May 2009 IT Trends – New Keywords. 2 A.T. Kearney /SCB/IT Vision What’s Hot in IT?

43

May 2009 IT Trends – New Keywords

-

Upload

kerry-paul -

Category

Documents

-

view

219 -

download

7

Transcript of May 2009 IT Trends – New Keywords. 2 A.T. Kearney /SCB/IT Vision What’s Hot in IT?

May 2009

IT Trends – New Keywords

2A.T. Kearney /SCB/IT Vision

What’s Hot in IT?

3A.T. Kearney /SCB/IT Vision

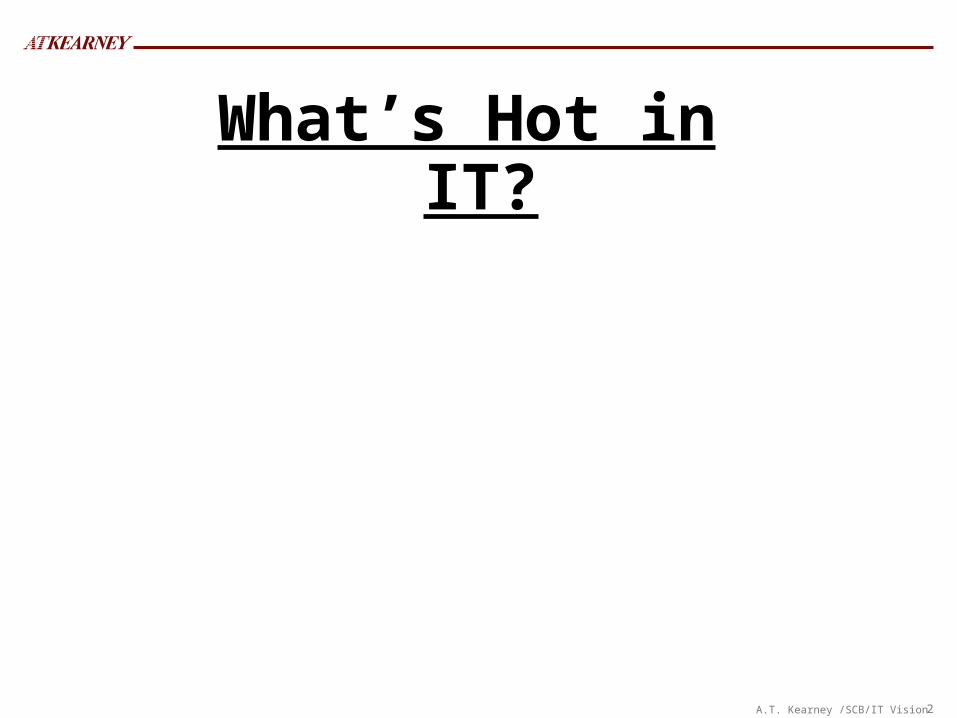

What’s Hot in IT?

SOAWeb Services

Web 2.0

Memory DB

Green IT

Cloud Computing

Open Source

SaaSUtility Computing

SEAP, XTP

4A.T. Kearney /SCB/IT Vision

What’s Hot in IT?

Point of view-Just Personal interesting?

-Technological advancement?

-Industrial aspect?

-From the $$ point of view? – Business, Personal

5A.T. Kearney /SCB/IT Vision

Who are you?

- Researcher/Professor

- CEO/CSO/CTO/CIO/COO

- Engineer

- Law Maker/Politician/Regulator

6A.T. Kearney /SCB/IT Vision

Industry Domain (1/2)- Government

- Banking & Finance

- Professional Services

- Insurance

- Manufacturing

- Information Technology

- Health Care

- Education

- Utilities

- Transportation

- Telecommunications

- Retail

- Energy

- Consumer Products

- Pharmaceuticals

- Media

- F&B

- Electronics

- Constructions & Engineering

- Metals & Natural Resources

- Hospitality & Travel

- Chemicals

7A.T. Kearney /SCB/IT Vision

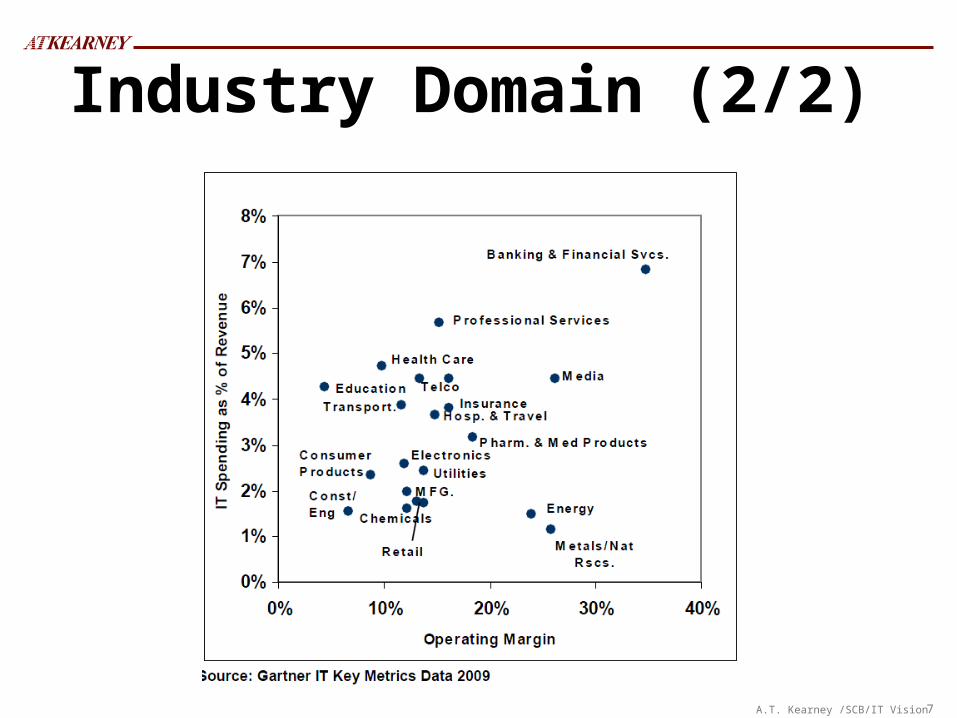

Industry Domain (2/2)

8A.T. Kearney /SCB/IT Vision

Let’s assume that

You are the CIO of commercial bank.

9A.T. Kearney /SCB/IT Vision

Overview Of Banking Industry And Technology Trends

10A.T. Kearney /SCB/IT Vision

Customer centricity is the dominant theme

1. Industry consolidation – emergence of pan-European and pan-Atlantic institutions

2. Commoditization – little scope for game-changing innovation and low barrier to entry

3. Relentless focus on customers – service seen as point of differentiation

— focus on analytical techniques to drive advocacy

— Channel integration to allow ‘one view’ for customers and banks

— preference for best of breed self-evaluation, customer service, product customization etc.

4. Competition from non-traditional sources – especially in payments as well as retailers

5. SME integration – bundled products, pricing, dedicated platforms, non-traditional offerings, supply chain and payment integration

11A.T. Kearney /SCB/IT Vision

Innovation is at the detail level and importance is on execution

1. There are no break through technologies that will change the landscape – it is not a game of big-strokes

2. Developments at three levels

— Customer interface. Biometrics, convergence and divergence of channels and integration

— Products. Bundling, customization, pricing, etc

— Operations. Six sigma, shared services, offshore, etc

— Technology. Focus on managing “change versus run” the bank investments

3. Exception is cards and payments

— ‘War on cash’

— Nearly 40% of revenue and moving from engine room into profit center

— Innovation on multiple fronts: contact-less, pre-paid, mobile payments, etc

— Alternatives such as PayPal, ‘DebitMan’ etc

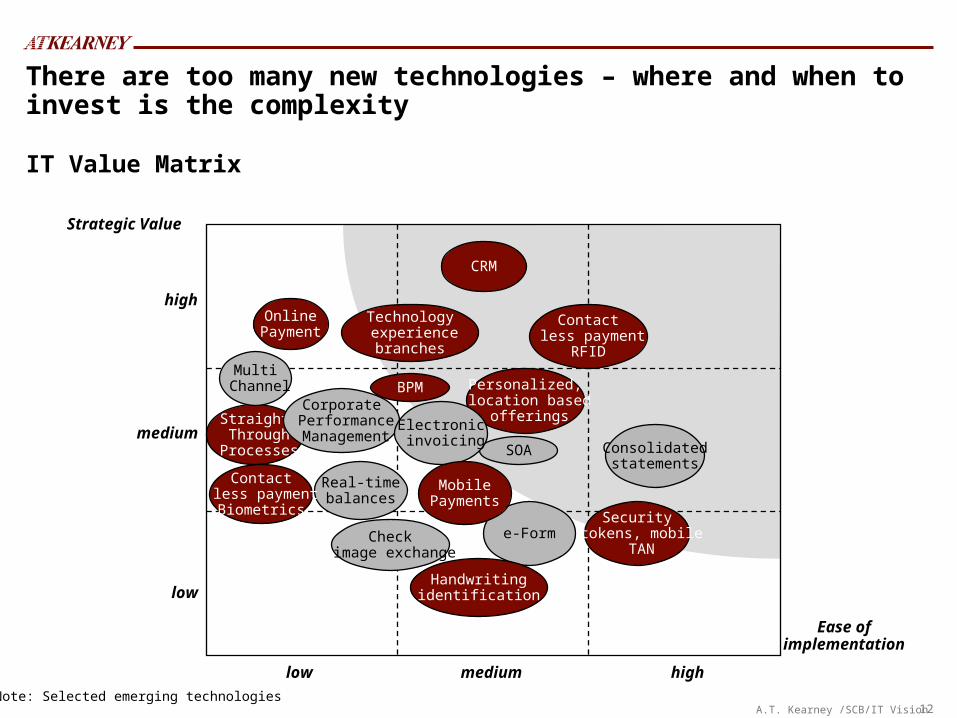

12A.T. Kearney /SCB/IT Vision

high

medium

low

low medium high

Ease of implementation

Strategic Value

CRM

There are too many new technologies – where and when to invest is the complexity

IT Value Matrix

Consolidatedstatements

Personalized, location based

offeringsStraight Through

Processes

Multi Channel

Real-timebalances

Contact less payment

Biometrics

SOA

BPMCorporate

Performance Management

Electronic invoicing

e-FormCheck image exchange

Note: Selected emerging technologies

Contact less payment

RFID

Handwritingidentification

Security tokens, mobile

TAN

OnlinePayment

Technology experiencebranches

MobilePayments

13A.T. Kearney /SCB/IT Vision

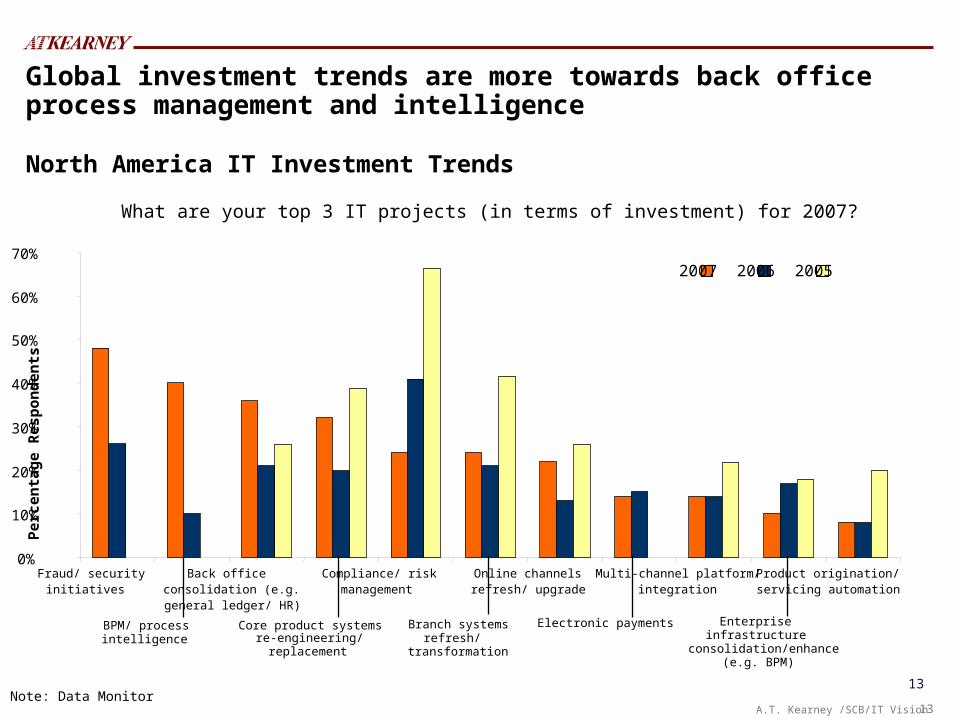

Global investment trends are more towards back office process management and intelligence

North America IT Investment Trends

Note: Data Monitor13

0%

10%

20%

30%

40%

50%

60%

70%

Fraud/ securityinitiatives

Back officeconsolidation (e.g.general ledger/ HR)

Compliance/ riskmanagement

Online channelsrefresh/ upgrade

Multi-channel platform/integration

Product origination/servicing automation

Per

cen

tag

e R

esp

on

den

ts

2007 2006 2005

BPM/ processintelligence

Core product systemsre-engineering/replacement

Branch systemsrefresh/

transformation

Electronic payments Enterpriseinfrastructure

consolidation/enhance(e.g. BPM)

What are your top 3 IT projects (in terms of investment) for 2007?

14A.T. Kearney /SCB/IT Vision

Deep Dive In Banking Trends And IT Innovation

15A.T. Kearney /SCB/IT Vision

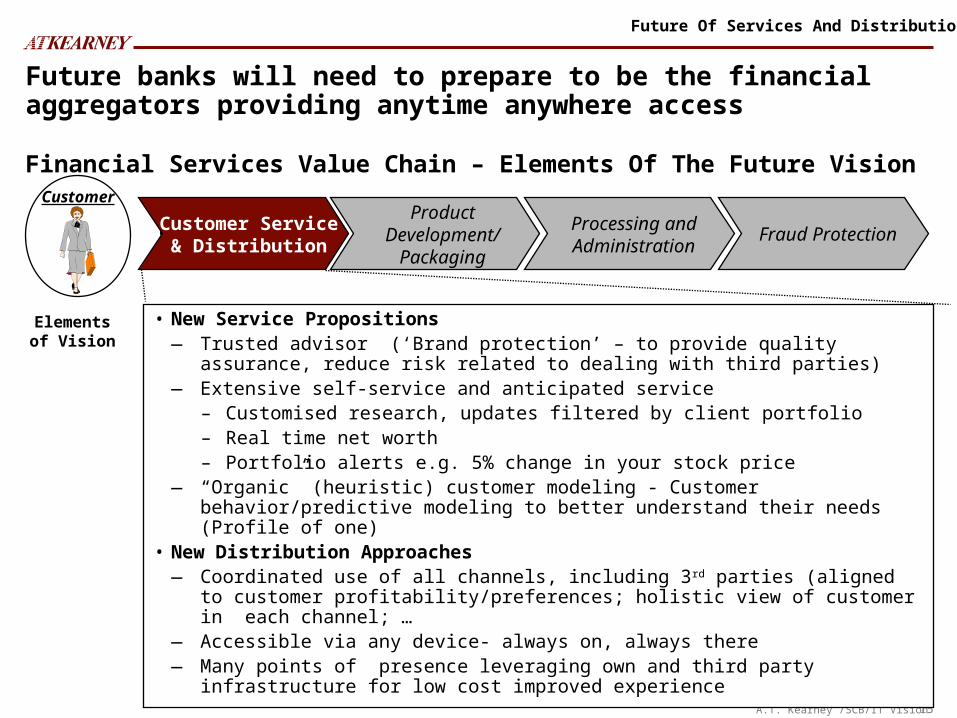

Future Of Services And Distribution

• New Service Propositions― Trusted advisor (‘Brand protection’ – to provide quality assurance, reduce risk related

to dealing with third parties)― Extensive self-service and anticipated service

– Customised research, updates filtered by client portfolio– Real time net worth – Portfolio alerts e.g. 5% change in your stock price

― “Organic” (heuristic) customer modeling - Customer behavior/predictive modeling to better understand their needs (Profile of one)

• New Distribution Approaches — Coordinated use of all channels, including 3rd parties (aligned to customer

profitability/preferences; holistic view of customer in each channel; …— Accessible via any device- always on, always there— Many points of presence leveraging own and third party infrastructure for low cost

improved experience

Elements of Vision

Financial Services Value Chain – Elements Of The Future VisionCustomer

Customer Service & Distribution

Processing and Administration

Product Development/

Packaging

Future banks will need to prepare to be the financial aggregators providing anytime anywhere access

Fraud Protection

16A.T. Kearney /SCB/IT Vision

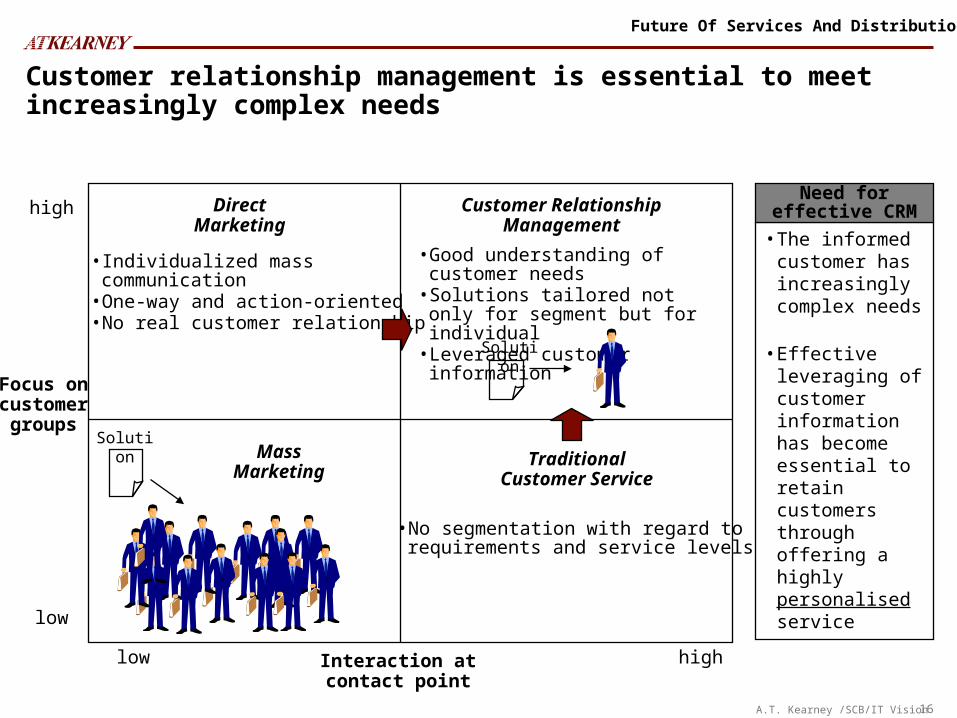

Customer relationship management is essential to meet increasingly complex needs

Focus oncustomer

groups

Customer RelationshipManagement

Interaction atcontact point

DirectMarketing

TraditionalCustomer Service

MassMarketing

• Individualized mass communication

• One-way and action-oriented• No real customer relationship

• Good understanding of customer needs

• Solutions tailored not only for segment but for individual

• Leveraged customer information

• No segmentation with regard torequirements and service levels

highlow

low

high

Solution

Solution

• The informed customer has increasingly complex needs

• Effective leveraging of customer information has become essential to retain customers through offering a highly personalised service

Need for effective CRM

Future Of Services And Distribution

17A.T. Kearney /SCB/IT Vision

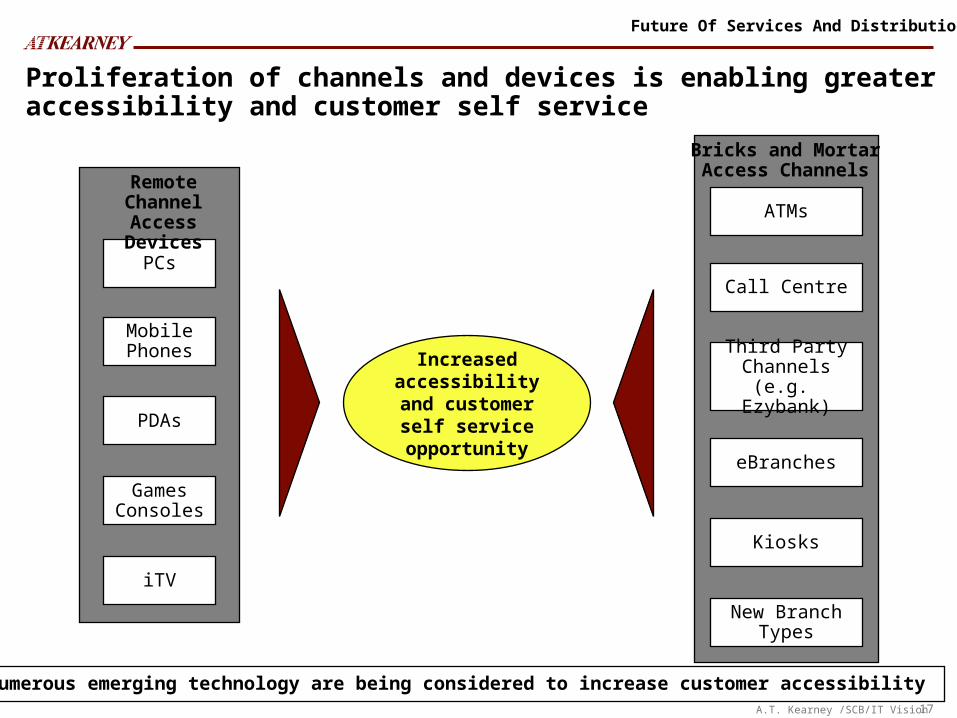

Proliferation of channels and devices is enabling greater accessibility and customer self service

PCs

PDAs

Games Consoles

iTV

Remote Channel Access Devices ATMs

Call Centre

Third Party Channels

(e.g. Ezybank)

eBranches

Bricks and MortarAccess Channels

Kiosks

New BranchTypes

Increased accessibility and

customer self service

opportunity

Mobile Phones

Numerous emerging technology are being considered to increase customer accessibility

Future Of Services And Distribution

18A.T. Kearney /SCB/IT Vision

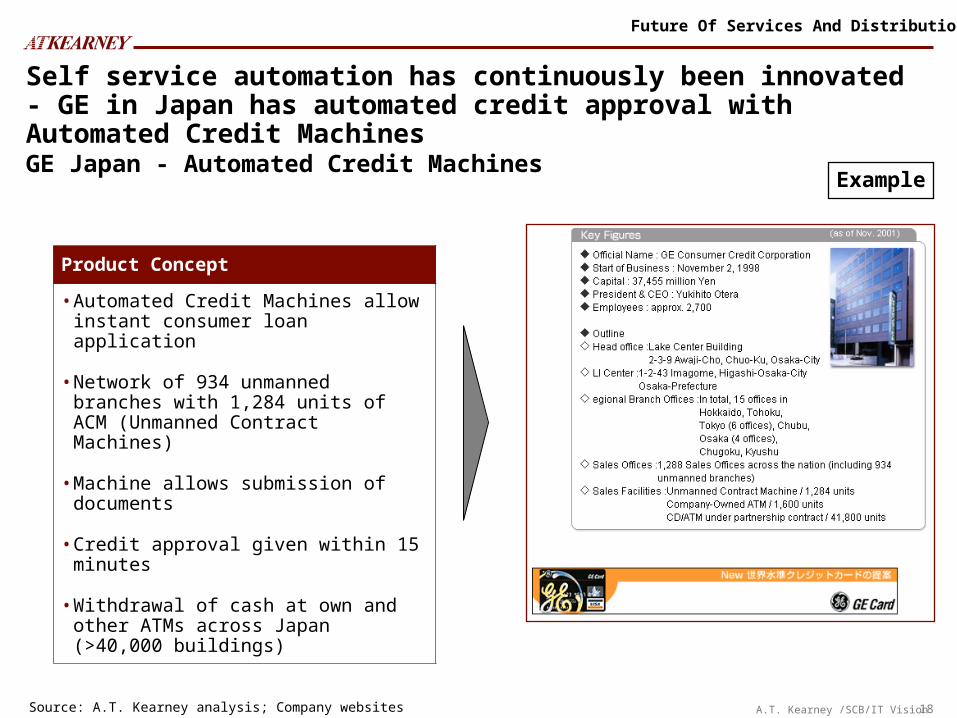

Self service automation has continuously been innovated - GE in Japan has automated credit approval with Automated Credit Machines

Product Concept

• Automated Credit Machines allow instant consumer loan application

• Network of 934 unmanned branches with 1,284 units of ACM (Unmanned Contract Machines)

• Machine allows submission of documents

• Credit approval given within 15 minutes

• Withdrawal of cash at own and other ATMs across Japan (>40,000 buildings)

Source: A.T. Kearney analysis; Company websites

GE Japan - Automated Credit MachinesExample

Future Of Services And Distribution

19A.T. Kearney /SCB/IT Vision

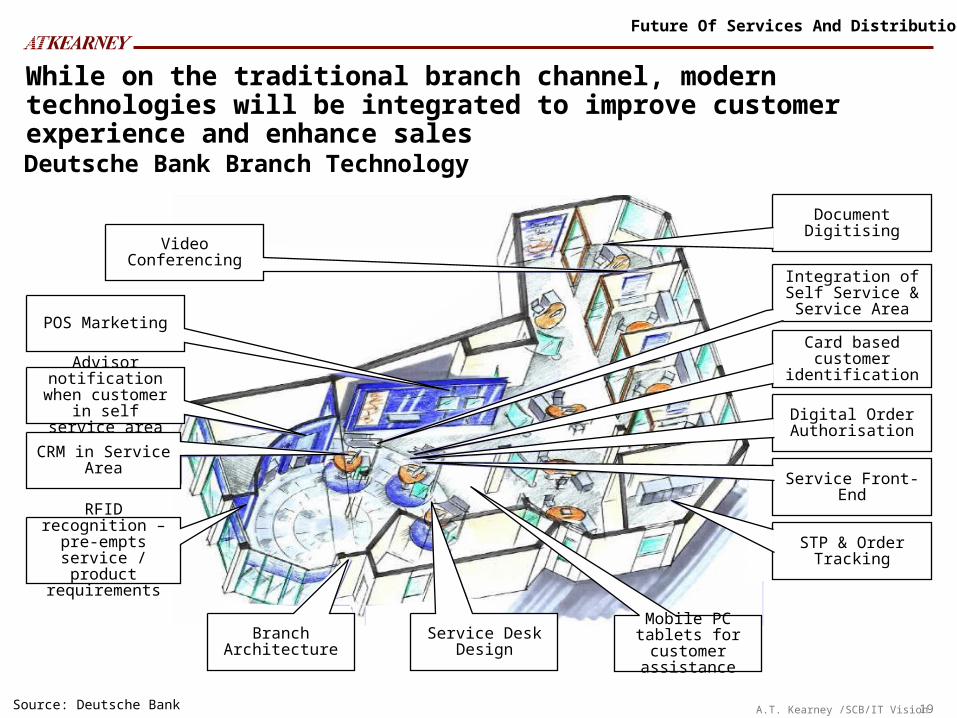

While on the traditional branch channel, modern technologies will be integrated to improve customer experience and enhance sales

CRM in Service Area

Advisor notification when customer in self service area

Video Conferencing

POS Marketing

Document Digitising

Integration of Self Service & Service

Area

Card based customer

identification

Branch Architecture

Service Desk Design

Digital Order Authorisation

Service Front-End

STP & Order Tracking

Source: Deutsche Bank

RFID recognition – pre-empts service /

product requirements

Mobile PC tablets for customer assistance

Future Of Services And Distribution

Deutsche Bank Branch Technology

20A.T. Kearney /SCB/IT Vision

Alternative channels have gained more recognition - Banks are offering customers individual, attractive and demand-oriented solutions via mobile

Quite a few retail banks are entering the mobile services market again with demand-oriented offers

Prepaid loading: customers can load their prepaid mobile cards directly via the transactions portal. The amount is booked directly from the account.

Push services: The customer can select individual criteria on the transactions portal according to which he receives result-based news via SMS. Example: M-TAN of the Postbank, result-based trigger, e.g. for receipt of cash or order execution, news services, SMS marketing

Benefits for bank: Differentiation in the market Purely electronic processing Proceeds for prepaid

loading Effective advertising of re-

entry into mobile services

Benefits for customer: Value-added services Easy-to-use functions Flexibility

Alternative Channels – Mobile Solutions

Future Of Services And Distribution

21A.T. Kearney /SCB/IT Vision

ABN AMRO deploys instant messaging to promote external collaboration with customers and partners

ABN AMRO deployed MindAlign IM to allow bank staff to collaborate externally with clients and partners, as well as internally within the organization

• IM to help the company to trade and sell more effectively, and to reduce its reliance on e-mail, which is more expensive, slower and less secure

• MindAlign rolled out to 2,500 staff in over 45 countries. The solution allows staff to disseminate information gleaned from in-person and telephone conversations in real-time to business clients, partners and colleagues

• ABN AMRO also uses IM to deliver research reports at regular times during the day. The solution allows groups of staff to communicate and collaborate on projects in realtime, and employees to create user communities pertaining to their own responsibilities.

• In addition, MindAlign preserves unstructured information through archiving and metadata access. Bank executives expect the solution to provide instant benefits to the company, increasing revenues by allowing staff to share information, news and documents in real time, and reducing costs by decreasing e-mail volume.

Alternative Channels - Instant Messaging

Future Of Services And Distribution

22A.T. Kearney /SCB/IT Vision

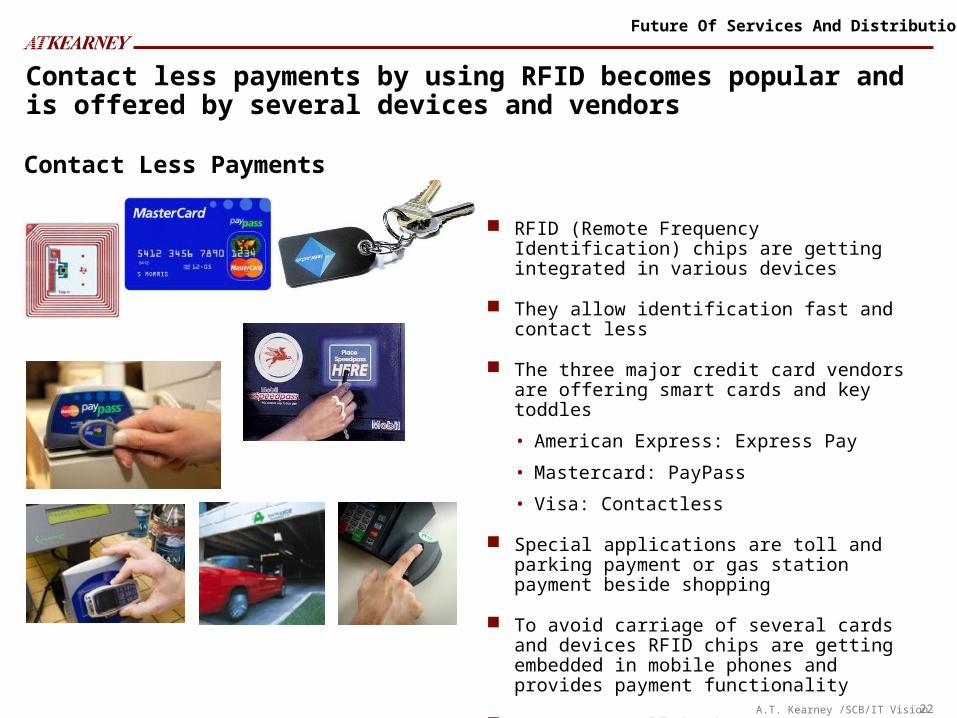

Contact less payments by using RFID becomes popular and is offered by several devices and vendors

RFID (Remote Frequency Identification) chips are getting integrated in various devices

They allow identification fast and contact less

The three major credit card vendors are offering smart cards and key toddles

• American Express: Express Pay

• Mastercard: PayPass

• Visa: Contactless

Special applications are toll and parking payment or gas station payment beside shopping

To avoid carriage of several cards and devices RFID chips are getting embedded in mobile phones and provides payment functionality

Next step will be biometric identification making devices redundant

Contact Less Payments

Future Of Services And Distribution

23A.T. Kearney /SCB/IT Vision

For business customers, Schwab has successfully automated trading and routine enquiries, and is adding further value through client advice and technological innovation

Source: Schwab Website; Schwab Press Releases; A.T. Kearney ResearchWebsite: http://www.schwab.com

• Pursuing a “clicks and mortar” touch point strategy:— Utilises physical branch, phone and web based distribution channels to maximise customer channel choice— And integrate “high tech” with “high touch”

• Using branches for customer acquisition, customer advice and facilitating transactions:— Offering segmented branch services

– Standard branches offer "Portfolio Consultation" which provides a service where investors can walk off the street into branches and get their existing portfolio analysed

– The invitation-only "Signature Service" branch offices provide services for high-end accounts beginning at $1 million

— Branches remain an important customer acquisition point with 70% customers acquired through branches

• Continuing to leverage technology to automate services:— Very successfully automated trading and routine inquiries to the internet with immediate confirmation of trades— Automating advice guidance to free up advisers to focus on providing higher value consultation:

– “Portfolio Checkup” is an on-line asset-allocation planner based on an investors tolerance for risk; – “Sell Analyser” is an online tool that evaluates the cost basis of the portfolio and recommend which to sell for tax

losses; – “Portfolio Tracker” allows investors to benchmark portfolios against standards/ indexes and identify under

performing segments— Introduced “Schwab Learning Center” – an interactive web based application to educate clients on investment— Introducing trading services via mobile phones using WAP technologies: Transmitting content (real time information)

to hand held devices via “Pocketbroker” — Launching an account aggregation service powered by Yodlee: Allowing investors to aggregate their on-line financial

information from a variety of sources such as brokerages, banks and credit card companies at no extra cost

Future Of Services And Distribution

24A.T. Kearney /SCB/IT Vision

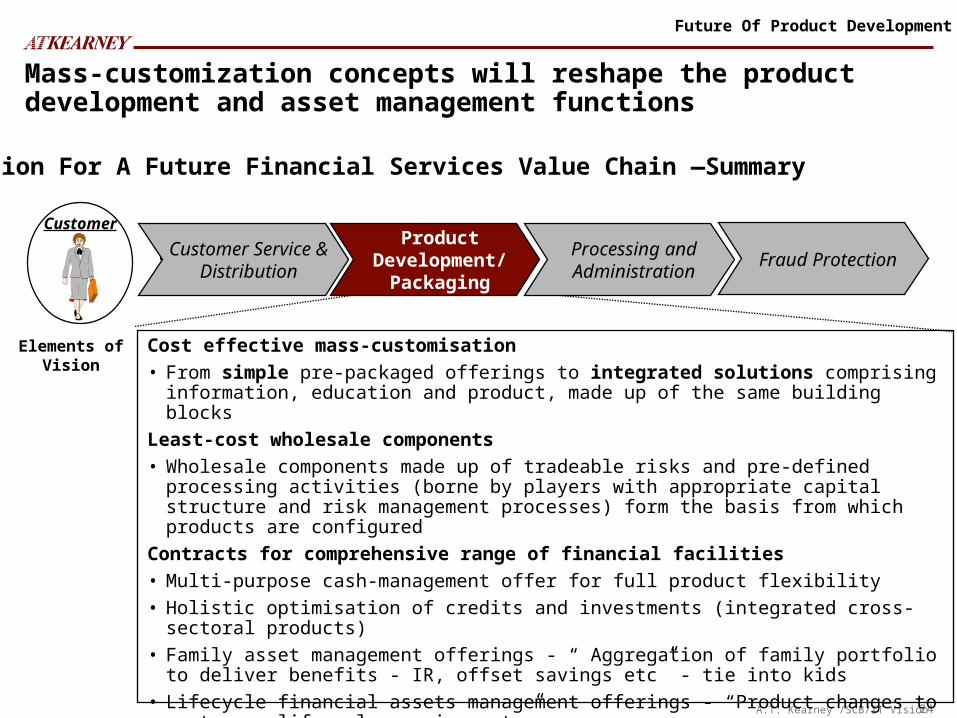

Future Of Product Development

Customer

Vision For A Future Financial Services Value Chain —Summary

Cost effective mass-customisation

• From simple pre-packaged offerings to integrated solutions comprising information, education and product, made up of the same building blocks

Least-cost wholesale components

• Wholesale components made up of tradeable risks and pre-defined processing activities (borne by players with appropriate capital structure and risk management processes) form the basis from which products are configured

Contracts for comprehensive range of financial facilities

• Multi-purpose cash-management offer for full product flexibility

• Holistic optimisation of credits and investments (integrated cross-sectoral products)

• Family asset management offerings - “ Aggregation of family portfolio to deliver benefits - IR, offset savings etc” - tie into kids

• Lifecycle financial assets management offerings - “Product changes to meet your lifecycle requirements”

Elements of Vision

Mass-customization concepts will reshape the product development and asset management functions

Customer Service & Distribution

Processing and Administration

Product Development/

PackagingFraud Protection

25A.T. Kearney /SCB/IT Vision

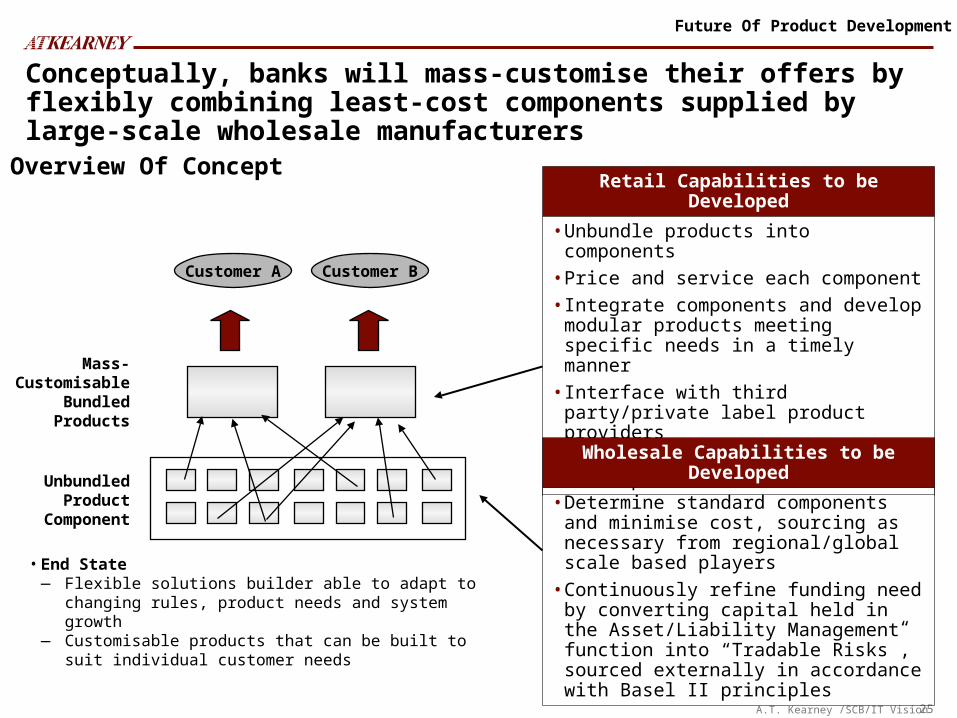

Conceptually, banks will mass-customise their offers by flexibly combining least-cost components supplied by large-scale wholesale manufacturersOverview Of Concept

Retail Capabilities to be Developed

• Unbundle products into components

• Price and service each component

• Integrate components and develop modular products meeting specific needs in a timely manner

• Interface with third party/private label product providers

• Manage permissions to enable cross-product collaboration

Customer A Customer B

Unbundled Product

Component

Mass-Customisable

Bundled Products

• End State— Flexible solutions builder able to adapt to changing rules,

product needs and system growth— Customisable products that can be built to suit individual

customer needs

Wholesale Capabilities to be Developed

• Determine standard components and minimise cost, sourcing as necessary from regional/global scale based players

• Continuously refine funding need by converting capital held in the Asset/Liability Management function into “Tradable Risks”, sourced externally in accordance with Basel II principles

Future Of Product Development

26A.T. Kearney /SCB/IT Vision

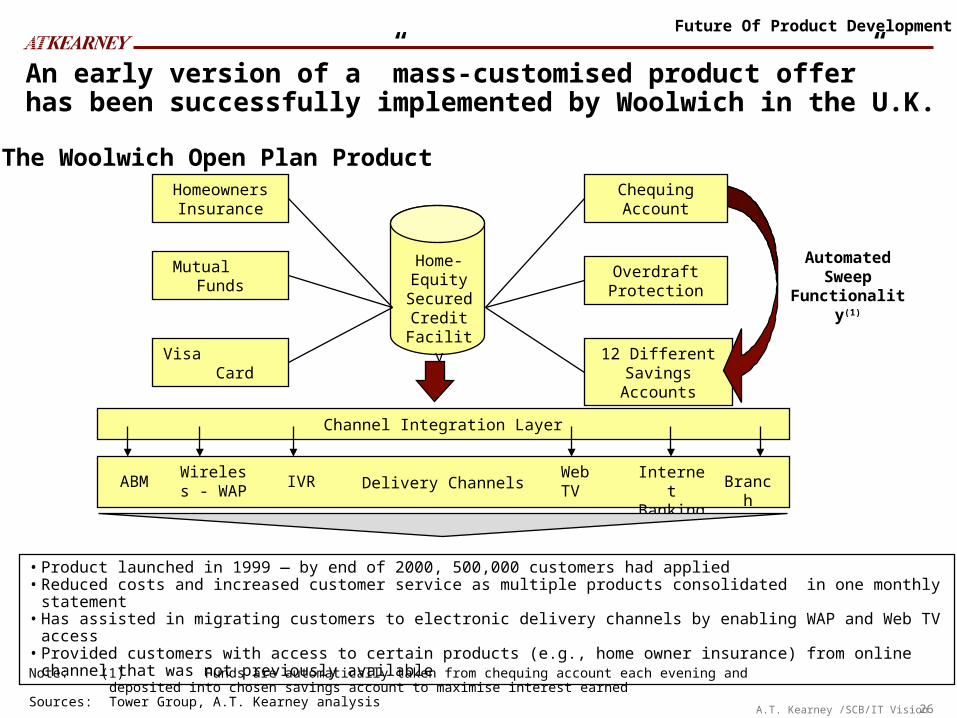

12 Different Savings Accounts

An early version of a ”mass-customised product offer” has been successfully implemented by Woolwich in the U.K.

Chequing Account

Home-Equity

Secured Credit Facility

Delivery Channels

Channel Integration Layer

Homeowners Insurance

Note: (1) Funds are automatically taken from chequing account each evening and deposited into chosen savings account to maximise interest earned

Sources: Tower Group, A.T. Kearney analysis

Overdraft Protection

The Woolwich Open Plan Product

• Product launched in 1999 — by end of 2000, 500,000 customers had applied• Reduced costs and increased customer service as multiple products consolidated in one monthly statement• Has assisted in migrating customers to electronic delivery channels by enabling WAP and Web TV access• Provided customers with access to certain products (e.g., home owner insurance) from online channel that was not previously

available

ABMWireless -

WAPWeb TV

BranchInternet Banking

IVR

Automated Sweep

Functionality(1)

Mutual Funds

Visa Card

Future Of Product Development

27A.T. Kearney /SCB/IT Vision

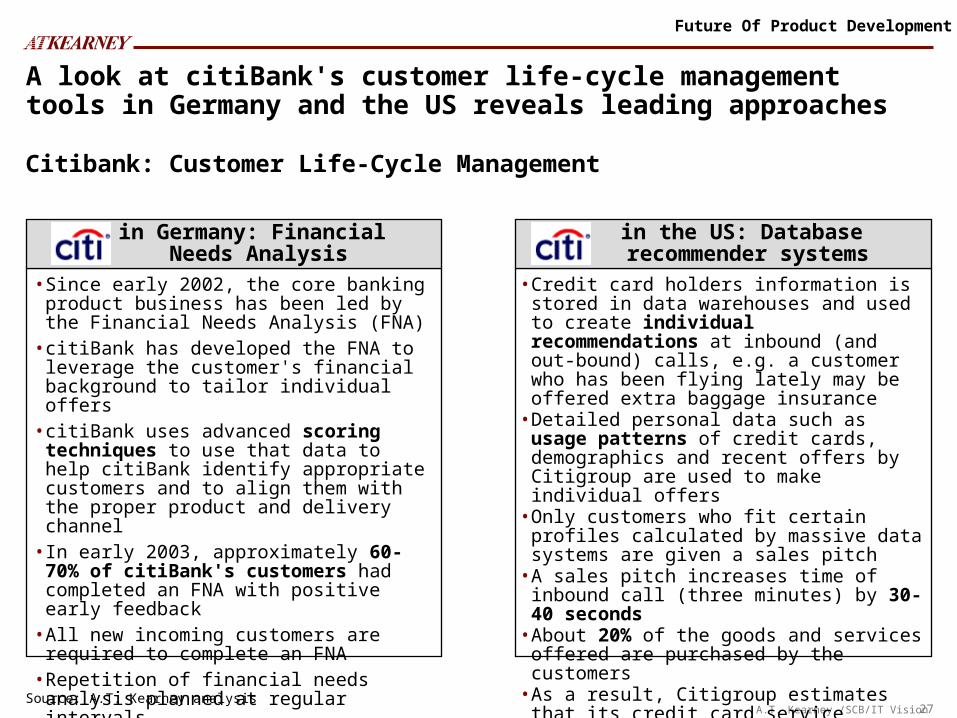

A look at citiBank's customer life-cycle management tools in Germany and the US reveals leading approaches

Citibank: Customer Life-Cycle Management

• Since early 2002, the core banking product business has been led by the Financial Needs Analysis (FNA)

• citiBank has developed the FNA to leverage the customer's financial background to tailor individual offers

• citiBank uses advanced scoring techniques to use that data to help citiBank identify appropriate customers and to align them with the proper product and delivery channel

• In early 2003, approximately 60-70% of citiBank's customers had completed an FNA with positive early feedback

• All new incoming customers are required to complete an FNA

• Repetition of financial needs analysis planned at regular intervals

in Germany: Financial Needs Analysis

• Credit card holders information is stored in data warehouses and used to create individual recommendations at inbound (and out-bound) calls, e.g. a customer who has been flying lately may be offered extra baggage insurance

• Detailed personal data such as usage patterns of credit cards, demographics and recent offers by Citigroup are used to make individual offers

• Only customers who fit certain profiles calculated by massive data systems are given a sales pitch

• A sales pitch increases time of inbound call (three minutes) by 30-40 seconds

• About 20% of the goods and services offered are purchased by the customers

• As a result, Citigroup estimates that its credit card service centers are bringing in 115-120% of their expenses through transforming account maintenance calls into up- and cross-sales

in the US: Database recommender systems

Source: A.T. Kearney analysis

Future Of Product Development

28A.T. Kearney /SCB/IT Vision

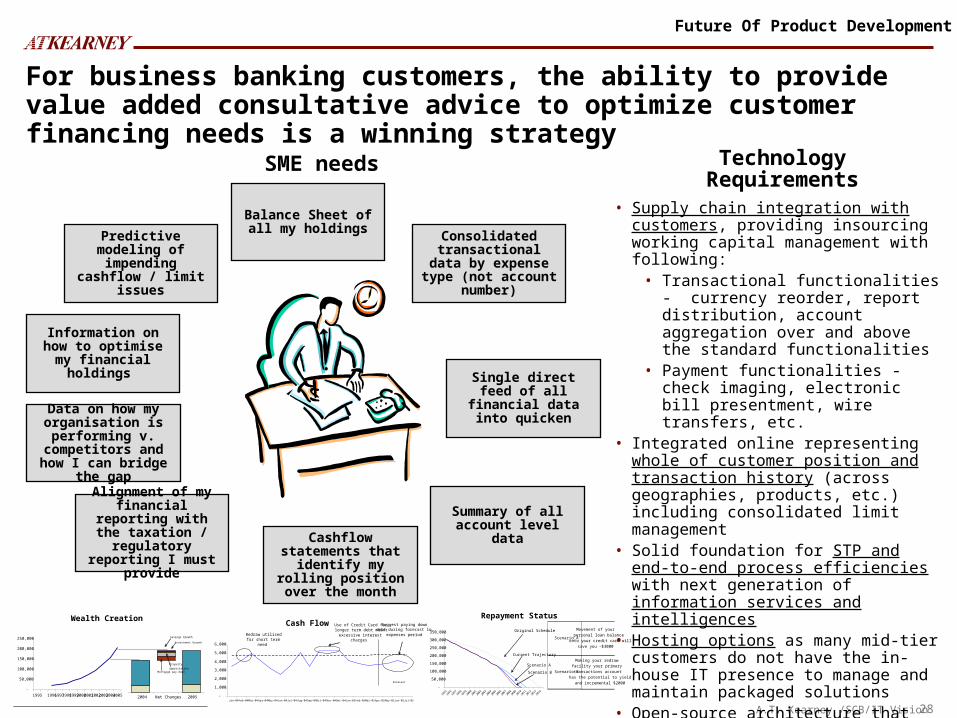

SME needs Technology Requirements

Consolidated transactional data by

expense type (not account number)

Single direct feed of all financial data into

quicken

Summary of all account level data

Balance Sheet of all my holdings

Cashflow statements that identify my

rolling position over the month

Predictive modeling of impending

cashflow / limit issues

Information on how to optimise my

financial holdings

Data on how my organisation is performing v.

competitors and how I can bridge the gap

Alignment of my financial reporting with the taxation /

regulatory reporting I must provide

For business banking customers, the ability to provide value added consultative advice to optimize customer financing needs is a winning strategy

Wealth Creation

-

50,000

100,000

150,000

200,000

250,000

1995 1996199719981999200020012002200320042005 2004 Net Changes 2005

Mortgage pay down

Property

appreciation

Investment Growth

Savings Growth

Cash Flow

-

1,000

2,000

3,000

4,000

5,000

6,000

Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04 Jul-04 Aug-04 Sep-04 Oct-04 Nov-04 Dec-04 Jan-05 Feb-05 Mar-05 Apr-05 May-05 Jun-05 Jul-05

Redraw utilised for short term

need

Use of Credit Card for longer term debt meant

excessive interest charges

Suggest paying down debt during forecast low

expenses period

Forecast

Repayment Status

Movement of your

personal loan balance

onto your credit card will

save you ~$3000

Making your redraw

facility your primary

transactions account

has the potential to yield

and incremental $2000

Scenario A

Scenario B

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Original Schedule

Current Trajectory

Scenario A

Scenario B

• Supply chain integration with customers, providing insourcing working capital management with following:

• Transactional functionalities - currency reorder, report distribution, account aggregation over and above the standard functionalities

• Payment functionalities - check imaging, electronic bill presentment, wire transfers, etc.

• Integrated online representing whole of customer position and transaction history (across geographies, products, etc.) including consolidated limit management

• Solid foundation for STP and end-to-end process efficiencies with next generation of information services and intelligences

• Hosting options as many mid-tier customers do not have the in-house IT presence to manage and maintain packaged solutions

• Open-source architecture that enables the bank to customize the solution and integrate it with other customer-facing products so that customer information flows seamlessly from one solution to another

Future Of Product Development

29A.T. Kearney /SCB/IT Vision

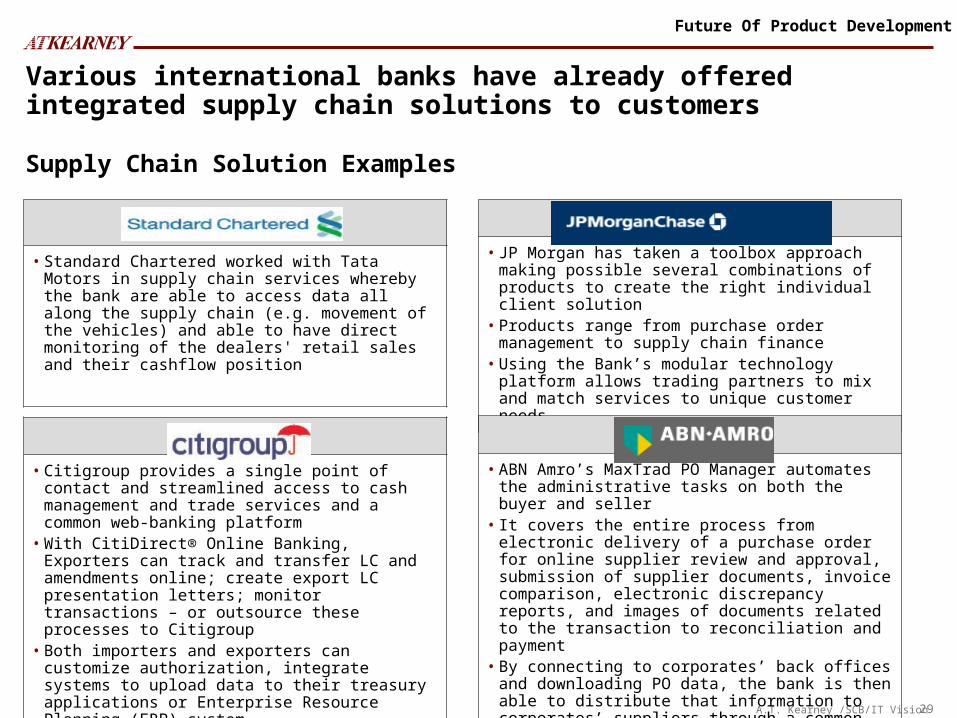

Various international banks have already offered integrated supply chain solutions to customers

Supply Chain Solution Examples

• Standard Chartered worked with Tata Motors in supply chain services whereby the bank are able to access data all along the supply chain (e.g. movement of the vehicles) and able to have direct monitoring of the dealers' retail sales and their cashflow position

• JP Morgan has taken a toolbox approach making possible several combinations of products to create the right individual client solution

• Products range from purchase order management to supply chain finance

• Using the Bank’s modular technology platform allows trading partners to mix and match services to unique customer needs.

• Citigroup provides a single point of contact and streamlined access to cash management and trade services and a common web-banking platform

• With CitiDirect® Online Banking, Exporters can track and transfer LC and amendments online; create export LC presentation letters; monitor transactions – or outsource these processes to Citigroup

• Both importers and exporters can customize authorization, integrate systems to upload data to their treasury applications or Enterprise Resource Planning (ERP) system

• ABN Amro’s MaxTrad PO Manager automates the administrative tasks on both the buyer and seller

• It covers the entire process from electronic delivery of a purchase order for online supplier review and approval, submission of supplier documents, invoice comparison, electronic discrepancy reports, and images of documents related to the transaction to reconciliation and payment

• By connecting to corporates’ back offices and downloading PO data, the bank is then able to distribute that information to corporates’ suppliers through a common message platform

Future Of Product Development

30A.T. Kearney /SCB/IT Vision

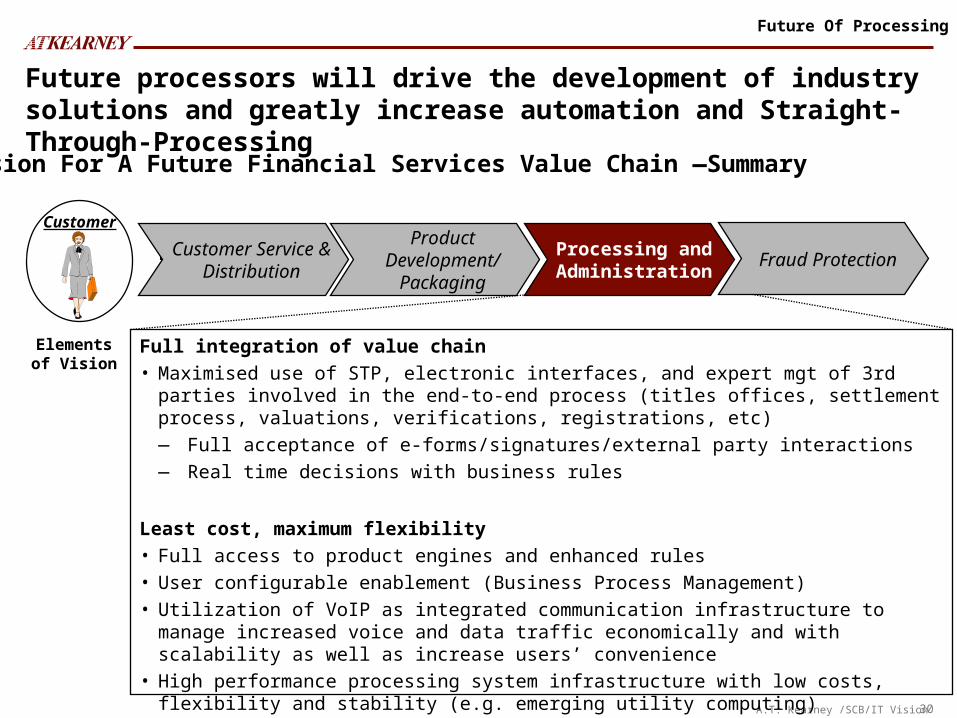

Future Of Processing

Customer

Future processors will drive the development of industry solutions and greatly increase automation and Straight-Through-Processing

Vision For A Future Financial Services Value Chain —Summary

Full integration of value chain• Maximised use of STP, electronic interfaces, and expert mgt of 3rd parties involved in the end-

to-end process (titles offices, settlement process, valuations, verifications, registrations, etc)― Full acceptance of e-forms/signatures/external party interactions― Real time decisions with business rules

Least cost, maximum flexibility• Full access to product engines and enhanced rules• User configurable enablement (Business Process Management)• Utilization of VoIP as integrated communication infrastructure to manage increased voice and

data traffic economically and with scalability as well as increase users’ convenience• High performance processing system infrastructure with low costs, flexibility and stability (e.g.

emerging utility computing)

Elements of Vision

Customer Service & Distribution

Processing and Administration

Product Development/

PackagingFraud Protection

31A.T. Kearney /SCB/IT Vision

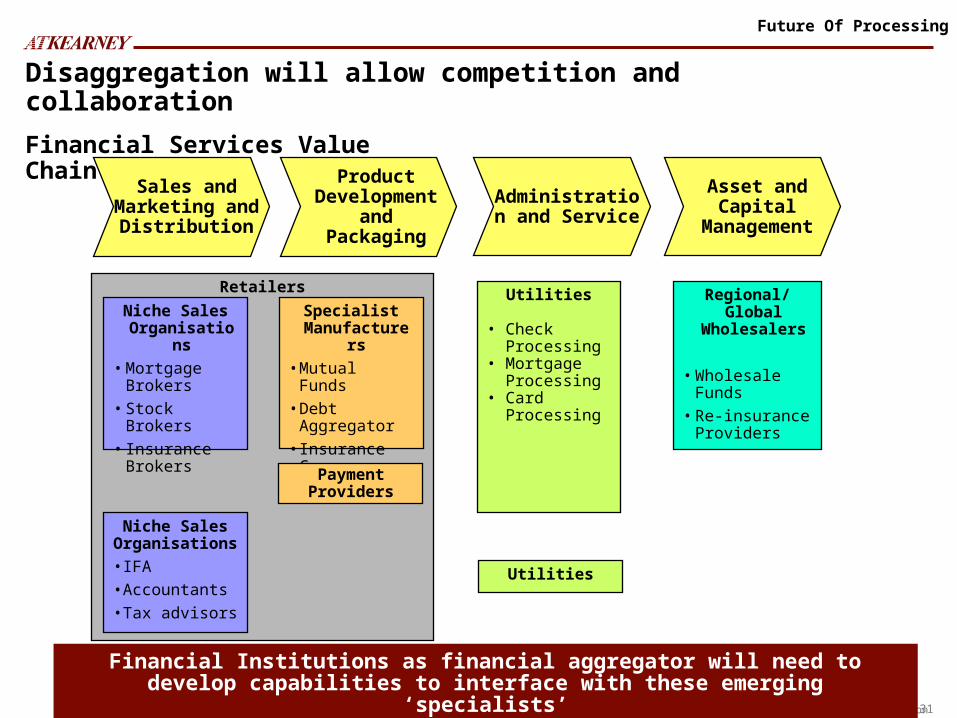

Disaggregation will allow competition and collaboration

Financial Services Value Chain

Sales and Marketing and

Distribution

Asset and Capital

Management

Administration and Service

Product Development

and Packaging

Retailers

Niche Sales Organisations

• IFA

• Accountants

• Tax advisors

Specialist Manufacturers

• Mutual Funds

• Debt Aggregator

• Insurance Co

Utilities

• Check Processing

• Mortgage Processing

• Card Processing

Regional/Global Wholesalers

• Wholesale Funds

• Re-insurance Providers

Niche Sales Organisations

• Mortgage Brokers

• Stock Brokers

• Insurance Brokers

Utilities

Payment Providers

Financial Institutions as financial aggregator will need to develop capabilities to interface with these emerging ‘specialists’

Future Of Processing

32A.T. Kearney /SCB/IT Vision

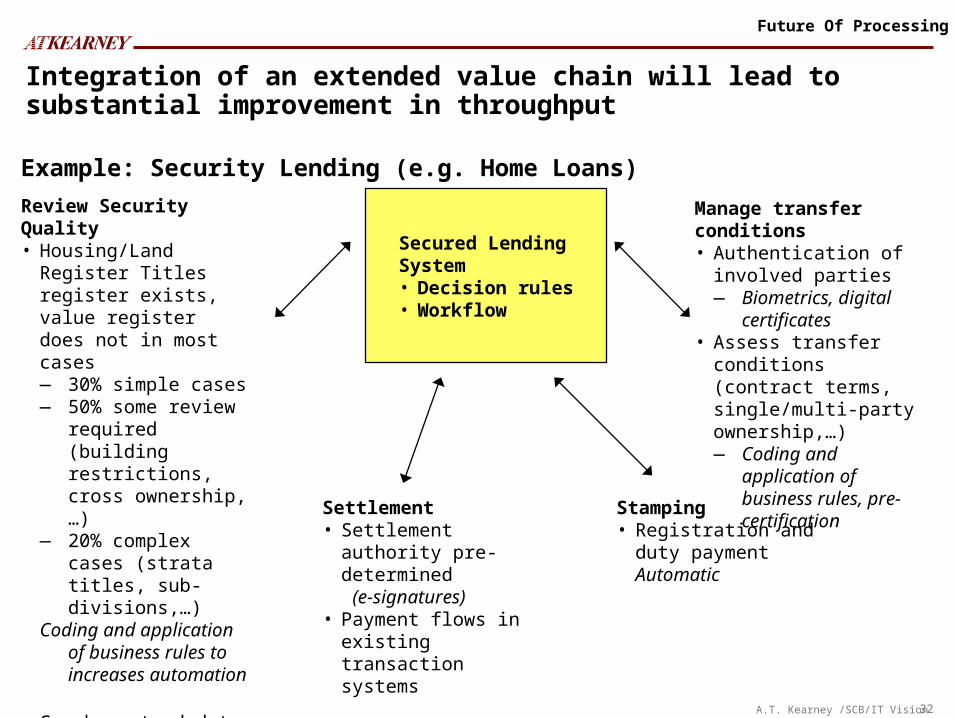

Integration of an extended value chain will lead to substantial improvement in throughput

Secured Lending System• Decision rules• Workflow

Review Security Quality• Housing/Land Register

Titles register exists, value register does not in most cases― 30% simple cases― 50% some review

required (building restrictions, cross ownership,…)

― 20% complex cases (strata titles, sub-divisions,…)

Coding and application of business rules to increases automation

• Can be extended to any security/any environment― Livestock register— Financial Instruments― …

Manage transfer conditions• Authentication of

involved parties― Biometrics, digital

certificates• Assess transfer

conditions (contract terms, single/multi-party ownership,…)― Coding and

application of business rules, pre-certificationSettlement

• Settlement authority pre-determined (e-signatures)

• Payment flows in existing transaction systems

Stamping• Registration and duty

paymentAutomatic

Example: Security Lending (e.g. Home Loans)

Future Of Processing

33A.T. Kearney /SCB/IT Vision

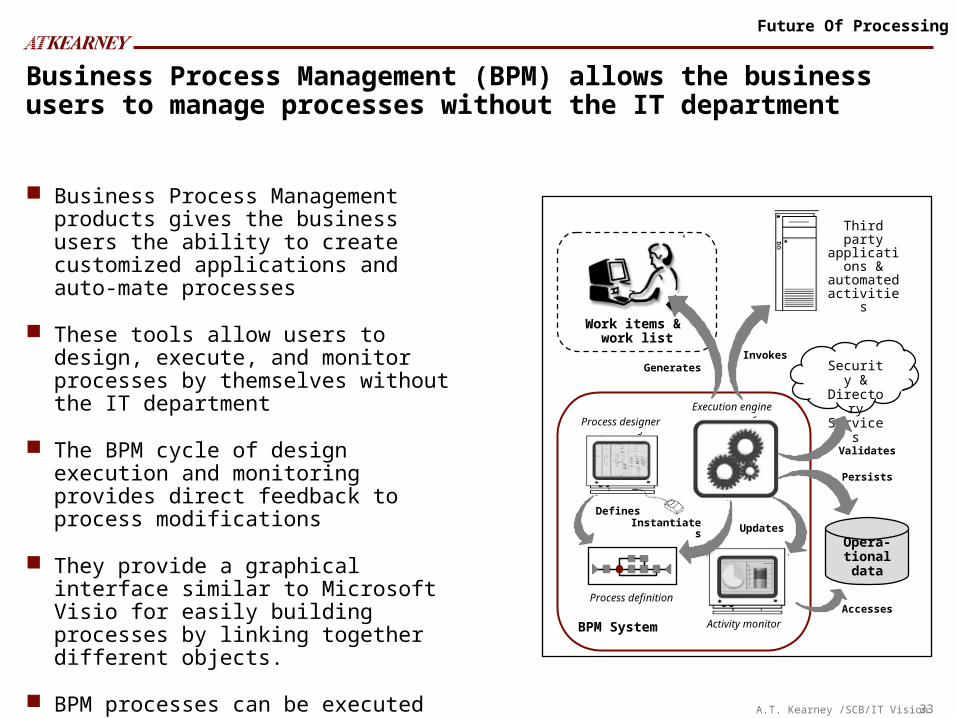

Business Process Management (BPM) allows the business users to manage processes without the IT department

Opera-tional data

Security &

Directory Services

Work items & work list

Third party applications & automated

activities

BPM System

Execution engine

Process designer

Activity monitor

Process definition

UpdatesInstantiates

Defines

Accesses

Persists

Validates

InvokesGenerates

Business Process Management products gives the business users the ability to create customized applications and auto-mate processes

These tools allow users to design, execute, and monitor processes by themselves without the IT department

The BPM cycle of design execution and monitoring provides direct feedback to process modifications

They provide a graphical interface similar to Microsoft Visio for easily building processes by linking together different objects.

BPM processes can be executed to interact with both employees and systems

BPM saves time and money

Future Of Processing

34A.T. Kearney /SCB/IT Vision

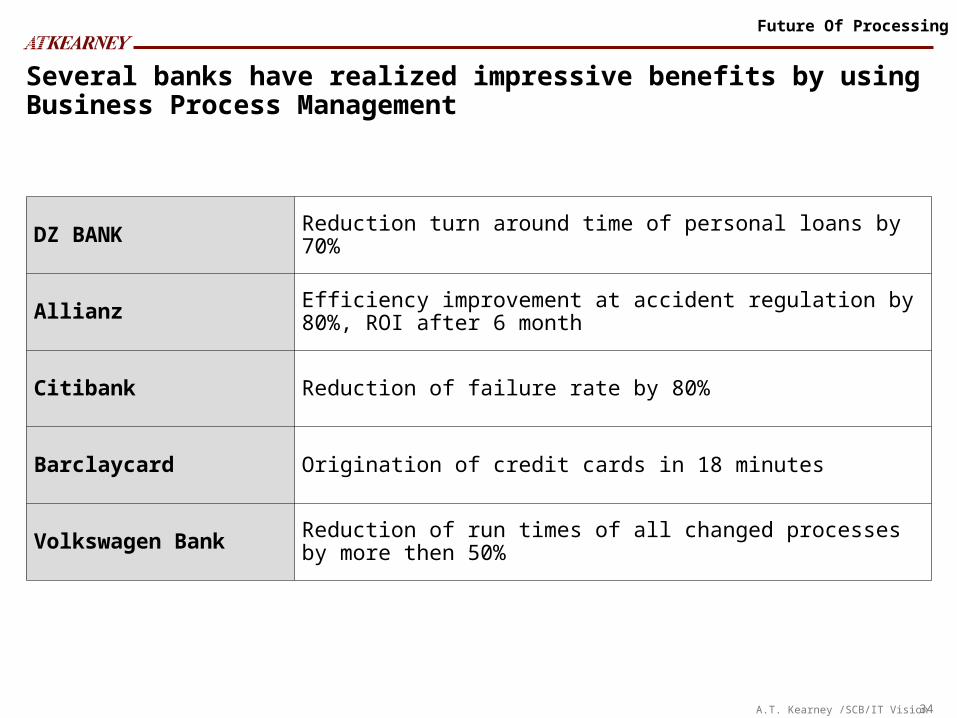

Several banks have realized impressive benefits by using Business Process Management

DZ BANK Reduction turn around time of personal loans by 70%

Allianz Efficiency improvement at accident regulation by 80%, ROI after 6 month

Citibank Reduction of failure rate by 80%

Barclaycard Origination of credit cards in 18 minutes

Volkswagen Bank Reduction of run times of all changed processes by more then 50%

Future Of Processing

35A.T. Kearney /SCB/IT Vision

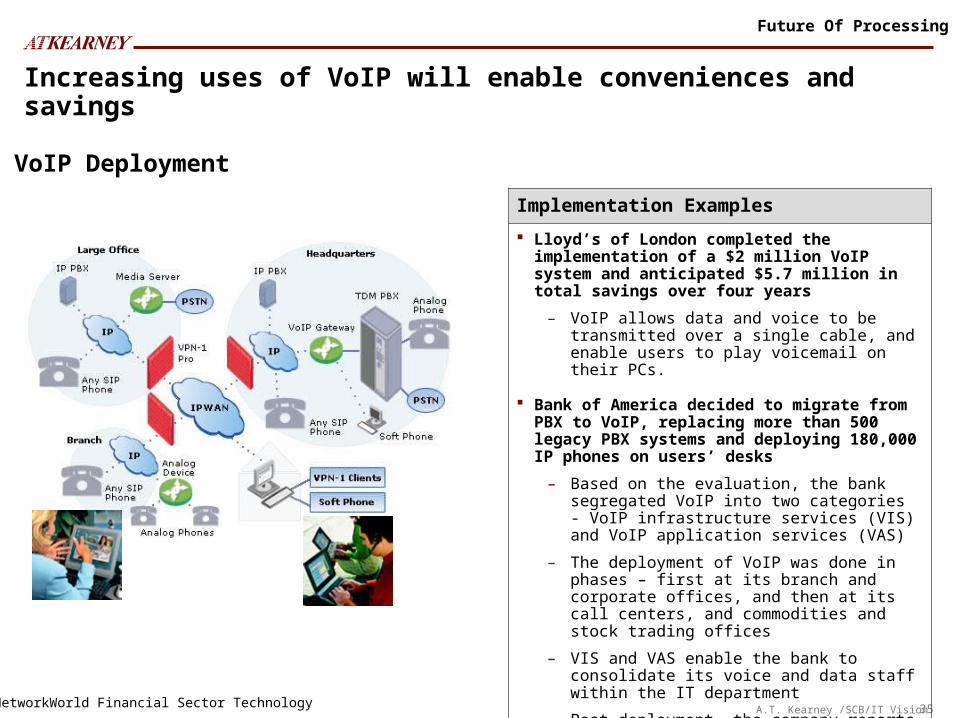

Increasing uses of VoIP will enable conveniences and savings

VoIP Deployment

Implementation Examples

Lloyd’s of London completed the implementation of a $2 million VoIP system and anticipated $5.7 million in total savings over four years

– VoIP allows data and voice to be transmitted over a single cable, and enable users to play voicemail on their PCs.

Bank of America decided to migrate from PBX to VoIP, replacing more than 500 legacy PBX systems and deploying 180,000 IP phones on users’ desks

– Based on the evaluation, the bank segregated VoIP into two categories - VoIP infrastructure services (VIS) and VoIP application services (VAS)

– The deployment of VoIP was done in phases – first at its branch and corporate offices, and then at its call centers, and commodities and stock trading offices

– VIS and VAS enable the bank to consolidate its voice and data staff within the IT department

– Post-deployment, the company reports significant reduction in telephony costs and enhanced employee productivity

Source: NetworkWorld Financial Sector Technology

Future Of Processing

36A.T. Kearney /SCB/IT Vision

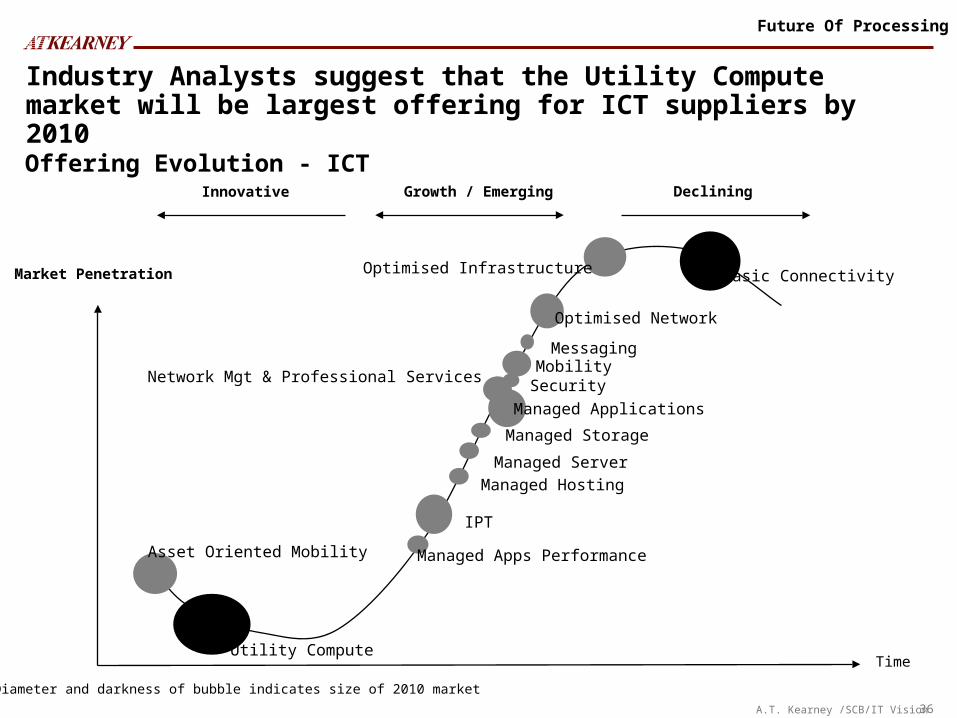

Industry Analysts suggest that the Utility Compute market will be largest offering for ICT suppliers by 2010

Offering Evolution - ICT

Time

Market Penetration Basic ConnectivityOptimised Infrastructure

Optimised Network

Messaging

SecurityMobility

IPT

Asset Oriented Mobility

Utility Compute

Managed Storage

Managed Server

Managed Hosting

Managed Apps Performance

Managed Applications

Network Mgt & Professional Services

DecliningGrowth / EmergingInnovative

Notes: (1) Diameter and darkness of bubble indicates size of 2010 marketSource: IDC

Future Of Processing

37A.T. Kearney /SCB/IT Vision

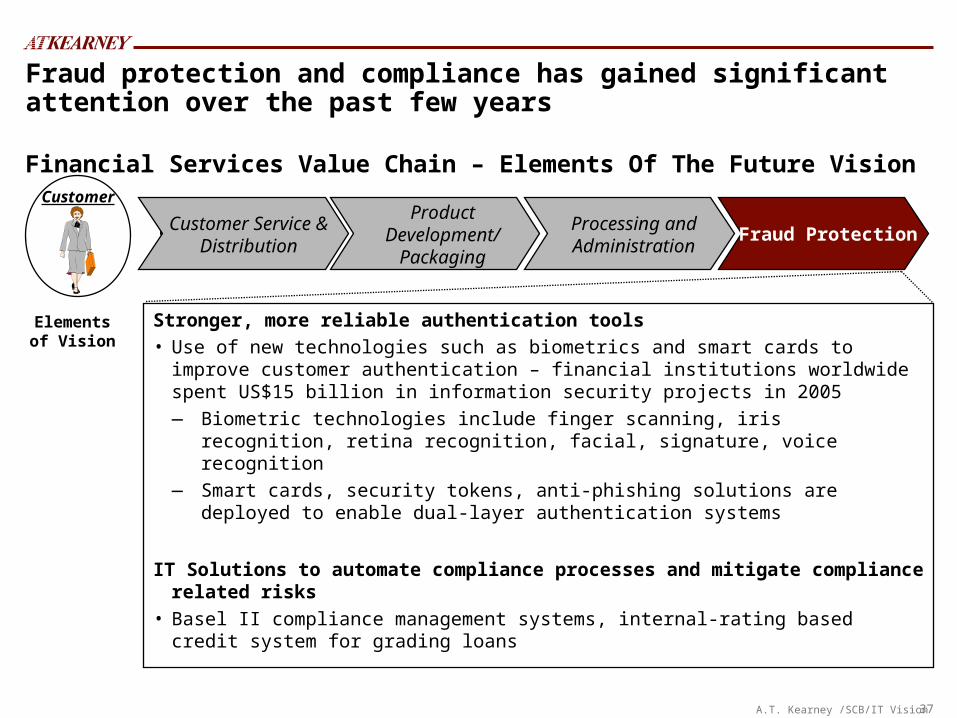

Elements of Vision

Financial Services Value Chain – Elements Of The Future VisionCustomer

Customer Service & Distribution

Processing and Administration

Product Development/

Packaging

Fraud protection and compliance has gained significant attention over the past few years

Fraud Protection

Stronger, more reliable authentication tools• Use of new technologies such as biometrics and smart cards to improve customer

authentication – financial institutions worldwide spent US$15 billion in information security projects in 2005― Biometric technologies include finger scanning, iris recognition, retina recognition,

facial, signature, voice recognition― Smart cards, security tokens, anti-phishing solutions are deployed to enable dual-layer

authentication systems

IT Solutions to automate compliance processes and mitigate compliance related risks• Basel II compliance management systems, internal-rating based credit system for grading

loans

38A.T. Kearney /SCB/IT Vision

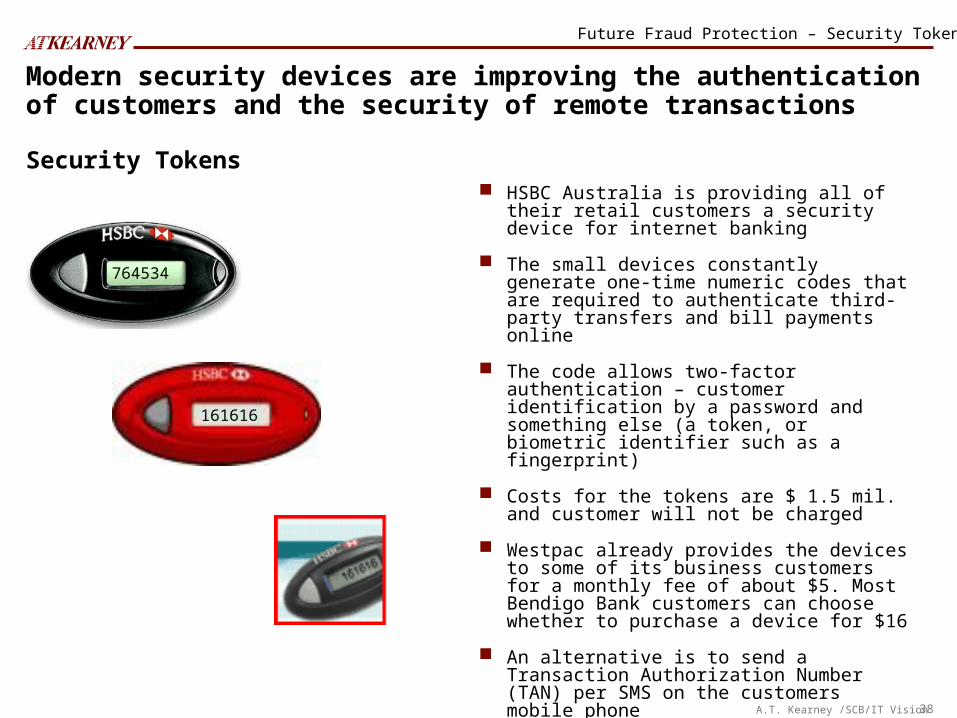

Modern security devices are improving the authentication of customers and the security of remote transactions

HSBC Australia is providing all of their retail customers a security device for internet banking

The small devices constantly generate one-time numeric codes that are required to authenticate third-party transfers and bill payments online

The code allows two-factor authentication – customer identification by a password and something else (a token, or biometric identifier such as a fingerprint)

Costs for the tokens are $ 1.5 mil. and customer will not be charged

Westpac already provides the devices to some of its business customers for a monthly fee of about $5. Most Bendigo Bank customers can choose whether to purchase a device for $16

An alternative is to send a Transaction Authorization Number (TAN) per SMS on the customers mobile phone

National Australia Bank and St George are sending SMS-generated codes to a customer's mobile phone

161616

764534

Security Tokens

Future Fraud Protection – Security Tokens

39A.T. Kearney /SCB/IT Vision

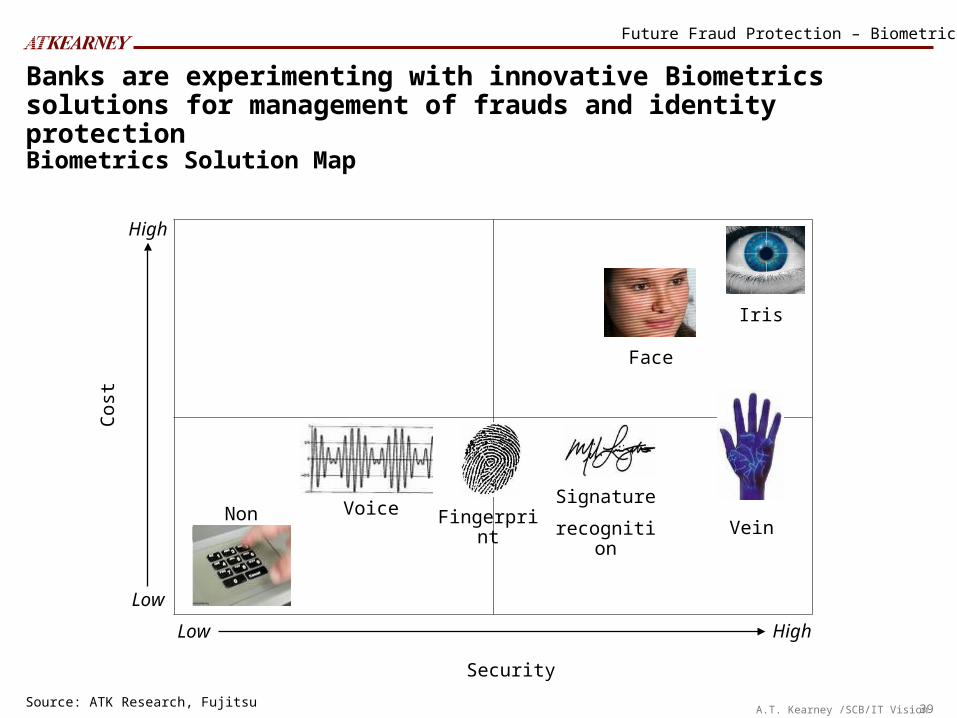

Banks are experimenting with innovative Biometrics solutions for management of frauds and identity protection

Source: ATK Research, Fujitsu

High

Low

HighLow

Security

Cos

t

Non Biometric FingerprintVein

Iris

Face

Signature

recognitionVoice

Biometrics Solution Map

Future Fraud Protection – Biometrics

40A.T. Kearney /SCB/IT Vision

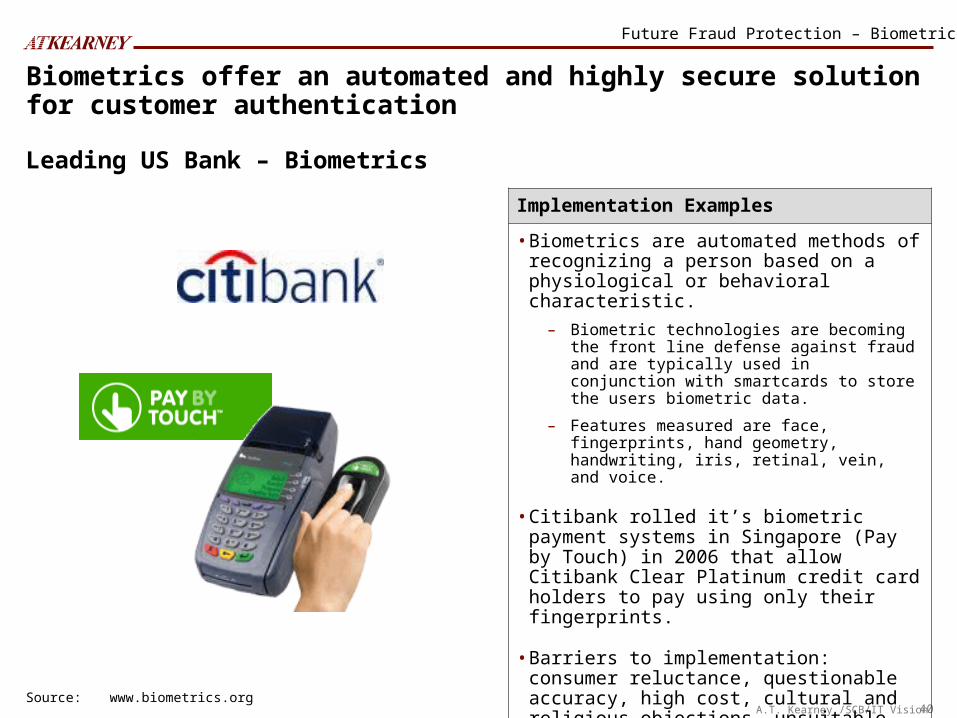

Biometrics offer an automated and highly secure solution for customer authentication

Source: www.biometrics.org

Implementation Examples

• Biometrics are automated methods of recognizing a person based on a physiological or behavioral characteristic.

– Biometric technologies are becoming the front line defense against fraud and are typically used in conjunction with smartcards to store the users biometric data.

– Features measured are face, fingerprints, hand geometry, handwriting, iris, retinal, vein, and voice.

• Citibank rolled it’s biometric payment systems in Singapore (Pay by Touch) in 2006 that allow Citibank Clear Platinum credit card holders to pay using only their fingerprints.

• Barriers to implementation: consumer reluctance, questionable accuracy, high cost, cultural and religious objections, unsuitable for some customers with injuries or missing fingers etc

Leading US Bank – Biometrics

Future Fraud Protection – Biometrics

41A.T. Kearney /SCB/IT Vision

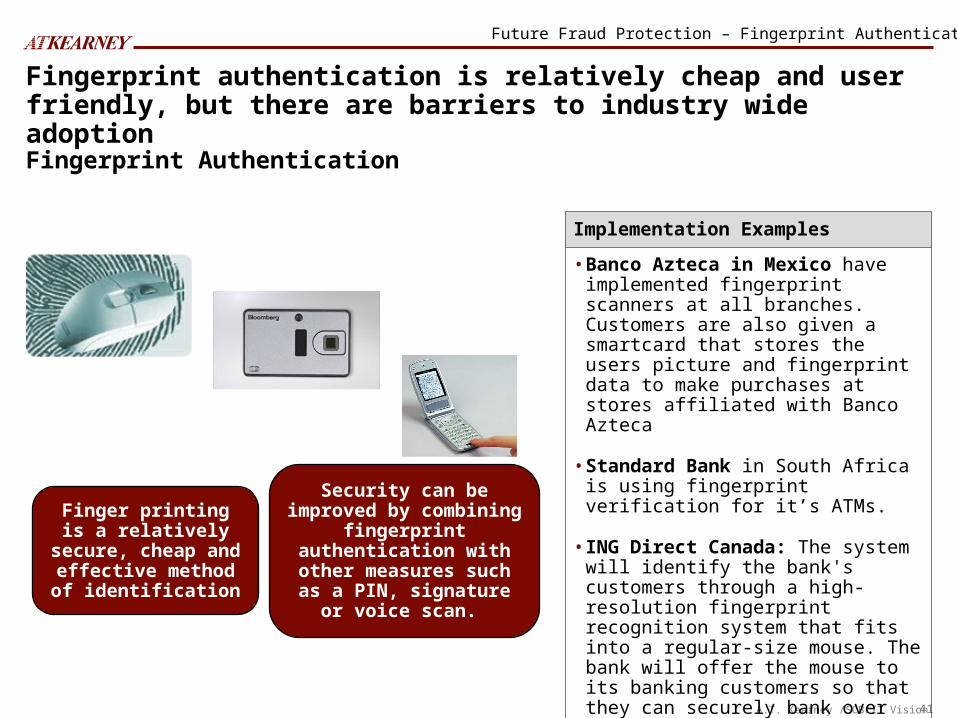

Fingerprint authentication is relatively cheap and user friendly, but there are barriers to industry wide adoption

Implementation Examples

• Banco Azteca in Mexico have implemented fingerprint scanners at all branches. Customers are also given a smartcard that stores the users picture and fingerprint data to make purchases at stores affiliated with Banco Azteca

• Standard Bank in South Africa is using fingerprint verification for it’s ATMs.

• ING Direct Canada: The system will identify the bank's customers through a high-resolution fingerprint recognition system that fits into a regular-size mouse. The bank will offer the mouse to its banking customers so that they can securely bank over the Internet.

Finger printing is a relatively secure,

cheap and effective method of

identification

Security can be improved by combining fingerprint authentication with other measures such as a PIN, signature or voice scan.

Fingerprint Authentication

Future Fraud Protection – Fingerprint Authentication

42A.T. Kearney /SCB/IT Vision

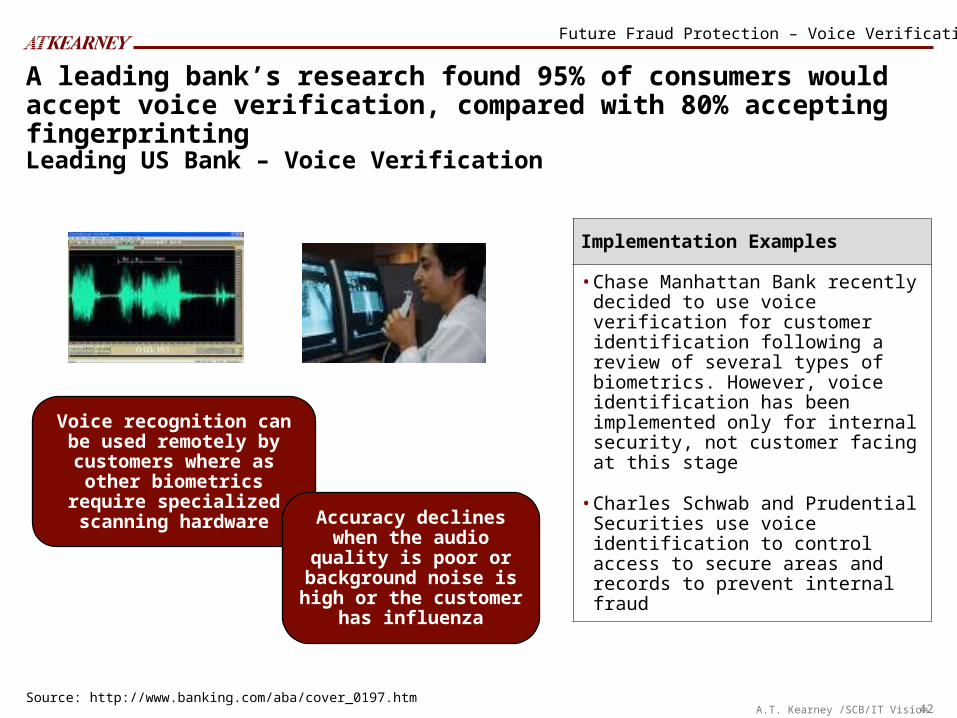

A leading bank’s research found 95% of consumers would accept voice verification, compared with 80% accepting fingerprinting

Source: http://www.banking.com/aba/cover_0197.htm

Voice recognition can be used remotely by customers

where as other biometrics require specialized scanning

hardwareAccuracy declines when the audio quality is poor or background noise is

high or the customer has influenza

Implementation Examples

• Chase Manhattan Bank recently decided to use voice verification for customer identification following a review of several types of biometrics. However, voice identification has been implemented only for internal security, not customer facing at this stage

• Charles Schwab and Prudential Securities use voice identification to control access to secure areas and records to prevent internal fraud

Future Fraud Protection – Voice Verification

Leading US Bank – Voice Verification

43A.T. Kearney /SCB/IT Vision

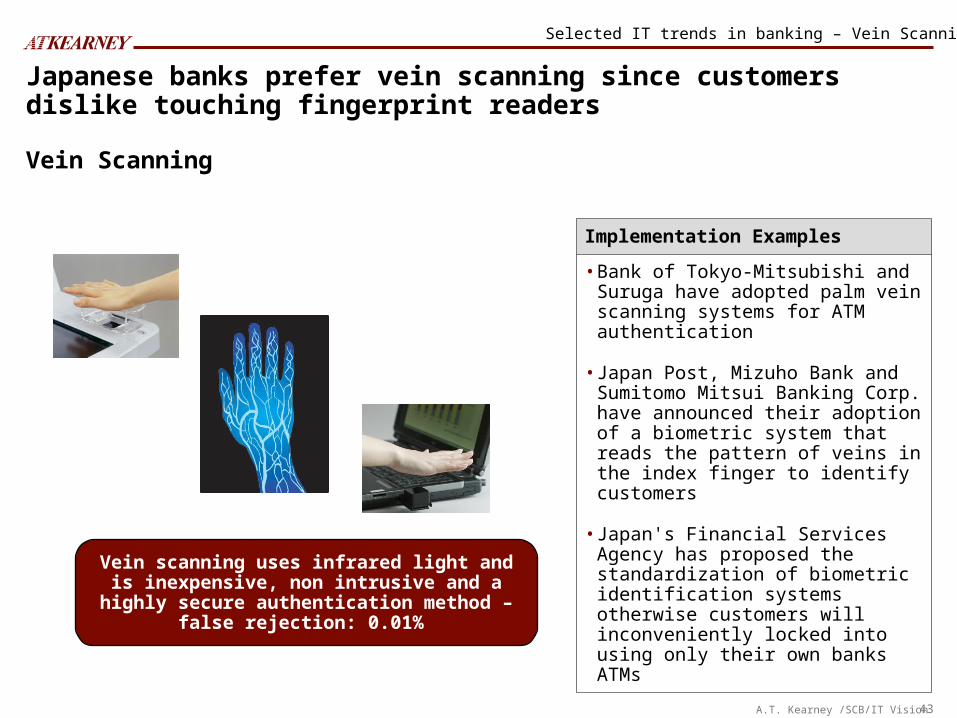

Japanese banks prefer vein scanning since customers dislike touching fingerprint readers

Implementation Examples

• Bank of Tokyo-Mitsubishi and Suruga have adopted palm vein scanning systems for ATM authentication

• Japan Post, Mizuho Bank and Sumitomo Mitsui Banking Corp. have announced their adoption of a biometric system that reads the pattern of veins in the index finger to identify customers

• Japan's Financial Services Agency has proposed the standardization of biometric identification systems otherwise customers will inconveniently locked into using only their own banks ATMs

Vein scanning uses infrared light and is inexpensive, non intrusive and a highly secure authentication method – false rejection: 0.01%

Selected IT trends in banking – Vein Scanning

Vein Scanning