Market Report 2011 October

18

1) Based on information available as of 17 th October, 2011 21 st October 2011 Economic and Steel Market Outlook 2011-2012 Q4-2011 Report from EUROFER ’s Economic Committee 1) EU macro-economic overview (y-o-y change in %) EUROFER Forecast October 2011 EU 2009 2010 2011 (f) 2012 (f) GDP -4.3 1.9 1.5 1.0 Private consumption -1.7 0.9 0.4 0.7 Government consumption 2.2 0.6 0.2 -0.1 Investment -11.8 0.0 1.9 2.3 Investment in mach. equip. -17.7 3.8 5.2 3.7 Investment in construction -6.3 -3.4 0.7 0.9 Exports -10.9 10.4 6.1 4.2 Imports -10.3 9.3 4.3 3.2 Unemployment rate 9.1 9.6 8.7 8.7 Inflation 0.7 1.9 2.8 2.0 Industrial production -13.8 7.1 3.8 2.3 (f) = forecast I. EU Macro-economic overview Recovery lost steam in Q2 Indicators weaken on r esurfacing of sovereign debt concerns Manufacturing to remain bright spot in darkened outlook ECB changing its policy stance Fragile recovery - no recession Risks skewed to the downside GDP growth in the second quarter of 2011 slowed to a disappointing 0.2% q-o-q. The recovery losing steam did not come as a surprise. The boost from mild weather conditions which had temporarily bolstered growth in early 2011 faded at the end of the first quarter. At the same time, the negative effect of austerity measures through fiscal tightening and subdued govern- ment consumption on domestic demand became more pronounced. Private consumption was rather dull, reflecting weak confidence levels and the effect of high inflation and fiscal tightening on disposable incomes. Meanwhile, slowing global economic growth dampened dynamics in interna- tional trade, thereby reducing export opportunities for EU exporters. The Euro‟s relative strength versus the US dollar has also hurt foreign trade in the second quarter. The strongest deceleration in economic growth was seen in the core countries Germany and France as well as in some smaller EU countries that

-

Upload

andra-elena-alexandrescu -

Category

Documents

-

view

220 -

download

0

Transcript of Market Report 2011 October

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 1/18

1) Based on information available as of 17

th October, 2011

21st

October 2011

Economic and Steel Market Outlook 2011-2012 Q4-2011 Report from EUROFER ’s Economic Committee 1)

EU macro-economic overview(y-o-y change in %)

EUROFER ForecastOctober 2011

EU 2009 2010 2011

(f)2012

(f)

GDP -4.3 1.9 1.5 1.0

Private consumption -1.7 0.9 0.4 0.7

Government

consumption2.2 0.6 0.2 -0.1

Investment -11.8 0.0 1.9 2.3

Investment in mach.equip.

-17.7 3.8 5.2 3.7

Investment inconstruction

-6.3 -3.4 0.7 0.9

Exports -10.9 10.4 6.1 4.2

Imports -10.3 9.3 4.3 3.2

Unemployment rate 9.1 9.6 8.7 8.7

Inflation 0.7 1.9 2.8 2.0

Industrial

production-13.8 7.1 3.8 2.3

(f) = forecast

I. EU Macro-economic overview

Recovery lost steam in Q2

Indicators weaken on resurfacing

of sovereign debt concerns

Manufacturing to remain bright

spot in darkened outlook

ECB changing its policy stance

Fragile recovery - no recession

Risks skewed to the downside

GDP growth in the second quarter of

2011 slowed to a disappointing 0.2%

q-o-q. The recovery losing steam did

not come as a surprise. The boost from

mild weather conditions which had

temporarily bolstered growth in early

2011 faded at the end of the first

quarter. At the same time, the negative

effect of austerity measures through

fiscal tightening and subdued govern-

ment consumption on domestic

demand became more pronounced.

Private consumption was rather dull,

reflecting weak confidence levels and

the effect of high inflation and fiscal

tightening on disposable incomes.Meanwhile, slowing global economic

growth dampened dynamics in interna-

tional trade, thereby reducing export

opportunities for EU exporters. The

Euro‟s relative strength versus the US

dollar has also hurt foreign trade in the

second quarter.

The strongest deceleration in

economic growth was seen in the core

countries Germany and France as wellas in some smaller EU countries that

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 2/18

2

had registered a robust performance in

the first quarter. Consequently, growth

differentials at the country level

narrowed to some extent.

Leading indicators head south

Due to sovereign debt concerns

resurfacing, leading indicators headed

south during summer. Readings had

already been under pressure during

the second quarter on concerns about

the sovereign debt crisis and the

vulnerability of EU‟s financial systems

and on evidence that global economic

growth had started to slow.

Agreement on a second bailout

programme of 109 billion Euro for

Greece could calm down market

turmoil only for a short while. Since

August, doubts about the progress

made by the Greek government on its

debt reduction programme fuelled

speculation on Greece not being able

to meet several critical fiscal targets

that are conditional to getting the next

instalment of the bailout money from

the EU, IMF and ECB.

Under the current circumstances,

rumours suffice to send big ripples into

the markets. Stock markets registered

hefty losses, bond spreads increased

and the Euro came under pressure.

Economic confidence in the EU

decreased quite significantly in August

and September.

Also other forward looking indicators

turned sour in recent months. The

Markit Eurozone Composite Output

index fell to below 50 in September,

reflecting that the assessment of

business activity in the corporate

sector has hit a two-year low. Also the

OECD leading economic indicators for

Europe lost strength in recent months.

Poor Q2 growth figures, not only in the

EU but also elsewhere in the advanced

economies, slipping indicators and

increased risk and uncertainty levels

related to the intensification of the

Eurozone sovereign debt crisis have

led to EUROFER‟s Economic

Committee revising its economic

growth forecasts for 2011 and 2012.

Manufacturing sentiment is weakening

Indicators on manufacturing activity

have been mixed lately.

Sentiment in industry has been losing

strength since April, and slipped further

in September to just above the long-

term average. In addition to a less

positive assessment of order intakes

and production expectations, the latest

surveys suggest that since July stocks

of finished products in the supply chain

are on the rise.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 3/18

3

Meanwhile, since June actual order

data have started to mirror weakening

business conditions as well. Month-on-

month growth in industrial new

bookings turned negative in June andJuly, more so in the Eurozone than in

the EU27.

Meanwhile, industrial production in July

and August continued to grow at a rate

of close to 5% year-on-year. Germany

registered in July even two-digit output

growth.

Underlying data show that particularly

output of capital goods continued to

increase at a healthy rate, with

demand increasingly supported by

domestic sales. Corporate investment

in machinery and equipment in Europe

has picked up following very weak

investment activity during the 2009

recession. This has broadened the

basis of the manufacturing recovery in

the EU which had been strongly reliant

on exports until this year.

Activity not seen falling off a cliff

The current mix of indicators and hard

data on industrial bookings and activity

appears to suggest that, while high

uncertainty and risk levels have a

negative impact on business

confidence, industrial momentum has

not yet grinded to a halt. Well-filled

order books in most manufacturing

sectors will for the time being cushion

the impact of slowing order intakes,

keeping industrial activity at a rather

satisfactory level.

Nevertheless, it is evident that output

will slow down or could even turn

temporarily negative in the months

ahead should the weakening trend in

new order intakes persist. The recent

depreciation of the Euro against the

US dollar could help improving the

competitiveness of Eurozone compa-

nies abroad and soften the effects of

such a downturn.

The outlook for 2012 is currently

clouded by more uncertainties than

some months ago. The central forecast

assumes investment growth in the EU

to continue at a rate of around 2% in

2012. Should the sovereign debt crisis

deteriorate to beyond a manageable

level, it will most certainly backfire on

industrial confidence and result in a

more pronounced slowdown or

reduction in corporate investment.

This will be exacerbated by tighteningcredit conditions in EU‟s financial

markets. Interbank lending is

reportedly showing signs of tension

since summer which appears to

suggest that access to credit could

become more difficult and cost of

lending for the private sector will rise.

Export demand is to remain another

important pillar supporting activity in

EU‟s manufacturing industry. However,the rebound in international trade

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 4/18

4

appears to have entered a soft patch.

EU‟s export opportunities are largely

shaped by the economic performance

of Asia and other emerging economies.

Capacity limits and monetary

tightening in response to high inflation

have in 2011 tempered GDP growth in

this part of the world. Growth prospects

for 2012 look nevertheless still rather

solid; inflation is easing and

governments could decide to stimulate

the economy by loosening up their

fiscal and monetary policies if

necessary.

Despite activity losing momentum,

manufacturing looks set to remain a

relatively bright spot on the overall

darkened EU economic landscape in

the remainder of 2011 and in 2012.

Consumption showing signs of sagging

The outlook for the other components

of domestic demand is bleak. Pressure

on EU governments to cut budgets

more rapidly has intensified in recent

months, not only in the debt-ridden

peripheral Eurozone countries but also

in the core countries with a structurally

solid budget and debt performance. As

a result, government spending across

the EU will be reduced more briskly

than projected before. Inevitably, this

will be felt in all sectors of the

economy.

Consumer confidence deteriorated

quite sharply in recent months due to

the sovereign debt crisis in the

Eurozone countries flaring up and on

concerns that the policy response is

too late and too little. As a result,

private consumption was quite sluggish

in Q2-2011.

The bottom line is that consumers fear

for their jobs, their income and

pensions; particularly in the peripheral

Eurozone countries fiscal retrenchment

and governments shedding jobs has

fuelled social instability.

The modest economic rebound in the

EU has so far not resulted in a

significant decline in unemployment.

In August, the EU27 unemployment

rate stood at 9.5% compared with

9.6% in the same month of 2010.

These figures hide huge differentials at

the country level: unemployment rates

range from around 4-5% in Austria and

the Netherlands to over 21% in Spain.

Generally speaking, employment

growth has been quite benign in the

Northern European countries in which

the manufacturing sector benefitted

strongly from the recovery in

international trade.

Harsh fiscal measures resulting in

downward pressure on household

income, weak job creation and high

unemployment will most likely result in

a certain degree of consumerretrenchment in 2012; our central

forecast sees private consumption

growth remaining below 1% next year.

The risks are clearly on the downside,

owing to unusual high uncertainties

clouding the consumers‟ assessment

of current and expected economic and

financial conditions.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 5/18

5

ECB seen changing its policy stance

Excessive public debt loads in the

peripheral Eurozone countries have

continued to spook financial markets.

Surging yields on government bonds

resulted in surging financing costs for

these countries. Due to rising concerns

about their ability to withstand further

pressure – with the focus shifting from

Greece and Portugal to Spain and Italy

– the ECB decided to purchase

Spanish and Italian debt securities.

This support operation was followed in

September by a move in the ECB

policy from a tightening to an easing

stance. The escalation in financial

market pressures, evidence of lower

inflation, combined with slowing GDP

growth in Q2 and continued weak

prospects for the remainder of the year

and into 2012 have been the catalysts

in the change in policy reaction.

Inflation has eased somewhat in recent

months owing to oil and food comingdown from their peaks registered in

early 2011. In August 2011, EU annual

inflation stood at 2.9% coming from

rates above 3% in the second quarter.

However, inflation is still substantially

higher than in the same period of 2010

when the annual inflation rate was

around 2%.

An interest rate cut appears to be on

the cards later this year, possiblyfollowed by another one in the first

months of 2012 should downside risks

to economic growth and inflation

persist.

The shift in ECB stance triggered

downward pressure on the Euro. The

currency had kept its strength during

the second quarter and in the July-

August period, remaining within a

rather narrow bandwidth of 1.40-

1.45US$, despite weakening indicators

and financial market woes.

Since early September however,

pressure started to mount and the Euro

exchange rate versus the US dollar

slipped recently below 1.35 US$.

The Euro depreciation is good news for

Eurozone exporters. It should be

supportive to softening the effects of

slowing dynamic in international trade

on EU exports. Against the background

of weakened economic growth

prospects for the Eurozone countries

and the likelihood of on-going financial

market turbulence chances are that theEuro will remain under downward

pressure for the time being

Fragile recovery – recession avoided

The latest forecasts for the macro-

economic framework in the remainder

of 2011 and in 2012 from EUROFER‟s

Economic Committee show downward

revisions for annual GDP growth in

2011 and 2012 in comparison with ourprevious outlook. EU economic growth

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 6/18

6

will amount to 1.5% in 2011, and

decelerate further to 1% in 2012.

In the July outlook a moderation in

growth had already been pencilled in,

due to the EU economy facing

significant headwinds and with already

high uncertainty levels potentially

weighing down on EU‟s overall growth

perspectives.

Over summer, risks and uncertainties

have intensified to unusually high

levels due to the Eurozone debt crisis

entering a critical stage.

A key issue is that financial markets

apparently have lost confidence in the

ability of EU political leaders to provide

structural solutions to the debt

problems in the peripheral Eurozone

countries. It is feared that the EU will

be sailing deeper into uncharted

territory while the ship‟s officers

continue to discuss about the best

course to safer waters.

Meanwhile, it is also clear that there is

no easy way out. Many options exist,

all of them will have a negative impact

on EU‟s economic performance which

will be extremely difficult to quantify

with respect to the direct and indirect

effects incorporated in the various

bailout-default scenarios.

The most likely scenario still appears

to be that European policymakers will

be able to contain the debt crisis in the

peripheral Eurozone countries. This“muddling through” scenario assumes

the implementation of the euro-area

financial stability measures announced

on July 21st 2011, together with the first

outline of necessary steps towards

improved governance of the euro area

and a further strengthening of the

capitalisation of EU banks. Future

steps could include a greater

harmonisation and co-operation infinancial crisis management and a

stronger role for the European

Commission including a larger budget.

However, reaching agreement on

these topics will be an even more

challenging „tour de force‟ and

encounter opposition from several EU

member states.

The central scenario also assumes the

continuation and probably inten-

sification of fiscal tightening which

inevitably will stifle economic growth,

which will make the road to recovery

longer and more difficult particularly for

the Southern European economies.

Nevertheless, the EU economy is seen

escaping a double-dip recession.

However, stringent austerity measures

imply that most governments are left

with very little room provide their ailing

economies with new stimulus

measures.

Internal risks have come to the fore

Early 2011 risks to the outlook for the

EU economy were rather diverse,

ranging from the internal risk of

Eurozone indebtedness to external

risks such as rising commodity, energy

and food prices fuelling inflation, the

instability in the Arab world and later

also the impact of the devastating

earthquake in Japan.

These external risks appear to have

become more balanced in recent

months, whereas the internal risks inthe EU have come to the fore and are

presently skewed heavily to the

downside.

These risks are not limited to the

financial and economic stability of

certain endangered Eurozone member

states, but pose a serious threat to the

stability of the banking sector in

Europe and abroad and as such also

to other EU members and the globaleconomy.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 7/18

7

USA GDP growth slows further in Q2 Data revisions reveal weaker

growth than earlier estimated No near term rebound expected

Growth to remain subdued GDP growth was only 1.3%(seasonally adjusted annualised rate)in Q2-2011. Moreover, the recentrevisions to US national accounts showthat the downturn during the recessionhas been deeper and the reboundslower than previously estimated.Private consumption came almost to ahalt in Q2 and manufacturing activity

lost much of the strength it had before.The exceptionally weak constructionand real estate markets continue to actas a drag on economic growth.Looking forward, confidence indicatorshave remained weak during Q3-2011.The ISM manufacturing index fell to just above 50 in August.The debate and last-minute agreementon raising the federal debt ceilingrevealed the lack of a credible fiscal

policy. This was confirmed by S&P‟sdowngrade of US long-term debtrating. Together with concerns aboutthe Eurozone debt crisis this hasintroduced new risks and uncertaintiesthat will dampen growth.Against the background of continuedhigh inflation, the high indebtedness ofthe federal, state and localgovernments as well as private

consumers, disappointing job creationand the persisting housing sectordownturn is it hard to see what couldbe driving a near term rebound of theeconomy.The Fed has indicated it will keep thefederal funds rate to close to zero until,but a third round of quantitative easinghas not yet been confirmed.GDP growth is forecast around 1.5% in2011 by most economic institutes. For

2012 economic growth is projected tobe nearing 2%.

Key emerging regions Growth in China holding up well,

no indication of sharp slowdown Fiscal and monetary policy in

BRICs could become loser if

necessary The Chinese economy continued togrow at a robust pace in Q2-2011;annual growth was 9.5%. So far thisyear, investment remained the driver ofgrowth despite fading support from thefiscal policy. No signals point to amarked near term deceleration of theeconomy. While weak growth in theadvanced economies does not bode

well for China‟s manufacturing sector,production and export held up ratherwell so far this year owing to continuedsolid demand from the Asian region.GDP growth is seen around 9% in2011 and at slightly below 9% in 2012.In India high inflation and interest ratesare putting investment under pressure.Combined with a moderation in exportgrowth, economic momentum slowedin recent months. Should this continue,

the central bank may revise itstightening policy. GDP is seen growingaround 7% in 2011 and 8% in 2012.Brazil‟s economy has been growingmoderately so far this year. Interestrates had been raised to controlinflation; this has attracted large capitalinflows. The central bank cut interestrates again in August on concernsabout the overvalued Real and weaker

than expected Q2 growth. GDP growthmay amount to 4% in 2011 and 2012.In Russia GDP growth slowed to 0.6%q-o-q in the 2nd quarter of this year.Manufacturing momentum hasremained fairly robust so far this year.Inflationary pressures have eased,supported by the appreciation of theRouble. Investment is seen picking upin 2012 supported by a fiscal boost.GDP is forecast to grow 3.5% in 2011

and 4% in 2012.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 8/18

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 9/18

9

Construction

Q2-2011 output growth slowed

down to below 2% y-o-y Uneven country performance Near term prospects to remain

subdued, some improvement in 2012

EU construction activity growth in theEU eased off to below 2% y-o-y in the2nd quarter of 2011, coming from 7.6%in the 1st quarter. Q1 constructionactivity had been boosted by mildweather conditions which helped

output to strengthen considerablycompared with the weak levelregistered in Q1-2010.Drilling down into country data revealslarge differentials in performance.Poland, Germany, Sweden and Francehave seen a positive trend inconstruction activity over the 1st half ofthe year, much in contrast with Spainand Hungary where a double-digit dropin activity was registered. The other EUcountries have on average seen

activity falling slightly or movingsideways at a rather depressed level.The recovery in Germany, France andSweden has been largely driven bynew projects and rising renovation andmodernisation activity in the privateresidential sector. Meanwhile in Polandthe key driver of construction outputgrowth remained civil engineeringinvestment in projects related to theEuro2012 football championship and

public infrastructure.

The outlook for the construction sector

for the coming months remains onbalance rather dim. Constructionsector confidence fell in September tothe lowest level since December 2010,signalling that construction companiesare not expecting any near termimprovement in market conditions. Onbalance, output in 2011 will increaseby almost 2.5%, primarily reflectingstrong growth in Q1 relative to 2010and despite an uneven performance at

the country level.These fundamentals are not likely tochange significantly going into 2012.The rebound in Poland, Germany,France and Sweden will continue,albeit at a slowing pace in the latterthree western European countries. Theother Central European countriesexcept Hungary expect someimprovement in market conditions in2012. Meanwhile, construction activityin Spain will hit bottom and move on

balance sideways. Activity inresidential and renovation andmodernisation projects will improvefurther, in contrast with publicly fundedinfrastructure and non-residentialactivity. Unfortunately this implies thatthe actual boost on demand forconstructional steel products will befairly small.All in all, construction output isprojected to increase almost 3% in

2012.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 10/18

10

Automotive

EU car sales slightly fell 1.3% y- o-y in 8m-2011

CV sales continued to rise Car exports remained firm Output +10% in 2011 Slowdown in 2012 to 3% In the first 8 months of 2011, EUpassenger car sales declined by 1.3%y-o-y. Sales in August rose almost 8%;the rebound was widespread with alllarge markets registering growth. Theweakest markets however remainedSpain, Greece and Portugal due to theextremely low levels of consumerconfidence in these debt-riddencountries.Commercial vehicles sales continuedto grow over summer; in August salesgrew by almost 16% y-o-y. Year-to-date sales rose more than 12% y-o-y.Particularly demand for medium and

heavy trucks remained buoyant, withsales in the 1st eight months of thisyear growing by just below 40%.Export demand remained robust inrecent months. German passenger carexports grew 17% y-o-y August and9% in September; 77% of total caroutput was for export in the January-September period.Automotive output grew by slightlymore than 10% y-o-y in Q2-2011;

continued strong growth since Q1-

2010 has resulted in output nearing thepre-crisis production level by mid 2011.Looking forward this is one explanationof output growth cooling down over thecoming quarters. The other one is therather weak outlook for privateconsumption, due to consumerconfidence falling rather sharply inrecent months. At the same timeprospects for investment have becomeclouded by uncertainties with respectto the general business climate in thecoming quarters. Also export demandis seen slowing on a par with theexpected moderation in globaleconomic growth.Output growth in 2011 is forecast toamount to just over 10%; while growthis positive in all EU countries with anautomotive manufacturing base,Germany and all Central European

countries will register double-digitgrowth this year.Market fundamentals are expected toweaken further in 2012, while stillremaining slightly positive andsupportive to further but significantlyslower output growth.On balance, automotive output in theEU is seen easing off to around 3%;activity in Central Europe will continueto increase at a faster pace than in

Western Europe.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 11/18

11

Mechanical Engineering

Growth in Q2 remained robust EU investment in machinery &

equipment is rising Output growth in 2012 limited

due to cooling investment and export growth

In the 2nd quarter of 2011, activity inthe mechanical engineering industry inthe EU increased almost 12% y-o-y;this is only a mild deceleration

compared to the close to 16% growthin the 1st quarter of this year.Increasingly, domestic demand - drivenby rising corporate investment inEurope - has been driving growth inoutput. Investment in machinery andequipment has been rising since late2010.Meanwhile, also exports continued tocontribute to the improvement inactivity and in order books.

First indications for the 3rd quartersignal a continuation of rather healthybusiness conditions. The Germanmechanical engineering associationVDMA reported a 14% y-o-y rise inorders in August, with domestic ordersgrowing 22% and export orders 9% y-o-y. The German industry nearingcapacity limits has boosted activity inother countries such as Austria, theNetherlands, Sweden and mostCentral European countries.

Business prospects for the remainderof 2011 and 2012 have remained quitepositive despite high uncertainty levelsimpacting on industrial sentiment.Order books have continued toincrease in recent months; the existingbacklog will guarantee activity stayingat overall satisfactory levels in thecoming quarters.EU investment in machinery and

equipment is projected to increase bymore than 3% in 2012, coming from4% in 2011.The competitive position of Eurozoneproducers on the key markets abroadcould improve if the EU remainsaround its current level of close to1.35US$. This could help to soften themoderation expected for growth inglobal GDP and international trade.On balance, mechanical engineering

output in the EU is seen rising by morethan 9% this year. This implies thataverage growth in the 2nd half of theyear will slow down to around 5% year-on-year.In 2012, output in the EU mechanicalengineering industry is seen keeping arather satisfactory pace. Activity isforecast to rise further by almost 3.5%,with growth in the 1st half probablyoutpacing growth in the remainder of2012, reflecting the industry nearing itscapacity limits again.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 12/18

12

Tubes

Moderation Q2-2011 tube output

growth momentum

Outlook for growth easing off

further in the months ahead

Firm demand from all tube client

sectors in 2012

Output in the steel tube industry in theEU continued to grow strongly in the2nd quarter of this year. Nevertheless,

compared with the extremely robustincrease in production in Q1-2011 ofmore than 22% y-o-y the decelerationto a growth of around 8% y-o-y wasquite significant.This trend could be observed in almostall EU countries.Since the 2nd quarter real consumptionin the steel tube using sectors hasbecome the main driver of demand

growth, whereas in the 1st

quarter alsoinventory replenishment had played asignificant role in the rise in tubedemand. Basically all client sectors ofthe tube industry have registered arobust rise in activity in Q2-2011.First estimations for output in the 3rd quarter show a further moderation inoutput growth to around 2.5%, closelyin line in the growth in activity expected

for the key client sectors.

The outlook for the coming months isfor output growth cooling further to 2%y-o-y in Q4. This looks also set tobecome the average growth rate in thefirst half of next year.Demand for small and medium-sizedsteel tubes should strengthen mildlyfurther over the forecast period, in syncwith the expected trend in activity in

the main tube using sectors such asautomotive, engineering and metalgoods.OCTG demand will be supported byhigher activity in the Middle East and asustained high level of activity in NorthAmerica, assuming that oil pricesremain close to their current levels.Solid pipeline project activity isforeseen to keep global demand for

large welded tubes at a satisfactorylevel in Eastern Europe, the MiddleEast and Asia.On balance, total steel tube productionin the EU is forecast to increase byalmost 9% in 2011. Output growth in2012 is projected to cool down toaround 2.5%.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 13/18

13

Domestic Appliances

Output in H1-2011 slightly lower than in the same period of 2010

Market expected to see some improvement in 2012

The latest figures for production ofelectric domestic appliances in the 1st half of 2011 signal that contrary toearlier estimates activity in this sector

has registered a slight decline in thefirst half of this year.Demand for electric domesticappliances has remained underpressure so far in 2011. Waningconsumer confidence and stilldepressed residential property marketsacross the EU have been acting as adrag on sales of white goods. Themodest improvement in new residentialhousing activity in some EU countries

has not been sufficient to unlock thedemand side potential in the EU.EU manufacturers of electric domesticappliances have been facing difficultmarket conditions since 2008. Incontrast to other manufacturingsectors, the gap with pre-crisisproduction levels has remained quitesignificant. Fierce competition andheavy pressure on profit margins haveresulted in manufacturers relocatingproduction to low-wage countries.Since 2005 Central Europe has seen a

marked increase in its domesticappliances‟ manufacturing capacity. Atthe country level, divergences in theevolution of sector activity persisted inQ1-2011. More recently, newcapacities have been built in EasternEurope (Slovenia, Russia) and Turkey.Meanwhile, competition with suppliers

from China and Korea has alsointensified.Near term prospects for this sector arenot particularly bright. Weak privateconsumption growth and the hesitantrecovery of the residential propertymarkets will keep demand in the EUrather subdued for the time being.First estimates and projections for the2nd half of this year signal outputmoving sideways, which will result in

production in the whole of 2011 fallingslightly compared with 2010.The outlook for 2012 is better as theresidential construction market isexpected to see a further, morewidespread rebound across the EU.The market will continue to becharacterised by fierce competition,however. Production of domesticappliances is forecast to increase byaround 3% in 2012, basically driven bya rise in output in Central Europe.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 14/18

14

Real Consumption

Forecast for real consumption - % change year-on-year

PeriodYear2010

Q111 Q211 Q311 Q411Year2011

Q112 Q212 Q312 Q412Year2012

4.8 13.8 7.6 2.3 1.7 6.1 0.6 1.9 2.4 3.2 2.0

Real consumption growth in Q2-

2011 rose 8% y-o-y

Slowdown in growth momentum

in H2-2011 and in early 2012 Mild acceleration consumption

growth in H2-2012

Real steel consumption in the EU

increased by more than 8% y-o-y in

Q2-2011, driven by still robust growth

momentum in the manufacturing

sectors. The deceleration from the

double-digit growth pace in the 1st

quarter marked the transition to a more

sustainable growth trend as the effectof temporary factors boosting activity

faded away.

Looking forward, a further cooling

down of real steel consumption growth

is on the cards for the coming quarters.

First estimates for Q3 real

consumption signal a further slowdown

in growth to just below 2.5% y-o-y, in

line with the manufacturing recovery

losing steam.

In Q4-2011 consumption growth may

slip below 2% y-o-y, which will result in

total real steel consumption in 2011

rising by around 6%.Prospects for 2012 have remained

mildly positive despite high levels of

uncertainty surrounding the outlook for

the steel using industries in the EU.

Activity in the manufacturing sectors

and in construction will continue to

grow, albeit in the case of the

manufacturing industry at a

significantly slower pace than in 2010

and 2011.Particularly in the first half of 2012 real

steel consumption is forecast to grow

only modestly.

From mid-2012 onwards improving

end-user fundamentals should result in

a modest acceleration in consumption

growth. On balance, real steel

consumption is projected to increase

by 2% in 2012.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 15/18

15

Apparent Consumption

Forecast for apparent consumption - % change year-on-year

PeriodYear2010

Q111 Q211 Q311 Q411Year2011

Q112 Q212 Q312 Q412Year2012

22.0 16.5 11.4 3.5 -1.6 7.5 -3.1 0.5 4.0 7.7 2.0

Q2-2011 apparent consumption rose 11% y-o-y

Imports take larger share of EU steel market

Distribution stocks rising in Q3 Real and apparent consumption

growth 2012 seen slowing down EU apparent steel consumptioncontinued to grow rather vigorously inQ2-2011. Growth was just over 11%,compared with 16.5% in the 1st quarter.Inventory replenishment continued tohave an effect on demand, but the keydriver for growth was clearly the solidincrease in real consumption.

Customs data confirm the continuationof high imports from third countriesentering the EU steel market in Q2.Imports grew 45% y-o-y and werealmost 20% up on the precedingquarter, rising to the highest quarterlylevel since Q3-2008. The huge rise inimports resulted in EU domesticdeliveries in Q2-2011 falling below theQ1 level and imports accounting for a21% share of the EU steel market.Supply pressures in the EU steelmarket have risen during summer.Particularly stocks in the distribution

chain have increased further as themarket entered the seasonally weakerholiday period while deliveries werestill coming in. At the current level of

distribution chain sales - which isunlikely to improve towards the end ofthe year - stocks account for 3 monthsof shipments. Ample stocks and shortdelivery times in combination withslowing demand growth and highlevels of uncertainty surrounding thebusiness climate in the months aheadimply that bookings will continue on ahand-to-mouth basis. Import licensedata suggest that import pressure

could ease to some extent, whichappears to be confirmed by July andAugust import data. In the whole of2011 apparent consumption is forecastto rise by 7.5%.In 2012, real consumption will driveapparent consumption growth, but acooling down is inevitable. The stockcycle effect is expected to be fairlyneutral. Imports are forecast to comedown from the high levels registered in2012. On balance, apparent steelconsumption is forecast to rise by 2%in 2012.

Annual ApparentConsumptionin Mio Tonnes

2004 179

2005 170

2006 195

2007 204

2008 188

2009 123

2010 150

2011 (f) 161

2012 (f) 164

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 16/18

16

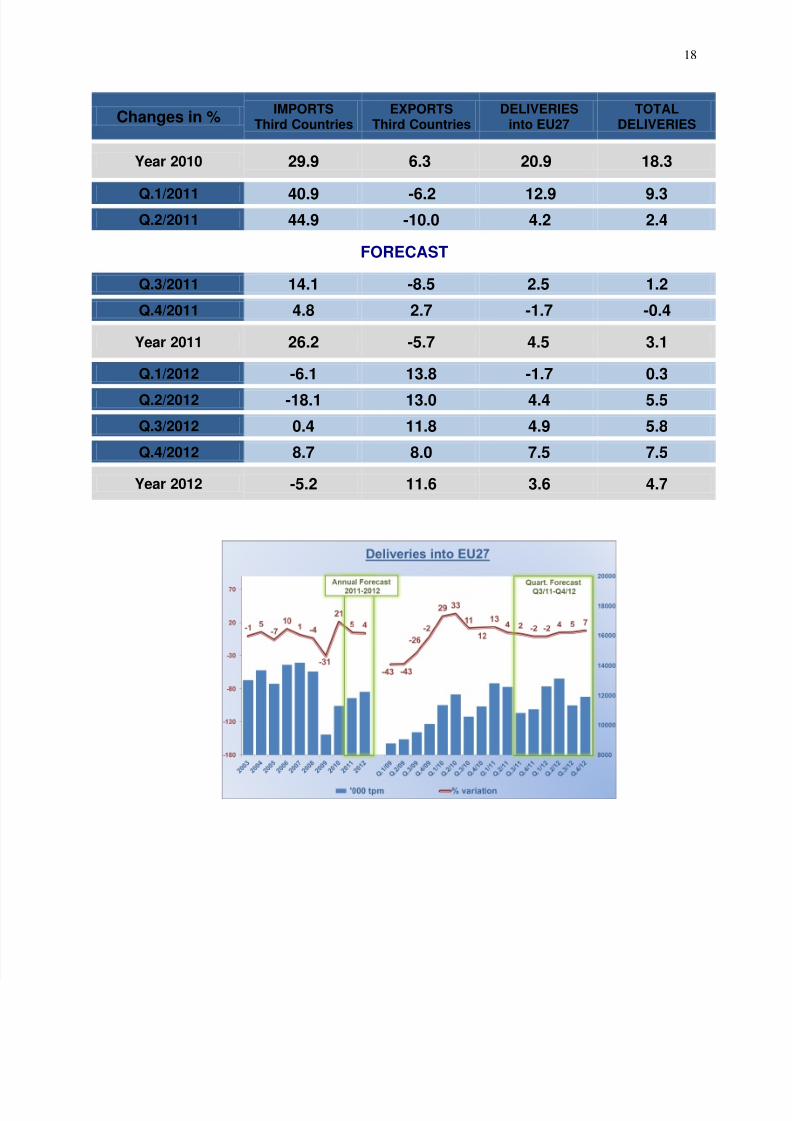

Imports

Rise in imports accelerated in Q2-2011

Particularly flat product imports rose sharply

Imports may slow down in the remainder of 2012

Imports in 2012 seen decreasing moderately

The latest steel trade figures confirmthat import pressure increased furtherin the 2nd quarter of 2011. Total third

country imports rose 45% y-o-y andwere almost 20% higher than in the 1st quarter of this year. At a monthly levelof just under 3.1 million tonnes, thirdcountry imports reached the highestlevel in three years‟ time. The share ofimports in the EU steel market was21% in Q2 compared with on averageof almost 16% in 2010.In line with the trend seen in 2010,particularly imports of flat products

have risen sharply so far this year. Inthe first 8 months of this year, quartoplate imports rose 89% y-o-y, coldrolled imports 68% and hot-rolled coilimports 43%. Total flat imports were51% up on last year compared with21% for long products. Within thisproduct group, differentials at theproduct level are significant with fallingwire rod and rebar imports being

overshadowed by a strong rise inmerchant bars.

With respect to the main countries oforigin, China has remained thedominant third country supplier forseveral products, most notably hot-dipped galvanised sheets and organiccoated sheets;

Meanwhile, nearby steel producerTurkey has stepped up its flat productdeliveries to the EU steel market. Inthe January-July period Turkey wasthe largest supplier of hot-rolled widestrip to the EU. Other countries suchas the Russian Federation and Ukrainehave kept a strong presence in the EUflat product markets as well.The latest import license informationand first estimates for Q3 point towards

a further y-o-y rise in imports but theyare seen moderating compared withthe Q2 level. Imports in the finalquarter are seen moving sideways,which will result in total imports risingby 30% in 2011.The outlook for 2012 is for a decreaseof around 5% in third country imports.The weakening growth trend indemand and the likelihood of the Euroremaining below 1.40US$ for sometime should be supportive to keepingimports at a reduced level.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 17/18

17

Exports

EU exports fell 10% y-o-y in 2011 EU net importer since 2011 Trade surplus in long products

only Exports seen falling by almost

6% in 2011 Exports may rise again in 2012 In the 2nd quarter of 2011, EU steelexports decreased by 10% compared

with the same quarter of 2010, whilerising 4% in comparison with the 1st quarter of the year. Particularly in the2nd quarter the competitive position ofEurozone exporters was negativelyaffected by the relative strength of theEuro.Over the first 8 months of 2011, flatproduct exports declined by 10% y-o-ywhereas long product exportsincreased by 3% y-o-y.

Since 2011, the EU is again a netimporter of steel products, to the tuneof 590,000 tonnes per month over theJanuary-August period. Whereas thereis a trade deficit in semis and flatproducts, long products continued torun a surplus.Net trade in long products amounted to488,000 tonnes per month in thisperiod with exports dominated byrebars and heavy sections.

The largest trade deficit persisted insemis, averaging 502,000 tonnes permonth over the 1st 8 months of thisyear.As far as the main export destinationsfor long products are concerned,

Algeria has remained the largest outlet.Exports in Q3-2011 are estimated tohave decreased to some extent incomparison with the Q2 level. A slightrise in in the quarterly export tonnageis forecast for the final quarter of theyear.This will result in total exports falling byalmost 6% in the whole of 2011.For 2012, EU steel exports areprojected to rise. The weaker Euroshould be supportive to Eurozoneexporters regaining market shareabroad. With unrest in the NorthAfrican markets cooling down, steelmills‟ export opportunities shouldimprove during the year.

8/2/2019 Market Report 2011 October

http://slidepdf.com/reader/full/market-report-2011-october 18/18

18

Changes in %IMPORTS

Third CountriesEXPORTS

Third CountriesDELIVERIES

into EU27TOTAL

DELIVERIES

Year 2010 29.9 6.3 20.9 18.3

Q.1/2011 40.9 -6.2 12.9 9.3Q.2/2011 44.9 -10.0 4.2 2.4

FORECAST

Q.3/2011 14.1 -8.5 2.5 1.2

Q.4/2011 4.8 2.7 -1.7 -0.4

Year 2011 26.2 -5.7 4.5 3.1

Q.1/2012 -6.1 13.8 -1.7 0.3

Q.2/2012 -18.1 13.0 4.4 5.5

Q.3/2012 0.4 11.8 4.9 5.8

Q.4/2012 8.7 8.0 7.5 7.5

Year 2012 -5.2 11.6 3.6 4.7