Managing the Emerging Foreign Exchange Risks Across all Sectors

42

Managing the Emerging Foreign Exchange Risks Across all Sectors James Okarimia Senior Vice President H. Pierson Associates Global Association of Risk Professionals September, 2016

-

Upload

global-association-of-risk-professionals-garp -

Category

Economy & Finance

-

view

119 -

download

1

Transcript of Managing the Emerging Foreign Exchange Risks Across all Sectors

Managing the Emerging Foreign Exchange Risks Across all Sectors

James OkarimiaSenior Vice PresidentH. Pierson Associates

Global Association of Risk ProfessionalsSeptember, 2016

2

The views expressed in the following material are the

author’s and do not necessarily represent the views of

the Global Association of Risk Professionals (GARP),

its Membership or its Management.

MANAGING THE EMERGING FOREIGN EXCHANGE RISKS ACROSS ALL SECTORS

LAGOS GARP CHAPTER PRESENTATIONJAMES OKORO JEFFREY OKARIMIA

JAMES OKORO JEFFREY OKARIMIA

He has been in the Banking and Financial Services Industry for 30 years. James has over 25 years banking and Financial Risk Management Advisory Experience and Head of Risk and Compliance for various Risk Advisory Activities. James has over16 years in Governance, Risk Management and Compliance, with extensive Basel II/III, Solvency II Framework, and Software Implementation experience gained internationally across numerous Global Financial Institutions including, ABNAMRO Bank Netherlands; African Development Bank - AFDB; Delta Lloyd Banking Group; Fortis Bank Belgium, Bear Sterns International, UK; American Express UK; Shearson Lehman, UK; Citi Bank, UK; Nat West Stock Brokers, UK; Union Bank of Nigeria UK etc.

James also worked for Big Four Consultancy Firms: KPMG Financial Services, Netherlands; IBM Global Business Services, Benelux; Parson Consulting UK; Tata Consultancy, Cognizant Technology Solutions, BeneluxJames has over 16 years of experience, extensively working on Capital Markets and Trading Risk system implementation and integration services across platforms like SAP, SAS, Oracle, Fermat, Moody’s SunGard, FinArch ,Summit, Murex , Fidessa, Calypso, Sophis and Globus Temenos systems

OVERVIEW• FX Risk Impact on all Business Sector• Challenge in Managing FX Risk• Introduction Of Foreign Exchange Trading Platform By

CBN• Recently Launched the Naira-Settled OTC FX Futures

Market By Central Bank of Nigeria and the Financial Markets Dealers Quotation (FMDQ)

• FX Trading Infrastructure and Platform• Mitigation with Currency Swap - FX Swap/Forward

Contracts

4

FX RISK EXPOSURE AND IMPACT ON ALL BUSINESS SECTOR IN NIGERIA Manufacturing Industry Oil and Gas Industry FG and Local Governments Large Corporates and Conglomerates Hospitals and Health Care Companies SME’s Importers and Exporters Financial Services Industry

CHALLENGE IN MANAGING FX RISK

The Business Imperative• Given the potential impact that adverse FX movements can have on cash flow though value

attrition, liquidity as a result of cash ‘trapped’ in foreign currencies, and ultimately on corporate results, FX Risk Management is a fundamental issue for Treasurers.

• Even the largest global corporations are not immune to the effects of negative volatility.

• With greater analyst scrutiny (for example, FX was the main topic that analysts wanted to discuss during the Apple quarterly results briefing despite the eye-watering results) and growing competition globally however, treasurers and CFOs cannot be complacent about managing their FX Risk.

An emerging focus on FX risk• Given the scale of the challenge, are treasurers focusing enough on this area? In some cases, it

appears that treasurers have paid more attention to Liquidity Risk over the past few years, with the exception of large Multinational Corporations and those with particularly Large Currency or Commodity Exposures

.

Challenge in Managing FX Risk

An emerging focus on FX Risk

• For Mid-Cap and Smaller Corporations in particular, the issue is how to address FX Risk Efficiently, particularly given Resourcing and Technology Constraints.

In Deloitte’s 2015 Global Corporate Treasury Survey, Volatility and Cash Repatriation were identified as the greatest challenges facing Treasurers, each of which was noted by 50% of participants, at least 10% more than issues such as cash visibility (40%), Treasury Technology (40%), Entering Restricted Markets (24%) and Managing Liquidity (29%).

This is not surprising, given the high levels of volatility in both the FX and Commodity Markets, continuing international expansion resulting in exposure to a growing number of currencies, and geopolitical insecurity in many parts of the world.

Furthermore, the ACT’s The Contemporary Treasurer 2015 study shows that 83% of Treasuries produce Board Reporting on Risk Management (which includes FX), emphasizing the importance and visibility of Treasury’s role in FX Risk Management

CHALLENGE IN MANAGING FX RISKAn emerging focus on FX Risk CFO & TREASURY MANAGER Are Taking the Responsibility of Managing FX Risk• For Corporations with a Defined Treasury Function, responsibility for FX policy definition is

usually clear, and the need to manage FX risk at a group level is one of the factors in deciding to Centralize Treasury.

• “As companies of all sizes expand their activities internationally, their FX Risk often becomes more difficult to manage, particularly where subsidiaries buy and sell in foreign currencies.

• Larger Multinationals overcome this growing scale and complexity of FX exposure by centralizing FX risk management into regional or global treasury centers with specialist systems and specific expertise”.

• “For smaller companies without a Central Treasury Function, this is more challenging, as the process of information gathering, designing and executing a hedging strategy, and implementing appropriate controls takes significant resource, particularly if responsibilities are shared across different functions or subsidiaries.”

• In some cases, even where Treasury Policy is determined Centrally, Execution may be dispersed more widely, particularly in companies with a more Decentralized Treasury Approach, and/ or where complex local market conditions make it more appropriate for local entities to manage exposure to a particular currency due to its volatility, currency controls or local liquidity conditions.

• Consequently, every company needs a clear definition of where responsibilities for defining and executing FX strategy should lie. Where these are disseminated, it makes sense to try to use a common platform to maintain a global view over exposures and hedging transactions

THE LAUNCH OF NAIRA-SETTLED OTC FX FUTURES MARKET BY CBN AND (FMDQ)

• The Naira-settled OTC FX Futures market has been kicked off by the CBN and FMDQ OTC Securities Exchange on June 27, 2016.

• The Naira-Settled OTC FX futures market started with the CBN selling the OTC FX futures contracts of non-standardized amounts for different tenors from one month through to 12 months, which will settle on bespoke maturity dates, providing liquidity in the product that will enable corporate treasurers effectively and efficiently manage their forex risk.

• The Naira-Settled OTC FX Futures has been defined by experts as a non-deliverable forwards i.e. contracts that obligate the counterparties to purchase or sell a specific currency (the US Dollar, which is a notional amount) on a predetermined future date (the settlement date) for a fixed rate agreed on the date the contracts were entered into (trade date).

LAUNCH OF THE NAIRA-SETTLED OTC FX FUTURES MARKET BY CBN AND (FMDQ)

• Simply put, the Naira-Settled OTC FX Futures contracts can be used to Hedge a Corporate’s Exposure to FX (in this situation, the US Dollar) whereby the rate at which the corporate will purchase (or sell) FX at a period of time in the future is predetermined and fixed. There is no obligation for the physical delivery of the currencies (Naira or US Dollar) and at maturity, net-settlement will be made in Naira based on the US Dollar notional amount, and determined by the difference between the agreed rate (on trade date) and spot FX rate (on settlement date).

FX TRADING INFRASTRUCTURE

- Central Bank of Nigeria- FMDA ( Financial

Markets & Dealers Association)

- FMDQ OTC Securities Exchange

- Securities and Exchange Commission

- SWIFT- FMDQ Trading

Systems- Reuters

terminals- Bloomberg- NIBSS

NAIRA-SETTLED OTC FX TRADING PLATFORM AND INFRASTRUCTURE

• Ahead of the establishment of a Central Counterparty (CCP), the Nigeria Inter-Bank Settlement System PLC (NIBSS) will act as the clearing and settlement infrastructure for the margining and settlement of the OTC FX Futures contracts.

• CBN, through the FMDQ OTC FX Futures Trading & Reporting System, will offer the Naira-settled OTC FX Futures contracts to all Authorized Dealers (and may, in addition, deal directly with its FXPDs on a two-way quote basis) who will in turn offer same to customers with trade-backed transactions.

FX TRADING MARKET PARTICPANTS

FX Spot

FX Futures

Fixed Income

Controlling Body

Counterparty

Central Bank

Central Bank

FMDQ OTC Securities Exchange

Importers

Importers &Investors

Investors

CBN, Authorised Dealers, Oil companies, Oil service companies, Exporters, end users

CBN, Authorised Dealers, Oil companies, Oil service companies, Exporters, end users

Corporates and individual investors

EXPLANATION OF HOW NAIRA-SETTLED OTC FX FUTURES WORKS IN PRACTICE

• The Naira-Settled OTC FX Futures are Non-Deliverable Forwards (i.e. a contract where parties agree to an exchange rate for a predetermined date in the future, without the obligation to deliver the underlying US Dollar (notional amount) on the maturity/settlement date).

• On the maturity date, it will be assumed that both parties would have transacted at the Spot FX market rate. The party that would have suffered a loss with the Spot FX rate will be paid a settlement amount in naira.

• This ensures that both parties enjoy the rate that had been guaranteed to each other through the OTC FX Futures.

• Settlement Amount = (Difference between the Agreed Rate and Spot Rate on the Maturity Date) x Notional Contract Sum.

EXPLANATION OF HOW NAIRA-SETTLED OTC FX FUTURES WORKS IN PRACTICE

• The Spot FX Rate is the FMDQ Spot FX Rate Benchmark -Nigerian Inter-Bank Foreign Exchange Fixing (NIFEX), which is an independent fixing of the Inter-Bank FX Market.

• NIFEX represents the daily average of the prevailing spot market rate of some selected banks at which the US dollar (USD) is traded against the Nigerian Naira (NGN). NIFEX is a ‘polled’ rate, meaning that a set of selected banks known as Reference Banks submit quotes which are processed to derive the NIFEX.

• The OTC FX Futures contract is an Effective Exchange Rate Management Tool supported by a Transparent Price Driven Two-Way Quote (2WQ) market

• The Central Bank of Nigeria (CBN) kicked off the market by acting as the seller of OTC FX

• Futures contracts have Defined Tenors i.e. 1Month (M), 2M, 3M, 6M, 9M, 12M, 18M and 24M.

NAIRA-SETTLED OTC FX FUTURES CONTRACTS TRADE FLOW

• FMDQ act as the ‘OTC FX Futures Exchange’ and its appointed agent; the Nigeria Inter-Bank Settlement System PLC (NIBSS) clears the Inter-Bank OTC FX Futures, i.e. collect initial and variation margins and settle the party to compensate on the maturity date.

• All trading of Naira-settled OTC FX Futures contracts are executed on the FMDQ OTC FX Futures Trading and Reporting System.

BENEFITS OF THE NAIRA- SETTLED OTC FX FUTURES

• The introduction of the OTC FX Futures market will encourage end- users to spread out their demand for Spot FX deals as they are now able to lock down the exchange rates for future FX requirements.

• This has the potential to eradicate the constant Front-Loading of FXrequirements and minimize the disequilibrium in the Spot FX market.

• End- users will make better judgement as to the timing of accessing the Spot FX market. The availability of the OTC FX Futures will improve the business planning practice of end-users and FX sellers, as the future exchange rate is guaranteed through the OTC FX Futures.

• An end- user (buyer of USD) may consider it wiser to delay the purchase of its USD requirement in the Spot FX market if the Spot FX rate is higher than the OTC FX Futures rate of a particular tenor.

• The end-user will borrow USD or obtain trade finance and simultaneously hedge its exchange rate exposure with an attractive OTC FX Futures contract sold by the CBN. At maturity of the OTC FX

• With Futures contract, Gives the end- user access to Spot FX market.

BENEFITS OF THE NAIRA- SETTLED OTC FX FUTURES

• The OTC FX Futures will be used to attract significant capital flows to the Nigerian Fixed Income and, Equity Markets as returns can now be enhanced as FX exposures are hedged. Foreign Portfolio Investors (FPIs) will be able to use the OTC FX Futures for capital protection.

• The envisaged increase of supply of US Dollars due to the OTC FX Futures offered by the CBN in the Spot FX market will cause the Spot FX rate to moderate

• OTC FX Futures, which are non-deliverable are ideal for FPIs and even Foreign Direct Investors (FDIs). OTC FX Futures can be used when the investor wants to hedge the exchange rate risk without interest in buying outright

• Forwards which will necessitate liquidation of its investment to pay for outright Forwards Banks will increase the liquidity in the OTC FX Futures market (by selling OTC FX Futures) if $/₦Spot FX rate starts dropping. This may cause the Spot FX rate to drop further.

SETTLEMENT ANALYSIS FOR NAIRA-SETTLED OTC FX FUTURES CONTRACTS

• Day 1: June 1, 2016 -Bank A buys a 3-month OTC FX Futures contract from the CBN on the FMDQ OTC FX Futures Trading and Reporting System with the following details:

• Buyer: Bank A, Seller: CBN, Notional amount: $1,000,000.00, OTC FX Futures Rate: $/N260.00, Benchmark: NIFEX, Maturity Date: August 31, 2016, Initial Margin: 5% (payable by both parties), Maintenance Margin: 60% of initial margin, Settlement Currency: Naira.

• The OTC FX Futures contract will be valued on a daily basis against the NIFEX to determine payment of variation margin amount.

Maturity Day: August 31, 2016 – NIFEX is $/N270• It is assumed that Bank A would have transacted (bought USD in the Spot FX market) at $/N270.00 which is higher than

the OTC FX Futures contract rate of $/N260.00.

• The Clearing House, NIBSS, will pay Bank A N10,000,000.00 (i.e. N10.00 [N270.00-N260.00] per USD) thereby bringing Bank A’s effective rate to $/N260.00 (N270.00 assumed paid in buying USD less N10.00 received on the OTC FX Futures) which is the OTC FX Futures rate.

• CBN is assumed to have transacted (sold USD in the Spot FX market) at $/N270.00 which is higher than the OTC FX Futures contract rate of $/N260.00.

• The Clearing House, NIBSS, will take N10,000,000.00 (i.e. N10.00 per USD) from the Margin Account of the CBN thereby bringing CBN’s effective rate to $/N260.00 (N270.00 assumed received in selling USD less N10.00 paid out on the OTC FX Futures) which is the OTC FX Futures rate.

• Both parties end up with an effective rate of $/N260.00 as this was the guaranteed rate for both parties. If NIFEX had been $/N250.00 on maturity date, Bank A would pay CBN N10.00 per USD.

USING FX DERIVATIVES TO MANAGE CURRENCY RISK• Derivatives are a great vehicle for hedging and managing

risk; they enhance liquidity and price discovery• However, they are complicated and one should understand

them before taking on any trades• The Nigerian capital and investment market is advancing

rapidly, only those with a good understanding of the market can take advantage of the opportunities it offers hence, operators must do all they can to expand the reach of participants thereby improving the economy generally.

• From all indications, derivatives will continue to be used as a Tool For Risk Reduction and Efficient Portfolio Management.

• As Nigeria positions itself to take advantage of the benefits of these dynamic financial instruments, it may be useful for regulators to provide clarity as to what can be traded in an exchange and OTC.

C r e a t i n g a c u l t u r e o f r i s k a w a r e n e s s ®

Global Association ofRisk Professionals

111 Town Square Place14th FloorJersey City, New Jersey 07310U.S.A.+ 1 201.719.7210

2nd FloorBengal Wing9A Devonshire SquareLondon, EC2M 4YNU.K.+ 44 (0) 20 7397 9630

www.garp.org

About GARP | The Global Association of Risk Professionals (GARP) is a not-for-profit global membership organization dedicated to preparing professionals and organizations to make better informed risk decisions. Membership represents over 150,000 risk management practitioners and researchers from banks, investment management firms, government agencies, academic institutions, and corporations from more than 195 countries and territories. GARP administers the Financial Risk Manager (FRM®) and the Energy Risk Professional (ERP®) Exams; certifications recognized by risk professionals worldwide. GARP also helps advance the role of risk management via comprehensive professional education and training for professionals of all levels. www.garp.org.

4 | © 2014 Global Association of Risk Professionals. All rights reserved.

FINANCIAL PRODUCTS

Fixed Income Securities

FX Futures

FX Spot

Bonds FGN States Corporates

Repos

NTB Biweekly OMO

Securities issued on which investors expect fixed incomes. They are always at a coupon. The current yield depends on the striking price.

Outright purchase or sale of one currency for another for delivery in 2 business days (T+2) after the dealing date. The Two business days are usually sufficient to complete administrative processes

Agreement to buy/sell fx at a certain future date at a price agreed upon on the transaction date. Rates in the forward market differ from spot rates mainly due to the concept of the time value of money

There are autonomous funds and intervention

funds. Counterparties include Central Bank, authorized dealers,

authorized buyers, oil companies, oil service companies, exporters

and end users.

RISK MITIGATION WITH CURRENCY SWAPSThree Methods:

1. Hedging with Currency Swaps2. Hedging with Forward Contracts3. Other Hedging Options

The hedge is an insurance policy. Whether you're transacting business abroad or simply holding onto foreign currencies as an investment, a fluctuation in currency can cause serious losses very quickly. A hedge is a way to guard against this: Invest in a position that offsets (bets against) an investment you already own, and any losses in one position will be buoyed up by gains in the other.

METHOD 1: HEDGING WITH CURRENCY SWAPS

1. SWAP CURRENCIES AND INTEREST RATES WITH A PARTY IN A CURRENCY SWAP

• In a such a swap, two parties agree to swap equivalent amounts of cash (called principal) as well as interest rate payments over a fixed period of time. The cash usually originates as debt (a party issues a bond) or as credit (a party gets a loan). The principals exchanged are usually equivalent amounts: Party A swaps $1,000,000 for €750,000 from Party B, based on the exchange rate. The swapped interest rate payments, however, are usually not the same.

• Here's a very basic example. Vitaly Partners, an Italian company, wants to hedge against the euro by buying dollars. Vitaly agrees on a currency swap with Brand USA, an American company. Over five years, Vitaly sends Brand USA €1,000,000 in exchange for the dollar equivalent, about $1,400,000. Vitaly agrees to swap interest payments with Brand USA as well: Vitaly will pay Brand USA 6% interest on its swapped principal, €1,000,000, while Brand USA will pay Vitaly 4.5% interest on its swapped principal, $1,400,000.

2. EXCHANGE INTEREST PAYMENTS IN A CURRENCY SWAP, NOT PRINCIPALS.

• The principal that the two parties agree to swap isn't actuallyexchanged. It is kept by both parties. The principal is what financiers call a notional principal, or an amount that is theoretically exchanged but actually kept. Why is the principal needed, then? It's needed to calculate the interest payments, which are the backbone of any currency swap.

3: CALCULATE YOUR INTEREST RATE PAYMENT.

• Interest rate payments are usually swapped at six-month or one-year intervals, and this is where the parties transfer currencies that help them hedge against fluctuations in their own currency. Let's look at an example:

• Vitaly agreed to swap €1,000,000 at 6% to Brand USA in exchange for $1,400,000 at 4.5%. Let's assume that interest rate payments are swapped every six months.

• Vitaly's interest rate payment will be calculated as follows: Notional principal x interest rate x frequency. Every six months, Vitaly will pay Brand USA €30,000, in euros. (€1,000,000 x .06 x .5 [180 days/360 days] = €30,000.)

• Brand USA's interest rate payment will be calculated as follows: $1,400,000 x .045 x .5 = $31,500. Brand USA will pay Vitaly $31,500, in dollars, every six months.

4. WORK WITH A PARTNERING FINANCIAL INSTITUTION TO MEDIATE THE SWAP.For simplicity, this example so far has avoided a third party that's involved in the swap — banks. When Vitaly sends its interest payments over to Brand USA, it does so by sending the bank the interest payment first; the bank takes a small cut and sends the rest of the interest payment on over to Brand USA. Ditto for Brand USA: it must also mediate the transaction through the bank, which takes a small cut from their swap for granting the privilege.

4. WORK WITH A PARTNERING FINANCIAL INSTITUTION TO MEDIATE THE SWAP

Why choose currency swaps instead of just buying foreign currency? Currency swaps involve two parties.

Remember Vitaly and Brand USA.

Vitaly gets a better interest rate on its loan of €1,000,000 in Italy than it would if it asked for the loan in America.

Likewise, Brand USA gets a better interest rate on its $1,400,000 loan in America than it would if it got the loan in Italy.

By agreeing to exchange interest rate payments, currency swaps bring together two parties that each have better loan agreements in their own countries and their own currencies.

METHOD 2: HEDGING WITH FORWARD CONTRACTS

• Purchase forward contracts. A forward contract is like a futures contract or derivative. It is an agreement to buy or sell a currency at a fixed price on a certain date.

• Here's an example: • Dave is worried that the price of the dollar is going to plummet

relative to the British pound. He has $1,000,000 in cash, which would fetch him about £600,000 at the then-current exchange rate. Dave wants to use a forward contract to lock in the exchange rate of the dollar relative to the pound. Here's what Dave does:

• Dave offers to sell Vivian $1,000,000 of US currency in exchange for £600,000 of British currency in six months. Vivian accepts the deal. This is a "forward contract."

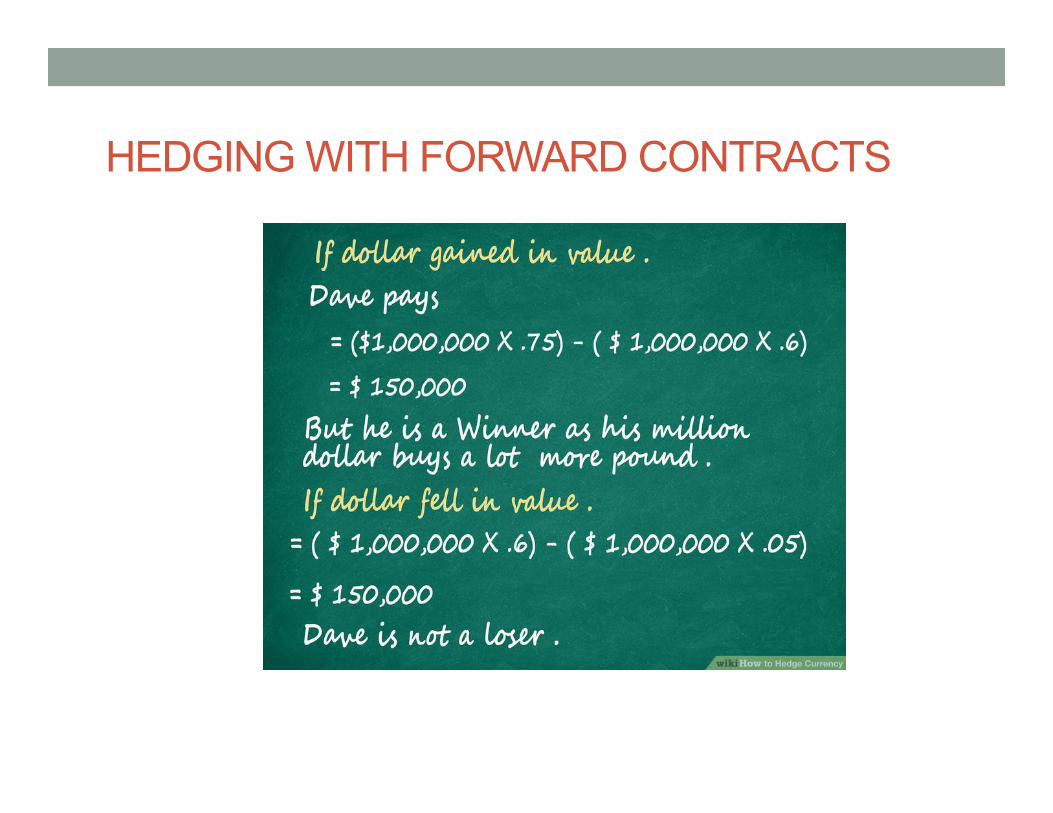

HEDGING WITH FORWARD CONTRACTS

HEDGING WITH FORWARD CONTRACTS• Evaluate the forward contract at the agreed-upon time. Let's continue with our

example of Dave offering a forward contract to Vivian. In six months (the agreed-upon time), there are three possible outcomes regarding the price of the dollar relative to the pound. Each of these possibilities affects the forward contract:

• The price of the dollar goes up relative to the pound. Hypothetically, let's say one dollar now fetches .75 pound instead of .6 pound. Dave pays Vivian the difference between the current price of exchange and the price agreed upon in the contract: ($1,000,000 x .75) - ($1,000,000 x .6) = $150,000.

• The price of the dollar goes down relative to the pound. Hypothetically, let's say one dollar now fetches .45 pound instead of .6 pound. Vivian agreed to pay Dave .6 pound for each of his dollars six months ago, so Vivian has to pay Dave the difference between the price agreed upon in the contract and the current price: ($1,000,000 x .6) - ($1,000,000 x .45) = $150,000.

• The exchange rate between the dollar and the pound stays the same. No exchange happens between partners in the contract.

HEDGING WITH FORWARD CONTRACTS

USE FORWARD CONTRACTS AS A WAY TO HEDGE AGAINST CURRENCY DROPS AND SPIKES.

Like any Derivative, a Forward Contract is a great way to ensure you don't lose a lot of money if a currency you have a sizable position in drops in value.

Here's how Dave came out by using a Forward Contract:

• If the dollar gained in value, Dave is a winner, although he still has to pay out. If one dollar fetches .75 pound instead of .6, Dave has to pay Vivian $150,000, but his million dollars suddenly buys a lot more pounds.

• If the dollar fell in value, Dave isn't a loser. Remember, Vivian owes him the exchange rate they agreed upon at the beginning of the contract. So it's as if the value of the dollar never fell. Dave takes the payout, none the poorer than he was before.

METHOD 3: OTHER HEDGING OPTIONS

BUY FOREIGN CURRENCY OPTIONS.• Foreign currency options give the purchaser the option to sell or buy

a foreign currency contract at a specific price on a specific date. This hedging technique is similar to forward contracts, except that the owner of the option is not required to exercise the option.

• When the specific date (known as the expiration date) of the contract arrives, the buyer of the contract can exercise the option at the agreed price (known as the strike price), if currency fluctuations have made it profitable for him/her. If fluctuations have made the option worthless, it expires without the company or individual exercising it.

BUY GOLD.• You can use gold and other precious metals to hedge currency

positions. Investors have used gold as a hedge since ancient times, and many investors still keep gold in their portfolios to guard against economic pitfalls or disasters

EXCHANGE SOME OF YOUR NATIVE CURRENCY FOR A FOREIGN CURRENCY.

One of the simplest ways to hedge your currency holdings is to buy some foreign currencies. If you live in a country that uses the Euro, for example, you can buy U.S. dollars, Swiss francs or Japanese yen (among others). If the value of the Euro drops relative to the other currencies, you’ve sheltered yourself to the extent that you own the other currencies.

BUY SPOT CONTRACTS.

A spot contract is an agreement to sell or buy foreign currency at the current rate and requires execution within two days. Spot contracts are essentially the opposite of futures contracts, where the deal is agreed upon well before the assets or goods are delivered, if at all.

39

• Contingent Credit Risk - Loss Profile Over Time• The average of the expected replacement cost curve

represents the loan equivalent

Single Currency Swap Cross Currency Swap

Maturity Time

Average

Exposure Exposure

Average

TimeMaturity

SINGLE CURRENCY & CROSS CURRENCY SWAP

QUESTIONS AND ANSWERS

40