MARKET OVERVIEW AND OUTLOOK - North Capital

20

1 1 MARKET OVERVIEW AND OUTLOOK OCTOBER 2020

Transcript of MARKET OVERVIEW AND OUTLOOK - North Capital

11

MARKET OVERVIEW AND OUTLOOKOCTOBER 2020

www.northcapital.co.uk

IN THIS ISSUE

October 2020

INTRODUCTION A word from Brian and Angus

HIGHLIGHTS Market highlights from the last 6 months

SPOTLIGHT: Under the Microscope Jennifer examines ESG Investing

MARKET OVERVIEW George and Daniel provide their analysis of the global markets

NOTEWORTHY Pieces of interest

2

4

5

10

16

Welcome to our latest edition of the North Capital Six Monthly. In our last edition we ended with an optimistic hope that the

“wheels will and need to start turning before too long”. Although the wheels did start to turn in late summer, they have slowed once again as, for many, we return to a period of deep uncertainty with cases of Covid-19 rising once more. We have no crystal ball as to where this journey will go next, but we remain optimistic that advances in treatment, testing and vaccines will all help to get us to a place where we can start to return to some sort of normality.

However, we can report that the North Capital team remain in good health we continue to work from home as the “new normal”. We have found that having a positive mindset as well as the right technology has allowed us to increase our productivity and enhance our business activity. Looking back at some of our achievements over the past six months, it is difficult to believe that we have managed to enhance our technology platform, improve our operating model and launch the VT North Capital Active Equity fund, all without physically being together as a group. Zoom and Teams have become our new virtual office and although there are some drawbacks, we think that we have achieved much without having to compromise on our most important objective, providing excellent client service.

We would also like to thank you all as clients for sharing your own concerns as well as your compassion for the health and well-being of our colleagues and families. For those of you that we have been able to meet up with recently, it has been hugely encouraging to get positive feedback on our overall service during this time.

One of the key investment beliefs that we highlighted last time, was the importance of remaining invested through challenging times. We know how difficult this is but, as you will read in our Economic and Market

www.northcapital.co.ukwww.northcapital.co.uk2

Brian O’ConnorChief Executive

Officer

Angus JackChief Investment

Officer

INTRODUCTIONOCTOBER 2020

update, it has proved once again to the case. The chance of picking exactly the right time to liquidate a portfolio and then reinvest at an equally opportune moment can only be done with the benefit of hindsight. Having a well diversified portfolio across asset classes and geographies stands a far greater chance of delivering on your investment objectives.

As you see in the article, there has been a great dispersion of returns across regions and sectors, with the UK market just about managing to break even over this year, whereas the US technology heavy index, the NASDAQ, is up over 40% in the same period - evidencing the importance of diversification. During the next few months there will be further periods of uncertainty and market volatility caused by events over which we have no control. It could be the US election or Brexit or further economic disruption because of Covid-19, we simply cannot predict. However, our investment philosophy of staying invested throughout

these periods is one of our key tenants and this, combined with having a well positioned portfolio, is key to delivering long term investment returns.

Also, in this edition, Jen has written an excellent piece to help explain some of technical aspects to Environmental, Social & Governance (ESG) investing. She has also explored some of the myths around performance and how much of the investment world is managing money on this basis. The last six months have seen a huge increase in the number of investors looking at this approach as a way to express their underlying moral principles. We have considerable resources in this area and are happy to discuss it at any point.

As a final comment, thank you for your continued support and we hope that you and your families remain safe and well at this difficult time. If we have not seen you recently, we hope to meet up with you in person before too long.

3October 2020

www.northcapital.co.uk4

HIGHLIGHTS

Covid-19 continues to undermine global economic activity

North Capital Management launches VT North Capital Active Equity Fund

UK equities fail to keep pace with international markets

Gold and Silver shine as investors look for protection from market volatility

Equity markets struggle to make headway as US election and 2nd wave cause uncertainty

Technology stocks near all-time highs

Governments support business and economies through massive fiscal stimulus

This chart shows performance for various asset classes (colour coded) across multiple time frames. Returns are reported in local currency, sorted in descending order for each column. Unless stated otherwise, each asset class is global in scope - see Disclaimer for full details. EM refers to Emerging Markets and UK Property to commercial property Data as at: 22nd October 2020Source: FE Analytics.

SPOTLIGHT:ESG, UNDER THE MICROSCOPE

www.northcapital.co.uk6

What are the ESG factors?

E The Environmental aspect looks at how a company’s business affects our planet in positive or negative ways. Factors include

climate change risk, waste disposal, pollution, and natural resource conservation.

The Volkswagen emission scandal is a prime example – it cost the company its reputation, its trust (with consumers and regulators) as well as financially in fines, penalties, financial settlements and buyback costs of $33.3bn.

S The Social criteria looks at a company’s stakeholder relationship from employees, to customers, to its impact on the communities

it operates in. However, recently the focus has been on background, race, and gender diversity within a company and its boardroom. Also included in the social criteria are employee welfare, supply chain labour standards, privacy and data security, and health and safety issues.

The online retailer Boohoo recently had a fall from grace when a Sunday Times investigation uncovered a Leicester factory was paying workers just £3.50 per hour and was not adhering to social distancing rules at the height of the pandemic.

In light of the scandal, the share price fell by 50% and led to its largest shareholder, Aberdeen Standard Investments, selling a large portion of its shareholding in the business.

G The Governance factor scrutinises the management of a company, the ethics it holds itself to and its responsibility to its

various stakeholders. This includes reviewing management structure, executive and employee compensation and employee relationships.

Ryanair has faced an onslaught of criticism towards its governance recently due to plans to pay the chief executive a six-figure bonus whilst furloughing staff and reviewing redundancies.

While these factors are simple to understand, there are different techniques that investors use to integrate them into their analysis. For example:

• Positive screening – investing in companies that are considered “best-in-class” on specific ESG metrics. For example, Shell is one of the largest oil and gas companies, however it may pass positive screening compared to its peers due to its commitment to take responsibility for its carbon footprint.

Environmental, Social and Governance (ESG) investing has experienced a meteoric rise. This set of criteria is increasingly popular with modern investors, and fund managers keen to tap into the zeitgeist. The focus on ESG from investment companies and clients alike has increased exponentially, with Industry reports that money in ESG funds has doubled from 2014 to 2019.

Jennifer Wilkes Assistant Investment

Advisor

7October 2020

• Negative screening – excluding companies from the investment universe based on ESG metrics. In contrast to the above, Shell is likely to be screened out due to the size of its current carbon footprint.

• Socially Responsible Investing (SRI) – eliminates or selects investments using a combination of positive and negative screening according to specific ethical guidelines. For example, SRI funds would typically negatively screen out ‘sin’ stocks, such as companies involved in, or associated with, weapons, alcohol, gambling or tobacco.

• Impact Investing – directing investment to companies with the aim of generating measurable beneficial environmental or social effects in addition to seeking a return on investment.

• ESG integration – the inclusion of ESG factors in the investment analysis alongside other factors. This does not mean positive/negative screening, however, investors will include ESG factors in their analysis and decisions.

Though some investors will use ESG from a moral standpoint, it can be a powerful tool for analysing outside the usual metrics. For example, it is highly

likely that regulations will become increasingly stringent on companies that are large emitters of fossil fuel gases. The Renewables Obligation scheme in the UK is one such example of this, which outlines the amount of renewable energy that must be sourced by electricity suppliers in order to reduce the UK’s reliance on fossil fuel gases, or else face a charge. ESG analysts understand that change cannot occur overnight and will instead be looking at the goals set by companies for reducing their carbon footprint, increasing the use of renewable power and how they stack up against their peer group. ESG fund managers often drive change by having a seat at the table. What they are referring to here is the power they possess as shareholders, voting at AGMs and demanding change from the board.

Reducing costs is not the only way in which companies can harness the power of an ESG story. An estimated eight million tons of plastic ends up in our oceans every year. Adidas has used this momentum to upcycle the ocean plastic into training shoes. A survey from Accenture found that half of consumers would pay more for sustainable products; this worked in Adidas’ favour with demand causing them to increase supply from one million pairs of recycled shoes in 2017 to 11 million in 2019. Some 81% of people

www.northcapital.co.uk8

said they expect to buy more environmentally friendly products over five years, and companies are aware of this growing demand. Of the companies surveyed, 44% noted business and growth opportunities as the driving force for their sustainability programs.

Executing ESG effectively can also lead to a reduction in operating expenses, such as raw material costs and human resources. Employee satisfaction can also greatly cost a firm, with estimations that replacing an employee can cost approximately one and half times their salary. As well as reviewing the ESG principles within a company’s four walls, it is also important to review their supply chain to ensure satisfaction and efficiency throughout. This can be problematic due to suppliers often subcontracting portions of large orders to other companies and the ESG implementation becoming diluted down the supply chain. General Mills, an American multinational manufacturer and marketer of branded consumer foods, discovered two-thirds of its total greenhouse gas emissions were occurring in its supply chain. It embarked on a challenge to cut emissions by 28% “from farm to fork to landfill” in 10 years, putting pressure on its suppliers to reduce their emissions or face their business being moved elsewhere.

Does a strong ESG proposition correlate with strong returns?

As shareholders and customers alike begin to hold companies to a higher standard, companies are aware that public perception of their brand can affect the top line. A World Economic Forum report stated that 25% of a company’s market value is attributed to its reputation and, with social media and 24-hour news, it is hard to brush bad press under the carpet.

Does ESG cause a compromise in returns? A recent study showed that companies ranking highest in ESG criteria tended to have lower price volatility and higher average returns compared to their lower ranking counterparts. Harvard Business reviewed the academic literature on sustainability and performance and found that 90% of the 200 studies analysed conclude that good ESG standards lower the cost of capital; 88% show that good ESG practices result in better operational performance; and 80% show that stock price performance is positively correlated with good sustainability practices.

Over a third of US high net worth baby boomer generation expressed the belief that “my investment decisions are a way to express my social, political or environmental values.” This statement alone is enough to give rise to a reason to invest in ESG given that they are a large demographic of investors for fund managers. However, this appeal greatly increases with the younger generations, with two thirds of their high

net worth millennial counterparts agreeing with this statement. Overall millennials are almost twice as likely to seek to invest in companies with a strong ESG proposition compared to non-millennials.

To encourage the integration of ESG into investment management, the UN PRI (Principles for Responsible Investment) created an aspirational set of investment principles:

• Principle 1: We will incorporate ESG issues into investment analysis and decision-making processes.

• Principle 2: We will be active owners and incorporate ESG issues into our ownership policies and practices.

• Principle 3: We will seek appropriate disclosure on ESG issues by the entities in which we invest.

• Principle 4: We will promote acceptance and implementation of the Principles within the investment industry.

• Principle 5: We will work together to enhance our effectiveness in implementing the Principles.

• Principle 6: We will each report on our activities and progress towards implementing the Principles.

In 2015, 139 countries adopted the UN Sustainable Development Goals (SDGs). These goals were designed to assist governments,

companies, and individuals in making an impact in dealing with the biggest challenges that are facing the world today from climate change to inequality to poverty by 2030. Many fund managers were inspired by this initiative and have launched impact funds that utilise the SDGs to measure their impact. This gives investors a useful overarching framework to aim towards and measure progress.

It is unlikely that investors will jump off the bandwagon anytime soon. However, when deciding to invest in ESG, it is important to complete due diligence on the style the fund manager is implementing, whether that be utilising ESG as additional analysis factors, or using a negative screening of ‘sin’ stocks.

Due to the large inflows into this space, it is also valuable to ensure fund managers are not marketing their products to appear more ESG friendly than they are, a process that has been termed greenwashing. ESG investing has moved past the boundaries of ethical investing as it becomes undeniable that effective integration is a powerful tool for mitigating risk by choosing sustainable businesses. Many indexes have created an ESG version which employ a “best-in-class” selection, with many tracking close to, or even outperforming the index in which they track, as seen in fig 1. This reinforces the point that investors do not have to forego returns to incorporate ESG into their portfolio.

9October 2020

Economic and Market InsightIn this new edition we cover some key economic themes. Although they are inevitably interlinked, financial markets (“Wall Street”) and the real economy (“Main Street”) often diverge, especially in the short-term. We have seen this over the past six months, with many businesses continuing to struggle, whilst many headline stock indexes make rapid rebounds.

These indexes, however, are not individual companies (although they are investable) but rather a collective representation of certain stocks. Performance therefore depends on the specific stocks they contain and their respective weights. The overarching theme of the recent stock rally has been large-cap US technology - Apple, for example, now has a higher market capitalisation than the FTSE 100 and makes up around 7% of the S&P 500, so it has substantial impact on that index.

MARKET OVERVIEW

George RenoufChief Operating

Officer

Daniel BrawleyInvestment Analyst

www.northcapital.co.uk10

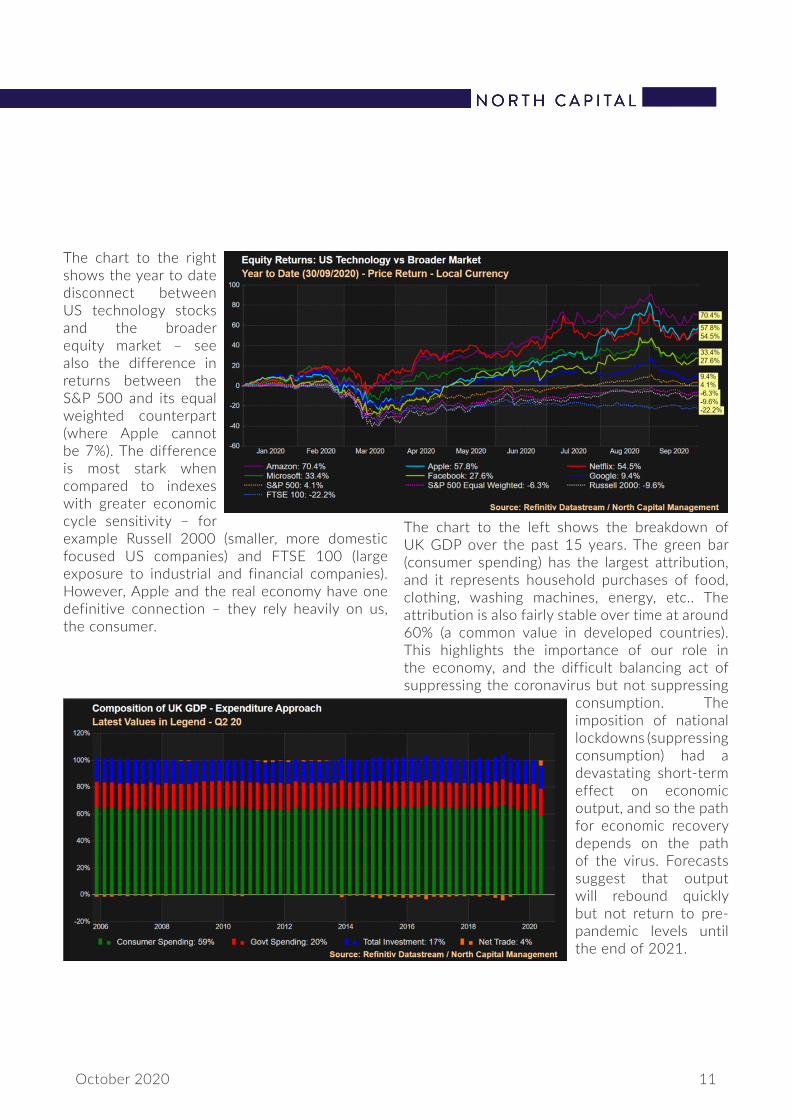

The chart to the right shows the year to date disconnect between US technology stocks and the broader equity market – see also the difference in returns between the S&P 500 and its equal weighted counterpart (where Apple cannot be 7%). The difference is most stark when compared to indexes with greater economic cycle sensitivity – for example Russell 2000 (smaller, more domestic focused US companies) and FTSE 100 (large exposure to industrial and financial companies). However, Apple and the real economy have one definitive connection – they rely heavily on us, the consumer.

The chart to the left shows the breakdown of UK GDP over the past 15 years. The green bar (consumer spending) has the largest attribution, and it represents household purchases of food, clothing, washing machines, energy, etc.. The attribution is also fairly stable over time at around 60% (a common value in developed countries). This highlights the importance of our role in the economy, and the difficult balancing act of suppressing the coronavirus but not suppressing

consumption. The imposition of national lockdowns (suppressing consumption) had a devastating short-term effect on economic output, and so the path for economic recovery depends on the path of the virus. Forecasts suggest that output will rebound quickly but not return to pre-pandemic levels until the end of 2021.

11October 2020

Consumer confidence (red, survey based) has moved in the right direction, but this does not reflect the recent rise in coronavirus cases and localised lockdowns. Consumers tend to be quite flexible, however, and adapt to their environment – for example, ordering takeaways from restaurants when sitting in is prohibited. How we handle coronavirus through the winter will be very important, although we are undeniably more prepared as a nation than we were in March. This re-shift in economic activity will not just be temporary, as there are many structural changes taking hold – such as the shift to flexible home working – which will benefit some companies at the expense of others.

As the UK Government continues to support the labour force (the consumer) and businesses, there will only be one economic certainty – debt, and a lot of it. Headline government debt as a percentage of GDP has already exceeded 100% a level not seen since the early 1960s. The 2020/21 UK budget deficit (how much more the government spends than it earns) is expected to swell to over £300bn – for 2019/20 this was around £60bn. However, the government is

essentially getting “free money” after the Bank of England slashed its base rate to 0.1%, with 10-year UK gilts yielding around 0.2% (it would have cost the Treasury 4.5% 15-years ago). There has been a wholesale reduction in central bank policy rates globally, which has been beneficial for fixed income investors in the short-term (bond prices move inversely with interest rates) but this will

make future returns for the asset class more challenging. Key central banks have also relaxed their inflation targets after opening the floodgates of money supply for asset purchase programmes; as a result, there has also been a recent uptick in long-run expected inflation.

www.northcapital.co.uk12 www.northcapital.co.uk

So, what does this all mean for investors? We have picked out some key considerations for the major asset classes:

Equities• Uncertainty as to how the coronavirus

affects corporate earnings is a major short-term risk

• Cheap debt should encourage companies to borrow and invest in operations

• Focus on companies with strong balance sheets, sustainable earnings, and business models set for the future

• Maintain diversification - large-cap technology has dominated the recent rally, but cyclical companies could benefit from restored global demand

• Increased need for selective stock picking – an opportunity for active managers to show their worth

Fixed Income• Active management is now more important

than ever - low/negative yields demand a strategic approach (not just buy and hold)

• High quality corporate bonds could be attractive as they offer higher yields than government bonds with potential for a reduction in credit spreads

• With policy rates in developed markets at record lows, invest globally with hedged currency risk

• Still an important asset class for many investors, even if primarily for risk management

Alternatives• Increased inflation (an uncertain prospect)

would support alternative assets, such as real estate and infrastructure

• Infrastructure assets may also benefit from increased fiscal spending to promote economic recovery

• Opportunity cost of holding zero-yield assets, such as gold, significantly reduced

• Hedge funds can complement fixed income exposure, targeting relatively low but steady returns

• Attractive entry point for private equity, with potential distressed sellers and lower valuations

All countries across the globe are facing their own particular pandemic related problems. Currently there appears to be a healthy level of global co-operation that will support a global economic recovery. Central banks have been explicit about an acceptance of moderately higher inflation in a post-covid world, and that interest rates will remain at these historic lows for longer – hardly a surprise given the levels of debt governments have had to borrow. This is likely to mean that real returns on cash and government bonds will remain low to negative for the foreseeable future. Investors therefore are faced with the prospect of accepting higher levels of risk in equities and fixed income in order to meet their return expectations.

When we turn our thoughts to visible signs of an economic recovery, then this will depend, as ever, on unlocking the pent-up demand of the consumer, who has been understandably subdued during this time. We should never underestimate the resilience of the consumer and that should offer support and confidence to the long-term investor during these challenging times.

13October 2020

ASSET CLASS ROUNDUP

Equities

• Broad equity market rebound over past six months

• Large-cap US technology has dominated, as highlighted by NASDAQ

• FTSE 100 relatively weak• Growth outperformed value, small-cap

outperformed large-cap• Broad reduction in corporate earnings,

although expectations largely exceeded

Fixed Income

• Benchmark yields generally stayed flat or drifted marginally lower

• Corporate bond spreads meaningfully reduced across all credit ratings

• Small increase in long-term inflation expectations

• Positive returns across most sectors, dominated by riskier high yield and emerging markets

www.northcapital.co.uk14

Oil

• Unprecedented negative pricing for West Texas Intermediate (WTI) in April, with traders paying for above capacity storage

• Production cuts in May and June, coupled with restored global demand, helped prices recover – but still well below pre-pandemic levels

Foreign Exchange

• US dollar under pressure as trade talks with China stall – upcoming election may add to price volatility

• Sterling broadly flat on trade-weighted basis, but appreciated against the dollar

• Brexit continues to drive sterling volatility and may cause further weakness as negotiations progress

Hedge Funds

• Difficult period for hedge funds, with large dispersion in returns across various strategies

• Strategy diversification remains key to achieving consistent return profile

• Aggregate returns have been modestly positive year-to-date, largely from equity rally participation in Q2

Private Equity

• Signs of corporate acquisitions and Initial Public Offerings (IPOs) following subdued period

• Potentially attractive entry point at lower valuation multiples

• Opportunity within distressed credit to provide liquidity on favourable terms

15October 2020

www.northcapital.co.uk16 www.northcapital.co.uk16

NOTEWORTHY

“The Chase” is overA treasure chest of gold coins and jewels, worth $2 million has been found 10 years after it was hidden in Wyoming. Arts and antiques collector Forrest Fenn hid the treasure a decade ago, leaving clues to its location in his self-published memoir “The Thrill of The Chase”. Hundreds of Thousands of people have searched for the treasure, and at least five have died in the attempt. Forrest, 90, sadly passed away shortly after the treasure was found, and has previously stated he wished for his remains to be buried in the same location as his treasure. In his own words, “They never knew that it was the chase they sought and not the quarry.”

A nice problem to haveRecently appointed CEO of Norway’s Wealth Fund, Nicolai Tangen agreed to liquidate his personal fund investments and place the proceeds in bank deposits, to ensure no conflicts of interest arise during his tenure. However, Norwegian banks have struggled to absorb the 8 billion Kroner (£661 million) sum. The Wealth Fund explained that, in Norway, “There is a limited number of banks with a sufficient rating and solvency that are relevant candidates for holding personal bank deposits of the scale involved… it therefore proved to be difficult to spread the deposits sufficiently to avoid substantial exposure to individual banks”. In order to fulfil the terms of his contact, Tangen has instead invested his fortune in Norwegian and foreign government securities.

Washing Old WishesAs North Carolina Aquarium entered its sixth month of mandated closure back in August, staff came up with a creative way to help pay the bills. Employees drained the massive 30-foot waterfall feature at the aquarium, cleaning, and sorting through 14 years’ worth of coins that wishers had thrown in. Spending over 10 hours sending change through a coin counter, the team managed to salvage a grand total of $8,563.71, which they will dedicate to animal care.

Ides of OctoberAn incredibly rare gold coin, commemorating the assassination of Julius Caesar is due to be sold at auction at the end of October. The coin was initially given a conservative estimate of £500,000 however, given it’s “rarity, artistry and fabled place in history” the coin is expected to achieve up closer to £5 million. The mint condition, 2,000-year-old coin was recently discovered in a private European collection and joins only two others in known existence. The first, on display in the British Museum and the other residing in the permanent collection of the Deutsche Bundesbank. Produced in 42 B.C, two years after the assassination, the coin bears a portrait of one of the assassins, two daggers, and the words EID MAR or ‘Ides of March’. The coin also features a pileus, or ‘cap of liberty’, given to Roman slaves when they were freed, symbolising Rome’s liberation from the tyrant Caesar.

April 2019

Disclaimer

All financial products carry a certain degree of risk and the value of investments and the income from them can fall as well as rise and you might not get back the original amount invested. This can result from market movements and also from variations in exchange rates between sterling and the currency in which a particular investment is denominated. More than one risk factor may impact an investment at any given time which means that risks can have quite unpredictable effects on the value of investments. Past performance is not an indicator of future results. Tax and legal information is provided based upon our understanding of current legislation and where appropriate applicable rates. These may change in the future and they may not apply to individual circumstances. North Capital does not give tax or legal advice and you must consult with an independent tax adviser and/or legal adviser for specific advice before entering into, refraining from entering into or exiting any investment or structure or planning. The opinions expressed in this document are our current opinions and should not be seen as investment advice or as an invitation to purchase or sell any investments. The material only represent the views of North Capital Management Limited unless otherwise expressly noted. The material is based on information that we consider reliable, but we do not represent that it is accurate, complete and/or up to date, and it should not be relied on as such.

Data as at 30th September 2020. Source: FE Analytics. Local currency returns.

18

58 North Castle Street, Edinburgh, EH2 3LU+44 (0) 131 285 0860 • [email protected]

www.northcapital.co.uk

Registered in Scotland • Registered Number SC509360 • Authorised and Regulated by the Financial Conduct Authority, Reference Number: 713442