MARCH 2015 MONETARY POLICY STATEMENT FOREIGN …

34

Bank of Papua New Guinea “MARCH 2015 MONETARY POLICY STATEMENT” & “FOREIGN EXCHANGE CONTROL DIRECTIVES” Mr. LOI M. BAKANI GOVERNOR BANK OF PAPUA NEW GUINEA Lae Chamber of Commerce and Industry Thursday 9 th April 2015

Transcript of MARCH 2015 MONETARY POLICY STATEMENT FOREIGN …

Bank of Papua New Guinea

“MARCH 2015 MONETARY POLICY STATEMENT” &

“FOREIGN EXCHANGE CONTROL DIRECTIVES”

Mr. LOI M. BAKANI

GOVERNOR

BANK OF PAPUA NEW GUINEA

Lae Chamber of Commerce and Industry Thursday 9th April 2015

Bank of Papua New Guinea

Presentation OutlinePart I: March 2015 Monetary Policy Statement1. Global Economy2. Monetary Policy Considerations & Issues3. Macroeconomic Indicators: BOP, Fiscal, Public Debt,

Exchange Rate & Inflation 4. Monetary Policy Stance

Part II: Foreign Exchange Control Directives 1. Domestic Foreign Exchange Market 2. Analysis of movements and transactions in Kina Vostro

accounts3. International reserves4. Foreign currency deposits5. Balances in onshore and offshore Foreign Currency Accounts 6. Aim of directives7. Way Forward8. Conclusion

Bank of Papua New Guinea

Part I: March 2015 Monetary policy

Statement

Bank of Papua New Guinea

1. The Global Economy

Source: Bloomberg

• Global growth is expected to pick up slowly in 2015.• Global inflation is also expected to pick-up slightly in 2015.• Most Central Banks policy rates for Advanced Economies are

expected to remain low, while US and UK are expected to increase.

Bank of Papua New Guinea

2. Monetary Policy Considerations & Issues• GDP in 2014 is estimated to have grown by higher than

the 8.4% reported in the 2015 Budget. • In 2015, projected GDP growth reflects full year of LNG

production and full capacity production for nickel & cobalt, as well as activity in the non-mineral sector.

• High economic growth & expansionary fiscal policy contributed to high import demand and depreciation of the Kina.

• Inflation is trending upwards.• Financing of the Budget deficit will be a challenge.• Declining oil and other commodity export prices have

implications for Gov’t Budget and foreign exchange reserves.

Bank of Papua New Guinea

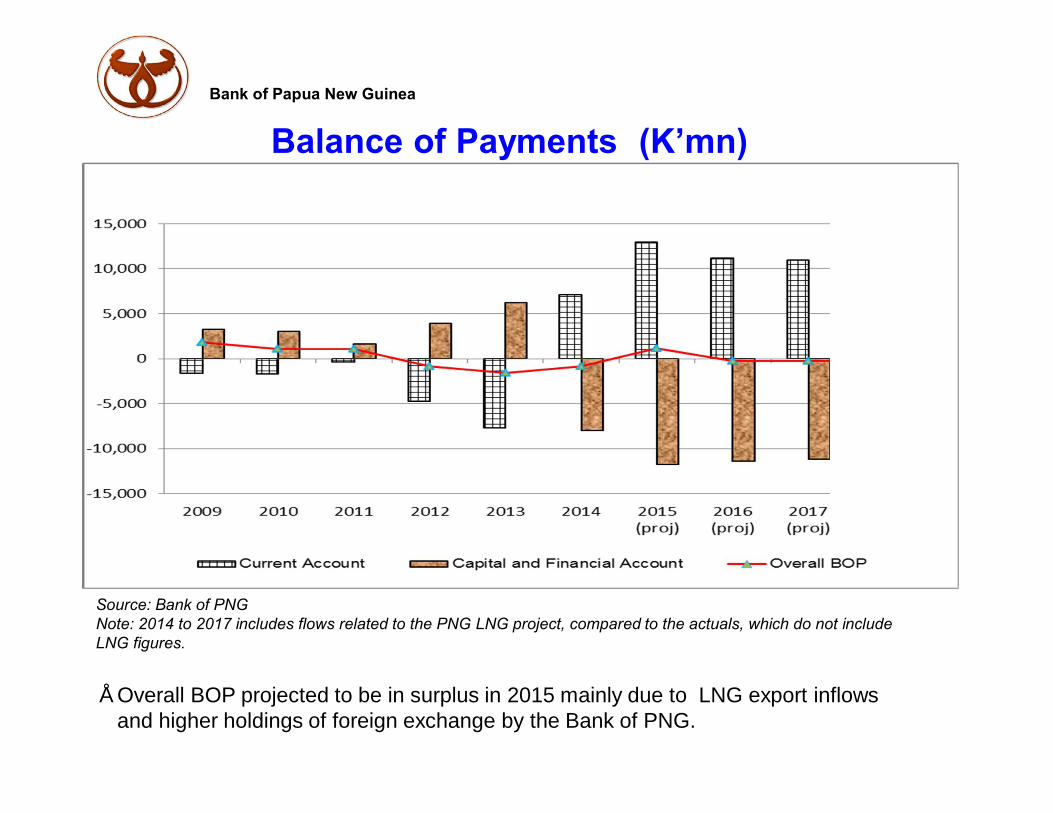

Balance of Payments (K’mn)

Source: Bank of PNGNote: 2014 to 2017 includes flows related to the PNG LNG project, compared to the actuals, which do not include LNG figures.

Source:

• Overall BOP projected to be in surplus in 2015 mainly due to LNG export inflows and higher holdings of foreign exchange by the Bank of PNG.

Bank of Papua New Guinea

Source: 2015 National Budget. 2014 outcome is preliminary.

Source:

-3,200

-2,700

-2,200

-1,700

-1,200

-700

-200

300

800

-1,500

500

2,500

4,500

6,500

8,500

10,500

12,500

14,500

16,500

2006 2007 2008 2009 2010 2011 2012 2013 2014Prel

2015Proj

2016Proj

2017Proj

Deficit / S

urplus R

even

ue &

Exp

endi

ture

Fiscal Operations of the Gov’t (K'm)

Revenue Expenditure Deficit/Surplus

• Third expansionary fiscal budget with a deficit of K2.3 bn in 2015 or 4.4% of nominal GDP• Expenditure to priority areas; transport infrastructure, agriculture, law and order, education and

health services and increased funding to provincial, district and local level Governments (LLGs).

Bank of Papua New Guinea

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000M

ar-0

3Ju

n-03

Sep

-03

Dec

-03

Mar

-04

Jun-

04S

ep-0

4D

ec-0

4M

ar-0

5Ju

n-05

Sep

-05

Dec

-05

Mar

-06

Jun-

06S

ep-0

6D

ec-0

6M

ar-0

7Ju

n-07

Sep

-07

Dec

-07

Mar

-08

Jun-

08S

ep-0

8D

ec-0

8M

ar-0

9Ju

n-09

Sep

-09

Dec

-09

Mar

-10

Jun-

10S

ep-1

0D

ec-1

0M

ar-1

1Ju

n-11

Sep

-11

Dec

-11

Mar

-12

Jun-

12S

ep-1

2D

ec-1

2M

ar-1

3Ju

n-13

Sep

-13

Dec

-13

Mar

-14

Jun-

14S

ep-1

4D

ec-1

4

%

K'm

illio

n

Public Debt to GDP

Public Debt (K'm) GDP nominal (K'm) Debt to GDP ratio (%)

Source: 2015 National Budget & Bank of PNG

• Shortfall in revenue in 2014 resulted in high debt financing.

• Public debt is expected to decrease to 27.8% of GDP in 2015 from 35.5% in 2014.

Bank of Papua New Guinea

Source: Bank of PNG

Source:

• The exchange rate has depreciated by 9.3% since the banding, from US$0.4130 to US$0.3745 as at 27th March 2015.

• The continued depreciation was due to high economic growth that led to increased import demand, while foreign exchange inflows were lower.

Bank of Papua New Guinea

Source: BPNG and NSO.

Source:

• Inflation is expected to be around 6.0% in 2015.• Inflationary pressures are expected mainly due to continued economic growth that

led to high import demand.

0

2

4

6

8

Annual Headline Inflation (percentage change)

Projections

Bank of Papua New Guinea

3. Summary

• Economic growth was boosted during the construction phase of the LNG project but inflation remained low

• Growth continued, supported by the expansionary fiscal policy of the Gov’t with spending in priority areas

• High growth contributed to increased import demand which led to the depreciation of the Kina

• BPNG intervened to support the foreign exchange market

• Despite the growth and depreciation, inflation has been manageable

Bank of Papua New Guinea

Summary (cont’d)• Monetary policy management was aimed at finding

a balance between high liquidity levels, rising interest rates from budget financing, and high import demand resulting in the depreciation of the Kina

• Advised caution in the 2014 September MPS on the high expectation of LNG revenue

• In March 2015, LNG revenue were much lower, further aggravated by low oil and other commodity export prices

Bank of Papua New Guinea

4. Monetary Policy Stance

• Given the projected revenue shortfalls, the Gov’t will have to make adjustments to its 2015 Budget

• Ongoing close coordination between Fiscal and Monetary Policies is important

• Coordination is enhanced by operation of new payments system-Kina Automated Transfers System (KATS)

• Also further progress on establishment of SWF• BPNG will maintain its stance of Monetary

Policy

Bank of Papua New Guinea

Part II: Foreign Exchange Control

Directives

Bank of Papua New Guinea

5. Observations in Forex Market• Over the last 2 years, undesirable activities in

the foreign exchange market were observed, which led to the introduction of the trading band in June 2014

• In 2014, BPNG observed:– Increased volume of activities conducted through

Vostro accounts of foreign banks– Increased transactions in onshore and offshore

Foreign Currency Accounts (FCAs)– Led to reduced foreign currency liquidity in

market– Affected businesses and kina depreciated.

Bank of Papua New Guinea

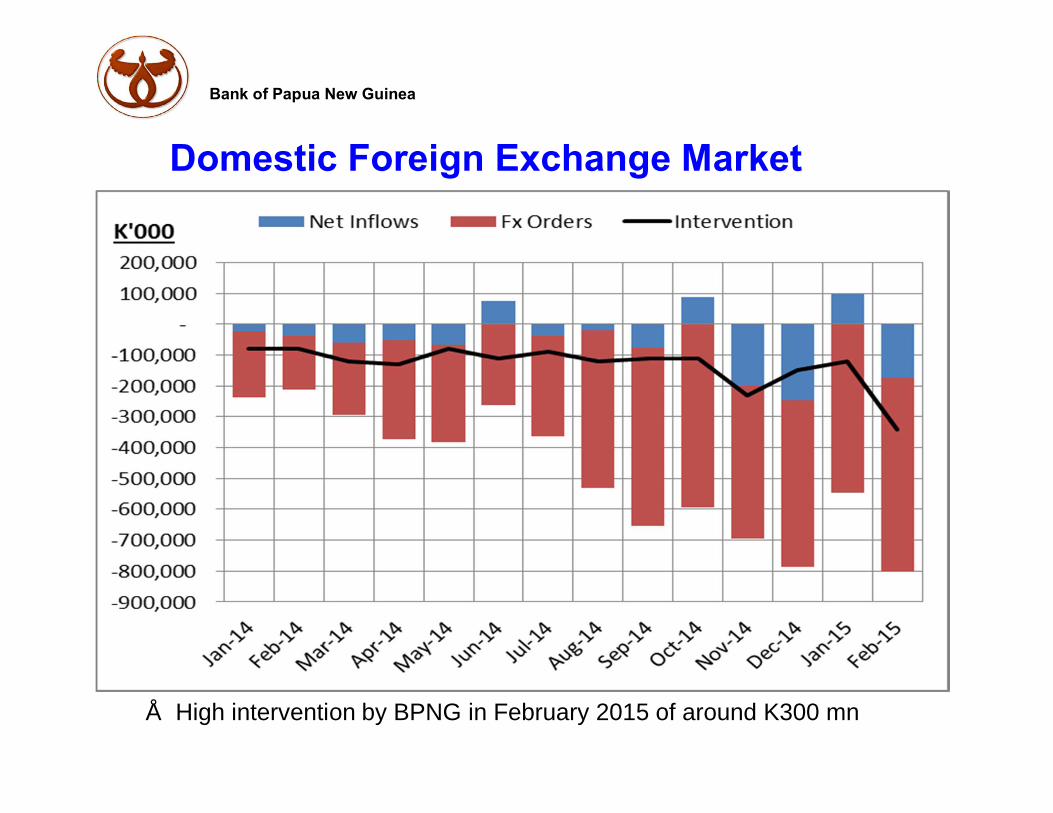

Domestic Foreign Exchange Market

Bank of Papua New Guinea

Domestic Foreign Exchange Market

• High intervention by BPNG in February 2015 of around K300 mn

Bank of Papua New Guinea

• Exchange rate depreciated by 9.3% since the banding

PGK/USD

Bank of Papua New Guinea

5.1 Kina Vostro Accounts• Kina Vostro accounts of foreign banks were used for

unauthorised banking business by: – Not using authorised foreign exchange dealers to convert kina

for foreign currency, in breach of Regulation 6 of the Central Banking (Foreign Exchange and Gold) Regulation 2000.

– Taking deposits from PNG resident entities• In 2014 the volume of kina transacted via the Vostro accounts

was approximately 50 percent of the turnover in the domestic foreign exchange market

• The large kina payments and receipts are not reported to BPNG because the foreign currency leg is done by foreign banks

• The transactions that involved the use of Vostro accounts were not subject to the exchange rate trading band

• Exchange rate spreads offered by foreign banks to PNG residents were much wider than 150 point spread in the domestic market

Bank of Papua New Guinea

Bank of Papua New Guinea

5.2 International Reserves (BPNG)

Bank of Papua New Guinea

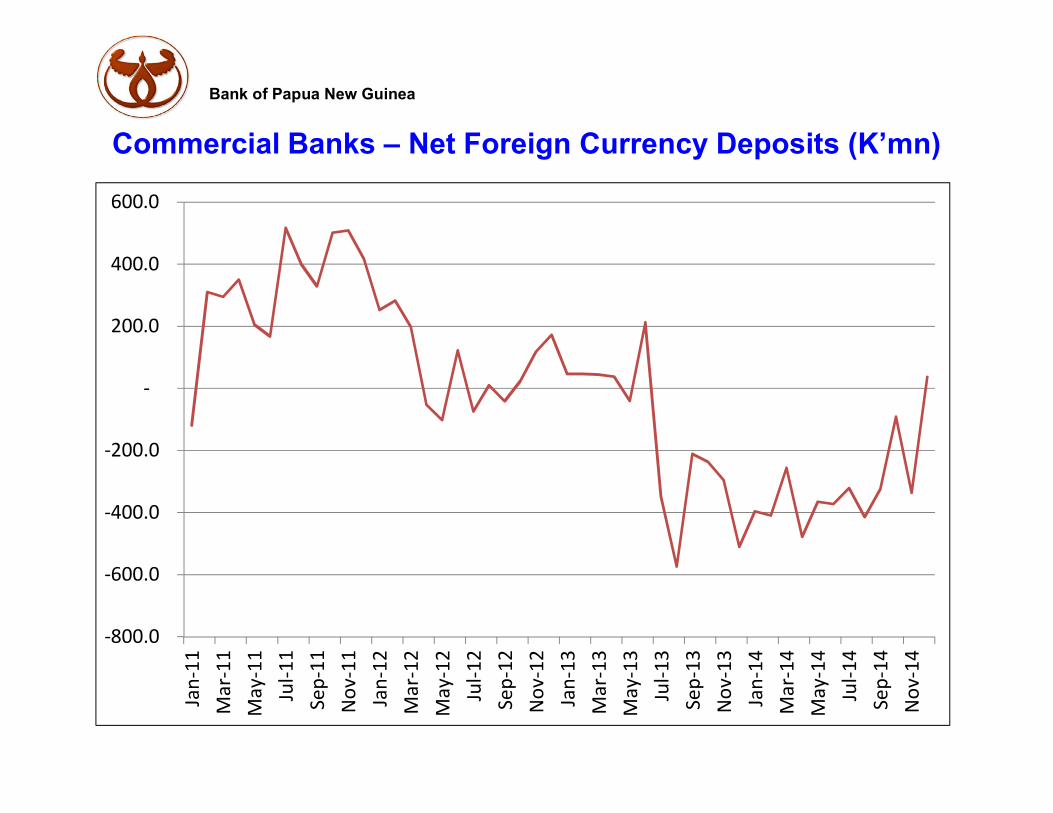

Commercial Banks – Net Foreign Currency Deposits (K’mn)

-800.0

-600.0

-400.0

-200.0

-

200.0

400.0

600.0Ja

n-11

Mar

-11

May

-11

Jul-1

1Se

p-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep-

12N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3Se

p-13

Nov

-13

Jan-

14M

ar-1

4M

ay-1

4Ju

l-14

Sep-

14N

ov-1

4

Bank of Papua New Guinea

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Jan-06 Nov-06 Sep-07 Jul-08 May-09 Mar-10 Jan-11 Nov-11 Sep-12 Jul-13 May-14

K' m

n

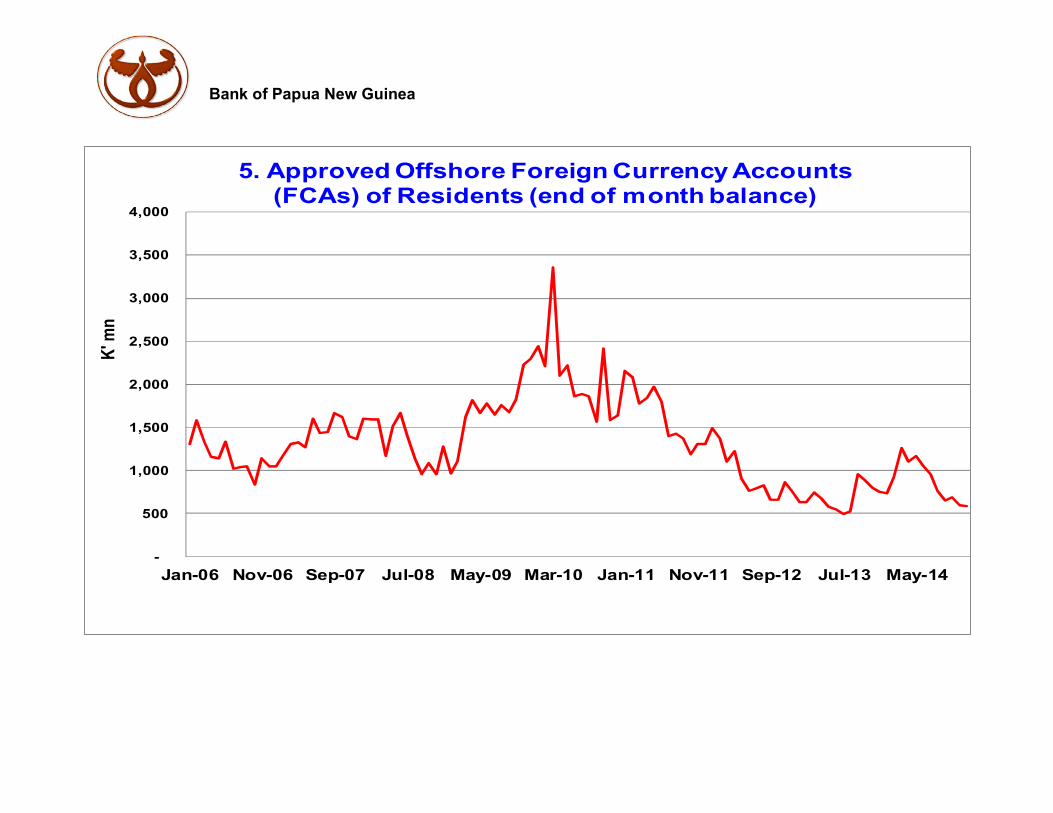

5. Approved Offshore Foreign Currency Accounts (FCAs) of Residents (end of month balance)

Bank of Papua New Guinea

Distribution of Foreign Currency Holdings

-

2,000.0

4,000.0

6,000.0

8,000.0

10,000.0

12,000.0

14,000.01-

Jan-

11

1-M

ar-1

1

1-M

ay-1

1

1-Ju

l-11

1-Se

p-11

1-N

ov-1

1

1-Ja

n-12

1-M

ar-1

2

1-M

ay-1

2

1-Ju

l-12

1-Se

p-12

1-N

ov-1

2

1-Ja

n-13

1-M

ar-1

3

1-M

ay-1

3

1-Ju

l-13

1-Se

p-13

1-N

ov-1

3

1-Ja

n-14

1-M

ar-1

4

1-M

ay-1

4

1-Ju

l-14

1-Se

p-14

1-N

ov-1

4

1-Ja

n-15

Offshore FCA Balance Onshore FCA Balance Net FC Deposits BPNG Reserve

• In aggregate, around K8bn forex reserves for PNG. Likely import cover of 11.8 months for total and 16.6 months for non-mineral, as at January 2015

Bank of Papua New Guinea

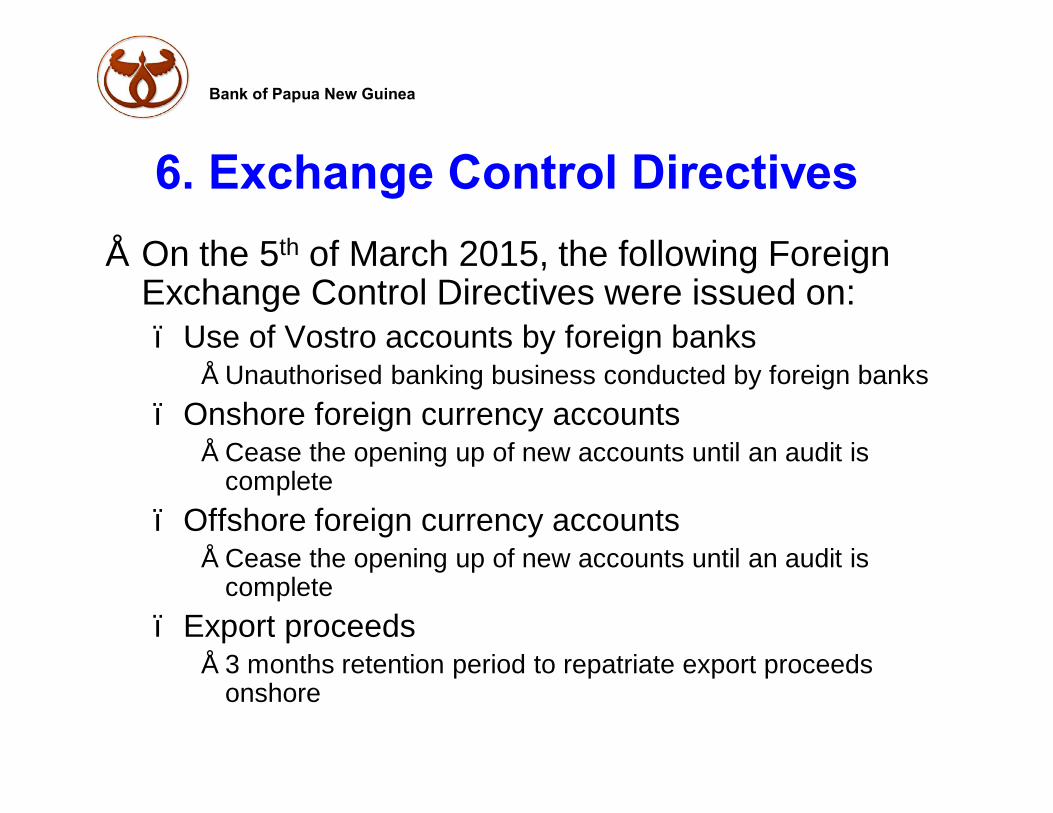

6. Exchange Control Directives• On the 5th of March 2015, the following Foreign

Exchange Control Directives were issued on:– Use of Vostro accounts by foreign banks

• Unauthorised banking business conducted by foreign banks– Onshore foreign currency accounts

• Cease the opening up of new accounts until an audit is complete

– Offshore foreign currency accounts• Cease the opening up of new accounts until an audit is

complete – Export proceeds

• 3 months retention period to repatriate export proceeds onshore

Bank of Papua New Guinea

Aim of the Directives • The Exchange Control Directives were

issued under the Foreign Exchange Manual

• They are not a re-introduction of foreign exchange controls or removal of exemption notices

• Not meant to frighten or scare anyone but restore order in the foreign exchange market

• Help address the imbalance in the foreign exchange market

Bank of Papua New Guinea

Planned Implementation • Authorised Foreign exchange dealers to

enforce directives with their customers• External audit conducted on onshore and

offshore foreign currency accounts (FCAs)• Pending the findings of the audit, a ban is

imposed on opening of new onshore and offshore FCAs

• Offshore Kina or foreign currency accounts for trade purposes are opened with the prior approval of BPNG

Bank of Papua New Guinea

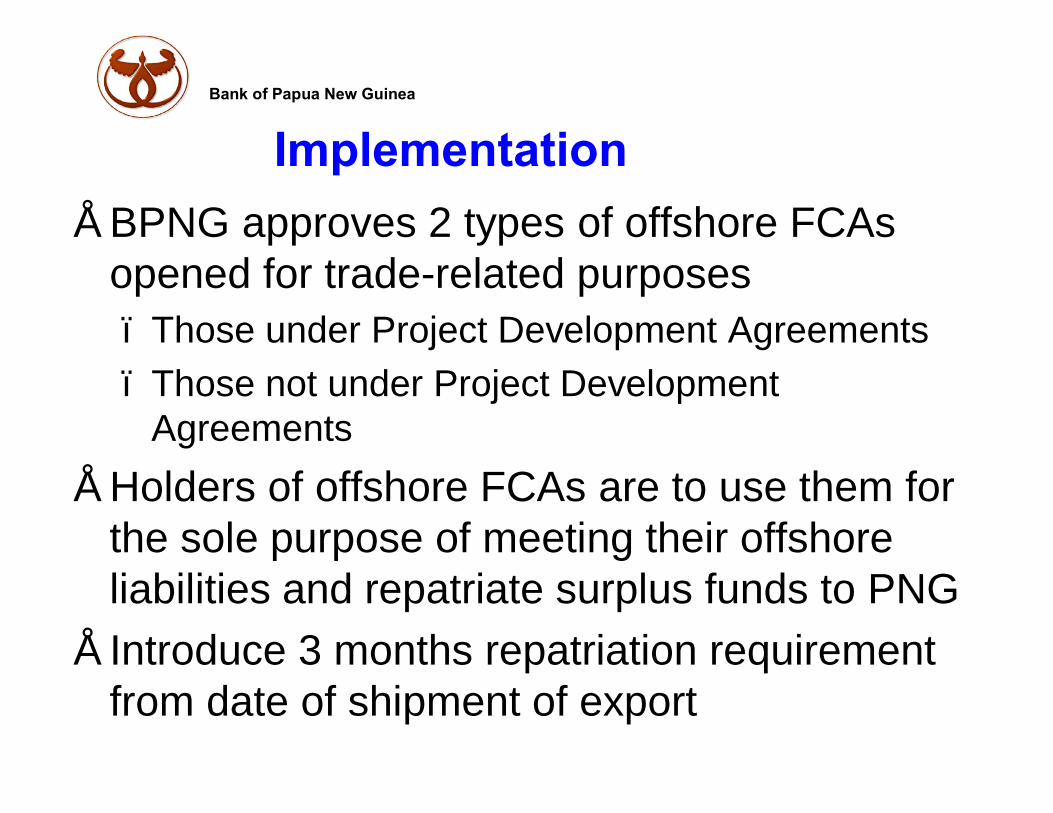

Implementation• BPNG approves 2 types of offshore FCAs

opened for trade-related purposes– Those under Project Development Agreements– Those not under Project Development

Agreements• Holders of offshore FCAs are to use them for

the sole purpose of meeting their offshore liabilities and repatriate surplus funds to PNG

• Introduce 3 months repatriation requirement from date of shipment of export

Bank of Papua New Guinea

Implementation • Holders of offshore FCA opened for trade

purposes without BPNG’s prior approval have 2 months (until 6th May) to close them down and convert the funds into Kina

• They can then apply to BPNG should they want an offshore FCA

• Breaches of the Directives will be dealt with in accordance with the Central Banking (Foreign Exchange & Gold) Regulation.

• Revised Foreign Exchange Manual will be issued with the new Directives

Bank of Papua New Guinea

8. Conclusion These Directives are aimed at stopping the use of Vostro accounts for unauthorised banking business• Restore order and help to address imbalance in

the foreign exchange market• It is not a crisis situation• Vostro accounts to be used only for authorised

purposes and resident entities (importers/exporters) should deal only with authorised dealers

• Authorised dealers or banks have to report transactions through Vostro accounts on the BOP forms

Bank of Papua New Guinea

• Offshore FCAs should be used only to pay for foreign liabilities of the holders

• Offshore FCAs for trade purposes are not exempted and requires BPNGs prior approval to open

• All offshore FCAs that are not for trade related purposes will be addressed by BPNG later

• Onshore FCAs should not be held for speculative purposes and any demand for foreign currency should be brought to the spot market

Conclusion (cont’d)

Bank of Papua New Guinea

• BPNG will make further decisions based on the findings of the audits on FCAs

• Any breaches of these Directives will be dealt with by the Central Banking (Foreign Exchange & Gold) Regulation

Conclusion (cont’d)

Bank of Papua New Guinea

• Penalties: – Fine of K100,000; or– Amount equal 25% of the total value of funds

or property involved, whichever is greater; or– Imprisonment for a term not exceeding five

years.– In addition, a court may order forfeiture of an

asset or order its sale to BPNG

Conclusion (cont’d)

Bank of Papua New Guinea

Thank YouThank You

www.bankpng.gov.pg