March 7, 2011 U.S. Lodging Industry Overview11Q4. YOY Employment Change. Source: Colliers PKF...

41

Accelerating success. March 7, 2011 March 7, 2011 U.S. Lodging Industry U.S. Lodging Industry Overview Overview Prepared for the Hunter Investment Hunter Investment Conference Conference R. Mark Woodworth PKF Hospitality Research

Transcript of March 7, 2011 U.S. Lodging Industry Overview11Q4. YOY Employment Change. Source: Colliers PKF...

Accelerating success.

March 7, 2011March 7, 2011U.S. Lodging Industry U.S. Lodging Industry

OverviewOverviewPrepared for the

Hunter Investment Hunter Investment ConferenceConference

R. Mark WoodworthPKF Hospitality Research

3. Profit growth expectations.3. Profit growth expectations.

2

2. Lodging forecast.2. Lodging forecast.

1. The economy.1. The economy.

4. Cap rates.4. Cap rates.

Good and Getting BetterGood and Getting Better

For a copy: [email protected] a copy: [email protected]

44--Quarter Moving Average Quarter Moving Average –– U.S. AllU.S. AllTotal Payroll Employment Change,Total Payroll Employment Change,Average Daily Room Night DemandAverage Daily Room Night Demand

Source: Colliers PKF Hospitality Research, Moody’s Analytics, Smith Travel Research3

U.S. Total Employment LevelsU.S. Total Employment Levels

8.3 Million Jobs Lost8.3 Million Jobs Lost

5+ Years From Peak5+ Years From Peak--toto--PeakPeak

Source: Moody’s Analytics, January 2011

12 Quarters

17 Quarters

22 Quarters

4

WeWe’’re Herere Here

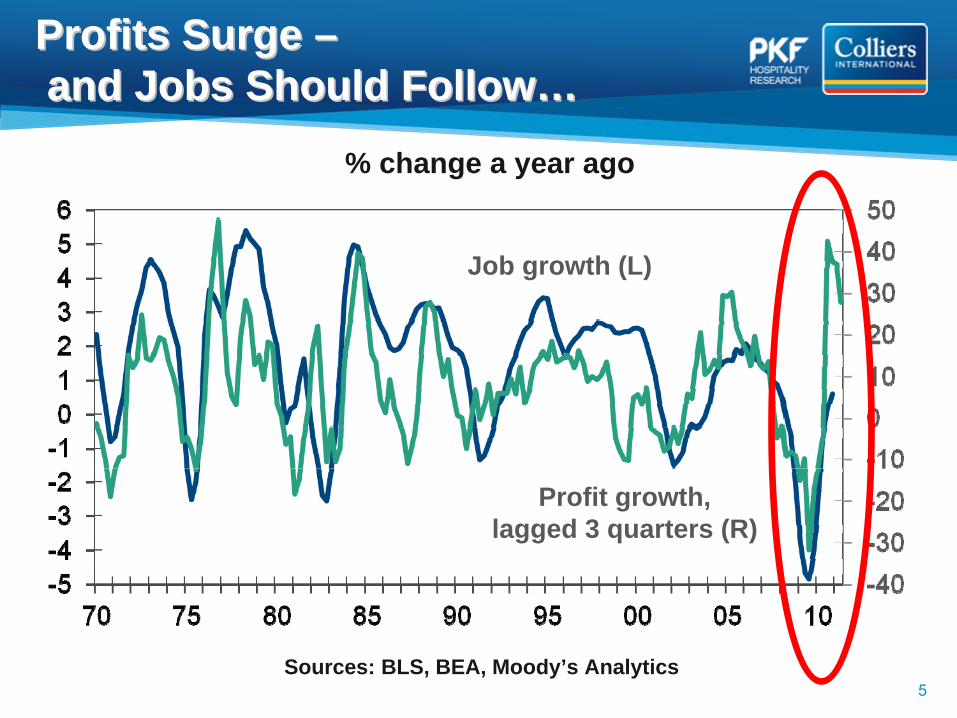

Profits Surge Profits Surge –– and Jobs Should Followand Jobs Should Follow……

Sources: BLS, BEA, Moody’s Analytics

Profit growth,lagged 3 quarters (R)

Job growth (L)

% change a year ago

5

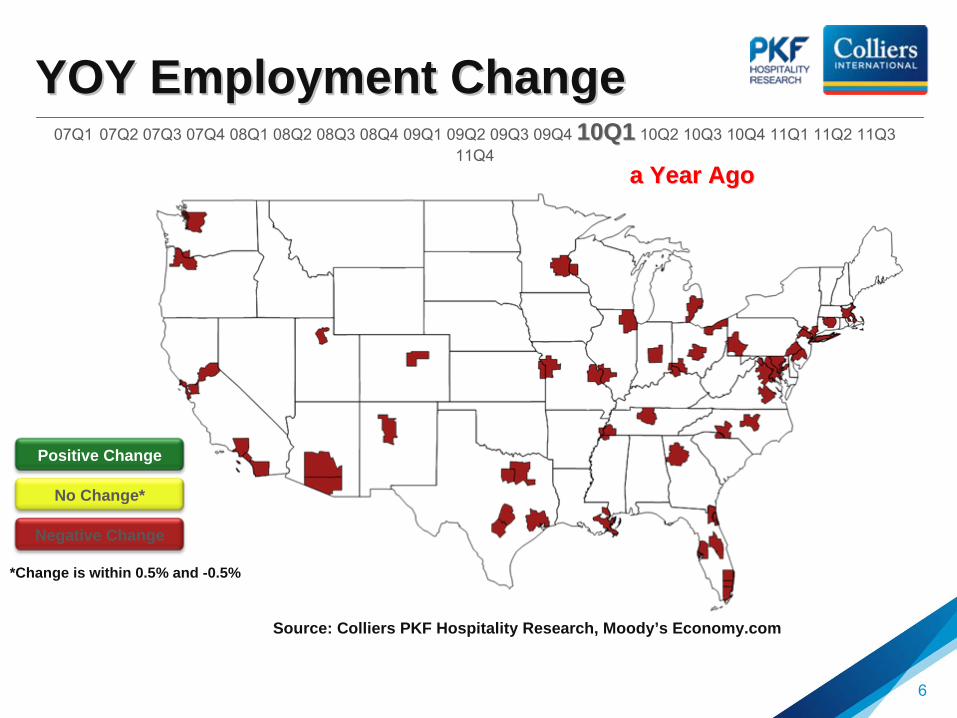

Positive Change

No Change*

Negative Change

07Q1

07Q2

07Q3 07Q4 08Q1 08Q2 08Q3 08Q4 09Q1 09Q2 09Q3 09Q4

10Q110Q1 10Q2 10Q3 10Q4 11Q1 11Q2 11Q3 11Q4

YOY Employment ChangeYOY Employment Change

Source: Colliers PKF Hospitality Research, Moody’s Economy.com

*Change is within 0.5% and -0.5%

6

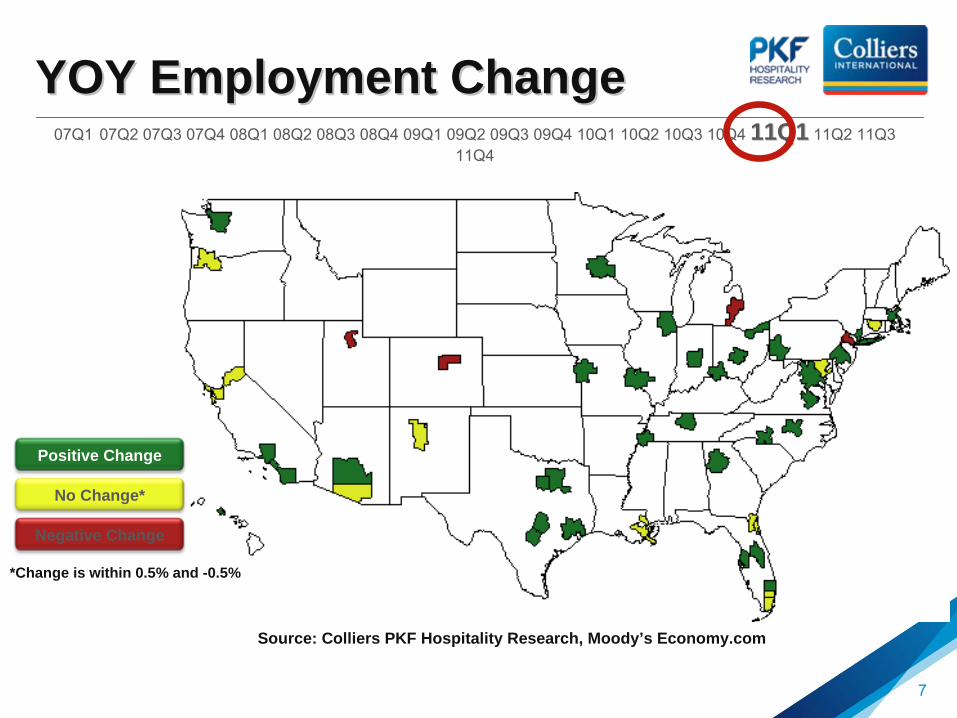

a Year Agoa Year Ago

Positive Change

No Change*

Negative Change

07Q1

07Q2

07Q3 07Q4 08Q1 08Q2 08Q3 08Q4 09Q1 09Q2 09Q3 09Q4 10Q1 10Q2 10Q3

10Q4

11Q111Q1 11Q2 11Q3 11Q4

YOY Employment ChangeYOY Employment Change

Source: Colliers PKF Hospitality Research, Moody’s Economy.com

*Change is within 0.5% and -0.5%

7

Positive Change

No Change*

Negative Change

*Change is within 0.5% and -0.5%

07Q1

07Q2

07Q3 07Q4 08Q1 08Q2 08Q3 08Q4 09Q1 09Q2 09Q3 09Q4 10Q1 10Q2 10Q3

10Q4 11Q1 11Q2 11Q3

11Q411Q4

YOY Employment ChangeYOY Employment Change

Source: Colliers PKF Hospitality Research, Moody’s Economy.com

8

Employment Levels Return to Historical Employment Levels Return to Historical Maximum in YearMaximum in Year……

Source: Colliers PKF Hospitality Research –

March 2011 –

May 2011 Hotel Horizons®

Report, Smith Travel Research 9

The map below displays the year in which Employment levels are forecast to once again achieve their historical maximum: 2 in 2011, 5 markets in 2012, 8 markets in 2013, 21 markets in 2014, and 14 in 2015 or later.

20112012201320142015 & Beyond

Economic Assumptions Driving Economic Assumptions Driving Our Forecasts:Our Forecasts:

PayrollEmployment

Real Personal

IncomeReal GDP CPI (Inflation)

2009 ‐4.3% ‐4.3% ‐1.9% ‐2.0% ‐2.6% ‐2.4% ‐0.3% ‐0.3%

2010 ‐0.5% ‐0.7% 1.3% 0.6% 2.9% 2.3% 1.6% 1.5%

2011 1.7% 0.1% 4.0% 2.4% 3.9% 1.4% 1.5% 0.8%

2012 2.4% 1.9% 3.8% 3.6% 4.0% 3.8% 2.5% 2.8%

2013 2.5% 3.2% 4.6% 3.8% 3.7% 4.5% 3.2% 3.1%

L.R.A. 1.2% 2.7% 2.7% 2.9%

Source: Moody’s Analytics, January 2011 L.R.A. = Long Run Average(July 2010) 10

Exports Rally in South and WestExports Rally in South and West……

Exports of goods and commodities, value: 2008Q2=100

Source: Census

Trade Through Southern PortsTrade Through Southern Ports Is ImprovingIs Improving……

Source: Census, Federal Reserve

Savannah

Value of exports and imports by customs districts, $ billions

Miami

3-mo moving averages

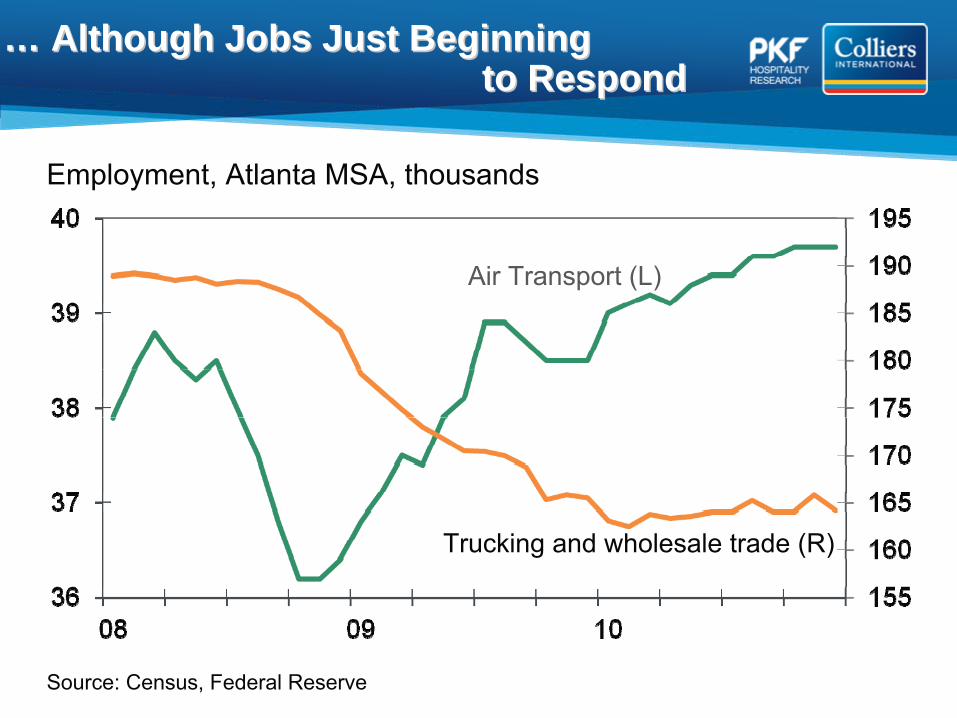

…… Although Jobs Just BeginningAlthough Jobs Just Beginning to Respond to Respond

Source: Census, Federal Reserve

Trucking and wholesale trade (R)

Employment, Atlanta MSA, thousands

Air Transport (L)

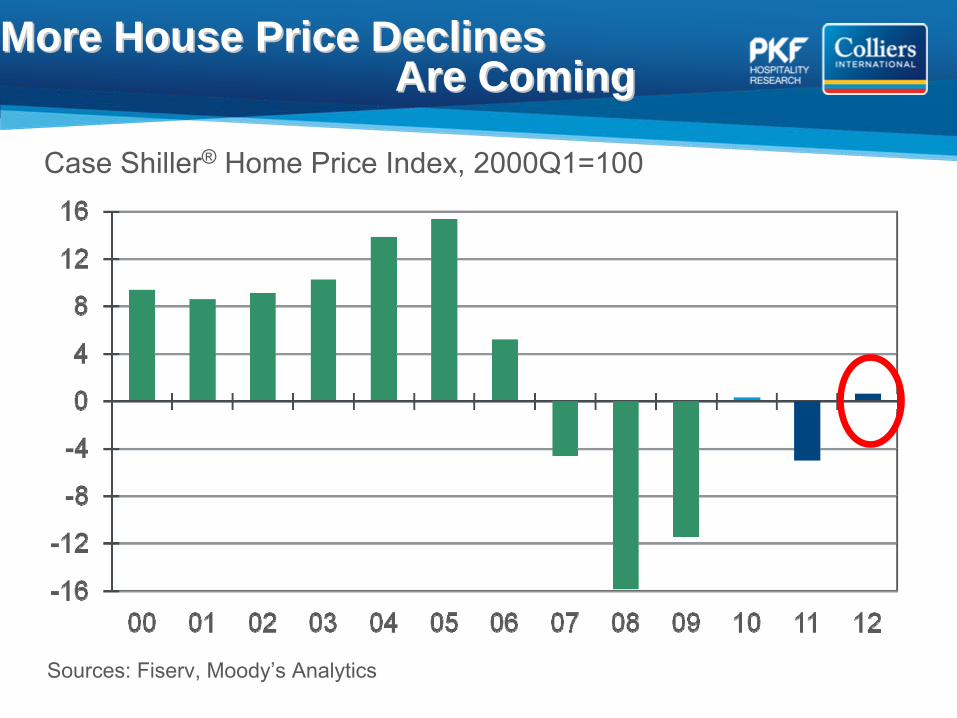

More House Price DeclinesMore House Price Declines Are ComingAre Coming

Sources: Fiserv, Moody’s Analytics

Case Shiller®

Home Price Index, 2000Q1=100

1. The Economy.

2. Lodging forecast.3.

Profit growth expectations.

4. Cap rate outlook.

1. The Economy.

2. Lodging forecast.3.

Profit growth expectations.

4. Cap rate outlook.

15

Good and Getting BetterGood and Getting Better

The Hotel Market CycleThe Hotel Market Cycle

16

Rapid Development

Occupancy Declines, ADR Follows

Development at Minimum

Levels

Lodging Decline, Leads Other Sectors

Occupancy Recovers

ADR and Margins Recover

Development Picks Up

Development Slows

Lodging Recovers, Lags Other Sectors

Long RunOccupancy

Rapid Development

Equilibrium ADR

U.S. is Here2011-2012

2013-2014

A Year Ago

Moving Along the Road to RecoveryMoving Along the Road to Recovery

Room rate discounting induces lodging demand.

True___False ___

Question:Question:

17

A Review of theA Review of the Drivers of Demand ChangeDrivers of Demand Change

Demand = f (Income, Employment ∆, ADR)

Real Personal Income (RPI)-

Sluggish but not the problem or solution

Employment ∆-

Who lost their jobs?

ADR –

Plunged!

18

44--Quarter Moving Average Quarter Moving Average –– U.S. AllU.S. AllTotal Payroll Employment Change,Average Daily Room Night Demand

Source: Colliers PKF Hospitality Research, Moody’s Analytics, Smith Travel Research

ForecastForecast

19

Long Term

Average 2006 2007 2008 2009 2010 2011F 2012F

Supply 2.2% 0.2% 1.3% 2.5% 3.0% 2.0% 0.7% .06%

Demand 1.5% 0.5% 0.7% ‐2.5% ‐6.1% 7.7%7.7% 4.0%4.0% 3.4%3.4%

Occupancy 62.2% 63.1% 62.8% 59.8% 54.5% 57.5% 59.4% 61.0%

ADR 2.9% 7.6% 6.4% 2.9% ‐8.5% ‐0.1% 3.8% 6.0%

RevPAR 2.3% 7.9% 5.9% ‐‐2.1%2.1% ‐‐16.6%16.6% 5.5%5.5% 7.1%7.1% 8.9%8.9%

National HorizonNational Horizon-- Forecasts through 2012Forecasts through 2012

And a Quicker And a Quicker Demand Demand

TurnaroundTurnaroundFor a Record For a Record

DeclineDeclineSource: Colliers PKF Hospitality Research –

March-May 2011Horizons®

Report, Smith Travel Research 20

Severe Rate Severe Rate Discounting Set Discounting Set

the Stagethe Stage

Approaching Long Approaching Long Run AverageRun Average

When Supply Change Reaches U.S. When Supply Change Reaches U.S. Long Run AverageLong Run Average

Source: Colliers PKF Hospitality Research –

March –

May 2011 Hotel Horizons®

Report, Smith Travel Research 21

20112012201320142015Beyond 2015

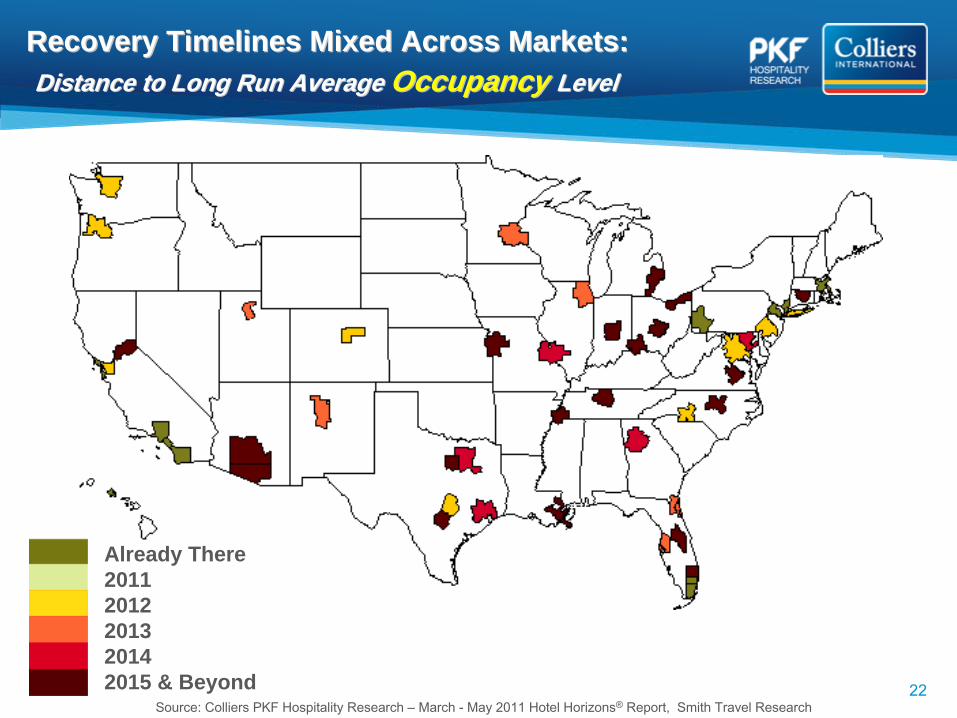

Recovery Timelines Mixed Across Markets: Recovery Timelines Mixed Across Markets: Distance to Long Run Average Distance to Long Run Average Occupancy Occupancy LevelLevel

22Source: Colliers PKF Hospitality Research –

March -

May 2011 Hotel Horizons®

Report, Smith Travel Research

Already There20112012201320142015 & Beyond

Recovery Timelines Mixed Across Markets: Recovery Timelines Mixed Across Markets: Year When Year When ADRADR Levels Return to Previous PeakLevels Return to Previous Peak

23Source: Colliers PKF Hospitality Research –

March –

May 2011 Hotel Horizons®

Report, Smith Travel Research

20112012201320142015 & Beyond

Nominal RevPAR Levels Return to Nominal RevPAR Levels Return to Historical Maximum in YearHistorical Maximum in Year……

Source: Colliers PKF Hospitality Research –

March -

May 2011 Hotel Horizons®

Report, Smith Travel Research 24

The map below displays the year in which nominal RevPAR levels are forecast to once again achieve their historical maximum: 1 market in 2010, 0 in 2011, 10 markets in 2012, 23 markets in 2013, 8 markets in 2014, and 8 markets in 2015 or later.

Already There20112012201320142015 & Beyond

25

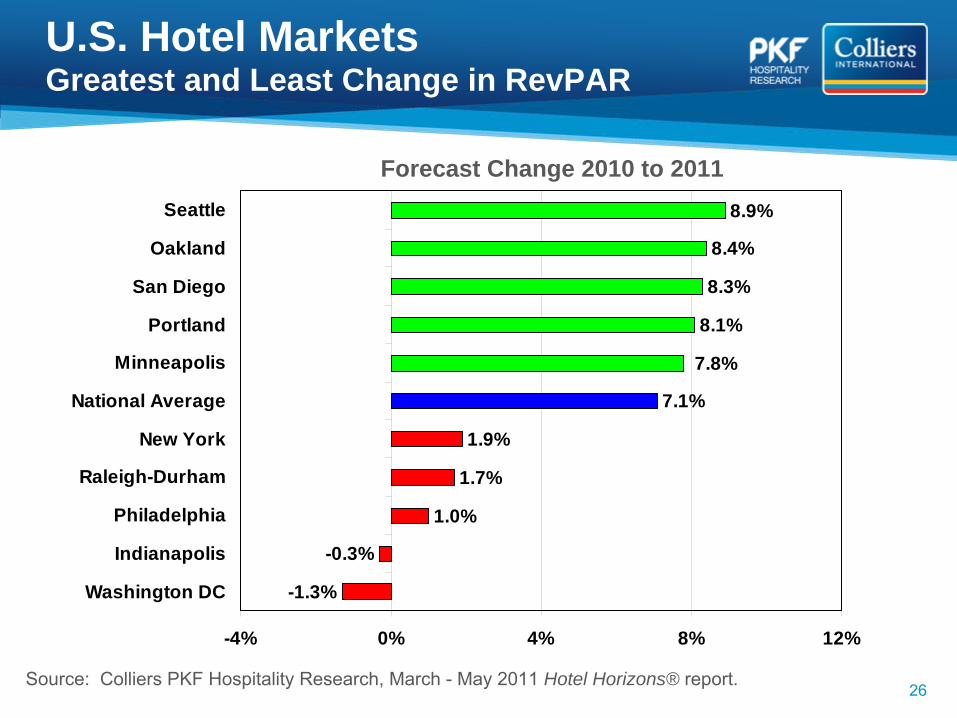

2011 RevPAR Forecast By Chain-Scale

Source: Colliers PKF Hospitality Research, March –

May 2011 Hotel Horizons® report.

6.4%

7.4%

5.3%

6.0%

7.1%

9.6%

0% 4% 8% 12%

Economy

Midscale without F&B

Midscale with F&B

Upscale

Upper-Upscale

Luxury

Forecast Change 2010 to 2011

-1.3%

-0.3%

1.0%

1.7%

1.9%

7.1%

8.1%

8.3%

8.4%

8.9%

7.8%

-4% 0% 4% 8% 12%

Washington DC

Indianapolis

Philadelphia

Raleigh-Durham

New York

National Average

Minneapolis

Portland

San Diego

Oakland

Seattle

Source: Colliers PKF Hospitality Research, March -

May 2011 Hotel Horizons® report.

Forecast Change 2010 to 2011

U.S. Hotel Markets Greatest and Least Change in RevPAR

26

1. The Economy.

2. Lodging forecast.

3. Profit growth expectations.4.

Cap rate outlook.

1. The Economy.

2. Lodging forecast.

3. Profit growth expectations.4.

Cap rate outlook.

27

Good and Getting BetterGood and Getting Better

RevPAR Components and NOI* ChangeRevPAR Components and NOI* Change

NOI Change = -0.02 + 2.07 ADR + 1.38 Occupancy R2= .97

Note: * Before capital reserve, debt service, rent, income taxes, depreciation, amortization.

Source: Colliers PKF Hospitality Research’s Annual Trends Database

28

29

-40%

-20%

0%

20%

40%

60%

80%

1937 1942 1947 1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012F

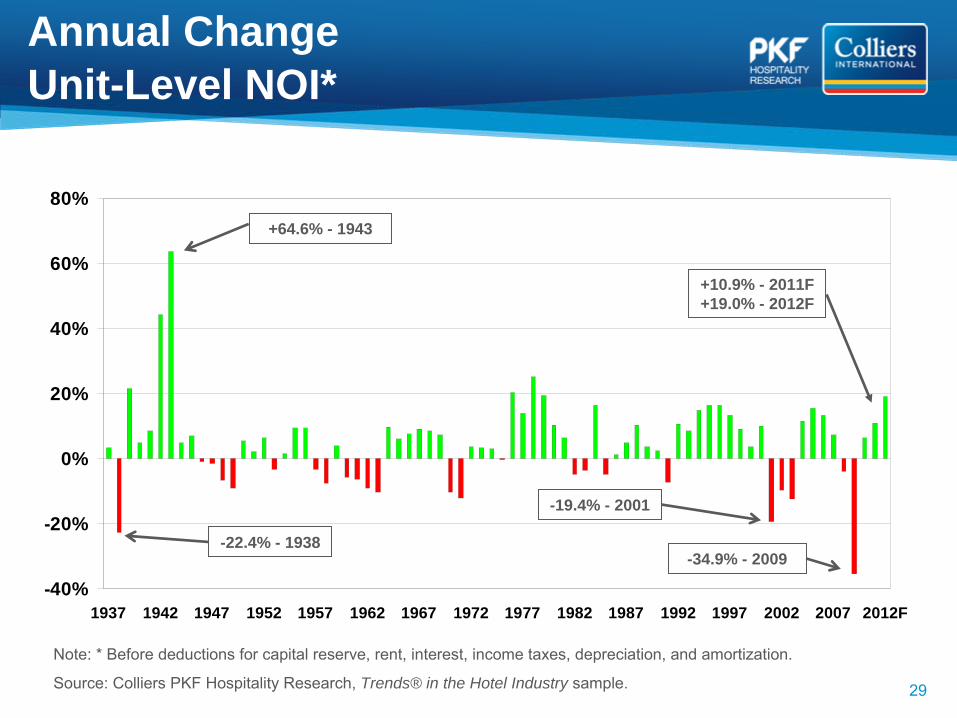

+64.6% - 1943

-22.4% - 1938

-19.4% - 2001

-34.9% - 2009

+10.9% - 2011F+19.0% - 2012F

Note: * Before deductions for capital reserve, rent, interest, income taxes, depreciation, and amortization.

Source: Colliers PKF Hospitality Research, Trends® in the Hotel Industry sample.

Annual Change Unit-Level NOI*

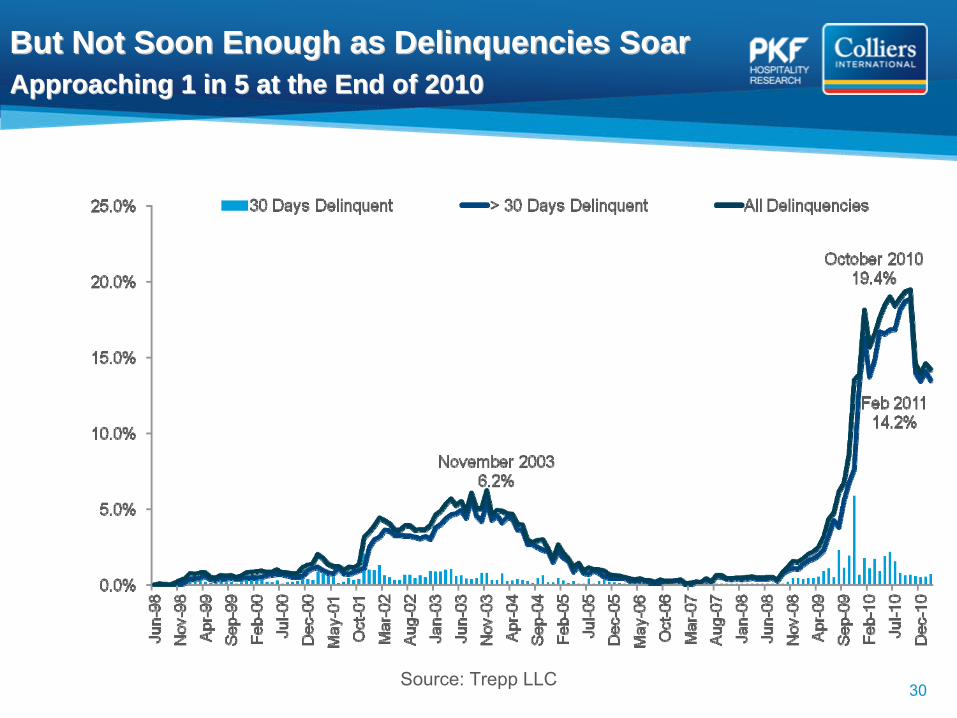

Source: Trepp LLC

But Not Soon Enough as Delinquencies SoarBut Not Soon Enough as Delinquencies Soar Approaching 1 in 5 at the End of 2010Approaching 1 in 5 at the End of 2010

30

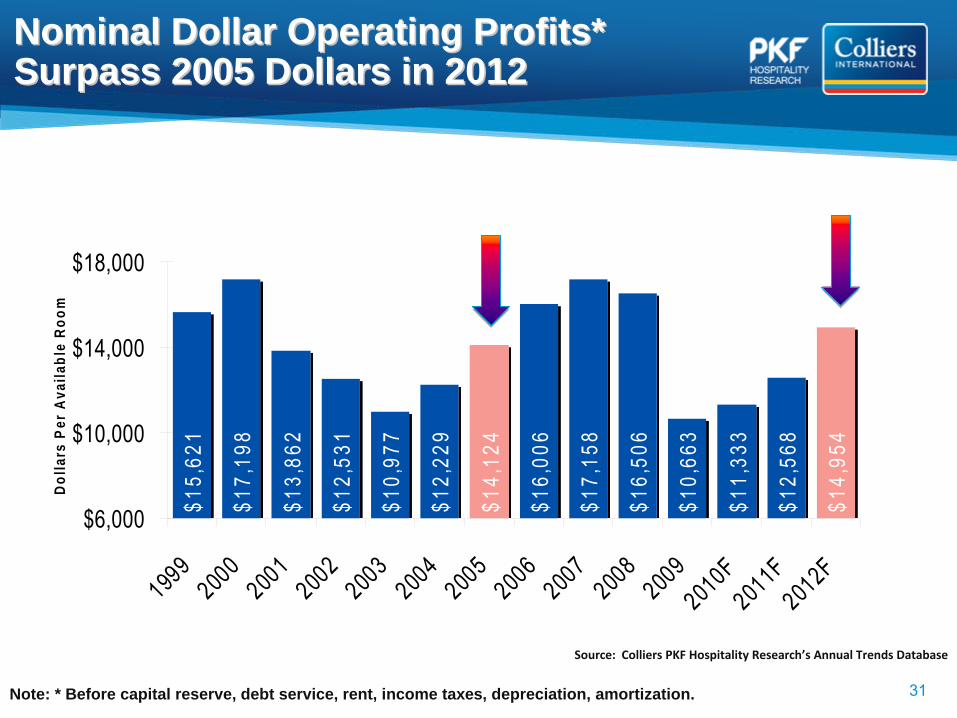

Nominal Dollar Operating Profits* Nominal Dollar Operating Profits* Surpass 2005 Dollars in 2012Surpass 2005 Dollars in 2012

$15,

621

$17,

198

$13,

862

$12,

531

$10,

977

$12,

229

$14,

124

$16,

006

$17,

158

$16,

506

$10,

663

$11,

333

$12,

568

$14,

954

$6,000

$10,000

$14,000

$18,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010F

2011F

2012F

Dolla

rs P

er A

vaila

ble

Room

Note: * Before capital reserve, debt service, rent, income taxes, depreciation, amortization.

Source: Colliers PKF Hospitality Research’s Annual Trends Database

31

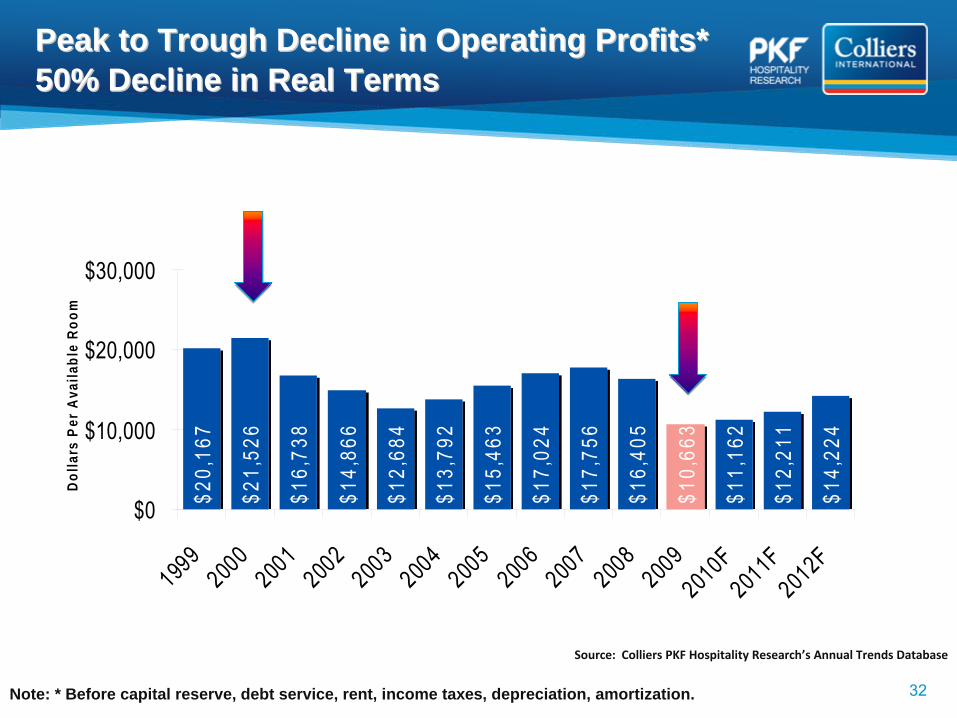

$20,

167

$21,

526

$16,

738

$14,

866

$12,

684

$13,

792

$15,

463

$17,

024

$17,

756

$16,

405

$10,

663

$11,

162

$12,

211

$14,

224

$0

$10,000

$20,000

$30,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010F

2011F

2012F

Dolla

rs P

er A

vaila

ble

Room

Peak to Trough Decline in Operating Profits* Peak to Trough Decline in Operating Profits* 50% Decline in Real Terms50% Decline in Real Terms

Note: * Before capital reserve, debt service, rent, income taxes, depreciation, amortization.

Source: Colliers PKF Hospitality Research’s Annual Trends Database

32

1. The Economy.

2. Lodging forecast.

3. Profit growth expectations.

4. Cap rate outlook.

1. The Economy.

2. Lodging forecast.

3. Profit growth expectations.

4. Cap rate outlook.

33

Good and Getting BetterGood and Getting Better

Hotel Cap Rate Forecasting ModelHotel Cap Rate Forecasting Model

Accounting for Growth and Risk Accounting for Growth and Risk (Gordon Growth Model)(Gordon Growth Model)

34

10-Year Treasuries10-Year Treasuries Moody’s Baa Corp Bond

Moody’s Baa Corp Bond

Changes in Income

Changes in Income

Moody’s AnalyticsMoody’s Analytics

Hotel Cap Rate

Hotel Cap Rate

PKF Hotel Horizons/ STR

PKF Hotel Horizons/ STR

RERC Survey/ RCA

Trans.

RERC Survey/ RCA

Trans.

R HotelR Hotel ΔRevPARΔRevPAR Risk Free AlternativeT10

Risk Free AlternativeT10

Market RiskBaa -

T10

Market RiskBaa -

T10

Data

Variables

The equity riskapplied to

hotels

Change inincome

Risk freealternative to

any investment

Proxy for allother rated

debt

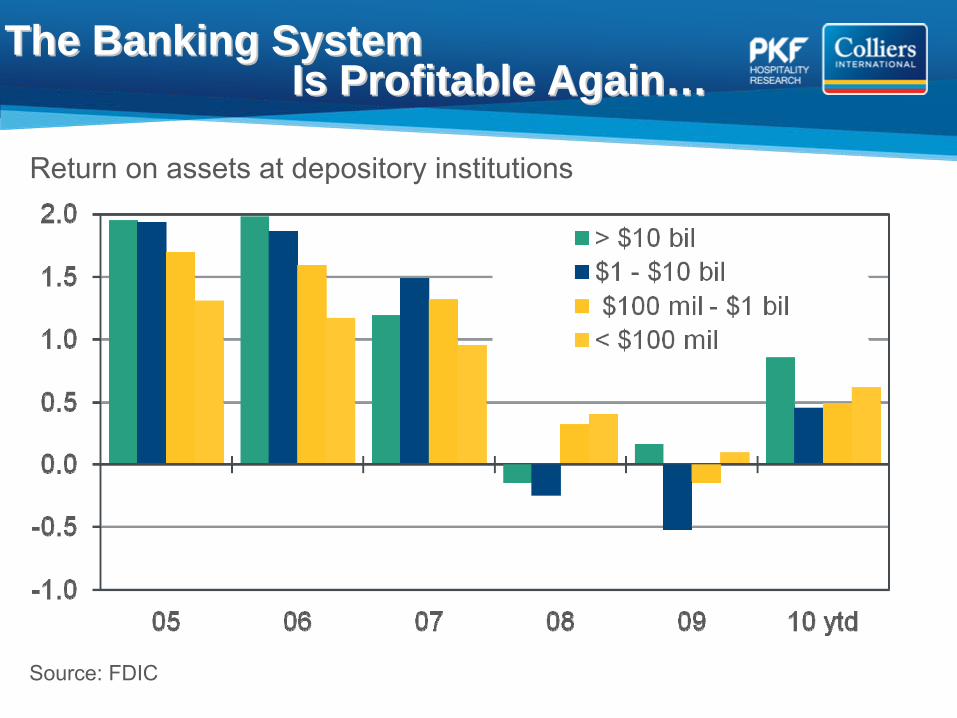

The Banking System The Banking System Is Profitable AgainIs Profitable Again……

Return on assets at depository institutions

Source: FDIC

……And the Credit Spigot Is Opening.And the Credit Spigot Is Opening.

Source: Federal Reserve Senior Loan Officer Survey

Net % of senior loan officers…

Willing to make a consumer loan (L)

Tightening standards for C&I loans to small businesses (R)

10.0

5.7

0

2

4

6

8

10

12

RERC Investor Survey Cap Rates

RCA Observed Transaction Cap Rates

Perceptions and Reality DivergePerceptions and Reality Diverge

37Source: RERC, RCA

Not Many Not Many BuyersBuyers

Forecasts of Return ComponentsForecasts of Return ComponentsLodging Risk Premium Stays Below L.R.A.Lodging Risk Premium Stays Below L.R.A.

10 Year Treasury Market Risk PremiumLodging Risk Premium Hotel Cap Rate

2005 4.3% 1.8% 2.8% 8.9%

2006 4.8% 1.7% 2.0% 8.5%

2007 4.6% 1.9% 1.5% 7.9%

2008 3.7% 3.8% 0.9% 8.4%

2009 3.3% 4.0% 2.0% 9.3%

2010 3.2% 2.8% 2.0% 7.9%

2011F 3.5% 2.4% 2.3% 8.2%

2012F 5.0% 2.0% 1.8% 8.8%

2013F 5.2% 1.7% 1.7% 8.6%

L.R.A. 5.3% 2.3% 2.7% 10.0%

Source: Colliers PKF Hospitality Research, RERC, RCA, Moody’s Analytics

Long Run Average (L.R.A.) = 1992-2010

38

The Cycle of Hotel Real Estate The Cycle of Hotel Real Estate EmotionsEmotions-- Relief and OptimismRelief and Optimism

2007

2004

2009-20102011

2008 – 1st

Half

2008 – 2nd Half

2011-12

39

SummarySummary

40

No Tailwinds Yet:No Tailwinds Yet:

* Persistent high levels of unemployment* Persistent high levels of unemployment

* Continued weakness in housing * Continued weakness in housing

* Higher inflation lifts appeal of hotels* Higher inflation lifts appeal of hotels

* Airline capacity constraints * Airline capacity constraints –– getting bettergetting better

Forecast bias = Forecast bias = veryvery slight positive.slight positive.

![Invariant Shape Features and Relevance Feedback for Weld ... · Sym [0 1] < 0.5 > 0.5 > 0.5 < 0.5 Sig [0 1] < 0.5 < 0.5 → 1 > 0.5 2.2 Generic Fourier descriptor](https://static.fdocuments.in/doc/165x107/5fb60fbe46489e03c70e3474/invariant-shape-features-and-relevance-feedback-for-weld-sym-0-1-05.jpg)