Mark Pervan - AME Research

18

1 1 AME Iron Ore Update Q1 2017

-

Upload

informa-australia -

Category

Business

-

view

125 -

download

2

Transcript of Mark Pervan - AME Research

11

AME Iron Ore UpdateQ1 2017

22

Global Commodity Sector Performances

We believe commodity markets bottomed in Q116after a substantial five-year decline

0

100

200

300

400

500

600

700

800

900

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Precious Energy Bulks Ags Industrial

Source: AME

33

Global Commodity Sector Performances

Source: AME

0

100

200

300

400

500

600

700

800

900

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Energy Bulks Industrial

We believe commodity markets bottomed in Q116particularly for the industrial commodities - energy, bulks and base metals

44

China Growth

China has managed a soft landingAfter substantially cooling the economy over the past 5 years

0

2

4

6

8

10

12

14

16

18

20

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Yo

Y %

China IP China GDP

Source: AME

55

0

2

4

6

8

10

12

14

16

18

20

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Yo

Y %

China IP China GDP

0

500

1,000

1,500

2,000

2,500

RM

B B

illio

n

China New Loans (RHS)

China Growth

China can re-ignite growth quicklyNew loans jumped sharply post the GFC and in 2016 to stabilise the economy

Source: AME

66Source: AME

China Property Prices & New Loans

Funds are quickly channelled into growth sectors like propertybut when conditions get overbought, tightening measures are triggered to cool the sectors

0

500

1,000

1,500

2,000

2,500

-8

-4

0

4

8

12

16

07 08 09 10 11 12 13 14 15 16 17

RM

B B

illio

n

Yo

Y %

Real Estate Prices China New Loans (RHS)

77Source: AME

China Property Prices & Steel Price

China property market is steels biggest end-userSteel prices have rallied with strong gains in property, and now look vulnerable to correction

-60

-30

0

30

60

90

-8

-4

0

4

8

12

16

07 08 09 10 11 12 13 14 15 16 17

Yo

Y %

Yo

Y %

Real Estate Prices China Rebar Price (RHS)

88

Iron Ore & Steel Prices

Steel prices have surprisingly outperformed iron oresuggests iron ore prices won’t fall as far

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

0

50

100

150

200

250

07 08 09 10 11 12 13 14 15 16 17

RM

B/t

on

ne

US

D/t

on

ne

Iron Ore Price China Rebar Price (RHS)

Source: AME

99

-10

0

10

20

30

40

11 12 13 14 15 16 17

Yo

Y %

Real Estate Infrastructure Manufacturing

Source: AME

China FAI Breakdown

Fresh funds are being channelled into infrastructurethis should cushion the downside for steel from slowing property demand

1010

-10

0

10

20

30

40

11 12 13 14 15 16 17

Yo

Y %

Real Estate Infrastructure Manufacturing

0

500

1,000

1,500

2,000

2,500

RM

B B

illio

n

China New Loans (RHS)

Source: AME

China FAI Breakdown

Fresh funds are being channelled into infrastructurethis should cushion the downside for steel from slowing property demand

1111Source: AME

Iron Ore Price & China Steel Mill Margins

China steel mill profitability has started to dip againif steel prices fall further, there’s no wriggle room for higher iron ore prices

-600

-400

-200

0

200

400

600

800

1000

1200

0

50

100

150

200

250

07 08 09 10 11 12 13 14 15 16 17

RM

B/t

on

ne

RM

B/t

on

ne

Iron Ore Price Steel Mill Margins (RHS)

1212

2013 & 2016 Global Iron Ore Cost Curve (CFR China)

Source: AME

0

10

20

30

40

50

60

70

80

90

100

0 200 400 600 800 1000 1200 1400

US

D/to

nne

Cumulative Production (Mt)

2013

2016

Iron ore industry costs have fallen substantially in the past 3 yearsin the absence of weaker oil prices and currencies further costs declines will be hard one

1313

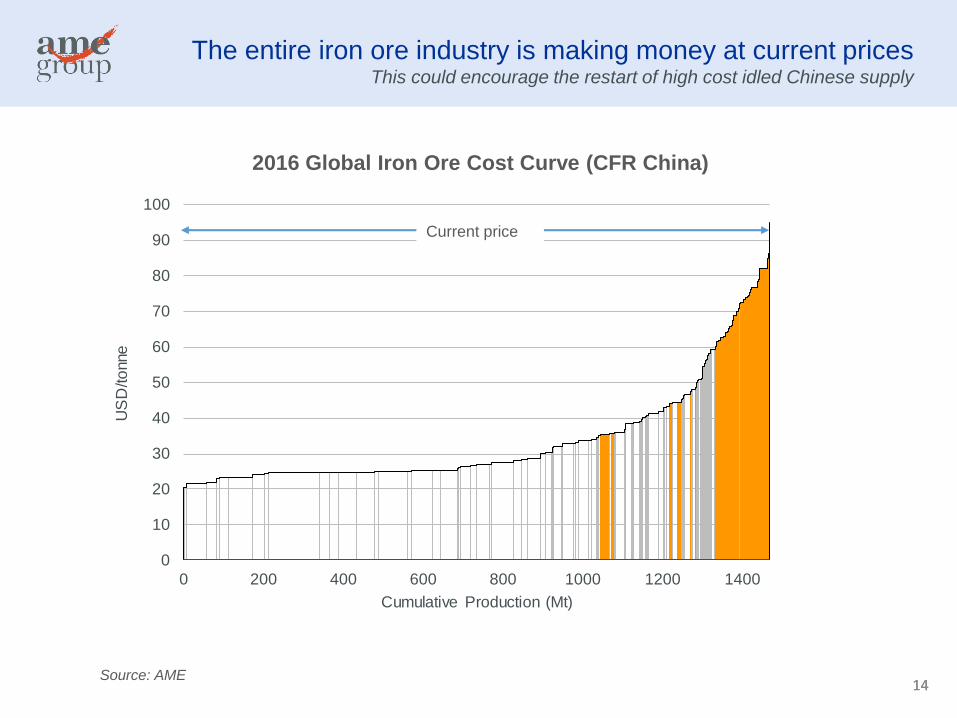

2016 Global Iron Ore Cost Curve (CFR China)

There’s been substantial price volatility in the past 12 monthsAllowing higher cost Chinese supply to remain operating

Source: AME

0

10

20

30

40

50

60

70

80

90

100

0 200 400 600 800 1000 1200 1400

US

D/to

nne

Cumulative Production (Mt)

12 month price range

1414

2016 Global Iron Ore Cost Curve (CFR China)

The entire iron ore industry is making money at current prices This could encourage the restart of high cost idled Chinese supply

Source: AME

0

10

20

30

40

50

60

70

80

90

100

0 200 400 600 800 1000 1200 1400

US

D/to

nne

Cumulative Production (Mt)

Current price

1515

2016 Global Iron Ore Cost Curve (CFR China)

Prices need to revert back to the 90th percentileImplying a price range of US$60-75/tonne over the next 12 months

Source: AME

0

10

20

30

40

50

60

70

80

90

100

0 200 400 600 800 1000 1200 1400

US

D/to

nne

Cumulative Production (Mt)

Current price

AME 12mth price forecast range

1616

Thank you

17

For further details, please visit our website at www.amegroup.com

Hong Kong

t: +852 2846 8220

London

t: +44 20 3752 7277

Sydney

t: +61 2 9262 2264

Toronto

t: +1 646 736 7887

Contact details and important notices

Forward looking information

Certain statements and graphics contained in this presentation may contain forward-looking information within the meaning of various securities

laws. Such forward-looking information are identified by words such as "estimates", "intends", "expects", "believes", "may", "will" and included,

without limitation, statements regarding the company's plan of business operations, production levels and costs, potential contractual arrangements

and the delivery of equipment, receipt of working capital, anticipated revenues, mineral reserve and mineral resource estimates, and projected

expenditures. There can be no assurance that such statements will prove to be accurate; actual results and future events could differ materially

from such statements. Factors that could cause actual results to differ materially include, among others, metal prices, risks inherent in the mining

industry, financing risks, labour risks, uncertainty of mineral reserve and resource estimates, equipment and supply risks, regulatory risks and

environmental concerns. Most of these factors are outside the control of the company. Investors are cautioned not to put undue reliance on

forward-looking information. Except as otherwise required by applicable securities statutes or regulation, the company expressly disclaims any

intent or obligation to update publicly forward-looking information, whether as a result of new information, future events or otherwise.

Copyright @AME Group 2016

Copyright @ AME Group 2015

1818

China’s One Belt, One Road (OBOR)

Belt and Road’ strategy will take natural resources from the westand use excess capacity to sell refined product into the east

Moscow

Rotterdam

Venice

AthensIstanbul

Tehran

Nairobi

Colombo

Kolkata

Jakarta

Fuzhou

Xi’anDushanbe

New

Supply

New

Demand