Market Timing Using Market Internals - Nomura Group · PDF filemarket timing using market...

16

© Market Timing Using Market Internals ANY AUTHORS NAMED ON THIS REPORT ARE RESEARCH ANALYSTS UNLESS OTHERWISE INDICATED PLEASE SEE ANALYST(S) CERTIFICATION(S) ON PAGE 92 AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 95 May 2010 Shanthi Nair [email protected] +44 20 7102 4518

Transcript of Market Timing Using Market Internals - Nomura Group · PDF filemarket timing using market...

©©

Market Timing Using Market Internals

ANY AUTHORS NAMED ON THIS REPORT ARE RESEARCH ANALYSTS UNLESS OTHERWISE INDICATED

PLEASE SEE ANALYST(S) CERTIFICATION(S) ON PAGE 92 AND IMPORTANT DISCLOSURES BEGINNING ON

PAGE 95

May 2010

Shanthi Nair

+44 20 7102 4518

Market Timing is a difficult task

Fewer independent bets or breadth

Need high level of skill to achieve a reasonable level of IR

Signals need to be intuitive and provide reasoning

A market timing signal based on market internals.

Information derived only from the market

1

Global Market Timing Indicator

Based on signals derived from market movements

We categorise the market’s internal characteristics along five broad dimensions:

Volume

Breadth

Volume Divergence

Trend

Risk Aversion

Provides an intuitive framework within which to analyse market movements

2

Global Market Timing Indicator

Component Signals - Volume

Market ‘internal’ that depends on supply and demand for securities

Volume generally used to determine the conviction of a move in stocks

Empirical findings support the relationship between positive volume and price change.

Behavioural reasons for formation and continuation of volume trends

Market movements stronger when supported by increasing volume in that direction.

3

Page 5

Global Volume Signal and FTSE World Index

100

150

200

250

300

350

400

450

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

-1.2

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Source: Nomura Strategy Research

Index

Global Net Volume

Signal (RHS)FTSE World Index (LHS)

Level

4

Global Market Timing Indicator

Component Signals - Breadth

Market breadth refers to the fraction of the overall market participating in an up or down move.

Indicative of sentiment

Positive market breadth implies that bullish sentiment controlling momentum

Two component indicators:

Price dispersion: Measures the spread of directional price movements.

Volume dispersion: Measures how widely dispersed directional volume movements are.

5

Page 7

Global Breadth Signal and FTSE World Index

100

150

200

250

300

350

400

450

500

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

Source: Nomura Strategy Research

Index Global Breadth

Signal (RHS)FTSE World Index (LHS)

Level

6

Global Market Timing Indicator

Component Signals – Volume Divergence

The amount of volume in a market is generally seen as an indicator of liquidity.

Low volume could imply market movements in excess of normal relationships.

Some evidence that certain investors underreact to the information contained in order flow.

Volume-divergence signal measures extent to which returns have moved in excess of underlying

volume.

Liquidity is generally mean-reverting and this signal captures the possibility of reversion.

7

Page 9

Global Volume Divergence Signal and FTSE World Index

100

150

200

250

300

350

400

450

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Source: Nomura Strategy Research

Index

Global Vol.

Divergence Signal

(RHS)

FTSE World Index (LHS)Level

8

Global Market Timing Indicator

Component Signals – Trend

Several behavioural reasons why trend occur

‘Representativeness heuristic’: causes trend-chasing as people believe trends have systematic

causes.

Important to assess whether the market is following a trend.

Many trend strategies underperform due to the lags involved.

Adaptive moving average: more responsive and takes into account how noisy recent market

movements have been.

9

Page 11

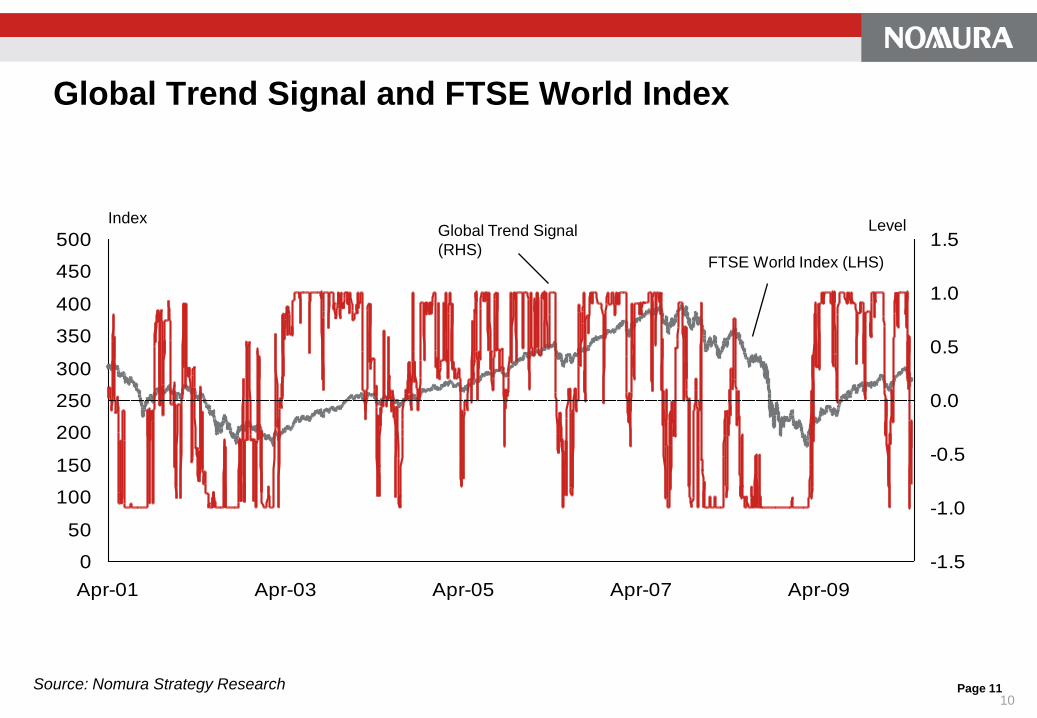

Global Trend Signal and FTSE World Index

0

50

100

150

200

250

300

350

400

450

500

Apr-01 Apr-03 Apr-05 Apr-07 Apr-09

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

Source: Nomura Strategy Research

IndexGlobal Trend Signal

(RHS)FTSE World Index (LHS)

Level

10

Global Market Timing Indicator

Component Signals – Risk

Risk is fundamental to all asset pricing models

High risk aversion indicates that market is generally close to a bottom

Three components:

Implied to realised volatility

Put-call ratio

Average idiosyncratic volatility

11

Page 13

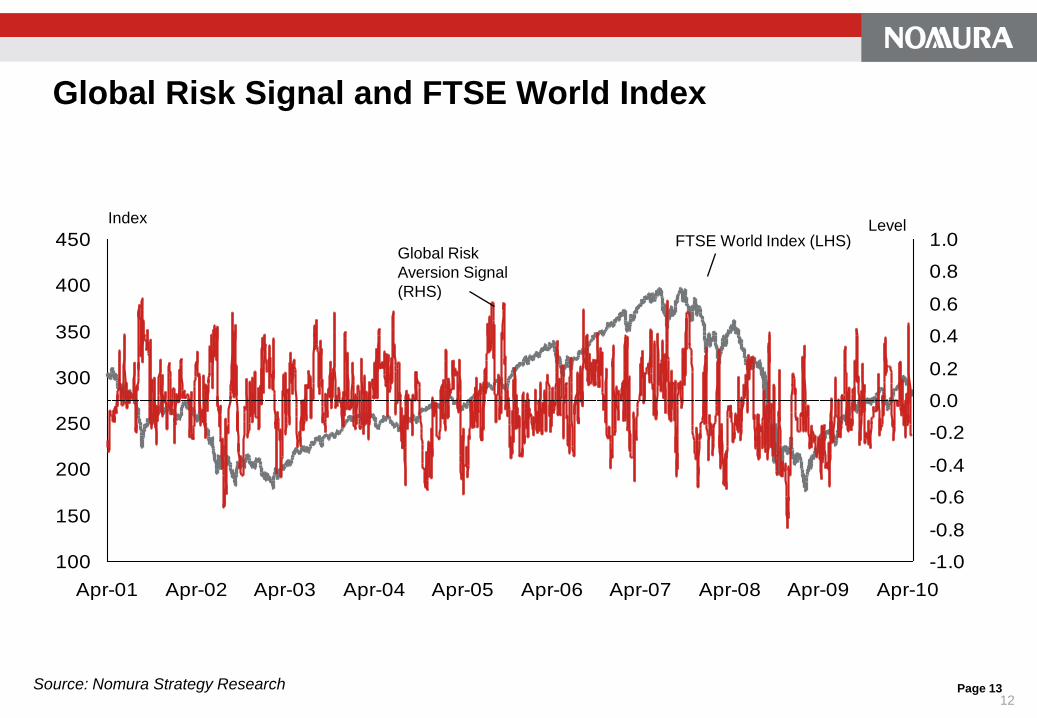

Global Risk Signal and FTSE World Index

100

150

200

250

300

350

400

450

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Source: Nomura Strategy Research

Index

Global Risk

Aversion Signal

(RHS)

FTSE World Index (LHS)Level

12

Page 14

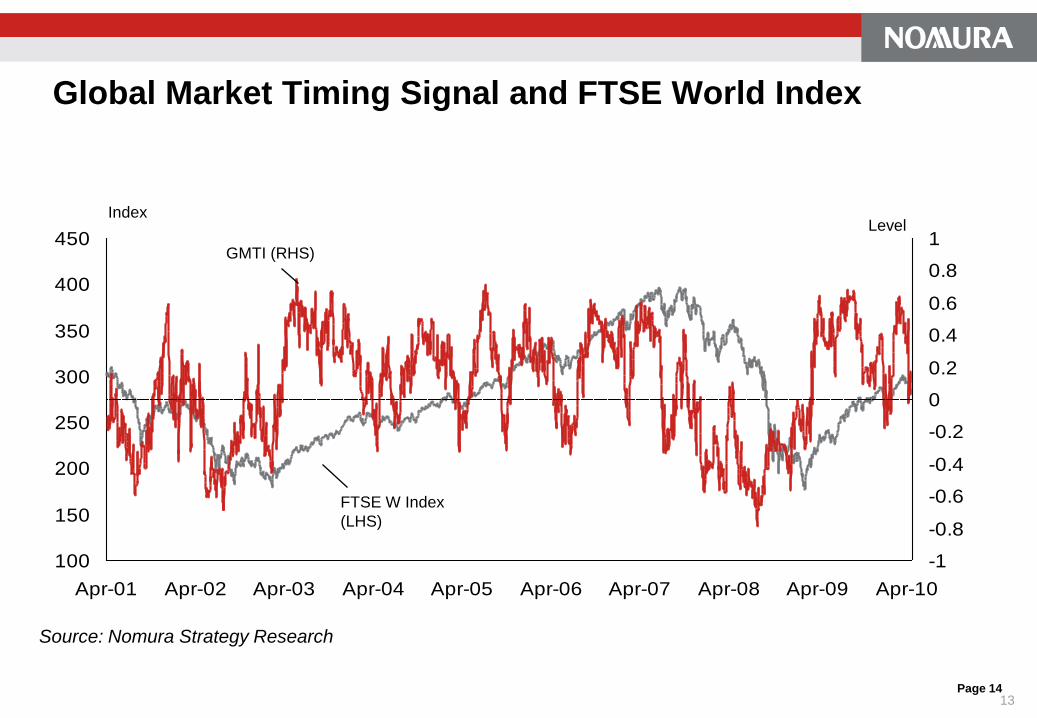

Global Market Timing Signal and FTSE World Index

100

150

200

250

300

350

400

450

Apr-01 Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

-1

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Source: Nomura Strategy Research

Index

GMTI (RHS)

FTSE W Index

(LHS)

Level

13

Page 15

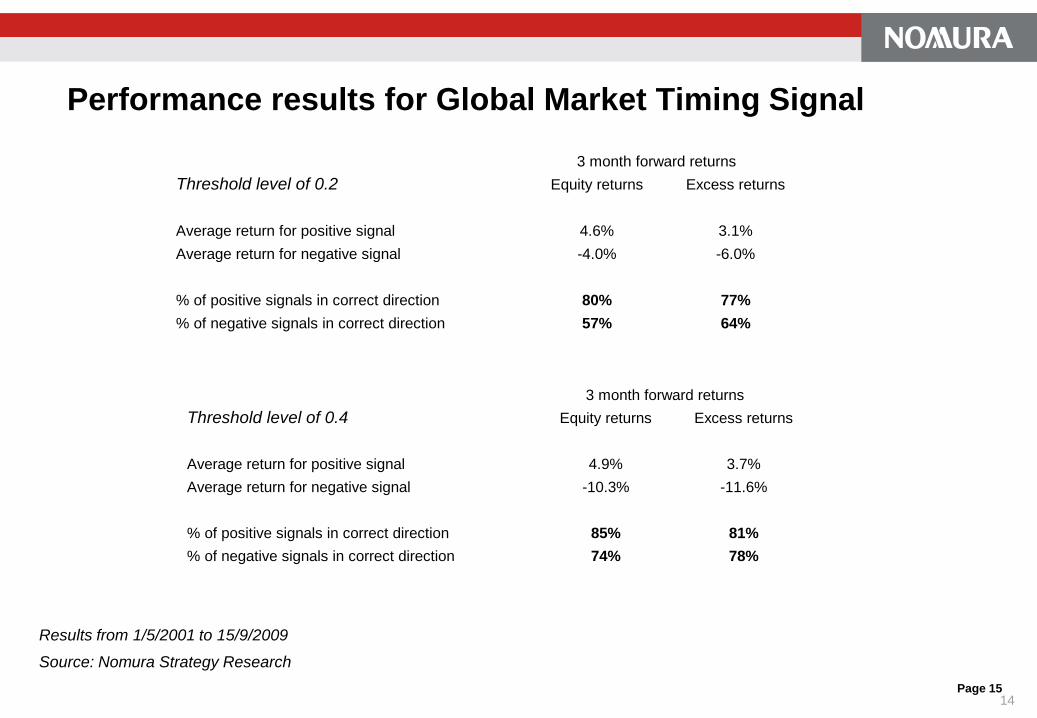

Performance results for Global Market Timing Signal

3 month forward returns

Threshold level of 0.2 Equity returns Excess returns

Average return for positive signal 4.6% 3.1%

Average return for negative signal -4.0% -6.0%

% of positive signals in correct direction 80% 77%

% of negative signals in correct direction 57% 64%

3 month forward returns

Threshold level of 0.4 Equity returns Excess returns

Average return for positive signal 4.9% 3.7%

Average return for negative signal -10.3% -11.6%

% of positive signals in correct direction 85% 81%

% of negative signals in correct direction 74% 78%

Results from 1/5/2001 to 15/9/2009

Source: Nomura Strategy Research

14

Performance of Global Market Timing Indicator – Long/ShortWeekly rebalancing

50

100

150

200

250

300

350

400

450

05/2001 05/2002 05/2003 05/2004 05/2005 05/2006 05/2007 05/2008 05/2009 05/2010

Chart shows the absolute performance of the strategy using the Global Market Timing Signal to go long/short equities (FTSE World Index, total

returns, $ terms) with the remaining proportion in Cash (6m LIBOR). The signal is smoothed over 10 days and the rebalancing is done on a

weekly basis. Performance is shown prior to transactions costs.

Source: Nomura Equity Strategy

May 2001=100

Market Timing

strategy

Signal level % Equities

< -0.4 -100%

>-0.4 and < -0.2 -50%

>-0.2 and < 0.2 0%

> 0.2 and < 0.4 50%

> 0.4 100%

Return Risk Return/Risk

Market Timing 16.1% 12.9% 1.25

15