Master Thesis Agile Organizations - CORE SE · leading to a potential increase in flexibility and...

60

Agile Organizations How can financial service institutions embrace agility in their organizations? September 2016 Master Thesis – Novancia Business School Paris Copyright © COREtransform GmbH Nico Malena

Transcript of Master Thesis Agile Organizations - CORE SE · leading to a potential increase in flexibility and...

Agile Organizations

How can financial service institutions embrace agility in their organizations?

September 2016 Master Thesis – Novancia Business School Paris Copyright © COREtransform GmbH

Nico Malena

Master Thesis Nico Malena © CORE 2016 II

Abstract

The financial service industry is facing significant structural change. Digitalization, as one major

driver, offers almost endless opportunities to existing players and new market entrants, as given

entry barriers are challenged. The changes in consumer behavior can be leveraged by an

established financial institution to maintain or even improve its current position, if its organization

is capable to adopt accordingly. New market entrants have the advantage of being flexible,

whereas existing institutions are bound to their rigid structures. Agile, created as a project

management methodology, could be a possible solution for existing institutions in establishing the

required capabilities throughout an entire organization and making up for a lack of flexibility.

Thus, this study is motivated by the following research question: How can financial service

institutions embrace agility in their organizations? Based on one-to-one interviews with

experienced professionals, differentiating case examples are discussed and the challenges

leading to a potential increase in flexibility and speed are addressed. Additionally, the common

principles of Agile will be expanded upon and placed into the perspective of an organization driven

by technology.

Master Thesis Nico Malena © CORE 2016 III

Table of Contents

Abstract ........................................................................................................................................II

List of Figures .............................................................................................................................. V

List of Tables ............................................................................................................................... V

List of Abbreviations ................................................................................................................... VI

1 Introduction ..............................................................................................................................1

2 Structural Change ....................................................................................................................3

2.1 Technological Developments and Customer Behavior....................................................3

2.2 Regulatory Changes and Market Liberalization ..............................................................6

2.3 Industry Disruption and Competitive Landscape .............................................................8

2.4 Conclusion: The Need to Adapt .................................................................................... 10

3 Can Agile be a Solution?........................................................................................................ 12

3.1 Brief Historical Overview ............................................................................................... 12

3.2 Agile Methodologies and Practices ............................................................................... 12 3.2.1 The SCRUM Methodology ................................................................................. 14 3.2.2 The Agility within Agile ....................................................................................... 15

3.3 Cultural Aspects of Organizational Agility ..................................................................... 16 3.3.1 Values and Principles ........................................................................................ 17 3.3.2 Prerequisites ...................................................................................................... 18

3.4 Expected Improvements from Agile .............................................................................. 20 3.4.1 Time = Time-to-market & Bouncebackability ..................................................... 21 3.4.2 Costs = Budget & ROI ....................................................................................... 22 3.4.3 Scope = Outcome & Continuity .......................................................................... 23 3.4.4 Summary: The Project Management Triangle ................................................... 23

3.5 Keys for Success .......................................................................................................... 24 3.5.1 Agile Starts on Top ............................................................................................ 24 3.5.2 Agile is more than a Process ............................................................................. 25 3.5.3 Agile Challenges Organizational Velocity .......................................................... 25 3.5.4 Agile’s Architectural Requirements .................................................................... 26

3.6 Author’s Thoughts on Literature .................................................................................... 27

4 Primary Research Design ...................................................................................................... 28

4.1 Research Aim ............................................................................................................... 28

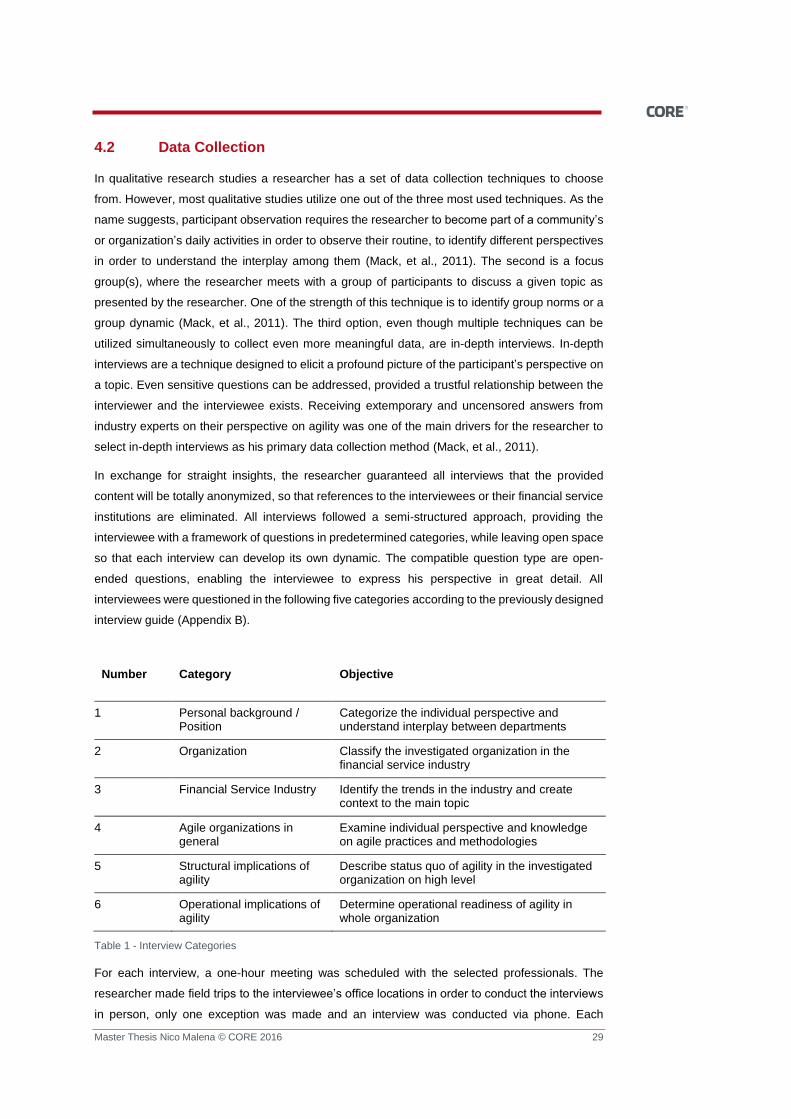

4.2 Data Collection .............................................................................................................. 29 4.2.1 Research Participants ........................................................................................ 30

4.3 Reliability and Validity ................................................................................................... 31

4.4 Data Evaluation ............................................................................................................. 32 4.4.1 Data Preparation ................................................................................................ 32 4.4.2 Data Analysis ..................................................................................................... 32

5 Case Studies .......................................................................................................................... 34

5.1 Case Study: Financial Service Institution A ................................................................... 34

Master Thesis Nico Malena © CORE 2016 IV

5.2 Case Study: Financial Service Institution B ................................................................... 35

5.3 Case Study: Financial Service Institution C .................................................................. 37

5.4 Case Study: Financial Service Institution D .................................................................. 38

6 Concluding Statements .......................................................................................................... 40

6.1 Agile – The Drive for Speed .......................................................................................... 40

6.2 Agile – In Need for a Specific Mindset .......................................................................... 41

6.3 Agile – Unleashing Technology ..................................................................................... 42

6.4 Agile – Useful to a certain Degree................................................................................. 43

6.5 Agile – Requires Discipline ........................................................................................... 44

7 Recommendations & Open Topics ........................................................................................ 45

Bibliography ................................................................................................................................ 47

Author ......................................................................................................................................... 51

About Novancia Business School Paris ...................................................................................... 52

About COREinstitute .................................................................................................................. 53

Master Thesis Nico Malena © CORE 2016 V

List of Figures

FIGURE 1 - DEVELOPMENT OF CAPITAL MARKET IN GERMANY .............................................................. 1

FIGURE 2 - DATA TRAFFIC IN CORRELATION WITH PRICE INDEX ............................................................. 4

FIGURE 3 - DEVELOPMENT OF MOBILE ONLINE SERVICES..................................................................... 5

FIGURE 4 - REGULATORY REQUIREMENTS IMPACTING THE CTB BUDGET ............................................... 7

FIGURE 5 - REGULATORY CHANGES TOWARDS MARKET LIBERALIZATION ............................................... 7

FIGURE 6 - INVESTMENTS INTO FINTECHS ......................................................................................... 9

FIGURE 7 - FINTECHS ATTRACTING SMES ........................................................................................ 9

FIGURE 8 - THE SCRUM METHODOLOGY ....................................................................................... 14

FIGURE 9 - THE OPENNESS OF AGILE DELIVERY FRAMEWORKS ........................................................... 16

FIGURE 10 - A COMPARISON OF PROJECT SUCCESS RATES ............................................................... 21

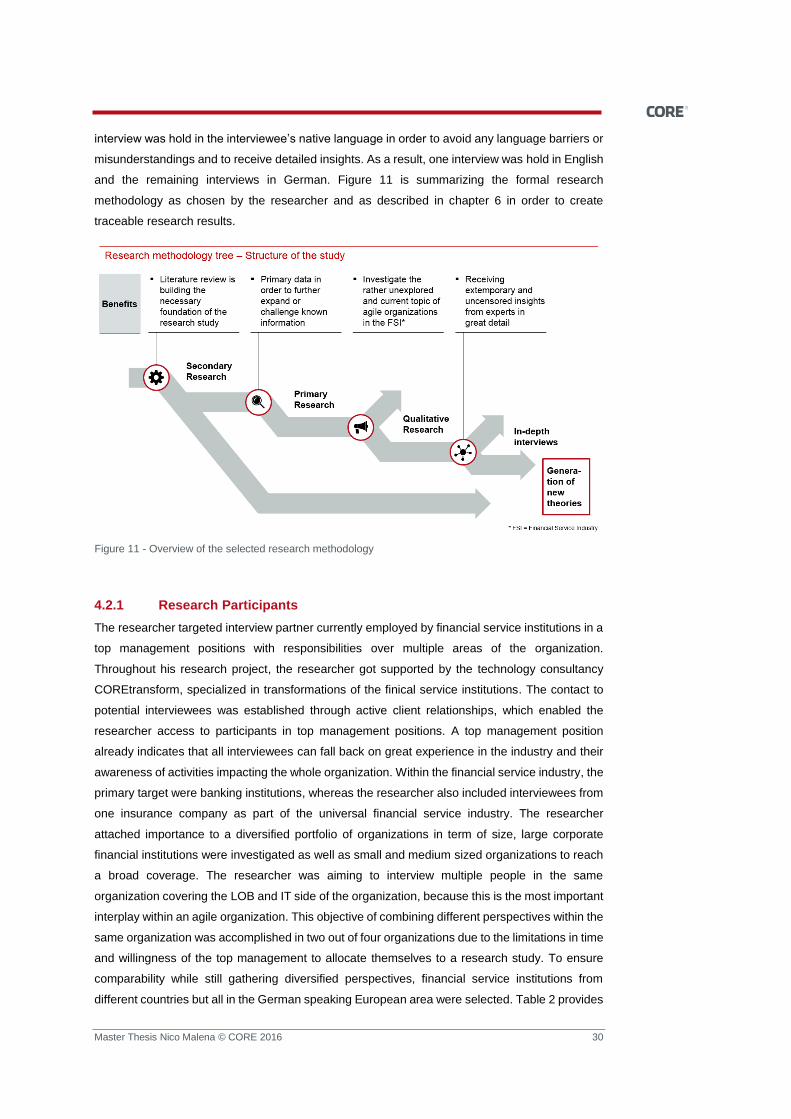

FIGURE 11 - OVERVIEW OF THE SELECTED RESEARCH METHODOLOGY ............................................... 30

List of Tables

TABLE 1 - INTERVIEW CATEGORIES ................................................................................................ 29

TABLE 2 - OVERVIEW RESEARCH PARTICIPANTS .............................................................................. 31

Master Thesis Nico Malena © CORE 2016 VI

List of Abbreviations

Abbreviation Description

AI Artificial Intelligence

API Application programming interface

ATM Automated teller machine

B2B Business to business

B2C Business to business

CBS Core banking system

CtB Change the bank

FDD Feature driven development

HR Human resources

IoT Internet of things

IT Information technology

LOB Line of business

M2M Machine to machine

PSD Payment service directive

SME Small and medium sized enterprises

STEM Science, technology, engineering and mathematics

TDD Test driven development

ROI Return on investment

RtB Run the bank

UAT User acceptance test

VC Venture capital

XP Extreme programming

46

Master Thesis Nico Malena © CORE 2016 1

1 Introduction

“Banks are dinosaurs; they can be bypassed.” (Gates, 1994)

More than 20 years ago, Bill Gates predicted the modern development in the financial service

industry. According to him, both, the ways of communication as well as the interaction partners,

were about to change in favor of customer satisfaction. Today at least, extracts of this provocative

statement and its meaning can be validated considering the impact of the digitalization. The

financial services industry is going through a transformation process, mostly driven by the

tremendous technological developments in the digital age.

Anywhere, anytime and possibly at no additional costs; today’s principles are allowing start-ups

to enter the financial services industry and to challenge traditional market leaders. An increasing

number of ‘attackers’ is disturbing existing financial systems by leveraging technological

advantages in order to offer more contemporary and user friendly customer solutions. As of now

a number of industry outsiders established successful business models in several market

segments within the financial service industry, which requires traditional financial institutions to

react. In contrast to new market entrants, large financial institutions have limitations due to their

organizational setting in regard to the necessary flexibility to deal with the rising complexity and

diversity.

As a result, most institutions are introducing major transformation initiatives with the long-term

goal of creating more flexible organizations, which are able to keep up with arising developments

and challenges. This need for change gets even more essential in the light of the pressuring cost

and income trends. The capital requirements are rising, whereas profits generated through the

credit business are decreasing and transaction fees paid by banking customers are about to clear

out due to the competitive situation (Figure 1) (Knippschild, 2014) (Baller, et al., 2015). This also

limits the possibility to pass on mounting costs to customers. In order to sustain the changing

market conditions, financial institutions are required to establish new revenue streams or to

reinforce existing ones through innovative ideas and the successful implementation of such.

Figure 1 - Development of capital market in Germany

(Deutsche Bundesbank, 2016) (EZB; Thomson Reuters, 2015)

46

Master Thesis Nico Malena © CORE 2016 2

The application of agile methodologies and practices has been identified by industry experts as

one of the key pillars within the targeted transformation (Jauber, et al., 2014). Thus, the intended

objective of an agile organization is to establish a flexibility within an organization, which adopts

to changing conditions and considers them as an opportunity rather than as a threat.

With the following analysis, the aim is to contribute to the ongoing discussion around agile

organizations. First, the concept of ‘Agile’ will be reviewed and discussed based on most recent

literature on the topic. Key success factors mentioned by practitioners will be pointed out and the

results of the primary field research conducted in the German speaking market will be presented,

giving depth to the concept in concrete case studies.

The overall goal is to elaborate and discuss suitable framework conditions for financial institutes

to embrace agility in their organizations in order to master present and future changes in the

market. The objective is not to determine if being agile or if certain agile practices are beneficial

for an organization. This has been extensively discussed in the literature without clearly

measurable results, as we will see. The focus is rather on how an organization in the financial

service industry can embrace agility to make the most out of it. Open questions are: Where are

the boundaries or limitations of agile methodologies and practices? In which circumstances are

they most effective? Particularly the in-depth empirical case studies are designed to shed light on

the interplay between the contextual and organizational phenomena.

46

Master Thesis Nico Malena © CORE 2016 3

2 Structural Change

Over the past decades the financial service industry has been rather conservative in terms of their

product and service offering as well as the utilization of upcoming communication channels. One

reason for this were the high entry requirements, preventing non-banking organizations to enter

the market. Based on this, large financial institutions were not required to develop or innovate

their business models in order to remain profitable. However, regulatory changes and digital

technology enhancements lowered entry barriers for industry outsiders, which led to a changed

macro-environmental landscape (Baller, et al., 2015). Some financial institutions already took first

visible actions to protect their market share they adapted their branch footprint and / or concept

to meet the evolving needs of customers (Ghose, et al., 2016). Generally, the management teams

of financial institutions are expected to find solutions to strengthen their organization’s position

and potentially grow the business while adapting to the changing market conditions. Three main

drivers initiating the change have been identified as they are broadly discussed in the literature:

Technological enhancements affecting the customer behavior

Regulatory requirements leading to market liberalization

Industry disrupters increasing the competition in the market

Those drivers of change are further examined in the following paragraphs, as they do not only

have an impact on the industry, but also redefine how organizations have to operate going forward

in order to be successful.

2.1 Technological Developments and Customer Behavior

Regardless of the industry, the ongoing digitalization impacts all businesses. Products and

services are demanded at any time, at any place and instantly after their release. The basis for

this development is the rising availability and usage of the online services. In Germany, the

broadband data traffic increased by more than 23-times in between 2004 and 2014. This growth

is negatively correlated to the price development of telephone and internet services during the

same timeframe. The decrease in costs and resulting affordability, supported by the availability

46

Master Thesis Nico Malena © CORE 2016 4

of technological improvements such as the DSL high speed connection, facilitated the significant

increase of the broadband internet usage in the past decades (Figure 2).

According to the network traffic increase, the amount of data which needs to be processed rises

accordingly. As reported by Stuart Bilick, an IBM industry expert, this is also one of the main

challenges financial intuitions and other business have to overcome in present times. How do we

handle the exponentially increasing amount of data? (Pahuja, 2015). However, the increasing

amount of data can also be a great opportunity for businesses to gain valuable insights into their

customer’s minds. Customer data are considered as a major asset of financial institutions. They

can be extracted from different sources, starting from transaction behavior and channel usage

even to social media. The resulting user profiles can then be leveraged to increase revenue by

providing a personalized customer experience. This opportunity has been identified by many

financial institutions. According to a survey conducted by The Economist Intelligence Unit in 2016,

financial institutions have ranked the technology developments in the field of data analytics as the

greatest potential for success. As a result, the participating organizations are planning to invest

the largest amount of monetary resources into the development of this capability as part of their

digital transformation (The Economist Intelligence Unit, 2016).

The second item on the list of important capabilities according to the same survey is mobile

computing and it is expected to consume a similar amount of resources (The Economist

Intelligence Unit, 2016). Simultaneously to the broadband internet traffic, mobile data traffic is

expected to reach a peak year after year in the near future, leading to an even greater amount of

data in circulation. While an increase, in terms of number of devices and data processed is

projected for all device types such as smartphones, tablets and laptops, the most significant

increase is expected for machine to machine (M2M) modules (Figure 3). M2M describes the

automated data exchange between different types of electronical devices (Wilson, 2016). Those

include devices such as smartphones, cars or even heaters. By the end of 2020, more than 50

billion devices will be connected and will exchange information autonomously. This tremendous

Figure 2 - Data traffic in correlation with price index

(VATM; Dialog Consult, 2016) (Statistisches Bundesamt, 2016) (Böhning, et al., 2015)

46

Master Thesis Nico Malena © CORE 2016 5

ecosystem of connected devices is referred to as the Internet of Things (IoT) and it will impact all

possible areas of life (Iyer, 2016).

This trend is also creating new opportunities for financial institutions. Banks already started to

utilize the IoT concept, for example in order to optimize the operation of their automated teller

machine (ATM) fleet. Processes are being automated and instant monitoring increases the

efficiency of their ATMs. Proposed next steps are video chats with personals tellers or extended

user analytics with the underlying objectives to increase customer satisfaction, to expand the

service portfolio and to reduce costs ( American Banker, 2015). An important cornerstone for

financial institutions in order to further utilize the IoT is the ability to integrate services and devices

into other platforms without large integration efforts, based on the existence of standardized

application programming interfaces (API). APIs have been a standard method of interconnecting

systems for decades, but due to new regulations and the progressing market liberalization, it just

recently became a topic in the financial services industry (Bannister, 2015).

All steps forward from a technological point of view would not be of any interest for financial

institutions unless they directly influence customer behavior. However, the technological

enhancements are being used by customers to a great extent, which puts the digital

transformation on top of most financial institution’s priority list, as it is seen as a great opportunity

(The Economist Intelligence Unit, 2016). The available set and usage of communication channels

for banking customers has expanded in the past few years. In Germany alone, approximately 75

percent of the people are actively using online banking and this figure has been stable for the

years since 2012. In the same period of time, the usage of mobile banking apps on smartphones

doubled to 21 percent, whereas the usage of tablets reached a high of 13 percent. The trend of

both device types as an entry point for banking transaction is expected to grow further (Böhning,

et al., 2015). Some banking executives in regions outside of Europe are already reporting that the

transaction volume for mobile has overtaken volumes across all other channels (Jauber, et al.,

2014). This increasing importance of online services leads to a situation in which fewer customers

are walking into branches for their banking needs (Ghose, et al., 2016).

The projection as per Figure 3, in which the usage and number of devices among all

communication channels is further rising, indicates that the various channels are complementing

Figure 3 - Development of mobile online services

(Cisco Systems, 2015) (Cisco Systems, 2015)

46

Master Thesis Nico Malena © CORE 2016 6

instead of replacing one another. This creates the customer’s expectation to experience the same

quality of services among all channels. In other words, financial institutions are obliged to create

an omni-channel experience by providing a consistent experience across all possible customer

entry points. This includes amongst others, banking apps on smartphones and the remaining

physical branches. Customers are looking for smart, simple and easy to use solutions within a

convenient reach. Those attributes will be crucial to reach a high customer satisfaction level in

the future (Jauber, et al., 2014).

The speed of innovations will not slow down and new or existing technologies, such as cashless

payments, will impact the financial services industry sooner rather than later. Financial

organizations are obligated to monitor any technological developments even though an

immediate impact is not expected. Also a close relationship to their customers can be valuable,

for example through social media. The goal is to be in a position to anticipate changing customer

behavior and introduce proactive measures as early as possible in order to seize the arising

opportunities (Jauber, et al., 2014).

2.2 Regulatory Changes and Market Liberalization

Institutions holding licenses for credit and financial services are eligible to obtain ownership or

possession of funds or securities of customers. This is the main differentiator between them and

non-banking organizations which are restricted to take possession of customer funds with the

intention of using them for own profit driven activities (BaFin, 2016). The entire regulatory

construct is witnessing constant alterations in order to facilitate the changes in the market. The

number of new regulations for financial institutions passed by the EU parliament has increased

by 45 percent in the timeframe from 2009 to today (Figure 4). In general, regulators are defining

rules and requirements to reach the following four long term objectives (Böhning, et al., 2016):

Stabilization of the financial markets

Market liberalization

Consumer protection

Optimization of the state income

The financial crisis of 2008 triggered significant regulatory adjustments as the stability of the

financial markets was not secured during that time without governmental support (Deutsche

Bundesbank, 2013). As a response to the immense losses and since the introduction of the Basel

III, financial institutions are required to increase their level of capital in order to secure loss

absorption and risk coverage of their capital. Basel III is a comprehensive set of reforms,

developed by the Basel Committee of Banking Supervision, to strengthen the regulation of the

banking sector (Bank for international settlements, 2016). However, the mandatory increase in

equity capital is freezing funds within banking organizations which could have been allocated to

business development activities.

46

Master Thesis Nico Malena © CORE 2016 7

Alongside the additional changes related to Basel III, the overall growth and complexity of

regulatory requirements as shown in Figure 4 is impacting the budgetary flexibility of financial

institutions. Adjustments or amendments to existing reforms entail efforts for the financial

institutions in order to fulfill the new requirements in a set timeframe. The larger the number of

regulations that are adjusted or amended, the more resources get occupied by the implementation

of those changes. The ‘Run the Bank’ (RtB) budget for maintenance and infrastructure within IT

departments of financial institutions is not expected to absorb those additional costs. As the only

option, the annual ‘Change the Bank’ (CtB) budget allocated to business development activities

gets directly impacted and is expected to further decrease (Figure 4). As a reflection of the

continuously growing number of regulations, the CtB budget for business development activities

is projected to reach a down of six percent in about four years. The minimal proportion of the

overall budget available for change indicates limited funds for adoption in the evolving financial

services industry and leaves only small room for failure (Pukropski, et al., 2013).

However, regulatory changes do not only have financial implications to organizations in the

industry. In order to rebuild trust, regulators are liberalizing the market to create a competitive

situation favorable for the consumer (Böhning, et al., 2016). Several regulations have been

Figure 4 - Regulatory requirements impacting the CtB budget

(Böhning, et al., 2016)

Figure 5 - Regulatory changes towards market liberalization

(Böhning, et al., 2016)

46

Master Thesis Nico Malena © CORE 2016 8

enforced in the past years with the intention to simplify transactions and raise the convenience

level of consumers in the EU (Figure 5). Amongst others, consumers are now able to transfer

funds to accounts in other European countries at no charges due to the introduction of SEPA, a

standardized transaction format and process. Motivated by technological developments, the

revised payment service directive (PSD II) is the next step on this path. The PSD II promotes

innovation as account information and transaction will be accessible for third party service

provider and it further improves the security of payment services within the EU (Beijer, et al.,

2016). Based on this, the previously mentioned API technology will be of great importance. A

standardized access will significantly impact the interconnectivity of financial institutions with third

party service provider and potentially amongst financial institutions themselves. Financial

institutions are in position to leverage this in their own interest by enhancing their value proposition

for customers. However, this opportunity is a threat at the same time, as the market will be less

restricted so that industry outsiders have more options to disrupt the existing financial system

(Zingmark, 2015).

2.3 Industry Disruption and Competitive Landscape

The aforementioned digital revolution as well as regulatory changes created an environment in

which non-banking organizations can benefit from the vast opportunities to enter the industry by

distinguishing themselves from established financial institutions with customer-centric products

and services. As a result, the competitive situation reached a first turning point as an increasing

number of direct banks and FinTechs entered the market. Direct banks also known as digital

banks are institutions providing consumer banking services exclusively via online channels and

without a physical branch network (Böhning, et al., 2015). FinTechs are a dynamic consortium of

new market entrants at the intersection of the financial services and technology sectors. The

common definition describes them as technology-focused start-ups, which are disrupting the

traditional financial service industry with more innovative and user firendly products and services

(Kashyap, et al., 2016).

Business needs of personal as well as corporate customers have not changed much in the past

years. However, new market entrants are conceptualizing new use cases by taking advantage of

a common interest to reduce complexity and to simplify processes (DealSunny, 2016). As a result,

FinTechs introduced competitive solutions as alternatives to the existing products and services

for payment transactions, lending operations, asset management and Business Intelligence (BI)

tools. Each of those sectors is witnessing growth, whereas especially the payment transactions

in terms of transaction volumes and the lending operations measured by the financing volume

are gaining further importance (Böhning, et al., 2015).

The upwards trending user figures are attracting more investors to fund the promising variety of

projects. Consequently, the venture capital (VC) investments and number of FinTechs were

increasing exponentially over the past years on a global level and especially in Germany. From

12 billion USD in 2014, the VC investment was up by almost two-thirds in 2015 with 19 billion

USD, even though it started from low single-digit billions of USD per year earlier in the decade

(Figure 6). Statistics are showing that three-quarter of the invested capital are deployed into the

customer segments of personal individuals and small and medium sized enterprises (SME). Both

46

Master Thesis Nico Malena © CORE 2016 9

segments together account for half of the profits generated by traditional financial institutions,

causing them to pay closer attention.

Business-to-Consumer (B2C) solutions can convince new clients with a better experience due to

low switching costs. This makes individuals to easy attractable targets. Business-to-Business

(B2B) solutions need to overcome several more barriers, such as corporate clients' greater need

for product / service customization and a corporate procurement department's focus on safety

and supplier risk, all of which increase switching costs (Ghose, et al., 2016). But FinTechs have

also identified great potential within the B2B sector by targeting SMEs. A major success factor for

those organizations and at the same time one of the biggest challenges is the access to funds.

Money lending services and products offered by the large financial service intuitions are mostly

designed for major corporations. The complexity and scale of those solutions do not fulfill the

needs of many smaller organizations. This leads to a rising number of start-ups offering lending /

financing solutions built for the specific use cases of SMEs. Taken together, employing multiple

solutions simultaneously can have a significant positive effect on an SME’s balance sheet

situation, leaving small businesses with more cash, improved working capital management and

more stable and secured funding (Figure 7).

Many new players streamline their focus on a single-purpose solution, designed to offer an

improved solution for just one product or service. Compared to large financial institutions that are

often slowed down by technical depth of old systems, a rigid organizational structure and a

multifaceted cost structure, agile start-ups are able to drive more radical innovation, as they are

Figure 6 - Investments into Fintechs

(Ghose, et al., 2016) (Kanning & Krohn, 2016)

Figure 7 - FinTechs attracting SMEs

(Ventura, et al., 2015)

46

Master Thesis Nico Malena © CORE 2016 10

often able to start from ‘a clean slate’ (Ventura, et al., 2015). Traditional financial institutions might

have to deal with even larger threats as only single solution provider going forward. Most FinTechs

are not directly competing with each other, making partnerships of service and product integration

possible. As just one example, ‘number 26’, a successful German based FinTech recently

announced its cooperation with ‘transferwise’, building an attractive and powerful consortium of

services for consumers (TransferWise, 2016).

Even though the development of FinTechs is ‘booming’, the impact on traditional players is still

limited due to a lack of scalability in their services. It is critical for large financial service institutions

in Europe to elevate the created customer experience through innovation and user friendliness

before FinTechs reach scale and outperform them. In other regions such as China, this tipping

point already passed to the disadvantage of the traditional players (Ghose, et al., 2016). Should

we transform our own organization or build partnerships with successful start-ups; and if so, in

which way? Those questions have to be addressed sooner rather than later. BBVA, a Spanish

banking giant, recently increased its FinTech funds up to 250 million USD (BBVA, 2016). Those

investments or collaborations are very promising, considering the fact that banks can provide the

most important assets in this business, which FinTechs have to build up from scratch: customers

(Hieronimus, et al., 2012).

2.4 Conclusion: The Need to Adapt

The profitability of traditional income streams within financial service institutions is trending

downwards, which is creating an urgency for the creation of alternative solutions in order to close

the imminent income gap. Technological developments have to be considered as a great

opportunity for this purpose as new ways of communication are leading to new customer demands

which can be addressed with new or improved products and services. However, the speed of the

technological development is not expected to slow down. Financial institutions cannot sit back

once they adapted to the most recent enhancements as they always have to be prepared for the

next ‘big thing’. Change is going to be the only constant factor and this need for continuous

flexibility has to be reflected in the people’s minds as well as in the structure of the IT systems

hosting all products and services (Bilick, 2015).

Furthermore, the budget available to introduce measures for improving ongoing business

activities is becoming tighter. The increasing capital requirements and rising resource demands

triggered by new or adjusted regulations is limiting the funds designated to change. While there

is an absolute necessity to satisfy the rising demands of customers, the room for failure becomes

increasingly smaller. Institutions have to balance the risks associated to anything new or

innovative with the possible outcome of a failure or success. Taking one wrong decision to launch

a large project which is failing could already slow down an entire organization’s reaction time to

leverage other arising opportunities in the same or following periods. In consideration of the

devastating success rates of large scaled projects with four percent, the choice and sizing of the

transformation initiative are considered to be a critical factor within large financial service

organizations (Böhning, et al., 2015). Successful organizations will have to find a way to manage

their organization highly efficient and without the hesitation to become innovative.

46

Master Thesis Nico Malena © CORE 2016 11

Another exceedingly critical resource for large financial institutions is time. The number and

coverage of industry attackers is rising as the variety of products and services is growing and the

targeted customer segments are further expanding. New market entrants are challenging existing

business models of large institutions and they increase the cost pressure with user friendly

solutions providing an improved customer experience. Even though the impact is still limited, the

momentum can change abruptly and the market leaders have to be prepared for that.

In conclusion, the assumption can be raised, that new technologies are influencing the

consumer’s behavior which requires adaptations to the present product and service offerings and

to the way information is used and exchanged between financial institutions and their customers.

At the same time, the growing competition is creating an urgency while the budgets for required

transformation initiatives are limited. Observers note that large organizations in this industry

should start to adapt to the changing environment today and use the existing resources in an

efficient manner in order to maintain their leading positions. In this regard, agile became a ‘buzz

word’ and in the following chapters, opportunities are discussed how it can be leveraged to cope

with those challenges.

46

Master Thesis Nico Malena © CORE 2016 12

3 Can Agile be a Solution?

How often do people find themselves in situations where things do not go according to plan? A

decision needs to be taken whether the predetermined path should be followed rigorously

potentially facing issues or if new findings along the way should be used to make adjustments

(Rawsthorne & Shimp, 2016). Agile is specifically designed for such a scenario and expected to

be a possible solution for various reasons which are being discussed in this chapter. First, a brief

introduction to the concept of ‘Agile’ will be given, explaining its origins and then showing the

methodologies and practices as described in the literature. Following, the expected improvements

of agile over traditional practices are pointed out. This chapter will then be completed with an

overview of the existing literature on critical keys towards a successful increase of agility within

an organization.

3.1 Brief Historical Overview

Due to the previously discussed drivers of change, many experts are sharing the opinion that

financial institutions are required to go through a major transformation, which has started in some

cases already. But how do you become a leader in the digital age and separate yourself from

laggards? The one thing that is frequently linked to organizational transformations is the need to

become more agile. Agile is a military word derived from strategies applied by forces on the

battlefield. The objective is to adapt and exploit the chaos of the battlefield and to do it faster and

better than the enemy does, in order to succeed (Rawsthorne & Shimp, 2016). In a professional

context, agile was born in 2001 as a project management framework designed for the

development of complex IT solutions. It promotes iterative and adaptive thinking by breaking down

larger projects into small work-pieces in order to embrace flexibility and continuous improvements

(Goulstone, 2016). At its heart is rapid decision making, small cross-functional teams working

side by side, regular touchpoints checking progress updates and sharing problem situations to

find quick solutions. Teams are engaged to produce new quality outputs in form of functioning

product increments or features in short consecutive development cycles. Those are instantly

made available for stakeholder and users to provide direct feedback (Paul Willmott, 2015).

One of the banks which already conducted a transformation towards an agile organization is

Capital One in the US. Its CEO Richard Fairbank knows: “We’re going to need to think more like

technology companies and maybe a little less like banks” (2015). Due to its agile setup, Capital

One is able to release up to 400 new products every day, allowing them to provide customers

with innovative and user friendly solutions rather like Apple or Amazon than traditional financial

institutions (Pahuja, 2015).

3.2 Agile Methodologies and Practices

“We are all in the software business now, regardless of the product or service we provide, […].”

(Gothelf, 2014).

With this statement in mind, the demand for successful software delivery practices are rising.

Many global players in different industries like Google, Microsoft or SunCorp adopted agility in

46

Master Thesis Nico Malena © CORE 2016 13

their organizations (Cooke, 2012). The creation and rise of agile goes back to the remarkable

high failure rate of software development projects in the 1990s. Projects constantly missed their

deadlines, substantially overrun budgets and dissatisfied customers with faulty deliverables. At

this time, the waterfall delivery framework was widely applied among IT departments. This

methodology implies that the necessary stages within a software delivery cycle analyze, design,

built, test and integrate are undertaken serially, requiring the full completion of one stage before

the next one can be initiated. The completion of every stage gets approved by the responsible

manager which is supposed to reduce the overall business risk in the delivery. However, the

approach was showing high failure rates as previously stated and three key pain points causing

poor success rates have been identified (Cooke, 2012).

The first is over-planning. Traditional IT projects usually start with the creation of extensive

requirement documents. Several layers of documents are created with ascending levels of

technical details for different audiences. This process can take months, consumes large amounts

of resources and leads to a pillar of documents which can create misalignments between IT and

the line of business (LOB) in the worst case scenario. This practice does not allow any changes

along the process to reflect changing conditions while unclear defined requirements can lead to

conflicts due to possible misinterpretations. This becomes even more critical considering the

second key pain point of insufficient communication and the strict separation between IT and the

LOB, after the creation of the requirement documents is completed. Lastly, the ‘all at once’

delivery results in a large risk, as problems are discovered at the very end when they are most

evident and very costly to resolve (Cooke, 2012).

In order to improve the common software development practices, a group of highly regarded

specialists came together in Utah in 2001 to develop new standards in form of principles and

processes in the field of software development. The result was the ‘Agile Manifesto’, a guideline

established as a framework for successful software deliveries. By now, the guiding principles of

the Agile Manifesto have been transformed into a set of software development and project

management methodologies. However, the broad range of agile methodologies shares the same

basic objectives (Cooke, 2012):

Incremental planning over upfront planning in order to respond to ongoing changes in

the environment.

Prioritize your actions in order to satisfy the most demanding customer needs first.

Release quality outputs in form of customer value from the beginning and continue to

build upon the first deliverable.

Address potential technical risk as early as possible in the process, so that changes will

not set back the progress by much or be unnecessary costly.

Utilize frequent feedback cycles through a continuous delivery of business value in form

of functional software features.

Create a trustful environment in which your staff is empowered to continuously deliver

high business value outputs.

46

Master Thesis Nico Malena © CORE 2016 14

Encourage interdisciplinary communication between IT and business to increase the

quality of the deliverables.

Many methodologies following those guidelines have been established over the past decades

including SCRUM, Extreme Programming (XP), Kaban, Feature Driven Development (FDD), Test

Driven Development (TDD) and several more. SCRUM is the worldwide most used agile

methodology due to its simplicity. In order to get a deeper insight in an agile delivery framework,

the SCRUM methodology is elaborated in the following paragraphs, followed by a chapter

dedicated the flexibility within agile deliver frameworks. (Francois, 2013).

3.2.1 The SCRUM Methodology

In the SCRUM methodology, the acting persons are confronted with individual flexibility instead

of strict regulations. Therefore a great emphasis is put on the interaction within self-organized

teams. As part of the structure, three roles, four regular meetings and three artefacts such as the

product deliverable are defined as shown in figure 8.

The product owner is responsible for the quality and return of investment (ROI) of the newly

developed or updated product by consolidating the demands of all involved stakeholders including

customers into a list of requirements, called product backlog. Besides, it is part of his responsibility

to decide on the priority ranking of all requirements while being aware of existing dependencies.

The projects team’s main duty is the implementation of the given requirements leading to a

valuable software feature, whereas value is measured based on customer’s satisfaction. The

team combines interdisciplinary profiles such as requirements analysts, system architects,

developers and testers in order to cover all required skills. Knowledge and progress sharing is a

key activity within the team, so that individual members can benefit from each other the most. The

SCRUM team evaluates how many of the top prioritized product requirements can get delivered

Figure 8 - The SCRUM methodology

(Wintersteiger, 2013)

46

Master Thesis Nico Malena © CORE 2016 15

within the upcoming delivery cycle called sprint as part of their sprint planning meeting. This

meeting is hosted by the SCRUM master, who is primary a facilitator and coach. Even though the

team is mainly self-organized, the SCRUM master can be seen as a leader without disciplinary

responsibility, who is engaged to create an environment in which the team is able to perform best

(Wintersteiger, 2013).

A sprint is a fixed time-box with a duration of usually two weeks (deviation possible), in which

product requirements in scope of the current sprint backlog will be designed, developed,

integrated and tested in order to deliver a functioning product increment. As part of the sprint

routine, short daily meetings will be hold to share the past progress, next steps and blocking

issues among all team members. The underlying goals are to learn from each other, to solve

problems faster, to avoid repeating problems of the same type and to check on the overall sprint

progress based on the previously set targets. At the end of each sprint a fully functioning software

feature is delivered, which can be evaluated by all stakeholders while performing the tests of the

targeted use cases. This is done in the sprint review meeting. At this point, the roll-out acceptance

is granted and / or required product improvements in form of defects are detected. To close the

loop on the one end, those have to be added back to the product backlog and ranked in the

requirement list according to their priority. In order to complete one delivery cycle, a meeting with

the entire delivery unit consisting of product owner, SCRUM team and SCRUM master is

organized to discuss possible process improvements for future iterations. According to the

process flow, the next sprint would then be kicked off with another sprint planning meeting and

the iteration is repeated accordingly (Figure 8) (Wintersteiger, 2013).

3.2.2 The Agility within Agile

One more out of many other related agile methodologies is XP. As its name indicates, the

emphasis within this methodology is on the programming part within the delivery cycle. However,

XP consists of many process elements similar or even equal to SCRUM. The development team

is also working in iterations in order to be responsive to possible requirement changes.

Furthermore as seen before, the delivery cycles are time boxed and the product deliverables build

upon another. Unlike the SCRUM methodology, developers and tester within XP are more bound

to certain practices, which are constantly aiming for immediate feedback.

TDD is one of them, in which a software developer is writing the required test cases and scenarios

to validate his code prior to undertaking development work. This helps to verify requirements and

identify misinterpretations before the implementation starts. Another practice is the so called ‘pair

programming’. Here, two developers are pairing to work together on the same assignment in order

to increase accountability and knowledge sharing. A third one is continuous integration, which

indicates that newly developed code is immediately integrated into a production environment. The

result is instant availability of product features enabling instant feedback from users. This practice

requires an automated testing procedure in order to ensure that the updated product is not

introducing errors or limiting the existing functionality (Cooke, 2012).

46

Master Thesis Nico Malena © CORE 2016 16

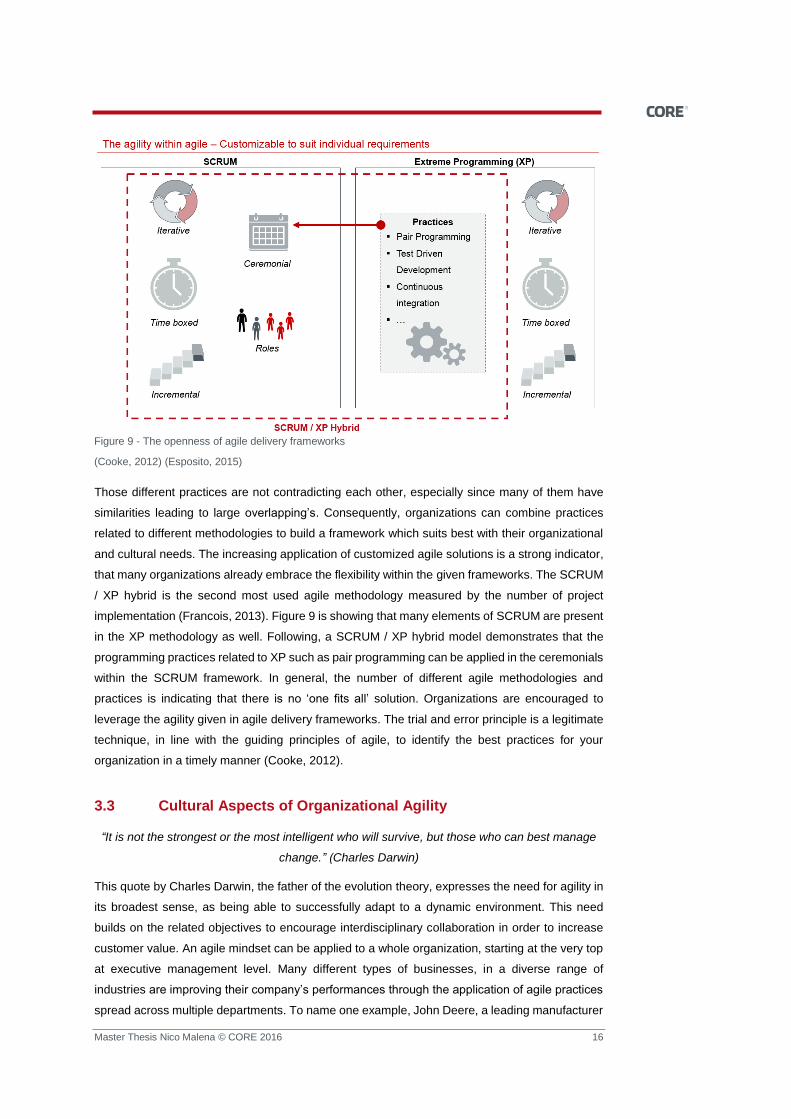

Those different practices are not contradicting each other, especially since many of them have

similarities leading to large overlapping’s. Consequently, organizations can combine practices

related to different methodologies to build a framework which suits best with their organizational

and cultural needs. The increasing application of customized agile solutions is a strong indicator,

that many organizations already embrace the flexibility within the given frameworks. The SCRUM

/ XP hybrid is the second most used agile methodology measured by the number of project

implementation (Francois, 2013). Figure 9 is showing that many elements of SCRUM are present

in the XP methodology as well. Following, a SCRUM / XP hybrid model demonstrates that the

programming practices related to XP such as pair programming can be applied in the ceremonials

within the SCRUM framework. In general, the number of different agile methodologies and

practices is indicating that there is no ‘one fits all’ solution. Organizations are encouraged to

leverage the agility given in agile delivery frameworks. The trial and error principle is a legitimate

technique, in line with the guiding principles of agile, to identify the best practices for your

organization in a timely manner (Cooke, 2012).

3.3 Cultural Aspects of Organizational Agility

“It is not the strongest or the most intelligent who will survive, but those who can best manage

change.” (Charles Darwin)

This quote by Charles Darwin, the father of the evolution theory, expresses the need for agility in

its broadest sense, as being able to successfully adapt to a dynamic environment. This need

builds on the related objectives to encourage interdisciplinary collaboration in order to increase

customer value. An agile mindset can be applied to a whole organization, starting at the very top

at executive management level. Many different types of businesses, in a diverse range of

industries are improving their company’s performances through the application of agile practices

spread across multiple departments. To name one example, John Deere, a leading manufacturer

Figure 9 - The openness of agile delivery frameworks

(Cooke, 2012) (Esposito, 2015)

46

Master Thesis Nico Malena © CORE 2016 17

of agricultural and constructions machines, started applying agile practices in parts of their IT

department. With time running by, the whole organization got infected by the convincing

advantages that agile provides. To name one out of several positive outcomes, John Deere was

able to cut down the time-to-market for new products, from the idea to the release, by 50 percent.

In most cases, the starting point for the application of agile methodologies within an organization

is the IT department. Internal references, who are showing even small improvements, establish a

positive momentum and encourage other teams and departments to follow the lead. Out of

curiosity, they would evaluate options to leverage new practices themselves in order to boost their

own performance. This can be considered as the most common sequence of how agile can

spread over a whole organization (Rigby, et al., 2015). Thus, an agile organization is not just

about using tools and following processes; it is the people and it involves the whole operational

system to enhance qualities, routines and relationships to produce outputs that meet their

customer’s expectations (Holebeche, 2015). Roles and processes can be customized, as long as

they stay in line with the guiding values and principles that agile stands for.

3.3.1 Values and Principles

3.3.1.1 The Customer is the first Priority

Agile is not about the ’how’ but rather about the ‘why you do certain things’. One of the most

striving principles within an agile organization is ‘the customer comes first’ and the obsession to

deliver actual value as the first priority. The entire staff is encouraged to put in significant effort to

deliver exactly what their customer wants. This implies the introduction of continuous customer

engagement models, enabling organizations to develop a truly deep understanding of their

customer needs. The gained insights empower financial institutions to create added value with

more personalized services and products, meeting or even exceeding their customers’

expectations. Added value in the context of organizational agility is the fulfilment of actual

customer demands and not only the release of additional features or services without an impact

on a customer’s user behavior (Gothelf, 2015).

3.3.1.2 Decisions have to be made quickly

In an environment in which uncertainty is omnipresent and where things can shift overnight, it is

necessary that decisions are made quickly. In a non-agile organization, decisions are run past

several management layers, ensuring everyone is brought in, before direction can shift. These

processes are slow and provide cover in the event, that things turn out to go sideways.

Organizational agility requires decision-making to be done in the customer’s best interest

(Gothelf, 2014). Every person in an organization is encouraged to take decisions. However, in

order to prevent a chaos with a lot of aimless or random decisions, people are made accountable

for all of their actions. Accountability is not used in the sense of blameworthiness, but you have

to explain why you took a decision which led to a certain action. Therefore, decisions are expected

to be supported by facts or reasonable assumptions to make the thought process comprehensible

for an external observer at a future point in time. In simple terms, you are asked to make the best

decisions possible, based on the information available at the time of the decision making

(Rawsthorne & Shimp, 2016).

46

Master Thesis Nico Malena © CORE 2016 18

3.3.1.3 Create a Learning Culture with high Transparency

Good decisions come from experience and the less blame-setting an organization is, the easier

it is for an individual to gain valuable experiences and for an organization to become agile

(Rawsthorne & Shimp, 2016). Very high project success rates are a sign for incremental progress

and not for being highly innovative. Aiming for fundamental breakthroughs brings risks and risks

bring failures, but agile organizations establish a learning culture that takes advantage of

‘intelligent failures’. In evolving industries such as the financial services you can make use of the

trial and error logic. A higher number of attempts improves your odds to succeed, but at the same

time losses have to be managed and kept to a minimum. Prior to taking action, the impact of a

potential failure needs to be evaluated in order to prevent significant damages to the business. In

line with this approach goes the ‘be quick and fail fast’ principle. Early releases, aiming to test

previously made assumption, can either validate made assumptions or provide first evidence of

failure and a potential waste of resources in the future (McGrath, 2011). At this point, quick

ruthless decisions are needed to dispose projects or parts of the organization that no longer add

value (Holebeche, 2015). Obviously, failures are not always useful, especially if they occur

multiple times based on the same mistake or misleading assumption. Agility demands a high level

of transparency to convert failure into knowledge and to share it with your peers in order to add

value and create benefits to the entire organization (McGrath, 2011).

3.3.1.4 Interdisciplinary Collaboration is a Necessity

Transparency also plays a role when it comes to the alignment of enterprise interests with

individual interests. The reason for this is that the intra-organizational communication and

interaction channels need to result in an extended interdisciplinary collaboration. Starting at a

strategic level, participation is encouraged at all levels. Strategizing is a rather continuous process

due to changing environmental conditions than a static event, which is completed with the creation

of an annual business plan. Everyone is expected to be externally aware - sensing changes in

the environment, empowered to speak up and to introduce actions to take advantage of new

opportunities or to mitigate unforeseen risks. This concept goes hand in hand with the idea that

short term gains will lead to long term advantages and the principle of having a long term strategy

with a short term execution (Jauber, et al., 2014). For today’s financial service institutions,

interdisciplinary collaboration and the break-up of department silos is especially important at the

interface between IT and the LOB. A common mistake in the past was that the LOB developed

and designed an idea and left the actual implementation to the IT department without any

additional support. However, the IT department was rather focused on increasing efficiency and

standardizing the system-infrastructure than creating value through the implementation of new

ideas. This misconception of not working together for the same cause creates tension between

the business units and might prevent a successful transformation (Pegasystems, 2016).

3.3.2 Prerequisites

3.3.2.1 Outside the Organization

Is agility something which can add value to any organization, especially in the financial service

industry? In this chapter, the prerequisites and conditions favorable for agile methodologies and

practices are discussed. First, the market environment needs to be considered. Are the existing

46

Master Thesis Nico Malena © CORE 2016 19

conditions and customer preferences frequently changing or is the market rather stable and

predictable? With a remark to chapter 2, the structural changes in the financial service industry,

it can be noted that financial service institutions are required to constantly make adjustments. In

accordance with this goes the general customer engagement and the question whether

customers are available for a frequent exchange of feedback (Rigby, et al., 2016).

Furthermore, the overall speed of how innovation progresses can make a difference needs to be

evaluated. If the competition is closing gaps very quickly and time to market plays a significant

role, organizations have to optimize the cycles from the idea to the actual launch of the product

or service. This constraint can get even more difficult, if an organization reaches limits in regard

to its resource capacity. Pressuring timelines are mitigated with increased resource allocations,

leading to budget overruns and might have negative implications to the overall quality of the

deliverables. In this case, the flexible allocation of resources leading to quick first results can be

a solution (Cooke, 2012). This leads to another necessary requirement: the minimum viable

product cannot be a fully completed error-free product in an agile project. If an early release or

limited functionality, delivered in order of their priorities, does not add any value to a customer’s

situation, the application of agile practices is at least questionable. Going one step further, if an

early release with interim mistakes could be harmful to a customer, it could have a catastrophic

impact for the organization as a consequence. Leaving the financial service industry and looking

at the pharmaceuticals for example, the early release of a new drug could be bad for a customer

or patient, but it could also completely ruin the institution who is selling it (Rigby, et al., 2015).

3.3.2.2 Inside the Organization

There are certain requisites outside an organization which are expected to be fulfilled. However,

the situation inside an organization is more crucial for the utilization of agile practices. Even

though it relates to the own staff and processes, it does not necessary mean that it is easier to

control or influence. Starting from team leads to managers and directors, people who used to

maintain a heavy-handed control over day-to-day activities of their staff, will need to be willing to

exchange control in favor of trust and employee empowerment. Agile methodologies and

practices are designed to make an easy shift in mindsets for people in managing positions, as

they can foresee the results. According to the process, the next tangible deliverable is never more

than a few weeks away. Given this constellation, there should be enough confidence to bypass

the dispensable need for close monitoring (Cooke, 2012). Empowering managers can be less

concerned about tactile design, but rather whether the strategic goals are being achieved or not

(Gothelf, 2014).

Then again, the required skills and competencies, in order to operate effectively in an agile

delivery framework and to be able to take the right decisions, are rather indispensable. Especially

the so called STEM (science, technology, engineering and mathematics) competencies are of

significant importance in the continued development of business models and the organizational

adaptability (Böhning, et al., 2015). One of the resulting implications relates to human resources

(HR) as the traditional style of hiring does not build organizational agility. Specific competencies

have to be attracted, but not by purely filling gaps in a discipline silo. Recruiters have to assess

more than just the visible skills of given candidates, such as the experience in a specific field.

Instead, ways have to be found to evaluate a person’s ability to collaborate, to be creative and

46

Master Thesis Nico Malena © CORE 2016 20

their curiosity in terms of willingness to learn (Gothelf, 2014). This is not an easy task, but in the

end the objective is to find candidates such as ‘an accountant with an interest in software

development’, a person aware of and able to understand the importance of diverse disciplines

(Gothelf, 2014).

Furthermore, the people in an organization have to be open to new practices and release

themselves from their business as usual routines. Mainly in large and traditional firms it is hard to

establish a momentum seeking for change. Agile is not going to change an entire department

overnight. It is a learning process, which is continuously progressing and involving more and more

parties within the organization. However, this openness to abandon well established processes

and engage in new principles, such as a higher degree of self-organization or the shift away from

upfront documentation to extended communication and personal interaction, is vital (Cooke,

2012).

In order to become a truly agile organization, central processes have to be adjusted to create the

necessary framework. One of them relates to the way an enterprise budget is managed. The

resource allocation of profit driven organizations can be motivated by the return of a project while

it encourages flexible acting and thinking. Jeff Gothelf takes an interesting position in his article

“Bring agile to the whole organization” (Gothelf, 2014) by suggesting that larger corporations

should follow the example of startups and treat each team as such. Project teams have to apply

for funds and at the end of each funding period the teams must present their cases to the financing

department in order to get refunded. This process would allow more flexibility with only short-term

commitments while being more result driven (Gothelf, 2014). Although it is an interesting

approach, it also kicks off the discussion on how to measure results. A finance officer tends to

measure results based on the return on investment (ROI), but projects such as the modularization

of an existing legacy system do not generate a direct ROI. Nevertheless, such projects are crucial

for the sustainability of an organization. Therefore, the idea points in the right direction, but the

implementation needs to be aligned with the long-term strategy of an organization.

3.4 Expected Improvements from Agile

“The overall results clearly show that waterfall projects do not scale well, while agile projects

scale much better.” (The Standish Group, 2015)

The Standish Group is publishing a “Chaos Report YYYY” on an annual basis, indicating the most

challenging project success criteria as well as the success rates based on a large number of IT

projects spread across various industries. Overall, the results are providing soft evidence that an

agile delivery approach returns greater achievements than the traditional waterfall approach, as

shown in figure 10. However, the questions arises: How to measure success? The commonly

known metric to measure project success, also known as the project management triangle,

consists of three dimensions: time, costs and scope. The time relates to the set deadlines, budget

indicates the maximum amount of resources planned in order to deliver the predetermined scope,

which are desired features and functionalities (Bohnic, 2014). This traditional metric is lacking

customer outcome, as a consumer might remain unsatisfied even though the targets were

reached in all three dimensions. The Standish Group already addressed this constraint in its most

46

Master Thesis Nico Malena © CORE 2016 21

recent study (Figure 10) by replacing the scope with perceived customer value, resulting in a

seven percent decrease in the calculated project success rate (Erik Weber Consulting, 2015).

Especially in consideration of the perceived customer value, agile is showing greater chances of

success compared to the waterfall approach. Nevertheless, the question remains how accurate

the perceived customer value can be measured without the direct involvement of customers in

the study. In the following chapters, the expected improvements attached to agile methodologies

and practices are further discussed in a global enterprise view and detached from a project

perspective. The structure of the expected improvements is inspired by the three dimensions of

the traditional project management triangle time, budget and scope.

3.4.1 Time = Time-to-market & Bouncebackability

As broadly discussed in the second chapter, the financial service industry is exposed to many

changing determinants. Technological developments are resulting in higher customer

expectations. Regulatory requirements are liberalizing the market and new market entrants offer

contemporary solutions tailored for specific customer needs. The most essential variable in this

context is the time you need in order to react and leverage the given circumstances. With too

much time passing by, a change or new development in the financial service industry can turn

quickly from a great opportunity into a great risk, if an organization is too slow to provide their

customers with a valuable solution. Even if trends are acted on proactively, an extensive upfront

planning in advance to the implementation of new ideas in non-agile methodologies, results in a

lack of responsiveness to ongoing changes and it usually takes months to create them (Cooke,

2012). The longer the time gap between requirement documentation and the implementation of

such, the greater is the risk that it either does not suit the customer need any more or others have

been faster with an offer addressing the same need (Pegasystems, 2016).

Agile organizations embracing short iterative delivery cycles are able to provide tangible

outcomes rapidly on a regular basis. This is accomplished by focusing team efforts on incremental

but fully functional, fully tested and production-ready product or service features that can be

released to the customer well in advance to the end of the project lifecycle (Cooke, 2012). In order

to avoid a misconception at this point, agile is not directly increasing the efficiency of the staff to

implement a predefined scope in less time. However, the adapted organizational structure allows

Figure 10 - A comparison of project success rates

(The Standish Group, 2015)

46

Master Thesis Nico Malena © CORE 2016 22

the organization to focus on the highest priority features, which can be released in incremental

deliverables to cut the time to market (Cooke, 2012).

The overall duration to complete a project or initiatives is not necessarily shorter, as i.e.

developers are not programming faster than before. Even though certain indicators are given,

also a positive impact on the entire project lifecycle is possible. According to the principle ‘think

big, but act small, practical and fast while constantly adjust’, a large US based corporation outside

the finical service industry was able to compress the time needed to launch a new product into

the market by 75 percent. With the transition from a traditional sequential to an iterative approach,

unnecessary steps in the process have been eliminated to develop immature prototypes, which

have been further improved along the process. This is one of the major benefits of agile, the quick

releasing of small product or service increments to be expanded and stabilized along the project,

based on instant feedback, gathered directly from the consumer (Rigby, et al., 2016). The time

saved can be quite significant, as a project could have been heading in the wrong direction for

years without incremental testing (McGrath, 2011).

In an environment in which time is a critical factor, and especially financial institutions have to

take actions instantly, agile provides a framework to address this requirement. There may be

mistakes in a fast moving organization, but a truly agile organization establishes a bounce-back-

ability to act fast and thus being able to constantly adjust and reshape along the way (Holebeche,

2015).

3.4.2 Costs = Budget & ROI

According to a Harvard Business Review study, the average cost overrun of IT projects is

projected with 27 percent (Flyvbjerg & Budzier, 2011). As if this would not be alarming enough,

the real pitfall is, that one out of six software projects exceeds its initial estimate by 200 percent

and more. Cost overruns in this dimension can have serious impacts on an organization’s financial

stability, depending on the size of the project, and challenges the future existence. One of the key

activities in order to avoid such a scenario, according to the same study, is the ability to avoid

changes to the scope during the project (Flyvbjerg & Budzier, 2011). However, this contradicts

with the given circumstances in the financial service industry, which are frequently shifting and

change is considered as the only constant factor (Bilick, 2015).

Agile methodologies and practices are providing a framework which enables organizations to

meet budgetary limitations while being open to new requirements. A precise project cost estimate

is replaced by a budget to create value in a defined business sector (Madden, 2014). In contrast

to the waterfall approach, the scope in an agile project is rather flexible, while the time and budget

are fixed. During the project lifecycle, the execution ability is guaranteed, as a working product is

created containing a set of features, according to the highest priorities and the greatest customer

value. Even though a better cost control is given, it cannot be ensured that at a certain point in

time all targeted features will be implemented. But still the situation, in which an organization has

to allocate additional resources to get a product ready for production, does not need to be faced.

Thus, at a predetermined point in time, a production-ready product is delivered, which is expected

to contain room for further improvements or extensions (Cooke, 2012).

46

Master Thesis Nico Malena © CORE 2016 23

In terms of costs and return, agile methodologies and practices can be considered as more

beneficial than alternative approaches during both, project failure or success. A product delivered

in time, costs and scope, based on the waterfall approach, does not guarantee success and profits

till it is launched and actual customer feedback can be gathered. In a worst case scenario, an

organization invested a large amount of resources for a product or service, which does not

address any needs. This scenario is impossible in an agile organization, as product increments

are delivered and tested rapidly and failures are detected instantly. Therefore, the decision can

be made to shift priorities in order to avoid a continued allocation of unprofitable resources

(McGrath, 2011). Assuming the same project, consisting of multiple product features, would suit

a customer need, it would start to generate return after its release. In contrast to a sequential

delivery approach, in which all features are released at the same time once the project is