Managing stability challenges in growth promoting ... · Managing stability challenges in growth...

27

0 Managing stability challenges in growth promoting utilization of capital flows: the Bangladesh experience ALLAH MALIK KAZEMI Advisor to Governor, Bangladesh Bank IMF-UKaid Seminar on Managing Capital Flows Mauritius, March 02, 2015

Transcript of Managing stability challenges in growth promoting ... · Managing stability challenges in growth...

0

Managing stability challenges in growth promoting utilization of capital flows:

the Bangladesh experience

ALLAH MALIK KAZEMI Advisor to Governor, Bangladesh Bank

IMF-UKaid Seminar on Managing Capital Flows

Mauritius, March 02, 2015

1

Outline

o Growth support focused eclectic stance in managing

capital flows

o Cautious, limited openness for outflows of resident

owned capital

o Growth and stability outcomes of Bangladesh’s stance

on openness to capital flows

o Outlook for the path ahead

2

Growth support focused eclectic stance in managing capital flows

3

Capital inflows: opportunities & risks

o Foreign private capital inflows are needed for investment and growth acceleration in developing economies like Bangladesh;

o But volatility of the capital flows entail risks for macroeconomic and financial stability;

o QE and other monetary loosening measures of advanced economies have amplified the opportunities and risks.

4

Bangladesh’s growth support focused eclectic stance:

o Seeks to channel inflows into growth promoting uses underpinning stability with:

— liberal permissibility of inflows into real sector productive undertakings

— cautiously regulating access into the volatility prone financial sector.

5

Bangladesh’s growth support focused eclectic stance:……(cont’d)

o Access to external financing inflows widened and facilitated for private sector productive undertakings

— not hurrying into sovereign bonds issuance for budget financing, presumably from concerns about public sector’s fund utilization efficiency;

o Domestic currency is freely convertible for all trade related and other current external transactions;

o Local and foreign productive undertakings can freely access and extend short term trade credits;

o They can also raise project related longer term external financing, subject to prior viability scrutiny by a BOI Committee chaired by Bangladesh Bank Governor.

6

o Public sector’s external financing needs are met:

— mainly with concessional assistance from development partners

— partly with non-concessional project related borrowings subject to prior clearance of a high level committee, chaired by Finance Minister.

Bangladesh’s growth support focused eclectic stance:……(cont’d)

7

o FDI equity inflows are freely permissible in wholly foreign owned and joint venture real sector industrial undertakings;

— Post tax profits/dividends/disinvestment proceeds of foreign equity including capital gains are freely repatriable.

o FDI equity inflows into banks and other financial sector entities require prior regulatory approval;

— Post tax profits/dividends and disinvestment proceeds thereon are also freely repatriable.

Bangladesh’s growth support focused eclectic stance:……(cont’d)

8

o Banks in Bangladesh can borrow or lend abroad for short tenors only for trade related transaction settlements in correspondent banking arrangements with counterparts abroad;

o Term borrowings abroad by banks and financial institutions require regulatory approval, accorded sparingly only for longer term local lending.

Bangladesh’s growth support focused eclectic stance:……(cont’d)

9

o FPI inflows can freely move into listed stocks and bonds, including in Treasury bonds,

— Post-tax profits/dividends/yields and disinvestment/ redemption proceeds thereon including capital gains are freely repatriable.

o FPI inflows are not allowed into short term (one year and lower) money and Treasury bills markets, to avoid destabilization risks from volatile surges.

Bangladesh’s growth support focused eclectic stance:……(cont’d)

10

Cautious, limited openness for outflows of resident owned capital

11

Openness for resident owned capital outflows

o Limited domestic savings vis-a-vis high domestic investment demand preclude free permissibility of capital outflows for resident-owned investments abroad.

o Repatriation remains mandatory for export proceeds and foreign earnings of residents.

o Exporters can freely use ‘retention quota’ portion of their repatriated export proceeds in setting up offices abroad to facilitate marketing and inputs sourcing.

o Non-exporter businesses can also spend funds up to specified amounts without prior approval for similar purposes.

12

Openness for resident owned capital outflows..(cont’d)

o Banks and financial institutions are not free to invest abroad or to extend loans to non-resident clients.

o With prior approval, banks may incur modest capital outflows for setting up branches or subsidiaries abroad.

o Expatriates working in Bangladesh with valid permits are free to:

— remit abroad up to 3/4th of monthly earnings,

— to take back all savings with post tax profits while returning.

13

Growth and stability outcomes of Bangladesh's stance on openness to capital flows

14

o Liberal access to lower cost external financing for real sector undertakings has helped uphold output competitiveness, underpinning growth and stability.

o Restrictive stance on footloose short term external inflows into domestic financial sector has helped maintain Taka exchange rate stability,

— avoiding abrupt swings from transient inflow and outflow surges,

— aiding price and financial stability.

Growth and stability outcomes of Bangladesh's stance

15

o With no speculative exposure to QE generated liquidity inflows, unwinding thereof should pose no significant stability concern for Bangladesh.

o Careful simultaneous attention to growth and stability

concerns in capital flows management is paying off well in terms of:

— sustained spell of 6+ percent annual average real GDP growth for well over a decade amid prolonged global growth slowdown,

— single digit inflation on steadily declining path.

Growth and stability outcomes of Bangladesh's stance….(cont’d.)

16

Bangladesh’s growth projection (7% by 2019) highest in South Asia, with inflation convergent around 5%

-2

0

2

4

6

8

10

12

1995

19

97

1999

20

01

2003

20

05

2007

20

09

2011

20

13

2015

20

17

2019

Bangladesh India Pakistan Sri Lanka

Projection

Perc

ent

GDP Growth

0

2

4

6

8

10

12

14

16

18

20

22

24

1995

19

97

1999

20

01

2003

20

05

2007

20

09

2011

20

13

2015

20

17

2019

Perc

ent

Projection

Inflation

Source: World Economic Outlook (Sept. 2014), IMF

17

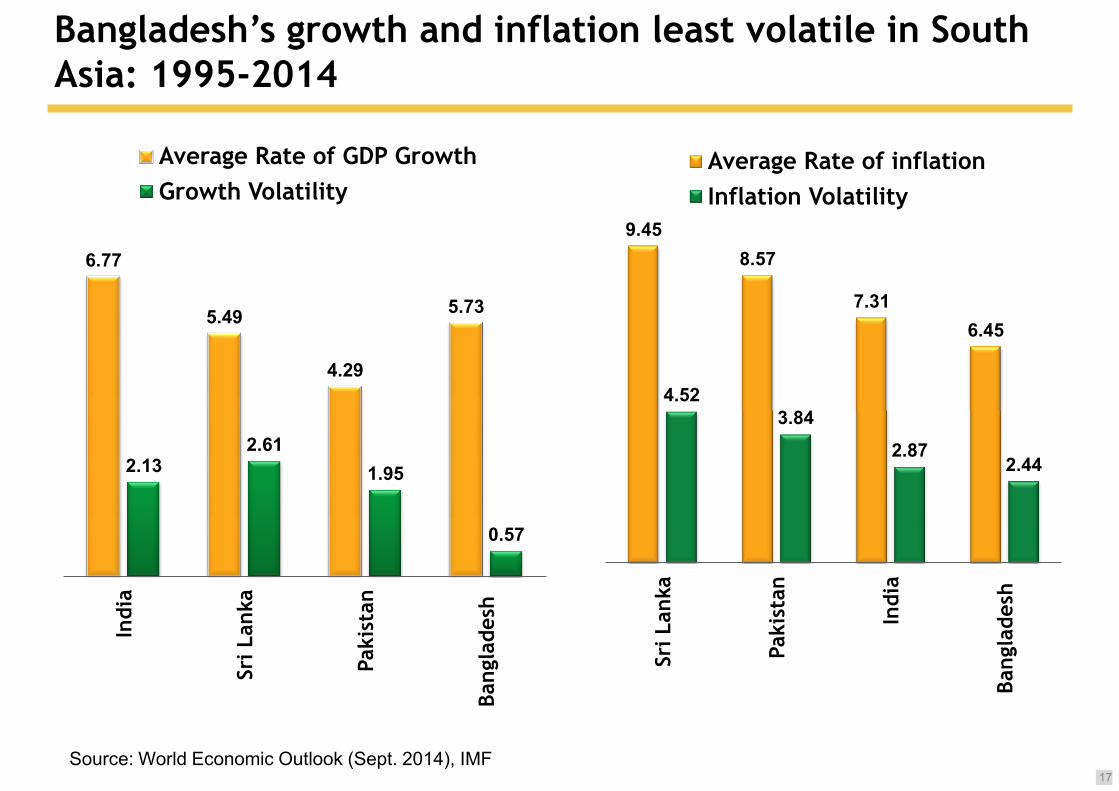

Bangladesh’s growth and inflation least volatile in South Asia: 1995-2014

6.77

5.49

4.29

5.73

2.13 2.61

1.95

0.57

Indi

a

Sri L

anka

Paki

stan

Bang

lade

sh

Average Rate of GDP Growth Growth Volatility

9.45 8.57

7.31 6.45

4.52 3.84

2.87 2.44

Sri L

anka

Paki

stan

Indi

a

Bang

lade

sh

Average Rate of inflation Inflation Volatility

Source: World Economic Outlook (Sept. 2014), IMF

18

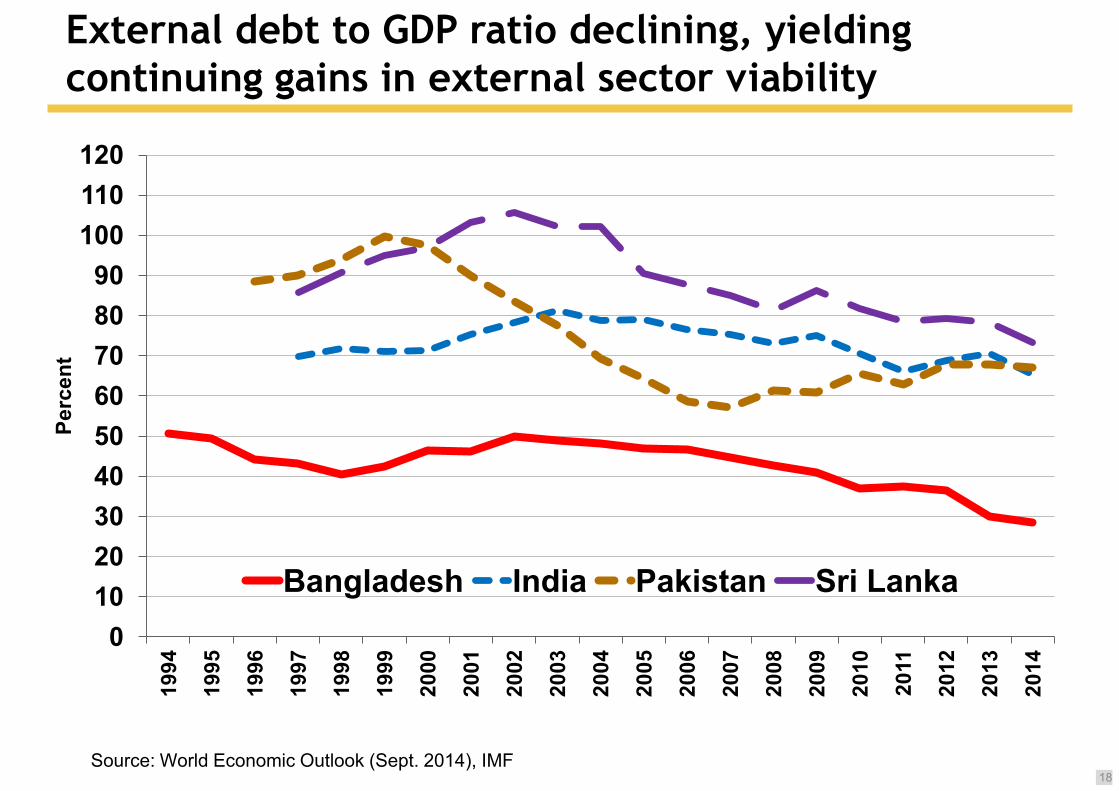

External debt to GDP ratio declining, yielding continuing gains in external sector viability

0 10 20 30 40 50 60 70 80 90

100 110 120

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Perc

ent

Bangladesh India Pakistan Sri Lanka

Source: World Economic Outlook (Sept. 2014), IMF

19

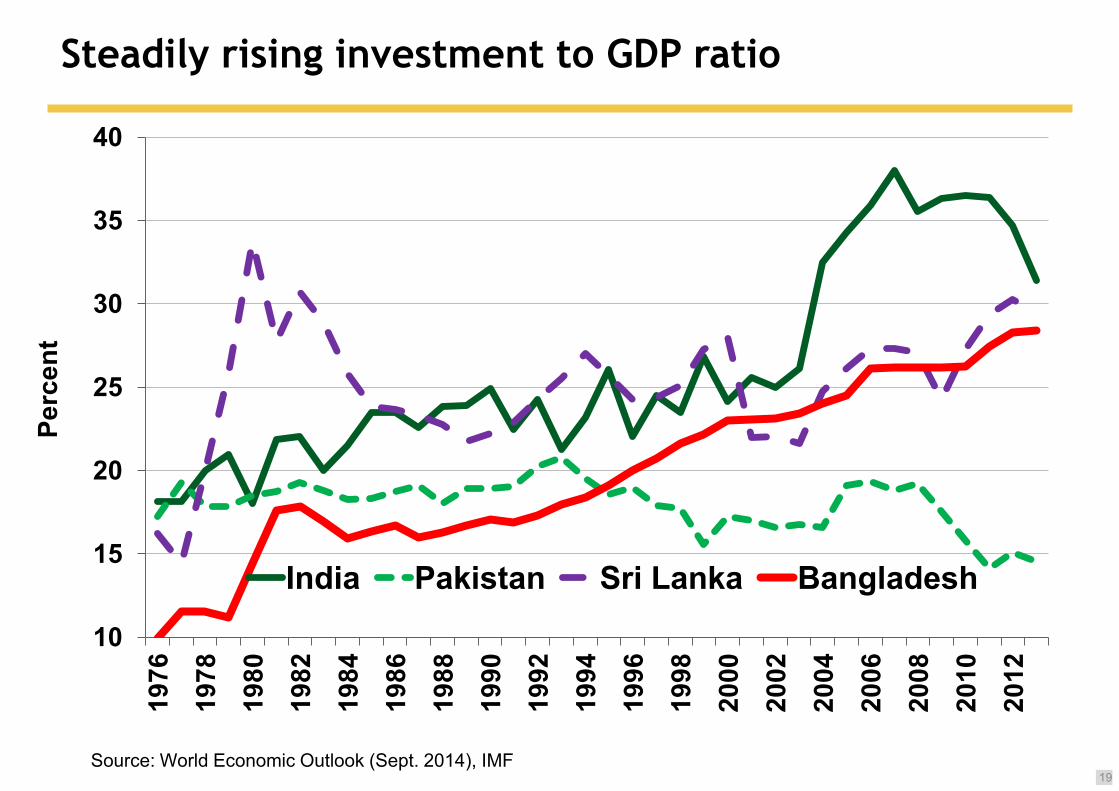

Steadily rising investment to GDP ratio

10

15

20

25

30

35

40 19

76

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Perc

ent

India Pakistan Sri Lanka Bangladesh

Source: World Economic Outlook (Sept. 2014), IMF

20

Strong FX reserves growth enhancing confidence for foreign investments in Bangladesh

Source: IMF 2014

o Rising foreign exchange reserves already comprising 6 month’s import cover and 23% backing for broad money base.

Total Reserves excluding Gold

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

1980

19

82

1984

19

86

1988

19

90

1992

19

94

1996

19

98

2000

20

02

2004

20

06

2008

20

10

2012

Perc

ent

Bill

ion

USD

FX reserve (left axis) FX reserve/GDP (right axis)

Bill

ion

USD

Net financial flows

21

o Bangladesh’s financial sector suffered no stability impairment in the GFC and its aftermath, productive economic segments suffered no liquidity crunch.

o Sustained stability and viability gains are cumulating into a robust confidence base for foreign investors.

o Steadily rising FDI inflows are still relatively modest however, due to acute physical infrastructure deficiencies.

o Scarcity of serviced industrial zones now receiving priority attention of the authorities.

Growth and stability outcomes..(cont’d)

22

Outlook for the path ahead

23

Outlook for the path ahead

o Beginning in the late 1980s, widening of Bangladesh economy’s external openness has proceeded in gradual, measured steps in line with:

— gains in macroeconomic and financial sector stability

— external sector viability, and

— capabilities in external sector data collection, capital flow measurement and management.

o With the cautious gradualist approach, none of Bangladesh’s liberalization steps needed reversal in regional and global crises.

24

Outlook for the path ahead..(cont’d)

o Bangladesh is on course for coming out of low income and least developed country categorizations in the near future.

o Already dwindling concessional financing from development partners will then dry up altogether, needing substantial recourse to non concessional financing from international markets.

o Authorities are positioning Bangladesh economy in readiness for this eventuality, with:

— continued strengthening and consolidation of the stability and viability gains

— regulatory, supervisory and resource utilization capacities.

25

Outlook for the path ahead..(cont’d)

o Progress on this path is anchoring confidence of external investors and will enable full phase out of the remaining regulatory controls on capital flows.

o IMF and other global forums minding global balance and stability will have important supportive role to play in preventing severe jolts from new regional or global crises.

26

Thank you