Markov CM&KPIs BulgariaExper Lahore 2013 010213

21

Change management and Key performance indicators The Experience of Bulgaria NATIONAL REVENUE AGENCY January 2013 Stoyan Markov, Deputy Executive Director, [email protected]

-

Upload

write2hannan -

Category

Documents

-

view

216 -

download

0

Transcript of Markov CM&KPIs BulgariaExper Lahore 2013 010213

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 1/21

Change management and Key performanceindicators

The Experience of Bulgaria

NATIONAL REVENUE AGENCY

January 2013

Stoyan Markov, Deputy Executive Director,

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 2/21

2

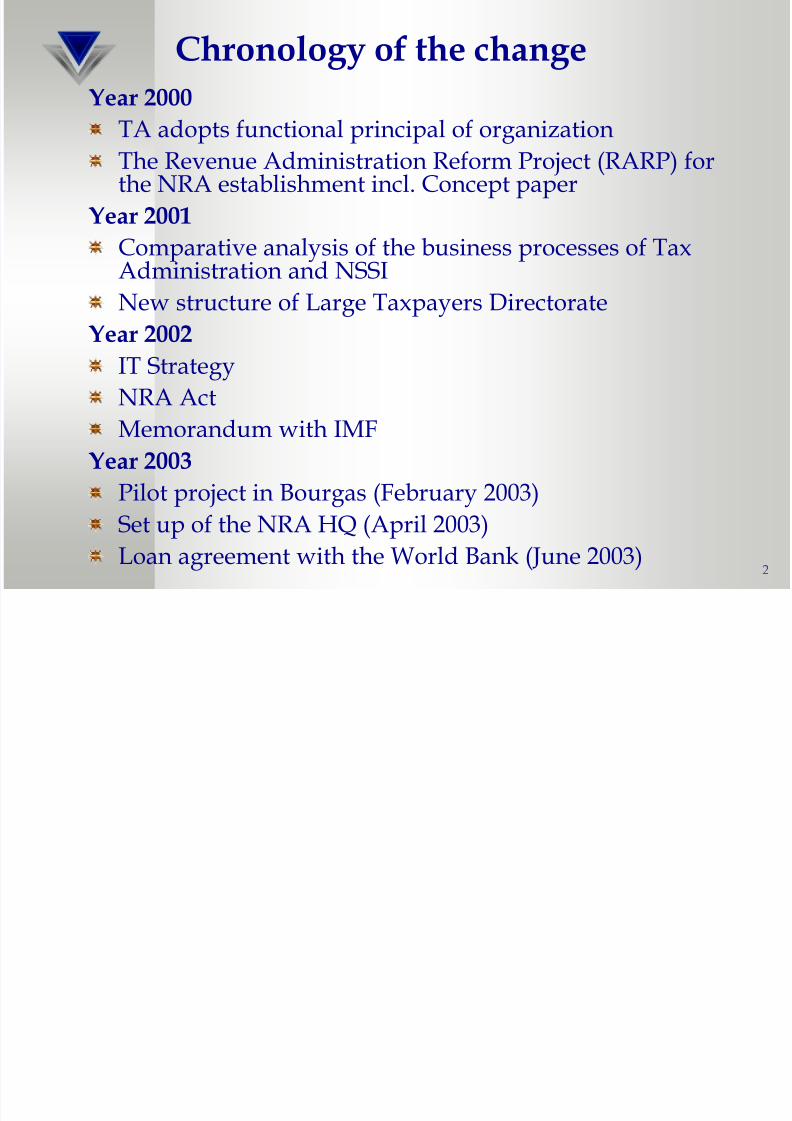

Chronology of the change

Year 2000

TA adopts functional principal of organizationThe Revenue Administration Reform Project (RARP) forthe NRA establishment incl. Concept paper

Year 2001

Comparative analysis of the business processes of Tax

Administration and NSSINew structure of Large Taxpayers Directorate

Year 2002

IT Strategy

NRA Act

Memorandum with IMF

Year 2003

Pilot project in Bourgas (February 2003)

Set up of the NRA HQ (April 2003)

Loan agreement with the World Bank (June 2003)

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 3/21

3

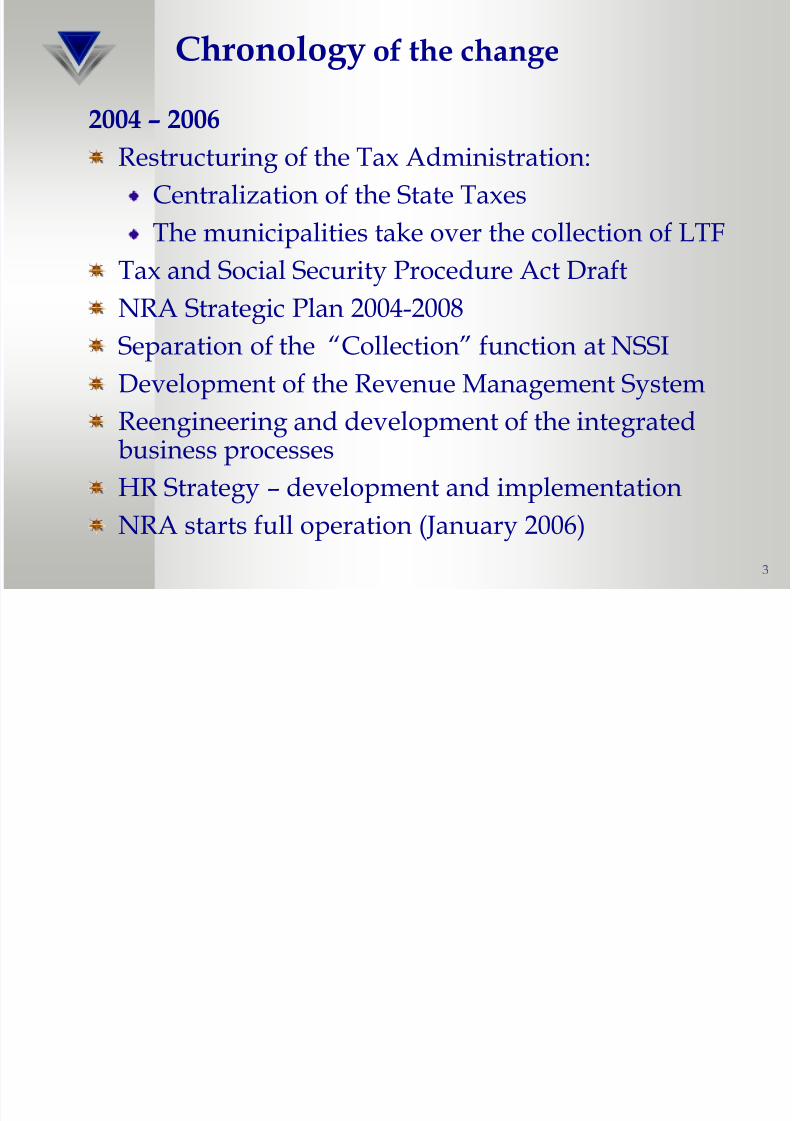

Chronology of the change

2004 – 2006

Restructuring of the Tax Administration:

Centralization of the State Taxes

The municipalities take over the collection of LTF

Tax and Social Security Procedure Act DraftNRA Strategic Plan 2004-2008

Separation of the “Collection” function at NSSI

Development of the Revenue Management System

Reengineering and development of the integratedbusiness processes

HR Strategy – development and implementation

NRA starts full operation (January 2006)

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 4/21

4

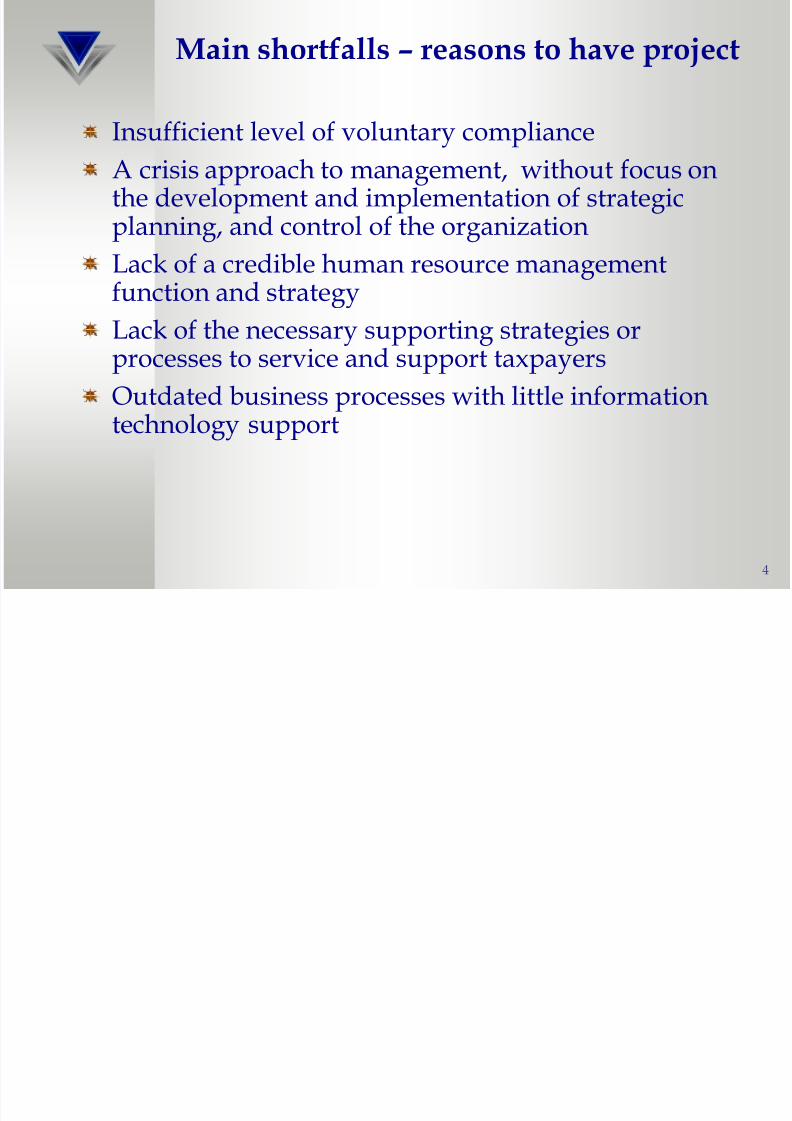

Main shortfalls – reasons to have project

Insufficient level of voluntary complianceA crisis approach to management, without focus onthe development and implementation of strategicplanning, and control of the organization

Lack of a credible human resource managementfunction and strategy

Lack of the necessary supporting strategies orprocesses to service and support taxpayers

Outdated business processes with little informationtechnology support

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 5/21

5

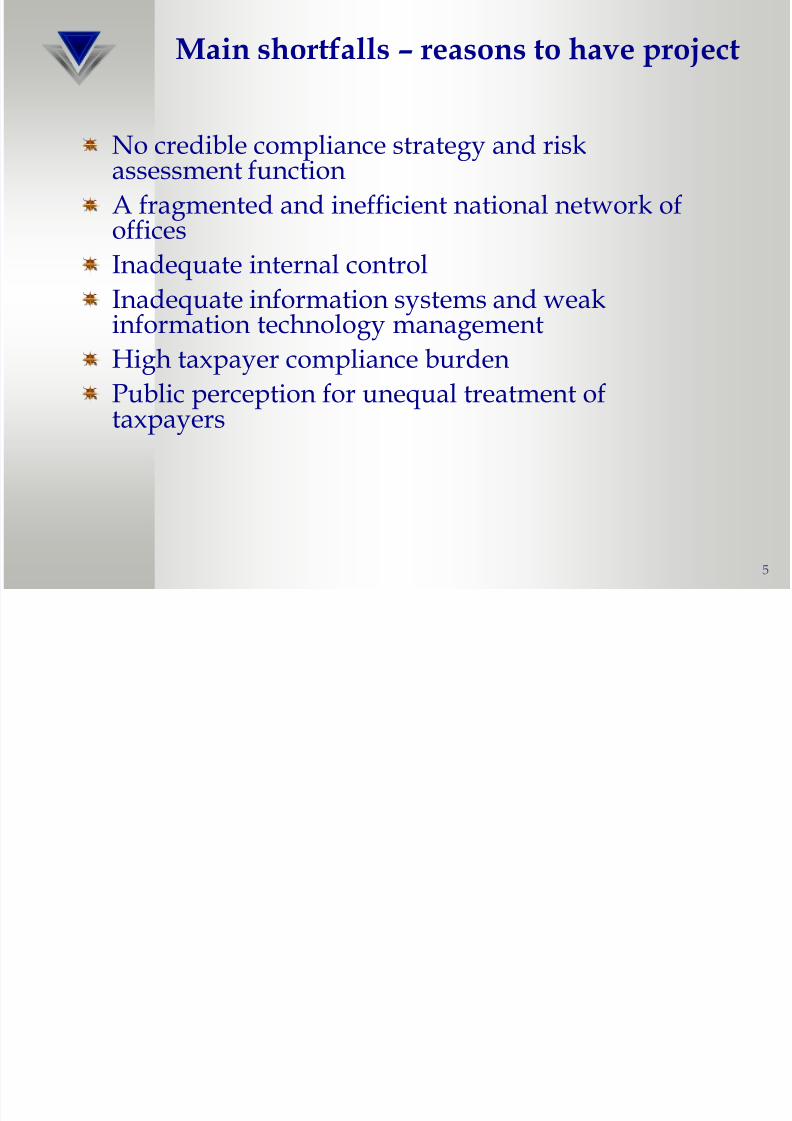

Main shortfalls – reasons to have project

No credible compliance strategy and riskassessment function

A fragmented and inefficient national network ofoffices

Inadequate internal controlInadequate information systems and weakinformation technology management

High taxpayer compliance burden

Public perception for unequal treatment oftaxpayers

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 6/21

6

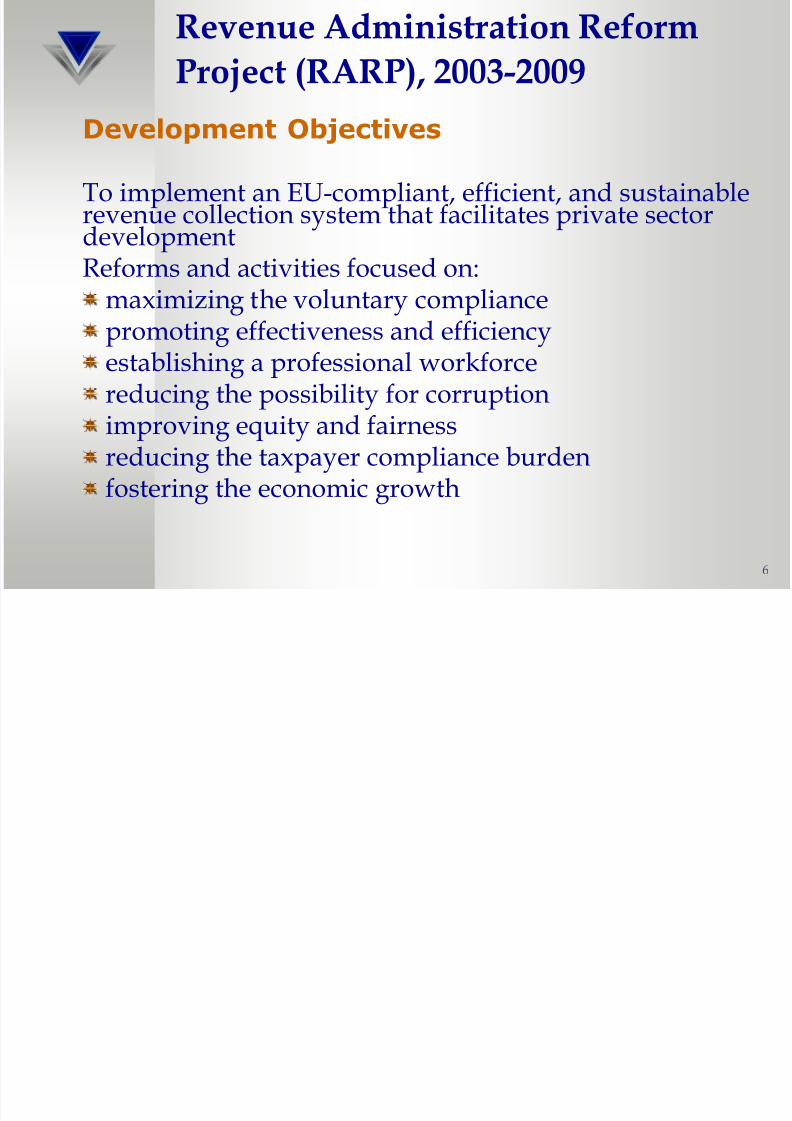

Revenue Administration Reform

Project (RARP), 2003-2009

Development Objectives

To implement an EU-compliant, efficient, and sustainablerevenue collection system that facilitates private sectordevelopment

Reforms and activities focused on:maximizing the voluntary compliancepromoting effectiveness and efficiencyestablishing a professional workforcereducing the possibility for corruptionimproving equity and fairnessreducing the taxpayer compliance burdenfostering the economic growth

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 7/217

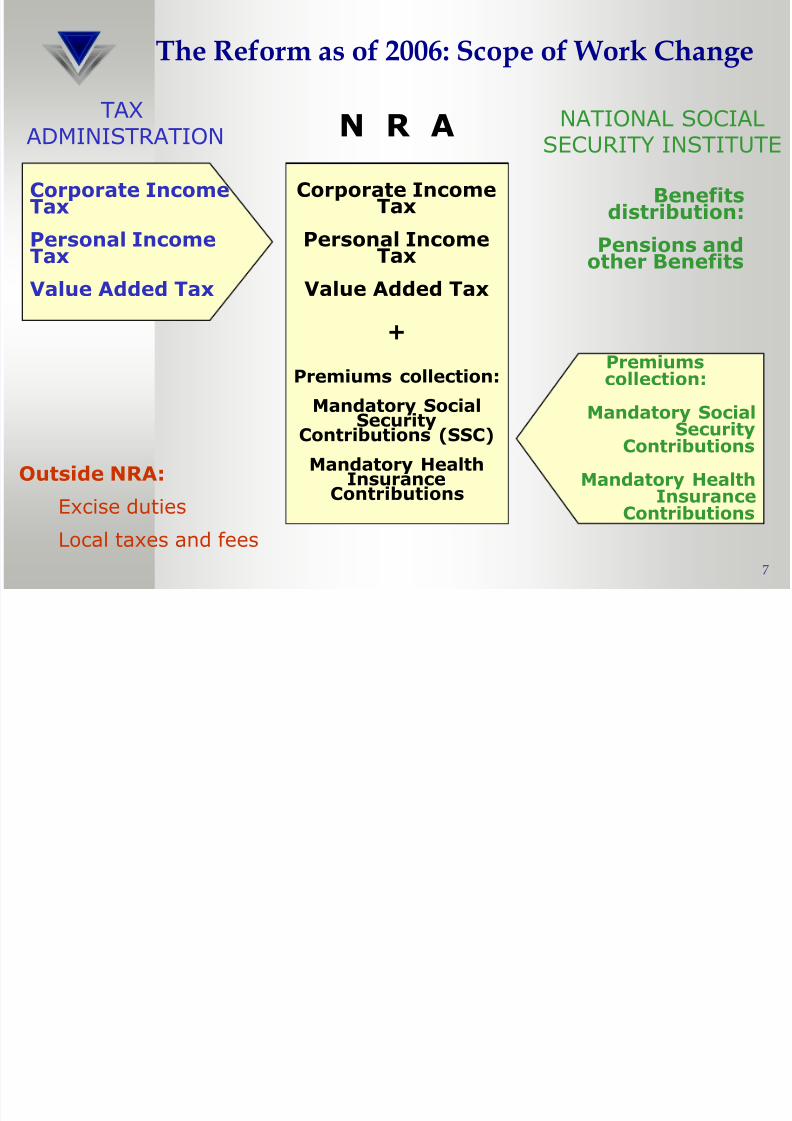

The Reform as of 2006: Scope of Work Change

Corporate IncomeTax

Personal IncomeTax

Value Added Tax

Outside NRA:

Excise duties

Local taxes and fees

Corporate IncomeTax

Personal IncomeTax

Value Added Tax

+

Premiums collection:

Mandatory SocialSecurityContributions (SSC)

Mandatory HealthInsurance

Contributions

Premiumscollection:

Mandatory SocialSecurityContributions

Mandatory HealthInsurance

Contributions

Benefitsdistribution:

Pensions andother Benefits

TAX

ADMINISTRATION N R ANATIONAL SOCIAL

SECURITY INSTITUTE

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 8/218

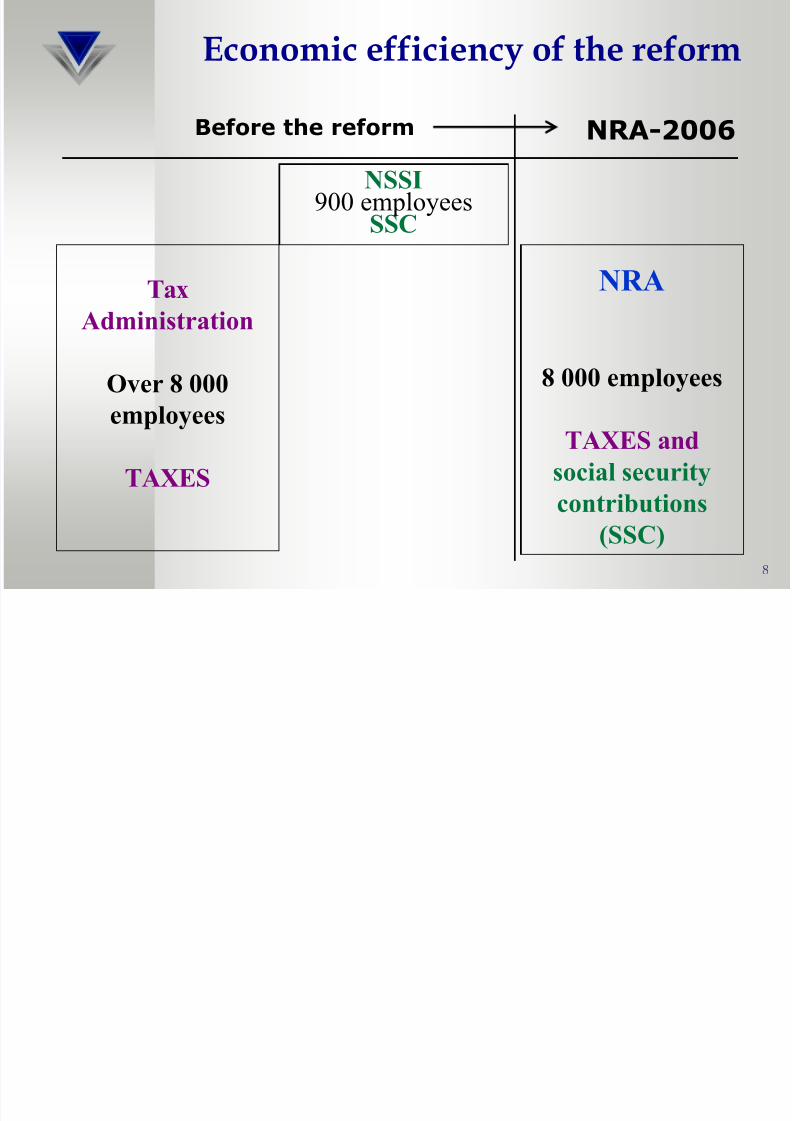

NSSI900 employees

SSC

Before the reform NRA-2006

Economic efficiency of the reform

Tax

Administration

Over 8 000

employees

TAXES

NRA

8 000 employees

TAXES and

social security

contributions

(SSC)

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 9/219

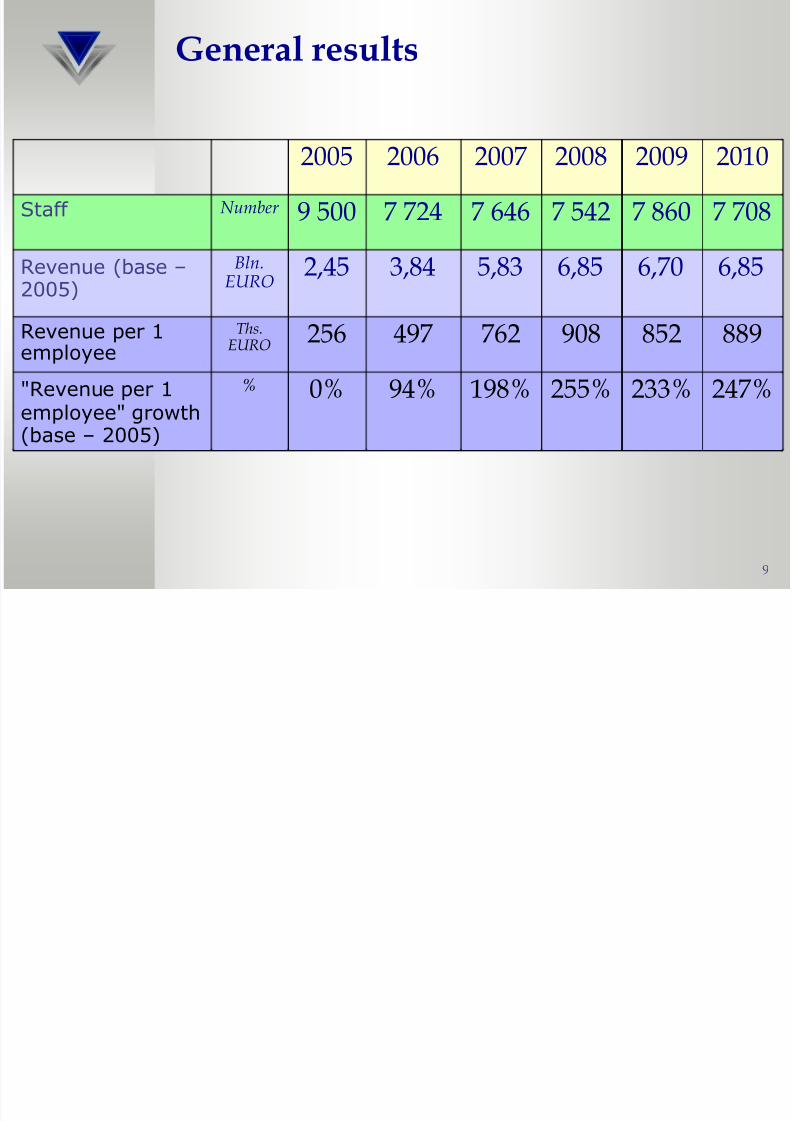

General results

2005 2006 2007 2008 2009 2010

Staff Number 9 500 7 724 7 646 7 542 7 860 7 708

Revenue (base–

2005)

Bln.

EURO 2,45 3,84 5,83 6,85 6,70 6,85

Revenue per 1employee

Ths.

EURO256 497 762 908 852 889

"Revenue per 1

employee" growth(base – 2005)

% 0% 94% 198% 255% 233% 247%

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 10/2110

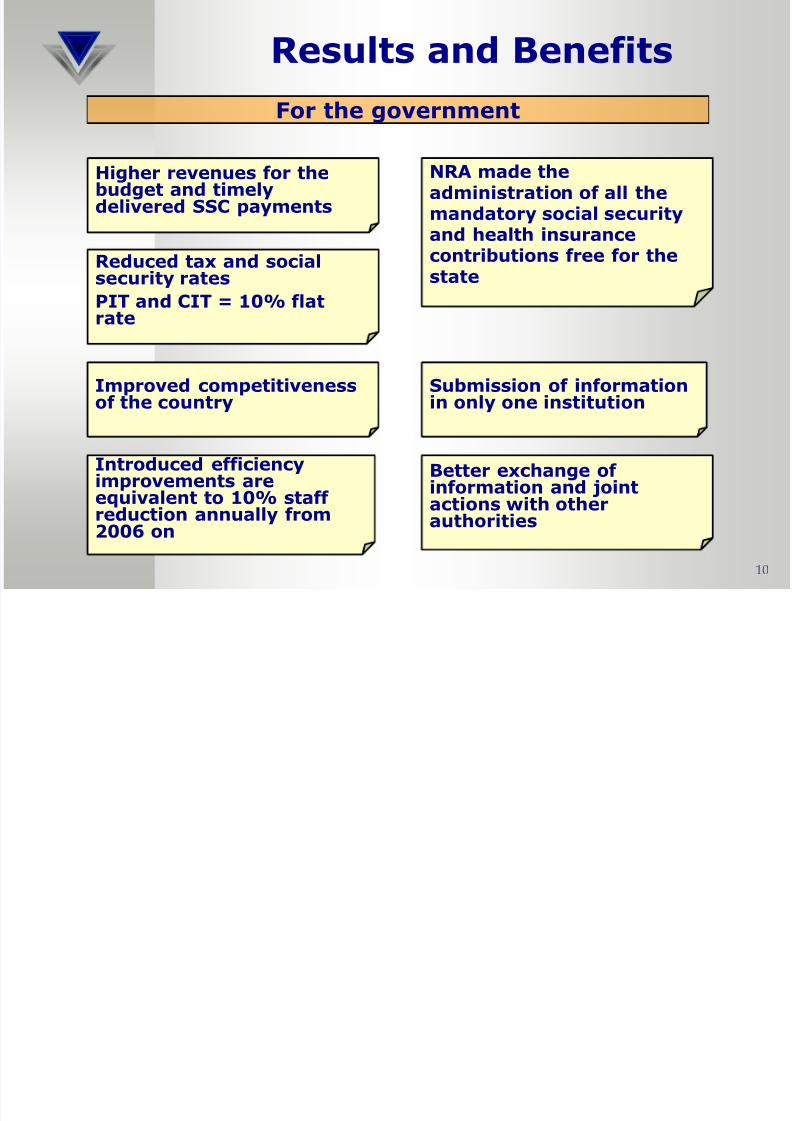

For the government

Results and Benefits

Higher revenues for thebudget and timelydelivered SSC payments

NRA made theadministration of all themandatory social securityand health insurancecontributions free for the

state

Submission of informationin only one institution

Introduced efficiencyimprovements areequivalent to 10% staffreduction annually from2006 on

Reduced tax and social

security ratesPIT and CIT = 10% flatrate

Better exchange ofinformation and jointactions with otherauthorities

Improved competitivenessof the country

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 11/21

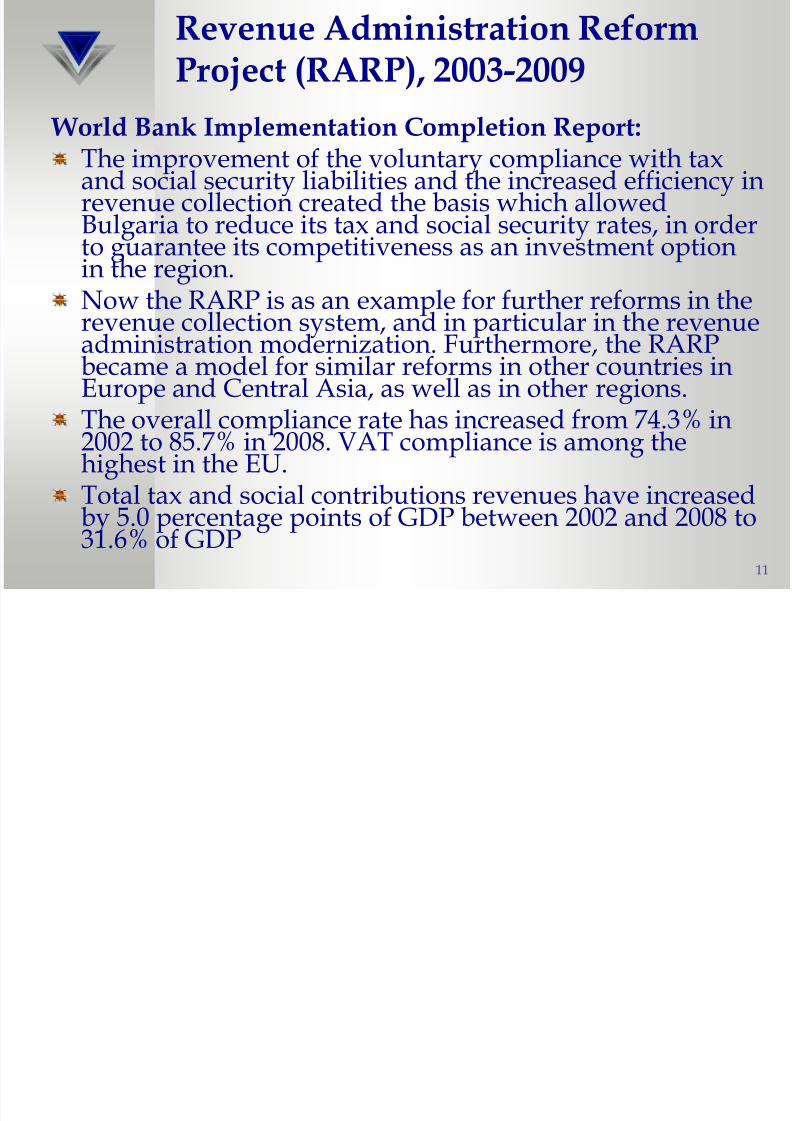

11

Revenue Administration ReformProject (RARP), 2003-2009

World Bank Implementation Completion Report:The improvement of the voluntary compliance with taxand social security liabilities and the increased efficiency inrevenue collection created the basis which allowedBulgaria to reduce its tax and social security rates, in orderto guarantee its competitiveness as an investment option

in the region.Now the RARP is as an example for further reforms in therevenue collection system, and in particular in the revenueadministration modernization. Furthermore, the RARPbecame a model for similar reforms in other countries inEurope and Central Asia, as well as in other regions.

The overall compliance rate has increased from 74.3% in2002 to 85.7% in 2008. VAT compliance is among thehighest in the EU.Total tax and social contributions revenues have increasedby 5.0 percentage points of GDP between 2002 and 2008 to

31.6% of GDP

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 12/21

12

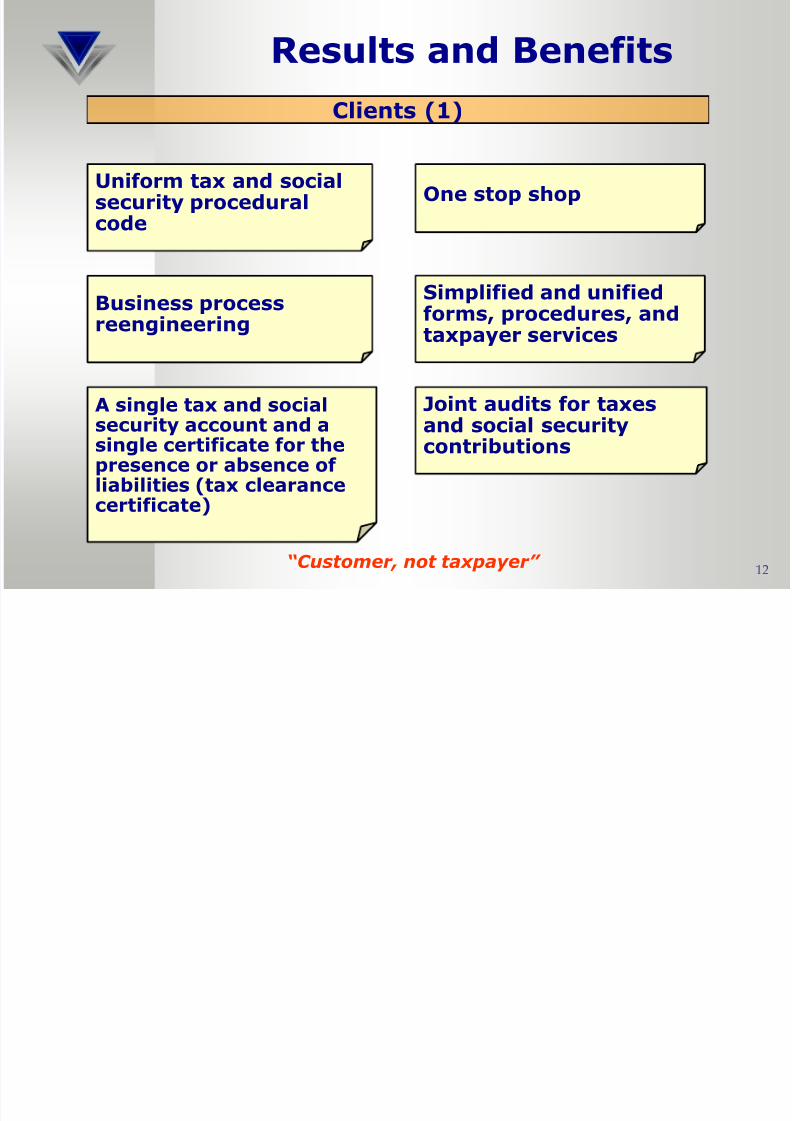

Clients (1)

Results and Benefits

“Customer, not taxpayer”

A single tax and socialsecurity account and asingle certificate for thepresence or absence ofliabilities (tax clearancecertificate)

One stop shop

Joint audits for taxesand social securitycontributions

Simplified and unifiedforms, procedures, andtaxpayer services

Uniform tax and socialsecurity proceduralcode

Business processreengineering

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 13/21

13

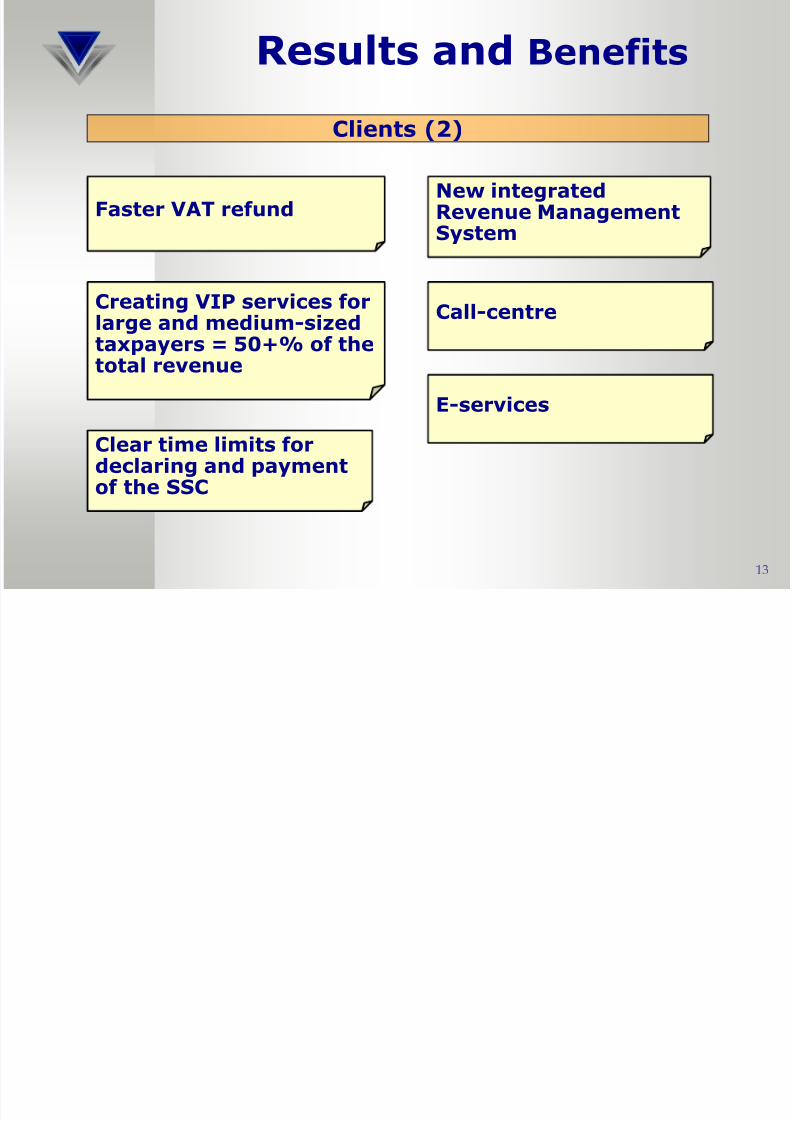

Clients (2)

Results and Benefits

Faster VAT refund

Creating VIP services forlarge and medium-sizedtaxpayers = 50+% of thetotal revenue

New integratedRevenue ManagementSystem

E-services

Call-centre

Clear time limits fordeclaring and paymentof the SSC

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 14/21

14

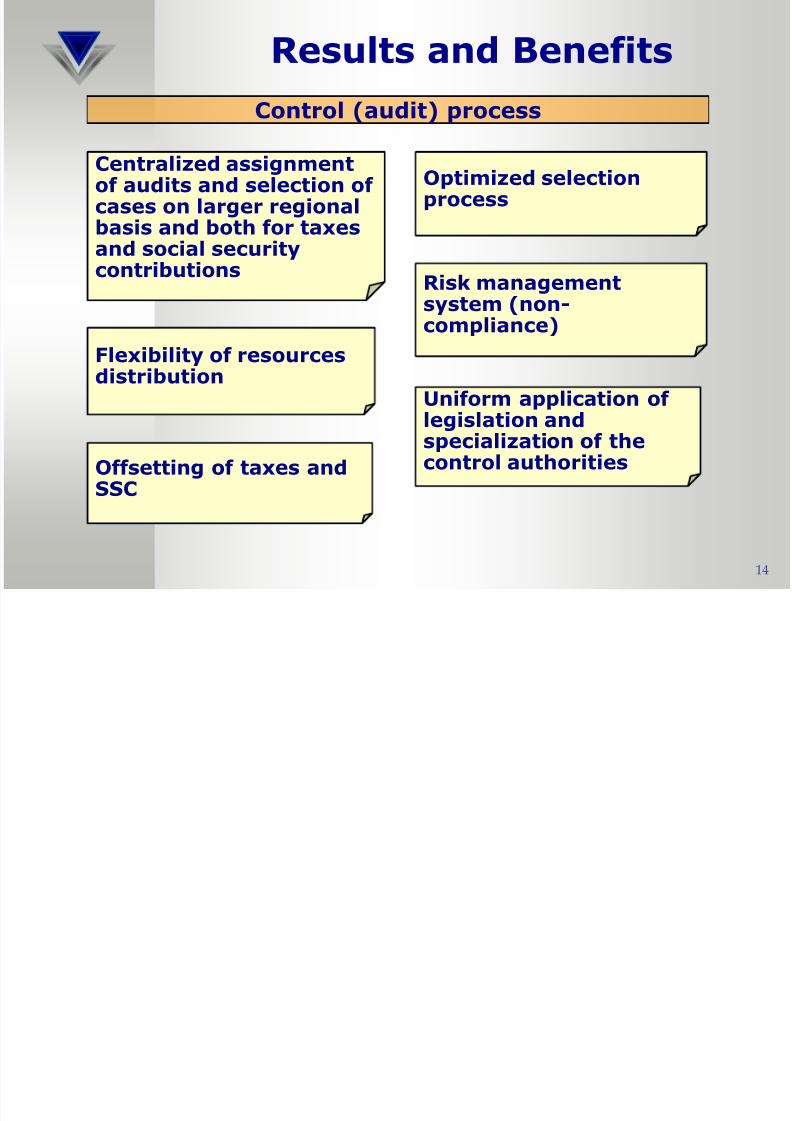

Control (audit) process

Results and Benefits

Centralized assignmentof audits and selection ofcases on larger regionalbasis and both for taxesand social security

contributions

Flexibility of resourcesdistribution

Optimized selectionprocess

Risk managementsystem (non-compliance)

Uniform application of

legislation andspecialization of thecontrol authoritiesOffsetting of taxes and

SSC

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 15/21

15

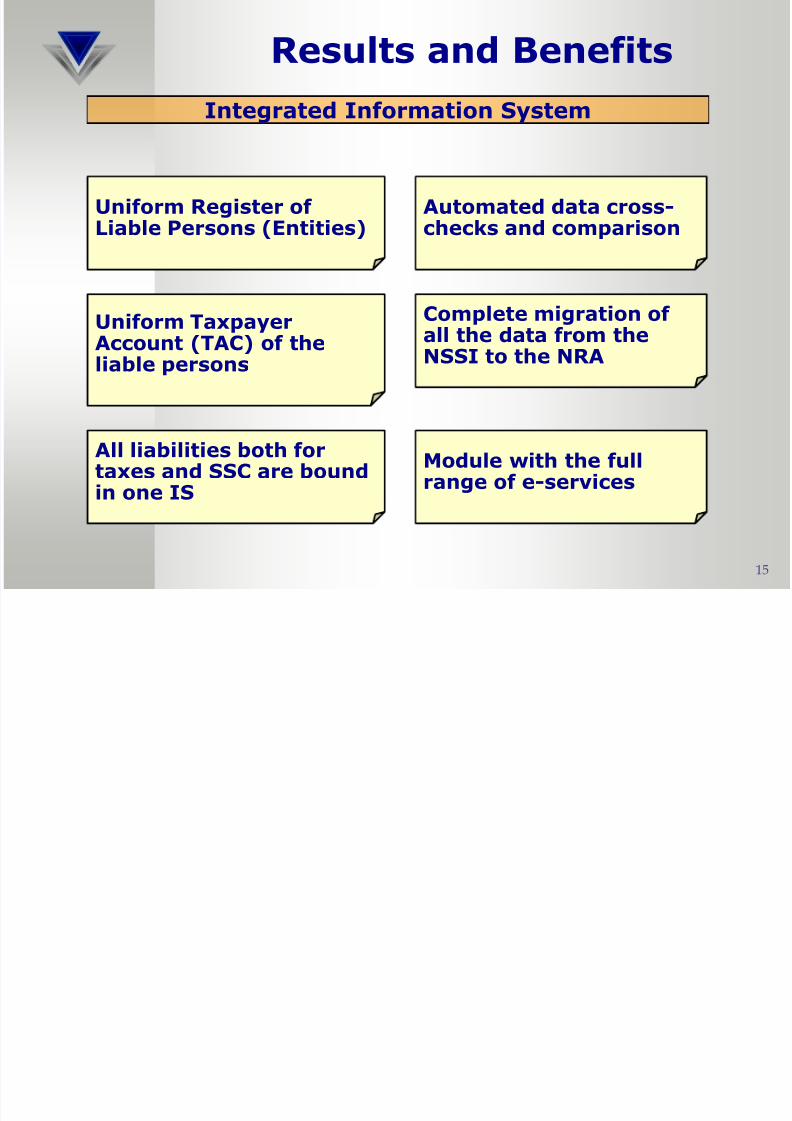

Integrated Information System

Results and Benefits

Uniform Register ofLiable Persons (Entities)

Uniform TaxpayerAccount (TAC) of theliable persons

Automated data cross-checks and comparison

Complete migration ofall the data from theNSSI to the NRA

Module with the fullrange of e-services

All liabilities both fortaxes and SSC are boundin one IS

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 16/21

16

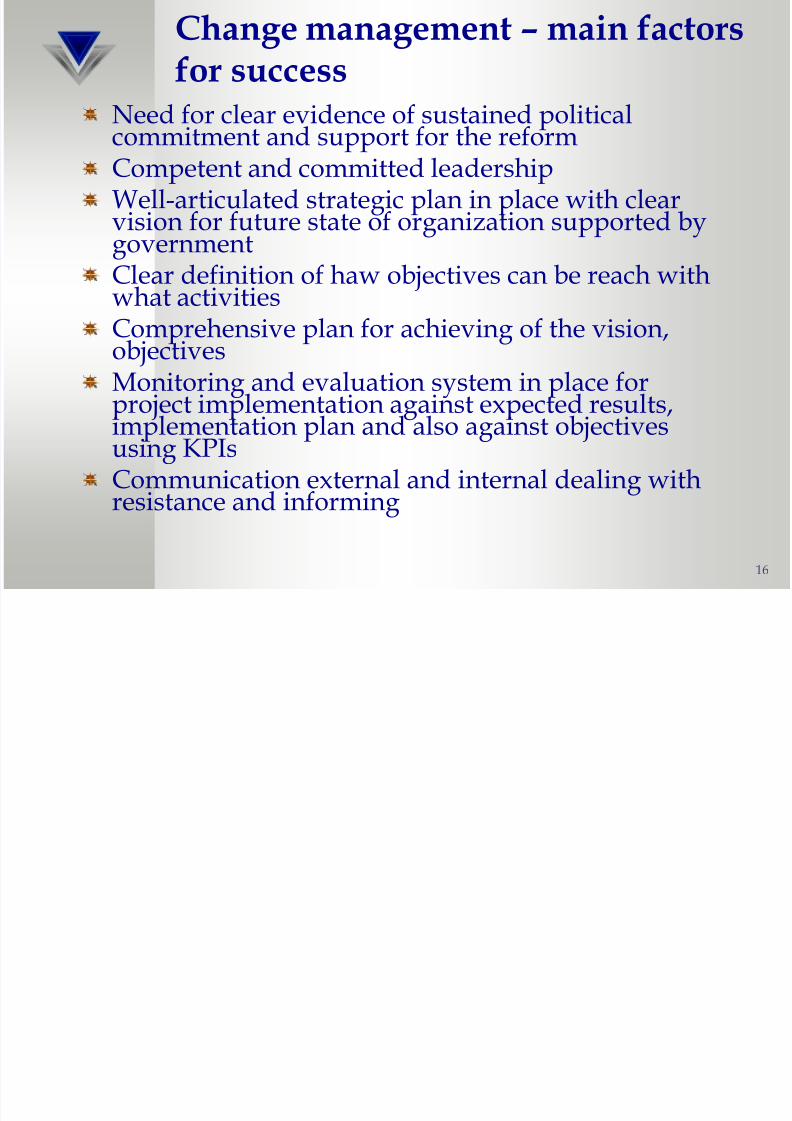

Change management – main factorsfor success

Need for clear evidence of sustained political

commitment and support for the reformCompetent and committed leadershipWell-articulated strategic plan in place with clearvision for future state of organization supported bygovernment

Clear definition of haw objectives can be reach withwhat activitiesComprehensive plan for achieving of the vision,objectivesMonitoring and evaluation system in place for

project implementation against expected results,implementation plan and also against objectivesusing KPIsCommunication external and internal dealing withresistance and informing

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 17/21

17

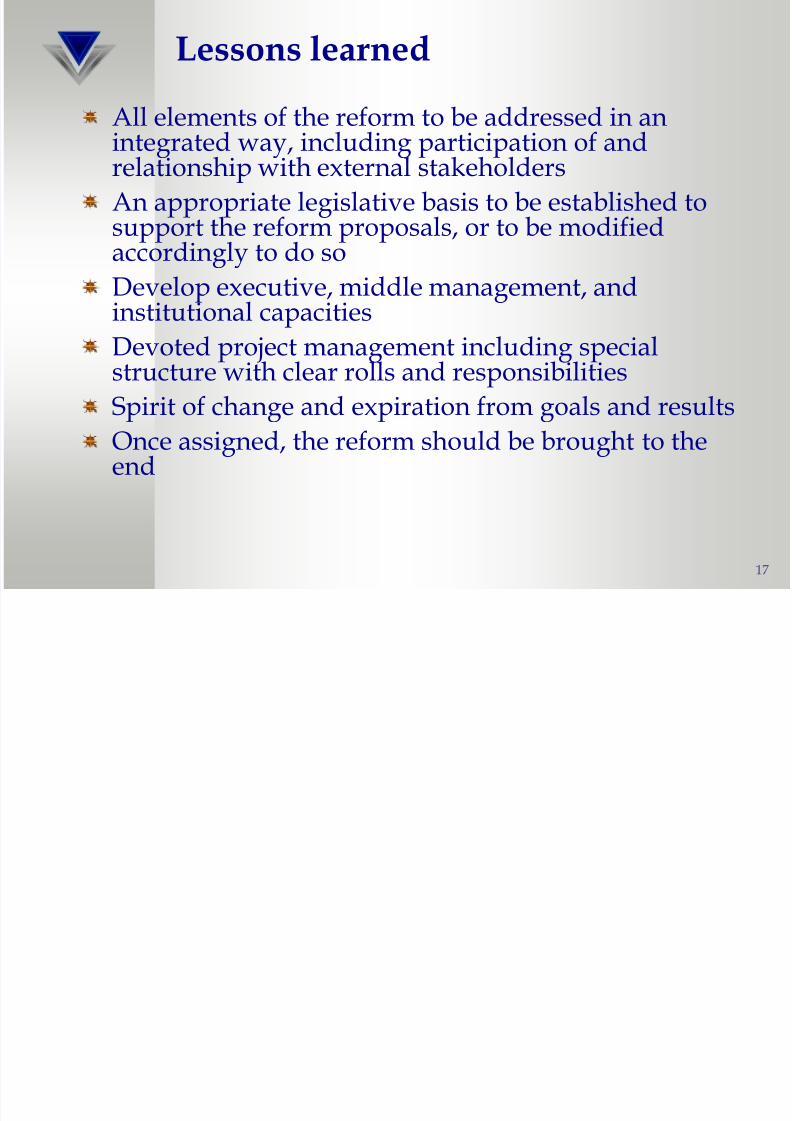

Lessons learned

All elements of the reform to be addressed in an

integrated way, including participation of andrelationship with external stakeholders

An appropriate legislative basis to be established tosupport the reform proposals, or to be modifiedaccordingly to do so

Develop executive, middle management, andinstitutional capacities

Devoted project management including specialstructure with clear rolls and responsibilities

Spirit of change and expiration from goals and resultsOnce assigned, the reform should be brought to theend

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 18/21

18

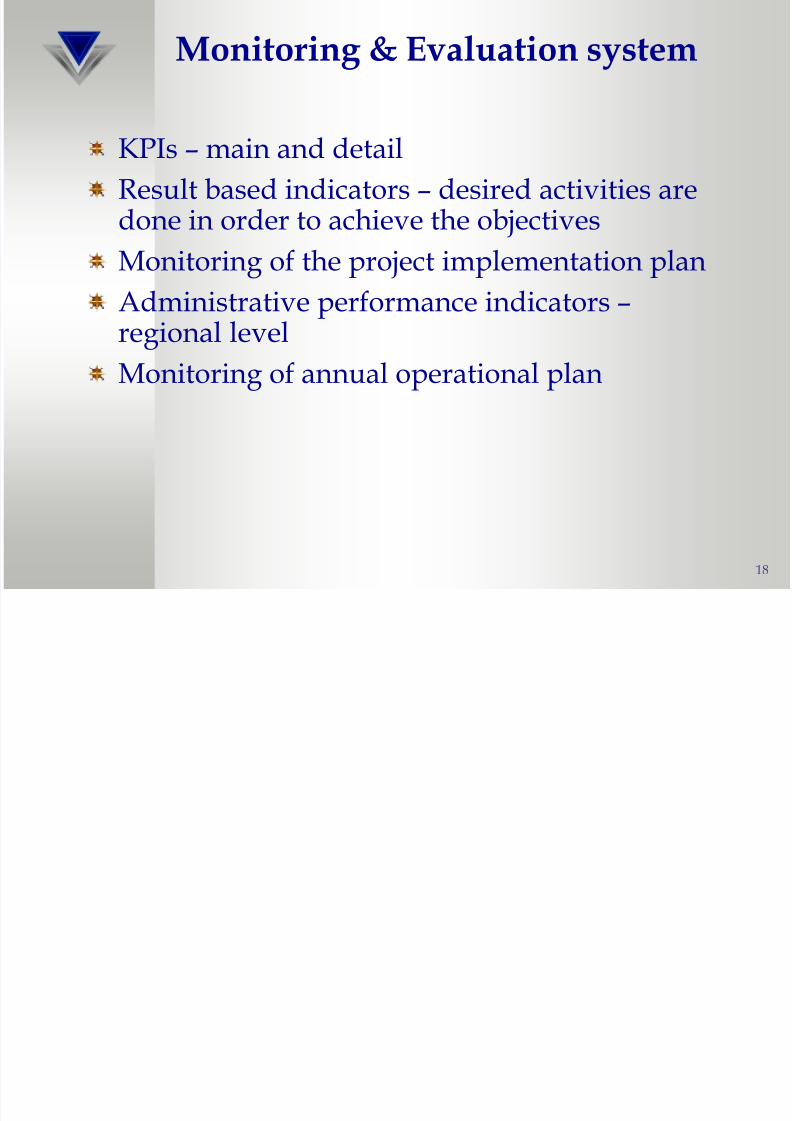

Monitoring & Evaluation system

KPIs – main and detail

Result based indicators – desired activities aredone in order to achieve the objectives

Monitoring of the project implementation plan

Administrative performance indicators – regional level

Monitoring of annual operational plan

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 19/21

19

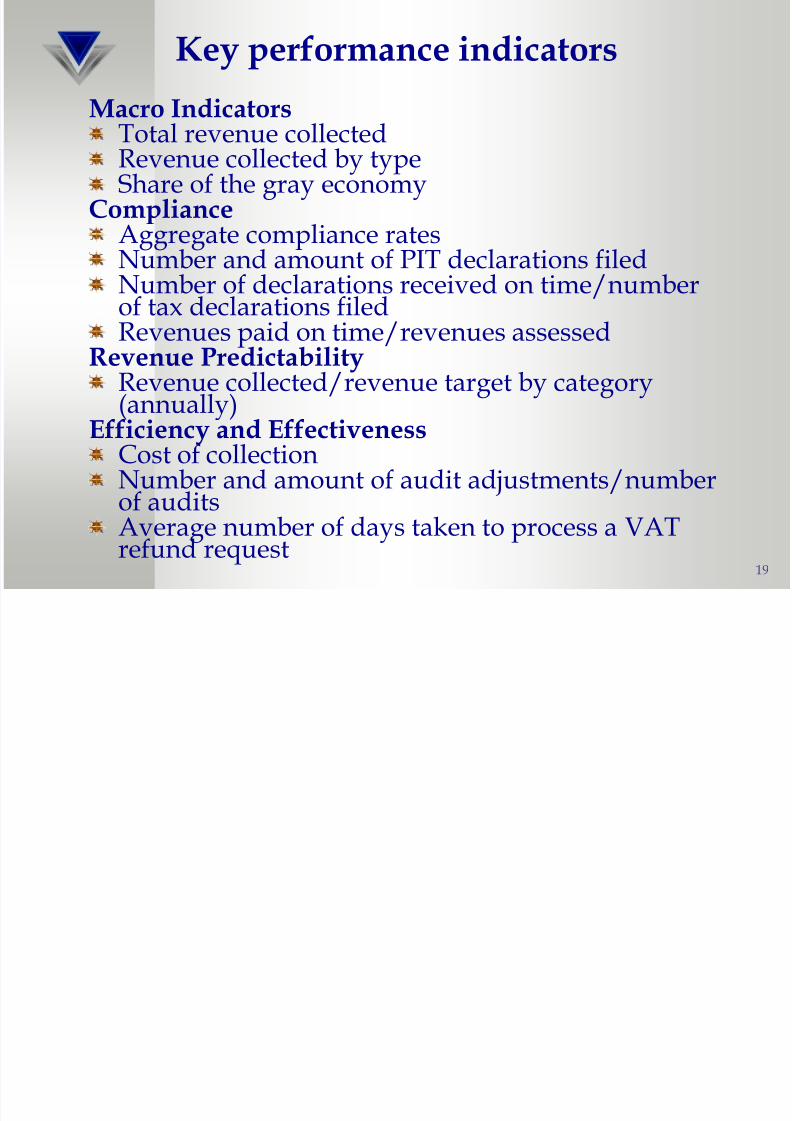

Key performance indicators

Macro Indicators

Total revenue collectedRevenue collected by typeShare of the gray economy

ComplianceAggregate compliance ratesNumber and amount of PIT declarations filedNumber of declarations received on time/numberof tax declarations filedRevenues paid on time/revenues assessed

Revenue PredictabilityRevenue collected/revenue target by category

(annually)Efficiency and EffectivenessCost of collectionNumber and amount of audit adjustments/numberof auditsAverage number of days taken to process a VAT

refund request

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 20/21

20

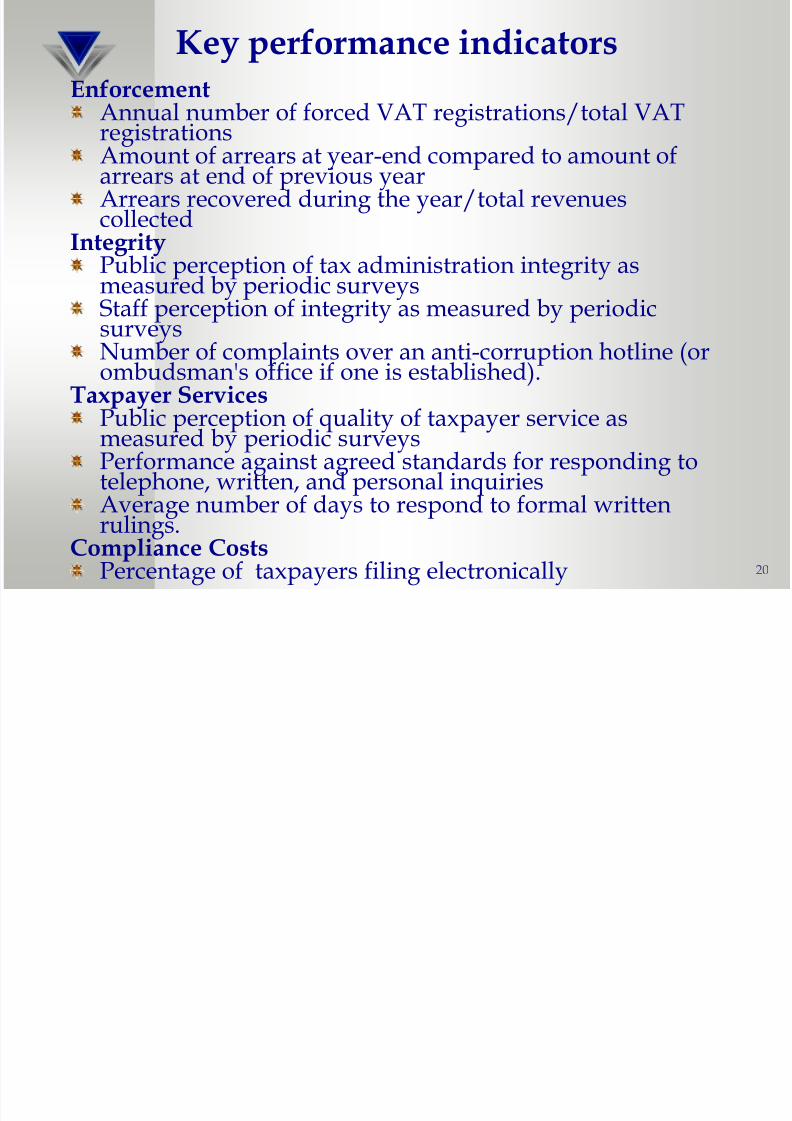

Key performance indicatorsEnforcement

Annual number of forced VAT registrations/total VAT

registrationsAmount of arrears at year-end compared to amount ofarrears at end of previous yearArrears recovered during the year/total revenuescollected

Integrity

Public perception of tax administration integrity asmeasured by periodic surveysStaff perception of integrity as measured by periodicsurveysNumber of complaints over an anti-corruption hotline (orombudsman's office if one is established).

Taxpayer Services

Public perception of quality of taxpayer service asmeasured by periodic surveysPerformance against agreed standards for responding totelephone, written, and personal inquiriesAverage number of days to respond to formal writtenrulings.

Compliance CostsPercentage of taxpayers filing electronically

8/13/2019 Markov CM&KPIs BulgariaExper Lahore 2013 010213

http://slidepdf.com/reader/full/markov-cmkpis-bulgariaexper-lahore-2013-010213 21/21

21

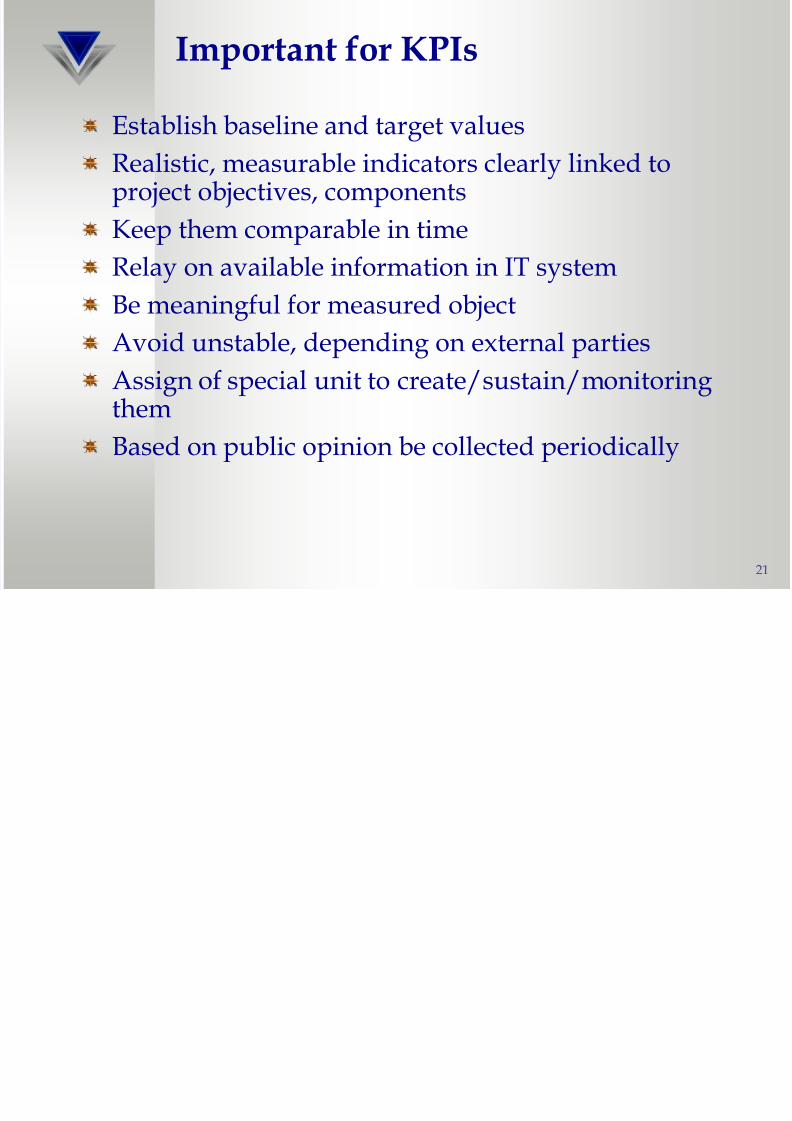

Important for KPIs

Establish baseline and target valuesRealistic, measurable indicators clearly linked toproject objectives, components

Keep them comparable in time

Relay on available information in IT systemBe meaningful for measured object

Avoid unstable, depending on external parties

Assign of special unit to create/sustain/monitoring

themBased on public opinion be collected periodically