MassHousing Mortgage Insurance Fund Annual Report, June 30 ...

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

MassHousing First Mortgage Program

Primary Home Purchase

Property Type LTV CLTV Min. FICO Max DTI

1 Unit

95.01 - 97.0%

105%1

680 41%

80.01 - 95.0% 660 45%

< 80.0% 640 45%

2 Unit2 < 95.0% 105%1 680 45%

3 – 4 Unit2 < 95.0% 105%1 700 45%

• 1CLTV - Only Fannie Mae Approved Community Seconds Allowed – (City/County 2nds, City/County Grants, Other Fannie Mae approved seconds)- ROC

is responsible for the review and approval of all Community 2nds and documentation and must ensure that it meets FNMA guidelines for Community Seconds

• 2Minimum six (6) months reserves required for all multi-family 2-4 units • Income and Loan Limits per County - http://www.massresources.org/masshousing-loans.html#income • Homebuyer and Landlord Education/Counseling required https://www.masshousing.com/portal/server.pt/community/home_buyers/225/home_buyer_counseling • Maximum “Gross Ratios” for Multi-Family Units:

• Gross Ratio = DTI ratios without any inclusion of rental income from the other units • 2 Unit – Gross Ratios 50/58 (Housing/Debt)----no consideration for rental income • 3- 4 Unit – Gross Ratios 60/68 (Housing/Debt)----no consideration for rental income

• Rate Locks/Reservations must be completed by Corporate Lock Desk and must not be completed prior to DU Approve/Eligible Findings and SPM Underwriter Approval – Reservations and Rate Locks must be completed within 20 days of the DU used for Final Approval. Submit a Rate Lock request form accompanied by the Final SPM approval prior to 2:30 PM EST.

Revised December 4, 2014 1

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Appraisal Requirements

• Full Fannie Mae appraisal is required regardless of DU Findings – Form(s) 1004 , 1073 • 1004d if the appraisal > 90 days at time of SPM Final underwriting and/or minimum 2055 w/1004MC if the appraisal

is >120 days at closing. • Closing is defined as the date the Note is executed by the Borrower(s) • MassHousing Appraisal Requirements:

• All MassHousing first mortgage Lenders must be registered on the FNMA UNIFORM COLLATERAL DATA PORTAL (UCDP) website in order to electronically submit the required appraisal reports

• The Lender or its agent must upload the appraisal into UCDP and ensure the appraisal’s “Successful” submission before closing the loan

• The Lender must enter the Doc File ID into www.emasshousing.com and provide a copy of the Submission Summary Report (SSR) in every loan package submitted to Titan for review

• Lender must provide an updated Fannie Mae SSR on UCDP if Titan conditions for updated appraisal • Appraisals must be first generation (original document) appraisals that are either sent or pulled directly from

your appraisal source. • If the lender delivers the XML based appraisal to Titan to satisfy the requirement for a first generation appraisal,

the PDF copy of the actual appraisal is also required. • Uploading your appraisal into your LOS system or scanning and transmitting the appraisal will translate to Titan

Lenders Corp as an edited appraisal (not acceptable) • All MassHousing first mortgage lenders must comply with the Appraiser Independence Policy as required by

Fannie Mae (See documents on emasshousing.com

Assets

• Two month complete bank statements, all pages • Reserves established by DU. EXCEPTION: Minimum 6 months reserves required for all multi-family 2-4 units • Acceptable Sources of Down Payment

• Liquid Assets • Gift from family member or household member • Must be entered separately on AUS • Follow Fannie Mae Selling Guide for acceptable gift donors. Refer to www.fanniemae.com for additional

details. • Real estate equity from the sale of another home (HUD-1 required) • 401k or retirement funds if they are the borrowers contribution • Terms of withdrawal should be documented • Bonus income that can be verified with a 2 year history (may not be used as qualifying income if used

as down payment) • Windfall” assets such as tax refunds, inheritance, insurance settlement must have acceptable

documentation provided for the source of these funds

Revised December 4, 2014 2

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

• Grants from a town, city, or non-profit are allowed only if it is an acceptable Fannie Mae Community Second (B5-5.1-02, Community Seconds Loan Eligibility (08/26/2014) and is approved by MassHousing (MassHousing requires the documentation review of each grant program every 6 months)

• MassHousing will not purchase loans that include a rebate to the buyer from the licensed real estate broker's commission

Assumable • No

Automated Underwriting

• Only Desktop Underwriter (DU)permitted – • Acceptable Findings:

• “Approved/Eligible” • “Out of Scope” considered on a case by case basis- please contact Operations Manager for details &

consideration • In Express Loan – Mortgage Applied For: Fannie Mae

Bond Program: Massachusetts Housing Bond

Borrower Eligibility

• Owner-Occupied only. • Non-Occupant Co-Borrowers are not permitted • Co-Signors are not permitted • Name Affidavit (AKA) – Required when the borrower(s)’ name(s) on any documents in the loan file does not match

the borrower(s)’ signature(s) and printed name(s) exactly as they appear on the original note. • Power of Attorney (POA) - is only allowed if the borrower is fulfilling a military obligation

Revised December 4, 2014 3

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Borrower Minimum

Contribution

• 1 Unit - 97% LTV / 105% CLTV • 3% down can be from a gift or MassHousing approved grant *

• 2 to 4 Unit - 95% LTV / 105% CLTV • 3% must be borrower’s own funds (remaining 2% may come from a gift or MassHousing approved grant) *

• *CLTV: Second mortgage must be an acceptable Fannie Mae Community Second (B5-5.1-02, Community Seconds Loan Eligibility (08/26/2014)) and approved by MassHousing

Cash Reserves • Established by DU • EXCEPTION: Minimum 6 months reserves required for all multi-family 2-4 units • Reserves may come from Gift

Condo Approval

• Follow Fannie Mae published Condo Guidelines or the below- the more restrictive guideline • Limited Review is allowed in accordance with Fannie Mae Guidelines (for existing properties only) • Lender must verify that MassHousing Condominium Exposure limits have not been exceeded. See

Condominium Projects: MassHousing Exposure limits document at www.emasshousing.com • 2 – 4 Unit New and/or converted condominium presold/sold requirements:

• Two unit – 50% presale/sold required • Three unit – 25% presale/sold requirement • Four unit – 50% presale/sold requirement

• New or newly Converted Projects of more than 4 Units – at least 70% of the total units in the project or subject legal phase must have been conveyed or be under a bona fide contract for purchase to owner –occupant principal residences or second home purchases

Revised December 4, 2014 4

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

• Existing complex: 50% owner occupancy required HOA must have been established • Commercial space: may not exceed 20% of the total square footage of the project • No single entity may own more than 10% of units (other than developer during initial sales period) • All two unit condos must have an executed arbitration agreement • 2 – 4 Unit existing projects require 75% Owner-Occupancy • Financing conversions of 2 to 4 family properties to condominiums:

• No more than one unit per development • No one entity may own more than one unit • 2nd on a 2 unit 1st unit sold/pre-sold must be O/O • 2rd on a 3 unit 1st unit sold/pre-sold must be O/O • 3rd on a 4 unit 1st & 2nd unit sold/pre-sold must be O/O

• Lofts & Studios allowed with kitchen & separate bath • Minimum of 600 square feet living space • Existing Condo projects of more than 4 Units require 50% Owner-Occupancy • HO 6 Policy required when the Master Policy does not cover wall-in and fixtures. Policy must be paid in full

for the first year at time of closing. See SPM Condo guides for additional HO6 requirements • For Condo or PUD developments with 25 or more units, only 25% of the Units may be MassHousing loans.

This percentage is applied to all phases until all phases are completed and will be confirmed using MassHousing’s Condominium Exposure List

Conversion Of Principal Residence

• Not Allowed – Eligible Borrowers must not have any ownership interest in any other property at time of closing

Credit

• Rescoring not allowed • Minimum of most recent 12 months clear credit history • AUS Approved/Accept Findings - Each Borrower should have a minimum of 3 active traditional

trade lines, opened for at least 12 months and have been active during that period. • AUS Approved/Accept Findings and Fico > 640 – Alternative tradelines with a 0x30 in the last 12 months

may be used to meet the 3 tradeline requirements • Bankruptcy wait periods are as of the date of the loan application

o Chapter 7 and Chapter 11 – A 4 year waiting period is required and measured from the discharge or dismissal of the Chapter 7 or Chapter 11 bankruptcy action

Revised December 4, 2014 5

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

o Chapter 13 – A 2 year waiting period is required for Chapter 13 bankruptcies that were discharged

o Chapter 13 – A 4 year waiting period is required for Chapter 13 bankruptcies that were dismissed • Foreclosures – A 7 year waiting period is required, from completion date of the foreclosure to credit report

date. Less than 7 years may be considered on a case by case basis under extenuating circumstances. Refer to www.fanniemae.com for additional details.

• Previous Short Sales (pre-foreclosure) or deed in lieu are subject to waiting periods based upon LTV ratios and are measured from the date of the credit report • Two years 80% maximum LTV • Four years 90% maximum LTV

• Collection Accounts – Regardless of the DU findings, borrowers must pay off in full all collections, judgments, and charge-off accounts prior to closing.

• Unpaid Medical Collections – considered on a case by case basis and must be reviewed and approved by MassHousing Risk Analyst- SPM UW to review with MassHousing UW

• Out Of Scope Credit Requirements: • Non-traditional Credit requirements (only allowed on MassHousing Mortgages with MIPlus) • For borrower’s with no credit score: • Minimum of 4 sources

• Cancelled rent checks • Utility bills • Insurance letter • (12 month history for all 4 – contact MassHousing underwriter for approval)

• All borrowers on a loan that is using non-traditional credit due to and out of scope finding

must complete an acceptable Homebuyer Education Program • Note: follow Fannie Mae requirements for manual underwriting for Out of Scope loans • Must be manually underwritten by a MassHousing Underwriter • A written approval from MassHousing is required to be in the closed loan file

DAP (Down

payment Assistance Programs)

• FNMA approved Community 2nds only

Revised December 4, 2014 6

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

DTI Ratios & Credit Scores

• Ratios and Credit Scores for 1 Unit Property • LTV’s 95.01% to 97%

• minimum credit score 680 • maximum debt ratio of 41%

• LTV’s 95% • minimum credit score 660 • maximum debt ratio of 45%,

• LTV’s <80% • minimum credit score 640 • maximum debt ratio 45%

• Ratios and Credit Scores for 2-4 Unit Property • Gross Ratio Test

• 2 Unit: minimum credit score 680 • maximum total debt ratio without rent 58% • 3 & 4 Unit: minimum credit score 700 • maximum total debt ratio without rent 68%

• Net Ratio Test • 2 to 4 Unit: after rental income deduction, Maximum net ratio 45% • Add 75% of rental income for a 2 unit, and • 65% for a 3 or 4 unit, for tenant occupied units; (must have proof tenant is remaining) or • Add 50% of market rent for vacant rental unit (from appraisal)

DU Findings (Desktop

Underwriter)

• LTV < 80% - Approved Eligible Findings only • LTV > 80% - Approved Eligible or Out of Scope ONLY if the finding is due to insufficient credit

Deed Restriction

• Affordable Housing Deed Riders must be approved in writing by MassHousing and a copy of the

approval must be in the closed loan file • Contact Kathy Moore @ [email protected] or 617-854-1063 • Underwriting Considerations

• Duration of Resale restriction • Either Resale restriction terminates at foreclosure or deed in-in-lieu of foreclosure, or • Resale Restriction survives foreclosure

• Calculation of LTV • If Resale restriction terminates at foreclosure or deed in-in-lieu of foreclosure, then MassHousing

allows either the appraised value without restriction, or lesser of sales price re-sale or appraised value • If Resale Restriction survives foreclosure, then Appraised value must be the sales price or appraised

value with restrictions

Revised December 4, 2014 7

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

• If the restriction terminates at foreclosure or deed in-in-lieu of foreclosure • Use Market Value without restriction • Appraiser must describe within the appraisal:

• The resale restriction • Sponsoring or monitoring agent • Basis of the subsidy program • Borrower requirements

• Appraisal Report to include the statement: “This appraisal is made on the basis of a hypothetical condition that the property rights being appraised are without resale restriction and other restrictions that are terminated automatically upon the latter of foreclosure or the expiration of any applicable redemption period, or upon recordation of a deed-in-lieu of foreclosure.”

• If Resale Restriction survives foreclosure • Property should be appraised at the subsidized value or FMV, which ever is less • Appraiser must describe within appraisal

• The resale restriction • Sponsoring or monitoring agent • Basis of the subsidy program • Borrower requirements

• Appraisal report must note the existence of the resale restriction and comment on any impact the resale restrictions have on the property’s value and marketability.

• Loan Settlement Consideration: • Title Policy must insure that any present or future violation of the restricted covenants and conditions

will not result in a forfeiture or reversion of title or a lien for damages, or have an adverse impact on the fair market value of the property

EEM • Not Allowed

Eligible Properties

• Owner Occupied, Principal Residences that consist of one, two, three, and four-residential units. Existing Properties and New Construction.

• No more than 15% commercial space is allowed in a subject property • Minimum square footage is 600 square feet for all property types. • Party Wall Agreement Requirements: Any property subject to a mutual easement agreement for joint

driveways or party walls require that all future owners have unlimited Unrestricted use of said driveway or party wall

• Private Road Requirements: must have: • A permanent recorded “easement” (nonexclusive, non-revocable, without trespass) from the

Revised December 4, 2014 8

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

property to a public street or road, and provisions for road maintenance. The Easement must provide: • Who is responsible for payment of repairs, including each party’s representative share; • Default remedies in the event a party to the agreement or covenant fails to comply with his or

her obligations; and, • The effective term must be perpetual and binding on all future owners

• 2 Unit New Construction - allowed only in Targeted Areas. Targeted City Areas: Boston, Chelsea, Cambridge, Everett, Fall River, Lawrence, Lynn, North Adams, and Somerville

• 3-4 Units – Existing structures must be Owner Occupied and must have been first occupied as a residence at least 5 years prior to the closing date. Age of property must be a minimum of 5 years as shown on the appraisal. Review appraisal to ensure that no comments within the appraiser indicate that the 3-4 unit subject property has not been occupied for at least 5 years.

• Ineligible Property: • Two residential building on one lot • > 15% commercial space on the subject property • < 600 square feet • Manufactured Homes • Non-Warrantable Condos

Eligible Purpose • Purchase

Verbal Employment Verification

Requirements

• Salaried/Wage Earners: • Verbal VOE must be performed within 10 business days prior to the date of the note • Lender must verify the employer’s company name and telephone number through an independent

third party, such as a CPA, www.theworknumber.com, phone book, www.anywho.com, etc. • Lender must also verify the employer’s contact information, such as name, address, and phone

number independently through directory assistance (411), the white pages, etc. • Self Employed Borrowers:

• Lenders must verify the existence of the borrower’s business within 30 calendar days prior to the note.

• Existence of the borrower’s business must be verified by a third party, such as a CPA, regulatory agency, or the applicable licensing bureau if possible.

• Borrower’s business address and phone listing must be verified by using the telephone book, the internet, or 411 Directory Assistance

• If the contact is made verbally, then a verbal verification of employment must be completed to

Revised December 4, 2014 9

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

document the source of the verification information

Escrow Hold-back

• Allowed, provided it is for minor conditions or deferred maintenance that will not affect the livability, soundness, or structural integrity of the property at a cost not to exceed $7500.

• Written estimate of repair items should be obtained by a licensed professional. • Escrow holdback should be 1.5 times the actual amount • All other SPM Standard Escrow Hold-back policy requirements apply as follows: • Escrow Hold-backs are permitted and funds may be withheld in escrow only if (1) ADVERSE WEATHER

conditions prevent completion of major outdoor items, usually new construction items (walkways, driveways, exterior painting, landscaping, garages, etc.), or (2) DEFERRED MAINTENANCE when the seller will not pay or allow work to be done before close, usually on REO properties.

• Escrow Hold-backs for adverse weather conditions requirements: • Withholding 1 ½ times the dollar amount necessary to complete the postponed items (as documented by

an “Estimate” from a licensed professional) from the proceeds due the seller at closing. • Fully completed and executed SPM Escrow Holdback Agreement – Funds to be held by Closing Agent • HUD 92300 “Mortgage Assurance of Completion” fully completed, executed, & dated • The items that need to be completed do not affect the livability of the house, and the dwelling is

habitable, safe, and complete if new construction • The deferred work cannot be completed prior to the close, but will be completed within 90 business days

of closing • It is the Regional Operations Center responsibility to follow up with a 1004D/CIR to evidence that

all the work has been satisfactorily completed and all conditions 92800.5B Conditional Commitment of the have been complied with.

• It is the Regional Operations Center responsibility to follow up with a revised HUD 1 settlement statement showing the disbursement of funds for the repairs & reinspection fee.

• Escrow Hold-backs for deferred maintenance requirements: • Withholding 1 ½ times the dollar amount necessary to complete the postponed items (as documented by

an “Estimate” from a licensed professional) from the proceeds due the seller at closing. • Fully completed and executed SPM Escrow Holdback Agreement – Funds to be held by Closing Agent • UW to review & approve Work Estimate to ensure it is reasonable to expect all repairs to be completed

within 10 business days and adequately address the repair.

First-time Homebuyer

• Any borrower who has not held an ownership interest in a principal residence at any time during the

Revised December 4, 2014 10

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Definition three years preceding the closing date of the new mortgage. • All First time homebuyers must provide 3 years of completed Federal 1040’s tax returns

Flood Insurance

• Reminder: Life of Loan Flood zone determination and Flood insurance requirements must be met as per SPM Policy.

• For additional information, you may use this link: http://www.fema.gov/

Flipping Policy

• Standard SPM Flipping policy • OPS “Flip” field In UW screen must be correctly populated. (Note: instructions were previously

communicated and requires field to be completed for all flips resold 0180 days)- • SFR Detached/Attached, Condo, PUD, 1-4 Units • Primary Residence • Maximum LTV/CLTV of 95% • The maximum number of ownership transfers within the most recent 90 days is limited to ONE. (E.G.

multiple title/ownership transfers within a 90 day period is not permitted) • If the Seller is an entity (LLC, trust, etc), documentation showing legal registration of the entity such as

articles of operation with the seal, or a business license. • The borrower(s) can have no affiliation with the entity of any kind

• Standard SPM policy regarding acceptable purchase contract documentation applies, including but not limited to:

• Complete executed purchase contract is in file with all addenda attached and reviewed by UW • Seller is currently on title and must remain on title throughout closing

• The Underwriter will be responsible to evaluate appraisal report to ensure: • The subject property’s sales history makes sense for the market as addressed on appraisal report • Appraiser must confirm property improvements made for properties that were purchased through a

distressed sale and where substantial renovations to the property were made and is now selling for a profit

• The renovations must be documented and verified • Increase in value must be supported by Appraiser’s comments and photo’s reflecting Seller’s improvements/rehab/capital improvements were made to the property beyond normal “clean

up”, repairs and refurbish

Geographic Restriction

• Limited to properties located in the State of Massachusetts only

Revised December 4, 2014 11

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

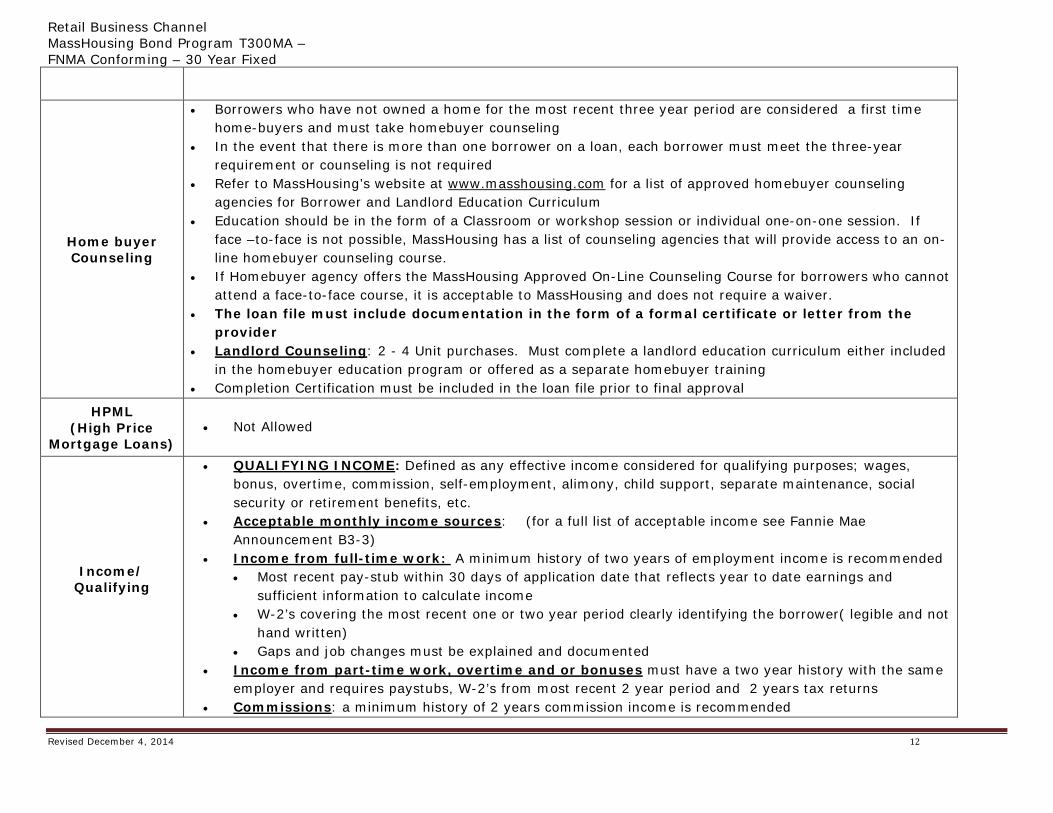

Home buyer Counseling

• Borrowers who have not owned a home for the most recent three year period are considered a first time home-buyers and must take homebuyer counseling

• In the event that there is more than one borrower on a loan, each borrower must meet the three-year requirement or counseling is not required

• Refer to MassHousing’s website at www.masshousing.com for a list of approved homebuyer counseling agencies for Borrower and Landlord Education Curriculum

• Education should be in the form of a Classroom or workshop session or individual one-on-one session. If face –to-face is not possible, MassHousing has a list of counseling agencies that will provide access to an on-line homebuyer counseling course.

• If Homebuyer agency offers the MassHousing Approved On-Line Counseling Course for borrowers who cannot attend a face-to-face course, it is acceptable to MassHousing and does not require a waiver.

• The loan file must include documentation in the form of a formal certificate or letter from the provider

• Landlord Counseling: 2 - 4 Unit purchases. Must complete a landlord education curriculum either included in the homebuyer education program or offered as a separate homebuyer training

• Completion Certification must be included in the loan file prior to final approval

HPML (High Price

Mortgage Loans) • Not Allowed

Income/ Qualifying

• QUALIFYING INCOME: Defined as any effective income considered for qualifying purposes; wages, bonus, overtime, commission, self-employment, alimony, child support, separate maintenance, social security or retirement benefits, etc.

• Acceptable monthly income sources: (for a full list of acceptable income see Fannie Mae Announcement B3-3)

• Income from full-time work: A minimum history of two years of employment income is recommended • Most recent pay-stub within 30 days of application date that reflects year to date earnings and

sufficient information to calculate income • W-2’s covering the most recent one or two year period clearly identifying the borrower( legible and not

hand written) • Gaps and job changes must be explained and documented

• Income from part-time work, overtime and or bonuses must have a two year history with the same employer and requires paystubs, W-2’s from most recent 2 year period and 2 years tax returns

• Commissions: a minimum history of 2 years commission income is recommended

Revised December 4, 2014 12

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

• To verify Commission income: <25% of total income require most recent paystub, completed Form 1005 or Form 1005(S), W-2 and tax returns for the most recent two year period

• To verify Commission income >25%: copies of federal income tax for the past two years and either a completed 1005 or 1005(S) form and borrowers most recent paystub and IRS W-2 for most recent two year period

• Self Employed Borrowers: • Lender must verify that borrower has at least a 24 month history as evidenced by two years personal

and business (if applicable) federal tax returns • Supporting Documentation

• Determine consistency in income stream • Overall income is steady or increasing from year to year

• Income from alimony, child support and separate maintenance: • A minimum of six months of documented receipt of income is required for alimony and child support

income or per DU findings • A copy of a divorce decree or separation agreement (if the divorce is not final) or another type of

written legal agreement or court decree describing the payment terms for the alimony or child support that verifies three years’ continuance

• Documentation that verifies any applicable state law that mandates alimony, child support, or separate maintenance payments, which must specify the conditions under which the payments must be made (Court Order)

• If a borrower who is separated does not have a separation agreement that specifies alimony or child support payments, the lender should not consider any proposed or voluntary payments as income

• Review the payment history to determine its suitability as stable qualifying income • Unemployment income can only be used if:

• It is seasonal unemployment compensation, clearly associated with seasonal layoffs, expected to recur, and reported on the borrower’s signed federal income tax returns

• Non-taxable income may be “grossed up” by 15% for purposes of ratio calculations but if “grossed up” the same figure must be used for calculating compliance income

• Social security, and disability or VA benefits from the borrower’s own account requires the award letter and proof of current receipt, or, if from another person’s account, award letter and proof of current receipt • Verify proof of 3 years continuance for both

• Retirement or pension income; award letter; 2 years federal tax returns; IRS W-2 or 1099 and proof of current receipt • If the retirement income is from a distribution of a 401(k) IRA or Keogh retirement account determine

Revised December 4, 2014 13

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

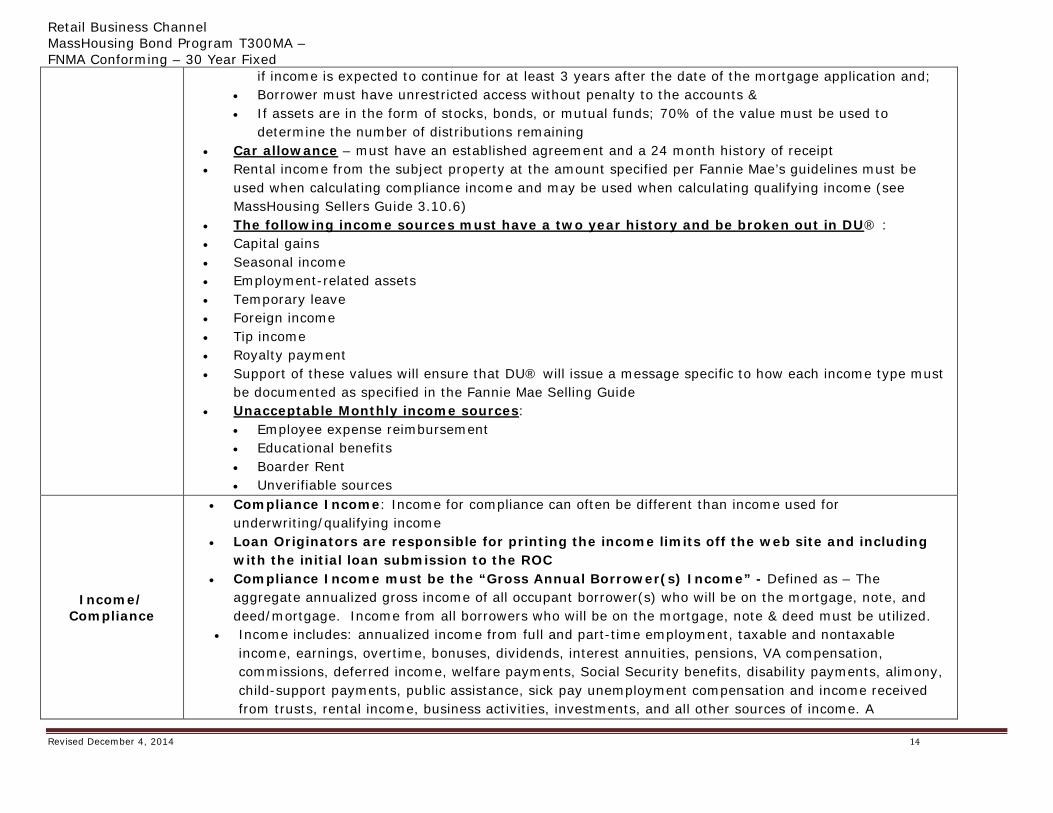

if income is expected to continue for at least 3 years after the date of the mortgage application and; • Borrower must have unrestricted access without penalty to the accounts & • If assets are in the form of stocks, bonds, or mutual funds; 70% of the value must be used to

determine the number of distributions remaining • Car allowance – must have an established agreement and a 24 month history of receipt • Rental income from the subject property at the amount specified per Fannie Mae’s guidelines must be

used when calculating compliance income and may be used when calculating qualifying income (see MassHousing Sellers Guide 3.10.6)

• The following income sources must have a two year history and be broken out in DU® : • Capital gains • Seasonal income • Employment-related assets • Temporary leave • Foreign income • Tip income • Royalty payment • Support of these values will ensure that DU® will issue a message specific to how each income type must

be documented as specified in the Fannie Mae Selling Guide • Unacceptable Monthly income sources:

• Employee expense reimbursement • Educational benefits • Boarder Rent • Unverifiable sources

Income/ Compliance

• Compliance Income: Income for compliance can often be different than income used for underwriting/qualifying income

• Loan Originators are responsible for printing the income limits off the web site and including with the initial loan submission to the ROC

• Compliance Income must be the “Gross Annual Borrower(s) Income” - Defined as – The aggregate annualized gross income of all occupant borrower(s) who will be on the mortgage, note, and deed/mortgage. Income from all borrowers who will be on the mortgage, note & deed must be utilized.

• Income includes: annualized income from full and part-time employment, taxable and nontaxable income, earnings, overtime, bonuses, dividends, interest annuities, pensions, VA compensation, commissions, deferred income, welfare payments, Social Security benefits, disability payments, alimony, child-support payments, public assistance, sick pay unemployment compensation and income received from trusts, rental income, business activities, investments, and all other sources of income. A

Revised December 4, 2014 14

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

percentage of rental income from subject property (that which was used to qualify) must be included. Nontaxable income must be included at an amount used to qualify (including the grossed up amount (at no more than 115%) if used in qualifying

• All borrowers on the note must be on the mortgage and deed • No person may be added to the mortgage or deed after closing • Multi-family Compliance Income must include a percentage of rental income • Non-taxable income for Compliance Income must be calculated based on the same amount used for

qualifying income

Ineligible Properties

• 3-4 Unit New Construction is not eligible • No more than 15% commercial space is allowed in a subject property • Manufactured housing (mobile homes and cooperatives) are not eligible • Minimum square footage is 600 square feet for all property types

Revised December 4, 2014 15

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

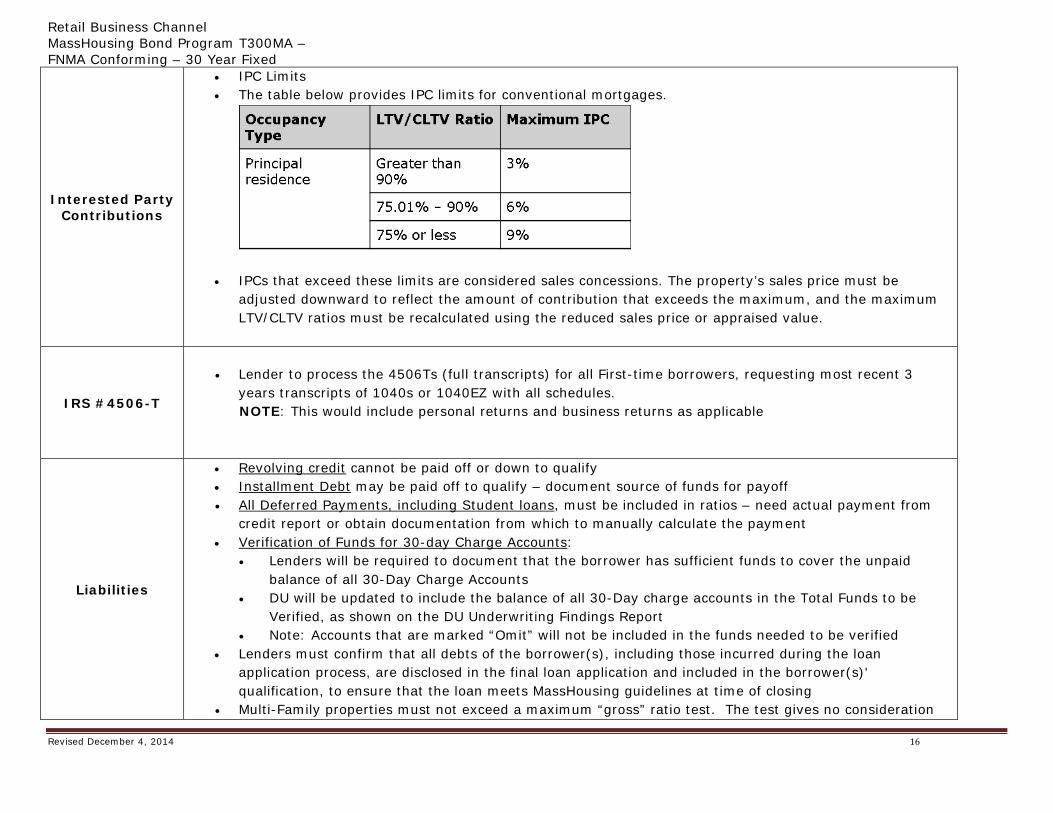

Interested Party Contributions

• IPC Limits • The table below provides IPC limits for conventional mortgages.

• IPCs that exceed these limits are considered sales concessions. The property’s sales price must be

adjusted downward to reflect the amount of contribution that exceeds the maximum, and the maximum LTV/CLTV ratios must be recalculated using the reduced sales price or appraised value.

IRS #4506-T

• Lender to process the 4506Ts (full transcripts) for all First-time borrowers, requesting most recent 3

years transcripts of 1040s or 1040EZ with all schedules. NOTE: This would include personal returns and business returns as applicable

Liabilities

• Revolving credit cannot be paid off or down to qualify • Installment Debt may be paid off to qualify – document source of funds for payoff • All Deferred Payments, including Student loans, must be included in ratios – need actual payment from

credit report or obtain documentation from which to manually calculate the payment • Verification of Funds for 30-day Charge Accounts:

• Lenders will be required to document that the borrower has sufficient funds to cover the unpaid balance of all 30-Day Charge Accounts

• DU will be updated to include the balance of all 30-Day charge accounts in the Total Funds to be Verified, as shown on the DU Underwriting Findings Report

• Note: Accounts that are marked “Omit” will not be included in the funds needed to be verified • Lenders must confirm that all debts of the borrower(s), including those incurred during the loan

application process, are disclosed in the final loan application and included in the borrower(s)' qualification, to ensure that the loan meets MassHousing guidelines at time of closing

• Multi-Family properties must not exceed a maximum “gross” ratio test. The test gives no consideration

Revised December 4, 2014 16

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

to rental income from the subject on 2 – 4 Units and is the borrower’s gross income against gross expense

• Two unit properties cannot exceed 58% gross ratio • Three-to-four unit properties cannot exceed 68% gross ratio

Loan Fees • MassHousing Processing - $300 • Tax Service - $75 • Insurance Tracking Fee - $31

Manual UW • Not Allowed

Max Borrower Points

• Maximum of 2 points charged to Borrower – 2% is inclusive of any origination fee, processing fee, underwriting fee or any Lender fee. (Non 3rd Party)

Max.# RE owned • Borrower may not have any ownership interest in any other property at time of closing and must occupy

the subject property as their primary residence with occupancy within 60 days of closing

Maximum Loan Amount

http://www.massresources.org/masshousing-loans.html#income • Refer to link for Maximum Loan Limits based on actual property location • Targeted Areas are – Boston, Chelsea, Cambridge, Everett, Fall River, Lawrence, Lynn, North

Adams, and Somerville • 1 Unit - $417,000 Max • 2 Unit - $533,850 Max • 3 Unit - $645,300 Max • 4 Unit - $801,950 Max

MERS

• Lenders must close all loans using Uniform Instrument 3022(MERS). Note and Mortgage must include

unique 18-digit MIN that will be generated by MassHousing at time of funds reservation. MERS Members may use the MIN which is generated by their origination system.

MI Plus

• MI Plus is an endorsement to all MI policies issued after July 1, 2004, by the Mortgage Insurance Fund. MI Plus provides benefit payments in the event the borrower becomes unemployed and is eligible to receive benefits from the Commonwealth of Massachusetts Department of Labor, Division of Unemployment Assistance (DUA). There is no additional premium above the cost of the MI.

• Lender Paid MI is available – Refer to Rate sheets for pricing

Mortgagor’s Affidavit

• Required on all loans

Revised December 4, 2014 17

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

• Borrower(s) must sign at time of application and must sign the “Reaffirmation at Title Closing” • Loan Officer must sign at time of application

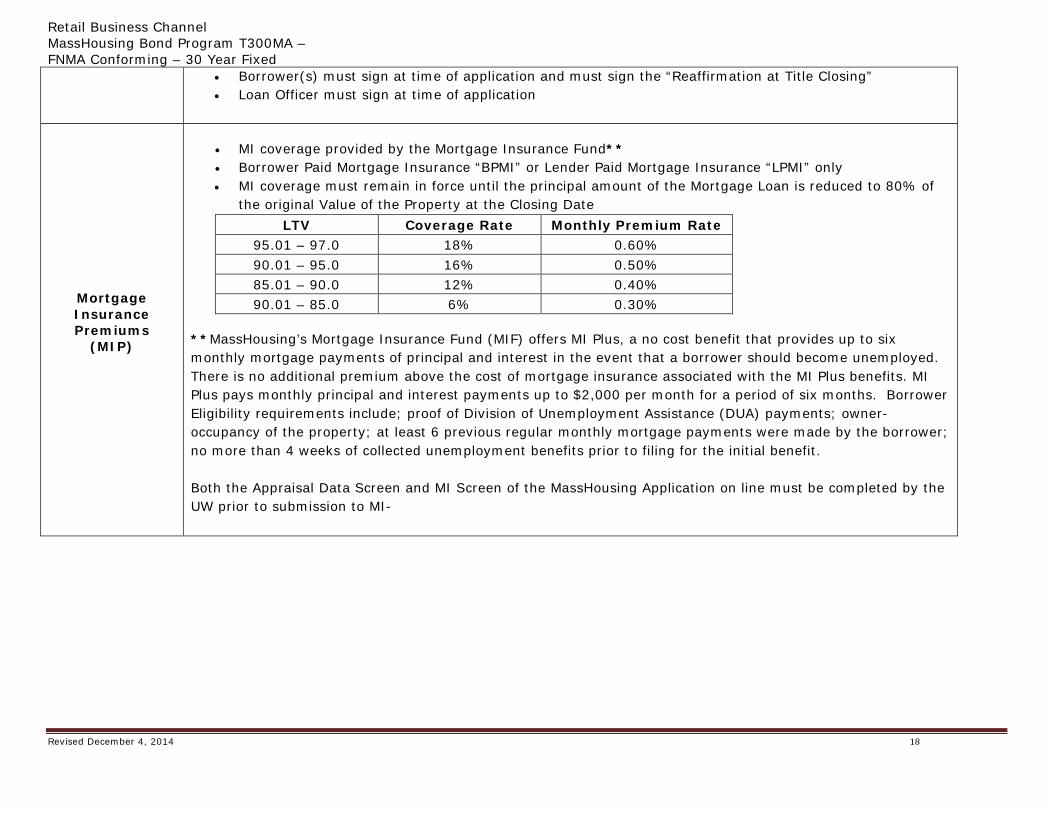

Mortgage Insurance Premiums

(MIP)

• MI coverage provided by the Mortgage Insurance Fund** • Borrower Paid Mortgage Insurance “BPMI” or Lender Paid Mortgage Insurance “LPMI” only • MI coverage must remain in force until the principal amount of the Mortgage Loan is reduced to 80% of

the original Value of the Property at the Closing Date LTV Coverage Rate Monthly Premium Rate

95.01 – 97.0 18% 0.60% 90.01 – 95.0 16% 0.50% 85.01 – 90.0 12% 0.40% 90.01 – 85.0 6% 0.30%

**MassHousing’s Mortgage Insurance Fund (MIF) offers MI Plus, a no cost benefit that provides up to six monthly mortgage payments of principal and interest in the event that a borrower should become unemployed. There is no additional premium above the cost of mortgage insurance associated with the MI Plus benefits. MI Plus pays monthly principal and interest payments up to $2,000 per month for a period of six months. Borrower Eligibility requirements include; proof of Division of Unemployment Assistance (DUA) payments; owner-occupancy of the property; at least 6 previous regular monthly mortgage payments were made by the borrower; no more than 4 weeks of collected unemployment benefits prior to filing for the initial benefit. Both the Appraisal Data Screen and MI Screen of the MassHousing Application on line must be completed by the UW prior to submission to MI-

Revised December 4, 2014 18

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Revised December 4, 2014 19

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

New

Construction

• 1 - Family Allowed • 2 - Family Allowed only if in Targeted Area: (Target Area - Boston, Cambridge, Chelsea, Everett, Lynn,

Lawrence, Fall River, North Adams, Somerville) • 3 - 4 Family NOT ALLOWED

Revised December 4, 2014 20

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Occupancy

• Primary Residence / Owner Occupied Only • Additional Occupants: An occupant of the residence, related or unrelated, need not meet the three year

ownership interest requirement if this occupant is not a Mortgagor.

Pre-Closing Requirements

• DU Final Submission • Lender is responsible for performing a final DU submission to ensure that the data matches

emasshousing.com and the final 1003 and 1008 • Lenders should be reviewing product type, property type, loan purpose, sale price and appraised

value as well as: • Terms of transaction (rate, loan amount, sales price, address) • Present and proposed housing payment • First time homebuyers are correctly noted in DU

• Verified income found on the final FNMA form 1003 or 1008 may not exceed the amounts found in DU or www.emasshousing.com

• Borrowers Gross Annual Income in emasshousing.com must match the documented income on final 1003 & 1008 to ensure loan meats MassHousing Compliance

• Lender must confirm the accuracy of Loan Officer name and License # in emasshousing.com

• The lender must reflect the minimum amount of assets needed to complete the transaction • The lender must also reflect any and all gift funds • Any assets entered into DU must be documented regardless if they are needed for closing • Lenders will receive a discrepancy condition from Titan when a material discrepancy exists between

the final 1003 and the AUS, which might require the lender to resubmit the file to DU, for example: •

Power of Attorney • The use of Power of Attorney is only allowed if the borrower is fulfilling a military obligation

Revised December 4, 2014 21

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Private Road

• Private Road Maintenance agreements must have a permanent recorded “easement” (nonexclusive, non-revocable, without trespass) from the property to a public street or road, and provisions for road maintenance. The Easement must provide:

• Who is responsible for payment of repairs, including each party’s representative share; • Default remedies in the event a party to the agreement or covenant fails to comply with his or her

obligations; and, • The effective term must be perpetual and binding on all future owners

Recapture

• First-Time Homebuyers obtaining financing through the sale of tax exempt bonds could be subject to

recapture. • Recapture is only due when:

• The home is sold within nine (9) years; and • The home is sold for a profit; and, • The borrower’s income increases substantially based on the federal recapture income limitations

tables for the year and the market area • NOTE: MassHousing will reimburse borrowers for the amount of recapture tax paid to the IRS if they sell

or transfer their home in the nine years following loan closing. MassHousing will provide disclosure to the borrowers after closing if they are subject to recapture, with information on what is required by MassHousing to reimburse borrowers for payment of recapture tax to IRS

Rate Lock

• Rate Locks/Reservations must be completed by Corporate Lock Desk and cannot be requested until the loan is final approved and CTC-

• Reservations and Rate Locks must be completed within 20 days of the DU used for Final Approval. • Submit a Rate Lock request form accompanied by the Final SPM approval prior to 2:30 PM EST- via e-

mail to [email protected]. • Secondary will lock the loan for 30 days with the investor, will input the lock information in OPS, and will

notify the ROC staff the lock is complete • ROC Staff can view the lock and upload to the efolder

Revised December 4, 2014 22

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Secondary Financing/ DPA

• Grants from a town, city, or non-profit are allowed only if it is an acceptable Fannie Mae Community Second (B5-5.1-02, Community Seconds Loan Eligibility (08/26/2014) and is approved by MassHousing (MassHousing requires the documentation review of each grant program every 6 months)

Title Policy Requirements

• Survey or Plot map required for all loans unless title policy insures MassHousing’s valid first lien position against survey defects.

• Survey must not be over 120 days old at the time of loan closing

Verbal Verification of Employment

• Verification of Employment History: • Lenders must verify the employer’s company name and telephone number through an independent third

party, such as a CPA, www.theworknumber.com, phone book, www.anywho.com, etc., and compare the information to the loan application.

• Employer contact information must be independently verified by the lender including name of the employer, address and phone number verified through directory assistance (411 directory assistance, the white pages, etc.)

• Employment should be verified through the employer's Human Resources department, Payroll department, or with the company's owner.

• If the existence of the employer cannot be verified, the loan file is not eligible for purchase by MassHousing.

• The verbal verification must include the name and title of the person who confirmed employment, the date of the call, the source of the phone number, and the name and title of the person performing the review from the lending institution.

• Another verbal verification of employment (VOE) must be performed within 10 business days prior to the date of the note

• Verification of Self Employment: • Lenders must verify the existence of the borrower’s business within 30 calendar days prior to the date of

the note. • The existence of the borrower’s business must be verified by a third party, such as a CPA, regulatory

agency, or the applicable licensing bureau if possible. • The borrower’s business address and phone listing must be verified by using a public information source

such as the telephone book, the internet, or 411 Directory Assistance

Revised December 4, 2014 23

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Underwriting

• Underwriter is responsible for completing the on line application found at Emasshousing.com-

Required Documentation

https://www.emasshousing.com/portal/server.pt/community/login/300/first_mortgage_forms See Below

Revised December 4, 2014 24

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Revised December 4, 2014 25

Retail Business Channel MassHousing Bond Program T300MA – FNMA Conforming – 30 Year Fixed

Revised December 4, 2014 26