Marktausblick für Rostfreie Stähle -...

39

© Copyright SMR GmbH 2016 www.smr.at -0- Marktausblick für Rostfreie Stähle Fokus auf Europa u nd Deutschland © SMR GmbH - Steel & Metals Market Research This data collection may not be copied, published or disclosed to third parties without the permission of SMR GmbH. Edelstahl Rostfrei Convent 2016 28 st January 2016 Essen, Germany presented by Markus A. Moll Managing Director Steel & Metals Market Research

Transcript of Marktausblick für Rostfreie Stähle -...

© Copyright SMR GmbH 2016

www.smr.at- 0 -

Marktausblick für Rostfreie Stähle

Fokus auf Europa und Deutschland

© SMR GmbH - Steel & Metals Market Research

This data collection may not be copied, published or disclosed to third parties without the permission of SMR GmbH.

Edelstahl Rostfrei Convent 201628st January 2016

Essen, Germany

presented by

Markus A. Moll

Managing Director

Steel & Metals Market Research

© Copyright SMR GmbH 2016

www.smr.at- 1 -C

ON

FE

RE

NC

ES

2016

PR

OJE

CT

S

2014

Austria

GR

OU

P / T

EA

M /

LO

CA

TIO

N

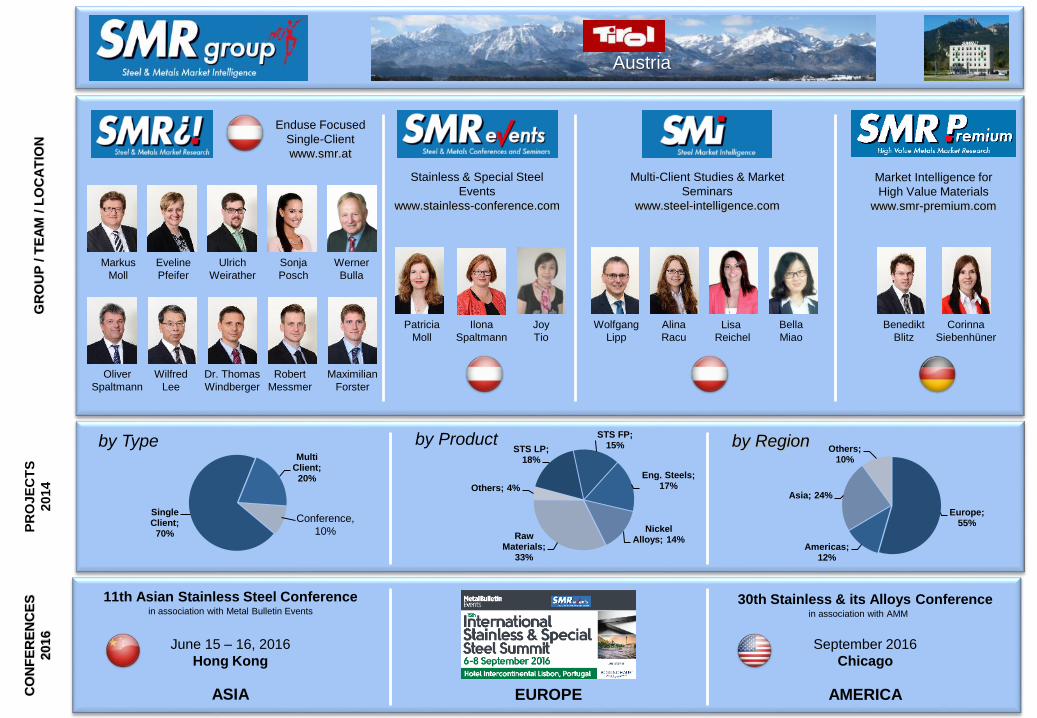

by Type by Regionby ProductSTS LP;

18%

STS FP; 15%

Eng. Steels; 17%

Nickel Alloys; 14%Raw

Materials; 33%

Others; 4%

Europe; 55%

Americas; 12%

Asia; 24%

Others; 10%

Single Client;

70%

Multi Client;

20%

Conference,

10%

Benedikt

Blitz

Wolfgang

Lipp

Alina

Racu

Patricia

Moll

Ilona

Spaltmann

Joy

Tio

Enduse Focused

Single-Client

www.smr.at

Multi-Client Studies & Market

Seminars

www.steel-intelligence.com

Stainless & Special Steel

Events

www.stainless-conference.com

Corinna

Siebenhüner

Market Intelligence for

High Value Materials

www.smr-premium.com

Oliver

Spaltmann

Dr. Thomas

Windberger

Eveline

Pfeifer

Markus

Moll

Sonja

Posch

Ulrich

Weirather

Robert

Messmer

Wilfred

Lee

Werner

Bulla

Maximilian

Forster

Lisa

Reichel

Bella

Miao

ASIA EUROPE AMERICA

in association with Metal Bulletin Events

June 15 – 16, 2016

Hong Kong

11th Asian Stainless Steel Conferencein association with AMM

September 2016

Chicago

30th Stainless & its Alloys Conference

© Copyright SMR GmbH 2016

www.smr.at- 2 -

Fahrplan

1. Überblick

2. Blick auf Deutschland

3. Ausblick 2016

4. China – Eine Zeitbombe?

5. Fokus auf Rohstoffe

© Copyright SMR GmbH 2016

www.smr.at- 3 -

CAGR 1950 – 2015e:

5 % p.a.

Deflated 304 price

(Index base since 1967)

100 Years of Success …Stainless Crude Steel Production vs. Price

© Copyright SMR GmbH 2016

www.smr.at- 4 -

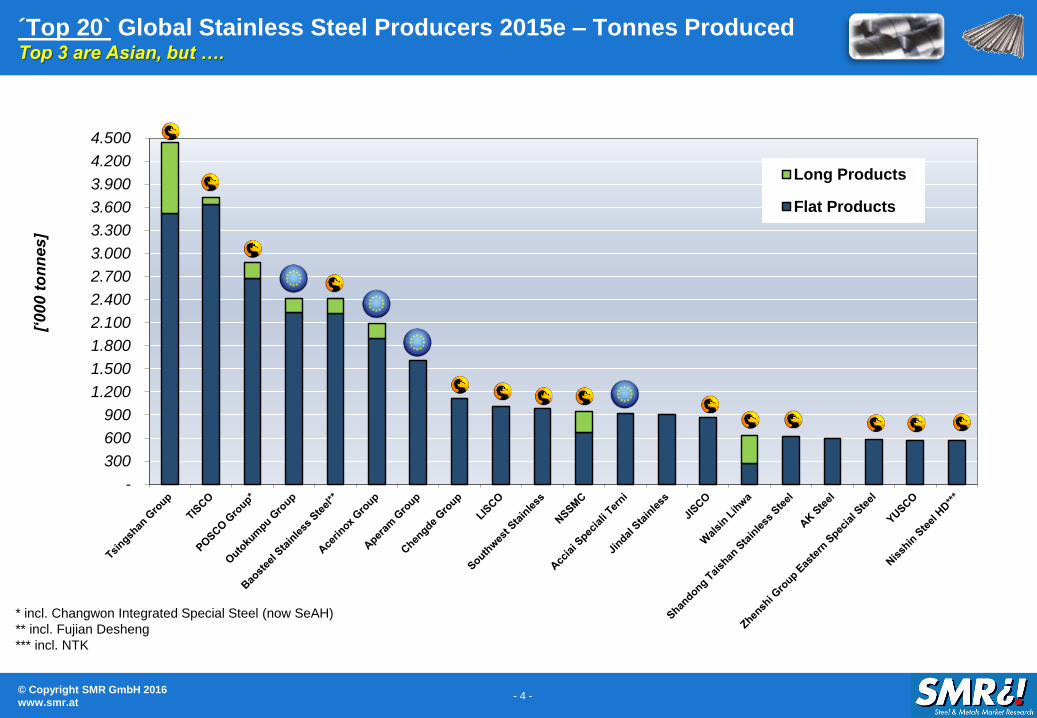

-

300

600

900

1.200

1.500

1.800

2.100

2.400

2.700

3.000

3.300

3.600

3.900

4.200

4.500

[‘0

00

to

nn

es

]

Long Products

Flat Products

´Top 20` Global Stainless Steel Producers 2015e – Tonnes ProducedTop 3 are Asian, but ….

* incl. Changwon Integrated Special Steel (now SeAH)

** incl. Fujian Desheng

*** incl. NTK

© Copyright SMR GmbH 2016

www.smr.at- 5 -

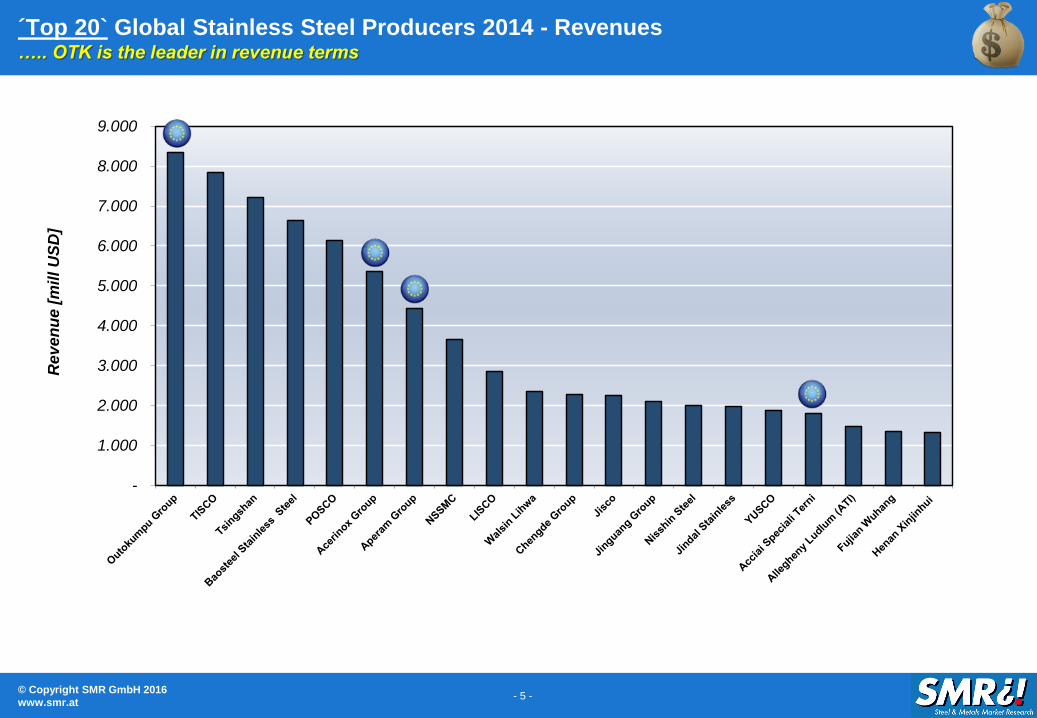

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

Rev

en

ue [

mill U

SD

]

´Top 20` Global Stainless Steel Producers 2014 - Revenues….. OTK is the leader in revenue terms

© Copyright SMR GmbH 2016

www.smr.at- 6 -

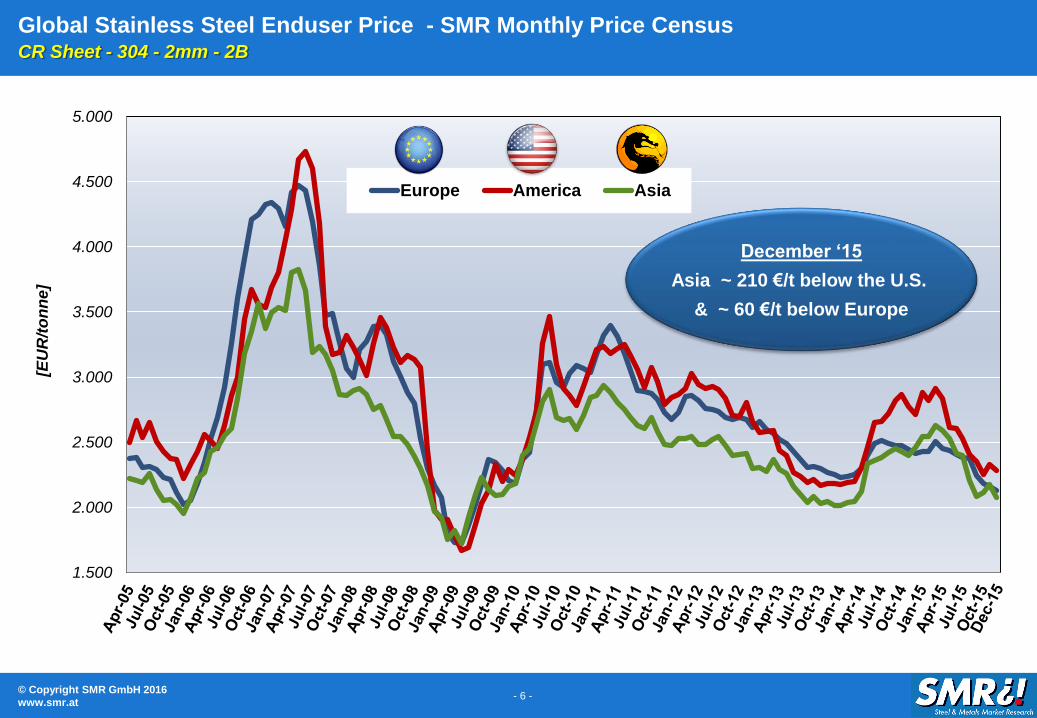

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

[EU

R/t

on

ne

]

Europe America Asia

Global Stainless Steel Enduser Price - SMR Monthly Price CensusCR Sheet - 304 - 2mm - 2B

December ‘15

Asia ~ 210 €/t below the U.S.

& ~ 60 €/t below Europe

© Copyright SMR GmbH 2016

www.smr.at- 7 -

Stainless Steel Long Products: European* Market Volume 2000 – 2015e

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

-

150

300

450

600

750

900

1.050

1.200

1.350

1.500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015e

Imp

ort

Pe

ne

tra

tio

n

[ ´0

00 m

etr

ic t

on

ne

s]

European Demand external Imports Import Penetration

* incl. Turkey

Included:

for Demand: - Hot rolled bars - Forged bars - Wire rod

for Imports: - Hot rolled bars - Forged bars - Wire rod - Wire - Bright bars - Profiles

© Copyright SMR GmbH 2016

www.smr.at- 8 -

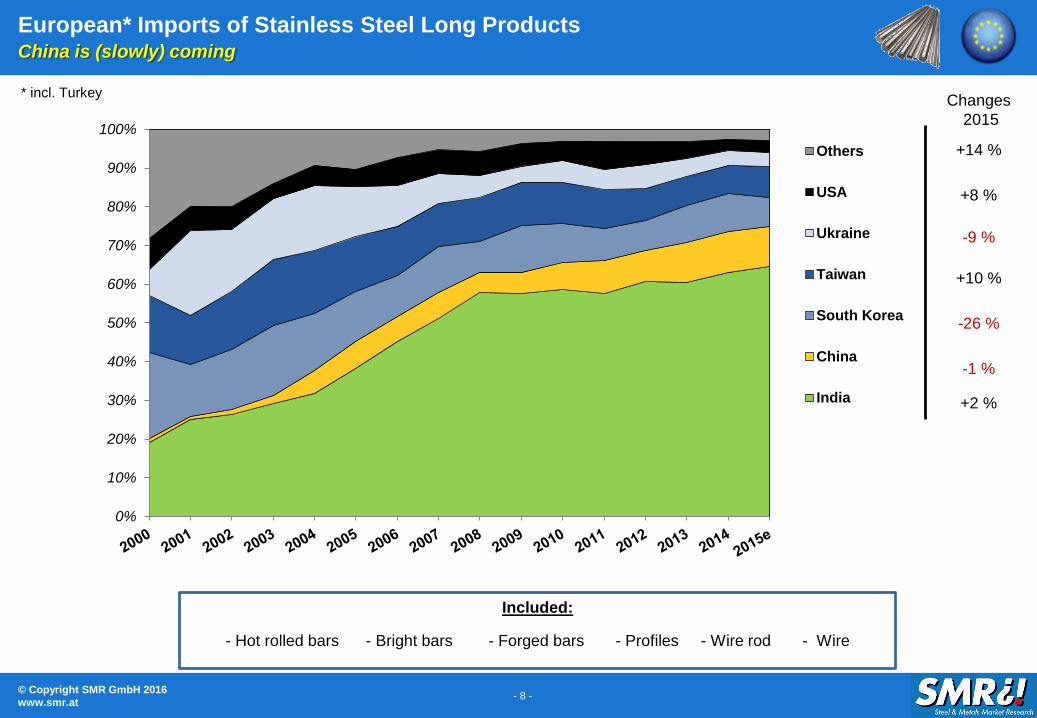

European* Imports of Stainless Steel Long ProductsChina is (slowly) coming

* incl. Turkey

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Others

USA

Ukraine

Taiwan

South Korea

China

India

Included:

- Hot rolled bars - Bright bars - Forged bars - Profiles - Wire rod - Wire

Changes

2015

+2 %

-1 %

-26 %

+10 %

-9 %

+8 %

+14 %

© Copyright SMR GmbH 2016

www.smr.at- 9 -

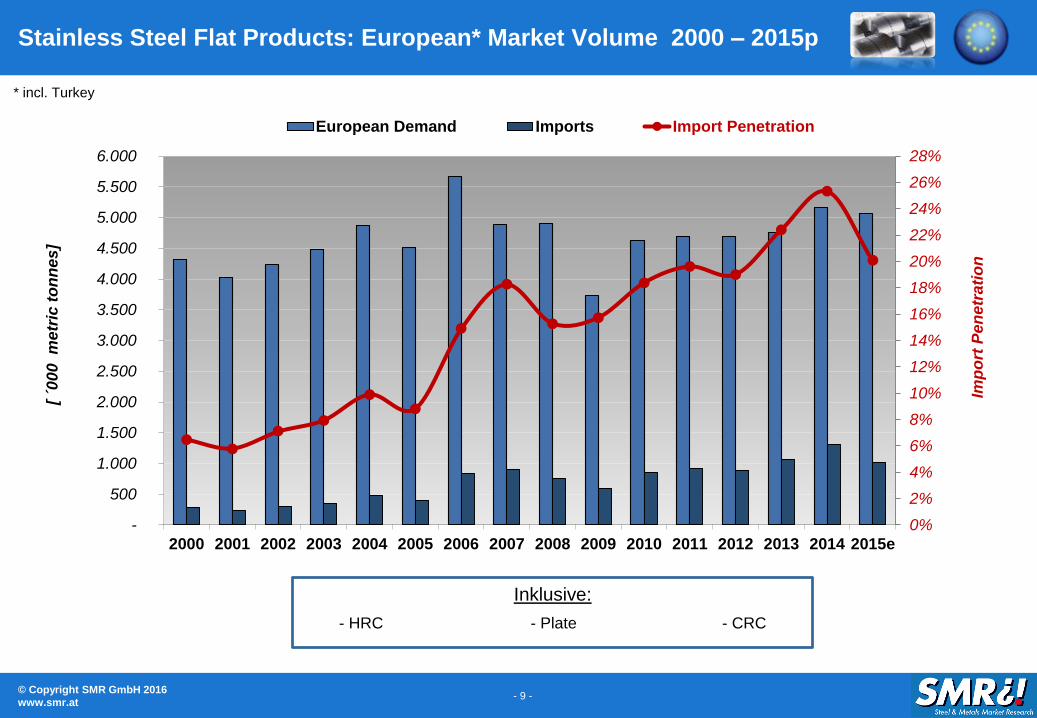

Stainless Steel Flat Products: European* Market Volume 2000 – 2015p

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

-

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5.500

6.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015e

Imp

ort

Pe

ne

trati

on

[ ´0

00

m

etr

ic t

on

nes

]

European Demand Imports Import Penetration

Inklusive:

- HRC - Plate - CRC

* incl. Turkey

© Copyright SMR GmbH 2016

www.smr.at- 10 -

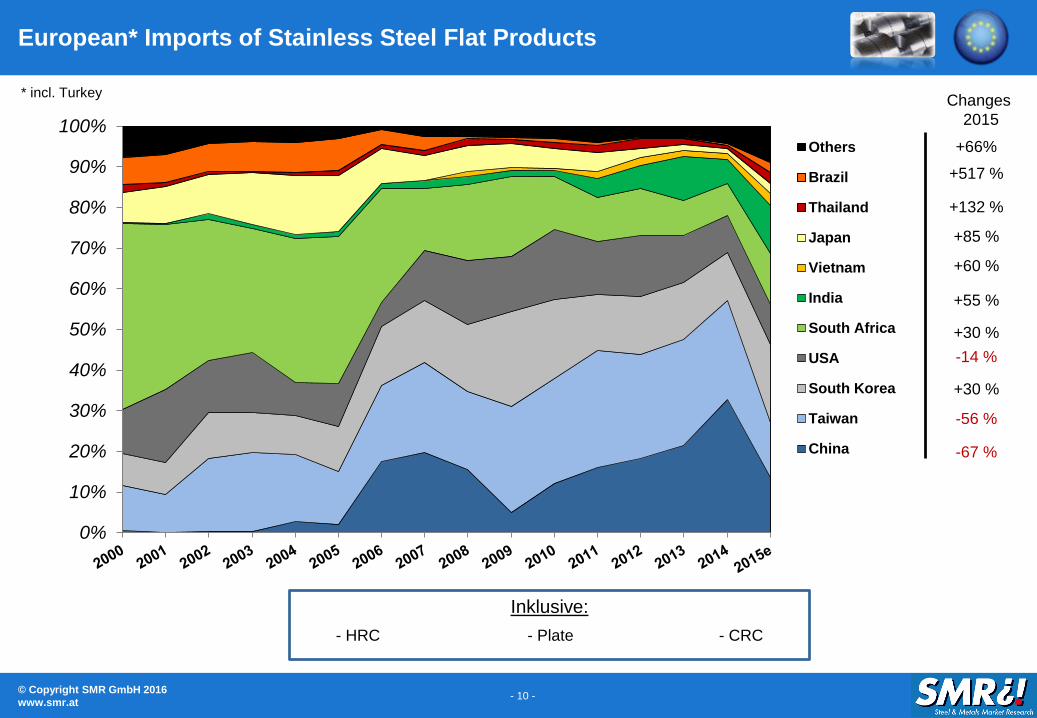

European* Imports of Stainless Steel Flat Products

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Others

Brazil

Thailand

Japan

Vietnam

India

South Africa

USA

South Korea

Taiwan

China

* incl. Turkey

Inklusive:

- HRC - Plate - CRC

Changes

2015

-14 %

+30 %

+55 %

+60 %

+85 %

+517 %

+66%

+132 %

+30 %

-56 %

-67 %

© Copyright SMR GmbH 2016

www.smr.at- 11 -

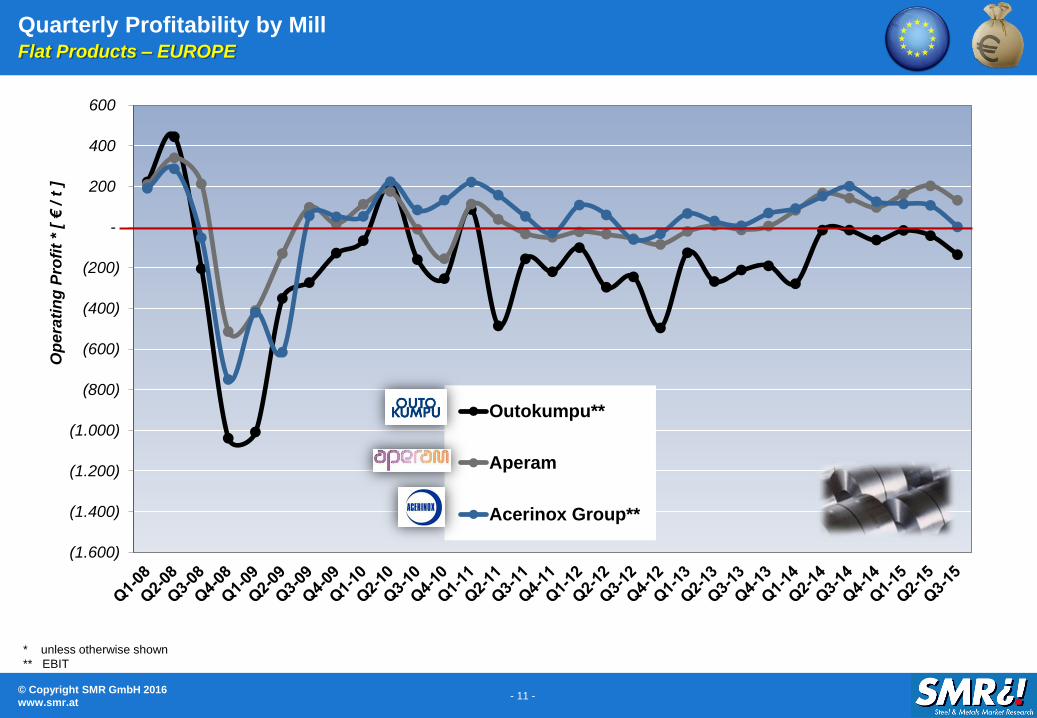

Quarterly Profitability by MillFlat Products – EUROPE

(1.600)

(1.400)

(1.200)

(1.000)

(800)

(600)

(400)

(200)

-

200

400

600

Op

era

tin

g P

rofi

t *

[ €

/ t

]

Outokumpu**

Aperam

Acerinox Group**

* unless otherwise shown

** EBIT

© Copyright SMR GmbH 2016

www.smr.at- 12 -

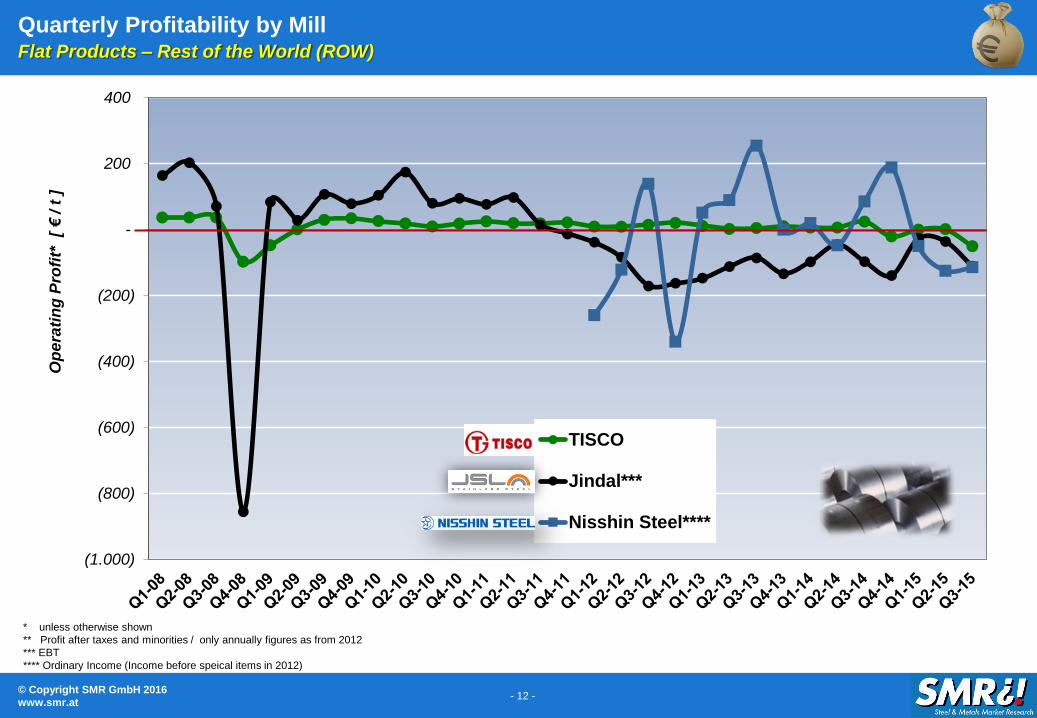

Quarterly Profitability by MillFlat Products – Rest of the World (ROW)

(1.000)

(800)

(600)

(400)

(200)

-

200

400

Op

era

tin

g P

rofi

t*

[ €

/ t

]

TISCO

Jindal***

Nisshin Steel****

* unless otherwise shown

** Profit after taxes and minorities / only annually figures as from 2012

*** EBT

**** Ordinary Income (Income before speical items in 2012)

© Copyright SMR GmbH 2016

www.smr.at- 13 -

Table of Contents

1. Overview

2. Focus on Germany

3. Outlook 2016

4. China – A ticking bomb?

5. Focus on Raw Materials

© Copyright SMR GmbH 2016

www.smr.at- 14 -

Long Term Apperant Consumption 1991 – 2015eAll Product Forms

- 14 -

800

1.000

1.200

1.400

1.600

1.800

2.000

[ in

To

nn

en

]

Long Term Growth:

+ 1.5%

Apparent Consumption = Production + Imports - Exports

Price Peak

(Upstocking)Recession

(2. Gulf War)

Financal

Crisis

Nickel

Bubble

Bursts

Massive

Upstocking

Recession

(1. Gulf War)

Economic

BoomPre-Crisis

Level

© Copyright SMR GmbH 2016

www.smr.at- 15 -

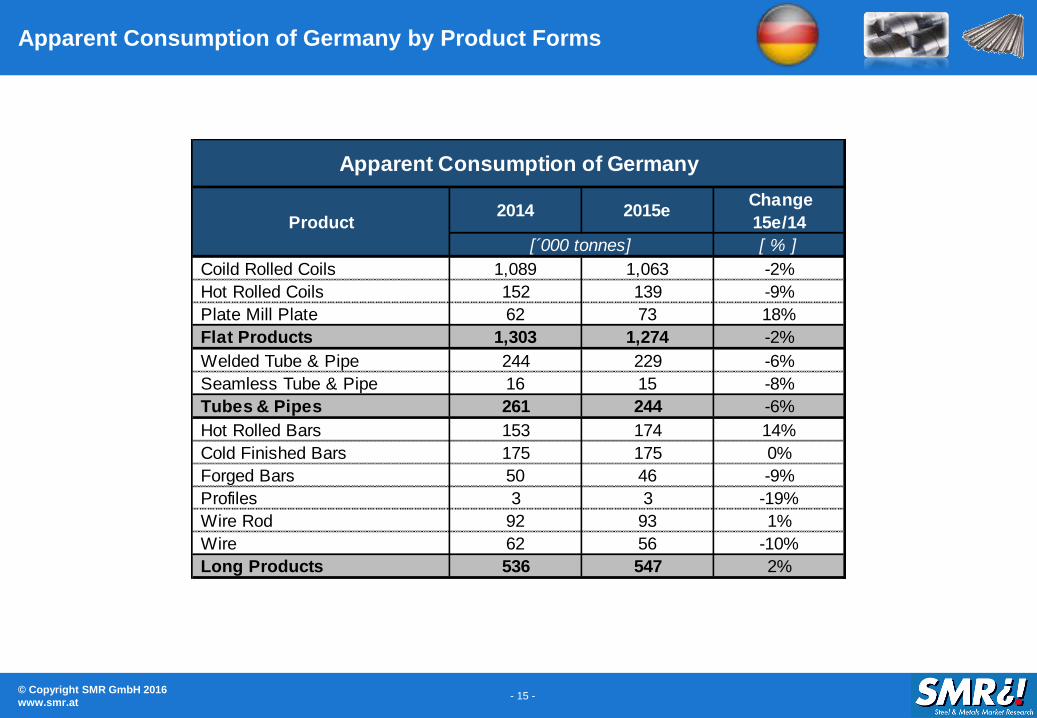

Apparent Consumption of Germany by Product Forms

[ % ]

Coild Rolled Coils 1,089 1,063 -2%

Hot Rolled Coils 152 139 -9%

Plate Mill Plate 62 73 18%

Flat Products 1,303 1,274 -2%

Welded Tube & Pipe 244 229 -6%

Seamless Tube & Pipe 16 15 -8%

Tubes & Pipes 261 244 -6%

Hot Rolled Bars 153 174 14%

Cold Finished Bars 175 175 0%

Forged Bars 50 46 -9%

Profiles 3 3 -19%

Wire Rod 92 93 1%

Wire 62 56 -10%

Long Products 536 547 2%

Apparent Consumption of Germany

Product2014 2015e

Change

15e/14

[´000 tonnes]

© Copyright SMR GmbH 2016

www.smr.at- 16 -

German Imports of Stainless Steel Long ProductsNur Indien stört die Europäische „Idylle“

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Others

Belgium

Switzerland

Netherlands

United Kingdom

Sweden

Austria

India

France

Spain

Italy

* incl. Turkey

2014 2015e Change

[%]

Italy 74 78 5%

Spain 64 63 0%

France 62 63 2%

India 42 42 0%

Austria 13 16 18%

Sweden 16 15 -7%

United Kingdom 16 12 -23%

Netherlands 14 10 -30%

Switzerland 10 9 -3%

Belgium 7 9 29%

Others 42 44 6%

TOTAL 301 299 -1%

German LP

Imports [kt]

© Copyright SMR GmbH 2016

www.smr.at- 17 -

German Imports of Stainless Steel Flat ProductsOTK liefert zunehmend aus den Niederlanden (Terneuzen)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Others

Sweden

Finland

Spain

Italy

France

Netherlands

Belgium

2014 2015e Change

[%]

Belgium 347 344 -1%

Netherlands 221 305 38%

France 151 195 29%

Italy 135 139 3%

Spain 107 115 8%

Finland 59 55 -6%

Sweden 47 49 4%

Others 160 159 -1%

TOTAL 1,227 1,362 11%

German FP

Imports [kt]

* incl. Turkey

© Copyright SMR GmbH 2016

www.smr.at- 18 -

Table of Contents

1. Overview

2. Focus on Germany

3. Outlook 2016

4. China – A ticking bomb?

5. Focus on Raw Materials

© Copyright SMR GmbH 2016

www.smr.at- 19 -

Purchasing Manager Index - Where do we stand in the business cycle?Die erste IFO indikation für 2016 zeigt eine deutliche verlangsamung in Deutschland

25

30

35

40

45

50

55

60

65

Ind

ex o

f 50 =

‘B

rea

k E

ven

Po

int’

EU USA China Germany

* below 50 the industry contracts / above 50 it is expected to expand

48

49

50

51

52

53

54

55

56

57

58

59

© Copyright SMR GmbH 2016

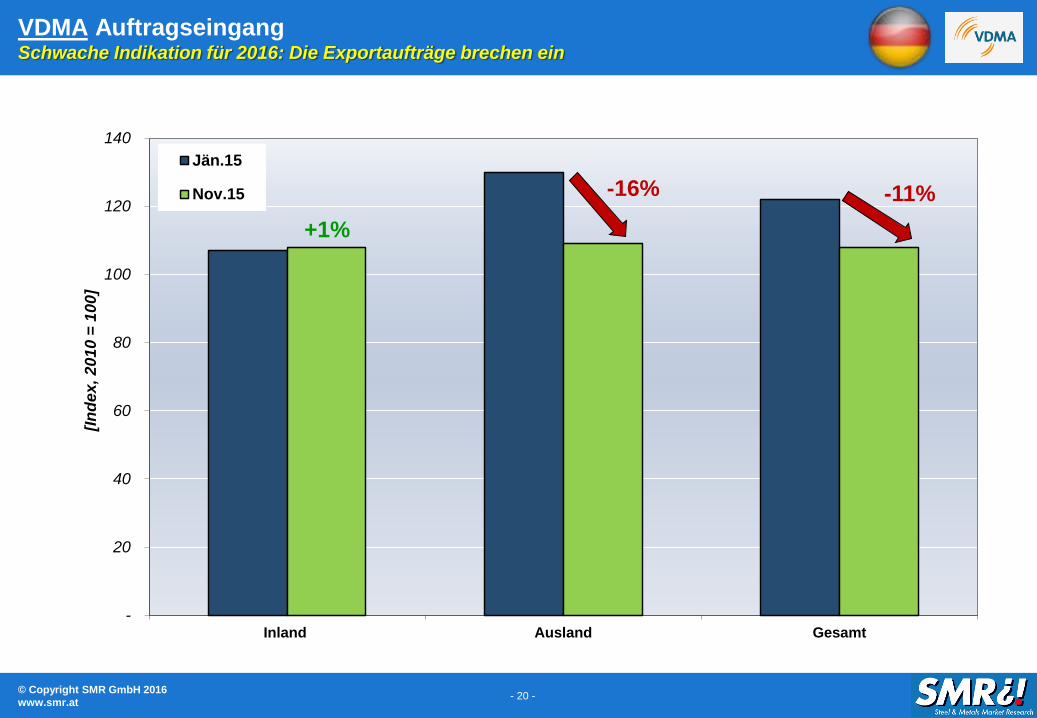

www.smr.at- 20 -

-

20

40

60

80

100

120

140

Inland Ausland Gesamt

[In

dex

, 2

01

0 =

10

0]

Jän.15

Nov.15

VDMA AuftragseingangSchwache Indikation für 2016: Die Exportaufträge brechen ein

+1%

-16% -11%

© Copyright SMR GmbH 2016

www.smr.at- 21 -

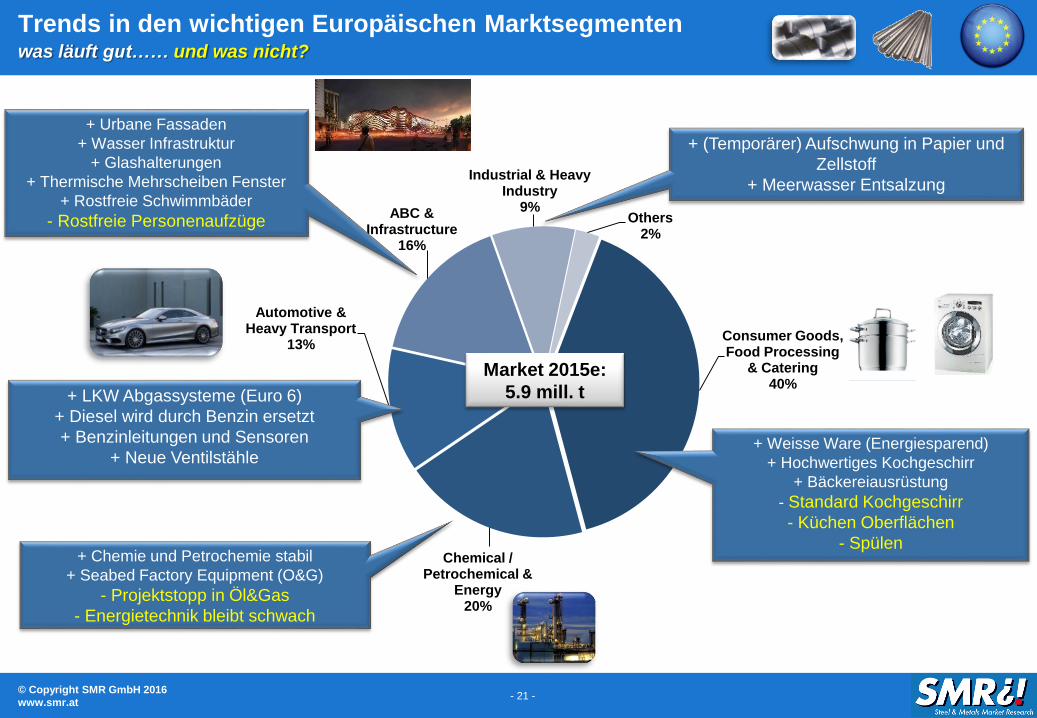

Consumer Goods, Food Processing

& Catering40%

Chemical / Petrochemical &

Energy20%

Automotive & Heavy Transport

13%

ABC & Infrastructure

16%

Industrial & Heavy Industry

9%Others

2%

Trends in den wichtigen Europäischen Marktsegmentenwas läuft gut…… und was nicht?

+ Weisse Ware (Energiesparend)

+ Hochwertiges Kochgeschirr

+ Bäckereiausrüstung

- Standard Kochgeschirr

- Küchen Oberflächen

- Spülen+ Chemie und Petrochemie stabil

+ Seabed Factory Equipment (O&G)

- Projektstopp in Öl&Gas

- Energietechnik bleibt schwach

+ Urbane Fassaden

+ Wasser Infrastruktur

+ Glashalterungen

+ Thermische Mehrscheiben Fenster

+ Rostfreie Schwimmbäder

- Rostfreie Personenaufzüge

+ (Temporärer) Aufschwung in Papier und

Zellstoff

+ Meerwasser Entsalzung

+ LKW Abgassysteme (Euro 6)

+ Diesel wird durch Benzin ersetzt

+ Benzinleitungen und Sensoren

+ Neue Ventilstähle

Market 2015e:

5.9 mill. t

© Copyright SMR GmbH 2016

www.smr.at- 22 -

-

100

200

300

400

500

600

700

800

900

1.000

1.100

1.200

[ '0

00

to

nn

es

]

Sinks & Construction Components

Exhaust Systems / O. Transport.

Small Appliances / Lifestyle Products

Heat Exchangers / O. Process Equip.

Tubes

Wire Products

Cutlery

Flow Control

Fasteners

Appliances

Catering & Utensils

Offshoring EuropeGute Neuigkeiten: Die Marktverlagerung nach Asien hat sich deutlich verlangsamt (schwacher Euro)

Langzeittrend +6% p.a.

© Copyright SMR GmbH 2016

www.smr.at- 23 -

Deutschland: Marktentprognose 2016

Ma

rktv

olu

me

n 2

01

6

Ma

rktv

olu

me

n2

01

5

Prozess-ausrüstung

Konsumgüter

Transport

Bau

Exporte (Direkt/Indirekt)

Importe (Direkt/Indirekt)

Lagerabbau

1.400

1.450

1.500

1.550

1.600

1.650

[‘0

00

to

nn

es

]

-1,7%

© Copyright SMR GmbH 2016

www.smr.at- 24 -

Table of Contents

1. Overview

2. Focus on Germany

3. Outlook 2016

4. China – Eine Zeitbombe?

5. Focus on Raw Materials

© Copyright SMR GmbH 2016

www.smr.at- 25 -

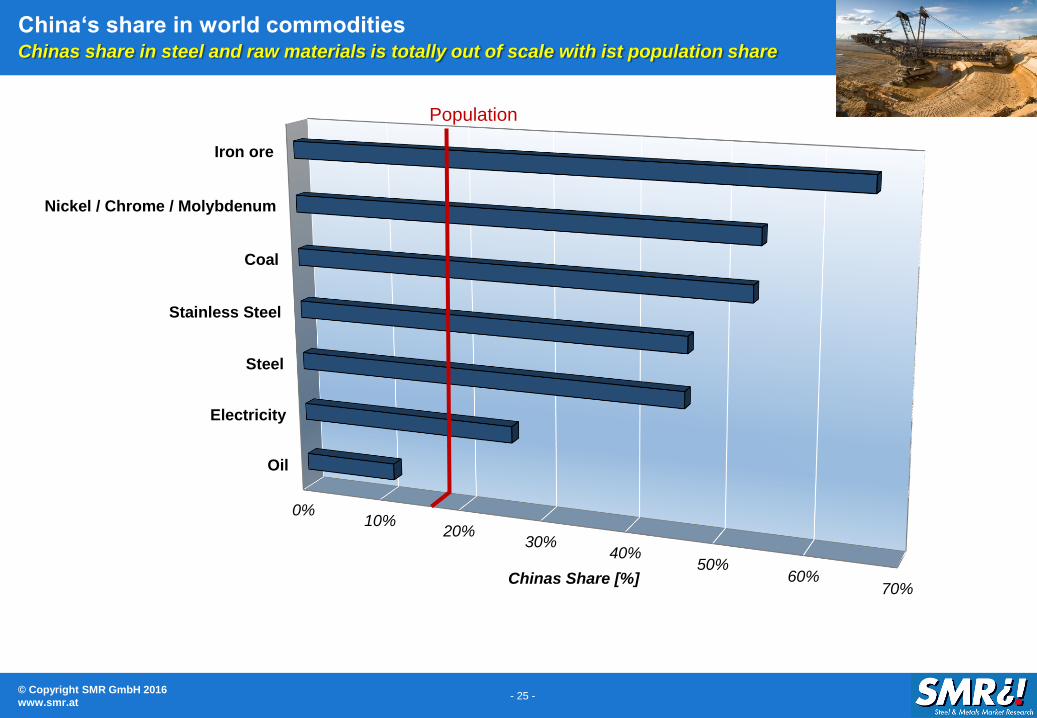

China‘s share in world commoditiesChinas share in steel and raw materials is totally out of scale with ist population share

0%10%

20%30%

40%50%

60%70%

Oil

Electricity

Steel

Stainless Steel

Coal

Nickel / Chrome / Molybdenum

Iron ore

Chinas Share [%]

Population

© Copyright SMR GmbH 2016

www.smr.at- 26 -

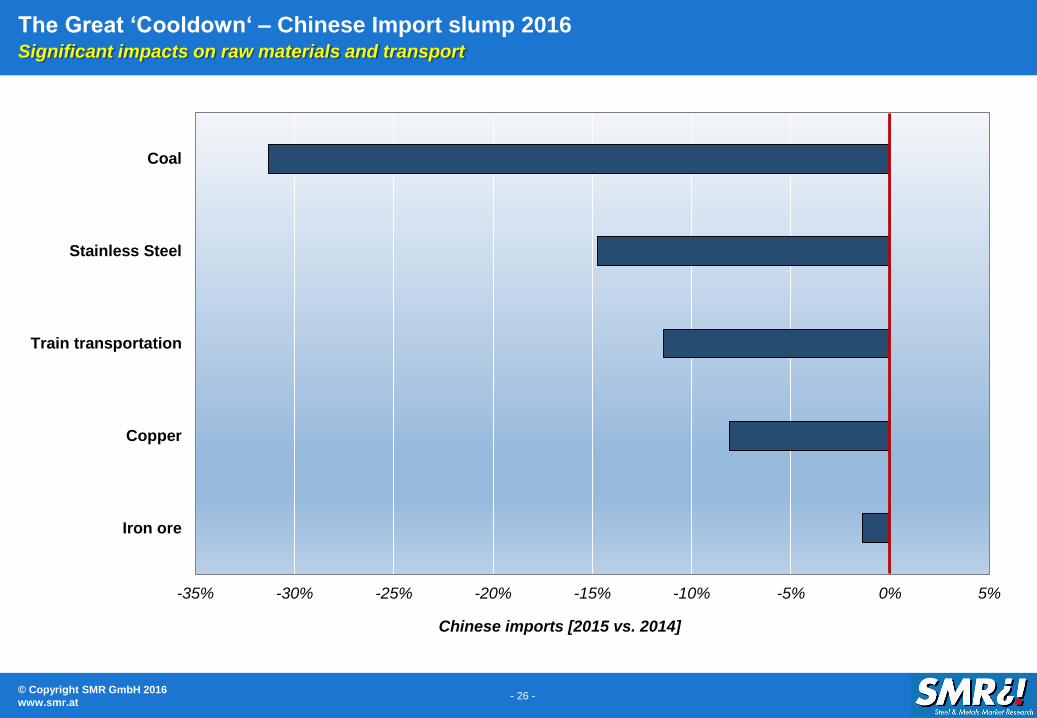

The Great ‘Cooldown‘ – Chinese Import slump 2016Significant impacts on raw materials and transport

-35% -30% -25% -20% -15% -10% -5% 0% 5%

Iron ore

Copper

Train transportation

Stainless Steel

Coal

Chinese imports [2015 vs. 2014]

© Copyright SMR GmbH 2016

www.smr.at- 27 -

Chinese Official GDP GrowthPredicted growth for 2015 is 6,5%

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

GD

P, c

on

sta

nt

pri

ce

s a

nd

ex

ch

an

ge r

ate

Really?

© Copyright SMR GmbH 2016

www.smr.at- 28 -

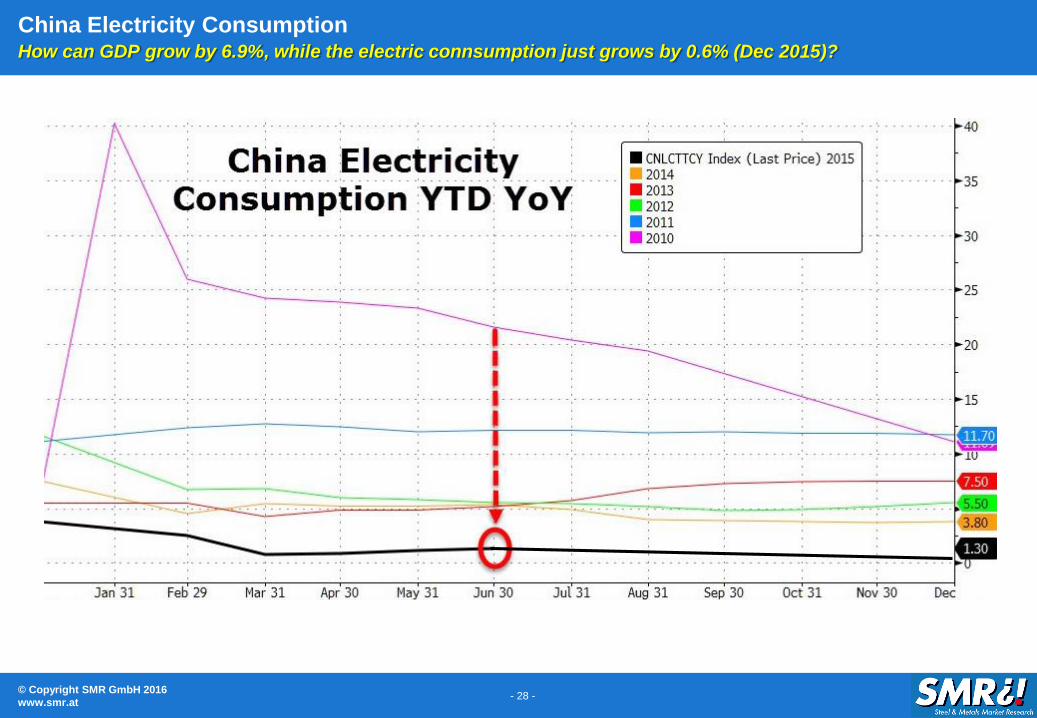

China Electricity ConsumptionHow can GDP grow by 6.9%, while the electric connsumption just grows by 0.6% (Dec 2015)?

© Copyright SMR GmbH 2016

www.smr.at- 29 -

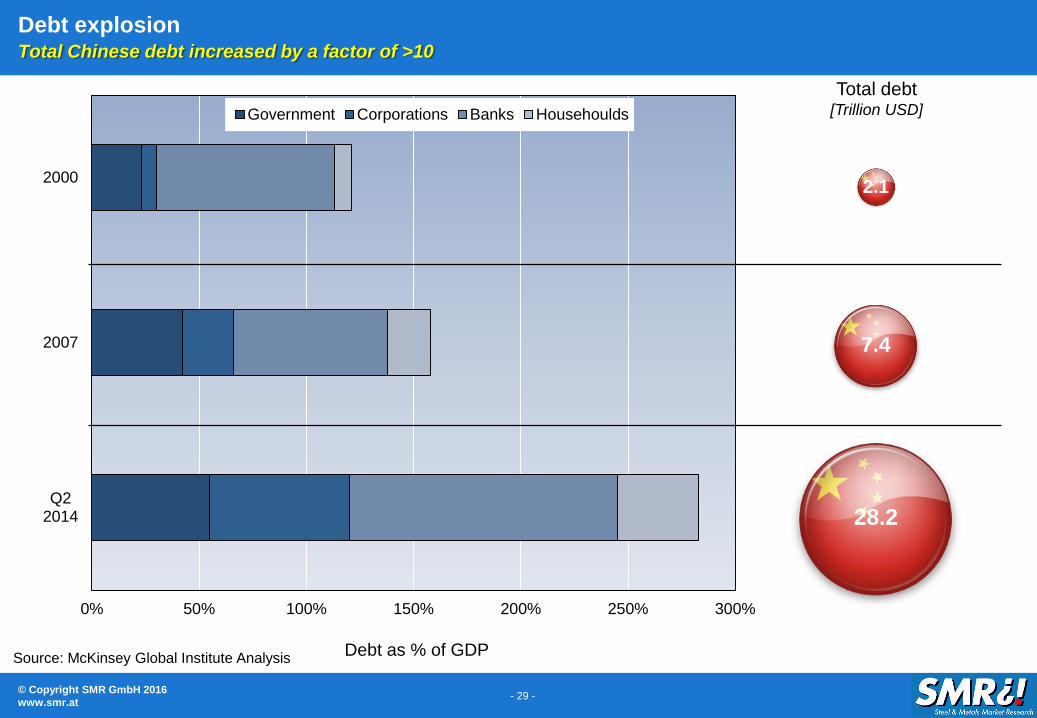

Debt explosionTotal Chinese debt increased by a factor of >10

Source: McKinsey Global Institute Analysis

0% 50% 100% 150% 200% 250% 300%

Q22014

2007

2000

Debt as % of GDP

Government Corporations Banks Househoulds

Total debt[Trillion USD]

28.2

7.4

2.1

© Copyright SMR GmbH 2016

www.smr.at- 30 -

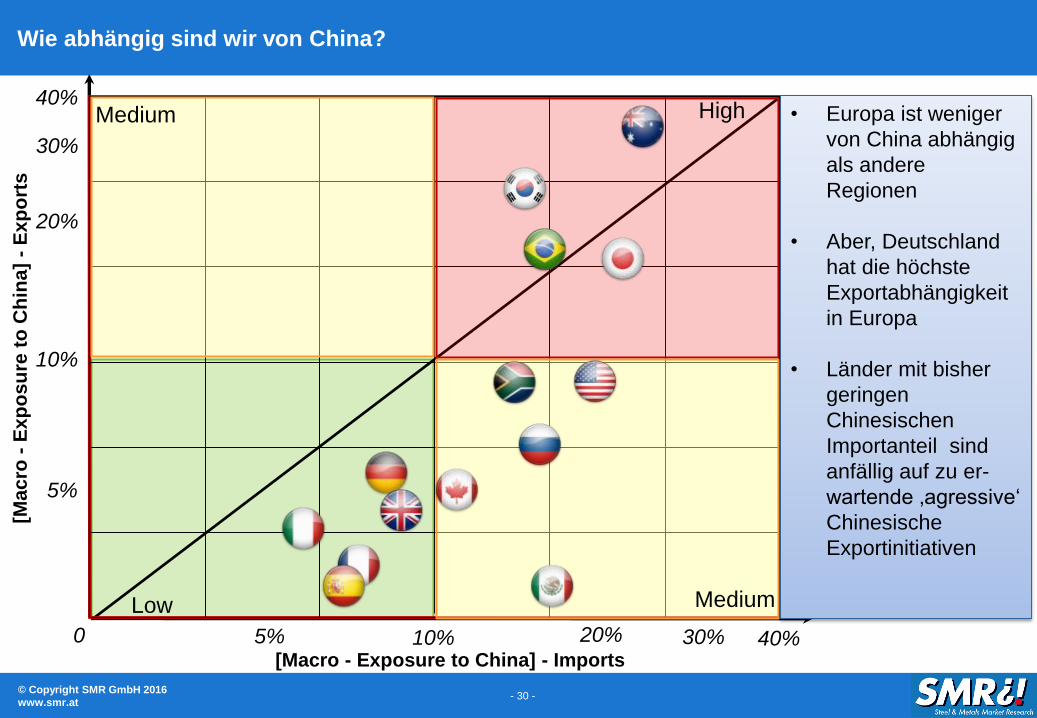

Wie abhängig sind wir von China?[M

acro

-E

xp

osu

re t

o C

hin

a]

-E

xp

ort

s

[Macro - Exposure to China] - Imports

0

10%

20%

30%

40%

5%

40%10% 30%5% 20%

• Europa ist weniger

von China abhängig

als andere

Regionen

• Aber, Deutschland

hat die höchste

Exportabhängigkeit

in Europa

• Länder mit bisher

geringen

Chinesischen

Importanteil sind

anfällig auf zu er-

wartende ‚agressive‘

Chinesische

Exportinitiativen

High

Low Medium

Medium

© Copyright SMR GmbH 2016

www.smr.at- 31 -

Table of Contents

1. Overview

2. Focus on Germany

3. Outlook 2016

4. China – A ticking bomb?

5. Focus on Raw Materials

© Copyright SMR GmbH 2016

www.smr.at- 32 -

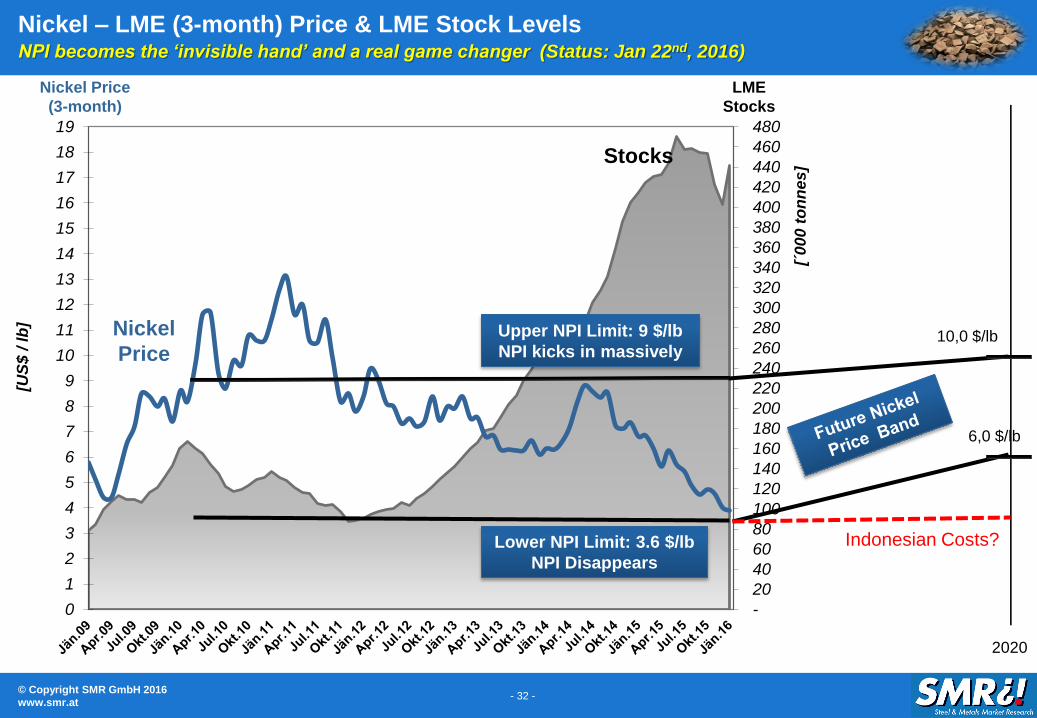

Nickel – LME (3-month) Price & LME Stock LevelsNPI becomes the ‘invisible hand’ and a real game changer (Status: Jan 22nd, 2016)

-

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

320

340

360

380

400

420

440

460

480

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

[´0

00

to

nn

es

]

[US

$ /

lb

]

Nickel Price

(3-month)

Nickel

Price

Stocks

LME

Stocks

2020

10,0 $/lb

6,0 $/lb

Upper NPI Limit: 9 $/lb

NPI kicks in massively

Lower NPI Limit: 3.6 $/lb

NPI Disappears

Indonesian Costs?

© Copyright SMR GmbH 2016

www.smr.at- 33 -

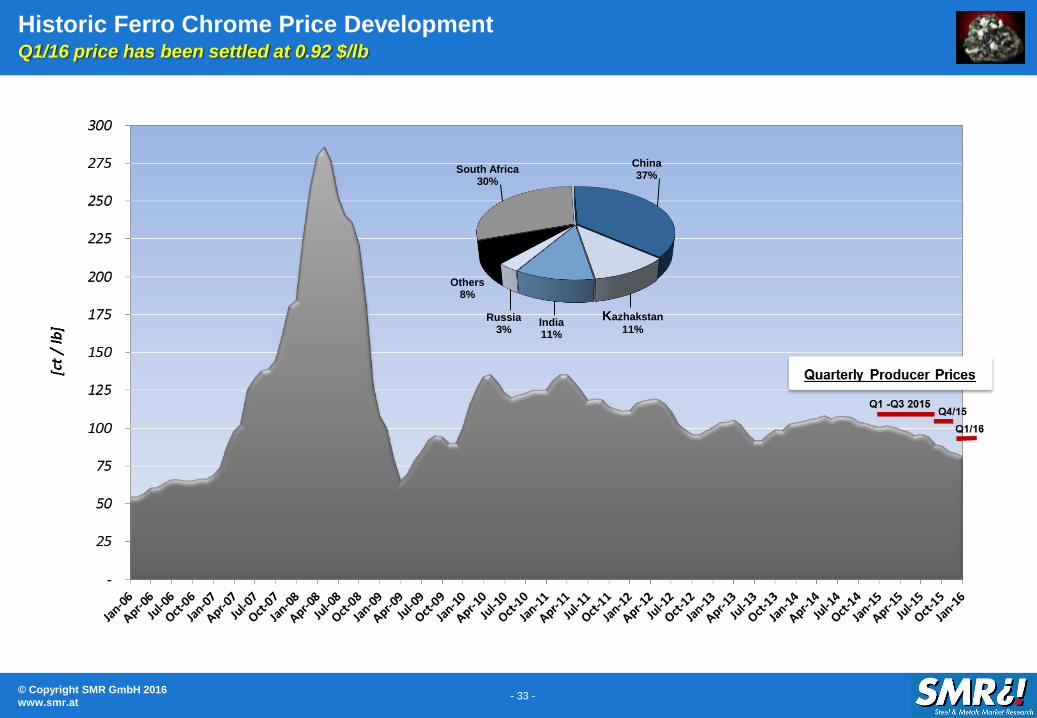

South Africa30%

China37%

Kazhakstan

11%India11%

Russia3%

Others8%

Historic Ferro Chrome Price DevelopmentQ1/16 price has been settled at 0.92 $/lb

© Copyright SMR GmbH 2016

www.smr.at- 34 -

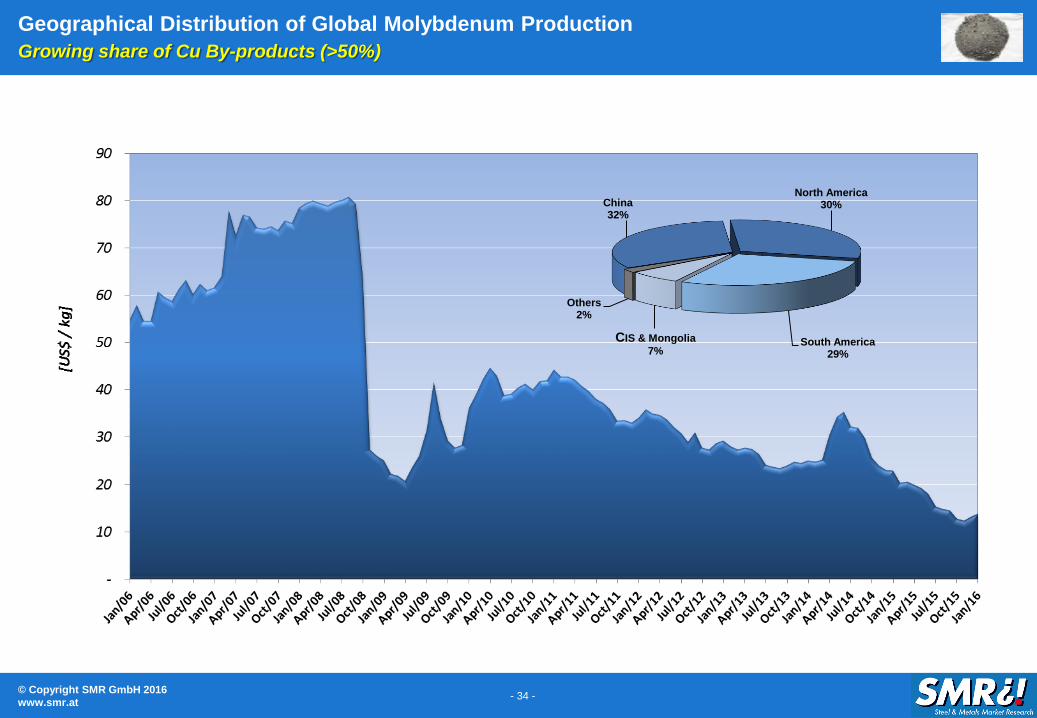

Geographical Distribution of Global Molybdenum Production

Growing share of Cu By-products (>50%)

China32%

North America30%

South America29%

CIS & Mongolia

7%

Others2%

© Copyright SMR GmbH 2016

www.smr.at- 35 -

Stainless Steel Scrap Market (Status: January 2016)The Stainless scrap is tightness has eased in Europe

(1.200)

(1.000)

(800)

(600)

(400)

(200)

-

200

400

US

$ / t

Dif

fere

nc

e:

Th

eo

reti

c M

inu

s R

ea

l S

cra

p P

ric

e

Real Intrinsic Value Discounts vs. Theoretic Values

(based on Ni 90 - Cr 85 - Fe 100 ‘rule’)

Too

Cheap

Too

Expensive

Average 11.5 % Discount

Today 17.7 % Discount!

© Copyright SMR GmbH 2016

www.smr.at- 36 -

Our Events 2016.... Where the Market talks’

For more information please visit: www.stainless-conference.com / www.metalbulletin.com/events / www.amm.com/events

October 2016

Chicago, USA

30th Stainless & its Alloys Conference

in association with

June 15 - 16, 2016

Hong Kong

11th Asian Stainless Steel Conferencein association with

September 6 - 8, 2016

Lisbon, Portugal

15th International Stainless & Special Steel Summit

in association with

© Copyright SMR GmbH 2016

www.smr.at- 37 -

Unsere Seminare in 2016

1st March 2016

Istanbul, Turkey

Stainless Market Seminar Turkey

8. März 2016

Düsseldorf, Germany

Edelstahl Marktseminar Deutschland

© Copyright SMR GmbH 2016

www.smr.at- 38 -

Fragen oder Kommentare?