Non RC-526 Dismissal (AAO JUL022014 01-B7203) more money issues et al...

(b)(6)

U.S. Citizenship and Immigration Services

MATTER OF A-J-C-

Non-Precedent Decision of the Administrative Appeals Office

DATE: AUG. 22, 2016

APPEAL OF IMMIGRANT INVESTOR PROGRAM OFFICE DECISION

PETITION: FORM I-526, IMMIGRANT PETITION BY ALIEN ENTREPRENEUR

The Petitioner seeks classification as an immigrant investor. S~e Immigration and Nationality Act (the Act) section 203(b)(5), 8 U.S.C. § 1153(b)(5). This fifth preference (EB 5) classification makes immigrant visas available to foreign nationals who invest the requisite amount of qualifying capital in a new commercial enterprise that will benefit the United States economy and create at least 10 full-time positions for qualifYing employees.

The Chief, Immigrant Investor Program Office (IPO), denied the petition. The Chief concluded the Petitioner did not establish that she placed at least $500,000 at risk, 1 met the job creation requirements, or would manage doing business as

the a new commercial enterprise (theNCE).

The matter is now before us on appeal. The Petitioner does not submit additional evidence or an appellate brief to support her appeal. In a statement, she maintains that the Chief erred in his findings and that she is eligible for the immigrant investor classification. She does not, however, offer any arguments or point to any evidence to support her position that the Chiefs findings are erroneous.

Upon review, we will summarily dismiss the appeal because the Petitioner has not identified specifically any erroneous conclusion of law or statement of fact for the appeal. See 8 C.F.R. § 103.3(a)(l)(v).

I. LAW

The regulation at 8 C.F.R. § 103.3(a)(1)(v) provides, in pertinent part, we "shall summarily dismiss any appeal when the party concerned fails to identify specifically any erroneous conclusion of law or statement of fact for the appeal." Under the regulation, a summary dismissal is appropriate if the Petitioner makes general assertions that do not specifically identify an error in the Chiefs decision.

1 In this case, the required amount of capital is $500,000 because the investment is in a targeted employment area (TEA). The regulation at 8 C.F.R. § 204.6(t) explains that the minimum investment amount is generally S 1 ,000,000, but may be adjusted down to $500,000 if the investment is in a TEA.

Matter of A-J-C-

The Petitioner must state any arguments she wishes ,us to consider on appeal, even if she had previously raised the arguments before the Chief. See 8 C.F.R. § I03.3(a)(l)(v).

II. ANALYSIS

The Petitioner's Form I-290B, Notice of Appeal or Motion, does not identify specifically any erroneous conclusion of law or statement of fact for her appeal. In part 3 of the form, "Information About the Appeal or Motion," the Petitioner, through counsel, checked the box that reads: "I am filing an appeal to the AAO. My brief and/or additional evidence will be submitted to the AAO within 30 calendar days of filing the appeal." Along with the Form I-290B, the Petitioner submits the following statement: -,

The Appellant . . . together with counsel hereby submit this appeal challenging the decision of CIS [U.S. Citizenship and Immigration Services] with regard to the Appellant's Form 1-526, which was denied on January 29, 2016. It will be alleged and argued that there [sic] a number of errors in the decision: Appellant did show that she was actively involved in the process of investing the required amount of Capital ($500,000) and that the Capital was obtained by lawful means; that the investment will spur the creation of at least ten full-time jobs; and that the Appellant is and will be actively involved in the management of the new commercial enterprise.

We will be submitting a brief, with more complete legal arguments and relevant citations, within 30 days oftoday's date.

As of today's date, however, five months after the Petitioner's March 2016 appeal, we have not received a brief or additional evidence.

In his decision, the Chief evaluated the Petitioner's evidence, concluding that she did not demonstrate, by a preponderance of the evidence, her eligibility for the classification. Specifically, she did not show that: (I) at the time she submitted the petition, she had invested or was actively in the process of investing at least $500,000 of her funds in theNCE; (2) she met or would meet the job creation requirements; and (3) she had engaged or would be engaged in the management of theNCE. See 8 C.F .R. § 204.60). On appeal, the Petitioner has not identified specific materials in the record illustrating her eligibility, or provided any legal support to show that the Chiefs findings are erroneous. As she has not specifically identified any flawed conclusion of law or statement of fact for the appeal, we will summarily dismiss the appeal, pursuant to the regulation at 8 C.F.R. § 103.3(a)(l)(v).

ORDER: The appeal is summarily dismissed pursuant to 8 C.F.R. § I 03.3(a)(l)(v).

Cite as Matter of A-J-C-, ID# I2073 (AAO Aug. 22, 2016)

2

(b)(6)

U.S. Citizenship and Immigration Services

MATTER OF A-J-C-

Non-Precedent Decision of the Administrative Appeals Office

DATE: FEB. 1, 2017

MOTION ON ADMINISTRATIVE APPEALS OFFICE DECISION

PETITION: FORM I-526, IMMIGRANT PETITION FOR ALIEN ENTREPRENEUR

The Petitioner seeks classification as an immigrant investor based on an investment in a new commercial enterprise (theNCE). TheNCE owns and operates retail stores and

is engaged in the leasing and sale of electronics and furniture under franchise agreements with See Immigration and Nationality Act (the Act) section

203(b)(5), 8 U.S.C. § 1153(b)(5). This fifth preference employment based classification (EB-5) makes immigrant visas available to foreign nationals who invest the requisite amount of qualifying capital in a new commercial enterprise that will benefit the United States economy and create at least 10 full-time positions for qualifying employees.

The Chief, Immigrant Investor Program Office (IPO), denied the petition. The Chief concluded that the Petitioner did not invest, and was not in the process of actively investing, in the NCE. He also found that she did not demonstrate that the NCE has or will create at least 10 jobs for qualifying employees as a result of her investment, or that she has or will be engaged in the management of the NCE. We summarily dismissed her appeal, determining that she did not specifically identify any erroneous conclusion of law or statement of fact for the appeal.

The matter now before us is a motion to reconsider and motion to reopen. In support of her motions, the Petitioner submits additional evidence, and maintains that she has shown her eligibility for the immigrant investor classification.

Upon review,. we will deny the motions.

I. LAW

A foreign national may be classified as an immigrant investor if he or she invests the requisite amount of qualifying capital in a new commercial enterprise. The commercial enterprise can be any lawful business that engages in for-profit activities. The foreign national must show that his or her investment will benefit the United States economy and create at least I 0 full-time jobs for qualifying employees. This job creation should generally occur within 2 years of the foreign national's admission to the United States as a conditional permanent resident. Specifically, section 203(b )(5)(A) of the Act, as amended, provides that a foreign national may seek to enter the United States for the purpose of engaging in a new commercial enterprise:

Matter of A-J-C-

(i) in which such alien has invested (after the date of the enactment of the Immigration Act of 1990) or, is actively in the process of investing, capital in an amount not less than the amount specified in subparagraph (C), and

(ii) which will benefit the United States economy and create full time employment for not fewer than 10 United States citizens or aliens lawfully admitted for permanent residence or other immigrants lawfully authorized to be employed in the United States (other than the immigrant and the immigrant's spouse, sons, or daughters).

The implementing regulation at 8 C.F.R. § 204.6(e) includes the following definitions:

Capital means cash, equipment, inventory, other tangible property, cash equivalents, and indebtedness secured by assets owned by the alien entrepreneur, provided that the alien entrepreneur is personally and primarily liable and that the assets of the new commercial enterprise upon which the petition is based are not used to secure any of the indebtedness.

Employee means an individual who provides services or labor for the new commercial enterprise and who receives wages or other remuneration directly from the new commercial enterprise. . . . This definition shall not include independent contractors.

Invest means to contribute capital. A contribution of capital in exchange for a note, bond, convertible debt, obligation, or any other debt arrangement between the alien entrepreneur and the new commercial enterprise does not constitute a contribution of capital for the purposes of this part.

The regulation at 8 C.F.R. § 204.6G)(4)(i)(A) lists the evidence required to show the necessary job creation as follows: photocopies of relevant tax records, Forms I-9 (Employment Eligibility Verification), or other similar material for 10 full-time positions for qualifying employees. Alternatively, if the new commercial enterprise has not yet created the requisite 10 jobs, a petitioner must offer a comprehensive business plan demonstrating the new commercial enterprise's need for not fewer than 10 full-time employees. 8 C.F.R. § 204.6(j)(4)(i)(B). A comprehensive business plan as contemplated by the regulations should contain, at a minimum, a description of the business, its products and/or services, and its objectives. Matter of Ho, 22 I&N Dec. 206, 210 (Assoc. Comrn'r 1998). Elaborating on the contents of an acceptable business plan, Ho, 22 I&N Dec. at 213 states that the plan should contain a market analysis, the pertinent processes and suppliers, marketing strategy, organizational structure, personnel's experience, staffing requirements, timetable for hiring, job descriptions, and projections of sales, costs, and income. The decision concludes: "Most importantly, the business plan must be credible." !d.

2

(b)(6)

Matter of A-J-C-

Finally, a motion to reconsider a decision must offer the reasons for reconsideration and be supported by any pertinent precedent decisions to establish that the earlier decision was based on an incorrect application of law or USCIS policy. 8 C.F.R. § 1 03.5(a)(3). A motion to reconsider is based on the existing record and the petitioner may not introduce new facts or new evidence relative to her arguments. A motion to reopen must state the new facts to be provided and to be supported by affidavits or other documentation. 8 C.F .R. § 103 .5( a)(2). However, any new facts must relate to eligibility at the time the petitioner filed the petition. See 8 C.F .R. § 103 .2(b )(1 ), ( 12); see also Matter of Katigbak, 14 I&N Dec. 45, 49 (Reg'l Comm'r 1971). A motion to reopen seeks a new hearing based on new materials, as opposed to a motion to reconsider which contests the correctness of the original decision based on the previous factual record. Compare 8 C.F .R. § 103 .5( a)(2) and 8 C.F.R. § 103.5(a)(3).

II. ANALYSIS

We summarily dismissed the Petitioner's appeal as she did not submit additional documentation, offer any arguments, or point to any evidence in the petition to support her position that we erred in in dismissing her appeal of the Chief's decision. See 8 C.F.R. § 103.3(a)(l)(v). Similarly, on motion the Petitioner has not described any reasons or submitted evidence to show that we based our previous decision on an incorrect application of law or USCIS policy. We will therefore deny her motion to reconsider. See 8 C.F.R. § 103.5(a)(3).

On motion, the Petitioner submits additional evidence, and maintains that (1) she has invested at least $500,000 in theNCE, 1 (2) her investment in theNCE has and will create jobs for 10 qualifying employees, and lastly, (3) that she is engaged in the management of theNCE. We agree that the Petitioner has demonstrated that she will be engaged in the management of the NCE through her position as the quality control manager for the based upon her job title, position description, and the staffing plan for the store provided on motion. See 8 C.F.R. § 204.60)(5). However, the record, including materials that she offers on motion, does not establish that she has invested or is actively in the process of investing her own capital in theNCE, or that the requisite 10 jobs have or will be created as a result of her capital investment. We will thus deny her motion to reopen.

III. CAPITAL INVESTMENT AT RISK

The Chief denied the petition in part because the Petitioner's prospective investment arrangement with the' NCE did not appear to be a present commitment of funds. While the Petitioner had transferred $114,000 to the NCE, the transfer of the majority of her investment capital was predicated on the sale of real estate located in India. The record before the Chief did not demonstrate by a preponderance of evidence that the real estate could be sold or that the sale of the real estate would produce sufficient funding to the Petitioner to invest the requisite amount of

1 As the NCE is located in a targeted employment area, the required amount of capital is downwardly adjusted from

$1,000,000 to $500,000. See 8 C.F.R. § 204.6(e).

3

(b)(6)

Matter of A-J-C-

capital. The regulation at 8 C.F.R. § 204.6(j)(2) provides that a mere intent to invest, or prospective investment arrangements entailing no present commitment, will not suffice to show that the petitioner is actively in the process of investing. The Petitioner must show actual commitment of the required amount of capital.

New material provided on motion shows that the Petitioner sold real estate in India in June 2016 and transferred $249,980 to the NCE in October 2016. Additionally the Petitioner made other monetary transfers to theNCE in 2016 in the amount of $15,000, $6000, and $7000, respectively, bringing the total amount to $441,980 in transferred funds to the NCE. The petitioner provided a statement and evidence that sufficient funds are in the Petitioner's bank account in India and will be available for transfer in 2017 in order to complete the transfer of at least $500,000 in total to the NCE. The Petitioner indicates that the delay in the transfer of the funds is due to yearly limitations on currency transfers abroad that are imposed by India. While this new evidence demonstrates that the Petitioner may currently possess sufficient funds to be in the process of making the requisite capital investment in the NCE, we will explain why the record does not show that she was actively in the process of investing capital at the time of filing of the petition as required by section 203(b)(5)(A) of the Act.

First, the funds that the Petitioner has provided to the NCE to date have been consistently characterized as loans to the NCE in its federal tax returns and other documentation submitted in support ofthe petition. For example, theNCE's IRS Form 1065, U.S. Return of Partnership Income, and California Form 568, Limited Liability Company Return of Income, for 2013 and 2014 each show a note payable to the Petitioner in the amount of $114,000 in Schedule L. Likewise, a February 2013 resolution by the majority members of the NCE indicates that its officers signed a promissory note for the benefit of the Petitioner in the amount of $114,000 in order to finance the acquisition of a new store. The regulation at 8 C.F.R. § 204.6(j)(2) states that the required amount of capital must be placed at risk "for the purpose of generating a return on the capital placed at risk." A debt arrangement between the Petitioner and the NCE does not constitute qualifying contributions of capital. See Matter of So.ffici, 22 I&N Dec. 158, 162 (Assoc. Comm'r 1998) and 8 C.F.R. § 204.6(e).

Second, the Petitioner provided documentation, including federal and state tax returns, and a September 2013 amended operating agreement, to establish that the NCE, a limited liability company, is owned by several other ipdivid~als. The Petitioner's statements convey her intention to ultimately become a member of the NCE, and two resolutions executed by the NCE members who hold m~jority ownership show that the Petitioner may be granted membership in the NCE at a future date. The February 2012 resolution states that membership will be granted to her "if and when her legal status changes to EB5 Investor." The August 2016 resolution states that she will become a member upon her "a) investing $500,000 in the business and b) receiving a valid working immigration status in the United States." The record does not demonstrate that the Petitioner hOlds an equity interest in the NCE, but rather is a creditor of the organization. Therefore, the funds she has transferred to the NCE are not capital invested for the purpose of generating a return. See 8 C.F.R. § 204.6(j)(2) and 8 C.F.R. § 204.6(e).

4

(b)(6)

Matter of A-J-C-

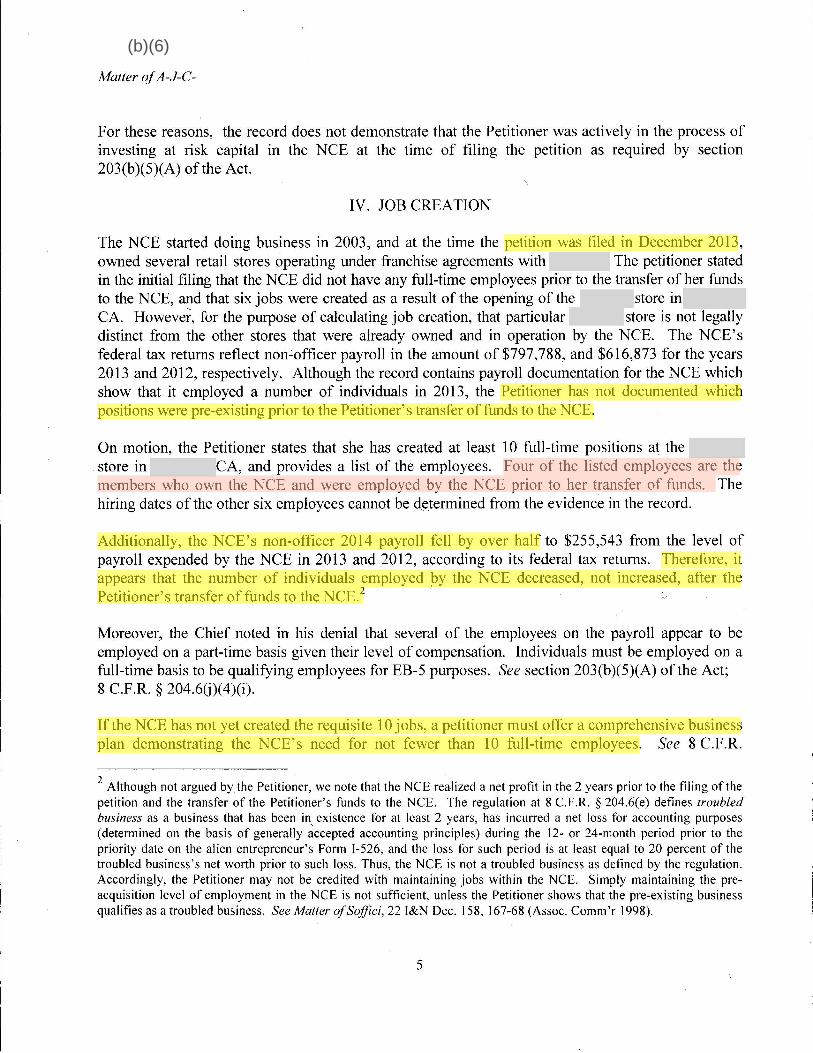

For these reasons, the record does not demonstrate that the Petitioner was actively in the process of investing at risk capital in the NCE at the time of filing the petition as required by section 203(b)(5)(A) ofthe Act.

IV. JOB CREATION

The NCE started doing business in 2003, and at the time the petition was filed in December 2013, owned several retail stores operating under franchise agreements with The petitioner stated in the initial filing that the NCE did not have any full-time employees prior to the transfer of her funds to the NCE, and that six jobs were created as a result of the opening of the store in CA. However, for the purpose of calculating job creation, that particular store is not legally distinct from the other stores that were already owned and in operation by the NCE. The NCE's federal tax returns reflect non.:.officer payroll in the amount of $797,788, and $616,873 for the years 2013 and 2012, respectively. Although the record contains payroll documentation for theNCE which show that it employed a number of individuals in 2013, the Petitioner has not documented which positions were pre-existing prior to the Petitioner's transfer of funds to the N CE.

On motion, the Petitioner states that she has created at least I 0 full-time positions at the store in CA, and provides a list of the employees. Four of the listed employees are the members who own the NCE and were employed by the NCE prior to her transfer of funds. The hiring dates of the other six employees cannot be d~termined from the evidence in the record.

Additionally, the NCE's non-officer 2014 payroll fell by over half to $255,543 from the level of payroll expended by theNCE in 2013 and 2012, according to its federal tax returns. Therefore, it appears that the number of individuals employed by the NCE decreased, not increased, after the Petitioner's transfer of funds to the NCE.Z r v

Moreover, the Chief noted in his denial that several of the employees on the payroll appear to be employed on a part-time basis given their level of compensation. Individuals must be employed on a full-time basis to be qualifying employees for EB-5 purposes. See section 203(b)(5)(A) of the Act; 8 C.F .R. § 204.6(j)( 4 )(i).

Ifthe NCE has not yet created the requisite 10 jobs, a petitioner must offer a comprehensive business plan demonstrating the NCE's need for not fewer than 10 full-time employees. See 8 C.F.R.

2 Although not argued by the Petitio~er, we note that theNCE realized a net profit in the 2 years prior to the filing of the

petition and the transfer of the Petitioner's funds to theNCE. The regulation at 8 C.F.R. § 204.6(e) defines troubled business as a business that has been in existence for at least 2 years, has incurred a net loss for accounting purposes (determined on the basis of generally ~ccepted accounting principles) during the 12- or 24-month period prior to the priority date on the alien entrepreneur's Form 1-526, and the loss for such period is at least equal to 20 percent of the troubled business's net worth prior to such loss. Thus, theNCE is not a troubled business as defined by the regulation. Accordingly, the Petitioner may not be credited with maintaining jobs within the NCE. Simply maintaining the preacquisition level of employment in the NCE is not sufficient, unless the Petitioner shows that the pre-existing business qualifies as a troubled business. See Matter ofSoffici, 22 I&N Dec. 158, 167-68 (Assoc. Comm 'r 1998).

5

(b)(6)

Matter of A-J-C-

§ 204.6G)( 4)(i)(B). The Chief denied the pet1twn in part because the updated business plan submitted in response to his RFE added an investment in a restaurant franchise to the original business plan which focused solely on the investment in an store. A Petitioner must maintain his or her eligibility throughout the application process, which is from the time she files the petition until she receives lawful permanent resident status. Material changes to the investment arrangement require the filing 'of a new Form 1-526 petition. See 8 C.F.R. § 103.2(b)(l); see also Matter of Izummi, 22 I&N Dec. 169, 175-76 (Assoc. Comm'r 1998) (USCIS cannot consider materially different facts that come into being only subsequent to the filing of a petition). We agree with the Chief that the addition of the restaurant franchise in the updated business plan is an impermissible material change to the original business plan submitted in support of the petition.

For these reasons, the Petitioner has n'ot established by a preponderance of the evidence that the NCE has met or will meet the employment creation requirements. Specifically, the Petitioner has not demonstrated that the requisite jobs have already been created as a result of her capital investment in theNCE. Alternatively, she has not submitted a business plan that is comprehensive, or that credibly demonstrates that her $500,000 investment will create, or that the NCE will need, no fewer than 10 new full-time positions. See 8 C.F.R. § 204.6G)(4)(i)(B).

V. CONCLUSION

The Petitioner has not demonstrated that we based our previous decision on an incorrect application of law or USCIS policy. We will therefore deny her motion to reconsider. See 8 C.F.R. § 103.5(a)(3). We have also considered the evidence offered on motion. We evaluated this evidence, together with previously filed document<;ttion, and conclude that the Petitioner has not shown her eligibility for the immigrant investor classification. We will thus deny the motion to reopen. See 8 C.F.R. § 1 03 .5(a)(2).

It is the Petitioner's burden to establish eFgibility for the immigration benefit sought. Section 291 of the Act, 8 U.S.C. § 1361; Matter ofOtiende, 26 I&N Dec. 127, 128 (BIA 2013). Here, the Petitioner has not met that burden. Accordingly, we will deny the motions.

ORDER: The motion to reconsider is denied.

FURTHER ORDER: The motion to reopen is denied.

Cite :as Matter of A-J-C-, ID# 161624 (AAO Feb. 1, 2017)

6

.

U.S. Citizenship and Immigration Services

MATTER OF A-J-C-

Non-Precedent Decision of the Administrative Appeals Office

DATE: AUG. 8, 2017

MOTION ON ADMINISTRATIVE APPEALS OFFICE DECISION

PETITION: FORM I-526, IMMIGRANT PETITION FOR ALIEN ENTREPRENEUR

The Petitioner seeks classification as an immigrant investor based on an investment in , a new commercial enterprise (NCE). See Immigration and Nationality Act (the Act)

section 203(b)(5), 8 U.S.C. § 1153(b)(5). TheNCE owns and operates retail stores and is engaged in the leasing and sale of electronics and furniture under franchise agreements with

. This fifth preference employment-based classification (EB-5) makes immigrant visas available to foreign nationals who invest the requisite amount of qualifying capital in a NCE that will benefit the United States economy and create at least I 0 full-time positions for qualifying employees.

The Chief of the Immigrant Investor Program Office denied the petition. He concluded that the Petitioner did not invest, and was not in the process of actively investing, at least $500,000 in the NCE. 1 He also found that she did not demonstrate theNCE would create at least 10 jobs tor qualifying employees or that she would engage in the management of theNCE. We summarily dismissed her appeal, determining that she did not specifically identify any erroneous conclusion of law or statement of fact for the appeal. We then denied her combined motions to reopen and reconsider our decision, finding that she did not demonstrate an at-risk investment in the NCE or the required job creation. 2 The matter is now before us on second combined motions to reopen and reconsider. We will deny the motions.

I. LAW

A motion to reopen is based on documentary evidence of new facts, and a motion to reconsider is based on an incorrect application of law or policy. The requirements of a motion to reopen are located at 8 C.F.R. § 103.5(a)(2), and the requirements of a motion to reconsider are located at 8 C.F.R. § 103.5(a)(3). We may grant a motion that satisfies these requirements and demonstrates eligibility for the requested immigration benefit.

1 As the NCE is located in a targeted employment area, the required amount of capital is downwardly adjusted from $1,000,000 to $500,000. See 8 C.F.R. § 204.6(1)(2). 2 Although we denied the previous combined motions, we agreed with the Petitioner that she will be engaged in the management of theNCE.

Matter of A-J-C-

II. ANALYSIS

The Petitioner files second combined motions to reopen and reconsider the matter. The filing does not meet the requirements for a motion to reconsider. As noted above, a motion to reconsider must establish that our previous decision was based on an incorrect application of law or policy, and that the decision was incorrect based on the evidence in the record at the time of the decision. 8 C.F.R. § 103.5(a)(3). While the Petitioner requests that we reconsider our previous decision denying her first combined motions, she does not explain how we had incorrectly applied any law or policy, or how we had otherwise erred. Thus, we will deny her motion to reconsider.

Similarly, the motion to reopen will be denied because the evidence the Petitioner presents on motion does not demonstrate her eligibility for the classification. See 8 C.F.R. § 1 03.5(a)(2). On motion, she submits additional documents and maintains that (1) she has invested at least $500,000 in the NCE, and (2) her investment in the NCE has created full-time jobs for 10 qualifying employees. For the reasons discussed below, however, the record, including materials that she offers on motion, does not sufficiently support her assertions. We will thus deny her motion to reopen.

A. Capital Investment

The documentation provided in support of the motion to reopen, along with the previously submitted material, does not show that the Petitioner was actively in the process of investing in the NCE at the time she filed the petition. See section 203(b)(5)(A)(i) of the Act; 8 C.F.R. § 103.2(b)(l). We denied the previous combined motions, in part, because her prospective investment arrangement with the NCE did not constitute a commitment of funds at the time of filing. 3 Page 2 of the petition indicated that the Petitioner began investing in theNCE in September 2012, and had invested a total of$114,000 when she filed the petition in December 2013. The funds that she provided to theNCE, however, were characterized as loans to theNCE in its· federal tax returns and other documentation in the record.

For example, we noted in our previous decision that the Schedule L of theNCE's IRS Form 1065, U.S. Return of Partnership Income; and California Form 568, Limited Liability Company Return of Income, for 2013 and 2014 show a note payable to the Petitioner in the amount of $114,000. Likewise, theNCE's February 2013 resolution indicates that its officers would sign a promissory note for the benefit of the Petitioner in the amount of $114,000. A debt arrangement between the Petitioner and theNCE does not constitute qualifying contributions of capital. See Matter (?(So.ffici, 22 I&N Dec. 158, 162 (Assoc. Comm'r 1998); 8 C.F.R. § 204.6(e) (defining "invest").

Additionally, we determined in our previous decision that the record did not demonstrate the Petitioner held an equity interest in the NCE at the time she filed the petition; instead, she was a

3 The regulation at 8 C.F.R. § 204.6(j)(2) provides that a mere intent to invest, or prospective investment arrangements entailing no present commitment, will not suffice to show that the Petitioner is actively in the process of investing. Instead, the Petitioner must show actual commitment of the required amount of capital. ·

2

Matter of A-J-C-

creditor of the organization. TheNCE's February 2012 and August 2016 resolutions show that she might become a member of theNCE at a future date. Specifically, the 2012 resolution states that membership will be granted to her "if and when her legal status changes to [that of an] EB[-]5 Investor." The 2016 resolution provides that she will become a member upon her "a) investing $500,000 in the business[,] and b) receiving a valid working immigration status in the United States." Her lack of an equity interest in theNCE did not support a finding that she had invested in the business. Based on the above, we found that she did not establish the funds she transferred to the NCE were capital invested for the purpose of generating a return. See 8 C.F.R. § 204.6(j)(2); 8 C.F.R. § 204.6(e).

On motion, the Petitioner maintains that she transferred $515,000 to theNCE through a succession oftransactions. She further asserts that she became a member of theNCE in 2016. She provides an excerpt from theNCE's internal accounting records and a 2017 statement from its accountant, who explains that the NCE's general ledger incorrectly termed her remittances to the NCE as "Notes Payable" to her, instead of "Additional Equity" from her. He also indicates: "[ e ]ffective December 31, 2018 [sic], [the Petitioner] has accepted 51% share in the ownership of [the NCE]." The Petitioner offers theNCE's 2016 state and federal tax returns, which bear no indicia that they were filed with the taxing authorities, to show that she acquired 51% ownership of theNCE and that her loans to the NCE were reclassified as contributed capital in that year.

Assuming arguendo that for accounting purposes, the accountant mistakenly characterized the Petitioner's multiple remittances as loans to, rather than capital investment in, the NCE, the record includes other documents verifying the Petitioner's status as a creditor, not an investor, at the time she filed her petition. Specifically, the evidence that is contemporaneous to her remittances to the NCE reveals that her funds, at least $114,000 of them, were loans to theNCE. TheNCE's February 2013 resolution states that its officers would execute a promissory note for the benefit of the Petitioner for $114,000. The company's 2013 and 2014 state and federal tax returns similarly reflect that the NCE owed the Petitioner $114,000. The purported accounting error does not sut1iciently explain the presence of these documents.

Likewise, though the Petitioner asserts that she acquired membership in theNCE in 2016, she did not provide sufficient documentary evidence substantiating her statement. On motion, she submits theNCE's updated business plan, which references a December 2016 resolution that admitted her as a member. She, however, has not offered a copy of this resolution. In addition, while a copy of the 2016 IRS Form 1065, Schedule K-1, Partner's Share of Income, Deductions, Credits, Etc., indicates that she owns 51% of the NCE, she has not demonstrated that this form was executed or properly filed. In light of the above, the record as a whole does not establish that she has invested in the NCE, or placed at least $500,000 at risk "for the purpose of generating a return on the capital placed at risk." See 8 C.F.R. § 204.6(j)(2).

Moreover, as discussed, the Petitioner must establish that all eligibility requirements for the immigration benefit have been satisfied from the time of the filing and continuing through adjudication. See 8 C.F.R. § 103.2(b)(l). To show her eligibility for the classification, she must

3

.

Matter of A-J-C-

establish that at the time of filing, she invested or was actively in the process of investing at least $500,000 in the NCE. 8 C.F.R. § 204.60). Evidence of her intent to invest, or of prospective investment arrangements entailing no present commitment, will not suffice to show that she was actively in the process of investing. 8 C.F.R. § 204.6(j)(2).

On motion, the Petitioner submits the NCE's tax documents that purportedly show she made her entire capital investment of $515,000 in 2016.4 Assuming arguendo that she did in fa~t invest this sum and take on membership in theNCE in 2016, she would not be eligible for the classification because she did not demonstrate an actual commitment of at least $500,000 in theNCE at the time she filed the petition in December 2013. See Matter oflzummi, 22 I&N Dec. 169, 175-76 (Assoc. Comm'r 1998) (USCIS cannot "consider facts that come into being only subsequent to the filing of a petition."); 8 C.F.R. § 103.2(b)(1). While the evidence might reflect her intent to invest at the time of filing, it is insufficient to establish an actual commitment of the necessary amount of funds.

B. Job Creation

Even if the Petitioner had shown that she was in the process of investing at least $500,000 in theNCE at the time of filing, 5 she would not be eligible for the classification because she did not demonstrate that her investment created or would create at least 10 full-time positions. Specifically, theNCE was an existing business. As such, to meet the employment creation requirements, the Petitioner must show the creation of at least 10 new full-time positions.

In 2013, theNCE owned four retail stores operating under franchise agreements with We denied the Petitioner's previous combined motions, in part, because while the record showed that the NCE employed a number of individuals, she did not document which positions were pre-existing prior to her transfer of funds to theNCE. Additionally, we observed that theNCE's federal tax returns revealed ~that its 2014 "salaries and wages (other than to partners)" fell by over half to $255,543 from the previous two years. Therefore, it appeared that the number of individuals the NCE employed decreased, not increased, after the Petitioner's initial remittance of funds to theNCE. We also noted that several of the employees on the payroll appeared to be employed on a part-time basis given their level of compensation. Individuals must be employed on a full-time basis to be qualifying employees for EB-5 purposes. See section 203(b)(5)(A)(ii) of the Act; 8 C.F.R. § 204.6(j)(4)(i). Lastly, we determined that at least four of the claimed new employees in the NCE's California, store were members who own the NCE, whom the NCE employed prior to the Petitioner's transfer of funds, while the record did not reveal the hiring dates of the six other claimed employees.

On motion, the Petitioner explains that theNCE sold three of its stores in 2013 and that the individuals employed in those locations now. work for their successor employer, which is not associated with the NCE. She maintains that she has created at least 10 full-time positions at the

4 As noted, the Petitioner has not demonstrated that these tax documents, like the 2016 IRS Form I 065, Schedule K-1, are executed or properly filed. . 5 For the reasons discussed above, she has not established an actual commitment of at least $500,000 in theNCE in 2013.

4

.

Matter of A-J-C-

NCE's remaining store, which is in California. As supporting documents, she submits a list of 26 employees that notes each person's rate of pay and employment start date; Form I-9s, Employment Eligibility Verifications; and 2016 Form W-2s, Wage and Tax Statements. Ofthe 22 Form W-2s provided, at least 13 of the individuals earned less than $6,000 in 2016. The Petitioner has not demonstrated that these employees worked on a full-time basis. Two of the remaining employees have been members of the NCE since its inception in 2003. These two employees and another full-time employee were already employed by the NCE prior to the Petitioner's initial transfer of funds. In light of the above, the Petitioner has not verified that the NCE has created at least 10 new full-time jobs since she commenced transferring funds.

As the Petitioner has not established the requisite job creation, she must offer a comprehensive business plan verifying theNCE's need for not fewer than 10 full-time employees. See 8 C.F.R. § 204.6G)( 4)(i)(B). The business plans in the record do not demonstrate that theNCE will create the necessary number of jobs. We note that theNCE operated at a -$249,888 loss according to its 2016 federal tax return.6 The updated business plan provided on motion gives general information about the California, store, and the economic conditions present in that community, but lacks details on the prospective steps that the NCE will undertake to increase the scope of its operations or number of full-time employees. For these reasons, the Petitioner has not shown that theNCE has met or will meet the employment creation requirements. See 8 C.F.R. § 204.6(j)(4)(i)(B).

Accordingly, we will deny the Petitioner's motion to reopen because the record is insufficient to demonstrate she invested or was actively in the process of investing in theNCE at the time she tiled the petition. She has additionally not established that the NCE has created or will create at least 10 fulltime positions for qualifYing employees as a result of her investment.

III. CONCLUSION

The Petitioner has not shown that we incorrectly applied any law or policy, or otherwise erred in our previous decision. Moreover, the record as a whole does not establish her eligibility for the immigration benefit sought.

ORDER: The motion to reconsider is denied.

FURTHER ORDER: The motion to reopen is denied.

Cite as Matter of A-J-C-, ID# 557776 (AAO Aug. 8, 2017)

6 TheNCE's 2016 IRS Form I 065 indicates that the "Ordinary business income (loss)'' was -$249,888.