Market Outlook - JB Nagarjbnagarca.org/wp-content/uploads/2012/07/Market-Outlook... · Birla Sun...

29

Copyright Aditya Birla Nuvo Limited 2013 Birla Sun Life Asset Management Company Limited Market Outlook Opportunities & Challenges

Transcript of Market Outlook - JB Nagarjbnagarca.org/wp-content/uploads/2012/07/Market-Outlook... · Birla Sun...

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Market Outlook Opportunities & Challenges

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

2

• Indian Markets

• 2013: Where we got lost

• 2014-15 : Winds of change- The way ahead

• India Inc.: On the path to recovery

• Budget view

• Valuations and Expectations

• Market Outlook

Agenda

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

-10%

-5%

0%

5%

10%

15%

20%

Mar-07

Mar-08

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

YoY%

YoY% 3MMA

3

Source: Morgan Stanley Research

Industrial Production – flat for the last ~2.5 years now

8%

9%

10%

11%

12%

13%

14%

15%

16%

Ja

n-1

3

Feb

-13

Ma

r-1

3

Apr-

13

Ma

y-1

3

Ju

n-1

3

Ju

l-1

3

Au

g-1

3

Se

p-1

3

Oct-

13

No

v-1

3

De

c-1

3

Ja

n-1

4

Feb

-14

Ma

r-1

4

Ap

r-1

4

CPI Food Inflation

CPI

%yoy

9.7%

8.6%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

Ap

r-0

2O

ct-

02

Ap

r-0

3O

ct-

03

Ap

r-0

4O

ct-

04

Ap

r-0

5O

ct-

05

Ap

r-0

6O

ct-

06

Ap

r-0

7O

ct-

07

Ap

r-0

8O

ct-

08

Ap

r-0

9O

ct-

09

Ap

r-1

0O

ct-

10

Ap

r-1

1O

ct-

11

Ap

r-1

2O

ct-

12

Apr-

13

Oct-

13

Ap

r-1

4

Reverse Repo Rate Repo Rate

91-Day T-Bill Yield

Policy inertia impacted investments & growth

3

4

5

6

7

8

9

10

11

12

Ma

r-07

Jun

-07

Se

p-0

7D

ec-0

7M

ar-

08

Jun

-08

Se

p-0

8D

ec-0

8M

ar-

09

Jun

-09

Se

p-0

9D

ec-0

9M

ar-

10

Jun

-10

Se

p-1

0D

ec-1

0M

ar-

11

Jun

-11

Se

p-1

1D

ec-1

1M

ar-

12

Jun

-12

Se

p-1

2D

ec-1

2M

ar-

13

Jun

-13

Se

p-1

3D

ec-1

3M

ar-

14

India Quarterly GDP Growth, %yoy

GDP Growth slowed down amid external and internal factors Persistent high inflation resulted in high rates, input costs

Increasing interest rates have hit margins, investments

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

4

India 2015 & beyond : The way ahead

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Key drivers:

1. Politics – stable, strong Government, after 30 years

2. Investment cycle: policy push + cyclical upswing

3. Inflation and interest rates to cool down

4. Current Account and Currency have stabilized

5. Budget View

5

Pillar of future growth

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

0%

2%

4%

6%

8%

10%

12%

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 E

GDP Growth : Pvt. + Public Consumption, Net Exports and others

GDP Growth attributed to GFCF change

6

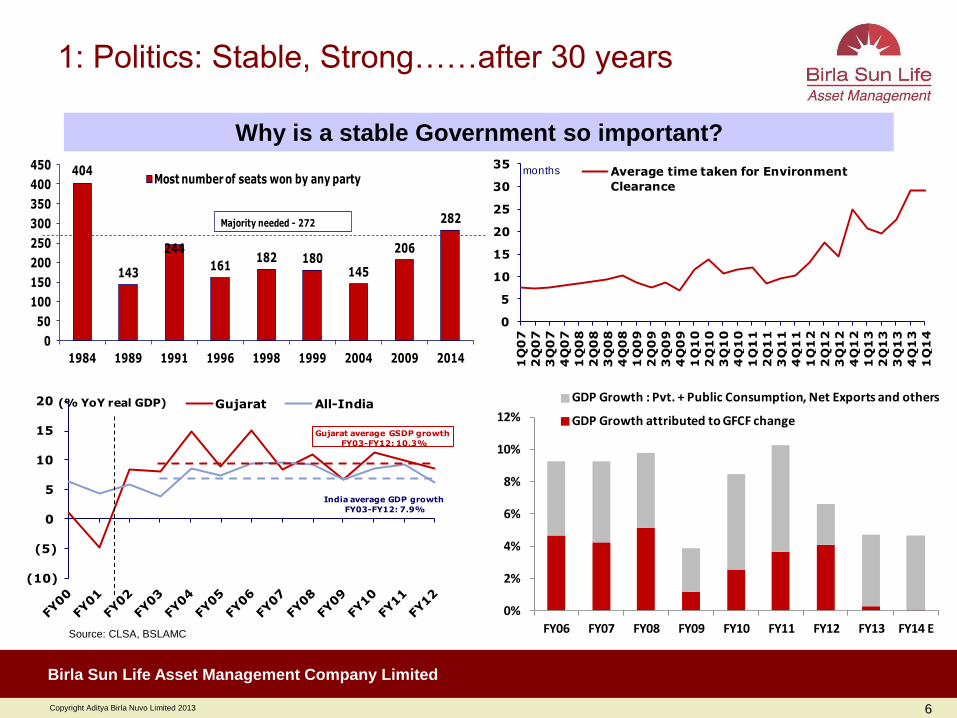

1: Politics: Stable, Strong……after 30 years

Why is a stable Government so important?

404

143

244

161182 180

145

206

282

0

50

100

150

200

250

300

350

400

450

1984 1989 1991 1996 1998 1999 2004 2009 2014

Most number of seats won by any party

Majority needed - 272

0

5

10

15

20

25

30

35

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

Average time taken for Environment

Clearance

months

(10)

(5)

0

5

10

15

20 Gujarat All-India(% YoY real GDP)

Gujarat average GSDP growth

FY03-FY12: 10.3%

India average GDP growth

FY03-FY12: 7.9%

Source: CLSA, BSLAMC

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

7

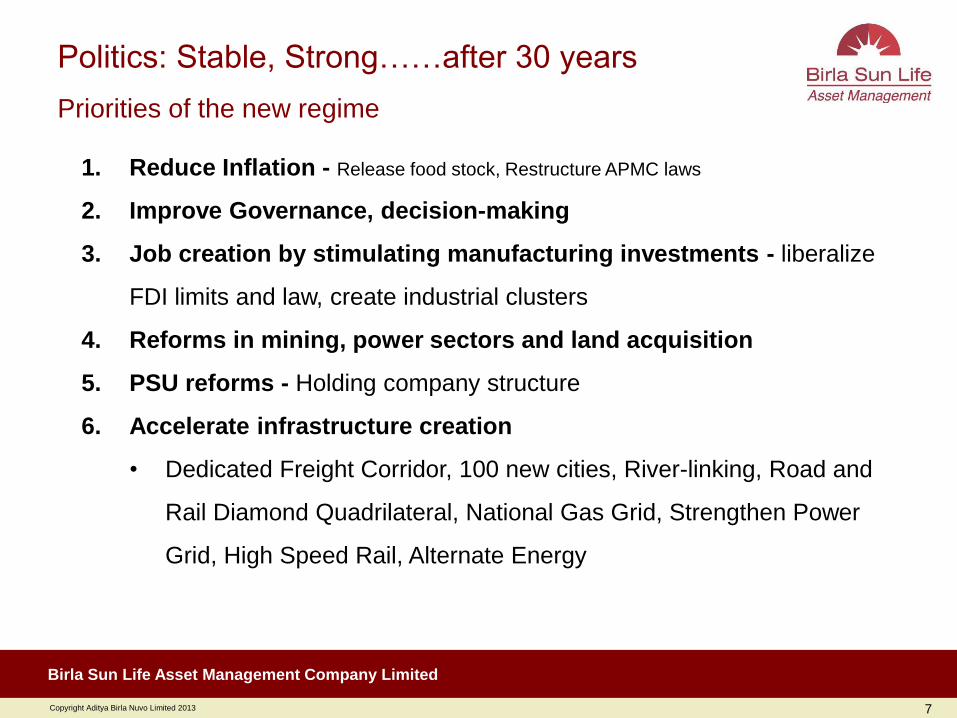

Politics: Stable, Strong……after 30 years

Priorities of the new regime

1. Reduce Inflation - Release food stock, Restructure APMC laws

2. Improve Governance, decision-making

3. Job creation by stimulating manufacturing investments - liberalize

FDI limits and law, create industrial clusters

4. Reforms in mining, power sectors and land acquisition

5. PSU reforms - Holding company structure

6. Accelerate infrastructure creation

• Dedicated Freight Corridor, 100 new cities, River-linking, Road and

Rail Diamond Quadrilateral, National Gas Grid, Strengthen Power

Grid, High Speed Rail, Alternate Energy

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

8

Investment cycle: Policy push + Cyclical upswing As bad as it gets: USD 130 billion projects stalled

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Sep

-96

Mar-

97

Sep

-97

Mar-

98

Sep

-98

Mar-

99

Sep

-99

Mar-

00

Sep

-00

Mar-

01

Sep

-01

Mar-

02

Sep

-02

Mar-

03

Sep

-03

Mar-

04

Sep

-04

Mar-

05

Sep

-05

Mar-

06

Sep

-06

Mar-

07

Sep

-07

Mar-

08

Sep

-08

Mar-

09

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

(Rsbn)

Private Sector Government

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Rs.

Bn

Projects UnderImplementation

Growth YoY %

-50%

0%

50%

100%

150%

200%

-

2,000

4,000

6,000

8,000

10,000

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Rs.

Bn

Projects StalledGrowth YoY %

Quarterly Investments added during the quarter

• Investment cycle suffered a virtual collapse.

Corporate sentiments were impaired due to

lack of clear road map, slowing GDP growth

and elevated cost of capital.

• Projects worth INR 8,000 bn got stalled – due

to Fuel linkages /EC/FC/Regulatory

Clearances, creating a large back log of capital

work in progress.

• Better policy framework and governance to

revive investments.

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Source: Edelweiss

109,600

-

20,000

40,000

60,000

80,000

100,000

120,000 De

lhi

Mumb

ai

Bangal

ore

Chenna

i

Hydera

bad

Gurgo

an

Cochin

Jaipur

TotalRs. Crs

MRTS projects under development 2013-2017

9

661193 244

-133 -5 -54

742

-41

486

140

470 500

3,300

5,500

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2000

-01

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14B

DFC

201

4-19

Railway Track addition in Kms.

Feeder routes

Trunk routes

Source: Barclays

The DFC impact

Source: NHAI

0

2000

4000

6000

8000

10000

12000

14000

16000

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

National Highway Projects Pipeline & Execution

Cummulative Projects Under Execution (km)

2 yr rolling execution (km)

Dedicated Freight Corridor

Mass Rapid Transit System

Investment cycle: The opportunity

• FDI in critical sectors like defense, media

• Policy for labor-intensive sectors like textiles

and construction are likely

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

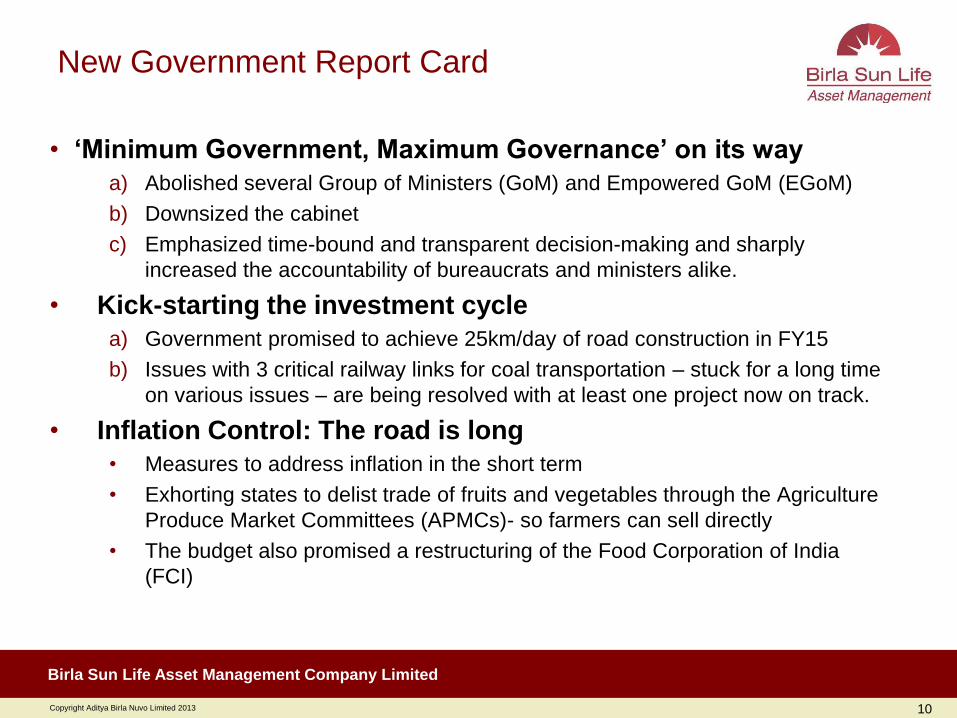

New Government Report Card

• ‘Minimum Government, Maximum Governance’ on its way

a) Abolished several Group of Ministers (GoM) and Empowered GoM (EGoM)

b) Downsized the cabinet

c) Emphasized time-bound and transparent decision-making and sharply

increased the accountability of bureaucrats and ministers alike.

• Kick-starting the investment cycle

a) Government promised to achieve 25km/day of road construction in FY15

b) Issues with 3 critical railway links for coal transportation – stuck for a long time

on various issues – are being resolved with at least one project now on track.

• Inflation Control: The road is long

• Measures to address inflation in the short term

• Exhorting states to delist trade of fruits and vegetables through the Agriculture

Produce Market Committees (APMCs)- so farmers can sell directly

• The budget also promised a restructuring of the Food Corporation of India

(FCI)

10

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

11

• Both the inflation matrix have registered a sharp decline in the month of June. Favorable base effects

will continue to provide lower inflation prints till November.

• More importantly the momentum of Core inflation in case of both wholesale and retail has been

trending down vs. its historical average.

• Going forward we expect inflation to atleast achieve RBI glide path thus creating a headroom for

monetary easing eventually.

Source: Bloomberg, BSLAMC

Inflation and Rates to cool down further

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Ap

r-0

5

Oct

-05

Ap

r-0

6

Oct

-06

Ap

r-0

7

Oct

-07

Ap

r-0

8

Oct

-08

Ap

r-0

9

Oct

-09

Ap

r-1

0

Oct

-10

Ap

r-1

1

Oct

-11

Ap

r-1

2

Oct

-12

Ap

r-1

3

Oct

-13

Ap

r-1

4

WPI Core WPI

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

CPI

Core CPI

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

• Industrial activity has shown green shoots since the beginning if the fiscal. High frequency data

such as automobile sales freight traffic etc. has also registered positive growth rates.

• The PMI for both manufacturing and services is back to expansionary mode. The business

expectation index also hits at revival continuation.

• The nascent sign of recovery in PMI and IIP reflect a cyclical upturn in GDP growth rate.

12

40.0

45.0

50.0

55.0

60.0

65.0

70.0

De

c-0

5

Jul-

06

Feb

-07

Sep

-07

Ap

r-0

8

No

v-0

8

Jun

-09

Jan

-10

Au

g-1

0

Mar

-11

Oct

-11

May

-12

De

c-1

2

Jul-

13

Feb

-14

PMI ManufacturingPMI Services

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Ap

r'0

6

Sep

'06

Feb

'07

Jul'0

7

De

c'0

7

May

'08

Oct

'08

Mar

'09

Au

g'0

9

Jan

'10

Jun

'10

No

v'1

0

Ap

r'1

1

Sep

'11

Feb

'12

Jul'1

2

De

c'1

2

May

'13

Oct

'13

Mar

'14

IIP

IIP and PMI pick up .. Early signs of recovery

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

13

• Dramatic reduction seen in India’s trade deficit

due to falling imports and rising imports

• Gold imports are down 70%. Non Oil, Non Gold

imports also down. Current account deficit for

quarter ended March 14 is the lowest in 4 years

• Indian Rupee is amongst the best performing in

the past 9 months

Source: Bloomberg, BSLAMC

Current Account and Currency have stabilized Policy responses have worked..

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Imports, 3mma

Exports, 3mma

90

95

100

105

110

115

120

125

130

Mar

-13

Apr-1

3

May

-13

Jun-

13

Jul-1

3

Aug-

13

Sep-

13

Oct-1

3

Nov-

13

Dec-

13

Jan-

14

Feb-

14

Mar

-14

Apr-1

4

May

-14

Indian Rupee

Brazilian Real

S. African Rand

Indo Rupiah

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Ma

r-0

1

Ma

r-0

2

Ma

r-0

3

Ma

r-0

4

Ma

r-0

5

Ma

r-0

6

Ma

r-0

7

Ma

r-0

8

Ma

r-0

9

Ma

r-1

0

Ma

r-1

1

Ma

r-1

2

Ma

r-1

3

Ma

r-1

4

Current Account

Capital Account

% of GDP,

quarterly annualised

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

14

Source: Bloomberg, BSLAMC

Budget The guiding post

Budget Overview 2014-15

GDP growth estimated between 5.4 - 5.9% as per the economic survey

Fiscal deficit budgeted at 4.1 % of GDP- and fiscal path 3.6% in FY16 and 3% in FY17.

Current account deficit expected at 2.1% of GDP

Revenue deficit projected at 2.9% of GDP

Net market borrowing to be Rs. 4.6 lakh crores

Road Map expected

Market expected clarity on Road map for GST & reforms for Subsidy rationalization.

Lack of clarity on the application of GAAR created uncertainty for a host of entities.

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

FY14 Deficit The fiscal deficit for FY14 was finally pegged at 4.5% of GDP v/s budget

estimates of 4.8% of GDP

Sharp cut in planned expenditure key reason (10.8% growth vs BE of 29.4%)

Revenues were running below budget estimates due to slowdown in economic activity and shortfall in divestment receipts

FY15 budget math: More realistic The fiscal arithmetic is based on nominal GDP growth of 13.4%, total

revenues rising 15.6% and expenditure rising 12.9%

GDP growth assumption moderately optimistic, expect receipts targets to be met on account of non-tax revenues

Higher expenditure budgeted for an investment starved economy

Upside risks to fiscal deficit unlikely

Budget Math and Our View

15

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

16

Source: Bloomberg, BSLAMC

Budget Key Sector announcements

Sector Impact Announcements

Infrastructure

Positive for all Road

developers/ Asset

Owners

NHAI allocation, Plan to construct 8000Km road,

Increase in planned Expenditure, REIT

Capital Goods Positive for T&D

companies New Feeder separation scheme

Capital Goods Positive for all

Industrial companies

Investment allowance of 15% for investments made

above Rs250mn as compared to Rs1bn earlier for a

period of 3 years.

Power Utilities

Positive for entire

sector

Govt. to oversee that all power companies to get

adequate coal supply

Banking Positive for Infra-

Finance

Banks to be permitted to raise long term funds for

lending to infrastructure sector

Banking and

Insurance

Positive for insurance

companies

Proposed to increase foreign ownership limit in the

insurance sector from 26% to 49% through the FIPB

route

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

17

India Inc: On the path to recovery

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

0%

2%

4%

6%

8%

10%

12%

FY91

FY92

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

Q1

FY14

Q2

FY14

Q3

FY14

Q4

FY15

E

FY16

E

FY17

E

GDP Growth Rate

Avg ('91-'13) = 6.63%

South

East

Asian

Crisis

18

Since ‘91 India’s growth has averaged 6.6%. We believe GDP growth has bottomed out in 2014

BoP

Crisis

Dot.Com

Bust & 9/11

Global

Financial

Crisis

Source: Bloomberg, BSLAMC

We expect cyclical bottom in GDP growth rates

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

19

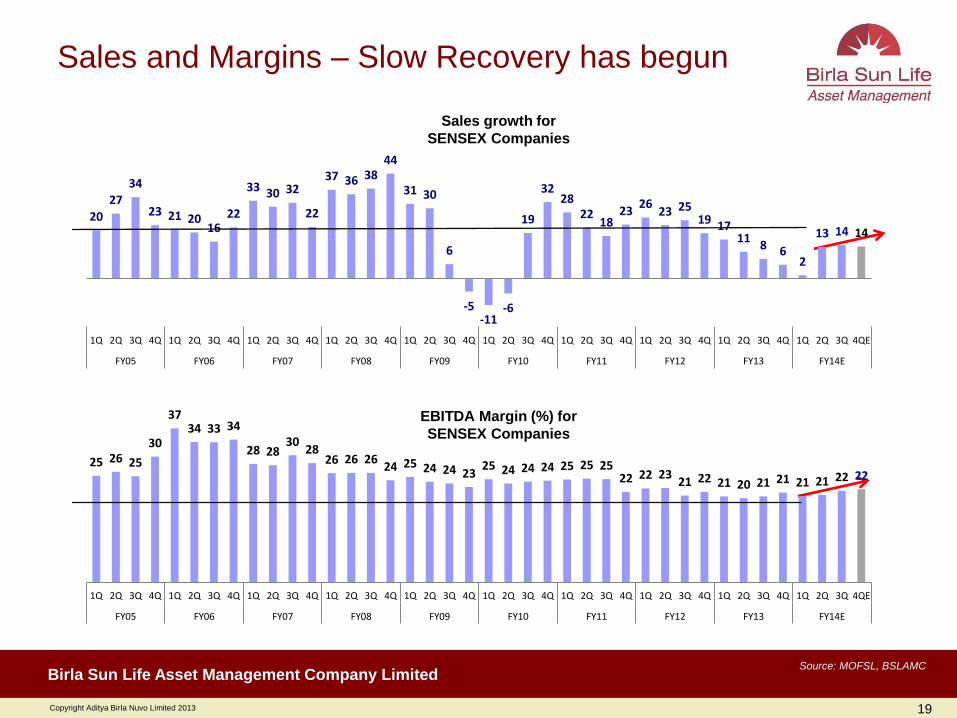

Sales and Margins – Slow Recovery has begun

Source: MOFSL, BSLAMC

Sales growth for

SENSEX Companies

EBITDA Margin (%) for

SENSEX Companies

20

27

34

23 21 20 16

22

33 30 32

22

37 36 38 44

31 30

6

-5 -11

-6

19

32 28

22 18

23 26

23 25 19 17

11 8 6

2

13 14 14

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4QE

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14E

25 26 25

30

37 34 33 34

28 28 30

28 26 26 26

24 25 24 24 23 25 24 24 24 25 25 25

22 22 23 21 22 21 20 21 21 21 21 22 22

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4QE

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14E

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

20

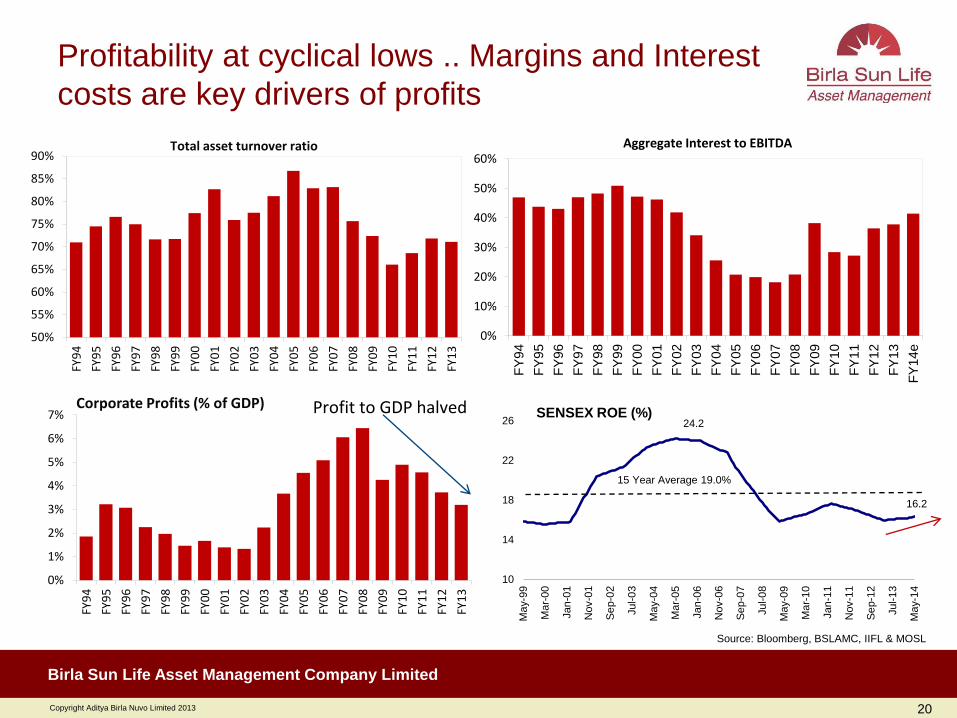

Profitability at cyclical lows .. Margins and Interest

costs are key drivers of profits

24.2

16.2

10

14

18

22

26

Ma

y-9

9

Ma

r-00

Jan

-01

Nov-0

1

Se

p-0

2

Jul-0

3

Ma

y-0

4

Ma

r-05

Jan

-06

Nov-0

6

Se

p-0

7

Jul-0

8

Ma

y-0

9

Ma

r-10

Jan

-11

Nov-1

1

Se

p-1

2

Jul-1

3

Ma

y-1

4

15 Year Average 19.0%

SENSEX ROE (%)

50%

55%

60%

65%

70%

75%

80%

85%

90%

FY9

4

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

Total asset turnover ratio

0%

10%

20%

30%

40%

50%

60%

FY

94

FY

95

FY

96

FY

97

FY

98

FY

99

FY

00

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14e

Aggregate Interest to EBITDA

Source: Bloomberg, BSLAMC, IIFL & MOSL

0%

1%

2%

3%

4%

5%

6%

7%

FY9

4

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

Corporate Profits (% of GDP) Profit to GDP halved

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Consensus expectations are still low

• Over the last four years we have seen an earning decline cycle. In FY12,FY13, FY14 we say

sharp cuts in Sensex earnings estimates.

• From Dec 2013 we saw consensus earning revision towards the positive side.

• Historically, analyst estimates for earning growth tends to lag in accelerating GDP growth

environment,. Over the course of next few years we expect upwards revision in estimates

21

Source: Morgan Stanley Research

1277

1129

1483

1287

1497

1352

1684

1576

1806

1834

1000

1150

1300

1450

1600

1750

1900

Apr2010 Oct2010 Apr2011 Oct2011 Apr2012 Oct2012 Apr2013 Oct2013 Apr2014

FY12

FY13

FY14

FY15E

FY16E

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

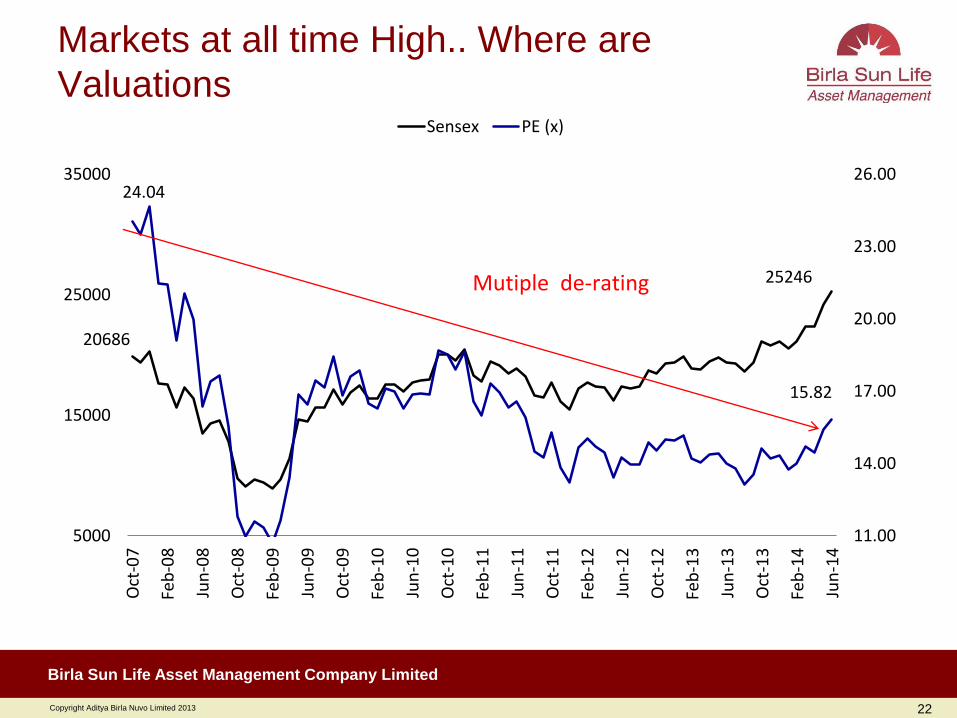

Markets at all time High.. Where are

Valuations

22

20686

25246

24.04

15.82

11.00

14.00

17.00

20.00

23.00

26.00

5000

15000

25000

35000

Oct

-07

Feb

-08

Jun

-08

Oct

-08

Feb

-09

Jun

-09

Oct

-09

Feb

-10

Jun

-10

Oct

-10

Feb

-11

Jun

-11

Oct

-11

Feb

-12

Jun

-12

Oct

-12

Feb

-13

Jun

-13

Oct

-13

Feb

-14

Jun

-14

Sensex PE (x)

Mutiple de-rating

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

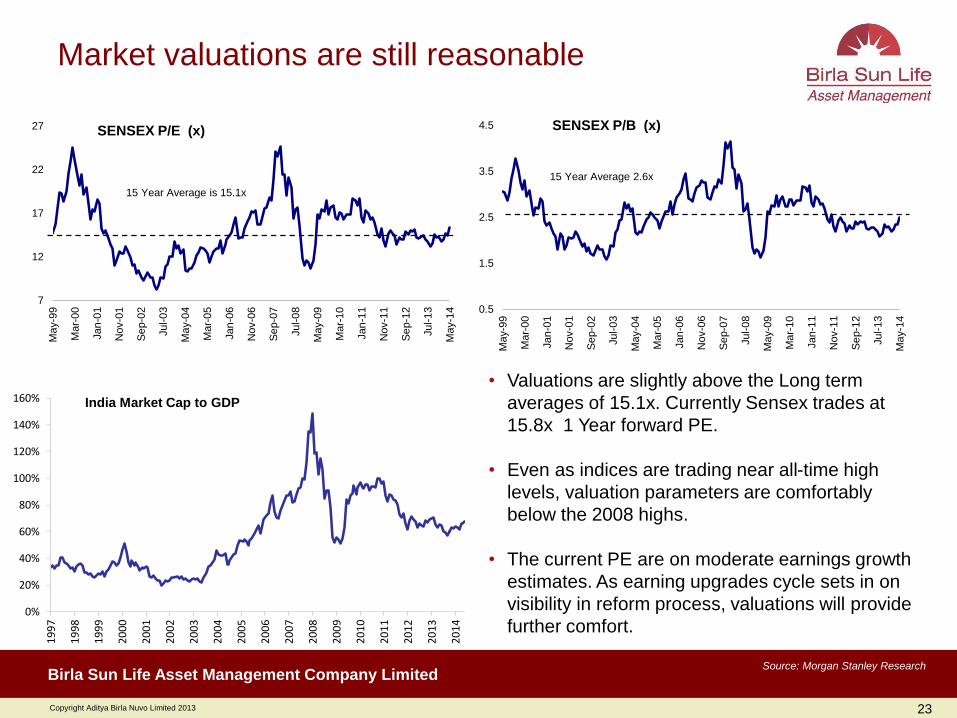

• Valuations are slightly above the Long term

averages of 15.1x. Currently Sensex trades at

15.8x 1 Year forward PE.

• Even as indices are trading near all-time high

levels, valuation parameters are comfortably

below the 2008 highs.

• The current PE are on moderate earnings growth

estimates. As earning upgrades cycle sets in on

visibility in reform process, valuations will provide

further comfort.

23

Source: Morgan Stanley Research

0%

20%

40%

60%

80%

100%

120%

140%

160%

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

India Market Cap to GDP

7

12

17

22

27

Ma

y-9

9

Ma

r-00

Jan

-01

Nov-0

1

Se

p-0

2

Jul-0

3

Ma

y-0

4

Ma

r-05

Jan

-06

Nov-0

6

Se

p-0

7

Jul-0

8

Ma

y-0

9

Ma

r-10

Jan

-11

Nov-1

1

Se

p-1

2

Jul-1

3

Ma

y-1

4

15 Year Average is 15.1x

SENSEX P/E (x)

0.5

1.5

2.5

3.5

4.5

May-9

9

Ma

r-00

Jan

-01

Nov-0

1

Se

p-0

2

Jul-0

3

Ma

y-0

4

Ma

r-05

Jan

-06

Nov-0

6

Se

p-0

7

Jul-0

8

Ma

y-0

9

Ma

r-10

Jan

-11

Nov-1

1

Se

p-1

2

Jul-1

3

Ma

y-1

4

15 Year Average 2.6x

SENSEX P/B (x)

Market valuations are still reasonable

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

24

Opportunities in valuation gaps, cyclical more

headroom..

Source: MOFSL, BSLAMC

Defensives vs Sensex P/B Cyclicals vs Sensex P/B

4.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

May

-04

No

v-0

4

May

-05

No

v-0

5

May

-06

No

v-0

6

May

-07

No

v-0

7

May

-08

No

v-0

8

May

-09

No

v-0

9

May

-10

No

v-1

0

May

-11

No

v-1

1

May

-12

No

v-1

2

May

-13

No

v-1

3

May

-14

FMCG-Sensex P/B +2 SD -2 SD Average

1.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

May

-04

No

v-0

4

May

-05

No

v-0

5

May

-06

No

v-0

6

May

-07

No

v-0

7

May

-08

No

v-0

8

May

-09

No

v-0

9

May

-10

No

v-1

0

May

-11

No

v-1

1

May

-12

No

v-1

2

May

-13

No

v-1

3

May

-14

Pharma-Sensex P/B +2 SD -2 SD Average

1.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

May

-04

No

v-0

4

May

-05

No

v-0

5

May

-06

No

v-0

6

May

-07

No

v-0

7

May

-08

No

v-0

8

May

-09

No

v-0

9

May

-10

No

v-1

0

May

-11

No

v-1

1

May

-12

No

v-1

2

May

-13

No

v-1

3

May

-14

Cap Goods-Sensex P/B +2 SD -2 SD Average

0.5

0.2

0.4

0.6

0.8

1.0

1.2

May

-04

No

v-0

4

May

-05

No

v-0

5

May

-06

No

v-0

6

May

-07

No

v-0

7

May

-08

No

v-0

8

May

-09

No

v-0

9

May

-10

No

v-1

0

May

-11

No

v-1

1

May

-12

No

v-1

2

May

-13

No

v-1

3

May

-14

Metals-Sensex P/B +2 SD -2 SD Average

Cyclical sectors trading below their LT average levels makes a compelling case for

mean reversion as outlook improves.

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

25

Sensex Historical Earnings Growth

Source: MOFSL, BSLAMC

81 129 181 250 266 291 278 280 216 236 272

348 450 523

718 833 820 834

1,024 1,123 1,184

1,338

1,525

1,802

FY9

3

FY9

4

FY9

5

FY9

6

FY9

7

FY9

8

FY9

9

FY0

0

FY0

1

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4E

FY1

5E

FY1

6E

FY93-96: 45% CAGR

FY96-03: 1% CAGR

FY03-08: 25% CAGR

FY08-14: 8% CAGR

FY14-16E: 16% CAGR

FY93-FY14: 14% CAGR

15.8

17.651 19.38

17.65

8

14

20

26Sensex PE (x)

Sensex CAGR -1%

Sensex CAGR 14%

Sensex CAGR 39% Sensex CAGR -1%

Correlation

of Earning

growth

and

PE Re-rating

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Outlook

Equity markets have rallied on decisive election outcome leading to hopes of improving

pace and quality of economic recovery.

• A pro-reform government coupled with decisive leadership will accelerate the reforms

and growth process.

• The depressed corporate profitability will improve over the next 3 to 5 of years as the

economy sees a cyclical uptick, clocking CAGR of 18% - driven by higher revenues,

operating leverage and interest costs savings.

• Even post the sharp run up- Sensex trades at 1year forward PE of 16.8x. Earning

upgrades cycle on visibility in reform process will provide further support to market and

valuations.

• We expect cyclical recovery in economy with average GDP growth of 6% over the next

5years with exit GDP of 7.5 to 8%. - equity returns will be driven both by earning

growth and valuation re-rating providing investor a good investment opportunity.

• In the current scenario, equity investments provide a compelling case over other asset

classes. Indian investors should increase their equity allocations and benefit from

Indian growth story.

26

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

27

Thank You

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Internal views, estimates, opinions of BSLAMC expressed herein may or may not materialize. These views, estimates,

opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy.

The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document(SID) of the

scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking

statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which

could materially impact or differ the actual results or performance from those expressed or implied under those statements.

This document is strictly confidential and meant for private circulation only and should not at any point of time be construed

to be an invitation to the public for subscribing to the units of Birla Sun Life Mutual Fund. Please note that this is not an

advertisement. The document is solely for the information and understanding of intended recipients only. If you are not the

intended recipient, you are hereby notified that any use, distribution, reproduction or any action taken or omitted to be taken

in reliance upon the same is prohibited and may be unlawful. Views expressed herein should not be construed as

investment advice to any party and are not necessarily those of Birla Sun Life Asset Management Company Ltd.(BSLAMC)

or any of their officers, employees, personnel, directors and BSLAMC and its officers, employees, personnel, directors do

not accept responsibility for the editorial content. Wherever possible, all the figures and data given are dated, and the same

may or may not be relevant at a future date. Further the opinions expressed and facts referred to in this document are

subject to change without notice and BSLAMC is under no obligation to update the same. While utmost care has been

exercised, BSLAMC or any of its officers, employees, personnel, directors make no representation or warranty, express or

implied, as to the accuracy, completeness or reliability of the content and hereby disclaim any liability with regard to the

same.

Recipients of this material should exercise due care and read the scheme information document (including if necessary,

obtaining the advice of tax/legal/accounting/financial/other professional(s) prior to taking of any decision, acting or omitting

to act. Further, the recipient shall not copy/circulate contents of this document, in part or in whole, or in any other manner

whatsoever without prior and explicit approval of BSLAMC.

28

Disclaimers

Copyright Aditya Birla Nuvo Limited 2013

Birla Sun Life Asset Management Company Limited

Statutory Details: Constitution: Birla Sun Life Mutual Fund (BSLMF) has been set up as a Trust under the Indian

Trusts Act, 1882. Sponsors: Aditya Birla Financial Services Private Limited and Sun Life (India) AMC Investments Inc.

(liability restricted to seed corpus of 1 Lac). Trustee: Birla Sun Life Trustee Company Pvt. Ltd. Investment Manager:

Birla Sun Life Asset Management Company Ltd.

Risk Factors: Mutual Funds and securities investments are subject to market risks and there can be no

assurance or guarantee that the objectives of the Scheme will be achieved. As with any investment in

securities, the NAV of the Units issued under the Scheme may go up or down depending on the various

factors and forces affecting capital markets and money markets. Past performance of the Sponsor / Investment

Manager / Mutual Fund does not indicate the future performance of the Schemes and may not necessarily provide a

basis of comparison with other investments. The names of the Schemes do not, in any manner, indicate either the

quality of the Schemes or their future prospects or returns. Unitholders in the schemes are not being offered any

guaranteed/assured returns. Investors should read the Statement of Additional Information / Scheme Information

Document/ Key Information Memorandum available at Investor Service Centers and with distributors carefully

before investing.

The Material provided in this communication cannot be reproduced or quoted anywhere without express permission

from Birla Sun Life Asset Management Company Ltd.

Statutory Details & Risk Factors

29

![British Columbia Labour Market Outlook 2010 - 2020 · Labour Market OutlookLabour Market Outlook British Columbia Labour Market Outlook: 2010-2020 [2] B.C. Labour Market Outlook,](https://static.fdocuments.in/doc/165x107/5e167e8e481eae63a43f8127/british-columbia-labour-market-outlook-2010-2020-labour-market-outlooklabour-market.jpg)