Market Structure: Key characteristics Key characteristics Knowledge/ Information Product homogeneity...

24

Market Structure: Key characteristics Key characteristics Knowledge/ Information Product homogeneity / brandin Barriers to entry / e Number of firms Interrelations hips within markets e.g. Boeing and Airbus Perfect Knowledge – every firm has access to the same info Products differentiated from competition – easier to control

-

Upload

bartholomew-elliott -

Category

Documents

-

view

227 -

download

8

Transcript of Market Structure: Key characteristics Key characteristics Knowledge/ Information Product homogeneity...

Market Structure: Key characteristics

Key characteristics

Knowledge/ Information Product homogeneity / branding

Barriers to entry / exitNumber of firms

Interrelationships within markets

e.g. Boeing and Airbus

Perfect Knowledge – every firm has access to the

same info

Products differentiated from

competition – easier to control

Course Specs

• Audit– Using your course specs, identify – two areas you are looking forward – two areas you are concerned about

Mergers and Demergers

Aims:• Investigate mergers/ takeovers in more

detail

• Consider why mergers are often not as beneficial in reality

• Why firms sometimes de-merge

Merger and Demerger Research

• Each of the following are planned or completed mergers/demergers. For each of them research:

The reasons for the merger (EG growth, economies of scale)The type of integration (EG horizontal or vertical)Was it agreed or hostile?How did stakeholders react eg employeesFor mergers that did not complete, what was the reason

British Airways and IberiaKraft and CadburysAsda and NettoL’Oreal and Body ShopVodafone and MannersmannICI and Zenneca Fosters sells off wine businessBoots and Dolland & AitchisonDaimler and ChryslerIntel and McAfee

CompanyThe reasons for the merger (EG growth, economies of scale)

The type of integration (EG horizontal or vertical)

Was it agreed or hostile?

How did stakeholders react eg employees

For mergers that did not complete, what was the reason

Anglo-American and Xstrata to merge?

• Mining giant Anglo American may merge with Swiss rival Xstrata.

• Both own coal and copper mining operations

• What might the benefits of the merger be?

Possible Reasons

• Synergy. The combined company is worth more than the sum of its parts. This includes cost reductions by removing duplicate departments. M&A means job losses!

• Economies of scale. Better deals because of increased order size, bulk-buying discounts etc.

• Increased revenue and market share. Increased size of the combined company increases market power and ability to set higher prices.

• Cross-selling. This is when the two companies involved in the deal sell each others products and services, increasing sales.

• Diversification. This helps smooth the earnings results of a company, which over the long term, is rewarded by a higher share price.

• Acquiring unique capabilities and resources. Sometimes it’s simply impossible for a company to create the technology, resource etc it needs to sustain its growth. It can be a lot simpler to just buy it.

• International Expansion. Acquiring a local competitor helps to get over culture issues, government policy, regulation and other issues related to international expansion.

What’s the difference between a merger

and a takeover?• Merger = where 2

companies combine to become one new company. Usually a combination of equals. Agreed by Directors of both companies.

• Takeover = where one company wants to buy another company and make it part of its existing business. This may or may not be agreed

The Merger or Takeover Process

Key terms: Acquirer/Predator and Target1. Acquirer buys some shares in Target2. Acquirer publicly announces decision to

merge/takeover3. Target Responds: Accepts, Negotiates or

Rejects/Defends – the latter is known as a ‘Hostile Takeover’

4. Share Price volatility and battle to persuade Target shareholders to sell. Media campaigns.

5. Sale agreed or Predator walks6. Possible Competition Commission investigations

– merger may be allowed, refused or approved subject to conditions

Can you name me any recent merger or

takeovers?

Kraft strategic objectives

• Build a High-Performing Organization: It’s no coincidence that our first strategy is about our people – since our employees are the ones powering our success. We have a strong leadership team. We have a simplified organization that puts local business units at the heart of the company so decisions are made closer to the consumer.

• Reframe Our Categories. We market many of the world’s leading and most beloved food brands. And we want our delicious products to give consumers millions of smiles every day. We’re doing this by focusing on building a global powerhouse in snacks, confectionery and quick meals … more delicious than ever.

• Exploit Our Sales Capabilities. We’re taking full advantage of our size and broad reach. We have one of the largest and most powerful sales forces in the food industry. This gives us an advantage that other competitors simply can’t match. In the U.S., store managers have a single sales representative who handles all of our products. In developing markets, we're expanding our distribution in smaller traditional outlets. And we’re working closely with our global customers like Carrefour, Tesco and Wal-Mart.

• Drive Down Costs Without Compromising Quality. For us, product quality always comes first. But we’re also always looking for ways to reduce costs, so we can invest more in making truly delicious products that people love.

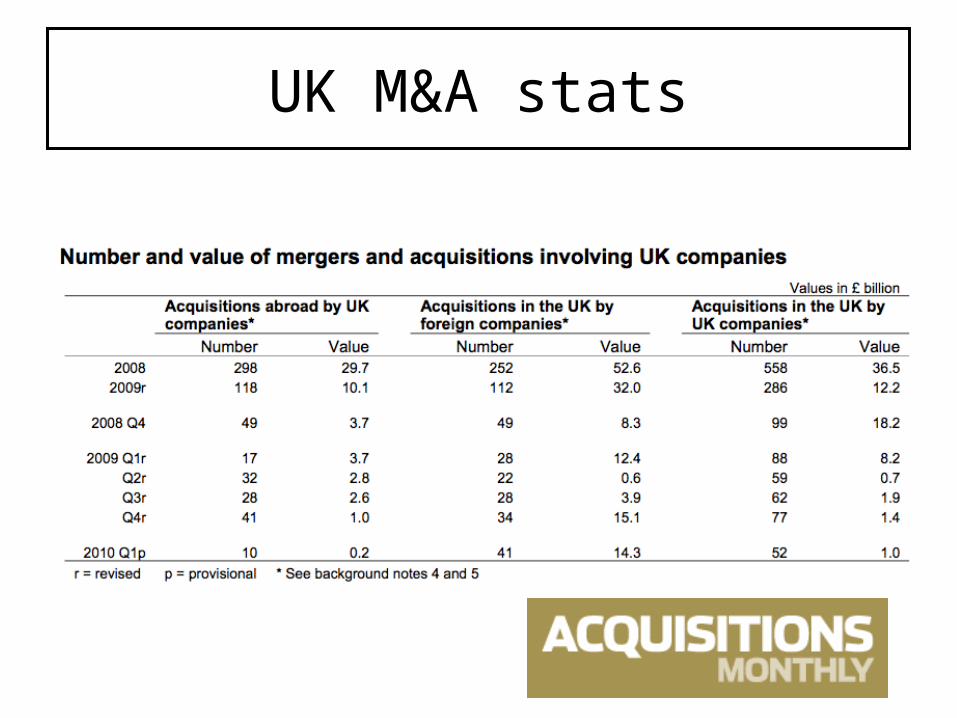

UK M&A stats

Ryannair attempts to takeover

Aer Lingus

Microsoft attempts to acquire Yahoo!

In the Microsoft Vs Yahoo! takeover battle, Microsoft had their initial offer of $31 a share, a 62% premium on Yahoo!’s pre-offer price, rejected, so they offered $33. But Microsoft resolutely refused to go any higher and in the end gave up.

Intel and McAfee

Some mergers fail at the first hurdle

• Hostile takeovers e.g. Philip Green’s bid for M & S• ‘Predator’ company unable to convince enough of

‘target’ shareholders to sell their shares• Disagreements between the two companies at

discussion stages• Competition law issues• Extreme costs of merger – lawyers, accountants,

merchant banks• Stock market volatility• Change in economic environment – business cycle• Problems at the ‘due diligence’ stage – eg

unforseen or more extensive liabilities in target (Pensions)

Even where mergers are successful

• There will inevitably short-run problems:– Combining two cultures– Combining two boards of directors– Integrating different systems e.g. ICT– Getting rid of duplication– Managing staff uncertainty and unions - job

losses– Costs of merger and integration issues

Why mergers sometimes don’t work

• Experts’ surveys suggest that over 75% of mergers/acquisitions fail to achieve the benefits which they are supposed to.

• Sometimes businesses ‘demerge’ - split into two or more independent businesses.

Reasons for Demergers

• Lack of Synergy and Diseconomies of ScaleSynergy is the belief that the merging of two or more firms will have a greater outcome than the sum of the two individual firms. 1+1=3

In reality there may not be this synergy – the two combined businesses do not impact on each other positively. There could be diseconomies as managers have to divide their time between two businesses which have little to do with each other

Reasons for Demergers

• Price The price of the demerged firms might be higher than the price of a single firm. Eg Poor performance of a part of a company may drag down the share price of the whole company

• Focussed CompaniesIn 1970’s conglomerative mergers were common. Since then there has been more evidence that focussing on one core business achieves greater profits and growth. So firms may sell off parts of their organisation that don’t fit with there core activities

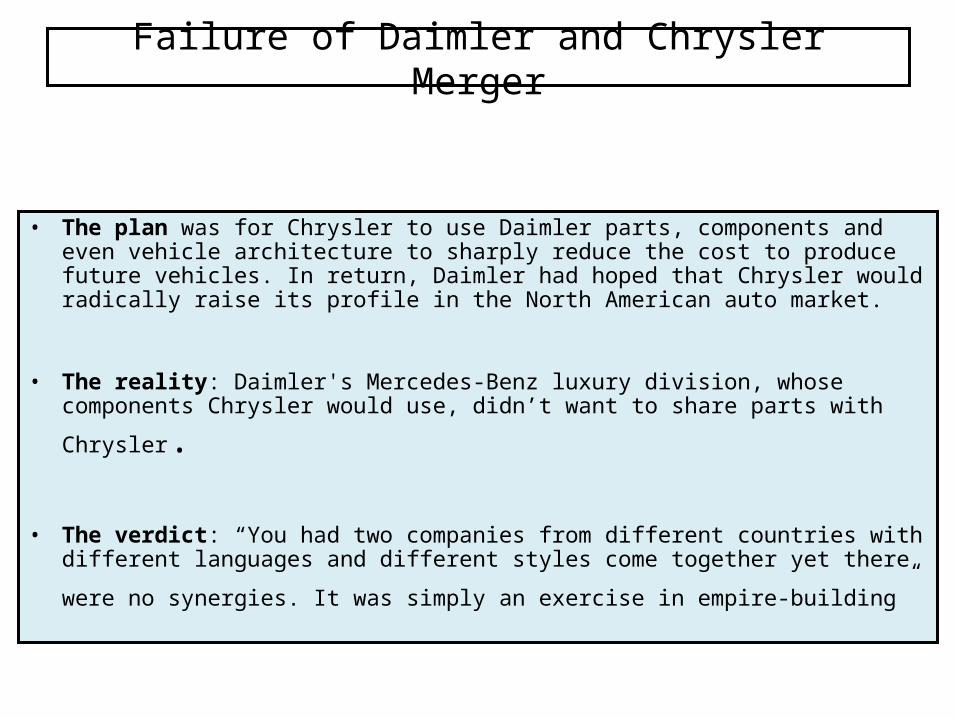

Failure of Daimler and ChryslerMerger

• The plan was for Chrysler to use Daimler parts, components and even vehicle architecture to sharply reduce the cost to produce future vehicles. In return, Daimler had hoped that Chrysler would radically raise its profile in the North American auto market.

• The reality: Daimler's Mercedes-Benz luxury division, whose components Chrysler would use, didn’t want to share parts with

Chrysler.

• The verdict: “You had two companies from different countries with different languages and different styles come together yet there were

no synergies. It was simply an exercise in empire-building”

Mergers and Efficiency

• No automatic gains in profit/efficiency

Productive efficiency will increase if the merger reduces average costs of production (Economies of Scale) but this doesn’t always occur.

Allocative efficiency will increase if the merged firm provides a wider range of goods, better quality products – but mergers often fail to achieve this as they tend to reduce competition in the market place

How does market structure affect business behaviour?

This lesson’s topic was….• And it covered…..• And a key term was…• And this meant….• and the reason that’s important is ….• And the lesson also covered…• And a key term was…• And…