Western Europe (EU-16) In Vitro Diagnostics Market Report & Forecast (2012 – 2015)

Upload

netscribes-incCategory

view

111download

0description

Insert Cover Image using Slide Master View

Do not distort

In Vitro Diagnostics Market – India

October 2014

2 IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

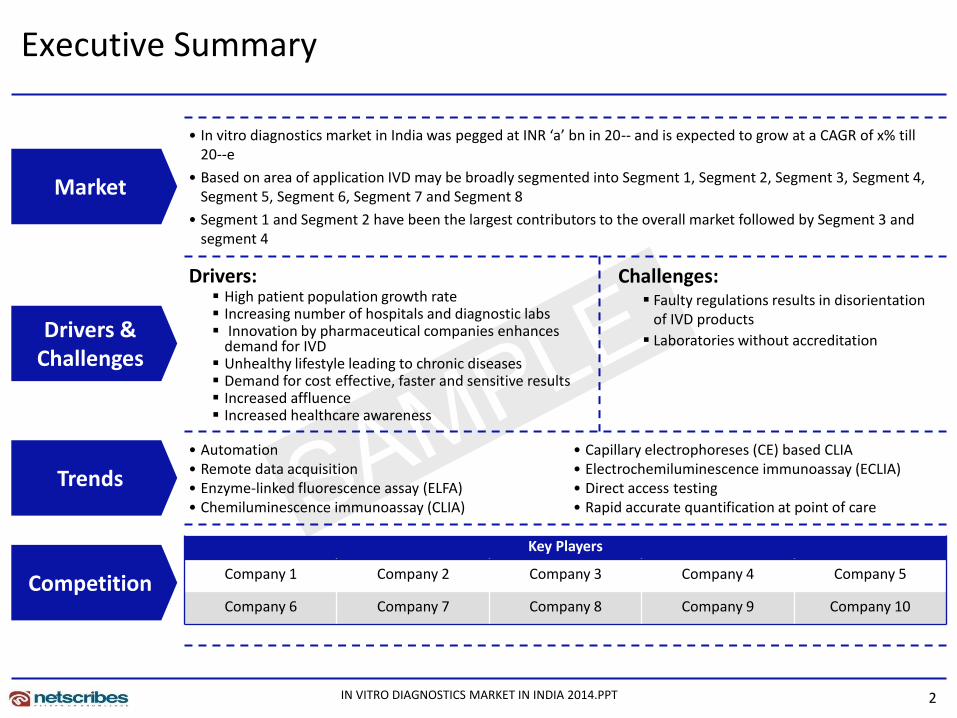

Executive Summary

Market

Drivers & Challenges

Competition

• In vitro diagnostics market in India was pegged at INR ‘a’ bn in 20-- and is expected to grow at a CAGR of x% till 20--e

• Based on area of application IVD may be broadly segmented into Segment 1, Segment 2, Segment 3, Segment 4, Segment 5, Segment 6, Segment 7 and Segment 8

• Segment 1 and Segment 2 have been the largest contributors to the overall market followed by Segment 3 and segment 4

Drivers: High patient population growth rate Increasing number of hospitals and diagnostic labs Innovation by pharmaceutical companies enhances

demand for IVD Unhealthy lifestyle leading to chronic diseases Demand for cost effective, faster and sensitive results Increased affluence Increased healthcare awareness

Challenges: Faulty regulations results in disorientation

of IVD products

Laboratories without accreditation

Trends

Key Players

Company 1 Company 2 Company 3 Company 4 Company 5

Company 6 Company 7 Company 8 Company 9 Company 10

• Automation • Remote data acquisition • Enzyme-linked fluorescence assay (ELFA) • Chemiluminescence immunoassay (CLIA)

• Capillary electrophoreses (CE) based CLIA • Electrochemiluminescence immunoassay (ECLIA) • Direct access testing • Rapid accurate quantification at point of care

3

•Macroeconomic Indicators

•Introduction

•Market Overview

•Drivers & Challenges

•Laws and Guidelines

•Trends

•Competitive Landscape

•Future Outlook

•Strategic Recommendations

•Appendix

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

4

Economic Indicators (1/3)

11

12

13

14

15

b2

a2

Q1

d1 c1

b1

a1

Q4

c4

b4

a4

Q3

c3

b3

a3

Q2

d2 c2

INR tn

2013-14 2012-13 2011-12 2010-11

GDP at Factor Cost: Quarterly

Inflation Rate: Monthly

-2

-1

0

1

2

q

Jul 2013 - Aug 2013

p

%

Nov 2013 - Dec 2013

t

Oct 2013 - Nov 2013

s

Sep 2013 - Oct 2013

r

Aug 2013 - Sep 2013

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

5

In vitro diagnostics has shown tremendous potential in India and…

• Indian IVD market was valued at INR ‘a’ bn in 20--

and is expected to reach INR ‘f’ bn by 20--, growing at

a CAGR of x%

• Indian IVD market is the third largest IVD market in

Asia after Country 1 and Country 2

• Private players contribute u% of the market while the

rest v% is contributed by public players

• Various factors such as rising prevalence of diseases,

growing affordability among patients, and increasing

penetration of health insurance have resulted in

growth in the demand for diagnostic services

• Indian market has traditionally been import

dependent but is now experiencing a transition

towards domestic manufacturing

• In terms of segments, Segment 1 and Segment 2

have been the largest contributors followed by

Segment 3 and Segment 4

The four segments together contribute more than y% of

the overall market

Market Overview – In Vitro Diagnostics Market Size and Growth

0

20

40

60

INR bn

x%

20--e

f

20--e

e

20--e

d

20--e

c

20--e

b

20--

a

Indian IVD Market – Segments

p% r%

s% q%

n%

m%

l% o%

Segment 5

Segment 8

Segment 7

Segment 6

Segment 3

Segment 2

Segment 1

Segment 4

Figures are for 2011

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

6

…is expected to consistently grow with greater emphasis on reagents

• Reagents contribute a greater share to overall

revenues in the IVD market than instruments

Instruments were pegged at INR a1 bn in 20-- and this is

expected to grow to INR f1 bn by 20--

Reagents were valued at INR a2 bn in 20-- and is expected

to reach INR f2 bn by 20--

• Market for IVD instruments is still import dependent

with majority of the analyzers being sourced from

other countries

Most of the analyzers are procured from the Country 1,

Country 2, and lately from Country 3 as well

Companies from these countries have their sales and

service points in most cities in India and hence, procuring

of analyzers is done within a few weeks

• Automation has become a standard norm in the

industry and new demand in the market are mostly

for such analyzers

• Demand for reagents continue to grow especially due

to the need to cater to a large installed base of IVD

instruments

Market Overview – In Vitro Diagnostics Market Size and Growth – Instruments

0

5

10

15

20--e

f1

20--e

e1

20--e

d1

20--e

c1

20--e

b1

20--

a1

INR bn

x1%

Market Size and Growth – Reagents

0

10

20

30

40

x2%

20--e

f2

20--e

e2

20--e

INR bn

d2

20--e

c2

20--e

b2

20--

a2

Elisa Kits and Rapid tests also constitute a part of the overall IVD market

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

7

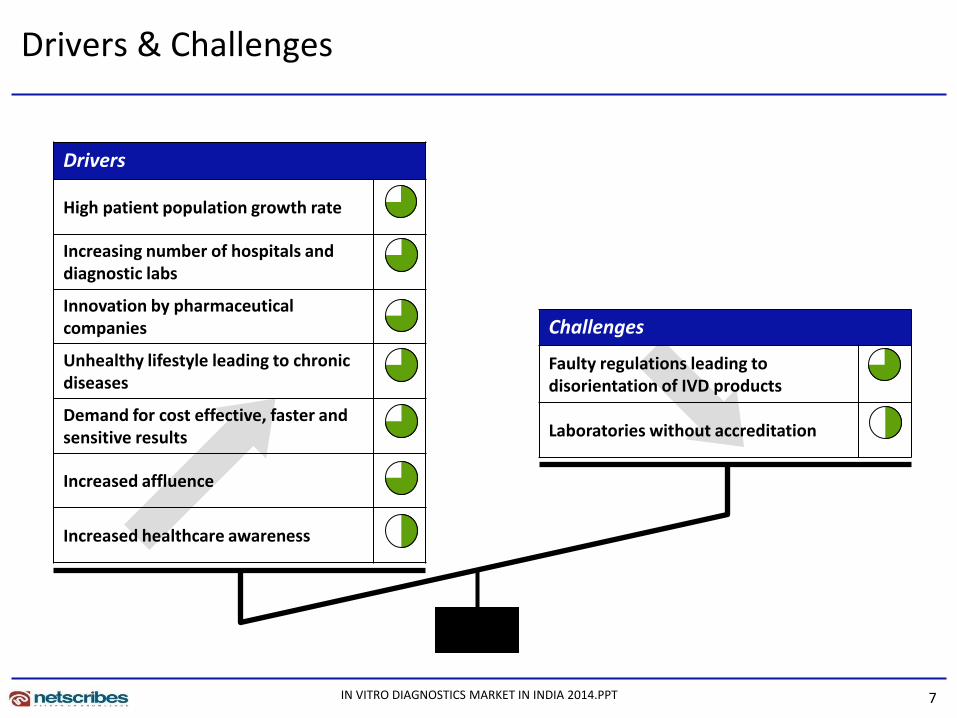

Drivers & Challenges

Drivers

High patient population growth rate

Increasing number of hospitals and diagnostic labs

Innovation by pharmaceutical companies

Unhealthy lifestyle leading to chronic diseases

Demand for cost effective, faster and sensitive results

Increased affluence

Increased healthcare awareness

Challenges

Faulty regulations leading to disorientation of IVD products

Laboratories without accreditation

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

8

Trends – Summary

`

Automation

Remote data acquisition

Chemiluminescence immunoassay (CLIA)

Enzyme-linked fluorescence assay (ELFA)

Trends

Capillary electrophoreses (CE) based CLIA

Rapid accurate quantification at point of care

Direct access testing

Electrochemiluminescence immunoassay (ECLIA)

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

9

SAMPLE Porter’s Five Forces Analysis

Competitive Rivalry

Bargaining Power of Suppliers

Bargaining Power of Buyers

Threat of Substitutes

Threat of New Entrants

Impact x

Impact x

Impact x

Impact x

Impact x

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

10

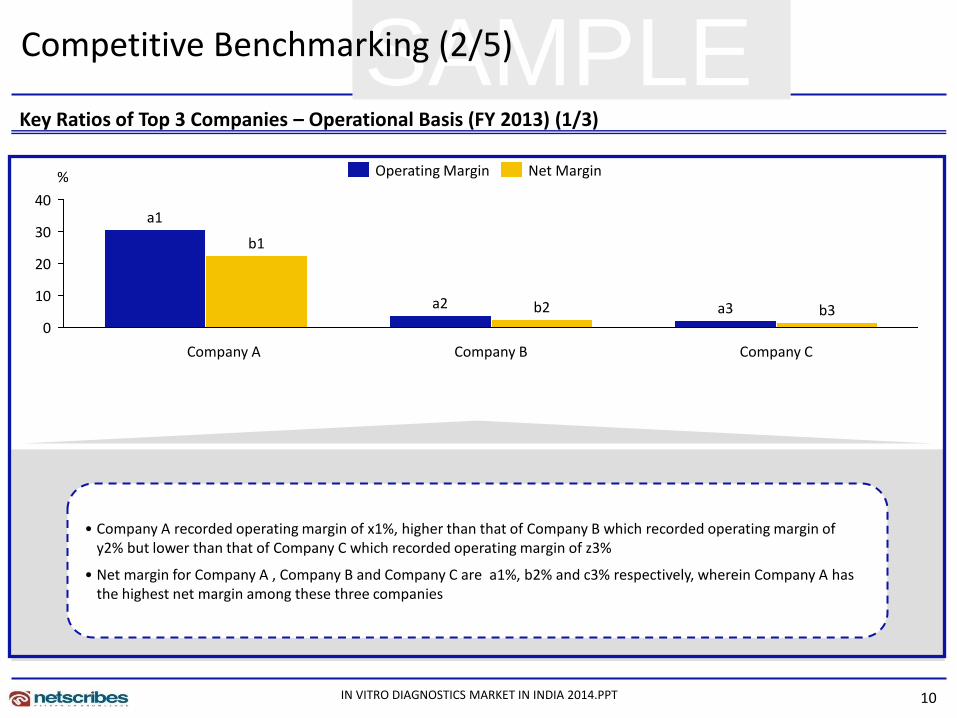

SAMPLE Key Ratios of Top 3 Companies – Operational Basis (FY 2013) (1/3)

Competitive Benchmarking (2/5)

0

10

20

30

40

%

Company C

b3 a3

Company B

b2 a2

Company A

b1

a1

Operating Margin Net Margin

• Company A recorded operating margin of x1%, higher than that of Company B which recorded operating margin of y2% but lower than that of Company C which recorded operating margin of z3%

• Net margin for Company A , Company B and Company C are a1%, b2% and c3% respectively, wherein Company A has the highest net margin among these three companies

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

11

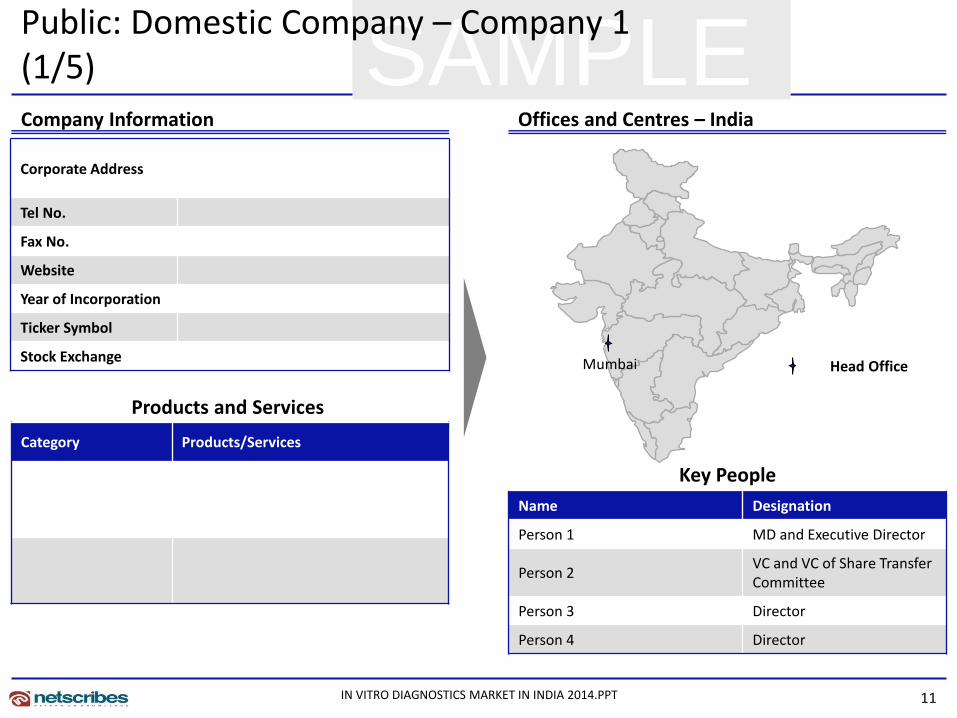

SAMPLE Public: Domestic Company – Company 1 (1/5)

Key People

Products and Services

Company Information Offices and Centres – India

Corporate Address

Tel No.

Fax No.

Website

Year of Incorporation

Ticker Symbol

Stock Exchange

Name Designation

Person 1 MD and Executive Director

Person 2 VC and VC of Share Transfer Committee

Person 3 Director

Person 4 Director

Head Office Mumbai

Category Products/Services

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

12

SAMPLE Financial Snapshot Key Ratios

Financial Summary

• The company earned a net profit of INR x1 mn in FY 2013, as compared to net profit of INR x2 mn in FY 2012

• The company reported total income of INR y1 mn in FY 2013, registering an increase of y2% over FY 2012

• The company earned an operating margin of z1% in FY 2013, an increase of z2percentage points over FY 2012

• The company reported debt to equity ratio of a1 in FY 2013, an increase of a3% over FY 2012

Key Financial Performance Indicators

Indicators Value (20/03/2014)

Particulars y-o-y change

(2013-12) 2013 2012 2011 2010

Profitability Ratios Operating Margin

Net Margin

Profit Before Tax Margin

Return on Equity

Return on Capital Employed

Return on Working Capital

Return on Assets

Return on Fixed Assets

Cost Ratios Operating costs (% of Sales)

Administration costs (% of Sales)

Interest costs (% of Sales)

Liquidity Ratios Current Ratio

Cash Ratio

Leverage Ratios Debt to Equity Ratio

Debt to Capital Ratio

Interest Coverage Ratio

Efficiency Ratios Fixed Asset Turnover

Asset Turnover

Current Asset Turnover

Working Capital Turnover

Capital Employed Turnover

Improved Decline

Net Profit/Loss Total Income

e

d

c

b

a

s

r

q

p

2013

a4

z4

2012

a3

z3

2011

a2

z2

2010

a1

z1

Public: Domestic Company – Company 1 (2/5)

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

13

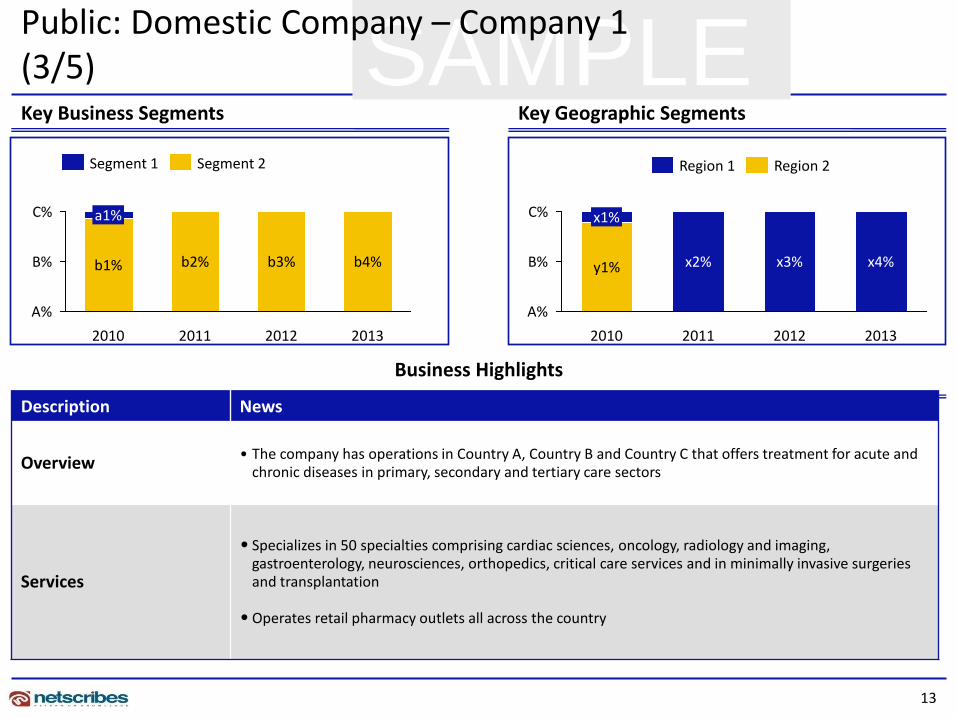

SAMPLE Public: Domestic Company – Company 1 (3/5) Key Business Segments Key Geographic Segments

A%

B%

C%

2013

b4%

2012

b3%

2011

b2%

2010

b1%

a1% C%

B%

A%

2010

y1%

x1%

2013

x4%

2012

x3%

2011

x2%

Region 2 Region 1

Business Highlights

Segment 2 Segment 1

Description News

Overview • The company has operations in Country A, Country B and Country C that offers treatment for acute and

chronic diseases in primary, secondary and tertiary care sectors

Services

• Specializes in 50 specialties comprising cardiac sciences, oncology, radiology and imaging, gastroenterology, neurosciences, orthopedics, critical care services and in minimally invasive surgeries and transplantation

• Operates retail pharmacy outlets all across the country

14

SAMPLE

T O

W S

Public: Domestic Company – Company 1 – SWOT Analysis (5/5)

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

15

SAMPLE Private: Domestic Company – Company 2 (1/5)

Key People

Products and Services

Company Information Offices and Centres – India

Name Designation

Person 1 Director

Person 2 Director

Person 3 Director

Person 4 Director

Corporate Address

Tel No.

Fax No.

Website

Year of Incorporation Head Office

Category Products/Services

Ready Meals

Instant Mixes

Others

Mumbai

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

16

SAMPLE Private: Domestic Company – Company 2 (2/5)

Shareholders of the Company Ownership Structure

Name No. of Shares held

23.6%57.4%

19.0%

Segment

Segment

Segment

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

17

SAMPLE Financial Snapshot Key Ratios

Particulars y-o-y change

(2013-12) 2013 2012 2011 2010

Profitability Ratios Operating Margin

Net Margin

Profit Before Tax Margin

Return on Equity

Return on Capital Employed

Return on Working Capital

Return on Assets

Return on Fixed Assets

Cost Ratios Operating costs (% of Sales)

Administration costs (% of Sales)

Interest costs (% of Sales)

Liquidity Ratios Current Ratio

Cash Ratio

Leverage Ratios Debt to Equity Ratio

Debt to Capital Ratio

Interest Coverage Ratio

Efficiency Ratios Fixed Asset Turnover

Asset Turnover

Current Asset Turnover

Working Capital Turnover

Capital Employed Turnover

Private: Domestic Company – Company 2 (3/5)

Improved Decline

Financial Summary

• The company earned a net profit of INR x1 mn in FY 2011, as

compared to net profit of INR x2 mn in FY 2010

• The company reported total income of INR x3 mn in FY 2011,

registering an increase of x4% over FY 2010

• The company earned an operating margin of x5% in FY 2011,

an increase of x6 percentage points over FY 2010

• The company reported debt to equity ratio of x7 in FY 2011, a

decrease of x8% over FY 2010

Net Profit/Loss Total Income

a

t

s

r

q

f

p

b

c

d

e

b4

a4

2011 2008

a1

b1

2010

a3

b3

2009

a2

b2

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

18

SAMPLE Description News

Overview • Company 2 has hospital network in Country A, Country B and Country C and is primarily headquartered in

Country D

• Presently located in 10 cities in India having hospitals in Region 1, Region 2 and Region 3

Facilities • Has core specialties in heart care, brain and spine, bone and joint and minimal access surgery

• Provides advanced medical diagnostics and treatment with personal care

Recognitions • Obtained NABH accreditation within one and a half years of beginning operation in India

• Hospital A, Region 1, Hospital B, Region 2 has been NABH accredited

Business Highlights

Private: Domestic Company – Company 2 (3/5)

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

19

SAMPLE

T O

W S

Private: Domestic Company – Company 2– SWOT Analysis (5/5)

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT

20

Thank you for the attention

About Netscribes, Inc. Netscribes, Inc. is a knowledge-consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment & business research, business & corporate intelligence, content-management services, and knowledge-software services. At its core lies a true value proposition that draws upon a vast knowledge base. Netscribes, Inc. is a one-stop shop designed to fulfil clients’ profitability and growth objectives.

In Vitro Diagnostics Market in India 2014 – India report is part of Netscribes’ Healthcare Series. For any queries or customized research requirements, contact us at:

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, “Netscribes” is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.

Phone: +91 22 4098 7600 E-Mail: [email protected]

IN VITRO DIAGNOSTICS MARKET IN INDIA 2014.PPT