23%

28%

38%

16%

7%

11%

1

2

3

4

>=5

36%

40%

16%

8%

0%

22%

22%

11%

7%

38%

43%

14%

16%

3%

24%

1

2

3

4

>=5

Apr-15Oct-14Apr-14

Global respondents Real estate respondents

Page 21Commentary provides analysisfor the global respondents.

29%

66%

44%

62%

29%

23%

9%

5%

33%

Apr-14

Oct-14

Apr-15

Increase No change Decrease

Deal pipelines remain healthy and future deal intentionsare solid...

12th Capital Confidence Barometer

How do you expect your deal pipeline to change over the next 12 months?

Global respondents Real estate respondents

12%

68%

30%

85%

25%

32%

3%

7%

38%

Apr-14

Oct-14

Apr-15

Page 22Commentary provides analysisfor the global respondents.

…and executives expect to complete more acquisitionsthan last year

12th Capital Confidence Barometer

How many acquisitions do you expect to complete in the next 12 months?

43%

36%

10%

4%

7%

1

2

3

4

>=5

56%

11%

5%

14%

14%

1

2

3

4

>=5

Apr-15

Global respondents Real estate respondents

► The increase in deal completions is driven by companies returning to the M&A market.► Positive M&A volumes in 2014 encourage confidence to transact.

Page 23Commentary provides analysisfor the global respondents.

…and executives expect to complete more acquisitionsthan last year

12th Capital Confidence Barometer

Is this more or less than the number of acquisitions you completed in the prior 12 months?

47%

50%

3%

49%

46%

5%

More Stay the same Less

Global respondents Real estate respondents

► The increase in deal completions is driven by companies returning to the M&A market.► Positive M&A volumes in 2014 encourage confidence to transact.

Page 24Commentary provides analysisfor the global respondents.

Valuations support continued dealmaking, potentialupside pressures in asset pricing

12th Capital Confidence Barometer

How do you think that buyers’ expectations currently compare to sellers’ (valuation gap)?

6%

53%

39%

2%

Significantly higher (25% or more) Somewhat higher (10-25% gap) The gap is small (<10%) No gap

2%

60%

38%

Global respondents Real estate respondents

► While currently high valuations may deter some dealmaking, the overall view of stability should offset anydownside risks.

► Share-based deals will be encouraged as regional differences in valuations bring opportunities to the table.► Outside risk of rising valuations in the Eurozone may affect M&A.

Page 25Commentary provides analysisfor the global respondents.

Valuations support continued dealmaking, potentialupside pressures in asset pricing

12th Capital Confidence Barometer

Do you expect the valuation gap between buyers and sellers in the next 12 months to:

4%

78%

18%

Contract Stay the same Widen

3%

70%

27%

Global respondents Real estate respondents

► While currently high valuations may deter some dealmaking, the overall view of stability should offset anydownside risks.

► Share-based deals will be encouraged as regional differences in valuations bring opportunities to the table.► Outside risk of rising valuations in the Eurozone may affect M&A.

Page 26Commentary provides analysisfor the global respondents.

Valuations support continued dealmaking, potentialupside pressures in asset pricing

12th Capital Confidence Barometer

What do you expect the price/valuation of assets to do over the next 12 months?

17%

78%

5%

Increase Remain at current levels Decrease

17%

83%

Global respondents Real estate respondents

► While currently high valuations may deter some dealmaking, the overall view of stability should offset anydownside risks.

► Share-based deals will be encouraged as regional differences in valuations bring opportunities to the table.► Outside risk of rising valuations in the Eurozone may affect M&A.

Page 27Commentary provides analysisfor the global respondents.

Innovative investment (shifts scope of your business – could be into another industry sector)Bolt-on (complement current business model)Transformative (high value acquisition which significantly changes the size and scale of your company)

Innovative dealmaking picks up in healthier M&A market

12th Capital Confidence Barometer

Your planned M&A activity will mostly be:

Global respondents Real estate respondents

73%

21%

6%

60%

24%

16%

► Companies are making bolder moves to shift the scope of their business.► Bolt-on acquisitions are still a focus for executives.

Page 28Commentary provides analysisfor the global respondents.

Companies are looking across borders for M&A targets,but most intend to transact close to home

12th Capital Confidence Barometer

Where is the main focus of your M&A strategy over the next year?

54%

30%

16%

Immediate region (countries close to home)Outside domestic market/immediate regionDomestic market (home country)

46%

24%

30%

Global respondents Real estate respondents

► Domestic M&A intentions are unusually low – only 16% – as companies seek divergent economic performancefrom cross-border dealmaking

► More than half of respondents are focused on their immediate region for cross-border transactions, driven by theease of acquiring in common economic trading areas.

Page 29Commentary provides analysisfor the global respondents.

The majority of acquisition capital will be allocated todeveloped markets

12th Capital Confidence Barometer

What percentage of your acquisition capital are you going to allocate to the emerging markets inthe next 12 months?

3%

1%

31%

61%

4%

Above 50%

25-50%

10-25%

Less than 10%

None

0%

3%

14%

61%

22%

Above 50%

25-50%

10-25%

Less than 10%

None

Global respondents Real estate respondents

► Companies are planning to invest the majority of acquisition capital to developed markets, but emerging marketswill still be targeted.

► Slowing growth across many emerging markets, driven by lower commodity prices, is impacting M&A decisions.► The potential upturn in major developed markets, particularly the Eurozone, will also be a key driver.

Page 30Commentary provides analysisfor the global respondents.

Investment destinations span developed and top-tieremerging markets

12th Capital Confidence Barometer

Which are the top destinations your company is most likely to invest in the next 12 months?Please rank your top 5 countries.

Global Real estate

Top destinations

Top 5 destination countries

UK AustraliaChina UKUS USGermany GermanyAustralia Brazil

► The US, UK and Germany are set to lead developed market growth through 2015.► China and India remain emerging markets of choice for many executives, driven by relatively strong growth and

massive market potential..

Australia

UK

US

Germany

Brazil

Page 31Commentary provides analysisfor the global respondents.

Regulatory and legislative opportunities impacting M&Adecisions; market share growth still a key consideration

12th Capital Confidence Barometer

What are the main drivers impacting your M&A strategy over the next 12 months?Select up to two.

51%

35%

35%

27%

22%

5%

5%

5%

Gain market share in existinggeographical markets

Move into new geographicalmarkets

Leverage regulatory/legislativeopportunities

Improve structural taxefficiencies

Acquire talent

Reduce costs, improve margins

Access newtechnology/intellectual property

Move into new product/servicesareas Apr-15

Global respondents Real estate respondents

► Companies continue to take advantage of changes to the regulatory or legislative environment.► M&A decisions are heavily impacted by tax implications.► Consolidation is expected to continue in many domestic markets across all sectors.

45%

37%

36%

27%

20%

16%

8%

5%

Leverage regulatory/legislativeopportunities

Gain market share in existinggeographical markets

Improve structural tax efficiencies

Move into new geographicalmarkets

Acquire talent

Move into new product/servicesareas

Access newtechnology/intellectual property

Reduce costs, improve margins

Page 32Commentary provides analysisfor the global respondents.

Internal capabilities still the main challenge todealmaking

12th Capital Confidence Barometer

What are the main challenges to your M&A strategy over the next 12 months? Select two.

Global respondents Real estate respondents

► Internal M&A and integration resources are a main challenge to companies’ M&A strategy.► Funding, quality and number of opportunities, and competition for assets are still concerns.

34%

34%

33%

31%

19%

17%

11%

8%

4%

4%

Deal execution and integrationcapabilities

Funding availability

Insufficientopportunities/suitable targets

Buyer competition

Lack of internal resources ormanagerial focus

Adverse political environment

Regulatory environment

Adverse economic environment

Valuation gap between buyersand sellers

Uncertain tax environment

35%

32%

32%

24%

19%

16%

16%

8%

5%

0%

Buyer competition

Funding availability

Insufficient opportunities/suitabletargets

Deal execution and integrationcapabilities

Regulatory environment

Adverse political environment

Lack of internal resources ormanagerial focus

Adverse economic environment

Valuation gap between buyers andsellers

Uncertain tax environment Apr-15

Page 33Commentary provides analysisfor the global respondents.

Commodity and currency fluctuations driving pooroperating cost assumptions

12th Capital Confidence Barometer

For acquisitions completed recently, what was the most significant issue that contributed to deals notmeeting expectations?

32%

19%

17%

11%

10%

8%

3%

Poor operating cost assumptions

Product/sales price and margindeterioration

Failure to achieve synergies

Sales volume declines/Loss ofcustomers

Poor execution of integration

Strategic value overestimated/purchaseprice multiple too high

Unforeseen liabilities (tax, HR, pensionetc)

25%

24%

16%

13%

11%

8%

3%

Product/sales price andmargin deterioration

Poor operating costassumptions

Failure to achieve synergies

Sales volume declines/Loss ofcustomers

Poor execution of integration

Strategic valueoverestimated/purchase price

multiple too high

Unforeseen liabilities (tax, HR,pension etc)

Apr-15

Global respondents Real estate respondents

Page 34Commentary provides analysisfor the global respondents.

0%Apr-15

Capital Agenda focus on optimizing and raising capital

12th Capital Confidence Barometer

On which of the following capital management issues is your company placing the greatestattention and resources today?

Global respondents

Real estate respondents

Global respondents

Real estate respondents

Global respondents

Real estate respondents

Global respondents

Real estate respondents

31%Apr-15 12%Apr-15

57%Apr-15

17%Apr-1530%Apr-15

53%Apr-150%Apr-15

Page 35Commentary provides analysisfor the global respondents.

We are increasing our measures taken to protect against potential cyber security breaches of our M&A process.We are more concerned about the cyber security of planned acquisitions or targets than we were 12 months ago.We are more concerned about the business impact of potential cyber security breaches than we were 12 months ago.In the past 12 months, we have decided not to pursue a planned acquisition due to cyber security issues.

38%

30%

32%

45%

41%

12%

2%

Cyber security around dealmaking is a key concern forexecutives

12th Capital Confidence Barometer

Which of the following statements do you most agree with?

Global respondents Real estate respondents

► Recent high-profile cyber attacks on companies raises concerns around all corporate activities.► Heightened concern is being translated into active measures to protect against security breaches.► Some deals are not being pursued due to concerns about cyber security issues.

Survey demographics

Page 37Commentary provides analysisfor the global respondents.

19%

15%

26%

24%

16%

$5bn or more

$3bn to $5bn

$1bn to $3bn

$500m to $1bn

$250m to $500m

Survey demographics -

12th Capital Confidence Barometer

What are your company’s annual global revenuesin US$?

What is your position in the organization?

What best describes your company ownership?

Publicly listed 67% Privately owned 28%

Family-owned 3%

Government/state-owned enterprise 2%

C-levelexecutive

52%SVP/VP/Director 31%

Head ofBU/dept.

17%

Global

Page 38Commentary provides analysisfor the global respondents.

Publicly listed 64% Privately owned 33%

Family-owned 3%

Survey demographics -

12th Capital Confidence Barometer

What are your company’s annual global revenuesin US$?

What is your position in the organization?

What best describes your company ownership?

8%

13%

25%

23%

31%

$5bn or more

$3bn to $5bn

$1bn to $3bn

$500m to $1bn

Less than $500m

C-levelexecutive

31%

SVP/VP/Director 36%

Head ofBU/dept.

33%

Real estate

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. Theinsights and quality services we deliver help build trust and confidence in thecapital markets and in economies the world over. We develop outstandingleaders who team to deliver on our promises to all of our stakeholders. In sodoing, we play a critical role in building a better working world for our people,for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of themember firms of Ernst & Young Global Limited, each of which is a separatelegal entity. Ernst & Young Global Limited, a UK company limited by guarantee,does not provide services to clients. For more information about ourorganization, please visit ey.com.

About EY’s Global Real Estate, Hospitality & Construction (RHC) sector

Today’s RHC sector must adopt new approaches to address regulatoryrequirements and financial risks, while meeting the challenges of expandingglobally and achieving sustainable growth. EY’s Global RHC sector bringstogether a worldwide team of professionals to help you succeed — a team withdeep technical experience in providing assurance, tax, transaction andadvisory services. The sector works to anticipate market trends, identify theimplications and develop points of view on relevant sector issues. Ultimately itenables us to help you meet your goals and compete more effectively.

2015 EYGM Limited.

All Rights Reserved.

ED None

This material has been prepared for general informational purposes only and is not intended to berelied upon as accounting, tax, or other professional advice. Please refer to your advisors forspecific advice.

ey.com/realestate