Material Availability and the Supply Chain: Risks, Effects ...

OCTOBER 2014

MATERIAL RISKS: HOW PUBLIC ACCOUNTABILITY IS SLOWING TAR SANDS DEVELOPMENT

Material Risks: How public accountability is slowing tar sands development

This paper was conceived, written and researched collectively by Tom Sanzillo, Lorne Stockman,

Deborah Rogers, Hannah McKinnon, Elizabeth Bast, and Steve Kretzmann. With assistance and/or

additional contributions from Adam Wolfensohn, and Amin Asadollahi.

October 2014

This is the first of a series of collaborative papers on the tar sands industry in Canada. The paper is intended

to identify issues, data and trends, which will be developed in greater detail in the coming months.

Institute for Energy Efficiency and Financial Analysis

http://www.ieefa.org/

Oil Change International

http://priceofoil.org

The Institute for Energy Economics and Financial Analysis (IEEFA) conducts research and analyses on

financial and economic issues related to energy and the environment. The Institute’s mission is to accelerate

the transition to a diverse, sustainable and profitable energy economy and to reduce dependence on coal

and other non-renewable energy resources.

Oil Change International (OCI) exposes the true costs of fossil fuels and identifies and overcomes barriers

to the coming transition towards clean energy. Oil Change International works to achieve its mission by

producing strategic research and hard-hitting, campaign-relevant investigations; engaging in domestic

and international policy and media spaces; and providing leadership in and support for resistance to the

political influence of the fossil fuel industry, particularly in the United States.

Cover image: Protestors against the Keystone XL pipeline conducting a sit in outside the White House

during the Tar Sands Action, September 3, 2011. ©Josh Lopez.

CONTENTS

Executive Summary 4

Public Accountability Makes a Difference: Shifting Markets, Increased Scrutiny and Changing Opinion 6

Keystone XL: public accountability as an investment risk 7

Lessons in the public accountability risk factor from U.S. coal experience 7

Troubling Trends: Public Accountability Impacts to Date 8

Underperforming stocks 8

Spending more, making less 10

Additional impediments and risks 13

Transportationbyrail 13

Legalaccesstotheresourceandtransportationroutes 14

Canadianactiononforeignownership 15

Costinflation 15

Costcurves,carbonriskandstrandedassets 15

Environmentalandotherregulatoryrisks 15

Rising costs and cancelled projects 16

Capexisdeclininginthetarsands 16

Cancelledprojects 17

Revenuelossesandmarketaccess 18

Thecostofdelays 18

Forecast Model: Impact of Market Pressures and Public Accountability on Tar Sands Production 20

Increased pipeline capacity critical to achievement of production goals 20

Reduced netback and avoided production/emissions 20

Capex forecast suggests end to boom times 22

Estimating the barrels at risk from pipeline infrastructure campaigns and the carbon impact 22

Conclusion 25

Appendix: Tar Sands Production by Company 26

Thisreportisforinformationandeducationalpurposesonly.Itis

intendedsolelyasadiscussionpiecefocusedonthetopicofthetar

sandsindustryandtheimpactofpublicaccountabilityeffortsand

marketforcesandtheimplicationsforindustryprofitability.Under

nocircumstanceisittobeconsideredasafinancialpromotion.

Itisnotanoffertosellorasolicitationtobuyanyinvestment

referredtointhisdocument;norisitanoffertoprovideanyform

ofinvestmentservice.

Thisreportisnotmeantasageneralguidetoinvesting,orasa

sourceofanyspecificinvestmentrecommendation.Whilethe

informationcontainedinthisreportisfromsourcesbelieved

reliable,wedonotrepresentthatitisaccurateorcompleteand

itshouldnotberelieduponassuch.Unlessattributedtoothers,

anyopinionsexpressedarethecurrentopinionsofOilChange

International(OCI)andtheInstituteofEnergyEconomicsand

FinancialAnalysis(IEEFA)only.

Certaininformationpresentedmayhavebeenprovidedbythird

parties.OCIandIEEFAbelievethatsuchthird-partyinformation

isreliable,butdonotguaranteeitsaccuracy,timelinessor

completeness;anditissubjecttochangewithoutnotice.Ifthere

areconsideredtobematerialerrors,pleaseadvisetheauthors

andarevisedversioncanbepublished.

OCIhasenteredintoacontractwithRystadEnergyfortheuseof

itsUCubedatabase.ThedatabaserepresentsRystad’scompilation

ofindustrydataandtrends.Muchofthedatausedinthisreportis

derivedfromthatdatabaseand,whereappropriate,supplemented

withindependentsourcesfromthetarsandsindustry,individual

tarsandproducerfinancialfilings,governmentalpublicationsand

businesstradepublications.Thesummaryandconclusionsinthis

paperarethoseofOCIandIEEFA.Thesummaryandconclusions

arenottobeconstruedastheopinionofRystadEnergy.

IMPORTANT INFORMATION

4

TheKeystoneXLtarsandspipelineisoneofthemosttalked

aboutNorthAmericanenergyandpoliticalissuesoftheera.Once

thoughtinevitable,theprojectandCanada’splantoexpandtar

sandsproductionhavebeenconfrontedbyanaccumulationof

economicandpoliticalriskscreatingaveritable‘carbonblockade.’

AsCanadianleadersandcitizenswrestlewithanindustry

plantomorethandoublethedailyoutputoftarsandscrude,

stakeholdersinandoutsideofCanadahavecreatedadebateover

localenvironmentalandglobalclimatecosts.U.S.andCanadian

decisionmakershavetakenasecondlookasprojectdelaystake

afinancialandpoliticaltollonproposedprojects.Thedelaysand

cancellationshaveexposedthefactthattarsandsinvestments,

oncethoughttobehighlylucrative,areshowingsignsoffinancial

weakness.Withgrowingpublicawarenessandmarkethesitancy,

expansionoftarsandsproductioninCanadawillremaincontested

terrainfortheforeseeablefuture.

IfCanadianoilproducersareabletosucceedwiththeirlarge

scalebuildoutplans,over21billionbarrelsoftarsandscrudewill

beproducedoverthenextsixteenyears(to2030).Inthattime,

industryintendstoincreasedailyproductionfromcurrentlevels

of2millionbarrelsperday(mbpd)topossiblyashighas4.8mbpd

orevenmore.

Tarsandsproductionislandlocked.Expansionoftransport

infrastructureisessentialtoproductiongrowth.TheKeystoneXL

pipelinecampaignhas,todate,delayedthispipelineinfrastructure

projectforoverfiveyears.Additionalcampaignshaveeffectively

delayedeveryproposedexportpipelineproject,including

NorthernGateway,AlbertaClipper,andEnergyEast.Thedelays

havecostproducersmoneyandtime,reducingthepricethey

havereceivedfortarsandscrudeassupplyhasoutpacedthe

capacityoftransportinfrastructuretocarrytarsandscrudeto

newmarkets.

DuringthedebateoverKeystone,marketchangeshavetaken

placethatarealsoweakeningthefinancialviabilityoftarsands

projects.In2014alone,threesignificantprojectshavebeen

canceledandmoreareinsignificantfinancialdistress.Junior

tarsandproducersare,asagroupfacingcapitalmarketaccess

problems.Inaddition,theindustryfacesagrowingconstellation

ofrisksasprojecteconomicsbecomepressuredbylowoilprices

andshrinkingrevenues,risingcosts,smallerprofitmargins,

toughercapitalmarkets,transportconstraints,environmental

challengesandprotectionistlegislation.

Mostanalystsconsistentlycite“transportationandinfrastructure

constraints”and“lackofinternationalmarketaccess”asmajor

reasonsforconcern.Thesefactorsaredirectlylinkedtopublic

accountabilityeffortsaroundclimateandotherenvironmental

issuesthatappearcertaintoonlygrowstrongerinthecoming

years.Inaddition,therecentfallinoilpricesonlyreducesmargins,

thusfurtherunderminingtheviabilityofprojectfinance.Tarsands

producersneedpipelinestomovetheirproductascheaplyas

possibletothemostlucrativemarketsmorethaneverbefore.

ThisreportisajointeffortbytheInstituteforEnergyEfficiency

andFinancialAnalysisandOilChangeInternationaltodescribethe

changeshappeninginthetarsandsmarket,discernthereasons

forthesechanges,andforecasttheimpactsofcontinuingtrends.

Ourprincipalfindingsare:

f Lack of market access, caused in large part by public

accountability actions driven by pipeline campaigns, has

played a significant role in the cancellation of three major tar

sands projects in 2014 alone- Shell’s Pierre River, Total’s Joslyn

North, and Statoil’s Corner Project.

f Combined, these projects would have produced 4.7 billion

barrels of bitumen that would in turn have released 2.8 billion

metric tonnes of carbon dioxide (CO2) into the atmosphere.

Thisisequivalenttotheemissionsof735coalplantsinoneyear,

orbuilding18newcoalplantsthatwilllast40yearseach.

f After years of increased spending in the tar sands, capital

expenditure (Capex) has peaked and has begun to decline.

WeprojectthatthiserosionofCapexspendinglevelsfrom

currentplanswillcontinueastarsandproducersincreasingly

acknowledgetheconstellationofrisksdescribedinthisreport.

f Public accountability in the form of pipeline campaigns

has been a major factor in reducing revenues to tar sands

producers.Overall,tarsandsproducerslost$30.9billion

between2010-2013duetowiderpricedifferentialscausedby

transportationbottlenecksandthefloodofcrudecomingfrom

tightoilfields.Ofthat,$17.1billionor55percentcanbecredibly

attributedtotheimpactofpublicaccountabilitycampaigns.

f Tar sands producers are underperforming the stock market.

NineoftenleadingtarsandsproducersinCanadahave

underperformedthestockmarketinthelastfiveyears.

f Leading industry experts have recently downgraded their

outlook for future tar sands production.Thisdowngradetakes

placeastransportationconstraintspersist.

EXECUTIVE SUMMARY

5

Inadditiontoevaluatingcurrentimpactsofpublicaccountability

todate,wealsohaveconstructedaforecastmodeltoestimate

whatcontinuedpublicpressureonpipelineinfrastructuremaydo

totarsandsproduction.Ourforecastanalysisprojectstrendsout

to2030andfindsthat:

f Ifpipelinecampaignsandassociatedpublicaccountability

effortscontinuetodrivetransportationconstraints,upto

6.9billionbarrelsoftarsandsoilcouldbeleftunderground.

Inotherwords,ifnonewpipelinesarebuilt,ourforecast

predictsthatanadditional4.1billiontonnesofCO2willnotbe

releasedintotheatmosphere.Spreadoverthe16yearsofthis

forecast,theseemissionsaretheequivalentoftheemissions

from67averageU.S.coalplantsornearly54millionaverage

passengervehicles.

f Capitalexpenditure(Capex)isexpectedtodeclinesteadilyfor

yearsandourforecastdoesnotenvisionitreturningtocurrent

levelsforatleast15years,ifever.Increasedinvestmentinthe

tarsandsisonlylikelytotakeplaceifallormostmarketaccess

issuesaresolved.

Tarsandspipelinecampaignsarearecentexampleofhow

publicadvocacyeffortscanaltercapitalinvestmentdecision

making.TheKeystoneXLcampaignhasmanagedthusfarto

delayafinalgovernmentaldecisionontheprojectwhileraising

publicawarenessabouttheenvironmentalcostsoftarsands

development.Thesecitizeninterventionshaveresultedin

increaseddiligencebygovernmentagencieswithpublichealth

andenvironmentalmandates,impairedtheprojectdevelopment

processofthecapitalmarketsandmobilizedapermanent,political

constituencyinsupportofalternativestotarsandsexpansion.

“There is no way we could have ever predicted that we would become the lightning rod for a debate around fossil fuels and the development of the Canadian oil sands.”Russ Girling, CEO, TransCanada, 2011

6 PUBLIC ACCOUNTABILITY MAKES A DIFFERENCE: SHIFTING MARKETS, INCREASED SCRUTINY AND CHANGING OPINION

Tarsandsandpipelinecampaignsarea

recentexampleofhowpublicadvocacy

effortscanshapecapitalinvestment

decisionmaking.TheKeystoneXL

campaigntostoptheprojecthasmanaged

thusfartodelayfinalgovernmental

decisionsontheprojectwhileraising

publicawarenessabouttheenvironmental

costsoftarsandsdevelopment.These

activistinterventionshaveresultedin

increaseddiligencebygovernment

agencieswithpublichealthand

environmentalmandates,impairedthe

projectdevelopmentprocessofthecapital

marketsandmobilizedapermanent,

politicalconstituencyinsupportof

alternativestotarsandexpansion.This

reportdocumentsthedetailedinterplay

ofpublicadvocacyeffortsandmarket

forcesintheCanadiantarsands.

KEYSTONE XL: PUBLIC ACCOUNTABILITY AS AN INVESTMENT RISKWhentheTransCanadaKeystoneXL

pipelinewasoriginallyproposedin2008,

therewasanexpectationthatitwould

receivenecessaryapprovalsquicklyand

beupandrunningbylate2011.Public

policy,publicopinion,andcapitalmarket

allocationswereinalignmenttopromote

theKeystonestorylineofinvestment

growthandeconomicprogressinthe

tarsands.

Timeandeventschangedthisstoryline.By

2011RussGirling,theCEOofTransCanada,

said“There is no way we could have ever

predicted that we would become the

lightning rod for a debate around fossil

fuels and the development of the Canadian

oil sands.”1Publicadvocacyeffortswere

alreadydrivingsignificantshiftsinpublic

opinionandpoliticaldebatein2011.Today,

publicoppositiontothepipelinehas

continuedtogrowandsupportforthe

pipelinehasdeclined.2

InCanada,campaignstoraiseawareness

aroundtarsandsandpipelinesare

clearlyhavinganimpactonpublic

opinionaswell.Pollingcompletedfor

theCanadianAssociationofPetroleum

Producers(CAPP)inlate2013showed

thatthemajorityofCanadians(51%)

believethat,“whilethereisaneedfor

energyinCanada,itdoesnotoutweigh

theenvironmentalriskswithoilsands

development.”Thesamesurveyalso

indicatedthat80%ofCanadianswould

assignthetarsandsindustryagradeof

Corlesswhenitcomestoprotecting

theenvironment.3Finally,recentNanos

polling,alsoinCanada,showsthatsupport

fortheKeystoneXLpipelineinCanadahas

droppedfrom60%to47%betweenApril

of2013andJanuaryof2014.4

Itisexpectedthatsometimeduringlate

2014orearly2015theUnitedStates

governmentwillmakeacriticaldecision

thatcouldmovetheprojectforwardor

causeitscancellationorfurtherdelay.

Whateverthedecision,thestorylineof

unfetteredgrowthattachedtoKeystone

andothertarsandsprojectshasbeen

permanentlyaltered.Growingpublic

sentimenttofindalternativestofossil

fuelswilldrivemuchofthedialogue.

Futureinstitutionaldecisionsbethey:

internationalagreementsonclimate

change,shiftsofcapitalallocation,change

inlaworregulation,and/oradoptionof

newparadigmsbyelectedleadersand

1 Cattaneao,C.“TransCanadaineyeofthestorm.”The Financial Post.September8,2011.http://business.financialpost.com/2011/09/08/transcanada-in-eye-of-the-storm/?__lsa=bf5b-4bd4

2Droitsch,D.“NewpollonKeystoneXLtarsandspipelineindicatinggrowingopposition,waningsupport.The Energy Collective.January30,2014.http://theenergycollective.com/danielle-droitsch/334201/new-poll-keystone-xl-tar-sands-pipeline-indicating-growing-opposition-pipel

3“Here’swhatCanadiansthingoftheoilsandsindustry.”National Post.October30,2013.http://business.financialpost.com/2013/10/30/heres-what-canadians-think-about-the-oil-sands-industry/?__lsa=21a3-b64e

4“SupportforKeystoneXLpipelineonthedecline:Nanos.”CBC News.January16,2014.http://www.cbc.ca/news/politics/support-for-keystone-xl-pipeline-on-the-decline-nanos-1.2498835

7

thepublicaremovingtowardeconomic

modelsthatcombineprofitabilitywith

protectionofpublichealth,climate,and

theenvironment.

Thesefactorsarematerialriskstothe

currentalignmentofcapitalinvestment

andprojectdevelopment.Thispaper

assertsthattherisks,typicallyunderstood

aspoliticalrisks,areknown,permanent,

predictablewithinreasonablestandards

ofprobability,shapethebehavior

ofinvestmentstakeholdersand,are

ultimatelyquantifiable.

LESSONS IN THE PUBLIC ACCOUNTABILITY RISK FACTOR FROM U.S. COAL EXPERIENCEOneoftheclearestareaswherepopular

mobilizationhasdemonstratedsignificant

impactoninvestmentdecisionmaking

relatestocoalplantinvestmentsinthe

UnitedStates.In2007theUnitedStates

plannedfor150newcoalplantstoreplace

oldonesthatwereagingout.5Fromits

inceptionthenewplanranintofinancial

headwindsandpublicoppositionledby

theSierraClub.By2010itwasclearthat

mostofthecoalplantswerenotgoingto

bebuilt.

DanielYergin,theprominentoilindustry

consultant,emphasizesthatenergy

marketsaredriventoalargeextentbya

complexnexusbetweencapitalmarkets,

governmentsupport,andpolitical

interests.AccordingtoYergin,public

campaigningagainstcoalwasaprimary

driverinchallengingtheplansofthis

politicallyprotectedenergysourceinthe

U.S.intofinanciallytoxicandunbuildable

unprofitableprojects:

In2011about25coalfiredplantswere

underconstructionintheUnitedStates.

Butpoliticalandregulatoryopposition

tocoalongroundsofglobalwarming

hasmountedtoalevelthatmakesit

difficulttolaunchnewconventional

coalplants.6

Newcoalplantproposalsoriginallyhad

thebackingofelectedofficials,investment

banks,utilitycompanies,andpublic

servicecommissionsandenvironmental

regulators.Inmanycasesinvestment

wassunkandpermitsacquiredbefore

proposalsweredropped.Investorsandan

increasinglistofotherstakeholdersfound

themountingrisksofchangingmarket

conditions,increasedregulation7andanti-

coalcampaignstoonumeroustomanage.

Thecanceledplantsinvolvedanestimated

$273billioninnewcapitalinvestment

andtheterminationofsupportfornew

plantsbykeyenergystakeholdersacross

thenation.8

Mostofthesecoalplantcancellations

occurreddespiteutilityandcoal

industryeffortstohavethemapproved.

Acombinationofchallengingmarket

conditionsandpublicaccountability

advocacyovershadowedindustryefforts

toexpandcoalfiredgenerationinthe

UnitedStates.9,10Thecumulativeimpact

oftheseriskshaseffectivelymadenew

coalplantsunbankable.11

Withoutachievinganynoteworthypublic

policygoalduringthatperiod(infact

federalclimatelegislationwasdefeated),

theclimatemovementsuccessfully

initiatedactionsthatdirectlyandindirectly

contributedtoashiftinperceptionthat

newcoalplantswerenotprofitableand

drovethecancellationthesenewenergy

investments.Climateactivistsaretoday

engagedinasimilarefforttoshiftthe

perceptionofinevitability,whichcontinues

tosurroundtarsandsdevelopment.

WhattheU.S.coalplantexperience

suggestsisthatintheabsenceofan

internationalornationalresponsetothe

challengeofenergyandclimate,local

leadersandinvestorssteppedintofill

thepolicyvoidandadoptedstrategies

thatledtothedefeatofsignificantnew

levelsofcoalfiredgeneration.Theblunt,

frankmessageofthisuniformrejectionof

newcoalplantstopolicymakersandthe

capitalmarketswas:FindAnotherWay.

Theimpactoftheseadvocacyefforts

highlightedtodecisionmakerstheclimate

andenvironmentalcostsandincreasingly

broughttobearfinancialperspectives

thatshowedaweakeconomicoutlookfor

coal.Inasignificantnumberofinstances

itisapparentthatcoalandutilityinterests

wouldhavebuilthighlyriskycoalplantsif

notfortheadvocacychallenges.12Inthe

broadersensetheindustry’s183failed

coalplants13createditsownstorylineofa

downwardspiral–astorylinethatwould

hindertheirfutureefforts.

5 NationalEnergyTechnologyLaboratory(NETL).Trackingnewcoal-firedpowerplants,coal’sresurgenceinelectricpowergeneration.2007.6 Yergin,D.TheQuest:Energy,securityandtheremakingofthemodernworld.NewYork:PenguinBooks,2011.7 Barradale,MerrillJones,“TheLogicofCarbonRisk:APractitioners’PerspectiveonInvestmentUnderUncertainClimatePolicy.”June21,2013.USAEEWorkingPaperNo.09-037.

http://ssrn.com/abstract=1529471orhttp://dx.doi.org/10.2139/ssrn.15294718 NationalEnergyTechnologyLaboratory(NETL).Tracking new coal-fired power plants, coal’s resurgence in electric power generation.2007.NETL’splanwouldhavecreated90GW

ofelectricityandcostapproximately$145billion.Forthepurposesofthispaper,thecostofconstructionisassumedtobefora600MWcoalplantatacostof$2500kw.Thefullcostfortheoriginalportfolioof150newplantsisestimatedat$225billion.The183plantswouldconservativelybevaluedat$273billion.Notallplantsweresponsoredbyinvestorownedutilities.Someweresponsoredbypublicpowerauthorities,othersbyruralelectriccooperatives–allrequireaccesstocapitalmarketswherereturnoninvestmentsiscalculatedagainstrisk.

9 Hertsgaard,Mark.“HowaGrassrootsRebellionWontheNation’sBiggestClimateVictory.”.Mother Jones,April2,2012.http://www.motherjones.com/environment/2012/04/beyond-coal-plant-activism

10Ward,Beth.“Onlackofcoalbuild-up,envirostoutwins,industrylistsseveralfactors,”Platts Coal Outlook.April18,2011.11 EdisonElectricInstituteFinancial Review (of Investor Owned Utilities), Construction,2013.p.49.12 Sanzillo,Tom.“Power4GeorgiansPlantWashington:TooHighaPriceforConsumers.”TR Rose Associates,2011.pg.41-43.13 Inadditiontothe150originalplantsothercoalplantproposalswerealsoannouncedandcanceled.AccordingtotheSierraClubasofSeptember14.2014,183newcoalplantproposals

havebeendefeated.http://content.sierraclub.org/coal/environmentallaw/plant-tracker

8

ThedebateovertheKeystoneXLpipeline

hasbroughtincreasedinterestinthetar

sandsindustryandthecompaniesinvolved

withit.ThedelaysonKeystone,andother

tarsandsprojectsarearesponsetopublic

demandsforgreateraccountabilityand

marketforcesnowcallingforasecond

lookatCanada’saggressiveplansfor

expandedsupplyandshipmentoftar

sandsproducts.

Thissectionofthepaperidentifies

financialbenchmarksandriskstoindustry

anddemonstrateshowdeteriorating

corporateandprojectfinanceis

diminishingthelikelihoodthatCanadian

tarsandsproducer’splansforexpansion

willmaterialize.

GrantUkrainetzoftheKoreanstate-

ownedoilcompany,summarizedthe

marketperceptionoftarsandsproduction

inOctober,2013:

Capital cost pressures in the oil sands

have tripled, operating costs in the oil

sands at least doubled, we had a change

in the oil sands royalty regime, we had

greater environmental regulations,

costs of compliance have increased,

we had continued delays in pipelines

that allow us to move products out to

maximize revenue, (there is) negative

public sentiment toward the oil sands,

plus you have the emergence of other

opportunities in the U.S. and elsewhere.14

UNDERPERFORMING STOCKS Ananalysisofmajortarsandscompanies’

stockrevealsthatalargemajority,while

profitable,areunderperformingrelativeto

marketbenchmarks.Thetentoptarsands

operatorsinCanadaproduce85%ofalltar

sandsproductionthatoccurredin2013.

FiveofthetoptenproducersareCanadian

basedandtheremainderarebasedinthe

UnitedStates,NetherlandsandChina.

ExxonMobil,ShellandConocoPhillipsare

globalleadersintheoilandgasindustry.

MosttarsandsproducersinCanadaare

engagedinabroadrangeofoilandgas

extraction,processing,marketing,and

distribution.Forsomeofthecompanies,

likeExxonMobil,Canadiantarsands

representasignificantshareofoverall

Canadianproductionbutonly9%ofthe

company’sannualproduction.

Areviewofeachcompany’sstock

performanceoverthelastfiveyears

revealsthefollowingpatterns(see

Figure1).16Onlyoneofthecompanies,

ConocoPhillips17(seefootnotebelow)

consistentlyledtheDowJonesIndustrial

Average.Theremainingcompanies,

whilelargelyprofitablelaggedthose

marketbenchmarks.Largeoilcompanies

commandsignificantinvestmentfrom

individualandinstitutionalinvestors.These

companiesaretraditionallyrelieduponto

leadtheglobaleconomyandthemajor

stockmarkets.Anyindicationthatthese

companiesarenotleadingeconomic

growthiscauseforconcern.

Thestockperformanceofthetentop

tarsandsproducersinCanadaraises

theseconcerns:

f Despitegrowth,tarsandsproducer

sharepriceshavesignificantlylagged

behindtheDowJonesIndustrial

Average(DJIA).

f TheDJIAhasincreasedby~57%since

2010.OnlyConocoPhillipshasposted

stockperformancethatexceededthis

growthmetric(130%oftheDJIA).The

otherninecompaniesrangedingrowth

from-44%to+33%.

f TheStandardandPoor'sToronto

ExchangeIndexroseby~19%during

TROUBLING TRENDS: PUBLIC ACCOUNTABILITY IMPACTS TO DATE

14 Catteano,Claudia.“Oilsandsinvestmentslowingbecauseoftoughmarket,notnewSOErules,execssay.”TheFinancialPost.April4,2014.http://business.financialpost.com/2014/04/04/oil-sands-investment-slowing-because-of-tough-market-not-new-soe-rules-execs-say/?__lsa=698a-6a9b7840-5316

15 RystadEnergyUCube(Sept.2014)16 Forthepurposeofthisanalysisindividualcompanystockperformancewascomparedtoitspeers,andtheDowJonesIndustrial(DJIA)averagefrom2009tothe

present.Theimpactoftarsandsperformancewithineachofthecompanieshasarelativelydifferentweightgiventheimportanceofthetarsandsoperatingsegmenttotheenterpriseasawhole.Thisanalysisismeanttobeusedincombinationwiththeotherfinancialmetricsprovidedinthisreporttoprovideabroaderunderstandingofcompanyandmarketperformance.

17 Conoco’sgainsaremoreattributabletoitsbroaderrestructuringplanincludingitsintensifiedinvestmentsinNorthAmericantightoilandspin-offofitsrefiningoperations.TheaggressivegrowthisnotattributabletoitsCanadiantarsandsoperation.

9Company Country 2013 Production (thousands bb/day)

Suncor Canada 398

Canadian Natural Resources Canada 196

ExxonMobil U.S.A. 172

Shell Netherlands 145

ConocoPhillips U.S.A. 115

Cenovus Energy Canada 103

Canadian Oil sands Canada 98

Imperial Oil Canada 71

Devon Energy U.S.A. 57

CNOOC China 49

Top 10 2013 Production 1,403

Total 2013 Production (All) 1,656

Top Ten Percentage of Total 85

Table 1. Top 10 Tar Sands Producers in Canada15

Dow Jones Indust. Suncor Can. Nat Res. Can. Oil Sands Cenovus Imperial

-60

-40

-20

0

20

40

60

80

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep-10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-14

Source:Companyfinancials,IEEFA

Figure 1: Stock Performance of Top 5 Tar Sands Companies between 2010 and 2014 Relative to the Dow Jones Industrial Average

10

thissameperiod.OfthefiveCanadian

basedcompaniesonlyImperialOil

surpassedthisIndex.

f IfConocoPhillipsisremovedfromthe

equation,theaverageofthetopnine

producersgrewbyonly~7%duringthe

period2010-2014,comparedtothe

DJIAat~57%.

f Suncor,Canada’sleadingtarsands

producergrewby~2.4%--just4%of

thegrowthleveloftheDJIAand12%

oftheTorontoIndex.

SPENDING MORE, MAKING LESS Eachofthetoptentarsandscompanies

hasintegratedoperationssuchas

conventionalandunconventional

production,refiningandmidstreamassets

inadditiontotheirtarsandsportfolios.

Tarsandsinvestmentsareconsidered

long-livedassetsthatshouldproduce

revenuefordecades.Inthecurrentclimate

theindustryisshowingsignsofweakness.

AsdemonstratedbyFigure2,tarsand

producersarespendingmoreoncapitals

projects,pressuredbyrisingoperational

expendituresandfacedwithdiminished

cashflow.

Amoredetailedanalysisofthespecific

companiesinCanada’starsandsportfolio

demonstrateshowtheseunderlying

dynamicsplayoutineachcompany.

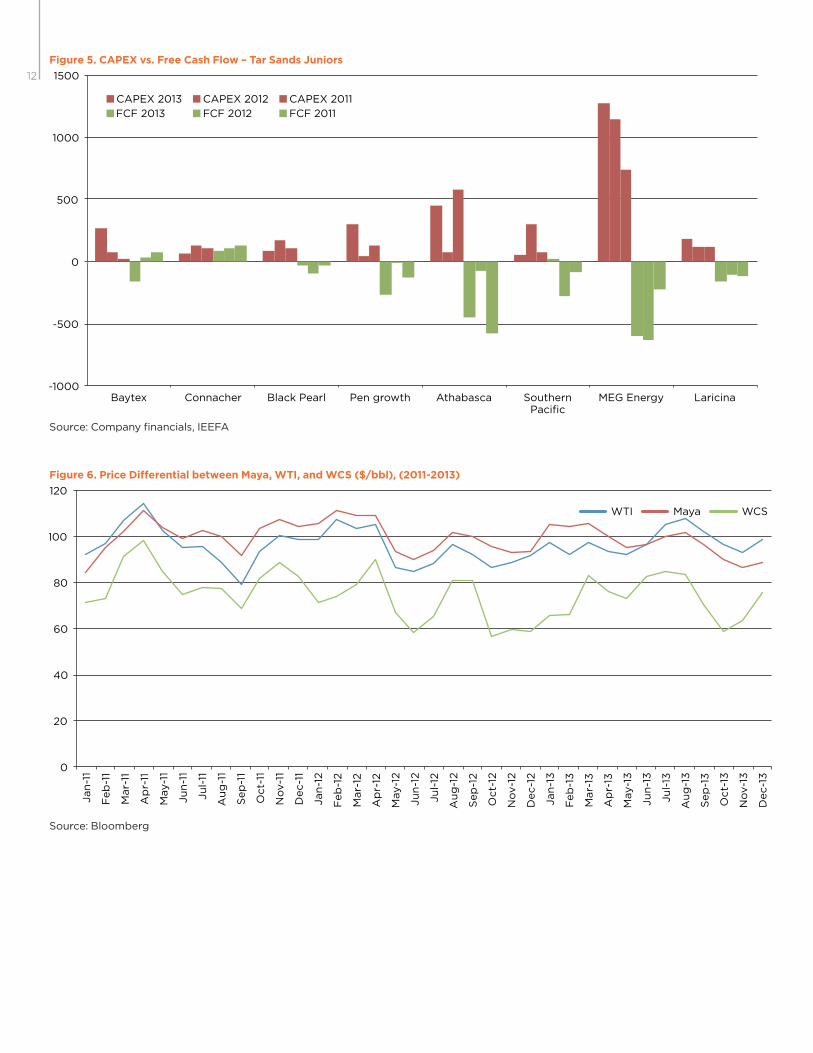

Largeindustryleadersandthesmaller

juniorcompaniesintheCanadiantar

sandsindustryhavebeenexpandingtheir

programsofcapitalexpenditure.Seven

ofthetoptenleadingcompanieshave

negativefreecashflow(seeFigure3and

4).Asimilartrendisoccurringwithregard

tothejuniortarsandsproducers(see

Figure5).Thistrendwherecompaniesrun

anegativecashbalance(whilefacingrising

operationalexpenses)inordertofinance

futurecapitalinvestmentisawarning

signalandrequiresadditionaldiligence

byinvestors.

Additionalanalysisshowsthatthe

revenuesideoftheequationfortarsands

producershastightenedinthelastfew

years.Tarsandsproductionisheavily

dependentuponhighcrudeprices.Since

2011theWesternCanadianSelect(WCS)

(Canadianoilsandsproduct)hastraded

ataconsistentlydiscountedpricetoWest

TexasIntermediateandMaya(Mexican)

oil(SeeFigure6).Thisisnotanticipated

tochange.

ThediscountbetweenWCSandWTI

increasedfrom$17.10in2011to$25.11in

2013.WCS’sweakenedpriceposition

tightenedoperatingmarginsforthe

industry.In2012,whenglobalcrude

pricesdropped,CanadianExploration

andProductioncorporateprofitsfell

morethan50percentto$7.1billion,the

lowestlevelseensince1999.

Relativelyweakstockperformance,

highcapitalandoperationalexpenditure,

andfallingpricessuggestascenario

ofweakeninglongtermperformance.

Couplingsuchmarginconstraintswith

transportationbottlenecksandother

troublingtrendsraisesareasonable

argumentthatoilsandsinvestments

maynotbethebestplaceforinvestors

toseekreturns.

Figure 2: Spending versus income in the tar sands 2008-2013

(15)

(10)

(5)

-

5

10

15

20

25

30

35

Bill

ion

US

D

2008 2009 2010 2011 2012 2013

Capex Opex Free Cash Flow

Source:OCI/IEFFA(RystadEnergyUCube,Sept.2014)

11

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

Suncor CanadianNat. Res.

Shell ExxonMobil

CanadianOil Sands

ConocoPhillips

Cenovus Imperial CNOOC Devon

Revenues 2013 FCF 2013

Source:Companyfinancials,IEEFA

Figure 3. Tar Sands Revenues vs. Free Cash Flow 2013

Figure 4. Tar Sands CAPEX vs. Free Cash Flow

Source:Companyfinancials,IEEFA

Suncor CNRL Can. Oil Sands

Cenovus Imperial Devon ExxonMobil Conoco Phillips

Shell CNOOC

CAPEX 2013 CAPEX 2012 CAPEX 2011

FCF 2013 FCF 2012 FCF 2011

-6000

-4000

-2000

0

2000

4000

6000

12

Figure 5. CAPEX vs. Free Cash Flow – Tar Sands Juniors

Source:Companyfinancials,IEEFA

CAPEX 2013 CAPEX 2012 CAPEX 2011

FCF 2013 FCF 2012 FCF 2011

-1000

-500

0

500

1000

1500

Baytex Connacher Black Pearl Pen growth Athabasca Southern Pacific

MEG Energy Laricina

Figure 6. Price Differential between Maya, WTI, and WCS ($/bbl), (2011-2013)

Source:Bloomberg

WTI Maya WCS

0

20

40

60

80

100

120

Jan

-11

Feb

-11

Mar-

11

Ap

r-11

May-1

1

Ju

n-1

1

Ju

l-11

Au

g-1

1

Sep

-11

Oct-

11

No

v-1

1

Dec-1

1

Jan

-12

Feb

-12

Mar-

12

Ap

r-12

May-1

2

Ju

n-1

2

Ju

l-12

Au

g-1

2

Sep

-12

Oct-

12

No

v-1

2

Dec-1

2

Jan

-13

Feb

-13

Mar-

13

Ap

r-13

May-1

3

Ju

n-1

3

Ju

l-13

Au

g-1

3

Sep

-13

Oct-

13

No

v-1

3

Dec-1

3

13

ADDITIONAL IMPEDIMENTS AND RISKSThefinancialperformanceoftarsands

companiesinthecurrentmarketraises

concernsaswell.Theforwardlooking

riskscenariocontainslogistical,financial,

economic,andpoliticalrisks.Taken

individuallyandcumulativelytherisks

suggestthatthecurrentsoftnessin

companyprofitabilityislikelytocontinue.

TarsandsCAPEXspendingisclearly

facingchangingconditions.

TransportationbyrailTransportationbottlenecksdrivenby

marketforcesandpipelinecampaigns

havehadsignificantmaterialcostsfor

theindustry.Asaresult,somecompanies

areplacinggreateremphasisonrail

transport.Railaddsconsiderablytothe

overallcostforbitumen,acommoditythat

alreadytradesatadiscountedpricedue

tolowerquality.Thereisgrowingconcern

withinindustrycirclesthattransportation

bottleneckswillnotresolvethemselves.

In2014,Deloittestates:

Falling Oil Price

Since July of 2014, the price of all crude oils has been dropping

quite sharply. The U.S. oil boom together with a slowing in

global oil demand growth has fueled a glut in global supply,

which has resulted in a sharp drop in prices. In October of 2014

the price of Western Canada Select was in the mid $70 range,

a level that if maintained would present serious problems for

many tar sands producers. Investment analysts at Raymond

James wrote the following to clients in early October:

“If there is one segment of the Canadian oil sector that we

believe has most felt the squeeze in recent months it is likely

oil sands producers. Not only are falling oil prices weighing on

one of the higher costs of oil supply globally, but we believe

producers are beginning to feel the effects of meaningful cost

inflation in the region once again.”18

And the Financial Times noted:

“…a drop in revenues amid weaker margins would add to

pressure on oil companies that have already been battling

higher costs and a drop in capital expenditure may impact future

growth. Other various deepwater, arctic, international shale and

tar sands projects could also be sidelined.”19

Depressed oil prices harm company balance sheets in the short

term. The persistence of low oil prices sends a market signal that

further capex investment is less profitable and requires constant

reevaluation. In a period of tight revenue and margins oil

companies are more likely to drop marginal, high cost projects.

Further delays and cancellations of tar sands projects is a likely

outcome of these new market realities.

“It’s also still possible that outstanding

transportation projects like the Keystone

XL and Northern Gateway pipelines will

never break ground. Indeed, the majority

of a group of industry experts we

surveyed in mid-2013 expect that neither

pipeline will be built.”21

Transportofbitumenbyrailalsofaces

ahostofrisksaspreparationcostsfor

transportarecomplicated.Weather,

routecongestionandsafetyregulations

alsocreateadditionalriskfactors

(SeeBox:WhyRailisNottheAnswer

forTransportingTarSands).22

“The oil sands are probably the one challenging (sector)... There are a couple of headwinds against that business overall. The first is really global perception … it’s not viewed as a favorable investment in lots of places.”Dan Barclay, head of BMO Capital Markets

18 RaymondJamesCanadaResearchCanadianEnergyMidweek:A Story Of Divergence Within A Broader Theme Of Fear October8,201419 http://www.ft.com/intl/cms/s/0/691032d4-5053-11e4-9822-00144feab7de.html#axzz3G2H9DSM820 Hussain,Y.“Foreigninvestors‘scaredoff’fromtheoilsands,M&Aexpertsays.”The Financial Post,2014.http://business.financialpost.com/2014/06/24/foreign-investors-

scared-off-from-the-oil-sands-ma-expert-says/?__lsa=ae6b-849221 Deloitte.Gaining ground in the sands 2014: Five rites of passage for an industry in pursuit of operational maturity.p.5.http://www2.deloitte.com/content/dam/Deloitte/ca/

Documents/international-business/ca-en-ib-gaining-ground-in-the-sands-2014.pdf22 Stockman,L.,Wrong side of the tracks: why rail is not the answer to the tar sands market access problem.OilChangeInternational,2014.http://priceofoil.org/content/

uploads/2014/09/OCI-Wrong-Side-of-the-Tracks_Final.pdf

14

LegalaccesstotheresourceandtransportationroutesCanadianFirstNationshaveaunique

setofconstitutionallyrecognizedlegal

rightsthathaveimportantimplications

forgovernmentsinrelationtotarsands

andtarsandsinfrastructuredevelopment.

Thisincludesrightsthatcanconstrain

accesstoboththeresourceitselfaswellas

transportationroutes.

Recently,asanexample,FirstNations

inCanadafilednofewerthanninelegal

challengestothefederalgovernment’s

decisiontoapprovetheNorthernGateway

pipelineproject.25FirstNationclaims

relatedtotheEnbridgeNorthernGateway

pipelinehavecreatedsufficientheadwinds

tothepointwhereitiswidelyregarded

asbeingunbuildable.26Inadditionto

this,theCanadianGovernmentisfacing

variousconstitutionalchallengesfromFirst

Nationsandcivilsocietyorganizations

relatedtotarsandsandinfrastructure

expansionandrestrictivelegislative

changestothepublichearingprocess.

FirstNationsarealsomountinglegal

challengestotarsandsdevelopmentand

expansionontraditionalterritory.For

example,theAthabascaChipewyanFirst

Nation,whosetraditionalterritoryisrichin

tarsandsdeposits,are,“activelyengaged

inamulti-pronglegalstrategytochallenge

publicpolicy,individualtarsandsprojects

andinadequateenvironmentalprotection

inAlberta’sAthabascatarsandsregion.”27

Theabovearejustafewexamplesof

variousFirstNationsleadlegalinitiatives

inCanada.IntheUnitedStates,Nebraskan

landownershavesuccessfullyasserted

landrightsclaimsinthefaceofthe

KeystoneXLpipeline.28,29

Why Rail is Not the Answer for Transporting Tar Sands23

Tar sands proponents claim that blocking pipelines will

not impact production because the bitumen can go by rail

instead. However, the idea that rail can profitably deliver the

roughly 4 million bpd capacity of currently proposed pipelines

is uncertain at best. Rail is beset with capacity limitations,

financial uncertainty, and political opposition.

Industry officials are also concerned that the promise of rail

as a pipeline alternative is overstated. When Steve Hanlon,

President and CEO of Gibson Energy Inc., a company that

operates a number of crude-by-rail terminals including one that

loads tar sands bitumen in Alberta, said, “Crude by rail is not a

panacea. It’s not going to replace pipe,” he was right.

In fact shipping bitumen to the Gulf Coast by rail has been

losing money for much of 2014 and only shipments tied to

long-term contracts have made the 3,000 mile journey. In the

first five months of 2014, only about 45,000 bpd arrived at the

Gulf Coast by rail. This is less than six percent of the capacity

of the proposed Keystone XL pipeline. While another 80,000

bpd went to other parts of the U.S. by rail, the industry needs

a profitable multi-million barrel per day pathway to coastal

markets and rail simply is not it.

A combination of high costs and poor returns is working

against bitumen-by-rail being much more than a niche activity.

These are summarized as follows:

Gulf Coast crude oil prices are being suppressed by the flood

of crude from fracked oil fields across America. Prices for tar

sands crude on the Gulf Coast do not cover the additional cost

of shipping dilbit 3,000 miles by rail.

Rail is an above ground mode of transport that is vulnerable to

weather and other unpredictable delays. Tar sands producers

must compete for access to capacity with oil producers in

North Dakota as well as shippers of commodities such as grain,

coal and manufactured and imported goods. Unlike pipelines,

price and service is not locked into decade long contracts

and is vulnerable to inflation and disruption. In addition rail

congestion in the United States is already having a negative

impact on coal producers.24

Large-scale terminals need to be built to handle the quantity

of crude and load multiple unit trains per day.

Transporting raw bitumen can save producers the cost of

shipping the diluent required for pipeline transport. However,

no unit train terminal currently possess the equipment to load

large volumes of raw bitumen.

The reduced profitability of shipping bitumen by rail means

that tar sands producers are less able to grow their production

capacity because they cannot profitably deliver bitumen to

distant markets.

While the transport of tar sands bitumen by rail may grow to

accommodate near-term production growth plans, weaknesses

in investment scenarios and rail capacity suggest U.S. rail

networks are insufficiently positioned to absorb 4 million bpd

of new oil sands product.

23 Formoredetailsandallreferences,pleaseseeStockman,L.Wrong side of the tracks: why rail is not the answer to the tar sands market access problem.OilChangeInternational,2014.http://priceofoil.org/content/uploads/2014/09/OCI-Wrong-Side-of-the-Tracks_Final.pdf,

24 Cox,CharlotteandDarrenEpps,“PRBcoaldeliveriestoupperMidwesthitagaininQ2asrailissuespersist.”SNL.September9,2014.25 Lanelaa,M.“NorthernGatewaypipeline:FirstNationsoutlineconstitutionalchallenges.”TheCanadianBroadcastingCorporation,2014.http://www.cbc.ca/m/touch/news/

story/1.270637626 Moore,D.“Despitefederalapproval,NorthernGatewayfaceslegalandpoliticalhurdles.”TheCanadianPress,2014.http://www.theprovince.com/business/waits+federal+decision+N

orthern+Gateway+pipeline+proposal/9947153/story.html27 AthabascaChipewyanFirstNations.HonourtheTreaties.http://www.honourtheacfn.ca/28 Stueck,W.“B.C.FirstNationschallengeNorthernGatewaypipelineinnewcourtaction.”TheGlobeandMail,2014.http://www.theglobeandmail.com/news/british-columbia/first-

nations-challenge-northern-gateway-pipeline-in-new-court-action/article19608617/29 “NebraskajudgeblocksKeystoneXLroute.”AlJazeeraAmerica.February19,2014.http://america.aljazeera.com/articles/2014/2/19/nebraska-law-thatallowedkeystonexlstruckdown.

html

15

CanadianactiononforeignownershipIn2012,theCanadiangovernment

introducednewforeignownership

regulationsregardinginvestmentin

Canadianoilresources.Thelaws,designed

toprotectCanadafromforeigninfluence

hadtheimpactofrestrictingcapital

investmentintothecountryatatime

whencompanieswerelookingtoexpand

investmentinoilsands.

Thischangeandthehostofotherissues

createaworrisomeinvestmentclimate.

WilliamQuinn,headofmergerand

acquisitionsatTDSecuritiesstated,“Five

yearsago,theoilsandshadthegreatest

scopefornon-Canadianinvestmentsin

Canada.That’schangeddramatically.”30

Quinnwasprimarilyreferringtothenew

regulatoryframeworkthatwasputin

placein2012toprotectCanadianassets

fromforeignownership.Eachtransaction

involvingforeigncapitalisvettedbythe

governmenttoassurethatCanadian

interestsareprotected.Consequently,

capitalexpenditureisprovingexceedingly

challengingparticularlyforthejuniorsas

theyhavelessabilitytoaccessthecapital

marketsthandotheirlargerpeers.31The

newCanadianprotectionistlegislation

driedupcapitalalmostimmediately

forthissegment.Giventhattarsands

productionisverycapitalintensive,a

readyaccesstolargesumsofmoneyis

needed.Canadiancapitalmarketsare

simplynotlargeenoughtofundsuch

production.Someforeigncapitalis

necessarytoexploittheseassetsmaking

thisathornyissueforgovernmentofficials.

Thejuniorpartofthetarsandsindustryin

Canadaproduceslessthan25percentof

totalannualproduction.Therearehowever

severaldozencompaniesinthebusiness.

Astructuralweaknessforasignificant

segmentoftheindustryonlyunderscores

theexpectationthatplannedproduction

willbeslowtomarket.Persistentmarket

accessproblemsincreasesthepotential

foramarketshakeoutwithmergers,

buyouts,bankruptciesandotherevents

thatsuggestalessthanrobustproduction

increase.

CostinflationThesinglegreatestfactorplacingupward

pressureonproductioncostsistheremote

locationofmostoftheproductionsites.

Remotelocationsplaceapremiumon

labor,steelandcementcostsonboththe

constructionandoperationsside.

Growingmarketuncertaintyinthetar

sandsisexacerbatedbycostinflation.32

JeffLyons,apartneratDeloitteCanada,

stated:

“Oil sands are economically challenging

in terms of returns...Cost escalation is

causing oil sands participants to rethink

the economics of projects. That’s why

you’re not seeing a lot of new capital

flowing into oil sands.”33

Costcurves,carbonriskandstrandedassetsTarsandsareconsideredhighcost,mega

projectsthatcouldconceivablyprovide

returnsfordecades.Thislongterm

investmentscenarioiscloudedbylong

termcostincreasesandcarbonrisk.The

InternationalEnergyAgencyestimates

thatcapitalcosts,inrealterms,havemore

thandoubledsince2000inoil,gas,and

coalextraction.34

Examiningacostcurveanalysisby

JPMorgan,35itbecomesapparentthat

thevarioustarsandsprojectsinAlberta

havehighbreakevencostsassociated

withthem.Forinstance,onlytwoprojects,

ChristinaLakeandFosterCreekhave

breakevencostsinthe$50-60/barrel

range.Theoverwhelmingmajorityoftar

sandprojectsfallinthebreakevenrangeof

$70-100/barrel.

RecentanalysisbytheCarbonTracker

Initiative(CTI)36confirmsthatthetarsands

arehometothehighestriskoilplaysin

theworld,withsomeprojectsrequiring

crudepricesashighas$150perbarrelto

breakeven.CTIstates,“Inordertosustain

shareholderreturns,companiesshould

focusonlow-costprojects,deferringor

cancellingprojectswithhighbreak-even

costs.”37

Moreandmoreanalystsareconcerned

aboutpotentialdowngradesbasedon

strandedassets.Shouldglobaltargetsbe

putintoplaceforGHGemissions,many

hydrocarbonassetscurrentlyonthe

booksofoilandgascompanieswillnotbe

burned.Thismakesthemstrandedassets.

Tarsandswouldmostlikelybeatthetop

ofthislistduetotheirinherentlyhighGHG

emissionprofile.Deloitteacknowledged

suchapossibilityinits2014reportontar

sandswhenitstated,“...someanalystsare

predictingcreditdowngradesasaresult

ofrisingcarbonconstraints.”38

InMarch,2013,Standard&Poor’s

suggestedthatrisingcarbonconstraints

wouldalterthecreditqualityofmany

smallercompanies..S&Ppredicted,

“adeteriorationinthefinancialriskprofiles

of[smaller]companiestoadegreethat

wouldpotentiallyleadtonegativeoutlook

revisionsandthendowngradesover

2014-2017.”39

CarbonTrackerInitiativehasidentified

1.2trillionUSDofglobaloilinvestment

thatwillbecomestrandedassetsif

governmentsacttotackleclimatechange

accordingtoatwodegreeCentigrade

commitment.Ofthis1.2trillion,over

40percentisconcentratedinthe

Albertatarsands.40

30 Haggett,S.“Canadaenergydealsreboundasshaleplaystrumpoilsandsininvestors’eyes.”Reuters,July2,2014.http://business.financialpost.com/2014/07/02/canada-energy-deals-rebound-as-shale-plays-trump-oil-sands/?__lsa=ae6b-8492

31 “Junioroilsandsproducersremainblockedfromaccesstoproject-makingequitymarkets,whilenearly1.5millionbarrelsperdayofcapacityhangsinthebalance,”Oil Sands Review,August,2014.

32 Gutscher,Cecile.“OilSanddreamevaporateswithbondholdersfacing40%loss.”Bloomberg News,August25,2014.http://business.financialpost.com/2014/08/25/oil-sands-dream-evaporates-with-bondholders-facing-40-loss/?__lsa=ae6b-8492

33 YadullahHussain“Cost-cuttingfevergripsoilsandsplayersaseconomicscalledintoquestion”The National Post,August22,2014http://business.financialpost.com/2014/08/22/fp-energy-aug-22-cost-cutting-fever/?__lsa=6b9e-9dfe

34 InternationalEnergyAgency.World energy investment outlook 2014 factsheet overview.2014.http://www.iea.org/media/140603_WEOinvestment_Factsheets.pdf35 CarbonTrackerInstitute,“CarbonSupplyCostCurves:Evaluatingfinancialrisksofoilcapitalexpenditures”,CTI,May2014,p.2136 CarbonTrackerInitiative.“Oil&gasmajors:FactSheets.”2014http://www.carbontracker.org/site/wp-content/uploads/2014/08/CTI_Oil_Gas_Majors_Company_Factsheets_

August_2014_FULL.pdf37 CarbonTrackerInitiative.“Oil&gasmajors:FactSheets.”2014http://www.carbontracker.org/site/wp-content/uploads/2014/08/CTI_Oil_Gas_Majors_Company_Factsheets_

August_2014_FULL.pdf38 Deloitte.Gaining ground in the sands 2014: Five rites of passage for an industry in pursuit of operational maturity.39 Standard&Poor’sRatingsServices.“WhatACarbon-ConstrainedFutureCouldMeanForOilCompanies’Creditworthiness.”March1,2013.40 CarbonTrackerInitiative.Carbon supply cost curves: Evaluating financial risk to oil capital expenditures.May2014.http://www.carbontracker.org/wp-content/uploads/2014/09/CTI-

Oil-Report-Oil-May-2014-13-05.pdf

16

Strandedassetsareofincreasingconcern

toinvestors,arecentinitiativesawover70

institutionalinvestorsrepresenting3trillion

USDinassetsrequest45companiesto

calculatetherisksofextractingso-called

unburnablecarbon.41Whilecompanies

areslowtorespondtoacknowledgethese

risks,thepressureisclearlygrowing.42

Themediumandlongterminstitutional

actionsthatcloudlongtermoiland

gasinvestmentscenariosstemfrom:

internationalagreementstorestrict

carbon,nationalgovernmentactions

respondingtoclimatechange,broad

privatesectorconsensustoshift

capitaltolowcarboninvestmentsand

continuedtargetingofcompanies,

lendinginstitutionsandgovernmentsby

demandingrestrictionsoncarbonuse.43

EnvironmentalandotherregulatoryrisksInadditiontoclimateandcarbon

law,increasedregulationrelatedto

environmentalandpublichealthprotection

aswellasenforcementrepresentadditional

constraintsonthefutureoftarsands

profitabilitygoingforward.Although

Canadianlawandenforcementhas

historicallysoughttoprovidealowcost

environmentforinvestment,heightened

scrutinyandpressurestemmingfrom

increasedpublicawarenessfornew

lawsandenforcementofexistinglaws

isgrowing.Somenotableareaswhere

increasedregulations,stringency,and

enforcementshouldbeexpectedare:

fWateruseandadversewaterquality

impacts;44

fLanduseandminingreclamation;45

fLackofcompliancewithlocalair

pollutionstandards,particularlyfor

sulfurdioxide,nitrogendioxideand

particulates;46

fHumanhealthimpactsfromtarsands

chemicalsleakingfromtailingslakes,as

wellasairbornechemicals;47

fLackofcompliancewithtailings

managementagreements;48,49

fIncreasedregulationandstringencyto

preventrailspillsandotheraccidents.50

Amorerobustandstringentregulatory

environmentwillalsoraisecostsand

reducetarsand’scompanies’profit

margins.

RISING COSTS AND CANCELLED PROJECTS Thehurdlestogrowthoutlinedinthe

abovesectionsarealteringtheoutlook

regardingfutureproduction.Recently

theCanadianAssociationofPetroleum

Producershasrevisitedits2030

productionforecast,downgradingits

tarsandsforecastfrom5.2millionbpd

by2030to4.8millionbpd.51Therevised

forecaststillassumesmediumterm

resolutionoftransportationbottlenecks,

butthedownwardforecastadjustment

fromCanada’sleadingoilandgastrade

associationandindustryadvocateisa

significantconcessiontomountingmarket

realities.Interestedreaderswillnotethat

thisrevisionwaspublishedonemonthprior

tothecurrentdeclineinoilprices.

Chineseoilcompaniesarealsoreviewing

theirinvestments.Manyoftheirprojects

havemetwithsignificantdelays,soaring

operationalexpenses,andweakreturns

–withexpertsconfirmingthatthereare

strongfeelingsof,“buyer’sremorse”

followingover$30billionininvestmentsin

recentyears.52Twomajorminingprojects

andoneinsituprojecthavebeencanceled

(formally“putonhold”)thisyearand

anothermajorminingprojectremains

unsanctionedamidskepticismthatitcan

bemadeviable.Dozensofotherplanned

tarsandsprojectshanginthebalance

asproducersstruggletocontainrising

costswhilewaitingtoseeiftransportation

constraintswilleverbesolved.

CapexisdeclininginthetarsandsInthecurrentmarketcontextCapital

Expenditure(Capex)inthetarsandsis

anindicatorofnotonlyinvestmentbut

alsoconfidenceinthefutureofthesector.

From2000Capexinthesectorgrew

steadilyuntil2006whenittailedoffand

thendippedsharplyduringthefirstfull

yearoftherecessionin2009.Since2010,

Capexhasgrownvigorouslyagain,partly

duetotheconfidenceinfutureproject

profitabilityandpartlyduetotherisingper

barrelcostofproduction.However,inthe

lastyeartherapidriseintarsandsCapex

ofrecentyearshasplateauedandbegun

todecline.

AccordingtotheAlbertaEnergyRegulator

(AER)oilsandscapitalexpenditurepeaked

in2012at$27.2billionCAD,decreasedto

$24.2billionCADin2013,andispredicted

todecreasefurtherto$23.7billionCAD

in2014.53

Recently,themarketpriceforoilhas

declinedtoalevelthatisbelowthe

breakevenpriceofmanyproposedtar

sandsprojects.TheAERreportedinMay

2014thattheaverageWTIoilpriceneeded

fortarsandscommercialityin2013wasup

$5perbarrelforin-situproductionandup

to$20perbarrelhigherforminingover

2012.54AccordingtotheAER,theWTI

pricenowneededforatarsandsmining

projecttoturnaprofitis$105/bbl.WTI

41 Douglass,Elizabeth.“Investorgrouppressescompanieson‘unburnablecarbon’.”Inside Climate News. October24,2013.http://www.bloomberg.com/news/2013-10-24/investor-group-presses-oil-companies-on-unburnable-carbon-.html

42 ThemostimportantdiscussioninthisareaisoccurringbetweenCarbonTrackerInitiativeandShellOil,See:http://s02.static-shell.com/content/dam/shell-new/local/corporate/corporate/downloads/pdf/investor/presentations/2014/sri-web-response-climate-change-may14.pdfandtheCarbonTrackerresponse:http://www.carbontracker.org/wp-content/uploads/2014/07/CTI_Shell_Response_Final_030714_Full2.pdf

43 Fenton,Cameron.“Howstudentsareleadingthefightagainstclimatechange.”The Huffington Post.March28,2013.http://www.huffingtonpost.ca/cameron-fenton/student-climate-change_b_2967164.html

44 EnvironmentalDefence.“Realitycheck:waterandthetarsands.”AccessedonOctober6,2014:http://environmentaldefence.ca/realitycheck45 OilSandsRealityCheck,Oil Sands Reality Check Website.AccessedonOctober6,2014:http://oilsandsrealitycheck.org/factcategory/land-species/46 EnvironmentalDefence.“Realitycheck:waterandthetarsands.”AccessedonOctober6,2014:http://environmentaldefence.ca/realitycheck47 Cotter,John.“EnvironmentalhealthrisksofAlbertaoilsandslikelyunderestimated:study.”The Globe and Mail,February3,2014.http://www.theglobeandmail.com/news/national/

environmental-health-risks-of-alberta-oilsands-probably-underestimated-study/article16667569/48 Cryderman,Kelly.“Oilsandsfirmswarnedontailingsponds.”The Globe and Mail,June12,2013.http://www.theglobeandmail.com/report-on-business/industry-news/energy-and-

resources/oil-sands-firms-warned-on-tailings-ponds/article12485574/49 McKinnon,Hannah.“Failingontailings–again.”Environmental Defence,February21,2014.http://environmentaldefence.ca/blog/failing-tailings-%E2%80%93-again50 Philips,Matthew.“Trainsthatgoboom.”Bloomberg Businessweek,February13,2014.http://www.businessweek.com/articles/2014-02-13/oil-train-explosions-u-dot-s-dot-regulators-

slow-to-react51 Howell,David.“CAPPtripsoilsandsproductionnumbersinlatestcrudeforecast.”Edmonton Journal,June9,2014.http://www.edmontonjournal.com/CAPP+trims+oilsands+producti

on+numbers+latest+crude+forecast/9922760/story.html52 Jones,Jeffrey.“ChinafacesbuyersremorseinCanada’soilpatch.”TheGlobeandMailAugust17,2014.http://www.bnn.ca/News/2014/8/17/China-faces-buyers-remorse-in-Canadas-

oil-patch.aspx53 http://www.aer.ca/documents/sts/ST98/ST98-2014.pdfp1-16AERforeseesaCapexrecoveryin2016,butthatisbasedonoptimismregardingtheresolutionofmarketaccessissues

andahigheroilprice.54 AlbertaEnergyRegulator.ST98-2014:Alberta’sEnergyReserves2013andSupply/DemandOutlook2014–2023.2014.Pg.3-26.http://www.aer.ca/documents/sts/ST98/ST98-2014.

17

hasbeenbelow$100/bblsinceAugust1,

2014andattimeofwriting(mid-October)

istradingat$85/bbl.Inthelast18months

WTIhasbeenover$105/bblforroughlya

monthtotal.

InlateJulyof2014,Suncor,thetoptar

sandsproducer,announcedanadditional

reductionof$1billioninplannedCapex

for2014.55SimilarlyCanadianOilSands

droppeditsfirsthalf2014capital

expenditureby$99millioncomparedwith

thefirsthalfof2013.56

Whilefallingoilpricesandrisksfor

increasedcostsonavarietyoffronts

clearlyplayarole,it’salsoclearthatdelays

insolvingthemarketaccessproblem–

completingpipelines–hascausedachillin

theinvestmentclimateinAlberta.InMayof

2014theCEOofURS,aconstructionand

engineeringfirmheavilyinvolvedinthetar

sandsnotedonanearningscallthat:

“In the first quarter, Oil & Gas revenues

were $758 million, a 6% decrease from

the same period last year. Uncertainty of

a takeaway capacity and the decision of

the -- uncertainty of the decision with the

Keystone XL pipeline is causing some of

our Canadian customers to delay capital

expenditure programs.”57

Themostconcretesignofthechangein

weatherfortarsandsproducersisthe

waveofprojectcancellationsthathasjust

started.

CancelledprojectsLackofmarketaccess,causedinlarge

partbypublicaccountabilityactions

drivenbypipelinecampaigns,hasplayeda

significantroleinthecancellationofthree

majortarsandsprojectsin2014alone-

Shell’sPierreRiver,Total’sJoslynNorth,

andStatoil’sCornerProject.

Twoofthesearelargetarsandsmines

thathavebeenplannedforyears-Royal

DutchShell’sPierreRiverMineandTotal

SA’sJoslynMine.Inaddition,oneof

Statoil’sinsituprojectswasalsocanceled

inSeptember.Thislastisofparticularnote

becauseofthegenerallymorefavorable

economicsenjoyedbyin-situprojects.

Whiletheindustryreferstoallthree

technicallyas“onhold”,wedonotforesee

marketconditionschangingtothedegree

necessarytorestartthesehugeprojects.

Inannouncingthecancellationofthe

CornerProject,aStatoilspokesman

notedthat:

“Costs for labour and materials have

continued to rise in recent years and are

working against the economics of new

projects. Market access issues also play

a role - including limited pipeline access

which weighs on prices for Alberta oil,

squeezing margins and making it difficult

for sustainable financial returns.”58

InFebruary2014,Shellannouncedthat

ithadwithdrawnitsongoingapplication

forapermitforthe200,000bpdPierre

RiverMine.Theproject’sapplicationhad

beeninprocesssincelate2007.Themine

wouldhavedisturbedover10,000hectares

andislocatedacrosstheAthabascaRiver

fromShell’songoingMuskegRiverand

Jackpineminingoperations.Chevronand

MarathonOilareminoritypartnersinall

threeprojects.

PierreRiverproductionwasestimated

topeakinthe2030sand40sataround

120,000bpdwithatotalofalmost1.5

billionbarrelsofbitumenproducedduring

itslifetime.59Producing,processingand

consumingthatbitumenwouldhavesent

anestimatedtotalof~900milliontonnesof

CO2intotheatmosphere.

55 http://www.suncor.com/en/newsroom/5441.aspx?id=186374056 http://www.marketwatch.com/story/canadian-oil-sands-announces-second-quarter-results-and-a-035-per-share-dividend-2014-07-31-16173531357 URSCEOMartinKoffelonQ12014Results-EarningsCallTranscript

May.13,2014http://seekingalpha.com/article/2216113-urss-urs-ceo-martin-koffel-on-q1-2014-results-earnings-call-transcript?page=258 http://www.statoil.com/en/NewsAndMedia/News/2014/Pages/25Sept_CornerPostponement.aspx59 RystadEnergy.UCube Database.(Sept.2014).60 Lewis,Jeff.“TotalSAsuspends$11BJoslynoilsandsmineinAlberta,laysoffupto150staff.”The National Post.May29,2014.http://business.financialpost.com/2014/05/29/total-sa-

suspends-11b-joslyn-oil-sands-mine-in-alberta-lays-off-up-to-150-staff/?__lsa=6798-9b3361 RystadEnergy.UCube Database.(Sept.2014).62 Tait,Carrie.“Totalshelves$11billionAlbertatarsandsmine.”The Globe and Mail.May29,2014.http://www.theglobeandmail.com/report-on-business/joslyn/article18914681/63 RystadEnergy.UCube Database.(Sept.2014).64 Lewis,Jeff.“SinopecmaybackawayfromNorthernLightstarsandslease:source.”The National Post,July9,2014.http://business.financialpost.com/2014/07/09/sinopec-may-back-

away-from-northern-lights-oil-sands-lease-source/?__lsa=6798-9b3365 SynencoEnergyInc.“NorthernLights,OilsandsMiningandExtractionProject:PublicDisclosureDocument,ProjectUpdate.”October2005.http://environment.alberta.ca/

documents/Synenco_Energy_Northern-Lights-Oil-Sands-Mine_PDD.pdf66 Lewis,Jeff.“SinopecmaybackawayfromNorthernLightstarsandslease:source.”The National Post,July9,2014.http://business.financialpost.com/2014/07/09/sinopec-may-back-

away-from-northern-lights-oil-sands-lease-source/?__lsa=6798-9b3367 RystadEnergy.UCube Database.(Sept.2014).NotethatRystadEnergymetricscategorizetheseprojectsasUncommercial.

InMay2014,Totalannouncedthatitwas

puttingtheCAD11billionJoslynMineon

indefinitehold.Theprojectwasapproved

bytheAlbertaregulatorin2011andwas

expectedtobeginproducing100,000bpd

in2020.60Totalwastheleadoperatorwith

partnersSuncor,OccidentalandInpex

Canada.OverUSD400millionhasbeen

spentontheminesofar.61AndreGoffart,

headofTotal’sCanadiandivisionstatedin

apressconferencethat:

“Joslyn is facing the same challenge

most of the industry world-wide [is],

in the sense that costs are continuing

to inflate when the oil price and

specifically the netbacks for the tar

sands are remaining stable at best –

squeezing the margins”.62

Theproject’sproductionwouldhave

peakedinthe2040sataround155,000

bpd.63By2100,theprojectcouldhave

producedover1.9billionbarrelsof

bitumen.Producing,processingand

consumingthatbitumenwouldhavesent

atotalof1.1billiontonnesofCO2intothe

atmosphere.

SinopecandTotal’sNorthernLightsproject

isanotherprojectatriskofcancellation.64

Themineboastsover1billionbarrelsof

recoverablebitumenandwasinitially

scheduledtostartoperationsin2010witha

capacityof100,000bpd.65Ananalysttold

Canada’sNationalPostinJuly2014that

Sinopec“ishavingtroublewithNorthern

Lightslikeeverybodyelse,”[…]“Youcan’t

throwmoneyintoablackholeforever.”66

Independentestimatesoftheproject

financesshowitfailstomeetprofitability

standards.67Projectviabilitycouldbe

enhancedifcostsdecreaseoralong-term

turnaroundinoilpricesoccurs.Thereis

nosignofeitherdevelopmentinthenear

future.

18

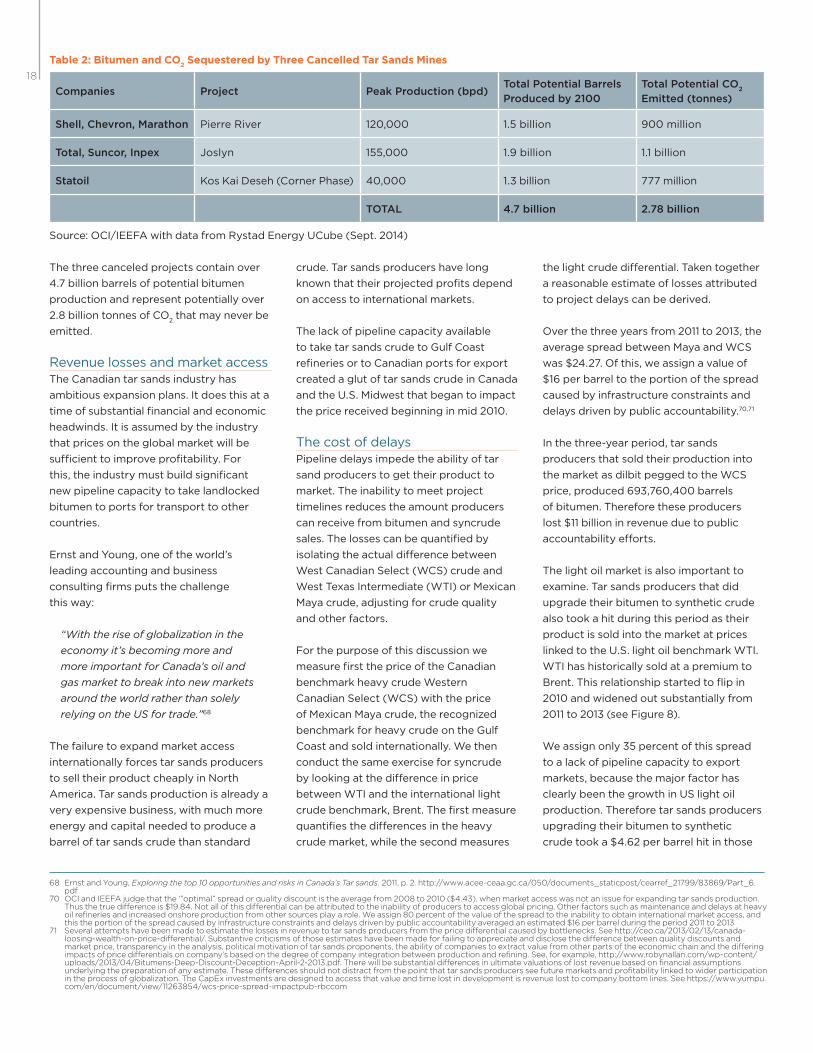

Thethreecanceledprojectscontainover

4.7billionbarrelsofpotentialbitumen

productionandrepresentpotentiallyover

2.8billiontonnesofCO2thatmayneverbe

emitted.

RevenuelossesandmarketaccessTheCanadiantarsandsindustryhas

ambitiousexpansionplans.Itdoesthisata

timeofsubstantialfinancialandeconomic

headwinds.Itisassumedbytheindustry

thatpricesontheglobalmarketwillbe

sufficienttoimproveprofitability.For

this,theindustrymustbuildsignificant

newpipelinecapacitytotakelandlocked

bitumentoportsfortransporttoother

countries.

ErnstandYoung,oneoftheworld’s

leadingaccountingandbusiness

consultingfirmsputsthechallenge

thisway:

“With the rise of globalization in the

economy it’s becoming more and

more important for Canada’s oil and

gas market to break into new markets

around the world rather than solely

relying on the US for trade.”68

Thefailuretoexpandmarketaccess

internationallyforcestarsandsproducers

toselltheirproductcheaplyinNorth

America.Tarsandsproductionisalreadya

veryexpensivebusiness,withmuchmore

energyandcapitalneededtoproducea

barreloftarsandscrudethanstandard

Companies Project Peak Production (bpd)Total Potential Barrels

Produced by 2100

Total Potential CO2

Emitted (tonnes)

Shell, Chevron, Marathon PierreRiver 120,000 1.5billion 900million

Total, Suncor, Inpex Joslyn 155,000 1.9billion 1.1billion

Statoil KosKaiDeseh(CornerPhase) 40,000 1.3billion 777million

TOTAL 4.7 billion 2.78 billion

crude.Tarsandsproducershavelong

knownthattheirprojectedprofitsdepend

onaccesstointernationalmarkets.

Thelackofpipelinecapacityavailable

totaketarsandscrudetoGulfCoast

refineriesortoCanadianportsforexport

createdaglutoftarsandscrudeinCanada

andtheU.S.Midwestthatbegantoimpact

thepricereceivedbeginninginmid2010.

ThecostofdelaysPipelinedelaysimpedetheabilityoftar

sandproducerstogettheirproductto

market.Theinabilitytomeetproject

timelinesreducestheamountproducers

canreceivefrombitumenandsyncrude

sales.Thelossescanbequantifiedby

isolatingtheactualdifferencebetween

WestCanadianSelect(WCS)crudeand

WestTexasIntermediate(WTI)orMexican

Mayacrude,adjustingforcrudequality

andotherfactors.

Forthepurposeofthisdiscussionwe

measurefirstthepriceoftheCanadian

benchmarkheavycrudeWestern

CanadianSelect(WCS)withtheprice

ofMexicanMayacrude,therecognized

benchmarkforheavycrudeontheGulf

Coastandsoldinternationally.Wethen

conductthesameexerciseforsyncrude

bylookingatthedifferenceinprice

betweenWTIandtheinternationallight

crudebenchmark,Brent.Thefirstmeasure

quantifiesthedifferencesintheheavy

crudemarket,whilethesecondmeasures

thelightcrudedifferential.Takentogether

areasonableestimateoflossesattributed

toprojectdelayscanbederived.

Overthethreeyearsfrom2011to2013,the

averagespreadbetweenMayaandWCS

was$24.27.Ofthis,weassignavalueof

$16perbarreltotheportionofthespread

causedbyinfrastructureconstraintsand

delaysdrivenbypublicaccountability.70,71

Inthethree-yearperiod,tarsands

producersthatsoldtheirproductioninto

themarketasdilbitpeggedtotheWCS

price,produced693,760,400barrels

ofbitumen.Thereforetheseproducers

lost$11billioninrevenueduetopublic

accountabilityefforts.

Thelightoilmarketisalsoimportantto

examine.Tarsandsproducersthatdid

upgradetheirbitumentosyntheticcrude

alsotookahitduringthisperiodastheir

productissoldintothemarketatprices

linkedtotheU.S.lightoilbenchmarkWTI.

WTIhashistoricallysoldatapremiumto

Brent.Thisrelationshipstartedtoflipin

2010andwidenedoutsubstantiallyfrom

2011to2013(seeFigure8).

Weassignonly35percentofthisspread

toalackofpipelinecapacitytoexport

markets,becausethemajorfactorhas

clearlybeenthegrowthinUSlightoil

production.Thereforetarsandsproducers

upgradingtheirbitumentosynthetic

crudetooka$4.62perbarrelhitinthose

Table 2: Bitumen and CO2 Sequestered by Three Cancelled Tar Sands Mines

Source:OCI/IEEFAwithdatafromRystadEnergyUCube(Sept.2014)

68 ErnstandYoung,Exploring the top 10 opportunities and risks in Canada’s Tar sands.2011,p.2.http://www.acee-ceaa.gc.ca/050/documents_staticpost/cearref_21799/83869/Part_6.pdf

70 OCIandIEEFAjudgethatthe‘”optimal”spreadorqualitydiscountistheaveragefrom2008to2010($4.43),whenmarketaccesswasnotanissueforexpandingtarsandsproduction.Thusthetruedifferenceis$19.84.Notallofthisdifferentialcanbeattributedtotheinabilityofproducerstoaccessglobalpricing.Otherfactorssuchasmaintenanceanddelaysatheavyoilrefineriesandincreasedonshoreproductionfromothersourcesplayarole.Weassign80percentofthevalueofthespreadtotheinabilitytoobtaininternationalmarketaccess,andthistheportionofthespreadcausedbyinfrastructureconstraintsanddelaysdrivenbypublicaccountabilityaveragedanestimated$16perbarrelduringtheperiod2011to2013

71 Severalattemptshavebeenmadetoestimatethelossesinrevenuetotarsandsproducersfromthepricedifferentialcausedbybottlenecks.Seehttp://ceo.ca/2013/02/13/canada-loosing-wealth-on-price-differential/.Substantivecriticismsofthoseestimateshavebeenmadeforfailingtoappreciateanddisclosethedifferencebetweenqualitydiscountsandmarketprice,transparencyintheanalysis,politicalmotivationoftarsandsproponents,theabilityofcompaniestoextractvaluefromotherpartsoftheeconomicchainandthedifferingimpactsofpricedifferentialsoncompany’sbasedonthedegreeofcompanyintegrationbetweenproductionandrefining.See,forexample,http://www.robynallan.com/wp-content/uploads/2013/04/Bitumens-Deep-Discount-Deception-April-2-2013.pdf.Therewillbesubstantialdifferencesinultimatevaluationsoflostrevenuebasedonfinancialassumptionsunderlyingthepreparationofanyestimate.Thesedifferencesshouldnotdistractfromthepointthattarsandsproducersseefuturemarketsandprofitabilitylinkedtowiderparticipationintheprocessofglobalization.TheCapExinvestmentsaredesignedtoaccessthatvalueandtimelostindevelopmentisrevenuelosttocompanybottomlines.Seehttps://www.yumpu.com/en/document/view/11263854/wcs-price-spread-impactpub-rbccom

19

Jan 03 Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15

20

10

0

(10)

(20)

(30)

(40)

(50)

US

$/b

bl

Maya - WTI WCS - WTI

Transportation bottlenecks led to inland crude price discounts relative to waterborn crude

Source:BaytexEnergyCorp.69

Figure 7. Price Differential between Maya, WTI, and WCS ($/bbl), Over Preceding Decade

69 BaytexEnergyCorp,Presentation“EnerCom’sTheOil&GasConference.”August17-21,2014,Slide25.http://www.enercominc.com/downloads_TOGC_2014/Baytex-Energy.pdf72 Theaveragespreadbetween2000and2009was$2.15perbarrelinfavorofWTI.From2010to2013itwas$11.05infavorofBrent.Thedifferenceis$13.19.

fouryears.Inthatperiodtheyproduced

1.3billionbarrelsofsyntheticcrude.The

lossduetopublicaccountabilityfrom

2010-2013amountsto$6.1billion.Public

accountabilityintheformofpipeline

campaignshasbeenamajorfactorin

reducingrevenuestotarsandsproducers.

Overall,tarsandsproducerslost$30.9

billionbetween2010-2013duetowider

pricedifferentialscausedbytransportation

bottlenecksandthefloodofcrudecoming

fromtightoilfields.Ofthat,$17.1billion

or55percentcanbecrediblyattributed

totheimpactofpublicaccountability

campaigns.

0

20

40

60

80

100

120

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Brent WTI

Thisisasignificantimpact,andithas

causedcancelledprojects,slowed

expansion,andavoidedemissions.As

concernoverclimatecontinuestogrow,

thesepublicaccountabilitycampaigns,

andtheirimpactsontarsandsexpansion,

willalsogrow.

Figure 8: Brent-WTI Spread 2000 – 201372

Source:Bloomberg

20

Tarsandsproductionislandlocked.

Expansionoftransportinfrastructure

isessentialtoproductiongrowth.The

KeystoneXLcampaignhas,todate,

delayedthispipelineprojectforoverfive

years.AdditionalpipelinestoCanadian

portsarealsodelayed.Thedelayshave

costproducersmoneyandtime,reducing

thepricetheyhavereceivedfortarsands

crudeassupplyhasoutpacedthecapacity

oftransportinfrastructuretocarrytar

sandscrudetonewmarkets.

Tarsandsindustryestimatesarefocused

onalargebuildoutofprojectsinthe

faceofdeterioratingfinancialconditions.

Variousforecastsexpecttarsands

productiontomorethandoubleby2030

andtheindustryplansfurtheraggressive

growthinthedecadesthatfollow.

Butpublicquestioningofthislevelof

growthwillcertainlycontinue.Ifopposition

totarsandsinfrastructurecontinuesto

besuccessful,itcouldleadtodozensof

projectcancellations,severalbillionbarrels

ofbitumenleftinthegroundandbillions

oftonnesofcarbondioxideaverted.

Thissectionusesindustrydatamodels

toestimatewhattheimpactofcontinued

campaignsuccessmightbe.The

conclusionsshouldbothtriggerserious

questionsforinvestorsandencourage

thoseopposingthetarsandsthattheir

effortswillleadtosignificantcarbon

savings.

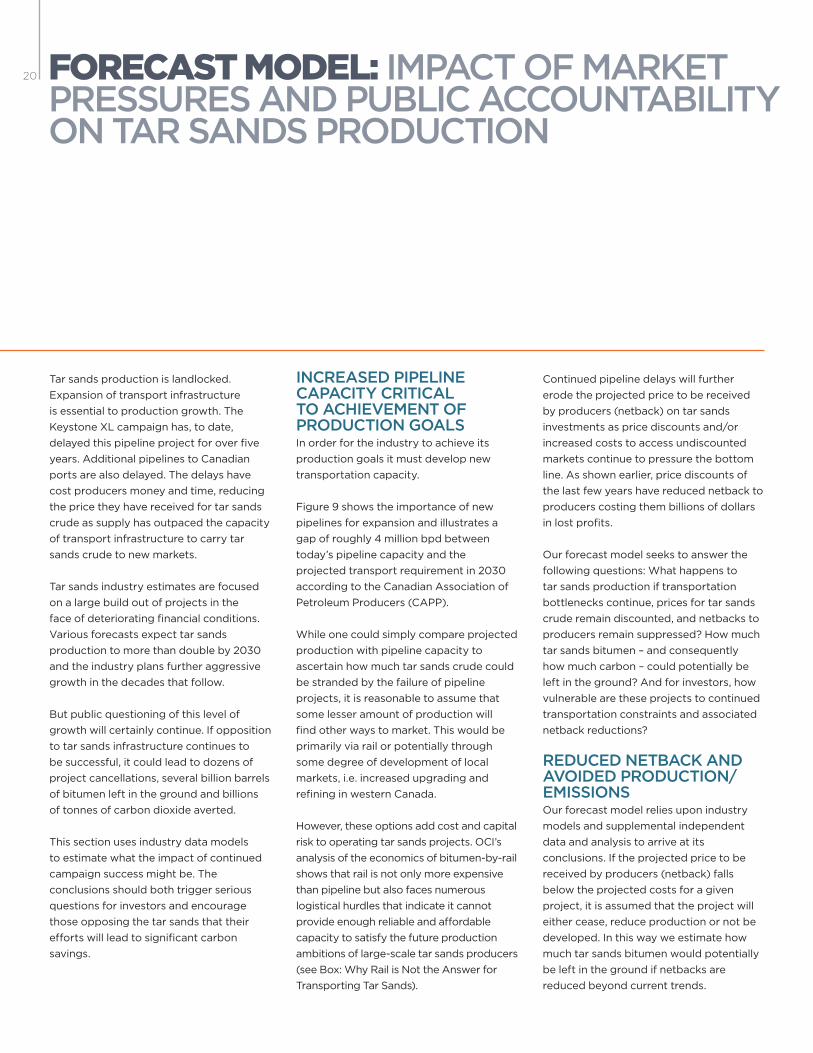

INCREASED PIPELINE CAPACITY CRITICAL TO ACHIEVEMENT OF PRODUCTION GOALS Inorderfortheindustrytoachieveits

productiongoalsitmustdevelopnew

transportationcapacity.

Figure9showstheimportanceofnew

pipelinesforexpansionandillustratesa

gapofroughly4millionbpdbetween

today’spipelinecapacityandthe

projectedtransportrequirementin2030

accordingtotheCanadianAssociationof

PetroleumProducers(CAPP).

Whileonecouldsimplycompareprojected

productionwithpipelinecapacityto

ascertainhowmuchtarsandscrudecould

bestrandedbythefailureofpipeline

projects,itisreasonabletoassumethat

somelesseramountofproductionwill

findotherwaystomarket.Thiswouldbe

primarilyviarailorpotentiallythrough

somedegreeofdevelopmentoflocal

markets,i.e.increasedupgradingand

refininginwesternCanada.

However,theseoptionsaddcostandcapital

risktooperatingtarsandsprojects.OCI’s

analysisoftheeconomicsofbitumen-by-rail

showsthatrailisnotonlymoreexpensive

thanpipelinebutalsofacesnumerous

logisticalhurdlesthatindicateitcannot

provideenoughreliableandaffordable

capacitytosatisfythefutureproduction

ambitionsoflarge-scaletarsandsproducers

(seeBox:WhyRailisNottheAnswerfor

TransportingTarSands).

Continuedpipelinedelayswillfurther

erodetheprojectedpricetobereceived

byproducers(netback)ontarsands

investmentsaspricediscountsand/or

increasedcoststoaccessundiscounted

marketscontinuetopressurethebottom

line.Asshownearlier,pricediscountsof

thelastfewyearshavereducednetbackto

producerscostingthembillionsofdollars

inlostprofits.

Ourforecastmodelseekstoanswerthe

followingquestions:Whathappensto

tarsandsproductioniftransportation

bottleneckscontinue,pricesfortarsands

cruderemaindiscounted,andnetbacksto

producersremainsuppressed?Howmuch

tarsandsbitumen–andconsequently

howmuchcarbon–couldpotentiallybe

leftintheground?Andforinvestors,how

vulnerablearetheseprojectstocontinued

transportationconstraintsandassociated

netbackreductions?

REDUCED NETBACK AND AVOIDED PRODUCTION/EMISSIONSOurforecastmodelreliesuponindustry

modelsandsupplementalindependent

dataandanalysistoarriveatits

conclusions.Iftheprojectedpricetobe

receivedbyproducers(netback)falls

belowtheprojectedcostsforagiven

project,itisassumedthattheprojectwill

eithercease,reduceproductionornotbe

developed.Inthiswayweestimatehow

muchtarsandsbitumenwouldpotentially

beleftinthegroundifnetbacksare

reducedbeyondcurrenttrends.

FORECAST MODEL: IMPACT OF MARKET PRESSURES AND PUBLIC ACCOUNTABILITY ON TAR SANDS PRODUCTION

21

74 RystadEnergyUCube(Sept.2014)73 BasedonCanadianAssociationofPetroleumProducers(CAPP),“CrudeOil:Forecasts,Markets&Transportation.”June2014.http://www.capp.ca/getdoc.

aspx?DocId=247759&DT=NTV75 RystadEnergy.UCube(Sept.2014).

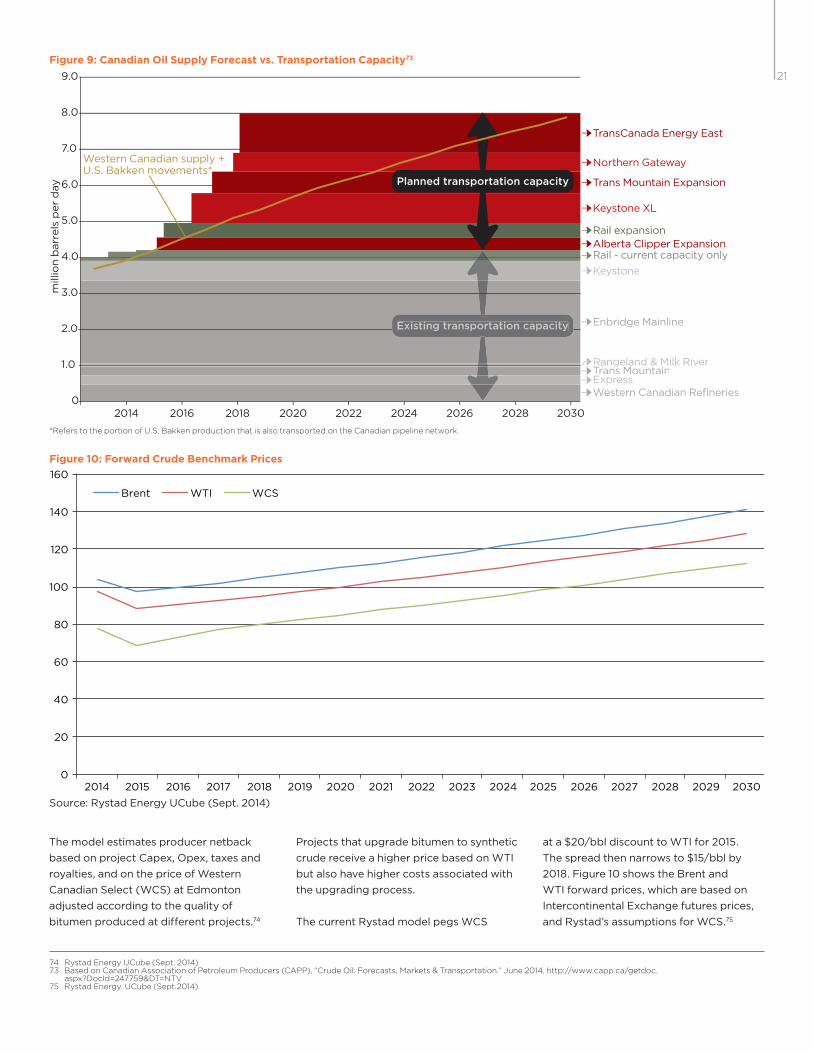

Themodelestimatesproducernetback

basedonprojectCapex,Opex,taxesand

royalties,andonthepriceofWestern

CanadianSelect(WCS)atEdmonton

adjustedaccordingtothequalityof

bitumenproducedatdifferentprojects.74

Projectsthatupgradebitumentosynthetic

crudereceiveahigherpricebasedonWTI

butalsohavehighercostsassociatedwith

theupgradingprocess.

ThecurrentRystadmodelpegsWCS

ata$20/bbldiscounttoWTIfor2015.

Thespreadthennarrowsto$15/bblby

2018.Figure10showstheBrentand

WTIforwardprices,whicharebasedon

IntercontinentalExchangefuturesprices,

andRystad’sassumptionsforWCS.75

Existing transportation capacity

Planned transportation capacity

0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Western Canadian supply + U.S. Bakken movements*

202420222020201820162014

mill

ion b

arr

els

per

day

203020282026

TransCanada Energy East

Trans Mountain Expansion

Northern Gateway

Alberta Clipper Expansion

Keystone XL

Rail expansion

Western Canadian RefineriesExpressTrans Mountain

Enbridge Mainline

Keystone

Rail - current capacity only