May 11, 2018 Opening Happiness: Coke’s Strategy for ...

26

Vicky Xu May 11, 2018 Opening Happiness: Coke’s Strategy for Success in China and India Introducing Coca-Cola: One of the Most Iconic Brands in the World Coca-Cola has an estimated worth of $83.8 billion – more than Budweiser, Subway, PepsiCo, and KFC combined (O’Reilly, 2015). It is the most widely distributed product, and is sold in every country other than Cuba and North Korea (O’Reilly, 2015). Competitors marvel at the company’s global success, and researchers puzzle over the firm’s global strategies. This paper will analyze Coke’s journey back into the Chinese and Indian market. As soon as the Chinese and Indian markets opened up to the world, Coca-Cola worked hard to establish itself in both emerging markets. Coca-Cola’s re-entry into China and India highlight the complex relationship between firm structures and institutions in emerging economies. In India, under the Foreign Exchange Regulation Act, the country placed a cap on all foreign equity participation at 40 percent (Chakravarti, 2013). Unwilling to give up majority stake of its company, Coke removed itself from the country in 1977 (New York Times, 1977)., but was able to re-enter in 1993. In China on the other hand, Coke was forced out by revolutionary expropriation in 1949, and re-enters almost 30 years later in 1978 (Chong, 2013). Current literature often focus on market entry decisions with relation to profit maximization. Entering an emerging market is a costly and difficult endeavour for companies. Past literature posit several different theories for firm structure choice. In emerging markets, due to lack of market structures and high levels of risk, most theories suggest that firms will invest less resources, and opt for more flexibility. Firm entry decisions are also closely tied with the institutional structures of the host country. In developed nations, formal institutions are known to be the main barrier to entry.

Transcript of May 11, 2018 Opening Happiness: Coke’s Strategy for ...

Vicky Xu May 11, 2018

Opening Happiness: Coke’s Strategy for Success in China and India

Introducing Coca-Cola: One of the Most Iconic Brands in the World

Coca-Cola has an estimated worth of $83.8 billion – more than Budweiser, Subway,

PepsiCo, and KFC combined (O’Reilly, 2015). It is the most widely distributed product, and is

sold in every country other than Cuba and North Korea (O’Reilly, 2015). Competitors marvel at

the company’s global success, and researchers puzzle over the firm’s global strategies. This

paper will analyze Coke’s journey back into the Chinese and Indian market.

As soon as the Chinese and Indian markets opened up to the world, Coca-Cola worked

hard to establish itself in both emerging markets. Coca-Cola’s re-entry into China and India

highlight the complex relationship between firm structures and institutions in emerging

economies. In India, under the Foreign Exchange Regulation Act, the country placed a cap on

all foreign equity participation at 40 percent (Chakravarti, 2013). Unwilling to give up majority

stake of its company, Coke removed itself from the country in 1977 (New York Times, 1977).,

but was able to re-enter in 1993. In China on the other hand, Coke was forced out by

revolutionary expropriation in 1949, and re-enters almost 30 years later in 1978 (Chong, 2013).

Current literature often focus on market entry decisions with relation to profit

maximization. Entering an emerging market is a costly and difficult endeavour for companies.

Past literature posit several different theories for firm structure choice. In emerging markets, due

to lack of market structures and high levels of risk, most theories suggest that firms will invest

less resources, and opt for more flexibility.

Firm entry decisions are also closely tied with the institutional structures of the host

country. In developed nations, formal institutions are known to be the main barrier to entry.

However, as long as companies play by regulations and laws, entry into a market is not difficult.

This is not the case in emerging markets such as China and India. In 1978, China had almost no

formal institutions in place, and in 1993, through India’s formal institutions were established,

they were poorly enforced. In both countries, there was a strong reliance on informal institutions.

Coke’s ability to enter each market relied heavily on the unique way it structured its firm.

Coke’s case contradict theories that firms should be structured for economic efficiency, or to

conform to local institutions. Coke’s joint venture structure served as a framework to help

establish local relationships necessary to navigate the host country’s institutions. It is argued that

the most optimal firm structure for entering emerging markets is a joint venture since it allows

firms to access informal institutions necessary for success.

Literature Review

This section will review prior literature on general market entry strategies in emerging

economies, and current theories on how both formal and informal institutions impact such

decisions. Although there is a range of literature studying market entry strategies in emerging

economies, the specific case of Coca-Cola’s market entry in China and India highlight the

interconnections between firm structure choice and host country institutions. The choice of firm

structure for a large multinational corporation is shaped by a variety of factors. In this paper,

foreign market entry mode is defined as “an institutional arrangement that makes possible the

entry of firm’s products, technology, human skills, management, or other resources into a foreign

country” (Root, 1998).

Modes of Entry

Johnson and Tellis (2008) identify five major categories for modes of entry in terms of firm

structure:

● Export: A firm’s goods are produced in the home market and sold in the host nation.

● License and Franchise: A formal right offered to a firm located in a host nation to use a

home firm’s proprietary technology or other knowledge resources in return for payment.

● Alliance: Agreement between a firm in the home market with a firm located in a host

nation to share activities in the host nation.

● Joint Venture: Shared ownership of an entity located in a host nation by two partners

● Wholly Owned Subsidiary: Complete ownership of an entity located in a host nation by a

firm located in the home nation to manufacture or sell goods/services in the host nation

When determining the mode of entry, a trade-off will always be made. For most

companies, the choice is a careful balance between control, resource constraints, and the risks

involved. As current literature have shown, in order to assume control, companies must commit

greater resources, and take on more market and political risk (Root, 1998).

Figure 1: From Anstrop (2013) showing how that the choice of entry is a function of the trade-off between control, resource commitment, and a dimension of flexibility and risk

Beyond these general considerations, entering emerging economies provides a unique set

of challenges. Because of emerging economies’ rapid growth and reform, there is less economic

and political stability, and higher risks (Arnold and Quelch, 1998). These places often lack basic

infrastructure such as distribution systems and communication channels. There is also a lack of

regulatory discipline and legal frameworks, and business regulations may change frequently and

unpredictably (Arnold and Quelch, 1998). Even when there are formal laws and regulations, their

enforcement appears arbitrary and weak. When market supporting institutions are weak, it is

costly and risky for firms to sustain control and market presence (Meyer, 2009). Moreover, in

emerging economies, national and local governments are more influential. This often means

higher levels of bureaucracy with excessive requirements for licenses, approvals, and paperwork

which are both time consuming and costly for firms (Arnold and Quelch, 1998).

Two main theories exist regarding market entry: the transaction-cost theory and the

resource-based theory. These theories differ in how they view the effect of firm control in a host

nation. This includes control over intangibles such as brand equity and marketing data, and

tangibles such as a patent. The control of complementary resources such as access to local

distribution channels is also important. Arnstorp (2013) provides a good literature review of the

two theories:

Transaction Cost theory

Broadly, this theory posits that that the higher the resource commitment and desired

control of an entry mode, the higher the cost. More specifically, it states that firms select

governance structure that minimize the transaction costs of carrying out its activities. The most

effective entry mode according to the transaction cost theory would be low resource and

commitment such as exporting. Wholly owned subsidiaries and joint ventures would be

considered high-cost entry modes since they require high levels of resource commitment

(Arnstorp, 2013). More costly entry modes should only be used when firms can expect to

generate enough profit.

Resource Based Theory

This theory suggests that as control increases, a firm’s chance of success should increase

since the firm is able to manage their key resources more effectively (Gatignon and Anderson

1988). Firm resources can be categorized into financial resources, physical resources, human

resources and organizational capital (Barney, 1991). When entering new markets, firms need to

determine how to use their resources, and develop and acquire new resource advantages.

Due to high cost and risks in China and India, the transaction cost theory suggests high

flexibility and low control modes of entry for Coke such as exporting or licensing. Coke

however, chose to operate as a joint venture in both countries – a method that is both high cost,

and has low flexibility. Moreover, despite being costly, the joint venture structure does not

increase Coke’s control in either country. The resource based theory would also predict low

chances of success for Coke.

Institutional Theory Perspective on Foreign Market Entry Strategy

Recognizing that basic market theories cannot capture entry mode decisions completely,

the role of institutions are considered. Institutions can be defined as both formal and informal

structures that constrain the choices of individuals and organizations. Most literature would

define formal institutions to be political, legal, and economic systems that include constitutions,

laws, regulations, property rights etc., and informal institutions to be social norms and values of

individuals and include sanctions, taboos, customs, traditions etc. (North, 1991). Though formal

rules may change quickly, especially in emerging economies, informal rules are deeply grounded

in the society, and are harder to change (North, 1991). Arnstorp (2013) provides a good literature

review on the contending theories of the effects of institutions.

There are two major pieces of literature, each with different approaches to institutional

theory. North (1991) developed an economic framework, in which he suggests that firms are a

rational economic actor that adapts to a market’s institutional framework in order to maximize

economic efficiency. Scott (1995) on other hand, provides a sociological approach of the theory,

and posits that firms seek legitimacy by adapting to the institutional frameworks. Both suggest

that firm choices are not driven by the firm capabilities, but are rather determined by the

institutional environment the firm chooses to enter.

Most literature agree that the institutions of host country play an important role on firm

entry mode. Previous research suggests that the more developed the institutional environment of

the host country is, the more likely entrant firms are to choose a high-control entry mode such as

a wholly-owned subsidiary (Meyer, 2009). It is only with better structural support that firms are

willing to devote high levels of resources to a country, and dedicate more resources to the market

entry (Arnstorp, 2013). Likewise to market entry theory, Coke’s case also contradicts

institutional theory. Despite the lack of, and poor enforcement of institutional structures in both

China and India, Coca-Cola chose to commit high levels of resources and entered as a joint

venture. Coca-Cola’s unique entry approach into China and India suggests that current theories

on firm structure and entry mode may need to be revised when applied to larger emerging

economies such as China and India.

Methods

The story of how Coke managed to re-enter each market is pieced together though

secondary interviews with Coke executives, newspaper articles, and shareholder reports. Coke

re-entered the Chinese market in 1978, and re-entered the Indian market in 1993. Because of the

historical timeframe, SEC filing and investor data could not be obtained.

China and India provide an interesting backdrop to the case of Coca-Cola due to their

varying institutional structures. As emerging markets with very different political regimes and

market structures, it is surprising Coke entered both markets using the same firm structure. To

better interpret Coke’s position in each country, it is important to understand the general

institutional environments of India and China. The following section will provide a brief

overview of the institutions in both countries.

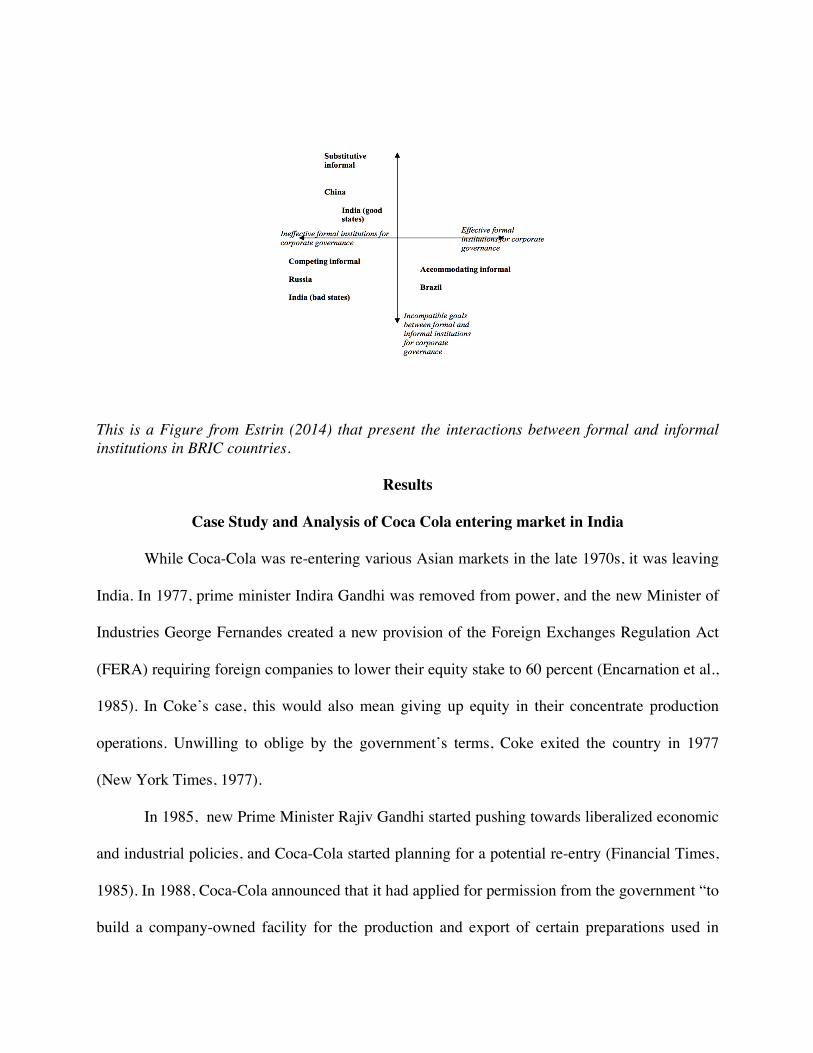

The literature review by Saul Estrin (2014) provides a good overview of the institutional

structures of China and India. It highlights that the informal institutions for corporate governance

compensate for ineffective formal corporate governance institutions.

Background on Chinese Institutions

Most literature would agree that China’s formal legal corporate governance structures

were ineffective as market-supporting institutions. There was weak rule of law, and weak

ownership protection for companies. However, informal institutions compensated for these

weaknesses in shareholder protection and rule of law. It was informal interactions between the

local state and private entrepreneurs that set the foundation for formal institutional reforms

(Estrin, 2014). During Chinese liberalization, the local state was heavily involved, and the

resulting property ownership contracts all involved the state. Generally, the reforms were not

conducive to a market economy. When Coke was returning in the mid-1970s, economic reform

was just beginning to occur, and there were nearly no formal institutions in place.

With the lack of formal institutions, informal institutions played a key role in supporting

private owners and the local states. Private assets could be assumed by the state almost

instantaneously; the government could revoke private companies’ right to exist and seize assets.

Therefore, informal institutions were used to establish firm legitimacy, and protect them from the

variable formal institutions. These methods included cultivating relations with government

officials, taking over ailing state-owned enterprises, donating services to the local community,

and concealing the private nature of ownership.

Background on Indian Institutions

India’s formal corporate governance institutions were very weak post-independence but

improved after the 1991 liberalization: capital markets were liberalized, and a takeover code

adopted in 1994 allowed for a basic market to develop. Steps were also taken to improve

corporate governance structures and disclosure practices. When Coke entered in 1993, India’s

market was significantly more developed compared to China. However, despite being

established, the formal regulations were often hard to navigate. Informal institutions were still

key to local and state governance.

The most important informal institutions that worked with formal governance institutions

were business groups. Past literature finds a positive correlation between the performance of

foreign and domestic corporations and affiliation with a business group. Literature shows that

informal institutions helped replace the largely ineffective formal legal framework.

In both China and India, despite the lack of or ineffective formal institutions, informal

mechanisms worked in their place. These substitutive informal institutions helped promote

positive investment outcomes both domestically in terms of entrepreneurship, and led to strong

flows of foreign direct investment (FDI).

This is a Figure from Estrin (2014) that present the interactions between formal and informal institutions in BRIC countries.

Results

Case Study and Analysis of Coca Cola entering market in India

While Coca-Cola was re-entering various Asian markets in the late 1970s, it was leaving

India. In 1977, prime minister Indira Gandhi was removed from power, and the new Minister of

Industries George Fernandes created a new provision of the Foreign Exchanges Regulation Act

(FERA) requiring foreign companies to lower their equity stake to 60 percent (Encarnation et al.,

1985). In Coke’s case, this would also mean giving up equity in their concentrate production

operations. Unwilling to oblige by the government’s terms, Coke exited the country in 1977

(New York Times, 1977).

In 1985, new Prime Minister Rajiv Gandhi started pushing towards liberalized economic

and industrial policies, and Coca-Cola started planning for a potential re-entry (Financial Times,

1985). In 1988, Coca-Cola announced that it had applied for permission from the government “to

build a company-owned facility for the production and export of certain preparations used in

making Coca-Cola concentrate” (Dow Jones Newswires, 1988). Coke planned to enter the

market as an exporter, and believed that their application was “in full compliance with the Indian

government regulations” (Dow Jones Newswires, 1988). In fact, Coke was so confident in being

approved that it had already agreed to appoint two major local companies as bottlers (New York

Times, 1989). In response to Coke’s confidence, Edward Shanks, president of another US soft

drink that set up franchise in India in 1987 warned to “take nothing for granted in India. This I

am sure will be a big political issue, regardless of how well Coke has its ducks lined up." (Wall

Street Journal, 1988).

Though the Commerce Ministry wanted to approve Coca-Cola’s proposal, other

politicians and large Indian companies saw the proposal as an abuse of India’s export processing

zone regulations. George Fernandes, now the Janata Party Leader, was still opposed to foreign

companies making soft drinks in India. The Parle company, the leader in the Indian soft drinks

market, thought it was a “bad decision” for the government to let Coke back in (Reuters, 1988).

To try and sway the Indian government, Coke promised to help India’s balance of payments with

more invested exports as “a gesture of good faith” (Financial Times, 1989). With conflicting

views, the decision about Coke’s re-entry was pushed back till after the upcoming election.

In March of 1990, with a newly elected government, Coca-Cola’s export-oriented plan

was rejected. The new prime minister Pratap Singh makes conflicting statements about India’s

stance on foreign investment (Wall Street Journal, 1990). Beyond the vocal objections by various

leaders in office, no formal information was provided by the government to explain the rejection

of the proposal (Reuters, 1990). Coca-Cola makes the statement that “India, by rejecting its

proposal, admits it doesn’t follow its own rules.” (Wall Street Journal, 1990).

By mid 1991, Coca-Cola had plans to make a fresh bid back into India. This time, it

planned to establish a joint venture with an Indian food processing company called Britannia

Industries (Reuters, 1991). The new offshore company would be named Britco Foods, and would

export snack foods, as well as produce Coca-Cola beverages for sale in India (Dow Jones, 1991).

By late 1991, Rajan Pillai, Chairman of Britannia Industries, had held informal talks with

ministers and officials, and said he was “confident in the proposal being approved” (Financial

Times, 1991). In the final agreement, 40% of the shares would be held by coke, and 60% held by

Pillai (Somal, 2015).

With the joint venture, Coca-Cola was controversially accused of “seeking entry into the

country by the back door” (Reuter, 1991). Coca-Cola was able to obtain an automatic license to

operate the joint venture by taking advantage of the Roa government’s policy of liberalization

(Somal, 2014). Many Indian soft drink producers accused Coca Cola of evading the rules by

creating a joint venture with a non-resident Indian (Reuters, 1991). They alleged that the joint

venture proposed products that did not fall under the high-priority category for automatic

approval under the liberalized procedures introduced (Reuters, 1992).

Unfortunately, this initial joint venture failed to take off as successfully as Coke had

hoped. Thus, Coke started looking at ways to partner with the Parle Group, who commanded 60

percent of India’s soft drink market. In late 1992, Coke was able to negotiate a strategic alliance

with Parle, acquiring their stable local brands, and gaining access to their nationwide bottling and

distribution infrastructure (Coca-Cola, 2012). Ramesh Chauhan, Parle's chairman said that under

the terms of the agreement, Coca-Cola was to form a joint venture with Parle, pay him a

consultancy fee of US $125,000 a year for five years, and give Parle the right of refusal to set up

bottling franchises (Reuters, 1994). On record, Coke said its business relationship with Parle was

''operational and functional." (Reuters, 1994). In October 1993, Coke made a grand entrance

back onto the Indian market (New York Times, 1993).

Case study and Analysis of Coca Cola entering market in China

In 1949, there was a wave of nationalization in China where foreign brands were all

removed; Coca-Cola factories were nationalized during this time. Chairman Mao also famously

deemed Coke to be a “bourgeois concoction” (Cendrowski, 2014). In the late 1970s, the Chinese

market was largely fragmented and unregulated. The soda industry in China was very provincial;

each province had its own local branded drink (Chong, 2013).

To Chinese communists, Coca-Cola was the symbol of Western capitalism and

consumerism, and for a long time, most officials in the Chinese government were against the

idea of Coca-Cola ever coming back to China (Cendrowski, 2014). China was a completely

different world back, as David Brooks, executive vice-president of Coca-Cola Greater China

describes, “It’s hard to conceive today how closed off China really was—it was like North Korea

today” (Cendrowski, 2014). However, when Deng Xiaoping came into power after Mao’s death

in 1976, he suggested a new open-door policy (Weisert, 2001). There was now possibility for

Coke to re-enter the Chinese market.

At this time, President Carter’s administration was also trying to establish diplomatic

relations with China (Boda, 2016). The role the American administration played in Coca-Cola’s

re-entry into China is often left out of literature. In the United States, Coca-Cola had an intimate

relationship with the Carter administrations. During Jimmy Carter’s presidential campaign, Coke

allowed Carter to use their aircrafts, and hosted fundraising luncheons to raise money for

Carter’s campaign (Boda, 2016). Once Carter become President, Pepsi was removed from the

White House, and Carter’s administration appointed Paul Austin, president of Coca-Cola as a

board member of the National Council for US-China Trade (Donovan, 2014).

The re-entry into China was carefully planned. In 1973, US companies were not allowed

to conduct business directly with Chinese companies. Thus, Coca-Cola established a new

company called Benetrade in Hong Kong to begin scouting the Chinese market (Nan, 2014). In

1974 at the Chinese Export Commodities Fair, Coca-Cola, under Benetrade, first approached the

China Nationals Cereals, Oil and Foodstuffs Corp (COFCO), a state-owned enterprise that was

the sole agricultural products importer and exporter operating under the direct control of the

central government (Nan, 2014).

Soon after, Austin visited China in 1975 to talk to government officials. On the trip, he

noted that “the Chinese people are sociable people,” and that “they like to have soft drinks.” He

also highlights that his “attitude was not pushy,” and that he chose to work with the government

by emphasizing that “the way to signal [China’s economic opening] to the world at large was to

bring in Coca-Cola - as the symbol of US foreign trade.” (Chong, 2013).

Carter’s relationship to Coca-Cola made the brand appear even more American in the

eyes of the Chinese. Many speculate that Carter’s administration may have leaked news to Coca-

Cola executives of the upcoming agreement between the US and China. Regardless, Coke had

already made plans to enter the Chinese market (Boda, 2016).

Peter Lee, was called by up Austin in the summer of 1977. At that time, Lee worked as a

chemist, and was heading to Coke’s base in Hong Kong. Austin asked Lee to be “an eye for the

company and see where China is going” (Cendrowski, 2014). Once in Hong Kong, Lee began to

communicate more with the China National Cereals, Oils, and Foodstuffs Corporation (COFCO).

As Lee recalls, “I sent many telexes to different departments over six or seven months. I never

received a response. Then suddenly, in December 1978, I received a response. It said, “We

understand what your company could offer. We welcome you to come to Beijing for

negotiations” (Cendrowski, 2014).

Lee arrived in Beijing to attend a meeting with officials. Present at the meeting were

three people from COFCO. During the meeting, Lee sold Coke as a product for tourists: “I

understand China now has an open-door policy—it’s open to tourists from all over world. We

have a product we believe most tourists would love” (Chong, 2013). Almost immediately after

on December 13, 1978, a deal was signed giving Coke the exclusive right to sell non-Chinese

made Coke in China. The contract allowed both sides to set up bottling plants and sell Coke in

the main cities and at scenic spots in China. However, only tourists visiting major cities were

allowed to buy Coke (Donovan, 2014). Before the plants were operational, COFCO was

responsible for consignment sale of the drink. Coca-Cola would provide a production line for the

bottling plant, while its Chinese counterpart would provide the buildings (Chong, 2013).

In the background, Dick Holbrook, the assistant US Secretary of State for the East Asian

and Pacific Affairs worked on establishing diplomatic ties with Chinese officials. Once Coke

signed the agreement, they “got a request from Carter not to announce until he had made an

announcement [about normalized diplomatic relations]” (Cendrowski, 2014). Two days after the

Coke deal on Dec. 15, 1978, the US government reached an agreement with China to normalize

diplomatic relations by opening embassies in each other’s countries (Boda, 2016).

Discussion

Analysis of entry methods in China and India

Coke re-entered China in 1978, and re-entered India in 1993. Despite the different

political regimes, market structures, and institutions, there are surprising similarities in Coke’s

market entry approach into each country. Arguably, the joint venture mode of re-entry allowed

Coke to integrate itself smoothly into each country’s informal institutions. The shared ownership

structure of a joint venture provided the opportunity for Coke to engage with local partners and

effectively acclimate itself to the local business environment. The following discussion will

analyze Coke’s firm structure choice against the back drop of each country’s political regimes,

market structures, and institutions.

Political Structures

China and India’s individual political structures played a large role in shaping Coke’s

decisions, and ability to enter each country. The Chinese state was very localized, and local

governments acted as key decision makers in communities. Despite localized power, the one

party system still gave the state ultimate control. Even with strong local relationships and a

strong local presence, private companies could still be assumed by the state instantaneously.

However, with one political party, Coke’s communication efforts were straightforward.

When initiating communication in China, Coke recognized that there was one major state-owned

enterprise to target: COFCO. This single company had complete power in food sales and

production in China. The meeting Lee had with Chinese officials when negotiating Coke’s

potential entry consisted of three COFCO members. By establishing connections with this state-

owned enterprise early, Coke started building its presence within government circles early.

With a one-party system, there was no opposition to Coke’s market entry beyond the

single government’s concerns about Western influence. The lack of opposition made

negotiations easier between Coke and the government. The government only had to satisfy itself,

and Coke only had to recognize what the government wanted. Thus, Coke crafted an image that

the Chinese government could collectively support. In Austin and Lee’s meetings, they

persuaded officials that “the way to signal [China’s economic opening] to the world at large was

to bring in Coca-Cola - as the symbol of US foreign trade” (Chong, 2013). Realizing that China

wanted to enter the global market, Coke sold itself as the perfect opportunity for China to

demonstrate its open door policy.

In India’s democracy on the other hand, the presence of different political parties meant

varying opinions on everything. The various political opinions on foreign direct investment made

Coke’s re-entry process difficult. There was constant change in India’s political stance. Each

election brought a different opinion into power. When George Fernandes’ party came into power

in 1977, there was an emphasis on supporting indigenous industries and thus foreign equity

participation was capped at 40 percent. Unwilling to give up decision-making authority, Coke

exits India. The next election brought more liberal economic policies, and Coke thought they

would be able to re-enter. However, Coke’s entry proposal fell during the timeframe of a new

election and was rejected by the next party in power.

When a country does not have a unified political stance, it is hard for foreign companies

to craft a marketable brand to the government. Unlike in China where Coke targeted the

appropriate state-owned enterprise to access key decision-makers, it was harder for Coke to

directly communicate with the decision-makers of India. Coke had to operate as an outsider.

When Coke drafted its first proposal, it made it “sweeter,” by adding additional incentives it

thought the government wanted. Coke believed its first proposal would be approved, showing the

company’s lack of information about the decision-making process. The Indian government’s

lack of transparency and institutional integrity made working with them difficult. When Coke

finally re-entered, it worked around the “formal” rules, and “entered through the back door.”

Instead of getting the government onboard, Coke worked with other businesses such as Parle,

and local businessman such as Pillai of Britannia Industries and Chauhan of Parle. These local

business partners were more integrated with local institutions and had more influence and access

to people in power.

In both countries, a joint venture approach allowed Coke to initiate communications

within the political structures. As a shared ownership agreement, a joint venture provided the

foundation for Coke to work intimately with government officials and local businessman. In both

cases, the local business partners were well established in the existing market environment, and

were crucial in helping Coke build relationships within the local political structures. The

partnerships allowed Coke to interact with key government decisions-makers through informal

networks. These informal interactions were an essential step in negotiating formal agreements.

Markets and Institutions

When Coke entered China in the mid-1970s, the market was fragmented and localized; it

was before the establishment of property rights, joint venture laws, and special economic zones.

However, the lack of structure and formal institutions is observed to have helped Coke enter

China’s market more effectively.

First off, there were no dominant competitors due to the fragmented market. Though

different regions had its own soft drink brand, there were no objections to Coke’s entry from

local drink manufacturers. The most likely reason for the lack of objection is that local

manufacturers had no idea about Coke’s potential re-entry into the market. Coke did not

communicate with local states, and worked directly with national officials to obtain legitimacy

and support at the national level. Backed by the national government, it would have been

difficult for local states to object against Coke’s re-entry.

Moreover, the Carter narrative is often left out of Coke’s entry back into China. Coke

managed to establish itself in China before diplomatic relations and market reforms, and its

success can be tied to Carter’s relationship with the Chinese government. Carter’s administration

appointed Paul Austin as a board member of the National Council for US-China Trade giving

Austin direct access to key decision makers of China’s market. Without formalized laws,

informal negotiations were the only option for market entry. Access to important people was the

most important step in entering the Chinese market.

In India, Coke’s exit in 1977 allowed Indian soft drink companies to grow rapidly.

Instead of a fragmented soft drink industry, large companies dominated. Parle, as the largest

stakeholder controlled 60 percent of the market. The chairman of Parle, Chauhan, also

controlled the All-India Soft Drinks Manufacturers Association, a major business group that had

many connections within the Indian government (Chakravarti, 2013). Even with formal

institutions in place, business groups held large amounts of power in governance. Both business

groups and opposition parties were very vocal in their objections against Coke’s re-entry.

Though India had established formal institutions such property rights, joint venture laws,

and business associations, these structures were confusing to navigate. For example, through

Coke’s first proposal appeared to follow all necessary guidelines, it was rejected. Decisions

made by government bureaucrats on permitting processes were elaborate, yet arbitrary, and the

final decisions often conflicted with formal rules. There was also strong influence from powerful

lobbyists such as the All-India Soft Drinks Manufacturers Association. Business groups appeared

to have significant leverage in government decisions. Ultimately when Coke re-entered, it relied

heavily on its joint venture partner Pillai in terms of using his local networks and connections.

Pillai held “informal negotiations” with government officials, directly demonstrating the impact

informal networks have on final decisions.

The crucial role of informal institutions is highlighted in Coke’s re-entry into both

countries. In China, informal institutions were the only access to the market, while in India,

informal institutions were necessary to overcome the arbitrary and confusing bureaucratic

systems.

Firm Structure

When re-entering the Chinese market, Coke formed the company Bertnade in Hong Kong

to work around policies preventing foreign companies from directly interacting with Chinese

firms. However, despite China’s lack of market structure and high risk environment, Coke did

not pursue a low resource mode of entry such as exporting, as the transaction cost theory would

suggest. Instead, Coke dedicated significant resources into China. Contrary to the resource based

theory, although Coke committed more resources, it did not hold much control over its

operations in China. The Chinese government commanded a lot of power against Coke. The

initial agreement placed heavy restrictions on Coke’s distribution methods and overall market.

The government also held the power to shut down Coke operations instantaneously.

Coke’s case in China challenges the institutional theory that firms are only likely to

employ high control entry modes in more developed institutional environments. However,

Coke’s entry strategy had merit. Because of the long exile in China, rather than re-entering the

market, Coke was essentially breaking into new territory. Coke needed to establish its

legitimacy to the Chinese government as a company who embodied China’s new foreign

policies. Legitimacy was more important than economic efficiency in China’s case. Resource

investment was necessary to re-establish itself as a brand, and compliance with the government

to was necessary to enter the country at all. Without high levels of investment, Coke would have

been unable to establish strong relationships with the Chinese government. It was only through

the joint venture with the state-owned enterprise COFCO that Coke could directly collaborate

with the government. This significantly mitigated risk of unforeseeable government actions, and

set the foundational relationship for formal business negotiations.

When Coke tried to re-enter the Indian market, it drafted a proposal to operate as an

export company. This move would validate the transaction cost theory; it made sense for Coke to

want a flexible, low cost firm structure such as exporting. In an emerging market, to minimize

risk and maximize profit, a low cost and high flexibility entry mode is ideal. However, the

proposal failed, and Coke is forced to consider other entry mode options. This case is a blatant

example of how institutions can forcibly shape a firm’s entry decision.

Transaction cost theory is right in predicting an export market as Coke’s most desired

form of entry, but India’s case shows that institutions play the more significant role in dictating

what a company does. Coke had no leverage within the Indian government. Recognizing it was

necessary to work within the system, Coke formed a joint venture with Britannico. After the joint

venture was established, the chairman of Britannico held informal talks with ministers and

officials, and was “confident” that Coke’s new proposal would be approved (FT, Housego,

1991). Despite holding the smaller market share in this joint venture, Britannica did not have

control over Coke’s concentrate production operations.

Through the joint venture in India, Coke leaders formed valuable relationships with local

business partners and accessed key players in the government system. Once Coke entered the

market, it acquired Parle’s brands in the country. By working with business partners already

familiar with the local industry, Coke obtained the networks necessary to communicate with

distribution markets and policy makers.

Though the cases challenge the conclusions of market entry theories, Coke’s success

highlight the merits, and even necessity of a joint venture entry mode. It is observed that the way

a firm structures itself cannot be for economic efficiencies. In the case of Coke in India,

institutions prevented the firm from operating in the most optimal way. In China’s case,

institutions are not strong enough to support entry modes that may have been the most optimal.

However, entry mode decisions should also not be to conform to the institutional frameworks of

a host country. The firm must still consider ways to take advantage of the local market and find

opportunities to maximize profit when possible. The reason for entering a new market is

ultimately to increase firm profitability in the long run.

Thus, it is observed that the structure a firm chooses is an opportunity to form necessary

relationships within the institutional networks of a country. These relationships are necessary for

accessing local information and leveraging the firm’s resources and strengths in local markets.

Coke’s case demonstrates that a joint venture is the optimal structural choice in emerging

markets. A joint venture connects the firm with the informal institutions of a host nation. The

joint ownership structure provides the unique and necessary structure that allows outside firms to

collaborate effectively with local players well acquainted with the local environment. The

relationships established through the formal partnership will mitigate risks in unstable political

and economic markets, and help firms transition more smoothly into the host nation.

Strengths and Limitations of the Study

This case study focused on the decision making process of Coca-Cola into China and

India. Most literature examine how the company evolves once it enters a market, and there is

little research on the journey of the initial entry into markets. The cases highlight the complex

systems firms need to navigate in order to enter emerging economies. Before agreements are

negotiated, years of behind the scenes work had to occur. The cases also challenge the

conclusions of institutional and market entry theories. This suggests that current theories may

need to be revised when applied to larger emerging economies such as China and India.

However, it is noted that the time frame of Coke’s entry decisions was a large variable in

the decision making process. When Coke was re-entering China in the late 1970s, it was leaving

India – the resources Coke had available during each period for global investments were very

different. Moreover, the global strategy of the firm could have changed over time. Perhaps when

entering China, Coke had a re-entry strategy of simply trying to enter new markets, whereas by

the time it was trying to re-enter India, it took a more profit maximizing position.

In the future, more research can be done to analyze the direct effects of the US

government’s diplomatic relationships on US firm entry strategies. More research can observe

how Coke and other US-based corporations choose to define themselves in foreign countries

depending on the diplomatic ties. A more detailed analysis of the US government’s relationship

with China and India during the time of Coke’s re-entry into the respective countries can help

define how governments affect corporation expansion efforts.

Conclusion

Coca-Cola’s re-entry process in China and India demonstrate that a joint venture is an

optimal firm structure choice when entering emerging markets. A joint venture provided the

framework for Coca-Cola to interact closely with local informal institutions. Through informal

institutional relationships, Coke obtained legitimacy and was able to mitigate risks in China and

India. Through its joint ventures, Coke obtained political access, which led to political support

and cooperation in both countries. Informal relationships between the host country companies

and government officials are more important than any formal legal processes in place. Informal

connections allowed Coke to access people in positions of power and demonstrate legitimacy to

people in governance. In regions like China with almost no formal institutions, informal

negotiations were the only way for firms to access the market. In regions like India with weak

formal institutions, informal institutions were important to building the right relationships for

leverage in the decision-making process. The structure Coke chose allowed it to form necessary

relationships within the institutional networks of a country. These relationships were critical for

accessing local information and leveraging Coke’s strengths in the local markets.

Works Cited

*The newspaper articles I used for India’s case study are not cited here. I used HBS’s computers when finding them, and for some reason I cannot access the Factiva database from my personal college account. I have the links to all the articles, and can work to site them at a later time!

Arnold, D., & Quelch, J. (1998, October 15). New Strategies in Emerging Markets. MIT Sloan Management Review.

Arnstorp, H. (2013). Foreign market entry strategies in developed and emerging economies. Norwegian University of Science and Technology. Barney, J. (1991). Firm Resources and Sustained Competitive Advantage. Texas A & M University, Journal of Management. Boda, T. (2016, October 31). The Cola Wars: The Creation of the Soda Giants: President Carter: Coca-Cola's Man. Retrieved from http://scalar.usc.edu/works/colawars/the-coke-presidencies-carter-and-reagan Cendrowski, S. (2014, September 12). Opening happiness: An oral history of Coca-Cola in China. Retrieved from http://fortune.com/2014/09/11/opening-happiness-an-oral-history-of-coca-cola-in-china/ Chakravarti, S. (2013, October 15). Coke back with Britannia. Retrieved from https://www.indiatoday.in/magazine/economy/story/19911115-coke-back-with-britannia-815058-1991-11-15 Chong, L.B. (2013). Managing a Chinese Partner: insights from global companies. Basingstoke, Hampshire : Palgrave Macmillan. Coca-Cola, India’s Parle Engage in War of Words. (1994). Reuters. Donovan, T. (2014). Fizz: How soda shook up the world. Chicago, IL: Chicago Review Press. Encamation, D. Foreign Ownership: When Hosts Change the Rules. The Harvard Business Review (1985). Encarnation, D. (1985). Foreign ownership: When hosts change the rules. The International Executive, 28(1), 10-11. https://hbr.org/1985/09/foreign-ownership-when-hosts-change-the-rules Estrin, S. (2014). A survey on institutions and new firm entry: How and why do entry rates differ in emerging markets? Economic Systems,34(3), 289-308. doi:10.1016/j.ecosys.2010.01.003

Gatignon, H. & Anderson, E. (1988), The Multinational Corporation's Degree of Control over Foreign Subsidiaries: An Empirical Test of a Transaction Cost Explanation, Journal of Law, Economics, and Organization, 4, issue 2, p. 305-36. Johnson, J., & Tellis, G. J. (2008). Drivers of Success for Market Entry into China and India. Journal of Marketing, 72(3), 1-13. doi:10.1509/jmkg.72.3.1 Meyer, K. E., Wright, M., & Pruthi, S. (2009). Managing knowledge in foreign entry strategies: A resource-based analysis. Strategic Management Journal, 30(5), 557-574. doi:10.1002/smj.756 Mok, Vincent, Dai, Xiudian and Yeung, Godfrey (2002) An internalization approach to joint ventures: the case of Coca-Cola in China. Asia Pacific Business Review Nan, H. (2014, November 24). Celebrating 35 Years of Coca-Cola in China. Retrieved from http://www.coca-colacompany.com/stories/celebrating-35-years-of-coca-cola-in-china North, D. C. (1991). Institutions, Institutional Change and Economic Performance. The Economic Journal, 101(409), 1587. doi:10.2307/2234910 O'Reilly, L. (2015, September 25). 15 mind-blowing facts about Coca-Cola. Retrieved from http://www.businessinsider.com/facts-about-coca-cola-2015-9 Panchal, S. (2014, August 14). Economic Milestone: Exit of the MNCs (1977). Retrieved from http://www.forbesindia.com/article/independence-day-special/economic-milestone-exit-of-the-mncs-(1977)/38431/1 Rasheed, H. S. (2005), Foreign Entry Mode and Performance: The Moderating Effects of Environment. Journal of Small Business Management, 43: 41-54. doi:10.1111/j.1540-627X.2004.00124.x Root, F. R. (1998). Entry strategies for international markets. Lexington, Mass.: Heath. Scott, R. (1995). Institutions and Organizations: Ideas, Interests, and Identities. Standford University. Shailashree, V., Mlemba, E.. (2016). Impact of National Culture on Organisational Culture. International Journal of Scientific Research and Modern Education. Somal, B. (2015). India on Sale Part 2: India Plundered.

Weisert, D. (2001). Coca-Cola in China: Quenching the thirst of a billion. The China Business Review.